U.S. Environmental Consulting & Engineering Industry by ...

42

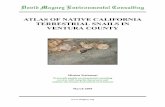

Volume XXXI Number 9/10 Environmental Business International Inc. Consulting & Engineering and IT in 2018 ENVIRONMENTAL FIRMS CHASE GROWTH, EMBRACE IT C haracterizing the environmental consulting & engineering industry in 2017 and 2018 has to start with the Trump Administration and the unpredict- able president Donald Trump. Admittedly this has been a principal topic of two pre- vious editions of Environmental Business Journal in 2018, so not much more space will be devoted here to the double-edged sword syndrome of ‘good for business but bad for the environment’ that results in a relatively neutral effect on the environ- mental industry, nor to the ‘Trump Effect’ and its impact on specific industry seg- ments or client sectors that was detailed in EBJ’s mid-2018 survey of the same name. e results of the 2018 midterm elec- tions and the change of control of the House of Representatives to the Demo- cratic Party should have more impact on politics then it does on short term envi- ronmental industry forecasts. Most ana- lysts agree with EBJ that economic factors like interest rates, tariffs and tax policy will have a more direct impact on the business the next two years. More outside of political control, but equally influential to environmental in- dustry growth, are the pace of develop- ment and infrastructure investment, and the movement of property values, stock market indices and oil prices. ese factors also collectively impact the gross domes- tic product (GDP), consumer confidence and other economic indicators that most environmental companies agree are more influential to their business prospects than the specific regulatory programs or fund- ing mechanisms for which they used to advocate more strenuously. ese factors are summarized on the tables on page 3. e tables update recent history and roll out updated short- and long-term forecasts from a variety of sourc- Inside EBJ e U.S. environmental consulting & engineering industry has shaken off environmental policy and political setbacks and worked to benefit client initiatives, investments and risk profiles in the increasingly deregulatory environment. 2018 growth at 4-4.5% will likely be a peak as more concerns cloud the horizon than the promise of new market drivers.............................................................................. 1-10 Technology Plays in Environmental Consulting & Engineering .................... 11-29 NV5 stays on leading edge in acquiring drone firm and building optimizer ............. 11 KCI commits to innovation strategy: acquires laser scanning firm LandAir ............. 14 GHD launches advisory and digital units to add ‘edge’ to existing services .............. 17 Tetra Tech invests in aviation technology and digital design tools ........................... 20 GZA’s Superfund sites are moving along towards remediation ................................. 22 SNC-Lavalin continuously seeks the best digital alliances to provide value-added propositions to their clients ..................................................................................... 24 ERM strives to be the leading digital EHS service provider with the strongest digital ecosystem of partners .............................................................................................. 27 EFCG reflects on technology trends and forecast scenarios for 2019 ....................... 30 J. Doehring says watch out for wildcards on the economic horizon ........................ 35 7 Mile Advisors predicts a moderate to strong outlook for 2019............................. 37 Small companies remain optimistic knowing some uncertainties are ahead ............ 39 U.S. Environmental Consulting & Engineering Industry by Media Source: Environmental Business International Inc., San Diego, Calif. EBJ’s annual model of the environmental consulting & engineering industry based primarily on revenue analysis, surveys and interviews of C&E firms, analysts and experts. Units in $mil. of revenues generated 4,220 3,730 3,670 3,560 3,270 3,460 3,730 4,020 4,710 5,200 5,040 5,590 1,980 2,500 3,890 4,900 5,560 6,770 1,750 2,630 3,560 4,530 5,230 6,550 1,250 1,230 1,590 2,010 2,440 2,710 980 1,160 1,830 2,180 2,610 3,010 - 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 1995 2000 2005 2010 2015 2020 Multi-Media Renew able Energy Natural Resources Air Quality Energy Mgmt/Efficiency Water Wastew ater Solid Waste Remediation Hazardous Waste

Transcript of U.S. Environmental Consulting & Engineering Industry by ...

Volume XXXI Number 9/10 Environmental Business International Inc.Consulting & Engineering and IT in 2018

ENVIRONMENTAL FIRMS CHASE GROWTH, EMBRACE IT

Characterizing the environmental consulting & engineering industry

in 2017 and 2018 has to start with the Trump Administration and the unpredict-able president Donald Trump. Admittedly this has been a principal topic of two pre-vious editions of Environmental Business Journal in 2018, so not much more space will be devoted here to the double-edged sword syndrome of ‘good for business but bad for the environment’ that results in a relatively neutral effect on the environ-mental industry, nor to the ‘Trump Effect’ and its impact on specific industry seg-ments or client sectors that was detailed in EBJ’s mid-2018 survey of the same name.

The results of the 2018 midterm elec-tions and the change of control of the House of Representatives to the Demo-cratic Party should have more impact on politics then it does on short term envi-ronmental industry forecasts. Most ana-lysts agree with EBJ that economic factors like interest rates, tariffs and tax policy will have a more direct impact on the business the next two years.

More outside of political control, but equally influential to environmental in-dustry growth, are the pace of develop-ment and infrastructure investment, and the movement of property values, stock market indices and oil prices. These factors also collectively impact the gross domes-tic product (GDP), consumer confidence and other economic indicators that most environmental companies agree are more influential to their business prospects than the specific regulatory programs or fund-ing mechanisms for which they used to advocate more strenuously.

These factors are summarized on the tables on page 3. The tables update recent history and roll out updated short- and long-term forecasts from a variety of sourc-

Inside EBJThe U.S. environmental consulting & engineering industry has shaken off environmental policy and political setbacks and worked to benefit client initiatives, investments and risk profiles in the increasingly deregulatory environment. 2018 growth at 4-4.5% will likely be a peak as more concerns cloud the horizon than the promise of new market drivers ..............................................................................1-10

Technology Plays in Environmental Consulting & Engineering ....................11-29NV5 stays on leading edge in acquiring drone firm and building optimizer .............11

KCI commits to innovation strategy: acquires laser scanning firm LandAir .............14

GHD launches advisory and digital units to add ‘edge’ to existing services ..............17

Tetra Tech invests in aviation technology and digital design tools ...........................20

GZA’s Superfund sites are moving along towards remediation .................................22

SNC-Lavalin continuously seeks the best digital alliances to provide value-added propositions to their clients .....................................................................................24

ERM strives to be the leading digital EHS service provider with the strongest digital ecosystem of partners ..............................................................................................27

EFCG reflects on technology trends and forecast scenarios for 2019 .......................30

J. Doehring says watch out for wildcards on the economic horizon ........................35

7 Mile Advisors predicts a moderate to strong outlook for 2019 .............................37

Small companies remain optimistic knowing some uncertainties are ahead ............39

U.S. Environmental Consulting & Engineering Industry by Media

Source: Environmental Business International Inc., San Diego, Calif. EBJ’s annual model of the environmental consulting & engineering industry based primarily on revenue analysis, surveys and interviews of C&E firms, analysts and experts. Units in $mil. of revenues generated

4,220 3,730 3,670 3,560 3,270 3,460

3,730 4,020 4,710 5,200 5,040 5,590

1,980 2,5003,890 4,900 5,560

6,7701,750 2,630

3,5604,530 5,230

6,550

1,250 1,230

1,590

2,0102,440

2,710

980 1,160

1,830

2,1802,610

3,010

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1995 2000 2005 2010 2015 2020

Multi-MediaRenew able EnergyNatural ResourcesAir QualityEnergy Mgmt/Eff iciencyWaterWastew aterSolid WasteRemediationHazardous Waste

Environmental Business Journal, Volume XXXI Number 9/10

2 Strategic Information for a Changing Industry

Environmental Business Journal ® (ISSN 0145-8611) is published by Environmental Business International, Inc., 4452 Park Blvd., #306, San Diego, CA 92116. © 2018 Environmental Business International, Inc. All rights reserved. This publication, or any part, may not be duplicated, reprinted, or republished without the written permission of the publisher. To order a subscription, call 619-295-7685 ext. 15 or visit us online at ebionline.org/ebj. A corporate electronic subscription with internal reproduction license and access to data starts at $1,250 and allows up to five registered users with rates increasing in five user increments. Discounted corporate subscriptions are available for firms with under 100 employees and single-issue access, non-profit or individual subscriptions are $995.

Editor in Chief: Grant Ferrier Federal Analyst: Andrew PatersonManaging Editor: Lyn Thwaites Research Manager: Laura CarranzaClient Services: Moe Wittenborne, Celeste Ferrier Contributors: George Stubbs, Jim Hight, Brian Runkel

EDITORIAL ADVISORY BOARD: Andrew Paterson; James Strock, Serve to Lead Group; P.S. Reilly, NextGen Today; Dr. Edgar Berkey; Walter Howes, Verdigris Capital; Paul Zofnass, President, EFCG

es into an instrument that we at EBJ use to help guide our environmental industry growth forecasts.

