VCB

71

ABOUT BANK & BANKING SYSTEM Introduction: Bank and banking are the most important and major factors in today's world economy. Each and every transaction is routed through banking. Not a single business is possible without banking activity. The bank and the business are related. Today we cannot imagine the business world without banking institution. Banking is an important as blood in the human body. Due to the development of banking, advances are increased and business activities developing so it is rightly said, "The development of banking is not only root but also the result of the development of the business world. " The word “bank” derived from the word “bancus” or “banquet” that is a bench. The activities and facilities provided by the bank such as collection of deposits from small investors, lending finance and leasing / cash credit, routine transaction is very important for economic growth on whole. Every economic activity is done through bank in this new era. So every economy whether it is developed, under developing or under developed need strong banking system from the economic point of view. The major task of bank and other financial institution is to act as intermediaries channeling, saving to

-

Upload

sndpdankhara -

Category

Documents

-

view

56 -

download

9

Transcript of VCB

ABOUT BANK & BANKING SYSTEM

Introduction:

Bank and banking are the most important and major factors in today's world economy.

Each and every transaction is routed through banking. Not a single business is possible without

banking activity. The bank and the business are related. Today we cannot imagine the business

world without banking institution. Banking is an important as blood in the human body. Due to

the development of banking, advances are increased and business activities developing so it is

rightly said, "The development of banking is not only root but also the result of the development

of the business world. "

The word “bank” derived from the word “bancus” or “banquet” that is a bench.

The activities and facilities provided by the bank such as collection of deposits from

small investors, lending finance and leasing / cash credit, routine transaction is very important

for economic growth on whole.

Every economic activity is done through bank in this new era. So every economy whether

it is developed, under developing or under developed need strong banking system from the

economic point of view. The major task of bank and other financial institution is to act as

intermediaries channeling, saving to investment requirements of savers are reconciled with the

credit need of investors and consumers.

Definition Of Banking

A banking company is defined as a company, which transacts the business of banking in

India. The Banking Regulation Act defines the businesses as banking by stating the essential

functions of a banker. It also states the various other businesses a banking company may be

engaged in and prohibits certain business to be performed by it.

“The business of banking may be defined as dealing in money and instrument of credit.”

The term ‘banking’ is defined as “accepting”, for the purpose of lending or investment, of

deposits of money from the public, repayable on demand or otherwise, and withdrawal by

cheques, draft, order or otherwise”.

“A bank is an institution which collect money from those who have it to spare, who are

saving it out of their income and lend this money who require it”

According to above definitions these are three important characteristics:

- Bank work as money trading.

- Bank collects deposits and provides interest on the deposits to people.

- Bank provides money or loan to people and collects interest on that.

History Of Banking In India

Banking in India has its origin as early as the Vedic period. It is believed that the

transition from money lending to banking must have occurred even before Manu, the great

Hindu Jurist, who has devoted a section of his work to deposits and advances and laid down rules

relating to rate of interest.

During the Moghal period, the indigenous banker played a very important role in lending

money and financing foreign trade and commerce. During the days of East India Company, it

was the turn of agency houses to carry on the banking business. The General Bank of India was

the first Joint Stock Bank established in the year 1786. The others which followed were the Bank

of Hindustan and Bengal Bank.

The Bank of Hindustan is reported to have continued till 1906 while the other two failed

in meantime. In the first half of the 19th century the East India Company established three banks:

the Bank of Bengal in 1809, the Bank of Bombay in 1840 and the Bank of Madras in 1843.

These three banks also known as Presidency Banks were independent units and

functioned well. These three banks were amalgamated in 1920 and a new bank, the Imperial

Bank of India was established on 27th January 1921. With the passing of the State Bank of India

Act in 1955, the undertaking of Imperial Bank of India was taken over by the newly constituted

State Bank of India. The Reserve Bank i.e. Central Bank was created in 1935 by passing Reserve

Bank of India Act 1934.

In the wake of Swadeshi Movement, a number of banks with Indian Management were

established in the country namely, Punjab National Bank Ltd, Bank of India Ltd, Canera Bank

Ltd, Indian Bank Ltd, the Bank of Baroda Ltd, the Central Bank of India Ltd. On July 19, 1969,

14 major banks of country were nationalized and in 15 th April, 1980 six more commercial private

sector banks were also taken over by the government.

Banking System

The money business performed by the earlier goldsmiths in England has been considered

as the beginning of banking. The goldsmiths who received money for safe custody against their

signed receipt had given an undertaking to return the money to the depositor or to the bearer on

demand. After developing their work they realized that landing others money for a fixed period

of time was profitable.

In 1770 first Indian banks know as bank of Hindustan was started and was close down

twenty year later. Then East India Company started three presidency banks with government

participation i.e.

o Bank of Calcutta 1806

o Bank of Bombay 1840

o Bank of Madras 1843

o Allahabad Banks 1865

o Alliance bank of Simla 1873

Unit Banking:

The method of unit banking is carrying on banking business through a single office, or in

some cases a few offices in a limited area. It is known as localized banking.

Branch banking is a method of carrying on banking business by big banking companies

having several branches throughout a country or territory. For example, in United Kingdom,

most part of the banking business is in the hands of five big banks.

Branch Banking:

Over the years, the structure of banking also has undergone tremendous changes.

Consequently, several systems of banking have emerged in the branch banking.

Branch banking is a system in which every bank work is a legal entity having one board

of directors and one group of shareholders and operates through a network of branches spread

throughout the country. The head office of the bank is located in a big city or state capital the

braches operate throughout the country. Thus branch banking is another name for de-localized

banking which arise on business through a number of offices.

Group Banking & Chain Banking:

If the affairs of a group of banking companies are controlled by a holding company it is

known as group banking.

In case a number of banks are controlled by one few individuals and interlocking

directorate through purchase of share of such banks, it is known as chain banking.

Investing Banking & Mixed Banking:

Investment banks invest or help investment of funds in the shares or bonds of joint stock

companies. These banks act as intermediaries between business corporations and investors.

The combination of investment banking with commercial banking is known as ‘mixed

banking’ mixed banking has certain important short comings.

Introduction Of Co-Operative Bank

Co-operative banks were first introduced India in 1904 by passing Co-operative Credit

Society Act(CCSA). This form of organization was intended to the agriculturists and artisans

coming together and educating them in the case of credit and inculcating the habit of saving co-

operation and self-help.

The distinguishing feature of Co-operative banks is the absence of profit motive. Co-

operative banks are very helpful to meet the requirements of small farmers, artisans, gruh udhyog

, small urban business etc. In India, Co-operative banks have been pioneers in mobilizing rural

deposits. Today however, the Co-operative banks have putting more weight on their lending

activities than on deposit mobilization.

All the Co-operative credit societies were brought under the purview of the Banking

Companies Act 1966. The RBI has been vested with the power and controls the Co-operative

banks. The government of India has encouraged the Co-operative movement in banking.

Therefore, Co-operative banks are developed from one place establishment to district level, state

level, state level, and also the central level. Co-operative banks raise their funds through various

means. They receive all kind of deposits and make them available as lend able fund to its

members.

Definition Of Co-Operative Bank

“A Co-operative is an autonomous association of a person’s united voluntarily to meet

their common economic, social and cultural needs and aspiration through a jointly owned and

democratically controlled enter price”

“Co-operation is an effective self-reliance done by organism”

“Co-operation is one type of organism in which people join willingly to encourage their equal

financial interest.”

“Co-operation is the step taken for equal profit or loss under mutual management by mutually

using their own resources and factors willingly.”

Primary Co-operative Societies

State Co-operative Bank

District Co-operativeBanks

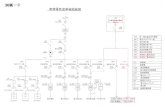

Structure of Co-Operative Bank

(Under Control of Reserve Bank of India)

Reserve Bank of India

State Co-operative Bank:

The State Co-operative Bank is federation of Central Co-operative Bank and acts as a

watchdog of the Co-operative banking structure in the state. Its funds are obtained from the share

capital, deposits, loans and overdrafts from the RBI. The State Co-operative Bank lends money

to central Co-operative Banks and Primary Societies and not directly to farmers.

Central Co-operative Banks:

These are the federation of primary in a district and are of two types those having a

membership of societies as well as individuals. The funds of the Banks consist of share capital,

deposits and overdrafts from State Co-operative bank and joint stocks. These bank finance

member societies within the limits of the borrowing capacity of societies, they also conduct all

the business of joint stock bank.

Urban Co-operativeBanks

ScheduledCo-operative

Bank

Non-ScheduledCo-operative

Banks

Primary Co-operative Credit Societies:

The Primary Co-operative Credit Societies are an association of borrowers and no

borrowers residing in a particular locality. The funds of the societies are derived from share

capital and deposits of members and loans from Central Co-operative Banks. The borrowing

power of member as well as of the society is fixed. The loans are given to members for the

purchase of cattle, fodder, fertilizers, pesticides, implements etc.

Urban Co-operative Banks:

Urban Co-operative bank has been defined as Primary Co-operative Bank in the banking

regulation Act 1949 (as applicable to Co-operative Societies), in terms of section 5(ccv) of the

said Act. The paid-up share capital and reserve of which are not less than rupees 5 lack, and the

bye-laws of which do not permit admission of the any other Co-operative society.

Most of the Urban Co-operative Banks are small in size and unitary in character. The

deposits of Urban Co-operative Banks are equivalent to 9% of commercial banks deposits. Few

states such as Maharashtra, Gujarat, Karnataka, Andhra Pradesh and Tamilnadu account for over

80% of urban Co-operative Banks in these 5 states is mainly on account of emergence of strong

Co-operative leadership.

Function of Co-Operative Bank

Co-operative Banks are formed on the principle of Co-operative to Extend Credit

facilities to farmers and small scale industrial concerns and promotes in general the habit

of thrift and self help among the low and middle income groups of the society.

Co-operative has been putting more weight on their lending activities than on deposit

mobilization.

The main function of Co-operative credit society was to provide cheap credit to the

members who are small people with small means and small needs and finance.

The Co-operative Banks have a three tier set up. The state co-operative bank, while

central district co-operative banks function at the district level and primary credit

societies work of the village level.

Co-operative banks proceed on the principle of co-operation. Co-operative Banks

maintain the cash reserve and liquid assets in relation to deposit only.

To arrange the programs regarding the Economic welfare of its members.

This bank supervises the functioning of primary credit society and gives training,

guidance and advice to the employee of credit society only.

The Varachha Co-Operative Bank Ltd.

Introduction:

The people in Saurashtra, located in western part of Gujarat, are always depending upon

the rain-fed cultivation. As a search for income generation in an alternate way for their survival,

the peoples have chosen Surat city, where there is a good scope for trade in Diamond and Textile

sector. Well of people have entered into the trading sector and the others on labour front. In a

phased manner, the population of the people, involved in diamond trade, belonging to Saurashtra

increased to a sizeable extent in Surat and in particular in the area of Varachha. It was become

obvious for a necessity of a bank for their own people; the efforts were taken by a well known

philanthropist, story writer and columnist in local dailies, Mr. P. B. Dhakecha, founder chairman

of The Varachha Co-operative Bank Ltd., Surat. As such, The Varachha Co-operative Bank Ltd.

came into existence on 16th October 1995 and Inauguration ceremony was done by on the hand

of Shree Swami Sachidanand. Some of the Varachha Co-operative Bank Ltd., directors are

belonging to diamond trade, who are official site holders of getting rough block diamonds from

foreign countries.

At the end of the first financial year the number of shareholders was 4484, Share Capital

Rs. 57.44 lakh, Deposits Rs. 2.70 crores, Advance Rs. 2.07 crores and profit stood at Rs. 4.77

lakh.

The Varachha Co-operative Bank Ltd. has gradually developed the Banking activities and

at the end of 5th year, with a network of 5 branches, the share capital and reserves raised to more

than Rs. 8 crores and the deposits have crossed 100 crores mark, which is a rare phenomenon in

Co-operative Banking Sector in all over India and the number of depositors have increased

58222. The Bank has been awarded with First Prize for the best performance among all Co-

operative banks in Surat District during the Financial Year 2000-01. At dated on 31 st March,

2009 the share capital raised Rs. 4.63 crores to Rs. 5 crores, reserves raised 39.07 crores to 42.71

crores and Advances Rs. 92.03crores. The deposit is Rs. 171.57 crores. Total 10 branches. At

dated on 31st march,2011 advances Rs.115.88 crores. The deposit is Rs 273.95 crores.

History And Development:

The Varachha Co-operative Bank Ltd., Surat was established with license No. BD Guj.

1153 p Date: 27/1/95. The Register office of the bank is at Affil Tower, L. H. Road, Surat-6

within the period of 4 month after obtaining license. The bank was inaugurated by the respected

saint swami Sachidanand, vice chairman of Surat district co-operative bank and other people on

16th October 1995 with opening of the bank by swami Sachidanand. With the help of the

progress of the varachha co-operative bank, the committee of varachha co-operative bank was

introduced Kamrej branch on dated 7th June, 1998

It was became the first giant and fast developed computerized and well staffed bank in

Varachha area. During its work bank get splendid respect and also account holder get more

satisfaction by better services.

By the attraction of the customers & good support of the board of directors, varachha co-

operative bank Ltd. Introduced second branch in ring road on dated 4 th July, 1999. And 2nd July

in 2000, the varachha co-operative bank introduced kadodara branch. Than the fourth branch of

varachha co-operative bank introduced in 28th January, 2001 at Kapodra. And the fifth branch

which was introduced on dated 26th February, 2001 at Katargam area.

Because of best services and customer satisfaction, The Varachha Co-operative Bank

Ltd., Surat build unbelievable growth and bank show its efficiency by launch five branches at

Kamrej started on 7th June 1998, Ring road branch was started on 4 th July 1999, Kadodara branch

was started on 2nd July 2000, Kapodra branch on started on 28th January 2001, Katargam branch

started on 26th February 2001, and Punagam branch started on 16th October 2008, Sachin branch

started on 10th May 2011, Navsari branch started on 15th January 2012, Ahmadabad branch

started on 15th April 2012. Recently bank has started its 11 th branch at Ankleshwar on 23rd

june,2012 and planning to open 5 new branch around surat city in the financial year 2012-13.

By this continues and high growth of The Varachha co-operative bank ltd., Surat it get

“Rashtra Vikas Ratna Award” on 15th December 2003 and first award for doing best banking

operation among co-operative banks of Surat district.

The main characteristics of The Varachha Co-operative Bank Ltd, Surat are:

Faith

Service

Transparency

Success

And also The Varachha co-operative Bank Ltd. gets rank in top co-operative bank of Surat

district.

Vision And Mission of The Varachha Co-Operative Bank Ltd

Mission:

The Varachha Co-operative Bank Ltd. Surat is Committed to satisfy its banking customers,

Share holders, employees and regulators through continually improving banking services,

innovation in products, technology up gradation, knowledge of team work and strengthening

customer relationship.

Vision:

Banking customer through faster services and innovative products.

Share holder through regular dividend.

Regulators through higher rating during inspection audits.

Technically qualified staff to meet challenges of high-tech banking.

Inter branch connectivity.

Banker’s presence in metros.

Introduction of full-fledged specialized branch.

No.1 Urban Co-operative Bank for business & profit per employee.

Objectives:

To give possible help and necessary guidance to members of the bank in the conduct of

business.

To do every kind of trust and agency business and particularly do the work investment of

funds, sale of properties and of recovery or acceptance of money.

To accept money document, security calculate article and goods every description for

keeping them in safe custody or for sending them from one place to other.

To act as a balancing center for surplus funds of co-operative societies. To organize and

develop co-operative societies within the district.

To redeem old debts.

To lend money on security to its members

SWOT Analysis

Strengths: o The staff member of the concern is well-experienced and trained enough.

o The bank is providing training to new employees.

o The accounts of share holders as well as customers are fully secured by insurance.

o The bank has good brand image.

o The turnover of manpower in the bank is very less and staff members are well satisfied

with the facilities given to them.

o The profit of the bank is continuously increases.

o Customers are serviced in the best manner.

o By honoring the social welfare concept the bank is providing society welfare.

Weakness:

o There is lack of linking performance.

o In recent competitive era, varachha bank not provide some modern facilities like ATM

service, debit card, credit card and even not website on intent for show the growth of

bank.

o Rules for deposits and loans are very strict opening deposit is high and they require

perfect documents, it can be limitation for slow inflow of deposits.

Opportunity:

o The bank has good market potential so that it can enhance or expand its business in

future. The bank has to start its branches in the areas like City Light, Adajan, and Sachin

and out of city or state should pick up the opportunity to discover the market.

Threat:

o If there will be any union, it will cause problem for the bank.

o If there will be any opening of new bank with more facilities than other banks, it will

hinder the progress of the bank.

o If there will any political pressure on the banking sector it will lead to decrease in

productivity and efficiency.

HRM

Introduction:

According to The Institute of Personnel Management , London , U.K. States that “

It is that part of management concerned with people at work and with their relationship

within an organization. Its aim to bring together and develop into an effective

organization the men & women who make up an enterprise and having regard for the

well being of the individual and working groups to enable them to make their best

contribution to its success.

In the HRM the recruitment , selection & induction , training & development , promotion

, wage & salary , personal records etc are create an important role.

Organization Structure

Board Of Directors

Managing Director/General manager

Assistant General Manager

Branch Manager

Officer Officer Officer

ClerkClerkClerkClerk

Recruitment and Selection:

Meaning of Recruitment:

Recruitment is generating of application or applicants for specific positions through three

common sources i.e., Advertisement, state employment exchange agencies and present

employees.

At present, The Varachha Co-Operative Bank undertaking ‘Rationalization’ i.e. it selects

candidates from inside the organization. Therefore, there is no need to recruit or select more

people from outside the organization. But when there is any vacancy in the organization, the

selection process is as under:

Advertisement in the newspaper.

Interview

Selection

Induction

The Varachha Co-Op. Bank Ltd takes written test & personal interview to recruit

the employee. The recruitment process is handled by the Board of Directors. They recruit only

post graduated qualify persons and then give post to perform the duty.

Selection:

“Selection means to select the best applicant out of all the application.”

In The Varachha co-operative Bank selection process is as follow.

A. Preliminary interview:

In this step bank can classified all the Qualified and unqualified employee and decide which

type employee are needed in our bank like skill, knowledge, education experience etc. in this

way bank decide the all employees.

B. Application form:

In this stage bank can to print one form in this form. Bank collect all the information about

employees like

Identifying Information

Personnel Information

Physical Characteristics

Family Background

Education

Reference etc.

C. Selection Test:

In this step bank take some psychological test for checking personnel mental level, some skill

like intellectual etc. so by this test help bank take selection test and select the employees.

D. Employment Interview:

In this step bank cover all the point which are not included in application form selection test

etc. bank give information about bank to employees and take his personnel information or

view about bank services.

E. Medical Examination:

The Varachha co-op. Bank Ltd. check physical feature of the candidate and then can select

them.

F. Reference Checks:

In this step bank can check the reference of candidate and check which person or institution

are known of candidate behavior then decided other step.

G. Final Approval:

Banks sees all the above step very carefully then takes any decision and selects the any

candidate out of total application for job.

Placement:

Placement means to assign any particular job to candidate for doing it and approve himself.

The Varachha co-op. Bank Ltd. take all the step for the select good candidate then assign job to

candidate.

After the select candidate give any task of candidate for performed it. In above way bank can

placement of any candidate.

Training and Development:

“Training means the changing of skill, knowledge, attitude or social behavior towards the

requirement of job and organization.”

After selection and placement step organization give the training of new candidate because new

candidate are totally unknown of our organization on so that person give the induction training.

Bank gives the induction training and this can involve some point which are as follow:

Give history of bank. Bank's ethics Bank’s organization structure Bank’s terms & conditions Bank’s rules & regulations Wages system Discipline of the bank Welfare facility Health and safety measures Job description etc.

In above way lot of information gives in the induction training and can do support the new candidate for doing easy work with senior staff member.

Promotion:

The Varachha co-operative Bank gives promotion to their employees on the basis of

experience, efficiency with his work. The employees are entitled to get promotion only when

they have performed their job with good, respectable and efficiently.

Transfer:

Transfer means that a literals shift passing movement of individual from one

position to another usually without involving any marketed changed in duties ,

responsibilities , skills needed or compensation.

In the bank transfer must be given to employee, after 4, 6 and 8 month from one

department to other department or one branch to other branch. So that he can able to handle

every department of bank.

Wages and Salary Administration:

In the Varachha Co-operative bank wages and salary is given on the basis of employee's

designation such as manager, system officer, officer, senior clerks, junior clerks and peons.

The Varachha Co-operative Bank give the wages according to seniority of employees and

give performance based. Bank gives the monthly salaries which are directly credited to the

employees account before the close of month.

The bank employee also given dearness allowance like – medical allowance, city

allowance, house rent allowance etc. at the rates which are decided in the meeting.

Personal records:

Name of employee

Local and Permanent

address

Appointment of training

Detail about past

Previous employment

Qualification

Promotion

Awards

Accident Record

Disciplinary Record

Retirement

Photograph and Height, Sex,

Marital Status, etc.

Finance

Introduction:

Financial statements are prepared for the purpose of presenting a periodical review or report

on the progress by the management and deal with

The status of investment in the business and

The results achieved during a period under review.

The statement disclosing status of investments knows as Balance sheet and the statement

showing the result is known as profit & loss A/c. A firm communicates financial information to

its share holder, creditors and other users through financial statements and reports. The financial

statements contain summarized information of the firm’s financial affairs, organized

systematically. The report is presented at bank’s annual general meeting along with new

proposals.

Definition:

“Financial statement is methodical analysis through classification, comparison and

interpretation of data in financial statement to diagnoses financial soundness (profitability,

viability, soundness).”

As the statements are used by investors and financial analysis to examine the firm’s

performance in order to make investment decisions they should be prepared very carefully and

contain as much information as possible. The financial statement are prepare from the accounting

records maintained by the firm. The focus of financial analysis is on key figures in the financial

statements and the significant relationship that exists between them. In brief, financial analysis is

the process of selection, relation and evaluation.

Financial Performance

No Particular

2008 2009 2010 2011 2012

1 No. of share holder 11569 12669 13566 17192 18837

2 Share capital(In Cr) 4.63 5.24 5.91 7.29 7.90

3

Reserve & surplus

39.17 42.71 46.41 51.98 58.53

4 Total deposit(In Cr) 168.27 171.57 224.16 273.95 289.70

5 Total Loan(In Cr) 80.23 92.03 94.89 115.88 155.88

6 Net Profit(In Cr) 2.81 3.02 3.15 4.05 5.06

7 Working Capital 221.15 226.96 320.38 347.09 374.31

8 No. of A/c holder 99907 105674 115528 121922 132277

9 No. of Loan Taker 89999215

7739 6593 7972

11 Dividend 12% 12% 12% 15% 15%

From the table it is clear that the bank had achieved a strong financial position with

around 300 crore deposit and it is sufficient for any co-operative bank to be registered as

a schedule bank.

Bank had increased sanctioning of loan and advances year by year which shows the

lending capacity of it.

The most important thing i.e. Net profit of the bank is increasing year by year which

shows good efficiency and confidence of the management.

Bank has get good depositor class customer base as it is seen in the number of account

holder every year increases which shows confidence of the society in the bank.

The shares holders are really get benefited when they get good return on their investment.

Bank gives 15% dividend from last two years.

Services Provided By the Varachha Co-Operative Bank

The Varachha Co-operative Bank Ltd. providing different kinds of facilities and services to

different member:

1. To Shareholder:

o As a member of share holder of varachha co-operative bank, Bank provides

accident insurance of Rs. 200000 to its share holders.

o The varachha co-operative bank provides dividend at 15% to its share holders.

o The Bank provides Scholarship to the children of its share holder for the purpose

of higher education and set of books every year.

2. To Employee:

o The Varachha Co-operative Bank provides life and accident insurance to their

each staff member.

o They also providing high interest rate on deposit and low rate of interest on loan

to their employees.

o They also provide personal computer & personal printer to their employees.

3. To Customer

o VAT (View Account Terminals) machine facility to tale of customer account. By

this machine customers can knows their balance by entering pin-code and account

number.

o They also providing tale banking & mobile banking facility to their customers. By

this process customer can know his/her account balance anywhere.

o Bank provides Safe deposit lockers to their customers.

o GEB bills collection facility is also available at Kamrej, Ring road, Kapodra,

Kadodara branches for customer.

Day To Day Operation

New account department:

New Account is opened as well as old accounts are closed in this department. 3 kinds of

Accounts are:

Current Account.

Saving Account.

Fixed Deposit (FD) Account.

Daily nearly on an average about 6 to 8 Current accounts and 10 to 15 saving account are

opened. The procedure for opening new accounts:

Requirements:

o Two photographs of the account holder

o If the account is opened for company or firm then the photograph of the directors or

proprietors or administrator,

o Documents which give true and fair residential address such as driving license, rationing

card, light or telephone bill, school living certificate etc.

o The minimum balance require for current account is Rs.5100

o The minimum balance for saving account is Rs.1100.

o Any account holder, current or saving, can’t close his account before completion of six

months in the bank.

Issue of cheque book and pass book:

This is important department of the bank. In this department new passbook and cheque

book are issued. The new account department gives details of new customers and according to

that new cheque book and passbook are issued.

Customers who are in need of a new cheque book have to apply a day before with a

counter given in the old cheque book. For each account holder it is compulsory to allow at least

five cheques to be cleared or presented to bank for issuing a new cheque book.

Draft, O.B.C, I.B.C Department:

As this bank is in co-operative sector it has limited branches in Surat. It does not have

any branch in any other part of the country. So in order to provide draft service of different cities

to its customers it has collaborate with certain banks.

If a customer wants a draft for Bombay, a bank must have its branch which can discount

the draft and if the bank do not have a branch than it has to joint with other bank.

The Varachha Co-operative Bank has arrangements with the I.D.B.I bank, HDFC bank

and YES bank for the issue of the draft, RTGS and NEFT in different cities of the country.

Token Department:

Token is issued after various strict verification of cheque such as signature, date, amount

(in figure as well as in words) etc. Bank has a special service for its customers i.e. up to

Rs.20,000 for saving account holders and no limit for current account holders can be withdrawn

directly from the cash counters without the procedure of Token.

Transfer Department:

In this department the cheque of the same bank is transferred from one account to other

account of customers. The entry of other department such as IBC (Inward Bill Collection) and

O.B.C (Outward Bill Collection) etc. is done from this department.

Loan Department

Meaning Of Loan:

Loan is type of promises under which bank gets ready to lend money to a borrower for a

fixed period. Borrower needs it for specific purposes so bank is ready for lending him a credit for

a specified period. In this period borrower has to repay it with interest and installments.

In other words “when a banker makes a advance in a lump-sum which cannot be paid

wholly or partly and which the customer has permission to withdraw subsequently, it is called a

loan.” Loan are promises for future payment, they have to be repaid in periods beyond a year and

are therefore long-term liabilities.

Loan can play a significant role in times when borrower needs funds for fixed assets or

non-respective type of activities and thus seeks money from the bank that is withdrawn in one

lump sum. The loan amount is normally repaid in installments. Loan may be short-term,

medium-term or long-term.

Loans and advances are classified into secured and unsecured.

Secured Loan or Advance:

Secured loan or advance means a “Loan or Advance made on the security of assets. The

market value of which is not at any time less than the amount of such loan or advance.”

Unsecured Loan or Advance:

An unsecured loan or advances means a “Loan or advance not so secured. A partly

covered loan or advance is partly covered by the security of assets, the market value of such

securities being less than the amount that has been lend or outstanding at any time.

Loan Procedure:

First of all, there is submission of loan application with all relevant documents normally

required, and submitted by borrower to the bank.

After submission of application, needed securities be obtained by bank and appraisal made

on the security as well as on the loan borrower and on its business.

The next step is that proposal being forwarded to Loan committee.

After clear scrutiny on the proposal, the board can give approval for sanctioning a loan.

Many times, some specific conditions being received from board.

After fulfilling the conditions the borrower must make documentation as required and

signing of paper as needed by bank.

At the last stage, banks make disbursement of loan under various types of loan scheme.

Loans & Advances:

Loan Type Rate (in %)Rebate (%)

Surety Loan for Members 14.00 1

Two Wheeler 13.00 1

Four Wheeler 13.00 1

Cash Credit / OD 13.00 -

Machinery Term Loan 14.00 1

Machinery TUF Loan 14.00 1

Gold loan 11.00 -

FD Loan + 2% -

NSC Loan 13.00 -

Housing Loan 12.00 1

Credit Schemes Offered By The Varachha Co-Op. Bank:

The Varachha co-op. bank has performed good work by offering various type of credit to

its customer. So bank also bring new schemes from time to time for increasing its effectiveness

and consumer base with existing customer. The followings are the various types of Credit

offered by the Varachha Co-operative Bank:

Vehicle Loan:

The Varachha co-operative Bank provides loan for purchasing various types of vehicle

such as two, three and four-wheeler.

Generally vehicle loan is completed within 3 years but above 1 lakh loan or generally for

four wheelers loans is to be completed within 5 years with monthly installments.

Limit: - There is no limit for Vehicle loan. Bank sanctioned credit up to 70 to 75% of

quotation.

Rate of Interest:

Particular Interest rate Rebate Net rate

Vehicle loanUp to Rs 1 lakh 13%

Above Rs 1 lakh 13%

1%

1%

12%

12%

Margin: - Margin for Vehicle loan is 25% to 30%.

Security: - Bank provides loans against equitable mortgage and against hypothecation of

the proposed vehicle to be purchased.

Requirement for Vehicle Loan: -

o All basic documents.

o Income evident of loan applicant as well as two guarantors.

o Photocopy of property submitted to bank.

Register certificate (RC) book of vehicle is kept by banks. When total installment of

vehicle loan is paid, at that time RC book and other original documents are given back to Loan

holder.

Cash Credit (CC)/Over Draft (OD):

A Cash Credit is a facility by which a banker allows his customer to borrow money up to

certain limit against either a bond of credit by one or more securities. This is most common mode

of borrowing by large commercial and industrial house in India because the advantage that

customer need not borrow the whole amount at one time but may draw such amount as he/she

requires at different times.

The bank provides these facilities to borrower for meeting their temporary needs and to

solve problem related to short-term capital.

Limit: - There is no limit for Cash Credit and Over Draft.

Rate of Interest: -

Particular Interest rate Rebate Net rate

Cash credit &

Over Draft loan

Up to Rs 2 lakh 13%

Above Rs 2 lakh 13%

-

-

13%

13%

Margin: - Margin for Cash Credit and Over Draft loan is 15% to 20%.

Security: - Bank provides loans against up to mortgage and hypothecation provide by

applicant.

Requirement for Cash Credit and Over Draft loan: -

o All basic documents.

o Evident of other income of proprietor or partner.

o Director signature.

o Firm’s last three years balance sheet and income tax return copy.

o Statement of last six month of firm’s account in the bank or other banks.

o To include certificate of company registration and articles of association if

applicant is private limited company.

Machinery Loan:

The Varachha Co-operative Bank sanctioned a loan to applicant who wants to adopt new

technology, machinery, equipment etc. for expanding his business.

Limit: - Maximum limit for Machinery loan is Rs. 99, 99,999/-

Rate of Interest: -

Particular Interest rate Rebate Net rate

Machinery loanUp to Rs 2 lakh 14%

Above Rs 2 lakh 14%

1%

1%

13%

13%

Margin: - Margin needed for Machinery loan is 25% to 35%.

Security: -Bank sanctioning loans against up to mortgage and hypothecation provided by

applicant.

Requirement for Machinery loan:

o All basic documents.

o Machinery list and Xerox of bills.

o Invoice of purchasing new machinery.

o Evident of other income of proprietor or partner.

o Director signature.

o Firm’s last three years balance sheet and income tax return copy.

o Statement of last six month of firm’s account in the bank or other banks.

