VERDIS Presentation - JUL 2015 - DEC INVESTORS

47

WE CONVERT FLARED GAS INTO ULTRA-CLEAN DIESEL

-

Upload

rob-ayasse -

Category

Documents

-

view

505 -

download

2

Transcript of VERDIS Presentation - JUL 2015 - DEC INVESTORS

WE CONVERT FLARED GAS

INTO ULTRA-CLEAN DIESEL

THE VERDIS ALTERNATIVE CONVERT WASTED GAS INTO ULTRA-LOW SULFUR DIESEL

Our GTL conversion units provide profitable alternative to gas-flaring | Operators can reduce

carbon footprint & generate significant cash-flows from valuable commodity | Produce Diesel,

naphtha, aviation fuel

CAPITAL REQUIREMENTS

$5-10 million to get first units manufactured and fielded with companies already strongly

interested | If closer to $10 million: could start parallel work on larger units | Projected

revenues: +$40 million revenue, EBITA +$35 million, within 5 years.

EXECUTIVE SUMMARY

GLOBAL GAS FLARING A MASSIVE CHALLENGE

Oil and Gas operators annually flare or vent $30 billion of natural gas | Precious energy

wasted | 400 million tons of damaging CO2 emitted

OUR PATENTED CATALYST A DISTINCTIVE COMPETITIVE ADVANTAGE

Our Fischer-Tropsch process and cobalt-ruthenium catalyst boost diesel yield from 50 to 94% |

By-products: usable water, co-generated electricity | Customer breakeven point – 3 year

average based on wholesale value of diesel and water produced | Environmental benefits add

further value

ISSUE & OPPORTUNITYVERDIS & ITS TECHNOLOGYCURRENT FOCUSINUVIK’S ENERGY CHALLENGE COMMERCIALIZATION

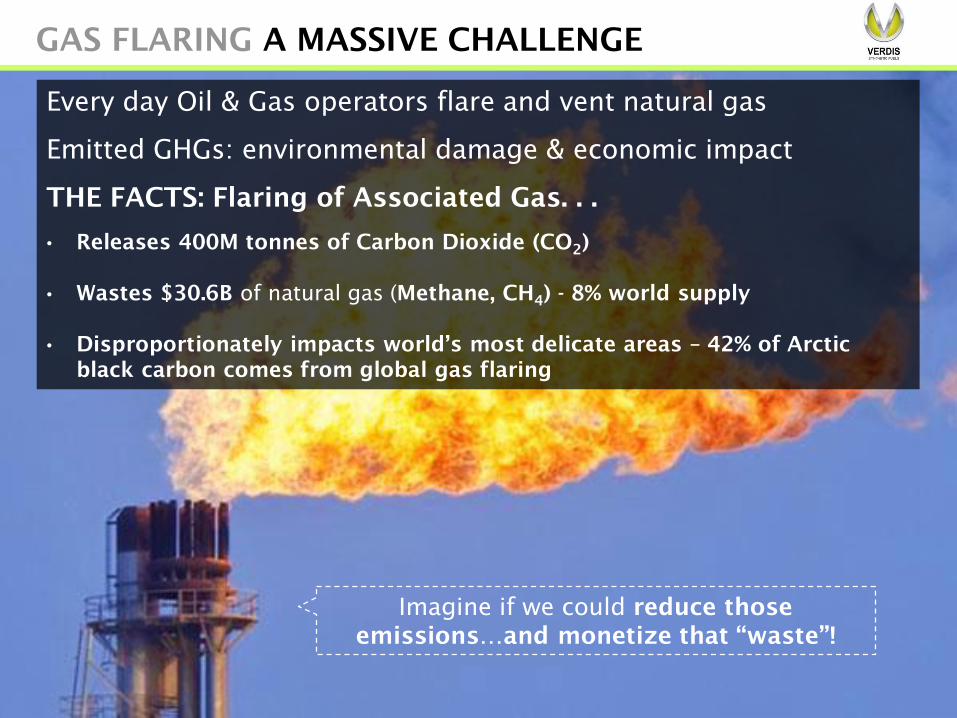

Every day Oil & Gas operators flare and vent natural gas

Emitted GHGs: environmental damage & economic impact

THE FACTS: Flaring of Associated Gas. . .

• Releases 400M tonnes of Carbon Dioxide (CO2)

• Wastes $30.6B of natural gas (Methane, CH4) - 8% world supply

• Disproportionately impacts world’s most delicate areas – 42% of Arctic

black carbon comes from global gas flaring

Imagine if we could reduce those

emissions…and monetize that “waste”!

GAS FLARING A MASSIVE CHALLENGE

STOP FLARING. MONETIZE YOUR WASTE!

WHY DO COMPANIES STILL FLARE?

VERDIS SYNTHETIC FUELS

GAS-TO-LIQUIDS MOBILE PROCESSING UNITS

CONVERT NATURAL GAS TO

MARKET-READY ULTRA-CLEAN DIESEL

This is the VERDIS poster From the ADIPEC 2012 Oil & Gas Show in Abu Dhabi, UAE

They lack a profitable, practical, alternative . . .

. . . So VERDIS is going to give them one!

