VALUE FOCUS - Mercer Capitalmercercapital.com › assets › Mercer-Capital_2014-Q1... · The...

19

VALUE FOCUS FOOD AND BEVERAGE Q1: Non-Alcoholic Beverages Q2: Alcoholic Beverages Q3: Food Processing Q4: Fast Food & Casual Restaurants 2014

Transcript of VALUE FOCUS - Mercer Capitalmercercapital.com › assets › Mercer-Capital_2014-Q1... · The...

VALUE FOCUSFOOD AND BEVERAGE

Q1: Non-Alcoholic BeveragesQ2: Alcoholic BeveragesQ3: Food ProcessingQ4: Fast Food & Casual Restaurants

2014

© 2014 Mercer Capital 1 www.mercercapital.com

Segment Focus

2014 First Quarter

Non-Alcoholic Beverages

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES

The non-alcoholic beverage industry is characterized by innovation and major shifts in beverage trends. For example, bottled water sales

may soon overtake carbonated soft drinks (“CSDs”) in terms of volume based on current growth rates. In 2013, CSDs continued to struggle

amidst negative consumption trends, necessitating healthier product offerings from CSD producers. As a whole, fruit juice consumption

continues to fall while RTD tea and coffee maintain positive volume growth.1

Sugar and corn are major inputs the industry. The price of corn decreased during the latter part of 2013 and is expected to continue

decreasing in 2014, while the price of sugar is expected to increase in 2014. Input prices for beverage packaging also greatly affect industry

profitability. Aluminum prices have been volatile in recent years and the price of plastic has steadily risen.2 For beverage distributors across

the industry, customized software for route optimization and intensive data collection are low-hanging fruit when it comes to managing

fuel costs.3

While Coca-Cola, Dr. Pepper Snapple,

and Monster all struggled to make year-

over-year gains in the market, PepsiCo

enjoyed an 8.5% increase in part due its

portfolio diversification outside of CSDs

and its growing presence in international

markets.

Although Starbucks shares enjoyed a

31% increase year-over-year, at the end

of the first quarter, shares were down

6.0% from year-end 2013, in part due

to rising coffee prices and difficulty with

this year’s Brazilian coffee crop. National

Beverage saw a 39% annual increase

amid speculation that the company

or its LaCroix brand could be sold to

Coca-Cola.

Public Company Performance

-100%

0%

100%

200%

300%

400%

500%

600%

700%

800%

3/31/09 9/30/09 3/31/10 9/30/10 3/31/11 9/30/11 3/31/12 9/30/12 3/31/13 9/30/13 3/31/14

PepsiCo The Coca- Cola Co. Dr. Pepper Snapple Group Inc. Monster Beverage Corp. National Beverage Corp. Starbucks Corp.

5 Year Change in Stock Prices for Publicly Traded Non-Alcoholic Beverages

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 2 www.mercercapital.com

According to Bloomberg, the non-alcoholic beverage industry had

63 pending or completed deals with an average value of $27 million

between March 31, 2013 and 2014. Deal volume is up 18.9% from

the previous twelve months when the industry had 53 deals with an

average value of $22.6 million.

Major recent transactions include Coca-Cola’s 10% interest in Green

Mountain Coffee Roasters. Coca-Cola’s acquisition comes as Green

Mountain is expected to expand its popular Keurig coffeemakers into

cold beverages.

Merger and Acquisitions

Acquirer Target Date Consideration Price/

RevenuePrice/

EBITDA

The Coca-Cola Company Green Mountain Coffee Roasters

2/27/14 $1.25 billion 2.84x 12x

Crestview Partners LP DS Waters of America Inc. 9/3/13 $920 million na na

Post Holdings Premier Nutrition Corpora-tion

9/1/13 $180 million na na

Source: Bloomberg

Non-Alcoholic Beverage Transactions

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital // Chart Data Source: Beverage World 3 www.mercercapital.com

Soda (CSDs)

According to Beverage World’s most

recent industry report, CSDs have expe-

rienced eight straight years of volume

and sales declines in the US, largely

due to changing consumer tastes and

continued negative publicity. Mid- cal-

orie offerings are the only CSDs that

exhibit more positive performance.

Pepsi’s, “Pepsi Next” sold 24 million

cases in 2012 and accounted for roughly

1% of Pepsi’s total volume. Coke has

also entered the market with mid-calorie

Sprite and Fanta offerings, but its most

successful product continues to be Coke

Zero with 8% sales growth in 2012.4

While CSDs still maintain the largest

market share within the non-alcoholic

beverage sector, continuous volume

and sales loss threatens their position.

In order to combat poor performance,

the industry is expected to adopt new

technology such as hybrid palletizing

and hot-fill technology for PET bottles

as a means of improving efficiency and

minimizing cost.5

New alternative sweeteners the at-home

carbonation trend may be ways to

increase CSD consumption. Home car-

bonation system manufacturer Soda-

Stream reported an uptick in first quarter

revenues in comparison to the prior year

and PepsiCo and Coca-Cola have both

entered partnerships with similar com-

panies in hopes of making their prod-

ucts accessible via home carbonation

systems in 2014.6

U.S. CSD Volume (Billions of Gallons)

U.S. CSD Brand Market Share

12,500

13,000

13,500

14,000

14,500

15,000

2007 2008 2009 2010 2011 2012

Source: State of the Beverage Market 2013, Beverage World

17.5%

9.9%

9.7%

7.2%

6.7% 5.9%

4.6%

2.5%

2.1%

1.9%

32.1%

Coca-‐ Cola

Diet Coke

Pepsi

Mountain Dew

Dr. Pepper

Sprite

Diet Pepsi

Coke Zero

Diet Mountain Dew

Diet Dr. Pepper

Others

Source: State of the Beverage Market 2013, Beverage World

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital // Chart Data Source: Beverage World 4 www.mercercapital.com

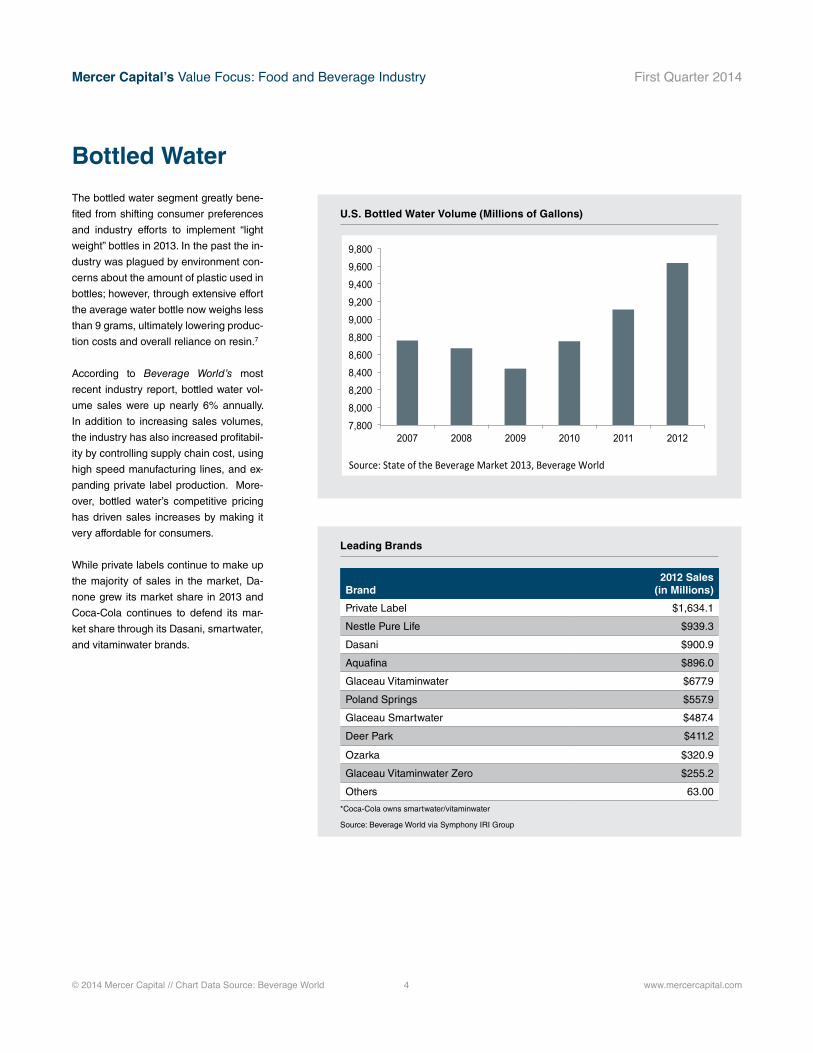

Bottled Water

The bottled water segment greatly bene-

fited from shifting consumer preferences

and industry efforts to implement “light

weight” bottles in 2013. In the past the in-

dustry was plagued by environment con-

cerns about the amount of plastic used in

bottles; however, through extensive effort

the average water bottle now weighs less

than 9 grams, ultimately lowering produc-

tion costs and overall reliance on resin.7

According to Beverage World’s most

recent industry report, bottled water vol-

ume sales were up nearly 6% annually.

In addition to increasing sales volumes,

the industry has also increased profitabil-

ity by controlling supply chain cost, using

high speed manufacturing lines, and ex-

panding private label production. More-

over, bottled water’s competitive pricing

has driven sales increases by making it

very affordable for consumers.

While private labels continue to make up

the majority of sales in the market, Da-

none grew its market share in 2013 and

Coca-Cola continues to defend its mar-

ket share through its Dasani, smartwater,

and vitaminwater brands.

