UNIT OUTLINE - University of Tasmania · UNIT OUTLINE Read this document ... BFA 715 Accounting...

37

UNIT OUTLINE Read this document to learn essential details about your unit. It will also help you to get started with your studies. BFA 715 Unit Title: Accounting Theory Semester 1, 2015 THIS UNIT IS BEING OFFERED IN: HOBART Unit Co-Ordinator: Associate Professor Trevor Wilmshurst CRICOS Provider Code: 00586B

Transcript of UNIT OUTLINE - University of Tasmania · UNIT OUTLINE Read this document ... BFA 715 Accounting...

UNIT OUTLINE

Read this document to learn essential details about your unit. It will

also help you to get started with your studies.

BFA 715 Unit Title: Accounting Theory

Semester 1, 2015

THIS UNIT IS BEING OFFERED IN: HOBART

Unit Co-Ordinator:

Associate Professor Trevor Wilmshurst

CRICOS Provider Code: 00586B

BFA 715 Accounting Theory 2

Contents Contact Details ........................................................................................................................................ 2

Unit Description ...................................................................................................................................... 3

Prior Knowledge &/or Skills OR Pre-Requisite Unit(s) ............................................................................ 3

Enrolment in the Unit ............................................................................................................................. 3

When does the unit commence? ............................................................................................................ 3

Table 1 - Intended Learning Outcomes and Generic Graduate Attributes for BFA 715 ......................... 4

Learning Expectations and Teaching Strategies/Approach .................................................................... 5

Learning Resources ................................................................................................................................. 6

Student Feedback via eVALUate ............................................................................................................. 9

Details of Teaching Arrangements ........................................................................................................ 10

Assessment ........................................................................................................................................... 12

Submission of Assessment Items .......................................................................................................... 15

Review of Assessment and Results ....................................................................................................... 16

Further Support and Assistance ............................................................................................................ 17

Academic Misconduct and Plagiarism .................................................................................................. 18

Study Schedule ...................................................................................................................................... 19

Tutorial/Workshop Schedule ................................................................................................................ 20

Contact Details Unit Coordinator/ Associate Professor Trevor Wilmshurst Lecturer Campus: Launceston Room Number: D101 Hobart TBA Email: [email protected] Phone: 6324 3570 Consultation: TBA

BFA 715 Accounting Theory 3

Unit Description

Accounting Theory represents the capstone of your studies in financial accounting and exposes you to the underlying theories and other influences that have played an important role in shaping accounting practice. Further, the unit considers emerging issues currently being addressed by researchers. In this way, the unit will give you an understanding of the historical and contemporary issues that have influenced the development of accounting practice, accounting regulation and accounting thought. Over time, accounting theory has focused on three main approaches or viewpoints. These are the descriptive (positive), normative and critical viewpoints. Using these theoretical points of view, this unit will help you examine current issues such as social and environmental accountability, the ethical and global dimensions of accounting, Conceptual Framework projects and the political context within which accounting policy decisions are made.

We present a theoretical framework for examining accounting issues and practices and a chance for you to develop high-level critical and analytical skills. This will help you present arguments and opinions on a broad range of accounting issues, with some authority. Knowing about historical and contemporary issues will also give you a foundation for understanding the rationale (main reasons) for current accounting policies and practices, and the directions in which accounting policies are likely to develop. In this way to better prepare you for the changes that the profession will inevitably need to be a part of.

Prior Knowledge &/or Skills OR Pre-Requisite Unit(s) The pre-requisite to complete this unit is a pass grade or better in BFA 605 Financial and Corporate Accounting. This background knowledge is essential to enable effective participation in the achievement of the outcomes expected in this unit. This unit offers the theoretical perspective for evaluating accounting practices and policies.

Enrolment in the Unit Unless there are exceptional circumstances, students should not enrol in this unit after the end of week two of semester, as the Tasmanian School of Business and Economics (TSBE) cannot guarantee that:

any extra assistance will be provided by the teaching team in respect of work covered in the period prior to enrolment; and

penalties will not be applied for late submission of any piece or pieces of assessment that were due during this period.

students enrolling late will be required to promptly complete any outstanding assessment tasks, pre reading for workshops and/or lectures and tutorials, and review lectures already presented

When does the unit commence? The unit’s teaching schedule commences in the week beginning 23 February, 2015.

BFA 715 Accounting Theory 4

Table 1 - Intended Learning Outcomes and Generic Graduate Attributes for BFA 715 Intended Learning Outcomes

Assessment Methods

Accounting Specific Outcomes

Graduate Attribute Outcomes In this unit you will learn:

In assessing this unit I will be looking at your ability to:

Learning Outcome 1

Describe and apply alternative theoretical frameworks

Develop an understanding of different theoretical perspectives and issues

Task 1

Task 4

Judgement:

The ability to develop an accounting opinion

The ability to examine, argue and evaluate an accounting issue critically.

Knowledge:

An ability to integrate both advanced technical accounting and theoretical knowledge

An ability to extend this knowledge to new situations in understanding current developments in accounting, projected change and suggestions for developments particularly through academia.

Application Skills:

An ability to research and apply advanced technical and theoretical accounting and related knowledge to current, evolving and new situations to address accounting issues at both a theoretical and practical level.

Communication and Teamwork:

An ability to both justify and to communicate both technical and theoretical accounting knowledge to both accountants and non-accountants

To offer advice and though on both current and new developments, and suggested new approaches to both technical and theoretical practices.

To achieve this in a collaborative environment, one in which, students must work together.

Self-Management:

An ability to critically assess the outcome(s) of activities undertaken

To reflect on any feedback whether personal observation or provided by participants

To assess action learning opportunities to apply to the individuals development, and, where appropriate, to offer guidance to further development to others.

To understand how such processes might be initiated.

Knowledge:

Ability to evaluate critically, complex ideas and concepts at an abstract level and to reflect on the meaning of these ideas and concepts;

An ability to demonstrate an understanding of recent theoretical developments in accounting;

The ability to interpret and evaluate, including the justification of, theoretical propositions, research methodologies and research/theoretical results and conclusions. [Tasks 1, 4 and 5]

Communication:

Demonstrate high-level written communication skills at an academic and professional level. [Task 2, 3 & 5]

The ability to articulate conclusions to culturally and linguistically diverse audiences; [Task 1 & 2]

To master critical oral discussion, including the ability to engage professional peers and academics in conversation in theoretical applications in accounting and to critique and/or justify research based studies. [Task 1 & 2]

Problem solving:

Demonstrate the ability to anticipate problems and to independently identify, define, investigate and research these problems; [Task 1-5]

The ability to creatively solve ambiguous and multifaceted problems by synthesising existing personal knowledge with an analysis and critical evaluation of information obtained from a variety of Australian and international sources; [Task 1-5]

The ability to effectively plan and execute a substantial research based project, capstone experience or piece of academic scholarship.[Task 4]

Global perspective:

The development of interpersonal skills that enable students to sensitively connect with, collaborate with/or lead people from diverse cultures and backgrounds, in both professional and academic contexts;[Task 1 & 2]

The ability to make and evaluate decisions using specialist knowledge that incorporates the potential influence of the global business environment. [Task 1, 2, 4 and 5].

Social responsibility:

The ability to identify issues and potential problems related to corporate social responsibility and sustainability in both Australian and international contexts;

The ability to determine and apply a legitimate ethical framework to personal, professional and academic endeavours in both Australian and international contexts.

[Tasks 1, 2, 4 and 5]

Learning Outcome 2

Critically reflect on theoretical work

Demonstrate an ability to draw out the main issues of a theoretical discussion and reflect upon them.

Task 1

Task 2

Task 3

Task 4

Task 5

Learning Outcome 3

Analyse emerging theoretical issues and evaluate social and ethical implications

Develop an understanding of emerging theoretical perspectives and issues

Task 3

Task 4

Task 5

Learning Outcome 4

Demonstrate oral and written communication skills

Present assignment and examination responses, and your interactions in tutorials

Task 1

Task 4

Task 5

Learning Outcome 5

Work in groups to reflect on theoretical issues

Discuss and interact with peers sharing ideas and your effectiveness as group spokesperson.

Task 1

Task 2

BFA 715 Accounting Theory 5

Learning Expectations and Teaching Strategies/Approach The University is committed to a high standard of professional conduct in all activities, and holds its commitment and responsibilities to its students as being of paramount importance. Likewise, it holds expectations about the responsibilities students have as they pursue their studies within the special environment the University offers. The University’s Code of Conduct for Teaching and Learning states:

Students are expected to participate actively and positively in the teaching/learning environment. They must attend classes when and as required, strive to maintain steady progress within the subject or unit framework, comply with workload expectations, and submit required work on time.

