UNITED STATES BANKRUPTCY COURT …omnimgt.com/cmsvol2/pub_47137/608746_809.pdf · Lathrop Business...

96

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF INDIANA INDIANAPOLIS DIVISION IN RE: ITT EDUCATIONAL SERVICES, INC. Debtor ) ) ) ) ) ) Case No. 16-07207-JMC-7A MOTION OF LATHROP BUSINESS PARK, LLC FOR ALLOWANCE OF ADMINISTRATIVE EXPENSE CLAIM PURSUANT TO 11 U.S.C. 503(b)(1) Lathrop Business Park, LLC, (also known as Pacific Edge and Development, Inc.) (hereinafter referred to as “LBP”), by and through its undersigned attorneys, hereby requests the entry of an order, pursuant to 11 U.S.C. § 503(b)(1), allowing LBP an administrative expense claim in the amount of Thirty Five Thousand Eight Hundred Fifty-Four Dollars and Eighty-Eight Cents ($35,854.88) as and for necessary costs and expenses of preserving the bankruptcy estate from the period of the bankruptcy filing on September 16, 2016, through the date the of rejection of the non-residential lease with debtor ITT Educational Services, Inc. (hereinafter referred to as “ITT”) on October 27, 2016. Alternatively, LBP, by and through its counsel, hereby requests the entry of an order, pursuant to 11 U.S.C § 365(d)(3) requiring the bankruptcy trustee to perform the obligations of ITT arising from the date of the order for relief on an unexpired lease of nonresidential property until the date the lease was rejected on October 17, 2016. During this period, ITT’s obligation to LBP totals $35,854.88. In support of its Motion, LBP states as follows: Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 9

Transcript of UNITED STATES BANKRUPTCY COURT …omnimgt.com/cmsvol2/pub_47137/608746_809.pdf · Lathrop Business...

UNITED STATES BANKRUPTCY COURT

SOUTHERN DISTRICT OF INDIANA

INDIANAPOLIS DIVISION

IN RE:

ITT EDUCATIONAL SERVICES, INC.

Debtor

)

)

)

)

)

)

Case No. 16-07207-JMC-7A

MOTION OF LATHROP BUSINESS PARK, LLC FOR ALLOWANCE OF

ADMINISTRATIVE EXPENSE CLAIM PURSUANT TO 11 U.S.C. 503(b)(1)

Lathrop Business Park, LLC, (also known as Pacific Edge and Development, Inc.)

(hereinafter referred to as “LBP”), by and through its undersigned attorneys, hereby requests the

entry of an order, pursuant to 11 U.S.C. § 503(b)(1), allowing LBP an administrative expense

claim in the amount of Thirty Five Thousand Eight Hundred Fifty-Four Dollars and Eighty-Eight

Cents ($35,854.88) as and for necessary costs and expenses of preserving the bankruptcy estate

from the period of the bankruptcy filing on September 16, 2016, through the date the of rejection

of the non-residential lease with debtor ITT Educational Services, Inc. (hereinafter referred to as

“ITT”) on October 27, 2016. Alternatively, LBP, by and through its counsel, hereby requests the

entry of an order, pursuant to 11 U.S.C § 365(d)(3) requiring the bankruptcy trustee to perform

the obligations of ITT arising from the date of the order for relief on an unexpired lease of

nonresidential property until the date the lease was rejected on October 17, 2016. During this

period, ITT’s obligation to LBP totals $35,854.88. In support of its Motion, LBP states as

follows:

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 9

I. JURISDICTION

1. On September 16, 2016, the above-captioned debtor, ITT, filed its voluntary

petition for relief under chapter 7 of title 11 of the United States Code (the “Bankruptcy Code”)

in the United States Bankruptcy Court for the Southern District of Indiana (the “Court”).

2. This Court has jurisdiction over this motion pursuant to 28 U.S.C. §§157 and

1334(b). This matter is a core proceeding pursuant to 28 U.S.C. §157(b)(2)(A). Venue is proper

in this District pursuant to 28 U.S.C. §1408 and 1409.