U.S. Bottled Water Volume (Millions of Gallons)

Leading Brands

Brand2012 Sales

(in Millions)

Private Label $1,634.1

Nestle Pure Life $939.3

Dasani $900.9

Aquafina $896.0

Glaceau Vitaminwater $677.9

Poland Springs $557.9

Glaceau Smartwater $487.4

Deer Park $411.2

Ozarka $320.9

Glaceau Vitaminwater Zero $255.2

Others 63.00

*Coca-Cola owns smartwater/vitaminwater

Source: Beverage World via Symphony IRI Group

Company

7,800

8,000

8,200

8,400

8,600

8,800

9,000

9,200

9,400

9,600

9,800

2007 2008 2009 2010 2011 2012

Source: State of the Beverage Market 2013, Beverage World

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 5 www.mercercapital.com

Bottled Water (continued)

Bottled Water Global Market Share (%)

Company 2013 2012 2011 2010 2009 2008

Danone 10.27 10.05 10.09 10.01 9.74 10.85

Coca-Cola Co/The 7.66 7.72 7.63 7.50 7.74 7.40

Nestle SA 7.28 7.63 7.88 8.20 8.12 8.41

PepsiCo Inc 3.59 3.69 3.77 3.75 3.76 4.16

Ting Hsin International Group 1.77 1.58 1.64 1.56 1.29 1.09

Hangzhou Yangshengtang Co Ltd 1.68 1.56 1.39 1.19 1.11 1.03

Hangzhou Wahaha Group Co Ltd 1.24 1.28 1.28 1.28 1.19 na

Acqua Minerale San Benedetto S 1.25 1.30 1.33 1.30 1.39 1.50

China Resources Enterprise Ltd 1.12 0.92 0.74 0.59 0.51 0.46

Bisleri International Pvt Ltd 1.12 0.96 0.86 0.77 0.70 0.59

Others 63.00 63.32 63.40 63.87 64.47 64.51

Source: Bloomberg

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital // Chart Data Source: Beverage World 6 www.mercercapital.com

Energy Drinks

The energy drink segment saw a 14% in-

crease in volume sales in the most recent

year, highlighting the continued recent

success within the segment. Despite the

increase in volume sales, this number is

lower than previous years’ growth, sug-

gesting that the market is quickly becom-

ing highly saturated.

New product innovation was a staple of

the segment between 2007 and 2009

and served to widen the scope of the

segment’s target consumer.8 However,

according to Beverage World’s 2013 in-

dustry report, the past year had the sec-

ond fewest new product innovations in

the last six years. Moreover, FDA pres-

sures with respect to caffeine content

and ingredient claims may have slowed

industry growth.

Overall, continued FDA scrutiny and a

potentially saturated market are expect-

ed to slow growth in the segment over the

coming years.

U.S. Energy Drink Volume (Millions of Gallons)

Leading Brands

Brand2012 Sales

(in Millions)

Red Bull $3,182.5

Monster $1,884.9

Monster Rehab $409.9

Rockstar $324.9

NOS $264.2

Java Monster $251.2

Monster Mega $231.7

AMP Energy $184.0

Red Bull Total Zero $147.3

Rockstar Sugar Free $144.2

Others 63.00

Source: Beverage World via Symphony IRI Group

US Energy Drink Volume

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012

Source: State of the Beverage Market 2013, Beverage World

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 7 www.mercercapital.com

Top 10 Brands Global Market Share (%)

Company 2013 2012 2011 2010 2009 2008

PepsiCo Inc 30.80 31.64 33.38 33.11 35.03 36.82

Coca-Cola Co/The 17.94 18.41 18.51 19.21 17.69 18.42

Red Bull GmbH 6.81 6.62 6.22 5.90 5.82 5.59

Otsuka Holdings Co Ltd 5.43 5.26 5.38 5.86 5.91 5.73

Monster Beverage Corp 5.23 4.93 3.86 3.29 2.88 2.14

TC Pharmaceutical Industries C 4.56 4.05 3.78 3.08 2.73 2.58

Suntory Holdings Ltd 2.98 0.90 0.95 1.04 1.30 na

Uni-President Enterprises Corp 1.90 1.80 1.77 1.75 1.50 1.46

Rockstar Inc 1.76 1.79 1.61 1.37 1.32 1.33

Thai Beverage PCL 1.34 0.08 0.08 0.09 0.09 0.05

Others 21.24 24.53 24.47 25.30 25.74 25.90

Source: Bloomberg

Energy Drinks (continued)

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 8 www.mercercapital.com

RTD Coffee and Tea

Tea

In 2012, RTD tea experienced another

period of modest growth as volume sales

grew almost 5%. RTD tea has enjoyed

this consistent growth pattern in the last

few years thanks to its perceived health

status and low calorie offerings.