These are some of the expectations we have of you as a student enrolled in this unit: This is a demanding unit worthy of an MPA course. It is planned to introduce many new, and often complex, concepts, and to extend your knowledge of the philosophy of accounting. We expect all aspects of your work to be of a high standard, including the academic content and the quality of presentation. Learning strategies If you are studying this unit you will already have developed learning skills and strategies that have helped you succeed in previous accounting units. However, this unit is different. It involves more reading, more theorising (and abstract thinking), a wider vocabulary of accounting terms and good verbal and writing skills. The emphasis is on reading, understanding, discussing and writing, and not on technical procedures. It is important that you prepare before you attend classes. This means reading the textbook and other material before workshops/tutorials/lectures. Otherwise, you will get very little benefit from attending, and won’t be able to contribute to the development of group knowledge. Encouraging you to study and learn independently is an important goal of university education. It is a feature of a reflective approach to learning in which you reflect on (think about) what it is you are learning and how you plan your learning strategy. The workshop/tutorial sessions in particular give an interactive forum for developing and sharing ideas. Participation is an important feature of this unit, and below are some questions that are useful to think about when you discuss issues: Are your points relevant to the discussion? Do they increase the understanding of the class? Is there continuity in your contributions or do your comments tend to be disjointed and isolated? (The best class contributions reflect thorough preparation and good listening, interpretive and integrative skills); Do your comments show that you are willing to put forward new and challenging ideas or are you always agreeable and “safe”? Are you able and willing to interact with others by asking questions, providing supportive comments or challenging constructively what has been said?

BFA 715 Accounting Theory 6

Don’t be reluctant to ask questions or contribute ideas, even if only partly formed, as these are often a basis for very constructive interaction. A wrong answer is often very useful! Depending on your reading and writing skills, you should succeed in this unit if you: • keep up-to-date with the reading; • consolidate your reading by making appropriate short notes and summaries; • give yourself plenty of time to write your assignments; • prepare for and actively participate in the tutorial sessions; • keep your reflective learning journal up to date, and take responsibility for your own learning. If you fall behind with your reading and rush your written work you may have too much to make up before the examination and will be under-prepared. It is a risk you must consider.

You must take responsibility for your learning

Work, Health and Safety (WH&S) The University is committed to providing a safe and secure teaching and learning environment. In addition to specific requirements of this unit, you should refer to the University’s policy at: www.utas.edu.au/work-health-safety.

Learning Resources

Prescribed Text A prescribed text is a resource that you must have access to for the purposes of studying this unit.

Deegan, C. 2014. Financial Accounting Theory. 4th Edition. McGraw-Hill Education. [This text is essential if you undertake this unit]

Recommended Texts A recommended text is a resource that you can use to broaden your understanding of the topics covered in this unit. You may also find a recommended text helpful when conducting research for assignments.

Chartered Accountants Financial Reporting Standards 2012 (or similar) – Statements of Accounting Concepts 1 and 2, and the Framework for the Preparation and Presentation of Financial Statements.

Fleet, W, Summers, J & Smith, B 2006, Communication Skills Handbook for Accounting, 2 edn, John Wiley & Sons, Brisbane.

Rankin, M., Stanton, P., McGowan, S, Tilling, M., Ferlauto, K. and Tilt, C. 2012. Contemporary Issues in Accounting. 9780730300267. John Wiley and Sons.

Neville, C 2007, The Complete Guide to Referencing and Avoiding Plagiarism, McGraw Hill Open University Press. ISBN. -13 9780335220892, -10 0335220894

The Framework is in CPA Australia’s Accounting Handbook and you can download it at http://www.aasb.com.au. You will need to bring all the required texts to each lecture and tutorial session. We may give you extra journal articles to read during the semester.

You will benefit from reading as broadly as possible, especially for your assignments. Accounting theory is about ideas, and the more literature you survey the more you will understand about alternative approaches to accounting. References that might be helpful include:

BFA 715 Accounting Theory 7

Belkaoui, A.R. 2004. Accounting Theory, 5th Edn, Thomson, London.

Brooks, L.J. 2004. Business & Professional Ethics for Directors, Executives & Accountants, 3rd Edn, Thomson Learning, Ohio, USA.

Evans, T.G. 2003. Accounting Theory, Contemporary Accounting Issues, McGraw-Hill, Roseville, NSW.

Gaffiken, M 2008. Accounting Theory: Research, regulation and accounting practice. Pearson Education Australia, Frenchs Forest, NSW

Godfrey, J, Hodgson, A., & Holmes, S. 2003. Accounting Theory, 5th Edn, John Wiley & Sons, Brisbane,

Henderson, S., Peirson, G. & Harris, K. 2004. Financial Accounting Theory, Pearson Education Australia, Frenchs Forest, NSW.

Schroeder, R.G., Clarke, M.W., and Cathey, J.M. 2013. Financial Accounting Theory and Analysis: Text and Cases. 11th ed. Wiley.

Whittred, G, Zimmer, I., & Taylor, S. 2004 Financial Accounting Incentive Effects and Economic Consequences, 6th Edn, Thomson, Southbank, Vic.

The library has available many texts in this area, and the University data base has access to many academic and professional journals in this area.

Other Recommended Resources In addition to the texts recommended above, students are also expected to be familiar with the key academic journals in the discipline from which useful insights may be derived. In particular, students are encouraged to review regularly the relevant papers that are published in: Journals and Periodicals

Within your time constraints, you should allow 9 hours for independent study (see later in this outline), we expect you to read beyond the textbooks, especially for tutorial sessions and other tasks. If you are aiming for a distinction grade you will need to keep up to date with new issues and developments.

You can do this by reading widely, including the financial press, journals of the professional accounting bodies and some scholarly literature. In reading the scholarly literature, you should focus on the theory given at the start and end of papers. Don’t be distracted by the research methodology as your main focus is on the theory developed through research and the conclusions drawn. The following are some journals that you may find readable and useful:

• Accounting, Auditing and Accountability Journal • Accounting Forum • Accounting Horizons • Accounting Organisations and Society • Australian Accounting Review • The British Accounting Review Critical Perspectives on Accounting

Useful Websites

IFRS www.ifrs.org/ AASB www.aasb.gov.au/ CA www.chartere.daccountants.com.au/ CPA www.cpaaustralia.com.au/ IPA www.publicaccountants.org.au/

BFA 715 Accounting Theory 8

My Learning Online (MyLO) Access to the MyLO online learning environment unit is required for this unit. The unit has its own MyLO site. To log into MyLO and access this unit, go to: http://www.utas.edu.au/mylo. To access the unit, select BFA 715. These instructions will help you to log in for the first time. For help using MyLO go to http://www.utas.edu.au/mylo. Technical requirements for MyLO

For help and information about setting up your own computer and web browser for MyLO, see: http://uconnect.utas.edu.au/ While on campus, you can access the University network and MyLO via a laptop computer or other mobile device. See: http://www.utas.edu.au/service-desk/uconnect/uconnect-on-campus MyLO can be accessed via Library computers and in computer labs on campus. See: http://www.utas.edu.au/it/computing-distributed-systems/computer-labs-facilities-and-locations For further technical information and help, contact the UTAS Service Desk on 6226 1818 or at http://www.utas.edu.au/service-desk during business hours.

Learning to use MyLO When you log into MyLO, you will see a unit called Getting Started with MyLO. Enter this unit to learn more about MyLO, and to practise using its features.

MyLO Expectations 1. Students are expected to maintain the highest standards of conduct across all modes of

communication, either with staff or with other students. Penalties may be imposed if the Unit Coordinator believes that, in any instance or mode of communication, your language or content is inappropriate or offensive. MyLO is a public forum. Due levels of respect, professionalism and high ethical standards are expected of students at all times.

2. Submission of assessment tasks via MyLO presumes that students have read, understood and abide by the requirements relating to academic conduct, and in particular, those requirements relating to plagiarism. All work submitted electronically is presumed to be “signed-off” by the student submitting as their own work. Any breach of this requirement will lead to student misconduct processes.

3. MyLO is an Internet service for teaching and learning provided by the University. It is

expected that you check your units in MyLO for updates at least once a day.

BFA 715 Accounting Theory 9

Using MyLO for BFA715 IMPORTANT!: Before you are provided with access to your unit’s MyLO resources, you must complete the Student Agreement form. To do this:

1. Access the unit’s MyLO site. 2. Locate the Begin Here folder and click on it to open it. You can find the Begin Here folder by

scrolling down until you see Content Browser OR by clicking on the Content button.

OR

3. Once you have opened the Begin Here folder, click on the Student Agreement file.

OR

4. Read the terms, then check the I agree box. You should now be able to access all available unit content on MyLO. You only need to do this once in each MyLO unit.

Other important resources on MyLO Students are expected to regularly check on MyLO for any updates in relation to the unit. Essentially, MyLO has been incorporated into the delivery of this unit to enhance students’ learning experience, by providing access to up-to-date course materials, and allowing for online discussion. In addition to the lecture slides which are uploaded on MyLO on a weekly basis, other unit-related materials such as supplementary readings and assessment guides can also be accessed on MyLO. Further, students are also expected to engage in an active discussion about issues related to the unit through the discussion forums or chat rooms that are available on MyLO: this is particularly helpful for distance students who may utilise the facilities available on MyLO to contact their fellow distance students and form groups to complete any group assessment tasks for this unit. In this regard, MyLO should be treated as the unit's critical platform for learning and communication.

Student Feedback via eVALUate At the conclusion of each unit, students will be asked to provide online responses to a number of matters relating to the learning and teaching within that unit. All students are asked to respond honestly to these questions, as all information received is used to enhance the delivery of future offerings.

Changes to this Unit Based on Previous Student Feedback None

BFA 715 Accounting Theory 10

Details of Teaching Arrangements At this stage this unit will be conducted as a WORKSHOP. Each week you will undertake the following:

1. One Hour lecture of the topic of interest for that Week 2. A mini Debate or Academic Forum with a research/theory focus 3. Team work in groups followed by brief reports back to the group

We have planned this unit to occupy, on average, 12 hours of your time for each of the 13 weeks of the semester. The hours are allocated between:

Workshop: 3 hours – composed of:

Lecture 1 hour

Student Centred Activities 2 hours

Independent study & assignments 9 hours (minimum) 12 hours per week If you are not a fast reader you may have to spend longer on independent study as it is expected that you will undertake a significant part of your learning by reading, independent study, group work and writing assignments. If you are working full time or work for more than 20 hours a week part-time you may find it very difficult to achieve the aims set for the unit.

Specific Attendance/Performance Requirements It is expected that you will attend all workshops, lectures or/and your allocated tutorial. As with other accounting units this unit involves incremental learning, and a failure to attend may impede your progress. If you enrol in units that clash with this unit you are advised to reconsider completing this unit in the current semester. This is a substantively face-to-face unit taught within a blended learning environment. If you choose to continue in this unit, being aware that other units you undertake clash, it is at YOUR RISK and you should be aware that in such circumstances no special arrangements will be extended nor special consideration given. It is expected that you will pass each component of the assessment required in this unit. Pay particular attention to the requirements in each part of the assessment, and especially pay attention to and gain an understanding of what is meant by plagiarism and the risks of not doing so. These are important responsibilities you must accept.

You are expected to attend all timetabled sessions

Materials, audio or visual provided on MyLO DO NOT, nor are they intended to, replace attendance at required face to face sessions. If you choose not to attend scheduled classes it is at YOUR RISK.

Communication, Consultation and Appointments TO KEEP UP WITH ANNOUNCEMENTS REGARDING THIS UNIT Check the MyLO News tool at least once every two days. The unit News will appear when you first enter our unit’s MyLO site. Alternatively, click on the News button (towards the top of the MyLO screen) at any time. WHEN YOU HAVE A QUESTION Other students may have the same question that you have. Please go to the Q&A Forum on our course’s MyLO site. Check the posts that are already there – someone may have answered your

BFA 715 Accounting Theory 11

question already. Otherwise, add your question as a new topic. Students are encouraged to support each other using this forum – if you can answer someone’s question, please do. We will attempt to respond to questions within 48 business hours. If your question is related to a personal issue or your performance in the unit, please contact the appropriate teaching staff member by email instead. WHEN YOU HAVE AN ISSUE THAT WILL IMPACT ON YOUR STUDIES OR THE SUBMISSION OF AN ASSESSMENT TASK If you have a personal question related to your studies or your grades, please contact teaching staff by email. However, please note that work commitments, commitments relating to other units nor time allocation issues are considered justifiable reasons for late submission of assessment tasks. A NOTE ABOUT EMAIL CORRESPONDENCE You are expected to check your UTAS email (WebMail) on a regular basis – at least three times per week. To access your WebMail account, login using your UTAS username and password at https://webmail.utas.edu.au/. You are strongly advised not to forward your UTAS emails to an external email service (such as gmail or Hotmail). In the past, there have been significant issues where this has occurred, resulting in UTAS being blacklisted by these email providers for a period of up to one month. To keep informed, please use your UTAS email as often as possible. *IMPORTANT* Please email teaching staff when you have a question or issue of a personal nature, for example, you have a family issue that is affecting your studies. For general questions about the unit, please add them to the Q&A forum on our unit’s MyLO site. This way, other students can also benefit from the answers. We receive a lot of emails. Be realistic about how long it might take for us to respond. Allow at least two (2) business days to reply. Staff are not required to respond to emails where students do not directly identify themselves, are threatening or offensive, or come from external (non-UTAS) email accounts. Please be advised I will respond ONCE to a non-UTAS email address primarily to remind you that your UTAS email address should be used in correspondence. When you write an email, you must include the following information. This helps teaching staff to determine who you are and which unit you are talking about.

Family name;

Preferred name;

Student ID;

Unit code (i.e., BFA715)

Questions

If your question is about an assessment task, please include the assessment task number or name.

BFA 715 Accounting Theory 12

Assessment

Assessment Schedule In order to pass this unit you must achieve an overall mark of at least 50% of the total available marks. However, I do expect students to achieve a minimum 40% in the examination in addition to an overall grade of 50%. Details of each assessment item are outlined below.

Assessment Items Due Date Value/Weighting Link to Learning Outcomes

Forum/Mini Debate At designated workshop

12 Marks/12% Refer to Table 1

Team Review and Report (and summary)

Progressive through semester

8 Marks/8% Refer to Table 1

Reflective Journal Weekly entry on MyLo 5 Marks/5% Refer to Table 1

Research Project 13 May 2015 25 Marks/25% Refer to Table 1

Examination As determined by Exams Office

50 Marks/50% Refer to Table 1

Total 100 Marks/100%

Assessment Item 1 – Forum/Mini Debates Task Description:

Students will be allocated to teams – Mini Debates will consist of 2 groups of 4 students, Academic Forums will consist of 4 students. Evidence of individual participation in whichever role you are allocated to will be required. Groups will be randomly formed.

Task Length

The equivalent of 3000 words. This will be discussed in the lecture component week 1.

Assessment Criteria:

Refer to the assessment rubric on page 28.

Link to Unit’s Learning Outcomes:

Refer to Table 1

Due Date:

Progressively across the semester dependent on the unit schedule as attached. Random groups will be determined in the first week of semester.

Value:

12 marks

BFA 715 Accounting Theory 13

Assessment Item 2 – Team Review and Report Task Description:

Groups, randomly selected, will be required to explore questions selected from the text. Each week selected groups will report back to the group. A report on responses to questions will be required to be loaded onto MyLo prior to the relevant Workshop to assist other students.

Task Length

400 to 500 words preparation per workshop plus three oral presentations throughout the semester

Assessment Criteria:

Refer to the assessment rubric on page 30.

Link to Unit’s Learning Outcomes:

Refer to Table 1

Due Date:

Progressively across the semester dependent on the unit schedule as attached. Random groups will be determined in the first week of semester.

Value:

8 Marks

Assessment Item 3 – Reflective Journal Task Description:

Students will be required to write brief reflections about the theoretical skills in accounting that they have acquired in the past week, and explore how this might contribute to a practicing accountants activities in the real world.

Task Length

200 words per week

Assessment Criteria:

Refer to the assessment rubric on page 33.

Link to Unit’s Learning Outcomes:

Refer to Table 1

Due Date:

Weekly activity throughout the semester. These will be monitored and will be required by Sunday evenings no later than 6.00pm.

Value:

5 Marks

BFA 715 Accounting Theory 14

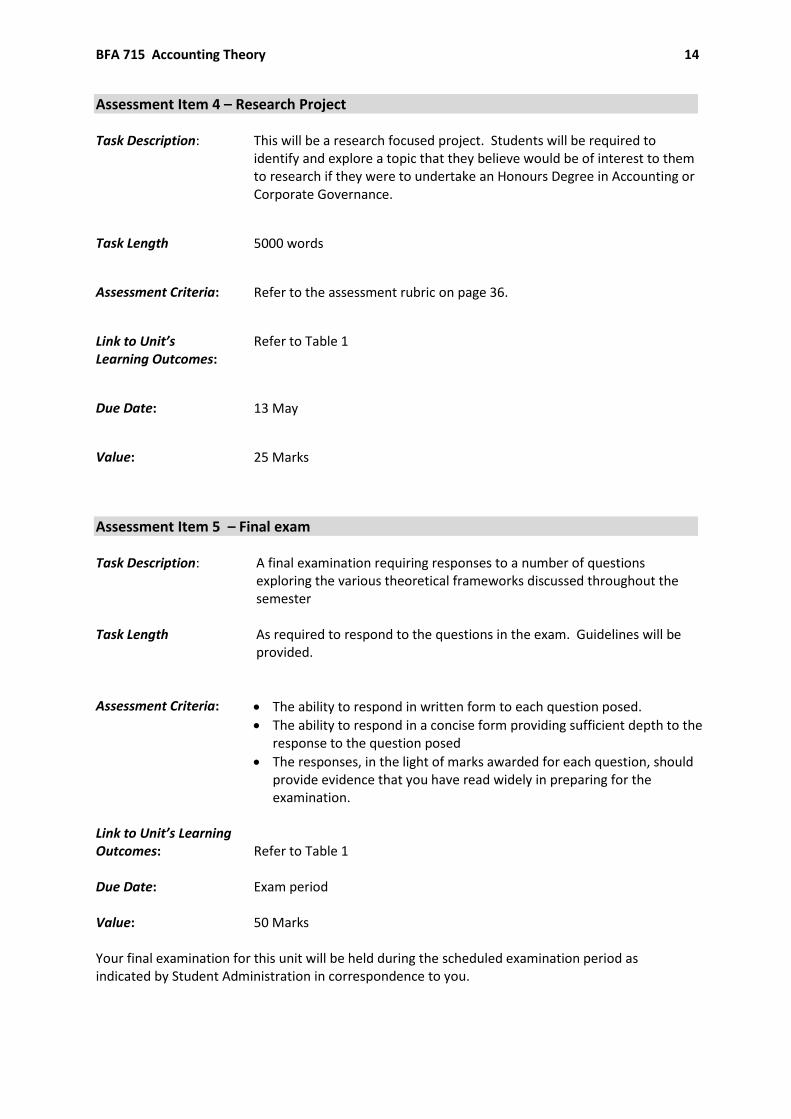

Assessment Item 4 – Research Project Task Description: This will be a research focused project. Students will be required to

identify and explore a topic that they believe would be of interest to them to research if they were to undertake an Honours Degree in Accounting or Corporate Governance.

Task Length

5000 words

Assessment Criteria:

Refer to the assessment rubric on page 36.

Link to Unit’s Learning Outcomes:

Refer to Table 1

Due Date:

13 May

Value:

25 Marks

Assessment Item 5 – Final exam Task Description:

A final examination requiring responses to a number of questions exploring the various theoretical frameworks discussed throughout the semester

Task Length

As required to respond to the questions in the exam. Guidelines will be provided.

Assessment Criteria:

The ability to respond in written form to each question posed.

The ability to respond in a concise form providing sufficient depth to the response to the question posed

The responses, in the light of marks awarded for each question, should provide evidence that you have read widely in preparing for the examination.

Link to Unit’s Learning Outcomes:

Refer to Table 1

Due Date:

Exam period

Value:

50 Marks

Your final examination for this unit will be held during the scheduled examination period as indicated by Student Administration in correspondence to you.

BFA 715 Accounting Theory 15

Examinations will normally be scheduled Monday to Saturday inclusive. Examinations may be held during the day or evening and students should consult the university information which will be made available towards the end of semester.

You are advised to make any necessary arrangements with employers now for time off during the examination period to sit this examination. Your participation at the scheduled time is not negotiable unless there are exceptional circumstances. Note that you will be expected to sit the examination at your recorded study centre. To find out more go to the Exams Office website: http://www.utas.edu.au/exams/home.

Submission of Assessment Items

Lodging Assessment Items Assignments must be submitted electronically through the relevant assignment drop box in MyLO. Students must ensure that their name, student ID, unit code, tutorial time and tutor’s name are clearly marked on the first page. If this information is missing, the assignment will not be accepted and, therefore, will not be marked.

Where appropriate, unit coordinators may also request students submit a paper version of their assignments.

Please remember that you are responsible for lodging your assessment items on or before the due date and time. We suggest you keep a copy. Even in ‘perfect’ systems, items sometimes go astray.

Late Assessment and Extension Policy In this Policy 1. (a) ‘day’ or ‘days’ includes all calendar days, including weekends and public holidays;

(b) ‘late’ means after the due date and time; and (c) ‘assessment items’ includes all internal non-examination based forms of assessment

2. This Policy applies to all students enrolled in TSBE Units at whatever Campus or geographical location.

3. Students are expected to submit assessment items on or before the due date and time specified in the relevant Unit Outline. The onus is on the student to prove the date and time of submission.

4. Students who have a medical condition or special circumstances may apply for an extension. Requests for extensions should, where possible, be made in writing to the Unit Coordinator on or before the due date. Students will need to provide independent supporting documentation to substantiate their claims.

BFA 715 Accounting Theory 16

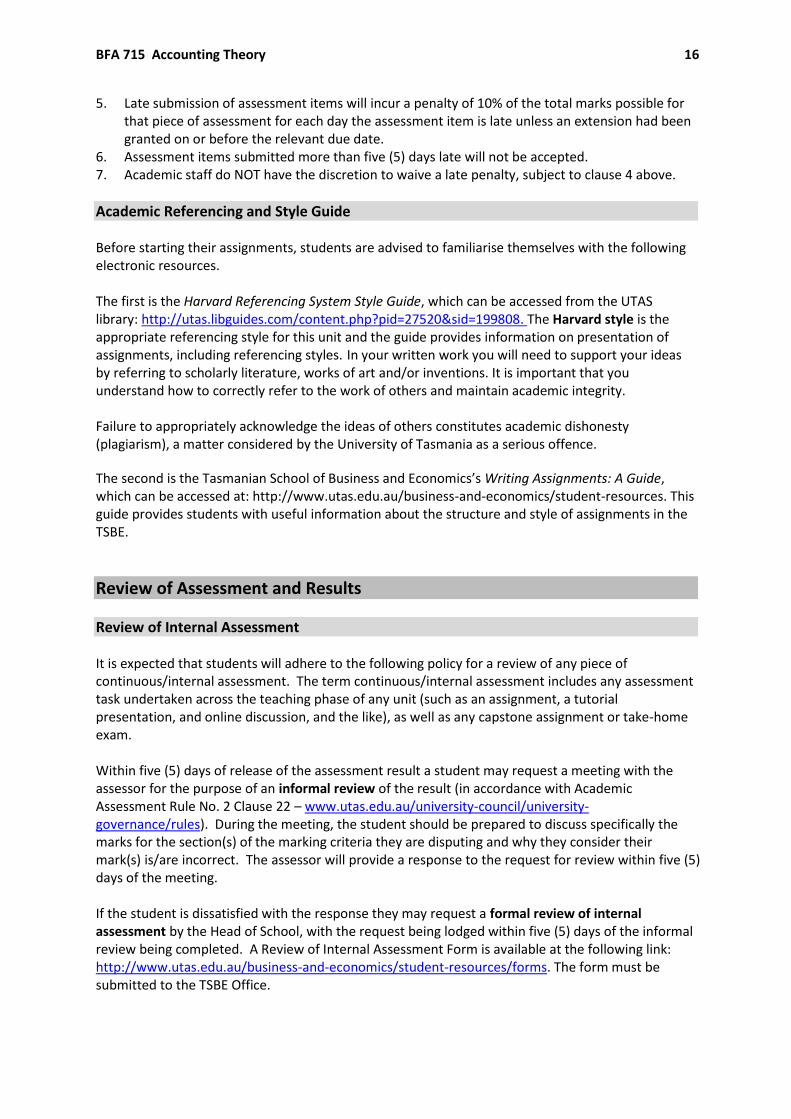

5. Late submission of assessment items will incur a penalty of 10% of the total marks possible for that piece of assessment for each day the assessment item is late unless an extension had been granted on or before the relevant due date.

6. Assessment items submitted more than five (5) days late will not be accepted. 7. Academic staff do NOT have the discretion to waive a late penalty, subject to clause 4 above.

Academic Referencing and Style Guide Before starting their assignments, students are advised to familiarise themselves with the following electronic resources. The first is the Harvard Referencing System Style Guide, which can be accessed from the UTAS library: http://utas.libguides.com/content.php?pid=27520&sid=199808. The Harvard style is the appropriate referencing style for this unit and the guide provides information on presentation of assignments, including referencing styles. In your written work you will need to support your ideas by referring to scholarly literature, works of art and/or inventions. It is important that you understand how to correctly refer to the work of others and maintain academic integrity. Failure to appropriately acknowledge the ideas of others constitutes academic dishonesty (plagiarism), a matter considered by the University of Tasmania as a serious offence.

The second is the Tasmanian School of Business and Economics’s Writing Assignments: A Guide, which can be accessed at: http://www.utas.edu.au/business-and-economics/student-resources. This guide provides students with useful information about the structure and style of assignments in the TSBE.

Review of Assessment and Results

Review of Internal Assessment It is expected that students will adhere to the following policy for a review of any piece of continuous/internal assessment. The term continuous/internal assessment includes any assessment task undertaken across the teaching phase of any unit (such as an assignment, a tutorial presentation, and online discussion, and the like), as well as any capstone assignment or take-home exam. Within five (5) days of release of the assessment result a student may request a meeting with the assessor for the purpose of an informal review of the result (in accordance with Academic Assessment Rule No. 2 Clause 22 – www.utas.edu.au/university-council/university-governance/rules). During the meeting, the student should be prepared to discuss specifically the marks for the section(s) of the marking criteria they are disputing and why they consider their mark(s) is/are incorrect. The assessor will provide a response to the request for review within five (5) days of the meeting. If the student is dissatisfied with the response they may request a formal review of internal assessment by the Head of School, with the request being lodged within five (5) days of the informal review being completed. A Review of Internal Assessment Form is available at the following link: http://www.utas.edu.au/business-and-economics/student-resources/forms. The form must be submitted to the TSBE Office.

BFA 715 Accounting Theory 17

Review of Final Exam/Result

In units with an invigilated exam students may request a review of their final exam result. You may request to see your exam script after results have been released by completing the Access to Exam Script Form, which is available from the TSBE Office, or at the following link – http://www.utas.edu.au/business-and-economics/student-resources/forms. Your unit coordinator will then contact you by email within five (5) working days of receipt of this form to go through your exam script.

Should you require a review of your final result a formal request must be made only after completing the review of exam script process list above. To comply with UTAS policy, this request must be made within ten (10) days from the release of the final results (in accordance with Academic Assessment Rule No. 2 Clause 22 – www.utas.edu.au/university-council/university-governance/rules). You will need to complete an Application for Review of Assessment Form, which can be accessed from http://www.utas.edu.au/exams/exam-and-results-forms. Note that if you have passed the unit you will be required to pay $50 for this review.

The TSBE reserves the right to refuse a student request to review final examination scripts should this process not be followed.

Further Support and Assistance If you are experiencing difficulties with your studies or assessment items, have personal or life-planning issues, disability or illness that may affect your study, then you are advised to raise these with your lecturer or tutor in the first instance. If you do not feel comfortable contacting one of these people, or you have had discussions with them and are not satisfied, then you are encouraged to contact:

DIRECTOR OF POSTGRADUATE PROGRAMS Name: Dr Rob Hecker Room: 304, Commerce Building, Sandy Bay Email: [email protected]

Students are also encouraged to contact their Undergraduate Student Adviser who will be able to help in identifying the issues that need to be addressed, give general advice, assist by liaising with academic staff, as well as referring students to any relevant University-wide support services. Please refer to the Student Adviser listings at www.utas.edu.au/first-year/student-advisers for your adviser’s contact details. There is also a range of University-wide support services available to students, including Student Centre Administration, Careers and Employment, Disability Services, International and Migrant Support, and Student Learning and Academic Support. Please refer to the Current Students website (available from www.utas.edu.au/students) for further information. If you wish to pursue any matters further then a Student Advocate may be able to assist. Information about the advocates can be accessed from www.utas.edu.au/governance-legal/student-complaints. The University also has formal policies, and you can find out details about these policies from the following link – http://www.utas.edu.au/registrar/student-complaints/.

BFA 715 Accounting Theory 18

Academic Misconduct and Plagiarism Academic misconduct includes cheating, plagiarism, allowing another student to copy work for an assignment or an examination, and any other conduct by which a student: (a) seeks to gain, for themselves or for any other person, any academic advantage or advancement

to which they or that other person are not entitled; or (b) improperly disadvantages any other student.

Students engaging in any form of academic misconduct may be dealt with under the Ordinance of Student Discipline. This can include imposition of penalties that range from a deduction/cancellation of marks to exclusion from a unit or the University. Details of penalties that can be imposed are available in the Ordinance of Student Discipline – Part 3 Academic Misconduct, see http://www.utas.edu.au/university-council/university-governance/ordinances. Plagiarism is a form of cheating. It is taking and using someone else’s thoughts, writings or inventions and representing them as your own, for example: • using an author’s words without putting them in quotation marks and citing the source; • using an author’s ideas without proper acknowledgment and citation; or • copying another student’s work. It also means using ones’ own work from previously submitted assessment items if repeating a unit. If you have any doubts about how to refer to the work of others in your assignments, please consult your lecturer or tutor for relevant referencing guidelines, and the academic integrity resources on the web at http://www.academicintegrity.utas.edu.au/ The intentional copying of someone else’s work as one’s own is a serious offence punishable by penalties that may range from a fine or deduction/cancellation of marks and, in the most serious of cases, to exclusion from a unit, a course, or the University. The University and any persons authorised by the University may submit your assessable works to a plagiarism checking service, to obtain a report on possible instances of plagiarism. Assessable works may also be included in a reference database. It is a condition of this arrangement that the original author’s permission is required before a work within the database can be viewed. For further information on this statement and general referencing guidelines, see www.utas.edu.au/plagiarism/ or follow the link under ‘Policy, Procedures and Feedback’ on the Current Students homepage.

BFA 715 Accounting Theory 19

Study Schedule

Week

Start of Week

Topic/s and activities

Text Chapter/s

Due Dates

1 Monday 23 February Introduction Ch1

2 Monday 2 March

Financial Reporting Environment Ch2

3 Monday 9 March

Financial Regulation Ch3

4 Monday 16 March

International Accounting Ch4

5 Monday 23 March

Measurement Issues Ch5

6a Monday 30 March

Normative Theory Ch6

Mid-Semester Break: 2 – 8 April 2015 inclusive

6b

Classes resume Thursday 9 April

7 Monday 13 April

Positive Accounting Theory Ch7

8 Monday 20 April

Systems Orientated Theory Ch8

9 Monday 27 April

CSR Factors Ch9

10

Monday 4 May Capital Markets Ch10

11

Monday 11 May Behavioural Research Ch11 13 May Research Project Due

12

Monday 18 May Critical Theory Ch12

13

Monday 25 May Revision

Examination Period: 6-23 June 2015

BFA 715 Accounting Theory 20

Tutorial/Workshop Schedule Please note that the tutorial schedule commences in week 2 of semester.

Week

Start of Week

Topic/s and activities

Text Chapter/s

2 Monday 2 March

Introduction, Financial Reporting Environment

Students should read the chapters from Deegan’s text, lecture slides and other material supplied such as team response to assessment tasks loaded on MyLo, and academic journal articles made available to supplement other material.

3 Monday 9 March

Financial Regulation

4 Monday 16 March

International Accounting

5 Monday 23 March

Measurement Issues

6a Monday 30 March

Normative Theory

Mid-Semester Break: 2 – 8 April 2015 inclusive

6b

Classes resume Thursday 9 April

7 Monday 13 April

Positive Accounting Theory

8 Monday 20 April

Systems Orientated Theory

9 Monday 27 April

CSR Factors

10

Monday 4 May Capital Markets

11

Monday 11 May Behavioural Research

12

Monday 18 May Critical Theory

13

Monday 25 May Revision

Examination Period: 6-23 June 2015

BFA 715 Accounting Theory 21

Indicative Time Allocation for Workshops Study area summary 60 minutes Directed Team work and report back 50 minutes Break 10 minutes Forum/Mini Debate (Assessment Task 1) x 2 60 minutes

Table 2: Semester Activities Schedule

Week Topic Area Forum (4 Presenters)

Directed Team Work, report back

Mini Debates (2 teams of 4)

Reflective Journal of Learning

1 Introduction

2 Financial reporting environment

Y

3 Regulation 4 Y Y

4 International accounting

Y 12 Y

5 Measurement 16 Y Y

6 Normative Theories 20 Y Y

7 Positive Accounting Theory

Y 28 Y

8 Systems Orientated Theories

32 Y Y

9 CSR Factors Y 40 Y

10 Capital Markets Y 48 Y

11 Behavioural Research

52 Y Y

12 Critical Theory Y 60 Y

13 Revision Y

BFA 715 Accounting Theory 22

Assessment Task 1 – Forums and Mini Debate Schedules

Assessment Task 1

Forum Topic Participants Role

Week 3 Historical Cost 1.

2.

3.

4.

Week 5 Conceptual Framework 1.

2.

3.

4.

Week 6 Disclosure – Voluntary and Regulated

1.

2.

3.

4.

Week 8 PAT 1.

2.

3.

4.

Week 11 System Orientated Theory

1.

2.

3.

4.

Mini Debate Topic Team 1 [For] Team 2 [Against]

Week 4 Motivation/Disclosure 1.

2.

3.

4.

1.

2.

3.

4.

BFA 715 Accounting Theory 23

Week 7 Accountability 1.

2.

3.

4.

1.

2.

3.

4.

Week 9 Culture 1.

2.

3.

4.

1.

2.

3.

4.

Week 10 Research in Accounting 1.

2.

3.

4.

1.

2.

3.

4.

Week 12 Critical Perspective 1.

2.

3.

4.

1.

2.

3.

4.

Week 3 Historical Cost Accounting [Forum] Historical Cost Accounting is a traditional valuation method as it reflects only on the past cost of the asset, however in the contemporary business environment companies must remain flexible and transparent. Issues that should be addressed include:

What Does Historical Cost Mean?

What are the criticisms of the historical costs method?

What alternatives are there to historical cost accounting?

How is historical accounting better than alternatives?

BFA 715 Accounting Theory 24

Week 4 Motivation/Disclosure [Mini Debate} “The main focus of prior research has been whether corporate social disclosures constitute a discharge of accountability or are part of a process of legitimation. Prior research, however, ignores the emergence of an alternate style of corporate social disclosure, the ‘solicited’ disclosure.” p.1 Van der Laan, S. 2009. The Role of Theory in Explaining Motivation for Corporate Social Disclosure: Voluntary Disclosures V. ‘Solicited’ Disclosures. The Australasian Accounting, Business and Finance Journal. Feb. V3/4. pp.15-29.

Team For: The motivation for disclosure has been for legitimacy purposes and focuses on perception.

Team Against: The motivation for disclosure has been for accountability purposes and focuses providing information.

Week 5 Conceptual Frameworks [Forum] The Conceptual Framework sets out the concepts that underlie the preparation and presentation of financial statements. It is a practical tool that assists the IASB when developing and revising IFRSs. The objective of the Conceptual Framework project is to improve financial reporting by providing the IASB with a complete and updated set of concepts to use when it develops or revises standards. Issue that should be addressed include:

What is a conceptual framework in accounting?

Why did the accounting community choose to develop a conceptual framework?

How does the conceptual framework assist in addressing accounting practice, and assist in filling gaps where rules do not exist?

Were there difficulties in preparing the conceptual framework? Is it complete? Why not?

Is the international framework comparable to the previous Australian version?

Week 6 Disclosure – Voluntary and Regulated [Forum] wiseGEEK noted: “An accounting disclosure is a statement released by a company, business, or corporation that identifies the financial strategies that are being used and reveals things like costs and profits for a certain calendar period. The main purpose of this sort of document is to inform both current and potential investors of the accounting strategies and methods used. These financial statements include, but are not limited to, the balance sheet, the statement of cash flows, the income statement, and the statement of stockholders’ equity. The full disclosure principle of most legal systems requires that any event that would have an impact on the financial statements should be revealed, and the laws of many countries set out specific guidelines for both how and when disclosures need to be made. Companies often release this sort of information in their annual reports, but there are a number of acceptable publication methods in most places.” http://www.wisegeek.org/what-is-accounting-disclosure.htm accessed 27 November 2014 Issues that you may wish to discuss include:

Do you agree with this view?

What do you understand by disclosure?

What types of disclosure are there?

Why do you think voluntary disclosures have increased significantly in recent years?

Indications of a movement to integrated reporting will impact on disclosure in what way(s)

BFA 715 Accounting Theory 25

Week 7 Accountability [Mini Debate] As an individual or business there is need for a level of accountability to ensure your life or business is governed above board. Accounting is part of the business systems every business must have to help manage the resources and processes. You can only tell the health of the company if you have the correct Accounting system in place. One of the reasons behind the failure of some businesses is the fact that there is minimal or no accountability of the leaders to the board or the board to the employees and [to other stakeholders]. If no one can be held responsible for the business' performance then that business suffers from stunted growth. Rabu, 05 September 2012 Accountability Through Accounting http://falandodepolicia.blogspot.com.au/2012/09/ accountability-through-accounting.html accessed 27 Nov 2 2014.

Team For: Argue the case for increased accountability by business in accounting disclosure Team Against: Argue the case against increased accountability by business in accounting disclosure

Week 8 Positive Accounting Theory [Forum] There is some confusion about what PAT is. If the definition of accounting theory (i.e., accounting theory seeks to explain and predict accounting and auditing practice) given in Watts and Zimmerman’s 1986 book is taken to mean PAT, studies of accounting choices and auditing practices constitute PAT. At the same time, they also seek to explain the economics-based empirical literature in accounting and they describe, in addition to accounting choice studies, capital market-based accounting research. They point out that Ball and Brown (1968) initially popularized positive research in accounting, suggesting that PAT includes both capital market-based accounting research and research in accounting choices. This paper takes PAT to include both research programs. This usage is consistent with Watts and Zimmerman’s (1986) assertion that when they use the term “positive” to differentiate it from “prescriptive” theory. Kabir, M. Humayun. Positive Accounting Theory and Science. Journal of CENTRUM Cathedra TM. pp.136-149. Issues to include:

What is PAT?

What are criticisms of PAT?

Does PAT assist in developing an understanding of accounting theory and practice?

Why did researchers seek alternate theoretical explanations in efforts to understand accounting practices?

BFA 715 Accounting Theory 26

Week 9 Culture [Mini Debate] “Accounting is far more than methodologies, numbers and financial statements. It holds to basic rules and standards to preserve the profession’s purpose, but is also shaped by a variety of internal and external forces. The accounting practice actually signified and symbolizes the culture in which it is performed.” p.4 Young, M. 2013. Cultural Influences on Accounting and Accounting Practice. http://digitalcommons.liberty.edu/cgi/viewcontent.cgi?article=1396&context=honors accessed 27 Nov 2014.

Many countries now adopt international accounting standards to guide accounting in practice.

Team For: IFRS is an appropriate direction for accounting practice to ensure consistency and comparability of accounting practice across the world.

Team Against: IFRS is not an appropriate direction for accounting standards as culture plays a significant role in the way accounting practice should be undertaken in a country, and differences between countries should be recognised.

Week 10 Research and Theory [Mini Debate] “Around 1970 there was a dramatic change in the approach to accounting research. Several reasons have been suggested for this change in methodological direction by those reviewing the development of accounting thought.” p.1 Gaffikin, M. 2007. Accounting Research and Theory: The Age of Neo-Empiricism. The Australasian Accounting, Business and Finance Journal. Feb. V1/1. pp1-19.

Team for: The conceptual framework is an example of theoretical development and research that has contributed greatly to the development of accounting practice.

Team Against: The conceptual framework is an example of theoretical development and research that has not contributed meaningly to the development of accounting practice if for no other reason than it has not been completed.

Week 11 System Orientated Theories [Forum] Legitimacy Theory and Stakeholder Theory are two theoretical perspectives that have been adopted by a number of researchers in recent years. The theories are sometimes referred to as “systems-oriented theories”. Within a systems-based perspective, the entity is assumed to be influenced by, and in turn to have influence upon, the society in which it operates. Within both legitimacy theory and Stakeholder theory, accounting disclosure polices are considered to constitute a strategy to influence the organisation’s relationships with the other parties with which it interacts. [Gray Owen and Adam 1996] According to Gray, Owen and Adams (1996), Legitimacy Theory and Stakeholder Theory are both derived from a broader theory which has been called “Political Economy Theory”. Issues that should be addressed include:

What do we mean by a ‘systems orientated theory’?

How does political economy theory play a role?

What do we mean by legitimacy theory (and social contract)?

What is meant by stakeholder theory?

Is institutional theory a systems orientated theory?

BFA 715 Accounting Theory 27

Week 12 Critical Perspectives [Mini Debate] “Critical theory has influenced research in many countries. … Broadbent asks why we need critical accounting…”p.10 Gaffikin, M. 2006. The Critique of Accounting Theory. Faculty of Business, University of Wollongong, Working Papers. 06/25.

Team For: Critical research has an important role in accounting research to encourage thought about current practice.

Team Against: Critical research has no role to play, it is vague and offers no advice as to what accounting practice should look like.

BFA 715 Accounting Theory 28

Assessment Task 1 – Mini Debates and Workshop Forums - Rubric: Mini Debates and Discussion Forums Criteria HD (high distinction >8)

Exceeding expectations

D (Distinction 7- <8)

Fully meeting expectations

CR (Credit 6 - <7)

Meeting expectations

PP (Pass 5 - <6)

Approaching expectations

NN (Unsatisfactory - <5)

Not meeting expectations

Overall: reflect in criteria below Responds creatively and knowledgably to the topic area.

Identify few if any areas for

improvement.

Responds fully to the topic area with well developed argument.

But areas of improvement

identifiable.

Responds competently to the topic area, arguments generally

well developed but displays

limited creativity and substantive gaps in knowledge identified.

Arguments generally not well developed and substantive

revisions identifiable

Responds inappropriately to the topic area. Substantive revisions

would be required to address the

topic adequately.

Preparation: Written Comprehensive, well developed presentation, well supported

arguments

Well developed, direction clear, well argued and logically

presented

Competent argument developed but gaps in content and clarity of

presentation less than clear

Gaps in knowledge clear. Claims predictable but not well

developed. Wider reading

lacking.

Material preparation an inappropriate response to the

argument to be developed.

Inadequate preparation clear.

Presentation: Oral Able to present clearly, concisely and with clarity. Creative choice

of presentation techniques.

Engage audience. Position on topic well developed and

defended.

Well developed, direction clear, well argued and logically

presented. Competent oral

presentation. Eye contact with audience.

Competent presentation but lacked creativity and was unable

to maintain audience attention

Presentation lacking in confidence and gaps in

knowledge clear. Inability to

respond to audience on some issues.

Poor presentation. Read directly from notes. Did not engage the

audience.

Analysis of Information Identified all the points in the case/article which should be

addressed and comprehensively

analysed and evaluated each point.

Identified most points in the case/article that should be

addressed and analysed and

evaluated each point.

Identified most points in the case/article that should be

addressed and a reasonable

analysis and evaluation of each point.

Identified some points in the case/article that should be

addressed but a limited analysis

and evaluation indicating only a partial understanding of the

topic.

Identified few or no points in the case/article that should be

addressed and analysed and

evaluated each point inadequately.

Engagement with Audience Engaged audience by:

maintaining eye contact, using suitable gestures and

body language

responding to the audience

in a confident manner

a conversational tone

fluent speech without

reading notes

questioning to suit content,

audience and purpose

clarified content with real world examples

Engaged audience by

maintaining eye contact, using suitable gestures and body language

responding to the audience in a confident manner

a conversational tone

fluent speech without reading notes

questioning to suit content, audience and purpose

clarified content with real world examples

Partially engaged audience by:

occasionally making eye contact and using limited

gestures and body language

responding to the audience

in a hesitant manner

halting speech with some reading of notes

questioning that suits content, audience and

purpose to some extent

did not clarify content with real world examples

Sat in front of an audience and:

occasionally made eye contact

asked questions from a script/slides

may have acknowledged their

responses

Response to Audience Responded successfully to all questions and supported responses with

authorities from the literature and/or logical reasoning

Responded successfully to some

questions and supported

responses with authorities from

the literature and/or logical

reasoning

Responded successfully to some

questions but did not support

them all with authorities from the

literature and/or logical

reasoning

Did not respond to any questions

successfully and did not support

them all with authorities from the

literature and/or logical

reasoning

An assessment will be completed for each student. Students will need to clearly identify their role in preparing the Debate or Forum.

BFA 715 Accounting Theory 29

Assessment Task 2 – Directed Team Work and Report Back*

Week Directed Team Work and Report Back (5 Minutes) Tasks (Deegan Text)(6 per team)

Team 1 Team 2 Team 3 Team 4 Team 5 Team 6 Team 7 Team 8 Team 9 Team 10

2 1.11,2.20 1.12,2.21 1.13,2.22 1.15,2.23 1.17,2.26 1.22,2.11 1.24,2.13 1.30,2.16 1.33,2.17 1.34,2.19

3 3.2, 3.25 3.5,3.28 3.8,3.29 3.13,3.30 3.12,3.32 3.17,3.34 3.18,3.35 3.21,3.33 3.24,3.31 3.19,3.11

4 4.1,4.34 4.3,4.33 4.4,4.31 4.5,4.28 4.6,4.25 4.8,4.24 4.9,4.23 4.10,4.19 4.12,4.32 4.15,4.29

5 5.1,5.20 5.2,5.21 5.4,5.14 5.5,5.22 5.6,5.23 5.7,5.24 5.8,5.25 5.9,5.27 5.10,5.29 5.13,5.30

6 6.1,6.32 6.3,6.30 6.5,6.29 6.6,6.28 6.7,6.27 6.8,6.26 6.10,6.20 6.11,6.18 6.12,6.14 6.13,6.15

7 7.1,7.33 7.3,7.29 7.4,7.25 7.5,7.24 7.7,7.22 7.8,7.20 7.9,7.30 7.11,7.18 7.13,7.31 7.14,7.15

8 8.1,8.23 8.7,8.26 8.9,8.27 8.11,8.28 8.14,8.29 8.16,8.30 8.17,8.31 8.19,8.36 8.20,8.37 8.21,8.42

9 9.5,9.27 9.8,9.28 9.9,9.29 9.10,9.33 9.12,9.34 9.18,9.39 9.20,9.40 9.24,9.41 9.25,9.42 9.26,9.45

10 10.1,11.3 10.4,11.4 10.10,11.7 10.18,11.9 10.19,11.13 10.20,11.15 10.24,11.17 10.25,11.11 10.28,11.18 10.26,11.12

11 12.1,12.11 12.2,12.12 12.3,12.13 12.4,12.14 12.5,12.15 12.6,12.16 12.7,12.17 12.8,12.18 12.9,12.19 12.10,12.20

Students will be allocated randomly to teams.

Teams will be selected at random to report back.

Only team members present at the workshop will receive an assessment

Each team each week will provide a brief solution on MyLo to the questions for which they were

responsible

BFA 715 Accounting Theory 30

Assessment Task 2 – Rubric - Directed Team Work and Report Back

Criteria HD (high distinction >8)

Exceeding expectations

D (Distinction 7- <8)

Fully meeting expectations

CR (Credit 6 - <7)

Meeting expectations

PP (Pass 5 - <6)

Approaching expectations

NN (Unsatisfactory - <5)

Not meeting expectations

Preparation – Written Full answer/response prepared. Evidence of wider reading.

Excellent resources provided to

workshop members

Full answer/response prepared. Quality resources provided to

workshop members

Largely well thought out response but gaps in the material.

Competent resources provided to

workshop members

A competent response to the question

No response made or the response was largely incorrect

Presentation - Oral Present clearly, concisely, comprehensively and with

clarity. Well developed,

direction clear, well argued and logically presented.

Well developed, direction clear, well argued and logically

presented.

Competent presentation but clarity and direction lacking.

Presentation lacking in confidence and gaps in

knowledge clear. Inability to

respond to audience on some issues.

Poor presentation. Read directly from notes. Did not engage the

audience.

Audience engagement Active input sought from

audience

Some input was sought from the audience but few questions posed

and audience input not sought

Presented well but sought no

active input.

Presented poorly and did neither

responded too or asked questions of the audience

Group participation Clear that all team members

actively contributed.

Evidence that there was joint

contribution.

Evidence that the group did meet

but no evidence that a team

prepared the work

Evidence that the team did not

meet.

No interaction identifiable

BFA 715 Accounting Theory 31

Task 3 – Reflective Journal Entries

Students are required to write a 200word reflective journal entry at the end of each week. This entry is to appear on MyLo by 10.00pm each Sunday. This reflective entry is for you to indicate what you have learnt in theory for that week. Remember reflection is: Reflection is an everyday process. We reflect on a range of everyday problems and situations all the time: What went well? What didn’t? Why? How do I feel about it? Structured reflection If we consciously reflect, maybe as part of our work or family role, there tends to be a rough process of ‘How did it go? What went well? Why? What didn’t? Why? What next?’ Examples might be of a football coach reflecting after a match, a teacher reflecting on a lesson, or simply a parent thinking about how best to deal with a teenager. In this kind of reflection, the aim is to look carefully at what happened, sort out what is really going on and explore in depth, in order to improve, or change something for next time. This brief guide will look at what is meant by reflection, suggest forms of structured reflection to improve the way you learn, and also outline how to use a model of reflection to structure a reflective assignment

Key elements of reflection

Reflection is a type of thinking associated with deep thought, aimed at achieving better understanding. It contains a mixture of elements:

1. Making sense of experience We don’t always learn from experiences. Reflection is where we analyse experience, actively attempting to ‘make sense’ or find the meaning in it.

2. ‘Standing back’ It can be hard to reflect when we are caught up in an activity. ‘Standing back’ gives a better view or perspective on an experience, issue or action.

3. Repetition Reflection involves ‘going over’ something, often several times, in order to get a broad view and check nothing is missed

4. Deeper honesty Reflection is associated with ‘striving after truth’. Through reflection, we can acknowledge things that we find difficult to admit in the normal course of events.

5. ‘Weighing up’ Reflection involves being even-handed, or balanced in judgement. This means taking everything into account, not just the most obvious.

6. Clarity Reflection can bring greater clarity, like seeing events reflected in a mirror. This can help at any stage of planning, carrying out and reviewing activities.

7. Understanding Reflection is about learning and understanding on a deeper level. This includes gaining valuable insights that cannot be just ‘taught’.

BFA 715 Accounting Theory 32

8. Making judgements Reflection involves an element of drawing conclusions in order to move on, change or develop an approach, strategy or activity.

3

Reflection and learning Reflecting on your learning, and as part of your learning, can help you take an objective view of your progress and see what is going well and what needs working on. Whatever form your reflection takes, it should initially involve you examining your feelings about an experience, then identifying areas to develop and starting to think about ways to do this.

A Template:

Reflective Learning Diary: Entry Date:

WHAT Brief notes indicating what you have completed this week. A critique of your weeks activities.

WHY Brief analytical notes: Why did you do this work? Was it useful? What learning outcomes were achieved? What part of the unit did this work assist you with?

REACTION What is your emotional response to this activity? How did you find it? Were you able to achieve what you intended? Did you face and embrace difficulties?

LEARNED What did you learn from the work you undertook?

GOAL SETTING What will you do next? How will you resolve any difficulties faced? Or implement improvements identified?

BFA 715 Accounting Theory 33

Assessment Task 3 – Rubric – Reflective Journal

Criteria HD (high distinction >8)

Exceeding expectations

D (Distinction 7- <8)

Fully meeting expectations

CR (Credit 6 - <7)

Meeting expectations

PP (Pass 5 - <6)

Approaching expectations

NN (Unsatisfactory - <5)

Not meeting expectations

Completion 12 10-11 8-9 6-7 <6

Depth of Reflection

Response demonstrates an in-depth reflection. Viewpoints and interpretations are insightful and well supported. Clear, detailed examples are provided, as applicable.

Response demonstrates a general reflection. Viewpoints and interpretations are supported. Appropriate examples are provided, as applicable.

Response demonstrates a minimal reflection Viewpoints and interpretations are unsupported or supported with flawed arguments. Examples, when applicable, are not provided or are irrelevant.

Response demonstrates a lack of reflection. Viewpoints and interpretations are missing, inappropriate, and/or unsupported. Examples, when applicable, are not provided.

Not complete

Required Components

Response includes all components and exceeds all requirements

Response includes all components and meets all requirements

Response does not fully meet the requirements

Response excludes essential components and/or does not address the requirements. Many parts are addressed minimally, inadequately, and/or not at all.

Not complete

Structure

Writing is clear, concise, and well organized with excellent sentence/paragraph construction. Thoughts are expressed in a coherent and logical manner. There are no more than three spelling, grammar, or syntax errors.

Writing is mostly clear, concise, and well organized with good sentence/paragraph construction. Thoughts are expressed in a coherent and logical manner. There are no more than five spelling, grammar, or syntax errors.

Writing is unclear and/or disorganized. Thoughts are not expressed in a logical manner. There are more than five spelling, grammar, or syntax errors.

Writing is unclear and disorganized. Thoughts ramble and make little sense. There are numerous spelling, grammar, or syntax errors throughout the response.

Not Complete

Evidence and Practice

Response shows strong evidence of synthesis of ideas presented and insights gained throughout

Response shows evidence of synthesis of ideas presented and insights gained

Response shows little evidence of synthesis of ideas presented and insights gained.

Response shows no evidence of synthesis of ideas presented and insights gained

Not complete

BFA 715 Accounting Theory 34

Task 4 – Research Focused Project - 25%

This project is intended to introduce you to the research process that underlies much of the work and theoretical discussions you have undertaken this semester. You will need to draw on skills learnt and on your thinking about the information provided in lectures and in the textbook, in the tutorials and through the academic journal articles you have read this semester.

This task will be completed in a number of parts identified below:

Identify an area of research that you believe is both important and of interest to you, and write a short paragraph indicating why you believe this area of research is important, and why it is interest to you. (350 words)

Briefly describe the research problem you would like to explore. Identify a research question that would lead your exploration of the problem. (250 words)

Find TEN (10) academic journal articles that relate to your area of research interest – write a maximum of ten lines for each article indicating why that article is relevant to your research, and why the information will contribute to being able to support the research investigation proposed. (1400 words max)

Normally when undertaking research we would have expectations about what the findings might be. In responding to your research question what result(s) would you expect to find? (200 words)

In 500 words indicate which of the accounting theories you have studied this year would help to you explain the expectations you have for your research question. What role would this theory play in your research? Why this theory more appropriate than other choices?

How would you collect the data to respond to your research question? Why do you think this approach is appropriate? For example, searching a data base, content analysis of annual reports, a mail, internet or telephone survey, conduct of interviews. (200 words).

Do you think that ethical considerations are important to your research? In undertaking research at UTAS ethical approval is required. What do you need to do at UTAS to obtain ethical approval? (200 words)

In seeking to respond to your Research Question(s) what questions would you need to ask respondents, or what questions would you need to ask to interrogate data collected from a data base or an annual report? Identify TEN (10) questions that you believe would need to be asked, and indicate why these questions would need to be asked to gather the information you require to respond to your research question. (400 words)

BFA 715 Accounting Theory 35

SECTION 2 — RATIONALE FOR RESEARCH PROPOSAL – Research Plan UTAS

In this section you bring together your response to the questions above in the preparation of a research plan. Rationale for the research may include a brief overview of current knowledge of the topic and a statement/s about the key hypotheses, questions and/or aims of the research (1500 words)

“The Research Plan provides the blueprint for a candidate's higher degree by research (HDR) and must be completed within the first six months (4 months for Masters, equivalent full time) of candidature.

The Research Plan maps the aims, methods, directions and milestones of the degree.

The Research Plan outlines the rationale, research context and structural outline. The Plan is a guiding document, and because the research process is, by its nature, dynamic, it should be continually updated.”

In this document you will argue the case for the research interest you identify, justification and support and identify academic literature that supports the research. You will also identify the question(s) you would ask. The first eight questions provide the guide to this section.

Task length

A maximum of 5000 words

The word limit specified for your assignment is a maximum. If you submit over-length work there is an automatic 10% penalty of available marks. It is at the discretion of the Unit Coordinator whether the words beyond the limit will be assessed. Title pages, reference lists and appendices are not included in word counts.

Links to learning outcomes:

Refer to the Table 1. Assessment criteria:

Marks awarded will be based on the criteria identified in the rubric for example students will need to demonstrate the following skills: evidence of research; relevance and understanding of the issues and concepts; strength of argument developed; use of language; quality of explanations and presentation style; readability of the essay and use of Harvard referencing.

Date due: 13 May 2015. You require both: Electronic copy loaded to MyLo by 12 midnight 13 May. A hard copy in the assignment box by 5.00pm 13 May.

BFA 715 Accounting Theory 36