Very low interest rates: What should pension schemes do? · The Correlation between US Equity and...

21

Very low interest rates: What should pension schemes do? Additional information: For Professional Investors only. Not Suitable for Retail Clients April 2012 Representing Schroders: Andrew Connell – Head of Liability Driven Investment Development Email: [email protected] Mark Humphreys – Head of UK Strategic Solutions Email: [email protected]

Transcript of Very low interest rates: What should pension schemes do? · The Correlation between US Equity and...

Very low interest rates:

What should pension schemes do?

Additional information: For Professional Investors only. Not Suitable for Retail Clients

April 2012

Representing Schroders:

Andrew Connell – Head of Liability Driven Investment Development

Email: [email protected]

Mark Humphreys – Head of UK Strategic Solutions

Email: [email protected]

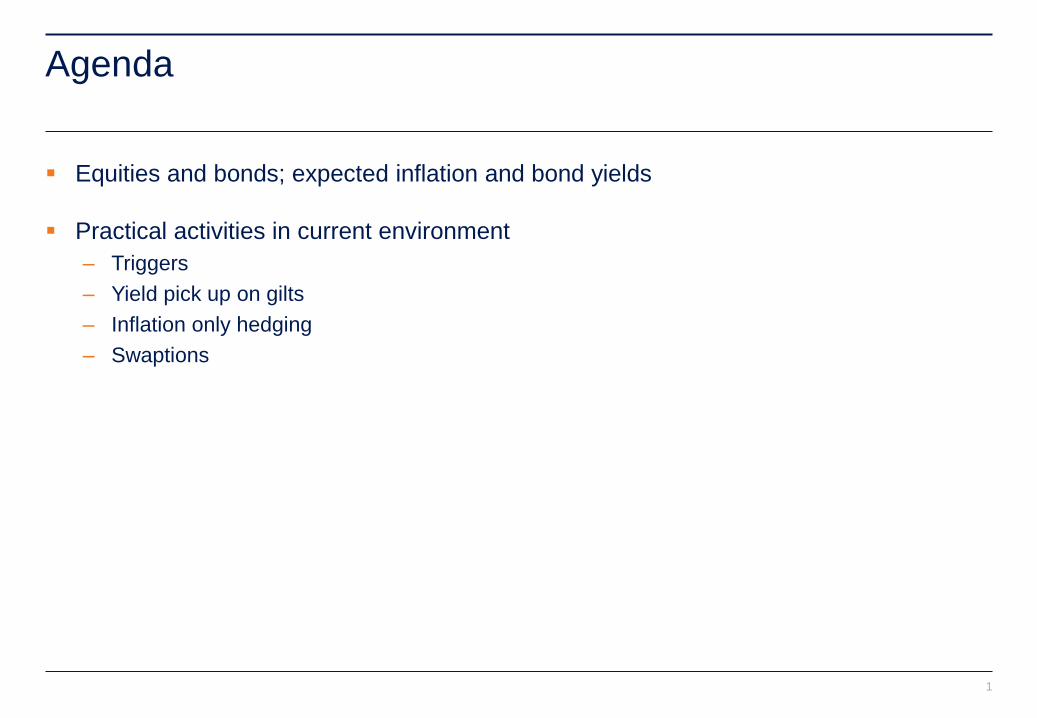

Agenda

1

Equities and bonds; expected inflation and bond yields

Practical activities in current environment

– Triggers

– Yield pick up on gilts

– Inflation only hedging

– Swaptions

Equity and bond returns

2

Negative equity/bond risk

premia over last 10 years

What are prospects for relative

returns in the future?

-10%

-5%

0%

5%

10%

15%

20%

UK Equity Returns in Excess of Gilts (%pa)

Source: Schroders, Barclays Equity Gilt Study 2011. Total returns in excess of long-dated UK gilts shown.

Equity risk premium

3

Equities risk premia looks

attractive

However, are equities cheap

or bonds expensive?