Going forward however, experts think that

RTD tea growth will likely slow as RTD

coffee provides additional competition.9

For example, in 2013 PepsiCo launched

its Starbucks-branded low calorie iced

coffee line, adding more options to the

growing RTD tea and coffee segment.10

Coffee

Within the RTD coffee segment,

Starbucks branded products remain

the leader in the U.S. The segment is

experiencing a resurgence in popularity,

reporting double-digit gains for the first

time since 2007.11 Near-term profitability

for RTD coffee beverages may be limited

due to continued increases in the coffee

prices. The price of Brazilian Arabica

soared to $1.75 per pound, up 74%

since year-end due to drought in Brazil

and concerns about the size of the 2015

crop.12

U.S. RTD Tea Volume (Millions of Gallons)

CompanyTing Hsin International GroupUni-President Enterprises CorpUnilever NVCoca-Cola Co/The

0

200

400

600

800

1,000

1,200

2006 2007 2008 2009 2010 2011 2012

Source: Beverage World

Starbucks

Brand Market Share (%) 2012 Sales (in Millions)

Starbucks Frappuccino Cappuccino 61.1 $763.5

Starbucks Doubleshot Cappuccino 28.3 $353.5

Starbucks 5.9 $73.8

Starbucks Frappuccino Light 2.1 $25.8

Starbucks Doubleshot Light 0.8 $10.1

Other 1.8 na

Source: Beverage Industry and Information Resources Inc.

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 9 www.mercercapital.com

RTD Tea Global Market Share (%)

Company 2013 2012 2011 2010 2009 2008

Ting Hsin International Group 10.86 9.75 14.16 15.02 11.82 9.58

Uni-President Enterprises Corp 7.76 7.01 6.02 5.70 5.00 5.36

Unilever NV 6.47 6.90 6.94 7.39 7.68 8.08

Coca-Cola Co/The 6.44 6.68 6.71 6.65 7.54 8.24

The JDB Group 6.19 5.95 na na na na

Ito En Ltd 4.99 5.38 5.02 4.95 5.02 5.31

Suntory Holdings Ltd 4.59 4.87 5.08 5.25 5.45 5.79

Nestle SA 3.70 4.03 4.43 4.42 4.88 5.29

Guangzhou Pharmaceutical Holdings 3.06 1.31 4.96 4.59 4.42 4.51

Kirin Holdings Co Ltd 2.90 3.16 3.22 3.27 3.49 3.83

Others 43.05 44.95 43.46 42.75 44.71 44.01

Source: Bloomberg

RTD Coffee and Tea (continued)

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 10 www.mercercapital.com

Fruit and Sports Drinks

Based on the most recent data from

Beverage World, sports drink volume

sales were up 2.3% annually due to the

success attributed to revamping the Ga-

torade brand and expanding low calorie

Powerade options. Gatorade continues

to dominate the market, controlling over

half the segment’s market share. The

future of the sports drinks segment will

likely continue to be defined by Gatorade

and Powerade as well as numerous small

volume, premium priced brands.13

On the other end of the market, fruit

drinks continued to decline in both sales

and volume, recently losing over 4% of

total non-alcoholic beverage market

share. The segment is largely affected

by the same growing health concerns

that push CSD drinkers towards other

products, including concerns about the

amount of sugar and caloric content.14

Leading Brands

Brand2012 Sales

(in Millions)

Gatorade G Series Perform $2,765.4

Powerade Ion4 $878.1

Gatorade G2 Perform $515.7

Gatorade $408.3

Powerade Zero $233.8

G2 $143.9

Gatorade Frost $105.7

Gatorade Cool Blue $68.8

Gatorade Fierce $66.1

Gatorade All Stars $56.1

Others 63.00

Source: State of the Beverage Market 2013, Beverage World

RTD Tea Global Market Share (%)

Company 2013 2012 2011 2010 2009 2008

Ting Hsin International Group 10.86 9.75 14.16 15.02 11.82 9.58

Uni-President Enterprises Corp 7.76 7.01 6.02 5.70 5.00 5.36

Unilever NV 6.47 6.90 6.94 7.39 7.68 8.08

Coca-Cola Co/The 6.44 6.68 6.71 6.65 7.54 8.24

The JDB Group 6.19 5.95 na na na na

Ito En Ltd 4.99 5.38 5.02 4.95 5.02 5.31

Suntory Holdings Ltd 4.59 4.87 5.08 5.25 5.45 5.79

Nestle SA 3.70 4.03 4.43 4.42 4.88 5.29

Guangzhou Pharmaceutical Holdings 3.06 1.31 4.96 4.59 4.42 4.51

Kirin Holdings Co Ltd 2.90 3.16 3.22 3.27 3.49 3.83

Others 43.05 44.95 43.46 42.75 44.71 44.01

Source: Bloomberg

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital 11 www.mercercapital.com

Food and beverage companies generally outperformed the market

in first quarter 2014. While the S&P 500 was up 1.3% from year-end

2013, food processing companies were up 1.6% and beverage com-

panies were up 5.5% (as measured by the Bloomberg Global Food

and Beverage Indices respectively). Beverage multiples continued to

expand during the first quarter along with an 18.9% increase in M&A

activity compared to the prior year.