Fixed Deposit(FD) Loan:

The Bank provides loan against fixed deposit. In fixed deposit loan applicant takes loan

against fixed deposit certificate. During this time certificate will have lien under the bank. This

loan is based on renewal and any applicants invest his money in fixed deposit scheme with

different rate.

Limit: - Bank can give loan up to 75% of against fixed deposit.

Rate of Interest:

Particular Interest rate Rebate Net rate

Fixed Deposit

Loan F.D. rate + 2% --F.D.rate+2

%

Margin: - Margin for fixed deposit loan is up to 25%.

Security: -Bank keeps fixed deposit certificate of borrower.

Requirement for Fixed Deposit loan:

o All basic documents relevant to applicant. No need of guarantors.

o Fixed deposit certificate of borrower.

Loan against Government Security:

The Varachha co-operative Bank provides also loan against government security such as

National Saving certificate, Kishan Vikas Patra(KVP) etc. For this loan, before making an

advance on the securities of the NSC& KVP, the bank should take an applicant in the prescribed

form from the borrower in whose name the certificate stand. This certificate should then be sent

to the concerned post office or the issuing authority for transfer to the lending banks name.

Banker should grant the advance after made on the certificate or after new certificate.

Limit: -Bank gives advance up to 65% against the NSC/KVP certificate.

Rate of Interest: -

Particular Interest rate Rebate Net rate

NSC/KVP Loan 13% -- 13%

Margin: - Margin need for NSC/KVP loan is 35%.

Security: -Bank keeps NSC/KVP certificate of borrower.

Requirement for NSC/KVP loan: -

o All basic documents relevant to applicant. No need of guarantors.

o NSC/KVP certificate of borrower.

Gold Loan:

Sometimes people need some financial help to meet their daily requirements. In these

circumstances the bank gives loan against the pledge of their jewelry considering the value of the

jewels. The bank issued major part on gold because gold loan is safety one. Borrower has no

need to bring any guarantor.

Limit: - Loans sanctioned against the gold. So on the basis of gold provide by applicant,

bank issued advance to him. Bank gives advance up to 60% of gold value.

Rate of Interest:

Particular Interest rate Rebate Net rate

Gold Loan 11% 1% 10%

Margin: - Margin need for Gold loan is 40%.

Security: - Loan provides against gold ornaments.

Requirement for Gold loan: -

o All basic documents and personnel information of applicant. No need of

guarantors.

o As a security gold ornaments provide by applicant.

Staff Loan:

Such credit is provided only to the staff members of the bank. This loan is provided for

meeting any financial needs, for any social occasion in family and for purchasing any respective

items such as vehicle, house etc.

Limit: - Bank gives loan amount up to Rs 30,000/-.

Rate of Interest: -

Particular Interest rate Rebate Net rate

Staff loan 6% -- 6%

Margin: - No need of margin for Staff loan.

Security: - Bank needs salary slip of applicant required for staff loan.

Requirement for Staff loan:

o One photocopies of applicant as well as two guarantors the work in the bank.

o Personnel information of applicant as well as two guarantors.

o Submit the application form with salary slip.

Other Services

Net Banking Service:

Bank Started Net Banking Service for their respective customer since 02-Oct-2009. With

help of Net Banking customer can view his/her account related information like statement,

inward clearing, outward clearing etc. from anywhere.

Any Branch Banking (ABB):

Customer can transact his/her account from any branches of the bank like cash receipt,

payment, transfer, balance inquiry, statement/passbook printing, deposit outward clearing etc.

CCTV Monitoring:

Bank’s all branches has CCTV Camera and all this connected and monitored at Head

Office. With the help of CCTV Bank is able to search any fraud with customer or employee of

the bank.

E-Payment Facility:

Bank has started E-payment facility for the customers of the Bank for the purpose of

payment of Income-Tax.

RTGS/NEFT Facility:

Real Time Gross Settlement (RTGS), National Electronic Fund Transfer (NEFT) Facility

available to the customer of the bank. By this facility customer can transfer his balance

throughout India of any Banks, which is member of RTGS/NEFT. Maximum limit of NEFT for

transferring funds is Rs.200000. If the customer wants to transfer more than this limit then they

have to refer RTGS compulsory. The fund transferring period in RTGS is maximum 8 hours,

which is set by the RBI.

Mobile Banking System:

Now you can get the information such as Balances, Transaction Details, Cheque Status,

Deposit rates and much more… sitting at your home or office.

Bank has a centralized mobile banking facility. Through this facility customer can know

his/ her balance via SMS for getting various details about their accounts like Current Balance,

Cheque Return Status, FD Rates, and Loan Rates etc. Bank also send regularly SMS to the

registered customer like cheque inward/ Outward return details, FD rates, any event etc.

VAT (View A/c Terminal) Machine:

VAT machine is available in the all branches of the bank.. With the help of VAT machine

customer can view various details of his/her A/c. like Balance, Statement etc. For avail this

facility customer should have registered his account with bank and get 4 digit passwords from

the bank’s Officers.

Locker Facility:

Locker Facility is also available at Bank’s Kamrej, Kapodra and Katargam Branches with

nominal rental. There is various types of locker followed by its size.

Franking of Adhesive Stamp:

Bank has Franking Machine under license from Government for stamping of Non

Judicial Stamp arranged by Revenue Dept. of Gujarat State.

Comparative Statement of Loan

2010 2011 2012

A) Short term Credit:

Gold Loan (Up to 1 lakh) 0.48 8.97 18.99

Cash credit 1.60 1.90 2.20

Overdraft 0.44 3.05 0.90

B) Medium& Long term

Credit:

Against NSC/KVP 0.0075 0.0039 0.0056

TWO Wheeler loan 0.71 1.34 1.81

Staff TWO Wheeler loan 0.02 0.07 0.08

FOUR Wheeler loan 1.67 7.98 11.56

Machinery Hypo.(TUF) loan 9.44 13.13 11.33

Staff Housing loan 0.39 0.38 0.44

Loan Against Fixed Deposit 0.07 0.15 0.23

Self Employment Loan 0.0029 0.12 0.20

Term Loan 0.09 0.25 0.58

Surety Loan 0.44 1.04 2.14

Particular Year (Amount in Crore)

1) Gold Loan( Up to 1 lakh) :-

YearLoan

2010 2011 2012

Gold Loan(Rs. In Crore)

0.48 8.97 18.99

2010 2011 20120

2

4

6

8

10

12

14

16

18

20

0.48

8.97

18.99

Gold Loan( upto 1 lakh)

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in 2009-10 the gold Loans are sanctioned of Rs. 0.48 Crore and in 2010-11

the gold loan are sanctioned of Rs.8.97 Crore which shows rapid increase in the credit to the

customers and increasing year by year.

2) Cash Credit(CC):-

YearLoan

2010 2011 2012

Cash Credit(Rs. In Crore)

1.60 1.90 2.20

2010 2011 20120

0.5

1

1.5

2

2.5

1.6

1.9

2.2

Cash Credit

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank has sanctioned cash credit of Rs. 1.6 crore and in

2010-11 of Rs. 1.9 Crore and in the year 2011-12 of Rs.2.2 crore. By doing comparison the

amount of loan, it is increased by 18.75% in the year 2010-11 as compared to year 2009-10 and

increase of 15.78% in the year 2011-12 as compares to year 2010-11 which shows the credit

policy of the bank.

3) Overdraft (OD):-

YearLoan

2010 2011 2012

Overdraft(Rs. In Crore)

0.44 3.05 0.90

2010 2011 20120

0.5

1

1.5

2

2.5

3

3.5

0.44

3.05

0.9

Overdraft

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank has sanctioned Overdraft of Rs. 0.44 crore and in

2010-11 of Rs. 3.05 Crore and in the year of 2011-12 of Rs.2.2 crore. By doing comparison the

amount of loan, it is increased by 593.18% in the year 2010-11 as compared to year 2009-10 and

decrease of 70.49% in the year 2011-12 as compared to the year 2010-11.

4) Loan against KVP/ NSC:-

YearLoan

2010 2011 2012

Against NSC/KVP

(In Crore)

0.0075 0.0039 0.0056

2010 2011 20120

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008 0.0075

0.0039

0.0056

Loan against NSC/KVP

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank has sanctioned credit against NSC/KVP of Rs.

0.0075 crore and in 2010-11 of Rs. 0.0039 Crore and in the year of 2011-12 of Rs.0.0056 crore.

By doing comparison the amount of loan, it is decreased by 48% in the year 2010-11 as

compared to year 2009-10 and increase of 43.59% in the year 2011-12 as compared to the year

2010-11.

5) TWO Wheeler loan:-

YearLoan

2010 2011 2012

TWO Wheeler loan

( In Crore)

0.71 1.34 1.81

2010 2011 20120

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

0.71

1.34

1.81

TWO Wheeler loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank has sanctioned two wheeler loan of Rs. 0.71 crore

and in 2010-11 of Rs. 1.34 Crore and in the year 2011-12 of Rs.1.81 crore. By doing comparison

the amount of loan, it is increased by 88.73% in the year 2010-11 as compared to year 2009-10

and increase of 35.07% in the year 2011-12 as compares to year 2010-11 which shows

continuous increase in the credit by the bank.

6) FOUR Wheeler loan:-

YearLoan

2010 2011 2012

FOUR Wheeler loan

( In Crore)

1.67 7.98 11.56

2010 2011 20120

2

4

6

8

10

12

14

1.67

7.98

11.56

FOUR Wheeler loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned four wheeler loan of Rs. 1.67

crore and in 2010-11 of Rs. 7.98 Crore and in the year 2011-12 of Rs.11.56 crore. By doing

comparison the amount of loan, it is increased by 377.84% in the year 2010-11 as compared to

year 2009-10 and increase of 44.86% in the year 2011-12 as compares to year 2010-11 which

shows continuous increase in the credit offered by the bank.

7) Staff Two Wheeler loan:-

YearLoan

2010 2011 2012

Staff Two Wheeler loan

(Rs. In Crore)

0.02 0.07 0.08

2010 2011 20120

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.02

0.07

0.08

Staff Two Wheeler loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned Staff Two wheeler loan of Rs.

0.02 crore and in 2010-11 of Rs. 0.07 Crore and in the year 2011-12 of Rs.0.08 crore. By doing

comparison the amount of loan, it is increased by 250% in the year 2010-11 as compared to year

2009-10 and increase of 14.29% in the year 2011-12 as compares to year 2010-11 which shows

continuous improvement in the staff facility offered by the bank.

8) Staff Housing loan:-

YearLoan

2010 2011 2012

Staff Housing loan

(Rs. In Crore)

0.39 0.38 0.44

2010 2011 20120.35

0.36

0.37

0.38

0.39

0.4

0.41

0.42

0.43

0.44

0.45

0.39

0.38

0.44

Staff Housing loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned Staff Two housing loan of Rs.

0.39 crore and in 2010-11 of Rs. 0.38 Crore and in the year 2011-12 of Rs.0.44 crore. By doing

comparison the amount of loan, it is decreased by 2.56% in the year 2010-11 as compared to

year 2009-10 and increase of 15.79% in the year 2011-12 as compares to year 2010-11 which

shows continuous improvement in the staff facility offered by the bank.

9) Machinery Hypothecation (TUF) loan:-

YearLoan

2010 2011 2012

Machinery Hypo.

(TUF) loan

(Rs. In Crore)

9.44 13.13 11.33

2010 2011 20120

2

4

6

8

10

12

14

9.44

13.13

11.33

Machinery Hypothecation (TUF) loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned Machinery Hypothecation (TUF)

loan of Rs. 9.44 crore and in 2010-11 of Rs. 13.13 Crore and in the year 2011-12 of Rs.11.33

crore. By doing comparison the amount of loan, it is increased by 39.08% in the year 2010-11 as

compared to year 2009-10 and decrease of 13.71% in the year 2011-12 as compares to year

2010-11 which shows credit offered for the development of small scale businesses by the bank.

10) Loan Against Fixed Deposit:-

YearLoan

2010 2011 2012

Loan Against Fixed Deposit

(Rs. In Crore)

0.07 0.15 0.23

2010 2011 20120

0.05

0.1

0.15

0.2

0.25

0.07

0.15

0.23

Loan Against Fixed Deposit

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned against FD of Rs. 0.07 crore and

in 2010-11 of Rs. 0.15 Crore and in the year 2011-12 of Rs.0.23 crore. By doing comparison the

amount of loan, it is increased by 114.28% in the year 2010-11 as compared to year 2009-10 and

increase of 53.33% in the year 2011-12 as compares to year 2010-11 which shows continuous

increase in the credit offered by the bank.