II. BACKGROUND

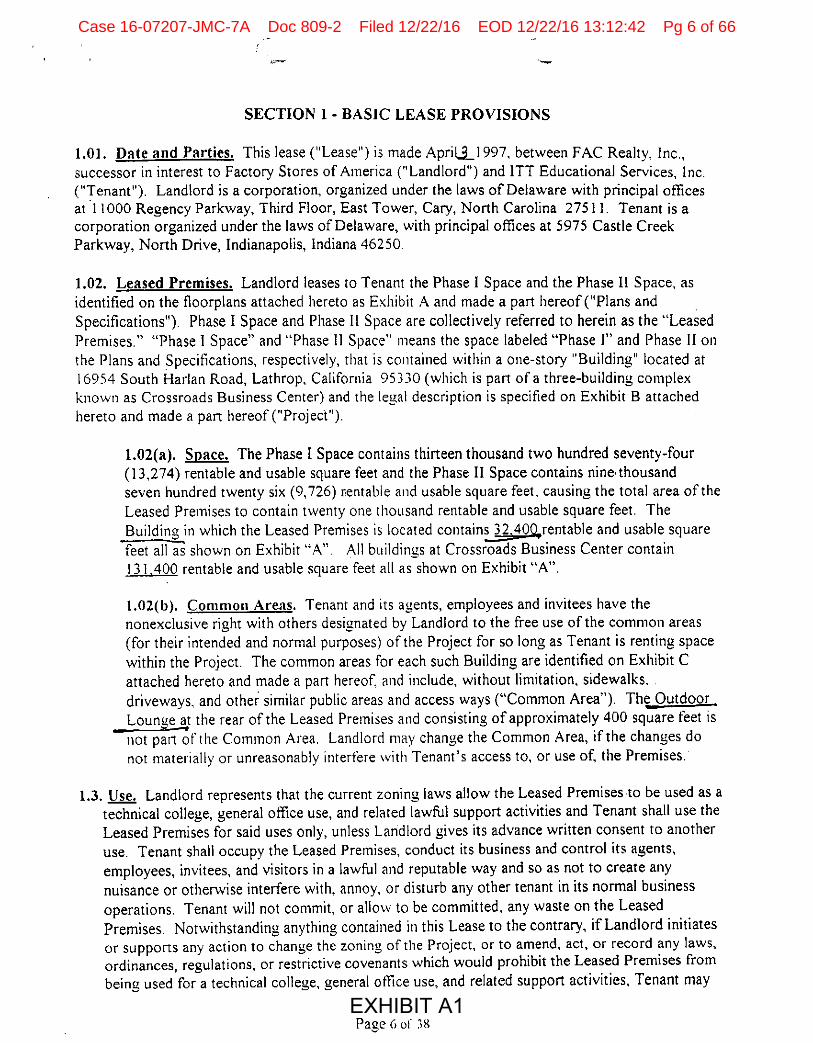

3. ITT entered into a contractual agreement with LBP’s predecessor in interest on

April 3, 1997, to lease nonresidential real property. On November 8, 2007, LBP and ITT

executed a First Amendment to Lease, wherein LBP assumed said Lease, and the parties

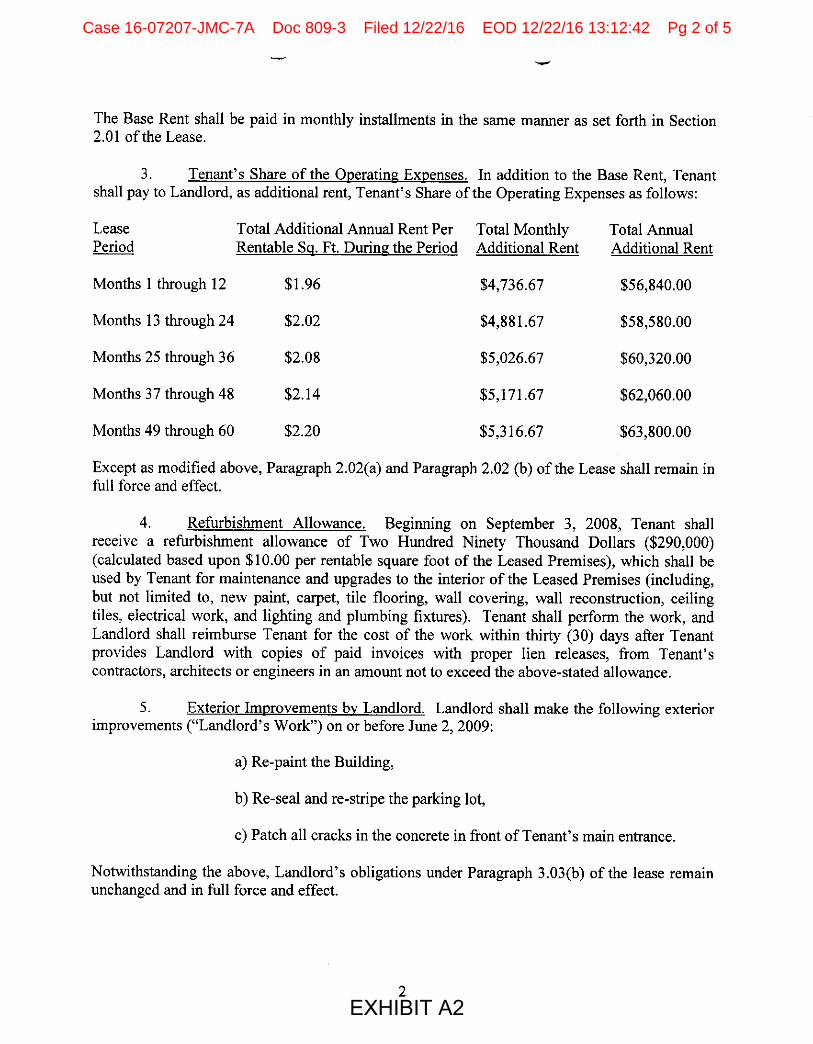

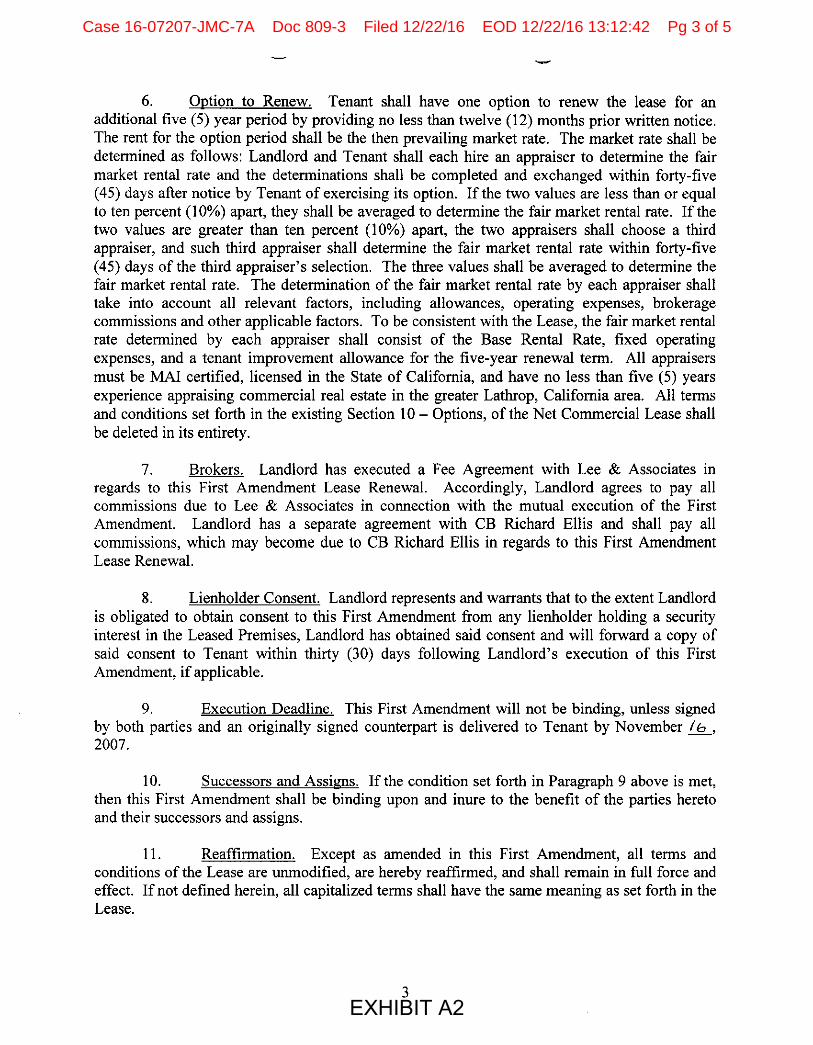

extended the term of the Lease to September 2, 2013. On June 1, 2012, LBP and ITT executed a

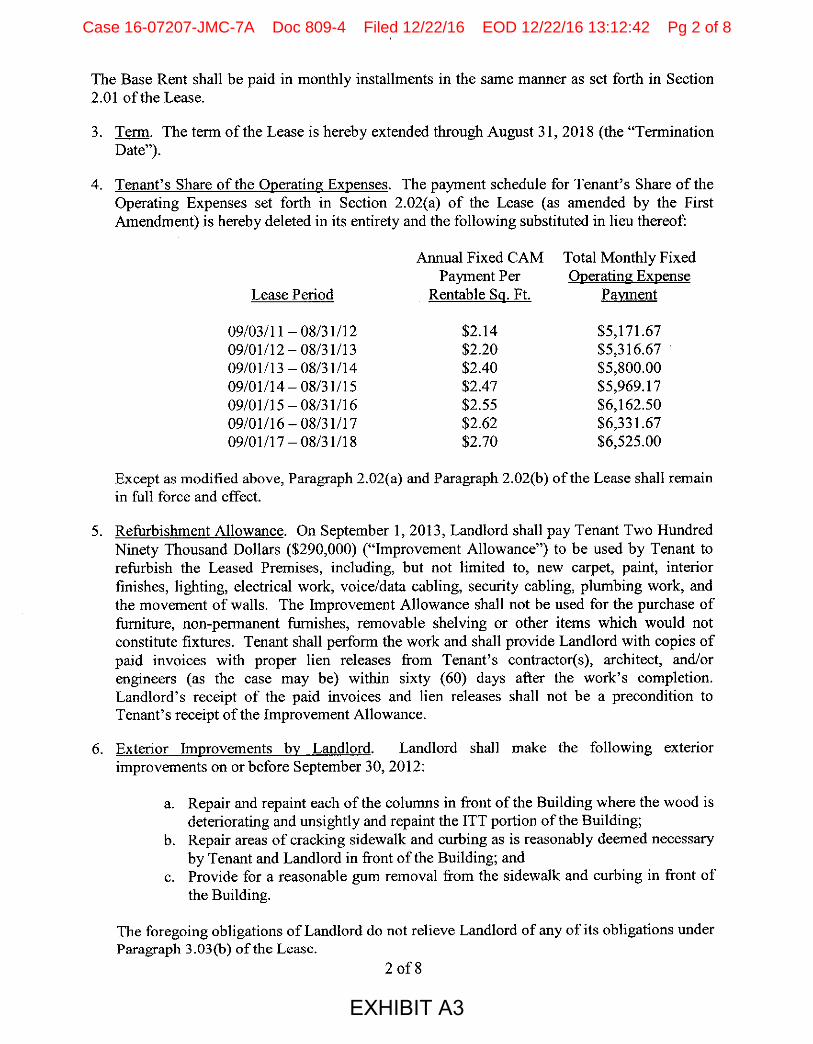

Second Amendment to the Lease extending the term of the Lease to August 31, 2018,

(hereinafter, collectively referred to as the “Lease”). True and correct copies of the Lease and

the amendments thereto are attached as Exhibit A1 through Exhibit A3.

4. On September 16, 2016, (the “Petition Date”), ITT filed a voluntary bankruptcy

petition in this court for relief under chapter 7 of title 11 of the Bankruptcy Code (the “Petition”).

A true and correct copy of the Notice of Chapter 7 Bankruptcy Case is attached as Exhibit B.

5. On October 31, 2016, attorneys for the trustee of the Bankruptcy estate sent a

Notice of Rejection of the non-residential Lease to LBP which had an effective date of October

27, 2016 (the “Rejection Date”). A true and correct copy of the Notice of Rejection is attached

as Exhibit C.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 9

6. Pursuant to the operative terms of the Lease, as of September 1, 2016, and

through August 31, 2017, base rent payments were to be paid in full by ITT in monthly

installments on the first day of each month in the amount of Twenty-Six Thousand Two Hundred

Twenty-Eight Dollars and Eighty-Three Cents ($26,220.83) (“Base Rent”) per month. (Please

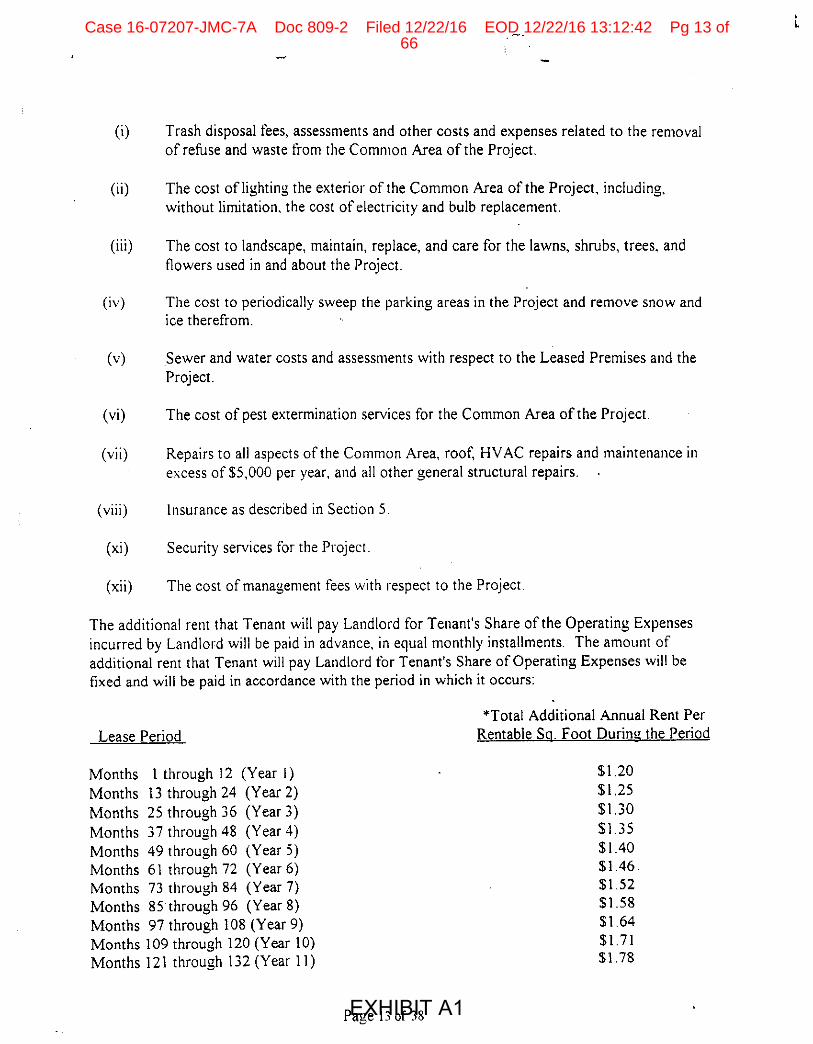

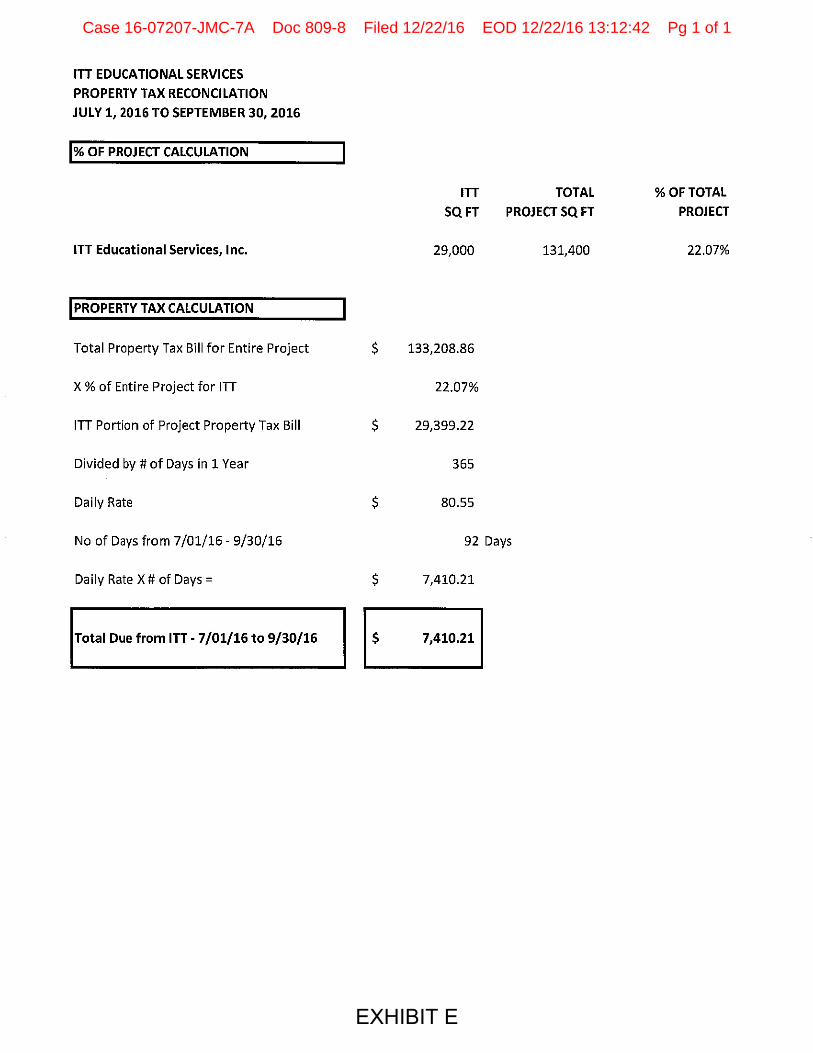

see Exhibit A3, page 1, ¶2.) ITT’s share of total monthly operating expenses as of September 1,

2016, and through August 31, 2017, were to be paid in full by ITT in monthly installments on the

first day of each month in the amount of Six Thousand Three Hundred Thirty-One Dollars and

Sixty-Seven Cents ($6,331.67) per month (see Exhibit A3, page 2, ¶4), and ITT’s pro rata share

of the cost of real estate taxes as of July 1, 2016, and through June 30, 2017, to be paid in

monthly installments in the amount of Three Thousand Three Hundred Two Dollars and Thirty-

Eight Cents ($3,302.38) (collectively “Additional Rents” unless specifically identified) per

month. A true and correct copy of the property tax information for the fiscal year 2016-2017 is

attached as Exhibit D. Please see also Exhibit A1, page 14, ¶2.02(b) which governs ITTs pro

rata share of the total property taxes. Furthermore, Exhibit E provides the square feet of the

Total Project, as the term is defined in the Lease, and the square footage of ITT’s leased

property.

7. In the interim of the Petition Date of September 16, 2016, and the Rejection Date

of October 27, 2016, LBP necessarily incurred costs to preserve the bankruptcy estate pending

the Trustee’s determination to assume or reject the lease, in the amount of the monthly Base Rent

and Additional Rents which came due in full on October 1, 2016, that is, $35,854.88.

8. LBP has submitted a Proof of Claim for the pre-Petition Date expenses incurred

and outstanding, that is, monthly Base Rent and Additional Rents which came due on September

1, 2016.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 3 of 9

9. As of the date of this Motion, LBP has not received payment for the cost and

expenses of preserving the estate for the period between the Petition Date and the Rejection

Date, which came due in full on October 1, 2016, as and for Base Rent and Additional Rents, nor

has LBP filed a Proof of Claim for this balance as of the date of this Motion.

III. RELIEF REQUESTED

10. LBP respectfully requests that this Court allow LBP’s administrative expense

claim in the amount of $35,854.88 for the necessary costs and expenses, including property taxes

in the amount of $3,302.38, of preserving the estate pursuant to sections 503(b)(1)(A) (actual and

necessary costs) and 503(b)(1)(B) (property taxes) of the Bankruptcy Code, or, alternatively,

pursuant to section 365(d)(3) of the Bankruptcy Code.

IV. BASIS FOR RELIEF

A. The Court Should Allow LBP an Administrative Expense Claim for Unpaid Post-

Petition Expenses Necessarily Incurred in Preserving the Estate

11. Section 503 of the Bankruptcy Code provides that, after notice and a hearing,

there shall be allowed administrative expenses, including the “actual, necessary costs and

expenses of preserving the estate . . . .” 11 U.S.C. § 503(b)(1)(A).

12. Section 503 of the Bankruptcy Code further provides that, after notice and a

hearing, there shall be allowed administrative expenses, including “any tax incurred by the

estate, whether secured or unsecured, including property taxes. . . .” 11 U.S.C. § 503(b)(1)(B).

13. Chapter 5 of the Bankruptcy Code, specifically section 503, is made applicable to

this Chapter 7 Bankruptcy proceeding under 11 U.S.C §103(a).

14. As is evident from the Bankruptcy Code’s “Rules of Construction,” the use of the

word “including”, as used in section 503(b)(1)(A), is not intended to be limiting. 11 U.S.C.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 4 of 9

§ 102(3). Thus, by implication, Congress did not intend the word “including” following the

words “actual, necessary costs and expenses of preserving the estate” of section 503(b)(1)(A), to

be exhaustive. Case law further supports this conclusion. “[T]he enumerated category for

administrative expenses does not necessarily preclude judicial construction to permit other

claims reasonably demonstrated to be ‘actual, necessary’ costs of administration….” (Varsity

Carpet Services v. Richardson (In re Colortex Industries) (1994) 19 F.3d 1371, 1377.)

The case of In re Pappas (2002) 277 B.R. 171, 176 further supports the conclusion that

the list in section 503(b)(1)(A) is not exhaustive. “The categories of administrative expense

listed in section 503(b) are intended to be illustrative, not exhaustive.” The Pappas court cited

11 U.S.C. § 102(3) which provides that the terms “includes” and “including” are not limiting.

Therefore, damages incurred by LBP as a result of ITT’s occupancy of the premises pending a

determination of whether to assume or reject the lease are a proper and necessary expense of

preserving the value of the bankruptcy estate, and as such, qualify for administrative expense

preference under 11 U.S.C. § 503(b)(1)(A).

15. Administrative expense damages incurred under 11 U.S.C. § 503(b) are further

entitled to priority under section 507(a)(2) of the Bankruptcy Code.

16. The case of In re HQ Global Holdings, Inc. (2002) 282 BR 169, 40 BCD 11,

specifically supports LBP’s position that landlords have administrative claims under 11 USCS

§ 503(b) for rent due post-petition and pre-rejection or assumption of a lease. The court relied on

section 503(b) of the Bankruptcy Code, stating:

“Section 503(b) provides in relevant part that: After notice and a hearing, there shall be allowed administrative expenses, . . . including-(1) (A) the actual, necessary costs and expenses of preserving the estate. 11 U.S.C. § 503(b). A lessor is generally entitled to an administrative claim under section 503(b) for the fair rental value of the lessor’s property actually used by the debtor.” Id. at 173.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 5 of 9

The HQ Global Holdings Court went on further that where “rent for the entire month is

due on the first of the month and, if the Debtors occupy the premises on the first, they must pay

that entire sum.” Id. at 174.

17. As evidenced by the Lease Agreements and the First and Second Amendments

thereto, subsequent to the Petition Date, ITT owed LBP Base Rent and Additional Rents,

including property taxes, which came due in full on October 1, 2016, in the amount of

$35,854.88. The Lease was rejected by the Trustee on October 27, 2016. LBP had not, and to

date has not yet, received payment for the Base Rent or Additional Rents for the month of

October 2016, and is accordingly entitled to an allowed administrative expense claim against ITT

in the aggregate amount of $35,854.88.

B. Alternatively, the Court Should Mandate that the Trustee Perform Obligations of

the Debtor Arising After the Petition Date and Prior to the Rejection of the Lease

18. Section 365(d)(3) of the Bankruptcy Code provides that “[t]he trustee shall timely

perform all the obligations of the debtor … arising from and after the order for relief under any

unexpired lease of nonresidential real property, until such lease is assumed or rejected,

notwithstanding section 503(b)(1) of this title.”

19. Chapter 3, specifically section 365, is made applicable to this Chapter 7

Bankruptcy proceeding under 11 U.S.C §103(a).

20. Bankruptcy courts have held that “[s]ection 365 provides for administrative

priority for expenses incurred in performing obligations on a nonresidential lease of real property

postpetition while the debtor-in-possession decides whether to assume or reject a lease…”(In re

BH S&B Holdings LLC (2010) 426 B.R. 478, 482.) The court in that case further reiterated,

“between the filing of a bankruptcy petition and a debtor-in-possession’s decision whether to

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 6 of 9

assume or reject an unexpired lease, section 365(d)(3) requires a debtor-in-possession to ‘timely

perform all the obligations of the debtor . . . notwithstanding section 503(b)(1) of this title.’

Expenses arising out of this performance are entitled to automatic administrative expense status.”

(Id. at 483.)

21. For these reasons, if the court denies LBP’s claim for October 2016 rent and

additional rents, including property taxes, as an administrative expense under section 503(b), the

court should alternatively provide administrative priority to this claim under section 365 of the

Bankruptcy Code.

C. The Court Should Compel Immediate Payment of LBP’s Administrative

Expense Claim

22. “Courts have discretion to determine when an administrative expense will be

paid.” HQ Global Holdings, Inc., (2002) 282 B.R. 169, 173. “In determining the time of

payment, courts consider prejudice to the debtor, hardship to the claimant, and potential

detriment to other creditors.” Id.

23. There is no valid reason to defer payment of LBP’s administrative expense claim.

Administrative claims are entitled to priority payment pursuant to 507(a)(2), second to only

domestic support, child support, and the trustee’s expenses of administering assets. Because ITT

is a legal entity with no children or spouse, administrative claims succeed only the Trustee’s

expenses. Accordingly, allowing immediate payment of the claim would not result in prejudice

to other creditors’ subordinate claims.

24. For these reasons, the Court should allow LBP’s administrative expense claim and

compel immediate payment thereof.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 7 of 9

V. RESERVATION OF RIGHTS

25. LBP reserves its right to assert claims against ITT for amounts not contemplated

by this Motion or allowed by the Court pursuant to section 503(b)(1) and to amend, modify

and/or supplement this request, as appropriate under the circumstances.

VI. NOTICE OF OPPORTUNITY TO OBJECT

YOU ARE NOTIFIED that your rights may be affected by this Motion. Parties in

interest have until January 4, 2017, at 4:00 p.m. (prevailing Eastern Time) to file an objection

to this Motion in accordance with L.R.S.D.Ind. B-9013-1. Objections must be in writing and

filed with the Bankruptcy Court Electronically (user account and password required) or, if not

permitted to file electronically, with the Clerk’s Office, 46 East Ohio Street, Room 116,

Indianapolis, Indiana 46204 and shall be served in time to arrive prior to the deadline set forth

above. Any objection must be served on the attorney for LBP at the address set forth below:

Steven A. Malcoun, Esq. MAYALL HURLEY, P.C. 2453 Grand Canal Boulevard, Second Floor Stockton, California 95207-8253 Telephone: (209) 477-3833 Facsimile: (209)473-4818 [email protected] NOTICE IS FURTHER GIVEN that pursuant to Bankruptcy Rule 6006(c) and the

Notice, Case Management and Administrative Procedures approved by this Court on October 4,

2016, this Motion is scheduled for hearing on January 11, 2017, at 1:30 p.m. (prevailing

Eastern Time) at the United State Bankruptcy Court, Room 325, 46 East Ohio Street,

Indianapolis, IN 46204.

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 8 of 9

NOTICE IS FURTHER GIVEN: IF NO OBJECTION IS TIMELY FILED, AN

ORDER MAY BE ENTERED BY THE COURT FOR THE RELIEF REQUESTED WITHOUT

FURTHER NOTICE OR HOLDING THE SCHEDULED HEARING.

WHEREFORE, for the reasons stated herein, LBP respectfully requests that the Court

enter an order, substantially in the form attached hereto as Exhibit F: (i) allowing LBP an

administrative expense claim in the amount of $35,854.88 for post-petition damages necessarily

incurred in preserving the estate; (ii) ordering the Trustee to pay LBP’s allowed administrative

expense claim immediately; and (iii) granting such other and further relief as the Court may

deem just and proper.

Dated: December 21, 2016 s/Steven A. Malcoun

____________________________________ Steven A. Malcoun California State Bar No. 084946 Mayall Hurley, PC 2453 Grand Canal Blvd. Stockton, CA 95207 (209)477-3833 (209)473-4818 [email protected]

Case 16-07207-JMC-7A Doc 809 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 9 of 9

UNITED STATES BANKRUPTCY COURT

SOUTHERN DISTRICT OF INDIANA INDIANAPOLIS DIVISION

IN RE: ITT EDUCATIONAL SERVICES, INC. Debtor

))))))

Case No. 16-07207-JMC-7A

CERTIFICATE OF SERVICE

The undersigned hereby certifies that on the 22th day of December, 2016, a copy of the

Motion of Lathrop Business Park, LLC For Allowance of Administrative Expense Claim

Pursuant to 11 U.S.C. 503(B)(1) was served electronically upon the parties entered in the

Court’s electronic filing system as of that date.

The undersigned further certifies that on the 22nd day of December, 2016, a copy of the

Motion of Lathrop Business Park, LLC For Allowance of Administrative Expense Claim

Pursuant to 11 U.S.C. 503(B)(1) was mailed by first-class United States mail, postage prepaid

and properly addressed to all parties listed on the attached Exhibit A.

Dated this 22th day of December, 2016. /s/ Steven A. Malcoun Steven A. Malcoun California State Bar No. 084946 Mayall Hurley, PC 2453 Grand Canal Blvd. Stockton, CA 95207 (209)477-3833 (209)473-4818 [email protected]

Case 16-07207-JMC-7A Doc 809-1 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 2

EXHIBIT A

Eboney Cobb Perdue Brandon Fielder Collins Mott LLP

500 E. Border Street, Suite 640 Arlington, TX 76010

Northwest Natural Gas Company 220 NW 2nd Ave.

Portland, OR 97209

Carl O. Sandin For clear Creek Independent

School District 1235 North Loop West, Suite 600

Houston, TX

Daniel Webster College, Inc. 20 University Drive Nashua, NH 03063

Rachel Obaldo Office of the Texas Attorney General

BK & Collections Division PO Box 12548

Austin, TX 78711-2548

McLintock & Associates, PC 1370 Washington Pike, Bridgeville, PA 15017

John P. Dillman PO Box 3064

Houston, TX 77253

Recovery Management System Corporation

For Synchrony Bank 25 SE 2nd Ave., Suite 1120

Miami, FL 33131-1605

Joseph A. Malfitano For Tiger Capital Group, LLC

747 Third Ave., 2nd Floor New York, NY 10017

ESI Service Corp 13000 N. Meridian Street Carmel, IN 46032-1404

Kevin Schwin Law Office of Kevin Schwin

1220 E. Olive Ave. Fresno, CA 93728

Jordan A. Lavinsky For Market-Turk Company

425 Market Street, 26th Floor San Francisco, 94105

T. Todd Egland

Belden Blaine Raytis, LLP PO Box 9129

Bakersfield, CA 93389-9129

TN Dept of Revenue c/o TN Atty General, BK Division

PO Box 20207 Nashville, TN 37202-0207

ITT Educational Service, Inc. 13000 N. Meridian Street

Carmel, IN 46032

Florida Department of Education Office of Student Financial

Assistance PO Box 7019

Tallahassee, FL 32314-7019

Tammy Jones Oklahoma County Treasurer

320 Robert S. Kerr, Room 307 Oklahoma City, OK 73102

Elizabeth Weller Linebarger Goggan Blair&

Sampson, LLP 2777 N. Stemmons Freeway,

Suite 1000 Dallas, TX 75207

Chris W. Halling For Solar Drive Business LLC 23586 Calabasas Rd., Suite 200

Calabasas, CA 91302

Paul Weiser Bachalter Nemer

16435 North Scottsdale Road, Suite 440

Scottsdale, AZ 85254-1754

Case 16-07207-JMC-7A Doc 809-1 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 2

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 3 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 4 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 5 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 6 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 7 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 8 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 9 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 10 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 11 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 12 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 13 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 14 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 15 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 16 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 17 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 18 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 19 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 20 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 21 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 22 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 23 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 24 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 25 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 26 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 27 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 28 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 29 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 30 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 31 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 32 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 33 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 34 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 35 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 36 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 37 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 38 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 39 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 40 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 41 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 42 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 43 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 44 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 45 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 46 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 47 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 48 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 49 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 50 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 51 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 52 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 53 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 54 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 55 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 56 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 57 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 58 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 59 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 60 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 61 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 62 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 63 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 64 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 65 of 66

EXHIBIT A1

Case 16-07207-JMC-7A Doc 809-2 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 66 of 66

EXHIBIT A2

Case 16-07207-JMC-7A Doc 809-3 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 5

EXHIBIT A2

Case 16-07207-JMC-7A Doc 809-3 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 5

EXHIBIT A2

Case 16-07207-JMC-7A Doc 809-3 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 3 of 5

EXHIBIT A2

Case 16-07207-JMC-7A Doc 809-3 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 4 of 5

EXHIBIT A2

Case 16-07207-JMC-7A Doc 809-3 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 5 of 5

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 3 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 4 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 5 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 6 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 7 of 8

EXHIBIT A3

Case 16-07207-JMC-7A Doc 809-4 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 8 of 8

EXHIBIT B

Case 16-07207-JMC-7A Doc 809-5 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 3

EXHIBIT B

Case 16-07207-JMC-7A Doc 809-5 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 2 of 3

EXHIBIT B

Case 16-07207-JMC-7A Doc 809-5 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 3 of 3

EXHIBIT C

Case 16-07207-JMC-7A Doc 809-6 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 1

EXHIBIT D

Case 16-07207-JMC-7A Doc 809-7 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 1

EXHIBIT E

Case 16-07207-JMC-7A Doc 809-8 Filed 12/22/16 EOD 12/22/16 13:12:42 Pg 1 of 1