Using Billing Information to Grow Your Lab Profitably · 2013-11-19 · Lab Outreach Source: P....

13

Lab Outreach Source: P. Thomas Hirsch, President and Cofounder, Laboratory Billing Solutions, (603) 766-8204, [email protected] Using Billing Information to Grow Your Lab Profitably Not all growth opportunities for outreach programs represent good business for the laboratory. In addition to making sure that you can adequately service the new clients you are pursuing, it is important to understand whether the growth meets your financial objectives. This article will help you to: ● Learn what type of billing information you should be looking at to determine whether your program is meeting your financial as well as service objectives. ● Understand the factors that determine client profitability and what variables can be affected to improve the contribution margin of a client or line of business. ● Recognize the collections pitfalls that should be mastered to ensure that you optimize the financial benefit of your program. What Type of Information is Helpful? “It’s a difficult process to get good information and understand how it can help you run your laboratory,” says P. Thomas Hirsch, President and Cofounder, Laboratory Billing Solutions. “The first thing you need to look at is patient activity and volume. One of the challenges for most labs is simply knowing how many patients they see on a daily basis. In terms of information you need to run your business, understanding your patient activity is the most important parameter. Even if you don’t know how much you are collecting at times, you always need to track overall patient volume on a daily and monthly basis, as well as by location. Hopefully, your billing function is going to generate claims based on the lab’s activity. Ideally, you want to know that you see on average 1,000 patients a day, you have 21.5 days a month of activity, and you should be averaging about 21,500 patient encounters a month. You want to know what the gross charges are associated with those encounters and you want to track how many CPT [current procedural terminology] codes you have per accession. You should be able to get this information independent of how well, or not well, the hospital does the billing function. However, this volume is going to drive many of your decisions as well as reconciling the financial implications of your business.” According to Hirsch, on a monthly basis you should also know what was billed out in terms of gross charges. It should roughly correlate with the volume that was produced on the lab system. “I refer to this as activity reporting. For example, if you have 10,000 patients a month and you know the average charge is $100 a patient, you should generate $1.0 million a month in charges. Did your billing system generate close to a $1.0 million in charges? The numbers do not always add up and part of the reason is that the lab activity is based on when the testing was ordered and billing is based on when the claim finally gets submitted. While you may know how many patients the lab processed in the

Transcript of Using Billing Information to Grow Your Lab Profitably · 2013-11-19 · Lab Outreach Source: P....

Lab Outreach Source: P. Thomas Hirsch, President and Cofounder, Laboratory Billing Solutions, (603) 766-8204, [email protected]

Using Billing Information to Grow Your Lab Profitably Not all growth opportunities for outreach programs represent good business for the laboratory. In addition to making sure that you can adequately service the new clients you are pursuing, it is important to understand whether the growth meets your financial objectives. This article will help you to: ● Learn what type of billing information you should be looking at to determine whether your program is meeting your financial as well as service objectives. ● Understand the factors that determine client profitability and what variables can be affected to improve the contribution margin of a client or line of business. ● Recognize the collections pitfalls that should be mastered to ensure that you optimize the financial benefit of your program. What Type of Information is Helpful? “It’s a difficult process to get good information and understand how it can help you run your laboratory,” says P. Thomas Hirsch, President and Cofounder, Laboratory Billing Solutions. “The first thing you need to look at is patient activity and volume. One of the challenges for most labs is simply knowing how many patients they see on a daily basis. In terms of information you need to run your business, understanding your patient activity is the most important parameter. Even if you don’t know how much you are collecting at times, you always need to track overall patient volume on a daily and monthly basis, as well as by location. Hopefully, your billing function is going to generate claims based on the lab’s activity. Ideally, you want to know that you see on average 1,000 patients a day, you have 21.5 days a month of activity, and you should be averaging about 21,500 patient encounters a month. You want to know what the gross charges are associated with those encounters and you want to track how many CPT [current procedural terminology] codes you have per accession. You should be able to get this information independent of how well, or not well, the hospital does the billing function. However, this volume is going to drive many of your decisions as well as reconciling the financial implications of your business.” According to Hirsch, on a monthly basis you should also know what was billed out in terms of gross charges. It should roughly correlate with the volume that was produced on the lab system. “I refer to this as activity reporting. For example, if you have 10,000 patients a month and you know the average charge is $100 a patient, you should generate $1.0 million a month in charges. Did your billing system generate close to a $1.0 million in charges? The numbers do not always add up and part of the reason is that the lab activity is based on when the testing was ordered and billing is based on when the claim finally gets submitted. While you may know how many patients the lab processed in the