11) Self Employment Loan:-

YearLoan

2010 2011 2012

Self Employment Loan (Rs. In Crore)

0.0029 0.12 0.20

2010 2011 20120

0.05

0.1

0.15

0.2

0.25

0.0029

0.12

0.23

Self Employment Loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned Self employed loan of Rs. 0.0029

crore and in 2010-11 of Rs. 0.12 Crore and in the year 2011-12 of Rs.0.23 crore. By doing

comparison the amount of loan, it is increased rapidly in the year 2010-11 as compared to year

2009-10 and increase of 91.67% in the year 2011-12 as compares to year 2010-11 which shows

continuous increase in the credit offered by the bank.

12) Term Loan:-

YearLoan

2010 2011 2012

Term Loan (Rs. In Crore)

0.09 0.25 0.58

2010 2011 20120

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.09

0.25

0.58

Term Loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned term loan of Rs. 0.09 crore and in

2010-11 of Rs. 0.25 Crore and in the year 2011-12 of Rs.0.58 crore. By doing comparison the

amount of loan, it is increased rapidly in the year 2010-11 as compared to year 2009-10 and

increase of 132% in the year 2011-12 as compares to year 2010-11 which shows continuous

increase in the credit offered by the bank.

13) Surety Loan:-

YearLoan

2010 2011 2012

Surety Loan (Rs. In Crore)

0.44 1.04 2.14

2010 2011 20120

0.5

1

1.5

2

2.5

0.44

1.04

2.14

Surety Loan

Year

Am

ount

( In

Cro

re)

Interpretation:-

The chart shows that in the year 2009-10 bank had sanctioned against FD of Rs. 0.44 crore and

in 2010-11 of Rs. 1.04 Crore and in the year 2011-12 of Rs.2.14 crore. By doing comparison the

amount of loan, it is increased by 136.36% in the year 2010-11 as compared to year 2009-10 and

increase of 105.76% in the year 2011-12 as compares to year 2010-11 which shows continuous

increase in the credit offered by the bank.

Research Methodology

Definition:

‘Research is the systematic investigation into and study of material and sources in order

to establish facts and reach to the conclusion.’

Research Problem:

The question may arise in mind that:

What is the role of cooperative sector in the development of urban and small scale businesses

around Surat area?

As a co-operative bank, what efforts had been made by the bank by offering different credit

schemes so that people can take the maximum advantage of these schemes?

From the credit schemes offered by the bank, which is the scheme that is most preferred by

the customers?

Research Objectives:

Primary objective:

To analyze the consumer preference and satisfacton level for various credit schemes offerd by

The Varachha Co-operative bank.

Secondary objective:

To study various Credit Schemes offered by The Varachha Co-operative Bank.

To analyze the awareness and frequency of credit used by and preference toward by the

customers.

To study the level of satisfaction of customers at The Varachha Co-operative Bank.

To analyze the consumer loyalty towards The Varachha Co-operative Bank.

To study why people rely more on The Varachha Co-operative Bank than other

commercial bank.

The main objective behind the research is to know the various schemes offered by the

bank and the best one which is most preferred by the customers. To know from the customer of

the bank that why they choose this bank to satisfy their financial requirement than other bank.

Advantage of Research:

From this research, the organisation will come to know the consumer preference and

satisfaction level toward various credit schemes offered by The Varachha Co-operative

Bank.

The Bank management can know, in which schemes and services they have to made

changes and improvement.

By studying the research, the bank management can add or remove scheme, if necessary.

Limitation of the study:

Questionnaire method can be applied only when respondents are literate and co-operative

but some respondents may be illiterate and not ready to give true information or give

insufficient information which brings the study on wrong path.

Time is main constraint of the research as we have to prepare report with the training

simultaneously.

This study is limited to only varachha area (L. H. Road Branch).

Sampling Design:

Sampling design is one of the most important aspects where the design must be

appropriate in order to have the desire result. The research was done using simple random

sampling. Sampling design includes various aspects and they are as follows:

Sampling Area: Surat (Varachha)

Sample Size: 250

Research Design:

Research design is one of the core things before making any kind of survey or study. It is

generally related with the feedback for the survey. Research design includes all that aspects

which is related from formulating a questionnaire to the presenting the data of the survey.

The questions have been asked must be related to the situation in the sense that they must

be related for the particular purpose only. We also have to decide about target audience before

targeting the customers. The language and content of the questionnaire must be so that the

respondent can understand and answer correctly.

Data collection methodology:

The information so collected when put into proper sequence and proper format and arranged as

per need of article is called Data.

Data Collection:

After choosing research, it is necessary to collect accurate and reliable data in order to

achieve research objective. The first issue in the data collection process is to determine whether

the information needed for the research problem has already been collected or require fresh.

Generally there are two method of collecting the data:

Primary data:

The data that are fresh and sophisticated generated for a specific purpose or a specific

research project called primary data. The researcher collects the data by using data collection

instrument. For this research, primary data collection method is chosen by using the

questionnaire.

Secondary data:

The data which is already exists somewhere and it was gathered or generated for some

other purpose in the past. Such data may be useful for other research but it is not much reliable

compared to the primary data method. For this report, secondary data is used, which are collected

from different sources such as bank’s annual reports, pamphlets, internet, brushers and old

reports.

Research Method:

Research design is broadly classified into three categories:

o Exploratory research design

o Descriptive research design

o Causal research design

For this research, descriptive research design is chosen. In Descriptive research design,

the researcher have to deal with problem statement like what, when, where, how etc. it is also

advisable to use descriptive research design when the researcher is new to the research field and

had no experience about the research area.

Scope of the study:

This research involves the study of:

o Only Varachha area covered into the study,

o Analysis of customer preference towards various credit schemes offered by the varachha

co-operative bank,

o Study area is focused to customer satisfaction level toward various credit schemes,

o Study is based on the primary data only,

o Bank members and credit holder can used to study,

o Service satisfaction review of the varachha bank’s customer by questionnaire.

Literature Review:

The purpose of this study is to investigate the differing preference and satisfsction level of

customer towards loans, deposits schemes, insurance and value added services rendered by

various banks in Combatore and Erode cities. By using non-convenient sampling, 300 samples

were taken at various branches and ATM centres, etc. simple percentage and Chi-square test

results revealed that business and vehicle loans are fast moving and customers had overall

satisfaction. Bank loans, bank deposit schemes showed a positive response and in value added

services, customer preference for net banking got the least rank. Among four basic services,

insurance services had paid limited attention and the studu recommends special attention on

banking insurance service satisfaction and the implication were recorded for future researches.

Author: T. vetrivel( Velalar college of Engineering & Technology)

Source: The IUP journal of marketing Management, Vol-4, pp 81-97, November 2010