Shares for Hillshire Brands increased 11% this quarter as both Tyson

Foods and Pilgrim’s Pride made bids for the company. Despite head-

winds in the carbonated soft drink sector and relatively flat sales,

Dr. Pepper Snapple Group was able to report a 46% increase in Q1

earnings in comparison to the prior year as the company benefited

from lower commodity prices and decreased spending on labor and

marketing, emphasizing the importance of cost controls for major

CSD producers. Consensus estimates for consumer staples in 2014

reflect decreasing expectations with earnings estimated to grow

5.1% (down from 5.8% at year-end 2013) and revenues estimated to

decreased by 6.5%.15

For restaurants, March brought positive results after severe weather

deterred consumers throughout the winter. 55% of restaurant opera-

tors surveyed reported same-store gains in March and 46% reported

an increase in traffic. 49% of operators expected to see an increase

in sales in the next six months, the highest level reported in nearly

two years.16

General Food & Beverage Overview

1 “State of the Beverage Market 2013,” Beverage World, May 2013. 2 “Soda Production in the US,” IBISWorld, June 2014.3 “Fleet managers turn to route optimization to cut delivery costs,”

Beverage Industry. May 2014.4 “State of the Beverage Market 2013,” Beverage World, May 2013. 5 “Soda Production in the US,” IBISWorld, June 2014.6 “Carbonated Soft Drinks Face Challenges And Critical Partnership

Decisions,” Seeking Alpha, April 2014.7 “State of the Beverage Market 2013,” Beverage World, May 2013. 8 Ibid.9 Ibid.10 “Starbucks Launches New Iced Coffee Line,” BevNet, Online,

Available http://www.bevnet.com/news/2013/starbucks-launches-

new-iced-coffee-line, Accessed July 23, 2014.

11 “2014 State of the Industry: Coffee and RTD Coffee,” Beverage

Industry. Online. Available http://www.bevindustry.com/arti

cles/87615-state-of-the-industry-coffee-and-rtd-coffee.12 ICO Indicator Prices. Online. Available, http://www.ico.org/prices/

p2.htm.13 “State of the Beverage Market 2013,” Beverage World, May 2013. 14 Ibid.15 “Can Consumer Staples Rebound?” Zacks, Online, Available

http://www.zacks.com/commentary/32930/can-consumer-sta

ples-rebound.16 “Restaurant sales, traffic rebound in March,” Nation’s Restaurant

News, Online, Available http://nrn.com/rpi/nra-restaurant-sales-

traffic-rebound-march.

References and Data Sources

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital // Data Source: Bloomberg 12 www.mercercapital.com