PRIORITY 1 - GAS FLARING

Current solutions target only extremely large gas deposits…

… leaving $20B+ market for S/M sized flares unexploited

VERDIS will provide Oil & Gas producers a profitable way to:

• Optimize value chains as profit driver

• Reduce emissions, lighten environmental foot print

• Promote corporate image/CSR

• Comply with emissions reduction targets

PRIORITY 2 - STRANDED GAS RESERVOIRS / REMOTE

LOCATIONS

• Large reserves remain unexploited for economic or technical reasons

• VERDIS units can do it, on land, offshore platforms, boats & barges

PRIORITY 3 – AUTHORITIES RESPONSIBLE FOR ENERGY

SECURITY

• A less expensive fast-track to domestic diesel production (Israel,

Leviathan field)

• To provide fuel, water & electricity to isolated communities with gas

supplies (Arctic region: City of Inuvik; desert communities)

UNTAPPED MARKETS

REGULATORY TRENDS

Agreed UNFCCC Global Objective: “stabilization of atmospheric GHG concentrations at a

level that would prevent dangerous anthropogenic interference with the climate system”

(limiting temperature rise to 2 C)

Pre-Summit Reduction Commitments:

• EU & Norway: binding target - at least 40% below 1990 level by 2030 (Key focus on Oil and

natural gas and other emissions from energy production)

• US: 26-28% below 2005 level by 2025 (EPA to set standards on methane emissions from landfills, oil and

gas sector)

• Russia: reduction of 25-30% from 1990 levels by 2030

• Canada: “intend to reduce” to 30% below 2005 levels by 2030

• China: 60-65% reduction per unit of GDP by 2030, after emissions peak

• India: yet to commit

ISSUE & OPPORTUNITYVERDIS & ITS TECHNOLOGYCURRENT FOCUSINUVIK’S ENERGY CHALLENGE COMMERCIALIZATION

VERDIS Synthetic Fuels, FZE

• VERDIS Synthetic Fuels was founded in Sharjah, UAE,

in 2010

• Subsidiary of Calgary-based Canada Chemical

Corporation (CCC)

• Dedicated to commercializing CCC’s

groundbreaking Gas to Diesel (GTL) technology

Canada Chemical Corporation

• Long track record of oil & gas sector innovation,

R&D excellence

• Within GTL, decided to target market-ready diesel

• It’s R&D staff, led by noted scientist Dr. Conrad

Ayasse, began work on GTD in the late 1990s

• Filed the first set of patents

VERDIS FUELS & IT’S TECHNOLOGY

WHO ARE WE?

VERDIS STRATEGIC PARTNERS

RESEARCH & DEVELOPMENT

Canada Chemical Corporation

Calgary, Canada (www.canchem.ca)

• Technology’s inventor, 20 years GTL experience

• VERDIS’ parent company, provides all technical support

• 2 Lab test rigs fully assembled and running

• Optimizing syngas reformer solutions

PROCESS ENGINEERING & UNIT MANUFACTURE

Suez Environmental Oil & Gas Systems

Melbourne Australia/Abu Dhabi, UAE (www.processgroupintl.com)

• Process engineering & manufacturing partner

• Expertise in skid-mountable “packaged plants”

• Collaborated with VERDIS on 0.25MMSCFD design

INNOVATION FINANCE

Innovation Norway

Tromsø, Norway (www.innovasjonnorge.no)

• Innovation grant funding for V-CPOX

• Ready to co-support further development opportunities

VERDIS Fischer-Tropsch process based on proprietary cobalt-rhenium

catalyst: boosted diesel output from 45-50% to 94%

(2n + 1) H2 + n CO → CnH(2n+2) + n H2O

METHANE DIESEL + WATER

FT CATALYTIC REACTION

PARAFFINIC SYNTHETIC DIESEL

0% Sulfur0% Aromatics

+

COMPETITIVE ADVANTAGE PROPRIETARY CATALYST

• Vehicle ready diesel

directly from FT

reactor

• No further refining

necessary

• Very high Cetane

number (78, versus

normal spec of 43)

• Zero sulfur or

aromatics content –

much cleaner

emissions

• Ideal blending stock

• Only process on the market converting gas directly

to ultra-clean diesel at low-pressure, directly from

the FT reactor, so no hydro-cracking or further

refining

• Significant CAPEX/OPEX savings (US DoE estimate: up

to 30%)

• By-products: industrial-use water (1.1:1 water to

diesel), possibility of surplus electricity

• Units could provide surplus electricity after startup –

virtually 0 waste (excellent for desert, arctic and

offshore use)

VERDIS PROCESS ADVANTAGES

“The uniqueness and novelty lies in the . . . catalyst design and operation to realize the optimal, economic small-scale GTL process for production of a liquid fuel product containing high diesel and low wax yields. This is the type of process design for which the syngas conversion community has been searching. . .”

- Leading GTL Expert Prof. Calvin H. Bartholomew, Brigham Young University

1998 THROUGH 2008

• Extensive R&D, bench-scale proof of concept

• Deep expertise in traditional syngas creation

• Worked on proprietary FT catalyst

• 2006: deployed a 25 MSCFD prototype on landfill in

Oklahoma City (actual photos on right)

• Prototype decommissioned in 2008

2008 THROUGH 2015

• Data from protoype: updated patents 2009

• VERDIS founded 2010

• 2012: Partnered with Process Group International

(www.processgroupintl.com) to design 0.25 MMSCFD

mobile unit

• Result: autothermal & steam reforming technically viable,

BUT temps too high, efficiency too low, for real customer

value

• 2012-2014: search for optimal syngas solutions, further

refined FT catalyst

• 2 emerging technologies: plasma & CPOX

• Funding from Innovation Norway (office in Tromsø)

25 MSCF/day Prototype

Prototype Deployment

VERDIS FUELS & IT’S TECHNOLOGY

GTD TECHNOLOGY DEVELOPMENT BY CCC & VERDIS

PLASMA-BASED SYNGAS REFORMER VALIDATION: JULY 2014 CERAMATEC TEST

TEST OBJECTIVES

Validate VERDIS catalyst combined with Ceramatec’s unique plasma-based syngas reformer in

a ¼ BBD GTL unit

TEST RESULTS

Exceeded all

expectations – best

Ceramatec has seen:

• 90% Diesel

(industry standard

45-55%)

• Only trace

amounts of wax

(0.08%)

• Predicted that

VERDIS 0.25

MSCFD unit would

achieve 10,000:1

conversion ratio,

beating even

Shell’s world-scale

‘Pearl’

VERDIS FUELS & IT’S TECHNOLOGY

• Plants smaller than Shell and Sasol,

but still not mobile

• September 2013: selected by Pinto to

field 2800 BBD plant in Ohio, USA

• Pant will produce mix of waxes,

solvents and lubricants

• Outputs to make ultraclean

transportation fuels will need further

refining

• 2006: PETROBRAS partnership

• 2012: completed demonstration plant,

processes 200,000 SCF/day of gas into

around 20BBD

• According to World Bank Global-Gas Flaring

Reduction Partnership: they produce around

20BBD of crude oil with a heavy wax

content which must be further refined

through hydro-cracking.

• A few majors active in large-scale GTL (Shell, Sasol).

• Very few looking at smaller-scale, mobile solutions. VERDIS’ prime target.

• Competitive advantage: unlike competitors, VERDIS product market-ready, no further

refining needed

• Offers more efficiency, flexibility, adaptability, so lower CAPEX and OPEX

COMPETITIVE ADVANTAGE: VERDIS

VERDIS Mobile VERDIS Fixed VERDIS SPP

(4 MMSCFD)

400 US BBD (63,600 L)

Transported in several

trucks, fixed location

Medium-scale gas-flaring

or mid-sized stranded gas

deposits

(25+ MMSCFD)

2500 US BBD (397,500 L)

Small Petrochemical Plant

Large scale gas-flaring

sites, or to develop whole

stranded gas fields

(1 MMSCFD)

100 BBD (15,900 L)

Fully mobile, moved on 3

standard trucks &

assembled in place

Small-scale gas flaring or

stranded gas deposits

PRODUCT ROADMAP

Synthetic Diesel (ULSD) is so clean

you can actually SEE the difference!

CUSTOMER VALUE PROPOSITION

Based on a gas to diesel conversion ratio of the smallest unit(10,000:1), for straight methane. Associated gas, with its mix ofhigher combustibles (ethane, propane) can yield up to 40% morediesel pr unit of gas converted.

• Customer BEP for single VERDIS mobile unit in a cross-section of markets based

exclusively on the wholesale value of diesel and water it will produce

• Breakeven point in most markets: 3 years

• Indirect or intangible benefits

could include:

o Tax breaks or carbon

credits

o PR benefits from

reduced flaring &

carbon emissions

o Meet corporate goals,

national laws or global

conventions

o Excess electricity

produced which may

be sold back to the

grid

• Ancillary benefits may

be as valuable as direct

economic benefits

-4

-2

0

2

4

6

8

10

12

Israel Australia China Canada Nigeria Russia UK Mexico USA UAE Qatar

BREAKEVEN YEARS - SELECTED MARKETSFlared Gas vs. Henry Hub FMV

Breakeven YR - AG Breakeven YR - FMV

ISSUE & OPPORTUNITYVERDIS & ITS TECHNOLOGYCURRENT FOCUSINUVIK’S ENERGY CHALLENGE COMMERCIALIZATION

Aker Solutions

Tromso, Norway

• Flaring on Norwegian Continental Shelf illegal – re-injection the norm

• New northern blocks have insufficient reservoir depth to re-inject

• Aker seeking novel solution for ~4 MMSCFD of AG on 2 new platforms

• Proposed 5 plasma-based reformers (of 1 MMSCFD each) & VERDIS FT catalyst

• Aker team vetted proposal

• September 2014: fully endorsed VERDIS technology as optimum offshore solution,

recommended it for both platforms

• Both projects on hold given current oil price

VERDIS FUELS & IT’S TECHNOLOGY

CURRENT FOCUS & CUSTOMER ENGAGEMENTS – 4 MMSCFD OFFSHORE OIL PLATFORMS

1. Small footprint

2. Low weight

3. Low pressure

4. High GHSV so that the reactor can be small

and light

5. Low pressure drop at high GHSV

6. High gas conversion (>95%)

7. High selectivity to CO (>95%)

8. No water needed

9. No pure oxygen needed

10. No feed gas pre-heat needed

11. No tail gas heat exchanger needed

12. Feasibility for some FT tail gas re-cycling

IDEAL SYNGAS PLANT FOR OFFSHORE PLATFORMS

20 Verdis Synfuels CONFIDENTIAL INFORMATION

V-CPOX

Reactor

Syngas

Water: flash

to atm.

