U.S. Bank 401(k) Savings Plan Summary Plan Description · PDF fileU.S. Bank 401(k) Savings...

61

U.S. Bank 401(k) Savings Plan Summary Plan Description January 2012 This document constitutes part of a prospectus covering securities that have been registered under the Securities Act of 1933. HR1201W (8/2012)

Transcript of U.S. Bank 401(k) Savings Plan Summary Plan Description · PDF fileU.S. Bank 401(k) Savings...

U.S. Bank 401(k) Savings Plan Summary Plan Description

January 2012

This document constitutes part of a prospectus covering securities that have been registered under the Securities Act of 1933.

HR1201W (8/2012)

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

1

TABLE OF CONTENTS About This Summary ........................................................................................................................ 4 Overview............................................................................................................................................. 4

The U.S. Bank Retirement Program ............................................................................................................... 4 Your Responsibility ........................................................................................................................................ 4

Benefits at a Glance ........................................................................................................................... 5 Eligibility ........................................................................................................................................................ 5 Your Contributions ......................................................................................................................................... 5 Annual Contribution Increase ......................................................................................................................... 5 Matching Contributions .................................................................................................................................. 5 Age 50 Catch-Up Contributions ..................................................................................................................... 6 Tax Advantages .............................................................................................................................................. 6 Plan Investments ............................................................................................................................................. 6 Investment Risks ............................................................................................................................................ 7 Making Changes ............................................................................................................................................. 7 Rollovers ........................................................................................................................................................ 7 Vesting ........................................................................................................................................................... 7 Withdrawals While Employed........................................................................................................................ 7 Plan Loans ...................................................................................................................................................... 8 Payment of Account When You Leave, Retire, Become Disabled or Die ..................................................... 8

Deadlines and Effective Dates .......................................................................................................... 9 Using the U.S. Bank Employee Service Center or the Internet to Access Your Account ......... 12

U.S. Bank Employee Service Center ............................................................................................................ 12 U.S. Bank Retirement Program Web Site .................................................................................................... 12

Eligibility to Participate .................................................................................................................. 12 Eligible Position ........................................................................................................................................... 12

Enrollment ....................................................................................................................................... 13 Making Contributions or Investment Election Changes ............................................................. 13 Your Contributions ......................................................................................................................... 14

Annual Contribution Increase ....................................................................................................................... 14 Legal Limits ................................................................................................................................................. 14 Advantages of Pre-Tax Saving ..................................................................................................................... 15 How the Plan Affects Your Pay ................................................................................................................... 16 Age 50 Catch-Up Contributions ................................................................................................................... 16 Rollover Contributions ................................................................................................................................. 17 Voluntary After-Tax Contributions .............................................................................................................. 18

Matching Contributions .................................................................................................................. 18 Match Eligibility ........................................................................................................................................... 18 Service .......................................................................................................................................................... 18 Former Employees who are Rehired ............................................................................................................ 19 Other Contributions ...................................................................................................................................... 19

Your Plan Investments .................................................................................................................... 21 Selection of Plan Investments....................................................................................................................... 22 Your Responsibility for Your Investments (Section 404(c) of ERISA) ....................................................... 22 Investment Restrictions ................................................................................................................................ 23 Risk of Loss .................................................................................................................................................. 25 Accumulation of Retirement Assets ............................................................................................................. 25 Plan Investment Options ............................................................................................................................... 26

Fixed Income Fund: .................................................................................................................................. 26 Bond Funds: ............................................................................................................................................. 26 Target Retirement Date Funds: ................................................................................................................. 27 Large Cap Equity Funds: .......................................................................................................................... 28 Small-Mid Equity Funds: ......................................................................................................................... 29 International Funds: .................................................................................................................................. 29

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

2

Piper Stock Fund: ..................................................................................................................................... 29 Company Stock Fund: .............................................................................................................................. 30

Investment Elections ....................................................................................................................... 32 Your Initial Election ..................................................................................................................................... 32 Changing Investment Elections for Future Contributions ............................................................................ 33 Changing Investment Elections for Your Current Account Balance ............................................................ 33

Notice of Your Rights Concerning Employer Securities ............................................................. 34 Personalized Account Information ................................................................................................ 35 Your Potential with the U.S. Bank 401(k) Savings Plan .............................................................. 36 Your Plan Accounts ......................................................................................................................... 36

401(k) Plans of Acquired Companies ........................................................................................................... 37 Withdrawals from the Plan While Actively Employed ................................................................ 37

20% Withholding for Withdrawal ................................................................................................................ 38 Additional Tax on Early Withdrawals .......................................................................................................... 38 Age 59½ Withdrawals .................................................................................................................................. 38 Rollover Account Withdrawals .................................................................................................................... 38 After-Tax Withdrawals ................................................................................................................................. 38 Non-Hardship Withdrawals .......................................................................................................................... 38 Hardship Withdrawals .................................................................................................................................. 39

Plan Loans ........................................................................................................................................ 40 When Loans Are Available .......................................................................................................................... 40 Application Fee ............................................................................................................................................ 41 Interest Rate and Deductions ........................................................................................................................ 41 Loan Repayments ......................................................................................................................................... 41 Outstanding Loan Balance and Default ........................................................................................................ 42 Loan Payoffs................................................................................................................................................. 42

Distributions From the Plan if You Are No Longer Employed By U.S. Bank ........................... 42 Form of Distribution ..................................................................................................................................... 42 When You Become Eligible for a Payout and When Payments Are Made .................................................. 43 If You Defer Payment .................................................................................................................................. 43 Tax Treatment of Distributions from Plan .................................................................................................... 44 Rollovers ...................................................................................................................................................... 44 Special Tax Rules for Rollovers of U.S. Bancorp Stock .............................................................................. 45 20% Withholding for Account Distributions ................................................................................................ 45 Additional 10% Tax on Early Payouts ......................................................................................................... 46 Making Your Decision ................................................................................................................................. 46

Distributions to Your Beneficiary If You Die ............................................................................... 46 Naming a Beneficiary ................................................................................................................................... 46

Claims Procedures ........................................................................................................................... 47 Benefits Administration Committee ............................................................................................................. 47 What Is a Claim? .......................................................................................................................................... 48 Steps in Filing a Claim ................................................................................................................................. 48 Administrative Processes and Safeguards .................................................................................................... 49 Time Periods................................................................................................................................................. 49 Limitations Period ........................................................................................................................................ 49 Exhaustion of Administrative Remedies ...................................................................................................... 49 Venue for Legal Action ................................................................................................................................ 49 Applicable Law for Legal Action ................................................................................................................. 49

Amendment and Termination of the Plan ..................................................................................... 50 Assignment and Alienation of Benefits .......................................................................................... 50 Qualified Domestic Relations Orders ............................................................................................ 50 Fees and Expenses ........................................................................................................................... 51

Plan Administration Fees ............................................................................................................................. 51 Asset Management Fees ............................................................................................................................... 51

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

3

Brokerage Fees ............................................................................................................................................. 51 Individual Fees ............................................................................................................................................. 51

Limitations on Transfers and Resales of U.S. Bancorp Common Stock and Piper Jaffray Common Stock ................................................................................................................................. 52 Tax Consequences of the Plan for U.S. Bank ................................................................................ 53 Securities and Registrations ........................................................................................................... 53 Voting of Shares and Tender Offers .............................................................................................. 53 Incorporation of Certain Documents by Reference ..................................................................... 54 Administrative Information ........................................................................................................... 55 Your Rights Under ERISA ............................................................................................................. 56

