Unleashing Collaborative IndustryUnleashing … 1 24 7 212 $XXX6 38 4 ‐ ...

23

Unleashing Collaborative Industry Unleashing Collaborative Industry Unleashing Collaborative Industry Unleashing Collaborative Industry Logistics Opportunities Logistics Opportunities February 2013 1

Transcript of Unleashing Collaborative IndustryUnleashing … 1 24 7 212 $XXX6 38 4 ‐ ...

Unleashing Collaborative IndustryUnleashing Collaborative IndustryUnleashing Collaborative Industry Unleashing Collaborative Industry Logistics OpportunitiesLogistics Opportunities

February 2013

1

Senior Leadership Focus On CollaborationSenior Leadership Focus On Collaboration

Collaboration Beyond Our Four WallsCollaboration Beyond Our Four Walls

Drive Efficiency To Fuel GrowthDrive Efficiency To Fuel Growth

2

Think Of Our Supply Chains As ONEThink Of Our Supply Chains As ONE

Consumer Goods Forum Has Published Future Supply Consumer Goods Forum Has Published Future Supply Chain Studies Focusing On Innovative CollaborationChain Studies Focusing On Innovative Collaboration

3

What Is The Consumer Goods Forum?What Is The Consumer Goods Forum?

h d l b l d kh d l b l d k The Consumer Goods Forum Is A Global Industry NetworkThe Consumer Goods Forum Is A Global Industry Network

The World’s Leading Association Of Retailers & Manufacturers The World’s Leading Association Of Retailers & Manufacturers ggAnd Their Business PartnersAnd Their Business Partners

A Global Organization With Headquarters In Paris And OfficesA Global Organization With Headquarters In Paris And Offices A Global Organization With Headquarters In Paris And Offices A Global Organization With Headquarters In Paris And Offices In Tokyo And WashingtonIn Tokyo And Washington

A Unique Platform To Develop Common Positions On Key A Unique Platform To Develop Common Positions On Key Strategic, Operational And NonStrategic, Operational And Non‐‐competitive Issues Affecting competitive Issues Affecting The Consumer Goods BusinessThe Consumer Goods Business

4

Collaborative Logistics Project OverviewCollaborative Logistics Project Overview

Purpose - Identify Collaborative Transportation OpportunitiesPurpose Identify Collaborative Transportation Opportunities

Hypothesis - Many Consumer Products Manufacturers & Retailers Have Redundant And Overlapping Logistics Infrastructures

Evolution‒ Currently Completing One-To-One Network Overlay Projects

We Believe That We Can Expand On This Approach By Completing An‒ We Believe That We Can Expand On This Approach By Completing An Analysis That Includes Multiple Trading Partners In The Same Geographies

Objectives‒ Confidentially Identify Transportation Network Collaboration Opportunities

Between CPG Companies & Retailers

‒ Reduce Costs And Improve Sustainable Business Practices

5

‒ Reduce Empty Miles & Improve Cube Utilization While Improving Service

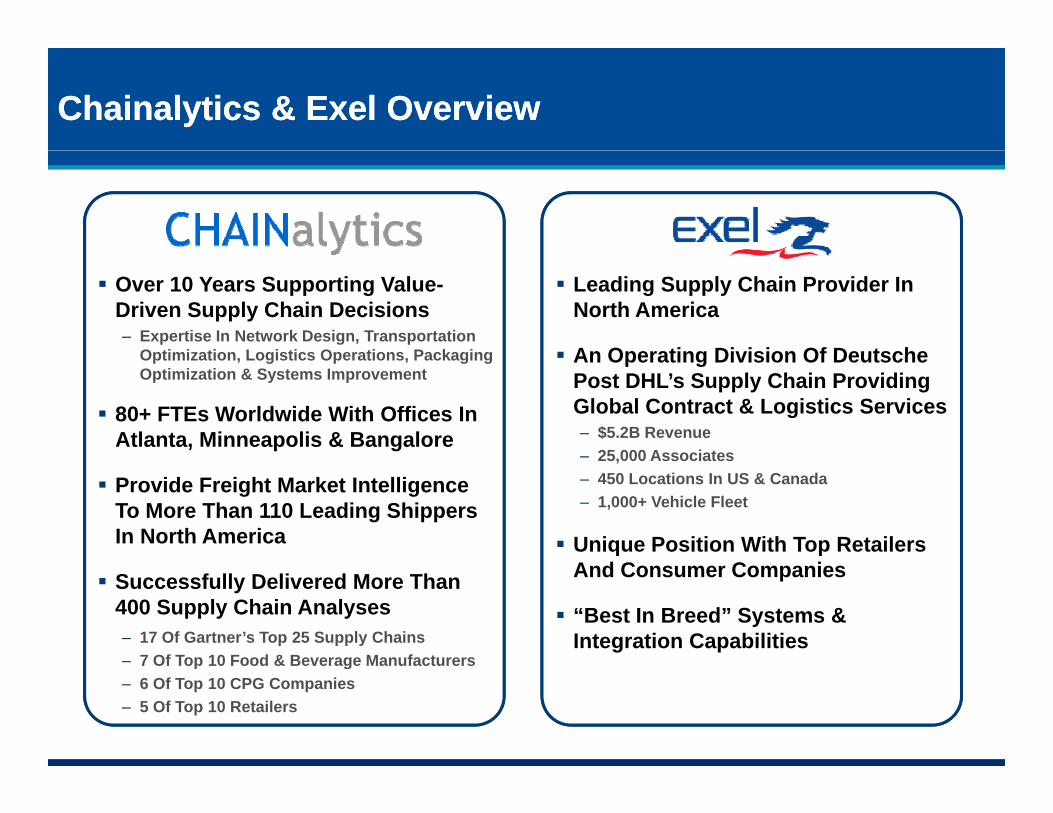

Chainalytics & Chainalytics & ExelExel OverviewOverview

Over 10 Years Supporting Value-Driven Supply Chain Decisions‒ Expertise In Network Design, Transportation

