Unleashing High Impact Sales Enablement · A value proposition that underscores how the bank is...

25

Unleashing High Impact Sales Enablement Presented by: Joanne Pollitt Principal Executive Advisor: CEB, now Gartner

Transcript of Unleashing High Impact Sales Enablement · A value proposition that underscores how the bank is...

Unleashing High Impact Sales Enablement

Presented by: Joanne Pollitt

Principal Executive Advisor: CEB, now Gartner

Unleashing High Impact Sales Enablement

The Unexpected Support That Best Drives Revenue

SURVEY DEMOGRAPHICS

Responses by Region, Percentage of Respondents

10%

22%

59%

9%

APAC

EMEA

North America

Latin America

15%

35%27%

7%

16%Analyst/Entry Level

Mid-Manager Level

Executive SeniorLevel

Executive Head ofBusiness Function

Head of Line ofBusiness

Responses by Seniority Level, Percentage of Respondents

N = 88.Source: CEB 2018 Commercial Banking Agenda Poll.

2018 COMMERCIAL BANK EXECUTIVE PRIORITIES

1. Delivering on

customer

expectations around products

2. Reducing points

of friction in

buying and service

3. Getting more

operating

efficiency from sales coverage

of commercial banking

executives expect to be

most concerned with growth through new

customers.

28%will focus on

operational efficiency

Three Business

Objectives

Top Concerns

50% 35%

33%

24%

8%

Technology and Products

(35%) will change the most.

Customer Experience

(33%)and Sales Model

(24%)are also expected to

change.

Talent Management (8%) will change the least.

Anticipated

Changes

TOP ECONOMIC CONCERNS

N = 88.Source: CEB 2018 Commercial Banking Agenda Poll.

50%

20%

28%

1%

Growth through NewCustomers

Growth throughExisting Customers

Lower Expensesthrough ImprovedOperational Efficiency

Lower Expensesthrough Cost Cutting

Top Economic Concerns for 2018, Percentage of RespondentsQ: What do you expect your business line’s top economic concern to be for 2018?

CRITICAL OBJECTIVES, BY BUSINESS LINE

N = 88.Source: CEB 2018 Commercial Banking Agenda Poll.

Critical Area Small Business Business Banking Middle Market

Mapping changing customer channel usage and expectations

72% 73% 72%

47% 48% 51%

Pinpointing how the bank can influence customer purchasing

in sales interactions

72% 68% 67%

51% 53% 56%

Utilizing tech partnerships and APIS to transform customer

experience

81% 75% 70%

60% 58% 44%

Scaling Bank supports for RMcustomer quality interactions

79% 78% 72%

49% 52% 56%

Removing RMs’ administrative and compliance burdens

72% 77% 67%

33% 40% 37%

Importance Confidence in Execution

CAN’T JUST HIRE MORE

38%

55% 54%52%

0%

10%

20%

30%

40%

50%

60%

0-2 Years 3-5 Years 6-10 Years More than10 Years

Percentage of RMs Whose Loan Generation is Greater Than the Bank MedianBy Tenure in Seat, North America

Average RM TenureMedian Number of Years in Current Role at Current Bank

2010 20140

3

65 Years

3 Years

N = 1,129.Source: CEB 2014 Sales Force Assessment.

N = 2,884 RMs (2010); 2,702 RMs (2014).Source: CEB 2010 and 2014 Sales Force Assessment.

CAN’T JUST WORK MORE

How Has Time Spent on Non-Client-Facing Work Changed in the Past Two Years?Percent of RMs Responding

Magnitude of Increase in RM Time Spent on Non-Client Facing Work Percent of RMs Responding, Among Those Who Reported an Increase

0%

50%

100%

0%

50%

100%

18%

69%

13%

Less than 20%

20%–50% Increase

Above 50% Increase

22.2% No Change

18.4% Decreased

52.9% Increased

N = 890, 507Source: CEB 2017 RM Sales Environment Readiness Assessment.

“We’ve been doing really well, but we’re like the duck on the water: it looks calm on the surface, but under the

water the feet are moving like crazy.”

Head of Sales Force,

North American Commercial Bank

ALL IN FOR TECHNOLOGY ENABLEMENT

Banks Making Investments in Sales Enablement Technology Now, by Type of TechnologyCommercial Banking Only, Global

0% 50% 100%

56% 35% 9%

54% 42% 4%

53% 42% 5%

52% 37% 11%

52% 42% 6%

51% 40% 9%

51% 38% 11%

50% 42% 8%Sales Content Management

Predictive Lead Analytics

Sales Intelligence

Sales Prospecting

Coaching Tools

Performance Management

Pricing, Configuration, and

Quoting Tools

Pipeline Management, and Forecasting

Making Major Investments/ Replacements Now

Have It, No Planned Change

Not Investing/ Unsure

“We view technology as an enabler, but it isn’t solving the root cause problem – which is a broken sales

process.”Group Vice President, North American Commercial Bank

N = 259.Source: CEB 2017 Financial Services Technology SurveyNote: Total does not equal 100% due to rounding.

