Values and Valuers - Avolonavolon.aero/wp/wp-content/uploads/2016/02/Avolon_Whitepaper_Value... ·...

16

Values and Valuers An Assessment of the Aircraft Valuation Business Dick Forsberg 18 February, 2016

Transcript of Values and Valuers - Avolonavolon.aero/wp/wp-content/uploads/2016/02/Avolon_Whitepaper_Value... ·...

Values and ValuersAn Assessment of the Aircraft Valuation Business

Dick Forsberg18 February, 2016

Dick Forsberg has over 44 years' aviation industry experience, working in a variety of roles with airlines, operating lessors, arrangers and capital providers in the disciplines of business strategy, industry analysis and forecasting, asset valuation, portfolio risk management and airline credit assessment. As a founding executive and Head of Strategy at Avolon, his responsibilities include defining the trading cycle of the business, primary interface with the aircraft appraisal and valuation community, industry analysis and forecasting, driving thought leadership initiatives, setting portfolio risk management criteria and determining capital allocation targets. Prior to Avolon, Dick was a founding executive at RBS (now SMBC) Aviation Capital and previously worked with IAMG, GECAS and GPA following a 20-year career in the UK airline industry. Dick has a Diploma in Business Studies and in Marketing from the UK Institute of Marketing is a member of the Royal Aeronautical Society and also a Board Director of ISTAT (The International Society of Transport Aircraft Trading).

Dick Forsberg Head of Strategy, Avolon

DisclaimerThis document and any other materials contained in or accompanying this document (collectively, the “Materials”) are provided for general information purposes only. The Materials are provided without any guarantee, condition, representation or warranty (express or implied) as to their adequacy, correctness or completeness. Any opinions, estimates, commentary or conclusions contained in the Materials represent the judgement of Avolon as at the date of the Materials and are subject to change without notice. The Materials are not intended to amount to advice on which any reliance should be placed and Avolon disclaims all liability and responsibility arising from any reliance placed on the Materials.

AcknowledgementThe Author wishes to acknowledge the work undertaken by the ISTAT Appraisers Group and their comprehensive Appraisers Handbook, from which the value definitions used in this paper have been taken.

Contents

Introduction 2

Key Messages 3

Choosing an Appraiser 4

What’s in a Value? 5

The Pros and Cons of Automation 7

Value the Money, Not Just the Metal 8

Variation and Volatility 9

The Influence of Appraisers 10

A Call to Arms 11

Funding the FutureAn Assessment of the Aircraft Valuation Business

1

This discussion paper examines the business of aircraft appraisals and valuations, both from the perspective of an end user and with a strategic eye on the broader industry’s future needs.

A wide range of values and value-related products is available to the industry, offered by an equally wide range of appraisal firms. Consequently, it can be difficult to differentiate between them and this paper offers some guidelines on what to look for when making that key appraiser selection.

How much does the typical customer know and understand about the values they have requested or about the appraisers they have commissioned? What are they getting from the appraisers and, equally important, what are they not getting or are potentially misunderstanding?

This paper provides a brief overview of the main types of valuations that are available and when they should be used, takes a critical look at automation and suggests that customers may be missing out through an over-reliance on instant results.

Today, most commercial aircraft are traded with lease and financing structures attached, yet buyers and sellers still too frequently rely on an incomplete valuation of the transaction, although appropriate appraisal products exist to provide the full picture. The paper explores the concept and benefits of Lease-encumbered Values.

The paper considers why appraisers’ value opinions may vary and how a greater appreciation of asset value volatility can assist investors to frame transactions in the context of likely value outcomes.

The commercial aviation industry has grown significantly over the past 15 years, not only doubling in size but also expanding the range and volume of asset-related transactions and the numbers of financiers and investors that are participating. The paper asks whether, as the demands of the industry become more exacting, appraisal services are keeping pace. What more should be done to ensure that future industry funding requirements can be met by attracting new types of investor that require levels of asset valuation rigour and transparency hitherto unseen in the sector?

The appraiser community today wields significant influence across the industry, where “only” a 1% reduction in appraised values would wipe over $2.5bn off the in service leased fleet. The challenge to the appraiser community is to rise to the responsibilities that go with that influence and to evolve into a consistently insightful, rigorous, transparent and reliable source of information supporting the 3500-plus aircraft deliveries and secondary trades that now take place each year.

Introduction

The commercial aviation industry has grown significantly over the past 15 years, not only doubling in size but also expanding the range and volume of asset-related transactions

“”

Values and ValuersAn Assessment of the Aircraft Valuation Business

2

• The ISTAT Appraisers Program has been setting standards and supporting the appraiser industry for over 25 years. Its Code of Conduct is observed throughout the appraiser community and adherence should be a prerequisite of any appraiser selection

• Automated on-line valuation products provide a cost-effective and speedy service for a range of applications, but their generic nature can mask significant value variances by excluding critical data

• A basic Desktop Appraisal will often provide a more detailed and accurate valuation than an on-line service and provides an opportunity for dialogue between appraiser and client which helps ensure that the resulting analysis is fit for purpose

• Although most aircraft are now traded with a lease attached, the standard appraisals that are typically used to benchmark asset value exclude the incremental financial benefits accruing from the associated lease

• Lease-encumbered valuations, which take account of the cash flows and income streams in assessing the all-in value of the aircraft and lease “package”, should be used as the basis for pricing such transactions

• The incremental lease-encumbered value in a lessor portfolio is a direct measure of the value added by the platform, its systems, processes and human capital

• Appraisers come in all shapes and sizes and selecting the right one for the job requires careful assessment

• In order to merit serious consideration as values providers, appraisers must conform to the ISTAT definitions and code of conduct for all of the relevant constituents of the range of appraisals and valuation services that they provide.

• The appraiser community, which has a significant and disproportionate influence on the industry, has remained relatively static compared to the changes seen in the commercial aviation sector over the past 15 years, in terms of size, product offering and competency.

• Changes are now required, not only to keep pace with current levels of market activity, but also to meet the standards of rigour, consistency and transparency that will be demanded by new investors seeking to enter the sector as aircraft complete the transition from alternative to mainstream investment class.

• A “Call to Arms” for appraisers highlights the key areas of focus:

– Appraisers should be able to demonstrate their track record of forecasting accuracy in a verifiable way using approved techniques that withstand scrutiny from experienced capital markets fund managers and investors.

– Appraisers must become more diligent in ensuring that changes made to current value opinions are reflective of the vintage of the asset and do not rely on the extrapolation of trading data from one age bracket to another

– Some valuation methodologies have not changed in 20-30 years. Appraisers must ensure that their skills and IP are at the cutting edge to meet the standards of rigour and governance that a $100bn+ per annum industry demands

– Appraisers should publish their methodologies, core assumptions, sample size and volatility data

– Appraisers must be Thought Leaders, prepared to raise and discuss challenging issues and to share best practices within the appraiser community.

– More industry professionals are needed to step up to the challenge of securing ISTAT accreditation, which would be facilitated by streamlining the ISTAT certification process – without diluting the standards

– Appraisers and their customers must work more closely with one another, developing greater mutual understanding through increased openness, dialogue and transparency.

Key Messages

Funding the FutureAn Assessment of the Aircraft Valuation Business

3

Choosing an Appraiser

More than a dozen aircraft appraisal companies offer a range of valuation, technical and associated advisory and support services to the commercial aviation industry. Whilst the output of their appraisal work is ostensibly homogenous – an opinion of the value of an aircraft at a point in time - the processes whereby they reach their opinions can be very different.

When selecting an appraiser, therefore, as with any product or service, clients are well advised to think carefully about their requirements and who is best placed and resourced to meet those needs.

Price should not be the prime determinant in selecting an appraiser, but, as with most things, you will usually get what you pay for. In the selection process it is important to consider:

• the need and ability to build a long-term relationship and to be able to engage in dialogue

• the need and ability to develop a good understanding of the valuation methodologies and philosophy applied by the appraiser

• whether the appraiser has key essential qualities such as access to a meaningful spectrum of value data, intellectual capital, modelling capability and analytical manpower

• the quality of analysis, insightfulness and depth of intimacy with the market

• the historical accuracy of the values produced and an ability to measure performance

• the range and scope of their valuation and other supporting products

• the frequency of value updates and revisions – at least quarterly to minimise step changes and year-end distortions

• where they sit in the range of values available across the spectrum of appraisers (more on this in section 7)

• whether they are widely used by banks, lessors, investors and stakeholders or is their business primarily focussed on one niche.

clients are well advised to think carefully about their requirements and who is best placed and resourced to meet those needs.

“”

Values and ValuersAn Assessment of the Aircraft Valuation Business

4

What’s in a Value?

Aircraft values come in a number of different forms, each of which can be provided at varying levels of detail, depending on what they are to be used for. Most appraisers adhere to standards, guidelines and definitions that have been developed and set out by ISTAT, through its Appraisers Program, which will be 27 years old in March 2016. The definitions are published in ISTAT's Appraisers’ Program Handbook, the most recent revision of which was published in January 2013. These definitions, along with a detailed Code of Conduct which includes important ethical considerations, should be central to every appraiser’s business activities and strictly adhered to.

It is worth summarising the main value definitions from the Handbook, as these cover most of the day to day value requirements of our industry.

Firstly, Base Value, which is the Appraiser's opinion of the underlying economic value of an aircraft in an open, unrestricted, stable market environment with a reasonable balance of supply and demand, and assumes full consideration of its “highest and best use.” An aircraft’s Base Value is founded in the historical trend of values and in the projection of value trends and presumes an arm’s-length, cash transaction between willing, able and knowledgeable parties, acting prudently, with an absence of duress and with a reasonable period of time available for marketing. In most cases, the Base Value of an aircraft assumes its physical condition is average for an aircraft of its type and age, and its maintenance time status is at mid-life, mid-time (or benefiting from an above-average maintenance status if it is new or nearly new, as the case may be).

Market Value (or Current Market Value if the value pertains to the time of the analysis) is the Appraiser's opinion of the most likely trading price that may be generated for an aircraft under the market circumstances that are perceived to exist at the time in question. Market Value assumes that the aircraft is valued for its highest, best use, that the parties to the hypothetical sale transaction are willing, able, prudent and knowledgeable, and under no unusual pressure for a prompt sale, and that the transaction would be negotiated in an open and unrestricted market on an arm’s-length

basis, for cash or equivalent consideration, and given an adequate amount of time for effective exposure to prospective buyers.

Fair Market Value is synonymous with Market Value, because the criteria typically used in those documents that use the term “Fair” reflect the same criteria set forth in the above definition of Market Value. By itself, the term “Fair” does not bring any additional qualifications to the appraised value, but it is a term sometimes used in leases, sales contracts, tax regulations and legal documents, and is sometimes accompanied with a specific definition to which the contracting parties have agreed. In such cases an Appraiser may be required to determine their value according to that particular definition.

Distress Value, Forced Sale Value, Liquidation Value are terms to describe the Appraiser's opinion of the price at which an aircraft (or other assets such as an engine or spare parts) could be sold in a cash transaction under abnormal conditions – typically an artificially limited marketing time period, the perception of the seller being under duress to sell, an auction, a liquidation, commercial restrictions, legal complications, or other such factors that materially reduce the bargaining leverage of the seller and give prospective buyers a significant advantage that can translate into heavily discounted actual trading prices. Depending on the nature of the assignment, the appraiser may be asked to qualify his opinion in terms of disposition within a specified time period, for example 60 days, 90 days or six months as the needs may be. Apart from the fact that the seller is uncommonly motivated, the parties to the transaction are otherwise assumed to be willing, able, prudent and knowledgeable, and negotiating at arm's-length, normally under the market conditions that are perceived to exist at the time, not an idealized balanced market.

Lastly, Securitized Value or Lease-Encumbered Value is the Appraiser’s opinion of the value of an aircraft under lease, given a specified lease payment stream (rents and term), an estimated future residual value at lease termination and an appropriate discount rate.

Funding the FutureAn Assessment of the Aircraft Valuation Business

5

Each of the value definitions can be provided at varying levels of detail, depending on the circumstances and purpose of the valuation. Again, ISTAT provides some definitions as to what to expect at each level:

• DESKTOP APPRAISAL - does not include any inspection of the aircraft or review of its maintenance records. It is based upon assumed aircraft condition and maintenance status or information provided to the appraiser or from the appraiser's own database. A desktop appraisal would normally provide a value for a mid-time, mid-life aircraft.