Optimization Logistics Operations Packaging

Leading Supply Chain Provider In North America

An Operating Division Of DeutscheOptimization, Logistics Operations, Packaging Optimization & Systems Improvement

80+ FTEs Worldwide With Offices In Atlanta, Minneapolis & Bangalore

An Operating Division Of Deutsche Post DHL’s Supply Chain Providing Global Contract & Logistics Services‒ $5.2B Revenue‒ 25 000 Associates

Provide Freight Market Intelligence To More Than 110 Leading Shippers In North America

25,000 Associates‒ 450 Locations In US & Canada‒ 1,000+ Vehicle Fleet

Unique Position With Top Retailers

Successfully Delivered More Than 400 Supply Chain Analyses‒ 17 Of Gartner’s Top 25 Supply Chains‒ 7 Of Top 10 Food & Beverage Manufacturers

And Consumer Companies

“Best In Breed” Systems & Integration Capabilities

6

7 Of Top 10 Food & Beverage Manufacturers‒ 6 Of Top 10 CPG Companies‒ 5 Of Top 10 Retailers

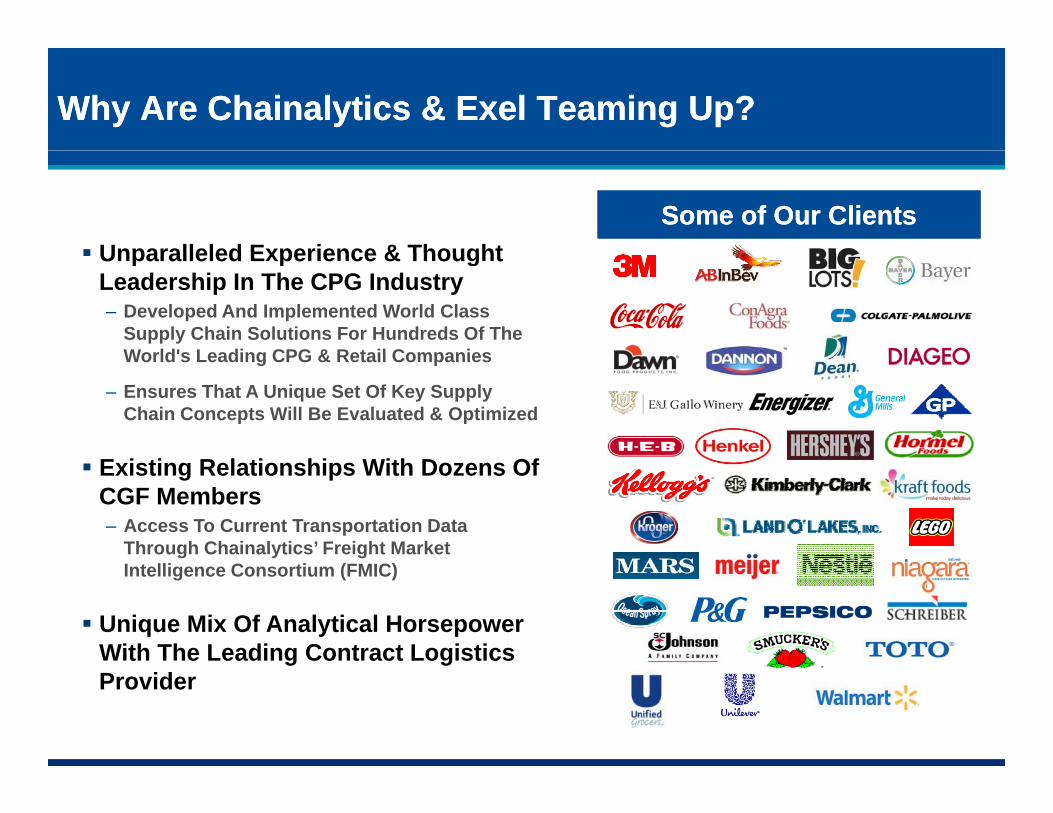

Why Are Why Are ChainalyticsChainalytics & & ExelExel Teaming Up?Teaming Up?