Air

cooler

Syngas

Water

FT

Plate

Reactor

Gas

Oil

Water

Air

Cooler

to 50 C

Separator

Fuel

gas

Oil

Water

Dowtherm J

Naphtha

BP

R

Pipeline

125 C

Diesel

Quench water

Separator740 C

Separator

VERDIS SYNFUELS OFFSHORE GTL PROCESS SCHEMATIC

OBJECTIVES ACHIEVED: much lighter, smaller footprint, lower temp & pressures,

50% fewer unit operations – fully optimized offshore solution

Air and

Associated Gas

blower

(1-3 bar)

50 C

210 C

Compress

to 13 bar Pre-

heat

Re-

cycle+FG Chiller

to 4 C

To

Quench

Catalytic

hydrogenation

Platform

use

Gas

No wax, no olefins,

No alcohols

21

10MMSCFD OFFSHORE PLANT (SOUTH-EAST ASIAN FIELD)

COST: $70 Million

Breakeven Point: 13 months

Accumulated Profit & Loss (10 yrs): $576,069,470

Net Present Value (5% discount rate): $408,454,971

Internal Rate of Return: 92.2%

COST: $100 Million

Breakeven Point: 19 months

Accumulated Profit & Loss (10 yrs): $546,069,470

Net Present Value (5% discount rate): $379,883,542

Internal Rate of Return: 64.2%

125MMSCFD OFFSHORE PLANT (FPSO-Mounted)

COST: $875 Million

Breakeven Point: 15 months

Accumulated Profit & Loss (10 yrs): $5,968,956,250

Net Present Value (5% discount rate): $4,199,734,860

Internal Rate of Return: 78%

COST: $1.25 Billion

Breakeven Point: 22 months

Accumulated Profit & Loss (10 yrs): $5,593,956,250

Net Present Value (5% discount rate): $3,842,592,003

Internal Rate of Return: 54%

ISSUE & OPPORTUNITYVERDIS & ITS TECHNOLOGYCURRENT FOCUSINUVIK’S ENERGY CHALLENGE COMMERCIALIZATION

INUVIK’S ENERGY CHALLENGE

Geography

• Small, relatively isolated community

• Challenging winter road conditions, so supply chain

vulnerability

Infrastructure

• 2 power plants: one natural gas, one diesel (backup)

• Local Ikhil well depleted in 2012

• Forced reliance on diesel doubling energy bills

• LNG fuel now trucked on Dempster Highway from BC

at considerable expense

• January 2014: first LNG plant opened

• Landed diesel cost: $0.97, Retail: $1.55 (May 2015)

INUVIK’S ENERGY CHALLENGE

Key Success Factors

• Guaranteed supply of reasonably-priced feed gas

• Balancing volume required by gas supplier with Inuvik’s energy needs

• Buy-in from Inuvik’s residents

• Support from municipal, territorial and federal governments

Possible Functions and Stakeholders

VERDIS Fuels (with technical partners)

• GTL plant design and manufacture (with Suez Environmental as EPC partner)

• Winterization of GTL plant (expertise from Aker Solutions office in Tromsø, Norway)

• Overall project management and key stakeholder engagement

Possible Sources of Co-Funding

• Town of Inuvik

• Northwest Territories Power Corporation?

• Government of NWT?

• Federal government (NRCAN, Environment Canada, DIAND)?

• Canadian Polar Commission?

• Innovation Norway (has already shown interest)

• Norwegian Research Council’s Demo2000 program

INUVIK’S ENERGY CHALLENGE

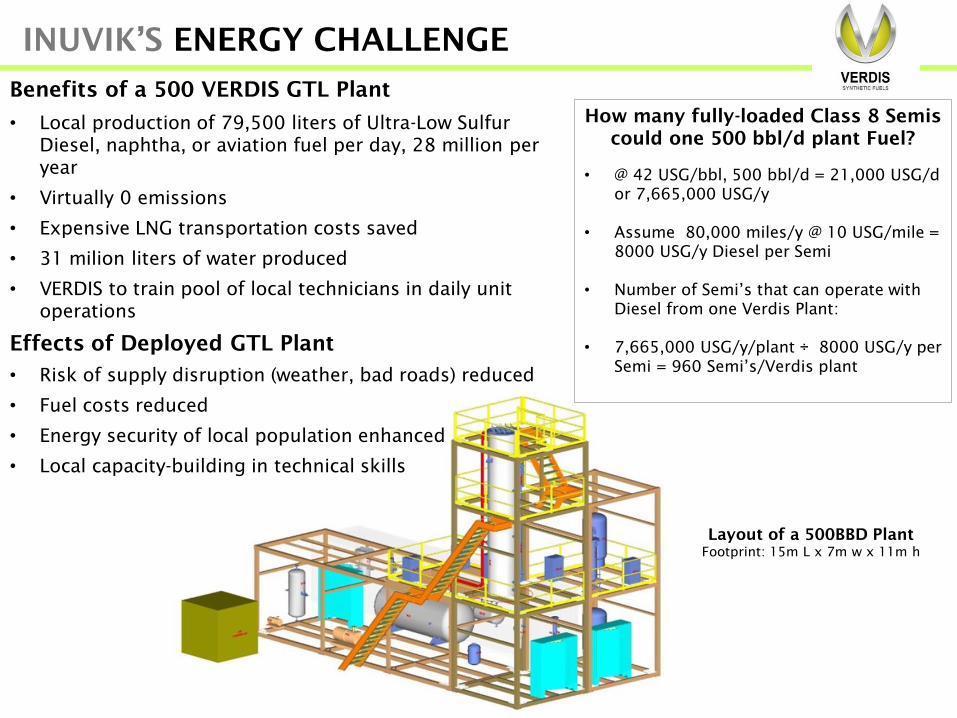

Benefits of a 500 VERDIS GTL Plant

• Local production of 79,500 liters of Ultra-Low Sulfur

Diesel, naphtha, or aviation fuel per day, 28 million per

year

• Virtually 0 emissions

• Expensive LNG transportation costs saved

• 31 milion liters of water produced

• VERDIS to train pool of local technicians in daily unit

operations

Effects of Deployed GTL Plant

• Risk of supply disruption (weather, bad roads) reduced

• Fuel costs reduced

• Energy security of local population enhanced

• Local capacity-building in technical skills

Layout of a 500BBD Plant

Footprint: 15m L x 7m w x 11m h

How many fully-loaded Class 8 Semis

could one 500 bbl/d plant Fuel?