Source: Schroders,

Cyclically adjusted earnings yield – 10yr gov bond yield

Dec 1985 – Feb 2012 Current Average Discount

Price/Earnings 15.7 24.5 -36.0%

Shiller Price/Earnings 21.9 23.9 -8.2%

Dividend Yield 2.1 2.3 -9.5%

Valuation

Correlation regimes

4

Equity and bond correlations vary over

time

Generally

– High inflation → positive correlation

– Disinflation → positive correlation

– Very low inflation or deflation

→ low or negative correlation

The Correlation between US Equity and Bond Returns

Source: Deutsche Bank, Robert Shiller database, Datastream.

Inflation risk premia effect dominates discount rate

Historic real rates and inflation

5

Source: Schroders

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

RPI Swaps - 20 year

Real Swaps - 20 year

Real rates have become

more expensive

RPI expectations have not

‘decoupled’

Faith in inflation targeting

mechanism still in place

Capturing opportunities – governance challenge

6

Source: Bloomberg, Schroders

1994 bond market sell-off – UK gilt yield rose by almost 3% in 8 months

Gilt yields spike again in 1999

4

5

6

7

8

9

10

1993 1994 1995 1996 1997 1998 1999

Yie

ld %

UK 10 Year Government Bond Yield

Triggers to capture a range of scenarios

7

LDI Tranche 1

Cash

LDI Initial

Liabilities

Liability hedging

Asset exposure

Liabilities

Portfolio Structure

Gilts Equities

Gilts

Trigger levels LDI coverage of index linked cashflows

(If average real yield is…)

Funding level* <0.4% >0.6% >0.8% >1.0%

<90% 20% 20% 67% 85%

>90% 20% 67% 85% 85%

LDI Tranche 2

Liability risk coverage is extended as

funding level improves and / or market

rates become more attractive

Source: Schroders, for illustration purposes only.

Practical activities in current environment

Low Interest Rate Environment What Pension Schemes can do

9

Source: Schroders, Bloomberg. For illustration only. As at 31 March 2012.

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

Ma

r 0

7

Sep

07

Ma

r 0

8

Sep

08

Ma

r 0

9

Sep

09

Ma

r 1

0

Sep

10

Ma

r 1

1

Sep

11

20 year inflation swap 20y zero coupon interest rate swap

From an historic perspective inflation is at an attractive level while interest rates are expensive

Look for yield pick up on Gilts

Hedge Inflation only

Swaptions – an alternative to triggers

Yield Pick Up - Synthetic Gilts

10

Expect yield pickup of 40bps or more

Historical comparison of 6m LIBOR and repo rate

Unlocking a Higher Gilt Yield Exploiting the relationship between 6m Libor and repo rate

11

-

50

100

150

200

250

300

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Difference in bps (RHS) 6m Repo 6m Libor

Source: Schroders, Bloomberg. For illustration only. From 31 January 2002 to 31 January 2012.

Funding leg for a swap - 6 month LIBOR

Synthetic Gilts - driven by the repo rate

Correlation between rates, approx. 98%

Repo rate is generally lower than LIBOR

Prior to the credit crunch

– difference between repo and Libor rates

was low and stable

Since the credit crunch

– difference has expanded and

relationship is more volatile

Retain exposure to gilt and capture return benefit

Replicate Physical Gilt Returns Structure of solution

12

Source: Schroders, Bloomberg. For illustration only. *Current average funding difference between synthetic gilt and cash using 6 month

LIBOR as proxy. Subject to market conditions. Please see important information in Risk Modelling Disclaimer.