• EXTENDED DESKTOP APPRAISAL - is still characterized by the absence of any on-site inspection of the aircraft or its maintenance records, but does include consideration of maintenance status information that is provided to the appraiser from the client, aircraft operator, or in the case of a second opinion, possibly from another appraiser's report. An extended desktop appraisal would normally provide a value that includes adjustments from the mid-time, mid-life baseline to account for the actual maintenance status of the aircraft.

• FULL APPRAISAL - includes an inspection of the aircraft and its maintenance records. This inspection is aimed solely at determining the overall condition of the aircraft and records to support the value opinions of the appraiser, and would not, for example, include opening of inspection panels on the aircraft or a detailed review of record archives. A full appraisal would normally provide a value that includes adjustments from the mid-time, mid-life baseline to account for the actual maintenance status of the aircraft, and possibly other adjustments to reflect the findings of the inspection of the aircraft and its records.

• COMPREHENSIVE APPRAISAL - includes a detailed inspection of the aircraft and records. Sufficient detail is required, for example, to insure that the records are in sufficiently good order to allow for the re-registration of the aircraft in a different country.

• FINANCIAL APPRAISAL - determines the value of an aircraft to an investor based upon the income earning potential from its lease and residual value. A financial appraisal may be done in conjunction with either desktop or full appraisals.

Since the appraisal methodologies work at different levels of detail and granularity, each is better suited to some types of transactions or requirements than others. The majority of customers will find that their needs can be met either by a Desktop Valuation or an “Opinion Letter”. The former contains a limited element of narrative commentary to support values which are adjusted to reflect maintenance condition, utilisation and as much, or little, of the actual aircraft specification as the customer is able to provide. An Opinion Letter is an even briefer document which is simply a statement of the appraised value, but will often suffice for routine requirements.

The additional technical and maintenance detail provided in an Extended Desktop or Full on-site Inspection can be particularly helpful where older aircraft are involved or where repossession is on the cards. A full blown, tyre kicking, rivet counting, record checking Comprehensive Appraisal provides the ultimate, gold-plated valuation service, where the value reflects the realistic achievable sale price for the aircraft or its components "as is, where is". Whatever the purpose and detail of the valuation, it is important to keep in mind the definitions of “base” or “market”, “full life” or “half life” value.

In the days before on-line systems became ubiquitous, it is fair to say that the basic level of understanding from the user’s perspective was generally quite high. The only way to obtain an aircraft valuation was by requesting one of the “manual” methodologies from an appraiser. Having made the request, a dialogue between appraiser and client ensured that the valuation selected was appropriate for its purpose and that all relevant information about the asset in question had been provided. These checks and balances served the industry well and the majority of values provided were fit for purpose and used accordingly. This remains the case today where manual appraisals are requested, but automation is putting distance between the appraisers and their clients, increasing the potential for misunderstanding.

Values and ValuersAn Assessment of the Aircraft Valuation Business

6

If you are involved in leasing, financing, trading or otherwise making investment decisions involving commercial aircraft, there is a high probability that you will have requested and downloaded values from one or more of the automated on-line valuation services offered by several of the industry’s leading appraisal companies. First introduced 17 years ago, in 1999, these products are now estimated to account for over 50% of valuation requests for some of the appraisers that provide them and, for many users of aircraft values, be they buyers, sellers, lenders, lessors, manufacturers, bankers, financial advisors or analysts, these on-line tools have become their principal, or in some cases their only, source of aircraft values, replacing Desktop Valuations in many instances.

Yet how many consumers of value data truly understand what they are getting from these products? And, equally importantly, what they are not getting.

In today’s automated, instant world, it often seems that the internet can immediately provide the answer to every question and that high-tech solutions to every-day tasks produce results that are as good, if not better, than the steam-driven technology they replace. In this context, however, it is important to bear in mind that even the least granular level of manual value analysis, the Desktop Appraisal, is likely to take account of more information and provide a more accurate valuation than an on line request. Why? Because an on line product, in order to run efficiently in real time and be intuitively user friendly, will of necessity apply a more generic, simplified approach to the

analysis. Minority variants of specific aircraft types may be omitted from the selection menu; only the highest value specification options may be shown – perhaps no more than basic weight and thrust; a generic specification taken from a commercial fleet database may not reflect the specific msn requested; broad-brush adjustments from half life to zero time maintenance condition may throw up anomalies.

In other words, whilst the on-line valuations will provide a rapid (and low cost!) set of values, they may ignore key elements of the aircraft which, taken together, produce a significant upward or downward impact on the total. Whilst the scope of such variances will typically increase with aircraft age, very young aircraft are not immune. In most cases, a bespoke desktop appraisal will quickly produce a more accurate result.

However, on-line valuations are well-suited to the routine tracking of aircraft or portfolio value movements, for obtaining ball-park order of magnitude values, for comparing the relative virtues of different aircraft, for benchmarking the performance of a loan against key covenants and for a range of general audit and analysis tasks. They are normally accurate within the limitations of their generic nature and there is no waiting period.

The Pros and Cons of Automation

these products are now estimated to account for over 50% of valuation requests for some of the appraisers that provide them

“”

Funding the FutureAn Assessment of the Aircraft Valuation Business

7

One fundamental aspect of Base Values and Market Values, whether obtained on-line or through desktops or more detailed manual appraisals, is that they provide valuations of the aircraft as a stand-alone asset. Although the “leasability” of the aircraft type may be one of the factors taken into consideration when reaching a value determination (since leasing would come under the definition of “highest and best use”), standard appraisals do not take into consideration any value enhancement, or decrement, deriving from an associated lease structure which generates cash flows and an income stream for the aircraft owner. In an industry where arguably more than 90% of aircraft are now traded (other than for part-out) with a lease attached, it is perhaps surprising to some that the baseline appraisal definition continues to be for a single aircraft transaction with no lease attached, taking no benefit from the asset’s capabilities as a revenue generator. Some appraisal users, indeed, may be unaware of this important distinction.

The tendency of stakeholders in the industry to “default” to base and market value appraisals is at odds with other asset investment classes. In the commercial real estate market, for instance, there is a range of recognised definitions for valuations that reflect the income-generating status of the property, working upwards (in value terms) from Site Value, through Rebuild Cost, Vacant Use and Alternative Use to Subject to Tenant. In aviation parlance, this range of values may be considered to span Scrap Value, Full/Half Life and Lease Encumbered Value.

In order to assess the true value of the aircraft plus the associated financing and leasing structures (the “tenant”), therefore, it would be appropriate to undertake the more rigorous and bespoke Lease-Encumbered Valuation, also known as a Securitized Valuation or a Financial Valuation. Although there is no single defined approach for this analysis amongst the appraiser community, the most commonly used methodology takes account of the present value of the net cash flows over the lease term, including any maintenance return condition adjustments and other risk mitigants, discounted at an appropriate rate for the credit quality of the lessee, plus the future value of the asset at lease maturity, also discounted but using a level slightly above the risk-free rate (typically US Treasuries) associated with the lease term.

These valuations come with a health warning however. The ISTAT Appraisers Handbook notes that “the Appraiser may not be fully aware of the credit risks associated with the parties involved, nor all related factors such as the time-value of money to those parties”. In other words, appraisers may understand aircraft, but they are not usually expert credit analysts. Any additional information and guidance that the client can provide to assist the appraiser’s choice of credit-related discount rate is therefore likely to produce a more nuanced and appropriate output.

A diligently undertaken LEV analysis will often, though not always, result in incremental value over and above the ISTAT-defined base or market value of the stand-alone asset. In certain circumstances, lease encumbrance can have a downward impact on the value where, for example, the lease has been contracted during a period of market softness, perhaps with a weak airline credit and at a depressed lease rate. Nevertheless, using this approach to establish the all-in value of the aircraft and associated lease “package” as it would accrue to the aircraft owner should be considered as the basis for negotiating the majority of lease-encumbered aircraft or portfolio trades.

The tendency of stakeholders in the industry to “default” to base and market value appraisals is at odds with other asset investment classes.

“”

Value the Money, Not Just the Metal

Values and ValuersAn Assessment of the Aircraft Valuation Business

8

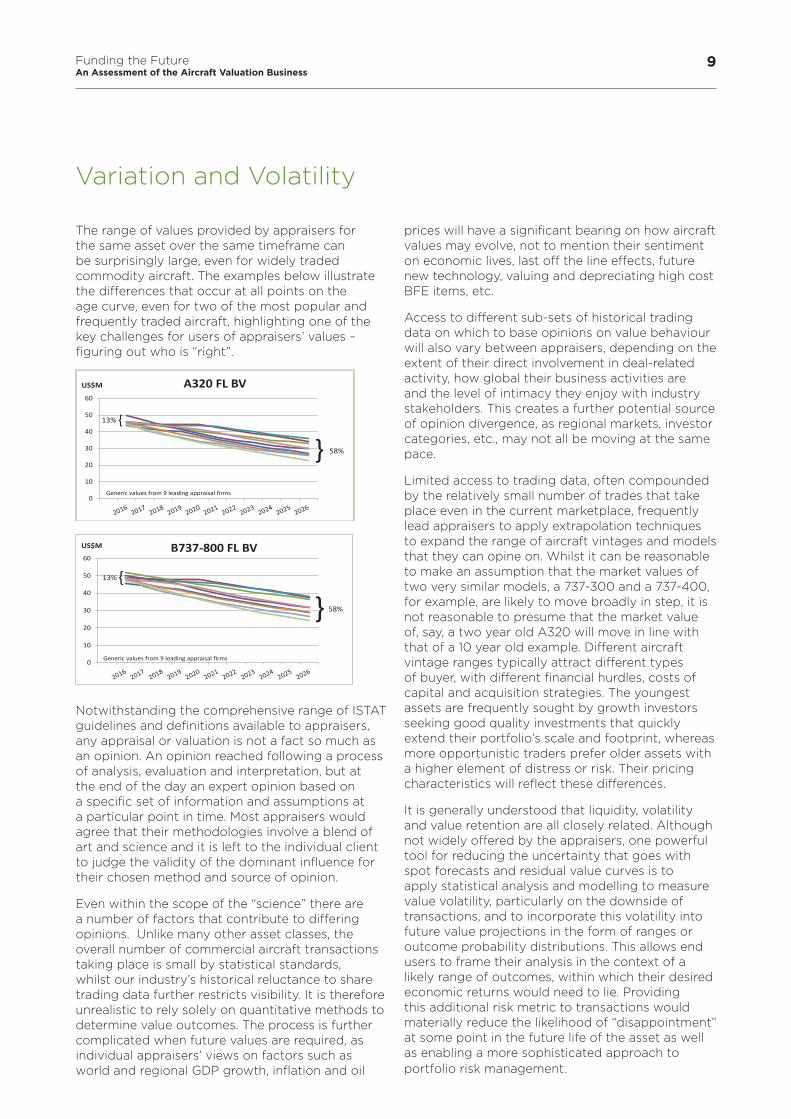

The range of values provided by appraisers for the same asset over the same timeframe can be surprisingly large, even for widely traded commodity aircraft. The examples below illustrate the differences that occur at all points on the age curve, even for two of the most popular and frequently traded aircraft, highlighting one of the key challenges for users of appraisers’ values – figuring out who is “right”.

0

10

20

30

40

50

60

A320 FL BVUS$M

58%}13%

Generic values from 9 leading appraisal firms

{

0

10

20

30

40

50

60B737-800 FL BVUS$M

} 58%

13%

Generic values from 9 leading appraisal firms

{

Notwithstanding the comprehensive range of ISTAT guidelines and definitions available to appraisers, any appraisal or valuation is not a fact so much as an opinion. An opinion reached following a process of analysis, evaluation and interpretation, but at the end of the day an expert opinion based on a specific set of information and assumptions at a particular point in time. Most appraisers would agree that their methodologies involve a blend of art and science and it is left to the individual client to judge the validity of the dominant influence for their chosen method and source of opinion.

Even within the scope of the “science” there are a number of factors that contribute to differing opinions. Unlike many other asset classes, the overall number of commercial aircraft transactions taking place is small by statistical standards, whilst our industry’s historical reluctance to share trading data further restricts visibility. It is therefore unrealistic to rely solely on quantitative methods to determine value outcomes. The process is further complicated when future values are required, as individual appraisers’ views on factors such as world and regional GDP growth, inflation and oil

prices will have a significant bearing on how aircraft values may evolve, not to mention their sentiment on economic lives, last off the line effects, future new technology, valuing and depreciating high cost BFE items, etc.

Access to different sub-sets of historical trading data on which to base opinions on value behaviour will also vary between appraisers, depending on the extent of their direct involvement in deal-related activity, how global their business activities are and the level of intimacy they enjoy with industry stakeholders. This creates a further potential source of opinion divergence, as regional markets, investor categories, etc., may not all be moving at the same pace.

Limited access to trading data, often compounded by the relatively small number of trades that take place even in the current marketplace, frequently lead appraisers to apply extrapolation techniques to expand the range of aircraft vintages and models that they can opine on. Whilst it can be reasonable to make an assumption that the market values of two very similar models, a 737-300 and a 737-400, for example, are likely to move broadly in step, it is not reasonable to presume that the market value of, say, a two year old A320 will move in line with that of a 10 year old example. Different aircraft vintage ranges typically attract different types of buyer, with different financial hurdles, costs of capital and acquisition strategies. The youngest assets are frequently sought by growth investors seeking good quality investments that quickly extend their portfolio’s scale and footprint, whereas more opportunistic traders prefer older assets with a higher element of distress or risk. Their pricing characteristics will reflect these differences.

It is generally understood that liquidity, volatility and value retention are all closely related. Although not widely offered by the appraisers, one powerful tool for reducing the uncertainty that goes with spot forecasts and residual value curves is to apply statistical analysis and modelling to measure value volatility, particularly on the downside of transactions, and to incorporate this volatility into future value projections in the form of ranges or outcome probability distributions. This allows end users to frame their analysis in the context of a likely range of outcomes, within which their desired economic returns would need to lie. Providing this additional risk metric to transactions would materially reduce the likelihood of “disappointment” at some point in the future life of the asset as well as enabling a more sophisticated approach to portfolio risk management.

Variation and Volatility

Funding the FutureAn Assessment of the Aircraft Valuation Business

9

A good deal has changed since the first automated values went on line in 1999. At that time, 13,000 commercial jets were in service, of which 20% were leased. Today’s fleet is 85% larger, with 40% under lease management. 1100 aircraft were delivered in 1999, with a $40bn price tag, of which lessors financed 25%. Last year lessors financed almost 40% of 1500 aircraft deliveries valued at well over $100 billion and the in-service leased fleet is now valued at more than $260 billion. The last 17 years has seen at least a dozen new western leasing companies enter the market alongside the more recent influx of Chinese and Japanese lessors. Ten of today’s Top 20 operating lessors were not around 17 years ago. Some of the world’s largest financial institutions now own operating lessors. Capital markets products, including EETCs and both secured and unsecured bonds, have taken off, providing more than $20bn of liquidity over the past two years, and private equity investors have become significant participants in the industry.

Yet the appraiser world has remained relatively static, with just a handful of new entrants over the years. Moreover, the number of formally qualified appraisers (accredited by ISTAT) has not kept pace with the growth in commercial aircraft fleets and financing activity. In 1999, 35 professionals held an ISTAT appraiser certification. Today that number has risen to 53, a 50% increase over a period when the world fleet almost doubled and the demand for appraisals has grown even faster. Remarkably, there are still no appraisal firms headquartered outside the USA or UK.

The appraisal community remains varied in its scope, product offerings and resources. Appraisal firms range from “full service” data and analytics-based platforms providing multi-product advisory services supported by valuation and technical teams of 50+ people through to one- and two-person businesses offering a narrow range of office-based services that rely on a network of industry contacts to maintain a real-time database.

During the 1990s, many of the leading appraisers underwent considerable upheaval in thinking and methodology as they developed, refined and overhauled their modelling, forecasting and analytical capabilities. In contrast, the 2000s have so far seen the appraisers largely quiescent. There have been some notable exceptions, where basic provision of data has been supplanted by thoughtful analytics and insight that leverage off the data, but many of the appraisers are doing today more or less what they did 15 years ago, with perhaps the addition of an automated on-line service.

This is disappointing, as appraisers now, more than ever, exert a disproportionate influence on the views on aircraft values held by all of the key market constituents. They influence the level of advance offered on a secured loan, along with the term and amortisation schedule; the minimum amount that an airline can expect to receive when seeking sale and leaseback financing for a new delivery and the maximum that a lessor will aim to pay on that same transaction; they set benchmark levels that set floors or ceilings in price negotiations for aircraft trading; accounting impairments may be triggered by mark-to-market requirements from lenders or auditors. The impact of even small variations in values across a portfolio of aircraft can be very significant, not only through direct changes to the balance sheet but also as a result of funding adjustments triggered under lender covenants and other financing requirements.

