Unit 1-tk-part-2

31

Corporate Tax Planning - Unit I RESIDENTIAL STATUS (AY: 2016-17) Dr. THULASI KRISHNA. K, Ph.D. Dept. of Management Studies MITS – Madanapalle, A.P., India

-

Upload

madanapalle-institute-of-technology-science -

Category

Law

-

view

136 -

download

0

Transcript of Unit 1-tk-part-2

Corporate Tax Planning - Unit I

RESIDENTIAL STATUS (AY: 2016-17)

Dr. THULASI KRISHNA. K, Ph.D.

Dept. of Management Studies

MITS – Madanapalle, A.P., India

Residential Status Dr.TK

• Determination of residential status of a person is very important for the purpose of levy of

income tax, as income tax is levied based on the residential status of tax payer.

• What is essential is the status during the previous year and not in the assessment year.

Moreover, the concept of residential status is nothing to do with the nationality or domicile

of a person.

• The residential status of the assessee may change from year to year.

• An Indian, who is a citizen of India, can be non-resident for Income Tax purposes,

whereas a foreigner can be resident of India for Income Tax purpose.

Tax Liability = Total Income * Rate of Tax

Residential Status ≠ Citizenship

Residential Status

Resident Non - Resident

Ordinarily Resident

Not Ordinarily Resident

Section 6(1)

Section 6(6)

Taxable Entity

A taxable entity can be:

• An Individual

• A Hindu Undivided Family

• A firm

• An Association of Persons

• Joint stock company

• any other person

• The following table explains how these are subcategorized with respect to theirresidential status.

INDIVIDUAL/HUF

RESIDENT

ORDINARY

NOT-ORDINARY

NON-RESIDENT Others Included in the Definition of

“Person”

RESIDENT NON-RESIDENT

Determining the Residential Status of An Individual

• Section 6(1): This section applies to individuals. If an individual is to qualify as

resident of India, he has to fulfill at least one of the following two basic

conditions:

Condition Explanation

1 He is in India in the previous year for a period of 182 days or more

2He is in India for a period of 60 days or more during the previous year and

365 days or more during 4 years immediately preceding the previous year

Exceptions:

In the following two cases, an individual needs to be present in India for a period of 182 days

or more in order to become resident in India:

1. An Indian citizen who leaves India during the previous year for the purpose of taking

employment outside India

2. An Indian citizen leaving India during the previous year as a member of the crew of an

Indian ship.

3. An Indian citizen or a person of Indian origin who comes on visit to India during the

previous year (a person is said to be of Indian origin if either he or any of his parents

or any of his grand parents was born in undivided India).