Unparalleled Experience & ThoughtSome of Our ClientsSome of Our ClientsSome of Our ClientsSome of Our Clients

Unparalleled Experience & Thought Leadership In The CPG Industry‒ Developed And Implemented World Class

Supply Chain Solutions For Hundreds Of The World's Leading CPG & Retail CompaniesWorld s Leading CPG & Retail Companies

‒ Ensures That A Unique Set Of Key Supply Chain Concepts Will Be Evaluated & Optimized

Existing Relationships With Dozens Of CGF Members ‒ Access To Current Transportation Data

Through Chainalytics’ Freight Market

Intelligence Consortium (FMIC)

Unique Mix Of Analytical Horsepower With The Leading Contract Logistics

7

g gProvider

Chainalytics Freight Market Intelligence ConsortiumChainalytics Freight Market Intelligence Consortium

Provides Freight Market Intelligence,

SAMPLE COMPANY July 2011 Model - TruckloadModel-Based Benchmarking Consortium

StatisticsAnnual Shipment Volume 189,631 Loads

Estimated Market Cost 277,684,161$ Reported Annual Cost 278,646,063$

Percent Above / Below Market 0 35% AT MARKET

Long Haul Volume

SAMPLE COMPANY July 2011 Model - TruckloadModel-Based Benchmarking Consortium

StatisticsAnnual Shipment Volume 189,631 Loads

Estimated Market Cost 277,684,161$ Reported Annual Cost 278,646,063$

Percent Above / Below Market 0 35% AT MARKET

Long Haul Volume

Provides Freight Market Intelligence, Benchmarking, & Comparative Analysis To Its Members In A Private Forum‒ TL (Dry Van, Temp Control, Flatbed, IM), LTL, Ocean

Percent Above / Below Market 0.35% AT MARKETValue Above / Below Market 961,903$

Load Statistics Number of Loads PercentLoads BELOW Market 92,539 49%

Loads AT Market 36,298 19%Loads ABOVE Market 60,793 32%

Value Statistics Value PercentActual Value BELOW Market 107,842,874$ 39%

Actual Value AT Market 56,186,568$ 20%Actual Value ABOVE Market 114,616,622$ 41%

Statistics Coversheet statistics are based on all-in rates inclusive of fuel.

Long Haul (For loads >=250 miles)Annual Shipment Volume 141,198 loads 411 loads 5,162 loads 42,860 loads

Estimated Market Cost 181,329,901$ 641,763$ 9,794,499$ 85,917,997$ Reported Annual Cost 175,825,353$ 663,384$ 9,701,273$ 92,456,054$

Percent Above / Below Market -3.04% BELOW MARKET 3.37% ABOVE MARKET -0.95% AT MARKET 7.61% ABOVE MARKETValue Above / Below Market (5,504,548)$ 21,621$ (93,227)$ 6,538,057$

Load Statistics Count Percent Count Percent Count Percent Count Percent

Dry Van Temperature-Controlled Flatbed Intermodal

Percent Above / Below Market 0.35% AT MARKETValue Above / Below Market 961,903$

Load Statistics Number of Loads PercentLoads BELOW Market 92,539 49%

Loads AT Market 36,298 19%Loads ABOVE Market 60,793 32%

Value Statistics Value PercentActual Value BELOW Market 107,842,874$ 39%

Actual Value AT Market 56,186,568$ 20%Actual Value ABOVE Market 114,616,622$ 41%

Statistics Coversheet statistics are based on all-in rates inclusive of fuel.

Long Haul (For loads >=250 miles)Annual Shipment Volume 141,198 loads 411 loads 5,162 loads 42,860 loads

Estimated Market Cost 181,329,901$ 641,763$ 9,794,499$ 85,917,997$ Reported Annual Cost 175,825,353$ 663,384$ 9,701,273$ 92,456,054$

Percent Above / Below Market -3.04% BELOW MARKET 3.37% ABOVE MARKET -0.95% AT MARKET 7.61% ABOVE MARKETValue Above / Below Market (5,504,548)$ 21,621$ (93,227)$ 6,538,057$

Load Statistics Count Percent Count Percent Count Percent Count Percent

Dry Van Temperature-Controlled Flatbed Intermodal

Uses A Model-Based Benchmarking Approach To Normalize The Drivers Which Impact Overall Costs

Load Statistics Count Percent Count Percent Count Percent Count PercentLoads BELOW Market 84,208 60% 164 40% 2,234 43% 5,932 14%

Loads AT Market 28,792 20% 24 6% 1,174 23% 6,311 15%

Loads ABOVE Market 28,198 20% 223 54% 1,754 34% 30,617 71%

Value Statistics Value Percent Value Percent Value Percent Value PercentActual Value BELOW Market 93,798,530$ 53% 202,669$ 31% 3,240,325$ 33% 10,601,350$ 11%

Actual Value AT Market 40,974,129$ 23% 31,813$ 5% 2,346,247$ 24% 12,834,381$ 14%Actual Value ABOVE Market 41,052,694$ 23% 428,902$ 65% 4,114,701$ 42% 69,020,323$ 75%

Comparative Ranking TOP THIRD BOTTOM THIRD MIDDLE THIRD BOTTOM THIRD

Load Statistics Count Percent Count Percent Count Percent Count PercentLoads BELOW Market 84,208 60% 164 40% 2,234 43% 5,932 14%

Loads AT Market 28,792 20% 24 6% 1,174 23% 6,311 15%

Loads ABOVE Market 28,198 20% 223 54% 1,754 34% 30,617 71%

Value Statistics Value Percent Value Percent Value Percent Value PercentActual Value BELOW Market 93,798,530$ 53% 202,669$ 31% 3,240,325$ 33% 10,601,350$ 11%

Actual Value AT Market 40,974,129$ 23% 31,813$ 5% 2,346,247$ 24% 12,834,381$ 14%Actual Value ABOVE Market 41,052,694$ 23% 428,902$ 65% 4,114,701$ 42% 69,020,323$ 75%

Comparative Ranking TOP THIRD BOTTOM THIRD MIDDLE THIRD BOTTOM THIRD

Semi-Annual Or Quarterly Updates

Over $18B In TL With Over 90 Shipper ppMembers

8

Market Dynamics are Significant for Shippers 2 Year Review by Mode

2011 20122010

S Ch i l ti FMICSource: Chainalytics FMIC

9

While Transportation rate increases have been relatively low over the past few years, shippers will need to find creative ways to control rate inflation

The The Industry Case For Industry Case For CollaborationCollaboration

Macro demands are straining transportation networksRetailers demand for smaller faster more frequent shipmentsRetailers demand for smaller, faster, more frequent shipments Sustainability (consolidation programs = minimized carbon emissions)Cost reductions (optimized shipping, lower inventories, capital

avoidance) Fluctuating diesel fuel costs

Multi-Company Supply Chain initiatives are needed to address these challenges Peer to peer collaboration is good but slow to unlock value. For later phases of collaboration to be successful an industry-wide

focus must be taken.

10

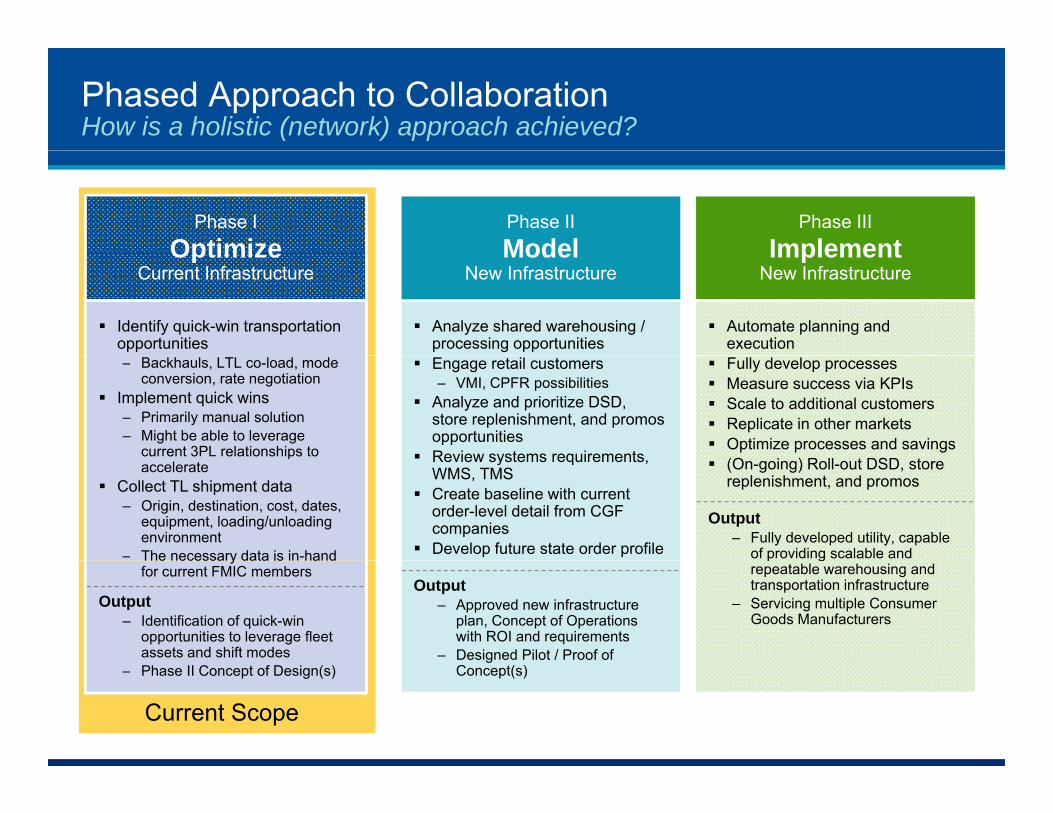

Phased Approach to CollaborationHow is a holistic (network) approach achieved?

Phase IOptimize

Phase IIModel

Phase IIIImplement

Analyze shared warehousing / processing opportunities

Optimize Current Infrastructure

Identify quick-win transportation opportunities

ModelNew Infrastructure

Implement New Infrastructure

Automate planning and execution

Engage retail customers– VMI, CPFR possibilities

Analyze and prioritize DSD, store replenishment, and promos opportunities

Review systems requirements

– Backhauls, LTL co-load, mode conversion, rate negotiation

Implement quick wins– Primarily manual solution– Might be able to leverage

current 3PL relationships to

Fully develop processes Measure success via KPIs Scale to additional customers Replicate in other markets Optimize processes and savings

(O i ) R ll DSD Review systems requirements, WMS, TMS

Create baseline with current order-level detail from CGF companies

Develop future state order profile

paccelerate

Collect TL shipment data– Origin, destination, cost, dates,

equipment, loading/unloading environment

– The necessary data is in-hand

(On-going) Roll-out DSD, store replenishment, and promos

Output– Fully developed utility, capable

of providing scalable and

Output– Approved new infrastructure

plan, Concept of Operations with ROI and requirements

– Designed Pilot / Proof of

The necessary data is in hand for current FMIC members

Output– Identification of quick-win

opportunities to leverage fleet assets and shift modes

p grepeatable warehousing and transportation infrastructure

– Servicing multiple Consumer Goods Manufacturers

11

Concept(s)

Current Scope

– Phase II Concept of Design(s)

Phased Approach to CollaborationHow is a holistic (network) approach achieved?

Phase IOptimize

Phase IIModel

Phase IIIImplement

Analyze shared warehousing / processing opportunities

Optimize Current Infrastructure

Identify quick-win transportation opportunities

ModelNew Infrastructure

Implement New Infrastructure

Automate planning and execution

Engage retail customers– VMI, CPFR possibilities

Analyze and prioritize DSD, store replenishment, and promos opportunities

Review systems requirements

– Backhauls, LTL co-load, mode conversion, rate negotiation

Implement quick wins– Primarily manual solution– Might be able to leverage

current 3PL relationships to

Fully develop processes Measure success via KPIs Scale to additional customers Replicate in other markets Optimize processes and savings

(O i ) R ll DSD Review systems requirements, WMS, TMS

Create baseline with current order-level detail from CGF companies

Develop future state order profile

paccelerate

Collect TL shipment data– Origin, destination, cost, dates,

equipment, loading/unloading environment

– The necessary data is in-hand

(On-going) Roll-out DSD, store replenishment, and promos

Output– Fully developed utility, capable

of providing scalable and

Output– Approved new infrastructure

plan, Concept of Operations with ROI and requirements

– Designed Pilot / Proof of

The necessary data is in hand for current FMIC members

Output– Identification of quick-win

opportunities to leverage fleet assets and shift modes

p grepeatable warehousing and transportation infrastructure

– Servicing multiple Consumer Goods Manufacturers

12

Concept(s)

Current Scope

– Phase II Concept of Design(s)

Phase 1 OpportunitiesPhase 1 Opportunities

Analysis Of Common Lanes & Corresponding Networks‒ Back Hauls/Fleet Utilization‒ Comingled LTL‒ Mode Conversion

Identify “Quick-Win” Transportation Opportunities‒ Identify Quick-Win Transportation Opportunities

Develop Innovative Concepts & Designs (I E Shared Leased 3PL Fleets Etc )(I.E. Shared Leased 3PL Fleets, Etc.)

13

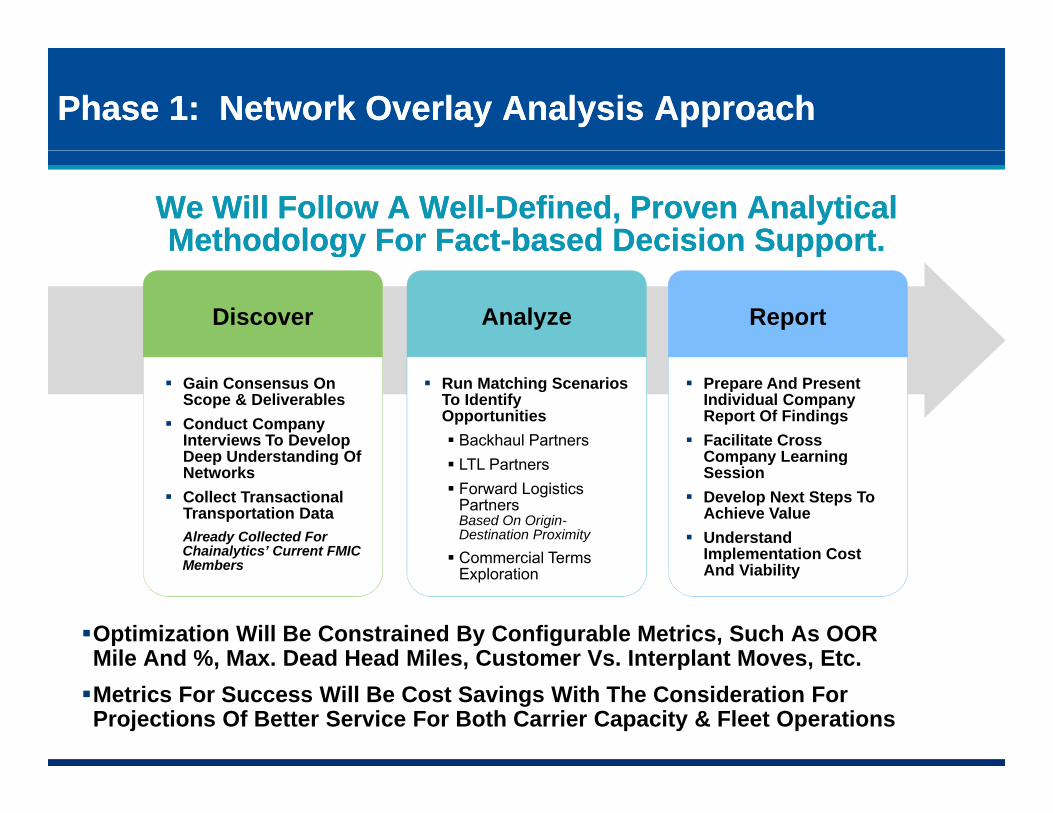

Phase 1: Network Overlay Analysis ApproachPhase 1: Network Overlay Analysis Approach

We Will Follow A WellWe Will Follow A Well--Defined, Proven Analytical Defined, Proven Analytical Methodology For FactMethodology For Fact--based Decision Support.based Decision Support.gygy pppp

Discover Analyze Report

Gain Consensus On Scope & Deliverables

Conduct Company Interviews To Develop Deep Understanding Of

Prepare And Present Individual Company Report Of Findings

Facilitate Cross Company Learning

Run Matching Scenarios To Identify Opportunities Backhaul Partners

Deep Understanding Of Networks

Collect Transactional Transportation Data Already Collected For Chainalytics’ Current FMIC M b

Company Learning Session

Develop Next Steps To Achieve Value

Understand Implementation Cost

LTL Partners Forward Logistics

Partners Based On Origin-Destination Proximity

Commercial Terms

Optimization Will Be Constrained By Configurable Metrics, Such As OOR Mile And %, Max. Dead Head Miles, Customer Vs. Interplant Moves, Etc.

Membersp

And ViabilityCommercial Terms Exploration

14

Mile And %, Max. Dead Head Miles, Customer Vs. Interplant Moves, Etc.Metrics For Success Will Be Cost Savings With The Consideration For Projections Of Better Service For Both Carrier Capacity & Fleet Operations

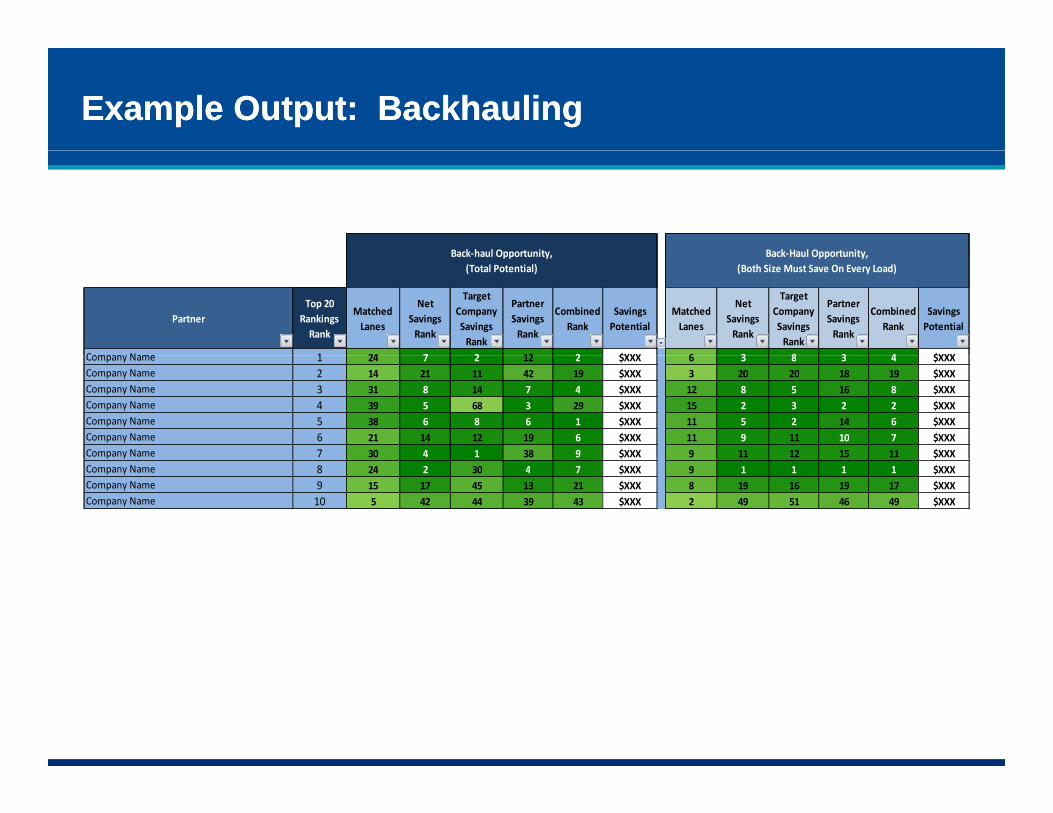

Example Output: BackhaulingExample Output: Backhauling

Back haul Opportunity Back Haul OpportunityBack haul Opportunity Back Haul Opportunity

PartnerTop 20

Rankings Rank

Matched Lanes

Net Savings Rank

Target Company Savings Rank

Partner Savings Rank

Combined Rank

Savings Potential

Matched Lanes

Net Savings Rank

Target Company Savings Rank

Partner Savings Rank

Combined Rank

Savings Potential

Company Name 1 24 7 2 12 2 $XXX 6 3 8 3 4 $XXX

Back‐haul Opportunity, (Total Potential)

Back‐Haul Opportunity, (Both Size Must Save On Every Load)

PartnerTop 20

Rankings Rank

Matched Lanes

Net Savings Rank

Target Company Savings Rank

Partner Savings Rank

Combined Rank

Savings Potential

Matched Lanes

Net Savings Rank

Target Company Savings Rank

Partner Savings Rank

Combined Rank

Savings Potential

Company Name 1 24 7 2 12 2 $XXX 6 3 8 3 4 $XXX

Back‐haul Opportunity, (Total Potential)

