Vade-mecum on grants - europafacile.net¹/BandoEAC10_04/vadem_sub_en... · The purpose of the...

68

- 1 - VADESUBV_EN010799.DOC EUROPEAN COMMISSION VADE-MECUM ON GRANT MANAGEMENT Version 1.8. 2000

-

Upload

truongthuy -

Category

Documents

-

view

226 -

download

1

Transcript of Vade-mecum on grants - europafacile.net¹/BandoEAC10_04/vadem_sub_en... · The purpose of the...

- 1 -

VADESUBV_EN010799.DOC

EUROPEAN COMMISSION

VADE-MECUM ON GRANT MANAGEMENT

Version 1.8. 2000

- 2 -

FOREWORD

Grants account for an important part of Community expenditure. They give theCommunity a flexible instrument adapted to its objectives in the different areas ofCommunity policies. But the Community also depends on the active participation andinvolvement of civil society at large in pursuing its policy objectives.

Outside institutions sometimes perform functions of general European interest. Heregrants can offer an efficient method of promoting EU policy aims. Altogether, suchinstitutions and organisations committed to the project of European construction have animportant role to play.

Managing public funds always carries a special responsibility. Not only must thetaxpayer’s money be spent in a judicious and economic way, but spending decisions mustalso obey sound rules which are transparent to the public and to potential beneficiaries.Grant management is a particularly sensitive area, given the fact that the Communitydoes not receive a full market equivalent for its expenditure.

Setting sound and transparent standards for the management of Community funds hasbeen a priority of this Commission from the very outset. This was the ambition thatprompted us to embark on the task of drafting a Vade-mecum that would provide theCommission with a common framework for awarding and monitoring direct grants andthat could be applied in any policy area where there are no sector-specific rules.

The purpose of the Vade-mecum, then, is to serve as a reliable reference guide for usersconfronted by the many issues that arise in the day-to-day management of grants. It isbased on extensive interdepartmental consultation throughout its drafting in order toreconcile operational and financial demands.

Proper observance of the rules and recommendations contained here will facilitate theimplementation of spending decisions. At the same time, the Vade-mecum will also serveas a reference guide for explaining the Commission’s policy to the budget authority, theEuropean Court of Auditors, and the public at large.

Anita Gradin Erkki Liikanen

July 1998

- 3 -

VADE-MECUM ON GRANT MANAGEMENT

TABLE OF CONTENTS

1. INTRODUCTION..................................................................................................... 10

1.1. Purpose of the Vade-mecum............................................................................ 10

1.2. How to use the Vade-mecum........................................................................... 10

1.3. What is a grant? ............................................................................................... 11

1.4. Expenditure coding table................................................................................. 13

1.5. Compulsory procedures ................................................................................... 14

1.5.1. Programming and publicising grants ................................................. 14

1.5.2. Transparent award procedures........................................................... 14

2. PROPOSING OR RENEWING PROGRAMMES................................................... 16

2.1. Defining objectives.......................................................................................... 16

2.2. Ex ante evaluation of programmes .................................................................. 16

2.3. Defining the rules for awarding grants under a particular programme............ 17

2.4. Programme budgeting...................................................................................... 17

2.5. Spontaneous grants .......................................................................................... 18

3. PUBLICISING GRANT PROGRAMMES............................................................... 19

3.1. General publicity ............................................................................................. 19

3.1.1. Addendum to “Grants and loans from the European Union”............ 19

3.1.2. Other .................................................................................................. 19

3.2. Specific publicity............................................................................................. 19

3.2.1. Call for Proposals .............................................................................. 19

3.2.2. Media for calls for proposals ............................................................. 20

- 4 -

4. CRITERIA FOR ACCEPTING APPLICATIONS AND AWARDINGGRANTS................................................................................................................... 21

4.1. Professional ethics ........................................................................................... 21

4.1.1. The service ethic................................................................................ 21

4.1.2. Quality of service............................................................................... 21

4.2. Reaching a wide range of beneficiaries ........................................................... 22

4.3. Sound financial management........................................................................... 22

4.4. Selection criteria .............................................................................................. 22

4.4.1. Treatment of incomplete applications ............................................... 22

4.4.2. Eligibility of applicants ..................................................................... 22

4.4.3. Applicants’ financial capacity to complete the proposedoperation ............................................................................................ 24

4.4.4. Applicants’ technical capacity to complete the proposedoperation ............................................................................................ 25

4.5. Award criteria .................................................................................................. 25

4.5.1. Operations must match the objectives defined by theCommission, including the requirement that Communityfunding be publicised......................................................................... 25

4.5.2. The expected results of the operation must further the policyobjective of the programme............................................................... 26

4.5.3. The operation must be of sufficiently high quality............................ 26

4.5.4. The operation must be cost-effective................................................. 26

4.5.5. The operation must not be the subject of a procurementprocedure ........................................................................................... 26

4.5.6. The operation proposed by the applicant must not receivedouble financing ................................................................................ 26

4.5.7. Operations for which an application has been made must not,as a rule, have started yet ................................................................... 27

4.5.8. Proposed operations which, directly or indirectly, conflictwith the policies of the Union or may be linked with anunsuitable image must be rejected..................................................... 27

- 5 -

5. PROCEDURE FOR AWARDING GRANTS .......................................................... 28

5.1. Composition of examining committees........................................................... 28

5.2. Operation of committees ................................................................................. 28

5.3. Avoiding multiple funding for the same operation ......................................... 28

6. FINANCIAL MANAGEMENT RULES APPLICABLE BYDEPARTMENTS REGARDING GRANTS ............................................................ 30

6.1. Rules concerning the budget of the operation assisted.................................... 30

6.1.1. The applicant’s forward budget ......................................................... 30

6.1.2. Revenue ............................................................................................. 30

6.1.3. Eligible costs ..................................................................................... 30

6.1.3.1. Direct costs eligible ........................................................... 31

6.1.3.2. Indirect costs and overheads eligible................................. 32

6.1.4. Ineligible costs ................................................................................... 32

6.1.5. Contributions in kind......................................................................... 33

6.1.6. The agreed budget.............................................................................. 34

6.2. Calculating the amount of the grant ................................................................ 35

6.2.1. On the basis of the forward budget.................................................... 35

6.2.2. On the basis of the final accounts...................................................... 36

6.3. Special rules applicable to running costs grants .............................................. 37

6.3.1. Limitation on the award of running costs grants ............................... 37

6.3.2. Costs eligible for running costs grants .............................................. 38

6.3.3. Time limit for introducing an application.......................................... 38

6.3.4. Rule governing surpluses................................................................... 38

6.3.5. Principle of setting a ceiling on this type of grant as aproportion of the beneficiary’s annual running costs in orderto limit dependence on the Community budget................................. 39

6.3.6. Start-up grants and three-year limit for a single beneficiary ............. 39

- 6 -

7. RULES RELATING TO THE GRANT AGREEMENT BETWEEN THECOMMISSION AND THE BENEFICIARY............................................................ 40

7.1. Provisions to be included in the agreement proper.......................................... 40

7.1.1. Beneficiary......................................................................................... 40

7.1.1.1. Full legal name .................................................................. 40

7.1.1.2. Address .............................................................................. 41

7.1.1.3. Name and function of the signatory................................... 41

7.1.2. Subject matter (Article 1) .................................................................. 41

7.1.3. Duration (Article 2) ........................................................................... 41

7.1.3.1. Duration of the operation in months.................................. 41

7.1.3.2. Starting date of the operation ............................................ 41

7.1.4. Financing the operation (Article 3).................................................... 41

7.1.5. Payment arrangements (Article 4) ..................................................... 42

7.1.6. Reports and other documents to be submitted by thebeneficiary (Article 5)........................................................................ 42

7.1.7. General administrative provisions (Article 6) ................................... 42

7.1.8. Annexes to the agreement (Article 7)................................................ 42

7.1.9. Final provisions ................................................................................. 42

7.2. General terms and conditions .......................................................................... 42

7.2.1. Part A - Legal and administrative provisions .................................... 43

7.2.1.1. Performance (Article 1) ..................................................... 43

7.2.1.2. Liability (Article 2)............................................................ 43

7.2.1.3. Conflict of interest (Article 3) ........................................... 43

7.2.1.4. Termination of the agreement (Article 4).......................... 43

7.2.1.5. Confidentiality (Article 5) ................................................. 43

7.2.1.6. Visibility (Article 6) .......................................................... 43

7.2.1.7. Ownership/use of results (Article 7).................................. 44

- 7 -

7.2.1.8. Interim/ex post evaluation of the operation (Article8)........................................................................................ 44

7.2.1.9. Amendment of the agreement (Article 9).......................... 44

7.2.1.10. Jurisdiction (Article 10)..................................................... 44

7.2.2. Part B - Financial provisions ............................................................. 44

7.2.2.1. Eligible costs (Article 11).................................................. 44

7.2.2.2. Statements of costs and repayment arrangements(Article 12) ........................................................................ 44

7.2.2.3. Interest on late payment (Article 13) ................................. 44

7.2.2.4. Technical and financial control (Article 14)...................... 45

7.2.2.5. Repayment of the grant (Article 15).................................. 45

8. MONITORING AND AUDIT .................................................................................. 46

8.1. Monitoring....................................................................................................... 46

8.1.1. Purpose .............................................................................................. 46

8.1.2. Monitoring tools ................................................................................ 46

8.2. Audit ................................................................................................................ 46

8.2.1. General audit objectives .................................................................... 46

8.2.2. Planning the audit .............................................................................. 47

8.2.2.1. Selecting the beneficiaries to be examined duringon-the-spot audits .............................................................. 47

8.2.2.2. Preparatory work before the audit mission........................ 48

8.2.3. On-the-spot examination and testing of systems ............................... 48

8.2.4. Audit reports ...................................................................................... 48

8.3. Recovery of debts ............................................................................................ 49

9. EVALUATING THE RESULTS OF PROGRAMMES ........................................... 51

9.1. Evaluation process........................................................................................... 51

9.2. Evaluation of small programmes..................................................................... 52

- 8 -

9.3. Planning and periodicity of evaluations .......................................................... 53

10. EX POST PUBLICITY.............................................................................................. 54

10.1. Obligation to publish a list of grants awarded................................................. 54

10.2. Scale of ex post publicity................................................................................. 54

10.3. Methods of ex post publicity ........................................................................... 54

ANNEXES ........................................................................................................................ 55

1. STANDARD GRANT APPLICATION FORM ....................................................... 56

1.1. Particulars of grant applicant........................................................................... 56

1.2. Particulars of operation for which a grant is requested ................................... 58

1.3. Supporting documents to be included with the grant application ................... 61

1.3.1. Documents to be included with all grant applications....................... 61

1.3.2. Documents to be included where available ....................................... 61

2. CROSS-CHECKING INFORMATION OBTAINED FROM APPLICANTSWITH OTHER SOURCES OF INFORMATION .................................................... 62

2.1. Identifying departments likely to hold information about an applicant........... 62

2.1.1. Finding all payments made to a payee............................................... 62

2.1.2. Finding all commitments made to a payee ........................................ 62

2.1.3. Finding all managing departments..................................................... 62

2.2. Detailed review of the situation of an applicant already entered inSINCOM.......................................................................................................... 62

2.2.1. Identifying links between different payees ........................................ 62

2.2.2. Identifying the position of payees as regards the recovery ofsums owed ......................................................................................... 63

2.2.3. Identifying secondary beneficiaries ................................................... 63

- 9 -

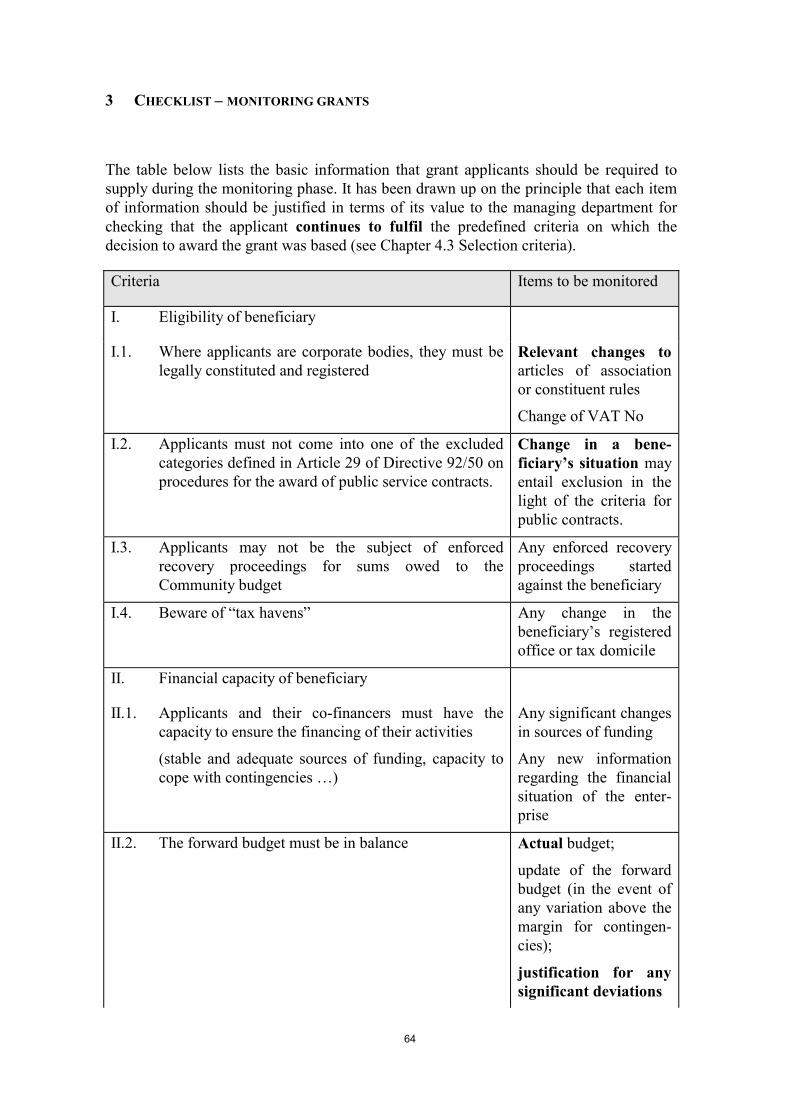

3. CHECKLIST – MONITORING GRANTS............................................................... 64

4. CHECKLIST – AUDITING GRANTS..................................................................... 66

5. GRANT AGREEMENT................................................................................................

5.1. Model agreement .................................................................................................

5.1.1 Grants for specific operations……………………………………………

5.1.2 Grants for running costs………………………………………………….

5.2. General terms and conditions applicable to grant agreements of theEuropean Communities .......................................................................................

