University “Alexandru Ioan Cuza” of Iaşi Faculty of ...phdthesis.uaic.ro/PhDThesis/Ungureanu,...

36

University “Alexandru Ioan Cuza” of Iaşi Faculty of Economics and Business Administration Doctoral School of Economics and Business Administration Domain: Accounting ACTUALITIES AND PERSPECTIVES CONCERNING METHODOLOGY OF COSTS CALCULATION - Summary of doctoral thesis - Scientific coordinator, Professor Ph.D. Neculai TABĂRĂ Ph.D. Student, Sebastian UNGUREANU Iaşi 2014

Transcript of University “Alexandru Ioan Cuza” of Iaşi Faculty of ...phdthesis.uaic.ro/PhDThesis/Ungureanu,...

University “Alexandru Ioan Cuza” of Iaşi

Faculty of Economics and Business Administration

Doctoral School of Economics and Business Administration

Domain: Accounting

ACTUALITIES AND PERSPECTIVES CONCERNING

METHODOLOGY OF COSTS CALCULATION

- Summary of doctoral thesis -

Scientific coordinator,

Professor Ph.D. Neculai TABĂRĂ

Ph.D. Student,

Sebastian UNGUREANU

Iaşi

2014

University “Alexandru Ioan Cuza” of Iaşi

Faculty of Economics and Business Administration

Doctoral School of Economics and Business Administration

Domain: Accounting

ACTUALITIES AND PERSPECTIVES CONCERNING

METHODOLOGY OF COSTS CALCULATION

- Summary of doctoral thesis -

Scientific coordinator,

Professor Ph.D. Neculai TABĂRĂ

Ph.D. Student,

Sebastian UNGUREANU

Iaşi

2014

University “Alexandru Ioan Cuza” of Iaşi

Faculty of Economics and Business Administration

Doctoral School of Economics and Business Administration

Domain: Accounting

_________________________________

_______________________

We do know that on 12 December 2014, at 10.00 in room R402, Mr.

UNGUREANU SEBASTIAN will sustain in the public meeting, doctoral thesis with theme

ACTUALITIES AND PERSPECTIVES CONCERNING METHODOLOGY OF COSTS

CALCULATION to obtain a PhD title in ACCOUNTING.

Doctoral committee, approved by Decision the Rector of University Alexandru Ioan

Cuza from 22.10.2014 number 16798 composed of the following:

Președinte: Professor Ph.D. Costel ISTRATE, University “Alexandru Ioan Cuza” of Iaşi

Scientific coordinator: Professor Ph.D. Neculai TABĂRĂ, University “Alexandru Ioan Cuza”

of Iaşi

Reviewers:

Professor Ph.D. Ion PEREȘ, West University of Timişoara;

Professor Ph.D. Ioan POPA, University “Babeș Bolyai” of Cluj Napoca;

Professor Ph.D. Dorina BUDUGAN, University “Alexandru Ioan Cuza” of Iaşi.

We invite you to participate in the presentation session the thesis. The thesis can be

consulted at Library of the Faculty of Economics and Business Administration

CONTENTS SUMMARY OF DOCTORAL THESIS

CONTENTS OF DOCTORAL THESIS ...........................................................................

INTRODUCTION ...............................................................................................................

THE PURPOSE AND OBJECTIVES OF THE THESIS.............................................. 8

METHODOLOGY OF SCIENTIFIC RESEARCH .................................................... 10

SUMMARY OF THE MAIN PARTS OF THE DOCTORAL THESIS .................... 12

CONCLUSIONS AND PROPOSALS ........................................................................... 15

BIBLIOGRAPHY ................................................................................................................

CONTENTS OF DOCTORAL THESIS

INTRODUCTION...........................................................................................................................5

CHAPTER 1

CONCEPTUAL DELIMITATIONS CONCERNING COST CALCULATION ................. 12

1.1. Cost calculation, genesis, references and evolution................................................12

1.1.1. Actual stage of knowledge in the specialty literature ...................................... 12

1.1.2.1. Moments in the evolution of managerial accounting from before 1949 ...... 16

1.1.2.2. Aspects of management accounting in the period 1949 – 1989...............16

1.1.2.3. Highlights on management accounting in the present time...................... 18

1.2. Concepts on cost calculation .................................................................................. 20

1.2.1. Definition of the cost calculation .................................................................... 25

1.2.2. Concept of the cost .......................................................................................... 25

1.2.3. Place and role of the cost calculation .............................................................. 26

1.2.4. Expenses, costs constitutive elements ............................................................. 28

1.3. The information costs - the result of cost calculation............................................. 30

1.4. Typology of costs in the the making decision ........................................................ 34

1.5. Principles and factors organization of management accounting and cost calculation

.................................................................................................................................................. .43

1.5.1. Principles of applied in the calculation costs of production ........................... 43

1.5.2. Factors that condition the organization of the cost calculation ....................... 50

1.6. Production in the vision of managerial accounting ................................................ 52

1.6.1. Areas of spending ............................................................................................ 53

1.6.2. Costs carriers....................................................................................................55

CHAPTER 2

NEW DIMENSIONS OF THE TYPE COST INFORMATION IN DECISION MAKING

....................................................................................................................................................... 58 2.1. Importance of a cost information in decision making ............................................ 58

2.2. Decision making ..................................................................................................... 62

2.3. Management Accounting essential source of information for the organization ..... 64

2.3.1. Management accounting and organizational management.............................. 68

2.3.2. Using a cost information in decision making .................................................. 71

2.3.3. The costs of the decision making process ....................................................... 73

2.4. Life cycle cost methodology .................................................................................. 79

2.4.1. Using the methodology ................................................................................... 79

2.4.2. Information needed for the classification of the methodology and life cycle

costs ....................................................................................................................................... 82

2.4.3. Example of applying the methodology L.C.C. ................................................ 86

2.5. The hidden Costs of organization ........................................................................... 88

2.6. Strategic cost management ..................................................................................... 91

2.7. The planning company data system to reflect the strategy..................................... 94

2.8. Control of management and modernization of accounting information processing

instruments ................................................................................................................................ 97

2.8.1. The problem of the management control........................................................ 97

2.8.2. Principles and role of management control in the company's management .. 103

CHAPTER 3

TRENDS IN THE METHODOLOGY OF COSTS CALCULATION ................................ 106 3.1. The system of calculation methods and the cost allocation ................................. 106

3.2. Management methods the costs. Definition and classification of methods of cost

calculation ............................................................................................................................... 114

3.2.1. Classical methods of cost calculation ............................................................ 115

3.2.1.1. Global method of cost calculation .......................................................... 115

3.2.1.2. Method of cost calculation of manufacturing phases ............................. 116

3.2.1.3. Method of cost calculation on commands .............................................. 118

3.2.2. Evolved methods of cost calculation ............................................................. 119

3.2.2.1. Standard cost method ............................................................................. 119

3.2.2.2. Machine-hour-rate method ..................................................................... 121

3.2.2.3. Georges Perrinmethod ............................................................................ 123

3.2.2.4. Direct Costing method ............................................................................ 125

3.2.3. Modern methods of cost calculation in the context of the new problematic of

production, a technologies and informatization .................................................................. 127

3.2.3.1. Activities based costing method ............................................................. 127

3.2.3.2. Activities based management ................................................................. 131

3.2.3.3. Target costing method ............................................................................ 134

3.2.3.4. Kaizen Costing method .......................................................................... 136

3.2.4. Factors that determine selecting the method of cost calculation ................... 139

3.3. Perspectives in the methodology of cost calculation ............................................ 141

CHAPTER 4

PARTICULARITIES OF COST CALCULATION AT SC AEROSTAR S.A. BACĂU ... 146 4.1. The aviation industry in Europe and worldwide .................................................. 146

4.1.1. Context global şi european ............................................................................ 149

4.1.2. The European aeronautics industry ............................................................... 152

4.1.2.1. Romanian aeronautics industry .............................................................. 153

4.1.2.2. Common development policy in the aeronautical sector ....................... 155

4.2. Change of strategy to development in aviation industry ...................................... 156

4.2.1. Niche segment in research - development - innovation ................................ 158

4.2.2. Promotion of capabilities romanian aviation sector at the international level

............................................................................................................................................. 159

4.3. National economic environment at S.C. Aerostar S.A. Bacau ............................. 159

4.3.1. Company overview ........................................................................................ 160

4.3.2. Products and services supplied by the company, the level of technical and

market positioning...............................................................................................................163

4.4. The production activity at S.C. Aerostar S.A. Bacau...........................................167

4.4.1. Implementation of the method A.B.C. at Aerostar company........................172

4.4.2. Modernization cost calculation through Target Costing method..................183

CONCLUSIONS AND PROPOSALS.........................................................................201

BIBLIOGRAPHY..........................................................................................................208

LIST OF TABLES.........................................................................................................226

LIST OF FIGURES......................................................................................................227

LIST OF ANNEXES.....................................................................................................228

INTRODUCTION

Management accounting is an system of information that collects and processes

information in assessing and managing the company's performance. The current economic

environment, characterized by competitiveness, is a challenge for management accounting

because its instruments are highly influenced by historical, cultural, technical, etc.

The companies have started to pay attention to human behavior and cultural aspect,

considering human intelligence as the main economic resource. Performance in the current

economic environment involves the development and use of computer systems and management

costs. Being oriented control and decision costing is one of the basic components of the system

profitable management of the company. As an information tool, it deals with the producing and

providing the necessary information on costs and is used as a management tool in decision

making on increasing profitability. The local political and economic context in slow

development of the national economy had a negative impact on changes as a result of

globalization, increased competition, revamping production processes etc. Reasons why they

management accounting has evolved somewhat difficult to separate and the international level.

During the time, introduced new methods and tools of management accounting as a result of the

direct influence exercised by the literature and practice internationally.

Doctoral thesis on "Actualities and perspectives concerning methodology of

costs calculation" has as main objective the implementation of relevant solutions to

modernize information system cost. In approaching the levels of management accounting

information system, to ensure the effective leadership of the company objectives are traced in

terms of costs and responsibilities related of deviations.

The costing methodology is a coherent set of techniques and procedures in relation to

which must implement all actions required to achieve the fundamental objective of management

accounting and control certain internal conditions of production through costs. Management

accounting has the tools and resources necessary to support this approach by new methods of

calculation and cost management, targeting business processes and adapt more easily to changes,

whatever their nature. In modern vision that modern accounting is not a succession of technical

operations, which are designed to accurately record economic transactions, but to support

management decisions through relevant financial and accounting data. Modern calculation

methods adapted advanced industrial technologies, assisted by computing systems implemented

in countries with developed economies have become classics alternative calculation methods

applied in companies in Romania. This involves providing logistical and conceptual terms,

including opening to accept change management vision on the modernization of the company in

terms of organizational, technological, and managerial accounting.

AIMS AND OBJECTIVES OF THESIS

Field management accounting provides the opportunity for multiple experimental studies,

because of the possibility of choosing the organization and method of calculation.

Literature, quite rich in this area, providing sufficient opportunities both in terms of theoretical

research and practical. We believe that all these changes, both at the international level and

nationally, is both a cause and a challenge for any passionate researcher of the management

accounting. We approached this subject in order to consider the application of modern methods

of costing the aviation industry in Romania by example. New trends in the use of advanced

production technologies make it necessary to change the management accounting vision and

orientation to support management decisions. The research purpose is to improve the

methodology of cost calculation tackling the calculation in the aviation industry.

In this respect, the scientific approach is not limited to theoretical, but went on to check

the extent to which these methods can be applied in the study, with the advantages,

disadvantages compared to modern classical methods.

By conducting research we aimed to obtain answers to current issues in the field of

management accounting with an approach through the aviation industry.

For achieving the research purpose, we considered the following objectives:

- studying the conceptual stage current management accounting and cost calculation in

national and international literature;

- follow parts and evolution of management accounting in Romania;

- knowledge of the nature of the information provided by costing;

- Determining role in modernizing management control instruments accounting treatment

information;

- substantiation of managerial decisions based on the information on costs;

- implementation methodology lifecycle costs of products;

- presentation of classical, modern and advanced costing applied in Romanian companies

to identify their advantages and disadvantages;

- analyze the current situation and developments at global aerospace and European level;

- analyze the peculiarities of aerospace companies' activities in Romania;

- microenvironment analysis of a company producing aerospace systems;

- application of modern methods of costing the aerospace companies;

- proposal to modernize the management accounting by the method of costing Activity

Based Costing (ABC) in a company that manufacture aerostructures field;

- proposal for implementation of the method of costing Target Costing in the aviation

industry, aiming to maximize profit.

Thesis “Actualities and perspectives concerning methodology of costs calculation” treats

with a theoretical and practical approach following:

- the importance and role of management accounting in the management of companies;

- the quality of information provided by management accounting and costing;

- accuracy of the information provided by management accounting and costing, as

mainstay in decision making;

- the efficiency of traditional calculation methods in terms of the economic environment

characterized by competitiveness;

- the implementation of modern methods of costing the companies in Romania;

- receptivity companies to apply modern methods of costing;

- consequences costing method change in national enterprises.

THE METHODOLOGY OF SCIENTIFIC RESEARCH

Doctoral thesis was made based on the knowledge gained from the study of literature and

practical experience in aerospace, using three types of qualitative research, as follows:

theorizing, testing and precision.

The paper involved literature review, presentation and discussion of the current state of

knowledge to understand and explain theories, phenomena, existing concepts or to develop new

research, theories, concepts, methods and techniques of management accounting.

The developed theories or assumptions have been tested and verified in order to obtain answers

or feedback from other researchers, practitioners and the general public, this being achieved by

articles published in national conferences, international journals.

Both the theorization and testing must be performed exactly and precisely in order to achieve

quality research that is useful academia and practice.

Making a qualitative research involved the review of the theoretical background of the topic

studied or studying the behavior and practice existing methods within companies in Romania.

After setting objectives of the research topic, the next step of the scientific approach involved

identifying the type of research, qualitatively or quantitatively, which is most suitable for the

theme addressed.

Qualitative research are those that allow outline the main aspects of the problem or research

topic and diagnosis of the situation, identify hypotheses for future research descriptive.

Instead, quantitative investigations have the role to define, characterize and quantify relevant

aspects identified using qualitative methods, which are used to quantify certain phenomena, to

establish statistical data and to verify and test existing theories or developed using specific

methods.

Thus the specific and traits from field research, this scientific approach is in category of

qualitative research connected at the same time, quantitative elements.

1. Qualitative research concerns: conceptual analysis on companies and their role in the

development of the industry in which they operate; conceptual analysis of financial and

management accounting; presentation objectives and the role of management accounting and

cost calculation; analytical presentation and classification methods of costing identified at

international level; presenting ways to exploit the information provided by management

accounting and costing; emphasizing the role of management accounting and cost calculation in

the decision making process of each company.

2. Quantitative research concern: comparative studies on the evolution of the main

economic and financial company level, nationally and internationally; reflecting the current state

of research in management accounting and cost calculation in Romania; study aimed at tackling

the costing the aviation industry, methods of calculation and management tools used in the

Romanian companies. Research methods used in this scientific approach are: document analysis,

comparative method, participant observation and non-participating.

We can see that the research methods are a combination of the methods listed longitudinal

transverse, which are used to build a descriptive research, basing on theoretical and conceptual

aspects of management accounting, cost accounting, costing methods, ways the use of

information and their utility in decision making, to proceed to empirical research by studying the

behavior profile companies, national and international level, through the practices, methods of

calculation and management tools used.

Starting from the theories, concepts, models and existing methods and their practical

implementation, this research can be classified as research that is based on deductive approach,

but then go to the inductive approach, due to theoretical and conceptual transposition practical

issues identified.

Informational resources used in formulating this research include national and

international specialized books, scholarly articles published in reputable journals, recognized

national or international laws, regulations, national and international professional bodies, studies

and surveys conducted by various professional organizations .

SUMMARY OF MAIN PARTS OF DOCTORAL THESIS

In Chapter 1, "Conceptual delimitations concerning cost calculation" I approached the

theoretical concepts, typology and peculiarities cost calculation.

I also made a picture of the genesis and evolution of cost calculation both in Romania

and worldwide. Cost calculation supports the control processes and decision making, is a key

component of the company's management system.

The major conclusion of this chapter is that, given an efficient cost management system,

managers are able to integrate cost calculation and analysis of the company's strategic approach

to create a competitive advantage.

In Chapter 2, "New dimensions of a cost information in decision making" we turned to

the decision making process to analyze the multitude of decisions that can be taken based on cost

data type. Since the the overall activity of a company is represented by cost, they are the basis of

most decisions made by managers. Whether it aim to buy / sell at certain prices, whether they

will introduce / give up certain products in the portfolio, whether it be to improve certain

processes or production technologies, managers will always use costs. In this respect, as evident

from this chapter, a cost information is useful when managers offered to place and time.

The costs of decision-making

To make the right decision the manager must consider only the relevant expenditure, ie

raw materials, and indirect variable costs because they are avoidable, that would not occur if the

company does not manufacture these hydraulic systems.

Anlizând data in the table no. 1, that the alternative to hydraulic devices in the company

factory is cheaper to 748,000 lei (the difference between the total value acquisition and total

value our own production).

Table no. 1 Comparative data on the cost of in the decision making

Source: own calculations performed, the data are taken from www. Aerostar.ro

For decision making must consider only future costs, costs will depend on the decision,

and no costs will be used to assess the cost of production. Identifying costs depend on the

circumstances of the decision in a particular situation can be a cost associated, and another does

not.

In conclusion, it is impossible to determine the costs that will be associated in any case.

To identify them, should be know all the the circumstances in which the decision must be

brewed with the principle that the costs of those future costs that differ from one alternative to

another. Whenever circumstances change, the decision should be reviewed. Such circumstances

may include decreased demand or acquisition of additional capacity.

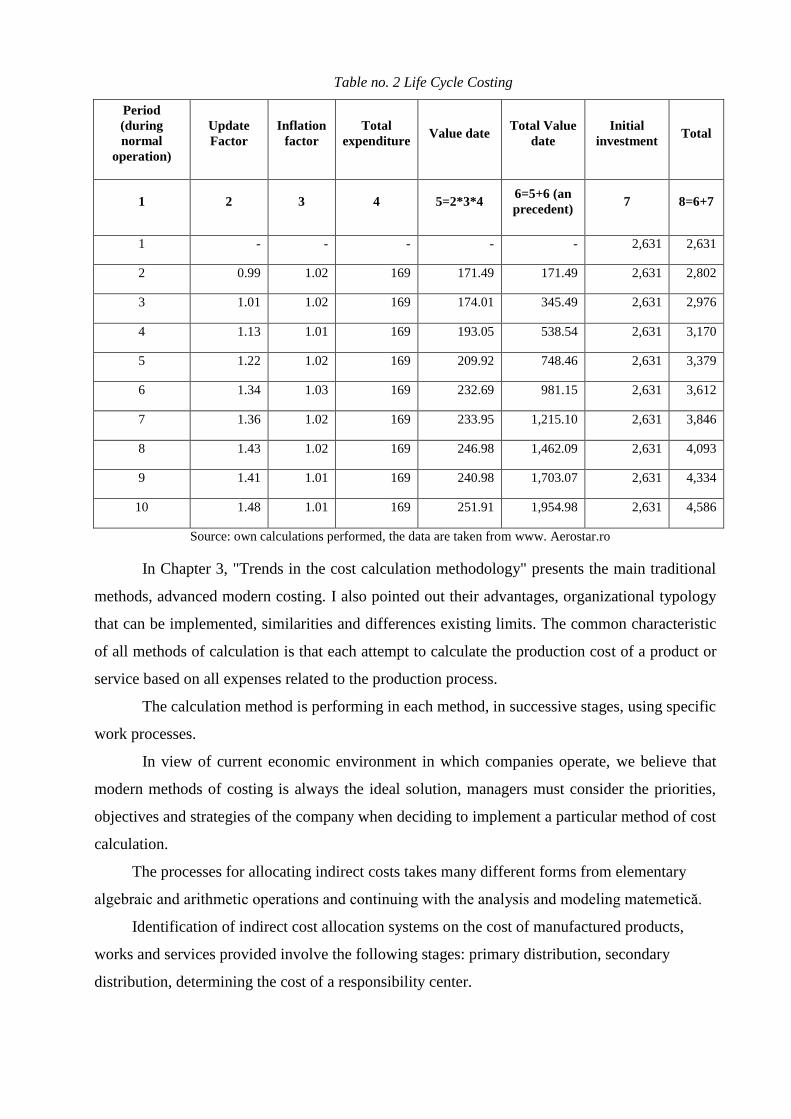

Life cycle cost methodology

In table no. 2 to calculate the life cycle cost of the product, the cost being determined by

adding the "initial investment" to "total value date".

Application of this methodology of calculation the following advantages:

- helps to better information for long-term investment decisions;

-the methodology is the basis pricing strategy, based on experience and learning;

- allow evaluation and comparison of alternative strategies for the use, operation, testing,

inspection and maintenance of products;

- facilitate evaluation and comparison of different approaches to replace, rehabilitate and extend

the useful life of products;

- focus on reducing the cost of logistics support.

No Name costs Total value of our

own production

Total value

acquisition

0 1 2 3

1 Raw materials and materials direct 1,804,000

2 Direct labor 706,000 706,000

3 Indirect variable costs 512,000

4 Fixed costs 428,000 428,000

5 Cost of acquisition 3,064,000

Total 3,450,000 4,198,000

Table no. 2 Life Cycle Costing

Period

(during

normal

operation)

Update

Factor

Inflation

factor

Total

expenditure Value date

Total Value

date

Initial

investment Total

1 2 3 4 5=2*3*4 6=5+6 (an

precedent) 7 8=6+7

1 - - - - - 2,631 2,631

2 0.99 1.02 169 171.49 171.49 2,631 2,802

3 1.01 1.02 169 174.01 345.49 2,631 2,976

4 1.13 1.01 169 193.05 538.54 2,631 3,170

5 1.22 1.02 169 209.92 748.46 2,631 3,379

6 1.34 1.03 169 232.69 981.15 2,631 3,612

7 1.36 1.02 169 233.95 1,215.10 2,631 3,846

8 1.43 1.02 169 246.98 1,462.09 2,631 4,093

9 1.41 1.01 169 240.98 1,703.07 2,631 4,334

10 1.48 1.01 169 251.91 1,954.98 2,631 4,586

Source: own calculations performed, the data are taken from www. Aerostar.ro

In Chapter 3, "Trends in the cost calculation methodology" presents the main traditional

methods, advanced modern costing. I also pointed out their advantages, organizational typology

that can be implemented, similarities and differences existing limits. The common characteristic

of all methods of calculation is that each attempt to calculate the production cost of a product or

service based on all expenses related to the production process.

The calculation method is performing in each method, in successive stages, using specific

work processes.

In view of current economic environment in which companies operate, we believe that

modern methods of costing is always the ideal solution, managers must consider the priorities,

objectives and strategies of the company when deciding to implement a particular method of cost

calculation.

The processes for allocating indirect costs takes many different forms from elementary

algebraic and arithmetic operations and continuing with the analysis and modeling matemetică.

Identification of indirect cost allocation systems on the cost of manufactured products,

works and services provided involve the following stages: primary distribution, secondary

distribution, determining the cost of a responsibility center.

A coherent system of performance measurement involves structuring the company's

responsibility centers.

This method of allocating primary and secondary costs enables rapid determination of

indirect costs per center and sector analysis of the company.

Allocation of indirect costs, regardless of the nature and content, is made properly if all the

following conditions:

- - Between base and distribution expenses allocated to have a positive relationship, a

relationship of interdependence, as the size of the share of indirect costs in a given category,

which returns the type of activity, sector or carrier costs, always depends on the size allocation

base that characterize in total bases. This condition can not be taken into account when allocating

the base is too small to shared expenses;

- allocation basis to be used to distribute a single or at most costs of a particular group

overheads constituted by the possibility distribution relative to said base;

- utilization of the allocation of costs to be possible under similar conditions, all or at least

most companies in a particular sector, in order to achieve comparability of costs between

companies with same activity;

- both in pre-calculated and after calculation, it is necessary to use the same basis of

apportionment of expenses to ensure comparability between actual costs and the pre-calculated;

- use of the bases of cost allocation , over a long period of time because changing it affects

comparability dynamic product cost.

Determining the cost of a unit of work is based on indirect costs related to major centers

and structure, the nature of which is determined by the specifics of each individual.

As can be seen in the table no. 3 cost of a unit of work is determined by dividing the total

indirect costs due to the secondary distribution, the number of work units consumed.

Table no. 3 Allocation of indirect costs

Source: own calculations performed, the data are taken from www. Aerostar.ro

No Explanations Amount of

distributed

Auxiliary centre The main centers The center of

the structure

Personnel

management

Connected

supply Supply Divizia 1 Divizia 2 Divizia 3 Selling Administration

0 1 2 3 4 5 6 7 8 9 10

1 Consumables 420,000 42,000.00 84,000.00 42,000.00 63,000.00 63,000.00 42,000.00 42,000.00 42,000.00

2 External services 240,000 36,000.00 60,000.00 36,000.00 24,000.00 24,000.00 24,000.00 24,000.00 12,000.00

3 Current repair costs 610,000 61,000.00 152,500.00 122,000.00 61,000.00 61,000.00 61,000.00 30,500.00 61,000.00

4 Taxes 120,000 18,000.00 30,000.00 - - - - - 72,000.00

5 Indirect labor 840,000 84,000.00 168,000.00 84,000.00 126,000.00 126,000.00 84,000.00 84,000.00 84,000.00

6 Maintenance costs 25,000 - - - 5,000.00 5,000.00 6,250.00 - 8,750.00

7 Other general costs 36,000 - - - - - - - 36,000.00

8 Depreciation of fixed assets 85,000 - 17,000.00 17,000.00 12,750.00 12,750.00 8,500.00 17,000.00 -

9 Total primary distribution 2,376,000.00 241,000.00 511,500.00 301,000.00 291,750.00 291,750.00 225,750.00 197,500.00 315,750.00

10 Distribution management

personal 0

-

327,552.00 65,510.40 16,377.60 98,265.60 16,377.60 65,510.40 49,132.80 16,377.60

11 Distribution connected

supplies 0 86,552

-

577,010.00 57,701.00 86,551.50 28,850.50 86,551.50 173,103.00 57,701.00

12 Total secondary

distribution 2,376,000 0 0 375,079 476,567 336,978 377,812 419,736 389,829

13 Nature unit of work (UBR)

units

bought spare parts hours car

products

obtained

products

sold

cost of

production

14 Number of units of

workers(UBR) 15,000 7,000 3,200 4,500 4,000 120

15 The cost per unit of work

(the cost of UBR) 20.07 41.68 91.17 50.17 49.38 2,631.25

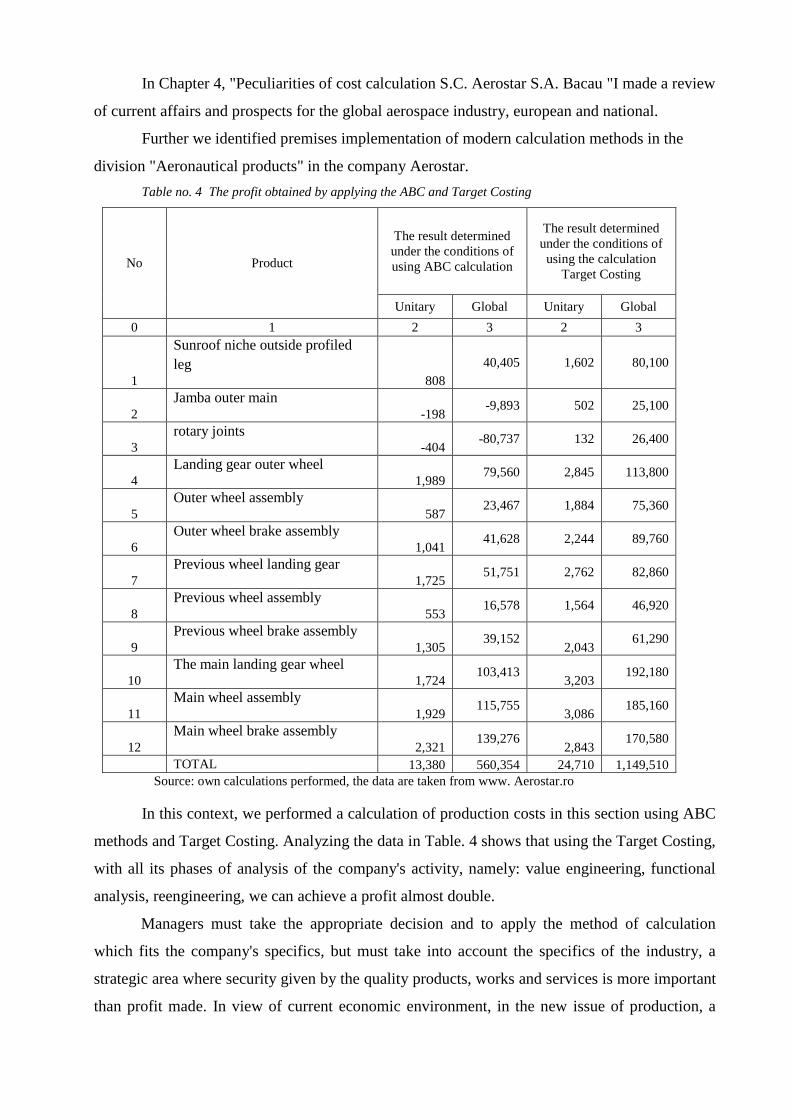

In Chapter 4, "Peculiarities of cost calculation S.C. Aerostar S.A. Bacau "I made a review

of current affairs and prospects for the global aerospace industry, european and national.

Further we identified premises implementation of modern calculation methods in the

division "Aeronautical products" in the company Aerostar.

Table no. 4 The profit obtained by applying the ABC and Target Costing

No Product

The result determined

under the conditions of

using ABC calculation

The result determined

under the conditions of

using the calculation

Target Costing

Unitary Global Unitary Global

0 1 2 3 2 3

1

Sunroof niche outside profiled

leg 808

40,405 1,602 80,100

2

Jamba outer main -198

-9,893 502 25,100

3

rotary joints -404

-80,737 132 26,400

4

Landing gear outer wheel 1,989

79,560 2,845 113,800

5

Outer wheel assembly 587

23,467 1,884 75,360

6

Outer wheel brake assembly 1,041

41,628 2,244 89,760

7

Previous wheel landing gear 1,725

51,751 2,762 82,860

8

Previous wheel assembly 553

16,578 1,564 46,920

9

Previous wheel brake assembly 1,305

39,152 2,043

61,290

10

The main landing gear wheel 1,724

103,413 3,203

192,180

11

Main wheel assembly 1,929

115,755 3,086

185,160

12

Main wheel brake assembly 2,321

139,276 2,843

170,580

TOTAL 13,380 560,354 24,710 1,149,510

Source: own calculations performed, the data are taken from www. Aerostar.ro

In this context, we performed a calculation of production costs in this section using ABC

methods and Target Costing. Analyzing the data in Table. 4 shows that using the Target Costing,

with all its phases of analysis of the company's activity, namely: value engineering, functional

analysis, reengineering, we can achieve a profit almost double.

Managers must take the appropriate decision and to apply the method of calculation

which fits the company's specifics, but must take into account the specifics of the industry, a

strategic area where security given by the quality products, works and services is more important

than profit made. In view of current economic environment, in the new issue of production, a

technologies and computerization, companies in the aviation industry must adopt a series of

policies concerning production and activity costing follows:

- volume of production must be based on orders received from customers, profitability is

determined by how quickly the finished products can be obtained to meet customer orders;

- management of companies have focused on elements "key" in making profits, reduce

inventory and response time to customer requests;

- to facilitate the operations of collection, centralization and data processing operations

concerning record indicated that consumption of stocks does not occur as they occur, but when

the finished products are produced or sold; because such an approach does not generate wrong

information should be made based on forecast production volume orders received from

customers;

- the total elimination of waste in all stages of the manufacturing process, from design to

delivery, through a process of continuous improvement;

- maintaining a high level on product quality, product quality is given by the raw materials used

and the continuous inspection activities of the production process in the order to extract and

eliminate any irregularities;

- should be encouraged continuous improvement of labor, cultivation correctness employees;

they are considered part of a team, being deeply involved in the production process;

- to your attention must be product managers but not the process, and this process is the most

important dimension of organizational, ie the ability to communicate;

- considering that the new production environment has significantly reduced the number of direct

labor hours and expenses concerning labor force indicators essential in determining the cost of

production, it is necessary to use different methods of allocating indirect costs, traditional

calculation of production costs are not an alternative due to instability in time and space

production and management priori impossibility of production;

- increasing importance indicator "number hour car" rather than "number of direct labor hours"

in this context to determine indirect cost allocation rates used term "theoretical capacity".

CONCLUSIONS AND PROPOSALS

The paper "Actualities and perspectives concerning methodology of costs

calculation" during the course of the research imposed the involvement of several disciplines:

accounting basis, financial accounting, management accounting, financial analysis, management,

computer science, economics and statistics features of the aviation industry.

In the study we addressed the application of principles of management accounting and

cost calculation in the aviation industry.

From the analysis were drawn the following conclusions:

1. Management accounting has been an ascending evolution in the role of collecting

information on costing, to support the information in making management decisions.

Managerial decisions for determining the medium and long term strategies are based on a

cost provision of information in a short time.

The new targets are set, adapted their methods of calculation and determined human,

material and time needed to implement management option and plans to improve existing work.

At present the following trends are emerging regarding management accounting:

• management accounting is considered as an integrated system;

• the existence of divergent views regarding the application tier accounting system

using management accounts;

• use of information lead to addressing limiting costing methods adapted model of

automatic data processing;

• application of modern methods of costing information to provide a cost in real time;

• the creation of modern software to allow full implementation of calculation methods,

involving a large number of specialists in different fields of activity: production,

technological knowledge of all phases, specialists in economics and accounting,

calculation methods for implementation cost information system programmers to

create characteristic industry, specialists in marketing and management;

Financial Accounting by economic circumstances - it generates financial, operating

expenses and financial centralized as it is the basis on which costs and extraordinary ones are not

taken into account as cost elements.

Financial accounting is an observation of economic phenomena while management

accounting, studying in detail all aspects of the cost and proposed management and control

models and solutions to eliminate disturbing phenomena of company activity.

2. Identifying the consequences of implementing modern methods of costing in a

company in the aviation industry

Field of aerospace implies a changing and diversifying attributed satisfy desires,

preferences, needs and requirements of customers growing. Aircraft production worldwide has

been characterized in recent decades by a tendency to concentrate producers, through mergers

and acquisitions, the need to develop new and innovative solutions in increasingly complex

technically, to meet customers regarding their safety and comfort.

Under the conditions of current business environment aviation industry companies should

consider:

- technical and technological restructuring of production activities as a factor for

determining the company's efficiency, increase competitiveness and to face competition in

domestic and foreign market. The main objective of general strategic production is the

rehabilitation departments in order to increase the quality of manufactured products given the

competitive conditions and the particular importance it manifests company.

- typology of market relations - production due to barriers imposed by national authorities

which establish joint production capacity oriented regional development. From the need to have

a complete and accurate quantification of costs, relevant and analysis exercise, establishing

deviations and activities generating additional costs, proposing measures to improve and correct

slippages in real time are processes that occur for implementation modern methods of costing.

3. The benefits of applying modern methods of cost calculation

Modern methods of cost calculation changing vision company accounting organization,

and the organization of information flows. There are several methods of cost calculation that

occurred in response to management accounting in technical and technological progress, the

need to provide timely accounting information to decision makers. Among modern methods of

cost calculation addressed in this thesis are: methods Activity Based Costing (ABC), Target

Costing and Kaizen Costing.

Applying modern methods of cost calculation bring important advantages in managing

the company's situation by identifying cost centers and cost information system strategies.

These methods have the basic principle analysis of activities and processes of the cost,

which changes the traditional optical methods. In this context, not products or services at a cost,

but the activities and processes. Another important aspect is the monitoring of indirect costs,

identify sources that generate them, and activities that trigger them. You have exceeded mere

phase costing to cost-effectively manage torque performance that must make the transition from

AB.C. the A.B.M .

In addition, past the simple cost analysis to develop a management control directly

related to the strategies adopted by management. Production systems are influenced by factors

derived from the global economy in recent years. These factors evidently put their mark on the

organization of industrial production. Globalization has determined a change of option buyers

due to increased access to information and their choices are influenced and changed quickly.

Managers must take into account the progress of informatics and virtual communication so must

constantly adapt products and services and meet customer requirements.

The formation of partnerships in the supply chain is an effective way to ensure the necessary

resources, especially since half of the built-in products and services comes from suppliers.

Suppliers should be selected so as to be able to respond and they diversified requirements on the

content and structure of materials.

Reducing stocks is important because businesses are investing significant financial resources in

stocks and growth stocks value slows the possibility of effective responses to market

requirements.

Product development is determined by the development of communication systems. Companies

can easily find out what are the trends in consumer preferences and adapt products or services to

them.

The mass production on order is a variation order to respond to certain categories of

customers, no matter what region is, however, managers must redesign the technological

production so as to respond quickly to specific requests.

Users are increasingly aware that their options are particularly important for productive

companies, such production must face the pressures of increasingly high.

Delegation of authority to subordinates is important for enhancing the efficiency of

production and implementation of modern methods of cost calculation, but this involves a high

level of staff training and institutional ethics well implemented.

Each employee who is in a leadership position should be responsible and interested in

increasing company productivity. Quality of products and services is a basic concept in the

aviation industry, which is a strategic area.

Using modern methods of cost calculation the following advantages:

• shows a high flexibility in the allocation of costs on areas of interest (customers,

products, profit centers, etc.);

• offers relevant information on the long-term variable costs that are useful to managers

in order to take strategic decisions;

• Indirect costs can be individualized product in modern factories there are a growing

number of non-productive activities;

• provide useful financial measures (factors, criteria of cost) and non-financial

measures;

• focus on early stage development costs - product design;

The limits of these methods relate to:

• weight collecting adequate information on certain activities that cross the boundaries

of departments of enterprises;

• high employment levels during all phases of development (design, implementation,

control).

• the heavy workload both in the implementation phase and in the application;

• existence of priorities for the conduct of the company's current activity on the

classical model.

4. Software and management accounting

Using accounting software has become a reality in all Romanian companies. Product

market specializing in accounting, financial especially is highly developed. Specialists in

informatics offer products increasingly more efficient at prices ever lower. Most programs are

made with modules that meet the requirements of financial accounting, management accounting

is a relatively underdeveloped. This is easy to understand, because of the confidential nature of

management accounting firms producing accounting software are keen to include a broader

market as buyers and to offer products with a high degree of generality, specific financial

accounting. Creating a software for management accounting requires high costs because the

design is enforcing teams of specialists in various fields, with command of profile activity to

study long specifics of management accounting. Costs are high, given that each company can opt

for a method of calculation imposed by several factors specific to each company (character

production method of organization). Basically it performs a software product for a company or

an industry.

Standard accounting programs used by companies have a predefined set of menus that

can not be changed after the needs and specific activity. Such programs provide an important aid

in the efficiency of processing, but the information provided limits, especially in terms of

management accounting.

The software on the market offers many advantages on bookkeeping, among which:

- reducing the time of data collection of documents;

- the creation and organization of databases, the management, suppliers, customers;

- generating financial reports - accounting;

- automatic generation of accounting records;

- automatic generation of annual financial statements;

- making comparative analysis of financial indicators;

- generating fiscal declarations.

Bookkeeping using automated technique is effective, but the set of information generated

by programs is post factum and record documents after conducting production processes, without

giving managers the opportunity to correct certain deficiencies in real time.

There isn't effective communication between financial and accounting records,

production and management activities as in relation to management and management accounting,

financial accounting functions in a relatively independent manner. In recent years began to

develop integrated systems management company that provides business process monitoring all

access the same database for all departments. The visibility of the company's business is global,

and decisions are based on access to complete and complex databases.

5. Author's own contributions concerns:

• designing a synthesis of elements that have characterized the evolution of the concept

of cost to ensure that traditional cost calculation methods applied in companies can be

improved and have many limitations, using an approach from past to present, from

international to national level;

• present the main contributions of the literature, the development of knowledge in the

topic;

• presentation of case studies on different issues of costing, both conceptually and in

practical terms;

• identify the main trends that have marked the evolution from traditional cost

accounting to modern methods applied in an environment of advanced technologies;

• identify the main limitations of traditional management accounting in relation to

modern methods of management accounting costing;

• description of the organization of management accounting in the company SC

Aerostar SA and propose solutions by applying modern costing;

• conclusions and proposals to develop and improve the efficiency of the company SC

Aerostar etc .;

• make an analysis economic - financial the key indicators were calculated both at

company level and at national level, the field;

• conducting a study on the current situation of the aviation industry, global, European

and national level;

• conducting practical studies on costing methods Activity Based Costing (ABC) and

Target Costing;

• conducting a study comparing modern calculation methods implemented in a sector

of the company.

6. Suggestions for improving the activity in the company studied

From studies that applied to streamline the company's business managers must address a

new optic regarding the organization and functioning of management accounting, with direct

implications in decision making at different hierarchical levels, as follows:

• increase the use of type information provided by management accounting cost for

analyzing the efficiency of the company and their products;

• modernization of production technologies to increase business efficiency, product

quality;aplicarea unor metode moderne de calculaţie a costurilor pentru a se obţine

informaţii de tip cost în timp util, în timpul desfăşurării proceselor productive în

vederea ameliorării deficienţelor;

• reorganization of management accounting in terms of the treatment of indirect costs

and streamline support activities;

• the use of advanced computer programs that facilitate increased efficiency costing

information system;

• modernization of strategic and operational management for better resource

management to reduce costs;derularea de programe de formare profesională a

personalului pentru creşterea gradului de implicare în activităţile companiei;

• development and implementation of marketing strategies.

7. Perspectivele cercetării

• to promote the usefulness of management accounting as actual support management

decisions;

• promoting the business of modern concepts of management accounting methods;

• analysis methods to reduce costs by applying modern methods of management

accounting;

• study of the effects generated by the use of modern methods of management

accounting;

• development of management accounting modules of the system software to develop

integrated accounting information system and increase connections with other specialized

information systems within the company.

In this context, we emphasize that the management accounting and cost calculation in

terms of value is the modeling of resources related to the objectives of the company.

Manager must adapt to future changes, accepting uncertainty, requiring reflection

convinced that: "If it moves quickly, any company can suddenly discover that its cars are

obsolete. But more dangerous than cars are rusted rusty ideas. In today's ever-changing climate,

can it really an organization to remain adaptable ideas of yesterday? "

BIBLIOGRAPHY

BOOKS

1. Achim S.A., Contabilitate pentru manageri, Editura Risoprint, Cluj-Napoca, 2009

2. Alazard C., Separi S., Contrôle de gestion, Manuel Applications, Editura Dunod, Paris, 1998

3. Albu N., Albu C., Instrumente de management al performanţei, vol. I şi II, Editura

Economică, Bucureşti, 2003

4. Albu N., Albu C., Soluţii practice de eficientizare a activităţilor şi de creştere a performanţei

organizaţionale. Gestiunea dezvoltării durabile prin Balanced Scorecard, Editura CECCAR,

Bucureşti, 2005

5. Allen B.R., Brownlee E., Cases in Management Accounting and Control Systems, 4th

edition,

Prentice Hall, 2004

6. Almăşan A.C., Contabilitatea de gestiune în industria comunicaţiilor, Editura Mirton,

Timişoara, 2010

7. Andone I., Tabără N., Contabilitate, tehnologie şi competitivitate, Editura Academiei Române,

Bucureşti, 2006

8. Anthony R.N., Govindarajan V., Management Control Systems, 12th

Edition, Editura McGraw

– Hill, International Edition, 2007

9. Anthony R.N, The Management Control Function, Harvard University Press, Boston, 1988

10. Baciu A., Duția T., Sistemul informațional integral al costurilor, Editura Dacia, Cluj-Napoca,

1981

11. Bauman Z., Globalizarea şi efectele ei sociale, Editura Antet, Bucureşti, 1999

12. Berliner, C., Brimson, J.A., Cost management for today’s advanced manufacturing ,The

CAM-1 Conceptual Design, Harvard Business School, Boston, 2007

13. Berry A.J., Broadbent J., Otley D., Management control. Theories, Issues and Performance,

Second Edition, Palgrave Macmillan, 2005

14. Boisselier P., (Coordinateur), Contrôle de gestion, Vuibert, Paris, 2013

15. Borcea D., Contabilitatea industrială şi planul de conturi, Editura Didactică și Pedagogică,

București, 1943

16. Bouquin H., Contabilitate de gestiune, traducere şi studiul introductiv Tabără N, Editura

TipoMoldova, Iaşi, 2004

17. Bouquin H., Comptabilité de gestion, 3e édition, Edition Economica, Paris, 2004

18. Bouquin H., Le contrôle de gestion en milieu ou en situation spécifique, filière Master CMA

Dauphine, 2006-2007

19. Bordei D., Tehnologia modernă a panificaţiei, Editura Agir, Bucureşti, 2005

20. Briciu S., Sistemul informaţional privind contabilitatea de gestiune şi calculaţia costurilor în

industrie, Editura Argus, Bucureşti, 2000

21. Briciu S., Burja V., Contabilitatea de gestiune. Calculaţia şi analiza costurilor, Editura Ulise,

Alba Iulia, 2004

22. Briciu S., Jaradat M.H., Socol A., Teiuşan S.C., Managementul prin costuri, Editura

Risoprint, Cluj-Napoca, 2005

23. Briciu S., Tamas S.A., Dobra I.B., Sas F., Contabilitatea managerială a firmelor din comerţ,

Editura Risoprint, Cluj-Napoca, 2005

24. Briciu S., Contabilitate managerială. Aspecte teoretice şi practice, Editura Economică,

Bucureşti, 2006

25. Briciu S., Căpuşneanu S., Rof M.L, Topor D., Contabilitatea şi controlul de gestiune,

instrumente pentru evaluarea performanţei calităţii, Editura Aeternitas, Alba Iulia, 2010

26. Budugan D., Georgescu I., Berheci I., Beţianu L., Contabilitate de gestiune, Editura

CECCAR, Bucureşti, 2007

27. Budugan D., Contabilitate şi control de gestiune, Editura Sedcom Libris, Iaşi, 2002

28. Buglea A., Analiză financiară, Concepte şi studii de caz, Editura Mirton, Timişoara, 2005

29. Burlaud A., Simon C.J., Comptabilité de gestion, 3e édition, Vuilbert, Paris, 2003

30. Burlaud A., Simon C.J., Comptabilité de gestion, coûts/contrôle, 2e édition, Librairie Vuibert-

Février, Paris, 2000

31. Burlaud A., Simon C.J., Controlul de gestiune, traducere Corina Lascu Cilianu, Editura CNI

Coresi, Bucureşti, 1999

32. Caraiani C., Dumitrana M. (coord.), Contabilitate de gestiune şi Control de gestiune, Ediţia a

II-a, Editura InfoMega, Bucureşti, 2005

33. Caraiani C., Dumitrana M. (coord.), Control de gestiune, Editura Universitară, Bucureşti,

2010

34. Călin O, Ristea M., Bazele contabilităţii, Editura Naţional, Bucureşti, 2000

35. Călin O., Man M., Manolescu M., Călin C.F., Contabilitatea de gestiune şi calculaţia

costurilor”, Editura Tribuna Economică, Bucureşti, 2005

36. Călin C. (coord.), Contabilitate managerială, Editura Didactică şi Pedagogică, Bucureşti,

2008

37. Călin O., Contabilitate managerială, Editura Didactică şi Pedagogică, Bucureşti, 2008

38. Călin O., Contabilitate de gestiune, Editura Economică, Bucureşti, 2002

39. Căpuşneanu S., Contabilitate de gestiune şi calculaţia costurilor. Aplicaţii, Ediţia a II-a,

Editura Economică, Bucureşti, 2003

40. Cârstea Gh., Călin O., Calculaţia costurilor, Editura Didactică și Pedagogică, București, 1980

41. Chadwick L., Contabilitate de gestiune, Editura Teora, Bucureşti, 2008

42. Chatfield M., The Origins of Cost Accounting, Management Accounting, 1971

43. Ciobanu I., Managementul strategic, Editura Polirom, Iaşi, 1998

44. Colasse B., Fundamentele contabilităţii, traducere Tabără N., Editura TipoMoldova, Iaşi,

2009

45. Colasse B., Introducere în contabilitate, traducere Tabără N., Editura TipoMoldova, Iaşi, 2011

46. Collette Cr., Richard J., Comptabilité générale, Dunod, Paris, 2000

47. Collis J., Hussey R., Business Accounting, an introduction to financial and management

accounting, Palgrave Mac Millan, New York, 2007

48. Coombs H., Hobbs D., Management Accounting. Principles and Applications, SAGE, Jenkins

E. Publications Ltd., London, 2005

49. Coude R., Molès, A., Méthodologie vers une science de l’action, Entreprise Moderne

d’Édition, Paris, 1964

50. Cristea H., Contabilitatea şi calculaţiile în conducerea întreprinderii, Ediţia a II-a, Editura

CECCAR, Bucureşti, 2007

51. Cristea H., Ghid pentru înţelegerea și aplicarea Standardelor Internaţionale de Contabilitate,

Stocuri, Editura CECCAR, București, 2004

52. Crum L.W., Ingineria valorii, Editura Tehnică, Bucureşti, 1976

53. Cucui I., Man M., Costurile şi contabilitatea de gestiune, Editura Economică, Bucureşti, 2004

54. Dashchenko A., Reconfigurable manufacturing systems and transformable factories, Springer,

Netherlands, 2006

55. Deaconu S.C., Îndrumar în contabilitate, Editura Universitară, Bucureşti, 2008

56. Deaconu A., Valoarea justă – concept contabil, Editura Economică, Bucureşti, 2009

57. Demeestère R., Lorino R., Mottis N., Contrôle de gestion et pilotage de l’entreprise, 2e

édition, Dunod, Paris, 2002

58. Demeestère R., Comptabilité de gestion et mesure de performances, Dunod, Paris, 2004

59. Demetrescu C.G., Istoria contabilităţii, Editura Ştiinţifică, Bucureşti, 1972

60. Deshayes C., Contrôle de gesion. Gestion prévisionnelle et contrôle budgétaire, Aengde/Clet,

Paris, 1991

61. Diaconu I., Costuri, preţuri și tarife în economia modernă, Editura Tradiţie, București, 1997

62. Diaconu P., Contabilitate managerială, Editura Economică, Bucureşti, 2002

63. Diaconu P. (coord.), Contabilitate managerială aprofundată, Editura Economică, Bucureşti,

2003

64. Doupnik T., Perera H., International Accounting, McGraw-Hill, South Carolina, 2006

65. Drăgan C.M., Sistemul costurilor normate, Editura Politică, București, 1985

66. Drury C., Management and Cost Accounting, 6th

Edition, Thomson Learning, London, 2006

67. Dubrulle L., Comptabilite de gestion, Economica, Paris, 2002

68. Dubrulle L., Contabilitate de gestiune, traducere şi revizie ştiinţifică Dumitrana M.,

Coordonatori: Niculescu M., Burlaud A., Editura Economică, Bucureşti, 2002

69. Dumbravă P., Pop At., Contabilitatea de gestiune în industrie, ediţia a II-a, actualizată şi

completată, Editura Intelcredo, Cluj-Napoca, 2011

70. Dumitru M., Calu D. A., Contabilitatea de gestiune şi calculaţia costurilor, Editura Contaplus,

Bucureşti, 2008

71. Dumitru C.G., Doros A., Accounting. Solved problems, applications, case studies, Editura

Universitară, Bucureşti, 2011

72. Dumitru C.G., Ioanăş C., Contabilitatea de gestiune şi evaluarea performanţelor, Editura

Universitară, Bucureşti, 2005

73. Dumitru C.G., Lepădatu Gh., Samara S., Contabilitate - probleme rezolvate, studii de caz,

Editura Universitară, București, 2009

74. Dumoulin C., Management des systèmes d’information, Editions d’Organisation, Paris, 1986

75. Dykman Th.R., Bierman Jr. H., Morse D.C., Cost Accounting. Concepts & Managerial

Applications, Second editionm College Division, South-Western Publishing Co., Cincinnati,

Ohio, 1994

76. Ebbeken K., Possler L., Ristea M., Calculaţia şi managementul costurilor, Editura Teora,

Bucureşti, 2006

77. Edmonds Th.P., Edmonds C.D., Olds Ph.R, McNAir F.M., Tsay B.Y., Schneider N.W.,

Milans E.E., Fundamental Financing and Manageriale Accouting Concepts, McGraw-Hill

Irwing, New York, 2007

78. Emery F.E., Organizational Planning and Control Systems, Teory and Technology,

Macmillan, New York, 1969

79. Epuran M., Băbăiţă V., Grosu C., Contabilitate şi control de gestiune, Editura Economică,

Bucureşti, 1999

80. Eros – Stark L., Pântea I.M., Analiza situaţiei financiare a firmei, Editura Economică,

Timişoara, 2001

81. Feleagă N., Îmblânzirea junglei contabilităţii, Editura Economică, Bucureşti, 1996

82. Firescu V., Contabilitatea de gestiune, Editura Tribuna Economică, București, 2006

83. Fleichman R., Tyson Th., Cost Accounting during the Industrial Revolution: The Present State

of Historical Knowledge, The Economic History Review, 1992

84. Garner P., Historical Development of Cost Accounting. The Accounting Review, 1947

85. Garrison H.R., Managerial accounting concepts for planning, control decision making,

Editura Irwin, Boston, 1998

86. Garrison H.R., Ray H., Noreen E.W., Managerial accounting, McGraw-Hill, Boston, 2003

87. Gervais M., Contrôle de gestion et planification de l`entreprise, 3e edition, Economica, Paris,

1990

88. Gervais M., Contrôle de gestion, 8e édition, Economica, Paris, 2005

89. Giroux, G., American Big Bussines and Cost Acounting, 1980

90. Glyn J., Murphy M., Perrin J., Abraham A., Accounting for managers, Cengace Learning,

Third Edition, 2003

91. Gowthorpe C., Business Accounting and Finance, First edition, Thomson Learning, London,

2003

92. Grosanu A., Calculaţia costurilor pe centre de profit, Editura Irecson, Bucureşti, 2010

93. Grosu C., Contabilitate de gestiune, Editura Mirton, Timişoara, 2003

94. Guedj N. (coordinateur) et al., Le contrôle de gestion, Pour améliorer la performance de

l’entreprise, Editions d’Organisations, 3e édition, Paris, 2001

95. Gutierrez F., Cost and Management Accounting in Preindustrial Revolution Spain.

Accounting Historians Journal, 2005

96. Hansen Don R., Mowen, M.M., Management Accouting, 2nd

Edition, College Division South-

Western Publishing Co, Cincinnati, Ohio, 1992

97. Harrington H.J., Harrington J.S., Management total în firma secolului XXI, Editura Teora,

Bucureşti, 2000

98. Hawkins A., 100 idei geniale de reduceri de costuri de la companii de top din întreaga lume,

Editura Adevărul Holdings, Bucureşti, 2010

99. Hlaciuc E., Metode moderne de calculaţie a costurilor, Editura Polirom, Iaşi, 1999

100. Horngren, C.T., Foster, G., Cost Accounting, A Managerial Emphasis, 7th edition, Prentice

Hall, 2007

101. Horomnea E., Fundamentele ştiinţifice ale contabilităţii. Doctrină. Concepte. Lexicon, Editura

TipoMoldova, Iaşi, 2008

102. Horomnea E., Tabără N., Georgescu I., Budugan D., Beţianu L., Bazele contabilităţii:

concepte, modele, aplicaţii, Editura Sedcom Libris, Iaşi, 2008

103. Horomnea E., Dimensiuni ştiinţifice, sociale şi spirituale în contabilitate. Geneză, doctrină,

normalizare, decizii, Ediţia a II-a, Editura TipoMoldova, Iaşi, 2011

104. Horomnea E., Tabără N., Georgescu I., Istrate, C., Budugan D., Beţianu L., Dicu R.,

Introducere în contabilitate, Editura TipoMoldova, Iaşi, 2012

105. Hoyle B.J., Schaefer Th., Doupnik T., Fundamentals of Advanced Accounting, Second

Editions, McGraw-Hill Education, Richmond, 2006

106. Horváth & Partners, Controlling, sisteme eficiente de creştere a performanţelor firmei, Ediţia

a II-a, Editura C.H. Beck, Bucureşti, 2009

107. Iacob C., Contabilitatea gestiunii interne a unităților economice, Editura Certi, Craiova, 1994

108. Iacob C., Drăcea R.M., Contabilitate analitică şi de gestiune, Editura Tribuna Economică,

Bucureşti, 1998

109. Iacob C., Ionescu I., Controlul de gestiune la nivelul firmei, Editura Tribuna Economică,

Bucureşti, 1999

110. Innes J., Handbook of Management Accounting, Elsevier CIMA Publishing, Oxford, 2004

111. Ionaşcu I., Dinamica doctrinelor contabilităţii contemporane. Studii privind paradigmele

contabilităţii, Editura Economică, Bucureşti, 2003

112. Ionaşcu I., Filip A.T., Mihai S., Control de gestiune, Editura Academiei de Studii Economice,

Bucureşti, 2001

113. Ionaşcu I., Filip A.T., Mihai S., Control de gestiune, Ediţia a II-a Editura Economică,

Bucureşti, 2006

114. Ionete E., Ghid de bune practici pentru siguranţa alimentelor, Editura Uranus, Bucureşti,

2005

115. Istrate C., Contabilitatea nu-i doar pentru contabili!, Editura Universul Juridic, Bucureşti,

2010

116. Jiambalvo J., Managerial accounting, 4th

edition, Wiley&Sons Ltd., London, 2006

117. Jones M., Accounting, Second Edition, Cardiff Bussiness School, John Wiley & Sons ltd.,

Cardiff , 2006

118. Kaplan R.S., Atkinson A.A., Advanced management accounting, 3rd

edition, Prentice Hall

International, 1989

119. Kinney M.R., Kinsey J.P., Raiborn C.A., Cost Accounting, Thomson/Southwestern, 2006

120. Lauzel P., Compatibilité analytique et contrôle de gestion, Sirey, Paris, 1964

121. Lauzel P., Bouquin H., Contrôle de gestion et budgets, 7e édition, Sirey, Paris, 1997

122. Lauzel P., Bouquin H., Comptabilité analitique et gestion, 4 édition, Editions Sirey, Paris,

1985

123. Lawrence D.M., Tehnici ale analizei şi ingineriei valorii, Editura Tehnică, Bucureşti, 1979

124. Lesnard C., Organisation & Gestion de l’Entreprise, Dunod, Paris, 1991

125. Lorino P., Le contrôle de gestion stratégique. La gestion par les activités, Dunod, Paris, 1991

126. Lucey T., Management Accounting, 3rd

Edition, D.P. Publications, London, 1992

127. Mahoney S., English for Accounting, Editura All, Bucureşti, 2009

128. Malo J.L., Mathé J.C., L’essentiel du contrôle de gestion, Deuxième édition, Editions

d’Organisation, Paris, 2002

129. Manolache M., Propunere plan unitar de conturi, Editura Economică, Braşov, 1947

130. Marinescu I., Preţurile și interdependenţa lor, Editura Academiei Române, Bucureşti, 1982

131. Mateş D., Matiş D., Cotleţ D., Pereş C., Dumitrescu A., Domil A., Şteţ M., Contabilitatea

financiară a entităţilor economice, Editura Mirton, Timişoara, 2006

132. Mateş D. (coord.), Contabilitate financiară – Concepte de bază. Tratamente specifice. Studii

de caz, Editura Mirton, Timişoara, 2010

133. Matiş D., Bazele contabilităţii. Fundamente şi premise pentru un raţionament profesional

autentic, Editura Casa Cărţii de Ştiinţă, Cluj, 2010

134. Matiş D., Pop A., Contabilitate financiară, Ediţia a III-a, Editura Casa Cărţii de Ştiinţă, Cluj,

2010

135. Melyon G., Comptabilité analytique – principes, techniques et évolutions, Éditions ESKA,

Paris, 1994

136. Melyon G., Comptabilité analytique, 3 édition, Éditions Bréal, Paris, 2004

137. Michailesco C., Contribution a l’etude des determinants de la qualite de l’information

comptable diffusee par les entreprises francais, Universite de Paris Daufine, Paris, 1998