Back‐Haul Opportunity, (Both Size Must Save On Every Load)

Company Name 1 24 7 2 12 2 $XXX 6 3 8 3 4 $XXXCompany Name 2 14 21 11 42 19 $XXX 3 20 20 18 19 $XXXCompany Name 3 31 8 14 7 4 $XXX 12 8 5 16 8 $XXXCompany Name 4 39 5 68 3 29 $XXX 15 2 3 2 2 $XXXCompany Name 5 38 6 8 6 1 $XXX 11 5 2 14 6 $XXXCompany Name 6 21 14 12 19 6 $XXX 11 9 11 10 7 $XXXCompany Name 7 30 4 1 38 9 $XXX 9 11 12 15 11 $XXX

Company Name 1 24 7 2 12 2 $XXX 6 3 8 3 4 $XXXCompany Name 2 14 21 11 42 19 $XXX 3 20 20 18 19 $XXXCompany Name 3 31 8 14 7 4 $XXX 12 8 5 16 8 $XXXCompany Name 4 39 5 68 3 29 $XXX 15 2 3 2 2 $XXXCompany Name 5 38 6 8 6 1 $XXX 11 5 2 14 6 $XXXCompany Name 6 21 14 12 19 6 $XXX 11 9 11 10 7 $XXXCompany Name 7 30 4 1 38 9 $XXX 9 11 12 15 11 $XXXp y $ $Company Name 8 24 2 30 4 7 $XXX 9 1 1 1 1 $XXXCompany Name 9 15 17 45 13 21 $XXX 8 19 16 19 17 $XXXCompany Name 10 5 42 44 39 43 $XXX 2 49 51 46 49 $XXX

p y $ $Company Name 8 24 2 30 4 7 $XXX 9 1 1 1 1 $XXXCompany Name 9 15 17 45 13 21 $XXX 8 19 16 19 17 $XXXCompany Name 10 5 42 44 39 43 $XXX 2 49 51 46 49 $XXX

15

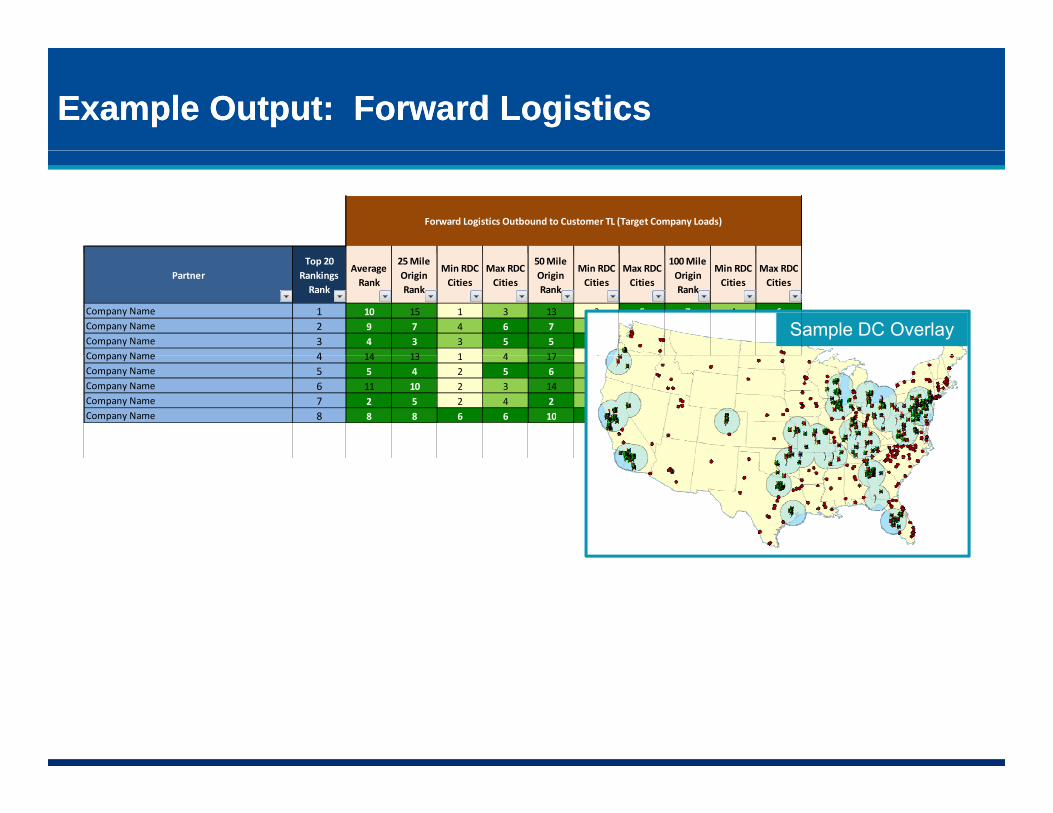

Example Output: Forward LogisticsExample Output: Forward Logistics

Forward Logistics Outbound to Customer TL (Target Company Loads)Forward Logistics Outbound to Customer TL (Target Company Loads)

PartnerTop 20

Rankings Rank

Average Rank

25 Mile Origin Rank

Min RDC Cities

Max RDC Cities

50 Mile Origin Rank

Min RDC Cities

Max RDC Cities

100 Mile Origin Rank

Min RDC Cities

Max RDC Cities

Company Name 1 10 15 1 3 13 2 5 7 4 6Company Name 2 9 7 4 6 7 4 6 11 5 6Company Name 3 4 3 3 5 5 5 5 3 6 6Company Name 4 14 13 1 4 17 2 5 14 5 6