If anything clouds the current econom-ic outlook it is the seeming inevitability of a correction. While the term ‘correction’ is more frequently used for the stock market and by the investment community, it can apply to industry performance and the GDP as well. Economists would gener-ally assert that a 5-10% ‘correction’ in the stock market from a prolonged bull market run is not necessarily a precursor to eco-nomic collapse, but even the current slide of the 13-14% that the S&P 500 and the DJIA have fallen as 2019 begins from their October 2018 peaks has already stoked fears of a wider economic growth correc-tion and has had a direct impact on pri-vate investor activity, as well as corporate investments.

As the accompanying charts showing annual growth rates of key environmen-tal segments compared to the GDP il-lustrate, the environmental industry has shown waves of growth above and below economic growth rates throughout its history. Most notable has inevitably been recession, and especially the Great Reces-sion, but not to be underestimated is the impact of government shutdown or bud-get sequestration that contributed to down cycles in 1996-1997 and 2013-2014. The wall-faceoff government shutdown that the Trump Administration orchestrated to usher in the new Congress in 2019 there-fore could be expected to have an impact of possibly a year or two of hobbled growth if history is any guide.

GROWTH PEAK IN 2018 This edition of Environmental Busi-

ness Journal and the accompanying data set in spreadsheet format provides EBJ’s final analysis on 2017 environmental con-sulting & engineering industry growth of 4%, updates our forecast to 2022 and per-formance of the top 600 or so companies competing in the market. The expectation is that the year 2018 will end up with growth between 4% and 4.5%, which is higher than any year since 2012. The con-sensus among analysts and professional service consultants that serve the C&E in-dustry is that 2018 was the best year for

U.S. Environmental C&E Industry vs. GDP Growth: 1990-2020

Source: Environmental Business International Inc., annual model of C&E industry.

Annual Growth in U.S. Environmental Services; 2000-2020

Source: Environmental Business International Inc., San Diego, CA, environmental contracting includes two seg-ments: Hazardous Waste Management and Remediation/Industrial Services

-4%

-2%

0%

2%

4%

6%

8%

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19

USA GDP grow th C&E Grow th

-9%

-6%

-3%

0%

3%

6%

9%

00 02 04 06 08 10 12 14 16 18 20

Env'l Contracting Grow th

C&E Grow th

Env'l Lab Grow th

Environmental Business Journal, Volume XXXI Number 9/10

3 Strategic Information for a Changing Industry

Environmental Industry: Key Growth Factors2004-2008

2009-2010

2011-2013

2014-2016

2017 20182019-2020

2020-2022

Economic Growth (GDP) + -- + +n + + +n n

Property Values ++ - - + + + + n+

Federal Government Spending + + - n - n- n n

Oil & Gas, Commodity Prices ++ -- + -- + n+ - +

Construction Activity + -- + ++ + + + +

State & Local/Infras. Spending + - - n n n n+ +

Environmental Policy & Regs - n n+ n+ -- -- - -

Recession R r

Average Env’l Industry Growth 5.9% -0.4% 3.8% 3.6% 4.6% 4.0% 3.5% 3-4%

Average C&E Growth 6.8% -0.4% 2.2% 1.7% 4.0% 4.3% 3.2% 2-3%

Average Env’l Contracting Growth 3.4% -0.1% 2.8% 0.0% 1.6% 1.0% 1.0% 1-2%

Environmental Infrastructure 4.5% 3.1% 4.1% 3.3% 4.1% 4.1% 4.0% 3-4%

Average US GDP Growth 2.2% -0.3% 1.9% 2.1% 2.3% 2.6% 2.1% 2-3%

Average Oil Price Growth 27.9% -3.6% 12.5% -24.1% 23.8% 31.2% -4.7% 0-4%

Construction Activity 6.8% -13.2% 4.1% 9.4% 4.1% 5.7% 5.5% 3.9%

Source: EBJ, Environmental Business International Inc., Environmental Industry Summit 2018 presentations by Grant Ferrier updated throughout the year

Key Market Driver & Forecast Elements: Segment Growth 2014-2020e

2014 2015 2016 2017 2018e 2019e 2020e

GDP: USA 2.4% 2.4% 1.5% 2.3% 2.6% 2.4% 2%

GDP: Global 3.4% 3.1% 3.2% 3.7% 3.9% 3.9% 4%

Oil Price -9% -47% -16% 24% 31% -5% -5%

Natural Gas Price 18% -40% -4% 19% 7% -4% -2%

US Oil & Gas Production 17% 7% -6% 6% 15% 9% 6%

Stock Market (S&P/DJIA) 9% -1% 11% 22% 4% 6% 8%

U.S. Construction (PIP) 11.0% 10.7% 6.5% 4.1% 6% 5% 4%

Housing Price Index 4.3% 5.6% 5.6% 6.4% 5% 4% 2%

Housing Starts 8.5% 10.8% 5.6% 2.5% 3% 3% -5%

Water/Wastewater Rates 3.9% 3.3% 3.9% 3.7% 3% 3% 4%

EPA Budget 3.8% -1.2% 0.0% -0.5% -5% -2% 2%

Environmental Industry 4.5% 2.9% 3.6% 4.6% 4.0% 3.6% 3.4%

Environmental C&E 1.3% 2.4% 1.4% 4.0% 4.3% 3.4% 3.0%

Environmental Contracting -0.7% 0.1% 0.5% 1.6% 1.0% 1.0% 1.1%

Environmental Infrastructure 3.3% 3.1% 3.5% 4.1% 4.1% 3.9% 3.9%

Sources: Economic growth rates are a consensus of reputable sources like IMF, EIU and others; Oil price forecast for 2018 and 2019 based on annual average price estimated by U.S. EIA’s industry outlook; Construction a consensus of US Census, FMI and Dodge estimates; Housing Starts from US Census; Water rates from EBJ’s index of three water/wastewater rate surveys and EPA budget from EPA Budget in Brief and EBJ estimates; EBJ Segments are estimates derived from multiple sources but predominantly complia-tions of company revenues and forecasts in each segment; Environmental Contracting includes hazardous waste management and remediation/industrial services; Environmen-tal Infrastructure includes solid waste, water utilities and wastewater treatment works segments.

Environmental Business Journal, Volume XXXI Number 9/10

4 Strategic Information for a Changing Industry

Share of Top Companies in U.S. C&E Industry 2000-2017

Source: Environmental Business International Inc. (San Diego, CA), C&E industry database. Unlike the table below where yearly totals are made up from ranking fixed by 2017 environmental C&E revenues, top ranked firms are resorted every year. 2013 was a notable year with federal government sequestration and close to $1 billion in revenue was lost by C&E firms., heavily weighted to the top tier.

19% 19%22% 21% 21% 22% 22% 23%

26% 27% 26% 27% 28% 26% 27% 26% 27% 28%30% 29%33% 30% 31% 32% 32% 34%

38% 39% 40% 41% 41%39% 38% 36% 38% 37%

44% 43%48%

45% 47% 49% 50%53%

57% 58% 58% 60% 61% 59% 57% 56% 56% 55%53% 53%58% 56% 59% 61% 63%

68%73% 74% 75%

78% 78% 76% 73% 73% 73% 73%56% 56%

62% 60%64% 66%

70%75%

80% 82% 83%86% 86% 84%

81% 81% 81% 81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2002 2004 2006 2008 2010 2012 2014 2016

T o p 5 C &E T o p 10 C &E T o p 30 C &E T o p 100 C &E T o p 200 C &E

Top 5 & 10 U.S. Environmental C&E Firms 1995-2017 (Gross Environmental C&E Revenues in $mil)

1995 2000 2005 2010 2011 2012 2013 2014 2015 2016 2017

AECOM - 355 778 1,768 2,230 2,281 2,128 3,009 3,036 2,942 3,018

Jacobs 130 152 348 237 261 347 546 597 611 830 2,675

Tetra Tech 109 466 930 1,414 1,406 1,667 1,322 1,605 1,580 1,772 1,959

Stantec - 44 220 645 680 646 720 754 701 1,246 1,268

Arcadis 129 154 450 1,143 1,136 1,086 1,031 1,332 1,248 933 911

ERM 226 309 487 655 771 905 941 940 946 888 902

Golder 80 133 363 798 925 1,168 1,174 986 563 785 817

Leidos (SAIC) 150 196 380 699 621 624 361 301 280 367 541

Black & Veatch 373 352 364 354 335 369 391 380 397 427 493

CDM Smith 307 431 448 607 530 464 489 505 485 484 490

Total C&E: Net 15,510 17,410 22,340 26,830 27,800 29,030 28,630 28,990 29,690 30,100 31,300

Top 5 in 2017 368 1,171 2,726 5,207 5,713 6,027 5,746 7,297 7,175 7,724 9,831

Top 5 Share 2% 6% 11% 17% 18% 18% 18% 22% 21% 23% 28%

Big 10 in 2017 1,504 2,592 4,769 8,320 8,895 9,556 9,102 10,408 9,846 10,675 13,074

Big 10 Share 9% 13% 19% 28% 28% 29% 28% 32% 29% 31% 37%

Source: EBJ database of C&E firms; Top 10 are ranked by gross environmental consulting & engineering revenues in 2017

many of their clients in a number of years, but many approach 2019 with some cau-tion. EBJ forecasts growth of over 3-3.5% for the C&E industry in 2019, guided by the economic input factors summarized and detailed on page 3.

The looming scenario of a recession and its depth and duration of course impacts any forecast. Indeed the outlook for short-range business planning and resource allo-cation inside of companies should account for likely recession and possible timetables, so environmental industry companies are best advised not to overshoot their project execution and business development re-source allocations given the possibility of recession scenarios, and the possibility of another capital R recession.

For the environmental contracting seg-ments, which include hazardous waste management and remediation & industri-al services, the outlook for growth is some-what more modest in the 1-2% range, with higher weight put on industrial out-put, property values, federal budgets, and oil & gas industry dynamics.

Environmental Business Journal, Volume XXXI Number 9/10

5 Strategic Information for a Changing Industry

2016 U.S. C&E Market Matrix: by Media by Service ($mil)

By Media/ServiceHaz

WasteRemed-iation

Solid Waste

Waste-water

Water EnergyAir

QualityNRM RE

Multi-Media

Total

Invs/Assmt/Audit 748 1,731 396 623 1,017 416 199 1,121 123 - 6,370

Lab/Testing Svcs 20 102 - 142 128 - 25 27 - - 440

Permiting/Compl. 525 102 138 849 1,107 - 822 134 254 - 3,930

Design 813 1,425 413 1,245 1,535 224 448 766 146 284 7,300

Project Mgmt. 426 1,273 482 628 642 96 249 294 169 - 4,260

Monitoring 16 148 17 170 161 8 274 120 - - 910

Information Mgmt 66 25 17 57 54 24 149 40 - 363 800

O&M 16 25 9 1,302 321 8 75 - 54 - 1,810

Pollution Prev. 482 25 138 340 - - 75 - - - 1,060

SEM 56 51 - 57 54 8 50 53 - 1,271 1,600

other 112 183 112 249 332 16 125 115 23 352 1,620

Total 3,280 5,090 1,720 5,660 5,350 800 2,490 2,670 770 2,270 30,100

Source: Environmental Business International Inc., San Diego, CA, based primarily on annual surveys of C&E firms, units in $mil.

U.S. Environmental Consulting & Engineering Market by Customer, 2015-2018

2015 2016 2017 2018 2015 2016 2017 2018

Chemical/Pharma 2,100 2,190 2,350 2,520 7.1% 4.3% 7.3% 7.2%

Oil & Gas 1,920 1,930 2,090 2,240 -10.3% 0.5% 8.3% 7.2%

Primary metals 320 330 330 350 3.2% 3.1% 0.0% 6.1%

Metals Fab/Coating 450 460 480 510 2.3% 2.2% 4.3% 6.3%

Mining 670 670 710 750 3.1% 0.0% 6.0% 5.6%

Tech/Electonics Mfg 360 370 410 450 2.9% 2.8% 10.8% 9.8%

Transpo. (auto/aero) 750 750 790 840 4.2% 0.0% 5.3% 6.3%

Pulp & Paper 400 390 400 420 2.6% -2.5% 2.6% 5.0%

Other Mfg. 970 990 1,030 1,090 4.3% 2.1% 4.0% 5.8%

Water Utilities 1,220 1,280 1,360 1,450 6.1% 4.9% 6.3% 6.6%

Power Utilities 1,920 2,020 2,140 2,280 7.3% 5.2% 5.9% 6.5%

Solid Waste Util/Cos 570 580 610 640 5.6% 1.8% 5.2% 4.9%

Pet. Retail/Gas Stations 760 760 770 810 2.7% 0.0% 1.3% 5.2%

Banks, Law, Real Estate 1,540 1,600 1,670 1,780 5.5% 3.9% 4.4% 6.6%

RE Developers 550 590 630 680 7.8% 7.3% 6.8% 7.9%

Other 470 490 510 540 4.4% 4.3% 4.1% 5.9%

Private Total 15,020 15,450 16,330 17,400 3.0% 2.9% 5.7% 6.6%

Federal 8,050 7,880 7,940 7,970 1.4% -2.1% 0.8% 0.4%

State 1,570 1,600 1,660 1,720 1.9% 1.9% 3.8% 3.6%

Local 5,050 5,170 5,370 5,560 2.4% 2.4% 3.9% 3.5%

Government Total 14,670 14,650 14,970 15,250 1.8% -0.1% 2.2% 1.9%

Total C&E 29,690 30,100 31,300 32,650 2.4% 1.4% 4.0% 4.3%

Source: Environmental Business International, Inc., San Diego, CA, units in $mil.

Environmental Business Journal, Volume XXXI Number 9/10

6 Strategic Information for a Changing Industry

U.S. Census Data on Environmental Consulting Services for 2015: NAICS Code 54162

FirmsEstablish-

mentsAvg

OfficesEmployees

Avg Employees

Est Rev @150k

Estimated Share

500+ Employees 72 706 9.8 143,720 1,996 21,560 69%

100-500 Employees 117 527 4.5 15,657 134 2,350 8%

20-100 Employees 625 1,000 1.6 22,838 37 3,430 11%

<20 Employees 7,680 7,771 1.0 26,028 3 3,900 12%

Total: NAICS Code 54162 8,494 10,004 1.2 208,243 25 31,240 100%

Source: Environmental Business Journal adapted from U.S. Census Bureau, 2015 data; Revenues per employee estimated at $150,000 per employee.

Gross Revenue Performance of Environmental C&E Firms in EBJ Database: 2009-20172009 2010 2011 2012 2013 2014 2015 2016 2017

Flat 7% 8% 9% 9% 8% 8% 7% 8% 11%

Growth 33% 65% 57% 60% 64% 62% 73% 69% 67%

Decline 60% 28% 34% 31% 29% 30% 19% 23% 23%

Source: EBJ’s database of C&E firms; 600-700 with revenues reported in 2009-2017; Flat represents less than 1% growth or decline or ‘Flat’ in response to survey or interview

Infrastructure segments mostly associ-ated with solid waste, drinking water and wastewater systems all look to post more steady annual growth of 3-5% as invest-ment momentum continues in these still largely underfunded assets. More trends on the infrastructure segments and the environmental testing segment will be presented in a subsequent environmental industry overview edition of EBJ.

Business trends in the consulting & engineering segment can usually be sum-marized in clients, services, media, geogra-phy and companies which are the 5 main dimensions that EBJ uses to break down the C&E business in the analytical frame-work of its C&E industry model. Detailed tables and charts on the C&E industry are presented in the following pages with vary-ing levels of detail and in the C&E dataset.

Noteworthy highlights in the client breakdowns include the significantly high-er growth in private sector markets in the last two years, compared to government growth rates. Since the year 2015, private sector markets for environmental con-sulting & engineering firms have gained a net of $2.4 billion in annual revenues compared to only half a billion dollar gain in government markets. Oil & gas and chemicals, due to both their size and their relative growth, have paced this recent pri-vate sector growth. Power and water utility companies and renewable energy as well as property developer markets have also

Revenue Performance of U.S. Environmental C&E Firms by SizeFirms 2013

Firms 2017

Net 2017

2015 Growth

2016 Growth

2017 Growth

Big >1 bil 6 4 7,582 -0.1% -0.4% 2.8%

Large>100 mil 45 46 11,526 2.2% -0.2% 5.4%

Mid 20-100 mil 135 148 5,566 4.9% 3.4% 3.4%

Small 10-20 mil 142 153 1,980 3.8% 3.2% 2.1%

Small 5-10 mil 187 219 1,388 4.1% 6.3% 5.7%

Small 1-5 mil 767 790 1,719 3.0% 5.2% 5.1%

Small <1 mil 6,694 6,718 1,541 5.0% 5.6% 4.7%

Total 7,976 8,078 31,302 2.4% 1.5% 4.0%

Source: Environmental Business Journal’s annual models of the U.S. environmental consulting & engineering industry. Note: Prior to 2017 firms of 1-2 persons or sole proprietorships were not counted in the number of firms columns and totals were in the 3,200-3,300 range

Distribution of U.S. Environmental C&E Firms in 2017

Envl Revs Only FirmsGross

Env’l C&EAverage

Net Env’l C&E Revs

% of Mkt% of Gross

Big >1 bil 4 8920 2230 7,582 24% 25%

Large>100 mil 46 13248 288 11,526 37% 38%

M 20-100 mil 148 6254 42 5,566 18% 18%

S 10-20 mil 153 2084 14 1,980 6% 6%

S 5-10 mil 219 1446 6.6 1,388 4% 4%

S 1-5 790 1800 2.3 1,719 5% 5%

S 0.2-1 mil 2109 1015 0.5 997 3% 3%

S <200k 4609 554 0.1 544 2% 2%

Total 8078 35321 4.4 31,302 100% 100%

Source: Environmental Business Journal’s annual model of the U.S. environmental consulting & engineering industry.

Environmental Business Journal, Volume XXXI Number 9/10

7 Strategic Information for a Changing Industry

U.S. Environmental Consulting & Engineering Industry

Source: EBI Inc., San Diego, CA, based primarily on annual surveys of C&E firms, units in $mil.

1,330 1,410 1,240 1,470 2,100 2,7801,710 1,640 1,720 2,280 2,6803,3401,750 2,730 2,920

3,2603,970

4,840

5,0905,130

7,170

8,7508,050

8,040

3,5904,230

5,950

6,4606,620

7,690

1,3501,450

2,240

2,7403,630

4,690

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1995 2000 2005 2010 2015 2020

Other

S tate & Lo c al

F ederal

Indus trial

P o wer

Oil & G as

C hemic al

posted well above average growth, and as EBJ’s rolling ‘Snapshot’ surveys show, oth-er high-growth client categories include healthcare, tech, and to a lesser extent hospitality, retail and institutional markets like universities and K-12 education that manage a significant platform of real estate and the incumbent risks associated with land assets and the built environment.

OIL PRICE SWINGS No private sector market discussion

is complete without reference to the per-petually unpredictable fluctuations of oil prices that can play an outsized role in environmental industry dynamics, at least for the many companies who count them amongst their major clients. As the Brent crude price charts on page 9 show, crude oil prices peaked at $140 a barrel in July 2008, but crashed to $35 a barrel at the end of December 2008 during the global financial crisis that became known as the Great Recession. Six months later, by the end of June 2008, the price had recovered somewhat, doubling to $70 a barrel, and then increased fairly steadily the next three years to hit $120 a barrel in April 2011.

The price of Brent crude traded in a fairly consistent range between $100 and $120 a barrel for the next three-and-a-half years in 2011-2014. Brent crude saw the $100 per barrel price for the last time in September 2014, and it then collapsed by half to $50 a barrel in only 4 months by January 2015, and bottomed out a year later at $26 a barrel on January 20th 2016. Starting in February 2016 at around $30 a barrel it took more than 18 months to get to $60 in October 2017, an oft cited threshold for upstream development of horizontal drilling or shale oil resources in North America. To the surprise of most analysts the price continued to over $80 a barrel in May 2018, and hit a 4-year peak at $86 on October 4th 2018. At the end of 2018 the price of Brent crude had dropped back to $50 a barrel more in line with, but significantly lower than 2019 average per barrel price of $61 expected by the U.S. Energy Information Administration. Suf-fice it to say the cycle of oil price volatil-ity is unlikely to change, making industry forecasts and predictions problematic, but environmental service companies are fairly

U.S. Environmental Consulting & Engineering Industry by Client

Source: EBJ annual model of the U.S. environmental consulting & engineering units in $mil

U.S. Environmental C&E Industry: US vs. non-US Revenues

Source: Environmental Business International Inc. EBJ annual model of the U.S. environmental consulting & engineering firms based primarily on annual surveys and revenue analysis of C&E firms, units in $mil and $bil.

2,150 2,280 2,440 2,720 2,880 2,880 2,680 2,690 2,860 3,050 3,190 3,3401,630 1,710 1,820 1,990 2,120 2,300 2,470 2,610 2,770 2,960 3,100 3,2503,180 3,260 3,410 3,620 3,720 3,840 3,970 4,010 4,200 4,460 4,650 4,8408,470 8,750 9,010 9,210 8,350 7,940 8,050 7,880 7,940 7,970 8,000 8,0406,580 6,460 6,510 6,590 6,420 6,470 6,620 6,770 7,030 7,280 7,550 7,690

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Chemical Oil & Gas Pow er Industrial Federal State & Local Other

18.1 19.5 21.1 22.5 23.3 22.2 22.5 23.2 24.1 23.4 23.6 24.1 24.4 25.5 26.8 27.7 28.5

2.602.81

3.033.36 3.83 4.01 4.29 4.56 4.91 5.28 5.40 5.64 5.69 5.79

5.89 6.09 6.30

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2004 2006 2008 2010 2012 2014 2016 2018 2020

USA Non-US

Environmental Business Journal, Volume XXXI Number 9/10

8 Strategic Information for a Changing Industry

Source: Environmental Business International Inc. (San Diego, CA), Envi-ronmental Business Journal & EBI Report 728. Figures in EBJ’s list of top ranked C&E firms are revenues generated for calendar year 2017 in gross environmental consulting & engineering (C&E) not including construction and remediation construction, but including project management/construction management. Environmental construction (air, waste, water), remediation con-struction and federal waste management or contracting services are counted in the middle column labeled Cont/HW. This list is a result of independent research and EBI surveys. In some cases, revenues are approximations derived from executives, analysts and reputable business information sources and published materials. Although EBI has made every reasonable effort to be accurate, figures are not the result of internal or external audits and are not guaranteed to be accurate. Errors and omissions are unintentional.

Top U.S. Environmental C&E Firms in 2017Company Gross $mil Cont/HW Env’l C&EAECOM 18,482 1,233 3,018 Jacobs (CH2M in 2017) 15,125 1,560 2,675 Tetra Tech 2,850 839 1,959 Stantec Consulting 3,093 - 1,268 Arcadis 3,503 50 911 ERM 902 - 902 Golder Associates 997 - 817 Leidos 10,581 - 541 Black & Veatch 3,361 381 493 CDM Smith 1,173 331 490 Ramboll 1,620 - 486 SNC-Lavalin (Atkins in ‘17) 9,080 - 454 ICF 1,246 - 436 HDR Inc. 2,362 672 425 Fluor Corp. 18,678 1,870 391 GHD 1,373 123 372 Brown and Caldwell 363 - 363 Parsons 3,486 123 330 Wood Group (Amec FW in 2017) 6,328 760 316 NV5 368 - 313 TRC Companies 887 - 310 Carollo Engineers 272 - 272 GeoSyntec Consultants 285 - 251 Hazen and Sawyer 244 - 244 Louis Berger (WSP in 2018) 948 - 237 WSP Global 5,050 79 224 Burns & McDonnell 2,683 62 206 Woodard & Curran 203 - 199 OBG: O’Brien & Gere 271 - 198 WorleyParsons 3,290 - 197 Weston Solutions Inc. 297 - 196 Cardno Ltd. 880 - 194 Battelle 887 - 177 SCS Engineers 185 19 166 Terracon Consultants, 660 - 165 Bureau Veritas 617 - 160 Apex Environmental* 156 - 156 Huntington Ingalls 7,441 - 150 Kleinfelder Inc. 372 - 149 EA Engineering Sci and Tech 146 - 146 Michael Baker Corp. 611 - 141 Haley & Aldrich Inc 192 - 134 North Wind Inc 269 70 132 Mott MacDonald 2,278 - 131 Navarro Research and Engineering 148 - 120 Trinity Consultants 118 - 118 ATC Group Services 253 70 117 Langan EES 248 - 112 Ecology & Environment 105 - 105 GEI Consultants 162 - 102 CEC Civil & Environmental Consultants 135 - 99 SWCA Environmental Consultants 97 - 97 Anchor QEA 91 - 91 HydroGeologic 90 - 90 Bechtel Group 25,617 1,705 88 Freese & Nichols 151 - 88

accustomed to being prepared for their oil & gas compa-nies to either turn on or turn off the demand spigot on a moment’s notice.

RESILIENCY SHOOTS UP SERVICE CHARTSService trends show information management and in-

formation technology applications as the highest rated growth categories for C&E firms. IT applications and the increasing strategy amongst C&E leaders to acquire and develop their own proprietary IT assets is a trend delved into later in the profiles included in this edition (see pages 11-29). The relatively generic categories of project man-agement and project engineering are rated for growth not too far behind IT, but notably ahead of investigations or impact statements or permitting or most other forms of ‘front-end’ work which fell down the ranking list (see table on page 10), as construction trumps analysis & planning.

Resiliency planning debuted on EBJ’s survey list and ranks 4th out of 20 service sub-categories. Resiliency in the face of adverse weather events and natural disasters, and yes even long term climate change impacts, all have seen notable increases in demand across almost all client sec-tors. While resiliency and climate change adaptation proj-ects are not often standalone projects or the primary objec-tive on integrated projects, they are increasingly required elements of more and more projects related to any form of asset management, and particularly infrastructure. (Cur-rent research by EBI on climate change adaptation practice areas will be published in an upcoming edition of CCBJ.)

A final note on services is that private sector remedia-tion, redevelopment and brownfields moved up the charts to the 5th rated service category in terms of prospects for growth in the next 2 years, but that government reme-diation fell all the way to the bottom, notwithstanding a number of companies who reported some recovery in their Department of Defense remediation projects in 2018.

Looking at the environmental consulting & engineering industry by media, perhaps the most telling story is to look at market breakdowns in 5 year increments as portrayed on the chart on page 1. Here you can see the steady growth of water and wastewater markets from less than $2 billion in annual revenues in 1995 to $6-7 billion in 2020, and air quality markets going from $1.2 billion to $2.7 billion.

Environmental Business Journal, Volume XXXI Number 9/10

9 Strategic Information for a Changing Industry

USA Energy-Related Carbon Dioxide Emissions By Fuel 1990–2016 (million metric tons of carbon dioxide)

Source: U.S. Energy Information Administration, Short-Term Energy Outlook Figures, June 2018; Natural gas CO2 emissions surpassed those from coal in 2016. CO2 emissions from petroleum and other liquids, which have been the largest source of energy-related CO2, have been increasing since 2012 after remaining relatively constant from 2004 to 2007 and then generally decreasing through 2012. Since the beginning of the 2007–09 recession, coal CO2 emissions have also generally declined. Although total coal CO2 emissions in 2016 were lower than those from petroleum and other liquids, coal is more carbon intensive, with more CO2 released per Btu of energy. The decline in coal CO2 emissions has contributed to a lower overall carbon intensity of U.S. energy consumption and kept emissions below pre-recession levels. Natural gas CO2 emis-sions have increased every year since 2009. The natural gas share of electricity generation has grown as coal declined, partially offsetting the decline in coal CO2 emissions from coal, and natural gas CO2 emissions sur-passed coal in 2016. However, because natural gas produces more energy for the same amount of emissions as coal, growth in natural gas consumption contributed to the overall 2016 decline in total emissions.

0

1000

2000

3000

4000

5000

6000

7000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Coal Natural Gas Oil

Consulting work related to the ongoing generation of hazardous waste and com-pliance associated with hazardous waste management and exposure to hazardous materials has been the only significant cat-egory to decline in annual revenue from 1995 to 2015, losing about $1 billion. Market growth in remediation services has held up, although the rate has reduced in recent years. The emergence of renewable energy consulting & engineering services, as well as the sustained position of natu-ral resource markets is also evident on the charts.

In terms of companies the fairly unique characteristic of the environmental con-sulting & engineering business that the top companies do not inexorably take over more and more market share has been noted in the past in EBJ, but is worth reit-erating. The combined factor of the federal government sequestration in 2013, fol-lowed by the oil price crash highlighted the heavy dependence of the larger environ-mental consulting & engineering firms on those two major market categories, prob-ably more than any industry structural dynamic has impeded the competitiveness of the largest firms. That being said there are factors that feed growth into the lower tiers of the market including the broad-based client sectors in municipal and state government markets and small industry. Also the environmental consulting & en-gineering business has relatively low barri-ers to entry for those with qualifications or experience who want to launch their own business or branch off from existing firms. This latter effect has been in evidence for some time in the industry, and generally is exaggerated during larger waves of merger and acquisition activity, not unlike we have seen in recent years.

The fluidity of talent is not the most welcome syndrome to executives. A re-cent EBJ Environmental Industry Sum-mit panelist called for a truce of compa-nies hiring away his managers at 20-30% raises, impractical yes, but indicative of the likely perpetual competition for tal-ent in the environmental industry. While the people performing the project work are generally the same people, the corpo-rate players booking that revenue have changed over time. The table and chart on

Crude Oil Price 2003-2019: Brent Spot Price (Dollars per Barrel)

Crude Oil Price 2016-2019: Brent Spot Price (Dollars per Barrel)

Source: U.S. Energy Information Administration citing Thomson Reuters

0

20

40

60

80

100

120

140

J an-03 J an-05 J an-07 J an-09 J an-11 J an-13 J an-15 J an-17 J an-19

0

20

40

60

80

100

J an-16 J an-17 J an-18

Environmental Business Journal, Volume XXXI Number 9/10

10 Strategic Information for a Changing Industry

Percent of U.S. Personal Transportation Units or ‘Cars’: 2020-2050

2018 Survey

2017 Survey

2018

Self-Driving in 2020 7.8% 10.05% -2%

Self-Driving in 2030 17.9% 20.23% -2%

Self-Driving in 2050 36.8% 40.43% -4%

Electric in 2020 11.4% 12.25% -1%

Electric in 2030 26.1% 23.17% 3%

Electric in 2050 44.3% 44.03% 0%

US Life Expectancy

2018 Survey

2017 Survey

% Change in 2018

2020 78.6 78.8 (0.2)

2030 80.1 80.2 (0.1)

2040 81.6 81.9 (0.3)

2050 83.4 83.8 (0.4)

2100 85.2 86.7 (1.5)

Source: EBJ 2017 & 2018 Snapshot Surveys.

Ranking of Environmental Markets by Services2018 Rank

2017 Rank

IT/EMIS software/systems/training 1 4

Project mgmt./Construction mgmt. 2 1

Design and project engineering 3 2

Resiliency planning 4 --

Private remed/redev/brownfields 5 7

Operations & maintenance 6 5

Permitting/compliance 7 12

Industrial waste mgmt/in-plant svcs 8 6

Water recycling/reuse 9 8

Energy: Performance contracting 10 11

Green building design/construction 11 14

Outsourcing EHS functions 12 3

Impact Assessment & Permitting 13 --

Investigations/assessments/audits 14 10

Monitoring & analytical work 15 9

Smart growth/”green” planning 16 16

Ecological restoration 17 18

Waste minimization 18 13

Solid waste diversion/recycling 19 15

Gov’t remed/base closure/conv 20 17

Source: EBJ Snapshot Surveys in 2018: “Prospects for growth in the next two years”

page 4 illustrate that the top 5 companies account for just 28% of the C&E market today and the top 10 only 37%. And as the table at the bottom of the page shows today’s top 5 represented only 2% of the market in their corporate entities in 1995. Comparing these numbers to other indus-tries shows why many still characterize the C&E industry as fragmented and holding potential for future M&A opportunities. The availability of capital also supports ongoing consolidation, but a still relatively finite number of actively acquiring firms and the large number of small growing firms indicate that the level of fragmenta-tion will remain relatively high compared to other industries.

Comparing recent growth as a function of company size (see table on page 6) shows that the largest companies at least have re-turned to positive revenue performance from collective decline in 2013 and 2014, although in aggregate the largest firms still trail smaller companies in growth. Mid-size companies have perhaps been more aggressive in acquiring and promoting or-ganic growth, and that looks to continue with the dynamics of active private equity investors, seasoned management and more engaged internal shareholders feeding the

drive for growth.

One last note on the company ‘universe’ in environmental consulting & engineer-ing as EBJ has called it, we have added a sub-category at the small end of the market given the availability of more accurate U.S. Census data based on North American Industry Classification (NAICS) system codes and elimination of double count-ing in government databases. The raw data somewhat restructured from the U.S. Census Bureau is presented on page 6 with EBJ’s universe model portrayed below. The EBJ model previously did not count sole proprietorships or 1- and 2-person compa-nies in the firm count, but given their large numbers we have now included the line item at the bottom of the chart. This in-creases the total environmental C&E firm count to from 3,600 to 8,000, although the revenue contribution from the smallest companies to the entire industry has only changed marginally from EBJ’s previous C&E industry model that estimated the revenue contribution but not the absolute numbers of sole proprietorships.

Nevertheless firms generating less than $1 million in annual environmental C&E revenue represent 5% of the industry, and $5 million or less about 10% of the indus-try, so as one observer said, “anybody can be a consultant.” And while barriers to en-try are low, the prevailing concern is there being sufficient quality engineers and proj-ect managers to sustain growth and client relations in a still growing and expanding market in terms of types of expertise de-manded by the diverse client base.

We can all admit that the environmen-tal consulting profession lacks glamor and that not many Halloween trick-or-treaters dress up as environmental consultants or climate change resilience specialists, but glamor is not what got most of the first generation of company owners into the profession in the first place. Perhaps to-day’s political dynamics and new wave of environmental, economic and social chal-lenges will instigate a new wave of talent into the industry. The environmental in-dustry can only hope so. There is certainly much more work to be done.

Environmental Business Journal, Volume XXXI Number 9/10

11 Strategic Information for a Changing Industry

NV5 Acquires SkysceneIn December 2017, NV5 Global

acquired Skyscene LLC, a leading provider of Unmanned Aerial Vehicle (UAV) flight services headquartered in San Diego, California. NV5 antici-pates that the acquisition of Skyscene will initially add $5 million to opera-tions. The acquisition was made en-tirely in cash and will be immediately accretive to NV5’s earnings. Integrat-ing NV5’s LiDAR (Light Detection and Ranging) mapping technology with Skyscene’s UAV flight services positions NV5 as one of the leading UAV LiDAR aerial mapping service providers in the nation. Traditionally provided with fixed wing aircraft or helicopters, the use of UAV LiDAR adds value to NV5 clients by provid-ing higher resolution mapping, rapid mobilization, and more cost effective services than can be achieved using manned aerial vehicles or traditional survey methods.

NV5 STAYS ON LEADING EDGE IN ACQUIRING DRONE SERVICES FIRM SKYSCENE AND BUILDING OPTIMIZER ENERGENZ

NV5 Global, Inc. is a provider of professional and technical engineering and consulting solutions ranked #45 in the Engineering News Record Top 500 Design Firms list. NV5 serves public and private sector clients in the infrastructure, energy, construction, real estate and en-vironmental markets. NV5 primarily focuses on five business verticals: construction quality assurance, infrastructure engineering and support services, energy, program management, and environmental solutions. The Company operates out of more than 100 locations nationwide and abroad in Macau, Hong Kong, and the UAE. Since its inception in 2009, NV5 has grown into a client focused consulting firm with $500M in annual revenues. The firm’s growth has been accomplished through a combination of strategic acquisitions and organic growth with a focus on cross-selling services throughout the NV5 platform.

Scott Kvandal serves as Chief Synergy Officer of NV5. He has over thirty years of experience in the infrastructure engineering industry. Most recently, Mr. Kvandal was Chief Operating Of-ficer of the Western Region of Bureau Veritas North America, where he grew the firm to national leader in code compliance and operating revenue within his group to $120 million. Before joining Bureau Veritas, Scott was President of Berryman & Henigar, and earlier, he served as President of Barrett Consulting Group. As Chief Synergy Officer of NV5, Scott is responsible for enhancing the cross-selling of services between the firm’s five business verticals leading to ac-celerated organic growth.

EBJ: Which are the key technology solutions that NV5 provides? How is technology changing the way that NV5 operates?

Kvandal: NV5 is continually seek-ing ways to enhance the value of services provided to our clients through new and evolving technologies. Two new technolo-gies that NV5 has incorporated into the delivery of our service offerings is the use of Unmanned Aerial Vehicles (UAVs), commonly referred to as “drones” and our energy management and sustainability services through the recent acquisition of Energenz by NV5.

USING UAVS WITH ADVANCED SCANNING EQUIPMENT

Entry-level UAV applications are use-ful in taking pictures and videos. However, a completely different level of expertise, technology and equipment are required for creation of full planimetric drawings or full engineering-grade topographic maps with surfaces and mark-outs. The substan-tial technology investment, experience and commitment are simply beyond the in- house capabilities and resources of most organizations.

Our UAV division provides aerial map-ping using LiDAR and digital imagery. These different but complimentary datas-ets are often used in conjunction to pro-duce planimetrics, topographical maps, 3D surfaces with break lines and contours, as well as overhead and underground util-ity mapping and design. We operate UAVs that carry highly sophisticated equipment on board; for example, a survey-grade LiDAR scanner and IMU (Inertial Mea-surement Unit), thermal cameras, multi-spectral cameras and cameras designed for stereo collection for photogrammetry.

Terrestrial (land-based) and manned aircraft LiDAR has been in use for a num-ber of years, but until recently, the technol-ogy for acquiring LiDAR data from UAVs has been unavailable.

UAV data collection is performed by our highly trained and certified pilots. They set up NV5’s state-of-the art equip-ment and operate it correctly, following safety guidelines out in the field while working near high tension lines, power lines and transmission poles. Each system is equipped with an onboard Global Navi-gation Satellite System (GNSS) receiver, which is used to create a post-processed

trajectory when paired with a local base station on the ground. Finally, data is tied down to, and checked against survey ground control to ensure that the accuracy standards for each project are being met.

We are committed to keeping up-to-date on accuracy standards, and often reference publications such as the United States Geological Survey’s LiDAR Base Specification and the American Society for Photogrammetry and Remote Sensing’s Accuracy Standards for Digital Geospatial Data.

ENERGENZ: TECHNOLOGY TO OPTIMIZE BUILDINGS

Today building lifecycle management is governed by two overriding missions: to keep energy efficiency at an all-time high and operating costs at an all-time low. However, in a world where physical in-frastructures haven’t quite kept pace with its digital counterparts, organizations are soon realizing the value proposition that resilient structures and energy-efficient buildings bring. Effective energy use goes far beyond motion-sensor lighting, and there is a real opportunity for improving

Environmental Business Journal, Volume XXXI Number 9/10

12 Strategic Information for a Changing Industry

the operational value of mechanical sys-tems in a building. In such a scenario, En-ergenz is redefining efficiency in the built environment by diving deep into compli-cated mechanical systems to discover the hidden defects followed by quantifying and fixing those defects with controls opti-mization. Primarily an engineering consul-tancy, Energenz partners with clients to re-duce operating costs in energy spend while improving the life of a building through environmentally safe measures.

Following a technology and data-driven approach, Energenz has a team of engi-neers that use software to carry out ana-lytics on big data in order to monitor and continuously commission a building.

EBJ: How does NV5 differentiate from competitors from the technology stand-point?

UAV SERVICESSome companies have their own in-

house UAV group, but the capabilities are usually limited and not sufficient for engineering design. Building a substantial in-house UAV operation is not practical for most organizations. They might invest in the equipment only to realize they do not have the highly-experienced, dedicated staff or necessary training to provide qual-ity UAV mapping services.

Even organizations with full aviation departments find it challenging to intro-duce UAVs into their operations. The as-sociated expense for equipment and crews is often a barrier to entry.

Instead, it’s more efficient and econom-ically viable for companies to work with an experienced, full-service UAV mapping provider like NV5. We are invested in pro-viding the best UAV mapping services by having a dependable UAV division. We employ full-time highly-trained licensed pilots, mapping staff and a management team that continually provide these ser-vices to clients and teaming partners.

MONITORING BASED COMMISSIONING (ENERGENZ)

Many of our competitors follow a tra-ditional approach to optimizing buildings, a one-off type of assessment that looks at a

snap shot of information from the build-ing data and relies on physical inspections and manual spreadsheet based analysis by a team of engineers. This approach tends to be cyclical, initially energy savings are achieved and costs are decreased.

However, over time (12 – 36 months), the building will drift back to its original state and the process will need to be carried out again.

Utilizing technology, Energenz con-nects to a building and continuously gathers thousands of data points at very granular time intervals. This not only al-lows us to do a much deeper dive into the opportunities for energy savings in a more efficient manner, it also enables us to con-tinually monitor and further optimize the building over time. The end result is that we not only significantly reduce the energy costs within the building, we maintain these reductions over time.

EBJ: You acquired Skyscene about a year ago. Can you give us some back-ground on the technologies that you acquired through Skyscene?

Kvandal: NV5 first began contract-ing Skyscene as a subconsultant for pro-viding drones, licensed pilots, and UAV operational knowledge for existing NV5 projects. NV5 has an expansive survey department that has been using terrestrial LiDAR equipment for a number of years. Our power delivery energy clients have been requesting more detailed inspections of their electrical transmission and distri-bution facilities in which a survey grade LiDAR unit mounted on a UAV would provide. After some initial testing and veri-fication of the accuracy in data collection, NV5 acquired Skyscene in 2017.

Many use a one-off assessment that looks at a

snapshot of information from building data... Energenz

connects to a building and continuously gathers thousands

of data points.

The combination of NV5’s expertise in the use of LiDAR scanning equipment and processing, combined with the experience and expertise in advanced UAV operations, has proven to be a powerful combination and has now become a differentiator in the marketplace.

EBJ: Can you provide an overview of the type of demand that this type of technologies have on an industry level?

UAV SERVICESThe uses for UAV services have been

expanding both in nature and in volume as the industry becomes more aware of the potential applications. The demand and nature of UAV applications has continued to increase as we educate our current and future clients with the capabilities of us-ing UAVs with a variety of technological sensors.

A few of the applications in highest de-mand include:

• Inspections of power utility in-frastructure

With the use of UAV LiDAR tech-nology, NV5 is not only able to provide detailed inspections of aerial facilities in a safe manner but also able to import the LiDAR data into PLS-CADD classifica-tion and design software. We are able to provide an entire, full-service solution to our clients from start to finish.

• Mining Operations Support Ser-vices

With the use of UAVs and remote sen-sors, NV5 is able to periodically map min-ing operations and quickly provide accu-rate measurements of mining volumes that cannot be provided using conventional surveying techniques.

• Topographical Mapping thru Vegetation

Because of the nature of LiDAR scan-ning, NV5 is able to map the surface to-pography through thick vegetation, for ex-ample, thru sugar cane fields. This cannot be performed using conventional survey-ing methods without clearing or damaging the vegetation.

Environmental Business Journal, Volume XXXI Number 9/10

13 Strategic Information for a Changing Industry

• Topographic Mapping

Whereas using conventional survey-ing and use of manned aircraft for topo-graphic mapping is commonplace today, we believe that UAV mapping will be the standardized delivery approach in the fu-ture. Our UAVs carry the same equipment on board as a manned aircraft, but UAVs can fly lower and slower, capturing denser, more accurate data.

• Solar Farm Installations and Per-formance Monitoring

In addition to providing the necessary topographic mapping required for the de-velopment of new photovoltaic solar, NV5 is able to use UAVs mounted with thermal cameras that can be used in conjunction with specialized software applications to monitor the individual photovoltaic pan-els’ performance. This ability not only provides owners to routinely evaluate their solar field’s performance but gives them detailed information of panel performance that is otherwise necessary to be collected manually and thereby incurring extensive labor costs.

• Commercial Roof-Mounted Photovoltaic Installations

During the design process for a large roof mount (>1MW), a detailed roof plan is critical to maximizing system opera-tion, permitting and safe operation of the project long-term. Traditionally, attaining a detailed roof plan requires a significant amount of time and investment compar-ing as-built drawings, online aerial imag-ery, and a detail site visit with multiple people actually pulling tape to locate fea-tures and validate dimensions. The high resolution imagery, LiDAR and other im-aging technologies offered by NV5’s UAVs cuts out a majority of that investment as we are able to provide a detailed roof plan from a single UAV flight with sufficient detailed imagery to ensure that return site visits are not required. Additionally, the collected data enables designers to opti-mize roof arrays with greater confidence to the real world shade profile throughout the day and year.

Finally, NV5’s UAV group’s rapid de-ployment and short lead time to turn-

around final roof plan drawings saves time and money in the solar project’s develop-ment cycle.

EBJ: Have the technology acquisitions had an impact in NV5’s overall profits?

Kvandal: The acquisition of both Skyscene and Energenz have been accre-tive to NV5’s earnings. With that said, the growth of these new technologies is somewhat buffered by the ability of our clients to understand (it requires an educa-tion) the technology, its ability to provide more accurate data and the value of the enhanced service offering. For instance, while the power and energy utilities have quickly embraced the use of UAV tech-nologies, others like State Departments of Transportation have been more reluc-tant to adopt the new technology. Often, we have provided a real test in the clients’ use of conventional technology to that of using UAVs. The increased accuracy com-bined with a more cost-effective solution quickly becomes apparent, but it requires an education process.

We believe that we are a little ahead of industry’s full acceptance... We want to be

on the “leading edge”, but not on the “bleeding edge” as we integrate new technologies.

EBJ: What was the main reason behind these acquisitions?

Kvandal: The main reason for the ac-quisitions was primarily responding to an identified need in the industry but, in the case of Skyscene, we were encouraged from one of our utility clients as they had a high demand for the service and were unable to develop the technology internally.

EBJ: Change and integration is always challenging. How have you been able to complement the services that you provide with these new technologies? What type of training did you provide to NV5’s personnel regarding the new technology?

Kvandal: The integration of the tech-nologies has been quite synergistic without too many challenges. The integration of new technologies, which have recognized to be of high value to our clients, has been embraced by our technical teams and cli-ent managers. The challenge in the case of UAV services, has been the speed at which we can train our staff in the efficient pro-cessing of data. For every hour of data col-lection flight time, there is typically one to two days of data processing time required by well-trained and experienced data pro-cessors.

As a team of engineers and consultants, we view the software and technology we use as a tool to provide value to our clients through our services. We invest significant time and effort into improving the tech-nology in order to enhance these service offerings and deliver them more efficiently and cost effectively.

There have been opportunities to utilize the technology for other NV5 services such as commissioning, training is provided to the engineers within this business unit, so they can effectively utilize these tools to enhance their processes and differentiate from the competition.

EBJ: Why do you consider that the transaction was performed at the right time? How does it fit in your overall growth strategy?

Kvandal: We believe that we are a little ahead of industry’s full acceptance of these new technologies. But, this is exactly where NV5 wants to be positioned. We want to be on the “leading edge”, but not on the “bleeding edge” as we integrate new tech-nologies. NV5 was well experienced in the use and application of terrestrial LiDAR. Combining the use of LiDAR with a drone was a natural next step technology.

NV5’s tag line is “Delivering Solutions – Improving Lives”. Part of our strategy is to incorporate new technologies into the delivering our solutions, i.e., Delivering Solutions – Thru Leading Technologies”.

EBJ: Do you have in-house personnel devoted to technology related R&D?

Kvandal: NV5 does not have a team of personnel dedicated to developing new

Environmental Business Journal, Volume XXXI Number 9/10

14 Strategic Information for a Changing Industry

technologies. We believe the strategy of identifying new technologies developed in the industry and integrating them into our service offerings is a faster and more cost-effective solution for NV5.

EBJ: Will you consider acquiring ad-ditional technology related companies? Which are the technologies that you believe would be of high value to your organization and your clients?

Kvandal: We are looking into incorpo-rating new technologies for use in the en-ergy compliance regulations and sustain-ability as well as in the security of facilities and property.

EBJ: Are you currently using technol-ogy as a way of diversifying NV5’s rev-enue streams into a more recurring or subscription-based revenue as opposed to the traditional project based, “time for money” model?

Kvandal: We like the recurring revenue model and believe our Energenz services are well-suited for the subscription-based revenue model. We financially engage with our clients using a subscription- based model where we charge a monthly fee. This subscription-based revenue makes us extremely “sticky” with our clients. They literally see the NV5 logo in front of them every day. This not only positions us per-fectly for additional services such as Com-missioning and MEP design, we continue to have that long-term relationship with every client we sign up, this is so powerful in itself. As a large portion of this service is automated once we are set up, it also en-ables us to recognize revenue not tied to head count and achieve higher margins due to breakage, much like a Netflix ac-count.

EBJ: How do you think that tech services M&A is driving growth in the environmental industry?

Kvandal: NV5 seeks to acquire new technologies in order to add value to our clients and differentiate our firm in the marketplace.

KCI COMMITS TO INNOVATION STRATEGY: ACQUIRES LASER SCANNING FIRM LANDAIR

KCI is a 100-percent employee-owned engineering, consulting and construction firm serv-ing clients throughout the United States. Their multi-disciplined service offerings allow them to provide exceptional turnkey expertise to federal, state and local government agencies, as well as institutional and private-sector clients. Operating out of more than 40 offices in 17 states and the District of Columbia, KCI’s team of more than 1,400 professionals offer technical expertise in transportation, resource management, environmental, telecommunications, utilities, facili-ties, and construction. Over the last decade, KCI has grown dramatically, more than doubling the size of their team, their top line sales, and bottom line net operating income. This growth has been achieved through a combination of organic growth and strategic acquisitions. KCI has completed one or two acquisitions each calendar year since 2012.

KCI CEO/President Nate Beil, PE, DWRE, joined KCI Technologies Inc. in 1988. Within four years, he started the company’s Water Resources Division, which became one of KCI’s top-performing business units. From 1995 to 2001, Nate served as head of KCI’s Environmental Group, and in 2001 he was promoted to manager of the firm’s Mid-Atlantic region. He has served as president of KCI since 2006, and assumed the role of CEO in 2018.

Thomas Sprehe, PE, BCEE, is a Senior Vice President and Director of Innovation and Technology. He joined KCI in 1997, assuming the role of vice president and head of the envi-ronmental division. In 2002, he was promoted to senior vice president and named manager of KCI’s environmental market, which includes the firm’s water, wastewater, solid waste and geo-technical engineering, hazardous waste and environmental compliance, and industrial hygiene practices. In 2017, Tom took on the role of director of innovation and technology.

EBJ: You acquired LandAir Surveying a little over a year ago. Can you give us an overview about LandAir Surveying and the technologies that you acquired?

KCI: Founded in 2001 by President and CEO H. Tate Jones, PLS, LandAir began as a traditional surveying company but quickly embraced the ongoing tech-nological evolution occurring within the industry. In 2005, the firm began offering laser scanning and has since grown in ca-pabilities and reputation to be considered among the top 3-D laser scanning firms in the country. Their team offered an array of geospatial services, including aerial map-ping, helicopter and fixed wing LiDAR (Light Detection and Ranging), terrestrial laser scanning, drone data capture, aerial photography, building information mod-eling (BIM) and virtual construction ser-vices.

EBJ: Can you provide an overview of the type of demand that this type of technologies have on an industry level?

KCI: LiDAR, laser scanning and un-manned aerial systems (drones) dramati-

cally improve the quality of visual in-spection, engineering and construction monitoring while reducing the overall cost of these services. Liability reduction is a major driver for 3-D modeling, as con-struction interferences may be significantly reduced. In construction, 3-D modeling allows for efficient pre-fabrication of com-ponents prior to installation in the field, as well as providing an essential tool for future asset management of those compo-nents by the owner.

Applying these technologies to service areas that had been performed using con-ventional methodologies is having signifi-cant impacts by reducing labor costs and improving efficiencies. They reduce the need for manpower while improving deliv-erables through applied technology.

In many ways, KCI has had to generate demand for the services through educa-tion and improved service. By introducing these technologies and then proving their efficiency, we have seen demand grow sig-nificantly to the point where our clients ask for these services. KCI is currently under contract with a state department

Environmental Business Journal, Volume XXXI Number 9/10

15 Strategic Information for a Changing Industry

KCI Acquires LandAir Surveying

In August 2017 KCI acquired Lan-dAir Surveying (LAS), a Georgia-based consulting firm that is a recognized leader in utilization of advanced tech-nology. LandAir offers a complete range of surveying services, with a unique spe-cialization in terrestrial laser scanning and transportation surveying.

LandAir’s staff of 27 now offers an array of geospatial services, including aerial mapping, helicopter and fixed wing LiDAR (Light Detection and Ranging), terrestrial laser scanning, drone data capture, aerial photography, building information modeling (BIM) and virtual construction services.

With regards to the acquisition, LAS was already well-established in the mar-ketplace, was well-equipped, and already employed many highly-trained surveyors and technicians. Their team had already completed the R&D on the technologies, such as analyzing different software and equipment, and confirmed both their ef-fectiveness and profitability. As a firm with an established reputation in the field, LAS offered KCI a foundation with which to expand this segment of our business.

EBJ: Have you performed other recent technology investments that have had or will have a great impact in the com-pany?

KCI: Several years ago, participants in KCI’s Emerging Leaders Program pro-posed creation of an Innovation Incubator (i2) that would be used to fund develop-ment of innovation and technologies with-in the firm. This annual competition en-courages employees of all levels to submit ideas for funding. This ‘Shark Tank’ type program has given technological champi-ons the ability to advance their passions and ideas in several key areas, including machine learning, building information management systems, etc.

Our Director of Innovation and Tech-nology, Tom Sprehe, oversees the i2 proj-ects and ensures that a business case is fulfilled during their development. Some of the projects involve improvements to

EBJ: Why do you consider that the transaction was performed at the right time? How does it fit in your overall growth strategy?

KCI: The timing fit into our strategic plan for geographic expansion. In addi-tion, embracing new technology is critical to increasing both our technical expertise and our ability to efficiently deliver higher quality projects to our clients.

EBJ: Change and integration is always challenging. Can you describe the ap-proach that you took while integrating LAS?

KCI: We had begun to utilize laser scanning and drones in-house before LAS joined the firm. Immediately following the acquisition, we began to integrate the tech-nology throughout the company, which is an on-going evolutionary process. For instance, recently, we created a company-wide ‘Drone Community’, led by LandAir staff, to standardize procedures and share knowledge and drone resources across all technical practices.

As part of our integration plan, manag-ers had to address several challenges:

• proper use and operation of un-manned aerial vehicles (UAVs), includ-ing training and licensing drone pilots

• standardizing the use of 3-D models and associated software

• managing large datasets.Each involved a learning process that

was then improved as we scaled the tech-nology up to the corporate level.

EBJ: You have in-house personnel de-voted to technology related R&D, cor-rect? Why did it make sense to acquire LAS instead of generating your own technologies?

KCI: KCI utilizes both organic growth and acquisition strategies to improve and add new technologies. In 2017, KCI es-tablished a formal innovation and technol-ogy program to adopt and develop new technologies for future business develop-ment. As part of this process, we created a new position – Director of Innovation and Technology – to lead R&D efforts and monetize successful initiatives.

of transportation to survey intersections for the documentation and improvement of Americans with Disabilities Act (ADA) compliance. By using laser scanning, we were able to reduce required manpower, deliver the work three times as fast as con-ventional methods, and provide more de-tailed information – a point cloud of each location. This improvement in service led the client to assign the firm another two years of work.

EBJ: Has the acquisition had an impact in KCI’s overall profits?

KCI: Yes. The acquisition of LandAir and implementing their technological approaches has directly lead to increased profitability in our Southeast and South Atlantic Region Survey Practices, which doubled their budget during the 2018 calendar year. Demonstrating how these technologies enhance our current work has also led directly to additional backlog with existing clients.

EBJ: What was the main reason for this acquisition? What opportunities did KCI see prior to the acquisition? How have you been able to complement the services that you provide with these new technologies?

KCI: LandAir was a nationally recog-nized industry leader in the use of mobile and terrestrial laser scanners for detailed data collection and development of exist-ing condition models (BIM), and they had pioneered application of drone technology for safe, efficient and accurate acquisition of aerial photogrammetry. KCI has been working to embrace laser scanning and 3-D modeling organically for several years prior to the acquisition; however, deployment of aerial drones for photography was rela-tively new for the firm. The LandAir team has helped KCI educate our project leaders on the benefits of these new technologies, introduce them to our diverse client base, and incorporate them into virtually every aspect of our business. From the design of structures such as bridges and buildings to inspecting utilities to performing natural resource assessments, the technologies that we’ve acquired have improved our service offerings and will continue to do so as we expand their use throughout KCI.

Environmental Business Journal, Volume XXXI Number 9/10

16 Strategic Information for a Changing Industry

internal processes, such as project tracking databases, and others involve adaptation of new technologies to our profession. Ex-amples include development and applica-tion of artificial intelligence and machine learning to utility surveys, and evaluation of new geophysical technologies to detect and map subsurface utilities and other underground anomalies. Development of new technology often includes creating or adapting software applications to facilitate data handling and analysis.

Outside of the i2 program, KCI con-tinues to adapt to and welcome new tech-nologies and methodologies that allow our team to better serve our clients. These instances can be need-driven, accelerating the research, development and application timeline in order to deliver a required so-lution. Recently, KCI engineers incorpo-rated mixed or augmented reality, using a Microsoft Hololens, to develop 3-D BIM models for a utility substation. Conversely, our construction management team iden-tified the need for a mobile e-construction suite and worked with our geospatial solu-tions and application development staff to create a mobile field services application, a cloud-based solution to improve construc-tion management and inspection work-flows and documentation.

EBJ: What are other key technology solutions that KCI provides?

KCI: In addition to those technolo-gies mentioned previously (laser scanning, BIM, drones, machine learning, e-con-struction, and mixed reality), the multi-discipline KCI team offers our clients an array of technology-based services; includ-ing geographic information systems; geo-spatial solutions; mobile, desktop and web application development; and asset man-agement, which are delivered through-out our various geographies and markets. Modeling, engineering and construction of natural resources, process engineering of water and wastewater treatment systems, design of sustainable buildings and elec-tric vehicle infrastructure are other great examples of our technical service offerings.

EBJ: How does KCI differentiate from competitors from the technology stand-point?

KCI: We have always been a leader and early adopter in the creative implementa-tion of technology, and we invest in our employees’ development of skills necessary to implement new technologies. Often, the greatest opportunities exist in combin-ing technologies such as aerial drones and LiDAR. We look to connect the dots in order to offer more value to our clients and better meet their needs.

EBJ: Will you consider acquiring addi-tional technology related companies?

KCI: Absolutely! As technology ad-vances across the spectrum of our services, we are always investigating growth oppor-tunities that complement our existing lines of business, or offer new areas of expan-sion. We continue to invest in preparation to support autonomous transportation and the expansion of electric vehicles, so that we will be ready to provide the ser-vices needed into the future. Infrastructure resiliency as a remediation strategy for cli-mate change is another area of focus, and we are actively seeking out both technolo-gies and firms that can help us meet those needs.

EBJ: How is technology shaping our industry? What trends have you noticed in the following areas:

1) SOFTWARESoftware applications have become

standard tools in the toolbox, and we are actively partnering with software develop-ers, as well as developing in-house solu-tions that create internal efficiencies and support client requirements. Big data will continue to drive the need for cloud-based information management, as well as ap-plications to facilitate processing large amounts of data efficiently.

2) DRONESThough unmanned aerial vehicles

(UAVs) are becoming the standard in our industry for both LiDAR and documen-tation, other unmanned remote sensing technologies, such as hyper-spectral and thermal imagery are being added to the payload to enhance the use of the plat-form. Aquatic and underwater drones are becoming increasingly used in water qual-ity monitoring, security applications and

condition inspection.