138. Mihăescu S.V., Controlul financiar în firme, bănci, instituţii, Editura Sedcom Libris, Iaşi,

2007

139. Militaru Gh., Managementul producţiei şi al operaţiunilor, Editura All, Bucureşti, 2008

140. Minu M., Contabilitatea ca instrument de putere, Editura Economică, București, 2002

141. Mintzberg H., Structure et dinamique des organisations, Editions D′Organisations, Paris,

2000

142. Mocanu M., Contabilitate de gestiune, Editura TipoMoldova, Iași, 2013

143. Moreno P., Begona M., Cost accounting in eighteen century Spain: The Rozal Textile factory

of Ezcaray, Accounting History, 2001

144. Morse W.J., Davis J.R., Hartgraves Al.L., Management Accounting. A Strategic Approach,

Second Edition, South Western College Publishing, Thomson Learning, United States, 2000

145. Munteanu I., Ioniţă V., Managementul cunoştinţelor - Un ghid pentru comunităţile de

practicieni, Editura Cartier, Chişinău, 2005

146. Needles Jr. B.E., Anderson, H.R., Caldwell, J.C., Principiile de bază ale contabilității,

traducere Levițchi, R., Editura ARC, Chișinău, 2000

147. Evian I.N., Contabilitatea industrială, Editura Didactică și Pedagogică, Bucureşti, 1947

148. Nikitin M., La naissance de la comptabilité industrielle en France, Thèse pour le Doctorat ès

sciences de gestion, Université de Paris-Dauphine, 2 tomes, 1992

149. Olariu C., Studiu costurilor. Teoria, calculaţia şi informaţia costurilor, Editura Didactică şi

Pedagogică, Bucureşti, 1971

150. Olariu C., Costul şi calculaţia costurilor, Editura Didactică şi Pedagogică, Bucureşti, 1977

151. Olariu C., Conducerea întreprinderii prin costuri, Editura Facla, Timișoara, 1975

152. Oprea C., Cârstea Gh., Contabilitate de gestiune şi calculaţia costurilor, Editura Genicod,

Bucureşti, 2002

153. Oprea C., Man M., Nedelcu M.V., Contabilitate managerială, Editura Didactică şi

Pedagogică, Bucureşti, 2008

154. Oprea D., Protecţia şi siguranţa informaţiilor, Editura Polirom, Iaşi, 2007

155. Oprea D., Meşniţă G., Dumitriu F., Analiza sistemelor informaţionale, Editura Universităţii

“Alexandru Ioan Cuza”, Iaşi, 2009

156. Oprea D., Analiza şi proiectarea sistemelor informaţionale economice, Editura Polirom, Iaşi,

1999

157. Oprea D., Premisele şi consecințele informatizării contabilității, Editura Graphix, Iași, 1994

158. Onofrei M., Management financiar, Ediţia a II-a, Editura C.H. Beck, Bucureşti, 2007

159. Paraschivescu M.D., Radu F., Managementul contabilităţii financiare, Editura Tehnopress,

2008

160. Păvăloaia W., Paraschivescu M.D., Olaru G.D., Radu F., Contabilitate financiară. Aplicaţii şi

studii de caz, Editura Economică, Bucureşti, 2007

161. Pătruţ V., Rotilă A., Contabilitate şi diagnostic financiar. Fundamente teoretice şi aplicaţii

practice, Editura Sedcom Libris, Iaşi, 2005

162. Pântea I. P., Managementul contabilităţii românești, Vol. II., Editura Intelcredo, Deva, 1998

163. Pereş I., Mateş D., Popa I. E., Pereş C., Domil A., Bazele contabilităţii – concepte şi aplicaţii

practice, Editura Mirton, Timişoara, 2009

164. Perrin G., Prix de revient et contrôle de gestion par la méthode GP, Dunod, Paris, 1963

165. Petrescu S., Diagnostic economico-financiar, Editura Sedcom Libris, Iași, 2004

166. Petrescu S., Mihalciuc C.C., Diagnostic financiar-contabil privind performanţa întreprinderii.

Aspecte teoretice şi aplicative de contabilitate şi analiză financiară, Editura Universităţii

Suceava, 2006

167. Petrescu S., Analiză si diagnostic financiar-contabil. Ghid teoretico-aplicativ, Ediţia a II-a

revizuită şi adăugită, Editura CECCAR, Bucureşti, 2008

168. Petrescu S., Evaluarea economică și financiară a întreprinderii, concepte, metode, procedee,

Editura Tehnopress, Iași, 2012

169. Petriș R., Bazele contabilităţii, Editura Gorun, Iași, 2002

170. Porter M., Competive advantage: creating and sustaining performance, The Free Press, New

York, 1985

171. Pop A. (coordonator), Dumbravă P., Fătăceanu Gh., Contabilitatea de gestiune în comerţ,

Editura Intelcredo, Deva, 1997

172. Pop A., Matis D., Contabilitate financiară, Editura Casa Cărţii, Oradea, 2010

173. Pop C., Pop V., Management şi dezvoltare, Editura TipoMoldova, Iaşi, 2007

174. Pop G., Tehnologia produselor de morărit şi panificaţie - îndrumar de laborator, Editura

Universităţii „Ştefan cel Mare”, Suceava, 2005

175. Pop G., Tehnologia produselor de morărit şi panificaţie, Editura Universităţii „Ştefan cel

Mare”, Suceava, 2005

176. Popa I.E., Briciu S., Bazele contabilităţii. Aplicaţii practice, Editura Economică, Bucureşti,

2009

177. Popa I., Man Al., Rus A., Audit financiar de la teorie la practică - Ghid practic, Editura

Risoprint, Cluj Napoca, 2009

178. Rachlin R., Sistemul complet de bugete ale firmei. Ghid practice şi formulare de lucru, Ediţia

a II-a, B.M.T Publishing House, 2007

179. Radu M., Metoda standard cost. Aspecte teoretice şi practice, Editura Valahia University

Press, Târgovişte, 2009

180. Radu M., Contabilitate de gestiune, Editura Bibliotheca, Târgovişte, 2010

181. Raiborn C. A., Mallouk B. M., Spraakman G., Barfield, J. T., Kinney M. R., Managerial

Accounting. First Canadian Edition, Transcontinental, 2004

182. Raulet Ch., Comptabilité analytique et contrôle de gestion, Éditions Dunod, Paris, 1994

183. Ristea M., Dumitru C.G., Contabilitatea şi managementul întreprinderii, Editura Tribuna

Economică, Bucureşti, 2005

184. Ristea M., Dumitru C.G., Prudenţă şi agresivitate în tratamentele contabile, Editura Tribuna

Economică, Bucureşti, 2008

185. Ristea M., Dumitru C.G., Ioanăş C., Contabilitatea societăţilor comerciale, vol. I-II, Editura

Universitară, Bucureşti, 2009

186. Roehl-Anderson J.M., Bragg St.M., The controller’s function. The work of the managerial

accountant, Wiley&Sons, New Jersey, 2005

187. Romney M.B., Steinbart P.J, Accounting Information Systems, 8th

edition, Prentice Hall, 2000

188. Rotar Stingheriu R., Tehnologia produselor fermentative - îndrumar de laborator, Editura

Universităţii „Ştefan cel Mare”, Suceava, 2005

189. Rusu D., Bazele contabilităţii, Editura Didactică și Pedagogică, București, 1980

190. Sabou F., Metoda standard cost, metoda direct costing – metode moderne ale contabilităţii

manageriale. Studia Universitatis, seria Știinţe Economice nr. 17, Partea a II-a, Universitatea

de Vest „Vasile Goldiş”, Arad, 2007

191. Savall H., Les coûts cachés et l′analyse socio-économiques des organisations, Encyclopédie

de Gestion, Economica, Paris, 1997

192. Scorţe M.C., Contabilitate internă de gestiune, Editura Universităţii, Oradea, 2005

193. Seal W., Garrison R.H., Noreen E.W., Management Accounting, Third Edition, Mc Graw–Hill

Inc., New York, 2009

194. Sgârdea F., Control de gestiune, Editura Lucman, Bucureşti, 2007

195. Simon H. A., Centralization vs. Decentralization in Organizing the Controller’s Departament,

Controllership Foundation, New York, 1978

196. Sîrbu C.G., Strategii de creştere a competitivităţii bazate pe analiza costurilor, Editura

Europlus, Galaţi, 2008

197. Smith J.A., Management Accounting, 4th

Edition, Elsevier, 2007

198. Socolov J., Kovalev V., In deffence of Russian Accounting: a reply to foreign critics. The

european Accounting Reviw, 1995

199. Swain M.R., Albrecht W.S., Stice J.D., Stice E.K., Management Accounting, Thompson

Corporation, USA, 2005

200. Tabără N., Contabilitate şi control de gestiune. Studii şi cercetări, Editura TipoMoldova, Iaşi,