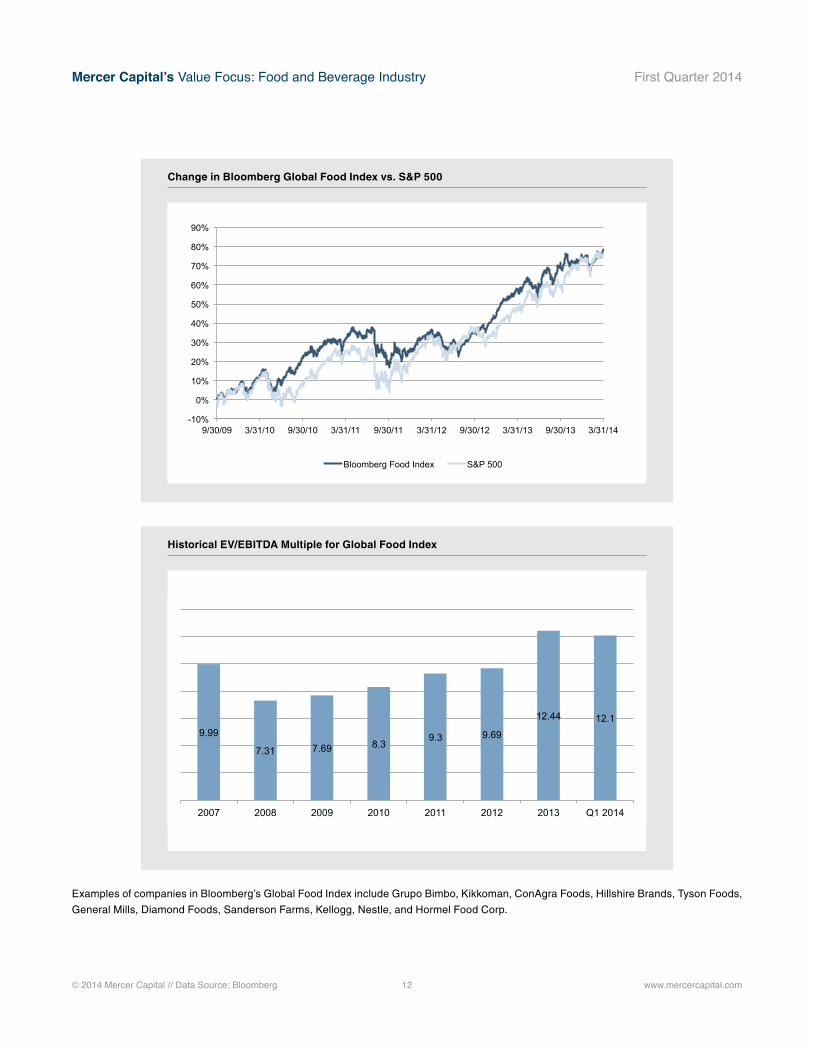

Change in Bloomberg Global Food Index vs. S&P 500

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

9/30/09 3/31/10 9/30/10 3/31/11 9/30/11 3/31/12 9/30/12 3/31/13 9/30/13 3/31/14

Bloomberg Food Index S&P 500

9.99

7.31 7.69 8.3 9.3 9.69

12.44 12.1

2007 2008 2009 2010 2011 2012 2013 Q1 2014

Change in Bloomberg Global Food Index vs. S&P 500

Historical EV/EBITDA Multiple for Global Food Index

Examples of companies in Bloomberg’s Global Food Index include Grupo Bimbo, Kikkoman, ConAgra Foods, Hillshire Brands, Tyson Foods,

General Mills, Diamond Foods, Sanderson Farms, Kellogg, Nestle, and Hormel Food Corp.

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

© 2014 Mercer Capital // Data Source: Bloomberg 13 www.mercercapital.com

Examples of companies in Bloomberg’s Global Food Index include Grupo Bimbo, Kikkoman, ConAgra Foods, Hillshire Brands, Tyson Foods,

General Mills, Diamond Foods, Sanderson Farms, Kellogg, Nestle, and Hormel Food Corp.

-20%

0%

20%

40%

60%

80%

100%

120%

140%

9/30/09 3/31/10 9/30/10 3/31/11 9/30/11 3/31/12 9/30/12 3/31/13 9/30/13 3/31/14

Bloomberg Beverage Index S&P 500

Historical EV / EBITDA MultipleBloomberg Beverage Index

8.51 9.57

10.96 10.29 10.81 11.44 11.85

2008 2009 2010 2011 2012 2013 Q1 2014

Change in Bloomberg Beverage Index vs. S&P 500

Historical EV/EBITDA Multiple for Beverage Index

© 2014 Mercer Capital // www.mercercapital.com 14

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

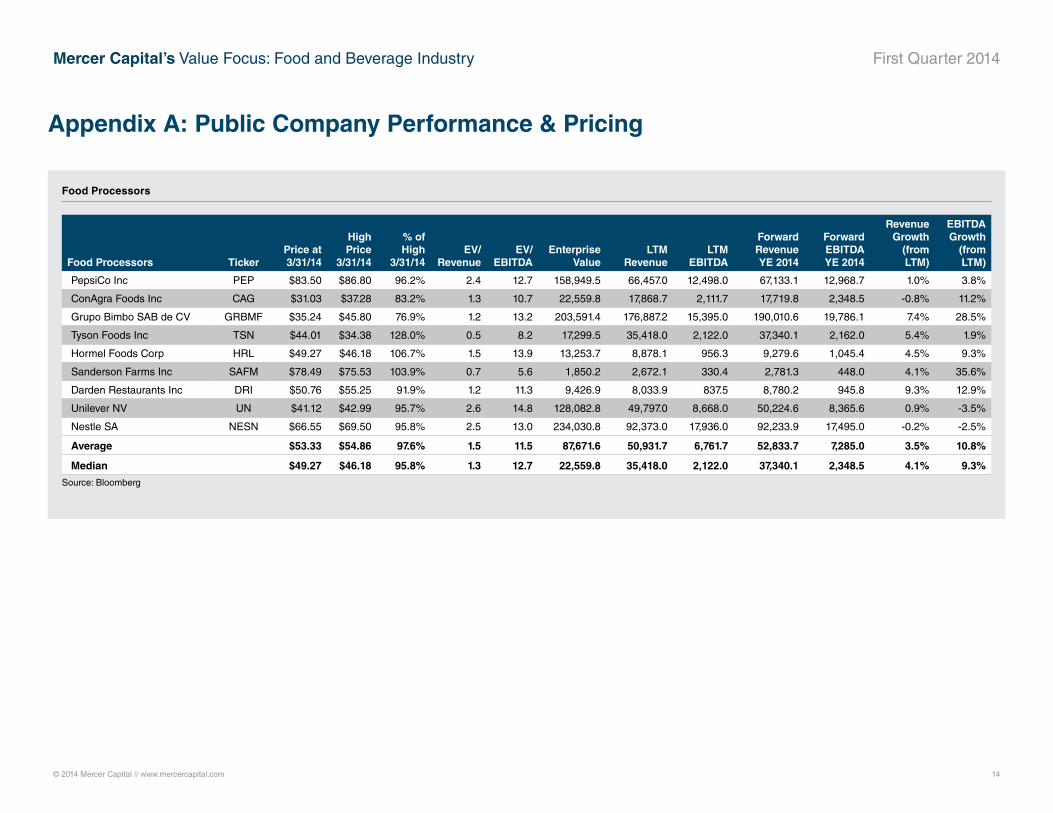

Appendix A: Public Company Performance & Pricing

Food Processors

Food Processors TickerPrice at 3/31/14

High Price

3/31/14

% of High

3/31/14EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2014

Forward EBITDA YE 2014

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

PepsiCo Inc PEP $83.50 $86.80 96.2% 2.4 12.7 158,949.5 66,457.0 12,498.0 67,133.1 12,968.7 1.0% 3.8%

