unv_coreport201115

20

PortfolioDirect/resources Resource sector portfolio construction for independent investors E.I.M. CAPITAL MANAGERS E.I.M. CAPITAL MANAGERS PTY LTD ABN 28 101 508 632 AFS Licence Number 261989 Update: 20 November 2015 Universal Coal PLC (UNV:AU) Rating Update This PortfolioDirect rating review is for the sole use of the PortfolioDirect/resources subscriber and subject to the terms and conditions relating to storage and distribution contained in the subscription agreement. This review of Universal Coal Limited has been prepared in accordance with the PortfolioDirect stock rating framework described on pages 2-4. PortfolioDirect/resources offers strategy and portfolio recommendations for independent investors. The rating framework has been developed to assist investors and their advisers to grade individual stock risk so as to better match stocks in their own portfolios with their personal risk profiles and to take account of the differing risk characteristics of potential investments when structuring their portfolios. A PortfolioDirect stock rating is not intended as a forecast of future share price movements. Share prices will be influenced by a range of factors including, significantly, macroeconomic conditions and the current cyclical positioning of the sector which are not taken into account in determining a stock rating. The PortfolioDirect analytical framework separates the view about market direction from the stock risk analysis contained in this review. The most important driver of a stock rating for a company being reviewed is an assessment whether the company to likely to meet its exploration and development targets within the timeframes sought by investment markets and, when development has occurred, its ability to maintain positive value momentum over future years. The Investment Decision Snapshot Commodity Exposure What is the mineral to which the company is principally exposed? Thermal coal for supply to the South African power utility Resource Quality How does the resource rank on the “GLOSS” rating scale? The company has been given an above average 3.5 grade on the 5 point resource quality rating scale Investment proposition Do investment returns depend on (i) a reduction in risk over the medium term, (ii) specific near term events or (iii) a future change in cyclical conditions? Investment returns will depend on directors being able to negotiate a competing bid for the company in response to the bid initiated by the company’s largest shareholder Risk profile How does the project rank on the PortfolioDirect risk rating scale? The company has been given a low risk score of 1.8 on the 5 point risk rating scale Portfolio positioning What roles could the company play in a portfolio? Are other companies able to fulfill these roles more effectively? The company’s commodity and geographic diversification and value driven upside has been superseded by the possibility of a maximum 32% near term trading gain from a takeover exit Liquidity How easily can buyers or sellers of the stock be accommodated? Liquidity is low which would preclude the company as an investment for many classes of investors

-

Upload

tony-wiggins -

Category

Documents

-

view

136 -

download

0

Transcript of unv_coreport201115

PortfolioDirect/resources Resource sector portfolio construction for independent investors

E.I.M. CAPITAL MANAGERS

E.I.M. CAPITAL MANAGERS PTY LTD ABN 28 101 508 632 AFS Licence Number 261989

Update: 20 November 2015

Universal Coal PLC (UNV:AU)

Rating Update

This PortfolioDirect rating review is for the sole use of the

PortfolioDirect/resources subscriber and subject to the

terms and conditions relating to storage and distribution

contained in the subscription agreement.

This review of Universal Coal Limited has been prepared in accordance with the PortfolioDirect stock rating framework described on pages 2-4.

PortfolioDirect/resources offers strategy and portfolio recommendations for independent investors. The rating framework has been developed to assist investors and their advisers to grade individual stock risk so as to better match stocks in their own portfolios with their personal risk profiles and to take account of the differing risk characteristics of potential investments when structuring their portfolios.

A PortfolioDirect stock rating is not intended as a forecast of future share price movements. Share prices will be influenced by a range of factors including, significantly, macroeconomic conditions and the current cyclical positioning of the sector which are not taken into account in determining a stock rating. The PortfolioDirect analytical framework separates the view about market direction from the stock risk analysis contained in this review.

The most important driver of a stock rating for a company being reviewed is an assessment whether the company to likely to meet its exploration and development targets within the timeframes sought by investment markets and, when development has occurred, its ability to maintain positive value momentum over future years.

The Investment Decision Snapshot

Commodity Exposure

What is the mineral to which the company is principally exposed?

Thermal coal for supply to the South African power utility

Resource Quality

How does the resource rank on the “GLOSS” rating scale?

The company has been given an above average 3.5 grade on the 5 point resource quality rating scale

Investment proposition

Do investment returns depend on (i) a reduction in risk over the medium term, (ii) specific near term events or (iii) a future change in cyclical conditions?

Investment returns will depend on directors being able to negotiate a competing bid for the company in response to the bid initiated by the company’s largest shareholder

Risk profile How does the project rank on the PortfolioDirect risk rating scale?

The company has been given a low risk score of 1.8 on the 5 point risk rating scale

Portfolio positioning

What roles could the company play in a portfolio? Are other companies able to fulfill these roles more effectively?

The company’s commodity and geographic diversification and value driven upside has been superseded by the possibility of a maximum 32% near term trading gain from a takeover exit

Liquidity How easily can buyers or sellers of the stock be accommodated?

Liquidity is low which would preclude the company as an investment for many classes of investors

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 2

Important Information Regarding the Preparation of this Report

This report is not intended as an offer or solicitation with respect to the purchase or sale of a security. Nothing in this report should be taken as a recommendation. Universal Coal has been rated without taking into account the particular objectives, financial circumstances or needs of any particular investor. Before taking any decision based on this communication, an investor should assess his or her own circumstances and seek professional advice.

This report is based on information disclosed publicly by Universal Coal at the date of the report, information otherwise available in the public domain at that time and analysis and technical inferences drawn by the staff of E.I.M. Capital Managers Pty Ltd, the publisher of PortfolioDirect.

Although the statements of fact in this report have been added from and are based upon sources E.I.M. Capital Managers believes to be reliable, their accuracy is not guaranteed and any such information may be incomplete or condensed. To the extent permitted by law, E.I.M. Capital Managers, its employees, consultants, advisers, officers and authorised representatives are not liable for any loss or damage arising as a result of reliance placed on the contents of this report.

All opinions and estimates in this communication, including the rating given to Universal Coal, constitute judgments by E.I.M. Capital Managers as at the report date and are subject to change without notice. The report publisher is under no obligation to make public any change in view about any matter referred to in this document.

E.I.M. Capital Managers may receive a fee in exchange for allowing Universal Coal to distribute this rating report in those jurisdictions in which it is lawful to do so and in accordance with any relevant laws or regulations. In the event Universal Coal (the company) has been given permission to use the report in this way, the company has agreed to remove the report from its website or cease any other form of distribution as soon as it is notified of a rating change or a more recent rating review has been prepared.

Universal Coal has not had an opportunity to comment on the report or request any amendments prior to its publication.

Trading in PortfolioDirect Rated Stocks by E.I.M. Capital Managers Stocks rated in accordance with the criteria outlined in this communication may be bought or sold by E.I.M. Capital Managers on behalf of clients or funds whose investments are managed by the firm. Specific investment objectives and individual portfolio considerations may result in transactions by E.I.M. Capital Managers that are not consistent with PortfolioDirect ratings for individual stocks.

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 3

Phase I: the exploration phase during which relatively small amounts of capital may be deployed with the prospect of a high return but when investors also risk losing all the funds subscribed prior to the company having an agreed development plan.

Phase II: the emerging production phase in which companies are able to demonstrate access to a commercial resource and add value by meeting key development milestones along an agreed development path.

Phase III: the phase of continuing operations in which organic volume growth is limited and commodity price movements become the dominant driver of earnings and value.

Phase IV: a period typically characterised by falling ore grades and rising costs requiring additional capital to prevent output contracting.

Stock Rating Criteria E.I.M. Capital Managers categorises sector investments based on the four phases in the life cycle of mining and oil and gas companies.

Phase I companies will be scored (on a five point scale) on their potential to confirm a commercially viable development within an acceptable investment market timeframe. The duration of the investment horizon might vary from time to time depending on market conditions but will usually extend to a period of up to 24 months. Judgements will be based on publicly available information, including clarifying conversations with company management, and the resulting geological inferences drawn by E.I.M. Capital Managers analysts.

Phase II companies will be scored on a five point scale on their capacity to deliver positive value momentum (i.e. the ability to generate increasing fundamental value over future years without any reliance on higher commodity prices).

Since Phase III companies, by definition, no longer have any material organic growth prospects, they will generally fail the ‘positive value momentum’ test. A Phase III company may still play an important portfolio role depending on its relative financial strength, its capacity to withstand periods of cyclical weakness due to the competitiveness of its cost structure and its potential, arising from a large resource base, to operate through multiple economic cycles. Phase III companies will be scored on a five point scale on their absolute value proposition and how they meet these additional criteria.

No inferences about share price performance should be drawn from the rating of an individual stock. Investment returns will be influenced by a range of factors, some of which are included among the PortfolioDirect rating criteria, as well as investment market expectations about a range of macroeconomic variables. The PortfolioDirect rating does not take account of macroeconomic or investment market conditions that play a role in setting the price levels of securities.

There may be points in the cycle when stocks assessed by PortfolioDirect as being relatively risky and given a relatively low score on the PortfolioDirect rating scale are capable of producing relatively strong investment returns. This may arise, for example, because of strong leverage to changes or expected changes in market conditions among stocks with unusually depressed share prices or very small current market values.

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 4

How does PortfolioDirect rate a Phase II company? The PortfolioDirect rating system scores a Phase II company on its underlying value, namely, whether the assessed asset value of the company exceeds its current market value and the extent (i.e. the size and duration) of future value uplift. The Phase II classification requires a company to have adopted a development plan that can be valued using conventional cash flow valuation techniques. Assessments of the value profile are made in a neutral commodity price setting.

The PortfolioDirect GLOSS quality rating and risk analysis feeds the discount rate used for valuation purposes.

QUALITY + RISK = PORTFOLIODIRECT RATING

Resource Quality "GLOSS" Rating (1)

0 2 4 6 8 10

Grade

Location

Orientation

Suitability

Size

PortfolioDirect assesses the quality of a mineral resource using its 5-point “GLOSS” rating.

GRADE using the best available in the industry as a benchmark for the highest rating

LOCATION whether a deposit is situated within an existing mineral province for which infrastructure currently exists

ORIENTATION usually the extent to which a mineral deposit can be characterised as Flat-Thick-Shallow or Dipping-Thin-Deep

SUITABILITY whether ore is suitable for processing by conventional industry practices or the extent to which a novel or unproven treatment process must be used

SIZE a measure of the life of a project with resources capable of sustaining a multi-decade operation receiving the highest rating

1. This graphic representation is for illustrative purposes only and does not represent the rating for any particular company.

What do we mean by ‘positive value momentum’?

Positive value momentum - the key criterion for judging Phase II companies - refers to an increase in value over 12 months, 18 months, etc without having to depend on a favourable change in macroeconomic conditions. The ideal company will have a value profile similar to that illustrated in the chart.

Positive value momentum will be a function of organic growth potential, duration to production, exploration potential (contributing to mine life extensions), lowered risk, reduced capi-tal spending and the capacity to withstand cyclical declines in raw

C ompany Va lue P rofile

0.00

2.00

4.00

6.00

8.00

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Shar

e Pr

ice

Value profi le

Current share pri ce

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 5

A Guide to the PortfolioDirect Rating Report Each PortfolioDirect company rating report addresses questions affecting business outcomes and potential investment standing under five separate headings. Primary Development Assets

n What are the most important geological or operational attributes of the company?

n Where are the assets located and what is the availability of local infrastructure? n What potential impact does location have on business outcomes? n How was ownership achieved - corporate exploration, acquisition or farm-in -

and what obligations remain to the vendors or partners? n Do historical outcomes on or near these exploration properties say anything

about likely mineral characteristics on the company’s own assets? n Are there identifiable technical issues that need addressing before further work

can be completed? Regulatory Standing

n What approvals have been received? n What additional approvals will be necessary to meet business goals? n Has the company been in breech of any regulatory requirements at this site or

elsewhere on any previous occasion? n Can the company show a commitment to environmental and social needs?

Project Potential

n What scale of development is anticipated or, if judgements about this cannot be made presently, what must happen before such a judgement can be made?

n What operational or market constraints might affect the project potential? n What is the likely range of project capital needs in the event of development?

Capacity to Meet Targets

n What skills does the company currently have available? n What additional or alternative skills will be needed for the next stage of

activities? n How does the track record of the existing management impact current

judgements about the capacity of the company to meet its targets? n What financial resources are currently available? Are they adequate for the

targets being set? n Are there unresolved technical, financial or regulatory matters that could impact

the achievement of business targets? Rating Discussion

n Into which development phase has the company been classified? n What are the key criteria against which the company is being benchmarked? n How does the company stand against the rating criteria for a company at this

stage of development? n Are there criteria which have been more or less important in coming to a rating

decision? n Are there matters which might affect the rating in the future? n Are there any special attributes displayed by the company that might impact on

its role in a portfolio? n How have historic investment returns affected judgements about current and

future market risk?

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 6

(This update should be read as part of the original rating report dated 12 November 2014 and subsequent updates which follow in this document.)

Recent Events What has happened to cause a review of the company’s PortfolioDirect rating? The company received an offer from its largest shareholder (Ichor Coal NV) to purchase all the shares it does not currently own for 16 cents per share placing a value on the company of A$80.9 million (ASX 21 August 2015).

An independent expert (KPMG) concluded that the proposed Ichor Coal purchase price was neither fair nor reasonable after having placed a value on the company of 26-34 cents a share (A$146.3-201.7 million) (ASX 20 October 2015).

Universal Coal directors have recommended that shareholders not accept the Ichor Coal bid in favour of an alternative cash offer of 25 cents sourced by the company but which remains incomplete and subject to further negotiation (ASX 2 & 13 November 2015).

What’s Different? How do recent events differ from prior expectations about what will drive company investment returns? The PortfolioDirect valuation prepared for its earlier rating reviews was consistent with the recent KPMG valuation being within the lower half of the range calculated by the independent expert.

Universal Coal investment returns were expected to come from a combination of a currently undervalued asset base and positive future value momentum through successful development of its South African coal projects. The Ichor Coal bid and the foreshadowed competing offer change the source and magnitude of potential returns.

Rating Impact What have been the key influences on a rating change? Directors will almost certainly recommend a bid at 25 cents if it is confirmed or, failing that, reluctantly engage with a strategically strengthened Ichor Coal to marginally raise its 16 cents bid price. Both alternatives are below the valuation underpinning the earlier PortfolioDirect ratings.

Without the existing and foreshadowed bids, there would have been no basis for changing the PortfolioDirect rating. However, neither bid will permit investors to benefit from the anticipated longer term development success. The PortfolioDirect valuation and the further investment upside from future positive value momentum, upon which the previous rating was based, are no longer feasible investment targets leading to a lowered PortfolioDirect rating.

Investment Consequences What is the impact of recent events on the investment prospects of the company and how investors should react? The company has been establishing itself as a niche low cost coal producer taking advantage of growing coal fired power use in South Africa. The company has met its previously foreshadowed targets for production and growth and, in doing so, has reduced its risk profile. It had offered a unique opportunity to diversify portfolios from a commodity perspective as well as geographically. Those characteristics would remain if the company could retain its independence.

The current market price of the company’s shares implies just a 35% chance that the foreshadowed improved offer will eventuate. This could be construed as too low given the explicit support for the alternative coming from directors. A bid at 25 cents per share now implies a 32% return. In the event the company is unable to consummate the foreshadowed transaction, investors face a downside risk to 16 cents, a potential loss of up to 16%.<

Company Rating Update Universal Coal PLC (UNV:AU)

NR 1 1+ 2 2+ 3 3+ 4 4+ 5

Resource Quality

Proj

ect R

isk

41 532

5432

Low High

Low

Hig

h

E.I.M. CAPITAL MANAGERS PortfolioDirect

Updated: 17 July 2015 7

Recent Events What has happened to cause a review of the company’s PortfolioDirect rating? The company has negotiated a A$55 million finance package that will cover the capital required for development of the New Clydesdale Colliery and allow the company to refinance the project debt used for the Kangala Colliery (ASX 22 June 2015).

The South African government approved the transfer of the mining right at New Clydesdale from the vendor to Universal Coal. The transfer approval will permit the recommissioning of the mine with a view to production commencing by the end of 2015 (ASX 2 July 2015).

The company confirmed that it had produced 712,000 tonnes ROM coal in the June 2015 quarter taking it to the targeted operational rate of 2.8Mtpa. The company’s cash flow statement for the quarter implied costs of $28/tonne of ROM coal (ASX 14 July 2015).

What’s Different? How do recent events differ from prior expectations about what will drive company investment returns? The finance arrangements confirm the ongoing mix between equity and debt making the cost of capital more certain than it had been and clarifying the resulting valuation of the company. The operating results and ministerial approval also confirm the company’s progress toward the targets it had set and on which investors can value the company.

Overall, recent events have not altered expectations but have highlighted the ongoing success of the company in reaching its stated development goals.

Rating Impact What have been the key influences on a rating change? The prior PortfolioDirect rating has been retained. As a Phase II company, a rating for Universal Coal depends on whether its project valuation exceeds the cost of an investment in the company and the extent to which the company can demonstrate positive value momentum in future years. Universal Coal meets the first valuation criterion and displays moderately positive value momentum based on the existing development plans.

At the time of the previous rating review, the company’s expansion opportunities were considered realistic and the track record of the management was judged to be sufficiently strong to permit an assumption that the foreshadowed development potential could be realised over an acceptable investment timeframe. The rating reflected these considerations.

Investment Consequences What is the impact of recent events on the investment prospects of the company and how investors should react? The company is establishing itself as a niche low cost coal producer taking advantage of growing coal fired power use in South Africa. Recent events are confirming the company’s ability to meet its previously foreshadowed targets for production and growth and, in doing so, have reduced the risk profile of the company.

The company’s positioning offers investors a unique opportunity to diversify their portfolios from a commodity perspective as well as geographically. Investors can use the company to retain an exposure to coal sales while bypassing the depressed international thermal and metallurgical coal markets. The company will be able to take advantage of more buoyant international coal market conditions, should they arise in the future, to rebalance sales between domestic and overseas markets depending on where sales offer the best returns.

Recent completion of the company’s debt funding arrangements will have removed a source of market risk for investors insofar as the necessity for a near term equity raising will have been reduced.<

Company Rating Update Universal Coal PLC (UNV:AU)

NR 1 1+ 2 2+ 3 3+ 4 4+ 5

Resource Quality

Proj

ect R

isk

41 532

5432

Low High

Low

Hig

h

E.I.M. CAPITAL MANAGERS PortfolioDirect

Updated: 24 April 2015 8

Recent Events What has happened to cause a review of the company’s PortfolioDirect rating? The company has reported upgraded resource estimates for a proposed integrated development of the Roodekop tenement and adjacent New Clydesdale Colliery on the southern margin of the Witbank coalfield in South Africa (ASX 13 April 2015). A 289% lift in proved and probable reserves to 40.75Mt is sufficient for a mine with an operating life of over 20 years.

Ministerial approvals are expected by the end of June 2015 and negotiations for long term sales contacts, initially for domestic customers, are “well advanced”, according to the company.

Confirmation that the Kangala operation had met completion tests in mid December has given the company access to operating cash flows making it easier to fund the balance of the New Clydesdale development costs with debt. The company had raised $24.5M through an October 2015 share placement.

The company has confirmed its intention to move to a further feasibility study into an underground development for export markets once full production is achieved.

What’s Different? How do recent events differ from prior expectations about what will drive company investment returns? The growth trajectory of the company is now better defined. The existing Kangala Mine is designed at 2.4Mtpa ROM coal for annual sales of between 1.8Mt and 2.1Mtpa. A staged development approach at the second development asset is set to double coal production within 12 months. Underground sources would lift company production to over 5 Mtpa ROM coal by 2017.

The newly confirmed production profile is higher than what had been included in the prior PortfolioDirect valuation lifting the assessed value of the company and adding positive value momentum through organically sourced growth in future years.

Rating Impact What have been the key influences on a rating change? The prior PortfolioDirect rating has been retained. As a Phase II company, a rating for Universal Coal depends on a project valuation exceeding the cost of an investment in the company and the company being able to demonstrate positive value momentum in future years.

The previous rating review had concluded that the prospective return from the Kangala property alone was below what would generally be regarded as acceptable but that expansion opportunities would underpin a higher return on the capital embedded in the business and justify an investment in the company.

The expansion opportunities were considered realistic and the track record of the management was judged to be sufficiently strong to permit an assumption that the potential could be realised over an acceptable investment timeframe. The rating reflected these considerations.

Investment Consequences What is the impact of recent events on the investment prospects of the company and how investors should react? The company is establishing itself as a niche low cost coal producer taking advantage of growing coal fired power use in South Africa. Recent events are confirming the company’s ability to meet its previously foreshadowed targets for production and growth.

The company’s positioning enables it to bypass the depressed international thermal and metallurgical coal markets which have stymied growth and profitability among other coal producers while providing investors with a unique opportunity to diversify their portfolios from a commodity perspective as well as geographically.<

Company Rating Update Universal Coal PLC (UNV:AU)

NR 1 1+ 2 2+ 3 3+ 4 4+ 5

E.I.M. CAPITAL MANAGERS PortfolioDirect

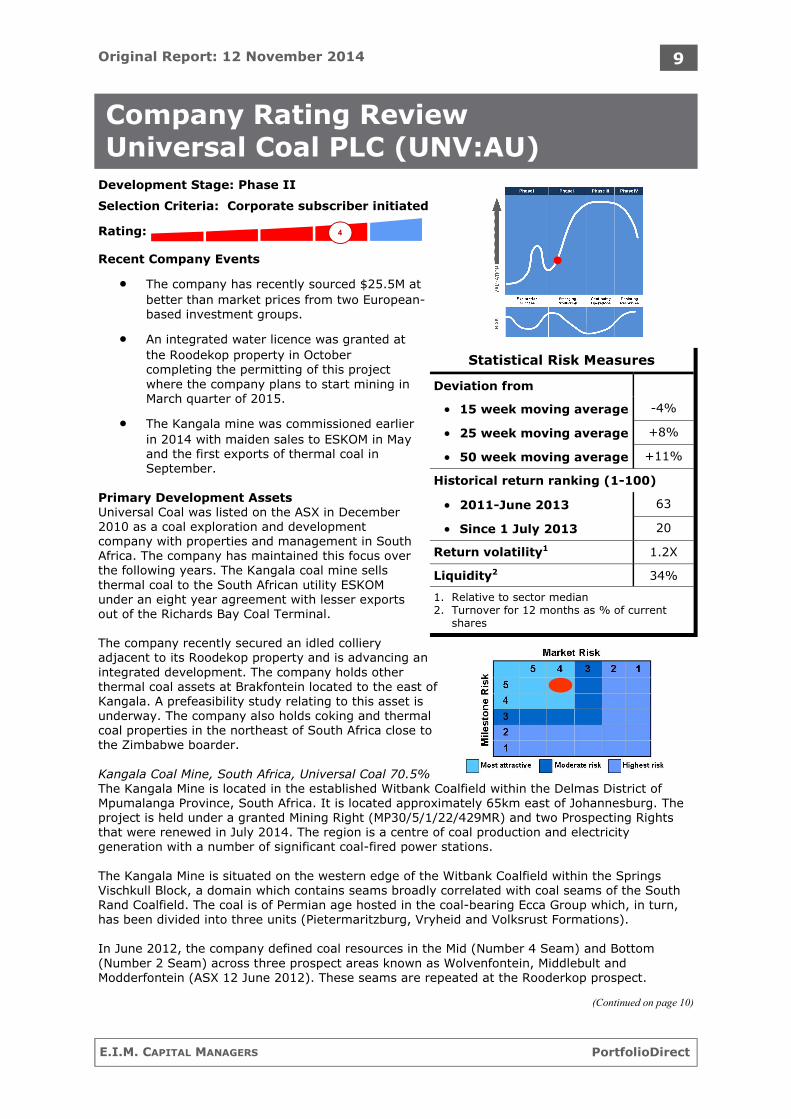

Original Report: 12 November 2014 9

Development Stage: Phase II

Selection Criteria: Corporate subscriber initiated

Rating:

Recent Company Events

• The company has recently sourced $25.5M at better than market prices from two European-based investment groups.

• An integrated water licence was granted at the Roodekop property in October completing the permitting of this project where the company plans to start mining in March quarter of 2015.

• The Kangala mine was commissioned earlier in 2014 with maiden sales to ESKOM in May and the first exports of thermal coal in September.

Primary Development Assets Universal Coal was listed on the ASX in December 2010 as a coal exploration and development company with properties and management in South Africa. The company has maintained this focus over the following years. The Kangala coal mine sells thermal coal to the South African utility ESKOM under an eight year agreement with lesser exports out of the Richards Bay Coal Terminal. The company recently secured an idled colliery adjacent to its Roodekop property and is advancing an integrated development. The company holds other thermal coal assets at Brakfontein located to the east of Kangala. A prefeasibility study relating to this asset is underway. The company also holds coking and thermal coal properties in the northeast of South Africa close to the Zimbabwe boarder. Kangala Coal Mine, South Africa, Universal Coal 70.5% The Kangala Mine is located in the established Witbank Coalfield within the Delmas District of Mpumalanga Province, South Africa. It is located approximately 65km east of Johannesburg. The project is held under a granted Mining Right (MP30/5/1/22/429MR) and two Prospecting Rights that were renewed in July 2014. The region is a centre of coal production and electricity generation with a number of significant coal-fired power stations. The Kangala Mine is situated on the western edge of the Witbank Coalfield within the Springs Vischkull Block, a domain which contains seams broadly correlated with coal seams of the South Rand Coalfield. The coal is of Permian age hosted in the coal-bearing Ecca Group which, in turn, has been divided into three units (Pietermaritzburg, Vryheid and Volksrust Formations). In June 2012, the company defined coal resources in the Mid (Number 4 Seam) and Bottom (Number 2 Seam) across three prospect areas known as Wolvenfontein, Middlebult and Modderfontein (ASX 12 June 2012). These seams are repeated at the Rooderkop prospect.

(Continued on page 10)

Company Rating Review Universal Coal PLC (UNV:AU)

Statistical Risk Measures

Deviation from

• 15 week moving average -4%

• 25 week moving average +8%

• 50 week moving average +11%

• 2011-June 2013 63

• Since 1 July 2013 20

Return volatility1 1.2X

Liquidity2 34%

1. Relative to sector median 2. Turnover for 12 months as % of current

shares

Historical return ranking (1-100)

4

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 10

The Mid Seam ranges from 0.98 to 3.75 metres in thickness containing bright to dull coal with high sulphur content. A minor parting occurs in places. The Bottom Seam ranges from 8.45 to 17.5 metres in thickness some 1.5 metres below the Mid Seam with four coal plies. The plies range from 0.5 metres to 8.6 metres in thickness offering some operational flexibility in terms of selective extraction. Coal exploration in the project area dates from over 30 years ago as established coal mining companies examined prospective areas on the margins of existing coal mining areas. The resource position at Kangala has not been updated to current reporting standards. The resource defined in the most recent annual report of the company is based on a June 2013 estimate revised for mine production (ASX 29 October 2014). Kangala Mine Coal Resource, 100% interest, June 2014, 2004 reporting guidelines Measured Resource 93.13 Mt Indicated Resource 19.35 Mt Inferred Resource 33.64 Mt Total 146.12 Mt The mine reserves shown in the most recent annual report of the company are reported according to current reserve reporting standards. The Kangala marketable reserve is divided into domestic thermal coal (62% average yield to product 20,16 MJ/kg) and export quality coal (27,25 MJ/kg). Kangala Mine Reserve, 100% interest, June 2014 Marketable Reserves Proved 22.288 Mt 14.515 Mt Probable - - Total 22.288 Mt 14.515 Mt The company presented a bankable feasibility study in April 2012 and announced an off take agreement with domestic thermal coal buyer Eskom (ASX 16 April 2012) which was documented in June (ASX 5 June 2012) and finalised in March 2013 following the commitment of mine finance (ASX 18 March 2013).The agreement covers 2.1Mtpa of 2.4 Mtpa ROM coal with a fixed price contract over eight years adjusted for inflation including a variable cost pass-through clause. The contract is renewable for a further eight year period with set initial coal delivery in April 2014. The company finalised an export sales agreement with Exxaro Coal the largest diversified Black Economic Empowerment (BEE) resources company in South Africa. Under the agreement, Universal Coal will supply up to 100,000tpa of export quality thermal coal from Kangala making road deliveries to the nearby Exxaro owned coal operation at Leeuwpan Mine. From a rail siding on that site coal is moved to the Richards Bay Coal Export Terminal where the company had obtained an annual export allocation of 51,000t. Universal Coal, which reported its first export shipment in September 2014, is seeking to increase the port allocation (ASX 22 July 2013, 24 September 2014). The coal is exported and marketed by Exxaro. The company has said it is assessing expansion opportunities at Kangala, utilising the resource base and installed plant capacity. Roodekop & New Clydesdale (Universal 74% Roodekop, 49% New Clydesdale) The Roodekop prospect is located in the Kriel region of Mpumalanga Province, South Africa, east of the Kangala operating mine. The area contains shallow defined resources of the same Permian age coal seams mined at Kangala. In addition to the Number 4 and Number 2 seams, the Number

(Continued from page 9)

(Continued on page 11)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 11

5 Seam separated by coarse grained sandstone has been developed. The Number 2 Seam has three plies for a collective thickness of 4.32 metres. The main seams have a collective thickness of 7-8 metres and extend over a strike of 4km with a broad width of 2km. The depth of cover to the Number 4 Seam is 12 metres. Resources have been estimated with a minimum thickness of 50cm using 117 cored vertical holes. Exploration at Roodekop dates from the early 1970s with historical drill results which match recent company work. The Roodekop resource sits adjacent to the New Clydesdale Colliery. The New Clydesdale Colliery is located 34km south of Emalahleni and is one of the oldest coal mines in South Africa. The mine commenced operations in 1949 and was placed on care and maintenance in December 2013. The mine is fully equipped with machinery and is able to operate three separate underground sections. The site has established road and rail infrastructure with a private rail connection with Transnet Freight Rail allowing direct export shipments. Historically, the mine produced 0.7-1.5Mtpa of export quality thermal coal from underground and open pit sources. The installed coal processing plant has a rated capacity of 2Mtpa ROM coal. Prior to being placed on care and maintenance, the mine was focused on resources in the Diepspruit area which is contiguous with the Roodekop resource held by Universal Coal. The company has outlined a number of synergies between the two resource positions including reduced pre-production development costs for Roodekop by drawing on existing coal processing plant and export infrastructure. The company also expects reduced operating costs with integrated overhead costs. In February 2014, the company announced the acquisition of the New Clydesdale Colliery from Exxaro Resources (with BEE group Ndalamo Resources retaining 51%) noting at that stage an operating life of 15 years with eight being open cut. Subsequent materials showed the asset cost $17M cash (ASX 3 February, 20 October 2014). The resource inventory at New Clydesdale dates from December 2012 and is currently the subject of a review by Universal Coal leading to a new mine design. The asset contains a resource of 54.5Mt with a reserve of 3.5Mt. The reserve estimation employed a minimum seam thickness of 1.5 metres and underground mine extraction factors. The product was defined as a 28 MJ/kg export thermal coal with 13-14% ash and 25.8% volatile matter. Recent company presentation materials outline a potential redevelopment of New Clydesdale with pre-production capital costs of $23M (100%) to be met by debt and offtake financing. The company plans initial mining activity in the March quarter of 2015. A restart of underground mining is planned for the second half of 2015. Some refitting of existing equipment will be required (ASX 20 October 2014). Universal Coal published a maiden reserve for Roodekop in March 2014 in line with current reporting standards (ASX 10 March 2014). The reserve statement shows three product specifications: a RB1 specification export thermal coal (product yield 21% to 27 MJ/kg product with 14% ash), a low phosphorus metallurgical coal (yield 16% to 26.4 MJ/kg with 17.5% ash, 0.007% P) and an ESKOM coal (31% product yield to 20.5 MJ/kg product with 15.8% ash). Roodekop Resource, 100%, March 2014 Measured 82.92 Mt Indicated 1.44 Mt Inferred - Total 84.36 Mt Universal Coal share 62.42 Mt Roodekop Reserve, 100%, March 2014 Proven 9.4 Mt Probable - Total 10.6 Mt

(Continued from page 10)

(Continued on page 12)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 12

New Clydesdale Resource, 100%, from 2012 as reported at acquisition Measured 31.24 Mt Indicated 23.3 Mt Inferred - Total 54.5 Mt The New Clydesdale resources were based on a range of seams (Seam 5, Seam 4 (upper and lower), Seam 2 (t, s and a) and Seam 1). New Clydesdale Reserve, 100%, from 2012 as reported at acquisition Proven 3.5 Mt Probable - Total 3.5 Mt Brakfontein 50.3% Universal Coal The Brakfontein asset is held under Prospecting Right MP30/5/1/1/2/1879PR and covers 879 hectares. The company has the right to negotiate its equity in the asset to 74%. The project is located approximately 25km from the Kangala mine (with sealed road access). The resource could be developed as a satellite to Kangala or as a stand lone operation with coal trucked to Kangala. The company expects to complete a feasibility study in 2015 (ASX 29 October 2014). Brakfontein resources are presented in the 2014 Annual Report of the company. Brakfontein Resource, 100%, October 2014 Measured 70.5 Mt Indicated 15.0 Mt Inferred 2.2 Mt Total 87.7 Mt Universal Coal share 44.1 M Coking Coal Assets The Berenice-Cygnus prospect is located in the Soutpansberg Coalfield 90km southwest of Musina in northern South Africa. The company has a 50% holding in the Berenice prospect with an option to acquire a further 24% interest. The project sits close to the Zimbabwe border and an existing rail line some 20km away. The company has defined a resource base in this area but has focused on its thermal coal assets in the Witbank field. The Berenice resource is the largest of the northern coking coal resource positions. The resource is highlighted as an “option on a massive, shallow coking coal project” in a recent company presentation (ASX 20 October 2014). Earlier scoping studies had appraised a large mine with an annual production rate of 10Mtpa. Berenice Resource, 100%, October 2014, based on 2004 reporting guidelines Measured 393.97 Mt Indicated 694.27 Mt Inferred 116,070 Mt Total 1,204.31 Mt Universal Coal share 602.16 M Regulatory Standing The Kangala Mine operates on a granted Mining Right. Universal Coal has been granted a Mining Right over its Roodekop resource. In addition to the Mining Right, Universal has been granted a Water Licence (October 2014) and a National Environmental Management Act (NEMA) Authorisation. Following the acquisition of the New Clydesdale asset, the company sought a Section 11 authorisation relating to a transfer of ownership. The acquisition of the New Clydesdale mine has received approval from the South African Competition Commission. Universal Coal has made a Section 102 application to consolidate its New Clydesdale and Roodekop mining rights and this application is expected to be granted in the December quarter of 2014. The company secured National Environmental Management Act (NEMA) Authorisation and a

(Continued from page 11)

(Continued on page 13)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 13

Mining Right for its Brakfontein area in August 2014 (ASX 21 August 2014). An application for an Integrated Water Licence has been sought which would complete permitting for the site. Project Potential Kangala The Kangala mine was the subject of a bankable feasibility study in April 2012 (ASX 16 April 2012), an off take agreement with ESKOM and subsequent mine development. The study outlined a mine operating at a rate of 2.4Mtpa ROM over an initial eight year period producing 2.1Mtpa of saleable product. The study noted a significant resource base in the area offering the potential to expand both the scope of operations and the mine life to over 16 years. The resource position has grown since this time (124Mt to 146.12Mt resources). The company outlined a pre-production development cost of $50M with ongoing operating costs of $13.5/t ROM coal. The study showed an anticipated annual EBITDA of A$15M (100% interest). In recent presentation materials, the mine life has been extended to 9.5 years (from a single pit) with scope to develop a second pit of similar scope (ASX 20 October 2014). Operating costs over the life of the mine are expected to average A$15/t. Project returns can be enhanced through potential expansions of the mine (given the installed capacity) either from further development of the Kangala resource or by trucking from Brakfontein which contains a resource of similar quality coal. Roodekop-New Clydesdale In early October 2014, Universal Coal committed to the development of a second mine at Roodekop following the receipt of an Integrated Water Licence, the announcement of further funding and the advancement of the acquisition of the New Clydesdale Colliery. A review of the New Clydesdale resources and a refinement of mine development plans are underway. In a recent presentation, the company outlined a development cost of $23M covering the works at Roodekop ($8.3M), environmental guarantees ($5.3M) and redevelopment costs for the New Clydesdale mine including refurbishment of existing plant and mining equipment (ASX 20 October 2014). The same presentation noted that the combined Roodekop-New Clydesdale complex has a production potential of 2Mtpa Rom two thirds of which would be fed from open cut and one third from underground sources. The primary product would be 6,000 kcal export quality thermal coal with lesser quantities of ESKOM quality material and low phosphor metallurgical coal (as noted in Roodekop resource statement). There is a resource base equivalent to at least 20 years of operations with at least five years from the two thickest underground seams. The company is yet to provide a detailed financial analysis of the mine with debt financing, final permitting and port access still outstanding requirements leading to mining. Capacity to Meet Targets The company has an appropriately experienced and qualified management team. Managing Director Mr. Tony Weber is a mining engineer and experienced company director. As a coal industry executive he has been involved with coal mine developments in South Africa. He is supported by other experienced coal mining executives Mr. Kevin Donaldson (Chief Development Engineer), Mr. Jaco Malan (Chief Geologist), Mr. Daryl Edwards (Chief Financial Officer), Ms Mnah Moabi (Chief Environmental Manager) and Mr. Shammy Luvhengo (Business Development Manager). The company has demonstrated a clear capability in dealing with the administration and management of its coal permits. It has obtained mining licences with relevant water and environmental permits. The company’s achievements in this area put it well ahead of others who have sought to participate in the South African industry. At a commercial level, in addition to securing new development properties such as the New Clydesdale asset, the company has advanced sales agreements for thermal coal to the key South

(Continued from page 12)

(Continued on page 14)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 14

African utility ESKOM to the point of coal delivery. Company executives have demonstrated exploration capability through the completion of a detailed infill drilling program leading to high confidence resource estimates and mine reserves. The company has demonstrated a capacity to undertake the various feasibility studies aimed at de-risking the financial and technical parameters of its projects. This is evident at Kangala which is now an operating mine. Optimisation work is underway at New Clydesdale relating to both the integration of an existing resource base at Roodekop and the redesign of the proposed underground mine. The first mining activity at Kangala took place in July 2013 with initial work on a box cut. First production was planned for February 2014 in anticipation of the first ESKOM delivery (ASX 23 October 2013). ESKOM subsequently requested a higher specification coal. Universal Coal amended its design for the Kangala coal handling and processing plant to accommodate this request. It lifted the plant capacity from 2.4Mtpa to 4.2Mtpa and doubled the stockpile design to 60,000t. Despite these changes, the mine development was delivered within its budget. The company announced first coal dispatches in April with first receipts from ESKOM in May (ASX 7 April, 5 May 2014). The initial phase of production has been based on production from a single box cut (which limits operational efficiency) with ongoing waste stripping costs and stockpile build activity. Operational improvements can be expected after this initial phase of mine development. The following operational statistics map this initial production phase. Volume March Quarter June Quarter September quarter Run of mine production 471,710 580,007 Feed to plant 385,476 505,662 Plant yield 100% 72% Domestic sales 375,333 342,933 Export sales - 182 For the September quarter, the company reported sales revenues of $12.16M with net operating cash flows of A$3.5M (ASX 15 October 2014). The company reported positive operational cash flows of $9.6M for the first six months of the operating life of the mine implying cash costs very close to the targeted $15/t. A higher rate of operating cash flow has been forecast for the first half of 2015. In September 2012, the company had announced a finance package with South African FirstRand Bank Limited following a tender process. The company secured senior debt of $31M with a term of 6.5 years from drawdown. In October 2014, the company announced that it had received $25.5M of new funds from two European-based coal investment entities. Frankfurt exchange listed coal company IchorCoal which has investments in several South African coal operations made a combined investment of $24.5M in the form of a placement of ordinary shares at 14.5c ($11.7) with the balance in convertible preference shares priced at 18c. The investment also included a subscription for 71.22M 18 month warrants with a strike price of 36c. Existing shareholder Coal Development Holding BV participated in a placement of ordinary shares at 16c (raising $1M) and converted an existing holding of loan notes into ordinary shares. The company had previously raised $13.6M through an equity placement to Coal Development Holding BV in late 2012 (ASX 31 December 2012). Both recent subscription agreements were announced in September (ASX 2 September 2014) and ratified at a general meeting of shareholders in October (ASX 16 October 2014). The capital raisings were completed at a significant premium to the market price of the company (60%) with proceeds to be primarily directed to completing the acquisition of the New Clydesdale asset.

(Continued from page 13)

(Continued on page 15)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 15

Two representatives from IchorCoal joined the board of Universal Coal. At the completion of the raising, Coal Development Holding BV held 29.48% of the ordinary shares of the company and IchorCoal held 18.51% (ASX 20 October 2014). At the end of September, the company held cash of $3.75M with $25.5M in new funds due from capital raising initiatives undertaken in October. The company had drawn debt facilities of $34.17M related to the development of the Kangala Mine. Key steps for the company moving forward will be to achieve steady state production at the Kangala mine of 2.4Mtpa Rom with 1.8Mtpa of saleable coal of which 1.7Mtpa will be for the domestic power utility. The company has set a target of first mine production from open cut sources at the New Clydesdale Colliery in the March quarter of 2015 (with saleable coal in the June quarter) and commencement of underground operations later in the year. The history of the company to date would suggest that these targets are within its capacity. Rating Discussion Universal Coal has been classified as a Phase II company. The key determinant of a rating for a Phase II company is the extent (i.e. the size and duration) of future value uplift. Any value uplift will be a consequence, usually, of some combination of organic growth, operational improvement, lower capital needs and a falling discount rate as project risk is reduced through the development cycle. With pre-production capital spending behind it, a company’s value profile would normally build with higher output. These assessments of the value profile are made in a neutral commodity price environment. Where current commodity prices are significantly above underlying industry costs, a lower price (at or nearer the marginal costs of production) will be assumed so as to measure the value proposition. This works against companies operating at the upper end of industry cost curves and favours those with the lowest cost outcomes. The rating analysis for a Phase II company boils down to the responses to two questions: is the company currently cheap on a cash flow valuation basis and will the valuation rise in the coming years. The rise in future valuation is critical to a rating because it signifies positive momentum whatever implied discount rate an investor might be using currently to value the company. The current A$42 million market value of the company is marginally below the PortfolioDirect assessed value of the future income stream using the standardised PortfolioDirect valuation model. As always, such valuations assume (erroneously) that all equity investors have the same risk tolerance and investment return target. The anticipated cash flows from the Kangala project as it is currently specified imply a return equivalent to a 10 year bond with a yield of approximately 7%. Looked at this way, investors are better able to asses whether the company can produce a return which adequately accounts for risk and is consistent with their own investment goals. This return is generally below the minimum PortfolioDirect would regard as acceptable from a resource sector investment but there are two mitigating factors in favour of the Universal Coal position. Firstly, Universal Coal is less exposed to international market conditions than the typical development company with consequently less downside risk to its future income flows as a result of adverse price movements or shifts in the quantity of coal being bought. Secondly, the company has plans to expand the capacity of the existing operation. Moves to fill the spare capacity from further resource development at Kangala or Brakfontein would boost the earnings capacity and require only modest incremental development capital. Company initiatives at Roodekop and New Clydesdale are pointing to the potential for further value momentum in future years. There appears to be considerable flexibly in terms of the configuration of the combined Roodekop-New Clydesdale operation. These are relatively low capital and operating cost opportunities which will enable the company to produce a higher quality coal than its current output from Kangala.

(Continued from page 14)

(Continued on page 16)

E.I.M. CAPITAL MANAGERS PortfolioDirect

Original Report: 12 November 2014 16

For most classes of investor, the return from current operations would not be adequate and there would be little basis for expecting a significant price re-rating in the absence of a change in market conditions. The rationale for a Universal Coal investment - and what will underpin a higher return on the capital embedded in the business - rests on realising the future expansion opportunities. The PortfolioDirect rating implies that these expansion opportunities are realistic and that the track record of the management is sufficiently strong to permit an assumption that the potential can be realised over an acceptable investment timeframe. n

(Continued from page 15)

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 17

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 18

Significant Investment Risks In addition to general equity market risks reflecting unexpected changes in global economic or political conditions, investors in the resources sector may incur further risks specific to investments in the sector.

Commodity market risk: Resources sector investment returns are generally more volatile than returns from other equity market sectors due to the earnings of resources companies being exposed to commodity price and foreign exchange movements. Commodity prices can be influenced by a range of factors including economic events, which might affect the volume of commodities used, monetary policies which might affect levels of speculation and changes in output reflecting levels of industry exploration, investment and production disruptions.

Operational risk: Companies may fail to meet their development goals as a result of unexpected external influences, including political conditions and natural phenomena, as well as the skill base and operational capabilities of company management. Companies engaged in exploration activities may fail to locate or define mineral deposits of a sufficient size to be commercially viable.

Funding risk: Since companies in the resources sector require ongoing funding for development, expansion and maintenance of output, changes in financial market conditions can affect the value of investments adversely through the cost or availability of capital.

Regulatory risk: The value of investments in the sector may be affected adversely by changes in government policies relating to the conditions under which mine developments are permitted, including the need for more stringent environmental controls, higher taxation or royalty rates or requirements for local equity participation.

Small companies risk: Small or early stage companies generally have less diversified income streams, less stable funding sources and weaker bargaining positions with their counterparties than larger companies. The securities of small companies may also be less liquid than those of larger companies making the purchase or sale of securities more difficult or costly to complete, possibly with an adverse impact on portfolio performance.

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 19

Abbreviations and Symbols lb pound cif cost, insurance and freight

oz troy ounce fob free on board

Koz 1,000 troy ounces fot free on truck

Mlbs million pounds g/t grams per tonne

kg kilogram ppm parts per million

t tonne RC reverse circulation

kt 1,000 tonnes RAB rotary air blast

Mt 1,000,000 tonnes U3O8 yellowcake (uranium)

Mtpa million tonnes per annum Fe/FeO iron/iron ore

kL kilolitre (1,000 litres) SiO2 silica

ML megalitre (one million litres) Al2O3 alumina

GL gigalitre (one billion litres) P phosphorus

ha hectare TiO2 titanium dioxide

m metre ZrO2 zirconium dioxide

m3 cubic metre LOI loss on ignition

km kilometre mg/l milligrams per litre

A$ Australian dollar Mj/kg mega joules per kilogram

$M million dollars EBITDA earnings before interest, tax, depreciation & amortisation

US$ United States dollar EBIT earnings before interest & tax

MG/GW megawatt/gigawatt ROM run of mine

ct carat LOM life of mine

bbl barrel MOU memorandum of understanding

mbd million barrels a day VTEM Versatile Time Domain Electromagnetic

MBOE million barrels of oil equivalent

E.I.M. CAPITAL MANAGERS PortfolioDirect

20 November 2015 20

PortfolioDirect/resources

Publisher E.I.M. Capital Managers

Chief Investment Strategist John A Robertson [email protected]

Head of Stock Research Tony Wiggins [email protected]

Joint Portfolio Manager Doug Goodall [email protected]

Technical Advisers See www.eimcapital.com.au/advcttee.htm

Information about PortfolioDirect www.portfoliodirect.com.au

Rating updates & market commentary www.eimcapital.com.au/PortfolioDirect/daily_views.htm