Upstream investment trends for Japanese LNG buyers · PDF fileUpstream investment trends for...

18

0 Ryuta KITAMURA JOGMEC Sydney Office Australian Gas Export Outlook 2014 24 th June, 2014 Upstream investment trends for Japanese LNG buyers and developers

Transcript of Upstream investment trends for Japanese LNG buyers · PDF fileUpstream investment trends for...

0

Ryuta KITAMURA

JOGMEC Sydney Office

Australian Gas Export Outlook 2014

24th June, 2014

Upstream investment trends for Japanese

LNG buyers and developers

1

Metals Strategy &

Exploration, and

Technology

Development

Mine Pollution

Control

Stockpiling Oil & Gas Upstream

Investment and

Research & Development

Mission Securing Stable Supply of Oil, Natural Gas, Coal and Mineral Resources for Japanese

Industries and Citizens

Established: February 29, 2004 [succeeded the functions of Japan National Oil Corporation(JNOC)]

President: Hirobumi Kawano

Capital: 502 Billion Yen (As of April, 2013) = around 5.02 Billion US$ (100US$/Yen)

Activities

Coal Strategy &

Exploration, and

Technological

Support

Geothermal

Resources

Development

Japan Oil, Gas and Metals National Corporation (JOGMEC)

2 JOGMEC Oil & Gas Upstream Project (Natural Gas)

(As of Mar 31, 2014)

Equity Capital (44)

Liability Guarantee (13)

Tangguh LNG Project

(Indonesia)

Abadi LNG Project

(Indonesia)

PNG LNG Project

(Papua New Guinea )

Wheatstone LNG Project

(Australia)

Rovuma Offshore Area 1

Project

(Mozambique)

Sakhalin I Project

(Russia)

Ichthys LNG Project

(Australia)

Kudu Project

(Namibia)

Cordova Shale Gas Project

(Canada)

Cutbank Dawson Shale Gas Project

(Canada)

North Montney Shale Gas Project

(Canada)

Horn River Shale Gas Project

(Canada)

(Source: JOGMEC)

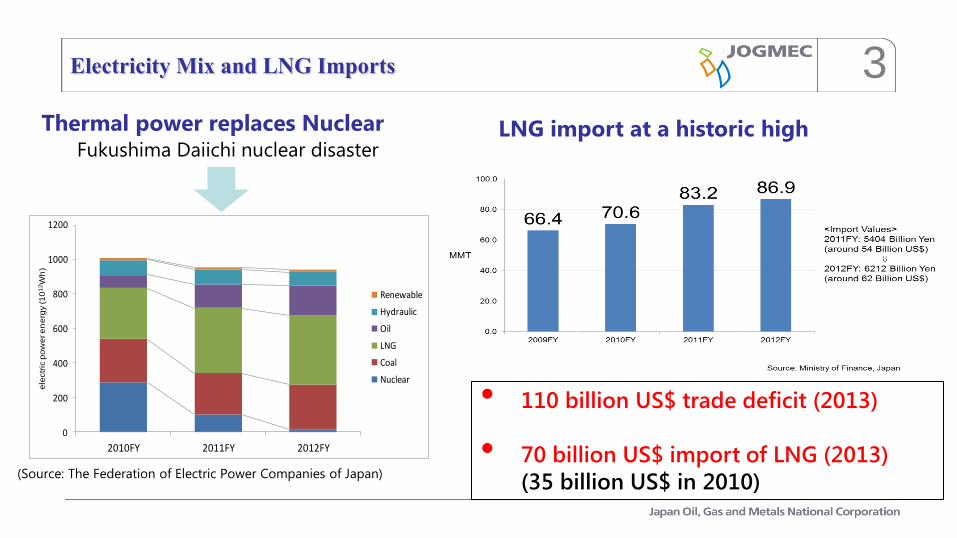

3 Electricity Mix and LNG Imports

0

200

400

600

800

1000

1200

2010FY 2011FY 2012FY

ele

ctr

ic p

ow

er e

ne

rgy (1

012W

h)

Renewable

Hydraulic

Oil

LNG

Coal

Nuclear

(Source: The Federation of Electric Power Companies of Japan)

Fukushima Daiichi nuclear disaster

Thermal power replaces Nuclear LNG import at a historic high

• 110 billion US$ trade deficit (2013)

• 70 billion US$ import of LNG (2013)

(35 billion US$ in 2010)

