Unit - IV -Entrepreneurship

21

UNIT -IV BREAKEVEN ANALYSIS

-

Upload

aparna-kalla -

Category

Documents

-

view

221 -

download

1

description

Role of KVIC, NABARD

Transcript of Unit - IV -Entrepreneurship

UNIT -IVBREAKEVEN ANALYSIS

INTRODUCTION

• A breakeven analysis is used to determine how much sales volume your business needs to start making a profit.

• The breakeven analysis is especially useful when you're developing a pricing strategy, either as part of a marketing plan or a business plan.

BREAK EVEN CALCULATER

• Fixed Cost:The sum of all costs required to produce the first unit of a product. This amount does not vary as production increases or decreases, until new capital expenditures are needed.

• Variable Unit Cost:Costs that vary directly with the production of one additional unit.

• Expected Unit Sales:Number of units of the product projected to be sold over a specific period of time.

•Unit Price:The amount of money charged to the customer for each unit of a product or service.

• Total Variable Cost:The product of expected unit sales and variable unit cost. (Expected Unit Sales * Variable Unit Cost )

• Total Cost:The sum of the fixed cost and total variable cost for any given level of production. (Fixed Cost + Total Variable Cost )

• Total Revenue:The product of expected unit sales and unit price. (Expected Unit Sales * Unit Price )

• Profit (or Loss):The monetary gain (or loss) resulting from revenues after subtracting all associated costs. (Total Revenue - Total Costs)

• BREAK EVEN POINT:Number of units that must be sold in order to produce a profit of zero (but will recover all associated costs).

• Break Even Point (IN UNIT)= Fixed Cost /S. Price- Variable Unit Cost

• Break Even Point (in Rs)=Fixed Cost/ S. Price-Variable unit Cost*Units

• For example, suppose that your fixed costs for producing 100,000 product were 30,000 rs a year.

• Your variable costs are 2.20 rs materials, 4.00 rs labour, and 0.80 rs overhead, for a total of 7.00 rs per unit.

• If you choose a selling price of 12.00 rs for each product, then:

• 30,000 divided by (12.00 - 7.00) equals 6000 units.

• This is the number of products that have to be sold at a selling price of 12.00 rs before your business will start to make a profit.

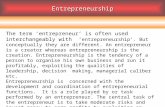

Break-Even AnalysisCosts/Revenue

Output/Sales

FC

VC

TCTR (p = £2)

Q1

Loss

Profit

USES OF BREAK EVEN POINT

• Helpful in deciding the minimum quantity of sales

• Helpful in the determination of tender price• Helpful in examining effects upon

organization’s profitability• Helpful in deciding about the substitution of

new plants• Helpful in sales price and quantity• Helpful in determining marginal cost

LIMITATIONS

• Break-even analysis is only a supply side (costs only) analysis, as it tells you nothing about what sales are actually likely to be for the product at these various prices.

• It assumes that fixed costs (FC) are constant • It assumes average variable costs are constant per unit of

output, at least in the range of likely quantities of sales. • It assumes that the quantity of goods produced is equal to

the quantity of goods sold (i.e., there is no change in the quantity of goods held in inventory at the beginning of the period and the quantity of goods held in inventory at the end of the period.

• In multi-product companies, it assumes that the relative proportions of each product sold and produced are constant.

Social Cost Benefit Analysis

What is Social Cost Benefit Analysis ?

• So, to reflect the real value of a project to society, we must consider the impact of the project on society.

Impact

Positive Negative (Social Benefit) (Social Cost)

Thus ,when we evaluate a project from the view point of

the society (or economy) as a whole, it is called Social Cost

Benefit Analysis (SCBA)/Economic Analysis.

• Social cost-benefit analysis is a systematic and cohesive economic tool(method) to survey all the impacts caused by an urban development project.

• It comprises not just the financial effects (investment costs, direct benefits like tax and fees, et cetera), but all the social effects, like: pollution, safety, indirect (labour) market, legal aspects, etc.

Core differences between CBA & SCBA

CBA SCBA• Limited range of effects are considered as it measures the profitability of individuals who are only a part of the society.

• The evaluator has to take a wider view as it tries to measure social values of the whole society.

• It is quantitative in nature.

• It can be quantitative or qualitative.

Scope of SCBA

• SCBA can be applied to both Public & private investments – ▫Public Investment:

SCBA is important specially for the developing countries where govt. plays a significant role in the economic development.

▫Private Investment:Here, SCBA is also important as the private investments are to be approved by various governmental & quasi-governmental agencies.

Objectives of SCBA

The main focus of Social Cost Benefit Analysis is to determine:1. Economic benefits of the project in terms of

shadow prices;2 The impact of the project on the level of

savings and investments in the society;3. The impact of the project on the distribution of

income in the society;4. The contribution of the project towards the

fulfillment of certain merit wants (self- sufficiency, employment etc).

Significances of SCBA

• CBA is unable to reflect social values. Hence SCBA has been emerged with some interesting significances. These significances also make the SCBA different from the CBA.

Market Imperfections Externalities Taxes & Subsidies Concern for Savings Concern for Redistribution Merit Wants

Significances of SCBA (Contd.)• Market Imperfections:

Market prices, the basis for CBA, do not reflect the

social values under imperfect market competition.

• Externalities:A project may have beneficial or harmful

external effects that are considered in SCBA, not in CBA.

• Taxes & Subsidies:From the social point of view, taxes & subsidies

arenothing but transfer payments. But in CBA,

taxes & subsidies are treated as monetary costs andbenefits respectively.

Significances of SCBA (Contd.)Concern for Savings:

In SCBA, the division between benefits & consumption is relevant wherein higher valuation is placed on savings.But in CBA such division is irrelevant.

Concern for Redistribution:

In SCBA, the distribution of benefits is very much concerning issue where commercial private firm does not bother about it.

Merit Wants:

Merit wants are important from the social point of view and therefore, SCBA considers these wants.

Approaches to SCBA

• There are two principal approaches for Social Cost Benefit Analysis. A. UNIDO Approach, and B. L-M Approach.

A. UNIDO Approach: This approach is mainly based on the publication of

UNIDO (United Nation Industrial Development Organization)named Guide to Practical Project Appraisal in 1978.

B. L-M Approach: I.M.D Little & J.A.Mirlees have developed this approach

for analysis of Social Cost-Benefit in Manual of Industrial Project Analysis in Developing Countries and Project Appraisal & Planning for Developing Countries.