Sell physical gilts

Replace existing exposure with equivalent gilts

Invest capital released into a cash fund

LDI funds and cash holdings

Synthetic gilt exposure

Physical Gilt holdings

Gilt

Before: Physical Gilt holdings

After: Synthetic Gilt Funds plus Cash

Gilt return

Cash Synthetic

Gilt Cash return

Ca

sh

– 0

.4%

*

Gilt

retu

rn

Gilt + 0.4%

Physical gilt exposure

Can be delivered in a pooled or segregated form

Inflation only hedging

13

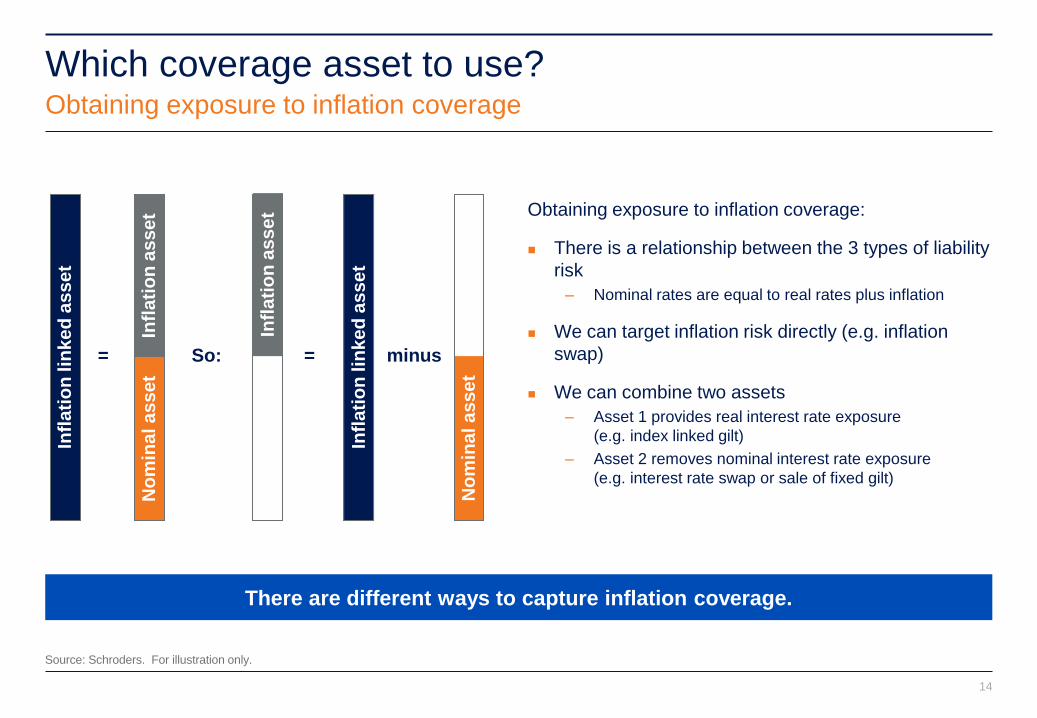

There are different ways to capture inflation coverage.

Which coverage asset to use? Obtaining exposure to inflation coverage

14

Source: Schroders. For illustration only.

Obtaining exposure to inflation coverage:

There is a relationship between the 3 types of liability

risk

– Nominal rates are equal to real rates plus inflation

We can target inflation risk directly (e.g. inflation

swap)

We can combine two assets

– Asset 1 provides real interest rate exposure

(e.g. index linked gilt)

– Asset 2 removes nominal interest rate exposure

(e.g. interest rate swap or sale of fixed gilt)

No

min

al a

ss

et

Infl

ati

on

lin

ke

d a

ss

et

=

Infl

ati

on

as

se

t

So:

No

min

al a

ss

et

Infl

ati

on

lin

ke

d a

ss

et

= minus

Infl

ati

on

as

se

t

0

20

40

60

80

100

120

140

160

180

200

2.0%

2.5%

3.0%

3.5%

4.0%

Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11

Difference (Right Hand Scale) Inflation Swap Index linked gilt less interest rate swap

Which coverage asset to use? Identifying the best value coverage asset through intelligent implementation

15

Source: Schroders, Bloomberg. For illustration only. As at 30 March 2012.

Obtaining coverage through a combination of index linked gilts and interest rate swaps offers clients

the opportunity to hedge at more attractive levels than inflation swaps

Absolute levels of inflation remain lower than 3 year average and are therefore attractive on an

historic basis

bps

Swaptions

16

Swaptions can be used as a potentially more efficient LDI implementation strategy than

triggers

Using Swaptions in a Low Rate Environment

A swaption is an option granting its owner the right but not the obligation to enter into an

underlying swap.