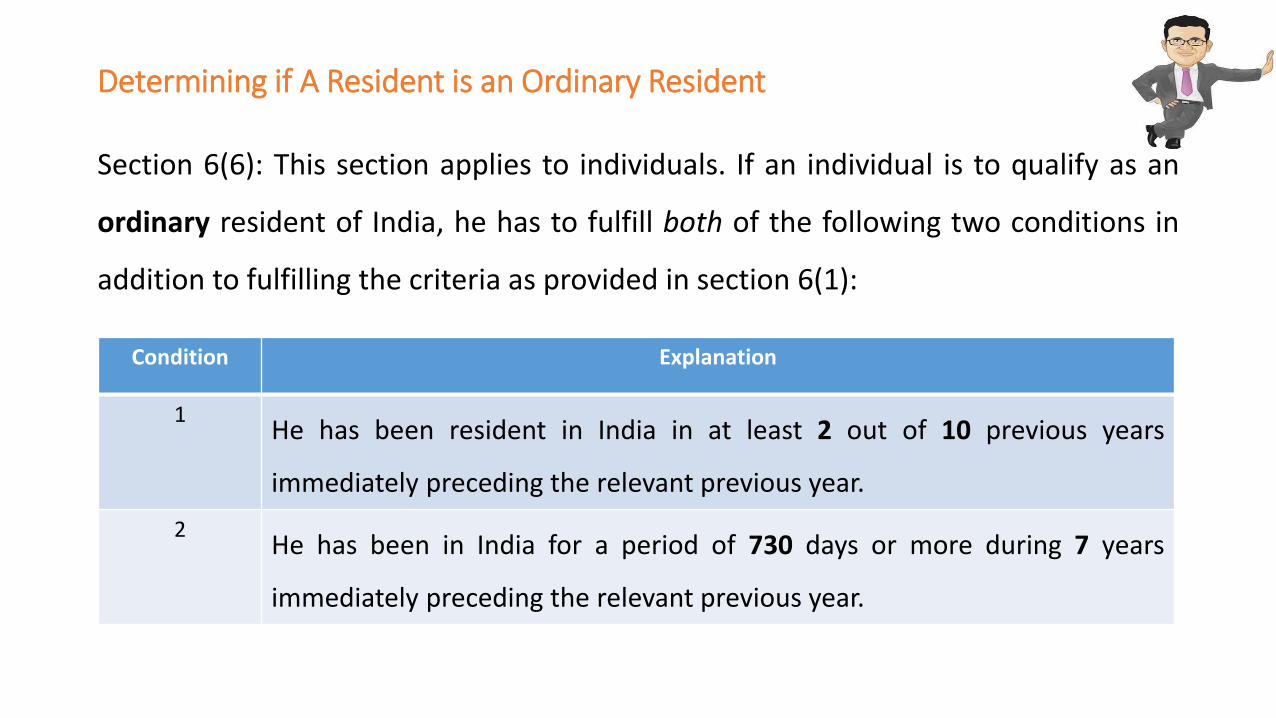

Determining if A Resident is an Ordinary Resident

Section 6(6): This section applies to individuals. If an individual is to qualify as an

ordinary resident of India, he has to fulfill both of the following two conditions in

addition to fulfilling the criteria as provided in section 6(1):

Condition Explanation

1He has been resident in India in at least 2 out of 10 previous years

immediately preceding the relevant previous year.

2He has been in India for a period of 730 days or more during 7 years

immediately preceding the relevant previous year.

• Individuals who satisfy any one of the basic conditions and do not satisfy the

two additional conditions, are classified as Resident but not ordinary resident.

• Individuals not satisfying anyone of the basic conditions will be classified as

Non-Resident.

Determining the Residential Status of HUF/Firm/AOP/AJP

• Section 6(2): This section applies to Hindu Undivided Family. The distinction under this

section is made as:

“A Hindu undivided family is said to be resident in India if control and management of

its affairs is wholly or partly situated in India. A Hindu undivided family is non-

resident in India if control and management of its affairs is wholly situated outside

India.”

• Control and management is situated at a place where the head, the seat and the

directing power are situated.

• Section 6(6)(b): A resident Hindu undivided family is an ordinarily resident in

India if the karta or manager of the family business satisfies the following two

additional conditions:

Condition Explanation

1He has been resident in India in at least 2 out of 10 previous years

immediately preceding the relevant previous year.

2He has been in India for a period of 730 days or more during 7 years

immediately preceding the relevant previous year.

Residential Status of Company

• As per section 6(3), an Indian company is always resident in India.

• A foreign company is resident in India only if, during the previous year, control

and management of its affairs is situated wholly in India.

• However, a foreign company is treated as non-resident if, during the previous

year, control and management of its affairs is either wholly or partly situated out

of India.

To put it simple,

• Resident: If Control and Management of its business affairs is wholly in India.

• Non-Resident: If Control and Management of its business affairs is wholly or

partly outside India.

• The residential status of a company and the place of its control and management

should not be decided by the location of the registered office of the company.

• As a rule, the direction, management and control, the head, seat, and directing power

of a company’s affairs are situated at the place where the directors’ meetings are held.

• Consequently, a company would be resident in the country if the meetings of directors

who manage and control the business are held there.

Case: Narottam & Periera Ltd., Vs CIT (1953)

• It is not what directors have power to do, but what they actually do, that is of

importance in determining the question of the place where the control is

exercised.

Definition of Company

Company [Sec. 2(17)]: The expression ‘company’ is defined to mean the following:

• Any Indian company; or

• Any body corporate incorporated under the laws of a foreign country; or

• Any institution, association or a body which is assessed or was assessable/assessed as a

company for any assessment year commencing on or before April 1, 1970; or

• Any institution, association or a body, whether incorporated or not and whether Indian or

non-Indian, which is declared by general or special order of the Central Board of Direct Taxes

to be a company.

Indian Company [Sec. 2(26)]:

An Indian company means a company formed and registered under the Companies Act, 1956. Besides, it includes the following:

• A company formed and registered under any law relating to companies formerly in force in any part of India other than the State of

Jammu and Kashmir and the Union territories;

• A corporation established by or under a Central, State of Provincial Act;

• Any institution, association or body which is declared by the Board to be a company under section 2(17);

• A company formed and registered under any law in force in the State of Jammu and Kashmir;

• A company formed and registered under any law for the time being in force in the Union territories of Dadra and Nagar Haveli, (State of)

Goa, Daman and Diu and Pondicherry.