The Influence of Appraisers

Values and ValuersAn Assessment of the Aircraft Valuation Business

10

Investing in commercial aircraft has come of age in the past 15 years, moving from an exotic asset class through to an alternative investment during the 2000s and the mainstream investment opportunity that is now provided by many lessor platforms. As this transition has taken place, the demands and sophistication of investors have also evolved, to the point where a high degree of rigour, consistency and transparency is required in all aspects of the valuation process. If these standards, which are considered a given in other sectors, are not met, investors will not have the confidence to invest in the scale needed to support the future growth of the industry.

The new standards of rigour, consistency and transparency will increasingly challenge some of the outlier appraisers, especially those with limited resources. Whilst there can be value in specialisation, only size brings the breadth of activities to tap all possible data sources, the manpower to analyse and validate that data and the IP to develop product enhancements that leverage the data. Consolidation amongst appraisers, therefore, is both necessary and inevitable, but with it must come a willingness not only to invest in and develop new products, but also to foster a more open attitude towards communicating with customers and investors – which increasingly will be one and the same.

As an integral and high profile industry constituent, the appraiser community needs to reflect on its role and the ways in which the various products are prepared and delivered. Processes, methodologies and data analysis must all be fit for purpose and provided in a timely, consistent and rigorous manner.

Responsiveness to changing market conditions is also now more than ever a core requirement for the industry. Whilst not advocating that the appraiser industry should lead the cycle with its market value reporting, it could arguably move faster to reflect inflection points such as have been seen over the past 12-18 months. Clearly, the fundamental lack of transparency that continues to be a sad legacy of the industry is at least partly to blame, as the paucity of timely trading data points leaves many appraisers with little to go on to distinguish a genuine trend from an outlier. Equally clearly, it is not acceptable to have market value opinions of one aircraft type and age bracket impacted by a small number of trades of significantly older, or younger, aircraft of a similar type. Proxies work up to a point, but more, and more relevant, data is ultimately the only solution to this problem. At the risk of sounding like a broken record, it is time that the industry (i.e. lessors and financiers) took another look at how to break the log jam of secrecy, without breaking commercial confidentiality or divulging their unique IPs.

A Call to Arms

If these standards, which are considered a given in other sectors, are not met, investors will not have the confidence to invest in the scale needed to support the future growth of the industry.

“”

Funding the FutureAn Assessment of the Aircraft Valuation Business

11

To summarise, there are 7 key areas where a “Call to Arms” for appraisers and industry professionals is required to focus minds and priorities:

1. Appraisers should be able to demonstrate their track record of forecasting accuracy in a verifiable way using approved techniques that that withstand scrutiny from experienced capital markets fund managers and investors.

2. Appraisers must become more diligent in ensuring that changes made to current value opinions are reflective of the vintage of the asset and do not rely on the extrapolation of trading data from one age bracket to another

3. Some valuation methodologies have not changed in 20-30 years. Appraisers must ensure that their data sources, analytical skills and IP are at the cutting edge to meet the standards of rigour and governance that a $100bn+ per annum industry demands

4. Appraisers should publish their methodologies, core assumptions, sample size and volatility data

5. Appraisers must be Thought Leaders, prepared to raise and discuss the challenging issues and to share best practices within the appraiser community

6. More industry professionals are needed to step up to the challenge of securing ISTAT accreditation, which would be facilitated by streamlining the ISTAT certification process – without diluting the standards

7. Appraisers and their customers need to work more closely with one another, developing greater mutual understanding through increased openness, dialogue and transparency

Values and ValuersAn Assessment of the Aircraft Valuation Business

12

Funding the FutureAn Assessment of the Aircraft Valuation Business

13

Values and ValuersAn Assessment of the Aircraft Valuation Business

14

AvolonThe Oval, Building 1Shelbourne RoadBallsbridge, Dublin 4Ireland

United States • Ireland • Dubai • Singapore • Hong Kong • China www.avolon.aero