U.S. Tax Seminar Inbound Investment in … · November 2013 6 U.S. Tax Seminar ... August 2013,...

22

U.S. Tax Seminar Inbound Investment in U.S. Real Estate 25 November 2013 Omri Yaniv, Tax Partner Tamar Sharon, Tax Manager www.pwc.com/il

-

Upload

vuongtuong -

Category

Documents

-

view

214 -

download

0

Transcript of U.S. Tax Seminar Inbound Investment in … · November 2013 6 U.S. Tax Seminar ... August 2013,...

U.S. Tax Seminar Inbound Investment in U.S. Real Estate

25 November 2013

Omri Yaniv, Tax Partner

Tamar Sharon, Tax Manager

www.pwc.com/il

November 2013

2

U.S. Tax Seminar

PwC

Agenda

1. Investments by Individuals

• Direct Investment in Residential Property

• Investment through Fund/ other Vehicle

2. Investments by Corporations

3. Investments by Institutional Investors

4. REITs

November 2013

3

U.S. Tax Seminar

PwC

Foreign Net Real Estate Investments in the U.S., by Buyer Origin, 2009–2013

Source: Emerging Trends in Real Estate 2014, PwC & Urban Land Institute, October 2013

November 2013

4

U.S. Tax Seminar

PwC

Foreign Real Estate Investments in the U.S., by Buyer Origin and Property Type

Source: Emerging Trends in Real Estate 2014, PwC & Urban Land Institute, October 2013

November 2013

5

U.S. Tax Seminar

PwC

Maturing Loans: Preferred Strategy for Lenders

Source: Emerging Trends in Real Estate 2014, PwC & Urban Land Institute, October 2013

November 2013

6

U.S. Tax Seminar

PwC

Anecdotes

• In 2012 foreign investments in U.S. real estate constituted 9% of total real estate investments. In comparison, between January - August 2013, foreign investors acquired approximately $22.8 billion in U.S. real estate 13% of all real estate transactions in the U.S. during that period!

(According to Real Capital Analytics)

• In recent years, foreign investors have played an increasing role in the residential market trend – particularly in Florida (e.g. investing in single-family homes, condos, multifamily apartments)

November 2013

7

U.S. Tax Seminar

PwC

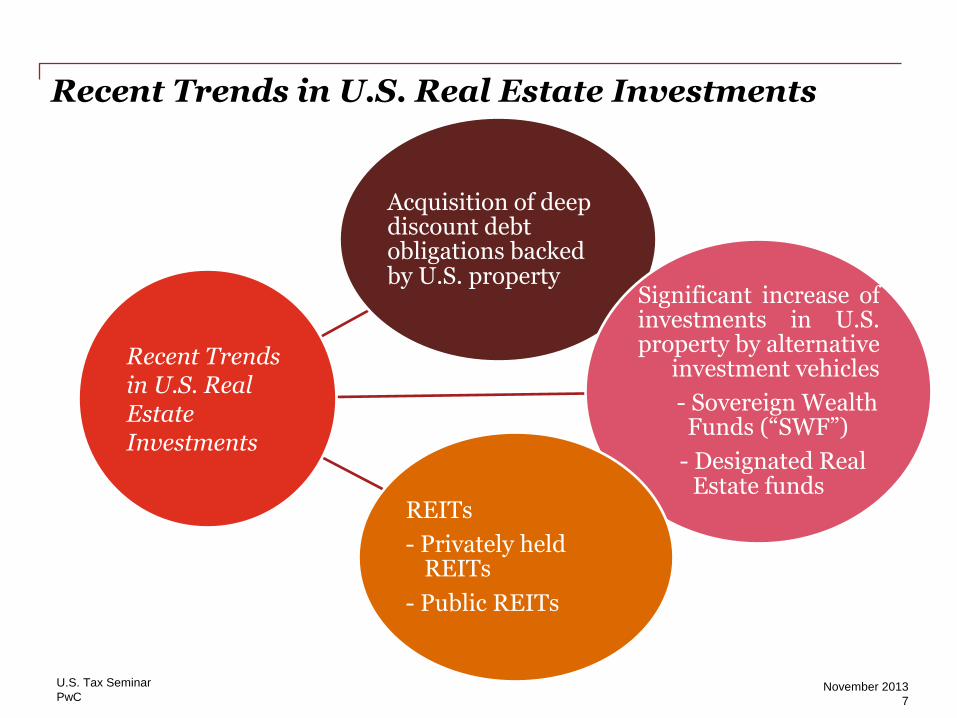

Recent Trends in U.S. Real Estate Investments

Acquisition of deep discount debt obligations backed by U.S. property

Significant increase of investments in U.S. property by alternative

investment vehicles

- Sovereign Wealth Funds (“SWF”)

- Designated Real Estate funds

REITs

- Privately held REITs

- Public REITs

Recent Trends in U.S. Real Estate Investments

November 2013

8

U.S. Tax Seminar

PwC

State Tax

Investment in U.S. Real Estate Property - by Individuals

Key U.S. Tax

Considerations

Ongoing taxation of

rental income

Taxation of Capital

Gains “CG” on

disposition

Estate tax

Repatriation upon Exit

Real Estate Transfer

tax

U.S. Compliance

Federal Tax

November 2013

9

U.S. Tax Seminar

PwC

Individual Israeli Residents Investing in U.S. Residential Property Common Investment Structures

Family member

U.S. Bank debt

(non-recourse)

U.S. Property

Israeli Family

Company

LLC

November 2013

10

U.S. Tax Seminar

PwC

Individual Israeli Residents Investing in U.S. Residential Property Key U.S. tax considerations

1. Rental income generally taxed at marginal tax rates on a net basis

2. State tax may / may not apply (e.g. Florida - no State tax, NY/CA – high State tax)

3. Long Term CG tax may apply if property held for >1 year. In most cases LTCG up to 20% Federal + State if applicable

4. Foreign individuals required to file a U.S. tax return (1040NR)

Family member

U.S. Bank debt

(non-recourse)

U.S. Property

Israeli Family

Company

LLC

November 2013

11

U.S. Tax Seminar

PwC

Individual Israeli Residents Investing in U.S. Residential Property Key U.S. tax considerations

5. Estate Tax – potentially may not apply (since asset is foreign partnership interest)

• Alternatives for prevention of Estate Tax:

- Life insurance policy

- Trust mechanism

Family member

U.S. Bank debt

(non-recourse)

U.S. Property

Israeli Family

Company

LLC

November 2013

12

U.S. Tax Seminar

PwC

Individual Israeli Residents Investing in U.S. Residential Property Key Israeli tax considerations

1. LLC requires election for pass-through treatment (for foreign tax credit purposes only)

2. Rental income - marginal tax rates (generally more attractive than 15%)

3. Foreign Tax Credit (“FTC”) -generally available within limitations.

Family member

U.S. Bank debt

(non-recourse)

U.S. Property

Israeli Family

Company

LLC

November 2013

13

U.S. Tax Seminar

PwC

Acquisition of Discounted Debt Secured by Property • Popular transactions in the wake of the

2008 financial crises:

• If properly structured – most tax-efficient investment in U.S. Real Estate since:

- Discount component is generally not taxed to foreign investors under U.S. tax rules and U.S. sourcing rules

- Interest component is generally not taxed to foreign investors assuming PIE applies

• Assumes “straight” debt (i.e., interest not contingent) and no “equity kickers”

• If property foreclosed then future appreciation taxable in U.S.

Others

Face value $100 Accrual interest $20 Acquisition price $60

U.S. Property

Israeli

Company

U.S. LP $ Bank

U.S. GP

Debt Acquisition of debt

Owner

November 2013

14

U.S. Tax Seminar

PwC

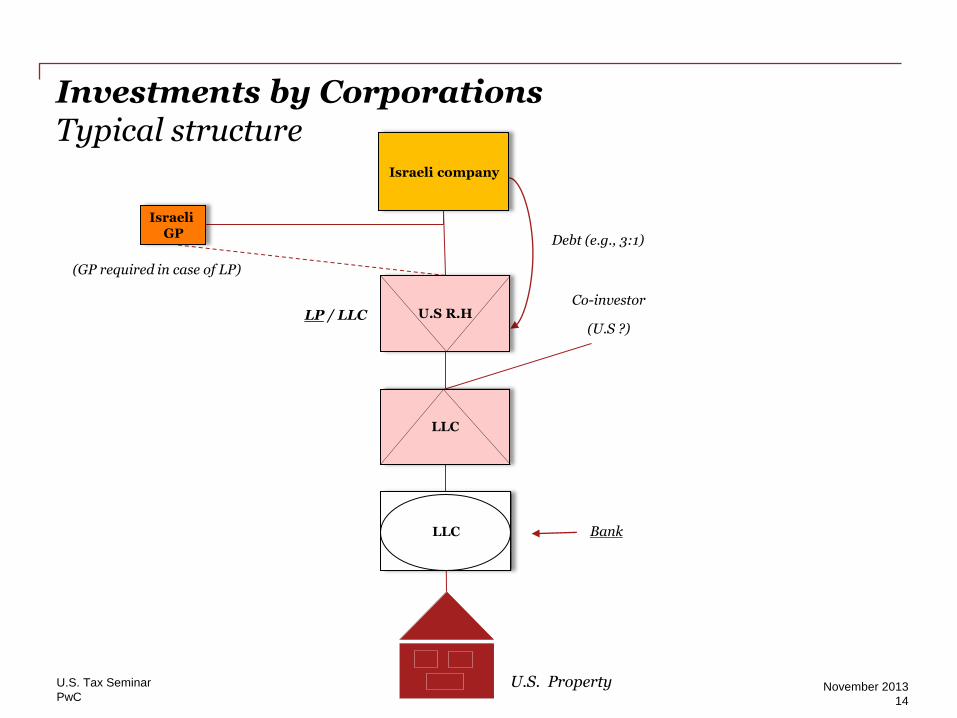

Investments by Corporations Typical structure

Co-investor

(U.S ?)

(GP required in case of LP)

Bank

Debt (e.g., 3:1)

/ LLC LP

LLC

U.S R.H

LLC

Israeli company

Israeli GP

U.S. Property

November 2013

15

U.S. Tax Seminar

PwC

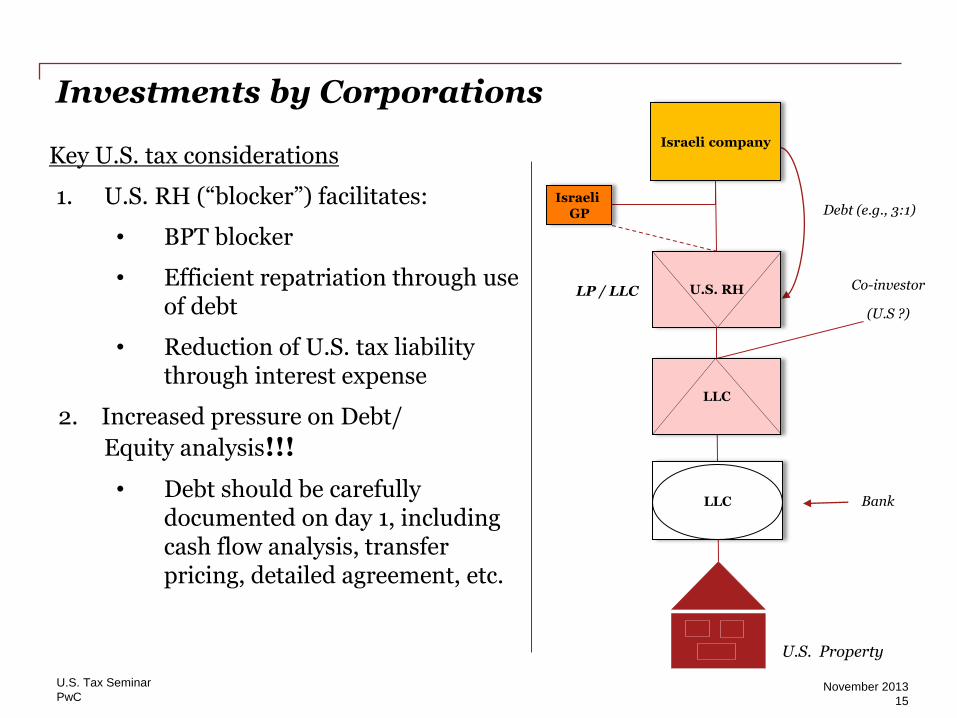

Investments by Corporations

Key U.S. tax considerations

1. U.S. RH (“blocker”) facilitates:

• BPT blocker

• Efficient repatriation through use of debt

• Reduction of U.S. tax liability through interest expense

2. Increased pressure on Debt/

Equity analysis!!!

• Debt should be carefully documented on day 1, including cash flow analysis, transfer pricing, detailed agreement, etc.

Co-investor

(U.S ?)

Bank

Debt (e.g., 3:1)

LP / LLC

LLC

U.S. RH

LLC

Israeli company

U.S. Property

Israeli GP

November 2013

16

U.S. Tax Seminar

PwC

Investments by Corporations Key U.S. tax considerations

3. Repatriation of remaining earnings through liquidation of U.S. RH

no withholding tax

4. Timing of interest deduction - critical

- 163(j)

- 267 (a)(3)

Bank

Debt (e.g., 3:1)

LP / LLC

LLC

U.S. RH

LLC

Israeli company

U.S. Property

Israeli GP

Co-investor

(U.S ?)

November 2013

17

U.S. Tax Seminar

PwC

Investments by Corporations Key Israeli tax considerations

1. Potential mismatch in timing of interest taxation

2. Foreign Exchange (if the principal component is denominated in USD)

3. VAT

4. Reporting based on K-1?

5. FTC in view of “tiered” LLC

Bank

Debt (e.g., 3:1)

LP / LLC

LLC

U.S. RH

LLC

Israeli company

U.S. Property

Israeli GP

Co-investor

(U.S ?)

November 2013

18

U.S. Tax Seminar

PwC

REITs Israeli Individuals U.S. Investors > 50%

Israeli Company

U.S REIT

Do not necessarily have to be

publicly traded

Facilitate one layer

of U.S. Taxation

Increasingly popular vehicles

November 2013

19

U.S. Tax Seminar

PwC

REITs

CG dividends

• 35% U.S. domestic WHT rate & State tax (if applicable)

• For foreign shareholders owning <5% no domestic U.S. WHT under certain conditions (e.g., if publicly traded REIT)

Ordinary income dividends

• On portion of distribution not designated as CG

• U.S. domestic WHT rate

- If individual owns <10% of REIT WHT rate of 25% (under the U.S.-Israel Double Tax Treaty)

- 30% U.S. domestic WHT in all other cases

REITs

Generally not taxed on earnings distributed to shareholders

WHT on dividends / CG

November 2013

20

U.S. Tax Seminar

PwC

REITs

Capital Gain on Sale of REIT stock

1. If REIT is DCR - no U.S. tax

2. If REIT is publicly traded and foreign shareholder holds <5% - no U.S. tax

3. All other cases, gain ECI taxed at marginal tax rate (on net basis)

November 2013

21

U.S. Tax Seminar

PwC

Scope and Limitations

The information contained in this presentation is for general guidance on matters of interest only. As such, it should not be used as a substitute for consultation with professional tax advisers.

This document was not intended or written to be used, and it cannot be used, for the purpose of avoiding any U.S. federal, state or local tax penalties.

Circular 230: this document was not intended or written to be used, and it cannot be used, for the purpose of avoiding U.S. federal, state or local tax penalties that may be imposed on the taxpayer.

©2013 Kesselman & Kesselman. All rights reserved.

In this document, “PwC Israel” refers to Kesselman & Kesselman, which is a member firm of PricewaterhouseCoopers

International Limited, each member firm of which is a separate legal entity. Please see www.pwc.com/structure for

further details.

PwC Israel helps organisations and individuals create the value they’re looking for. We’re a member of the PwC network

of firms with 169,000 people in more than 158 countries. We’re committed to delivering quality in assurance, tax and

advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com/il

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional

advice. It does not take into account any objectives, financial situation or needs of any recipient. Any recipient should not

act upon the information contained in this publication without obtaining specific professional advice. No representation or

warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication,

and, to the extent permitted by law, Kesselman & Kesselman, and any other member firm of PwC, its members,

employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you

or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision

based on it, or for any direct and/or indirect and/or other damage caused as a result of using the publication and/or the

information contained in it.

Thank you! Omri Yaniv, International Tax Partner, PwC Israel

972-3-7954-474

Tamar Sharon, International Tax Manager, PwC Israel

972 -3-7954-755