5.2.1 Grants for specific operations……………………………………………

5.2.2 Grants for running costs………………………………………………….

5.3. Model Financial Guarantee .................................................................................

5.4. Model Recovery Decision ...................................................................................

- 10 -

1 INTRODUCTION

1.1 Purpose of the Vade-mecum

The purpose of the Vade-mecum is to provide an easy-to-follow referenceguide for all those involved with grants, whether drawing up, proposing, orevaluating programmes or processing individual applications. As regards therecommendations and procedural rules set out here, it is taken as read thatCommission officials should coordinate across departments. This coversconsultation on a wide range of horizontal matters, be it implementing theVade-mecum or simply the day-to-day business of administering grants. Togive some examples, such matters would include consulting SCIC on thecost of conferences, checking beneficiary’s records in the Early WarningSystem, or adding to the general list of beneficiaries that receive corefunding from the Community budget.

Better prior publicity and the use of a standard application form, standardagreement, and other documents appended to the Vade-mecum should helpto prevent unnecessary consultations on financial and legal issues bothamong Commission departments and with beneficiaries.

The Vade-mecum is founded on experience and therefore can and shouldevolve in response to users’ practical concerns. Your personal involvementin further improving the Commission’s management standards will be mostwelcome.

1.2 How to use the Vade-mecum

The Vade-mecum comprises two kinds of rules:

– binding procedural rules that constitute the basic rules which managingdepartments must follow, and

– optional recommended managerial practices. These are intended tostandardise practice in Commission departments as far as possible and tohelp managing departments in their day-to-day work.

Both the rules and recommended managerial practices should be seen asprinciples for authorising departments to follow as lines of conduct.However, they are of course free – within the framework of the Vade-mecum- to adopt stricter – but not looser – standards as they see fit. The minimumprocedures that must always be observed are summarised below, at point 1.5of this chapter.

The ten chapters into which the Vade-mecum is divided reflect the variousstages of the process from drawing up a programme, deciding to award agrant, through to evaluating and publicising the results.

- 11 -

1.3 What is a grant?

Commission spending, as shown in the Expenditure coding table at the endof this section (What is a grant?), is broken down into the followingcategories:

(a) Spending on personnel

(b) Loans and participations

(c) Procurement spending, i.e. purchasing on the market a service orproduct, as defined in the procurement Directives and the FinancialRegulation

(d) Financial aid to promote a policy aim:

(i) paid to the beneficiary directly by the Commission (“grant”,sometimes also called “financial contribution”, “subsidy” etc.)

(ii) paid to the beneficiary indirectly via a Member State, via a foreigngovernment, or via a body designated by a State, in the context ofthe decentralised management of Community activities(“transfer”).

A grant is therefore a direct payment of a non-commercial nature by theCommission to promote an EU policy aim. Where such a payment is made toa government department in connection with a specific project, it issometimes called a “financial contribution”. However, as this distinction isnot relevant to the management principles set out in this Vade-mecum, it isnot made in the rest of this document nor is any difference made between“subsidy” and “financial contribution” in the Expenditure coding table.

The Vade-mecum is not concerned with financial aid granted via States orvia bodies designated by them (“transfers”), as for instance under the CAPand the Structural Funds. Procurement spending is only discussed to theextent that it is not permissible to use a grant to purchase services or goods.Where that is the purpose, the procurement rules apply.

In practice, the borderline between grants and procurement spending issometimes difficult to draw.

An operation of a non-commercial nature must not result in financial benefitfor the recipient. The recipient’s legal form and statutes will generallyprovide an indication of whether an operation is commercial or non-commercial. However, exceptions exist: Commercially oriented groupingsmay choose non-profit status for some of their activities and commercialenterprises may, exceptionally, engage in non-commercial activities.

To decide whether an operation’s primary aim is to promote an EU policy,the following three indicators should be looked at:

- 12 -

1. Primary interest: If the subject matter of the contract lies primarily inthe Commission’s administrative interest, the transaction has to beclassified as procurement spending. Mixed cases also have to betreated as procurement spending.

2. Degree of Community financing towards the cost of the operation:Full (100%) financing by the Commission will point to procurementspending, co-financing to a grant. However, there are also exceptions:procurement contracts may be financed jointly (e.g. with MemberStates), and eligible costs may be fully financed in justified cases.

3. Ownership: Is it the Commission or the recipient who owns theresult? The first case is typical for procurement spending, the secondfor grants. However, there may be some cases where the situation liessomewhere “in-between”.

Grants can be further divided into those governed by a Regulation whichincludes provisions on the award procedure (“regulated grants”) and thosethat fall either under a Regulation containing no such provisions or under nospecific Regulation at all. These used to be known as “non-regulated grants”.They are now governed by the rules set out in this Vade-mecum).

The Vade-mecum applies to “regulated grants” (such as the frameworkprogramme for research and technological development) only where thespecific regulations do not define management procedures. Where specificregulations exist, these apply even where they differ from the proceduresdescribed in this Vade-mecum.

Grants are generally part of a programme of related activities in pursuit of aparticular policy aim. The term “programme” as used in the Vade-mecum isto be taken to mean not only multiannual programmes involving grants butalso annual budget headings.

A “spontaneous grant” is a grant whose award is not preceded by a call forproposals or by publicity other than that such grants may be awarded.

The table below shows the criteria by which the different types ofCommunity spending are classified, serving as a guide for authorisingofficers before they book expenditure to the budget in SINCOM.

- 13 -

1.4 Expenditure coding table

EXPENDITURECATEGORY

RECIPIENT OWNERSHIP FINANCING FINANCIALBASE

PURPOSEACTIVITIESCOVERED

DIRECTEXPENDITUREMANAGEMENT

Govern-mental1

Privatenon-profit

Commer-cial

Commission Co-financing2

1. FINANCIAL AID

1.1 Grants

1.1.1. Spontaneousgrants3

N/Y Y 4 N/Y N Y 5 Cost Promotion Non-Commercial

Commission

1.2 Transfers6 Y N N N Y 5 Cost Promotion Non-Commercial

MS

2. LOANS ANDPARTICIPATIONS

Y Y Y N Y 5 Cost Promotion Any Comm. or MS

3. PUBLICPROCUREMENT

N Y Y Y N 5 Price Acquisition forCommission’sown purposes

Commercial Commission

4. PERSONNELEXPENDITURE

• • • Y • • Implement-ation

Tasks of theinstitution

Commission

1 Excluding public-sector enterprises, universities etc., which are considered as private.2 Co-financing of the activity.3 Defined as grants whose award is not preceded by a call for proposals or equivalent ex ante publicity.4 Acceptable if the action’s immediate objective is non-profit making.5 Typical case.6 Grants paid to beneficiaries indirectly via a Member State, a foreign government or a body designated by a State, in the context of decentralised management of Community

activities.

14

1.5 Compulsory procedures

The basic binding rules of the Vade-mecum can be summarised as follows:

1.5.1 Programming and publicising grants

The availability of grants must be publicised widely and in an easilyaccessible way. They should be cited on “Europa”, theCommission’s Internet server, mentioning the programme, its scopeand size, and where to address applications. It should be possible toobtain information, as well as an updated version of the publication“Grants and loans from the European Union” both through Europaand in print.

The criteria for awarding grants must comply with this rule on wideaccess1. While limiting the target population for grants is necessaryto achieve a measurable impact, this must not rule out previouslyunknown or new applicants. Thus targeting should be achieved byclearly defining the purpose of grants, as derived from the policygoals and desired impact.

1.5.2 Transparent award procedures

The following three principles must be observed when awardinggrants:

– Collective assessment

Proposals must be selected by a committee of Commission staff,with at least one member who does not belong to the unitawarding the grant. The committee acts independently in anadvisory capacity. Minutes of its meetings should be taken andsigned by all the members. If necessary advice from outsideexperts may be sought, depending on the technicality of aproposal. They will have to give a formal declaration that they donot stand to benefit in any way from the grant and are notassociated with it in any way. They must observe strictconfidentiality regarding the committee’s deliberations. Theauthorising officer takes the final award decision.

– Avoiding double funding for the same operation

Before making an expenditure commitment proposal authorisingofficers must take reasonable steps to check there is no doublefunding for the same operation and must create a third-partyrecord if none already exists.

– Ex post publicity

1 See “4.2”.

15

A list of all grants awarded should be published at least once ayear, giving the names and geographical locations of thebeneficiaries, what the grants were for, the amount granted andthe co-financing rate, and whether or not there was specific priorpublicity (such as a call for proposals). The only exceptionsallowed are where the beneficiary’s security would bejeopardised.

16

2 PROPOSING OR RENEWING PROGRAMMES

This chapter is intended for those responsible for proposing or renewingprogrammes involving the payment of grants for individual projects ororganisations. In this context, a programme may be just one single budget heading.

Awarding grants without any programming, solely in response to initiatives byapplicants, is completely against sound financial management principles.

2.1 Defining objectives

Proposals to allocate resources for subsidising particular activities ororganisations should be linked to policy priorities and based on a clearjustification of the need for Community financial support. They should alsospecify the results to be expected from Community involvement, preferablyin measurable and at least in verifiable terms. At the outset of a subsidyprogramme it is also important to provide for systematic monitoring of theachievement of these results.

For multiannual programmes, objectives are specified and monitoring andevaluation systems set up at the stage when a programme or renewal of anongoing programme is being proposed. Information on these is included inthe annual budget documents. For grants decided annually, objectives arespecified and evaluation arrangements defined in the documentsaccompanying the budget proposal.

2.2 Ex ante evaluation of programmes

Ex ante evaluation or appraisal of programmes should preferably be carriedout when Community measures involving grants are being planned or whenrenewal of a programme or budget heading is being proposed.

Such evaluations should:

• ask questions about the relevance and effectiveness of providing thegrants;

• identify the target group and the number of potential beneficiaries;

• assess to what extent achieving the programme’s objectives is feasible;

• list possible alternative measures through which these objectives could bepromoted.

• define indicators to be used for monitoring the implementation and resultsof the programme, and design the system for collecting monitoring data.

The most important product of ex ante evaluation should be a clear andreasoned description of the logic behind intervention, i.e. of the link betweenthe grants and their expected impact in terms of the objectives of theprogramme. Another important outcome at this stage will be a monitoring

17

plan, which should include a set of predefined indicators and a method tocollect the relevant data. These indicators should cover essential features ofprogramme implementation, such as the number of projects, types ofactivities funded, number of participants, etc. Without these initialpreparations later evaluation of the success of the programme will bedifficult.

For major new expenditure programmes, external ex ante evaluation isrecommended. In more routine cases or where the financial implications areless significant, internal assessment is sufficient. The effort devoted toevaluation should be proportional to the expenditure involved. In the case ofprogrammes being renewed, the mid-term evaluation results for the previousgeneration of the programme can usually be used.

2.3 Defining the rules for awarding grants under a particular programme

A programme needs to have clearly defined criteria for deciding whichparticular requests or proposals for a grant are eligible, and which of thosethat are eligible should be given a grant.

Defining award criteria should be based on adequate information about thepotential beneficiaries. Information about which groups are being targetedbecause of their contribution towards achieving the programme objectivesshould form part of the ex ante evaluation of the programme.

Selecting and finding the right target group is crucial if a programme is toattain its objectives. Before defining the award criteria you need to know:

(1) which attributes of the target group contribute to the objectives;

(2) what are the needs and motivations of the target group;

(3) what is the size of the target group;

(4) how to prioritise different categories of applicants (unless thepurpose is to cover the whole target group);

(5) which categories are to be excluded, for instance because of risks orlegal problems;

(6) what is the right level or proportion of grant for achieving theexpected results.

2.4 Programme budgeting

A budget proposal should not simply provide a justification for the generalprinciple of supporting certain activities or organisations. It should include atransparent calculation setting out the estimated number of beneficiaries andthe estimated average individual grant.

18

The revised financial statement introduced for the 1999 budget procedureprovides a general model for calculating the amount of appropriationsproposed for each budget heading:

(1) the measure or programme financed by a budget heading should bebroken down by its specific objectives;

(2) each of these objectives should be broken down into the activities tobe carried out to achieve them;

(3) for each of these activities an estimated volume of measurable resultsand an average unit cost should be presented so as to be able tocalculate the financing needed.

Applying this model means that realistic estimates of the number ofbeneficiaries and of the average amount of grant for the different categoriesof beneficiaries are needed. Ideally, a basis for these estimates is provided byanalysing information from earlier years. In the case of new programmes, theex ante evaluation should give some indication.

2.5 Spontaneous grants

Most projects financed under a given budget should be specified in advancethrough a call for proposals. However, in policy areas where innovativeideas and pilot projects play a particular role it may be appropriate for alimited portion of the total budget to be earmarked for proposals receivedspontaneously. In such cases a grant could be awarded without priorpublication of a call for proposals. To provide a programming framework,the possibility of grants being awarded in response to spontaneousapplications must be announced when the managing department informs thetarget population of the broad lines of the programme.2 However, allspontaneous grants must be indicated as such in the ex post publicityexercise.

2 See “General publicity”.

19

3 PUBLICISING GRANT PROGRAMMES

Grant programmes should be publicised as early as possible to inform potentialcandidates that grants are available and make it easier for them to respond to callsfor proposals. This is especially important for small organisations or where thegrants require setting up a network of partners.

It is vital that all information about programmes involving grant awards should bespecially designed for the general public and written in a clear and easilyunderstandable style so that potential applicants will be able to fill in the formsthemselves without needing to seek professional help.

3.1 General publicity

3.1.1 Addendum to “Grants and loans from the European Union”

On the basis of each year’s budget, all departments should prepare alist of the grants they can give, the amounts involved, and thecriteria for awarding them. These lists will then be included in acompendium setting out what grants are available from eachdepartment; if a department can award spontaneous grants thisshould be stated. The compendium will form an addendum to“Grants and loans from the European Union” and will be publishedon Europa, as well as being available in paper form.

3.1.2 Other

When issuing publications describing a Community programme,departments should make sure to include a section givinginformation on the subsidies planned under the programme.

They should also take steps to maintain ongoing visibility in thepress, in Commission Offices in the Member States, in the MemberStates’ Permanent Representations to the Union and in officesrepresenting national regions/Länder/provinces in Brussels, as wellas in Commission delegations in countries outside the Union.

3.2 Specific publicity

Although prior publicity should be the rule, it is not necessary where thebudget heading specifically indicates the beneficiaries.

3.2.1 Call for Proposals

A call for proposals is normally the most appropriate means ofpublicising a particular programme of grants. It must be carefullyworded so as to preclude a flood of applications likely to be rejectedsubsequently. Calls for proposals should therefore clearly set out thefollowing information:

– the context;

20

– the subject of the call for proposals;

– the total budget available for the programme;

– the likely number of beneficiaries (and hence the average amount of anygrant);

– the scale of Commission participation in percentage terms;

– whether or not contributions in kind are to be taken into account whencalculating the grant;

– the maximum amount of any grant;

– the rules governing which organisations and operations are eligible forassistance;

– the selection criteria for operations;

– the rules governing which categories of expenditure are eligible andwhich are not;

– the rules to be applied for evaluation (ex ante and ex post), monitoringand controls (technical and financial);

– the deadlines applicable;

– general arrangements for submitting applications for grants.

3.2.2 Media for calls for proposals

A call for proposals can be publicised in a number of ways:

– through the Official Journal of the European Communities;

– via the Europa web site;

– by sending it to preselected potential applicants in the light of theirresponse to a preliminary announcement or by targeted mailshots (e.g. forrecurrent subsidies);

– through publicity in the specialist press in certain cases;

– through special brochures and/or leaflets.

Dissemination via the Internet, with a link to the web page “Grantsand Loans from the European Union” is the minimum requirement.The choice of other media depends on which target groups theprogramme is aimed at.

21

4 CRITERIA FOR ACCEPTING APPLICATIONS AND AWARDING GRANTS

This chapter is aimed at those dealing with individual applications for grants under aparticular programme. It deals with the criteria for deciding which applications areeligible for consideration and which eligible applications are actually to be awardeda grant.

4.1 Professional ethics

Officials who handle subsidies are in constant contact with the public. Theiraccessibility, competence and courtesy therefore play a part in shaping theCommission’s public image. To help them provide high-quality servicewhile still complying with their specific obligations, they should consult the“Code of conduct for officials in their relations with the public”. This setsout the ethical principles that should underlie their work as well as practicaladvice to help them improve the quality of the service they offer the public.The code is available on EUROPA-Plus.

4.1.1 The service ethic

Loyalty: Whenever officials have to take account of differentinterests, they should assess each case bearing the Communityinterest in mind.

Independence: Officials must not allow their attitude to be alteredby outside influences. This means that they must not accept anyoutside offers (gifts, decorations) without prior authorisation fromtheir superiors. They must also inform their superiors if they have apersonal interest in a matter entrusted to them. Such an interest maybe direct or indirect, for example through a member of their family.Under the Staff Regulations officials are obliged to inform theinstitution if their spouse is in gainful employment. Officials shouldalways be on their guard against actual or potential conflicts ofinterest.

Duty to observe discretion: Officials must seek to balance the needfor discretion in divulging information and documents and the needfor greater transparency. They must not inform potentialbeneficiaries of the award of financial support until after a decisionhas been taken. However, they may tell potential beneficiaries whatstage in the procedure their application has reached. Officials mustalso take care not to divulge information about other applicants toanyone else.

4.1.2 Quality of service

In practice, high quality service will flow from careful and fairtreatment and monitoring of all grant applications (the name andtelephone number of the official responsible for a case should beindicated in all correspondence). The public expect all applications

22

to be dealt with swiftly, especially bearing in mind the inevitableorganisational constraints which beneficiaries face.

4.2 Reaching a wide range of beneficiaries

Grant management should make it possible to select beneficiaries on thebasis of the quality of their applications. Thus the beneficiaries will notalways be the same. The rules on ex ante and ex post publicity andapplication of the procedures described below will ensure that the range ofbeneficiaries gaining access to Community funds is as wide as possible.

4.3 Sound financial management

A number of criteria have to be considered when selecting beneficiaries forany grant, whatever the programme in question. The information requiredfrom grant applicants in order to undertake this examination is given in thestandard grant application form, reproduced in Annex 1.

The quantity and detail of the information required should be chosen withcost-effectiveness in mind. You should consider how useful it will be forprocessing the application, what capacity Commission departments(especially resources units/directorates) have to carry out any checksnecessary and to process the information, and what will be the cost of doingso, as well as the cost to the applicant of producing the information.

4.4 Selection criteria

4.4.1 Treatment of incomplete applications

An application should be considered incomplete not just if it is notsigned, for instance, or if not all the questions on the applicationform have been answered, but also if it is not accompanied by abalanced budget (income and expenditure), an adequate descriptionof the activity or project in question or the organisation’s statutes orequivalent, if this is required. However, departments are free to askfor and accept any additional information they think necessary.

4.4.2 Eligibility of applicants

As a rule, grants are awarded so that applicants will carry outoperations, and this involves certain rights and obligations on them.It is therefore important to know that applicants have the properlegal status to meet those obligations and can provide assurances asto their financial viability and professional integrity, guaranteeingthat they can complete the operation for which a grant is given.

• Corporate bodies must be properly constituted and registered under thelaw

To ensure that applicants are properly constituted under the law,they must be asked in the application form to give their business

23

name (full legal title), official registration number whereappropriate, legal status (association, commercial enterprise,university etc.) and VAT number. For verification purposes, it isadvised that they be asked to enclose with their application a copyof their articles of association or statutes and, where appropriate,of their official registration certificate.

• Eligibility of natural persons

Awards of grants to natural persons are not ruled out altogether,but they should be made only in special circumstances. In thiscase the person must accept individual responsibility forcompleting the operation for which a grant is given. Requesting afinancial guarantee may be considered in order to protect theCommunity’s financial interests.

• Eligibility of commercial organisations

In the case of commercial enterprises, procurement proceduresrather than grant award procedures should be the rule andmanaging departments must always consider first whether theprocurement procedure applies. In any event, a grant to acommercial organisation can only be made for a project whoseimmediate objective is non-commercial and strictly non-profit-making. The award of Community grants must always complywith Community competition policy rules.3

• Eligibility of intermediary agencies

Applications by agencies acting as intermediaries on behalf ofothers are not permitted, apart from duly authorised exceptionssuch as projects grouped in a single application.

• Applicants must furnish evidence of adequate legal status, financialviability and professional integrity to complete the project or activity forwhich a grant is given

• Applicants in any of the categories excluded from participating inprocurement contracts cannot be considered4

Departments also have the option of consulting outsidecommercial databases that may be able to provide usefulinformation on an applicant’s legal status or financial viability(insolvency, bankruptcy).

3 A conflict could arise if a major grant (above the de minimis threshold of competition policy) involveda Community funding rate close to 100%.

4 The categories excluded from tendering are defined in Article 29 of Directive 92/50 on tenderingprocedures for public service contracts.

24

Authorising departments must assess the risks posed as regardsviability and professional integrity by applicants who are flaggedby the SINCOM Early Warning System.

Departments must examine in detail the reasons why an applicanthas been entered in the Early Warning System and bear thosefactors in mind in their selection and award decision. It istherefore important to require applicants to indicate, whereappropriate, their VAT number, short name and acronym, andbank account number, since this information makes searcheseasier.

• Other grounds for alert by the Early Warning System

Besides those who fall into one of the categories excluded fromtaking part in procurement contracts, natural persons or corporatebodies may be flagged by the Early Warning System whereenforced recovery is under way for sums they owe to theCommunity budget. They may also be flagged as a result ofearlier controls by authorising departments, Financial Control orUCLAF in respect of other contracts or grants they have beenawarded.

In particular some applicants may be dummy companies/bodiesor may frequently change their business name, so that they are noteasily identifiable through the Early Warning System. It istherefore advisable, where appropriate, to look carefully at themembers of an applicant’s board of directors/executive board, atthe business name of subsidiary companies/associations/groupsand at the business name of any groups/companies that may havea stake in the applicant.

Commission departments should be wary in the case of applicantswho have their registered offices or bank account in countriesoutside the European Union, especially in “tax havens”.

4.4.3 Applicants’ financial capacity to complete the proposed operation

Applicants must have the capacity to finance their activitiesproperly. This principle also applies to other potential providers offunds besides the Commission.

It is important to check that applicants have stable sources of financesufficient to continue their activities throughout the operation and, ifnecessary, to play a part in financing it.

To ensure applicants have sufficient financial capacity, they shouldbe asked to include with their grant application form their annualaccounts for the last financial year (or their annual budget in the caseof public-sector bodies). Their financial capacity can also bechecked by consulting outside databases, as indicated earlier. An

25

audit certificate less than two years old from a registeredaccountancy firm offers a greater level of assurance. Even betterprotection for the Community budget can be obtained by requiring aguarantee equivalent to all or part of the grant being sought.

It is often useful to ask applicants to submit with their application anexplicit undertaking from each co-financing organisation to providethe amount of funding stated in the grant application for theoperation.

For further assurance beneficiaries may also be required to give anexplicit undertaking to cover their share of the financing and, ifnecessary, to finance expenditure not covered by the Communitygrant should other co-financers default.

It is for departments to assess the cost/effectiveness of eachpossibility and, depending on the kind of grant concerned, to decidewhich one to choose in order to be sufficiently sure of an applicant’sfinancial capacity.

4.4.4 Applicants’ technical capacity to complete the proposed operation

(1) Applicants must have the operational (technical andmanagement) capacity to complete the operation to besupported.

(2) In particular, the team responsible for the project/operationmust have adequate professional qualifications andexperience.

To check applicants’ technical capacity to complete the operation forwhich a grant is to be given, they may be asked to include with theirgrant application form a curriculum vitae of the staff who willactually be performing the work involved, as well as particulars ofinvolvement in any past or present operations financed by theEuropean Commission, contracts concluded with Commissiondepartments, and any other relevant information (e.g. activities onbehalf of other international organisations or Member States of theEuropean Union).

4.5 Award criteria

4.5.1 Operations must match the objectives defined by the Commission, including therequirement that Community funding be publicised.

The description of the operation must allow an assessment to bemade as to whether it matches the objectives of the grantprogramme. It must also specify by what means the Communityinvolvement in the project or activity will be publicised.

26

4.5.2 The expected results of the operation must further the policy objective of theprogramme

The results as described on the application form must also bemeasurable so that the extent to which they have been achieved canbe monitored, checked and subsequently evaluated. A further resultthat can be taken into account is whether or not the award of a grantwill contribute towards sustaining an organisation whose existenceis useful for achieving the policy objective of the programme.

4.5.3 The operation must be of sufficiently high quality

Although both the applicant organisation and the project might beeligible for consideration, actually awarding a grant may not bejustified if the project itself has not been well thought out orprepared.

4.5.4 The operation must be cost-effective

Assessing this involves asking such questions as: Do the probableresults stand in a reasonable relationship to the amount of the grant?Have better ways of achieving these results been overlooked? Isthere a way in which the same or equivalent results could beachieved with less cost to the EU budget (including costs ofadministration)? The breakdown of the budget, category bycategory, offers a way of ensuring that the amount of the grantawarded is the minimum necessary for the operation to becompleted.

4.5.5 The operation must not be the subject of a procurement procedure

Before awarding a grant, departments must always first examinewhether the activity or project should be the subject of aprocurement spending procedure.

4.5.6 The operation proposed by the applicant must not receive double financing

To forestall the risk of double financing, applicants must be requiredto indicate in their grant application what other grant applicationsthey have submitted or will be submitting to the Europeaninstitutions during that same year, indicating for each grant theCommunity programme concerned, the title of the operation and theamount of the grant.

The department responsible for awarding a grant is required toensure that there is no risk of double financing by consulting the listof commitments or payments recorded in SINCOM to see if thereare any in favour of the applicant by other Commission departments.If there are any doubts those departments should be contacteddirectly (see Annex 2).

27

Organisations can put in grant applications to several Commissiondepartments for separate operations or for the same operation,providing there is no double financing of the same expenditure. Inall cases consultation between departments is essential before givingan applicant organisation an answer.

If two or more departments intend to award a grant for differentparts of the same project or event, the beneficiary should beinformed by a joint letter.

4.5.7 Operations for which an application has been made must not, as a rule, havestarted yet

Grants for operations that have already started are only admissiblewhere it can be shown that the grant is necessary to ensure that theoperation is properly completed. However, the grant cannot coverany period before the application was submitted.

Awarding grants retroactively for operations that have already beencompleted is not allowed, since doing so serves neither to encourageactivities nor to promote the visibility of Community support.

4.5.8 Proposed operations which, directly or indirectly, conflict with the policies of theUnion or may be linked with an unsuitable image must be rejected

For example, all grants for projects that may be contrary to theinterests of public health (alcohol, tobacco, drugs), respect forhuman rights, people’s security, freedom of expression, etc., areprohibited.

28

5 PROCEDURE FOR AWARDING GRANTS

After applications have been sifted to eliminate excluded cases and ensurecompliance with the requirements, a selection has to be made from the proposalsthat remain. The following obligatory rules govern the constitution of thecommittee that will examine and select proposals, its composition, the nature of itsdeliberations and the extent of its powers.

5.1 Composition of examining committees

Depending on the importance of the series of grants and the amountinvolved, the department concerned should designate a committee consistingof a chairman and two or three officials (or other Commission staff)belonging to at least two units. Members of the committee, besides beingdrawn from managing units, may be taken from financial units in particular,and also from other departments.

Where the technicality of the subject requires, non-voting outside expertscan sit on committees. These experts must not have any direct or indirectinterest in an organisation applying for a grant (this is explicitly provided intheir contracts).

5.2 Operation of committees

The decisions of the committees (e.g. list of applicants drawn up initially,exclusion of certain applications, then selection and final choice) arerecorded in minutes signed by the members of the committee. These minutesare sent for information to Financial Control on request.

The committee may take its decisions by written procedure.

Where agreement cannot be reached, the committee decides by a majority ofits members. In the event of a tied vote, the committee chairman has thecasting vote.

The committee’s decisions are taken independently and in an advisorycapacity. Eventually the committee draws up a list of the proposals chosen inorder of merit, indicating the proposed amount to be financed by Communityfunds. On the basis of this list, the authorising officer adopts the final listand allocates the grants.

5.3 Avoiding double funding for the same operation

Departments are already able to monitor payments made to particularbeneficiaries by consulting the central third-party ledger (“fichier tiers”) inSINCOM 1. SINCOM 2 will allow them to monitor both commitments andpayments to individual beneficiaries through the central third-party ledger.

Before making an expenditure commitment proposal authorising officersmust take reasonable steps to check there is no double funding for the sameoperation and must create a third-party record if none already exists..

29

Entering the VAT number or an equivalent identification number will beparticularly important in this context.

30

6 FINANCIAL MANAGEMENT RULES APPLICABLE BY DEPARTMENTS REGARDINGGRANTS

This chapter is concerned with the rules for calculating the amount of any grant.

6.1 Rules concerning the budget of the operation assisted

6.1.1 The applicant’s forward budget

All grant applications must be supported by a forward budgetshowing all the costs and revenue that the beneficiary considersnecessary to carry out the project. A project can be a series of relatedoperations; in fact, related projects should be grouped together as asingle application. Related projects would be those with a link to acommon objective and a common organisational structure.

The forward budget must be:

– sufficiently detailed to allow identification, monitoring and control of theoperation(s) proposed;

– in balance, i.e. total revenue and total expenditure must be equal;

– expressed in euros, as a rule; in any event it will be converted into eurosto calculate the amount of any grant;

– accompanied by the calculations and specifications used in drawing it up.

6.1.2 Revenue

The income side of the forward budget should show:

– the direct monetary contribution from the applicant’s own resources;

– the contribution (grant) from any other fund providers.

– any income generated by the project (e.g. the yield from sales ofpublications during the operation, or the fees charged to participantsattending a conference);

– the grant sought from the Commission, with a breakdown where severalapplications have been made to the Commission; and lastly,

– any contribution in kind from the applicant’s own resources.

6.1.3 Eligible costs

The expenditure side of the budget submitted with the applicationmust be sufficiently detailed to allow “eligible costs” to bedistinguished from any “ineligible costs”. In the context of grants,the costs considered eligible for Community funding are those thatsatisfy the following criteria:

31

– the total amount of the costs must show that the organisation of theoperation satisfies the principles of sound financial management, inparticular as regards economicality and cost-effectiveness;

– the costs of the operation must be directly linked to achieving the objectof the agreement;

– the costs must be necessary to carry out the project and must be in linewith normal conditions on the market. They must be entered in accounts,identifiable and controllable.

6.1.3.1 Direct costs eligible

These are all costs directly generated by the operation andessential for its implementation. They would not have beenincurred if the operation had not been carried out.

The following direct costs are eligible, by nature:

– staff costs (unit cost per day for work on the project). These may includeother charges relating to the use of human resources provided that theyare specified in the call for proposals. Staff costs cannot exceed thesalaries and other charges normally practised by the applicant, nor exceedthe lowest rates generally accepted in the relevant market. Commissiondepartments are requested to specify explicitly the rules or ceilingsapplied to determine whether staff rates are acceptable or not;

– travel, accommodation and subsistence expenses at rates and on terms seton the basis of scales or rules laid down by Commission departments byreference to the best conditions available on the market;

– equipment (new or second-hand); these costs must be in line with normalmarket practice and must be essential for carrying out the operation. Costsof land and immovable property (depreciation/rental costs according tothe nature of the operation) are not covered. In exceptional cases theCommission may explicitly allow such costs, and in that event a specialclause will be included in the grant agreement. Acceptance of such costsmust be justified by reference to the objectives of the operation.5 Fulldepreciation can be accepted if the nature of the operation and/or the useof the property warrants it. In these cases the Commission will specify thefinal destination;

– charges for financial services in specific contexts (charges for banktransactions, insurance; normally the risk of exchange losses is excluded);

– costs of consumables and supplies;

– costs of services relating to eligible costs (such as transport costs);

5 Such as sustainability in the case of development projects.

32

– subcontracting, but only where the Commission has given advancewritten agreement (the rules applicable to the beneficiary also apply to thesubcontractor);

– information dissemination costs;

– other costs stemming from obligations under the grant agreement (audits,specific evaluations for the operation, reports, translations, certificates,deposits, etc.);

– a “contingency reserve” of no more than 5% of the eligible direct costs;

6.1.3.2 Indirect costs and overheads eligible

Depending on the nature of the operation and the targetobjectives, the awarding department may, on the basis ofcriteria that must be specified in the call for proposals, setflat rates for the amount of overheads eligible. Themaximum amount that can be accepted is 7% of total directcosts eligible.

Overheads are calculated according to the standards,policies and generally accepted accounting standards of thebeneficiary which are thought to be reasonable by theCommission.

Overheads exclude such categories of costs which couldeasily be object of a direct imputation in conformity withthe generally accepted accounting standards of thebeneficiary as well as the costs that are financed by othersources.

Overheads can include the following positions,administration and management fees, depreciation(according to the calculation methods of the nationallegislation of the beneficiary) of buildings and equipment,rents, maintenance costs, telecommunication and postalfees, heating, light, water, electricity or other forms ofenergy, office furniture, personnel costs insofar they are notalready covered as direct costs and insurances.

Indirect costs are not eligible in the case of funding for aspecific operation carried out by organisations receivingrunning cost grants.

6.1.4 Ineligible costs

The following costs are ineligible:

(1) fixed capital costs;

33

(2) general provisions (for losses, possible future liabilities,etc.);

(3) debts owed;

(4) interest paid;

(5) doubtful debts;

(6) exchange losses, unless specifically provided for by way ofexception;

(7) extravagant expenditure;

(8) contributions in kind.6

6.1.5 Contributions in kind

Contributions in kind are not eligible costs, but are taken intoaccount in calculating the rate of funding granted by theCommission grant for the project.

Small organisations in particular, such as NGOs, often apply for partof their contribution to the costs of a project to be in kind. Suchcontributions in kind can appear on both sides of the forwardbudget, on the income side as the money equivalent of the servicesor materials contributed and as an equal amount on the expenditureside, but separately from the rest of the budget since they cannotcount as eligible costs.

In particular, contributions in kind include:

– land, immovable property whether in its entirety or in part, durable capitalgoods,

– raw materials,

– unpaid charity work by a private individual or corporate body.

The following conditions must be met:

– the amount declared by the beneficiary as contributions in kind must bevalued either on the basis of objective factors or on the basis of officialscales laid down by an independent authority or by an outsideindependent professional;

– the cost of private charity work must be valued in accordance with thenational rules regarding the calculation of hourly, daily or weekly labourcosts, if such rules exist.

6 But see 6.1.5.

34

Since it is often small non-governmental organisations that dependon this kind of support, Commission departments must not rule themout whenever such organisations may reasonably be expected toapply for grants. Departments must clearly indicate whether or notcontributions in kind are allowed in the call for proposals orwhatever other means of publicity is used. If contributions in kindare allowed, they will not count as eligible costs but will involve anincrease in the grant, either in terms of the amount awarded or interms of the percentage of eligible costs.

Where contributions in kind are taken into account, the Communitycontribution is limited to the level of actual expenditure incurred, inother words to total eligible costs excluding the value ofcontributions in kind.

6.1.6 The agreed budget

A budget is to be incorporated in the grant agreement (a model isincluded, on ICON).

(a) The expenditure side will contain only eligible costs, brokendown by heading and amount. It will explicitly set out theconditions under which any overheads are included.

(b) The income side will set out:

– the contribution which beneficiaries undertake to find, either from theirown resources or from other sources.

– any income that the project is expected to generate;

– the Commission grant or grants.

The eligibility period for costs must be specified in the agreementgoverning the Community contribution. This provision will set thestarting and ending dates for eligibility and will indicate any termsfor exceptional retroactivity back to the date of submission of theapplication, and any other exceptions.

Retroactive grants for operations already completed are not allowed.Grants for operations that have already begun should remain theexception and the conditions must be set out in the call forproposals. In this case, the grant may not cover a period prior to thedate of submission of the grant application.

The dates taken into account for the eligibility of costs are the dateswhen the costs were generated and not the dates when theaccounting documents were drawn up.

Where contributions in kind are taken into account, their amountmust be included in the grant agreement, since the beneficiary has tobe under an obligation to provide them.

35

Any change which the beneficiary wishes to have made to the termsof the agreement that would imply a change in the basic purpose ornature of the operation must be submitted for prior approval by theCommission. Such changes must be set out in an addendum to theagreement.

Where the change does not affect the basic purpose of the operationand the financial impact is limited to a transfer between headings ofthe budget involving an increase of less than l0% of a heading foreligible costs, the beneficiary may apply the change and inform theCommission without delay. Otherwise, prior approval must besought from Commission departments. If no increase is permissiblefor certain categories of costs, these must be specified in theagreement.

6.2 Calculating the amount of the grant

6.2.1 On the basis of the forward budget

The maximum amount of any grant is the total amount of actualeligible costs (i.e. not counting the value of contributions in kind).This is an absolute limit which applies in all cases. However, only inrare cases can a 100% grant be justified. In the vast majority of casesthe beneficiary should be required to find the money to pay for a partof the project (co-financing principle).

(a) Where the project does not generate any income:

– if the award criteria lay down an automatic percentage rate, the actualamount of the grant is fixed by applying this rate to the figure for totaleligible costs;

– in other cases, the actual amount is decided by the grant selectioncommittee in the light of their assessment of the project's contribution tothe policy aim of the programme grant in question, subject to anymaximum above.

(b) Where the project will generate an income, this is taken intoaccount :

– if the award criteria lay down an automatic percentage rate, this is appliedto eligible costs less the income generated;

– in other cases, the grant that would otherwise have been given is reducedpro rata by the ratio of such income to eligible costs.

The principle of cost-effectiveness should be applied in such cases.For instance, if there is a good project whose staff costs or totalbudget appear too high compared to similar projects, instead ofturning down the application, consideration should be given toawarding a lower grant than normal.

36

The amount of the grant is expressed in euros.

The Commission will specify the overall level of the grant:

– either as a maximum figure not to be exceeded (with an indication of totaleligible costs in percentage terms);

– or by indicating the categories of costs that the Community grant willcover and up to what ceiling (as a figure and as a percentage of actualexpenditure).

The first option facilitates project management, whereas the secondmakes auditing after the project has been completed easier.

With regard to the payment of advances, the normal rule is that forall grants, payment is made in at least two instalments: an advanceand the balance, although provision can be made for payment solelyon the basis of the final accounts. The number of paymentinstalments depends on the financial risks involved. Where the risksare high, and if the beneficiary is not required to lodge a financialguarantee, thought might be given to using several instalments.Where the risks are lower, the recommended approach is to confinepayments to an advance, with the balance being paid after thebeneficiary has submitted the necessary supporting documents.

A grant may also be paid as a single payment in advance, but onlyon production of a letter of guarantee by the body receiving the grant(the cost of this guarantee would be considered eligible under thebudget of the operation supported). Of course, this latter option putsthe department in a very strong position, since if the beneficiarybreaks the terms of the agreement, the whole amount of the grantcan be reclaimed.

In the case of large grants (above 150 000 euros), advance paymentscould also be covered by a financial guarantee.

A standard financial guarantee form can be found at Annex 5.3.

The beneficiary will be required, within the time limit set in theagreement, to present the final accounts for the whole operation interms of eligible costs, which will then be assessed by theCommission departments to determine the balance of theCommunity contribution.

6.2.2 On the basis of the final accounts

The amount of a grant only becomes final after completion of theproject and presentation of the final accounts.

The grant is reduced if a comparison of the final accounts with thebudget set out in the agreement shows:

37

(1) that total income, including interest on advance payments,exceeds total expenditure; in this case the Commission grantis reduced proportionately by the excess amount. If severaldonors have contributed, the excess and reduction are sharedamong them;

(2) that eligible costs are less than in the agreed budget; in whichcase the Commission grant is reduced proportionately;

The grant is reduced, depending on circumstances, in the followingway:

– by reducing the balance payable after completion, or

– by requiring partial repayment of the advance paid (for the repaymentprocedure, see Chapter 8.3).

In no circumstances can the final Commission grant be higher thanset out in the agreement, even if costs exceed those in the agreedbudget. The contingency reserve in the agreed budget should be ableto absorb any reasonable unforeseen overrun of eligible costs.

6.3 Special rules applicable to running costs grants

The special points regarding grants towards running costs are the referenceto the Community budget and the fact that the beneficiary’s administrativecosts must be limited to a strict minimum. Expenditure yielding an increasein the beneficiary’s capital are excluded. Beneficiaries may be obliged, underthe law applicable, to provide for this kind of expenditure, as withremunerations in the form of share options, etc. In this event, such costs maybe assessed case by case, but without losing sight of the general principlethat the grant may not serve to increase the business capital of thebeneficiary. Organisations receiving a running costs grant are eligible toapply for a grant for a project under another programme, but in this caseindirect costs are not eligible (see “Indirect costs and overheads eligible”).

The following special rules apply in the case of grants to cover the generalrunning costs of an organisation.

6.3.1 Limitation on the award of running costs grants

Running cost grants can only be awarded:

(a) where this is authorised to a named organisation by a budgetheading or in the remarks to a budget heading;

(b) under a budget heading that specifically provides for suchgrants.

38

6.3.2 Costs eligible for running costs grants

Costs eligible are those necessary to ensure the normal running ofthe beneficiary organisation and to enable it to pursue its statedobjectives.

The same rules for calculating and checking eligible and ineligiblecosts apply as for project grants except that:

– all reasonable overheads are eligible, and

– a different rule applies in the event of income exceeding expenditure (see6.3.4 below “Rule governing surpluses”).

Besides the items listed below in connection with grants for specificoperations, beneficiaries must include the following with theirapplication for a running costs grant:

– an organisation chart and a description of the tasks of staff;

– a full list of other fund providers;

– proof of an organised accounting system;

– their latest financial statements (balance sheet, profit and loss account).

6.3.3 Time limit for introducing an application

Organisations seeking a running costs grant must apply within thefirst half of their financial year.

6.3.4 Rule governing surpluses

If an organisation realises a surplus of income over expenditure atthe end of a financial year for which it received a running costsgrant, part of the surplus up to 5% of total income for that year andany part that is earmarked for some multiannual or other project inthe following year can be carried over to the following year.

However, where there is any surplus above 5% that is not earmarkedfor specific future use, a repayment has to be made. This iscalculated by determining what proportion of the organisation’s totalincome for the year in question was accounted for by theCommission grant and applying the resulting percentage to the non-earmarked surplus above 5%.

The amount calculated is either repaid direct or deducted from thefollowing year’s grant.

39

6.3.5 Principle of setting a ceiling on this type of grant as a proportion of thebeneficiary’s annual running costs in order to limit dependence on theCommunity budget.

As a general rule, it is recommended that a minimum level offunding for the beneficiary’s budget should come from sources otherthan the EU budget. In the 1998 budget, Parliament introduced aminimum requirement of 10 % of external co-financing for grants inPart A. In the 2000 budget this was increased to 20%.

Contributions in kind do not count as external co-financing.

6.3.6 Start-up grants and three-year limit for a single beneficiary

Budget headings which allow running cost grants to be given toorganisations selected by the Commission can be used to finance theestablishment of new organisations. Such “start-up” grants,however, can only be paid for a maximum of 3 years, after which theorganisation has to cover its general running costs from its ownresources and non-EU grants.

However, these organisations may, of course, still apply for projectfunding from the EU budget.

40

7 RULES RELATING TO THE GRANT AGREEMENT BETWEEN THE COMMISSION ANDTHE BENEFICIARY

After the decision to award a Community grant has been taken, and once a financialcommitment proposal has been drawn up and duly approved by the FinancialController, a contract has to be concluded defining the reciprocal rights andobligations of the parties (Commission and beneficiary). The contract has to beconcluded before 31 December of the year in which the financial commitment wasmade.