In the aforesaid cases, a company, corporation, institution, association or body will be treated as an Indian company only if its registered

office is in India.

Domestic Company:

• As per Section 2(22A), "domestic company" means an Indian company, or any

other company which, in respect of its income liable to tax under this Act, has

made the prescribed arrangements for the declaration and payment of dividends

within India in accordance with section 194.

Foreign Company:

• As per Section 2(23A) of the Income Tax Act, 1961, Foreign Company is a

company which is not a domestic company. Thus, all those companies which do

not qualify the conditions to be considered domestic company shall be

considered foreign companies.

Industrial Company:

• It means a company which is mainly engaged in the business of generation or

distribution of electricity or any other form of power or in the construction of

ships or in the manufacture or processing of goods or in mining.

The following activities are held as ‘manufacture’ or ‘processing’ of goods on the basis of judicial

pronouncements:

• Book publishing

• Mixing different types of tea to arrive at a desired blend

• Manufacture and selling of carpets but having major source of income from sale of import entitlement

(generated by export of carpets)

• Production of cinematographic films

• Tailoring clothes

• Conversion of computer cash vouchers, invoices, etc., into balance sheet, stock account, etc.

• Sorting out, washing, drying and blending wool.

• Undergoing a change in a commodity as a result of some operation (many be manual or mechanical)

and as a result a new and distinct commodity emerges.

A Company in which Public are Substantially Interested: [Sec. 2(18)]

• Owned by Government/RBI – A company owned by the Government or the RBI or in

which not less than 40% shares (in terms of value) are held by the Government or the

Reserve Bank or a corporation owned by the Reserve Bank. Ex. BEML, BHEL, BPCL etc.

• Section 25 companies – A company registered under section 25 of the Companies Act,

1956, namely companies for promotion of commerce, art, science, religion, charity and

prohibiting the payment of any dividends to its members. Ex: International Bible Society

India, Association of Lady Entrepreneurs of Andhra Pradesh, Ravindranath Medical

Foundation, etc.

• A company without share capital - A company having no share capital and declared by the

Central Board of Direct Taxes to be a company in which the public are substantially interested.

• Nidhi or Mutual Benefit Society- A company which carries on, as its principal business, the

business of acceptance of deposits from its members and which is declared by the Central

Government under section 620A of the Companies Act to be a Nidhi or Mutual Benefit Society.

• Company owned by a Co-operative Society - If it is company in which shares carrying at least 50%

of the voting power have been allotted unconditionally to or acquired unconditionally by, and are

throughout the relevant previous year beneficially held by, one or more cooperative societies; or

• Listed Companies - If it is company which is not a private company as defined in Section 3 of the

Companies Act, 1956 and equity shares of the company were, as on the last day of the relevant

previous year, listed in a recognised stock exchange in India;

Investment Company:

• It means a company whose gross total income consists mainly of income which is

chargeable under the heads ‘Income from House Property’, ‘Capital Gains’ and

‘Income from other sources’.

Ex.: Larsen & Toubro Mutual Fund, Tata Investment Corporation

Widely-held Company

• A company in which the public are substantially interested is known

as widely-held company.

Closely-held Company :

• A company in which the public are not substantially interested is

known as a closely-held company.

Ex.: Family owned companies

Incidence Of Tax for Corporate Assessees

Particulars Resident in India Non-resident in India

Indian income Taxable in India Taxable in India

Foreign income Taxable in India Not Taxable in India

• Indian income is always taxable in India irrespective of the residential

status of the taxpayer.

• Foreign income is taxable in the hands of resident in India. Foreign income

is not taxable in the hands of non-resident in India.

Indian Income

Any of the following three is an Indian income –

• If income is received or deemed to be received in India during the previous year and at

the same time it accrues or is deemed to accrue in India during the previous years.

• If income is received or deemed to be received in India during the previous year but it

accrues outside India during the previous year.

• If income is received outside India during the previous year but it accrues or is deemed

to accrue in India during the previous year.

Foreign Income

If the following two conditions are satisfied, then such income is ‘foreign

income’-

• Income is not received or not deemed to be received in India; and

• Income does not accrue or does not deemed to accrue in India.

•Thank You