USSTUDYTOURMASTER

90

1 US STUDY TOUR OCTOBER 2014 US STUDY TOUR October 2014

-

Upload

rhyll-gardner -

Category

Documents

-

view

60 -

download

0

Transcript of USSTUDYTOURMASTER

1

US STUDY TOUR OCTOBER 2014

US STUDY TOUR October 2014

2

US STUDY TOUR OCTOBER 2014

LinkedIn Visit

7 second game Why are you where you avenue - eg why are you passionate about finance and why should I work with you/for you. Current job - what are you doing - anything below that, no one looks at. Endorsements - pushed by LinkedIn algorithms. People endorse you because they like you. Pace of change is much greater. MOEK (??) online education - massive online education - access to best professors. LinkedIn us only 11 years old! Medallia - NPS based Gainsight is another one Citi is very active on LinkedIn - they build Groups. But the quality of your Group is v important also - the right type of people LinkedIn Mission - to create an economic opportunity for all members eg help people find a job, change their job, share their knowledge - post blogs and share

Linkedin – who are theY?

Company Overview

• Founded in 2002 by team members from PayPal and

Socialnet.com.

• LinkedIn allows users to create profiles and connections to each other in an online social network which may represent

real-world professional relationships.

• As of 2013, the site has over 300 million members across

200 countries (93 million in America, 6 million in Australia).

• In 2013 the company generated $1.52 billion in revenue – a

combination of membership fees and advertising revenue.

What could LinkedIn provide BOQ?

• As a dominant social media outlet, LinkedIn could provide

BOQ with an advertising outlet, catered to professionals

both young and old.

3

US STUDY TOUR OCTOBER 2014

updates. 10% of journey only 300mill. They want to be 3 bill Zing is a huge competitor in some parts of the world. Brazil and India are great sources of new ideas eg uploading resumes rather than filling in. Companies - 7x no of employees is the benchmark for no of followers. Think about how you enable them to promote your vision values etc. this is how you monetise mobile. Create an environment to make your followers successful. Success Stories of customers Regulation You, your industry, and about them. Content must be relevant it is about your brand. Influencers - a way for LinkedIn to be differentiated in the news. Editors work with them to bring content to the community.

4

US STUDY TOUR OCTOBER 2014

Wells Fargo Visit

Wells Fargo – Who are they?

Company Overview

• Founded in 1852 – now the 4 th largest bank in the US by assets and the largest by market capitalisation.

• Acquired Wachovia in 2008 for $14.8bn.

• Company Vision: “We want to satisfy all our customers’

financial needs and help them succeed financially”

• Prides itself as a community-based bank: although having a

national presence, their behaviour is aligned towards a

smaller bank, focusing on customer relations.

• Major customer segments: individuals, small businesses and

large businesses.

• Major business groups:

• Community banking (individuals and SMEs)

• Consumer Lending (mortgages, vehicle loans, credit

cards, student lending)

• Wholesale banking (larger and medium-sized

businesses)

Wells Fargo at a Glance

$1.6tn Assets

$21.9bn Net Income

$826bn Loan Portfolio

12,500 Locations

70m Customers

9000 Team Members

$276bn Market Value of Stock

Key Strategic Priorities

Putting Customers

First

Growing Revenue

Reducing Expenses

• Outstanding customer service.

• Always attempt to understand the customers’ financial objectives prior to

offering them products and solutions.

• Multi-channel approach: stores, ATMs, phone banks, internet and mobile

banking channels. Channel integration ensures the best customer

experience.

• Envisage to gain more business from current customers, attract customers

from competitors and acquire other businesses.

• “You can’t buy your way to greatness. You have to earn it from your current

customers”

• “When we find wise ways to reduce our expenses, we free up funds to

benefit our customers, invest in the future and reward our shareholders”

• Top 500 innovative company: always looking for ways to simplify operations.

• Envisage to enhance the customer experience.

5

US STUDY TOUR OCTOBER 2014

Wells Fargo Talk – Innovation (Brian Pearce) 450 mill customers US only in Retail 270000 employees A lot of physical locations - branches and lending centres - and a lot of phone calls but online and mobile have most interactions. But branch interactions are key. Strategy is very physical distribution focused. 82 product lines. Usage of and leverage of branch central to things though. Stagecoach legacy - transferring value Innovation agenda built around Keep my data secure - next generation fraud and authorisation Know me - age of context Simplify and connect with me - digital omnichannel Internet of Things - Everyday, everywhere banking. Present the agenda to the development and product team and they use their "10% time" (semi formal arrangement) to do the development - agreed with their managers. Wells Fargo view - having the best customer experience is the best differentiator. Wells Fargo Labs R&D - test new software Demo/prototypes - bring ideas to life and socialise. Team member pilots and Customer pilots for beta testing Multichannel Labs - view demos and experience future concepts across devices and across channels. Spark Inspire Enable - a converted conference room, moves around to conferences etc AIB allow customers to experiment and explore in their stores. Innovation = Process + Ideas -> Innovation Bootcamps for brainstorming Employee engagement benefits from innovation - Bootcamps, labs, prototypes Follow a customer for a week - you realise the problems you create in their lives Culture of the bank is very anti-hierarchy Drive through teller locations - used to put drivers livens in a tube.....now there is pre- staging and authentication from the App. Can also be leveraged to walk up

6

US STUDY TOUR OCTOBER 2014

experiences (Drive through locations - only where it gets very hot eg Texas or very cold eg) Start in-store experience through url sent by text. 85% of products are sold in the store. A reduced customer needs identification, edit/confirm customer info, use finger for e- signature Send a thank you text Use of beacons - blue tooth low energy devices. Eg use to let the banker know when you arrive in store - take a picture, get s welcome pop up, beacon sends signal when you arrive and to the stage director at the branch. The stage director has a dashboard and it measures wait time, allows recognition, shows completed

Oculus Rift – Gaming (now owned by Facebook).

