Update on Growth Strategy June 2016 - continental.com€¦ · › Conti founded new Intelligent...

26

http://www.continental-ir.com Ticker: CON ADR-Ticker: CTTAY Twitter: @Continental_IR Update on Growth Strategy June 2016 Wolfgang Schaefer – CFO

Transcript of Update on Growth Strategy June 2016 - continental.com€¦ · › Conti founded new Intelligent...

http://www.continental-ir.com

Ticker: CON ADR-Ticker: CTTAY Twitter: @Continental_IR

Update on Growth Strategy June 2016

Wolfgang Schaefer – CFO

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 2

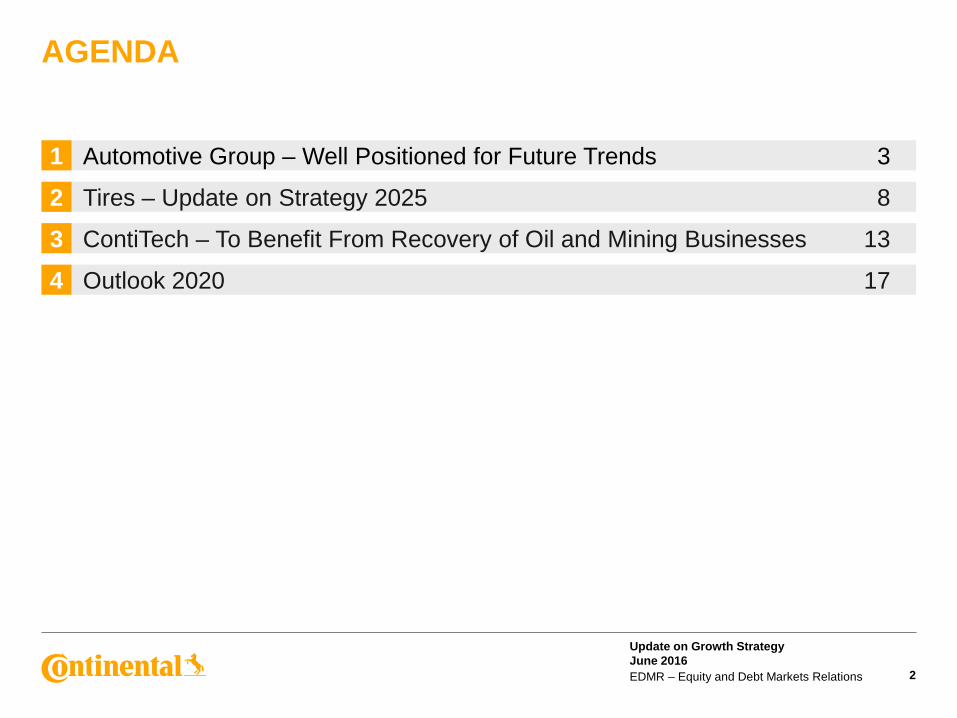

AGENDA

Automotive Group – Well Positioned for Future Trends 1 3

Tires – Update on Strategy 2025 2 8

ContiTech – To Benefit From Recovery of Oil and Mining Businesses 3 13

Outlook 2020 4 17

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

Mobility Services

Electric Mobility

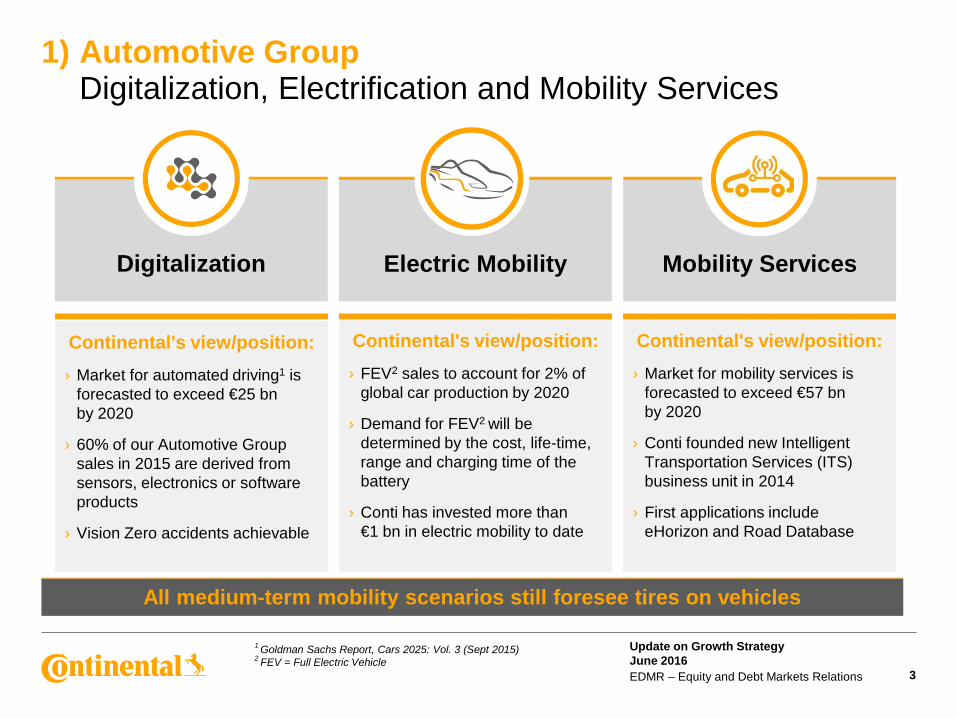

1) Automotive Group Digitalization, Electrification and Mobility Services

Digitalization

Continental's view/position: › Market for automated driving1 is

forecasted to exceed €25 bn by 2020

› 60% of our Automotive Group sales in 2015 are derived from sensors, electronics or software products

› Vision Zero accidents achievable

Continental's view/position: › FEV2 sales to account for 2% of

global car production by 2020

› Demand for FEV2 will be determined by the cost, life-time, range and charging time of the battery

› Conti has invested more than €1 bn in electric mobility to date

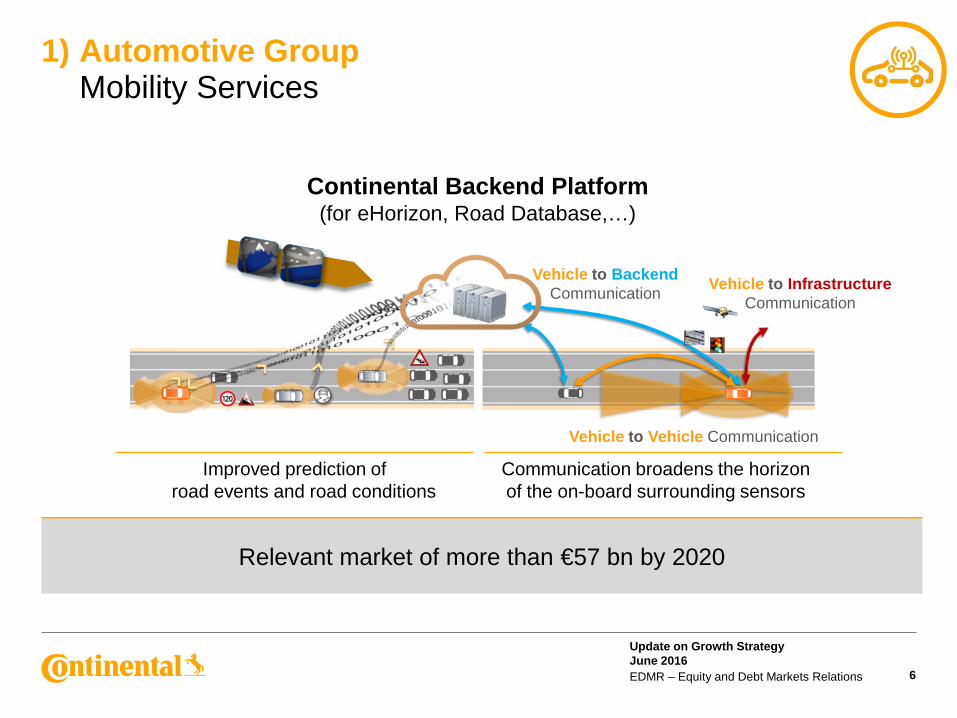

Continental's view/position: › Market for mobility services is

forecasted to exceed €57 bn by 2020

› Conti founded new Intelligent Transportation Services (ITS) business unit in 2014

› First applications include eHorizon and Road Database

All medium-term mobility scenarios still foresee tires on vehicles

1 Goldman Sachs Report, Cars 2025: Vol. 3 (Sept 2015) 2 FEV = Full Electric Vehicle

3

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 4

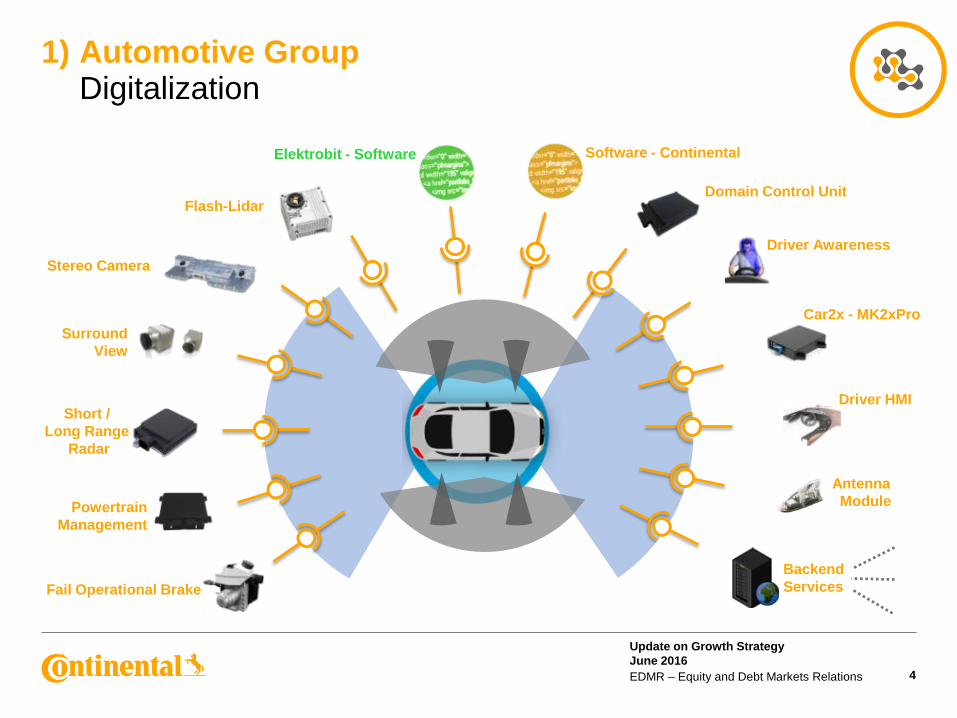

1) Automotive Group Digitalization

Powertrain Management

Surround View

Fail Operational Brake

Car2x - MK2xPro

Stereo Camera

Antenna Module

Short / Long Range

Radar

Flash-Lidar Domain Control Unit

Software - Continental Elektrobit - Software

Backend Services

Driver Awareness

Driver HMI

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

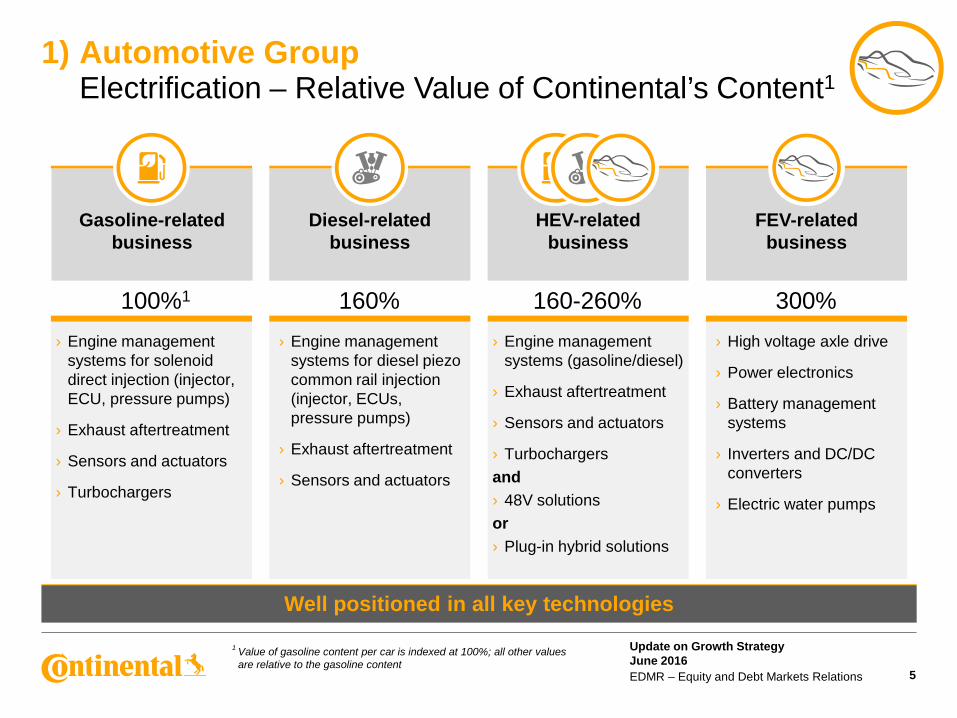

HEV-related

business

Gasoline-related

business

1) Automotive Group Electrification – Relative Value of Continental’s Content1

Diesel-related

business

› Engine management systems for diesel piezo common rail injection (injector, ECUs, pressure pumps)

› Exhaust aftertreatment

› Sensors and actuators

› Engine management systems for solenoid direct injection (injector, ECU, pressure pumps)

› Exhaust aftertreatment

› Sensors and actuators

› Turbochargers

› Engine management systems (gasoline/diesel)

› Exhaust aftertreatment

› Sensors and actuators

› Turbochargers and › 48V solutions or › Plug-in hybrid solutions

Well positioned in all key technologies

FEV-related

business

› High voltage axle drive

› Power electronics

› Battery management systems

› Inverters and DC/DC converters

› Electric water pumps

100%1 160% 160-260% 300%

1 Value of gasoline content per car is indexed at 100%; all other values are relative to the gasoline content

5

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 6

1) Automotive Group Mobility Services

Improved prediction of road events and road conditions

Vehicle to Infrastructure Communication

Vehicle to Backend Communication

Vehicle to Vehicle Communication

Communication broadens the horizon of the on-board surrounding sensors

Continental Backend Platform (for eHorizon, Road Database,…)

Relevant market of more than €57 bn by 2020

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

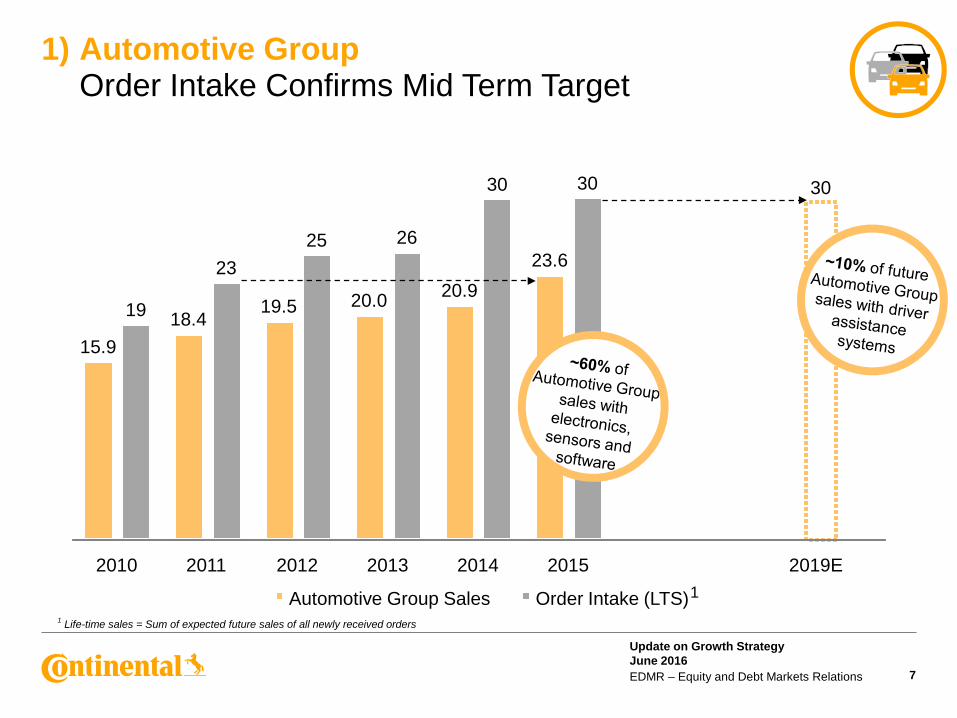

15.9 18.4

19.5 20.0 20.9 23.6

30

19

23 25 26

30 30

2010 2011 2012 2013 2014 2015 2019E

Automotive Group Sales Order Intake (LTS)

7

1) Automotive Group

Order Intake Confirms Mid Term Target

1 Life-time sales = Sum of expected future sales of all newly received orders

1

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

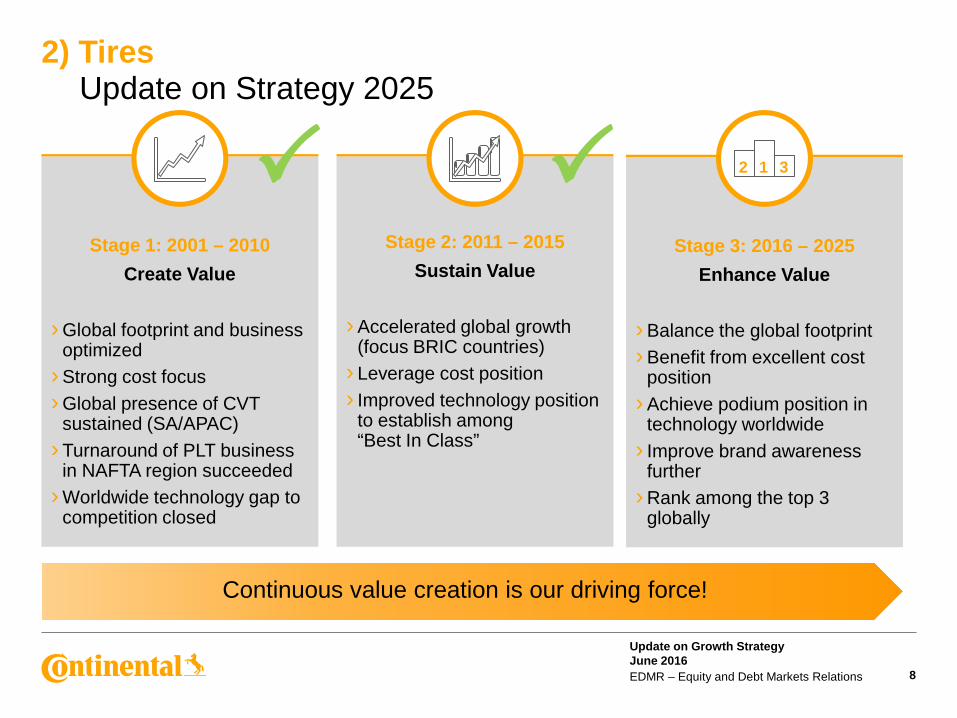

Stage 2: 2011 – 2015 Sustain Value

› Accelerated global growth

(focus BRIC countries) › Leverage cost position › Improved technology position

to establish among “Best In Class”

8

2) Tires Update on Strategy 2025

Continuous value creation is our driving force!

Stage 3: 2016 – 2025 Enhance Value

› Balance the global footprint › Benefit from excellent cost

position › Achieve podium position in

technology worldwide › Improve brand awareness

further › Rank among the top 3

globally

2 1 3

Stage 1: 2001 – 2010 Create Value

› Global footprint and business

optimized › Strong cost focus › Global presence of CVT

sustained (SA/APAC) › Turnaround of PLT business

in NAFTA region succeeded › Worldwide technology gap to

competition closed

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

0%

25%

50%

75%

100%

2010 2015 2025 target

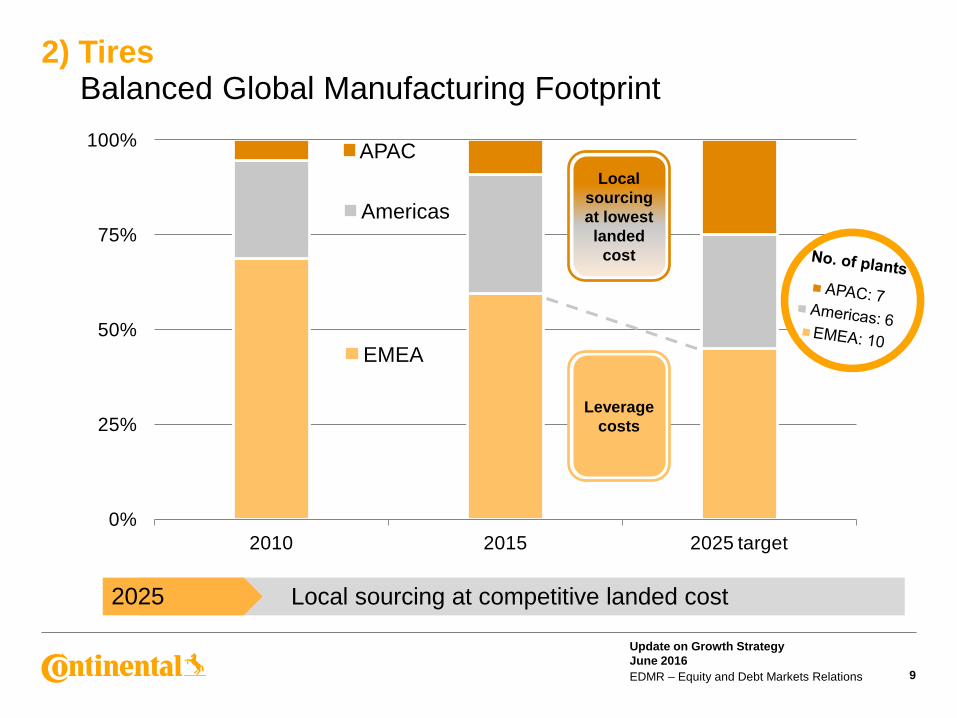

2) Tires Balanced Global Manufacturing Footprint

2025 Local sourcing at competitive landed cost

9

Local sourcing at lowest landed

cost

Leverage costs

APAC

Americas

EMEA

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

0%

20%

40%

60%

80%

100%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

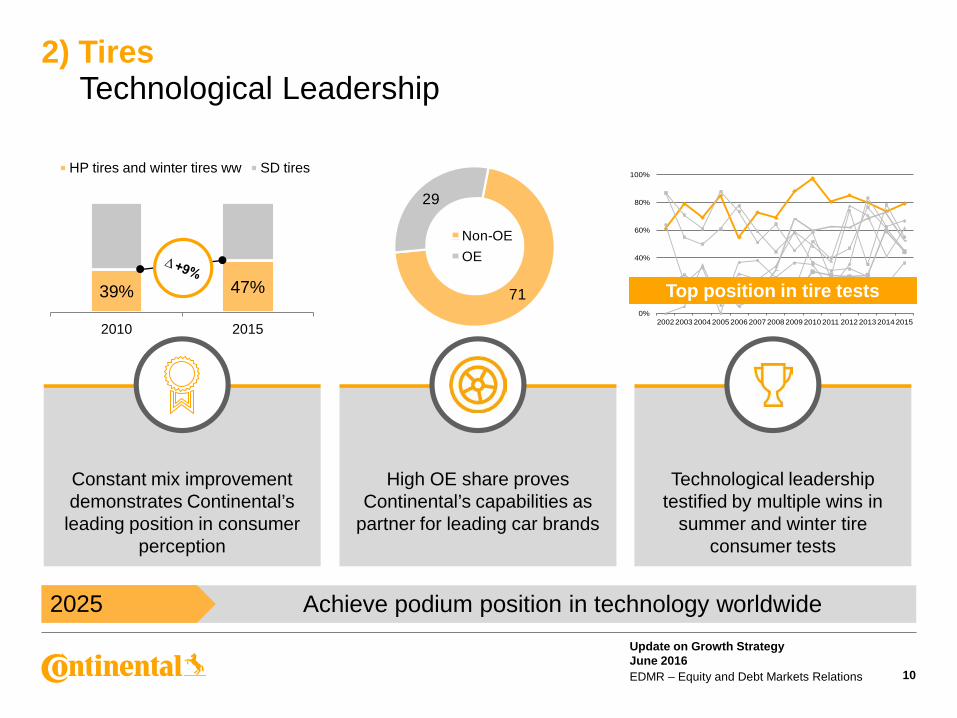

2) Tires Technological Leadership

10

Top position in tire tests

Technological leadership testified by multiple wins in

summer and winter tire consumer tests

Constant mix improvement demonstrates Continental’s

leading position in consumer perception

2025 Achieve podium position in technology worldwide

39% 47%

2010 2015

HP tires and winter tires ww SD tires

71

29

Non-OEOE

High OE share proves Continental’s capabilities as

partner for leading car brands

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

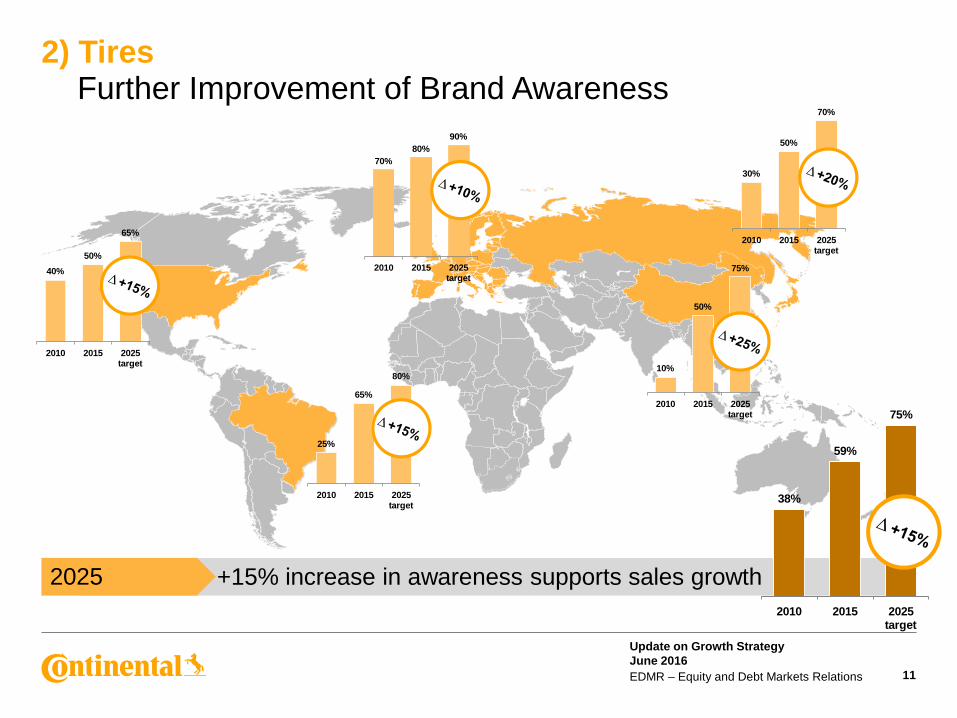

2) Tires Further Improvement of Brand Awareness

2025 +15% increase in awareness supports sales growth

11

40%50%

65%

2010 2015 2025 target

70%80%

90%

2010 2015 2025 target

25%

65%

80%

2010 2015 2025 target

30%

50%

70%

2010 2015 2025 target

10%

50%

75%

2010 2015 2025 target

38%

59%

75%

2010 2015 2025 target

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

0

40

80

120

2010 2015 2025 target

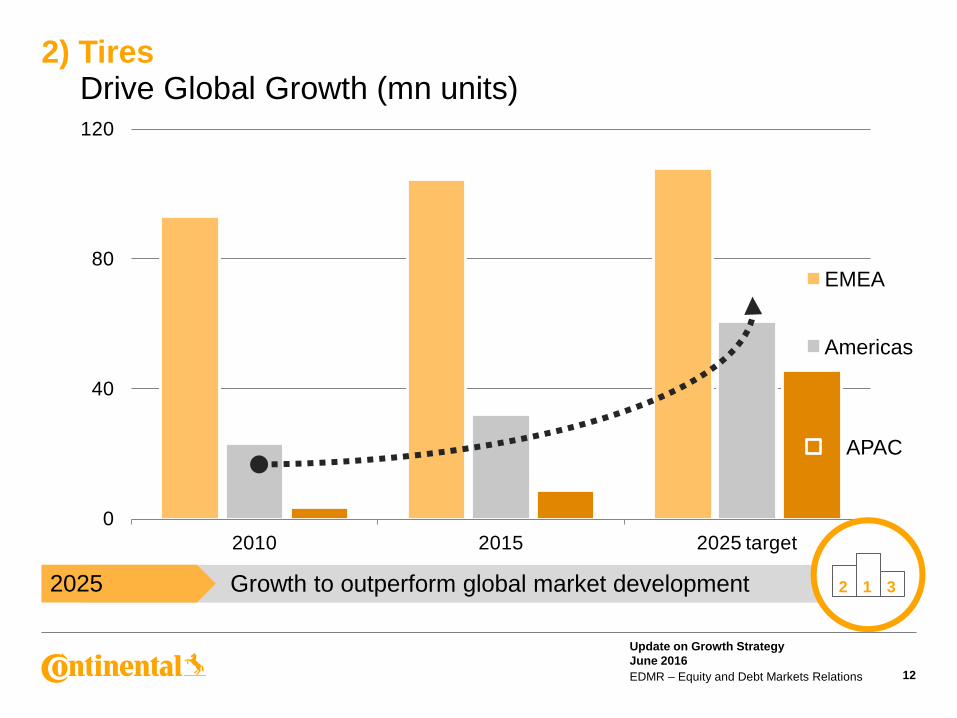

2) Tires Drive Global Growth (mn units)

2025 Growth to outperform global market development

12

2 1 3

APAC

Americas

EMEA

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

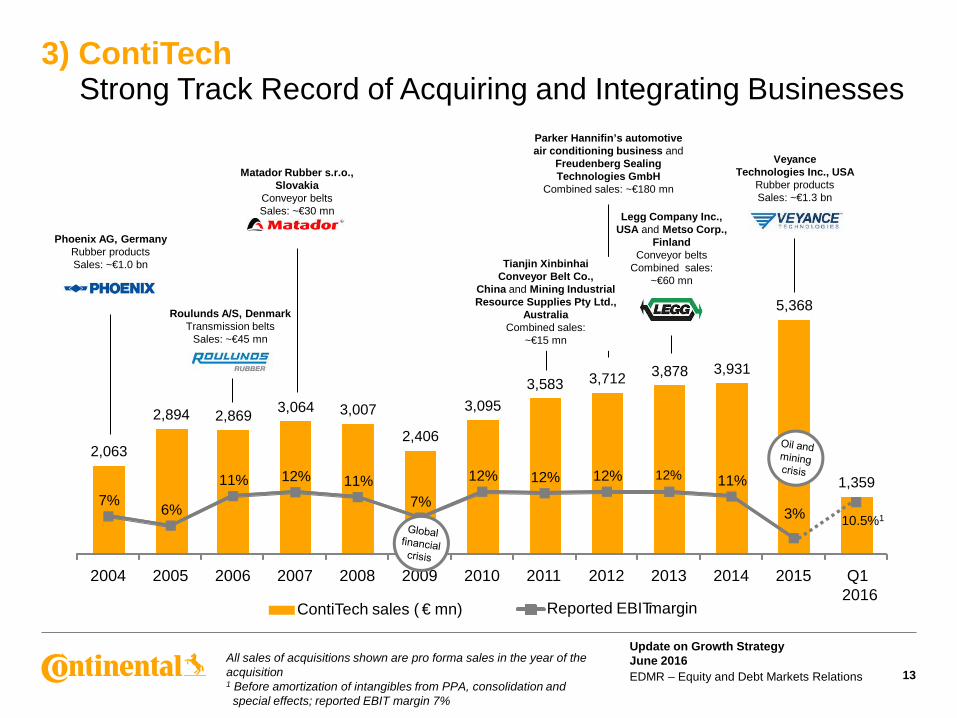

Parker Hannifin’s automotive air conditioning business and

Freudenberg Sealing Technologies GmbH

Combined sales: ~€180 mn

13

3) ContiTech Strong Track Record of Acquiring and Integrating Businesses

Phoenix AG, Germany Rubber products Sales: ~€1.0 bn

Roulunds A/S, Denmark Transmission belts

Sales: ~€45 mn

Matador Rubber s.r.o., Slovakia

Conveyor belts Sales: ~€30 mn

Tianjin Xinbinhai Conveyor Belt Co.,

China and Mining Industrial Resource Supplies Pty Ltd.,

Australia Combined sales:

~€15 mn

Legg Company Inc., USA and Metso Corp.,

Finland Conveyor belts

Combined sales: ~€60 mn

Veyance Technologies Inc., USA

Rubber products Sales: ~€1.3 bn

2,063

2,894 2,869 3,064 3,007

2,406

3,095 3,583 3,712 3,878 3,931

5,368

1,359 7% 6%

11% 12% 11% 7%

12% 12% 12% 12% 11%

3% 10.5%1

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1 2016

ContiTech sales ( € mn) Reported EBIT margin

All sales of acquisitions shown are pro forma sales in the year of the acquisition 1 Before amortization of intangibles from PPA, consolidation and special effects; reported EBIT margin 7%

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 14

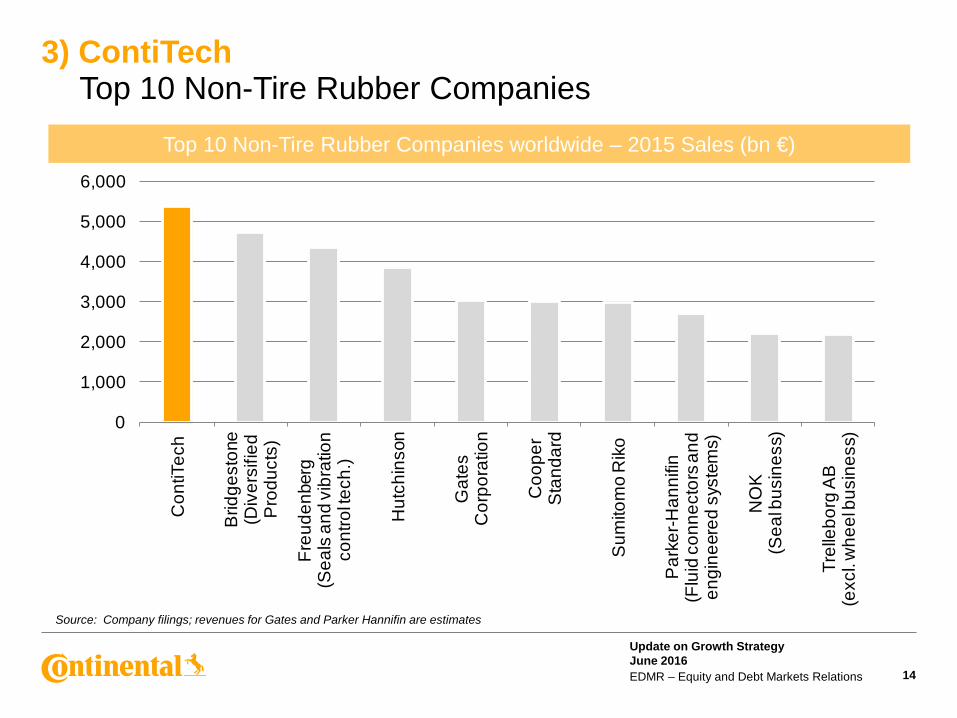

3) ContiTech Top 10 Non-Tire Rubber Companies

Top 10 Non-Tire Rubber Companies worldwide – 2015 Sales (bn €)

Source: Company filings; revenues for Gates and Parker Hannifin are estimates

0

1,000

2,000

3,000

4,000

5,000

6,000C

ontiT

ech

Brid

gest

one

(Div

ersi

fied

Pro

duct

s)

Freu

denb

erg

(Sea

ls a

nd v

ibra

tion

cont

rol te

ch.)

Hut

chin

son

Gat

esC

orpo

ratio

n

Coo

per

Sta

ndar

d

Sum

itom

o R

iko

Par

ker-H

anni

fin

(Flu

id c

onne

ctor

s and

en

gine

ered

sys

tem

s)

NO

K(S

eal b

usin

ess)

Trel

lebo

rg A

B

(exc

l. whe

el b

usin

ess)

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 15

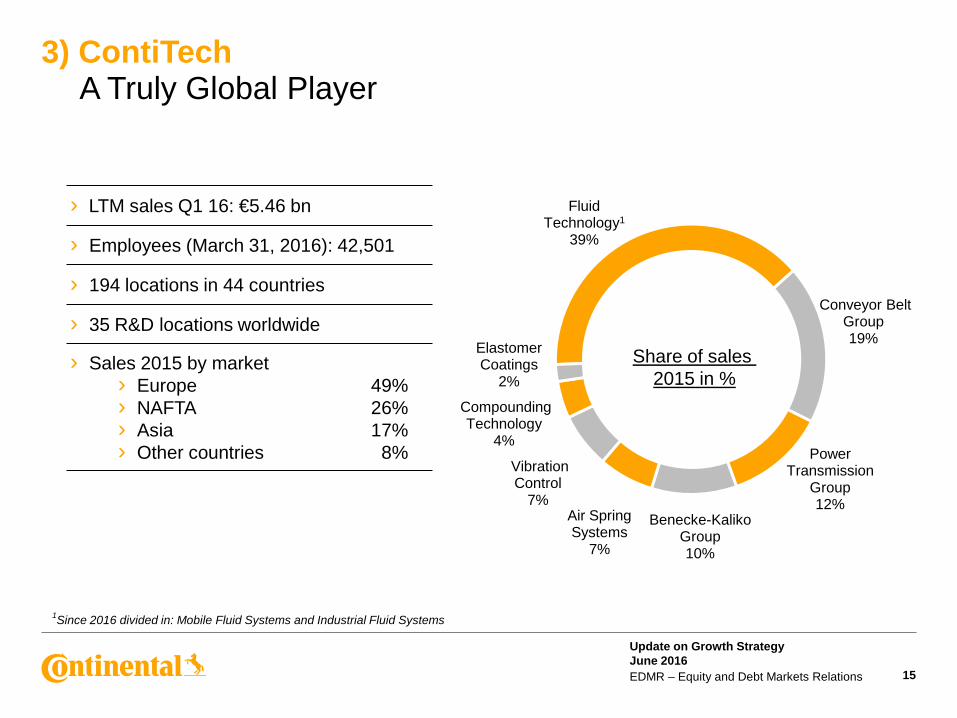

3) ContiTech A Truly Global Player

› LTM sales Q1 16: €5.46 bn

› Employees (March 31, 2016): 42,501

› 194 locations in 44 countries

› 35 R&D locations worldwide

› Sales 2015 by market › Europe 49% › NAFTA 26% › Asia 17% › Other countries 8%

Fluid Technology1

39%

Conveyor Belt Group 19%

Power Transmission

Group 12%

Benecke-Kaliko Group 10%

Air Spring Systems

7%

Vibration Control

7%

Compounding Technology

4%

Elastomer Coatings

2% Share of sales

2015 in %

1Since 2016 divided in: Mobile Fluid Systems and Industrial Fluid Systems

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

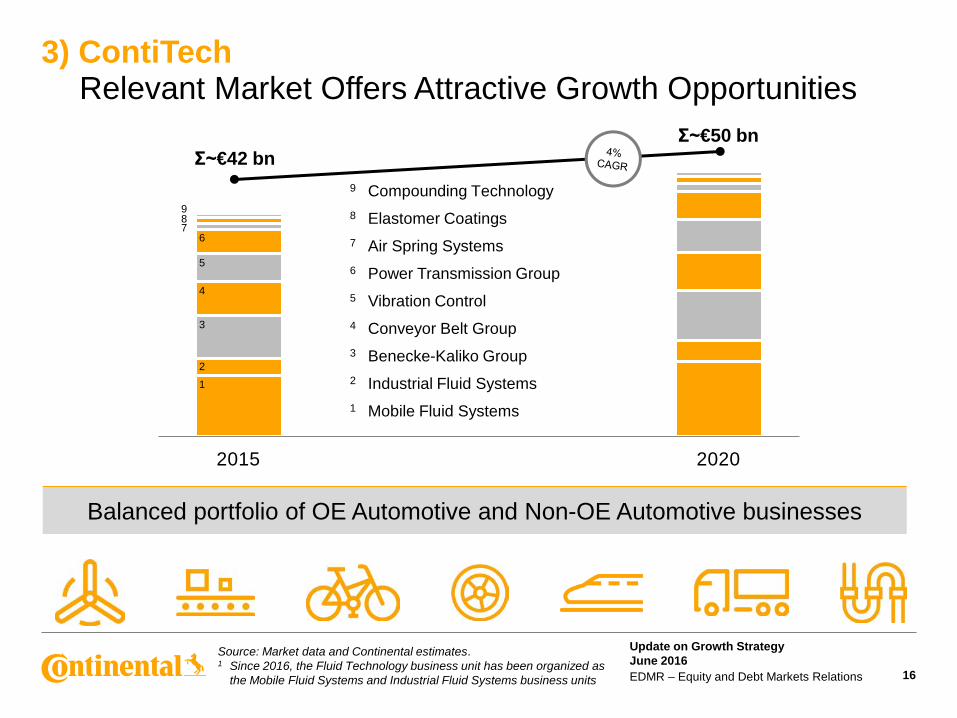

2015 2020

16

3) ContiTech Relevant Market Offers Attractive Growth Opportunities

Source: Market data and Continental estimates. 1 Since 2016, the Fluid Technology business unit has been organized as

the Mobile Fluid Systems and Industrial Fluid Systems business units

Σ~€50 bn Σ~€42 bn

1 Mobile Fluid Systems

3 Benecke-Kaliko Group

4 Conveyor Belt Group

5 Vibration Control

6 Power Transmission Group

7 Air Spring Systems

8 Elastomer Coatings

9 Compounding Technology

2 Industrial Fluid Systems

Balanced portfolio of OE Automotive and Non-OE Automotive businesses

1

2

3

4

5

6 7 8 9

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations

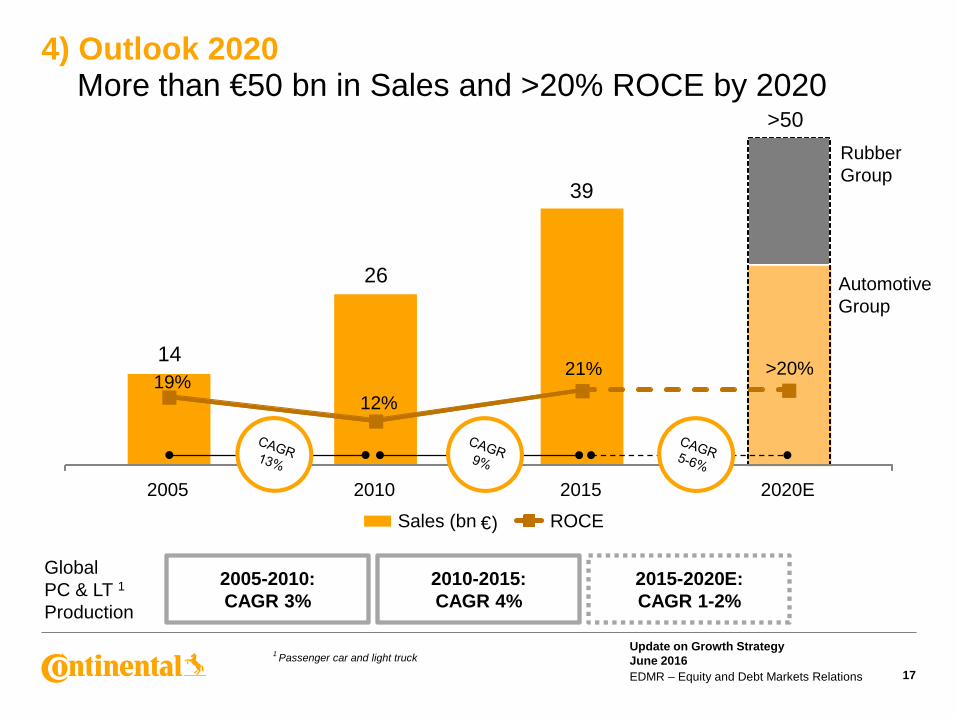

14

26

39

>50

19% 12%

21% >20%

2005 2010 2015 2020E

Sales (bn € ) ROCE

17

4) Outlook 2020 More than €50 bn in Sales and >20% ROCE by 2020

1 Passenger car and light truck

2005-2010: CAGR 3%

2010-2015: CAGR 4%

2015-2020E: CAGR 1-2%

Rubber Group

Automotive Group

Global PC & LT 1 Production

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 18

Thank you!

Official Sponsor of the UEFA European Football Championship™

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 19

Disclaimer

› This presentation has been prepared by Continental Aktiengesellschaft solely in connection with the 18th European CEO Conference from June 14 – 16 in Paris, organized by Exane BNPP. It has not been independently verified. It does not constitute an offer, invitation or recommendation to purchase or subscribe for any shares or other securities issued by Continental AG or any subsidiary and neither shall any part of it form the basis of, or be relied upon in connection with, any contract or commitment concerning the purchase or sale of such shares or other securities whatsoever.

› Neither Continental Aktiengesellschaft nor any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss that may arise from any use of this presentation or its contents or otherwise arising in connection with this presentation.

› This presentation includes assumptions, estimates, forecasts and other forward-looking statements, including statements about our beliefs and expectations regarding future developments as well as their effect on the results of Continental. These statements are based on plans, estimates and projections as they are currently available to the management of Continental. Therefore, these statements speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events. Furthermore, although the management is of the opinion that these statements, and their underlying beliefs and expectations, are realistic as of the date they are made, no guarantee can be given that the expected developments and effects will actually occur. Many factors may cause the actual development to be materially different from the expectations expressed here. Such factors include, for example and without limitation, changes in general economic and business conditions, fluctuations in currency exchange rates or interest rates, the introduction of competing products, the lack of acceptance for new products or services and changes in business strategy.

› All statements with regard to markets or market position(s) of Continental or any of its competitors are estimates of Continental based on data available to Continental. Such data are neither comprehensive nor independently verified. Consequently, the data used are not adequate for and the statements based on such data are not meant to be an accurate or proper definition of regional and/or product markets or market shares of Continental and any of the participants in any market.

› Unless otherwise stated, all amounts are shown in millions of euro. Please note that differences may arise as a result of the use of rounded amounts and percentages.

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 20

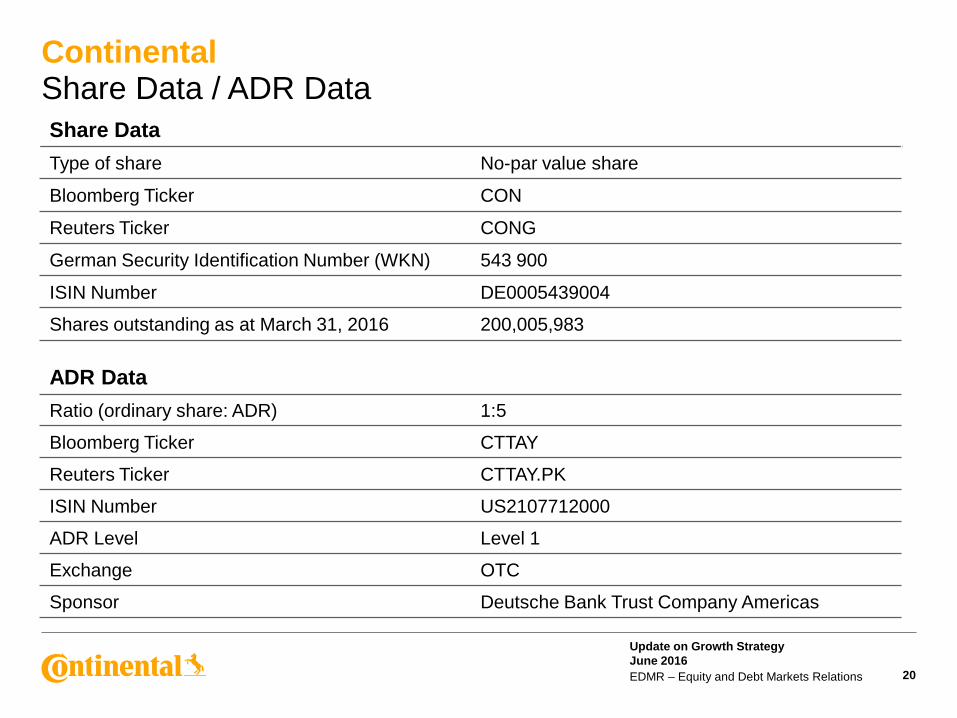

Continental Share Data / ADR Data Share Data Type of share No-par value share

Bloomberg Ticker CON

Reuters Ticker CONG

German Security Identification Number (WKN) 543 900

ISIN Number DE0005439004

Shares outstanding as at March 31, 2016 200,005,983

ADR Data Ratio (ordinary share: ADR) 1:5

Bloomberg Ticker CTTAY

Reuters Ticker CTTAY.PK

ISIN Number US2107712000

ADR Level Level 1

Exchange OTC

Sponsor Deutsche Bank Trust Company Americas

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 21

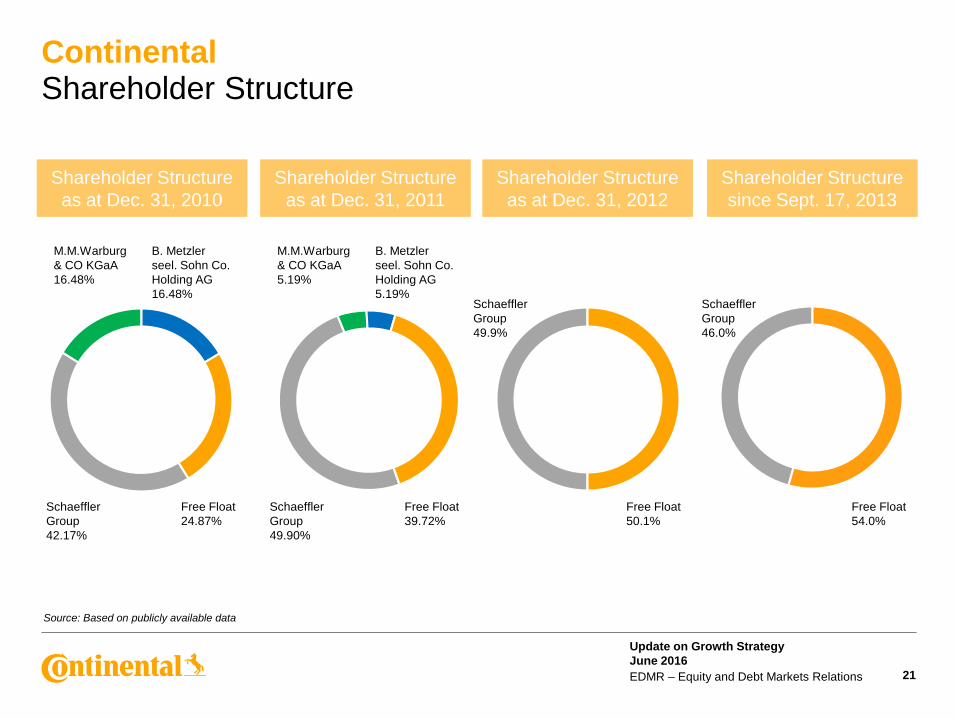

Continental Shareholder Structure

Source: Based on publicly available data

Shareholder Structure as at Dec. 31, 2010

Shareholder Structure as at Dec. 31, 2011

Shareholder Structure as at Dec. 31, 2012

Shareholder Structure since Sept. 17, 2013

M.M.Warburg & CO KGaA 16.48%

M.M.Warburg & CO KGaA 5.19%

B. Metzler seel. Sohn Co. Holding AG 16.48%

B. Metzler seel. Sohn Co. Holding AG 5.19%

Schaeffler Group 42.17%

Schaeffler Group 49.90%

Schaeffler Group 49.9%

Schaeffler Group 46.0%

Free Float 39.72%

Free Float 50.1%

Free Float 54.0%

Free Float 24.87%

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 22

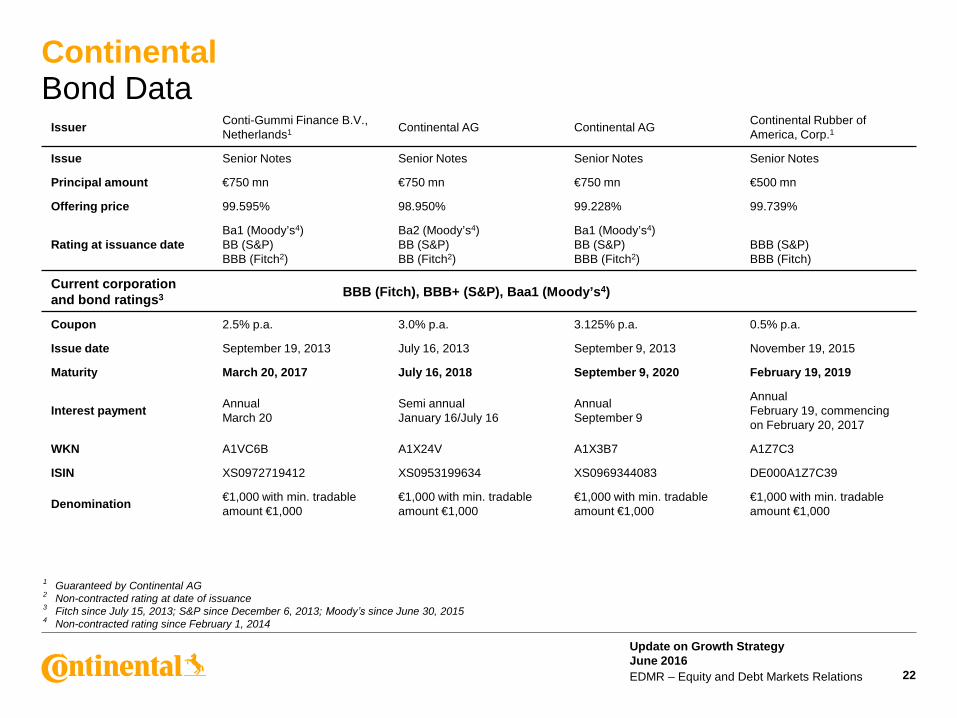

Continental Bond Data

Issuer Conti-Gummi Finance B.V., Netherlands1 Continental AG Continental AG Continental Rubber of

America, Corp.1

Issue Senior Notes Senior Notes Senior Notes Senior Notes

Principal amount €750 mn €750 mn €750 mn €500 mn

Offering price 99.595% 98.950% 99.228% 99.739%

Rating at issuance date Ba1 (Moody’s4) BB (S&P) BBB (Fitch2)

Ba2 (Moody’s4) BB (S&P) BB (Fitch2)

Ba1 (Moody’s4) BB (S&P) BBB (Fitch2)

BBB (S&P) BBB (Fitch)

Current corporation and bond ratings3 BBB (Fitch), BBB+ (S&P), Baa1 (Moody’s4)

Coupon 2.5% p.a. 3.0% p.a. 3.125% p.a. 0.5% p.a.

Issue date September 19, 2013 July 16, 2013 September 9, 2013 November 19, 2015

Maturity March 20, 2017 July 16, 2018 September 9, 2020 February 19, 2019

Interest payment Annual March 20

Semi annual January 16/July 16

Annual September 9

Annual February 19, commencing on February 20, 2017

WKN A1VC6B A1X24V A1X3B7 A1Z7C3

ISIN XS0972719412 XS0953199634 XS0969344083 DE000A1Z7C39

Denomination €1,000 with min. tradable amount €1,000

€1,000 with min. tradable amount €1,000

€1,000 with min. tradable amount €1,000

€1,000 with min. tradable amount €1,000

1 Guaranteed by Continental AG 2 Non-contracted rating at date of issuance 3 Fitch since July 15, 2013; S&P since December 6, 2013; Moodyʼs since June 30, 2015 4 Non-contracted rating since February 1, 2014

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 23

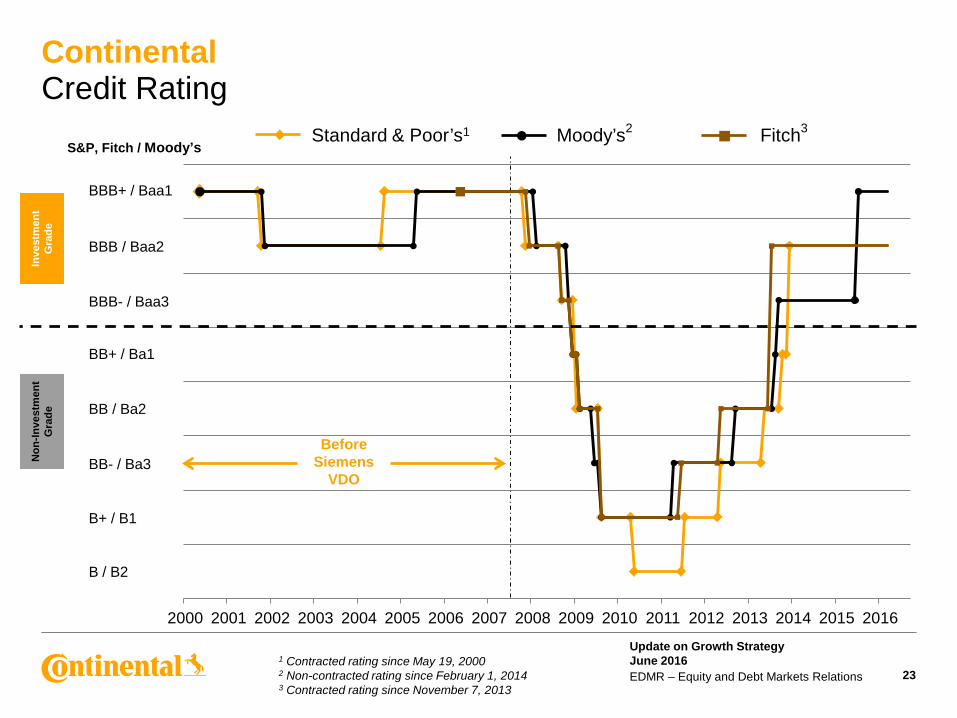

Continental Credit Rating

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BBB+ / Baa1

BBB / Baa2

BBB- / Baa3

BB+ / Ba1

BB / Ba2

BB- / Ba3

B+ / B1

B / B2

S&P, Fitch / Moody’s Standard & Poor’s1 Moody’s2 Fitch3

Before Siemens

VDO

Non

-Inve

stm

ent

Gra

de

Inve

stm

ent

Gra

de

1 Contracted rating since May 19, 2000 2 Non-contracted rating since February 1, 2014 3 Contracted rating since November 7, 2013

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 24

Continental Useful Links

Continental Investor Relations website http://www.continental-ir.com

Annual and interim reports http://www.continental-corporation.com/www/portal_com_en/themes/ir/financial_reports/

2015 Fact Book http://www.continental-corporation.com/www/portal_com_en/themes/ir/financial_reports/

Investor Relations events and presentations

http://www.continental-corporation.com/www/portal_com_en/themes/ir/events/

Sustainability at Continental (presentation and fact sheet for investors)

http://www.continental-ir.com

Corporate Social Responsibility http://www.continental-sustainability.com

Corporate Governance Principles http://www.continental-corporation.com/www/portal_com_en/themes/ir/corporate_governance/

Continental share http://www.continental-corporation.com/www/portal_com_en/themes/ir/share/

Continental bonds and rating http://www.continental-corporation.com/www/portal_com_en/themes/ir/bonds/

Continental IR mobile website http://continental.ir-portal.de

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 25

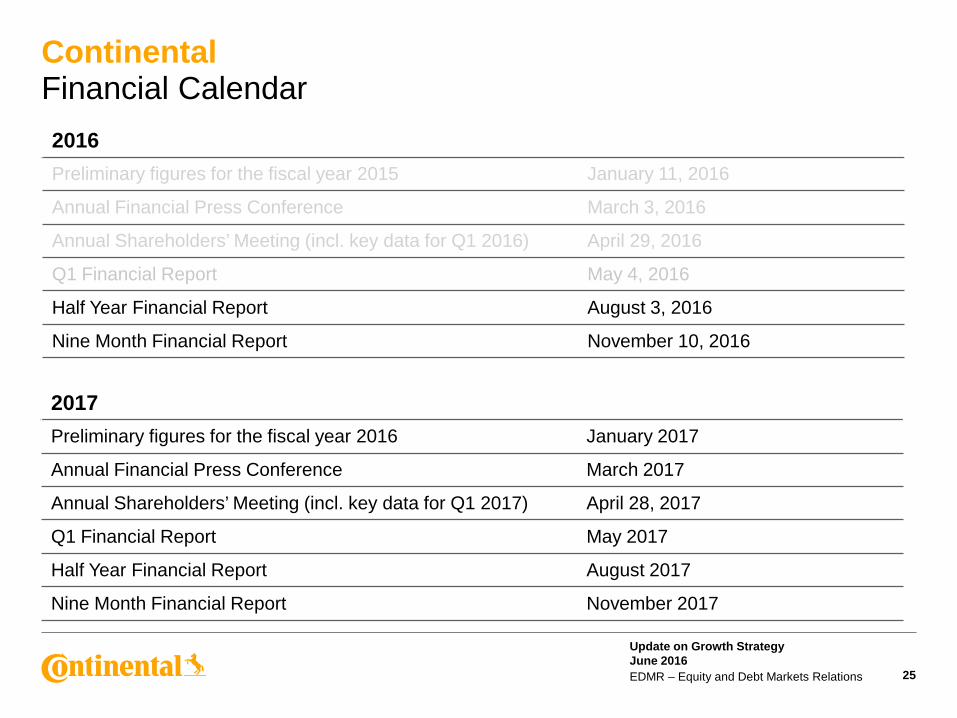

Continental Financial Calendar

2017 Preliminary figures for the fiscal year 2016 January 2017

Annual Financial Press Conference March 2017

Annual Shareholders’ Meeting (incl. key data for Q1 2017) April 28, 2017

Q1 Financial Report May 2017

Half Year Financial Report August 2017

Nine Month Financial Report November 2017

2016 Preliminary figures for the fiscal year 2015 January 11, 2016

Annual Financial Press Conference March 3, 2016

Annual Shareholders’ Meeting (incl. key data for Q1 2016) April 29, 2016

Q1 Financial Report May 4, 2016

Half Year Financial Report August 3, 2016

Nine Month Financial Report November 10, 2016

Update on Growth Strategy June 2016 EDMR – Equity and Debt Markets Relations 26

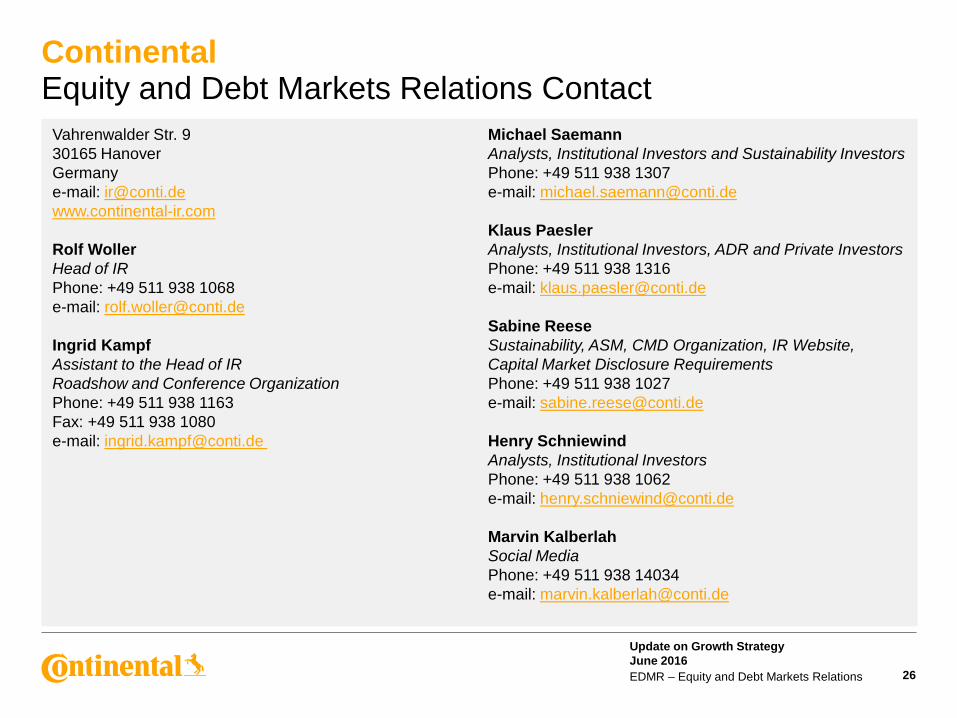

Continental Equity and Debt Markets Relations Contact

Vahrenwalder Str. 9 30165 Hanover Germany e-mail: [email protected] www.continental-ir.com Rolf Woller Head of IR Phone: +49 511 938 1068 e-mail: [email protected] Ingrid Kampf Assistant to the Head of IR Roadshow and Conference Organization Phone: +49 511 938 1163 Fax: +49 511 938 1080 e-mail: [email protected]

Michael Saemann Analysts, Institutional Investors and Sustainability Investors Phone: +49 511 938 1307 e-mail: [email protected] Klaus Paesler Analysts, Institutional Investors, ADR and Private Investors Phone: +49 511 938 1316 e-mail: [email protected] Sabine Reese Sustainability, ASM, CMD Organization, IR Website, Capital Market Disclosure Requirements Phone: +49 511 938 1027 e-mail: [email protected] Henry Schniewind Analysts, Institutional Investors Phone: +49 511 938 1062 e-mail: [email protected] Marvin Kalberlah Social Media Phone: +49 511 938 14034 e-mail: [email protected]