month of April, billing activity is based on what was billed out of the system. You could easily have a situation where the charges may be a $1.0 million for the month but the hospital only bills out $750,000 because they’re a week behind in order entry in terms of registering claims.” As a result, the best way to determine whether billing is keeping up with the lab it to look at several months of gross charges compared to patient activity. Is the average charge level consistent with what you think it should be? Is the number of tests per requisition consistent? Several issues can cause discrepancies, including: ● Have all lab patients been registered and is there usually a backlog? ● How many claims/dollars are suspended or on an edit for missing information? ● Are claims with missing information researched or written off? “Invariably it’s a challenge to make the lab system data correlate well with the billing system since charges get generated on their own time frame independent of the date of service. There are a lot of factors that impacts your ability to get paid for everything that you produce on the lab side. However, regardless of how you do your billing, it’s important to understand whether you are at least billing for all the patient activity and work you are doing,” Hirsch emphasizes. “Ultimately, what really tells you whether you’re successful is cash. Independent labs primarily care about cash while hospital labs, because they are part of the larger system, are worried about accrual rates and what they’re going to report in terms of gross revenue and their contractuals—which makes what comes in as cash is almost irrelevant. While its interesting how different people focus on different things, ultimately cash is the determination of how well you’re doing with your laboratory. What’s difficult in many hospital labs is that while they can tell you their gross revenue, they can’t always tell you their cash collections. The reason is that hospitals often post charges at the account level with everything else associated with a patient—in other words, they don’t differentiate lab receipts. And even when cash is applied, it’s not date-of-service based—it is based on when the cash is collected and posted. So it’s hard to tie it back to patient activity,” he says. Most labs assume an accrual rate as a percent of charges to gauge revenues. “In other words, overall a hospital may collect 35% of charges so it will apply that number to the laboratory. However, the laboratory’s collection rate may not be similar due to the fact that the patient payer mix for lab services can be dramatically different than the hospital’s general mix. Also many payer contracts may pay for outpatient lab services on a fee schedule whereas other services are paid as percentage of charges. Using the percent of charges represented by the Medicare fee schedule is another measure that hospitals utilizes to measure performance. Unfortunately any of these measurements may give you a false sense of security.”

Hirsch notes that the challenge for everybody in this business is to validate what they are truly collecting and what they should collect—i.e., the percentage of collections being assumed. “One of the things you can do is look at EOBs [explanation of benefits] from your top payers and review the top 50 tests to see how they are being paid. Another option is to come up with an accrual rate for a payer. However, you need to adjust it for frequency because the payer may pay 30% of charges for one test and 50% on another. So you need to weigh the volume to come up with a collection rate.” The mix has a dramatic impact on what you realize in collections. “For example, a lot of people don’t want to do a contract if it’s 90% of Medicare. However, when you look at many Blue Cross plans, they pays 90% of Medicare. Compared to Medicare you are going to be surprised that your revenue per CPT code and accession is much higher with Blue Cross than it is with Medicare. The reason is that pap smears and certain screening tests such as lipid profiles pay relatively well whereas some tests ordered by Medicare recipients pay less well, such as PTs [prothrombin time] and UAs [urinalysis]. So even though Blue Cross is 90% of Medicare, your revenue per accession and CPT code can be higher. Understanding how all your payors pay and focusing on opportunities to get better reimbursement where you have high volume of tests can make a real difference,” Hirsch suggests. In general, he comments, most labs are doing far worse than they think they are. “It’s really hard to understand what you are getting paid and you don’t want to assume it’s worse than you think. What we do for clients is actually look at all the adjudicated claims for all their financial classes. For example, we will look at 10,000 claims for Medicare that were fully adjudicated where they are getting paid 35% of charges and Medicare is 30% of their payer mix. We are able to create an overall collection rate by applying this process to each payer and adding up the percentages to get a total of what can be expected - a number that your business can generate if you do everything right. Many people have had to adjust their thinking about their business and what really was profitable and what wasn’t.” Basic Laboratory Economics While the activity of your gross charges and what you collect is important at the macro level, the next most important thing is to understand what your costs are at the CPT and accession level. “It’s nice to know that I get paid 40% of charges. However, the next thing I want to understand is what does that mean at the CPT code and accession level? All the labs report their financials at the accession level, however, it’s harder sometimes at the CPT level—for example, do they include the venipuncture and travel fees, or just tests? The reason we try to bring the business back to revenue per accession and CPT code is because that’s what your costs are based on. They’re not based on charges. They’re based on your accession and test volume, and the capital you deploy to support your laboratory. Some costs are primarily accession based, such as logistics, customer service, phlebotomy, accessioning, and billing. Other costs are test or CPT code based, such as reagents, technical labor, and send out tests. Finally, you have overhead costs such as space, IT, and some instrumentation that may be fixed, or at least it’s a step

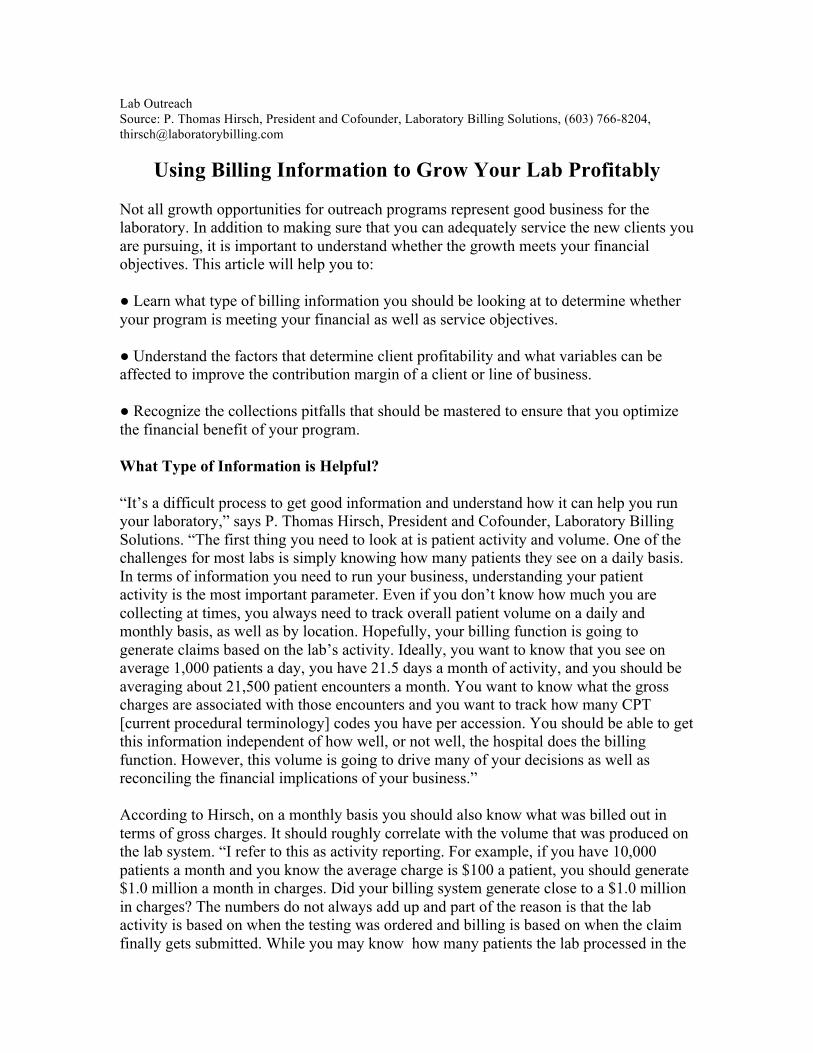

function. You really need to understand your fixed and variable costs and understand when you look at a client or a payer relationship how it relates to your cost,” Hirsch says. According to Hirsch, by simply determining the lab’s cost parameters, you have a clear-cut mechanism to evaluate the profitability of your payer contracts, as well as ultimately your clients. “A lab that understands its unit costs can easily compare its costs to the revenues received by each payer. It will also quickly becomes self-evident what payers are profitable, which contracts are profitable on only a marginal basis, and what contracts are loss leaders. If you struggle with getting this level of information it can be very difficult to make decisions about where you want to invest resources and what type of business you want to go after. Most lab struggles at even getting this level of information. However, the imperative is to be able proactive act on the information to improve the lab’s financial performance.” Understanding Payer Profitability and Revenue Exhibit I illustrates a common way to look at profitability by financial classes. “If your costs are $30 a requisition, for example, you need to know which of your payers or financial classes are paying at least at the rate of your costs. This chart is a representative sampling of a month’s worth of one lab’s data. It tells you that Aetna is 14.6% of the business, Blue Cross is 24.1%, and Medicare is 23.6%. The average revenue per accession is $34.50 and the average revenue per test is $11.90. You can then look at the payers and see which ones are contributing any margin to the lab. While every contract may not be profitable on a fully allocated basis, each arrangement should at least cover marginal costs. You cannot do all your business on a marginal cost basis and you need to be selective where you do price in this manner. One of the great controversies or myths about this business is that marginal costs are only 40% or less of revenue. Marginal costs end up being closer to 75% of fully allocated costs over time,” he points out.

Revenue by Financial Class at CPT Code and Accession Level Exhibit I

“Despite the dramatic growth the larger labs have achieved through acquisitions, doubling or tripling in size in the last 10 years, their unit costs have stayed constant or increased slightly,” Hirsch adds. “And while Quest and LabCorp enjoy far lower supply costs than other labs, their overall costs are not materially lower than well run regional labs. However, they have overhead costs that smaller labs don’t. They are shipping samples much further, most of their production is done on third shift where they’re paying third-shift differential, and they need more instrumentation to produce tests in a shorter production window. Their costs aren’t lower across the board. So when you read an announcement that one of the large labs has done a deal with United Healthcare or Aetna and it appears like it is priced 65 or 70% of Medicare, don’t wonder how they’re making money on it because they’re not. They get infatuated with their theoretical marginal costs and think that the incremental volume justifies the pricing.” Exhibit II illustrates revenue/cost trends at LabCorp and how they doubled in size from 2000 to 2007. “They started doing more esoteric tests, but when you look at their cost per accession you would have thought if they doubled in size over seven years, their unit cost would not have increased much in the same time period, but LabCorp’s did materially,” he notes. Revenue /Cost Trends at LabCorp 2000 - 2007 Exhibit II

“As illustrated in Figure 3, you would As illustrated in Exhibit III on the following page, United is only paying $24 an accession while the costs are $30—but perhaps on a marginal basis this typical lab can hang in there. However, the capitated HMO that is paying $18 an accession is a loss leader. You should renegotiate that or minimize that as part of the business because there’s no money to be made and you are missing an opportunity to service more profitable business.” Most labs do not fully understand the margin impact of each contract.

Understand what Contracts are Profitable Exhibit III

Understanding Client Profitability and Revenue According to Hirsch, while you may have less flexibility regarding which payers you work with, the same discipline to reviewing contracts can be applied at the account level and you may be in a position to do more about this information unilaterally. “You really need to understand which clients are profitable, why they may not be, and what you can do about it.” One issue that affects client profitability is whether they generate an inordinate amount of edits, such as medical necessity where there isn’t appropriate documentation and a high percentage of the work is denied. Other factors include whether the client’s payer mix is unfavorable compared to other practices (i.e., it is more of a capitated plan), whether there is more bad debt based on the amount of co-pays, deductibles, and self-pays that the practice had, does the client sends business only from HMO or select insurers, and whether the test mix ordered by the specialty is simply not well reimbursed regardless of the payer. “We had a client where they were only getting the capitated work from a particular client for approximately $8 a requisition and the rest of the work was going to another laboratory. Our advice was that if they couldn’t get all of the business to make it viable, they should tell the client to send the capitated work to that lab as well. They couldn’t afford to service the client. In addition, based on the state you’re in, the payer mix, and what doctors order, some practices are more profitable than others and some specialties just aren’t as attractive as others,” he says. Another activity of profitability is clearly the number of tests per patient encounter. “You want to make sure that your client revenue meets your marginal costs. While you may have strategic reasons for keeping some clients, you want to at least make sure that there is rationale for all of your business. For example, if you want to keep a material client that has a revenue of $13 a test, but only averages 1.2 test per accessions, at least understand why.”

● Edits. “There clearly is a correlation between the percentage of work that a client generates and requires follow up and the actual revenue that can be realized from the practice. “For all our clients, we basically track the percentage of work that hits an edit and how long it takes to get them cleared. While some practices with a high percentage of edits have high collection rates, invariably the longer it takes to process claims the greater chance of not getting paid. Initially, I also thought that clients that have a high percentage of edits would be normally less profitable—but that wasn’t the case. It really depends on how good our clients are at getting us information that’s needed to collect that revenue. The whole edit game is getting more significant. None of the payers really want to pay and they are looking at ways to make you work a little harder to get the money. That’s why managing how well your clients respond for missing information, such as giving you appropriate diagnosis information, is a critical aspect of the business,” Hirsch explains. ● Payer Mix. Another major issues in terms of client profitability is obviously the payor mix. If you have a high percentage of capitated work it can make it very difficult for a client to pass your revenue thresholds. Be leery of the clients who just send you managed care work. Being able to analyze this is important because you have a finite capacity to service your business and if you devote a lot of your resources on unprofitable business, you’re undermining the rest of your business. While you try to service everybody the same, you could end up compromising your service for your most profitable clients while meeting the requirements of the business you really don’t want. You need to be selective.” However, a reasonable revenue per CPT code or accession is only part of the equation, Hirsch comments. “You need to compare it with similar practices to make sure the numbers make sense. The percentage of charges is a good indicator for some specialties. For example, I was looking at some endocrinologists for a client and noticed that there was one that was $35 a requisition. However, the percentage of charges that were paid was only 17%. Upon closer examination, they had a lot of send outs and compared to other endocrinologists who were in the $50 a requisition category, this wasn’t as profitable business.” In the end, you need to look at many different indicators because no one metric by itself tells you everything you need to know. “For example, you look at price per accession and per CPT code because both are telling you something different about the business. Since so much of a lab’s business is accession-based, you can often afford to have a lower reimbursement per CPT code if doctors order more CPT codes per requisition,” he explains. ● Test Mix. “Another issue obviously that affects client profitability is what they order. One of the ironies of the [lab] business is that tests are reimbursed at widely different rates even though they cost the same to produce. This is really a function of the history of the Medicare fee schedule for the last 20 years. However, it really costs you roughly the same to do a urinalysis and a PT as it does to do a metabolic, a TSH [thyroid-stimulating hormone], or a lipid profile in your laboratory. While there are really no material

differences, you have practices that order a lot of a certain type of tests (i.e., protimes, urinalysis, single chemistry tests) that are less profitable. At the end of the day, 80 percent of your costs are accession based rather than test based. So when you look at business lines such as nursing homes that tend to order fewer tests per requisition, it can be very difficult to make money of you are not effectively billing for travel. Since many costs are encounter-based - i.e., phlebotomy, logistics, accessioning, customer service, and billing. “A laboratory that experiences more tests per requisition, to some extent independent of the mix, are usually more profitable - unless a disproportionate amount of their work is capitated at low fees. Utilization rates range from 2.5 to 4.5 CPT codes per accession.” ● Field Costs. Another area to look at in terms of profitability is field costs. “Everyone makes investments in infrastructure in terms of new patient service centers (PSC’s), in-office phlebotomists, stat labs, or expanded courier routes in order to maintain or add new clients. While these investments are built into your total cost numbers you still need to examine these resources independently. Again, you have only so many PSC’s you can manage and staff every day. If you have many marginal locations you run the risk of having staffing issues that can compromise service where you can less afford it. As a general rule, the cost of an in-office phlebotomist or a patient service center should be no more than 20 to 25 percent of the revenue you get from that location. A client who averages $45 a requisition is not a good deal if the cost of the phlebotomist represents half the practice’s revenue.” According to Hirsch, analyzing client revenue is the same as looking at financial classes. “You want to understand key metrics such as what percentage of gross charges you’re paid, how much volume they generate, what you get paid on a test and accession basis, and how many tests they generate per requisition. Again, this is helpful information to better understand what work you may or may not be getting from clients. [See Exhibit IV] Perhaps they have issues that you need to investigate—i.e., edits or test mix. You need to determine what you can do to make the client more profitable or whether you should retain them.” Client Revenue at CPT Code and Accession Level Exhibit IV

Optimizing Collections to Sustain Margin According to Hirsch, even if you don’t know what your gross charges are, you still need to collect payments. “There are many issues that impact how well you can collect in the laboratory. In fact, when you look at the claims that get denied on the front and back-end and you are looking at about 30% of your business that may not be paid initially. Anywhere from 10 to 25% of Medicare requisitions lack appropriate medical necessity documentation. The next culprit is missing or invalid diagnosis. There are also file definition issues in many lab systems—i.e., test claims that are not defined, and missing UPINs [unique physician identification numbers], that can hold up another 10 to 15% of the work. Finally, missing requisitions because of a lack of proper process controls and other interface issues can account for a surprising number of claims that never get billed. Compounding these issues, the average lab has from 5 to 20 days of billing in process at any given time in addition to pending tests and waiting 72 hours to bill Medicare.” Following up on missing information is a challenge. “A recent study noted that perhaps as many as 50% of hospital and independent labs acknowledge that their follow-up processes are inadequate or non-existent. This represents 20 to 30% of the revenue that might not be collected. Very few labs systematically analyze edit information to identify opportunities to modify client behavior and simply focus on reconciling the missing information. You want to be proactive and get to the point where you can impact clients to do a better job. Tracking response rates and the amount of edits that are not resolved can also tell you more about the quality of your client’s business,” Hirsch says. Exhibit V is an example of a report that Hirsch would generate to look at the number of accessions that hit an edit. “Your goal is to get all the information you need to bill. However, if you’re not even looking at the systemic reasons for why bills are not initially generated and following up at the client level, you’re leaving a lot of potential revenue on the table.” Edit Performance by Client Exhibit V

Managing accounts receivable (AR) is another challenge in addition to the upfront problem of getting missing information. “Managing claims that aren’t paid and days sales outstanding [DSO’s] is an area where labs can do better. Every lab has DSO’s in the greater than 150 day category. Reasons include patients that wait until the final notice to inform you of their coverage/policy number, insurers that take several inquires to tell you the patient is no longer covered by their plan(s), and claims that are rejected and need to be investigated and resubmitted. Having accurate contractual targets by payer will enable you to set realistic expectations for the older AR in terms of cash collections,” Hirsch advises. Many labs and hospitals write-off claims greater than 180 days, which is a significant lost revenue opportunity given the cycle issues associated with lab billing. “Software should be able to sort outstanding claims by payer, date of service, and last bill date to help manage claims and ensure they are being worked proactively. While the average percentage of claims that are denied is 10 to 12%, it can be higher if you don’t have up front edits in place. Working the rejected claims requires a systematic undertaking, but critical in capturing up to 10% of the lab’s remaining potential revenues. When you have multiple payers to track over an extended period there are plenty of opportunities for claims to become neglected. Capabilities to identify issues and quickly focus resources can help optimize collections and realize more revenue. Exhibit VI illustrates how to segregate a financial class detail by the last bill date. “Ultimately, you want to work every single claim on your AR. If your hospital is doing your billing, ask them to give you a report about what’s outstanding and what is being done to reconcile it. Keep in mind that there’s a tendency to write off claims a lot sooner than necessary,” he comments. ATB Detail by Financial Class Exhibit VI

According to Hirsch, while DSO’s is an important measure of the speed of collections, it is not necessarily indicative of how good a job you are doing of optimizing collections. “A lot of billing systems don’t include the work that’s unbilled as part of the DSO

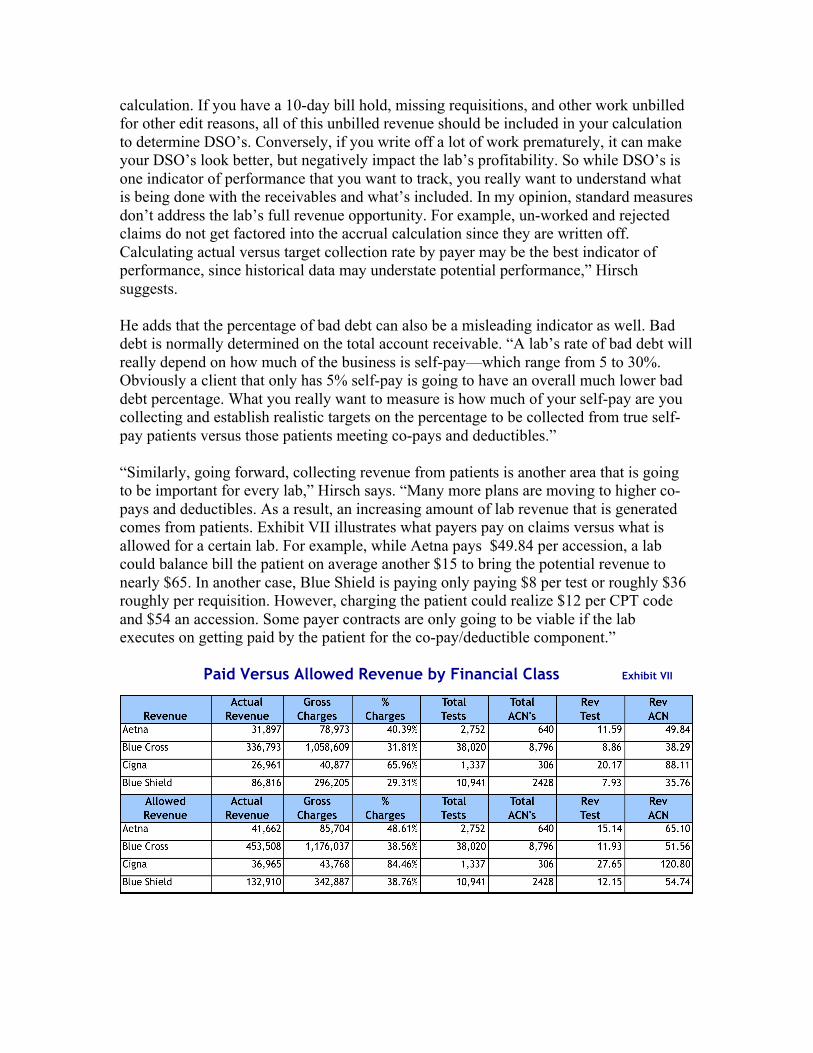

calculation. If you have a 10-day bill hold, missing requisitions, and other work unbilled for other edit reasons, all of this unbilled revenue should be included in your calculation to determine DSO’s. Conversely, if you write off a lot of work prematurely, it can make your DSO’s look better, but negatively impact the lab’s profitability. So while DSO’s is one indicator of performance that you want to track, you really want to understand what is being done with the receivables and what’s included. In my opinion, standard measures don’t address the lab’s full revenue opportunity. For example, un-worked and rejected claims do not get factored into the accrual calculation since they are written off. Calculating actual versus target collection rate by payer may be the best indicator of performance, since historical data may understate potential performance,” Hirsch suggests. He adds that the percentage of bad debt can also be a misleading indicator as well. Bad debt is normally determined on the total account receivable. “A lab’s rate of bad debt will really depend on how much of the business is self-pay—which range from 5 to 30%. Obviously a client that only has 5% self-pay is going to have an overall much lower bad debt percentage. What you really want to measure is how much of your self-pay are you collecting and establish realistic targets on the percentage to be collected from true self-pay patients versus those patients meeting co-pays and deductibles.” “Similarly, going forward, collecting revenue from patients is another area that is going to be important for every lab,” Hirsch says. “Many more plans are moving to higher co-pays and deductibles. As a result, an increasing amount of lab revenue that is generated comes from patients. Exhibit VII illustrates what payers pay on claims versus what is allowed for a certain lab. For example, while Aetna pays $49.84 per accession, a lab could balance bill the patient on average another $15 to bring the potential revenue to nearly $65. In another case, Blue Shield is paying only paying $8 per test or roughly $36 roughly per requisition. However, charging the patient could realize $12 per CPT code and $54 an accession. Some payer contracts are only going to be viable if the lab executes on getting paid by the patient for the co-pay/deductible component.” Paid Versus Allowed Revenue by Financial Class Exhibit VII

Hospital vs. Independent Lab Licensure The table below illustrates the pros and cons of having a hospital versus an independent lab licensure.