Receive Information About the Plan and Benefits ....................................................................................... 56 Prudent Actions by Plan Fiduciaries............................................................................................................. 56 Enforce Your Rights ..................................................................................................................................... 56 Assistance with Your Questions ................................................................................................................... 57

Appendix A: Investment Fund Performance ................................................................................ 58

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

4

About This Summary This summary and prospectus provide an overview that is intended to give participants in the U.S. Bank 401(k) Savings Plan (the “Plan”) and their beneficiaries a general idea of their benefits, rights and obligations under that Plan. It is, however, only a summary. It does not describe every feature, nor is it used to administer the Plan. The Plan’s official terms are in the Plan document entitled “U.S. Bank 401(k) Savings Plan (2002 Restatement),” along with the amendments to that document. The Plan administrator will only use the official Plan document to administer the Plan and resolve any disputes. If there is a discrepancy between this summary and the Plan document, the Plan document will control. Neither the receipt of this booklet nor the use of the term “you” indicates that you are eligible for a benefit under the Plan. Only those employees who satisfy the eligibility requirements and other criteria contained in the Plan are eligible for a benefit. Neither the receipt of this booklet nor the terms of the Plan creates a right for any employee to be retained in U.S. Bank’s employment. Please note that this summary uses a number of terms, such as “compensation” and “year” in the place of more formal terms (“Recognized Compensation” and “Plan Year”) defined in the Plan. We do this to make the summary easier to read. The Plan’s defined terms, however, not the summary’s terms, are used to administer the Plan. Also, U.S. Bancorp adopted and maintains the Plan for the benefit of its employees and employees of related business entities, as listed on Schedule I to the Plan document. However, for simplicity, in this summary, the term “U.S. Bank” is generally used when referring to the Plan sponsor or to your employer. This summary also constitutes part of the Plan prospectus required to be delivered to you under the Securities Act of 1933. Before enrolling in the Plan you should carefully read this summary and the other documents referenced by this summary, including the investment fund performance which is included as Appendix A to this summary. If you have questions after reading this summary, call the U.S. Bank Employee Service Center at 800-806-7009. If you have questions about the Plan or Plan administration, or need further information, please contact the Plan Administrator at the address and phone number listed under the Administrative Information section. Overview The U.S. Bank Retirement Program When you retire from U.S. Bank, the benefits from your company-sponsored retirement plans, along with social security, personal investments and savings, can help provide you with financial security during your retirement years. Your 401(k) Plan account can be an important part of your overall retirement plan. Please read the individual sections of this summary for more information. Your Responsibility To get the most from the Plan, you should:

• Carefully review the information about the Plan;

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

5

• Pay attention to deadlines. If you miss a deadline, your request will be delayed until the next processing cycle;

• Carefully review your account on a regular basis by logging on to the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank;

• Review your account after you change your investment elections to confirm that the changes have been implemented and that your investment allocation reflects how you want your assets invested;

• Keep your beneficiary designations updated; and • Contact the U.S. Bank Employee Service Center at 800-806-7009 if you have questions not

answered in this summary. Remember, you are responsible for selecting your investments and monitoring them to achieve your retirement goals. Benefits at a Glance The following highlights some of the most important features of the Plan. Be sure to read the entire summary carefully. Eligibility You are eligible to participate in the Plan on your hire date, so long as you are a regular, permanent, non-temporary employee working in an eligible position. Eligible employees are automatically enrolled with a 2% deferral into one of the Target Retirement Date Fund options based on your date of birth and an assumed retirement at age 65. Your first pre-tax contribution will generally begin with your second paycheck from U.S. Bank. You become eligible for U.S. Bank matching contributions on the first day of the month after you complete one year of service (12 consecutive months) in which you have worked 1,000 hours in an eligible position. Once you meet the initial eligibility requirements for the employer matching contribution, you will continue to be eligible in future years regardless of how many hours you work, assuming you contribute to the Plan and meet all other criteria. For more information on eligibility, see the “Eligibility to Participate” and “Match Eligibility” sections. Your Contributions You can contribute up to 75% of your eligible pay on a pre-tax basis to the Plan through regular payroll deductions. Federal law limits the total dollar amount you can contribute. This limit is periodically adjusted for changes in the cost of living as required by federal law. Certain other legal limits may further reduce your contributions. For more information on your contributions and legal limits, see the “Legal Limits” section. Annual Contribution Increase You have the option to elect to have your contribution rate automatically increased each year by electing an annual rate increase and a target contribution rate. For more information on Annual Contribution Increase, see the “Annual Contribution Increase” section. Matching Contributions Once you meet the eligibility requirements, U.S. Bank makes an annual matching contribution of $1 for every $1 you contributed during that year, up to 4% of your eligible pay. The matching

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

6

contribution is automatically invested in the U.S. Bancorp ESOP Stock Fund. After the matching contribution is made, you can change how it is invested. For more information on the match, see the “Matching Contributions” section. Age 50 Catch-Up Contributions You are eligible to make a catch-up contribution if you are age 50 or older during the calendar year and for that year you contribute the maximum dollar amount of elective contributions generally permitted under federal law. If you reach the maximum dollar amount for elective contributions, catch-up contributions are automatic and will begin at the same percent as your current elective contributions. Federal law limits the amount you can contribute as a catch-up contribution. For more information on catch-up contributions, see the “Age 50 Catch-Up Contributions” section. Tax Advantages Your contributions to the Plan are deducted before most income taxes are withheld, but they are subject to FICA tax (i.e., the tax for social security and Medicare). In most (but not all) states, your contributions, the U.S. Bank match, and your investment gains are not subject to federal taxation as long as they remain in the Plan. For information about the application of state tax laws, consult your tax advisor. For more information on federal tax advantages, see the “Advantages of Pre-Tax Saving” section. Plan Investments You may invest your Plan account in one or more of a wide variety of investment funds.

• Stable Value Fund • Bond Index Fund • Active Bond Fund • Target Retirement Date Income Fund • Target Retirement Date 2010 Fund • Target Retirement Date 2015 Fund • Target Retirement Date 2020 Fund • Target Retirement Date 2025 Fund • Target Retirement Date 2030 Fund • Target Retirement Date 2035 Fund • Target Retirement Date 2040 Fund • Target Retirement Date 2045 Fund • Target Retirement Date 2050 Fund • Target Retirement Date 2055 Fund • Target Retirement Date 2060 Fund • US Large Cap Equity Index Fund • Active US Large Cap Equity Fund • US Small-Mid Equity Index Fund • Active US Small-Mid Equity Fund • International Equity Index Fund • Active International Equity Fund • U.S. Bancorp ESOP Stock Fund

NOTE: The Piper Jaffray Stock Fund is an investment option in the Plan for any dollars already invested in this fund. No new dollars may be invested or transferred into the Piper Jaffray Stock Fund. Participants may only transfer out of this fund.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

7

For more information on plan investments, see the “Your Plan Investments” section. Investment Risks The investment funds involve various degrees of risk, and amounts invested in the Plan are not insured or guaranteed in any way. For more information on the risks of investing, see the “Your Plan Investments” section and in particular, the “Risk of Loss” section and the “Note the following about Plan investment funds” in the “Accumulation of Retirement Assets” section. Making Changes You can change the investment mix of your account balance on any day the New York Stock Exchange is open. Changes confirmed by 3 p.m., Central time, are normally effective the same day. An earlier cutoff time could apply in unusual circumstances or if the New York Stock Exchange closes early. You may elect to change or stop your contribution rate or change the investment of your future contributions at any time. Both of those types of changes will be effective for the next pay period if made by the cut-off time in your current pay period. Changes may be made by calling the U.S. Bank Employee Service Center at 800-806-7009 or accessing the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank. For more information on making investment and contribution rate changes, see the “Investment Elections” section. Rollovers Rollovers are generally accepted into the Plan. For more information on making rollover contributions, see the “Rollover Contributions” section. Vesting You are immediately 100% vested in your entire account balance, including matching contributions. Withdrawals While Employed Generally, five types of withdrawals from your Plan account are available while you are still employed by U.S. Bank: • withdrawal of after-tax accounts; • non-hardship withdrawal from certain accounts; • hardship withdrawal; • age 59½ withdrawal; or • withdrawal of rollover accounts. Most withdrawals have significant tax implications. Before requesting a withdrawal, carefully review the “Withdrawals from the Plan While Actively Employed” section. If you became an employee of U.S. Bank as a result of the acquisition or merger of your former employer, you may have the ability to make other withdrawals from your account. For more details about your withdrawal options, call the U.S. Bank Employee Service Center and request a “Payment Rights” from a service center representative or access the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

8

Plan Loans If you are an active employee, you may be able to borrow money from your account. Through payroll deduction, you repay the amount you borrow, plus interest, to your own account. For more information on Plan loans, see the “Plan Loans” section. Payment of Account When You Leave, Retire, Become Disabled or Die You can receive a distribution of your entire account if you: • retire; • become totally and permanently disabled; • attain age 70½; or • leave U.S. Bank for any other reason. You may request a distribution of your entire account by calling the U.S. Bank Employee Service Center or accessing the U.S. Bank Retirement Program Web site. Requests received by phone or online by 3 p.m., Central time, each business day will generally be processed that same day. ACH is available if the distribution if made payable to you. If you request that your distribution be rolled over to another qualified plan or to an Individual Retirement Account (IRA), a check will be mailed two business days later. If you are requesting a stock distribution for that portion of your account held in the U.S. Bancorp ESOP Stock Fund or the Piper Jaffray Stock Fund, a statement will be sent approximately two weeks after your cash distribution is issued. For more information on distributions once you terminate employment, see the “Distributions From the Plan if You Are No Longer Employed by U.S. Bank” section. You pay taxes on the money when you receive it; however, special tax advantages may be available. For information on payouts and tax implications, see the “Tax Treatment of Distributions from the Plan” section. If you die, your beneficiary will receive the funds in your account. For more information on death benefits, see the “Distributions to Your Beneficiary If You Die” section.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

9

Deadlines and Effective Dates You can use this chart as a reference when enrolling in the Plan, changing contribution amounts, or requesting loans, withdrawals or distributions. All transactions may be initiated by calling the U.S. Bank Employee Service Center at 800-806-7009 or by accessing the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank. All requests must be received by the deadline shown. Requests received after the deadline will be processed with the next cycle. Request How To Initiate Deadline Approximate Date of

Change/Payment Opting out of automatic enrollment

Call the U.S. Bank Employee Service Center or access the Web site

Generally 5 business days after hire date

Effective as soon as administratively possible

Changing your contribution rate

Call the U.S. Bank Employee Service Center or access the Web site

Changes can be made at any time during the month

Effective as soon as administratively possible – usually within one to two pay periods after change

Changing investment mix for your current account balance

Call the U.S. Bank Employee Service Center or access the Web site

3 p.m., Central time, any business day*

Changes confirmed by 3 p.m., Central time, are effective the same business day using values as of the market close

Changing investment of your future contributions

Call the U.S. Bank Employee Service Center or access the Web site

Changes can be made at any time during the month

Effective with your next contribution

Dividend payout or reinvestment election

Call the U.S. Bank Employee Service Center or access the Web site

Typically two business days before the ex-dividend date**

Effective for that quarter’s dividend

Annual Contribution Increase

Call the U.S. Bank Employee Service Center or access the Web site

December 1 of each year

Effective on the January 15 pay of the next year

Age 50 catch-up contribution

Automatic if you reach the IRS annual contribution limit

N/A Commences when you reach the IRS annual contribution limit

* Earlier cutoffs will apply if the New York Stock Exchange is closed or closes earlier than 3 p.m., Central time. ** The ex-dividend date is generally two business days before the dividend record date. NOTE: The processing times indicated above are the times it will normally take to process the indicated transactions. These processing times are not guaranteed and are subject to change. Many events could delay the processing of particular requests, including holidays, unusual market events, unavailability of mutual fund data, improper instructions, systems failures, and unusual transaction volumes. While the Plan administrator will do its best to assure that transactions are processed according to this schedule, neither the Plan nor the Plan administrator is liable for failure to process by the times indicated.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

10

Request How to Initiate Deadline Approximate Date of Change/Payment

After-tax, age 59½ or rollover account withdrawal*

Call the U.S. Bank Employee Service Center or access the Web site – no form required

3 p.m., Central time, on any business day**

Processed daily; ACH available if withdrawal is made payable to you; if rollover, can only be made by check which is mailed two business days later

Non-hardship withdrawal*

Call the U.S. Bank Employee Service Center or access the Web site – no form required

3 p.m., Central time, on any business day**

Processed daily; ACH available if withdrawal is made payable to you; if rollover, can only be made by check which is mailed two business days later

Hardship withdrawal* Call the U.S. Bank Employee Service Center or access the Web site to request a form

3 p.m., Central time, on any business day**

Processed daily; ACH or check mailed two business days later, once required documentation is approved

General Loan* Call the U.S. Bank Employee Service Center or access the Web site

3 p.m., Central time, on any business day**

Processed daily; ACH or check mailed two business days later

Primary Residence Loan*

Call the U.S. Bank Employee Service Center or access the Web site to request a form

3pm, Central time, on any business day, once required documentation is approved**

Processed daily; ACH or check mailed two business days later, once required documentation is approved

* Most withdrawals have significant tax implications. Before requesting a withdrawal, please consult your tax advisor. ** Earlier cutoffs will apply if the New York Stock Exchange is closed or closes earlier than 3 p.m., Central time. NOTE: The processing times indicated above are the times it will normally take to process the indicated transactions. These processing times are not guaranteed and are subject to change. Many events could delay the processing of particular requests, including holidays, unusual market events, unavailability of mutual fund data, improper instructions, systems failures, and unusual transaction volumes. While the Plan administrator will do its best to assure that transactions are processed according to this schedule, neither the Plan nor the Plan administrator is liable for failure to process by the times indicated.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

11

Request How to Initiate Deadline Approximate Date of Change/Payment

Payment of account if you leave U.S. Bank*

Call the U.S. Bank Employee Service Center or access the Web site – no form required

3 p.m., Central time, on any business day**

Processed daily; ACH available if distribution is made payable to you; if rollover, can be made via direct deposit or by check, depending on IRA provider. If rollover is by check, payment can be sent directly to IRA provider or your home. If shares of U.S. Bancorp and/or Piper Jaffray common stock are requested, please allow two weeks to receive your statement from the stock transfer agent.

Account balance inquiry

Call the U.S. Bank Employee Service Center or access the Web site

N/A Account balance is valued daily at the end of each business day

* Most withdrawals have significant tax implications. Before requesting a withdrawal, please consult your tax advisor. ** Earlier cutoffs will apply if the New York Stock Exchange is closed or closes earlier than 3 p.m., Central time. NOTE: The processing times indicated above are the times it will normally take to process the indicated transactions. These processing times are not guaranteed and are subject to change. Many events could delay the processing of particular requests, including holidays, unusual market events, unavailability of mutual fund data, improper instructions, systems failures, and unusual transaction volumes. While the Plan administrator will do its best to assure that transactions are processed according to this schedule, neither the Plan nor the Plan administrator is liable for failure to process by the times indicated.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

12

Using the U.S. Bank Employee Service Center or the Internet to Access Your Account U.S. Bank Employee Service Center The U.S. Bank Employee Service Center is the U.S. Bank interactive voice response (IVR) system and customer service center. The U.S. Bank Employee Service Center IVR is generally available 24 hours a day, Monday through Saturday, and after 12 p.m., Central time, on Sunday, via touch-tone phone. Service center representatives can assist you from 8 a.m. to 8 p.m., Central time, Monday through Friday, excluding holidays. Call 800-806-7009, select the Retirement Benefits option, and follow the prompts to access your account or to speak with a service center representative. U.S. Bank Retirement Program Web Site You can access your account online by logging onto www.yourbenefitsresources.com/usbank. The site is secure and enables you to: • enroll in or make changes to your existing Plan account; • inquire about current benefits, including contribution elections, account balances, fund

investment returns, or loan and withdrawal availability; • view or print your statement; and • request transactions, including changes to your investment of current or future balances,

dividend payout elections, contribution elections, loans, withdrawals, or distributions. The Web site is generally available 24 hours a day, Monday through Saturday, and after 12 p.m., Central time, on Sunday. Eligibility to Participate You are eligible to participate in the Plan on your hire or rehire date with U.S. Bank (or one of its participating affiliates), so long as you are a regular, permanent, non-temporary employee working in an eligible position. Information about the U.S. Bank 401(k) Savings Plan is provided to new employees in their new employee orientation materials and in a 401(k) mailing shortly after their hire or rehire date. Special eligibility rules may apply to employees of acquired companies. Also, there are separate rules to determine when you are eligible to receive the employer matching contribution. These rules can be found in the “Matching Contributions” section. Eligible Position To be eligible, you must be classified by U.S. Bank as an employee on both payroll and personnel records and must not be in one of the following excluded classes of employees:

• employees of U.S. Bank affiliates that are not participating employers in the Plan; • employees employed outside the United States (unless the Benefits Administration

Committee specifically acts in writing to cover such employees); • employees employed in a division or facility that was not in existence on January 1, 2002,

that is, was acquired, established, founded or produced by the liquidation or similar discontinuation of a separate subsidiary (unless the Benefits Administration Committee specifically acts in writing to cover such employees);

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

13

• employees who become employees due to a merger or acquisition (unless the Benefits Administration Committee specifically acts in writing to cover such employees);

• employees who are accruing a benefit under any other tax-qualified defined contribution plan of U.S. Bank or its affiliates; and

• certain employees whose terms and conditions of employment are established by collective bargaining agreements (unless the applicable collective bargaining agreement expressly provides for their participation.

Persons who are not classified by U.S. Bank as an employee on both payroll and personnel records are not eligible to participate in the Plan. This means that leased employees, independent contractors, and similar persons are not eligible. U.S. Bank’s classification of a person is conclusive for the purpose of the foregoing rules. No reclassification shall result in a person being retroactively eligible for benefits under the Plan. Any uncertainty concerning a person’s classification shall be resolved by excluding the person from being eligible. Enrollment If eligible, you will be automatically enrolled with a 2% deferral into one of the Target Retirement Date Fund options based on your date of birth and an assumed retirement at age 65. Each fund is managed to the specific retirement date included in its name (that is, the Target Retirement Date Income Fund, 2010, 2015, 2020, 2025, 2030, 2035, 2040, 2045, 2050, 2055 and 2060 Fund). You may opt out of contributing to the Plan or you may choose a different deferral rate or investment options at any time by: • Logging onto www.yourbenefitsresources.com/usbank; or • Calling the U.S. Bank Employee Service Center at 800-806-7009 and selecting the 401(k)

option. Service center representatives are available to assist you from 8 a.m. to 8 p.m., Central time, Monday through Friday, except holidays.

For more information, see the “Investment Elections” section. Note: If you do not wish to make contributions to the 401(k) Plan, you need to complete the steps above within five business days after your hire date. If you miss the deadline, you can still make changes or suspend contributions at any time, but any contributions already made must remain in the Plan. If you do change or suspend your contributions, the changes will take place as soon as administratively possible, generally within one or two pay periods. If you decide to enroll at a different deferral rate, you must choose a pre-tax contribution percentage (a percentage of pay before federal and state taxes are deducted) from 1% to 75% (in 1% increments). In addition to deciding how much to contribute, you must also decide how to invest your contributions. You can choose among a wide variety of investment funds. See the “Your Plan Investments” section. Making Contributions or Investment Election Changes You can adjust the investments of your Plan account throughout the year. See the “Deadlines and Effective Dates” section for applicable transaction deadlines. Earlier cutoffs will apply in unusual circumstances or if the New York Stock Exchange closes earlier than 3 p.m., Central time.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

14

The processing times indicated in this summary are the times it will normally take to process the indicated transactions. These processing times are not guaranteed and are subject to change. Many events could delay the processing of particular requests including unusual market events, unavailability of mutual fund data, improper instructions, systems failures, and unusual transaction volumes. While the Plan administrator will do its best to be sure that transactions are processed according to this schedule, neither the Plan nor the Plan administrator is liable for failure to process by the times indicated. If you make more than one change of the same nature before the deadline, only your last change before the deadline will become effective. For example, if you change your contribution percentage to 3% on March 18, and then make another change to 4% on March 23, the change to 4% will take effect on April 1. Call the U.S. Bank Employee Service Center or access the U.S. Bank Retirement Program Web site to make changes to your Plan account. Your Contributions Each pay period, you can contribute up to 75% of your “401(k) Savings Plan Compensation.” This contribution level is subject to the maximum dollar limit set by federal law. Your 401(k) Savings Plan Compensation equals your wages for federal income tax withholding purposes plus any pre-tax contributions you make to the Plan, to a cafeteria plan for medical and other welfare benefits, and to medical and dependent care spending accounts. Your 401(k) Savings Plan Compensation does not include any merchandise, the value of stock awards, severance payments, expense allowances, payments of deferred compensation, retention bonuses, long term cash incentive awards, long-term disability pay, insurance or health assessment awards, or any other welfare or fringe benefit. For simplicity, this summary sometimes uses the word “pay” to refer to your 401(k) Savings Plan Compensation. Any pay received more than thirty days after your termination of employment is not considered 401(k) Savings Plan Compensation. Annual Contribution Increase You have the option to have your contribution rate increased each year by electing an annual rate increase and a target contribution rate. For example, you are currently contributing 2% of your eligible pay but would like to gradually increase that to 10%. Through this feature, you may elect an annual rate increase of 2% each year for the next four years until you reach your goal of 10%. Contribution increases must be elected by December 1 in order for your annual increase percentage to occur on your paycheck for January 15 of the following year. To elect the annual increase feature, log onto the U.S. Bank Retirement Program Web site or call the U.S. Bank Employee Service Center. Legal Limits Federal law limits the amount of money you can contribute on a pre-tax basis to all tax-deferred savings plans during a year, including the Plan and the plans of other employers. This annual limit is known as the “402(g) limit” because of the section of the Internal Revenue Code that describes the limitation. For 2012, this limit is $17,000. After 2012, the limit may be periodically adjusted for changes in the cost of living as required by federal law.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

15

It is your responsibility to monitor the 402(g) limit if you contributed to another 401(k) plan through a former employer during the calendar year. If you do exceed the 402(g) limit for the Plan year, you must contact the U.S. Bank Employee Service Center at 800-806-7009 prior to March 31 of the following Plan year to receive a refund. You should consult your tax advisor if you have any questions. Once your pre-tax contributions reach the 402(g) limit, payroll deductions will automatically stop, unless you are eligible to make age 50 catch-up contributions. For more information see the “Age 50 Catch-Up Contributions” section. Federal law also limits the amount of pay that can be taken into account in determining your matching contributions. For 2012, the compensation limit is $250,000. This limit is also subject to adjustment for changes in the cost of living. A small number of employees may be affected by an annual limit on the total amount that can be added to their Plan accounts. You will be notified if your contribution must be reduced or refunded. Finally, the pre-tax contributions and matching contributions of some highly compensated employees may have to be reduced to satisfy rules establishing a maximum difference between the average contributions of highly compensated employees and the average contributions of other employees. For this purpose, highly compensated employees are generally employees whose pay in the prior year exceeded a threshold amount. For 2012, the prior year (2011) pay threshold is $110,000. The threshold amount is adjusted periodically for increases in the cost of living as required by federal law. Advantages of Pre-Tax Saving An important feature of the Plan is that it allows you to make your contributions with pre-tax dollars. This means that you do not pay current federal – and in most cases, state – income taxes on the money you contribute, or on the earnings on your contributions. Your contributions are, however, subject to social security (FICA) taxes. Because you contribute on a pre-tax basis, saving for the future actually helps you reduce your current taxes. Of course, you will have to pay taxes when you take your money out of the Plan (or, if you roll the money to an IRA, when you take it out of the IRA). At that time, you may qualify for more favorable tax treatment, but that is not always the case. We encourage you to discuss your individual circumstances with your personal tax advisor to determine the likely tax effects to you of participation in the Plan.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

16

Example This example illustrates the near-term advantages of pre-tax savings. The employee in this example is married, and files a joint income tax return. State income taxes are not included in this example. With a Conventional Savings

Account With the 401(k) Savings Account

Employee earns $25,000 $25,000 Employee’s pre-tax savings - 0 - 1,500 Taxable pay $25,000 $23,500 Assumed federal tax (10%) - 2,500 - 2,350 Social security tax (7.65%) - 1,913 - 1,913 After-tax savings - 1,500 0 Employee’s net take-home pay $19,087 $19,237 By saving $1,500 in the Plan rather than in a conventional savings account, this employee gets an immediate tax break that results in a $150 increase in take-home pay for the year. That means the employee contributes $1,500 a year, but — because of the tax savings advantage of the Plan — has a net cost of only $1,350 ($1,500 – $150 = $1,350). The higher the tax bracket, the greater the savings. Employees who pay no income tax will have no tax savings. How the Plan Affects Your Pay The percentage of pay you choose to contribute to the Plan is deducted each pay period. Therefore, the dollar amount of your contributions will automatically increase if your salary increases or decrease if your salary decreases. The dollar amount may also change on account of overtime, commissions, bonus pay (other than retention bonuses), awards and incentive pay (other than long-term cash incentive awards). If you are expecting a change in your pay and want to change the percentage of your contribution, be sure to refer to the “Deadlines and Effective Dates” chart. Example You have annual 401(k) Savings Plan Compensation of $24,000 and elect to contribute 4% to the Plan. From your semi-monthly 401(k) Savings Plan Compensation of $1,000 ($24,000 divided by 24 pay periods), $40 is deducted for your Plan account ($1,000 multiplied by .04). If you receive a $500 bonus during any pay period and the full bonus amount is determined to be 401(k) Savings Plan Compensation, a total of $60 will be deducted from your compensation for that pay period: $1,000 + $500 = $1,500; $1,500 x .04 = $60. Age 50 Catch-Up Contributions In the year you attain age 50 and in each subsequent year, you may be eligible to make a “catch-up” contribution. A catch-up contribution is a contribution greater than the 402(g) limit. To be eligible to make a catch-up contribution, you must be at least age 50 by the end of the year for which the contribution is being made, and you must have contributed the maximum amount of elective contributions permitted under the 402(g) limit. Federal law limits catch-up contributions to $5,500 in 2012. This limit is subject to adjustment for changes in the cost of living.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

17

You do not have to make an election to make a catch-up contribution if you will reach the 402(g) limit. The Plan provides that when a qualifying participant reaches the 402(g) limit, catch-up contributions will begin at the same percent as the participant’s current elective contributions. To get the maximum catch-up contribution, a participant only needs to make sure that he or she contributes at a high enough percentage to contribute both the maximum amount of elective contributions and the maximum catch-up contribution. Example Suppose in 2012 you are over age 50, have 401(k) Savings Plan Compensation of $60,000, and elect to contribute 40% of your pay. The 402(g) limit for 2012 is $17,000 and the elective contributions you make will reach this amount in September. After you reach the 402(g) limit, deductions will continue to be taken out of your pay at the 40% rate through mid-December when your contributions total $22,500, including regular contributions of $17,000 and catch-up contributions of $5,500. If you are eligible but do not want to make a catch-up contribution, you will need to do one of the following: • reduce the percent of pay that you contribute for your elective contribution so that you do not

reach the 402(g) limit; or • reduce the percent of pay that you contribute to the Plan to zero once you reach the 402(g)

limit. Remember, unless you are contributing the maximum amount of elective contributions permitted under federal law (the 402(g) limit), you are not eligible to make a catch-up contribution. Rollover Contributions Under special rules, you can deposit (“roll over”) the taxable portion of your distribution from certain other retirement savings programs into the Plan. You may not roll over any after-tax contributions or Roth 401(k) contributions into the Plan. Such other programs include other tax-qualified pension, savings or profit-sharing plans, certain plans maintained by tax-exempt employers, and certain plans maintained by state and local governments. If you are actively employed by U.S. Bank, you can make a rollover contribution in two ways: • make a direct rollover (by check payable to the U.S. Bank 401(k) Savings Plan); or • receive a payout (by check payable to you) and deposit any of the taxable portion into the Plan

(by check payable to the U.S. Bank 401(k) Savings Plan) within 60 days after you receive it. Any money you roll over to the Plan will be credited to a special rollover source in your account. You can postpone paying income taxes on your rollover contributions and their earnings as long as they stay in this or another qualified plan or IRA. If you want to make a rollover contribution to the Plan, the Plan administrator will review your request to make sure your rollover deposit would not be a risk to the Plan’s tax-qualified status. The amount of money you roll over into the Plan is not eligible for the U.S. Bank matching contribution. To roll over qualified savings into the Plan, call the U.S. Bank Employee Service Center or access the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank to request the appropriate form. You should contact the Service Center prior to requesting a distribution from your prior employer's plan.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

18

Voluntary After-Tax Contributions You may not make voluntary after-tax contributions to the Plan, but your account may contain such funds if you made after-tax contributions to a predecessor plan. The Plan administrator will account for any such funds separately, since you have already paid tax on them. For information on taking distributions of after-tax funds, see the “After-Tax Withdrawals” section. Matching Contributions To help your savings grow, U.S. Bank will match your contributions $1 for each $1 you contribute, up to 4% of your eligible pay. This means you could have a matching contribution of up to 4% of your eligible pay added to your Plan account. This contribution is added to your account annually on a tax-deferred basis and is automatically invested in the U.S. Bancorp ESOP Stock Fund. After the matching contribution is made, you can change how it is invested at any time. Rollover contributions are not eligible for the match. The annual matching contribution is based on the actual total dollar amount you contribute during the year as a percentage of your total eligible 401(k) Savings Plan Compensation for the year. Matching contributions are contributed to your account after the end of the Plan year in which your contributions are made. For example, your match based on your 2012 contributions and pay will be deposited to your account in January 2013. Match Eligibility You will be eligible for employer matching contributions on the first day of the month after you have completed one full year of service in which you are credited with working at least 1,000 hours. Matching contributions will be credited on eligible 401(k) contributions made on and after the first day of the month following completion of this one-year service requirement. This means that if you contribute the IRS annual maximum amount allowed ($17,000 in 2012) before you become eligible for matching contributions, you will not receive any matching contributions for that year. Therefore, you should carefully consider the amount and timing of your 401(k) contributions during the first 12 months of your participation. Once you meet the initial eligibility requirements for the employer matching contribution, you will continue to be eligible in future years regardless of the number of hours you work, assuming you contribute to the Plan and meet all other eligibility criteria. Compensation received prior to the date you became eligible for employer matching contributions is not included in eligible pay for determining your matching contribution. Service You complete one year of service after twelve months of employment with U.S. Bank as long as you have earned 1,000 hours of service during that period. If you earn fewer than 1,000 hours of service during that period, you will complete the one year service requirement at the end of any subsequent calendar year in which you earn at least 1,000 hours of service. You earn an hour of service for each hour U.S. Bank pays you to work. You also earn hours of service when you are on certain paid or unpaid authorized leaves of absence, as follows: • For paid leaves, such as vacation, holiday, illness (sick time), jury duty, and short-term

disability, you earn an hour of service for each hour you normally would have been scheduled to work.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

19

• For an unpaid military leave from which you return to work within the time limits required by law, you earn one hour of service for each hour you normally would have been scheduled to work.

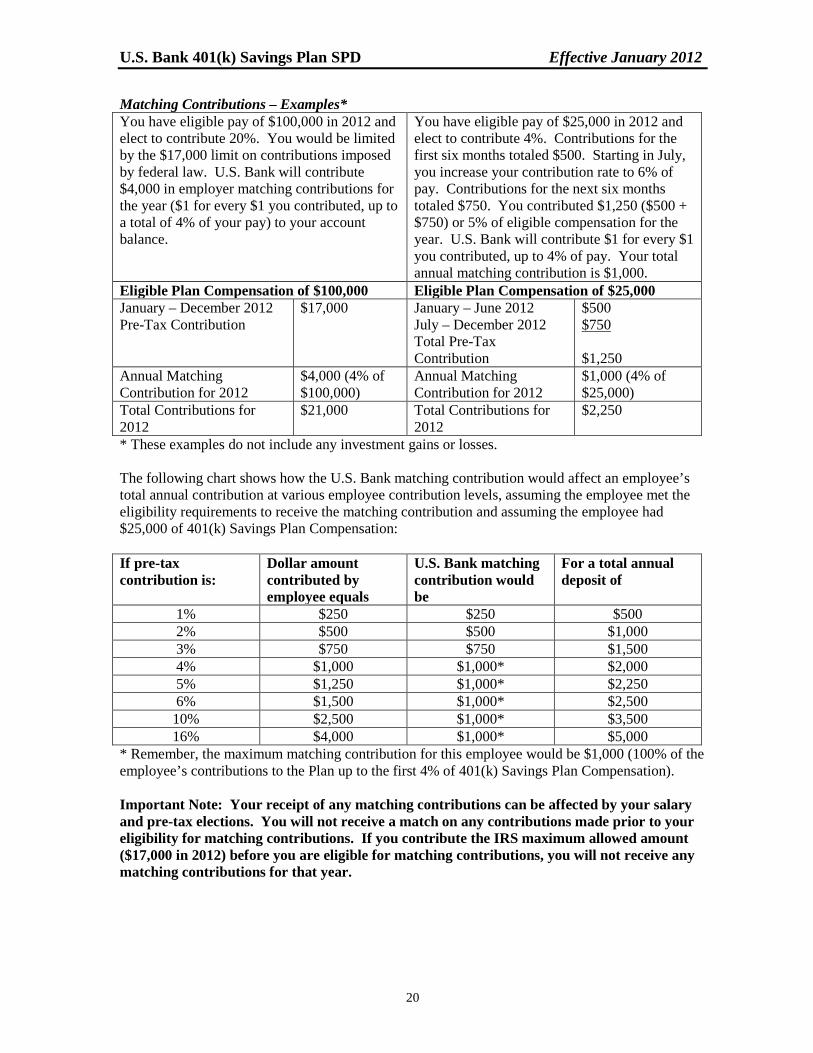

Former Employees who are Rehired If you are a rehired employee and you met the initial employer matching contribution eligibility requirements during your prior employment with U.S. Bank, you will be immediately eligible for the employer matching contribution assuming you contribute to the Plan and meet all other eligibility criteria. If you were not eligible to receive employer matching contributions during your prior employment with U.S. Bank and are later reemployed, then you must satisfy the eligibility requirements. These rules can be found in the “Match Eligibility” section. Other Contributions In addition to the U.S. Bank matching contributions in this section, the Plan allows U.S. Bank to make discretionary matching contributions. Any such contributions would be allocated in proportion to each participant’s pre-tax contributions. Matching Contributions – Examples*

* These examples do not include any investment gains or losses.

You were hired on August 15, 2011 and have 401(k) Savings Plan Compensation of $25,000. You became eligible to contribute on your hire date. You elected to contribute 4% of pay starting with your September 15, 2011 pay. You did not receive a match for 2011 because you were not eligible for matching contributions until September 1, 2012. At the end of 2012, U.S. Bank will contribute $333 for the year - $1 for every $1 you contributed, up to a total of 4% of your eligible pay (that is, pay earned from September 1, 2012 through December 31, 2012) to your account balance.

You were hired on March 1, 2000 and have been actively participating in the Plan since you were first eligible. In 2012, you have 401(k) Savings Plan Compensation of $25,000 and elect to contribute 4% of pay to the Plan. U.S. Bank will contribute $1,000 for the year ($1 for every $1 you contributed, up to a total of 4% of your pay) to your account balance.

Eligible Plan Compensation of $25,000 Eligible Plan Compensation of $25,000 September – December 2011 Pre-Tax Contribution

$333 January – December 2012 Pre-Tax Contribution

$1,000

Annual Matching Contribution for 2011

$0 Annual Matching Contribution for 2012

$1,000 (4% of $25,000)

Total Contributions for 2011 $333 Total Contributions for 2012

$2,000

January - December 2012 Pre-Tax Contribution

$1,000

Annual Matching Contribution for September – December 2012

$333 (4% of $8,333)

Total Contributions for 2012 $1,333

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

20

Matching Contributions – Examples* You have eligible pay of $100,000 in 2012 and elect to contribute 20%. You would be limited by the $17,000 limit on contributions imposed by federal law. U.S. Bank will contribute $4,000 in employer matching contributions for the year ($1 for every $1 you contributed, up to a total of 4% of your pay) to your account balance.

You have eligible pay of $25,000 in 2012 and elect to contribute 4%. Contributions for the first six months totaled $500. Starting in July, you increase your contribution rate to 6% of pay. Contributions for the next six months totaled $750. You contributed $1,250 ($500 + $750) or 5% of eligible compensation for the year. U.S. Bank will contribute $1 for every $1 you contributed, up to 4% of pay. Your total annual matching contribution is $1,000.

Eligible Plan Compensation of $100,000 Eligible Plan Compensation of $25,000 January – December 2012 Pre-Tax Contribution

$17,000 January – June 2012 July – December 2012 Total Pre-Tax Contribution

$500 $750 $1,250

Annual Matching Contribution for 2012

$4,000 (4% of $100,000)

Annual Matching Contribution for 2012

$1,000 (4% of $25,000)

Total Contributions for 2012

$21,000 Total Contributions for 2012

$2,250

* These examples do not include any investment gains or losses. The following chart shows how the U.S. Bank matching contribution would affect an employee’s total annual contribution at various employee contribution levels, assuming the employee met the eligibility requirements to receive the matching contribution and assuming the employee had $25,000 of 401(k) Savings Plan Compensation: If pre-tax contribution is:

Dollar amount contributed by employee equals

U.S. Bank matching contribution would be

For a total annual deposit of

1% $250 $250 $500 2% $500 $500 $1,000 3% $750 $750 $1,500 4% $1,000 $1,000* $2,000 5% $1,250 $1,000* $2,250 6% $1,500 $1,000* $2,500 10% $2,500 $1,000* $3,500 16% $4,000 $1,000* $5,000

* Remember, the maximum matching contribution for this employee would be $1,000 (100% of the employee’s contributions to the Plan up to the first 4% of 401(k) Savings Plan Compensation). Important Note: Your receipt of any matching contributions can be affected by your salary and pre-tax elections. You will not receive a match on any contributions made prior to your eligibility for matching contributions. If you contribute the IRS maximum allowed amount ($17,000 in 2012) before you are eligible for matching contributions, you will not receive any matching contributions for that year.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

21

Your Plan Investments The Plan offers you a choice of a wide variety of investment funds. The funds are a mix of passively managed index funds, actively managed funds and target retirement date funds. The Plan also offers a Stable Value Fund which is a fixed income fund that invests in a diversified portfolio of investment contracts selected from high quality insurance companies and institutions, and other eligible stable value investments. An additional investment is the U.S. Bancorp ESOP Stock Fund which invests primarily in U.S. Bancorp common stock. For your long-term retirement security, you should give careful consideration to the importance of a well-balanced and diversified investment portfolio, taking into account all your assets, income and investments. You are responsible for the investment of your account. You can make investment elections from time to time for both the assets currently in your accounts and for your future contributions to the Plan. Therefore, it is important that you review information about the investments. Fund fact sheets and prospectuses are available by logging onto www.yourbenefitsresources.com/usbank or by calling the U.S. Bank Employee Service Center. Please note, not all funds have prospectuses. The following pages provide information on the investments. Fixed Income Fund:

• Stable Value Fund Bond Funds:

• Bond Index Fund • Active Bond Fund

Target Retirement Date Funds:

• Target Retirement Income Fund • Target Retirement Date 2010 Fund • Target Retirement Date 2015 Fund • Target Retirement Date 2020 Fund • Target Retirement Date 2025 Fund • Target Retirement Date 2030 Fund • Target Retirement Date 2035 Fund • Target Retirement Date 2040 Fund • Target Retirement Date 2045 Fund • Target Retirement Date 2050 Fund • Target Retirement Date 2055 Fund • Target Retirement Date 2060 Fund

Large Cap Equity Funds:

• US Large Cap Equity Index Fund • Active US Large Cap Equity Fund

Small-Mid Cap Equity Funds:

• US Small-Mid Equity Index Fund • Active US Small-Mid Equity Fund

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

22

International Equity Funds: • International Equity Index Fund • Active International Equity Fund

Company Stock Fund:

• U.S. Bancorp ESOP Stock Fund (USB) NOTE: The Piper Jaffray Stock Fund (PJC) remains an investment option in the Plan for any dollars already invested in this fund. No new dollars may be invested or transferred into the Piper Jaffray Stock Fund. Participants may only transfer out of this fund. Each fund has a different earning potential and level of risk. It is up to you to choose the combination of earnings potential and investment risk that best matches your needs and investment tolerance. See the “Plan Investment Options” section for a brief description of the funds and their investment risks. Appendix A to this summary shows the performance results for each of the investment funds. Some Plan expenses are paid by U.S. Bank, and some are paid by the Plan. Expenses paid by the Plan reduce fund investment returns. As a result, rates of return on investments in the Plan will not exactly match the rates of return on investments made outside of the Plan. Keep in mind, however, that investments in the Plan are tax-deferred, unlike many investments outside the Plan. For further information on Plan expenses, see the “Fees and Expenses” section. Selection of Plan Investments The Compensation Committee (appointed by the Board of Directors of U.S. Bancorp) has the responsibility for selecting the investment funds offered under the Plan. The Compensation Committee from time to time may revise the investment funds offered under the Plan by adding or deleting funds that are available for investment. The Compensation Committee may also delegate its authority to select investments. Your Responsibility for Your Investments (Section 404(c) of ERISA) The Plan is intended to constitute a plan as described in Section 404(c) of the Employee Retirement Income Security Act of 1975 (ERISA) and Title 29 of the Code of Federal Regulations Section 2550.404c-1. Since you will be choosing how to invest your account, you will be responsible for any investment losses resulting from your investment elections. The fiduciaries of the Plan and U.S. Bank and its affiliates will not be liable for these losses. Information regarding Plan investments is available in each fund’s fact sheet and the prospectuses for the mutual funds. You may review the fund fact sheet or prospectus for an investment fund, or request a copy, by contacting the U.S. Bank Employee Service Center at 800-806-7009 or logging on to the U.S. Bank Retirement Program Web site at www.yourbenefitsresources.com/usbank. Please note, not all funds have a prospectus. In addition, upon request to the U.S. Bank Employee Service Center, the following additional information will be provided to you or your beneficiary about the investments: • a description of the annual operating expenses of each investment (e.g., investment

management fees, administrative fees, transaction costs) which reduce your rate of return; • copies of any prospectuses, financial statements and reports, and of any other materials relating

to the investments to the extent such information is provided to the Plan; • a list of the assets comprising each investment;

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

23

• information concerning the current value of the investments, as well as their past and current investment performance; and

• information concerning the value of the mutual fund or common stock shares or units held in your account.

Investment Restrictions Under the Plan, the Benefits Administration Committee (the “Committee”) may adopt any rule that (i) is not in conflict with the Plan, (ii) is necessary for administering the Plan, or (iii) is required in order to carry out the provisions of the Plan. Under this authority, the Committee may impose such investment and trading restrictions as it deems appropriate to achieve the goals of the Plan. In addition, to the extent a fund imposes a trading restriction on investors in the fund that temporarily restricts your ability to direct or diversify the assets in your account, to obtain a loan, or to obtain a distribution, such a trading restriction is an integral part of and is incorporated into the Plan. Moreover, a fund or the Plan may impose a fee on certain trading, such as moving quickly into and out of a fund. You should review the prospectus or fund fact sheets for each fund to determine if the fund (i) imposes any trading restrictions on your ability to move into or out of the fund, or (ii) imposes any fees on certain trades. U.S. Bank’s policy is that the 401(k) Savings Plan not be used as a vehicle for excessive short-term trading of funds, including short-term trading done to take advantage of either stale pricing or pricing anomalies in the net asset value of the investment funds available in the Plan. In order to minimize the negative effects of short-term trading, the Plan has implemented restrictions on trade activities for the investment funds in the Plan. Purchase Block The funds within the U.S. Bank 401(k) Savings Plan are subject to purchase blocks. Participants who transfer or reallocate any amount from any of the investment funds in the Plan, will be blocked for 30 or 60 calendar days, depending on the fund, before they can reallocate or transfer any amount back into that fund. The following U.S. Bank 401(k) Savings Plan funds are subject to a 30-day purchase block:

• Stable Value Fund • Active Bond Fund • Target Retirement Date Income Fund • Target Retirement Date 2010 Fund • Target Retirement Date 2015 Fund • Target Retirement Date 2020 Fund • Target Retirement Date 2025 Fund • Target Retirement Date 2030 Fund • Target Retirement Date 2035 Fund • Target Retirement Date 2040 Fund • Target Retirement Date 2045 Fund • Target Retirement Date 2050 Fund • Target Retirement Date 2055 Fund • Target Retirement Date 2060 Fund • Active US Large Cap Equity Fund

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

24

• Active US Small-Mid Equity Fund • Active International Equity Fund • U.S. Bancorp ESOP Stock Fund

The following U.S. Bank 401(k) Savings Plan funds are subject to a 60-day purchase block:

• Bond Index Fund • US Large Cap Equity Index Fund • US Small-Mid Equity Index Fund • International Equity Index Fund

Exclusions The purchase block restrictions do not apply to new contributions, loans, loan payments, withdrawals, distributions or rollovers. Redemption Fees As long as you are invested in a fund for the long term, you generally will not need to be concerned about redemption fees. These fees are designed to discourage excessive in-and-out trades and to reimburse the costs incurred to the funds from such trades. Some funds impose redemption fees on activities that move money out of a fund before a minimum period of time, known as a holding period. The fees apply only to transfers. The fees do not apply to other plan activities, such as:

• Contributions • Withdrawals • Loans • Loan repayments

Redemption fees are deducted from the amount you take out of a fund. Example: You transfer $5,000 out of a fund that you moved money into for the first time only 10 days ago. This fund carries a 2% redemption fee for transfers made before the 60-day holding period ends. Thus, a $100 redemption fee is assessed, and $4,900 is transferred. When you submit a request to move money out of a fund, any money held in the fund longer than the holding period is taken first. This minimizes the chance of any redemption fees on your transactions. Example: You have $10,000 in the International Equity Index Fund for the whole year. You elect to transfer $5,000 into the International Equity Index Fund today. A few days later, you transfer $8,000 out of the International Equity Index Fund, but the monies being transferred out are not subject to the redemption fee because the $8,000 comes from monies that have been in the fund longer than the 60 day holding period. Monies first into the fund are the first monies out (FIFO) of the fund when you elect to transfer monies out of the fund. The holding periods and redemption fee percentages may vary with each fund. Some funds have different levels of fees, so that a higher penalty may occur if money is transferred in a shorter time.

U.S. Bank 401(k) Savings Plan SPD Effective January 2012

25

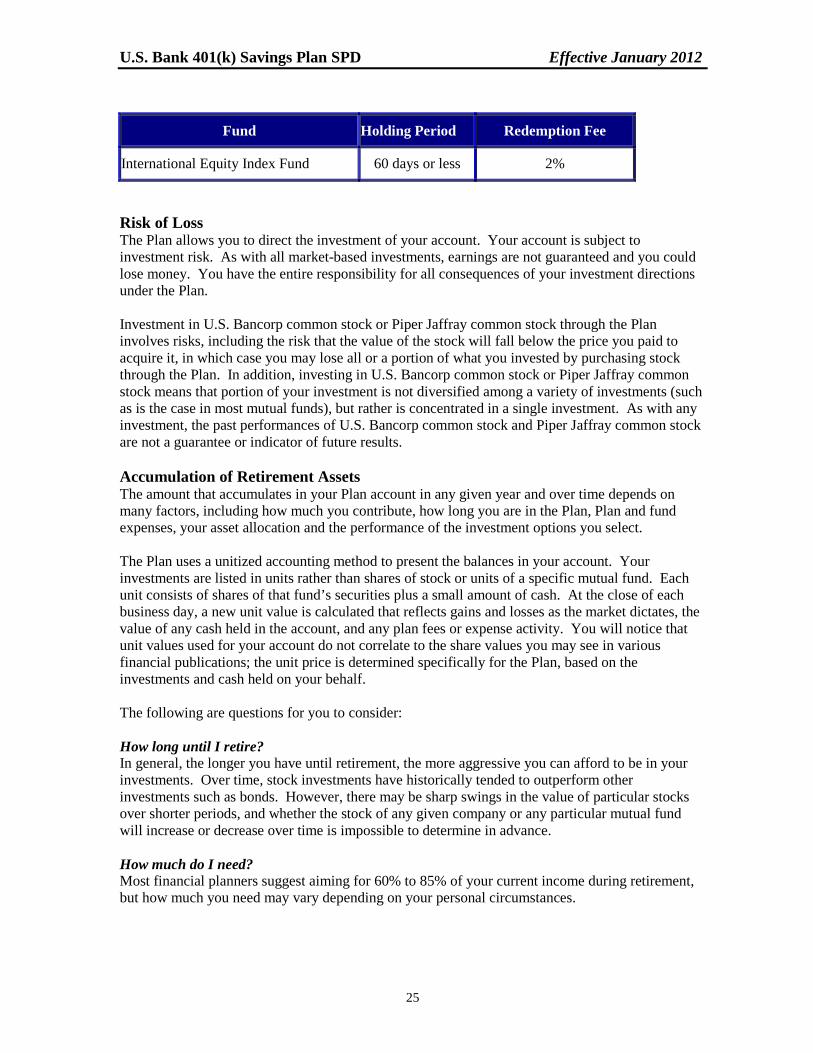

Risk of Loss The Plan allows you to direct the investment of your account. Your account is subject to investment risk. As with all market-based investments, earnings are not guaranteed and you could lose money. You have the entire responsibility for all consequences of your investment directions under the Plan. Investment in U.S. Bancorp common stock or Piper Jaffray common stock through the Plan involves risks, including the risk that the value of the stock will fall below the price you paid to acquire it, in which case you may lose all or a portion of what you invested by purchasing stock through the Plan. In addition, investing in U.S. Bancorp common stock or Piper Jaffray common stock means that portion of your investment is not diversified among a variety of investments (such as is the case in most mutual funds), but rather is concentrated in a single investment. As with any investment, the past performances of U.S. Bancorp common stock and Piper Jaffray common stock are not a guarantee or indicator of future results. Accumulation of Retirement Assets The amount that accumulates in your Plan account in any given year and over time depends on many factors, including how much you contribute, how long you are in the Plan, Plan and fund expenses, your asset allocation and the performance of the investment options you select. The Plan uses a unitized accounting method to present the balances in your account. Your investments are listed in units rather than shares of stock or units of a specific mutual fund. Each unit consists of shares of that fund’s securities plus a small amount of cash. At the close of each business day, a new unit value is calculated that reflects gains and losses as the market dictates, the value of any cash held in the account, and any plan fees or expense activity. You will notice that unit values used for your account do not correlate to the share values you may see in various financial publications; the unit price is determined specifically for the Plan, based on the investments and cash held on your behalf. The following are questions for you to consider: How long until I retire? In general, the longer you have until retirement, the more aggressive you can afford to be in your investments. Over time, stock investments have historically tended to outperform other investments such as bonds. However, there may be sharp swings in the value of particular stocks over shorter periods, and whether the stock of any given company or any particular mutual fund will increase or decrease over time is impossible to determine in advance. How much do I need? Most financial planners suggest aiming for 60% to 85% of your current income during retirement, but how much you need may vary depending on your personal circumstances.

Fund Holding Period Redemption Fee

International Equity Index Fund 60 days or less 2%