• @ 42 USG/bbl, 500 bbl/d = 21,000 USG/d

or 7,665,000 USG/y

• Assume 80,000 miles/y @ 10 USG/mile =

8000 USG/y Diesel per Semi

• Number of Semi’s that can operate with

Diesel from one Verdis Plant:

• 7,665,000 USG/y/plant ÷ 8000 USG/y per

Semi = 960 Semi’s/Verdis plant

1MMSCFD PLANT FOR INUVIK

COST: $50 Million

Breakeven Point: 38 months

Accumulated Profit & Loss (15 yrs): $229,171,875

Net Present Value (5% discount rate): $152,838,098

Internal Rate of Return: 40.3%

BREAKEVEN ANALYSIS FOR GTL IN INUVIK - $50 million

YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5 YEAR 6 YEAR 7 YEAR 8 YEAR 9 YEAR 10 YEAR 11 YEAR 12 YEAR 13 YEAR 14 YEAR 15

EXPENSES

Purchase Cost 50,000,000 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OPEX (incl.

annual maintenace, catalyst replacement, gas at $15 per MMSCF)

7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000

Total Expenses 50,000,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000 7,500,000

REVENUES

Ultra Low Sulfur Diesel ($1.25,

10,000:1 conversion ratio, 355 days of production)

35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125 35,278,125

Total Revenues 0 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125 27,778,125

Accumulated P&L 0 15,278,125 30,556,250 45,834,375 61,112,500 76,390,625 91,668,750 106,946,875 122,225,000 137,503,125 152,781,250 168,059,375 183,337,500 198,615,625 213,893,750 229,171,875

Simplified NCF - Yearly -50,000,000 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125 20,278,125

Accumulated Simplified NCF -50,000,000 -29,721,875 -9,443,750 10,834,375 31,112,500 51,390,625 71,668,750 91,946,875 112,225,000 132,503,125 152,781,250 173,059,375 193,337,500 213,615,625 233,893,750 254,171,875

Discounted Rate 5.0%

NPV 152,838,098

IRR 40.3%

Breakeven Point (months) 38

ISSUE & OPPORTUNITYVERDIS & ITS TECHNOLOGYCURRENT FOCUSINUVIK’S ENERGY CHALLENGECOMMERCIALIZATION

#1 RUSSIA

Gas Flared: 37.4 BCM

Gas Value: B$ 13.4

#2 NIGERIA

Gas flared: 14.6 BCM

Gas Value: B$ 5.2

#3 IRAQ

Gas Flared: 9.4 BCM

Gas Value: B$ 3.36

#5 UNITED STATES

Gas flared: 7.1 BCM

Gas Value: B$ 2.6

CURRENT PATENT RIGHTS

25 countries & European Patent Office

19 out of the 20 top flaring countries

~85% of the worldwide estimated flared volume, worth $26 Billion

EXPANSION PLANS FOR A GROWING MARKET

BUSINESS MODEL TRANSFORMING GAS TO DIESEL

PRINCIPAL REVENUE STREAMS

• Design & sale of GTL units, technology

licensing

• After sales support (spare parts,

maintenance, training, catalyst replacement -

~15% value of annual diesel yield)

• Long-term: fleet of equipment for lease

SECONDARY REVENUE STREAMS

• Remote, diagnostic, monitoring of deployed

conversion units

• Sale of surplus electricity produced during

the FT process

• Training of local technicians

• Consultancy fees

Offshore Gas Flare, Alaska

GO TO MARKET STRATEGY

Phase 1 – Post Launch

• Companies who have already expressed serious

interest (Pemex, EcoPetrol, Aker, CieQual)

• This will be enough demand as VERDIS ramps up

production

Phase 2 – First Units Deployed

• Leverage initial unit deployments as demonstration

• Specialist industry events (ADIPEC 2015)

• Environmental conferences

• Target companies in the World Bank’s Global Gas-

Flaring Reduction Partnership (GGFR)

Phase 3 – Building Stable Demand

• Word of mouth, industry publications

• Retention through excellence in value creation

25K SCF/day prototype , Oklahoma, USA

CUSTOMER ACQUISITION: CHANNELS & PHASING

ONGOING PRODUCT DEVELOPMENT

• Extremely encouraging results from prototype’s deployment in the US

• Feedback from customers and investors: love concept, need commercial-

sized demonstrator

• Benefits

o Demonstrate process to investors & customers

o Give VERDIS first sale

o Use as template for larger units

NEED FOR A TECHNOLOGY DEMONSTRATOR

CAPITAL REQUIREMENTS

WHAT IS OUR REQUIREMENT?

USD5-10 million investment in

exchange for 15-25% of VERDIS

WHAT WILL CAPITAL BE USED FOR?