“The advantage of a hospital-based lab is higher reimbursement. However, an independent lab can get higher reimbursement by having a hospital support them. While it’s harder for an independent lab to submit claims, ultimately it’s better to retain you hospital lab licensure if you are an outreach program. There are also other factors that affect a licensure decision.” Including: ● the lab is moved to an offsite location ● the lab is serving a market that extends beyond affiliated physicians and providers or a high percentage of the work is outreach rather than hospital based patients ● the outreach program is extensive, serving more than 1,000 patients daily ● ownership situation changes and involves more than one hospital or other owners

“In general, if you debating what to do, I would suggest sticking with a hospital-based licensure,” Hirsch says. Final Thoughts and Possible Strategies “You can not proactively manage the business if you do not have a clear understanding of the fundamental economics,” Hirsch emphasizes. “You also need to understand what payer and client arrangements add value for your laboratory and which relationships are problematic. You can start by knowing your fully loaded cost and net revenue per test (CPT) and accession. You need this information to make intelligent business decisions. But keep in mind that getting that information is only the start. I would guess that only 10 to 15% of the labs in this country have all the information they need to really manage their business - and of that number, only 5% act on the information proactively to better develop strategies to position themselves for success.” In terms of strategies for success with an outreach program, Hirsch says that one key is to exercise the discipline to discard low margin business. “You need to discard it or make it profitable. Understand what is consuming your resources and figure out how to make it work for you. Another strategy is to pursue more profitable markets or niches (i.e., practice specialties) that provide more favorable reimbursement and play to your lab’s strengths. You can also renegotiate payer contracts. When I operated a laboratory I was in negotiation with our payers continuously to create a win-win relationship. You also want to focus on specific tests and/or un-reimbursed services that can make the relationship more financially viable.” Other strategies include increasing carve outs and tying cap rates to utilization, adjusting pricing for certain tests or across the board, re-pricing to eliminate certain client bill arrangements, and revisiting cost structures—particularly for field costs associated with procuring the business. “It is really an ongoing process of challenging assumptions. However, instilling this type of discipline can make your program very profitable and a real contribution to the hospital,” Hirsch concludes.