7

US STUDY TOUR OCTOBER 2014

Google glass interactions - list of uses. Put card in front if glass and it scans and then pulls up expenses for the month and pie chart Bankers wearing glasses and using facial recognition - gets information up from CRM Small super geeky community. Some bars say "no google glasses allowed"

8

US STUDY TOUR OCTOBER 2014

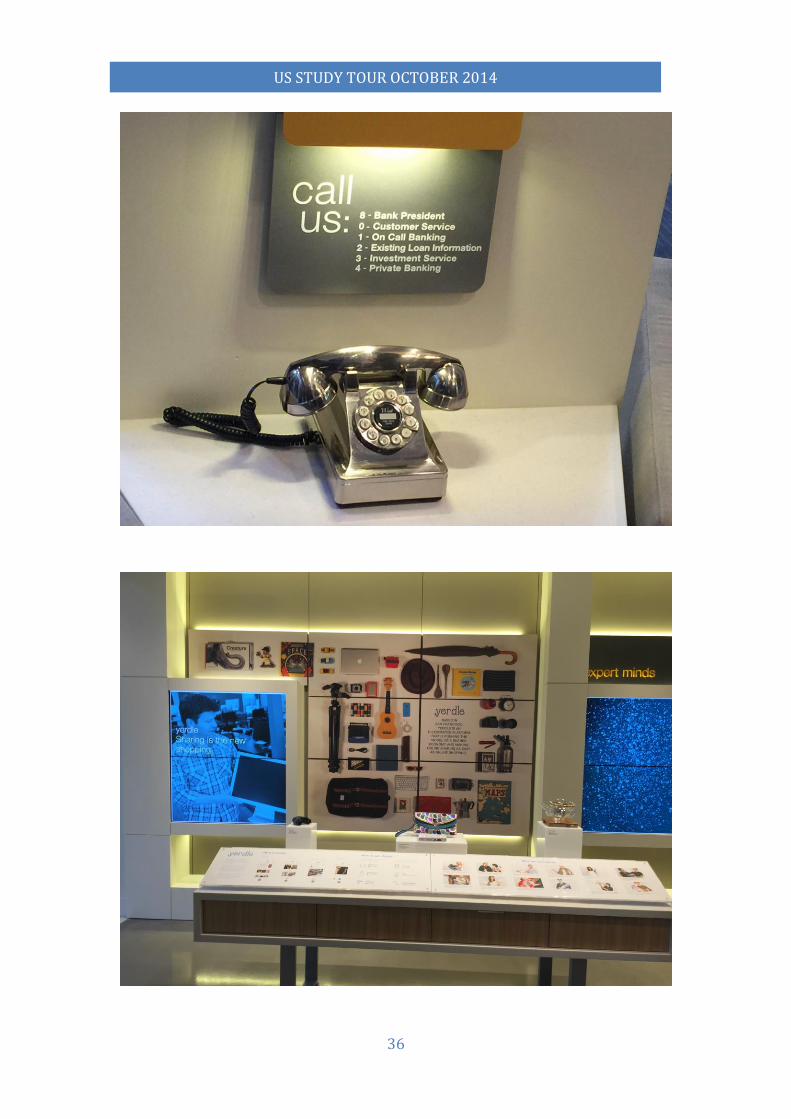

Capital One 360 Café Visit

Capital One 360 Café – Notes from Visit (Partnering with Peets Coffee) Capital One 360 is the online only bank 8 cafes nationally - had them for 10 years 3 Levels All have the same look but sizes vary - this one in SF is the largest Everything is done online - help customers do self service - but this is primarily a creative space. Space for customers to come in (Wifi did not work) Like to keep it festive - BBQ Bonanza, Halloween etc 2nd home for many customers. Mon to Fri 7am to 6pm The bank for main at not for wall st - $5Mill limit. Waffle vendor who has no retail shop but a huge online following. Art installations NFPs can rent conference rooms at reduced rates. Prime location near a major public transport hub. "We set out to create a bank that wasn't a bank. Done and Done" There is also ING Direct Cafe in Europe

Capital one 360 – who are they?

Company Overview

• Founded in 2000, previously ING Direct USA but acquired by Capital One in 2012 – focus on helping their customers save

time and money.

• Financial products are simple; e.g. savers fee-free checking

and savings accounts accessible online.

• Several products are targeted introducing children to savings

programs. But products extend to other simple home loans, savings accounts, and business accounts.

• Capital One 360 Cafes are a unique initial that combines a

bank with a coffee shop. Allows customers to discuss their financial needs in a friendly and relaxed environment.

• Significant online presence – utilising social media to stay in

touch with existing customers and contact prospective customers.

What could Capital One 360 provide BOQ?

• Capital One 360 have a comprehensive online presence which BOQ could adopt.

• Their target segments are different – there are

opportunities to establish child saving programs.

• Products are incredibly simple, which minimises

transaction costs and maximises customer ease.

