U.S. Private Equity Mergers & Acquisitions Activity€¦ · U.S. Private Equity M&A observations...

15

Q3 2019 Quarterly Insights U.S. Private Equity Mergers & Acquisitions Activity

Transcript of U.S. Private Equity Mergers & Acquisitions Activity€¦ · U.S. Private Equity M&A observations...

Q3 2019 Quarterly Insights

U.S. Private Equity Mergers

& Acquisitions Activity

Contents

Private Equity Activity

General Deal Overview

Deals by Size

Deals by Industry

Add-on Activity

Private Equity Overhang

Fundraising & Capital

Debt vs Equity

Private Equity Buyout Structure

Exits

Valuations

Who is buying

4

5

6

7

8

9

10

11

2

U.S. Private Equity M&A observations – 2019 YTD*

Source: PitchBook, LCD

* As of 9/30/2019

the

longest stock market bull run in history and a relatively strong economy. Valuations are at historic highs, and

PE sponsors have an incredible inventory of available capital. While the overall M&A market is showing strains

and has slowed from last year’s pace, PE activity remains strong by historic measures.

During 2019, we are witnessing the same phenomena that we have seen over the last several years in PE-

driven M&A:

• A historically high number of annual M&A transactions

• A continued buying frenzy among PE bidders at historically high multiples of EBITDA being paid due to an

oversupply of capital chasing too few quality companies/transactions

• PE funds continue to raise a record amount of capital from very willing limited partners

• Debt providers, particularly cash flow lenders, continue to provide historically cheap and available debt

financing

• Strategic balance sheets remain similarly very strong, a result of the very robust and growing U.S. economy

over the last ten years, accelerated by the Jobs Act of 2017

This activity has only recently been somewhat muted by selective macro economic issues, including tariff wars,

continued geopolitical tensions, slowing global economies and U.S. manufacturing output and continued

uncertainty regarding Brexit. Every cycle has uncertainty, and the question is whether an even short-term

economic slowdown can slow down this unprecedented M&A environment in private equity.

In our recent conversations with a wide variety of financial buyers of businesses, ranging from large and middle

market PE funds to family offices and fundless sponsors, several key themes are consistently repeated:

• Acknowledgement regarding how competitive the market is; consequently, that applies an upward force on

multiples while shortening the required diligence time frame to close a deal in order to prevail in an M&A

auction

• Increased use of “sponsor fund lines of credit” to remove the uncertainty of third-party financing

• Many generalist middle market firms are reviewing 1,000+ deals on an annualized basis, and on average

investing in only two or three platforms per year

• A focus on chasing transactions where the PE firm knows it can 1) have a very strong “angle” on the

business and believe that they can accelerate organic growth, 2) add scale and lower their blended

acquisition multiple by pursuing tuck-in acquisitions, and 3) therefore, be ultra competitive on pricing

• While deal volume remains high, PE firms are seeing “lower quality” businesses (i.e. customer

concentration, high capital expenditures relative to EBITDA, business cyclicality, flat or declining revenues

and/or compressed operating margins), with such businesses still trying to extract large multiples

With the Great Recession now one full decade in the rearview mirror,

we are still witnessing a historic M&A bull market among private equity (PE) players,

Kent Adams

Managing Director

Middle Market M&A

and Financial

Sponsor Coverage

Tim Ludwick

Vice President

Middle Market M&A

and Financial

Sponsor Coverage

The charts on the following pages support our view and what we are witnessing in the market. We continue to remain bullish given the

amount of capital (both equity and debt), available for transactions in the marketplace and no signs of a major market slowdown in PE

activity without a force majeure event or sustained economic slowdown in the U.S. Our bullishness is supported by the velocity by

which PE firms are participating in transactions for privately held businesses, including founder-owned, entrepreneurial led and PE

sponsor owned. PE is in the business of buying and selling businesses, and as average hold times have decreased, we continue to

expect an active M&A market over the next 12 months as owners seek to capitalize on the current bull market, and mitigate risk of

prolonged economic expansion and/or the 2020 election results.

3

U.S. Private Equity M&A observations – 2019 YTD*

$441bn

Total PE deal activity in

2019* down from $516bn

in Q1-Q3 2018, but

historically high level

29% Percentage of total

deals completed in the

IT sector, the most

active PE sector

6.0x

Average total debt to

EBITDA

$174bn

Total sponsor backed

transaction loan volume

$205mm

Median PE deal size,

up from $190.0mm

in 2018

Source: PitchBook, LCD

* As of 9/30/2019

$191bn

Total private equity

dollars raised

12.2x

Average EV/EBITDA

multiple paid by PE

firms, a historic high

3,883

Number of PE

transactions closed

40+ Advisory transactions

completed by BMO

and involving PE

since Q3 2018

4

General Deal Overview

Source: PitchBook

* As of 9/30/2019

Private Equity Activity

Deal volume in terms of both value and quantity through Q3 are

on pace to continue the bullish PE M&A run seen over the past ten years

Through the first three quarters of 2019, the total

number of U.S. private equity M&A deals is slightly

lagging the first three quarters of 2018, and the total

dollar value of such deals is also lower by 2%

Historically, deal value and quantity have strengthened

in the latter half of a respective year; however, it will

require a surge in activity in the last quarter of 2019 to

surpass the record levels of 2018 activity

The odds of a strong final quarter are met with

uncertainty with escalating geopolitical tension, slower

economic growth and a looming election year

Deal Activity – Annual Comparison, 2008 – 2019 YTD*

Share percentage of deal activity by deal value

`18YTD `19YTD*

35%

40%

25%33%

31%

36% Q1

Q2

Q3

$3

12

$1

41

$2

81

$3

29

$3

82

$4

38

$5

35

$5

61

$6

08

$6

31

$7

27

$5

16

$5

01

2,763

1,916

2,784

3,173

3,571 3,443

4,273 4,460 4,445

4,774

5,270

3,9733,883

0

1,000

2,000

3,000

4,000

5,000

6,000

$0

$150

$300

$450

$600

$750

$900

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 '18YTD '19YTD

Deal value ($B) Deal count (thousands)

5

Deals by Size

Source: PitchBook, FactSet

* As of 9/30/2019

Private Equity Activity

The middle market of PE M&A transactions continues to dominate in terms

of number of transactions and overall deal value volume. Billion dollar transactions, which

comprise less than 2% of the number of all deals, comprise 30% of total deal value

Enterprise Value – Annual Comparison, 2015 – 2019 YTD*

Since 2015, over

90% of the number of

closed PE M&A

transactions have

had enterprise values

of less than $500mm

Number of PE M&A

Deals by Size

Value of PE M&A

Deals by Size

Transaction values

ranging $100mm to

$1bn comprise 57%

of total deal value

since 2015

$Bn

$73 , 3%

$238 , 9%

$1,059 , 42%

$346 , 14%

$295 , 12%

$515 , 20%

2015 - 2018

Under $25M

$25M-$100M

$100M-$500M

$500M-$1B

$1B-$2.5B

$2.5B+

$12 , 3%

$54 , 12%

$205 , 47%

$58 , 13%

$33 , 7%

$80 , 18%

2019 YTD*

8,795, 46%

4,639, 25%

4,728, 25%

514, 3%197, 1%

79, 1%

2015 - 2018

Under $25M

$25M-$100M

$100M-$500M

$500M-$1B

$1B-$2.5B

$2.5B+

692, 36%

530, 28%

457, 24%

206, 11%

17, 1% 9, 1%

2019 YTD*

6

$80 , 3%

$479 , 19%

$323 , 13%

$215 , 9%$235 ,

9%

$505 , 20%

$691 , 27%

2015 - 2018

Materials & resources

IT

Healthcare

Financial services

Energy

B2C

B2B

$13 , 3%

$112 , 25%

$54 , 12%

$32 , 7%

$35 , 8%

$69 , 16%

$126 , 29%

2019 YTD*

PE M&A Transactions by Industry

Source: PitchBook, FactSet

* As of 9/30/2019

Private Equity Activity

B2B sector accounts for one-third of all PE

deals, B2B + IT deals comprise nearly half of PE deal value

Industry Sector Activity – Annual Comparison, 2015 – 2019 YTD*

Total Number of Deals by Sector

Total Value of Deals by Sector

The number of private equity

transactions by sector has

remained fairly balanced

over the past five years

Investments in the IT and

B2B sectors from 2015-2018

led all deal activity with 17%

and 34%, respectively; they

continue to be the strong

sectors through 2019 YTD*

at 19% and 37%,

respectively

Total deal values by sector

tend to fluctuate by a greater

degree year-over-year due

to large transactions that

deviate from the norm

Higher valuations in the IT

sector continue to dominate

the landscape and account

for $112bn of total deal value

YTD, up from $78bn YTD in

2018

$Bn

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019*

B2B

B2C

Energy

Financial services

Healthcare

IT

Materials & resources

7

Add-on Activity

Source: PitchBook, FactSet

* As of 9/30/2019

Private Equity Activity

PE backed portfolio companies are increasingly utilizing

tuck-in acquisitions to drive growth and value creation

Buyout Activity - Platform vs. Add-on, 2008 – 2019 YTD*

The percentage of PE acquisitions which comprise add-ons for existing portfolio companies has grown nearly each

of the past 10 years and now comprise two-thirds of all PE transactions

Number of Deals by Add-on Percentage

1,1

48

795

1,2

03

1,4

18

1,6

11

1,5

50

2,0

25

2,1

25

2,2

24

2,3

29

2,7

26

1,7

22

53%57% 56%

58% 57%61% 62% 62%

65% 64%66%

68%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019*

Add-on Add-on % of buyout

8

$151

$218

$238

$196

$121

$191

265251 249

207

131

0

50

100

150

200

250

300

$0

$50

$100

$150

$200

$250

2015 2016 2017 2018 '18YTD '19YTD

Capital raised ($B) Fund count

Capital Activity

Source: PitchBook, Bloomberg

* As of 9/30/2019

Private Equity Overhang

Given strong overall returns and the amount of capital that

institutional LPs have to deploy, PE fundraising is expected to continue

to be very strong from both middle market and mega PE funds

Capital Raised and PE Fund Count, 2015 – 2019 YTD*

The fundraising

environment remains

robust, with significant

institutional interest in

private equity investing

given strong, consistent

returns

Fundraising in the first

three quarters of 2019

appears to be slightly

declining in terms of the

number of new funds

closed; however, the total

capital raised has almost

surpassed the 2018 full-

year figure of $196bn

For comparison, as of

September 30th, 2018,

there were 143 closed

funds with approximately

$121bn of capital raised

Mega-funds ($5+ billion)

were the driving force in

the first three quarters of

2019. Blackstone closed

the largest PE fund ever

raised at $24.7bn, a title

previously held by Apollo

Global Management

PE Fundraising

Activity

143

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019*

$5B+

$1B-$5B

$500M-$1B

$250M-$500M

$100M-$250M

Under $100M

9

PE Buyout Structure

Source: PitchBook

Note: Due to rounding, the above numbers presented may not add up precisely to the totals indicated

Debt vs Equity

While average debt leverage is near record highs, as a total percentage of enterprise value, it

has slowly tempered vis-à-vis equity in recent years as EV/EBITDA multiples have expanded

Debt Capital / Equity Capital in PE Transactions

With relatively cheap

debt financing available,

in large quantities,

combined with high

multiples being paid, a

perfect storm exists for

deploying both debt and

equity capital to finance

PE transactions, with a

greater percentage

coming from equity, on

average

Sponsors are

increasingly taking only

moderate leverage at

close but will build in

flexibility to take debt

above closing leverage in

order to aggressively

pursue acquisitions

Higher leverage multiples

are an indication of both

strong deal flow quality

and sustained market

optimism

Debt Percentage

of PE Buyouts

42%

44%

46%

48%

50%

52%

54%

56%

58%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2015 2016 2017 2018 2019*

5.6

x

5.3

x

5.5

x

5.3

x

5.5

x

5.1

x

5.7

x

5.3

x

5.6

x

6.0

x

5.9

x

6.1

x

5.9

x

5.8

x

6.1

x

5.8

x

6.1

x

5.9

x

5.9

x

4.5

x

4.2

x

4.4

x

4.5

x

4.8

x

5.2

x 5.7

x

5.3

x

5.6

x

5.8

x

5.6

x

5.8

x

5.6

x

5.6

x

6.1

x

5.8

x

6.2

x

6.4

x

6.0

x

10.2x9.6x

9.9x 9.8x10.4x 10.3x

11.4x

10.5x11.2x

11.9x

11.4x11.9x 11.5x 11.5x

12.3x11.5x

12.3x12.3x

11.9x

0.x

2.x

4.x

6.x

8.x

10.x

12.x

14.x

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2015 2016 2017 2018 2019*

Debt/EBITDA Equity/EBITDA EV/EBITDA

10

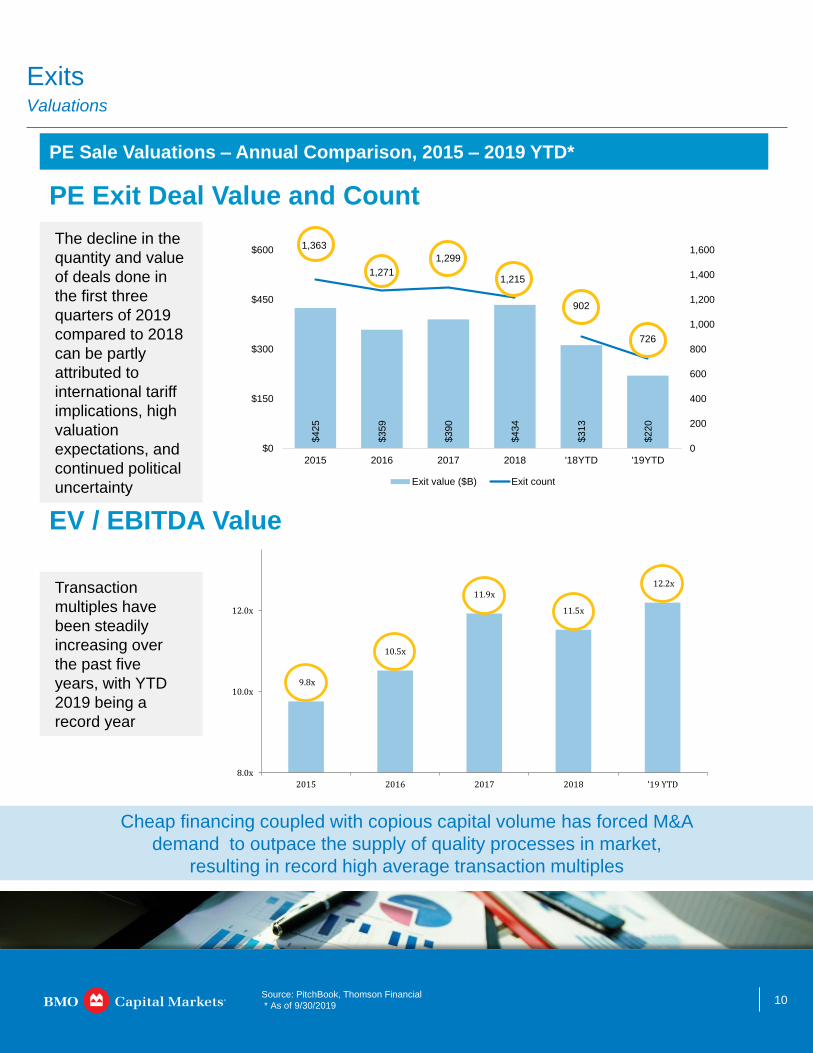

Valuations

Source: PitchBook, Thomson Financial

* As of 9/30/2019

Exits

Cheap financing coupled with copious capital volume has forced M&A

demand to outpace the supply of quality processes in market,

resulting in record high average transaction multiples

PE Sale Valuations – Annual Comparison, 2015 – 2019 YTD*

PE Exit Deal Value and Count

EV / EBITDA Value

The decline in the

quantity and value

of deals done in

the first three

quarters of 2019

compared to 2018

can be partly

attributed to

international tariff

implications, high

valuation

expectations, and

continued political

uncertainty

Transaction

multiples have

been steadily

increasing over

the past five

years, with YTD

2019 being a

record year

$425

$359

$390

$434

$313

$220

1,363

1,271

1,299

1,215

902

726

0

200

400

600

800

1,000

1,200

1,400

1,600

$0

$150

$300

$450

$600

2015 2016 2017 2018 '18YTD '19YTD

Exit value ($B) Exit count

9.8x

10.5x

11.9x

11.5x

12.2x

8.0x

10.0x

12.0x

2015 2016 2017 2018 '19 YTD

11

Who is Buying?

