VALUATING GREENHOUSE ENERGY CONSERVATION …

20

Hort culture Series o. 474 Dec_Imber 1979 VALUATING GREENHOUSE ENERGY CONSERVATION I"VESTMENTS USING DISCOUNTED CASH FLOW: AWORKSHEET David B. Perry and Jerry L. Robert on Department Qf Horticulture Oh 0 Agricultural Res rch and Development Center u.S. 250 nd Ohio 83 Sduth Wooster, Ohio

Transcript of VALUATING GREENHOUSE ENERGY CONSERVATION …

Hort culture Series o. 474 Dec_Imber 1979

VALUATING GREENHOUSE ENERGY CONSERVATION I"VESTMENTSUSING DISCOUNTED CASH FLOW: AWORKSHEET

~

David B. Perry and Jerry L. Robert on

Department Qf HorticultureOh 0 Agricultural Res rch and Development Center

u.S. 250 nd Ohio 83 SduthWooster, Ohio

This page intentionally blank.

INDEX

Discounted Cash FlowTime Value of MoneyDiscounting and the Discount RatePresent ValueNet Present Value

Discounted Cash Flow Worksheet for EvaluatingGreenhouse Energy Investments

Table 1. Example Placement of Values for Lettersin Discounted Cash Flow Worksheet

Table 2. Discounted Cash Flow Worksheet

i

12233

4

7

8

Table 3. Estimated Percent Gross Energy ConservationResulting From the Use of Three Major Energy Con-servation Measures 12

Table 4. Present Value of One Dollar Due at the Endof N Number of Years at X% Discount Rate 13

Figure 1. Illustration of the Discounting Process 11

PREFACE

Energy conservation, the adoption of energy-saving technologies, and thedevelopment of alternate energy sources have received considerable attention.While the on-going analysis of energy conservation technologies is very critical, it is equally important to evaluate the economics of the conservationmeasures. Energy conservation in commercial greenhouse production serveslittle purpose for grower/businessmen if the conservation measures are noteconomically justifiable. If there is to be widespread adoption of energyconservation measures or alternate energy sources, they must be the mosteconomical conservation measures.

This publication is an initial step in promoting greater economic analysisof greenhouse energy conservation investments for the individual grower. Aftera brief discussion of discounted cash flow, there is a worksheet for evaluatingany potential energy investments using discounted cash flow. For a more detaileddiscussion of greenhouse energy conservation investment criteria, methods forevaluating greenhouse energy conservation investments, and specific applicationsof discounted cash flow anlaysis for double-layer, air-inflated polyethylene overglass, internal cutrains, and glass laps sealants, see the OARDe companion publication, An Economic Evaluation of Energy Conservation Investment for Green-hou~, Research Bulletin 1114. .

12/79-500

-i-

This page intentionally blank.

EVALUATING GREENHOUSE ENERGY CONSERVATION INVESTMENTSUSIN'G DISCOUNTED CASH FLOW: A {~ORI(SHEET

David B. Perry & Jerry L. Robertson1

Prior to the 19708, the cost of energy for production of greenhouse cropsaccounted for only 5-10% of production expense. Inexpensive fuel enabled manygrowers to produce crops without regard to the type of temperature managementnecessary for conserving fuel use and in a manner that often amounted to inefficient use of greenhouse space. Many of these growers are less profitable today because of their inability to cope with an inflationary economYF stableprices for finished products, and rapidly rising production costs. Energy isnow the second largest single expense in the opera"tion of a corrrrnercial greenhouse, accounting for approximately 20% of production costs. Growers havelittle control over an inflationary economy, the minimum cost of labor, or product pric~s, but energy costs can be controlled and reduced. Today, all growers have available practical energy-saving practiceso These practices include(1) optimum maintenance of heating equipment, (2) proper location of temperature controls, (3) high boiler operating efficiency, (4) greater use of insulation, (5) use of high quality water in heati.ng systems p and (6) crop selection for lower temperature production~ Significant energy~savings can herealized with the use of these and other conservation measureSe As the fuelCOS"t continues to increase, growers will l1ave no option but to investigatemeans of reducing the energy use for the production unito

Tl1is paper presents a method, discounted casl1 flS?~, of evaluating the relative economic attractiveness of greenhouse energy conservation investments.After a brief discussion of discounted cash flow, the grower will find a worksheet. The worksheet is a step-by-step guide to use to evaluate a contemplat~

ed energy conserva"tion investment using discoun"ted cash flow.

DISCOUNTED CASH FLOW

A problem with examining investments "tl1~t en-tail both costs and benefitsover an extended period is placing a value on the costs and benefits realizedin the future. Due to a number of fae"tors, the fu·ttlre cash flows must be reduced in value to reflect inflation and "their relative value today.

Analysis of the initial investment and fu"ture cash flow carl be accomplished with the use of discounted cash flow. Discounted cash flow is a meansof comparing investments with different cash flow in different future periodso Using discounted cash flow, the future cash flow is discounted orreduced in value to reflect the time value of money associated wi·th actuallyreceiving cash flow as they extend farther into the future 0 By discountingthe cash flow, investments can be compared on the basis of what they areworth today. Determining what a fu·ture cash flow is worth today by discount-

1 Graduate Research Associate and Associate Professor, respectively, Departmentof Horticulture, Ohio Agricultural Research and Development Center and TheOhio state University.

-1-

-2-

ing it back to the present establishes the present value of the future cashflow. The concept of time value of money, discounting, discount rates, present value, and net present value will be elaborated on because they are centralto understanding discounted cash flow.

Time Value of Money

The concept of money having a time value shows awareness of inflation,o,pportunity cost, and the increasi11g risk associated with realizing cash flowin the future. Because money or, as in the case of energy conservation investments, the value of the net energy-savings realized due to reduced energy use,has a time value, ~\7e are willing to pay less today for money received five 'years from now, for example, than we would be willing to pay for the same amount of money received toda'y. The timing of the cash flow from an invest-ment is critical t<) the in'vestment decision. As cash flow extend fartherinto the ,future, they have less relative value today. Thus, discounted cashflow discounts or redl1.ces the value of the future net energy-savings at a ratethat is commensurate with the value that the individual or business places onthe money.

Discoul~ing and the Discount Rate

DiscOuIltirlg is easy to unders·tand if one first thinks of compound interest. If $100 is placed in a savings account for one year at 5% interest,there will be $105 in the account at the end of the year. At the end ofthe second year there will be $110.25, assuming annual compounding, becausethere is $5 iIlterest earned on the original $100, but 'there is also 5% or$.25 earned on the first years interest. In the same manner, the balanceof the account for any year in the future can be estimated. Discounting isthe opposite of compounding.

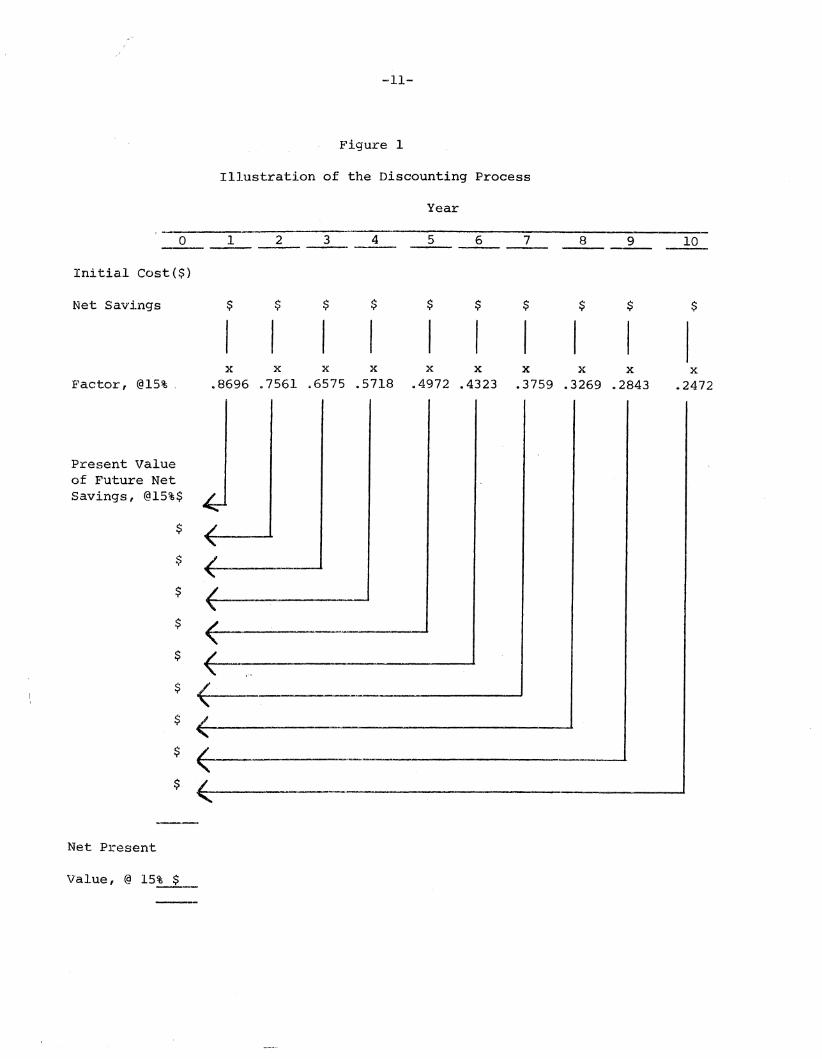

Basecl on the estimated perfOrnlal:1Ce of an investment, the future net cashflow is estimated for each year of the investment's life. Using discountedcash flow, the future cash flow estimates are discounted back to the presentat the discount rate. The discount rate is a specific percent b~l which futurecash flow is increasingly reduced in value for' each year that the cash flowextends into the future. To reduce the value of the future cash flow, discount factors that correspond to the percent discount rate are used. Forexample, in Figure 1, the discount factor at a 15% discount rate for ~ cashflow occurring one year from today is .8696. The factor at a 15% discountrate for a cash flow occurring two years from today is .7516. This means thatif a grower places a value of 15% on money, he would be willing to pay approximately $~87 for $1 one year from today and approximately $.76 for $1 two yearsfrom today. Similarly, the present value of any future cash flow or the present v'alue of th,e future energy-savings can be determined by multiplying thecash flow by the discount factor that corresponds to the percent discount rateand year in whicl} the~ cash flow occurs. Figure 1 illustrat:es the discountingprocess. In Figure 1, all estimated future ~ashflow is discounted back tothe present, so that all dollars can be thought of as if they are being realized

__•__.~ .,· •.~·,.~,,-,·_IU ,..,.. _......-___-_.••~---- ----,•• - •.• ' ,.-..

-3-

tOdayl. In other words, today's value or the present value of future cash flowis being determined~ If a relatively high discount rate is used, future cashflow is of comparatively less relative value today than if a lower discountrate is used. A table of discount factors for discount rates ranging from 8%to 26% over a period of one to ten years has been included with the discountedcash flow worksheet at the end of this publication. The worksheet is a stepby-~step procedure, which allows growers to evaluate energy conservation investments on their own i using their own costs and desired discount rates.

The discount rate can represent any of several possible alternatives.Frequently, the discount rate used by a given business is the cost of capitalfor the businessu For example, if an after-tax cost of capital of 15% hasbeen determined, 'the business would use a 15% discount rate in evaluatingproposed investments~ Many businessmen feel that at a minimum, an investm~nt

must have a rate of return that is at least equal to the firm's cost of capital~ The cost of capital is the firm's total cost of using funds 'from bothdebt and equity sources~ The discount rate can also represent the minimumreturn on invest~ent that the firm feels is acceptable compensation for theriskiness of the given investment 8 This rate may be more than the cost ofcapital rate because busi.nesses may add a risk premium when evaluating investmen'ts ~ The discount rate can als'o represent the rate at which the businesscan olytain ca.pital to finance the investment or it can be the opportunity costassociated with the funds used for the investment"

Prese:nt Value

Present value is a type of discounted cash flow technique. To determinef)reserrt value, projected future cash flow is multiplied by the discount ratefactor that corresponds to the discount rate for the year in which the cashflow occurs. Each" year's discounted cash flow is summed to determine thepresent value of all future cash flow, which is the present value of the investrnent. The present value indicates what the future stream of cash flowis """orth todcs:yo In other words ,investors should be indifferent between receiving $087 today or $1 one year from today if 15%, the discount rate, isperceived as being acceptable compensation, singe $.87 is what $1 is worthone year from today at that rate 0 See Figure 1 for an illustration of how:present value is determ,ined I)

Net Present Value

The net present value of an investment, determined by subtracting theinitial investment cost from the present value of the future cash flow (Figure1) I is a dire6t measure of the increase in net worth that a business willrealize by Ciloosing that investment. Any investment with a negative net pre,sent value .is not acceptable because it will decrease a business's net worth.

1 Discounted cash flow assumes that the ca~h flow for any given year occursin one lump sum at the end of tIle year. Energy-savings .will be' realizedon close to an annual basis, but, at worst, this assumption will causeonly small rounding errors. Discount rate factors can be interpolated between years if there is significant mid-year or quarterly cash flow,but because of the variable nature of month to month energy-savings,little would·be gained by doing so.

-4-

However j if the objective of making a given investment is prestige or convenience{or if the investment is required for health or safety reasons, for example, a negative net present value does not necessarily exclude an investmentfrom further consideration. An investment with a positive net present valueis acceptable, while an investment with a zero net present value is a marginalor brea]c-even investment. When com,paring several investments, the one with thehighest net present value at the discount rate used will increase an organization Us ne"t worth ·the most and is, therefore&, the best investment2 , 3. Thus,with energy conservation investments, one wants to maximize net present valuein order to maximize the dollar re·turn from the investments.

DISCOUNTED CASH FLOW WORKSHEET FOREVALUATING GREENHOUSE ENERGY INVESTMENTS

The following worksheet will allow you -to evaluate your own proposed investments i.n energy conservation equipment ,~y using discoun~ed cash flow analysis.All 'lalues for the letters, A, B &' C f e·tc 0' s110uld be entered in Table 2, whichwill evaluated the project over a ten year period. Table 1 illustrates theproper placement of the values for each letter.

10 au Total fuel costs for 19 = $ (A) A $for 8el .. fto (B) of ,production a.rea B sq. ft.

b .. Fuel cost/sq.ft .. for 19 A';'B = $ /squf-tu (C) C $ sq. ft.

2~ ao By using (conservation method)as an energy conservation measure, I willincur an initial installation expense ofapproximately $ /sqoft~ (D) and realize an estimated (see Table 3) gross energysavings of approximately ~ % (E)

b.. E7l00 = the decimal form of 'the estimatedgross percentage energy savings = ED

D $

E =

E'=

_____sq. ft.

%

----~---------.---....----~

3 C X ED = $ value of the gross energy savings/squfto f @ '(E) percent savings = F~ F = $ !sq.ft.

----~

2 TI\111ether tIle best investment, as meastlred by net present value, can be madewill depend on the necessary capital being available. This assumes anunlimited ca.pital market. In a ma.rk.et where the capital supply is restricted, par'ticularly the small businessman may not be able to obtain outsidecapital, which might limit investment choices regardless of, the net present values of the investments examined.

3 .A. direct netpresen't value compa.rison can only be made with investmentsof the same size. Therefore, when evaluating the positive net presentvalues of investments of significantly different amounts, considerationshould be given to the proportional or incremental net present value ascompared with the required investments.

4.

-5-

C - F = remaining fuel cost/sq. ft. afteradopting the (conservation method)energy conservation technique = Go G = $ /sq.ft.-------

5. Are there replacement or maintenance costsinvolved with this energy conservation technique? (Example, replacement of polyethylene.)

If yes, continue with step 6.If no, go to step 7.

6. The maintenance or replacement costs/sq. ft. , H, isthe total of the following:

a. materials, i.e. polyethylene $ /sq.ft./year

b. annual maintenance $ /sq.ft./year H

c. supplemental CO 2 (if necessary) =$ /sq.ft.year

d. other costs (please iden-tify) = $ /sq.ft./year

Place H maintenance and/or replacement costs in theworksheet table under the year in which they areexpected to be incurred. For example, the polyethylene used in the double-layer, air-inflatedpolyethylene over glass conservation method mustbe replaced on the average of every 2 years, sothere is a recurring materials replacement costevery two years. In addition, supplemental CO2may be necessary. If there is no cost for supplemental CO2 , for example, then "the cost wouldbe $0. The replacement and/or maintenancecost(s) must be calculated for each year.

/sq.ft.------ year

7. C (G + H) Net $ saving/sq.ft./yearNS = $ /sq.ft./year------_....

NS NS $ /sq.ft.------ year

The notation, NSl' NS2' NS3' etc~ is used in theworksheet example to indicate the net savings foryear I, net savings for year 2, net savings foryear 3, etc., respectively.

Inflation can be considered in the calculationsby inflating all costs at the estimated inflationrate/year, i.e. 8%/year, lO%/year, etc. An easyway to do this is to mUltiply each years costs byone p~us the decimal equivalent of the inflationrate. For example, if the inflation rate forthe next year is expected to be 10%, the costswould be multiplied by 1.10

-6-

In order to compare the energy conservation investments on as equal a basis as possible, theinvestments should be projected over equal periods of use. For example, t:he polyethylene usedin double-layer, air-inflated polyethylene overglass has a life, on the average, of two yearsand the fabric used for internal curtains has anestimated life of five years, so the common denominator for these two alternatives is ten years.Thus, these two investments should be compared ona ten year basis. Note, however, that the polyethylene and fabric replacement cost that wouldoccur in the projected tenth year should not beincluded. The benefits from the replacementoccur in years later than the tenth year and,therefore, are not within the scope of the projected period.

8. Repeat Step 7 for each projected year.

9. To determine the net percentage energy dollarsavings/sq.ft./year, divide NS for each yearby C. (NS;C). This will give a decimal number,for example, .44. Multiply this number by 100for the net percentage energy-savings in thatyear.

NS';'C x 100 = % net------ energy conservation/year%--------

10. The average percent net energy dollar-savings overthe life of the investment can be determined byadding all of the net percentage energy conservation numbers for each year determined in Step 9and then dividing that number by the number ofyears that the investment is being projected over(IO years in this case).

Average net energy $ savings %

11. To determine the value of the total net energy TNS = $conservation/sq. ft. over the life of the in-vestment, add the NS numbers for all years,such that NS l + NS 2 + NS 3 , etc. = $ (TNS)sq.ft.

/sq.ft.------

12. Table 4 presents discount rates from 8% to 26%.Select a discount rate based on the above explanation of what the rate can represent. Discount Rate = %

TABLE Ie Example Placement of Values for Letters in Discounted Cash Flow Worksheeto

YEAR 0 1 2 3 4 5 6 7 8 9 10

Initial installationexpense D

Energy expense/year C C C C C C C C C C

Energy expense/year@ E% reduction G G G G G G G G G G

Replacement and/ormaintenance cost/year H H H H H H H H H H

Net saving/year/sq. ft. NS1. .NS 2 NS3 NS4 NSS NS6 NS7 NSa NSg NSlO

Net percentage energy-I

'-oJ

savings/year NSl/C NS2/C NS3/C NS4/C NSS/C NS6/C NS7/C NSS/C NSg/C NSl"O/CI

Average % net energy-savings/year NSl + NS 2 + NS 3 + NS4 + NSS + NS 6 + NS 7 + NSS + NSg + NS lO

Total net savings/sq. ft. $ TNS/sq.ft.10

PV of TNS, @ X%discount rate $ TPV/sq.ft.

NPV of TNS, @ X%discount rate $ NPV/sq.ft.

TNPV of investment,@X% discount rate $ TNPV

TABLE 2:) Discounted Cash Flow Worksheet

Initial installationexpense

Energy expense/year

Energy expense/year,@ E% reduction

Replacement and/ormaintenance cost/year

Net savings/year/sq~fte

Net percentage energysavings/year

Average % net energysavings/year

Total net savings/sq~ft~

PV of TNS, @X%discount rate

NPV of TNS, @X%discount rate

TNPV of investment,@ X% discount rate

o 1 2 3 4 5

10

6 7

•• <_.c,-~_~=~~ __~_~ _

8

Jco!

-9-

13. Table 4 also presents what are called thefactors for each. discount rate for years l-ID. For example, at a 10% discount rate, thepresent value of $1.00 one year from today is$.0901. Thus, the dollar has been discountedby 10%. Similarly, the present value of $1.00two years from today, at a 10% discount rate, is$.8264. The same method will be used to discountthe net energy savings that are projected withthe adoption of a given energy conservation method.

14. Using the discount rate selected in Step 12, lookdown the column representing that rate in Table 4.These are the factors that wi1lbe used to discountt~e value of the net energy savings that have beenprojected. We want to know what the future savingsare worth today--in other words, the present value.For example, NS1 x the factor for year 1. at theselected discount rate = the present value of theenergy savings for year 1. Similarly, multiply theNS for each by the proper factor for that year.Add the present value (PV) of the NS for each yearto arrive at the present'value of the total netsavings/sq. ft. (TPV) at the selected-discount rate.The TPV is the value today of all the future netenergy-savings. See Figure 1 for an illustrationof the discounting process.

NS I x (factor) @ % discount rate ;: $+

NS 2 x (factor) @ % discount rate $+

NS3

x (factor) @ % discount;. rate $etc.

TPV/sq.ft. $

15. Once the present value has been calculated, it isa simple matter to calculate the net present value(NPV). To determine the NPV of the investment,subtract the initial cost of the investment (D)from the total present value (TPV). NPV is a directmeasure of the increase in net worth that a businesswill reaiize -by adopting a given investment.

( TPV/sq.ft.) (D/sq.ft.) = NPV/sq~ft. NPV/sq.ft. $

-10-

16. We are still working in sq.ft. units, so todetermine the total NPV for the greenhouserange, we should multiply the square footage(B) time the NPV/sq.ft. to determine the totalnet present value (TNPV) of the investment.

B x (NPV/sq.f,t.) = TNPV

LITERATURE CITED

TNPV $

10 Perry, David B. and Jerry L. Robertson. 1979. An economic evaluationof energy conservation investments for greenhouses. Ohio Agr. Res. &Dev. entre Res. Bul. 1114.

-11-

Fi9'ure 1

Illustration of the Discounting Process

Year

0 1 2 3 4 5 6 7 8 9 10---Initia.l Cost($)

N'et Savings $ $ $ $ $ $ $ $ $ $

Factor, @15% .J{ x x x

.8696 .7561 ~6575 .5718x x

.4972 .4323x x x

.3759 .3269 .2843x

.2472

Present Valueof Future NetSavings, @15%$

$

$

$

$

$

$

$

(;---{-__. _-.I

(-,----~----_----.

~_._, , ---J

$<*------------_---1.(-__----.__0<_--------------

{

Net Present

Value, @ 15~__

'I:AB:LE 3

Estilnated Percent Gross Energy Conservation Resulting FrOIn IrheUse of ThreeMajor Energy Conservation Measures.

A.verage Percentt " aEnergy Conserva_l0n

Range of PotentialPercent Energy ConservvationC

Do'uble-Poly__~._~llt

40%--60%d

Internal curtains

33%

Glass LapSeala.nts

15%

a

b

c

d

e

f

Percent of total fuel cost for' flea·ting greenhouses annually.

Roof area only covered.

Actual percen·t annual eller9Y C011S2J:"vation. realized depends on severalfactors, including severity of outside 'temperat:ures, type of green-house range, and condition of greenhouses(s} prior to use of conservation method.

Conservation realized influenced by rouount of greenhouse covered.

Conservation realized influenced by type of fabric, tightness ofthe seal inside the gree11house I and nUlnber of nig-hts t,hat curtainscan't be used due to possible snow loadu

Conservatioll realized is tligrlly dependen:t on condi tion of ,the green"·house prior to application.

TABLE 4" Present Value of One Dollar Due at the End of N Number of Years at X% Discount Rate 0

Discount RateYear 8% 10% 12% 14% 15% 16% 18% 20% 22% 24% 26%

1 .9259 .9091 .8929 .8772 .8696 .8621 .8475 08333 .8197 .8064 .7936

2 .8573 .8264 .7972 .7695 .7561 .7432 07182 06944 .6719 ,6504 06299

3 .7938 .7513 .7118 .6750 .6575 .6407 .6086 5787 .5507 .5245 .4999

4 .7350 .6830 .6355 .5921 .5717 85523 .5158 .4822 .4514 .. 4230 03967

5 .6806 .6209 .5674 .5194 .4972 .4761 .4371 .4019 ~3700 ~3411 .3149

6 .6302 .5645 .5066 .4556 .4323 .4104 .3704 .3349 .3033 .2751 .2499

7 .5835 .5132 .4523 .3996 .3759 .3538 .3139 .2791 .2486 .2218 .1983 I~WI

8 .5403 .4665 .4039 .3506 .3269 .3050 .2660 .2326 .2038 .1789 .1574

9 .5002 .4241 .3606 .3675 .2843 .2629 .2255 .1938 .1670 .1443 .1249

10 .4632 .3855 .3220 .2697 .2472 .2267 .1911 ,,1615 01369 .1163 .0991

~11 publications of the Ohio Agricultural Research and Development Cente~

are available to all on a nondiscriminatory basis without regard to race, color,national origin, sex, or religious affiliation.

This page intentionally blank.

This page intentionally blank.