CURRENT TOOLS DON’T HELP WITH OUTCOMES

63%

77% 77%

67%

46%

62%58%

66%

CRM Pricing Tools PipelineManagement

Sales Prospecting

Understand Customers Manage the Sales Process

Extent that Tools Fail to Help RMs Better Understand Customers or Manage the Sales Process More EffectivelyPercentage of RMs Neutral or Not Agreeing that the Tool Helps Them

N = 1,269.Source: CEB 2016 Sales Environment Readiness Assessment Survey

UNDERSTANDING SALES ENABLEMENT

50+ questions on team composition,

performance, tools and technology,

enablement supports, sales process,

culture.

24 Institutions

335 Sales Managers

1,651 Relationship Managers

1. Sales Environment Readiness Assessment

2. Qualitative Interviews

45-minute interviews with executives at 26 institutions across all business lines to understand their sales enablement strategies and challenges

Source: CEB Analysis

NEW MANDATE: ENABLE YOUR SALES FORCE

Executives’ Three Approaches to Sales Enablement

Talent Supports Process SupportsCustomer Interaction

Supports

Goal: Hire and Manage Talent

■ Hiring

■ Training

■ Coaching/

■ Incentives

■ Customer-Facing Time

■ Usable CRM

■ Customer Segmentation

■ Market Coverage

■ Leads Identification

■ Sales Process

■ Internal Collaboration

■ Specialists

■ Ethical Sales Culture

■ Commercial Insights

■ Customer

Needs

Understanding

■ Value Proposition

■ Relevant Messaging

■ Differentiated Products

■ Customer Accountability

■ Sales Discretion

Goal: Make Bankers More Efficient

Goal: Fulfill Customer Needs

Source: CEB Analysis

PROCESS AND TALENT ARE THE BIG BETS

Sales Enablement Strategy Prioritization, by Enablement ApproachPercentage of Initiatives, Among Total Initiatives in Sample

Customer Interaction Supports: 18%

Talent Supports: 39%

“We want leaders to focus more on coaching.”

“We are constantly training our people.”

“We’re trying to get new bankers ramped up faster.”

Process Supports: 43%“We’re trying to remove bureaucracy from RMs’ days and save them time.”“Our top priorities are getting a new CRM and improving lead generation capabilities.”

N= 26 InstitutionsSource: CEB Analysis; 2017 Research Interviews with Commercial Banking Executives

WHAT MATTERS MOST

Relative Impact of Improving Sales Enablement Approaches on RM Revenue Goal Achieved Percentage Point Change in RM Revenue Goal Achieved When RMs’ Perception of Bank Effectiveness Increases

N= 962Source: CEB 2017 Sales Environment Readiness Assessment

22.6%

11.0%

Improving Customer Interaction Supports

Improving Customer InteractionSupports

and Process Supports

The results of all other scenarios tested were not statistically significant.

CUSTOMERS WANT OUTCOMES

Traditional Overlap Between What Customers Valued and What Banks Offered

Source: CEB Analysis

Aligned Around Access

Current Disconnect Between What Customers Expect and What Banks Still Offer

Customers Valued: Access

■ Access to local knowledge■ Access to staff who could provide

reliable service support and match

needs to products

■ Access to financing

Banks Offered: Access

■ Access to local staff■ Access to RMs who could offer

reliable service, diagnose needs,

and provide solutions

■ Access to the balance sheet

Disconnect: Outcomes Versus Access

Banks Still Offer:

Access

■ Access to local staff■ Access to RMs who can

offer reliable service,

diagnose needs, and

provide solutions

■ Access to the balance

sheet

Customers Value:

Outcomes

■ Relevant and timely

information to drive

business outcomes

■ On-demand availability to

ensure timely business

outcomes

■ Access to financing on

their terms to deliver

business outcomes

INTERACTION SUPPORTS HELP DRIVE OUTCOMES

How Customer Interaction Supports Help RMs Drive Clients’ Business Outcomes

Source: CEB Analysis

+ +1. Guidance to

Understand Customer

Needs

Key Components of

Support to RMs:

■ A clear understanding of

customers’ basic needs.

■ A value proposition that

underscores how the bank is

uniquely positioned to help

customers achieve business

outcomes.

2. Unique Insight and

Products to Deliver

to Clients

Key Components of

Support to RMs:

■ Commercial insights that

help achieve customers’

business outcomes.

■ Useful messaging or

collateral that can be used

with customers.

■ Differentiated products and

services that help customers

achieve their business

outcomes in ways other

banks cannot.

3. Discretion—and

Accountability—to Tailor the

Interaction to the Client

Key Components of

Support to RMs:

■ Significant discretion on how

to sell.

■ Accountability for ensuring

customers receive the most

appropriate products and

services to meet their needs.

What RMs Need to Help Customers Achieve Outcomes

A NEW GOAL

Executives’ Three Approaches to Sales Enablement

Talent Supports Process SupportsCustomer Interaction

Supports

Goal: Hire and Manage Talent

■ Hiring

■ Training

■ Coaching/

■ Incentives

■ Customer-Facing Time

■ Usable CRM

■ Customer Segmentation

■ Market Coverage

■ Leads Identification

■ Sales Process

■ Internal Collaboration

■ Specialists

■ Ethical Sales Culture

■ Commercial Insights

■ Customer

Needs

Understanding

■ Value Proposition

■ Relevant Messaging

■ Differentiated Products

■ Customer Accountability

■ Sales Discretion

Goal: Make Bankers More Efficient

Goal: Fulfill Customer Needs

Source: CEB Analysis

New Goal: Help Customers Achieve Business Outcomes

PROCESS TO WHAT END: ENABLING OUTCOMES

Selected Process Support and End Goal

Source: CEB Analysis

SupportEnd Goal: Enable

Banker Efficiency

Customer Segmentation

and Market Coverage

Align Bank Resources to Service

Preference

Leads IdentificationIdentify Large Pool of

Prospective Customers

CRM PlatformAccurately Match Product to

Customer Need

End Goal: Enable

Customer Outcomes

Align Bank Resources

to Customer Outcomes

Identify Precise Customer

Segments Whose Outcomes the

Bank Can Deliver On

Accurately Identify Insight That

Drives Customer Outcomes

Specialists and Internal

Collaboration

Deliver Technical and Closing

Support to Drive Purchase of

Diverse Suite of Products

Deliver Specialized Insight and

Solutions Aligned with Client Goals

Ethical Sales CultureEnsure Compliance and Avoid

Mis-Selling

Ensure Accountability for Driving

Customer Outcomes

Appendix: Align Process Supports With Customer Outcomes

A Case Profile of BDC

ADJUST SERVICE MODEL TO MEET CUSTOMER NEEDS

Challenge: Enable RMs to Serve Customers Efficiently

Goal: Grow the bank by 10%

Understand Customers Better

Efficiently Serve Customers Meet

Customer Preferences Streamline

RM Portfolios Provide RMs Insight

Tools

Hire More Bankers Make

Bankers Do More Create

New Branches

Set Aggressive Cross-Sell Goals Expand

Into New Markets

Source: CEB analysis.

Solution: Bifurcate High and Low Touch Customers

—

Prefer more bank

interactions

Source: CEB analysis.

—

Prefer to interact

infrequently

via e-mail

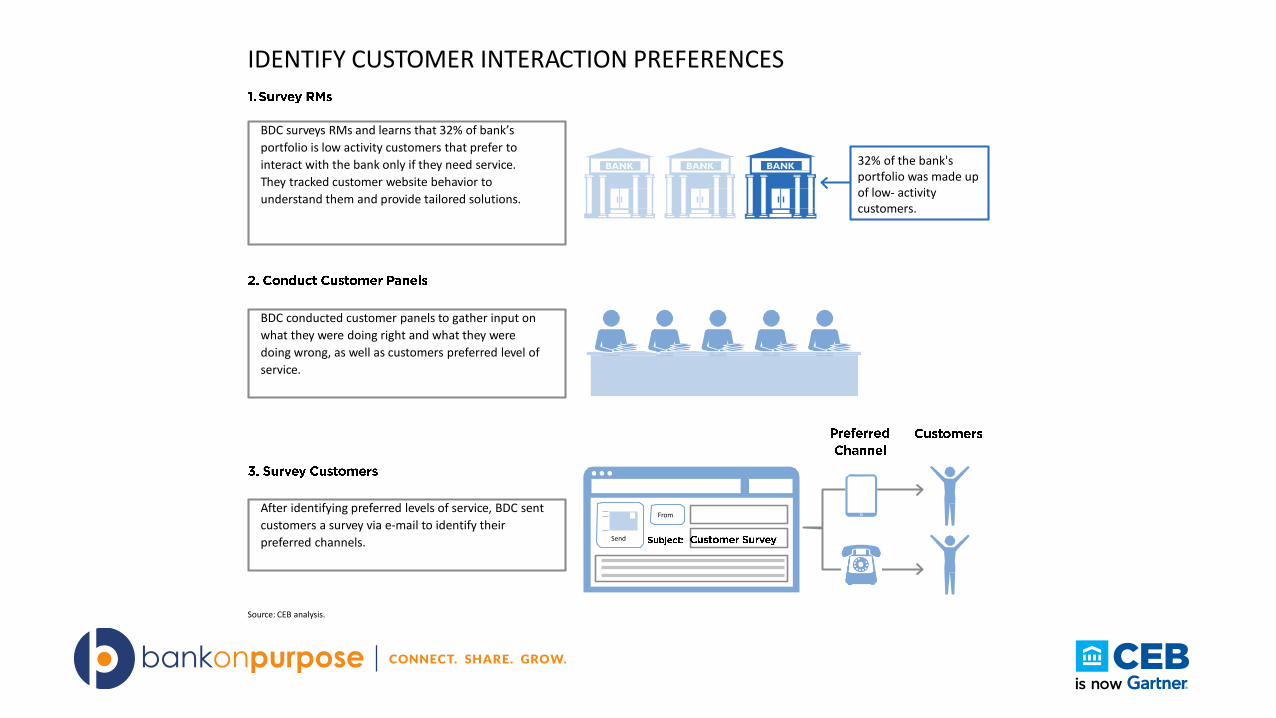

IDENTIFY CUSTOMER INTERACTION PREFERENCES

BDC conducted customer panels to gather input on

what they were doing right and what they were

doing wrong, as well as customers preferred level of

service.

After identifying preferred levels of service, BDC sent

customers a survey via e-mail to identify their

preferred channels. Send

From

BDC surveys RMs and learns that 32% of bank’s

portfolio is low activity customers that prefer to

interact with the bank only if they need service.

They tracked customer website behavior to

understand them and provide tailored solutions.

32% of the bank's portfolio was made up of low- activitycustomers.

Source: CEB analysis.

ALIGN PORTFOLIOS WITH INTERACTION PREFERENCES

Source: CEB analysis.

As customer financing needs change, they are reassigned to another RM portfolio to fit their new needs.

Type of Business: $2 M or Less in Sales Growth

Aspirations: Slow, Steady Number of Products:

1–3

Method of Contact: Phone or E-mail

Frequency of Contact: As Needed Expected

Needs: General Service

Type of Business: Over $2 M in Sales Growth

Aspirations: 15%+ Growth Rate Number of

Products: 3+

Method of Contact: In-Person

Frequency of Contact: Three Annual Meetings

Expected Needs: Customized Insight

LOW TOUCH: HELP BANKERS SERVE EFFICIENTLY

Outbound: Low-Touch E-mail Example Sent from Marketing Every Six Weeks

Source: CEB analysis.

Inbound: Customer Questions to Call Center

Customer on Phone

Call Center Employee

■ Account Log-Ins

■ Balance Inquiries

■ Payment Scheduling

■ Tax Forms

■ Advisory Services

■ Need to Contact an RM

■ Working Capital 101

F ro m S a ra h

Hello John,

Financial ratios provide valuable information about the health of your

business, get started today with our free ratio calculators. Thanks for choosing

BDC!

E-mails are signed by customer’s RM.

E-mail content is not sales ormarketing material, but help customers run their business more effectively.

Source: CEB analysis.

S e n d

HIGH TOUCH: HELP BANKERS SERVE EFFECTIVELY

RMs Conduct Customer Phone Calls or Site Visits Three Times a YearPre-Meeting: High Touch Customer Meeting Prep

During Meeting: App-Enabled Customized Conversation

■ Spent 0–5 minutes preparing

■ Googled customer information and

industry

■ Customer conversation was

insubstantial and non-business

related

■ Client-led with no insight

■ Spend 20–30 minutes preparing

■ Gather industry information to share with

customer

■ Pull up information on the structure of

customer’s current financing

■ Banker-led with insight

■ Generate preauthorized loan amounts for client in real-time

■ Run personalized business scenarios and compare growth margins in real time in

front of the client

■ Record notes directly into CRM system from iPad to reduce amount of RM time in the

office

■ Provide client proposal right then and there

Notifications

iPad 9:40 AM

Customer Name XXXXXXXXXX XXXXXXXXXX

Source: CEB analysis.

RESULTS

Client satisfaction has grown10 times Customers

reporting to be satisfied or very

satisfied has

jumped from 61% to 71%

12% change in new customer

acquisition

10% growth from 2015 to 2016

Repeat customers have increased,

and attrition has decreased.

High Touch Low Touch

Source: CEB analysis.