Source: PitchBook, Capital IQ,

* As of 9/30/2019

PE Exits

By measure of both deal value and quantity, the percentage of corporate

acquisitions of PE assets have been diminishing while secondary buyouts

have been steadily rising over the last five years

Purchasers of PE Assets– Annual Comparison, 2015 – 2019 YTD*

Corporations are more attracted to

M&A with increased public market

valuations, cash repatriations and

favorable borrowing conditions

making capital plentiful

Since 2015, the number of PE exits

to corporate buyers slightly favors

the number of sales to other PE

groups; however, in the first three

quarters, the number of SBO’s

(Secondary Buyouts) has outpaced

Corporate acquisitions by

approximately 44%

Number of Deals

by Buyer Type

Value of Deals

by Buyer Type

Considering most businesses that go

public have an enterprise value of at

least $1 billion, the IPO market

consists of a greater share of PE

exits in terms of deal value as

expected; however, the IPO category

is still trumped by corporate buyers

and other PE buyers

Private market valuations in many

sectors have been comparable to

public valuations, without the costs of

public ownership

($Bn)

$110.159%

52% 46%49%

35%

31%

39%44%

41%

48%

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2015 2016 2017 2018 2019 YTD

Corporate acquisition IPO SBO

$425

$359

$390

$195

$434

52% 52% 49% 46%

40%

45%45% 48%

51%

57%

0

200

400

600

800

1000

1200

1400

1600

2015 2016 2017 2018 2019 YTD

Corporate acquisition IPO SBO

1,3631,271 1,299

1,215

610

12 Source: Bloomberg, BMO Internal Pipeline(1), calendar YTD as November 4th, 2019.

BMO M&A expertise in Private Equity transactions

A Powerful M&A Practice

Experienced

team

• Global M&A practice with ~105 M&A professionals in nine offices around the world,

with ~80 M&A professionals in the U.S.

• Including over 30 Managing Directors and Directors

Full product

capabilities

• Sell-side, buy-side and cross-border advisory

• Recapitalizations and restructurings

• Fairness opinions

• Takeover defense

• Activism defense

• Leveraged and management buyouts

• Strategic alternatives review

Approach

• Deep sector expertise in close alignment with BMO’s industry groups

• M&A professionals partner with industry experts to drive enhanced insights and execution

• Dedicated capabilities in both large cap and middle market M&A advisory and financing

Proven

results • US$404 billion(1) of transaction value in 500+ deals since 2011

Select recent PE M&A transactions

Financial Advisor

Sale to

August 2019

Portfolio Company of

Financial Advisor

Sale to

August 2019

Portfolio Company of

Portfolio Company of

Financial Advisor

Portfolio Company Of

July 2019

Sale to

Financial Advisor

Portfolio Company of

June 2019

Portfolio Company of

Sale to

Financial Advisor

Sale to

July 2019

Financial Advisor Pending

Portfolio Company of

Acquisition of Maxim’s Homecare

Division

Financial Advisor

Sale to

January 2019

Portfolio Company of

Portfolio Company of

Financial Advisor

March 2019

Sale to

Portfolio Company of

Financial Advisor

May 2019

Portfolio Company of

Sale to

Financial Advisor

January 2019

Recapitalization by

Financial Advisor

Sale to

May 2019

Financial Advisor

January 2019

Acquired by

Portfolio Company of

13

About us: BMO Capital Markets

As a member of BMO Financial

Group (NYSE, TSX: BMO), we

leverage the financial strength

and capabilities of one of North

America’s leading financial

services organizations

Access to capital

• Initial public offerings

• Debt financing

• Equity financing

• Private equity financing

• Corporate lending

• Structured & project financing

• Securitization

Distribution

• Institutional

Equity sales & trading

Fixed income sales & trading

• Retail

Direct brokerage

Private banking

Strategy & growth

• Strategic advisory

• Mergers & acquisitions, including

cross-border opportunities

• Valuations & fairness opinions

• Acquisition & divestitures

• Leverage buyouts

• Restructurings & recapitalizations

• Take-over & activism defense

• Share buybacks

• Joint ventures and other

partnership models

Treasury & risk management

• Commodity products

• Money markets

• Trade finance

• Cash management

• Foreign exchange

Research

• Economics

• Commodities

• Debt

• Corporate

2,700+ professionals

33 locations

5 continents

We offer a complete suite of products and services:

BMO Capital Markets is a single-

stop provider. Depending on your

needs, you may use a combination

of our capabilities, or only one.

Our experience and deep sector

knowledge enable us to develop

the solution that fits you best

Americas Europe & Middle East

Atlanta

Boca Raton

Boston

Buffalo

Calgary

Chicago

Denver

Houston

Mexico City

Milwaukee

Minneapolis

Montreal

New York

Phoenix

Rio de Janeiro

San Francisco

Seattle

Toronto

Vancouver

Washington, D.C

Dublin

London

Paris

Zurich

Abu Dhabi

Mumbai

Asia & Australia

Beijing

Melbourne

Guangzhou

Hong Kong

Singapore

Shanghai

Taipei

14

Contacts

Lyle Wilpon Managing Director

Head of Global Advisory

New York, NY

Tel.: (212) 702-1738

Rob Stewart Managing Director

Co-Head of U.S.

Mergers & Acquisitions

New York, NY

Tel.: (212) 702-1131

Seth Prostic Managing Director

Co-Head of U.S.

Mergers & Acquisitions

Chicago, IL

Tel.: (312) 293-8365

Eric Nicholson Managing Director

Head of Middle Market

Mergers & Acquisitions

Minneapolis, MN

Tel.: (612) 904-5710

This material is prepared by the BMO Capital Markets’ Investment and Corporate Banking Department, for distribution to BMO Capital Markets’ clientele. It is not a product

of BMO Capital Markets’ Research Department. The views of the Investment and Corporate Banking Department may differ from those of the Research Department. No

part of this publication or its contents may be copied, downloaded, stored in a retrieval system, further transmitted, or otherwise reproduced, stored, disseminated,

transferred or used, in any form or by any means by any third parties, except with the prior written permission of BMO Capital Markets.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC),

Bank of Montreal Ireland p.l.c, and Bank of Montreal (China) Co. Ltd and the institutional broker dealer businesses of BMO Capital Markets Corp. (Member FINRA and

SIPC) in the U.S., BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada

and Asia, Bank of Montreal Ireland p.l.c. (authorised and regulated by the Central bank of Ireland) in Europe and BMO Capital Markets Limited (authorised and regulated by

the Financial Conduct Authority) in the UK and Australia. “Nesbitt Burns” is a registered trademark of BMO Nesbitt Burns Inc., used under license. “BMO Capital Markets” is

a trademark of Bank of Montreal, used under license. "BMO (M-Bar roundel symbol)" is a registered trademark of Bank of Montreal, used under license.

® Registered trademark of Bank of Montreal in the United States, Canada and elsewhere.

™ Trademark of Bank of Montreal in the United States and Canada.

© 2018 BMO Financial Group

Bank of Montreal or its subsidiaries (“BMO Financial Group”) has lending arrangements with, or provide other remunerated services to, many issuers covered by BMO

Capital Markets. The opinions, estimates and projections contained in this report are those of BMO Capital Markets as of the date of this report and are subject to change

without notice. BMO Capital Markets endeavors to ensure that the contents have been compiled or derived from sources that we believe are reliable and contain information

and opinions that are accurate and complete. However, BMO Capital Markets makes no representation or warranty, express or implied, in respect thereof, takes no

responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this report or its contents.

Information may be available to BMO Capital Markets or its affiliates that is not reflected in this report. The information in this report is not intended to be used as the primary

basis of investment decisions, and because of individual client objectives, should not be construed as advice designed to meet the particular investment needs of any

investor. This material is for information purposes only and is not an offer to sell or the solicitation of an offer to buy any security. BMO Capital Markets or its affiliates will buy

from or sell to customers the securities of issuers mentioned in this report on a principal basis. BMO Capital Markets or its affiliates, officers, directors or employees have a

long or short position in many of the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO Capital Markets

may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. The reader should assume that BMO Capital

Markets or its affiliates may have a conflict of interest and should not rely solely on this report in evaluating whether or not to buy or sell securities of issuers discussed

herein. All values in this document are in C$ unless otherwise specified.

![Private equity funds in norway activity report h1 2013[1]](https://static.fdocuments.us/doc/165x107/568bdc1a1a28ab2034b0f746/private-equity-funds-in-norway-activity-report-h1-20131.jpg)