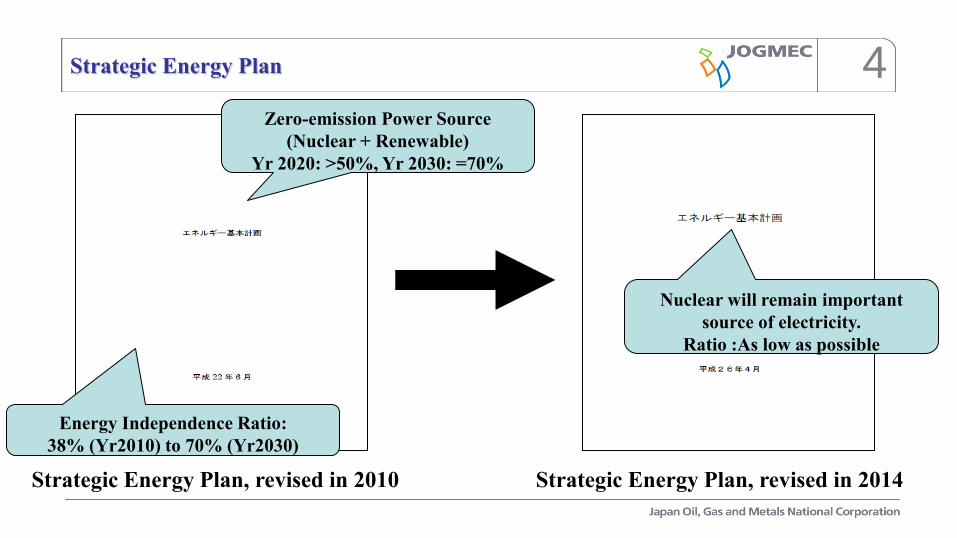

4 Strategic Energy Plan

Strategic Energy Plan, revised in 2010 Strategic Energy Plan, revised in 2014

Zero-emission Power Source

(Nuclear + Renewable)

Yr 2020: >50%, Yr 2030: =70%

Energy Independence Ratio:

38% (Yr2010) to 70% (Yr2030)

Nuclear will remain important

source of electricity.

Ratio :As low as possible

5 Japanese LNG Import Outlook

(Source: BREE Resources and Energy Quarterly, Mar 2014)

6 Upstream Investment by Utility Companies

in Australia & PNG

Stanley Sunrise / Evans Shoal

Pluto LNG

Ichthys LNG Darwin LNG

Wheatstone LNG

Crux

Gorgon LNG

Producing

• Darwin LNG FID in 2003 (First LNG in 2006)

• Pluto LNG FID in 2007 (First LNG in 2012)

Under Construction

• Gorgon LNG in 2009

• Wheatstone LNG in 2010-12

• QC LNG in 2011

• Ichthys LNG in 2011-12

Planning Stage

• Sunrise & Evan Shoal in 2000

• Crux in 2007

• Stanley in 2014*(Awaiting Completion)

Queensland Curtis LNG

(Source: JOGMEC Sydney Office)

Producing

Construction

Planning/Exploration

7 Upstream Investment by Japanese Utility Companies

• Osaka Gas acquired

WI for Sanga-Sanga

Block in Indonesia in

1990.

• Osaka gas invested in

Snorre oil field

offshore Norway from

2005.

• Utility companies are

expanding to North

America (2012-14).

(Source: JOGMEC Sydney Office)

Barnett (Shale) Snorre Oil Field

Cordova (Shale)

Sanga Sanga

(Bontang LNG)

Qalhat LNG

Pearsall (Shale)

Freeport LNG

Cove Point LNG

Producing

LNG Planning/Construction

Upstream (LNG Source)

8 Upstream Investment by Japanese LNG Buyers

(Tokyo Gas – Challenge 2020 Vision – )

(Source: Tokyo Gas “Challenge 2020 Vision”, Nov. 2011 )

9 Upstream Investment by Japanese LNG Buyers

(Osaka Gas – Field of Dreams 2020 – )

(Source: Osaka Gas “Field of Dreams 2020”, Mar. 2009 )

10

• Understanding Upstream Business Conventional -> Unconventional (CSG, Shale)

• Risk Hedge (Seller / Buyer)

• Equity Lifting

Key Word for Investing on Upstream Project

for Utility Companies

11 Browse FLNG

• MIMI is Japan Australia LNG Pty Ltd,

50:50 joint venture between Mitsubishi

& Mitsui.

MIMI established for North West Shelf

LNG project in 1985.

• Trading houses are active in exploration

projects as well as development projects.

Mitsui and Mitsubishi hold some other

exploration licenses offshore WA.

(Source: JOGMEC Sydney Office)

Upstream Investment by Japanese Trading Houses

in Australia & PNG

Canning Basin

Exploration

Talisman Gas

Project

NWS LNG

Meridian CSG

Casino/Henry

Gas Field Bass Gas Project

Otway Gas Project

Enfield/Vincent

Oil Field

Surat Basin CSG

PNG-LNG

Producing

Construction

Planning/Exploration

12 • Starting in SE Asia,

Middle East and

Australia 70’s to 80’s

– Brunei 1972 (1st Cargo)

– Abu Dhabi 1977

– Malaysia 1983

– North West Shelf 1989

• In Middle East 90’s to

early-00’s

– Qatargas 1996

– RasGas 1999

– Oman 2000

– Qalhat 2005

• Then, diversify globally

– Africa

– Latin America

– North America Producing

LNG Planning/Construction

Upstream (LNG Source) (Source: JOGMEC Sydney Office)

Upstream/LNG Investment by Japanese Trading Houses

Barnett (Shale)

Sakhalin 2 LNG

Tangguh LNG

Cameron LNG

Malaysia LNG

Qatargas / RasGas

LNG Abu Dhabi LNG

Brunei LNG

Equatorial Guinea

LNG

LNG Canada

(Cordova/Montney)

Oman/Qalhat

LNG

Peru LNG Mozambique

LNG

Eagle Ford (Shale)

Marcellus (Shale)

Alberta (CBM)

Cove Point LNG

Sanga Sanga

(Bontang LNG)

Donngi Senoro LNG

13 Upstream Investment by Japanese LNG Buyers

(Mitsubishi Corporation)

(Source: Mitsubishi Corporation “New Strategic Direction”, May. 2013 )

14 Key Word for Investing on Upstream Project

for Trading Houses

• LNG Value Chain

Production -> Liquefaction -> Shipping -> Marketing

• Tolling vs Upstream/Liquefaction Packaging

(Especially in North America)

• Conventional / Unconventional

Potential asset for LNG project

15 Emerging Japanese LNG Player

(Source: Wood Mackenzie “Emerging Japanese LNG Players”, March, 2014 )

• Producing & Developing LNG

INPEX - Tangguh, Darwin LNG, Ichthys,

Prelude

JX Nippon -PNG LNG

JAPEX - Sanga Sanga (Bontang LNG)

• Potential projects for LNG

INPEX - Abadi FLNG

INPEX & JGC - BC Shale w/Nexen

JAPEX - Pacific NorthWest LNG

• Liquefaction & Export project (Tolling)

IDEMITSU - Triton LNG

• LNG off-take

INPEX - Ichthys, (Abadi ?)

JX Nippon - Gorgon

JAPEX - MLNG 3, PNW-LNG

TOSHIBA - Freeport LNG

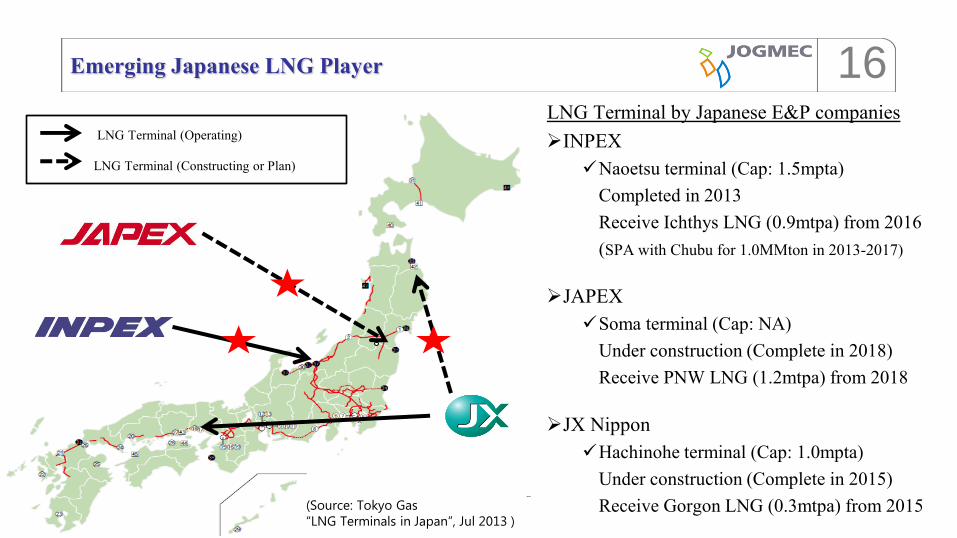

• LNG Terminal by Japanese E&P companies

INPEX

Naoetsu terminal (Cap: 1.5mpta)

Completed in 2013

Receive Ichthys LNG (0.9mtpa) from 2016

(SPA with Chubu for 1.0MMton in 2013-2017)

JAPEX

Soma terminal (Cap: NA)

Under construction (Complete in 2018)

Receive PNW LNG (1.2mtpa) from 2018

JX Nippon

Hachinohe terminal (Cap: 1.0mpta)

Under construction (Complete in 2015)

Receive Gorgon LNG (0.3mtpa) from 2015

16 Emerging Japanese LNG Player

(Source: Tokyo Gas

“LNG Terminals in Japan”, Jul 2013 )

LNG Terminal (Operating)

LNG Terminal (Constructing or Plan)

17 Conclusion

• LNG demand in Japan will remain high over the next 5years.

Almost half of the supply will come from Australia in 2019.

• Utility companies and Trading houses continue to be active

investing in upstream LNG projects to secure a stable and

diversified supply of LNG.

• E&P companies and other new players may enter the LNG

industry not only as a developer but also as a off-taker as well.