Final design optimization

Manufacture, delivery and line-in

of first full-sized commercial

unit

More capital: parallel

development of larger units

Time To Market

13 to 18 months to have first

unit fielded

Demonstrator to drive sales

• VERDIS anticipates ~$40 million in

revenues, generating $35 million

EBITA, in 5 years

• Despite significant working capital

required for the first 5 development

phases, from years 1 to 7, VERDIS

expects an Internal Rate of Return

of 114%

• This will generate Discounted Cash

Flows (DCF) of 73 million USD from

year 2 to 7

• Based on 10 times EBITA, company

would have an estimated value of

~290.0 million USD by year 7

YEAR ON YEAR SALES PROJECTIONS

FINANCIAL OUTLOOK

39,264

47,510

18,112

23,864

29,280

35,429

-5,000

5,000

15,000

25,000

35,000

45,000

Y Y+1 Y+2 Y+3 Y+4 Y+5 Y+6

IN K$

NET REVENUES DCF EBITA

Y Y+1 Y+2 Y+3 Y+4 Y+5 Y+6

NET REVENUES 0.0 1,500.0 5,442.6 29,252.2 39,264.1 43,190.5 47,509.6

EBITA -3,710.0 -85.0 2,146.3 21,559.7 29,280.1 32,208.1 35,428.9

DCF -3,669.38 -128.57 1,948.36 14,146.39 18,111.52 19,445.56 23,864.29

Y+2 Y+3 Y+4 Y+5 Y+6

K 250 12 14 16+10% +10%

M 2.5 0 2 2

BENEFITS OF VERDIS COMMERCIALIZATION

• ENVIRONMENTAL Oil and gas operators get profitable alternative to gas

flaring/venting, helps reduce 400 million tons of damaging CO2 this releases annually

• ENERGY EFFICIENCY Flaring/venting gas wastes ~3 trillion SCF (150 billion cubic

meters) of natural gas annually, worth over $30 billion.

• ENERGY SECURITY Countries with natural gas supplies but limited oil/conventional

diesel refining, could get a cost-effective fast-track to domestic diesel production,

reducing their reliance on foreign imports

• COMMERCIAL Mobile units (~250,000 SCF/day) could monetize gas deposits

uneconomical through conventional means with truck-mounted units. Large-scale

fixed facilities (25 million SCF/day+) could be built to produce diesel for market,

blending stock or diluent use

• HIGH-TECH EMPLOYMENT 5-10 engineering and lab tech jobs created in the VERDIS

R&D centre, 2-3 teams of 5 engineering techs needed to line-in, service & maintain

deployed GTD conversion units

FURTHER DUE DILIGENCE

To support your further consideration of the VERDIS opportunity,

we can provide . . .

TECHNICAL INFORMATION

• The Catalyst patent

• Independent 3rd

party technology review by leading GTL expert Prof. Calvin Bartholomew

• World Bank report “Associated Gas Utilization Through Mini GTL,” (April 2012) which reviews

VERDIS

• Technology FAQs

COMMERCIAL INFORMATION

• Business Plan Executive Summary (4 pages)

• Full Business Plan (120 pages)

• List and status of all patent filings

• Full 8 year financial projections and revenue modelling

• Schedule and budget for post-investment commercialization

• Customer Value Creation assessment in 10 selected VERDIS markets

• Plan for rollout of commercial and technical personnel

• Plan for development of VERDIS as a corporate entity ready to sustain large-scale growth

Rob AYASSE, MBACEO

Agata MATABUENA, MBA

Operations & Logistics

Renaud CLAUSSE, MBAFinance

Alan AYASSE, P.ENG

Engineering

Jorge GOMEZ, MBAStrategy & IT

Dr. Conrad AYASSEChief Scientist

We have gathered an experienced international management

team, and combined it with top-notch technical experts and scientists

VERDIS AMERICAS

R&D Lab | Canada

VERDIS EMEA

HQ in Sharjah | United Arab Emirates

VERDIS APAC

Finance | China

TEAM VERDIS

WHAT IS FREE ASSOCIATED PETROLEUM GAS?

Petroleum

(Complex mixture of liquid

hydrocarbons)

Free associated

petroleum gas

(Mixed gaseous hydrocarbons

mainly Methane, CH4)

Drilling rig

Anticline

Impervious rock

Gas flare stack

WHY IS GAS

FLARED?

• When crude oil

extracted from onshore

or offshore oil wells,

raw natural gas

produced as well

• When pipelines and

other transportation

infrastructure are

lacking, vast amounts

of such gas is deemed

unusable and is flared

or vented

• Flaring may occur at

top of a vertical flare

stack (as shown) or at

ground-level in an

earthen pit

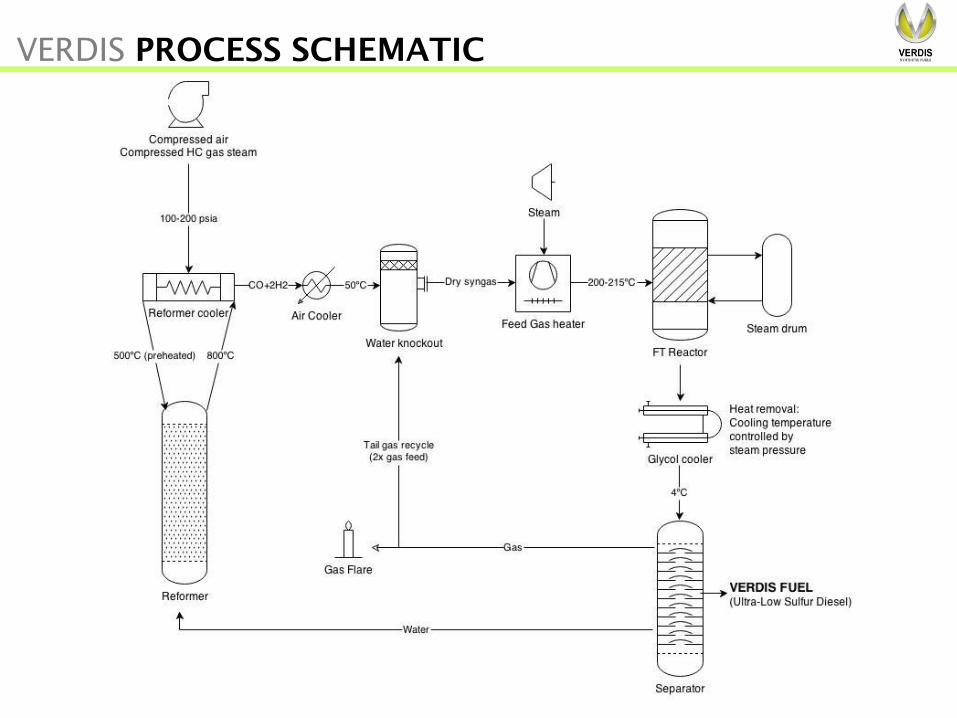

Feed gas

heater

Reformer

CoolerAir

cooler

Water

Knock-

out

Feed gas

heater

FT

reactor

Compressed Air

Compressed HC

gas Steam

100-200 psia

800 C 50 CCO+2 H2

Dry

Syngas

Steam

200-215 C

Heat

removalGlycol

cooler

Gas

Oil

Water

Flare or

combustor

Tail gas recycle (2x

raw feed)

Separator

4 C

VERDIS PROCESS SCHEMATIC

• Higher combustibles (ethane,

propane, etc.) improve diesel

production

• Inerts have no effect

• H2S degrades catalyst

performance and must be

removed, to a level >1 PPM

• This requires a standard gas

scrubber (SulfaTreat or zinc

oxide possible)

• OR: Canada Chemical

Corporation has a proprietary

Batch Oxidation technology

to convert H2S to elemental

sulfur

VERDIS PROCESS STEP 1 – INPUT GAS SCRUBBING

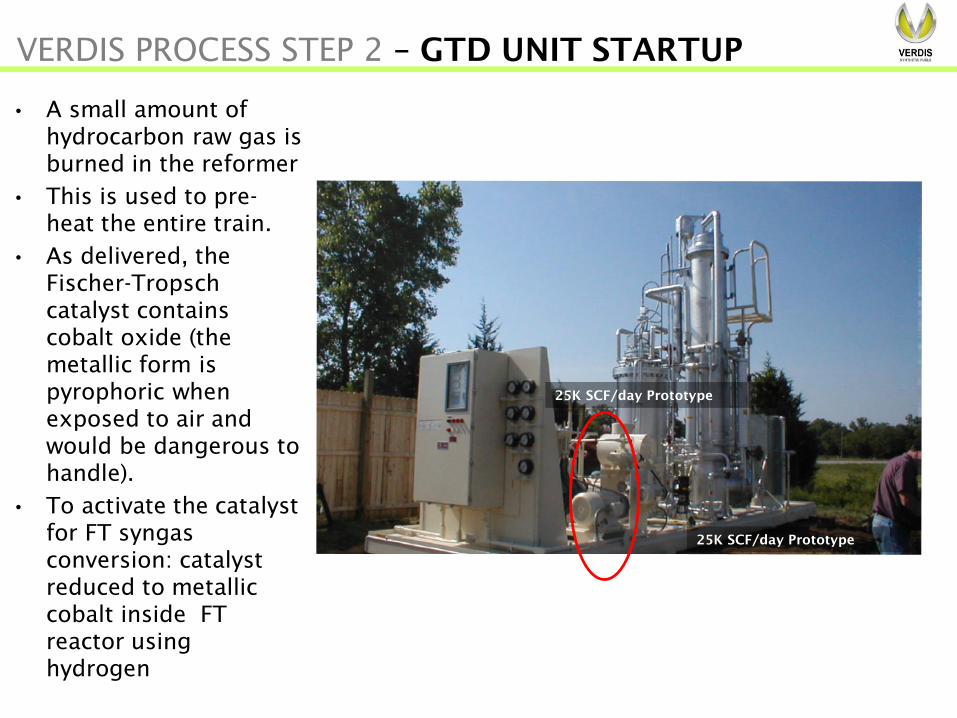

• A small amount of

hydrocarbon raw gas is

burned in the reformer

• This is used to pre-

heat the entire train.

• As delivered, the

Fischer-Tropsch

catalyst contains

cobalt oxide (the

metallic form is

pyrophoric when

exposed to air and

would be dangerous to

handle).

• To activate the catalyst

for FT syngas

conversion: catalyst

reduced to metallic

cobalt inside FT

reactor using

hydrogen

VERDIS PROCESS STEP 2 – GTD UNIT STARTUP

25K SCF/day Prototype

25K SCF/day Prototype

• Feed gas moves into a highly-advanced plasma-based

Syngas Reformer

• Required temperature and pressure (50PSI) is

achieved

• Gas fully prepared for conversion in next stage:

H2:CO ratio sought 2.0

• (Includes compressor, coolers, water knockout,

piping to storage)

VERDIS PROCESS STEP 3 – SYNGAS PRODUCTION

25K SCF/day Prototype

• FT Reactor tubes have optimized fin

shape to dissipate heat, enhance

reaction efficiency

VERDIS PROCESS STEP 4 – DIESEL PRODUCTION

25K SCF/day Prototype

• High capacity Fischer-Tropsch

reactor comprised of 4 inch catalyst

tubes

• Pressure <200PSI, cobalt catalyst

crystallite size 16NM

• Syngas converted into diesel, water,

naptha, tail gasses

• (Includes FT reactor, Dowtherm ®

coolant condenser, coolant

circulation equipment, synthesis gas

recycle loop)

Close-Up: FT Reactor with tail-

gas recycle

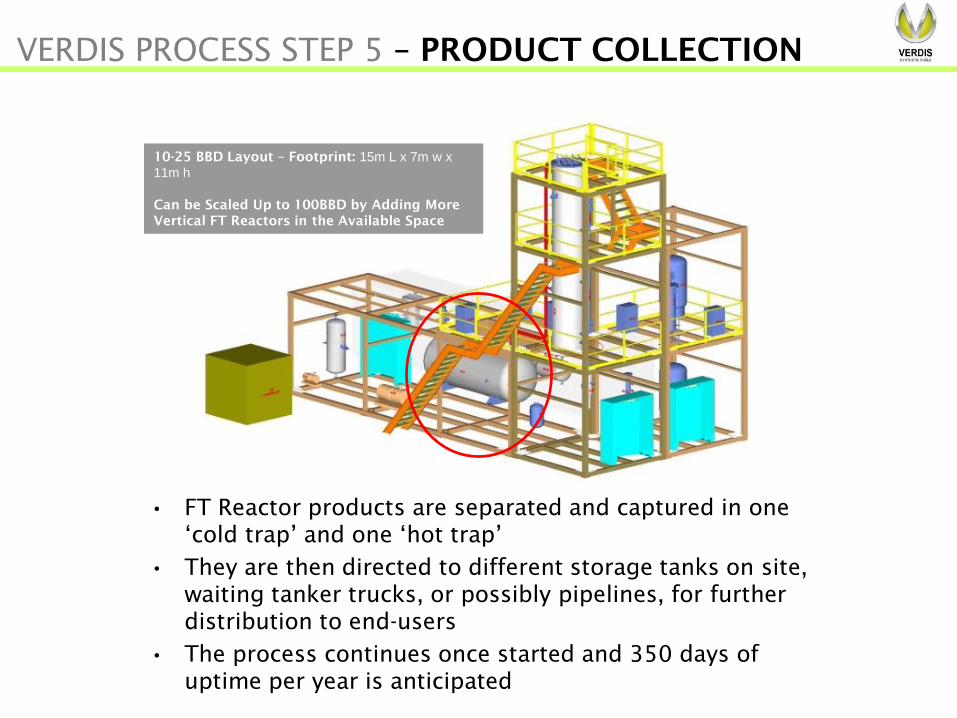

• FT Reactor products are separated and captured in one

‘cold trap’ and one ‘hot trap’

• They are then directed to different storage tanks on site,

waiting tanker trucks, or possibly pipelines, for further

distribution to end-users

• The process continues once started and 350 days of

uptime per year is anticipated

VERDIS PROCESS STEP 5 – PRODUCT COLLECTION

10-25 BBD Layout – Footprint: 15m L x 7m w x

11m h

Can be Scaled Up to 100BBD by Adding More

Vertical FT Reactors in the Available Space

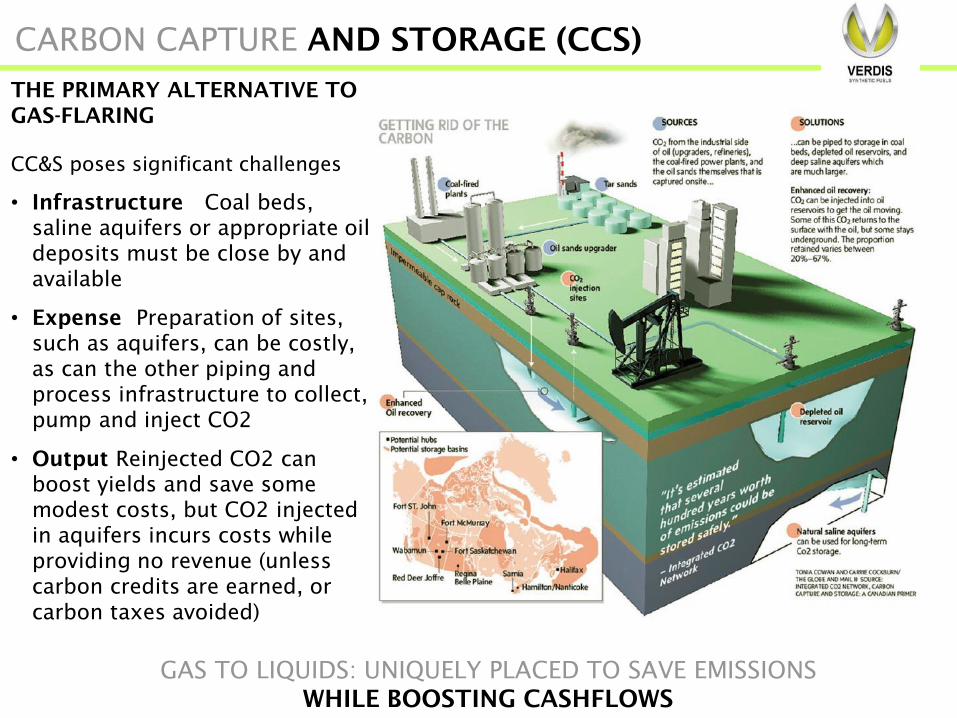

CARBON CAPTURE AND STORAGE (CCS)

THE PRIMARY ALTERNATIVE TO

GAS-FLARING

CC&S poses significant challenges

• Infrastructure Coal beds,

saline aquifers or appropriate oil

deposits must be close by and

available

• Expense Preparation of sites,

such as aquifers, can be costly,

as can the other piping and

process infrastructure to collect,

pump and inject CO2

• Output Reinjected CO2 can

boost yields and save some

modest costs, but CO2 injected

in aquifers incurs costs while

providing no revenue (unless

carbon credits are earned, or

carbon taxes avoided)

GAS TO LIQUIDS: UNIQUELY PLACED TO SAVE EMISSIONS

WHILE BOOSTING CASHFLOWS