PartnerTop 20

Rankings Rank

Average Rank

25 Mile Origin Rank

Min RDC Cities

Max RDC Cities

50 Mile Origin Rank

Min RDC Cities

Max RDC Cities

100 Mile Origin Rank

Min RDC Cities

Max RDC Cities

Company Name 1 10 15 1 3 13 2 5 7 4 6Company Name 2 9 7 4 6 7 4 6 11 5 6Company Name 3 4 3 3 5 5 5 5 3 6 6Company Name 4 14 13 1 4 17 2 5 14 5 6

Sample DC OverlayCompany Name 4 14 13 1 4 17 2 5 14 5 6Company Name 5 5 4 2 5 6 4 5 6 6 6Company Name 6 11 10 2 3 14 4 4 15 6 6Company Name 7 2 5 2 4 2 3 5 2 5 6Company Name 8 8 8 6 6 10 6 6 9 6 6

Company Name 4 14 13 1 4 17 2 5 14 5 6Company Name 5 5 4 2 5 6 4 5 6 6 6Company Name 6 11 10 2 3 14 4 4 15 6 6Company Name 7 2 5 2 4 2 3 5 2 5 6Company Name 8 8 8 6 6 10 6 6 9 6 6

16

Summary of DeliverablesSummary of Deliverables

Benefits Case Workbook Containing:g‒ Output From Overlay Analysis Of Common Lanes

& Corresponding Networks‒ “Quick-Win” Transportation OpportunitiesQuick Win Transportation Opportunities‒ Innovative Concepts & Designs

(I.E. Shared Leased 3PL Fleets, Etc.)

Debrief And Wrap-Up Meeting Of Participants To Review Results & Engage In Deeper Discussion About The FindingsAbout The Findings

Roadmap Of Next Steps

17

Project Work Plan: Phase 1Project Work Plan: Phase 1

Step Week 2 3 4 5 6 7 8 9 10

AssessmentProject Mobilization

1

Project MobilizationInterviewsData Validation and Collect Missing DataBuild and Validate Baseline NetworksReview Scenario Run Plan X

AnalysisAnalysisBackhaul, LTL, Mode ConversionRate AnalysisDevelop and Review Initial Thoughts X

ConclusionsIntegrate FeedbackFacilitate Recommendation Review Session XDevelop Imp and Future Phases PlanProgress Reviews ▲ ▲ ▲ ▲ ▲ ▲

Milestones ▲ ▲ ▲ ▲

Assumes 10-20 Participants With Readily-Available Data

Milestones ▲ ▲ ▲ ▲X indicates Sr. Mgt Meeting

potential for delay

18

Assumes 10 20 Participants With Readily Available Data Detailed Plans For Phases 2 & 3 Will Be Developed During Phase 1

What Is Required To Participate?What Is Required To Participate?

Provide 12 Months Of Freight DataTL LTL‒ TL, LTL

‒ Origin, Destination, Linehaul Cost, Fuel, Accessorials, Mode, Equipment, Service, IB/OB/Transfer, Ship Date, Del Date, Loading/Unloading Env., Weight, Cube, SCAC, Multi-stop, Distance

• Most Data Already On-hand For Chainalytics FMIC Members‒ MS Excel Data Template Will Be Provided

• Secure File Transfer Options For Large Files • Chainalytics Has 10 + Years In Handling Sensitive Data With FMICChainalytics Has 10 + Years In Handling Sensitive Data With FMIC

Commitment To Assign Resources‒ Participate In Discovery Calls, Answer Data Questions

Att d P R i M ti Fi l D li bl R i M ti‒ Attend Progress Review Meetings, Final Deliverables Review Meeting

Nominal Project Fee

19

Must Own Freight – Retailers & Manufacturers

Companies Committed Companies Committed To To Participate Participate To Date…To Date…

20

Project Work Fees: Phase 1Project Work Fees: Phase 1

PhasePhase DurationDuration Professional FeesProfessional Fees

OneOptimize Current

10 - 12 Weeks

$12,500 Fixed Professional Fees For Each FMIC Member Company $17,500 Fixed Professional Fees For Each Non-FMIC Company Current

InfrastructureWeeks $17,500 Fixed Professional Fees For Each Non FMIC Company

Plus Travel Expenses*

21

*Billed at cost, estimated at 15% of professional fees for Phase 1

So Why Should You Consider Participating?So Why Should You Consider Participating?

Cost Effective Way To Get Visibility To Trading Partner & CPG Transportation Opportunities Across The U.S. & Canada

Ability To Identify & Un-Lock Second-Order Transportation Opportunities (i.e. Shared Leased Fleets, Hub, Co-Load)

Demonstrate Value In Phase I To Fuel Industry Interest In Broader Collaboration Opportunities In WarehousingBroader Collaboration Opportunities In Warehousing

Forum To Facilitate & Drive Peer Collaboration

22

Thank You!Mike Hane mhane@chainalytics com 678 384 3581

23

Mike Hane, [email protected], 678-384-3581,Rudy Hagedorn, [email protected]

+49 171 693 5583