9

US STUDY TOUR OCTOBER 2014

Checkmate - photograph a cheque and it is deposited. Try to partner with people who have used the space to build their App here in SF. Help underprivileged women to start their small business. Just recently introduced cash deposits at the ATM. average age of customers is around 30. Capital and Simple are the only 2 banks in the US who have the technology to show the actual name of the store,the logo and the location for transactions on the online statement. Lab team upstairs in the site does innovation for the rest of the company. They use the design thinking technology. Capital One small business offers expanding -Sparkpay (like Square to accept mobile payments) Accountable only for the customer experience of the building - how it looks, wifi working, music etc Capital One 360 Cafe (continued) Digital Innovation - Capital 360 labs (engineering team) "Software is eating business" Major industries eaten by IPhone apps. Camera, travel agents, music, books,weather, maps. Banking is also being disaggregated. After many years of outsourcing decided to bring software development and systems back in house - along with acquisition of ING Direct. Great systems and IT acquisition. They were very proud of it. Capital One 360 is the old ING Direct rebranded. One of 6 partners who integrated with ApplePay Capital One Labs is a passionate team of entrepreneurs who are reimagining the way people interat with their money

10

US STUDY TOUR OCTOBER 2014

Vanguard of the organisation to pilot, experiment, fail. They partner within the business but also with external business models Labs in NY (big data), SF (payments) and DC (mobile) Launched an API platform - creating a funnel and starting up partnerships Different types of security solutions depending on circumstances. Always over conservative. Hothouses - an intense focussed problem solving/ solution development exercise Complex business problem - wireframes - clickable prototypes - high level architecture and implementation plan. Design thinking - release process. Looks for a potential solution by going through an interactive process. Hackathon - proving grounds for new ideas for internal and external issues. 1-2 days. Viability determined within 24 hours. 3rd party participation. Sponsor others - gets Capital One out there as a technology company. Accelerated talent adoption through acquisitions of small tech companies in Silicon Valley - Bankons was the beginning of the SF innovation labs. They want to be a technology company that offers banking services.

11

US STUDY TOUR OCTOBER 2014

12

US STUDY TOUR OCTOBER 2014

13

US STUDY TOUR OCTOBER 2014

14

US STUDY TOUR OCTOBER 2014

15

US STUDY TOUR OCTOBER 2014

16

US STUDY TOUR OCTOBER 2014

17

US STUDY TOUR OCTOBER 2014

18

US STUDY TOUR OCTOBER 2014

19

US STUDY TOUR OCTOBER 2014

HearSaySocial Visit

Notes from Presentations Hearsaysocial - Best practices in social media in financial institutions. 5 years old

Hearsay social –who are they?

Company Overview

• Established in California in 2009, Hearsay is a software

social media marketing management platform. It operates by

using social networks such as Facebook and LinkedIn as a way for clients to market to various customer bases.

• Some of the world’s largest financial services and insurance

firms rely on Hearsay Social to attract prospects, retain customers, strengthen relationships, and grow business on

social.

• 75% of their customer base is within the financial services

industry.

What could Hearsay Social provide BOQ?

• Comprehensive and tailored approach to creating

advertising strategies though social media – opportunity to

interact with a much broader, or more specific, customer group through targeted marketing strategies.

20

US STUDY TOUR OCTOBER 2014

Enterprise software for salespeople to better market and sell on social media. Social media is a great start - huge data source. Clara wrote a book.... 10 years old, 19 countries, Hearsay labs - relationship management for the Facebook era Startup funds provided by Sequoia Capital - the entrepreneurs behind the entrepreneurs. $3mill to start/hire - now financing expansion ($30mil) Challenge - doubling to company every year and maintaining the benefits of small. Plans to expand beyond Social to other digital advice (CRM systems) and to other industries ( but focussed on Fin Services primarily) 98% of the U.S. online population uses social networks Globally - the average person spends 2 hours a day engaging in social networks. Fastest growing sector is adults/ affluent

21

US STUDY TOUR OCTOBER 2014

22

US STUDY TOUR OCTOBER 2014

23

US STUDY TOUR OCTOBER 2014

24

US STUDY TOUR OCTOBER 2014

25

US STUDY TOUR OCTOBER 2014

26

US STUDY TOUR OCTOBER 2014

27

US STUDY TOUR OCTOBER 2014

28

US STUDY TOUR OCTOBER 2014

Edgar, Dunn & Company

Innovation in Financial Services and Payments

New technologies -

Applepay, PayPal,

MPOS(Smartphones and

Tablets for point of sales)

Consumers are looking

for convenience and security.

An explosion of new

payment methods has brought

a lot of new entrants to the

market……Real Time payments. P2P

Massive infrastructure cost to this when the current clearing

house is relatively low cost.

Edgar, dunn & company – who are they

Company Overview What could Edgar, Dunn & Co. provide BOQ?

• Established in California in 1978, began as a general

consulting firm but now specialises in payments and financial

services.

• Experience includes: product strategy, market strategy,

channel strategy, M&A strategy and integration.

• The firm’s global footprint maintains a close proximity with

the world’s most prolific entrepreneurial hubs, such as Silicon Valley, placing it at the forefront of emerging payment

technologies.

• Major clients include the majority of US regional and large

banks, more than 10 of the largest UK banks and more than

two-thirds of the top 25 US credit card issues.

• Expert advice regarding BOQ’s product, channel, market

and M&A strategies – particularly in the adoption of new

technologies to better service these areas.

29

US STUDY TOUR OCTOBER 2014

The banks are still part of the transfer but losing the totality of the

customer touch point

Facebook and Twitter are doing P2P payments. ….It’s a solution

without a problem - how comfortable are people sending $ on Facebook

given their history of changing settings etc.

Ripple- interesting concept to leverage cryptocurrencies and still

use banks. ….No centralised point of authority but all the members of

the community have the capability to authorise the transaction. You

need to go through a licensed FI so it takes away the uncertainty and

danger that may exist with a bitcoin only transaction.

Why would you use Bitcoin unless you were trading in something

illegal......Bitcoin has become a marketing tool more than anything else.

Softcard (formerly known as ISIS) - Limited to specific phones that

had the secure element in the phone.

Visa and MC gave merchants incentives to put in the contactless

terminals - every market globally has transitioned over a long period of

time. Easier for smaller and largest to change - mid size have the most

trouble.

MCX - launched by a group of merchants including Walmart to

challenge Visa and MC. Consumers would need to give merchants their

bank account information - trust issues. But there is the discount to

entice people into it.

Applepay - Unlike other mobile payments system it is working

with the existing payment structure (banks ,Visa, MCard Amex) - unlike

Google.

They don't want the regulatory guise that would come with

becoming a bank.

They will still build an ecosystem where you will buy a new phone

every 2 years.

30

US STUDY TOUR OCTOBER 2014

More sophisticated encryption than other systems

Issues with biometric security if the fingerprint gets compromised.

Apple expect to have 500 institutions signed up by end of 2015.

Apple take bps on credit and debit transactions - the issuer pays

most if not all of this.

Good customer experience - simple, card pops up and you

authenticate with your fingerprint and you are done.

Apple likely to get to loyalty at some point but not yet.

What else are banks doing? Many banks are splitting out

innovation centres to get traction. But at the moment, the only job

growth is in compliance!

31

US STUDY TOUR OCTOBER 2014

Twitter and Facebook ( they have all you info) powered by

payment partners in the background.

Google - doing 10 different things. Also competing with Amazon,

grocery chains with food delivery - all about the data they are collecting

32

US STUDY TOUR OCTOBER 2014

Umpqua Bank

Community Bank - open to everyone.

Not a traditional bank

They have offices on site open to the community also

They call them "stores". If an office is not being used, it is available to the community. Many

Umpqua Bank – who are they?

Company Overview

• Founded in 1953 as a very small regional bank.

• Vision: “Bank like you live”. Very customer orientated, seeing

themselves as “more like a friendly neighbour”.

• Have structured learning to earn and other community

programs.

• Major customer segments: individuals, small businesses,

larger commercial groups.

• Products: Mortgages, vehicle loans and leases, credit cards,

wealth management, retirement, education loans.

• Pride themselves on a vibrant workplace culture – numerous

awards.

$11.6bn Assets

$105.7m Net Operating Earnings

$78.9m Home Lending Revenues

$9.1bn Total Deposits

10% New Home Loan Growth (2013)

0.49% Non-performing Assets

Umpqua Bank at a Glance

3rd Best Bank to Work For

Key strategic Priorities

Maintaining a strong workplace culture

Empowering of associates. Ease in communication channels, access to leadership; avoiding the bureaucracy associated with being ‘big’.

Enhancing the customer experience

Flagship store opened in San Francisco named Retail Design Institute’s Store of the Year – incorporates new technologies with service options that create a one-of-a-kind customer experience.

Acquisition Activity

April 2013: Purchased Financial Pacific Leasing – national equipment leasing and small business lender. Goal to diversify revenues and opening new market opportunities across the country. September 2013: Merger with Sterling Financial Corporation - $10bn asset financial institution – put the company on a higher playing field with $22bn in assets, more resources, store density and higher earnings. Expansion of geographic footprint with 180 new stores, expense synergies of $85m, and 12% accretion to operating earning per share.

33

US STUDY TOUR OCTOBER 2014

events every month using the space.

9 to 6 opening hours.

Banker Bar for customer transactions

"Welcome the the worlds greatest bank"

Don't use advertising - word of mouth only.

Stores designed to suit the neighbourhoods- in Oregon it is like a garage

No product sales targets - unlike other banks, no pressure to sell.

34

US STUDY TOUR OCTOBER 2014

35

US STUDY TOUR OCTOBER 2014

36

US STUDY TOUR OCTOBER 2014

37

US STUDY TOUR OCTOBER 2014

38

US STUDY TOUR OCTOBER 2014

39

US STUDY TOUR OCTOBER 2014

40

US STUDY TOUR OCTOBER 2014

41

US STUDY TOUR OCTOBER 2014

42

US STUDY TOUR OCTOBER 2014

43

US STUDY TOUR OCTOBER 2014

44

US STUDY TOUR OCTOBER 2014

45

US STUDY TOUR OCTOBER 2014

46

US STUDY TOUR OCTOBER 2014

47

US STUDY TOUR OCTOBER 2014

48

US STUDY TOUR OCTOBER 2014

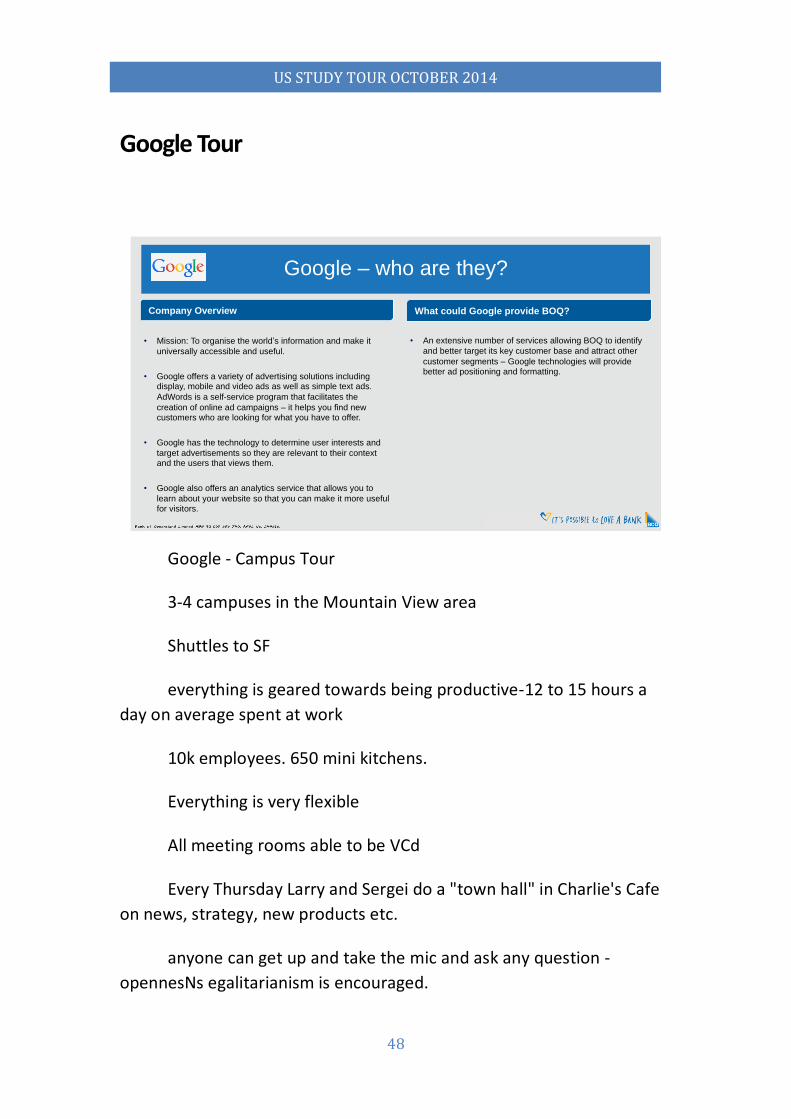

Google Tour

Google - Campus Tour

3-4 campuses in the Mountain View area

Shuttles to SF

everything is geared towards being productive-12 to 15 hours a

day on average spent at work

10k employees. 650 mini kitchens.

Everything is very flexible

All meeting rooms able to be VCd

Every Thursday Larry and Sergei do a "town hall" in Charlie's Cafe

on news, strategy, new products etc.

anyone can get up and take the mic and ask any question -

opennesNs egalitarianism is encouraged.

Google – who are they?

Company Overview

• Mission: To organise the world’s information and make it

universally accessible and useful.

• Google offers a variety of advertising solutions including display, mobile and video ads as well as simple text ads.

AdWords is a self-service program that facilitates the

creation of online ad campaigns – it helps you find new customers who are looking for what you have to offer.

• Google has the technology to determine user interests and

target advertisements so they are relevant to their context and the users that views them.

• Google also offers an analytics service that allows you to

learn about your website so that you can make it more useful for visitors.

What could Google provide BOQ?

• An extensive number of services allowing BOQ to identify

and better target its key customer base and attract other

customer segments – Google technologies will provide better ad positioning and formatting.

49

US STUDY TOUR OCTOBER 2014

Creating markets - eg Google wallet

About the user and what they want

But a lot they can't use and touch because the company is all

about protecting the user and the users privacy etc

No intention to become a bank at the moment.

They don't need to use mngmt consultants - they have the best

ones already working here.

Sergei runs GoogleX - secret projects

Anyone can have an idea and use their 20% time to work on it.

Has to be scalable. It's ok to fail.

Most developers use MacBooks and they are happy for employees

to have iPhones.

50

US STUDY TOUR OCTOBER 2014

51

US STUDY TOUR OCTOBER 2014

52

US STUDY TOUR OCTOBER 2014

53

US STUDY TOUR OCTOBER 2014

54

US STUDY TOUR OCTOBER 2014

55

US STUDY TOUR OCTOBER 2014

56

US STUDY TOUR OCTOBER 2014

57

US STUDY TOUR OCTOBER 2014

58

US STUDY TOUR OCTOBER 2014

59

US STUDY TOUR OCTOBER 2014

60

US STUDY TOUR OCTOBER 2014

Facebook Presentation and Tour

Campus 2 years old.

Head of Fin Services - sees technology and FB as the only places

that he can take banking where it will go in the next 10-15 years and still

retain the personal aspect

Designed for productivity

Phone serviced - Mobile Karma

If issue not resolved in 2-3 minutes, they will probably give you a

new phone!

Mission - to make the world more open and connected.

Underlies everything

8000k employees

1.35bill people on the platform

Facebook – who are they?

Company Overview

• Founded in 2004: online social networking service - currently

has around 1.32 billion active users worldwide.

• Recently acquired Instagram and WhatsApp, expanding and integrating its online social media presence.

• Revenue is at $7.87bn and Operating Income is $2.8bn.

Total assets equal $17.89bn. Facebook has 7,185

employees.

• Advertising comprises its primary source of revenue based

on clickthough rates.

What could Facebook provide BOQ?

• As a dominant social media outlet, Facebook could

provide BOQ with an advertising outlet, catering to a wide

range of demographic and socio-economic classes.

61

US STUDY TOUR OCTOBER 2014

Presentation on targeting tools and video capabilities that are new

to the platform.

Targeting, Insights and Management.

Fb has 60% penetration in US, UK and Spain - start getting into the

law of big numbers

Direct Mail

Branding

Online

They dint have the data about what people are buying in the

offline world like supermarkets so they partner with

Acxion

Datalogix

Epsilon

Core audience

Online and offline sources- targeting types ( interests, location,

demographics, behaviours) - sample segments ( interested in gaming,

newly engaged etc)

Incredible scale, real identity across devices, accurate targeting

and measurable

Custom audiences - the people you know on FB

Use"hashed" data - Sure 53. Not identifiable PII data

Takes seconds

Signals to use - email, phone number, Facebook user id, app user

id

62

US STUDY TOUR OCTOBER 2014

Use Intent Data

Core audiences

Custom audiences

People like someone else.

Pixels automatically gathering Fb ids on websites.

Audience insights - free information on anything uploaded on

custom lists on Facebook.

They have interfaces called ads manager and power editor, and

preferred marketing developer

Building brands with Facebook video ads

People are sending more and more through the mobile

environment.

Video consumption is growing rapidly. Really taking off on Fb.

Sight, sound and motion

Building for mobile first and mobile best

Building the best creative canvas possible

They have the reach and the repetition with the number of times

people access their newsfeed a day (avg 14 times)

80% of people have their phones with them for 22 hours a day.

They want to coach providers to put high quality video in so it can

compete with what your target wants to see abut their friends and

family. Reach the right people with relevant creative

63

US STUDY TOUR OCTOBER 2014

Aiming to provide the right advertising to people at the right time

in their lives - based on the information they have about people.

Payments platform - they already have payment credentials for

people who lay games and advertise

People are already doing payments

Can push their ids into a banks platform - how you bank can

become stronger on Facebook.

P2P payments - as countries become more cash less they will get

more traction.

Transferwise costs 80% less than Western Union - huge appetite

for people to move money.

They don't use email within the company- all Facebook messenger

and Facebook groups to communicate.

Completely different feel and culture to Google.

FaceTime requirements not applicable - very flexible.

Cafeteria - mostly all inclusive - line moves faster because people

don't have to pay.

Always in build mode - a lot looks unfinished in the campus to

remind people.

Company all hands- in Hacker Square - M team updates everyone.

Marks office is on the corner.

64

US STUDY TOUR OCTOBER 2014

65

US STUDY TOUR OCTOBER 2014

66

US STUDY TOUR OCTOBER 2014

67

US STUDY TOUR OCTOBER 2014

68

US STUDY TOUR OCTOBER 2014

69

US STUDY TOUR OCTOBER 2014

70

US STUDY TOUR OCTOBER 2014

71

US STUDY TOUR OCTOBER 2014

72

US STUDY TOUR OCTOBER 2014

73

US STUDY TOUR OCTOBER 2014

74

US STUDY TOUR OCTOBER 2014

75

US STUDY TOUR OCTOBER 2014

First Data Visit and Presentation

Primary focus on small to mid tier banks mainly US.

Leads the way in payments globally.

The plumbing before you get to the faucet

Headquartered in Atlanta. Operate in hundreds of countries globally

Privately held by KKR

Card issuing, merchant acquiring, prepaid loyalty, mobile commerce, data analytics

First data – who are they?

Company Overview

• Vision: “To shape the future of global commerce by

delivering the world’s most secure and innovative payment

solutions”

• First Data makes transactions faster and more secure

through its comprehensive product lines across: ATMs, debit

and credit cards, loan account processing, fraud and risk management services.

What could First Data provide BOQ?

• The company’s portfolio of transaction processing services

could be held against BOQ’s existing systems –

weaknesses could be identified and solutions could be implemented.

76

US STUDY TOUR OCTOBER 2014

Looking to partner with small innovative companies in Silicon Valley to harness

innovation and fill product gaps.

They offer distribution to their partners (4000 banks and 6million merchants)

Banks have core businesses being attacked by non- banks without the same

regulatory oversight. Simple, Movenbank, PayPal, Funding Circle, Amazon

Banks have no choice but to digitise, contextualise and differentiate

Don't drown in the sea of sameness

Don't become the Sears of banking - in the middle ground and nothing to either end

of the spectrum- can't make money because they are not at either end of the

spectrum.

combining technology and process to achieve goals.

Customer - eliminate silos, engage in contextual dialogue,treat customers as

individuals, engage in social media

User Experience- Common Ui across platforms, minimise clocks in digital channel,

pictorial guides rather than text, ensure consistency in the UX ( eg what ideo do)

Digital - mobilise every service, speed up transactions, digital marketing, enhance

customer service with digital (make sure all employees can use digital media)

Data - collect new data streams( incentives for customers to opt in), analyse data

(make it accessible to all BUs), protect data (make sur everyone understands

privacy), action from data, data for anti-fraud (develop process that make customers

feel more secure).

77

US STUDY TOUR OCTOBER 2014

Core technology- evaluate core banking systems, update ( or not), use of cloud and

SaaS solutions, outsource,

Security - evaluate security vis a vis UX, on-boarding, communicate security to

customers, utilise social media to develop a better view of customers

Compliance -automate using data ( use online and social media footprint), ensure

flexibility, communicate with regulators eg Lending Club now going IPO

Big themes for Commercial Banks

SMB lending

Supply Chain Finance

Go Mobile

Big data

SMB - mid, small and micro 26 mill in US

Square focus on micro businesses

SMBs are using more and more software - accounting, finance, operations, payroll

etc.

Banks should connect to those applications to target the SMBs

AWS - Amazon Web Servies - provides services to SMBs eg hardware not required,

use salesforce.com for CRM

20% approval rate for SMBS loans

Banks look at personal credit whereas credit unions and alternative lenders will use

social media

Smaller banks are being consolidated into the bigger ones and adopting their credit

policies.

SMB spend an enormous amount of time applying for credit - 26 hours.

78

US STUDY TOUR OCTOBER 2014

Lending Club and other disrupters will take their place.

lendio.com OCX, Creditera, Fundera, Boefly, lending club, funding circle, ondeck,

affirm connect SMBs and FIs

Problem solved with bank reach and distribution (they have the customers)

combined with alternative lender efficiency

Eg WBC and Society One

Mobile - SMBs use tablets for everything - opportunity for the bank to connect and

put a wrapper around this. SAP have promoted the mobileCFO - banks can add value

to this.

Big Data - Volume, velocity, variety,veracity/uncertainty. Insights without action are

useless

Banks can ensure their SMB gain insights from data.

Other Innovation Hubs for Fintech - London, Berlin, Israel

79

US STUDY TOUR OCTOBER 2014

Ripple Labs

BDM used to work for FiServ Chris Larrsen - started Prosper Ripple - what do distributed systems mean for payments? Everything here is in the payments area The problem with payments - esp cross border Bitcoin A protocol for Real time payments What does this mean for banks - the bottom line Ripple Labs is the company and Ripple is the protocol for real time funds settlement - powering settlement for instant low cost transfer 75 employees Founder of eloans started Ripple in 2012 Payments and Funds Settlement are 2 distinct activities. Cross border payments USD To JPY - requires several intermediaries - slow risky and expensive

Ripple – who are they?

Company Overview

• First established in 2004 with the latest system completed in

2011. Designed to eliminate Bitcoin’s reliance on centralised

exchanges, use less electricity and perform transactions quicker than Bitcoin.

• Vision: Provide liquidity for payments globally; any currency,

no fees, open markets – this will create greater efficiency and innovation for their customers.

• In 2014 contracted with 2 US banks to use Ripple for real-

time, cross-border payments. It will allow online banking to increase in speed, allow instant transfer or funds

internationally, and increase trade volume capabilities whilst

ensuring data security.

What could Ripple provide BOQ?

• Increased speed of BOQ’s transactions leading to greater

efficiency, trading volume, and customer satisfaction.

• Allow for instant fund transfers across boarders – opening the opportunity for efficient international fund

management.

80

US STUDY TOUR OCTOBER 2014

Lack of transparency- and inability to know whether payment will be available on any given day and what fees will be taken out Payment Instructions are sent in real time but settlement of funds always lag. Synchronisation and risk management required Bitcoin's breakthrough - decentralised currency and settlement ( but all the focus is on the currency aspect) Ripple is also distributed technology just like Bitcoin but with some differences To use the Bitcoin technology, you need to transact in Bitcoin- limitation for FIs and creates the need for Bitcoin exchanges and new players assume the custodian role (non regulated, non financial entities). The success of the model depends on the world adopting Bitcoin There are hundreds of other coins vying for the same adoption Ripple capabilities- a decentralised ledger, real time domestic and cross border settlement capabilities, lowers liquidity risk, lowers operational cost and fx costs. They bring market makers to the table and the function of providing liquidity is distributed across 10 market makers - the 2 institutions approve and know who the market makers/ liquidity providers are and they prefund accounts and then the messages execute 2 opposite intra-bank transfers. All they need is one major bank in each region to be able to do this. An additional tool for banks to send funds worldwide. Instructions and Settlement synchronised CBW Bank and Cross River Bank in the Us already using and the Fed Reserve has given public recognition. Lloyds about to use BBVA using Fidor was the first to use the Ripple protocol Top 5 banks in US currently integrating 4 in the UK and EU An additional 12+ globally.

81

US STUDY TOUR OCTOBER 2014

Standard Treasury

Disruptions in Fin Services Cofounder and CEO His 4th start up has sold 2 of them and at the moment he also runs an investment fund Started in late 2011 9 employees The vast majority of how we understand money is on a ledger in a spreadsheet. Digitisation creates a real tension inside FIs - they are used to creating products within their own infrastructure and distributing through their proprietary distribution channels How does 80% of the global population having a smart phone and all the access that provideschange how you manage your bank in a global credit market place Disaggregation - deposits, lending, payments all going in different directions. Standard Treasury - starting a bank to provide services and infrastructure to 3rd party eg Asperg or Wonga in the UK They will provide regulation as a service to non bank FIs - KYC and AML, Escrow, Trust. Banks feel like they need to own the relationship with their customer but the customer sees the bank as a place to store value and get some credit when they need it. They provide very little value to customers. They will compete against wholesale banks - eg Wells Fargo Citi Deutsche Walgreens - a rack filled with cards issued by white labelled banks. PayPal uses Wells Fargo as their bank and the fine print tells you that your account is

Standard treasury – who are they?

Company Overview

• Received $2.7m in funding in 2014: based in San Francisco, CA. Goal: to make it easier for businesses to deal with their

banks through standard APIs (application programming interface) that ease transfers and other transactions.

Integrating banking services for small businesses and start-ups is overly complicated.

• Banks generally do not create their own software, they

purchase it from other vendors.

• First product: RESTful API – processes electronic cheques,

book transfers, account opening and closing, and foreign

currency quoting and execution.

• Has contracted with one of America’s five largest banks and is working with several other mid-size and regional ones to

launch their own API platforms.

What could Standard Treasury provide BOQ?

• The opportunity to be an industry leader in Australia as a first-adopted of new technologies.

• The RESTful API would increase efficiencies within BOQ,

and increase the customer experience.

82

US STUDY TOUR OCTOBER 2014

with Wells Fargo. Chemical Bank provided a facility to Macdonalds so that they could lend money to their franchisees. Banks will always be able to generate significant value relative to the value that they create through better and better risk management. The concept of an API. Stripe, Braintree Stripe takes what Wells Fargo does and translates it API Banks should be an API provider Uber is a financial services company - a payment network. They collect $ from riders and distribute it to the drivers - they will start to provide credit to drivers for petrol and cars and probably also insurance based on where they are driving. AirBnB is a specific form of foreign exchange platform. Many vertically specific forms of payment and transaction popping up and no one complains about the margin they take because they perceive value in the transaction - unlike banks where they see no value. Bundling and Unbundling - a value in the bundle that is more than the value of the individual parts. What if the bank gave away the phone with unlimited calls and data based on the banking relationship - extend the bundling. Unbanked 1 in 6 Americans- increase financial inclusion by building a low cost bank to profitably bank these individuals- an opportunity for non banks. Will banks compete, partner or die? WONGA, Lending Club, Prosper - use various types of big data to underwrite the credit Most non banks use hedge funds to put up the capital. Banks have a technology and culture problem as well as a technology culture problem. Fiserv and Temenos - terrible software. An opportunity for banks to write their own software and give it away. But regulators don't want to certify anything that isn't already certified. Amazon Web Services - premier cloud provider in the world. The CIA and UK tax system run on AWS. UBS operates 12 data centres around the world but they operate on 20% utilisation. They pay people who are technically retired to maintain their systems because they are the only ones who know. Why not migrate to the cloud now? Wells Fargo still uses an IBM Mainframe from the 1970s. They now manufacture their own parts for it..... Vertically specific payments network. Standard Treasury will make it easier for them to integrate because they need to hold the money somewhere. 1 year away from launching "the bank" RBS had a critical outage and customers wee unable to get funds for a week - they

83

US STUDY TOUR OCTOBER 2014

survived because they were owned by the government. Most other banks wouldn't survive that. We live in a world we need to assume that the hardware will fail Banks have security by obscurity - if we don't talk about it, it must be secure. If they talk about how secure they are, they will be perceived to be secure. Most bank executives have no idea how technology works- they believe that if they pass the audit, it is secure. That is compliance, not security Facebook on a profit per employ basis is 30 times more profitable than JPMorganChase Close to half of Bank of America's employees at in IT Google runs on less than that number. Board,c-suite, executives- are they the people who can lead you to the future? Management are usually a mirror of the board.....very few banks get it. BBVA - the Chairman wrote a let in the financial paper talking about the digital disruption and the directions the bank was going in. You have to be willing to canabilise yourself otherwise someone else will come for you.

84

US STUDY TOUR OCTOBER 2014

85

US STUDY TOUR OCTOBER 2014

L'Atelier - BNP Paribas Group

Anticipating new digital trends thy will impact your business Natalie Dore - CEO Atelier North America Dogpatch - downtown SF - old factories transformed to new buildings for start ups and artistic community They share the space with some start ups Team of 7 - will be 10 next year Innovation tracking, sharing and taking action Detecting new uses of digital and analysing their impact on individuals and organisations Also have offices in nth and Sth America - HQ in Paris. Advisor in the BNP group on digital strategies - being on the ground allows early detection and relationship building - they have a huge network and loads of partnerships with start ups, think tanks, innovators, institutions and non profits and colleges and universities Profit Centre - Income for customers 50% BNP and 50% external customers Universities - Stanford and Berkeley

L’Atelier BNP Paribas – who are they?

Company Overview What could L’Atelier provide BOQ?

• Established in 1978: purpose is to bring innovative ideas to various industries and help them identify key trends in their

business.

• Main activities centre on online communication, online

marketing, e-commerce, CRM and company innovation –

services are provided in consulting, market monitoring and learning expeditions.

• Principle vocation is to place leading-edge IT innovations

within the context of specific company needs.

• Has established a present across Europe (Paris), the

Americas (San Francisco) and Asia (Shanghai) allowing it to

follow experimental initiatives in different environments.

• Previous clients include HP, IBM, Oracle and Adobe.

• Consulting:

• A comprehensive analysis of BOQ’s online

communication and marketing tools, an the opportunity

to transform these to meet leading edge technologies.

• Assist in aligning BOQ’s IT strategies with the general

company strategy.

• Sharpen BOQ’s view on the likely future impact of IT

on the company and the financial services market generally.

86

US STUDY TOUR OCTOBER 2014

Apple Google Facebook and Twitter Sequoia Capital and KPCB Topics Smart City - $1.5 trill in revenue will be generated from the Smart City market by 2020 Connected Objects (home and car)- 80bill connected objects in 2020 and $1900bill revenue worldwide Big data analytics - $114bill estimated turnover by 2018

87

US STUDY TOUR OCTOBER 2014

88

US STUDY TOUR OCTOBER 2014

89

US STUDY TOUR OCTOBER 2014

90

US STUDY TOUR OCTOBER 2014