Swaptions can lock in to the desired trigger level yield in nominal or real yields

Swaptions offer an uplift through the premium received ie scheme is selling an option

Depending upon the outcome the swaption:

– Is executed into the target yield at which the scheme is happy to extend LDI coverage, or

– Offers further opportunity to capture another premium if not exercised

Issue to consider

– Swaption has a specified maturity

– Yields rise and hit target but then retreat below target on expiry

– Can be closed out prior to expiry locking in target yield and part of premium

Premium can be used to buy protection on rates falling over the same period

17

Summary

18

Ex ante ERP attractive – but environment highly uncertain

Beware regime shifts in inflation and equity/bond correlations

Real and nominal yields low

There are practical things to be doing

– Triggers

– Yield pick up on gilts

– Inflation only hedges

– Swaptions

Important information

Past performance is not a guide to future performance. You should remember that the value of investments can go down as well as up

and is not guaranteed. Exchange rate changes may cause the value of overseas investments to rise or fall. Potential investors should

be aware that investment in global equity markets involves a degree of risk and should be regarded as a long term investment. The

data shown in this presentation represents past performance achieved for the global equity composite. There is no guarantee that this

performance will be repeated.

This document does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder

International Selection Fund (the “Company”). Nothing in this document should be construed as advice and is therefore not

a recommendation to buy or sell shares. Subscriptions for shares of the Company can only be made on the basis of its

latest prospectus together with the latest audited annual report (and subsequent un-audited semi-annual report, if

published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A. The

Company is not managed in order to qualify for UK distributor status. It may not meet the requirements of investors subject

to UK taxation. An investment in the Company entails risks, which are fully described in the prospectus.

For the purposes of the Data Protection Act 1998, the data controller in respect of any personal data you supply is Schroder

Investment Management Ltd. Personal information you supply may be processed for the purposes of investment

administration by the Schroder Group which may include the transfer of data outside the European Economic Area.

Schroder Investment Management Ltd may also use such information for marketing activities unless you notify it otherwise

in writing.

Schroder Investment Management Limited

31 Gresham Street, London EC2V 7QA

Telephone: 020 7658 6000 Fax: 020 7658 6965

Registration No 1893220 England

For your security, communications may be taped or monitored. Issued in January 2012.

Authorised and regulated by the Financial Services Authority

19

Important information

20

Derivatives – Investment

The strategy can use derivatives for investment purposes and may leverage the portfolio. These instruments can be more volatile than

investment in equities or bonds. The use of leverage can increase gains as well as losses and expose the strategy to increased risk.

The use of derivatives and leverage involves a higher degree of risk and may lead to a higher volatility in the unit prices of the funds.

Liability Driven Investment

Entering into derivative contracts introduces counterparty risk, the potential to incur a loss if the counterparty is unable to honour its

obligations. This means clients are exposed to potential losses if a counterparty were to default on its obligation. We mitigate much of

this risk by receiving collateral with a value at least equal to the exposure to each counterparty. Subject to minimum transaction limits,

the level of collateral will be updated on each business day. However, in the event of a default, there would be a cost involved in

liquidating and reinvesting.

Liability hedging strategies may also be subject to basis risk between the valuation methodology applied to a pension scheme’s

liabilities and that applied to the underlying contracts.

Derivative contracts may involve a commitment to meet LIBOR-based payments on the underlying strategies. There is a risk that the

assets of a pension scheme fail to deliver the returns needed to meet these payments which would result in a deterioration in the

scheme’s funding level.

Whilst hedging strategies are constructed to reflect the expected behaviour of pension fund liabilities, note that pension fund liabilities

can only be estimated and as such there may be a divergence between the performance of the hedge and an individual scheme’s

actual liabilities.

Third Party Data Warning

Third party data are owned by the applicable third party identified above and is provided for your internal use only. Such data may not

be reproduced or re-disseminated and may not be used to create any financial instruments or products or any indices. Such data are

provided without any warranties of any kind. Neither the third party data owner nor any other party involved in the publication of this

document can be held liable for any error. The terms of the third party’s specific disclaimers are set forth in the Important Information

section on our website www.schroders.co.uk.

Issued April 2012 by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA