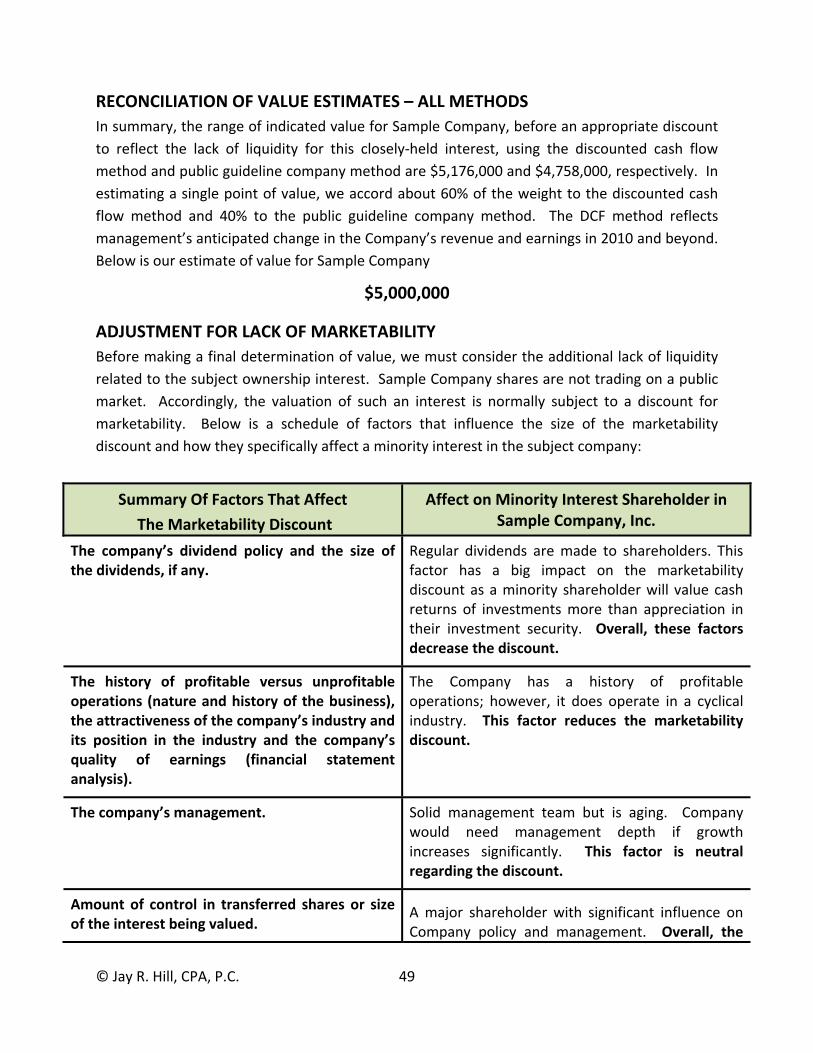

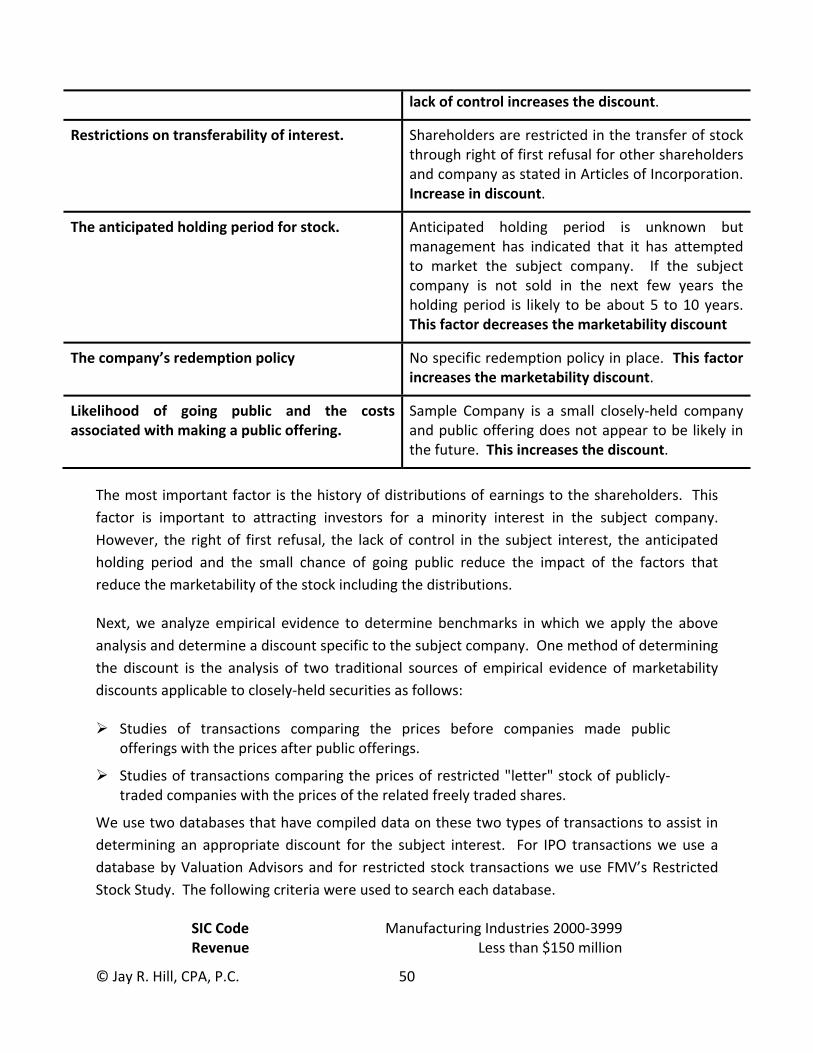

Valuation of Sample Company, Inc. -...

62

Valuation of Sample Company, Inc. April 30, 2010 Jay R. Hill, CPA, P.C. Jay R. Hill, CPA ABV

Transcript of Valuation of Sample Company, Inc. -...

Valuation of Sample Company, Inc. April 30, 2010

Jay R. Hill, CPA, P.C. Jay R. Hill, CPA ABV

Jay R. Hill, CPA, P.C. A Professional Corporation Phone (816) 505‐2038 6124 S. National Dr. Fax (816) 505‐2038 Cell (816) 674‐3141 Parkville, Missouri 64152 Email [email protected]

www.jrhillco.com John Sample, President Sample Company, Inc. We have been engaged to establish a reasonable estimate of the fair market value of a minority interest in the common stock of Sample Company, Inc. (herein referred to as either “Sample Company” or “the Company”), a Florida Corporation, as of April 30, 2010. It is our understanding that this valuation is solely for gift and estate tax purposes. The subject interest is expected to be between 1% to 49% of voting common stock. It is our understanding that you and other Company representatives agree to restrict the use of this report for the stated purposes and that no distribution of this report to outside parties to obtain credit or for any other purpose will occur. We conduct this valuation engagement and present our detailed report in conformity with the “Statement of Standards for Valuation Services No. 1” (SSVS) of the American Institute of Certified Public Accountants.1 Our analysis and report are also performed with reference to the Uniform Standards of Professional Appraisal Practice (“USPAP”) promulgated by the Appraisal Foundation and with IRS business valuation development and reporting guidelines including Revenue Ruling 59‐60 (C.B. 1959‐1, 237), as modified and amplified, which provides guidelines for the valuation of closely‐held corporate stock for federal income, estate and gift tax purposes. Revenue Ruling 59‐60, while used in tax valuations, is also used in many nontax valuations. The standard of value for this valuation is fair market value. A common definition reference is Revenue Ruling 59‐60, which defines fair market value as “the price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts.” In performing our valuation, we rely on the accuracy and reliability of historical financial statements along with other financial data and oral representations of Company representatives. We will not audit or review such financial statements or other data, and we do not express an opinion or any other form of assurance on them. Based on our valuation study of Sample Company as described in the body of this report, it is our opinion that the fair market value of a minority interest in Sample Company’s common stock as of April 30, 2010 is

1 SSVS defines a valuation engagement as “an engagement to estimate value in which a valuation analyst determines an estimate of the value of a subject interest by performing appropriate procedures, as outlined in the AICPA Statement on Standards for Valuation Services, and is free to apply the valuation approaches and methods he or she deems appropriate in the circumstances. The valuation analyst expresses the results of the valuation engagement as a conclusion of value, which may be either a single amount or a range.”

$370 per share

We base our conclusion on the documents and information in Exhibit A and our opinion is subject to the assumptions and limiting conditions listed in the last section of this report. No one should rely on this engagement to disclose errors, irregularities, or illegal acts, including fraud or defalcations, that may exist in the financial information and/or operations of the subject entity. July 2, 2010 Kansas City, Missouri

© Jay R. Hill, CPA, P.C. 1

Table of Contents

CERTIFICATION STATEMENT .............................................................................................. 2 INTRODUCTION .................................................................................................................... 3 METHODOLOGY AND GUIDELINES ............................................................................................. 3 STANDARD AND PREMISE OF VALUE .......................................................................................... 4 PROCEDURES AND DOCUMENTATION ....................................................................................... 4

OVERVIEW ............................................................................................................................. 5 NATURE AND HISTORY OF THE COMPANY ................................................................................. 5 PRODUCTS, PRODUCT QUALIFICATIONS AND CERTIFICATIONS ................................................. 5 DISTRIBUTION AND COMPETITION ............................................................................................. 6 MANAGEMENT AND EMPLOYEES ............................................................................................... 6 FACILITIES .................................................................................................................................... 7 FINANCIAL OVERVIEW ................................................................................................................ 7 STOCK OWNERSHIP AND TRANSFERS OF STOCK ........................................................................ 8

ECONOMIC AND INDUSTRY OUTLOOK ............................................................................... 9 NATIONAL ECONOMY OVERVIEW .............................................................................................. 9 ECONOMIC OUTLOOK ............................................................................................................... 13 REGIONAL AND LOCAL ECONOMIC OVERVIEW AND OUTLOOK .............................................. 14 INDUSTRY OVERVIEW AND OUTLOOK – AEROSPACE AND DEFENSE ....................................... 15 IMPACT ON COMPANY ............................................................................................................. 19

FINANCIAL STATEMENT ANALYSIS .................................................................................. 20 FINANCIAL POSITION OF COMPANY AND TRENDS ................................................................... 20 OPERATING RESULTS AND TRENDS .......................................................................................... 21 RATIO ANALYSIS ........................................................................................................................ 23 DETAILED FINANCIAL STATEMENTS .......................................................................................... 24

VALUATION ANALYSIS AND CONCLUSION OF VALUE ..................................................... 28 SUMMARY OF PERTINENT FACTORS ......................................................................................... 28 VALUATION ANALYSIS ............................................................................................................... 28 VALUATION METHODS CONSIDERED BUT NOT UTILIZED ........................................................ 29 DISCOUNTED CASH FLOW METHOD ......................................................................................... 30 PROJECTION ASSUMPTIONS ..................................................................................................... 34 RECONCILIATION OF VALUE ESTIMATES – DCF METHOD ........................................................ 39 PUBLIC GUIDELINE COMPANY METHOD .................................................................................. 40 DEVELOPMENT OF VALUE FACTORS – GUIDELINE COMPANIES .............................................. 40 RECONCILIATION OF VALUE ESTIMATES – ALL METHODS ....................................................... 49 ADJUSTMENT FOR LACK OF MARKETABILITY ........................................................................... 49 VALUATION SUMMARY AND CONCLUSION OF VALUE ............................................................. 53

ASSUMPTIONS AND LIMITING CONDITIONS .................................................................... 54 DOCUMENTS ANALYZED AND UTILIZED .......................................................................... 57 QUALIFICATIONS OF VALUATOR ...................................................................................... 58 INDEPENDENCE OF VALUATOR......................................................................................... 58 EXHIBIT C ‐ OMITTED

© Jay R. Hill, CPA, P.C. 2

CERTIFICATION STATEMENT Except as otherwise noted in this appraisal report, I certify that to the best of my knowledge and

belief: 1) The statements of fact contained in this report are true and correct. 2) The reported analyses, opinions and conclusions are limited only by the reported

assumptions and limiting conditions, and are my personal, impartial and unbiased professional analyses, opinions, and conclusions.

3) I have no present or prospective interest in the property that was the subject of this report,

and I have no personal interest or bias with respect to the parties involved. 4) I have no bias with respect to the property that was the subject of this report or to the

parties involved with this assignment. 5) My engagement in this assignment was not contingent upon developing or reporting

predetermined results. 6) My compensation for completing this assignment was not contingent upon the

development or reporting of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result or the occurrence of a subsequent event directly related to the intended use of this appraisal.

7) My analyses, opinions and conclusions are developed, and this report was prepared, in

conformity with the Uniform Standards of Professional Appraisal Practice. 8) No one provided significant business appraisal assistance to the person signing this certification. Jay R. Hill, CPA∙ABV

© Jay R. Hill, CPA, P.C. 3

INTRODUCTION We have been engaged to estimate the fair market value of a minority interest in the common

stock of Sample Company, Inc., a Florida Corporation, as of April 30, 2010 for gift and estate tax

purposes. It is our understanding that the results of this study will determine the per share

price of potential transfers of common stock by John Sample.

METHODOLOGY AND GUIDELINES

We have performed a valuation engagement and present our detailed report in conformity with

the “Statement of Standards for Valuation Services No. 1” (SSVS) of the American Institute of

Certified Public Accountants. SSVS defines a valuation engagement as “an engagement to

estimate value in which a valuation analyst determines an estimate of the value of a subject

interest by performing appropriate procedures, as outlined in the AICPA Statement on Standards

for Valuation Services, and is free to apply the valuation approaches and methods he or she deems

appropriate in the circumstances. The valuation analyst expresses the results of the valuation

engagement as a conclusion of value, which may be either a single amount or a range.”

SSVS addresses a detailed report as follows: “The detailed report is structured to provide sufficient

information to permit intended users to understand the data, reasoning, and analyses underlying

the valuation analyst’s conclusion of value.”

The valuation of an interest in a closely‐held entity requires the consideration of a number of

factors. Revenue Ruling 59‐60 outlines the basic methodology we employ in this valuation. The

factors in 59‐60 are essential in estimating the fair market value of a closely‐held entity; however,

we do not limit our valuation analysis to these factors.

Revenue Ruling 59‐60 – The factors in Revenue Ruling 59‐60 are as follows:

The nature of the business and the history of the enterprise from its inception. The economic outlook in general and the condition and outlook of the specific industry

in particular. The book value of the stock and the financial condition of the business. The earnings capacity of the company. The dividend‐paying capacity of the company. Whether or not the enterprise has goodwill or other intangible value. Sales of the stock and the size of the block of stock to be valued. The market price of stocks of corporations engaged in the same or similar line of

business having their stocks actively traded in a free and open market, either on an exchange or over‐the‐counter.

© Jay R. Hill, CPA, P.C. 4

STANDARD AND PREMISE OF VALUE

The standard of value that we are determining in this study is fair market value. Revenue

Ruling 59‐60 defines fair market value as:

The price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts.

Fair market value is also defined in a similar way in the International Glossary of Business

Valuation Terms as:

The price, expressed in terms of cash equivalents, at which property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arm’s length in an open and unrestricted market, when neither is under compulsion to buy or sell and when both have reasonable knowledge of the relevant facts.

The premise of value is going concern. The liquidation premise of value was considered and

rejected as not applicable, as the going‐concern value results in a higher value for the interest

than the liquidation value, whether orderly or fixed.

PROCEDURES AND DOCUMENTATION

In reaching our valuation conclusion, we perform certain procedures including the following:

Review and analyze the Company’s financial information from 2005 through 2009. Review and analyze other pertinent documents provided by management and the

Company’s outside accountant. Review and analyze economic, industry and equity market data. Interview management and make a site visit to the Company’s headquarters and

manufacturing facility.

Descriptions of the documents we use in this valuation are in Exhibit A. The

qualifications and independence of the valuator are set forth in Exhibit B.

© Jay R. Hill, CPA, P.C. 5

OVERVIEW

NATURE AND HISTORY OF THE COMPANY

Sample Company is a manufacturer of aerospace fasteners, specifically hex head bolts and

machine screws compliant with industry standards and certifications. Founded in 1995 by John

Sample, the Company’s products are sold to distributors who resell to original equipment

manufacturers, aftermarket repair companies and military users on a worldwide basis. The

Company’s primary manufacturing facility is located in Ft. Lauderdale, Florida.

PRODUCTS, PRODUCT QUALIFICATIONS AND CERTIFICATIONS

Sample Company manufactures hex head bolts and machine screws compliant to several parts

standards such as AN (Army‐Navy Aeronautical Standard), NAS (National Aerospace Standard)

and MS (Military Standard). No one standard product accounts for more than 2% of total

revenue.

OEMs

The Company is an approved manufacturer for the following original equipment manufacturers

(OEMs):

Aerostructures Airbus Allied Signal Aramco BAE Systems USA Boeing Defense & Space Bombardier Cessna Defense Logistics Agency Lockheed Martin Missiles & Space Lockheed Martin (Orlando) Lockheed (Sanders) McDonnell Douglas Pfalz ‐ Fugzeugwerke Raytheon

The Company has been approved by the above manufacturers for three years or more.

CERTIFICATIONS

Sample Company holds the following industry certifications:

AS9100/ISO9000 Registered

Defense Logistics Agency QSLM and DSCP Approval

© Jay R. Hill, CPA, P.C. 6

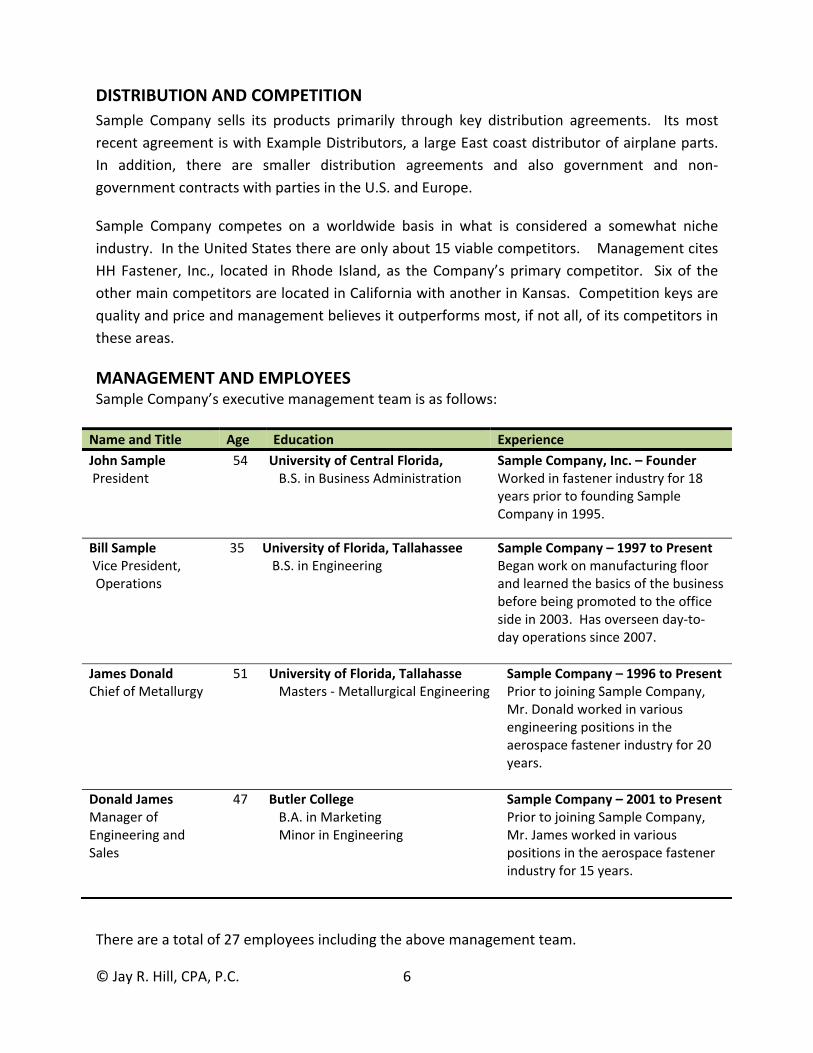

DISTRIBUTION AND COMPETITION

Sample Company sells its products primarily through key distribution agreements. Its most

recent agreement is with Example Distributors, a large East coast distributor of airplane parts.

In addition, there are smaller distribution agreements and also government and non‐

government contracts with parties in the U.S. and Europe.

Sample Company competes on a worldwide basis in what is considered a somewhat niche

industry. In the United States there are only about 15 viable competitors. Management cites

HH Fastener, Inc., located in Rhode Island, as the Company’s primary competitor. Six of the

other main competitors are located in California with another in Kansas. Competition keys are

quality and price and management believes it outperforms most, if not all, of its competitors in

these areas.

MANAGEMENT AND EMPLOYEES Sample Company’s executive management team is as follows:

Name and Title Age Education Experience

John Sample President

54 University of Central Florida, B.S. in Business Administration

Sample Company, Inc. – Founder Worked in fastener industry for 18 years prior to founding Sample Company in 1995.

Bill Sample Vice President, Operations

35 University of Florida, Tallahassee B.S. in Engineering

Sample Company – 1997 to Present Began work on manufacturing floor and learned the basics of the business before being promoted to the office side in 2003. Has overseen day‐to‐day operations since 2007.

James Donald Chief of Metallurgy

51 University of Florida, Tallahasse Masters ‐ Metallurgical Engineering

Sample Company – 1996 to Present Prior to joining Sample Company, Mr. Donald worked in various engineering positions in the aerospace fastener industry for 20 years.

Donald James Manager of Engineering and Sales

47 Butler College B.A. in Marketing Minor in Engineering

Sample Company – 2001 to Present Prior to joining Sample Company, Mr. James worked in various positions in the aerospace fastener industry for 15 years.

There are a total of 27 employees including the above management team.

© Jay R. Hill, CPA, P.C. 7

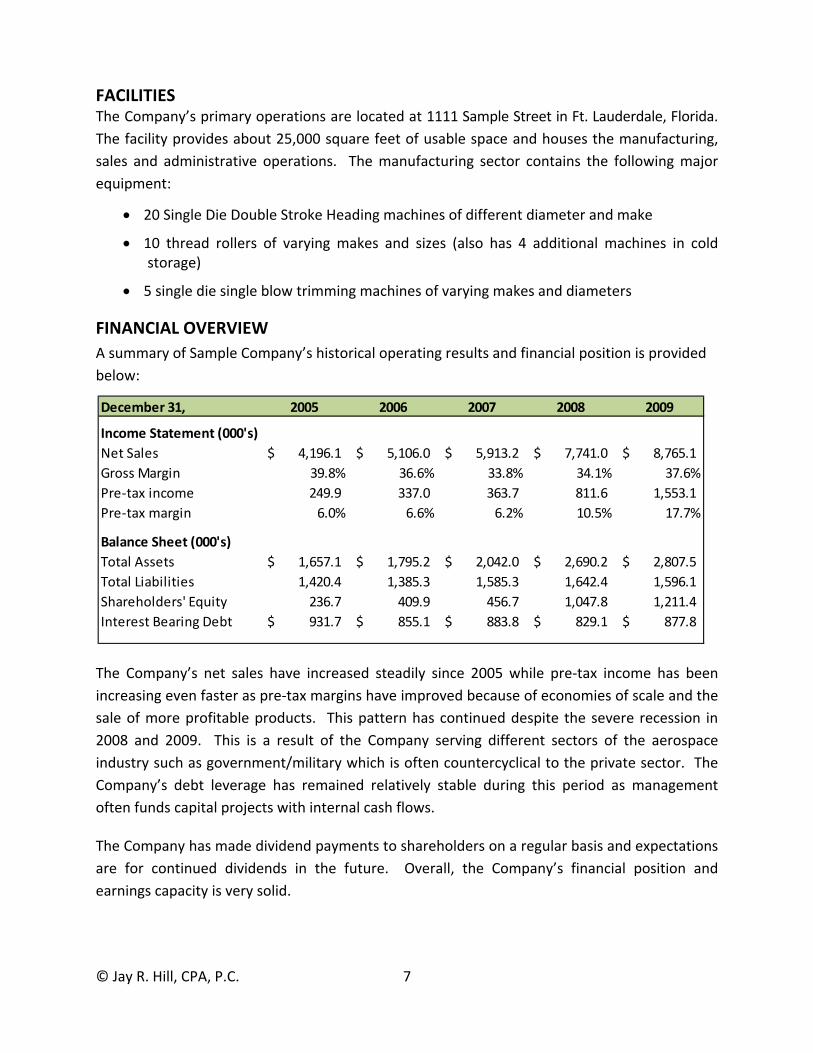

FACILITIES The Company’s primary operations are located at 1111 Sample Street in Ft. Lauderdale, Florida.

The facility provides about 25,000 square feet of usable space and houses the manufacturing,

sales and administrative operations. The manufacturing sector contains the following major

equipment:

20 Single Die Double Stroke Heading machines of different diameter and make

10 thread rollers of varying makes and sizes (also has 4 additional machines in cold storage)

5 single die single blow trimming machines of varying makes and diameters

FINANCIAL OVERVIEW

A summary of Sample Company’s historical operating results and financial position is provided

below:

The Company’s net sales have increased steadily since 2005 while pre‐tax income has been

increasing even faster as pre‐tax margins have improved because of economies of scale and the

sale of more profitable products. This pattern has continued despite the severe recession in

2008 and 2009. This is a result of the Company serving different sectors of the aerospace

industry such as government/military which is often countercyclical to the private sector. The

Company’s debt leverage has remained relatively stable during this period as management

often funds capital projects with internal cash flows.

The Company has made dividend payments to shareholders on a regular basis and expectations

are for continued dividends in the future. Overall, the Company’s financial position and

earnings capacity is very solid.

December 31, 2005 2006 2007 2008 2009

Income Statement (000's)

Net Sales 4,196.1$ 5,106.0$ 5,913.2$ 7,741.0$ 8,765.1$

Gross Margin 39.8% 36.6% 33.8% 34.1% 37.6%

Pre‐tax income 249.9 337.0 363.7 811.6 1,553.1

Pre‐tax margin 6.0% 6.6% 6.2% 10.5% 17.7%

Balance Sheet (000's)

Total Assets 1,657.1$ 1,795.2$ 2,042.0$ 2,690.2$ 2,807.5$

Total Liabilities 1,420.4 1,385.3 1,585.3 1,642.4 1,596.1

Shareholders' Equity 236.7 409.9 456.7 1,047.8 1,211.4

Interest Bearing Debt 931.7$ 855.1$ 883.8$ 829.1$ 877.8$

© Jay R. Hill, CPA, P.C. 8

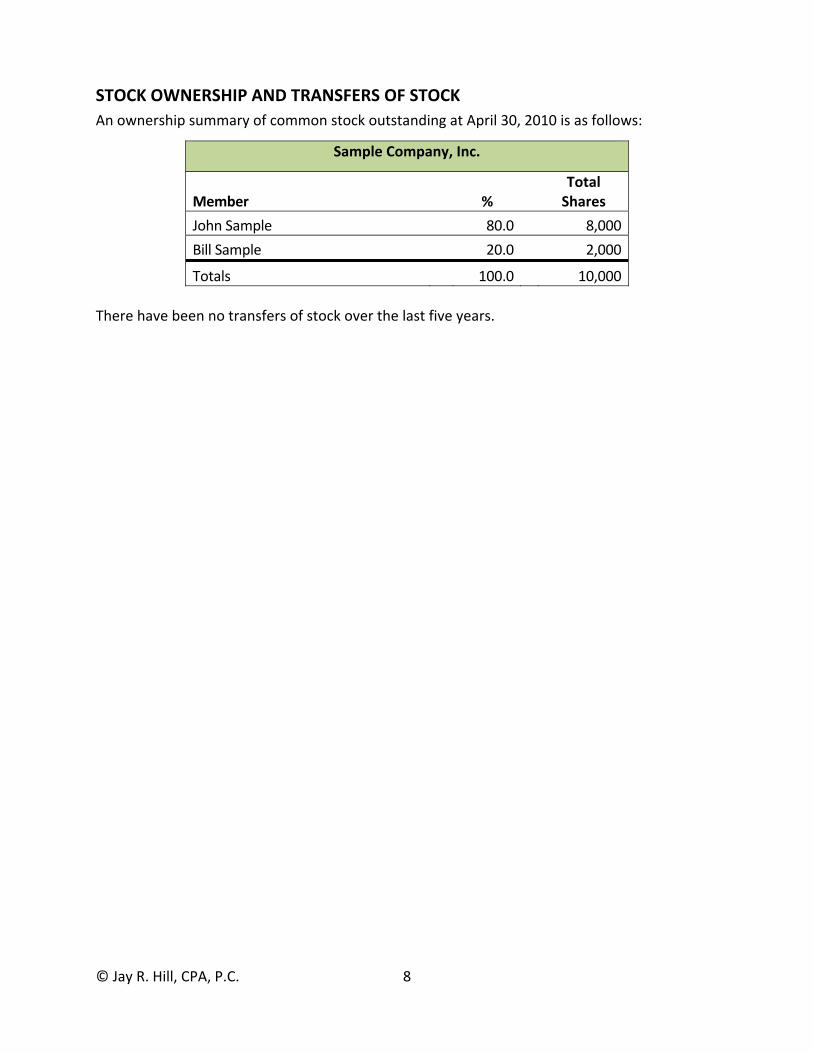

STOCK OWNERSHIP AND TRANSFERS OF STOCK

An ownership summary of common stock outstanding at April 30, 2010 is as follows:

Sample Company, Inc.

Member % Total

Shares

John Sample 80.0 8,000

Bill Sample 20.0 2,000

Totals 100.0 10,000

There have been no transfers of stock over the last five years.

© Jay R. Hill, CPA, P.C. 9

ECONOMIC AND INDUSTRY OUTLOOK Understanding the current state of the national economy and its impact on business entities in

the United States is important for the valuation of a privately held entity. The following section

discusses general economic indicators, their historical trends and outlook.

NATIONAL ECONOMY OVERVIEW2

The gross domestic product (GDP), the broadest measure of the U.S. economy, grew at a 3.2%

annual rate in the first quarter of 2010. The GDP is the total market value of goods and services

produced in the U.S. economy and is generally considered the most comprehensive measure of

economic growth. President Obama called this news “an important milepost on our road to

recovery.” He went on to say, “After the single biggest economic crisis in our lifetimes, we're

heading in the right direction.”

However, GDP growth this quarter was slightly less than some analysts had forecasted, as

economists surveyed by

Briefing.com forecasted

3.3% growth. "Despite a

softer headline number

than we had expected, this

is an encouraging report,"

said economist Peter

Newland of Barclays Capital.

After three consecutive quarters of economic growth, most economists now agree that the

recession ended at some point in the middle of 2009. Regardless, the recession still has not

been declared officially over. The National Bureau of Economic Research, which determines

the lengths of business cycles, said this month that it “would be premature” to set a date

marking the end of the recession and the start of an economic expansion. A major reason for

that decision was the high unemployment rate.

Christina Romer, chair of the White House Council of Economic Advisers, also remains cautious.

“Given the severity and depth of the recession,” stated Romer, “it will take a number of

quarters of robust growth and strong employment gains to return the economy to full health

and full employment.”

2 Most of the contents of the economic outlook section of this valuation report are quoted from the Economic Outlook Update™ 1Q 2010 published by Business Valuation Resources, LLC, © 2010, reprinted with permission. The editors and Business Valuation Resources, LLC, while considering the contents to be accurate as of the date of publication of the Update, take no responsibility for the information contained therein. Relation of this information to this valuation engagement is the sole responsibility of the author of this valuation report.

AFTER THREE CONSECUTIVE QUARTERS OF ECONOMIC GROWTH, MOST ECONOMISTS NOW AGREE THAT THE RECESSION ENDED AT SOME POINT IN THE MIDDLE OF 2009. REGARDLESS, THE RECESSION STILL HAS NOT BEEN DECLARED OFFICIALLY OVER.

© Jay R. Hill, CPA, P.C. 10

With consumer spending experiencing its biggest rate of increase in three years, it was the

largest contributor to this quarter’s GDP growth. “Consumer spending has come out of the

deep freeze,” said Sung Won Sohn, economics professor at Cal State University Channel Islands.

“To be sure, the job market is poor and yet to show sustained recovery, but consumers are

feeling better about the future.”

Josh Bivens, an economist with the Economic Policy Institute, notes that disposable personal

incomes remained flat this quarter, indicating that personal spending rose simply because

savings rates fell. “A recovery that relies on savings rates retreating back to their pre‐recession

minimums would be extremely fragile,” warns Bivens.

State and local government spending declined for a third straight quarter, dragging the GDP

down. The decline in state and local government spending was the biggest drop since 1981.

This is largely due to budget crises. “Given balanced budget rules at the state‐level, this implies

that states will be cutting spending and/or raising taxes for years to come and hence exerting a

powerful drag on growth,” states Bivens.

The 3.2% growth in the first quarter of 2010 was the third straight quarter of economic growth.

The economy grew at a 5.6% annualized rate last quarter. The largest contributions to growth

came from personal consumption expenditures and a rise in inventory investment, which

added 2.55 and 1.57 percentage points to the GDP, respectively.

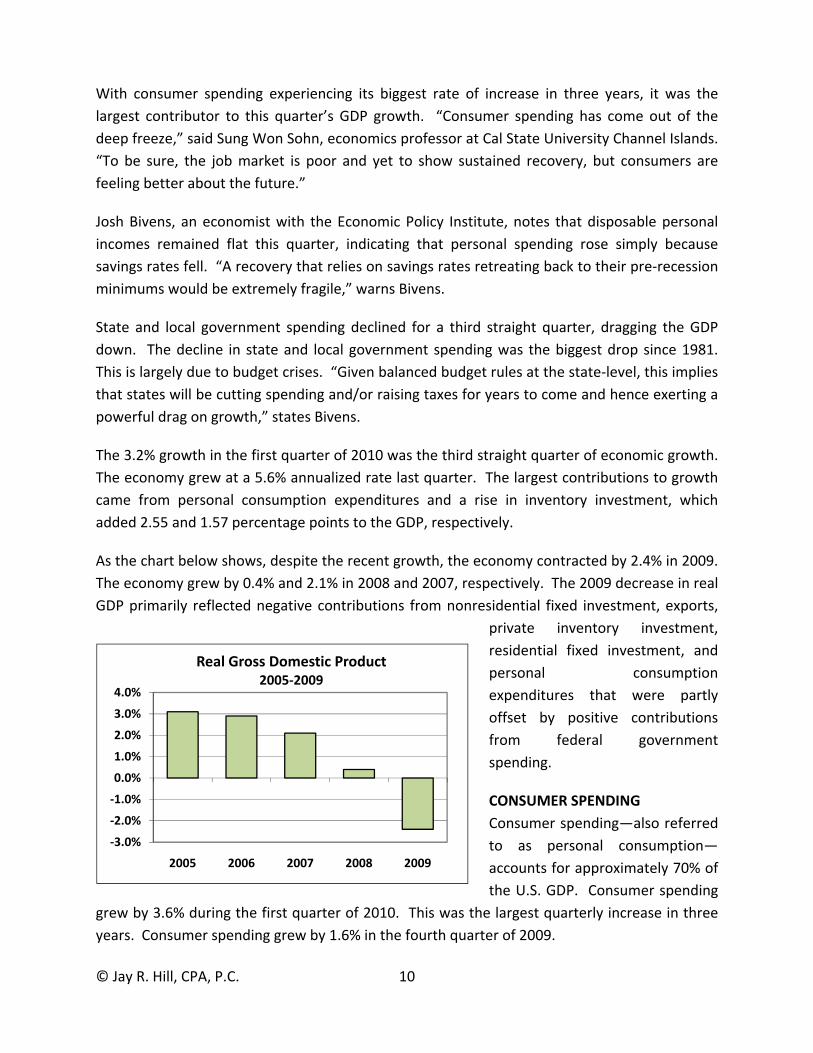

As the chart below shows, despite the recent growth, the economy contracted by 2.4% in 2009.

The economy grew by 0.4% and 2.1% in 2008 and 2007, respectively. The 2009 decrease in real

GDP primarily reflected negative contributions from nonresidential fixed investment, exports,

private inventory investment,

residential fixed investment, and

personal consumption

expenditures that were partly

offset by positive contributions

from federal government

spending.

CONSUMER SPENDING

Consumer spending—also referred

to as personal consumption—

accounts for approximately 70% of

the U.S. GDP. Consumer spending

grew by 3.6% during the first quarter of 2010. This was the largest quarterly increase in three

years. Consumer spending grew by 1.6% in the fourth quarter of 2009.

‐3.0%

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2005 2006 2007 2008 2009

Real Gross Domestic Product2005‐2009

© Jay R. Hill, CPA, P.C. 11

GOVERNMENT SPENDING

Total government spending decreased at a rate of 1.8% in the first quarter. Government

spending fell 1.3% in the fourth quarter of 2009 but grew 2.6% in the third. This quarter’s

decline in government spending had a negative 0.37 percentage point effect on the first‐

quarter GDP. The previous quarter’s decline in government spending had a negative 0.26

percentage point effect on the fourth‐quarter GDP. The primary reason for these declines was

severe cutbacks by state and local governments. Total government spending grew by 1.8% in

2009, 3.1% in 2008, and 1.7% in 2007.

Federal government spending increased at a rate of 1.4% this quarter. Federal government

spending remained unchanged in the previous quarter but grew 8.0% in the third quarter of

2009. Federal government spending grew by 5.2% in 2009, after growing 7.7% in 2008 and

1.3% in 2007.

BUSINESS INVESTMENT AND INVENTORIES

Business spending, also known as nonresidential fixed investment, grew at a rate of 4.1% in the

first quarter. This is the second straight quarter of growth. Business spending increased at a

rate of 5.3% in the fourth quarter of 2009, but decreased by 5.9% in the third. Business

spending declined by 17.8% in 2009, after growing 1.6% in 2008 and 6.2% in 2007.

Business spending on structures (nonresidential structures) continued to decrease this quarter,

dropping at an annual rate of 14.0%. This quarter’s drop marks seven consecutive quarterly

declines. Business spending on structures decreased at a rate of 18.0% in the previous quarter

and 18.4% in the third quarter of 2009. Business expenditures on equipment and software

increased at an annual rate of 13.4% in the first quarter—the third consecutive quarterly

increase.

Business investments in inventories rose this quarter. The change in real private inventories

added 1.57 percentage points to the first‐quarter change in real GDP, after adding 3.79

percentage points to the fourth‐quarter change in 2009. Private businesses increased

inventories $31.1 billion in the first quarter, following decreases of $19.7 billion in the fourth

quarter and $139.2 billion in the third.

CONSUMER PRICES AND INFLATION RATES

Inflationary pressures remained essentially flat in the first quarter. The Federal Open Market

Committee (FOMC) stated in their most recent release that they expect inflation to “remain

subdued for some time.”

According to the U.S. Department of Commerce, the price index for gross domestic purchases

increased 1.7% in the first quarter. The price index for gross domestic purchases measures

© Jay R. Hill, CPA, P.C. 12

prices paid by U.S. residents. In the fourth quarter, the index increased 2.0%. Excluding food

and energy prices, the price index for gross domestic purchases increased by 1.1% in the first

quarter, compared with an increase of 1.5% in the previous quarter.

The U.S. Department of Labor reported that the Consumer Price Index for All Urban Consumers

(CPI‐U) increased 0.1% (seasonally adjusted) in March. The index was unchanged in February

and increased 0.2% in January. Over the last 12 months, the index increased 2.3% before

seasonal adjustment. The index decreased 0.3% in 2009 after increasing 3.8% in 2008 and 2.9%

in 2007.

MANUFACTURING

The Federal Reserve published that industrial production rose 0.1% in March after rising 0.3% in

February. Industrial production is the total output of factories and mines in the U.S. During the

first quarter, total industrial production grew at an annual rate of 7.8%, compared with an

annual rate of 6.9% in the fourth. Industrial production dropped 4.7% in 2009, after declining

6.7% in 2008. Manufacturing grew at an annual rate of 6.6% in the first quarter, up from a rate

of 5.6% in the fourth. Manufacturing decreased 5.0% in 2009, after declining 8.7% in 2008.

Capacity utilization increased to 69.5% during the first quarter, up from 68.2% during the fourth

quarter. Capacity utilization is the percentage of production capacity manufacturers actually

use. Capacity utilization was at 66.8% for 2009, down from 75.1% in 2008 and 79.0% in 2007.

The U.S. Census Bureau reported that new orders for manufactured durable goods in March

decreased $2.2 billion (1.3%) to $176.7 billion. This decrease followed three consecutive

monthly increases, including a 1.1% February increase. Excluding transportation, new orders

increased 2.8% in March. Excluding defense, new orders decreased 1.2%. Transportation

equipment, down two consecutive months, had the largest decrease, $5.9 billion or 12.9% to

$40.2 billion. This was due to nondefense aircraft and parts which decreased $6.5 billion.

The Institute for Supply Management reported that its monthly Manufacturing Index was at

59.6 at the end of the first quarter. This is up from a 54.9 reading at the end of the fourth

quarter of 2009 and a 52.4 reading at the end of the third. Any reading above 50.0 suggests

growth, whereas a reading below 50.0 indicates contraction.

INTEREST RATES

The Federal Open Market Committee (FOMC or the “Committee”) met twice during the first

quarter of 2010, issuing two statements on their target for the federal funds rate. The federal

funds rate is the interest rate at which a commercial bank lends immediately available funds in

balances at the Federal Reserve to another commercial bank. At both meetings the FOMC

decided to keep the target for the federal funds rate unchanged at a range of 0% to 0.25%.

© Jay R. Hill, CPA, P.C. 13

During the first quarter of 2010, the Board of Governors of the Federal Reserve System

increased the discount rate to 0.75% from the previous rate of 0.5%. The move was intended

to encourage financial institutions to rely more on money markets rather than the central bank

for short‐term liquidity needs. The discount rate is the interest rate a commercial bank is

charged to borrow funds, typically for a short period, directly from a Federal Reserve Bank. The

board of directors of each Reserve Bank establishes the discount rate every 14 days, subject to

the approval of the Board of Governors.

UNEMPLOYMENT AND PERSONAL INCOME

The U.S. Department of Labor reported that unemployment averaged 9.7% during the first

quarter, down from 10.0% in the previous quarter. At the start of the recession in December

2007, the unemployment rate was 5.0%.

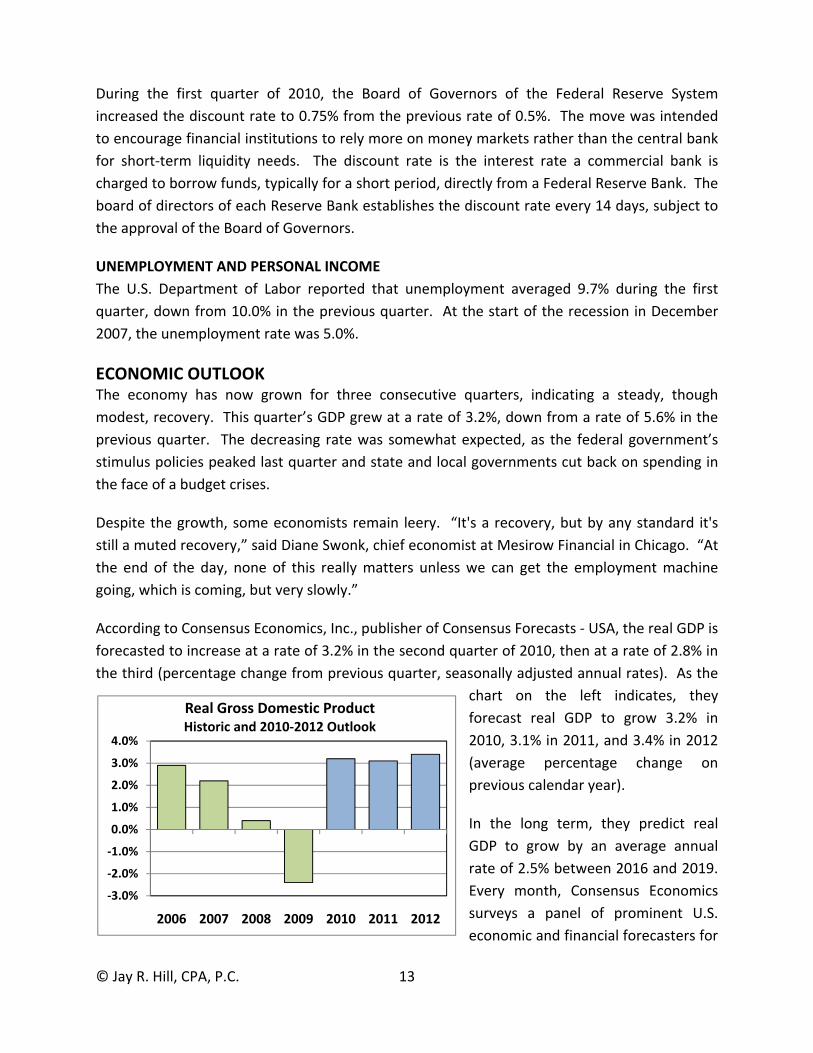

ECONOMIC OUTLOOK The economy has now grown for three consecutive quarters, indicating a steady, though

modest, recovery. This quarter’s GDP grew at a rate of 3.2%, down from a rate of 5.6% in the

previous quarter. The decreasing rate was somewhat expected, as the federal government’s

stimulus policies peaked last quarter and state and local governments cut back on spending in

the face of a budget crises.

Despite the growth, some economists remain leery. “It's a recovery, but by any standard it's

still a muted recovery,” said Diane Swonk, chief economist at Mesirow Financial in Chicago. “At

the end of the day, none of this really matters unless we can get the employment machine

going, which is coming, but very slowly.”

According to Consensus Economics, Inc., publisher of Consensus Forecasts ‐ USA, the real GDP is

forecasted to increase at a rate of 3.2% in the second quarter of 2010, then at a rate of 2.8% in

the third (percentage change from previous quarter, seasonally adjusted annual rates). As the

chart on the left indicates, they

forecast real GDP to grow 3.2% in

2010, 3.1% in 2011, and 3.4% in 2012

(average percentage change on

previous calendar year).

In the long term, they predict real

GDP to grow by an average annual

rate of 2.5% between 2016 and 2019.

Every month, Consensus Economics

surveys a panel of prominent U.S.

economic and financial forecasters for

‐3.0%

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2006 2007 2008 2009 2010 2011 2012

Real Gross Domestic ProductHistoric and 2010‐2012 Outlook

© Jay R. Hill, CPA, P.C. 14

their predictions on a range of variables including future growth, inflation, current account and

budget balances, and interest rates.

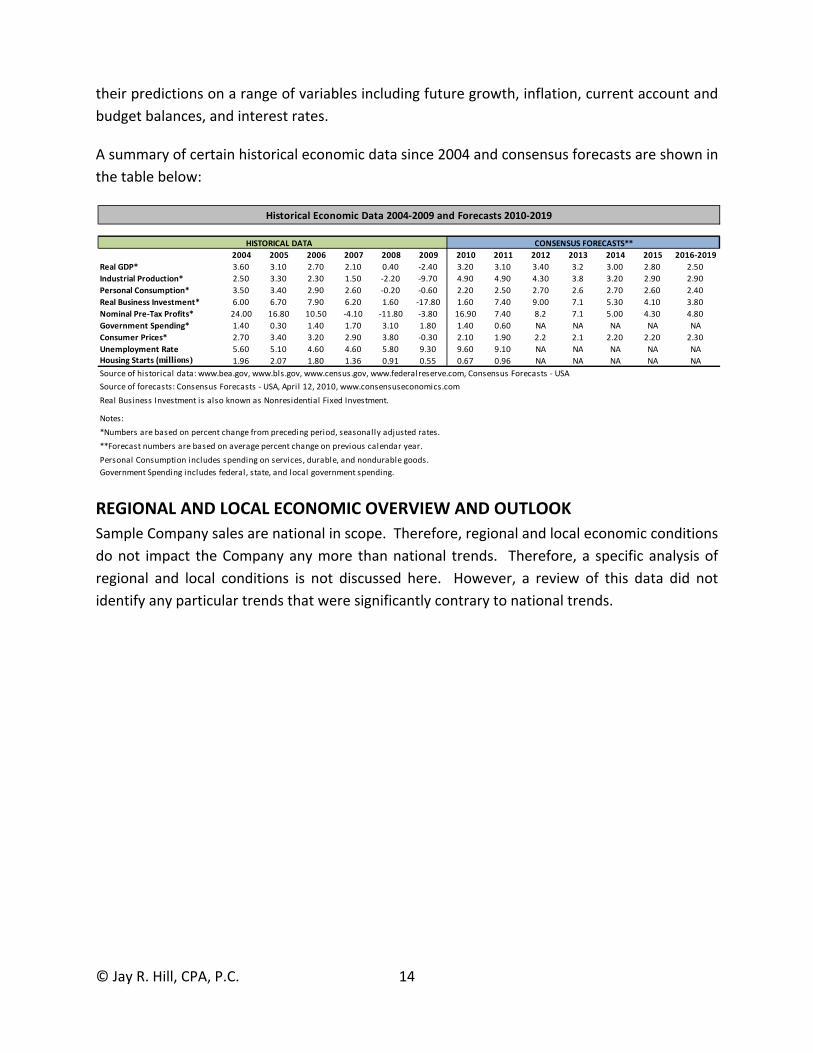

A summary of certain historical economic data since 2004 and consensus forecasts are shown in

the table below:

REGIONAL AND LOCAL ECONOMIC OVERVIEW AND OUTLOOK

Sample Company sales are national in scope. Therefore, regional and local economic conditions

do not impact the Company any more than national trends. Therefore, a specific analysis of

regional and local conditions is not discussed here. However, a review of this data did not

identify any particular trends that were significantly contrary to national trends.

Historical Economic Data 2004‐2009 and Forecasts 2010‐2019

HISTORICAL DATA CONSENSUS FORECASTS**

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016‐2019

Real GDP* 3.60 3.10 2.70 2.10 0.40 ‐2.40 3.20 3.10 3.40 3.2 3.00 2.80 2.50

Industrial Production* 2.50 3.30 2.30 1.50 ‐2.20 ‐9.70 4.90 4.90 4.30 3.8 3.20 2.90 2.90

Personal Consumption* 3.50 3.40 2.90 2.60 ‐0.20 ‐0.60 2.20 2.50 2.70 2.6 2.70 2.60 2.40

Real Business Investment* 6.00 6.70 7.90 6.20 1.60 ‐17.80 1.60 7.40 9.00 7.1 5.30 4.10 3.80

Nominal Pre‐Tax Profits* 24.00 16.80 10.50 ‐4.10 ‐11.80 ‐3.80 16.90 7.40 8.2 7.1 5.00 4.30 4.80

Government Spending* 1.40 0.30 1.40 1.70 3.10 1.80 1.40 0.60 NA NA NA NA NA

Consumer Prices* 2.70 3.40 3.20 2.90 3.80 ‐0.30 2.10 1.90 2.2 2.1 2.20 2.20 2.30

Unemployment Rate 5.60 5.10 4.60 4.60 5.80 9.30 9.60 9.10 NA NA NA NA NAHousing Starts (millions) 1.96 2.07 1.80 1.36 0.91 0.55 0.67 0.96 NA NA NA NA NA

Source of historical data: www.bea.gov, www.bls.gov, www.census.gov, www.federalreserve.com, Consensus Forecasts ‐ USA

Source of forecasts: Consensus Forecasts ‐ USA, April 12, 2010, www.consensuseconomics.com

Real Business Investment is also known as Nonresidential Fixed Investment.

Notes:

*Numbers are based on percent change from preceding period, seasonally adjusted rates.

**Forecast numbers are based on average percent change on previous calendar year.

Personal Consumption includes spending on services, durable, and nondurable goods.

Government Spending includes federal, state, and local government spending.

© Jay R. Hill, CPA, P.C. 15

INDUSTRY OVERVIEW AND OUTLOOK – AEROSPACE AND DEFENSE3

Sample Company is a manufacturer that serves the aerospace and defense industry throughout

the United States. A description of this industry and its outlook is below.

CURRENT PERFORMANCE

The aircraft, engine and parts manufacturing industry comprise both civil and military

segments. The commercial segment is sensitive to downstream demand for scheduled and

non‐scheduled air transport globally. When the financial situation is tight, people tend to

reduce spending on discretionary items, such as air travel, and substitute for other cheaper

modes of transport. Falling disposable income also undermines holiday travel as people are

more likely to stay home. In the military division, the industry is sensitive to federal funding on

defense, technology advancement in aerospace products, political developments, procurement

policies and the threat to homeland security/national security. When there is an increase in

funds allocated towards the budget for defense, there is a strong likelihood that demand for

military aerospace products will increase. When the US Government increased its defense

budget in 2002 due to the Iraq and Afghanistan war, it led to increased spending on military

equipment. Demand for US aircraft, engines and parts is also partially dependent on the value

of the US dollar; US products are more competitive globally when the dollar is weak.

AIRCRAFT ORDERS

The industry has shown an increase in both orders and deliveries since 2005, which is being

driven by improving technology and growth in smaller markets such as regional jets and very

light jets. Interestingly, there has been a divergence in recent times from the oil prices and the

level of aircraft orders and manufacturing, where traditionally higher oil prices and lower airline

profitability has reduced demand for new aircraft. Instead, demand for new aircraft has been

pushed upwards by improving technology, which has created an operating climate such that

the demand for new and more fuel efficient aircraft is, at present, positively related to

increases in the price of oil and jet fuel.

The new generation of technology is being enhanced by advances in construction techniques,

engine efficiencies, and lightweight construction materials. Airlines are now choosing to

upgrade their fleets instead of running older aircraft, as the cost benefit of purchasing new

planes now outweighs the cost of running the older aircraft with 20 year old technology.

However, during 2009, the industry has experienced a drop in orders and numerous

cancellations, blamed on poor economic conditions. At the same time, the delay in the

production of the 787 Dreamliner has reduced confidence in buyers. Orders are expected to

increase during 2010 due to a recovery in confidence.

3 Most of the parts of the industry overview and outlook section are quoted from IBISWorld Industry Market Research Reports – Tanning Salons in the US, reprinted with permission

© Jay R. Hill, CPA, P.C. 16

SMALL JETS FLYING HIGH

The last five years have seen strong growth in the small and light aircraft segment. Business

jets have increased in popularity with the growth in fractional ownership operations such as

those operated by NetJets. Fractional ownership has allowed businesses to gain access to very

light jets (VLJ) at a fraction of the cost of the aircraft by sharing the ownership of the aircraft

among many different entities. This trend has come about due to increasingly crowded airports

and the higher occurrence of delays to flights across the country. Companies such as Textron

Inc's Cessna have benefited greatly from the popularity of VLJs; their phenomenal increase in

backlog was mentioned earlier.

The growth in smaller aircraft manufacturing is expected to continue, although is under threat

by the current economic conditions and tightening of larger company's budgets. The benefits

of flying on smaller aircraft remain valid despite the current business climate, however, there

will be a drop in demand from those whose decision to adopt the VLJs was marginal to begin

with.

REVENUE IS TURBULENT

Aircraft, engine and parts manufacturing industry revenue is expected to increase at an

annualized rate of 1.1% during the five years to 2010, to $130.11 billion. Revenue per

establishment grew from $88.3 billion in 2005 to $93.2 billion in 2009, and will drop slightly to

$93 billion in 2010. This indicates that the rise in sales has been faster compared with the

increase in industry participation; industry participation has fallen due to tough operating

conditions since 2008.

INDUSTRY OUTLOOK – AEROSPACE AND DEFENSE

During the 2010 to 2015 period, industry revenue is expected to rise from $130.11 billion at

end of 2010 to $166.3 billion. This represents an annualized increase in revenue of 5.0%.

Revenue is predicted based on: an increase in air passenger traffic; increased demand resulting

from technology advances; weak US dollar and growing demand for exports; reasonable growth

in US defense budget; and the introduction of unmanned combat aerial vehicles as strike

aircraft.

The Federal Aviation Administration (FAA) stated in a 2004 report forecast that by 2015, US

commercial air carriers will transport nearly 1.1 billion passengers (up 4.3% annually) just over

1.1 trillion passenger miles (up 4.8% annually). Growth in traffic is expected to continue

especially on North Atlantic routes and in the near future Trans‐Pacific routes as airlines fight

for direct flights into China. The industry is also reliant on export sales especially in the LCA

oligopoly market which is dominated by Boeing and Airbus. Exports are likely to increase over

© Jay R. Hill, CPA, P.C. 17

the next five years, especially among developing nations that are constantly improving their air

transport infrastructure to cater to increasing air travel demand due to higher wealth.

IBISWorld believes that oil prices will range between $90 and $115 over the next five years.

The price of jet fuel is linked directly with crude oil but is more volatile as the cost of refining is

higher. While the oil price is expected to stabilize somewhat, it will remain very high over the

next five years and will add pressure to airframe and engine manufacturers for more fuel

efficient products and cause airlines to acquire larger capacity aircraft with lower fuel burn per

seat. In addition, high fuel prices will have an impact on the aircraft retirement cycle retiring

less fuel efficient types out of the market at a faster rate.

As mentioned earlier, advances in technology have increased the advantage of new aircraft

over existing aircraft to the extent that airlines are undertaking significant fleet renewal

programs. IBISWorld estimates that the fleet renewal process will continue to occur

throughout the five years to 2015, and will be a strong source of growth throughout the

industry. Worldwide GDP growth will ensure growth markets in the Asia Pacific region will

continue to aggressively expand their fleet sizes.

The Trade Weighted Index is estimated to increase at a marginal annualized rate of 0.3% over

the five years to 2015. This mean that the dollar will remain low based on a historical average,

creating a competitive advantage for US manufacturers. While some industry products such as

aircraft are less price competitive, others such as engine parts, parts and auxiliary equipment

are sold in very competitive global conditions. In addition, exports are expected to increase

significantly when Boeing's 787 "Dreamliner" is introduced to the market.

IBISWorld estimates that the US Department of Defense budget will grow at a reasonable pace

over the outlook period. Public expenditure on defense is projected to increase at 2.2% per

annum. IBISWorld believes that the majority will be attributed to systems, communications

equipment and unmanned aerial vehicles in preparation for the Future Combat System (FCS)

project (prototypes were fielded in 2008 with full scale production by 2010). US army spending

is expected to have peaked in 2008 and will decline until 2011 due to decreased supplemental

spending. Supplemental spending is in place primarily to pay for continuing military operations

in Iraq and Afghanistan.

The next wave of aircraft will be unmanned combat aerial aircraft (UAV) headed by the US army

FCS project. The US army's request for UAV procurement is expected to total $15,354.8 million

between financial years 2005 to 2011. UAV's aircraft will be used for dull, dirty and dangerous

missions although manned aircraft will still fly these missions. Helicopter sales are expected to

stabilize after consecutive years of strong growth as demand will be determined by operations

rather than war. In addition, the Federal Government in its 2007 budget has cleared funding

© Jay R. Hill, CPA, P.C. 18

for the acquisition of 183 F‐22 fighters which can extend the production line of this model until

2012.

IBISWorld forecast that profitability will increase over the five years to 2015, buoyed by new

aircraft models such as the 787 Dreamliner. The regional aircraft market is also expected to

release new designs and models in the outlook period further contributing to profitability

growth. As new aircraft come to market, they will be able to command higher margins and this

will lead to an increase in profits. Net year orders for Boeing aircraft increased from 277 in

2004 to 1028 in 2005, and 1423 in 2007. This will translate to higher revenue and profit in the

future.

Profit is likely to decrease slightly in the military sector as increasing program collaboration

between allied nations to split the risk associated with new developments (e.g. F35 ‐ Lightning

Strike II ‐ Joint Strike Fighter) will mean lower margins for companies when the manufacturing

of such products take place. The mounting US budget deficit may also reduce the potential

margins expected by prime contractors. Finally, wages as a proportion to revenue are expected

to decrease over the next five years as companies transfer operations to countries with low

labor rates to reduce operating cost and utilize greater technology to improve efficiency.

IBISWorld estimates that the number of new establishments will not change over the next five

years. During the economic recovery period, demand for aircraft, engines and parts is expected

to grow at a solid rate, encoring new entrants in the more competitive part of the market (parts

manufacturing). However, major industry players will begin to acquire smaller operators to

expand market share or force them out of business with competitive prices. The industry is

declining and market share growth is hard to come by. Some major players will also expand to

states but they are more likely to expand to developing countries in order to increase

production capacity and to lower production cost. It is anticipated that over the next five to 10

years, approximately two‐thirds of the commercial aerospace market is forecast to be outside

the United States.

Employment numbers are likely to contract over the five years to 2015, falling at 0.3% per

annum. Wage costs will be up by 0.1% on yearly basis. While labor productivity is set to

continue to grow in light of newer technology, in the coming years, the industry may face a

shortage of skilled labor as demand for workers outstrips supply. This will cause an increase in

training costs needed to bring less‐skilled workers up to the requisite level to manufacture

increasingly complex engines and avionics systems. Wages will increase to reflect supply

shortages, with the average wage set to boost from $70,398 in 2010 to $71,970 in 2015.

© Jay R. Hill, CPA, P.C. 19

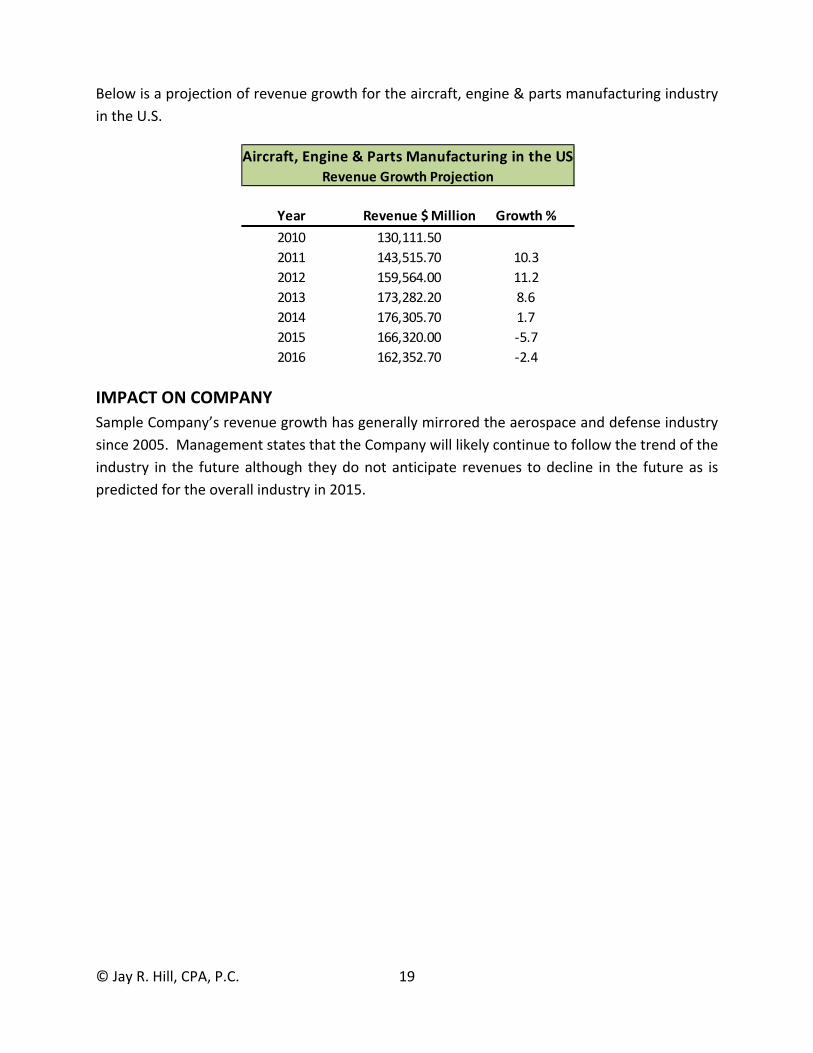

Below is a projection of revenue growth for the aircraft, engine & parts manufacturing industry

in the U.S.

IMPACT ON COMPANY

Sample Company’s revenue growth has generally mirrored the aerospace and defense industry

since 2005. Management states that the Company will likely continue to follow the trend of the

industry in the future although they do not anticipate revenues to decline in the future as is

predicted for the overall industry in 2015.

Aircraft, Engine & Parts Manufacturing in the US

Revenue Growth Projection

Year Revenue $ Million Growth %

2010 130,111.50

2011 143,515.70 10.3

2012 159,564.00 11.2

2013 173,282.20 8.6

2014 176,305.70 1.7

2015 166,320.00 ‐5.7

2016 162,352.70 ‐2.4

© Jay R. Hill, CPA, P.C. 20

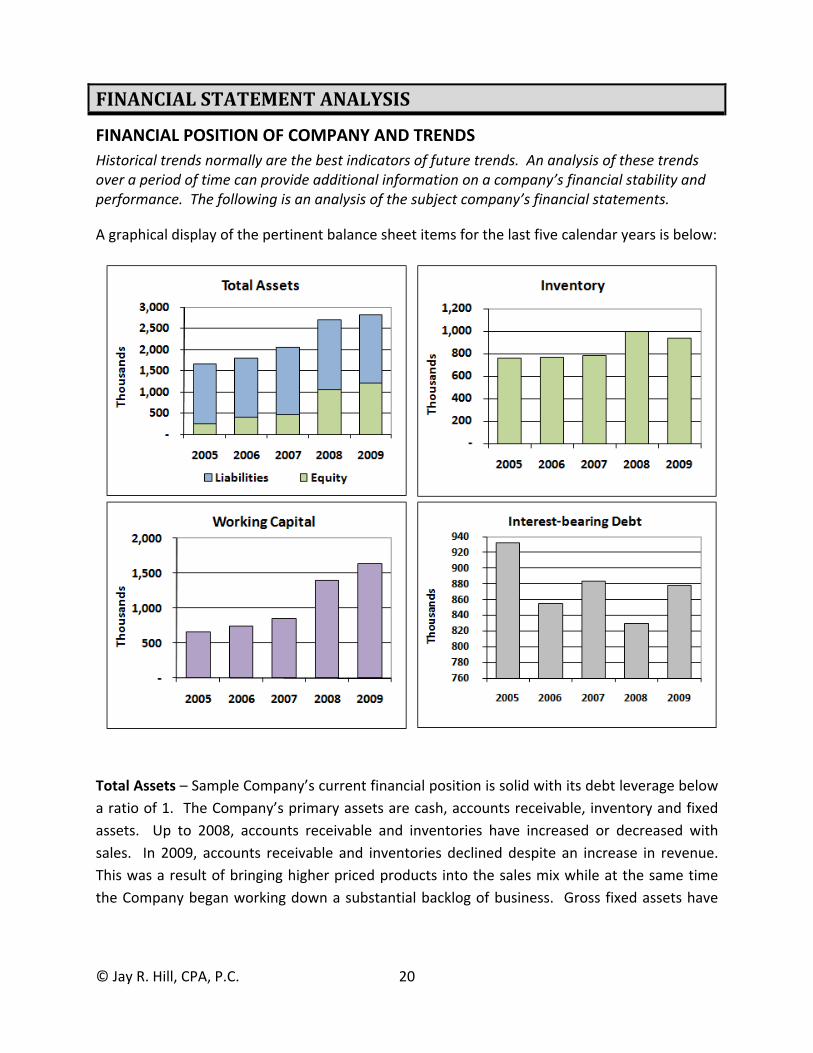

FINANCIAL STATEMENT ANALYSIS

FINANCIAL POSITION OF COMPANY AND TRENDS

Historical trends normally are the best indicators of future trends. An analysis of these trends over a period of time can provide additional information on a company’s financial stability and performance. The following is an analysis of the subject company’s financial statements.

A graphical display of the pertinent balance sheet items for the last five calendar years is below:

Total Assets – Sample Company’s current financial position is solid with its debt leverage below

a ratio of 1. The Company’s primary assets are cash, accounts receivable, inventory and fixed

assets. Up to 2008, accounts receivable and inventories have increased or decreased with

sales. In 2009, accounts receivable and inventories declined despite an increase in revenue.

This was a result of bringing higher priced products into the sales mix while at the same time

the Company began working down a substantial backlog of business. Gross fixed assets have

© Jay R. Hill, CPA, P.C. 21

increased as revenue has increased but net fixed assets have remained flat as a result of

accelerated depreciation.4

Inventory – Inventory is the Company’s largest net asset category and was $939,047 at the end

of 2009. Inventory decreased in 2009 despite a decrease in revenue as the Company reduced

purchases because of the uncertainty of future orders in 2010 and 2011. Inventory turnover

remained relatively stable at about 5.7 times per year. The Company’s raw inventory of steel

and other metal products have a long shelf life that lessens the risk associated with a slower

turnover rate versus other manufacturing industries.

Working Capital – At the end of 2009, Sample Company’s working capital was a comfortable

$1.6 million. Management does not expect significant increases in working capital to support

future revenue growth.

Interest‐Bearing Debt – The Company’s long‐term debt financing increased only slightly in

2009. Management anticipates maintaining its current debt level in the foreseeable future.

Overall, the risk level is low to moderate in connection with Sample Company’s financial

position. A detailed balance sheet history is at the end of this section following the ratio

analysis.

OPERATING RESULTS AND TRENDS

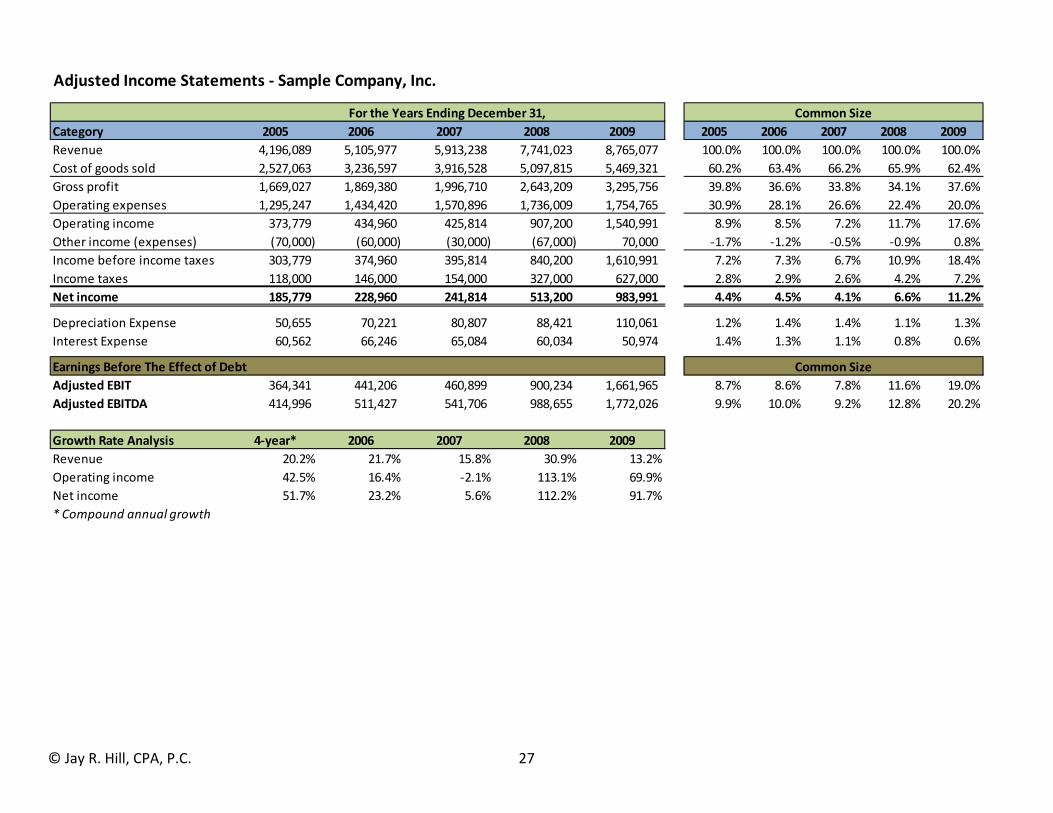

Adjustments to Historical Earnings

In evaluating the Company’s earnings capacity, we chose to make adjustments to the last five

years of historical operating results for trend analysis and valuation purposes as follows:

1. Sec. 179 depreciation – In each of the last five years, the Company has elected to take

accelerated Sec. 179 depreciation expense. This accelerated expense does not reflect the

economic reality of the equipment put in service. The accelerated depreciation is

recalculated on a 5 year MACRS basis.

A summary of the adjustments to the historical income statements is shown below:

4 See the section entitled “Operating Trends and Results” for a description of the adjustment for this acceleration.

Adjustments 2005 2006 2007 2008 2009

Operating expenses:

Sec 179 Depr adjustment (1) (53,926) (37,959) (32,145) (28,568) (57,910)

Total operating expenses (53,926) (37,959) (32,145) (28,568) (57,910)

© Jay R. Hill, CPA, P.C. 22

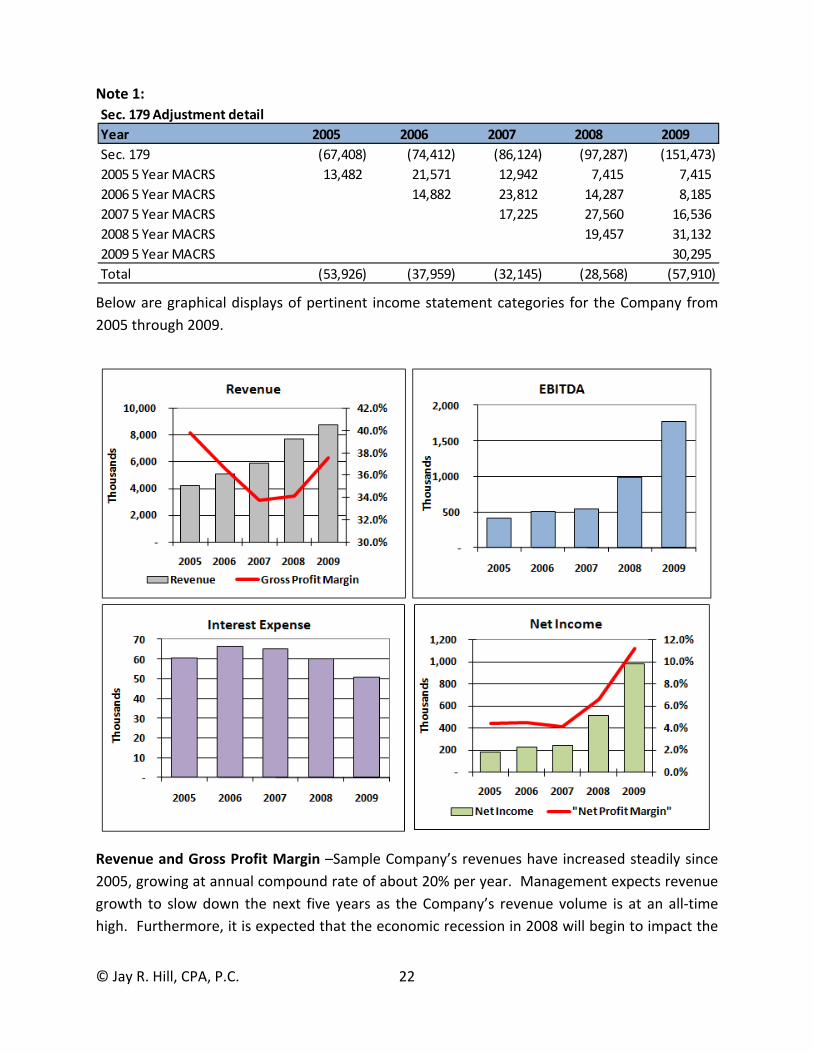

Note 1:

Below are graphical displays of pertinent income statement categories for the Company from

2005 through 2009.

Revenue and Gross Profit Margin –Sample Company’s revenues have increased steadily since

2005, growing at annual compound rate of about 20% per year. Management expects revenue

growth to slow down the next five years as the Company’s revenue volume is at an all‐time

high. Furthermore, it is expected that the economic recession in 2008 will begin to impact the

Sec. 179 Adjustment detail

Year 2005 2006 2007 2008 2009

Sec. 179 (67,408) (74,412) (86,124) (97,287) (151,473)

2005 5 Year MACRS 13,482 21,571 12,942 7,415 7,415

2006 5 Year MACRS 14,882 23,812 14,287 8,185

2007 5 Year MACRS 17,225 27,560 16,536

2008 5 Year MACRS 19,457 31,132

2009 5 Year MACRS 30,295

Total (53,926) (37,959) (32,145) (28,568) (57,910)

© Jay R. Hill, CPA, P.C. 23

aerospace industry, which has traditionally lagged behind the general economy in terms of

business cycles. The Company’s gross profit margin improved in 2009 as the Company’s

product mix included higher margin products.

Interest Expense – Interest expense is decreasing as interest rates have dropped. Interest

expense should remain relatively level as management anticipates its debt levels to remain

static along with rates.

EBITDA and Net Income – EBITDA (Earnings before interest expense, income taxes,

depreciation and amortization) and net income have increased along with revenues. Net profit

margins have also improved like gross profit margins. However, management is anticipating

profit margins to stabilize in 2010 as it does not anticipate its product mix to change

significantly from 2009.

Overall, the positive revenue and profit performance results in a low risk assessment of this

investment. Detailed historical balance sheets and income statements are shown at the end of

this section.

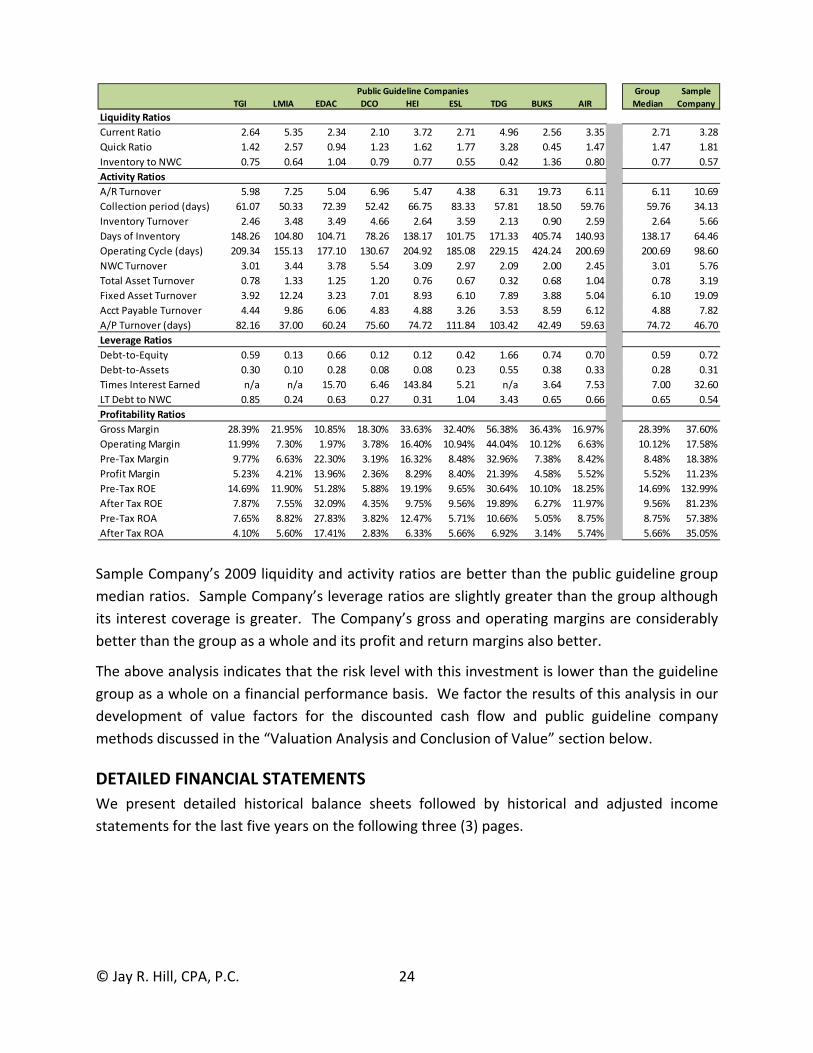

RATIO ANALYSIS

A ratio analysis of a company can lend further insight to the financial health of the company

and identify trends. Below is a ratio analysis of Sample Company in comparison to the group of

public companies that we are using as a benchmark to develop value factors applicable to the

subject company in the Public Guideline Company method.

© Jay R. Hill, CPA, P.C. 24

Sample Company’s 2009 liquidity and activity ratios are better than the public guideline group

median ratios. Sample Company’s leverage ratios are slightly greater than the group although

its interest coverage is greater. The Company’s gross and operating margins are considerably

better than the group as a whole and its profit and return margins also better.

The above analysis indicates that the risk level with this investment is lower than the guideline

group as a whole on a financial performance basis. We factor the results of this analysis in our

development of value factors for the discounted cash flow and public guideline company

methods discussed in the “Valuation Analysis and Conclusion of Value” section below.

DETAILED FINANCIAL STATEMENTS

We present detailed historical balance sheets followed by historical and adjusted income

statements for the last five years on the following three (3) pages.

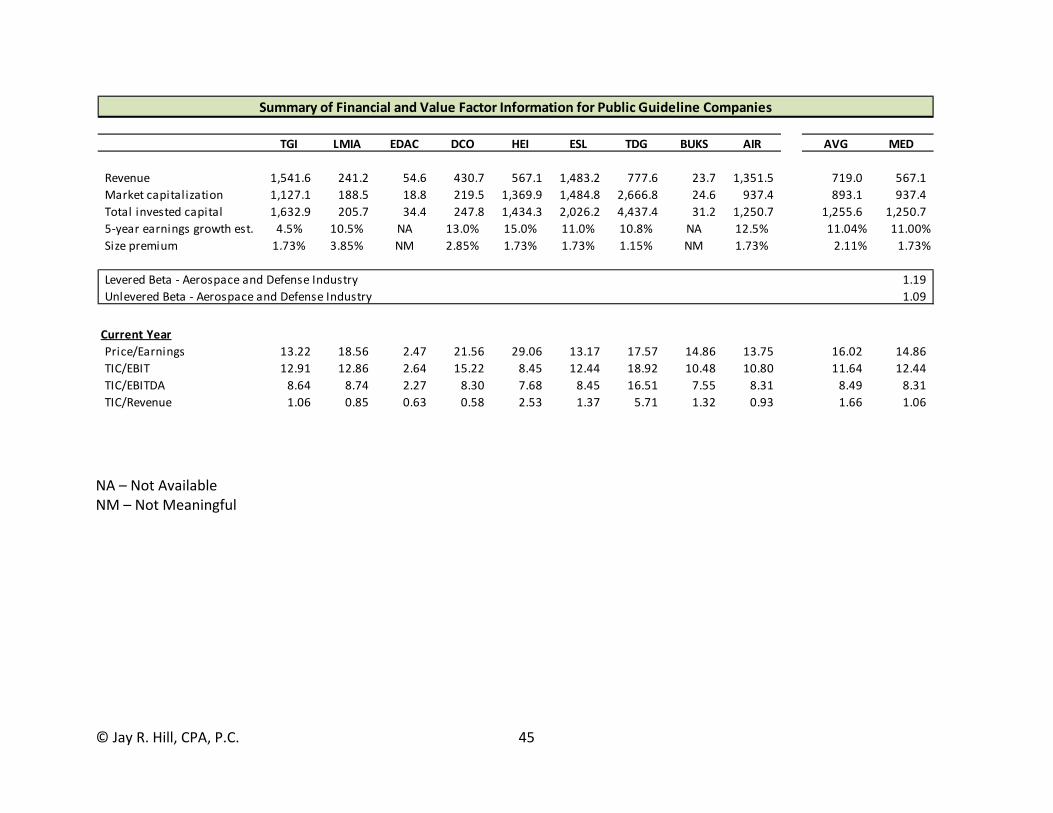

Public Guideline Companies Group Sample

TGI LMIA EDAC DCO HEI ESL TDG BUKS AIR Median Company

Liquidity Ratios

Current Ratio 2.64 5.35 2.34 2.10 3.72 2.71 4.96 2.56 3.35 2.71 3.28

Quick Ratio 1.42 2.57 0.94 1.23 1.62 1.77 3.28 0.45 1.47 1.47 1.81

Inventory to NWC 0.75 0.64 1.04 0.79 0.77 0.55 0.42 1.36 0.80 0.77 0.57

Activity Ratios

A/R Turnover 5.98 7.25 5.04 6.96 5.47 4.38 6.31 19.73 6.11 6.11 10.69

Collection period (days) 61.07 50.33 72.39 52.42 66.75 83.33 57.81 18.50 59.76 59.76 34.13

Inventory Turnover 2.46 3.48 3.49 4.66 2.64 3.59 2.13 0.90 2.59 2.64 5.66

Days of Inventory 148.26 104.80 104.71 78.26 138.17 101.75 171.33 405.74 140.93 138.17 64.46

Operating Cycle (days) 209.34 155.13 177.10 130.67 204.92 185.08 229.15 424.24 200.69 200.69 98.60

NWC Turnover 3.01 3.44 3.78 5.54 3.09 2.97 2.09 2.00 2.45 3.01 5.76

Total Asset Turnover 0.78 1.33 1.25 1.20 0.76 0.67 0.32 0.68 1.04 0.78 3.19

Fixed Asset Turnover 3.92 12.24 3.23 7.01 8.93 6.10 7.89 3.88 5.04 6.10 19.09

Acct Payable Turnover 4.44 9.86 6.06 4.83 4.88 3.26 3.53 8.59 6.12 4.88 7.82

A/P Turnover (days) 82.16 37.00 60.24 75.60 74.72 111.84 103.42 42.49 59.63 74.72 46.70

Leverage Ratios

Debt‐to‐Equity 0.59 0.13 0.66 0.12 0.12 0.42 1.66 0.74 0.70 0.59 0.72

Debt‐to‐Assets 0.30 0.10 0.28 0.08 0.08 0.23 0.55 0.38 0.33 0.28 0.31

Times Interest Earned n/a n/a 15.70 6.46 143.84 5.21 n/a 3.64 7.53 7.00 32.60

LT Debt to NWC 0.85 0.24 0.63 0.27 0.31 1.04 3.43 0.65 0.66 0.65 0.54

Profitability Ratios

Gross Margin 28.39% 21.95% 10.85% 18.30% 33.63% 32.40% 56.38% 36.43% 16.97% 28.39% 37.60%

Operating Margin 11.99% 7.30% 1.97% 3.78% 16.40% 10.94% 44.04% 10.12% 6.63% 10.12% 17.58%

Pre‐Tax Margin 9.77% 6.63% 22.30% 3.19% 16.32% 8.48% 32.96% 7.38% 8.42% 8.48% 18.38%

Profit Margin 5.23% 4.21% 13.96% 2.36% 8.29% 8.40% 21.39% 4.58% 5.52% 5.52% 11.23%

Pre‐Tax ROE 14.69% 11.90% 51.28% 5.88% 19.19% 9.65% 30.64% 10.10% 18.25% 14.69% 132.99%

After Tax ROE 7.87% 7.55% 32.09% 4.35% 9.75% 9.56% 19.89% 6.27% 11.97% 9.56% 81.23%

Pre‐Tax ROA 7.65% 8.82% 27.83% 3.82% 12.47% 5.71% 10.66% 5.05% 8.75% 8.75% 57.38%

After Tax ROA 4.10% 5.60% 17.41% 2.83% 6.33% 5.66% 6.92% 3.14% 5.74% 5.66% 35.05%

© Jay R. Hill, CPA, P.C. 25

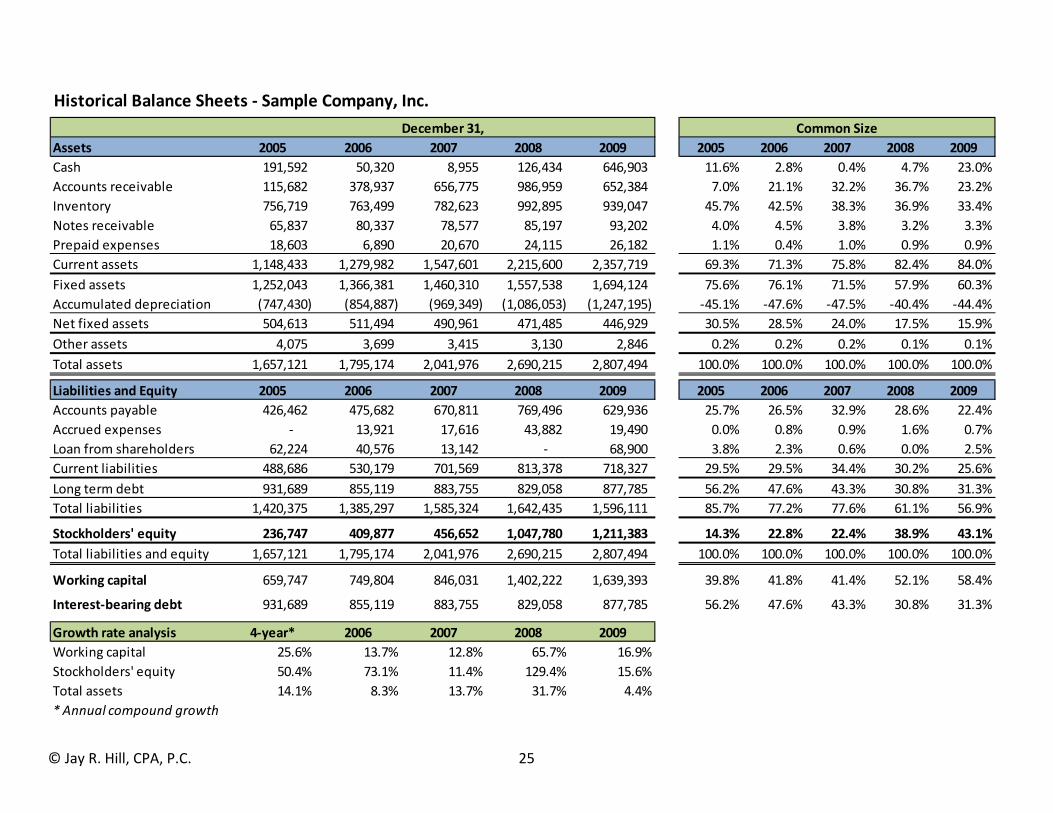

Historical Balance Sheets ‐ Sample Company, Inc.

December 31, Common Size

Assets 2005 2006 2007 2008 2009 2005 2006 2007 2008 2009

Cash 191,592 50,320 8,955 126,434 646,903 11.6% 2.8% 0.4% 4.7% 23.0%

Accounts receivable 115,682 378,937 656,775 986,959 652,384 7.0% 21.1% 32.2% 36.7% 23.2%

Inventory 756,719 763,499 782,623 992,895 939,047 45.7% 42.5% 38.3% 36.9% 33.4%

Notes receivable 65,837 80,337 78,577 85,197 93,202 4.0% 4.5% 3.8% 3.2% 3.3%

Prepaid expenses 18,603 6,890 20,670 24,115 26,182 1.1% 0.4% 1.0% 0.9% 0.9%

Current assets 1,148,433 1,279,982 1,547,601 2,215,600 2,357,719 69.3% 71.3% 75.8% 82.4% 84.0%

Fixed assets 1,252,043 1,366,381 1,460,310 1,557,538 1,694,124 75.6% 76.1% 71.5% 57.9% 60.3%

Accumulated depreciation (747,430) (854,887) (969,349) (1,086,053) (1,247,195) ‐45.1% ‐47.6% ‐47.5% ‐40.4% ‐44.4%

Net fixed assets 504,613 511,494 490,961 471,485 446,929 30.5% 28.5% 24.0% 17.5% 15.9%

Other assets 4,075 3,699 3,415 3,130 2,846 0.2% 0.2% 0.2% 0.1% 0.1%

Total assets 1,657,121 1,795,174 2,041,976 2,690,215 2,807,494 100.0% 100.0% 100.0% 100.0% 100.0%

Liabilities and Equity 2005 2006 2007 2008 2009 2005 2006 2007 2008 2009

Accounts payable 426,462 475,682 670,811 769,496 629,936 25.7% 26.5% 32.9% 28.6% 22.4%

Accrued expenses ‐ 13,921 17,616 43,882 19,490 0.0% 0.8% 0.9% 1.6% 0.7%

Loan from shareholders 62,224 40,576 13,142 ‐ 68,900 3.8% 2.3% 0.6% 0.0% 2.5%

Current liabilities 488,686 530,179 701,569 813,378 718,327 29.5% 29.5% 34.4% 30.2% 25.6%

Long term debt 931,689 855,119 883,755 829,058 877,785 56.2% 47.6% 43.3% 30.8% 31.3%

Total liabilities 1,420,375 1,385,297 1,585,324 1,642,435 1,596,111 85.7% 77.2% 77.6% 61.1% 56.9%

Stockholders' equity 236,747 409,877 456,652 1,047,780 1,211,383 14.3% 22.8% 22.4% 38.9% 43.1%

Total liabilities and equity 1,657,121 1,795,174 2,041,976 2,690,215 2,807,494 100.0% 100.0% 100.0% 100.0% 100.0%

Working capital 659,747 749,804 846,031 1,402,222 1,639,393 39.8% 41.8% 41.4% 52.1% 58.4%

Interest‐bearing debt 931,689 855,119 883,755 829,058 877,785 56.2% 47.6% 43.3% 30.8% 31.3%

Growth rate analysis 4‐year* 2006 2007 2008 2009

Working capital 25.6% 13.7% 12.8% 65.7% 16.9%

Stockholders' equity 50.4% 73.1% 11.4% 129.4% 15.6%

Total assets 14.1% 8.3% 13.7% 31.7% 4.4%

* Annual compound growth

© Jay R. Hill, CPA, P.C. 26

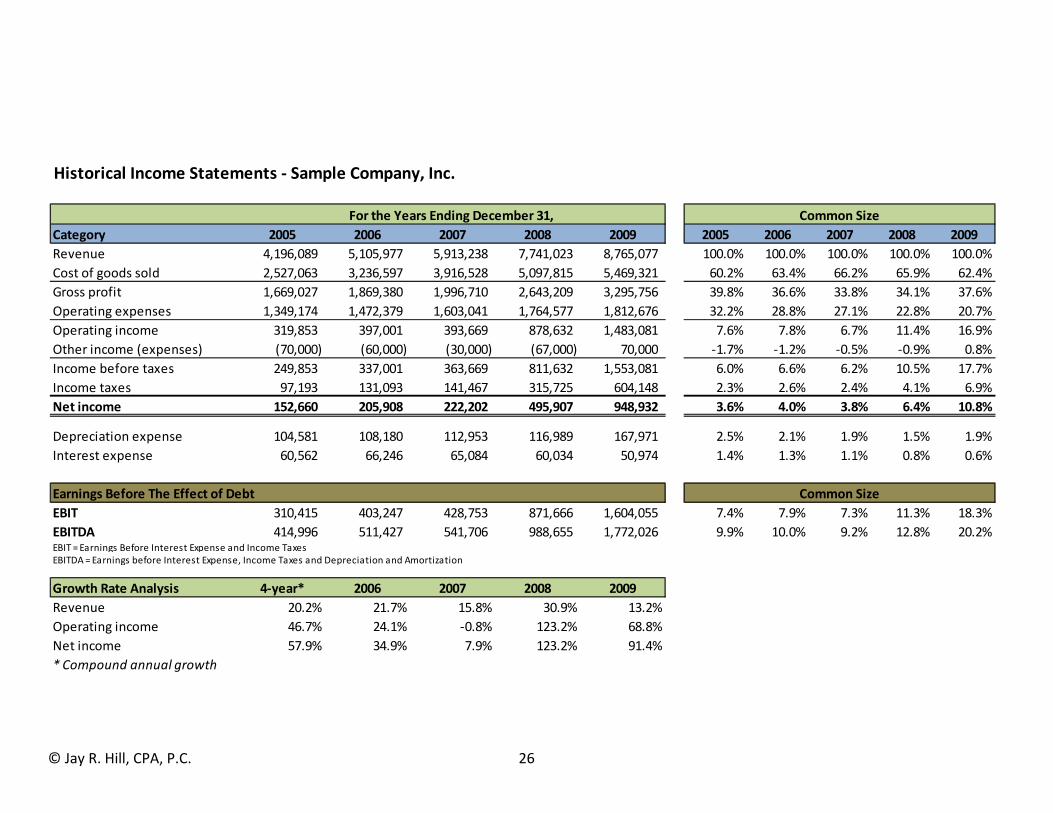

Historical Income Statements ‐ Sample Company, Inc.

For the Years Ending December 31, Common Size

Category 2005 2006 2007 2008 2009 2005 2006 2007 2008 2009

Revenue 4,196,089 5,105,977 5,913,238 7,741,023 8,765,077 100.0% 100.0% 100.0% 100.0% 100.0%

Cost of goods sold 2,527,063 3,236,597 3,916,528 5,097,815 5,469,321 60.2% 63.4% 66.2% 65.9% 62.4%

Gross profit 1,669,027 1,869,380 1,996,710 2,643,209 3,295,756 39.8% 36.6% 33.8% 34.1% 37.6%

Operating expenses 1,349,174 1,472,379 1,603,041 1,764,577 1,812,676 32.2% 28.8% 27.1% 22.8% 20.7%

Operating income 319,853 397,001 393,669 878,632 1,483,081 7.6% 7.8% 6.7% 11.4% 16.9%

Other income (expenses) (70,000) (60,000) (30,000) (67,000) 70,000 ‐1.7% ‐1.2% ‐0.5% ‐0.9% 0.8%

Income before taxes 249,853 337,001 363,669 811,632 1,553,081 6.0% 6.6% 6.2% 10.5% 17.7%

Income taxes 97,193 131,093 141,467 315,725 604,148 2.3% 2.6% 2.4% 4.1% 6.9%

Net income 152,660 205,908 222,202 495,907 948,932 3.6% 4.0% 3.8% 6.4% 10.8%

Depreciation expense 104,581 108,180 112,953 116,989 167,971 2.5% 2.1% 1.9% 1.5% 1.9%

Interest expense 60,562 66,246 65,084 60,034 50,974 1.4% 1.3% 1.1% 0.8% 0.6%

Earnings Before The Effect of Debt Common Size

EBIT 310,415 403,247 428,753 871,666 1,604,055 7.4% 7.9% 7.3% 11.3% 18.3%

EBITDA 414,996 511,427 541,706 988,655 1,772,026 9.9% 10.0% 9.2% 12.8% 20.2%EBIT = Earnings Before Interest Expense and Income TaxesEBITDA = Earnings before Interest Expense, Income Taxes and Depreciation and Amortization

Growth Rate Analysis 4‐year* 2006 2007 2008 2009

Revenue 20.2% 21.7% 15.8% 30.9% 13.2%

Operating income 46.7% 24.1% ‐0.8% 123.2% 68.8%

Net income 57.9% 34.9% 7.9% 123.2% 91.4%

* Compound annual growth

© Jay R. Hill, CPA, P.C. 27

Adjusted Income Statements ‐ Sample Company, Inc.

For the Years Ending December 31, Common Size

Category 2005 2006 2007 2008 2009 2005 2006 2007 2008 2009

Revenue 4,196,089 5,105,977 5,913,238 7,741,023 8,765,077 100.0% 100.0% 100.0% 100.0% 100.0%

Cost of goods sold 2,527,063 3,236,597 3,916,528 5,097,815 5,469,321 60.2% 63.4% 66.2% 65.9% 62.4%

Gross profit 1,669,027 1,869,380 1,996,710 2,643,209 3,295,756 39.8% 36.6% 33.8% 34.1% 37.6%

Operating expenses 1,295,247 1,434,420 1,570,896 1,736,009 1,754,765 30.9% 28.1% 26.6% 22.4% 20.0%

Operating income 373,779 434,960 425,814 907,200 1,540,991 8.9% 8.5% 7.2% 11.7% 17.6%

Other income (expenses) (70,000) (60,000) (30,000) (67,000) 70,000 ‐1.7% ‐1.2% ‐0.5% ‐0.9% 0.8%

Income before income taxes 303,779 374,960 395,814 840,200 1,610,991 7.2% 7.3% 6.7% 10.9% 18.4%

Income taxes 118,000 146,000 154,000 327,000 627,000 2.8% 2.9% 2.6% 4.2% 7.2%

Net income 185,779 228,960 241,814 513,200 983,991 4.4% 4.5% 4.1% 6.6% 11.2%

Depreciation Expense 50,655 70,221 80,807 88,421 110,061 1.2% 1.4% 1.4% 1.1% 1.3%

Interest Expense 60,562 66,246 65,084 60,034 50,974 1.4% 1.3% 1.1% 0.8% 0.6%

Earnings Before The Effect of Debt Common Size

Adjusted EBIT 364,341 441,206 460,899 900,234 1,661,965 8.7% 8.6% 7.8% 11.6% 19.0%

Adjusted EBITDA 414,996 511,427 541,706 988,655 1,772,026 9.9% 10.0% 9.2% 12.8% 20.2%

Growth Rate Analysis 4‐year* 2006 2007 2008 2009

Revenue 20.2% 21.7% 15.8% 30.9% 13.2%

Operating income 42.5% 16.4% ‐2.1% 113.1% 69.9%

Net income 51.7% 23.2% 5.6% 112.2% 91.7%

* Compound annual growth

© Jay R. Hill, CPA, P.C. 28

VALUATION ANALYSIS AND CONCLUSION OF VALUE

SUMMARY OF PERTINENT FACTORS

Sample Company is a manufacturer of aerospace fasteners, specifically hex head bolts and machine screws compliant with industry standards and certifications. The Company competes on a national basis with about 15 major competitors. Management depth is good and adequate to manage the Company’s growth in the future.

The general economy is slowly recovering from the greatest recession since the Great Depression. Although the overall economy experienced significant growth in the first quarter of 2010, most observers are cautious about the sustainability of the recovery. The general consensus is that more job creation is necessary to keep the economy on a growth pattern.

The aerospace and defense industry has enjoyed an increase in both orders and deliveries since 2005. This growth is being driven by improving technology and growth in smaller markets such as regional jets and very light jets. Defense spending has been driven by the expanding military budget as a result of the Iraq and Afghan wars. Despite the severe recession and the expected slow recovery, industry revenue is expected to rise from $130.11 billion at end of 2010 to $166.3 billion. This represents an annualized increase in revenue of 5.0%. However, growth is expected to be negative in 2015 from 2014 and again in 2016 as airlines finish turning over their fleets and military spending slows.

Sample Company’s financial position is solid with more than adequate working capital to support future revenue growth. The Company’s debt levels are expected to remain flat in the next five years.

The Company’s revenues have grown at a significant 20% annual growth rate since 2005. Profits have increased at a greater rate as profit margins increased as a result of the Company’s product mix shifting towards higher profit margin products. However, management is expecting revenue growth to slow in the next five years as a result of the increasing size of the Company and the aerospace and defense parts industry experiencing a decline in growth the next four and eventually negative growth in 2015 and 2016. Profit margins are expected to stabilize in 2010 and remain stable over the next four years.

VALUATION ANALYSIS

There are three traditional approaches to calculate the fair market value of a closely‐held business.

These approaches are the market, income and cost approaches. Below is a brief description of

these approaches.

Market Approach – This approach considers the prices from actual transactions of comparable investments, often with adjustments made to the derived price factors to reflect comparability differences with the subject investment.

Income Approach – This approach involves the estimation of the prospective economic benefits of ownership whereby the anticipated income stream from the subject investment is stated in current dollars by discounting the income stream by an appropriate rate of return.

© Jay R. Hill, CPA, P.C. 29

Cost Approach – This approach considers the investment necessary to reproduce or replace the subject investment adjusted for estimated depreciation and /or deterioration.

Normally, if the subject entity is an operating entity that sells a product or service, then the

most important factor to an investor is the subject entity’s earnings history and future earnings

stream. Conversely, if the subject entity is a holding entity that is holding assets for investment

purposes, then an investor’s interest is in the fair market value of the subject entity’s

underlying assets.

Sample Company is an operating company that sells products. Therefore, we use several

earnings methods under the income and market approaches to value the Company. A

summary of the methods we use to estimate the fair market value of a minority interest in

Sample Company are as follows:

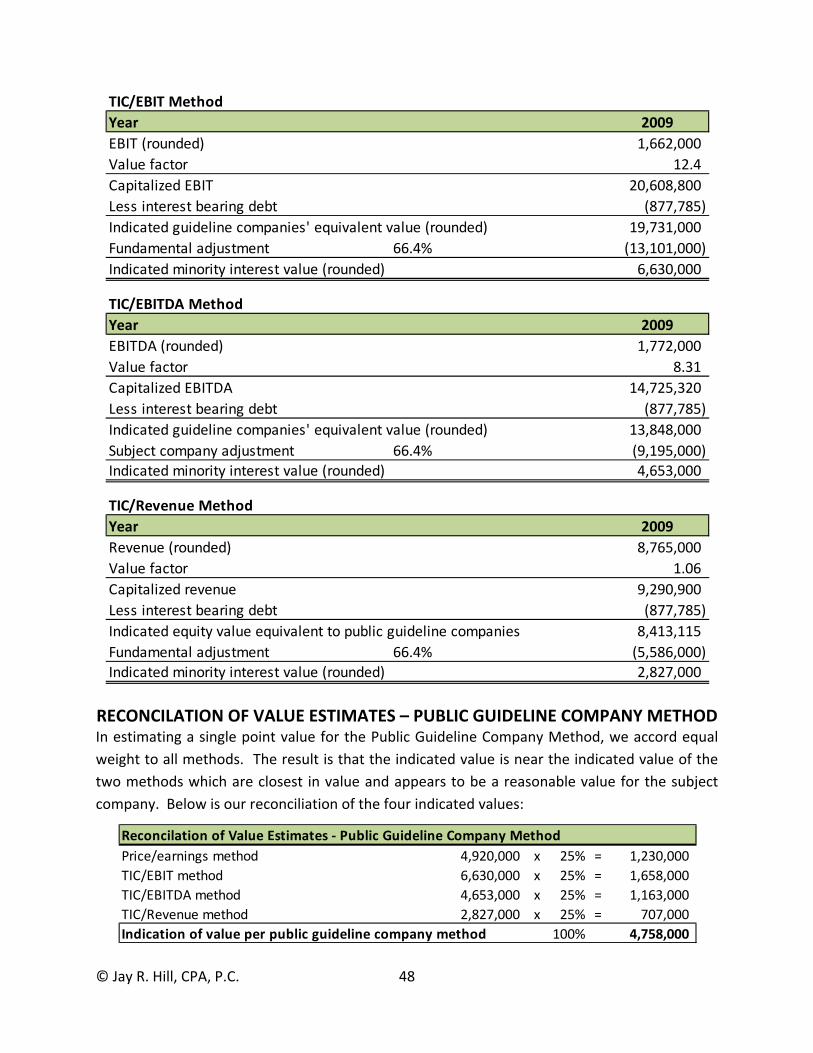

Discounted Cash Flow Method Public Guideline Company Methods

o Price/earnings method o TIC/EBIT method o TIC/EBITDA method o TIC/Revenue method

Below is a further description of these methods and the resulting value estimates we derive

from our use of these methods.

VALUATION METHODS CONSIDERED BUT NOT UTILIZED

Cost or Replacement Methods: These methods estimate the value of the underlying assets of the Company based on the fair market value cost or replacement value of the assets.

Reasons for not using these methods: These methods are normally performed for a controlling interest valuation because a minority interest normally cannot force the sale of the underlying assets. Furthermore, it is difficult to measure the intangible goodwill asset of an operating company with this method since earnings of the Company have a major impact on this asset.

The Capitalized Excess Earnings Method: This method is a hybrid of the capitalization of earnings method and the net asset value method. The method involves the estimate of the fair market value of the underlying assets and the estimation of the intangible or goodwill value of the earnings in excess of the required earnings on the underlying assets. The method was promulgated in Revenue Ruling 68‐609. However, the Internal Revenue Service also stated that the method should only be used if no other method is appropriate or applicable.

Reasons for not using this method: It is our opinion more appropriate methods are available to

value the subject company.

© Jay R. Hill, CPA, P.C. 30

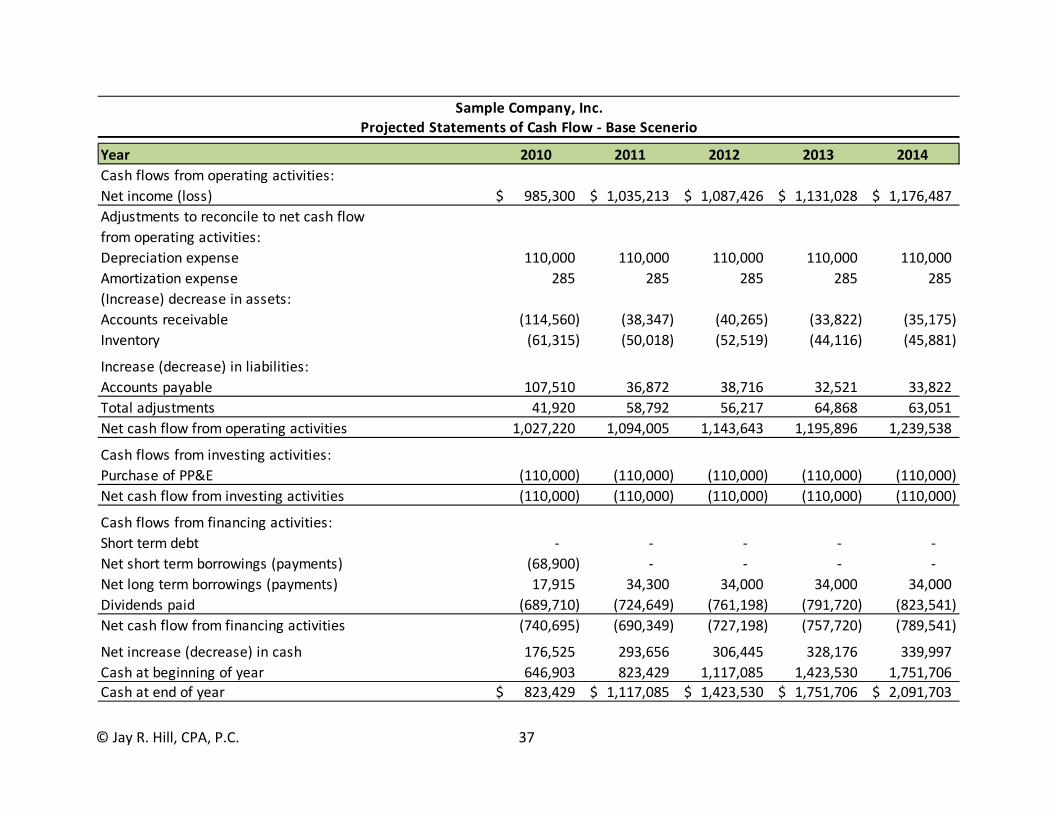

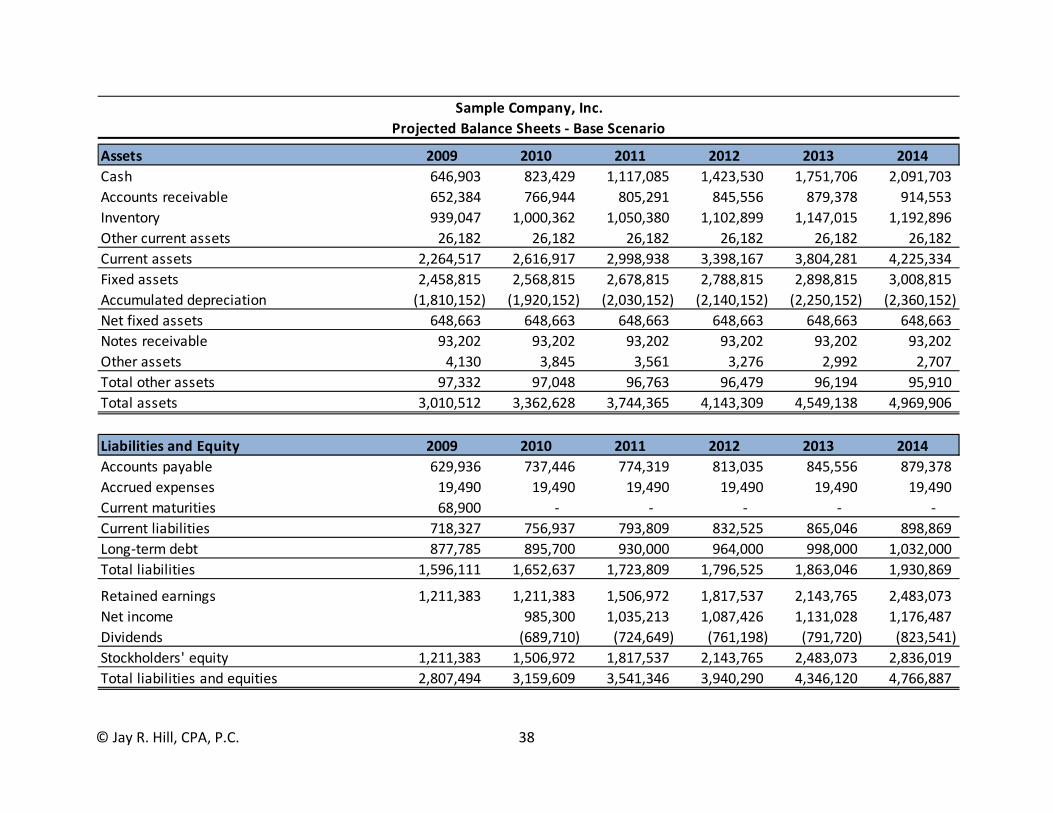

DISCOUNTED CASH FLOW METHOD

Frequently, a company’s historical operations provide a good indication of the future earnings

or growth rate of the business. In this instance, management is expecting sales volume and

earnings to be different from historical results. Therefore, an appropriate method to determine

the value of Sample Company is forecasting the cash flows of the Company and then

discounting these future cash flows to today’s dollars. The application of the discounted cash

flow (DCF) method requires the valuator to make several key decisions as follows:

1. The determination of the type of financial return to be forecast. 2. The determination if the selected return is one applicable to equity or invested

capital. 3. The number of years to be discretely forecast. 4. The selection of a discount rate appropriate to the type of return selected.

TYPE OF FINANCIAL RETURN TO BE FORECAST

In this instance, we select net cash flow because net cash flow is the return that may be

available to minority shareholders.

EQUITY OR INVESTED CAPITAL

We are valuing a minority equity interest so we assess the net cash flow available before

paying creditors, called invested capital, and then subtract the Company’s interest‐bearing

debt to determine an equity value for Sample Company.

NUMBER OF YEARS TO BE FORECAST

A discussion with management about the number of years it will take to stabilize revenue and

earnings growth reveals that a five‐year period of specific forecasting is appropriate.

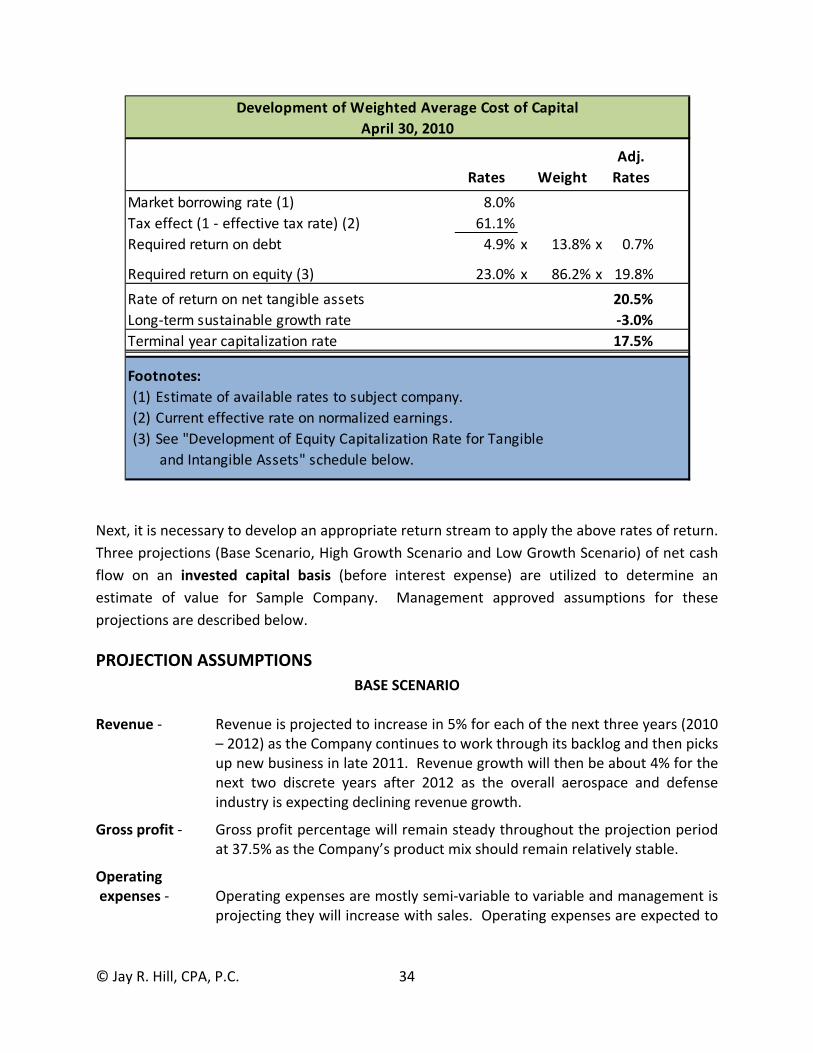

DEVELOPMENT OF DISCOUNT RATE – WEIGHTED AVERAGE COST OF CAPITAL

We estimate the appropriate present value discount rate for Central’s projected cash flows by

analyzing the Company’s weighted average cost of capital (WACC). The WACC combines the

present cost of the Sample’s debt capital and equity capital as determined from market‐derived

empirical evidence. The debt and equity costs, expressed as rates of return, are weighted

according to the capital structure of Sample Company as a minority shareholder can not

influence the capital structure of the Company.

DEBT RATE

We estimate the cost of Sample’s debt capital by reviewing the Company’s current debt

interest rates. The average rate is about 8%. Corporate interest expense is tax deductible,

therefore, we use the after‐tax cost of debt or 4.9% (.08 x [1 – 0.389]).

© Jay R. Hill, CPA, P.C. 31

EQUITY DISCOUNT RATE ‐ MODIFIED CAPM

We use the Modified Capital Asset Pricing Model (CAPM) to derive a rate of return or discount

rate to apply to the future net cash flow estimates of Sample Company’s operations. The CAPM

model is one of the primary aspects of the modern capital market theory. The model quantifies

the return an investor requires to invest in securities that bear the risk of failure to pay a return

on such investment or even a complete loss as opposed to the “guaranteed” or “risk‐free”

return on a U.S. treasury security. The additional return that an investor requires above the

risk‐free return is known as a “premium”. The pure CAPM model formula determines the

required return by summing the risk‐free rate and the additional return required by investors in

the market as a whole (known as systematic risk) adjusted for volatility of the price of the

particular security know as Beta as follows:

Required Return = rf + ß(rm ‐ rf)

Where: rf = risk‐free rate of return ß = Beta or volatility of the security rm = equity market return (rm ‐ rf) is referred to as the equity market risk premium

To value this closely‐held security, we modify the CAPM model to incorporate two other factors

as follows:

Size premium – Empirical studies indicate that investors require an additional return or premium purely based on the size of the underlying company of the subject stock. The smaller the company in terms of assets and revenues, the greater the required return.

Specific company or idiosyncratic risk – This is the additional return or reduction in return that an investor requires because of the specific company factors that separate the subject stock from the market and specific industry as a whole.

The Modified CAPM Model is as follows:

Required Return = rf + ß(rm ‐ rf) + rsize+/‐ Alpha

Where: rf = risk‐free rate of return ß = Beta or volatility of the security rm = equity market return rsize = additional return for smaller companies Alpha = specific company risk factors

We derive the applicable discount rate using the Modified CAPM Model for Sample Company

below:

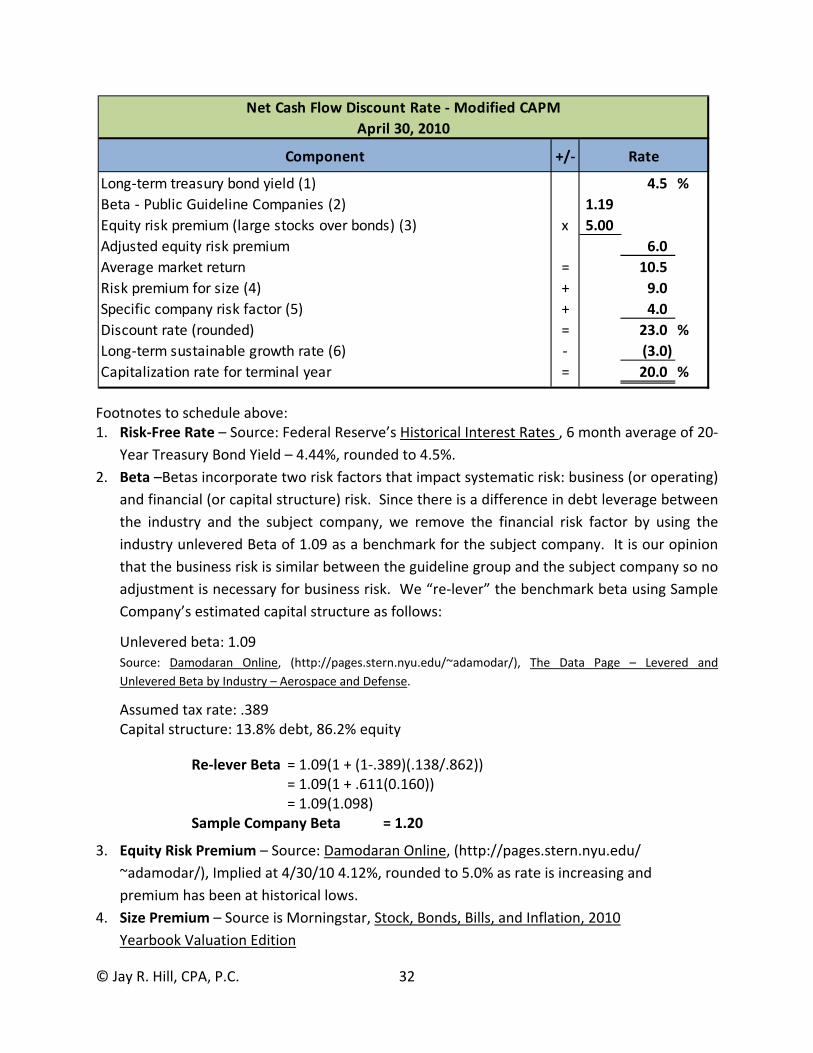

© Jay R. Hill, CPA, P.C. 32

Footnotes to schedule above: 1. Risk‐Free Rate – Source: Federal Reserve’s Historical Interest Rates , 6 month average of 20‐

Year Treasury Bond Yield – 4.44%, rounded to 4.5%.

2. Beta –Betas incorporate two risk factors that impact systematic risk: business (or operating)

and financial (or capital structure) risk. Since there is a difference in debt leverage between

the industry and the subject company, we remove the financial risk factor by using the

industry unlevered Beta of 1.09 as a benchmark for the subject company. It is our opinion

that the business risk is similar between the guideline group and the subject company so no

adjustment is necessary for business risk. We “re‐lever” the benchmark beta using Sample

Company’s estimated capital structure as follows:

Unlevered beta: 1.09 Source: Damodaran Online, (http://pages.stern.nyu.edu/~adamodar/), The Data Page – Levered and

Unlevered Beta by Industry – Aerospace and Defense.

Assumed tax rate: .389 Capital structure: 13.8% debt, 86.2% equity

Re‐lever Beta = 1.09(1 + (1‐.389)(.138/.862)) = 1.09(1 + .611(0.160)) = 1.09(1.098) Sample Company Beta = 1.20

3. Equity Risk Premium – Source: Damodaran Online, (http://pages.stern.nyu.edu/

~adamodar/), Implied at 4/30/10 4.12%, rounded to 5.0% as rate is increasing and

premium has been at historical lows.

4. Size Premium – Source is Morningstar, Stock, Bonds, Bills, and Inflation, 2010

Yearbook Valuation Edition

Net Cash Flow Discount Rate ‐ Modified CAPM

April 30, 2010

Component +/‐ Rate

Long‐term treasury bond yield (1) 4.5 %

Beta ‐ Public Guideline Companies (2) 1.19

Equity risk premium (large stocks over bonds) (3) x 5.00

Adjusted equity risk premium 6.0

Average market return = 10.5

Risk premium for size (4) + 9.0

Specific company risk factor (5) + 4.0

Discount rate (rounded) = 23.0 %

Long‐term sustainable growth rate (6) ‐ (3.0)

Capitalization rate for terminal year = 20.0 %

© Jay R. Hill, CPA, P.C. 33

Size Premium for the smallest public companies is as follows: 10th decile ‐ Smallest ‐ 6.28%, broken down further the premium is as follows: 10a ‐ Market Capitalization (millions) from $123.536 to $214.111 ‐ 4.45% 10b ‐ Market Capitalization (millions) from $1.007 to $123.516 ‐ 10.01% The smaller companies in the 10b decile are frequently reporting losses, which likely increases the premium. Sample Company is profitable but is a relatively small company in an industry niche. Therefore, a size premium a little lower than the 10b average or 9% is deemed appropriate for Sample Company which recognizes its profitability but small size.

5. Specific Company or Unsystematic Risk – Source is valuator's opinion based on the following risk factors:

a. Product innovation and diversity opportunities are limited. b. Relatively older management team.

6. Capitalization Rate for Terminal Year ‐ In addition to the discount rate to apply to the