VALU ORLD · An Integrated Cost Modeling Computer System for 8 , ... OFM undertook a study of...

48

VALU ORLD JOURNAL OF THE SOCIETY OF AMERICAN VALUE ENGINEERS VOLUME XVII, NUMBER 2 MAY 1994 Spec/aii Issue £3# ERECTING SAINT PETER'S OBELISK

Transcript of VALU ORLD · An Integrated Cost Modeling Computer System for 8 , ... OFM undertook a study of...

VALU ORLD JOURNAL OF THE SOCIETY OF AMERICAN VALUE ENGINEERS VOLUME XVII, NUMBER 2 MAY 1994

Spec/aii Issue

£ 3 #

ERECTING SAINT PETER'S OBELISK

CONTENTS

EDITORIAL

Vox Populi 1

ARTICLES

Value Engineering as a Budgeting Tool 2 Harvey C. Childs, AIA

An Integrated Cost Modeling Computer System for 8 , Construction VE Projects

ChansikPark, PhD and Ralph D. Ellis, Jr., PhD, PE

VEST: A Graded Approach to VE 15 Roger B. Sperling, CVS

Initiating VE Early in the Life Cycle of Products 17 Joseph J. O'Rourke, PE, CVS and GlenwoodL. Garvey, AIA

Value Engineering Contribution to Financial Flexibility 21

Arthur E. Mudge, CVS, FSAVE

EXECUTIVE SERIES

Testimony in the U.S. House of Representatives 25 Larry W. Zimmerman, PE, CVS, FSAVE Free Decision-Assistance Program Enhances VE with Risk Identification and 28 Quality Practices Database

Ernie Renner, Director U.S. Navy Best Manufacturing Practice Program

RELATED LITERATURE

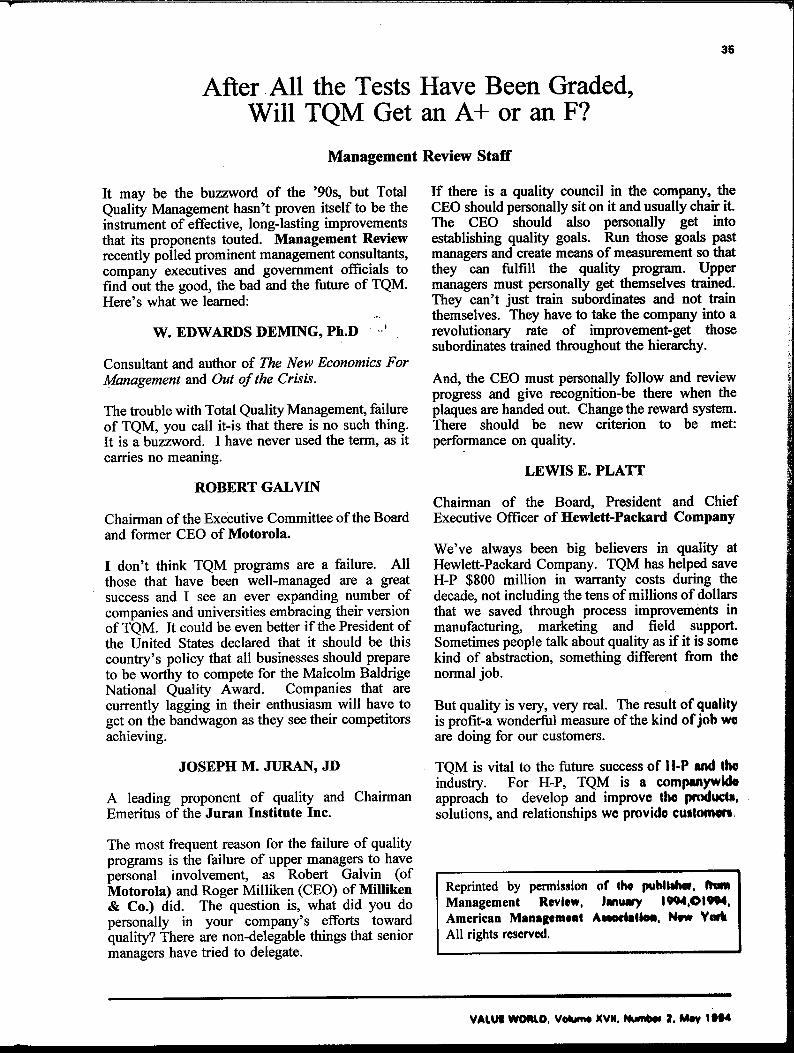

VE-Creative Steps Toward Total Cost Control 30 Del L. Younker, CCE, CVS After All the Tests have Been Graded, Will TQM Get an A+ or and F? 35

Management Review Staff

BOOK REVIEW

The Hidden Wealth of Cities: Policy and Productivity Methods for 39

American Local Governments, Kditcd by Edward ('. Hayes

SAVE BOOKSTORE BOOKS OF THE ISSUE

Function Analysis: The Stepping Stones to Good Value 40 Thomas J. Snodgrass, CVS and Muthiah Kasi, CVS Project Budgeting for Buildings 40 Donald E. Parker and Alphonse J. Ml'lsola. CVS, PE, FSAVE

Continued on Inside Back Cover

Editorial: Vox Populi

The voices that interest us the most are those of our readers and you certainly had something to say about the format changes in the last issue of Value World. Here is a sampling of the communiques we received.

" I am very much disappointed with your first issue of Value World. Judging by it, you are a compiler and not an editor."

"Congratulations on your first issue. In essence it looks good and I like most of the changes that you made."

"Throughout our normal day, we are bombarded with all kinds of documents that are black and white. I recommend that you add some color at least to the cover of Value World."

"It was a great shock and a severe disappointment to receive my January issue of Value World. After ten years, we finally had a product that presented a first-class image to the world in both appearance and content. The new format creates a very poor impression. It does not have style or quality."

"Congratulations on your inaugural issue of Value World. Good job. Good imagination. Your articles inside were a refreshing treat also. Keep up the good work."

"As you may know, many academics are big on attributes such as "status function"or "esteem function" when it comes to publications. While I don't necessarily support such views, I do live with my administrators who do. Unfortunately, the present Value World format and "look" will not provide for the functions of status or esteem as well as the past format did. In the previous appearance, including the picture and biography of the author did."

" I like your relaxing the computer disk requirement for offerings to Value World. There are a lot of people out there who cannot conveniently cope with that, so they do not offer that which is on their minds. I encountered the words "where appropriate" many times during my tenure as VE manager, spoken by the competition to roughen the playing field. It, therefore, gives some degree of satisfaction to read about that in the January issue of Value World. You have found the horseshoe. New gloves next?"

"Keep each issue more focused on our technical divisions. Cover should be a heavier stock and a different color. Put table of contents on inside cover. Use more font styles (e.g., bold and italics) in titles and quotes. There is too much white space."

"Then came the new-look Value World. Again I faced an unfamiliar format, but I was pleased to see the many

categories in the contents and the fine tribute to Editor Emeritus O. James Vogl, CVS, FSAVE."

And that was Vox Populi in action; prompting the format changes you see in this issue. These changes are the handiwork of our Production Editor, Doris Huston. Note the new feature Value Briefs that is intended to minimize white space while being informative. Note also the new feature SAVE Bookstore Books of the Issue. We hope you like the new features and changes but, at any rate, let us hear from you.

This special construction issue has a variety of articles starting with Harvey Childs' article on the budgeting process, followed by Drs. Park and Ellis' article on cost modeling, and Roger Sperling's article on a graded approach to the VE job plan.

Joe O'Rourke and Glen Garvey's article addresses an unusual application for VE in construction, namely, the oft-maligned public restroom. Next, Art Mudge reveals his expertise article on how VE can contribute to financial flexibility in both rich and lean years..

We have two articles in our Executive Series: The first is Larry Zimmerman's testimony to Congress on pending VE legislation. The second article is a description and offer of a free decision-assistance program by Ernie Renner, the Director of the U.S. Navy Best Manufacturing Practice Program.

Associate Editor Del Younker addresses cost control in construction in his article from Cost Engineering, the Journal of AACE International. The article After All the Tests Have Been Graded, Will TQM Get an A+ or an F? is from the AMA's Management Review. Coming on the heels of TQM discussions at our conference in New Orleans, the article is especially thought provoking. Read what Dr. W. Edward Deming, the recently deceased Dean of Quality, said about TQM.

Bemie Schulte offers sound advice for multiple-source contenders in "Perspective: And Now the Rest of the Story, our first essay in this issue. Third parties can submit VECPs against your contracts and get your share of the cost saving. You get to keep all the cost reduction. Now, ain't that a shame?

Roger Sperling returns with his delightful Perspective: Chaos Is Required in VE. Finally, Tom King closes this issue with a long-overdue salute to the grunts of the everyday world.

The upcoming September 1994 Value World will be a special healthcare issue. We have room for a few more articles and invite your contributions.

Goodnight and 30.

VALUE WORLD, Volume XVII, Number 2, May 1904

2

Value Engineering as a Budgeting Tool Harvey C. Childs, A I A

INTRODUCTION

The State of Washington has been a leader in the use of VE in the common school construction program (K-12) for the past ten years (1). Based on this success in 1990, the Office of Financial Management (OFM), which is the state budget office, implemented an additional VE program that broadens the use to all state agencies. This paper discusses the implementation and first results of the use of VE as a budgeting tool in a program called BEST, the acronym formed from Budget Estimate Team Study.

SELLING THE IDEA

In June of 1988, OFM undertook a study of capital planning and budgeting which included the following recommendations: 1) The state should strengthen all phases of its capital process, including planning, programming and monitoring; 2) Agencies should provide OFM and the Legislature with key information on capital project alternatives; and 3) The Department of General Administration, which manages construction projects for many non-university agencies, should identify opportunities for efficiencies and economies of scale in project planning, development, and execution (2).

To achieve these and other economies, OFM developed the requirement for a predesign phase on all major construction projects. (3). OFM developed the BEST process to evaluate predesign study findings.

BEST studies made it possible to develop highly refined programs of requirements prior to the commitment of the larger design and construction budgets. Real needs would be established and properly provided for, while unnecessary costs would be identified and eliminated. It would then be possible to establish appropriate and realistic project design and construction budgets.

The OFM elected not to perform BEST studies itself but to select projects and request funding for qualified value engineering firms to undertake the studies.

The primary responsibility of OFM would be to monitor each project to assure that all worthy BEST team recommendations were implemented in

the budget.

ADVANTAGES OF BEST STUDIES

There are several advantages to including VE in the budget evaluation process. These advantages are:

1. Prevention of project scope creep. BEST review will help insure the inclusion of all needed program elements and thus prevent project scope creep. Scope creep occurs when missing items in a project are discovered late in a project's design development, resulting in costly changes and additions to the project's scope. Performing a BEST study helps to maintain a strict budget to which the project must adhere right from the start. Project budgets based on unrealistic estimates precipitate enormous problems throughout the design and construction process.

2. Modification of space and construction standards. Modifications in facility space requirements and construction materials are the most effective area where capital savings can be found. In some designs, the program allocating space does not meet the project's real needs, or is used inefficiently. By analyzing a project at the predesign stage, the functional requirements of the project can be adjusted without detracting from the essential function.

3. First cost and life-cycle cost savings. The achievement of cost savings has to be emphasized along with the project improvements. Life-cycle costs are addressed during design but usually not stressed, only first costs become important. During predesign, the greatest opportunity exists to change designs which can impact not only the first cost, but more importantly, the life-cycle costs.

The study forces a tighter design. Staffing issues are identified and resolved early. Improvements in safety, security, design, and aesthetics also result.

4. Reduced adversarial relationships. Because the state budget office serves as a monitor of agency operations, there is a natural tension between agencies and OFM. However, the BEST process departs from the adversarial relationship

VALUE WORLD, Volume XVII, Number 2, Moy 1994

3

between OFM and state agencies by allowing them to work as a team to reduce costs and develop project improvements. The work plan to identify unnecessary costs and to improve project function compels in-house and outside experts to look beyond their own sphere and consider the impact of each decision on the total project. Since the goal of a BEST study is not simply to cut costs but to increase value, the study can and will identify necessary aspects of a project which are not being provided for adequately. Often, project improvement results because the elimination of unnecessary costs permits the inclusion of facility enhancements.

The creative team effort of the BEST process i

makes a budget review a more positive and fruitful' exercise rather than a difficult necessity, since both OFM and the state agencies benefit from the study. The VE study permits a budget analyst to join with the agency to maximize state dollars instead of having to work against the agency's understandable concerns with cost cutting.

Like any VE program, top management support is essential to be successful. This support was provided, and allowed the potential benefits to be realized. It was also critical to a successful BEST program to have clear project selection criteria and effective implementation procedures.

PROJECT SELECTION CRITERIA

Pareto's Law (80 percent of the cost normally occurs in 20 percent of the items) would suggest that relatively few projects would comprise the majority of costs. Therefore, it was recommended that efforts be concentrated on these selected larger projects. Cost and project size are generally good indicators of the potential for improved value. The following guidelines for identifying potential projects were established:

1. Projects involving expenditures of at least $5 million, with priority given to projects that are over $10 million.

2. Designs with a high degree of complexity.

3. Projects for which a standard or prototype could be developed (e.g. armory or prison).

In Washington State the capital budget adopted by the legislature usually includes either predesign funds or design/construction funds (projects which have completed predesign). It was recommended that BEST study projects would be selected from those that have completed predesign and met the

guidelines above.

IMPLEMENTATION OF BEST

The BEST process was accepted by OFM management and funds were made available to conduct four studies during the fall of 1992. To implement the program, OFM followed state law and requested qualifications from firms and individuals engaged in providing VE services, established a list of qualified BEST consultants, and negotiated contracts on the four projects selected. The contracting process also followed state law based on the scope of work described in the solicitation for proposals.

The studies would be conducted in Olympia on the capitol campus to allow for observation and monitoring of the process by all interested parties (executive, legislative and agency staff). Each study was scheduled for three, eight-hour, days. Each study followed the standard VE job plan and all teams were multi-disciplined with Certified Value Specialists as team leaders. At the conclusion of each study OFM, the agency, and the design team evaluated the ideas generated by the BEST team. Based on the results of the BEST study, final recommendations relating to the capital budget request for design and construction of each project were when made by OFM staff.

The following projects were selected and BEST studies conducted:

1. Western Washington University Haggard Hall Renovation. Haggard Hall was built in 1960 to house the science departments of chemistry, biology, and science education of what was then a teacher's college located in Bellingham. The building is being vacated with the construction of new science facilities. The 110,000 GSF building can no longer serve the needs of modern science instruction, but it is a sound building and with renovation can serve other needs of the university. One of these needs is for expansion of the library which is located in an adjacent building. In addition, other departments require office and support space on the campus.

The predesign study called for expansion of the library with a connecting passageway from the Wilson Library to Haggard Hall, and provision of stack space on the ground floor. Renovation of the second and third floors would accommodate the Departments of Computer Science and Foreign Languages. Abatement of asbestos within the existing building was required along with replacement of HVAC and electrical systems and meeting all code requirements. The exterior of the

VALUE WORLD, Volume XVII, Numb* 2, May I f f *

4

building would be upgraded by applying a new brick and concrete veneer panel system over the existing concrete structure. The total escalated project budget request equaled $23.1 million (4).

2. Green River Community College Center for Information Technology. The library at this Community College near Auburn is far short of the space required to serve current and projected levels of students. Also, science and skills labs are inadequate and undersized. Computer lab capacity to support academic and vocational instruction is insufficient.

The predesign study called for the construction of a Center for Information Technology and the related remodeling of two existing buildings constructed in the 1960's. The total predesign budget request for this project was $18.3 million. However, the State Board for Community and Technical Colleges, who is responsible for submitting budget requests on behalf of the various colleges in the system requested $14.6 million for this project (5).

3. Central Washington University Dean Science Building. Dean Hall was constructed in 1968 on the Ellensburg campus to serve the departments of Biological Sciences and Chemistry. The facility and its instructional equipment was virtually unchanged over the life of the structure. In 1987, the Science Education program was moved into the building after limited minor remodeling. Additional educational and research space and improved laboratory ventilation system were needed.

Predesign funds were provided to conduct an analysis for remodeling Dean Hall. At the conclusion of the study, it was determined that remodeling and expansion was not a viable option and effort was then concentrated on the planning and programming of a New Science Facility. The final outcome of the predesign study resulted in a budget request for a new science facility of 184,783 GSF at a total project cost of $87 million. Dean Hall was proposed for adaptive reuse as a separate project in the future (6).

4. University of Washington Physics Hall Remodeling. Upon completion of a new Physics/Astronomy building in 1994, the old Physics Hall on the Seattle campus will be available for reassignment. This building is over sixty years old and does not comply with a variety of life-safety, asbestos, ADA and seismic code requirements. The HVAC and electrical distribution systems are inadequate and need replacing. Renovation as a science facility is cost prohibitive.

The University's predesign study called for the complete renovation of the building. This-renovation includes a complete upgrade of all systems, the correction of fire and life safety, disabled code problems, and improvements to enhance seismic resistance. Included in the project is approximately a 20,000 gross square-foot (GSF) addition on the northeast side of the building, above sections of the building originally constructed to accommodate an addition. The project will provide over 170,000 GSF of usable space for University programs. The total budget request equaled $37.6 million (7).

RESULTS OF BEST STUDIES

The budget request for the four projects <that were selected for BEST studies exceeded $161 million. At the completion of the studies, OFM reviewed the reports provided as part of the BEST team contract and discussed the results with the agencies during the month of November. All four projects were included in the Governor's recommended capital budget presented in December, but at a reduced cost. The scope of one of the projects was reduced (Central Washington University) while another was increased (Green River Community College).

At the conclusion of the Legislative session, which also included extensive review of the agency requests and the BEST studies by the legislative staff, the projects were included in the appropriation bill and were funded. Funding was $36.2 million less than the original requests, allowing other projects to be included in the budget.

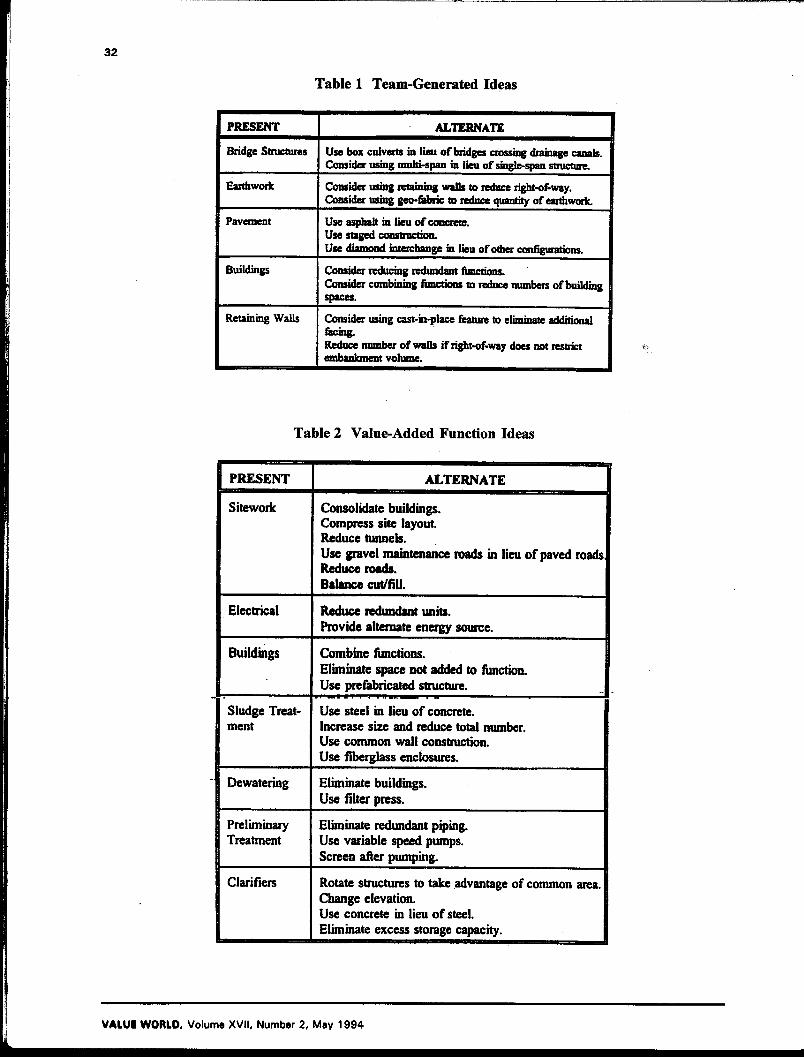

Table 1 displays the return-on-investment (ROI) for each project with respect to the cost of each study. The average ROI equaled $596 for each dollar spent on each study. It should be pointed out that the study cost does not include those costs incurred by the design team or agency personnel who participated in the process. Tables 2 through 5 give some of the ideas generated in BEST studies.

AGENCY REACTION TO BEST STUDIES

Needless to say, any time an agency request is reduced by the executive or legislative branch of state government those involved with the project request are not pleased. As stated previously, one of the advantages of doing a BEST study on requested projects is to reduce the adversarial relationship between the budget office and agencies. Although the BEST process inserts an independent third party into the budgeting process,

VALUE WORLD, Volume XVII, Number 2, May 1994

5

it has not always been met with open arms. Following are some of the comments expressed by the agencies whose projects are discussed in this paper:

1. Only during the VE team introductions on the first day of the study did the agency hear that they were welcome and encouraged to stay and participate in the rest of the study. Clearly, the philosophy of value engineering seems to have been compromised since it is crucial that the owner and the VE team work together to understand all the functional and operational costs.

2. None of the VE ideas were evaluated over a life-cycle format even though all of this information was available within the design document. '

3. The BEST conclusions and program decisions

product." says State Representative Helen Sommers, the Chair of the House Appropriations Committee and Past Chair of the House Capital Budget Committee.

John Fricke, Senior Budget Assistant for Capital and Transportation states, "We consider the BEST process very successful for two reasons. First, conducting these studies has let the design and construction industry know that there may be an independent review of their work product, which serves as an incentive to perform higher quality predesign studies for all state projects. This benefits both the state and the industry. Second, the BEST process is a model that has received overwhelming support from the design industry and most of the participants. It a process that should be instituted by many governments across the nation, and we have been communicating with them to spread the word."

The 1994 Washington State Legislature will be asked to address proposed legislation (ESHB2237)

were often made hastily with minimal data and consultation, pitted the OFM expert against the institution's expert, and often led to OFM prevailing even though the institution's expert may have been equivalent or greater.

4. While the BEST budget reviews produced some beneficial results, they are a duplication of the programming and cost estimating efforts completed during the predesign stage by the University and do not recognize the significant technical expertise at the University.

FUTURE OF BEST

"The BEST process is one step in a series of measures to reform the state's budget system and holds promise for substantially reducing capital budget costs while at the same it produces a better

that will codify the BEST process. This proposed legislation states in part, "The Office of Financial Management shall adopt a procedure for reviewing major construction projects at the predesign stage that will reduce long-term costs and increase facility efficiency. The procedures shall include, but not be limited to, the following elements: An identification of facility program, building quality and standards, and consistency with long-range facility plans; a system of cost standards to compare major capital construction projects; and a construction schedule that includes value engineering analysis and constructability review process."

The BEST process will continue as a tool used by the State Budget Office to evaluate major capital projects. Projects, funded for predesign in the last budget, will be submitted to OFM by July 1,1994 to be considered for inclusion in the next capital budget for design and construction. During August OFM will conduct the second round of BEST studies on eight to ten projects.

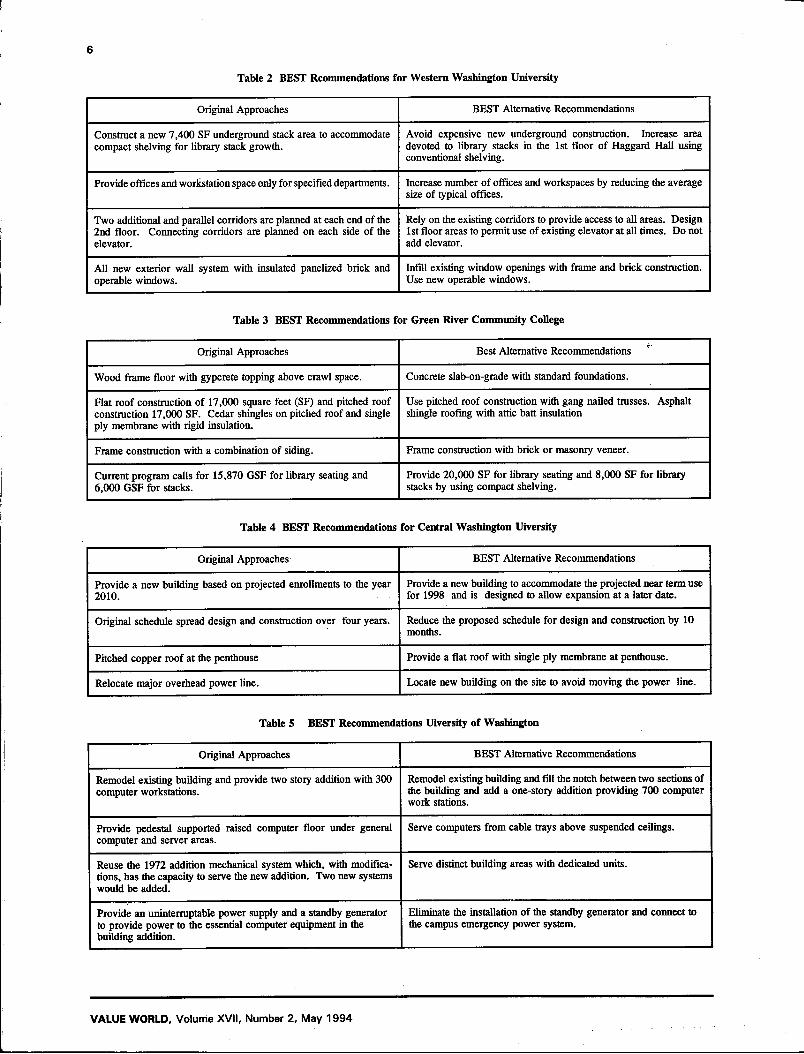

Table 1 Summary of BEST Sudy Results

Project Budget Request Approved Budget Study Cost ROI

Western Washington University $23,111,713 $17,312,971 $14,000 414:1

Green River Community College 14,588,000 15,944,725 15,000 90:1

Central Washington University 87,010,732 58,750,000 15,300 1,847:1

University of Washington 36,888,635 33,405,321 16,289 213:1

Totals $161,599,080 $125,413,017 $60,589 —

VALUE WORLD, Volume XVII, Number 2, May 1994

6

Table 2 BEST Rcommendations for Western Washington University

Original Approaches BEST Alternative Recommendations

Construct a new 7,400 SF underground stack area to accommodate compact shelving for library stack growth.

Avoid expensive new underground construction. Increase area devoted to library stacks in the 1st floor of Haggard Hall using conventional shelving.

Provide offices and workstation space only for specified departments. Increase number of offices and workspaces by reducing the average size of typical offices.

Two additional and parallel corridors are planned at each end of the 2nd floor. Connecting corridors are planned on each side of the elevator.

Rely on the existing corridors to provide access to all areas. Design 1st floor areas to permit use of existing elevator at all times. Do not add elevator.

All new exterior wall system with insulated panelized brick and operable windows.

Infill existing window openings with frame and brick construction. Use new operable windows.

Table 3 BEST Recommendations for Green River Community College

Original Approaches Best Alternative Recommendations *"

Wood frame floor with gypcrete topping above crawl space. Concrete slab-on-grade with standard foundations.

Flat roof construction of 17,000 square feet (SF) and pitched roof construction 17,000 SF. Cedar shingles on pitched roof and single ply membrane with rigid insulation.

Use pitched roof construction with gang nailed trusses. Asphalt shingle roofing with attic batt insulation

Frame construction with a combination of siding. Frame construction with brick or masonry veneer.

Current program calls for 15,870 GSF for library seating and 6,000 GSF for stacks.

Provide 20,000 SF for library seating and 8,000 SF for library stacks by using compact shelving.

Table 4 BEST Recommendations for Central Washington Uiversity

Original Approaches BEST Alternative Recommendations

Provide a new building based on projected enrollments to the year 2010.

Provide a new building to accommodate the projected near term use for 1998 and is designed to allow expansion at a later date.

Original schedule spread design and construction over four years. Reduce the proposed schedule for design and construction by 10 months.

Pitched copper roof at the penthouse Provide a flat roof with single ply membrane at penthouse.

Relocate major overhead power line. Locate new building on the site to avoid moving the power line.

Table 5 BEST Recommendations Uiversity of Washington

Original Approaches BEST Alternative Recommendations

Remodel existing building and provide two story addition with 300 computer workstations.

Remodel existing building and fi l l the notch between two sections of the building and add a one-story addition providing 700 computer work stations.

Provide pedestal supported raised computer floor under general computer and server areas.

Serve computers from cable trays above suspended ceilings.

Reuse the 1972 addition mechanical system which, with modifications, has the capacity to serve the new addition. Two new systems would be added.

Serve distinct building areas with dedicated units.

Provide an uninterruptable power supply and a standby generator to provide power to the essential computer equipment in the bunding addition.

Eliminate the installation of the standby generator and connect to the campus emergency power system.

VALUE WORLD, Volume XVII, Number 2, May 1994

7

REFERENCES

1. Harvey C. Childs, Win-Win-Win School Construction in Washington State, 1985 SAVE Conference Proceedings, Society of American Value Engineers.

2. Executive Consulting Group, Inc., Capital Planning and Budgeting Study, 1988.

3. Washington State Major Projects, Predesign Manual, 1992.

4. McLellan and Copenhagen, Inc. et al, Haggard Hall Renovation, Western Washington University Predesign Report, 1992.

5. Mahlum & Nordfors, Green River Community College Predesign Study, 1992.

6. The Tsang Partnership, Inc., Central Washington University Science Facility Predesign Study, 1992.

7. NBBJ, Inc., Old Physics Hall Predesign Study, University of Washington, 1992.

8. Hill Architecture, Haggard Hall Renovation Value Enhancement Study, Western Washington University, 1992.

9. Pacific Rim, Green River Community College Center for Information Technology, 1992.

10. Ackroyd, Inc., Central Washington University Science Facility Budget Evaluation Study, 1992.

11. Kramer, Chin & Mayo, Inc., Value Engineering Study Report Old Physics Hall Renovation, University of Washington, 1992.

Mr. Childs, AIA is the Capital Budget Assistant to the Governor in the State of Washington in the Office of Financial Management in Olympia, Washington.

Value Brief Internal Rate of Return

The relationship internal rate of return (IRR) is part of the more comprehensive subject of time value of money. IRR is defined as the rate of return at which the present value of future benefits equals the present value of costs.

IRR is extremely useful in evaluating the economic feasibility of large-scale construction projects. Value practitioners should calculate the IRR when evaluating the costs vs. benefits alternative approaches and the means of implementing functions.

The approach in calculating IRR is to equate the estimated cost of the project and the estimated return over the time period of interest. For example, consider a project to build a facility at an estimated cost of $100 million. The estimated net annual return from the facility over a period of ten years is $20 million.

From the time-value-of money viewpoint, the eestimated cost of $100 million is the present value cost. The present value of benefits is representated by the uniform series of annul payments over ten years. Equating the present

value of cost and the present value of benefits yields an LRR of 15.83 percent.

From an economic viewpoint, the investment in the construction project is the same as any other investment yielding a return of 15.83 percent annually for 10 years. An investment yielding a return of more than 15.83 percent over the ten-year period would be a better choice. From a practical viewpoint, however, consider the potential for capital appreciation and risk exposure before choosing among alternatives.

R e p r i n t e d from Understanding the Time Value of Money, Copyright ®1995, w i t h the p e r m i s s i o n of the cop y r i g h t owner, Management S c i e n c e .

VALUE WORLD, Volume XVII, Number 2, May 1994

An Integrated Cost Modeling Computer System for Construction VE Projects

Chansik Park, Ph.D and Ralph D. EUis, Jr. , P E , Ph.D

INTRODUCTION

VE studies begin with identifying and isolating items or areas of potentially low value and high cost. This procedure along with function analysis is one of the most important aspects of a VE study. It is difficult to find the low value, high cost items or areas in the modern facility which consists of thousands of system elements. For this identification process, VE practitioners often use cost modeling technique during the information phase of the VE job plan or the pre-workshop stage of a VE study, depending on the complexity of projects. It is very critical for the successful VE to develop a proper cost model since further VE efforts significantly rely on the analysis results of the cost model.

Although the VE application in the early stages of the project cycle is less expensive to implement than that in the later stages, VE can be applied in all stages of the cycle. The structure of cost model will vary with the project type. Hence there is a need to develop a general cost modeling system which can be applied to any type of project and any stage of the project cycle. In addition, at present time VE practitioners are not utilizing more or less the beneficial information gained from previous cost model developments. It would be advantageous to computerize the modeling technique, which allows the accumulation of previous cost model information for the use of future model developments.

This paper describes a computerized cost modeling system, called the Integrated Cost Modeling System (ICMS), which can be utilized in developing cost models for construction VE projects. Database, spreadsheet and rule-based expert system programming technologies are incorporated into ICMS.

ICMS enhances the efficiency, accuracy, and reliability of current cost modeling practices. The positive benefits of ICMS are at least threefold:

1. Users can customize cost input models for specific project types.

2. The system allows for users to develop a checklist database for project system elements.

3. Cost model information can be stored in a database for other applications.

STRUCTURE OF ICMS

ICMS consists of four major components: Custom Cost Model; Custom System Checklist Model; Estimated Cost Input Model; and Target Cost Input Model. All four components are programmed within the GURU (version 3.1) environment which provides various programming tools such as relational database, spreadsheet, form management, and expert system (1). The overall structure of ICMS is illustrated in Figure 1.

Based on user expertise in specific project types, various cost models and system checklist models can be customized within ICMS in the form of a database. These customized models are utilized for the estimated cost input model of a specific project. Target costs for project system elements are established by utilizing previous project cost information stored in the project database of ICMS. The established costs can be updated through detailed function analyses for specific system elements. And then a cost model analysis report which indicates potential VE areas is generated by comparing estimated costs with target costs. Finally, the report is stored in a project database for use in future development.

CUSTOMIZING COST MODELS

The initial step of developing a cost model for a construction VE project is to develop a breakdown structure of project system components. In doing so, value engineers classify the system components into major functional system elements. In other words, a function element is composed of some system components and has also a hierarchical function relationship with the other elements. This functional grouping of system elements differentiates the VE cost modeling technique from the other trade-oriented cost modeling techniques.

VALUE WORLD, Volume XVII, Number 2, May 1994

9

USER EXPERTISE PROJECT COST INFORMATION

CUSTOM COST MODEL

CUSTOM SYSTEM CHECKLIST

ESTIMATED COST INPUT MODEL

TARGET COST INPUT MODEL

PREVIOUS PROJECT COST INFORMATION

PROJECT DATABASE

Figure 1 Overall structure of ICMS.

It is obvious in construction that the structure of cost model varies with project types: the function elements of building projects are different from those of other construction projects such as bridge, highway, and dam. The VE expertise on specific projects would have a great impact on the cost model development. This expertise can be stored and customized in ICMS.

It should also be noted that general-elemental cost formats for facility design and construction have been developed by several government construction agencies such as the General Services Administration (GSA), GSA's Public Building Services, and the Environmental Protection Agency in conjunction with the American Institute of Architects and the Construction Specification Institute. (2, 3). These cost formats could be used in customizing cost models.

The customized cost model is built in the form of a database. Commonly, a database consists of records which contain various sources of data. The data sources are stored in various data fields of each record. ICMS uses a predefined database which provides the user with all necessary data fields in customizing the cost model.

The data fields are the following: system code, system name, unit, and unit measure. The system code field is used to represent a hierarchy of system elements. ICMS allows the user to break a functional element down to as many as four hierarchical levels. Therefore, the cost of a

functional element at some higher level represents the summation of functional element costs at the next lower level and below. The form of the custom system input model filled with a sample system element is illustrated in Figure 2.

CUSTOMIZING SYSTEM CHECKLIST MODEL

The checklist model database for functional elements at the lowest level can also be customized. This checklist model has been designed to store listings of components or items to be included and to be excluded in the classified functional elements.

This checklist not only serves as a reference for function grouping of project system components but also ensures the reliability and accuracy of cost estimates for function elements. A sample checklist is shown in Figure 3.

The fields of system code and system name are automatically imported from the customized cost model. Users provide necessary component data to the fields "WHAT TO INCLUDE" and "WHAT TO EXCLUDE" in the figure.

Component data can be obtained from cost data sources such as R. S. Means, Inc. and GSA's UNIFORMAT H (2, 4).

VALUE WORLD, Volume XVII, Number 2, May 1994

10

Record Number: 1 ~->next "<-prlor Enter-edit Esc-quit

[ CUSTOMIZE COST INPUT MODEL]

System Code 101 k

System name I FOUNDATION k

Unit I GSF b

Unit Measure I Gross Area k

Do you want DELETE (Type TRUE): I FALSE!

Figure 2 Custom system input model.

Record Number: 1 "->next "<-prior Enter-edit Esc-quit

(CUSTOMIZE SYSTEM CHECKLIST)

System Code |0^1

System name 1 EXTERIOR WALLS k

WHAT TO INCLUDE WHAT TO EXCLUDE

.facing materials .applied finishes to interior faces

.exterior applied finishes of exterior walls

.framing, wallboard, parapets .columns and beams in ext. walls

.exterior load-bearing wall .Venetian blinds

.exterior louvers & screens .other int. sun control devices

.exterior sun control devices .roof eaves and eaves soffits

.balcony walls & railings .glazed curtain walls

.exterior soffits

Do you want DELETE (Type TRUE): IFALS&

Figure 3 System checklist data base sample record.

VALUE WORLD, Volume XVII, Number 2, May 1994

11

ESTIMATED COST INPUT MODEL

The estimated cost input model is designed for the user to input estimated costs of function elements based from the VE studies.

This model is an extended database of the customized cost model, which allows the user to input quantity and cost of each system element. The user can choose a proper cost input base, either unit or total cost and needs only to input system costs in the lowest level. The system costs in the higher level are automatically calculated by ICMS.

The customized system elements are transferred from the customized model database. During this input process, the system elements can be added, edited, and deleted. The system checklist data can also be reviewed by using a query function programmed in this model. The accuracy and reliability of the cost estimates could be enhanced by interacting with the system checklist model. In addition, the time in developing the cost model would be significantly reduced by utilizing the customized cost model.

TARGET COST INPUT MODEL

The next step of cost modeling is to establish target costs for system elements. The term target cost can be defined as a minimum cost required to fulfill basic functions of a specific system element. In construction VE studies, target costs would be determined either before or after detailed function analyses for system elements. These costs are often determined by the VE team's experience with similar projects, or cost information from previous similar projects. Then, target costs are compared with estimated actual system costs. The areas or elements showing the biggest differences are isolated for further VE study.

In ICMS, target costs are determined by utilizing the system cost information from previous VE projects stored in the project database. The previous project system costs are queried and adjusted by time, location, and size by utilizing a rule-based expert system. Two pre-defined cost index databases have been designed for the time and location adjustments. ICMS allows the user to update the time index database and customize the location index database for its use of specific locations. Construction cost indexes such as those of R.S. Means Company Inc. and Richardson Engineering Services could be used as base indexes for these databases.

For the system testing purposes, sample databases have been created on the basis of the R. S. Means, Inc. historical cost indexes and city cost indexes. The form of the target cost input model filled with a sample system element cost data and its target cost determination procedure are illustrated in Figures 4 and 5.

The expert system employed in this model is a program which contains the knowledge about how to query and obtain necessary cost and index information from the project database and the index database. Target costs determined by this program are only approximate estimates before the detailed function analyses. They must be updated after the function analyses for the use of future

1 model developments.

Figure 6 illustrates a dependency diagram of the relationships among variables in the expert system. The top two boxes in the figure indicate data sources obtained from the user input and the cost and index databases. Arrows between variables represent the hierarchical dependency of variables used for rules of the expert system.

The equation used for the cost adjustments is shown in the bottom box of the figure. Appropriate city indexes for functional elements involving several CSI divisions are calculated by averaging the related division indexes.

Figure 7 illustrates the summary report of the project cost model which ICMS generates through a series of data conversion processes. The particular project shown is a healthcare facility.

The top half of Figure 7 shows the cost distribution of the functional elements.of the systems which are being studied. The bottom portion of the the illustration shows the cost distibutions and ratios of estimated cost to target cost of the functional elements.

CONCLUSION

A prototype system of ICMS has been successfully developed in Version 3.1 of the GURU environment. Key characteristics of ICMS are its customized cost model feature, and the accumulation and utilization of cost data. All component parts of the system have user-friendly menu-driven subsystems. A function analysis system, currently being developed, will be incorporated into the prototype system for the continuous update of target cost data. This enhancement will make ICMS a total cost modeling system.

VALUE WORLD, Volume XVII, Number 2, May 1994

12

[ TARGET COST INPUT MODEL

System Code 101 •

System name I FOUNDATION

System Cost I $465,888,001

Uni t IGSF h

Uni t Measure 1 Gross Area •

Quan t i t y 1 17,391.001

|Un i t C o s t | 1 $26,791

Target Uni t Cost | $ 2 1 . 0 0 |

I ENTER I S tar t Input lESCl Query(Y) or Quit(N)

Figure 4 Target cost input model.

PROJECT DATABASE

QUERY PREVIOUS

SYSTEM COSTS

COST INDEX DATABASE

RULE-BASED EXPERT SYSTEM

TIME & LOCATION ADJUSTMENT

I DETERMINE TARGET COST

TARGET COST INPUT MODEL

Figure 5 Target cost determination procedures.

VALUE WORLD, Volume XVII, Number 2, May 1994

13

SJfQSlMlnte r_H*TkMlndM DJN&.Ut.Mmc I^MCtLoeuknlntet S_COCeSytfMiCoda ID:PNjMIO CWCSOMrtMi RPNVMM C.Cui«lt

ADJUSTED TARGET COST =:

(S_COST) • (C_CfTY/P_QTY) * (C_YlNrW,YIND) • (CJ.IND/PJJND)

Figure 6 Expert system dependency diagram.

H i ttfCOQI Dat.f 11/19/1993

M W I MALT) CHS MCI LIFT Location ea inc fv i lU , FloNdt

w . DOSMUL

s m w n OF FRojstr STTTTEK cwr n s n a u m w

COM 3Y3TN WW UK IT aiMrTirr w n nor «8 N K H H I I C U C£F 1 U . 7 9 W tacrmuu. o r m,ntM «».« 02 8UB8TRUCTUM eti J70 ,OEO.C« *i».s« 10 imwt comnion,

o r ,370 ,0I0 .» (15.41 11 fOWPNBIT e s ,371,010.01 «>.» OS DJTHICK oaemucnoBii ,in>,oio.w n s . i s ca SUFfltSTMJGTUM 19 ,370,090.00 » 1 . » 12 I I I B K W C O F ,970,(40.10 W . M OS u o n m o r ,37»,MM0 » . M K Baffin* aasutcs CtF ,37i ,Hi . ia i s . a 01 F0MMTHM (SF ,J7I,WI.I<1 (2.W or CDNEnBS SVSTB1 « r ,171,101.10 to. 73

T O U L I 1 7 J . »

m m con TM-uwr o n m - m m tan c/v » » n o > ie .os t ,m.u 138.00 <U,0<0 l0W.0p I J UD,MS>,I0I.M •20.00 13 17,M«,W9.00 MS.DO I J « s , ru i ,«n . t» *1S.W »5.IJ0,0»0.0» 1.0 H,w7,oeo.ot S B . 0 0 K,B1D,O»0,O» 1.0 B , «1 , 0«0 .0» »O.00 u.eiOjOn.oi 1.0 X.Stt.OW.Ot M0 .CO <3,700,0W.M 1.2 >i,7M,0W.M BM « , n o , o o o . K ) 1.1 S Z . O H . M O . O I 15.00 5I.K0.C00.M 1.1 tl.WfcOH.Ot 8.00 •I.BO.Dof.Ce 1.1

m s . O K . o i U J ] >9U.tM.I0 1.1 $270,0*3. M to .n BB9,D0t.l0 1.0

H3,7 » , o o o . e o t w . e « 3 , » 1 , 1 M . « 0 *13D

swraot GrM KMT ID •"TBI COST •WTPtSMTIQrl

_HMIT cow-uagw

Figure 7 Sample summary report.

VALUE WORLD, Volume XVH, Number 2, May 1994

14

REFERENCES

1. GURU, Version 3.1, Micro Database Systems, Inc. Lafayette, IN, 1992.

2. Brian Bowen, Robert P. Charette, and Harold H. Marshall, UNIFORMAT II: A Recommended Classification for Building Elements and Related Sitework, National Institute of Standards and Technology, Special Publication 841, Gaitherburg, MD, August 1993.

3. Value Engineering for Wastewater Treatment Works, Office of Water Program Operations, United States Environmental Protection Agency, September 1984.

4. The Means Assemblies Cost Data, R.S. Means Company, Inc., Kingston, MA, 1992.

Dr. Park is a Certified Architectural Engineer in Korea.

Dr. Ellis is a Professor in the Civil Engineering Department of the University of Florida in Gainesville, Florida.

Value Brief International Quality Standards

More and more companies are entering the global market place i f only to ensure their survival. Many value practitioners already have international clients. Those who are doing business or contemplate doing business overseas should become familiar with the international quality management standards which are promulgated by the International Organization for Standardization (ISO).

These are the ISO 9000 series of FIVE standards. In the United States, they are equivalent to the Q 90 series promulgated by the American National Standards Institute (ANSI) and the American Society for Quality Control (ASQC).

Standard ISO 9000, Quality Management and Quality, is equivalent to ANSI/ASQC Q 90. This is the top-level standard and contains overall policy statements, definition of terms, and requirements for certification of organizations in accordance with the pertinent standard in the series. ISO 9000 also provides guidelines for determining which subordilate standard governs the industries of interest.

Standard ISO 9001, Quality Systems-Model for Quality Assurance in Designed Development, Production, Installation, and Servicing, is equivalent to ANSI/AMQC Q 91. It is the most comprehensive of all the standard in the series and applies to equipment manufacturers of their own design.

Standard ISO 9002, Quality Systems-Model for Quality Assurance in Production and Installation, is equivalent to ANSI/AMQC Q 92. It applies to equipment manufacturers of designs by others.

Standard ISO 9003, Quality System-Model, for Quality in Final Inspection and Test, is equivalent to ANSI/AMQC Q 93.. As the name indicates, it applies to the requirements and procedures for final inspection and test.

Standard ISO 9004, Quality Management and Quality System Elements-Guidelines, is equivalent to ANSI/AMQC Q 90. It applies to the overall quality organization of companies and delineates management responsibilities for quality assurance.

The standards are available from the American National Standards Institute, 1430 Broadway, New York, NY 10018 and the American Society for Quality Control, 310 Wisconsin Avenue, Milwaukee, WI 53203.

VALUE WORLD, Volume XVII, Number 2, May 1994

15

VEST: A Graded Approach to VE Roger B. Sperling, CVS

INTRODUCTION

VE at Scope Time (VEST) is the early application of value techniques used to clarify construction project scopes of work. It focuses on function analysis and creative brainstorming, leaving development of VE proposals to the design team. VEST is a good way to apply VE to smaller construction projects; larger projects still require full formal VE studies. This article shows how VEST can be used as a graded approach to VE to help improve facilities projects no matter what their size (1, 2).

VEST MATRIX

I f only one form of VEST were offered it would not be used in many cases; when flexibly applied VEST finds more uses. Often, project managers will use VEST to try VE for the first time.

The VEST Matrix in Table 1 provides a "shopping list" of options for three different scales of VEST:

•VEST A (1 to 2 hours): Single issue meetings.

•VEST B (2 to 4 hours): Project kickoff meetings.

•VEST C (8 to 16 hours): Scope and criteria development.

VEST applies value technology to plant facilities construction projects by convening meetings of project teams and other interested organizations to ask, in effect, "Why are we doing this project?" Each project and its manager have different needs.

The activities in the matrix, which all occur in a formal VE study, are based on the VE job plan. The comments communicate the intrinsic value of each activity to potential clients. Included activities are coded "X"; optional ones are "O."

Table 1 VEST Matrix

Activity VEST

A VEST

B VEST

c Comments

1-2 HR 2-4 HR 8-16 HR

Protect Information X X X Reviews scope and criteria ol Base Desiojn

Site Visit 0 X Included whenever possible

Cost/Worth Analysis X Focuses on costs of Base Design

Function Analysis X X X The key element

Creative Bralnstormlno X X X Idea generation

Idea Evaluation 0 X X Ranks ideas the primary resul

Advantaaes/Dteadvantaoes 0 0 X Documentina the details

Proposal Development 0 0 Included when time available

Final Presentation 0 Included when requested by client

Report Preparation X X Bound report documents complete study

Idea/Proposal Implementation X X X Done by PM, PE/A, design team. cBent/user

Xlnokided ForSlngle-lsHwrrMetbiguMA P*l = Project Manager O Optional For ScopWOIUrU o»v»lopm»nt ua* B or C PE/A * Protect Enslneer/Arefikect — Excluded For Pro|«ct Klckotf rrmUngi U M A or B

VALUE WORLD, Volume XVII, Number 2, May 1994

16

All VEST studies include the project information, function analysis and creative brainstorming phases of the job plan. As projects become larger and the VEST time increases more activities are added. VEST A utilizes only four activities; VEST B and VEST C use six and ten activities respectively. The main message of the matrix is that VEST can be tailored to any size project and any project issue.

EXAMPLES

CONCLUSION

VEST is not a full, formal VE study; but it does utilize the core of the VE job plan and applies function analysis to each project. By offering a matrix of VEST options VE, can be applied to small projects and others that otherwise might not receive the benefits of VE.

REFERENCES AND FOOTNOTES

Four brief examples of using VEST on smaller projects ($650,000 average estimated construction cost) demonstrate the benefits of doing VE early in the life of projects :

Uninteruptable Power Supply Buildings: Eight-hour VEST generated 67 ideas and found two new design approaches including using existing space and not constructing a new facility.

• Control Post: Twelve-hour VEST generated 129 ideas and identified 22 percent potential savings for new security facility.

Waste System: Eight-hour VEST generated 55 ideas and developed two design options involving segregating waste to reduce the need for secondary containment.

• Office Upgrade: Three-hour VEST generated 51 ideas and reduced project costs 24 percent by simplifying design of tenant improvements. The emphasis in VEST is idea generation and evaluation to sharpen the project scope. The return on investment is not based on dollars saved but functions improved.

1. Sperling, R., Value Engineering at Scope Time (VEST), Value World, January/February/March 1991, pp. 12f.

2. Sperling, R., VE at Scope Time (VEST); Three Construction Examples, Presented at the Society of American Value Engineers International Conference, Kansas City, MO, May 1991.

Mr. Sperling is SAVE National Director for Annual Conference Technical Programs and with Lewis & Zimmerman Associates, Inc. in Walnut Creek, California.

Value Brief General Services Administration

As the property manager and purchasing agent of the government of the United States, the General Services Adminsitration (GSA) sponsors manyVE studies. On March 28, 1994, the GSA published a solicitation for VE studies and related services with a dollar value of $3,750,00.

GSA is divided into four services in eleven regional areas. The four services are: Public

Buildings Service; Federal Supply Service; Information Resources Managment; and Federal Property Resouces Service. Among the major functions of the GSA are: the distribution of supplies, services, and personal property to federal agencies; the management of transportation and travel; the operation of Federal Information Centers; and the construction and operation of federal buildings.

VALUE WORLD, Volume XVII, Number 2, May 1994

17

Initiating V E Early in Life Cycle of Products Joseph J . O'Rourke, P E , CVS and Glenwood L . Garvey, AIA

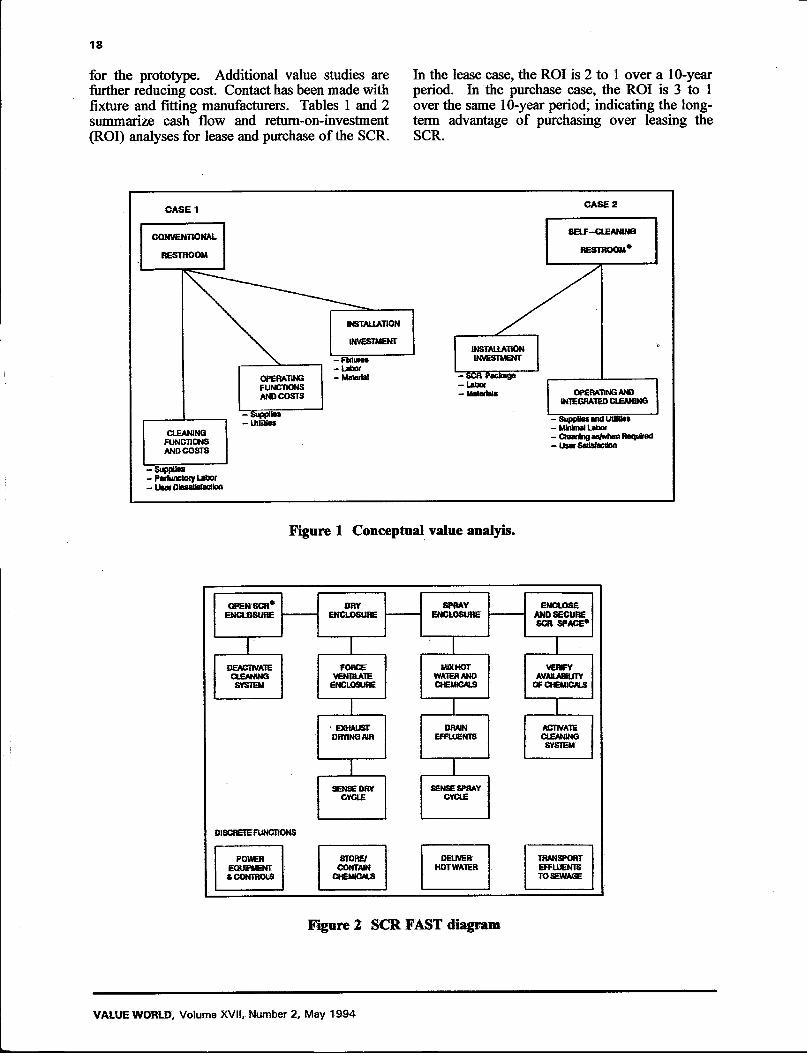

INTRODUCTION SCR Approach

This paper recognizes the advantages of initiating VE in the conceptual phase of a project. In this Depreciation $4.66 case, it started with the recognition of a need. Supplies/Utilities 0.50 There is no facility more familiar to mankind than Labor: 15 min/day 3.13 the public restroom. It is a fact that few are maintained to any acceptable standard of Total $8.29 cleanliness and sanitation. Initially, the project was conceived to be marketed to major oil Conventional Approach companies to upgrade the tens of thousands of. unsanitary and unsightly service station facilities. ..' Supplies/Utilities $0.91

Labor: 45 min/ day 9.39 APPROACH

We decided early that a VE study of the functions and costs involved in cleaning restrooms conventionally and the self-cleaning restroom (SCR) reliably clean would allow the design of the SCR to be evaluated on an iterative and progressive basis. The initial highlights and differences derived from the initial detailed value analyses between a conventional installation and the self-cleaning conceptual approach are depicted on Figure 1.

The initial FAST diagram for the self-cleaning restroom is shown in Figure 2. For the costs per function, each functions was estimated on procurement of single components. Although a higher installation cost for the self-cleaning concept was indicated, allowances that could be made later were identified for manufacturing and the economy of scale from production purchases.

We determined that the "make or buy" decisions process for assemblies and subsystems could also be made after the manufacturing design and specifications were completed with the lessons learned from fabrication of the demonstration model.

When the prototype model and patenting were completed, brochures and a video were produced to introduce the product and establish its marketability. At this point, the inaugural value analysis for the SCR was expanded to consider all aspects of conventional versus self-cleaning restroom life cycle costs.

The investigation of preliminary and installation costs, yielded the following expense daily information.

Total $10.30

The daily net saving for self-cleaning with depreciation is $2.01 and without depreciation $6.67. The extended savings for one year {i.e., 365 days) equate to $734 with depreciation; $2,435 without depreciation. Cumulatively, over a 10 year usage, the investment return to purchasers should range from about 14 percent the first year to about 145 percent at the end of the 10th year. Refinements of the manufacturing process, components, and materials are expected to significantly reduce the cost of SCR units as production orders increase.

To define SCR fully in the context of a commercial enterprise, the following requirements and constraints were included in the analysis of the undertaking:

1. Regulatory requirements associated with provisions for the accessibility and safety of handicapped, and environmental protection.

2.. National plumbing and electrical standards that apply to all aspects of the design.

3. Financing to bring the project to a state that would interest investors, part manufacturers and vendors, and potential buyers for the ultimate product.

A significant amount of personal investment has been made in terms of time and outlay for research to gain the technology upon which the patents are based. Additional expenditures were made for hardware and components which had to be adapted

VALUE WORLD, Volume XVII, Number 2, May 1994

18

for the prototype. Additional value studies are further reducing cost. Contact has been made with fixture and fitting manufacturers. Tables 1 and 2 summarize cash flow and return-on-investment (ROI) analyses for lease and purchase of the SCR.

In the lease case, the ROI is 2 to 1 over a 10-year period. In the purchase case, the ROI is 3 to 1 over the same 10-year period; indicating the long-term advantage of purchasing over leasing the SCR.

CASE 1 CASE 2

CONVENTIONAL

RESTROOM

SELF-CLEANING

RESTROOM*

CLEANING FUNCTIONS AND COSTS

-Supplies - militias

OPERATING AND INTEGRATED CLEANING

. Supplies and UtWks

- Claaning as>*hen RaqufeBd . User Satisfaction

- Supplies - Perfunctory Labor - U s « Dissatisfaction

Figure 1 Conceptual value analyis.

OPEN SCR ENCLOSURE

DRY ENCLOSURE

DEACTIVATE CLEANING SYSTEM

DISCRETE FUNCTIONS

POWER EQUIPMENT a> CONTROLS

SPRAY ENCLOSURE

FORCE VENTILATE

ENCLOSURE

' EXHAUST DRYING AIR

SENSE DRY CYCLE

STORE/ CONTAIN

CHEMICALS

MIX HOT WATER AND CHEMICALS

DRAIN EFFLUENTS

SENSE SPRAY CYCLE

DELIVER HOT WATER

ENCLOSE AND SECURE SCR SPACE*

VERFY AVAILABILITY

OF CHEMICALS

ACTIVATE CLEANING

SYSTEM

TRANSPORT EFFLUENTS TO SEWAGE

Figure ! SCR FAST diagram

VALUE WORLD, Volume XVtl, Number 2, May 1994

19

Table 1 Financial Analysis for Leasing the SCR

Y R - i Y f t - 2 VR-3 Y R - 4 YR-5 YFt-6 YR -7 VR-B YR-9 YR-10

S C R L E A S E C O S T S5.801 $4,973 $4,973 S4.S73 $4,973 1 $1.1851 _ w/ 6% Sales Tex Allowance Purchase Optc m and Purchase Option Less - Construction Savfrig ($2,000) — — - — - - — -- —

- Sales Concession — ($150) ($750) ($750) ($750) ($750) — — — —

— Tax Savings ($2,031) #1.740) ($1,740) ($1,740) ($1,740) ($415) - - - —

® .35 x Lease Cost Net SCR kwestment - Peryear $1,771 $2,962 $2,482 $2,482 $2,482 $20 — — - —

— Cumulative $1,771 (4.753 $ 7 2 3 5 $12220 $12220 $12220 $12220

9 End of Lease Period OPERATING EXPENSE SCR Expense

- Supplies/Utilities $0.50 $0.50 $0.50 $0.50 $0.50 $0.50 $0.50 $0.50 $ 0 4 0 $0.50 - Labor® 15 mbiVday $3.13 $3.13 $313 $3.13 $3.13 $3.13 $3.13 $3.13 $3.13 $3.13

TOTAL $ 3 8 3 $3.63 $3.63 $3.83 $3.63 $3.83 $3.83 $3.63 $3.63 $3.83 Expense to Keep Non-SCR rettrooms relisbty clean per Day

— Supplies/Utilities $1.00 $1.00 $1.00 $1,00 $1.00 $1.00 $1.00 $1.00 $1.00 $1.00 - Labor <SJ 45 min ./day 1228 $9.38 $9.36 $9.36 39.36 89.38 $9 36 S&2B $9.38

TOTAL $10.36 $10.3» $10.38 $10.36 $10.38 $10.38 $10.38 $10.38 $10.36 $10.38 Net Operating Savings w/SCR

- Per Day $6.78 $6.75 $8.75 $8.75 $6.75 $8.75 $8.75 $8.78 $8.75 $6.75 - Per Year $2,463.75 $2,463.75 $2,463.75 $2,483.75 $2,463.75 $2,463.75 $2,483.75 $2,483.75 $2,483.75 $2,463.76 — Cumulative $2,463.75 $4,827.50 $7.30125 $9,635.00 $12,318.75 $14,782.50 $1724828 $18,710.00 $22,173.75 $24,637.50

N E T CASH FLOW Cumulative Savings less $ 6 9 3 $ 1 7 4 $ 1 5 6 S I 3 7 $119 S 2 . 6 6 2 $ 5 , 0 2 6 S 7 . 4 9 0 $9,953 $ 1 2 , 4 1 7 Cumulative Net Investment

Savfcigt ® End of Savings 89 E n d el S-Yr. Usee Period 1 0 - Yr. ROI Period

Return o n I n v e s t m e n t CumulaUva Savings divided 1 3 9 % 104% 1 0 2 % 1 0 1 % 1 0 1 % 1 2 1 % 1 4 1 % 1 6 1 % 1 8 1 % 2 0 2 % by Net CumulaUva Investment

Cost of SCR UnK Lease Investment in SCR Unit Paid for with Savinga returned m ore than TWICE

Table 2 Financial Analysis for Purchasing the SCR

YR-1 YR-2 Y R - I YB -4 YR-S YR-e YR-7 YR-S YR-9 YR-10

SCR PURCHASE S19.000 -' _ - _ _ _ _ _ _ Plus 6% Salt* Tax Altowanca $1,140

L n t — Construction Saving

(12.000) _ - _ - - - - _ _ — Sale* Concession — - ($1,000) ($2,000) — — — •• — —

— Tax Saving* ($1,729) (81.330) ($1,330) ($1,330) ($1330) — — — - -«3> .35 x 5-Yr. DepreelstJon $»Aeil Net SCR Investment $18,411 $15,061 $12,751 $9,421 1 $»Aeil $8,081 s»,o»i 88,091 86.091 $8,091

Cost ot SCR Unit

OPERATING EXPENSE Expense to Keep SCR reliably dean par Day

- SuppiiesAAUitMs $0.5O 80.50 $0.50 $0.50 $0.60 $0.50 $0.60 $030 $0.50 $0.60 - Labor ® 15 mlnVday 1313 83.13 $3.13 $3.13 $3.13 S3.13 $3.13 $3.13 $3.13 83.13

TOTAL $3.63 $3.63 $3.63 $3.63 83.83 $3.63 $3.63 $3.63 $3.63 $3.63 Expense to Keep Non-SCR restroom* reliabiy dean per Day

- SupptlesAJUIrttts $1.00 $1.00 $1.00 $1.00 $1.00 81J00

$1.00 $1.00 $1.00 $1.00 - Labor ® 45 minYday $9.38 89.36 $9.38 8938 89.38 8938 8938 $9.38 S&2S 89.38

TOTAL $10.38 $10.36 $10.38 $10.38 $10.36 $1038 $1038 $1036 $1038 $10.36

NET SAVINQS W/ SCR Per Day $6.75 $6.76 $6.75 $6.75 $6 75 $6.75 $6.75 $6.75 $875 $6.75 Per Yeer $2,463.75 $2,463.75 $2,463.73 $2,463.75 S2.463.7S $2,463.75 $2,483.75 $2.45375 $2,463.78 $2,463.76 Cumuiativs $2,48375 $4,917.50 $738125 $9,655.00 $12319.75 $14.76250 $1724625 $19,710.00 $22,173.75 $24,637.50

NET CASH FLOW Cumulative Savings less ( $ 1 3 , 9 4 7 ) ( $ 1 0 , 1 5 4 ) ( $ 5 , 3 6 0 ) $ 4 3 4 $ 4 , 2 2 8 $ 6 , 6 9 2 $ 9 , 1 5 5 $ 1 1 , 6 1 9 $ 1 4 , 0 8 3 $ 1 6 , 5 4 7 Cumuiltrve Net Investment

ef Cumuiltrve Net Investment

Savings g> End of Sevtnge • End ef S-Yr. Period 10-Yr. ROI Pelted

RETURN ON rNVESTMENT Cumulative Savings dIvWed 1 5 % 3 3 % 5 8 % 1 0 5 % 152% 1 8 3 % 2 1 3 % 2 4 4 % 2 7 4 % 3 0 5 % by Net Cumulative Investmant by Net Cumulative Investmant

SCR Unit PaM Investment In S C R Unit tor with Savings returned m ore then 3—TIMES

VALUE WORLD, Volume XVII, Number 2, May 1994

20

The SCR was introduced to major companies as well as to investors and material and equipment suppliers. Following the funds received from private offering, marketing the product proceeded on a national scale with a view to international expansion. On the premise that service stations have the most obvious and immediate need for the SCR, the first sales were made to AMOCO for installation in its newest service station design.

The stations with SCR have received wide media coverage, arousing a wide range of interest in potential commercial patronage by other organizations. The media showed a restroom that features wall panels that rotate in order to create a smaller enclosure. A spray of water and specially formulated detergent is applied under pressure to the wall panels and fixtures. Rinse and dry cycles follow, similar to that of a dishwasher. From the standpoint of safety, an attendant, with a special key starts the cycles so that there is no chance, nor space, for an occupant to be exposed to the 'process.

In less than 25-minutes, the rotatable wall panels are swung back into place to reveal a glistening and completely cleaned facility with most types of graffiti removed. Service station patrons were favorably impressed and the most frequently question was "When can I get an SCR for my home?"

Following the sale to AMOCO, it was time to update the value studies to reflect potential for savings in material, component and fixture procurement and to develop the plan for production of multiple restroom units.

The VE objective at this point is to achieve economies for the larger units and increased production rates associated with projected sales. The VE^study took into consideration projected sales volume and the requirements for restrooms with more than one accommodation.

CONCLUSION

Clearly, there is a lesson to be learned from the SCR story. Value engineering and analyses have a concwrent life cycle that begins with the concept, follows it through research, development, design, manufacture, ultimate installation in the field, and then allows for feed back to improve a product and its costs.

Mr. O'Rourke is President of O'Rigineering, Inc. in Granada Hills, California.

Mr. Garvey is President of Glenwood L Garvey & Associates aid Self-Cleaning Environments in Santa Monica, California

Value Briei; Converting the Industrial-Military Complex

Conversion of the industrial-military complex to civilian purposes is an ongoing issue in the Congress and state legislatures, partly because of the end of the cold war and partly because of the current budget deficit. The problem is compounded by the past approach to funding military R&D and production.

During the cold war, the Pentagon sought congressional support by spreading contracts out to as many congressional districts as possible. Many members of the Congress looked to the defense budget to provide jobs for their districts, especially in hard times.

This political engineering distorted the so-called industrial base of the nation from which to convert to civilian production. Military contractors, seeking to make the transition, face the arduous task of retooling plants, reorganizing production processes,

retraining personnel, and developing new marketing and distribution networks.

The Advanced Research Projects Agency of the U.S. Department of Defense has initiated a project called Defense Technology Conversion, Reinvestment, and Transition Assistance. The 1993 Defense Appropriations Act provides the funding for programs comprising this project but also requires transitional cost sharing by contractors.

Value practitioners may be more interested in the Small Business Innovative Research (SBIR) program that does not require transitional cost sharing by small businesses. Information on the conversion program may be obtained from the Technology Reinvestment Project, 3701 North Fairfax Drive, Arlington, VA 22203-1714.

VALUE WORLD, Volume XVII, Number 2, May 1994

VALUE ENGINEERING CONTRIBUTION TO FINANCIAL FLEXIBILITY

Arthur E. Mudge, CVS, FSAVE

BACKGROUND

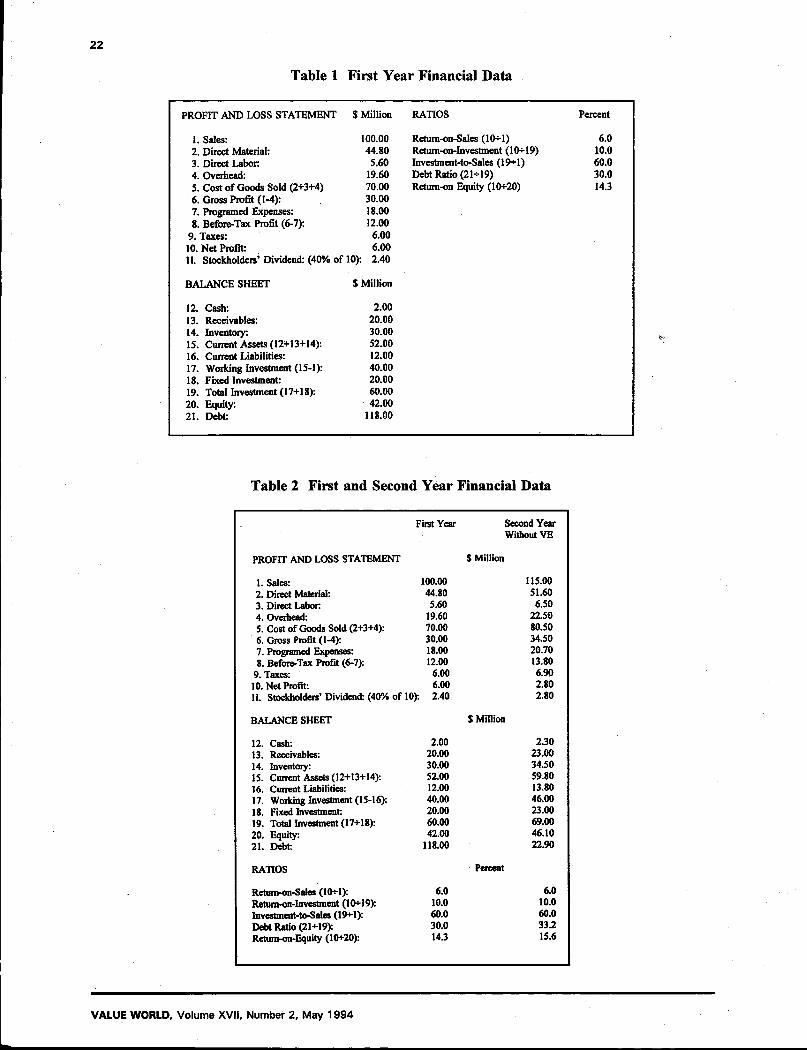

Shortly after the systematic approach of value analysis (later called cost improvement and value engineering), was born in 1947, the question that started to arise was: "What kind of financial benefits can be expected from this type of program?" This question triggered various answers from those who were involved and dedicated to' such programs. These individuals, proud of their accomplishments, answered the question quickly and honestly. For instance, the answer might have been something like this: "In our last VE study we were able to reduce product cost by $50,000." Or their answer could have been: "As the result of our VA Program, the company realized savings of a little over $5 million last year." Such answers, although truthful and to the point, do not give questioners much information to which they can relate.

The numbers may be meaningful to the individuals giving them but not necessarily to the listeners. Experience shows that people asking such questions relate much better to answers given as percentages. People can readily apply percentages to their own products in their own companies. Regarding the financial benefits of VE, a better answer would have been: "On our last VE study we were able to reduce the product cost by 3 percent. In questions regarding annual savings, a better answer would have been: "Last year, our VE program produced savings which equalled 4.15 percent of the company sales."

Percentages or ratios, such as return-on-sales, return-on-investment, investment-to-sales, debt ratio, and return-on-equity, give managers a better idea of the results they can expect from VE programs of their own. These managers can put their trust in such percentages, and therefore back VE programs with the investment of time and money. Dollar and the percentages convey the results and success of VE programs.

The more difficult question to answer is: "What is the contribution of a VE program to the overall finances of the company." This question is not an easy one to answer because it deals with the long-range effect of VE on many programs of a diverse nature.

FINANCIAL BENEFITS OF VALUE ENGINEERING

During the course of the cost improvement program at Joy Manufacturing Company, such questions were asked frequently by Operating Unit General Managers, Managing Directors, company vendors and customers, and by other companies who had heard about Joy's program. They were referred to the person best qualified to answer them, the Executive Vice President and Chief Financial Officer who was Mr. Andre R. Horn.

Mr. Horn answered such questions in the context of a hypothetical model company with the financial data given in Vable 1. The financial statement, balance sheet, and ratios in the table are similar to those of the typically successful companies of that time such as Joy Manufacturing Company.

Mr. Horn would point out that the ratios at the bottom of Table 1 are what most company managers use to measure the effectiveness of any given program. He developed these ratios through two years of operation of the model company, with and without VE, to illustrate the significant contribution of VE to a company's financial flexibility. Table 2 gives the financial data for the first and second year of operation without the benefit of VE.

The company has not yet introduced VE but, nonetheless, shows a 15 percent growth in sales. In addition, the company does show increases in the gross profit, before-tax profit, net profit, stockholders' dividend and equity. Such increases are heartily welcomed by both the management and the stockholders. The balance sheet in Table 2 also shows increases in the total investment and debt level. These increases adversely affect some of the ratios. Lurking at the end of the second year, a very serious problem begins to appear.

The first three ratios have remained the same (/.<?., Return-On- Sales, return-on-investment, and investment-to-sales) over the two years so there is no problem there. The problem lies in the debt ratio.

VALUE WORLD. Volume XVII, Number 2, May 1994

22

Table 1 First Year Financial Data

PROFIT AND LOSS STATEMENT $ Million RATIOS Percent

1. Sales: 100.00 Return-on-Sales (10+1) 6.0 2. Direct Maierial: 44.80 Return-on-investment (10+19) 10.0 3. Direct Labor 5.60 Investinent-to-Sales (19+1) 60.0 4. Overhead: 19.60 Debt Ratio (21*19) 30.0 5. Cost of Goods Sold (2+3+4) 70.00 Return-on Equity (10+20) 14.3 6. Gross Profit (1-4): 30.00 7. Programed Expenses: 18.00 8. Before-Tax Profit (6-7): 12.00

9. Taxes: 6.00 10. Net Profit: 6.00 11. Stockholders' Dividend: (40% of 10): 2.40

BALANCE SHEET $ Million

12. Cash: 2.00 13. Receivables: 20.00 14. Inventory: 30.00 15. Current Assets (12+13+14): 52.00 16. Current Liabilities: 12.00 17. Working Investment (15-1): 40.00 18. Fixed Investment: 20.00 19. Total Investment (17+18): 60.00 20. Equity: 42.00 21. Debt: 118.00

Table 2 First and Second Year Financial Data

First Year Second Year Without VE

PROFIT AND LOSS STATEMENT $ Million

1. Sales: 100.00 115.00 2. Direct Material: 44.80 51.60 3. Direct Labor: 5.60 6.50 4. Overhead: 19.60 22.50 5. Cost of Goods Sold (2+3+4): 70.00 80.50 6. Gross Profit (1-4): 30.00 34.50 7. Programed Expenses: 18.00 20.70 8. Before-Tax Profit (6-7): 12.00 13.80

9. Taxes: 6.00 6.90 10. Net Profit: 6.00 2.80 11. Stockholders'Dividend: (40% of 10): 2.40 2.80

BALANCE SHEET $ Million

12. Cash: 2.00 230 13. Receivables: 20.00 23.00 14. Inventory: 30.00 34.50 15. Current Assets (12+13+14): 52.00 59.80 16. Current Liabilities: 12.00 13.80 17. Working Investment (15-16): 40.00 46.00 18. Fixed Investment: 20.00 23.00 19. Total Investment (17+18): 60.00 69.00 20. Equity: 42.00 46.10 21. Debt: 118.00 22.90

RATIOS Percent

Return-on-Sales (10+1): 6.0 6.0 Return-on-investment (10+19): 10.0 10.0 Investment-to-Sales (19+1): 60.0 60.0 Debt Ratio (21+19): 30.0 33.2 Returns-Equity (10+20): 14.3 15.6

VALUE WORLD, Volume XVII, Number 2, May 1994

23

Despite the 15% increase in sales, the debt ratio has increased by 3.2% in just one year. This is a significant increase and shows that the company is not in financial balance. I f allowed to continue unchecked, the rate of increase could mean disaster in the not too distant future. This loss of financial balance by companies rapidly leads to the inability to borrow the operating and expansion capital.

To be conservative, Mr. Horn used the average of five years of results from Joy's cost improvement program. He then imposed these results of this successful cost improvement program on the model company.

The results are given in the third and fourth columns of Table 3. Sixty percent of savings' realized were in the direct material, 10 percent in direct labor, and 30 percent in overhead. The return-on-sales and return-on-investment have increased by 2.0 percent and 3.6 percent respectively while the investment-to-sales has decreased by 1.3 percent.

It is important to note that, because of the VE program, the 15 percent increase in sales has decreased the debt ratio. Even more important

Table 3 First and Second Year Fi:

from a management standpoint that is that the return-on-equity percentage has increased 5 percent over the first year and 3.7 percent over the second year because of the introduction of the VE program.

On several occasions, the question asked by managers was: "Those results look good when sales are steady or increasing; however, what happens i f sales are decreasing?"

Mr. Horn answered such questions by introducing a sales decrease rather than increase in the second year of the model company's operation. He then developed the profit and loss statement, balance

1 sheet, and rations for the second year with and without the benefit of a VE program..

Table 4 gives the model company's financial data with a 15 percent decrease in second year sales with and without VE. It can be noted that even with a sales decrease, VE has improved the company's financial situation. Gross profit, before-tax profit, net profit, and stockholders' dividend have increased. Total investment and debt are reduced while the equity is greater.

lancial Data with and without VE

Second Year Effect of VE Second Year Without VE With VE

PROFIT AND LOSS STATEMENT $ Million

1. Sales: 100.00 115.00 115.00 2. Direct Material: 44.80 51.60 (2.76) 4J.74 3. Direct Labor 5.60 6.50 (0.46) 6.04 4. Overhead; 19.60 22.50 (UJ) 21.12 5. Cost of Goods Sold (2+3+4): 70.00 80.50 (4.60) 75.90 6. Gross Profit (1-4): 30.00 34.50 4.60 39.10 7. Programed Expenses: 18.00 20.70 27.00 S. Before-Tax Profit (6-7): 12.00 13.80 4.60 11.40

9. Taxes: 6.00 6.90 2.30 9.20 10. Net Profit: 6.00 6.90 230 9.20 11. Stockboldera'Dividend: (40% of 10): 2.40 2.80 0.90 3.70

BALANCE SHEET S Million

12. Cash: 2.00 230 230 13. Receivables: 20.00 23.00 23.00 14. Inventory: 30.00 34.S0 (2.00) 3230 15. Current Assets (12+13+14): 52.00 ' 59.80 (2.00) 57.80 16. Current Liabilities: 12.00 13.80 (030) 1330 17. Working Investment (I5-16> 40.00 46.00 (130) 44.50 18. Fixed Investment 20.00 23.00 23.00 19. Total Investment (17+18): 60.00 69.00 (1.50) 6730 20. Equity: 42.00 46.10 1.40 4730 21. Debt 18.00 22.90 (2.90) 20.00

RATIOS Percent

Retam-co-Sales (10+1): RetenvOD-lavestment (10+19): InvestmcnMo-Sabs (19+1): Debt Ratio (21+19): Retunwjo-Eotuty (10+20):

SAVINGS AS A PERCENTAGE OF SALES

6.0 6.0 2.0 1.0 10.0 10.0 3.6 13.6 60.0 60.0 (13) 517 30.0 33.2 (3.6) 29.6 143 15.6 3.6 193

Five-Yeer Average: 4.01 Percent Savings Distribution

Material: 60 Percent Labor. 10 Percent Overhead: 30 Percent

VALUE WORLD, Volume XVII, Number 2, May 1994

24

Table 4 First and Second Year Financial Data with Decreased Sales and with and without

First Year Second Year Effect of VE Without VE

Second Year With VE

PROFIT AND LOSS STATEMENT $ Million

1. Sales: 1° 0 0 0

2. Direct Material: 4 4 8 0

3. Direct Labor: 5.60 4. Overhead: 1 9 6 0

5. Cost of Goods Sold (2+3+4): 70.00 6. Gross Profit (1-4): 30.00 7. Programed Expenses: 18 0° 8. Before-Tax Profit (6-7): 12.00 9. Taxes: «•« 10. Net Profit: 6 - 0 0

11. Stockholders' Dividend: (40% of 10): 2.40

85.00 38.08

4.76 16.66 59.50 25.50 15.30 10.20 S.10 5.10 2.40

(2.04 (0.34) (1.02) (3.40) 3.40

3.40 1.70 1.70 0.68

85.00 36.04 4.42 15.64 56.10 28.90 15.30 13.60 6.80 6.80 2.72

BALANCE SHEET S Million

12. Cash: 13. Receivables: 14. Inventory: 15. Current Assets (12+13+14): 16. Current Liabilities: 17. Working Investment (15-16): 18. Fixed Investment 19. Total Investment (17+18): 20. Equity: 21. Debt:

2.00 20.00 30.00 52.00 12.00 40.00 20.00 60.00 42.00 18.00

1.70 17.00 25.50 42.20 10.20 34.00 20.00 54.00 45.06 22.90

(1.50) (1.50) (0.60) (0.90)