ConAgra Foods Inc CAG $31.03 $37.28 83.2% 1.3 10.7 22,559.8 17,868.7 2,111.7 17,719.8 2,348.5 -0.8% 11.2%

Grupo Bimbo SAB de CV GRBMF $35.24 $45.80 76.9% 1.2 13.2 203,591.4 176,887.2 15,395.0 190,010.6 19,786.1 7.4% 28.5%

Tyson Foods Inc TSN $44.01 $34.38 128.0% 0.5 8.2 17,299.5 35,418.0 2,122.0 37,340.1 2,162.0 5.4% 1.9%

Hormel Foods Corp HRL $49.27 $46.18 106.7% 1.5 13.9 13,253.7 8,878.1 956.3 9,279.6 1,045.4 4.5% 9.3%

Sanderson Farms Inc SAFM $78.49 $75.53 103.9% 0.7 5.6 1,850.2 2,672.1 330.4 2,781.3 448.0 4.1% 35.6%

Darden Restaurants Inc DRI $50.76 $55.25 91.9% 1.2 11.3 9,426.9 8,033.9 837.5 8,780.2 945.8 9.3% 12.9%

Unilever NV UN $41.12 $42.99 95.7% 2.6 14.8 128,082.8 49,797.0 8,668.0 50,224.6 8,365.6 0.9% -3.5%

Nestle SA NESN $66.55 $69.50 95.8% 2.5 13.0 234,030.8 92,373.0 17,936.0 92,233.9 17,495.0 -0.2% -2.5%

Average $53.33 $54.86 97.6% 1.5 11.5 87,671.6 50,931.7 6,761.7 52,833.7 7,285.0 3.5% 10.8%

Median $49.27 $46.18 95.8% 1.3 12.7 22,559.8 35,418.0 2,122.0 37,340.1 2,348.5 4.1% 9.3%

Source: Bloomberg

© 2014 Mercer Capital // www.mercercapital.com 15

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

Appendix A: Public Company Performance & Pricing

Restaurants

Restaurants TickerPrice at 3/31/14

High Price

3/31/14

% of High

3/31/14EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2014

Forward EBITDA YE 2014

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

Frisch's Restaurants Inc FRS $23.67 $26.44 89.5% 0.7 6.3 133.4 204.4 21.0 206.0 na 0.8% nm

Ruby Tuesday Inc RT $5.61 $9.90 56.7% 0.5 nm 611.6 1,177.5 -0.9 1,165.3 39.8 -1.0% nm

Darden Restaurants Inc DRI $50.76 $55.25 91.9% 1.2 11.3 9,426.9 8,033.9 837.5 8,780.2 945.8 9.3% 12.9%

Denny's Corp DENN $6.43 $7.51 85.6% 1.6 11.1 740.8 460.0 66.9 464.8 81.7 1.0% 22.2%

Bob Evans Farms Inc/DE BOBE $50.03 $60.22 83.1% 1.2 11.7 1,658.7 1,336.1 141.7 1,334.5 142.7 -0.1% 0.6%

DineEquity Inc DIN $78.07 $85.74 91.1% 4.5 11.5 2,871.4 644.5 249.4 644.0 270.3 -0.1% 8.4%

Red Robin Gourmet Burgers Inc RRGB $71.68 $86.83 82.6% 1.1 10.8 1,118.1 1,017.2 103.5 1,148.8 118.9 12.9% 14.8%

Cracker Barrel Old Country Store Inc CBRL $97.24 $118.63 82.0% 1.0 10.1 2,716.3 2,662.1 269.0 2,679.6 283.8 0.7% 5.5%

Average $47.94 $56.31 82.8% 1.5 10.4 2,409.6 1,942.0 211.0 2,052.9 269.0 2.9% 10.7%

Median $50.40 $57.73 84.4% 1.1 11.1 1,388.4 1,097.4 122.6 1,157.0 142.7 0.7% 10.7%

Source: Bloomberg

© 2014 Mercer Capital // www.mercercapital.com 16

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

Non-Alcoholic Beverages

Non-Alcoholic Beverages TickerPrice at 3/31/14

High Price

3/31/14

% of High

3/31/14EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2014

Forward EBITDA YE 2014

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

PepsiCo Inc PEP $83.50 $86.80 96.2% 2.4 12.7 158,949.5 66,457.0 12,498.0 67,133.1 12,968.7 1.0% 3.8%

Dr Pepper Snapple Group Inc DPS $54.46 $54.46 100.0% 2.2 10.0 13,463.8 6,015.0 1,346.0 6,038.3 1,396.6 0.4% 3.8%

National Beverage Corp FIZZ $19.51 $21.47 90.9% 1.5 12.1 936.0 644.7 77.6 na na nm nm

Coca-Cola Co/The KO $38.66 $43.43 89.0% 4.5 17.1 208,235.7 46,395.0 12,173.0 46,655.7 13,173.9 0.6% 8.2%

Monster Beverage Corp MNST $69.45 $74.79 92.9% 5.0 18.2 11,603.3 2,298.3 638.6 2,454.2 725.7 6.8% 13.6%

Starbucks Corp SBUX $73.38 $82.50 88.9% 3.7 18.1 57,383.9 15,650.1 3,167.8 16,500.0 3,771.2 5.4% 19.0%

Average $56.49 $60.58 93.0% 3.2 14.7 75,095.4 22,910.0 4,983.5 27,756.3 6,407.2 2.8% 9.7%

Median $61.96 $64.63 91.9% 3.0 14.9 35,423.9 10,832.6 2,256.9 16,500.0 3,771.2 1.0% 8.2%

Source: Bloomberg

Appendix A: Public Company Performance & Pricing

© 2014 Mercer Capital // www.mercercapital.com 17

Mercer Capital’s Value Focus: Food and Beverage Industry First Quarter 2014

Alcoholic Beverages

Alcoholic Beverages TickerPrice at 3/31/14

High Price

3/31/14

% of High

3/31/14EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2014

Forward EBITDA YE 2014

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

Anheuser-Busch InBev NV BUD $105.30 $106.83 98.6% 5.1 12.7 218,427.34 43,195.0 17,188.0 47,764.5 19,234.2 10.6% 11.9%

Craft Brew Alliance Inc BREW $15.27 $18.70 81.7% 1.6 20.5 301.60 186.4 14.7 207.0 na 11.1% nm

Constellation Brands Inc STZ $84.97 $84.97 100.0% 4.8 18.4 23,289.71 4,867.7 1,262.6 4,863.2 1,369.7 -0.1% 8.5%

Diageo PLC DEO $124.59 $134.08 92.9% 28.6 83.5 322,580.95 11,260.0 3,863.0 10,519.9 3,680.7 -6.6% -4.7%

Boston Beer Co Inc/The SAM $244.73 $265.53 92.2% 4.0 21.9 3,173.53 787.0 144.8 917.0 175.0 16.5% 20.9%

Molson Coors Brewing Co TAP $58.86 $58.86 100.0% 3.6 14.6 15,111.48 4,193.6 1,032.9 4,234.6 1,285.4 1.0% 24.4%

Brown-Forman Corp BF/B $89.69 $89.74 99.9% 6.8 20.0 20,173.38 2,961.0 1,010.9 3,987.2 1,024.6 34.7% 1.4%

Average $103.34 $108.39 95.0% 7.8 27.4 86,151.1 9,635.8 3,502.4 10,356.2 4,461.6 9.6% 10.4%

Median $89.69 $89.74 98.6% 4.8 20.0 20,173.4 4,193.6 1,032.9 4,234.6 1,327.6 10.6% 10.2%

Source: Bloomberg

Appendix A: Public Company Performance & Pricing

Mercer CapitalFood & Beverage Industry Services

Contact Us

Copyright © 2014 Mercer Capital Management, Inc. All rights reserved. It is illegal under Federal law to reproduce this publication or any portion of its contents without the publisher’s permission. Media

quotations with source attribution are encouraged. Reporters requesting additional information or editorial comment should contact Barbara Walters Price at 901.685.2120. Mercer Capital’s Industry

Focus is published quarterly and does not constitute legal or financial consulting advice. It is offered as an information service to our clients and friends. Those interested in specific guidance for legal or

accounting matters should seek competent professional advice. Inquiries to discuss specific valuation matters are welcomed. To add your name to our mailing list to receive this complimentary publication,

visit our web site at www.mercercapital.com.

Mercer Capital has expertise providing business valuation and financial advisory services to companies in the food and beverage industry.

Industry Segments

Mercer Capital serves the following industry segments:

• Food processing

• Restaurants

• Nonalcoholic Beverages

• Malt, Wine, and Spirits

Services Provided

• Valuation of food and beverage industry companies

• Transaction advisory for acquisitions and divestitures

• Valuations for purchase accounting and impairment testing

• Fairness and solvency opinions

• Litigation support for economic damages and valuation and shareholder disputes

Contact a Mercer Capital professional to discuss your needs in confidence.

Matthew R. Crow, CFA, [email protected]

Timothy R. Lee, [email protected]

Nicholas J. Heinz, [email protected]

Travis W. Harms, CFA, CPA/[email protected]

Mercer Capital5100 Poplar Avenue, Suite 2600Memphis, Tennessee 38137901.685.2120 (P)

www.mercercapital.com

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES