UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS

171

● U N I F I E D G O V E R N M E N T ● W y a n d o t t e C o u n t y ● K a n s a s C i t y , K a n s a s UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS “Wyandotte County Strong Communites, Friendly People, & Exciting Entertainment!!!” COMPREHENSIVE ANNUAL FINANCIAL REPORT For the fiscal year ended December 31, 2010

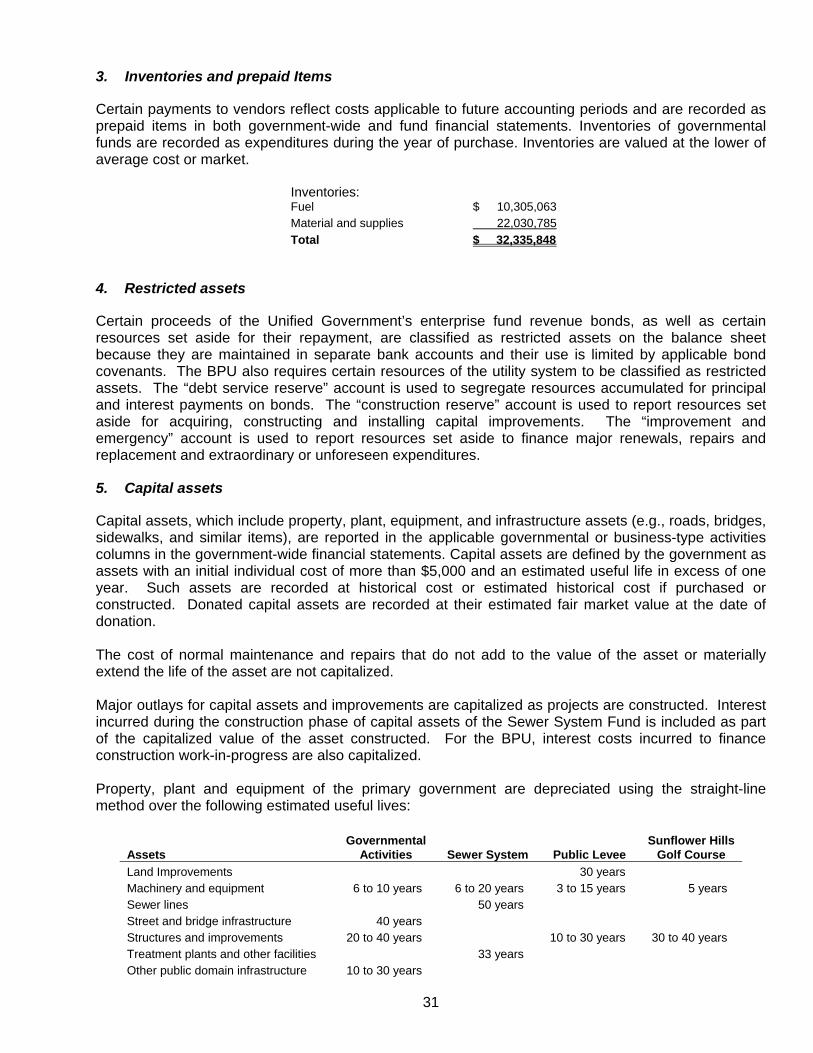

Transcript of UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS

● U

NIF

IED GOVERNMENT ●

Wyandotte County ● Kansas

City, K

ansa

s

UNIFIED GOVERNMENT OFWYANDOTTE COUNTY/KANSAS CITY, KANSAS

“Wyandotte CountyStrong Communites, Friendly People,

& Exciting Entertainment!!!”

COMPREHENSIVE ANNUAL FINANCIAL REPORTFor the fiscal year ended December 31, 2010

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS

COMPREHENSIVE ANNUAL FINANCIAL REPORT For the year ended DECEMBER 31, 2010

REASONABLE ACCOMMODATIONS WILL BE MADE TO QUALIFIED INDIVIDUALS WITH DISABILITIES ON AN AS NEEDED BASIS, PROVIDED ADEQUATE NOTICE IS GIVEN.

Prepared by:

Finance Department of the Unified Government of Wyandotte County/Kansas City, Kansas

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS COMPREHENSIVE ANNUAL FINANCIAL REPORT For the year ended DECEMBER 31, 2010

TABLE OF CONTENTS Page

INTRODUCTION Transmittal Letter ----------------------------------------------------------------------------------------------------------- i

Executive Staff ------------------------------------------------------------------------------------------------------------ xvii

Organizational Chart --------------------------------------------------------------------------------------------------- xviii

Certificate of Achievement for Excellence in Financial Reporting ------------------------------------------- xix

FINANCIAL SECTION

Independent Auditors’ Report ------------------------------------------------------------------------------------------- 2

Management’s Discussion and Analysis ----------------------------------------------------------------------------- 4

Basic Financial Statements

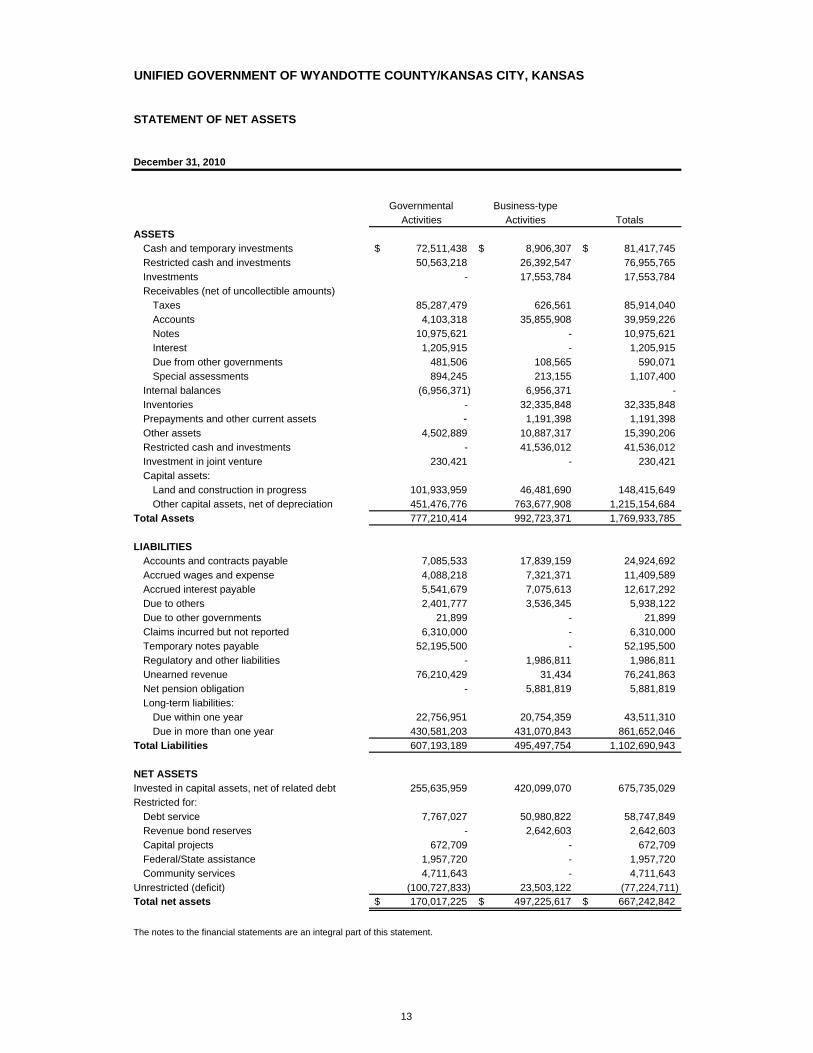

Government-wide Financial Statements: Statement of Net Assets ------------------------------------------------------------------------------------ 13 Statement of Activities --------------------------------------------------------------------------------------- 14

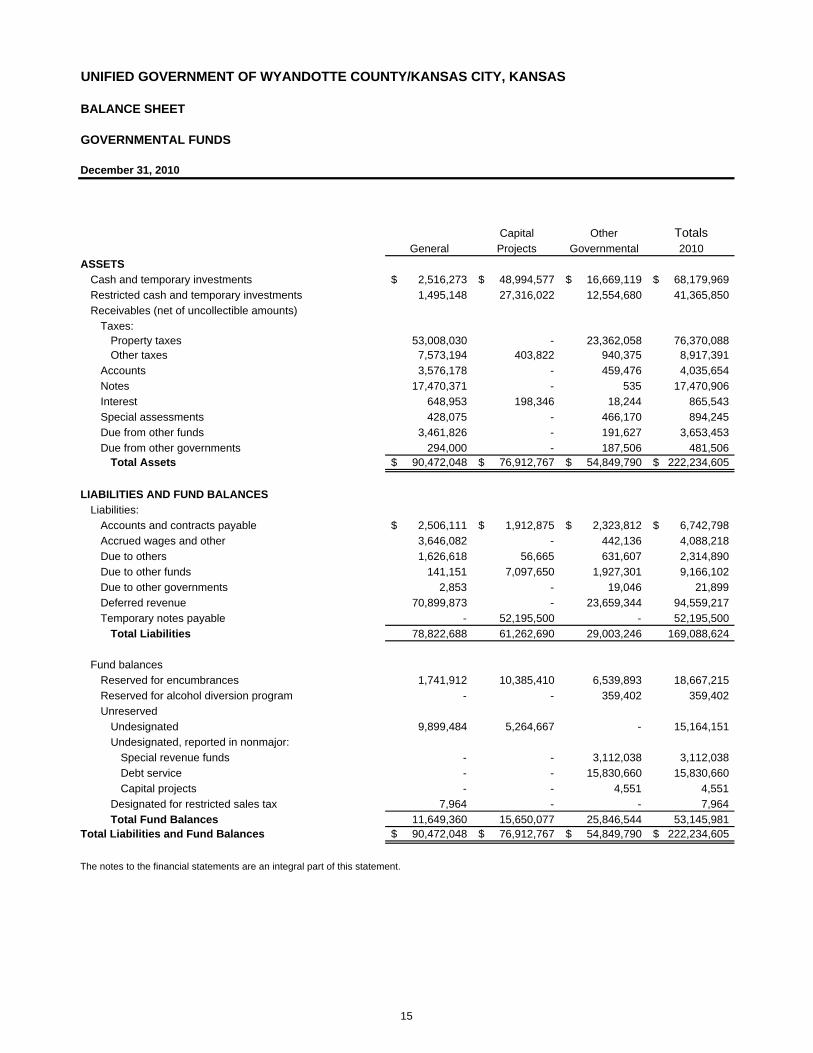

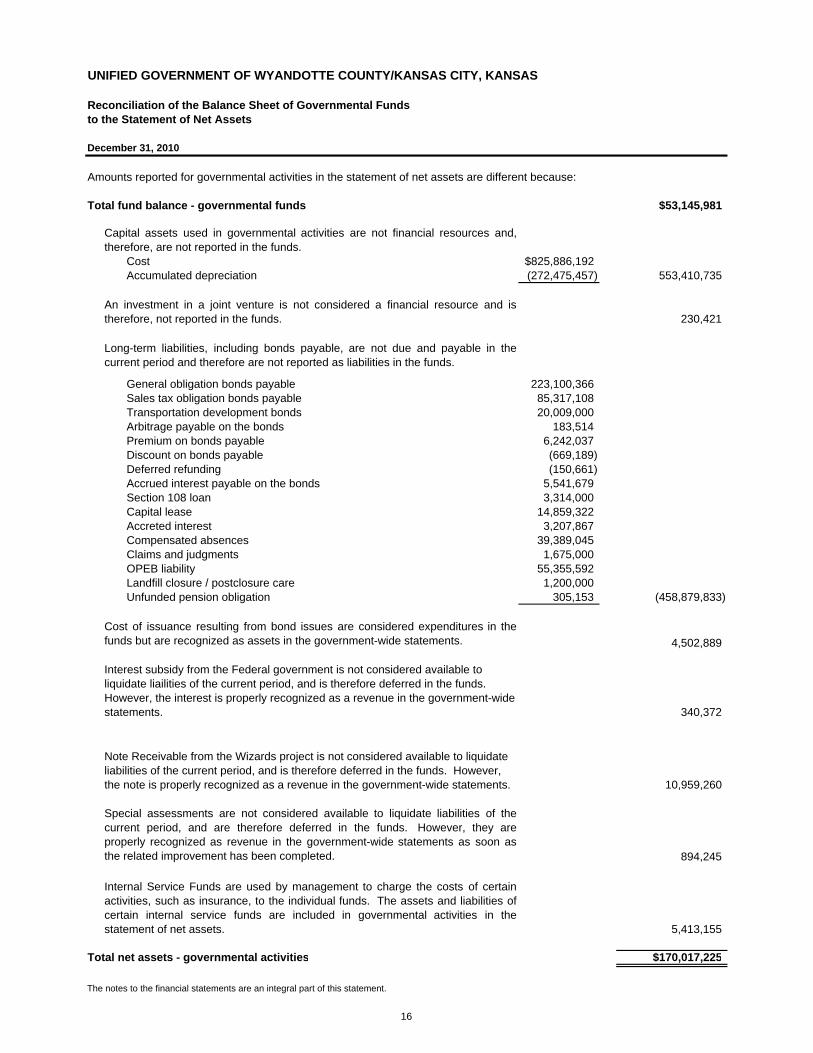

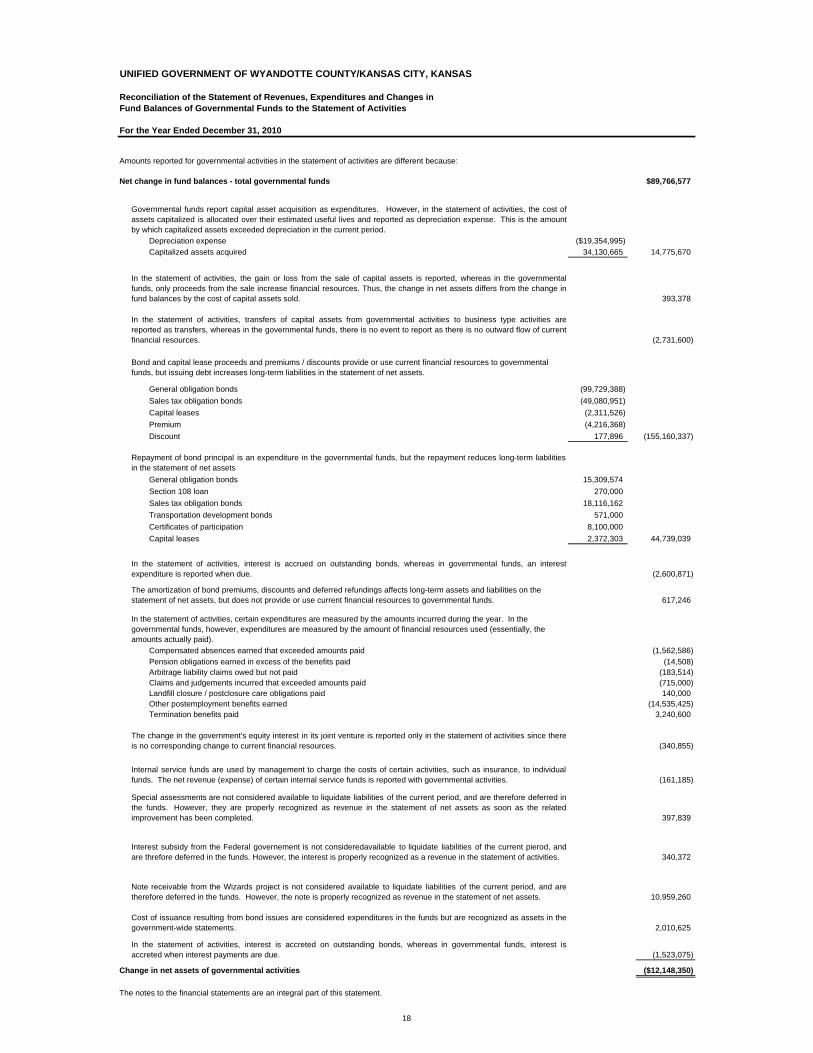

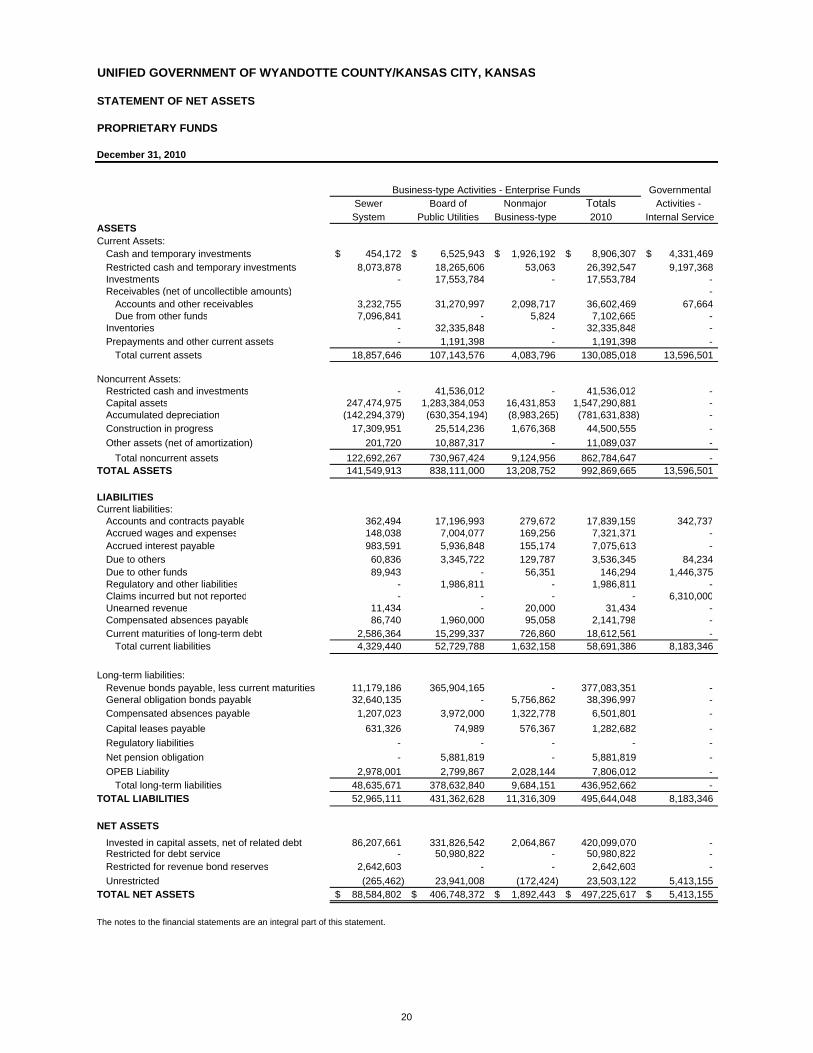

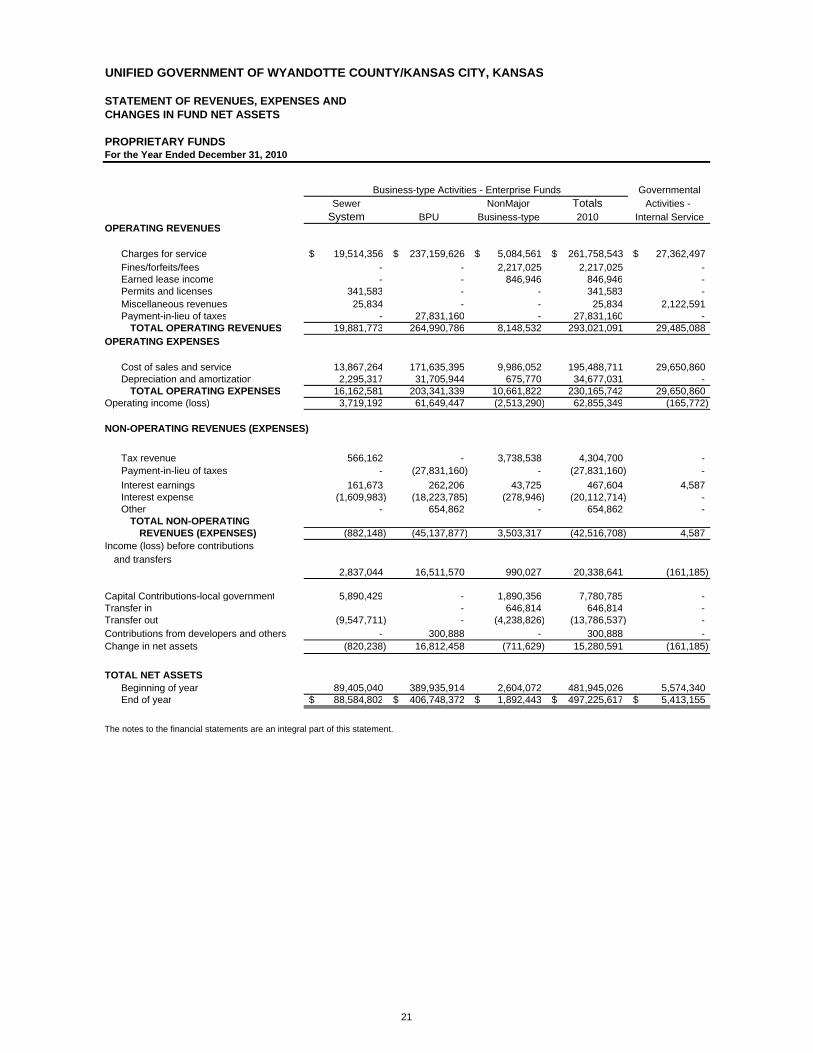

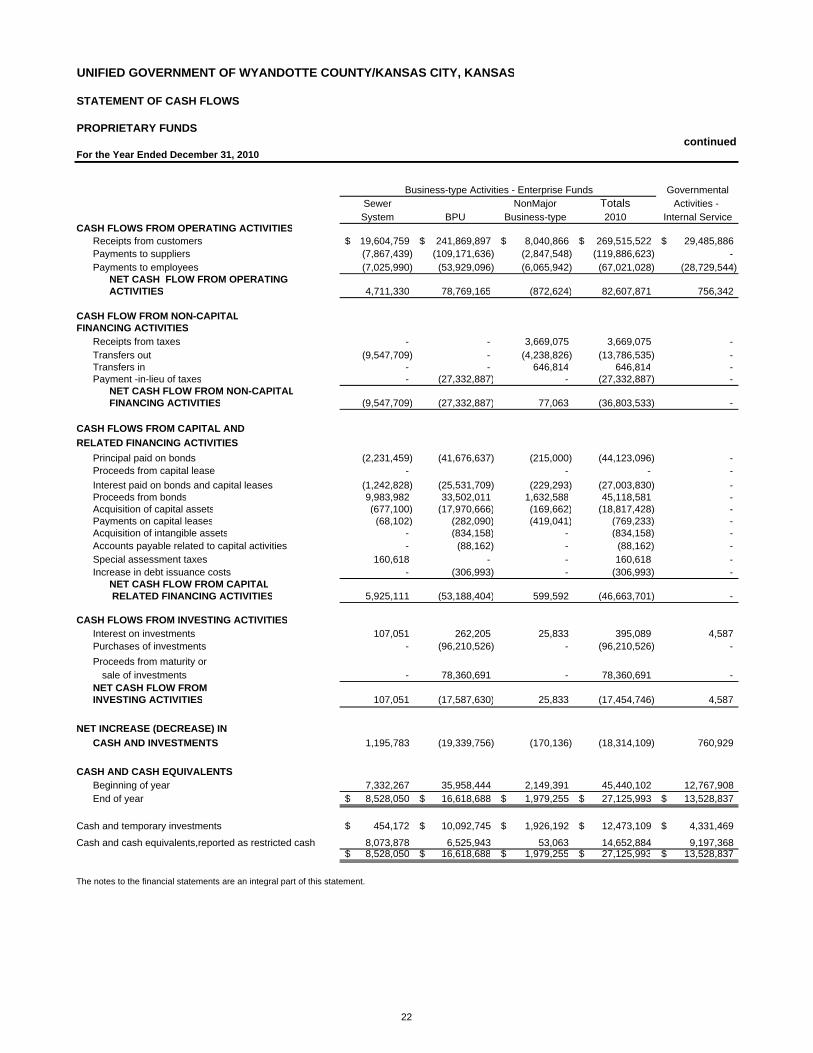

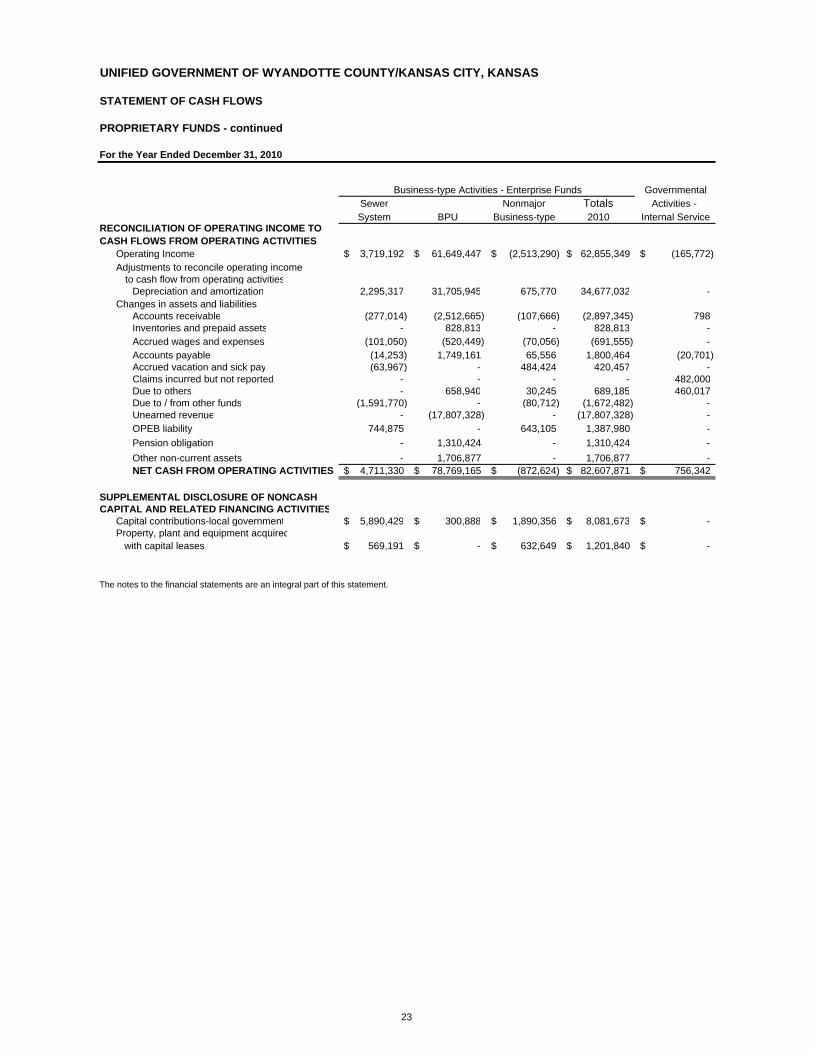

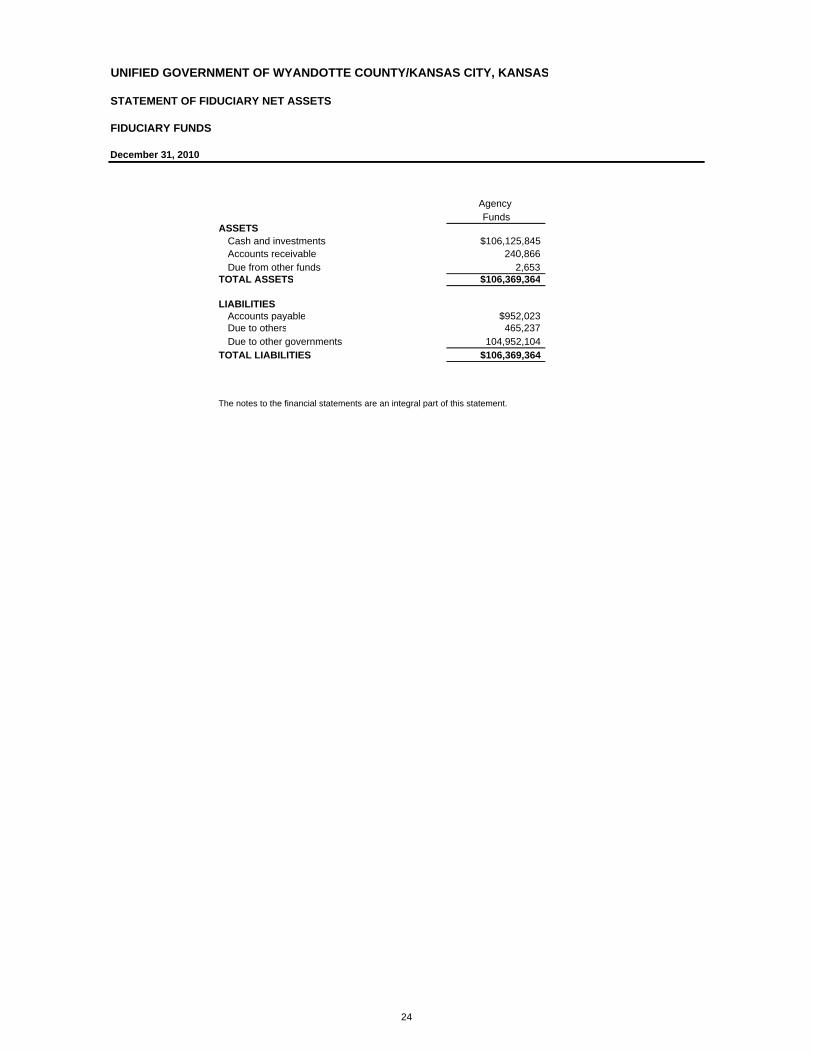

Fund Financial Statements: Balance Sheet – Governmental Funds ----------------------------------------------------------------- 15 Reconciliation of the Balance Sheet – Governmental Funds To the Statement of Net Assets ---------------------------------------------------------------------- 16 Statement of Revenues, Expenditures and Changes in Fund Balances – Governmental Funds -------------------------------------------------------------------- 17 Reconciliation of the Statement of Revenues, Expenditures and Changes to Fund Balances – Governmental Funds to the Statement of Activities --------------------- 18 Statement of Revenues, Expenditures and Changes in Fund Balances Budget and Actual – Budgetary Basis (Non-GAAP) – General Fund ---------------------- 19 Statement of Net Assets – Proprietary Funds --------------------------------------------------------- 20 Statement of Revenues, Expenses and Changes in Fund Net Assets - Proprietary Funds ---------------------------------------------------------------------------------------- 21 Statement of Cash Flows - Proprietary Funds -------------------------------------------------------- 22 Statement of Fiduciary Net Assets ----------------------------------------------------------------------- 24

Notes to the Financial Statements -------------------------------------------------------------------------- 25 Required Supplementary Information -------------------------------------------------------------------------------- 65

Combining Statements and Schedules:

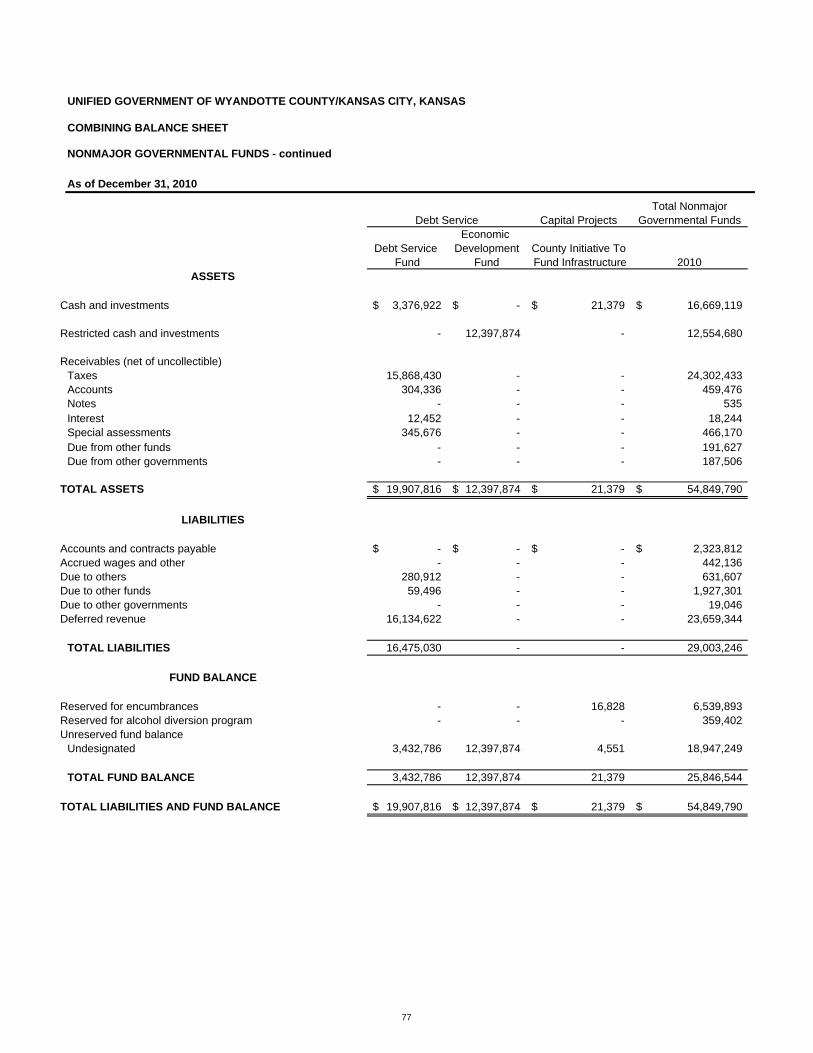

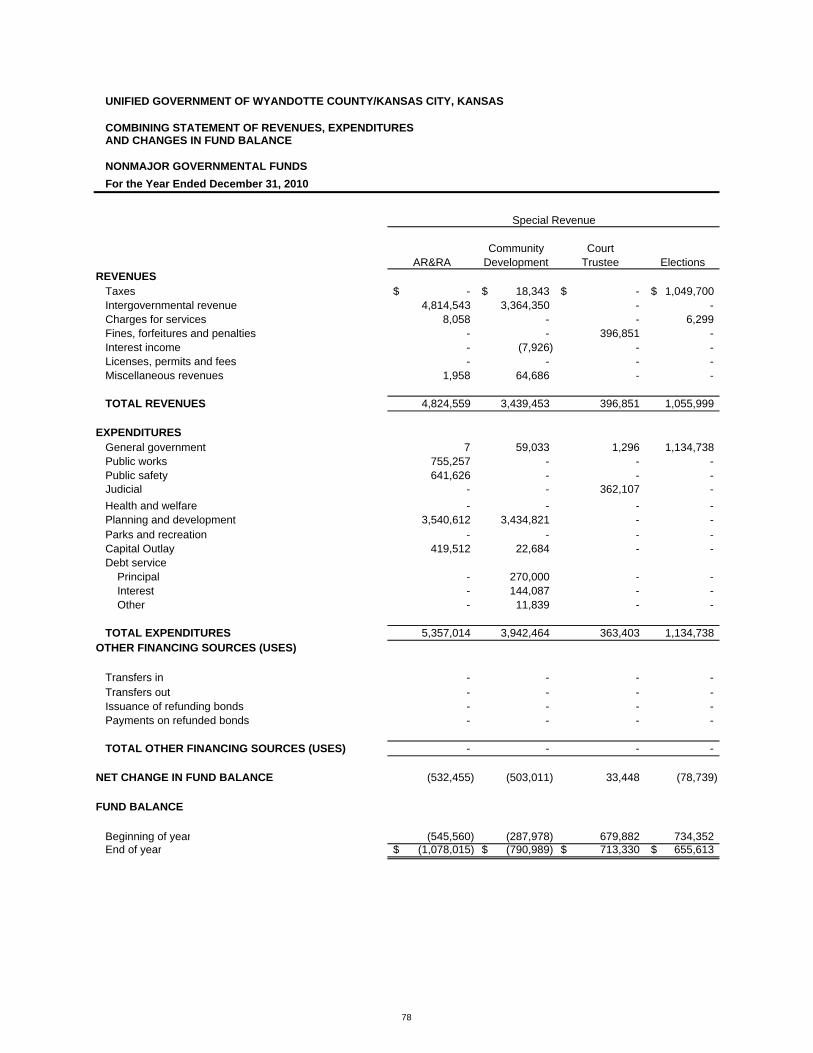

Governmental Funds --------------------------------------------------------------------------------------------- 67 Combining Balance Sheet – NonMajor Governmental Funds ------------------------------------ 72 Combining Statement of Revenues, Expenditures and Changes in Fund Balance – NonMajor Governmental Funds --------------------------------------------- 78 Schedule of Budgetary Accounts - Budget and Actual – Budgetary Basis (Non-GAAP)

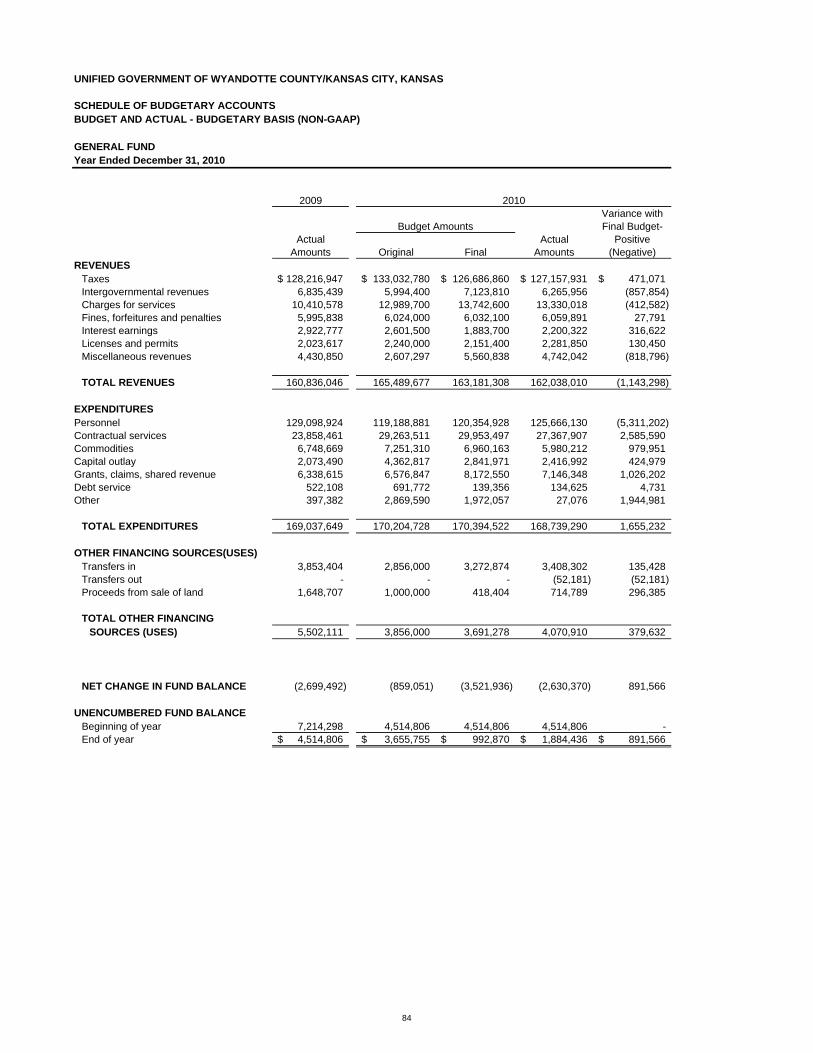

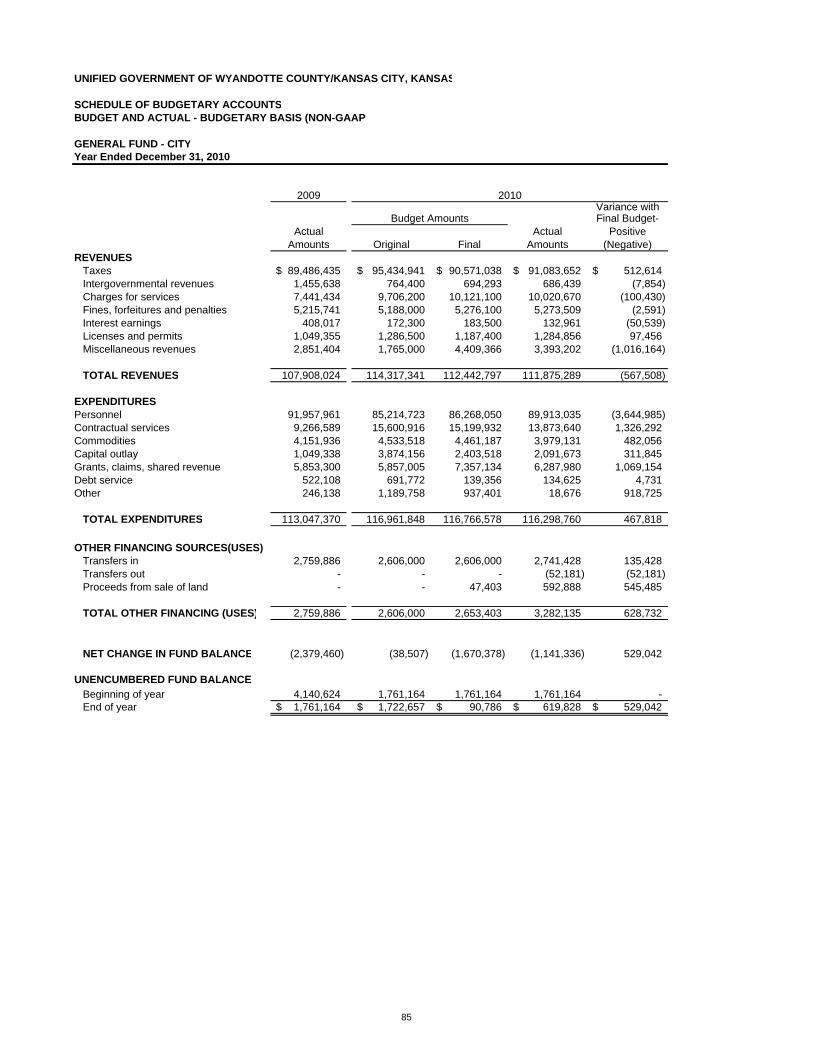

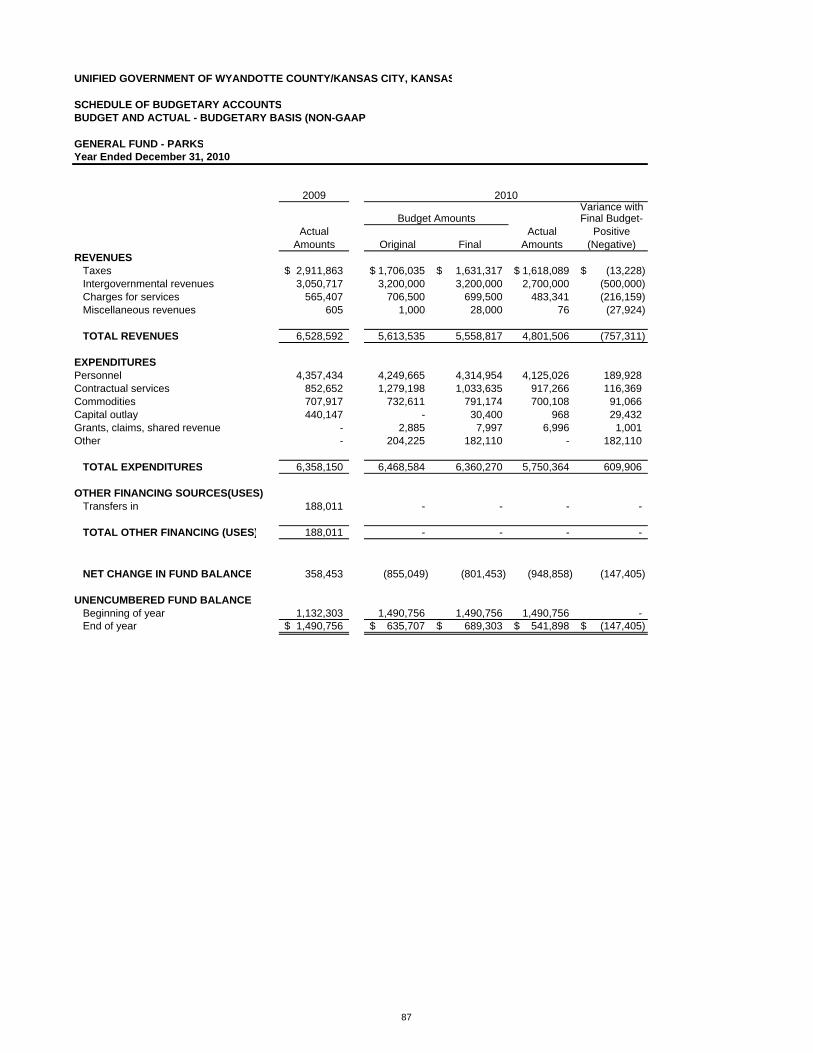

General Fund --------------------------------------------------------------------------------------- 84

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS COMPREHENSIVE ANNUAL FINANCIAL REPORT For the year ended DECEMBER 31, 2010

FINANCIAL SECTION (continued) Governmental Funds (continued):

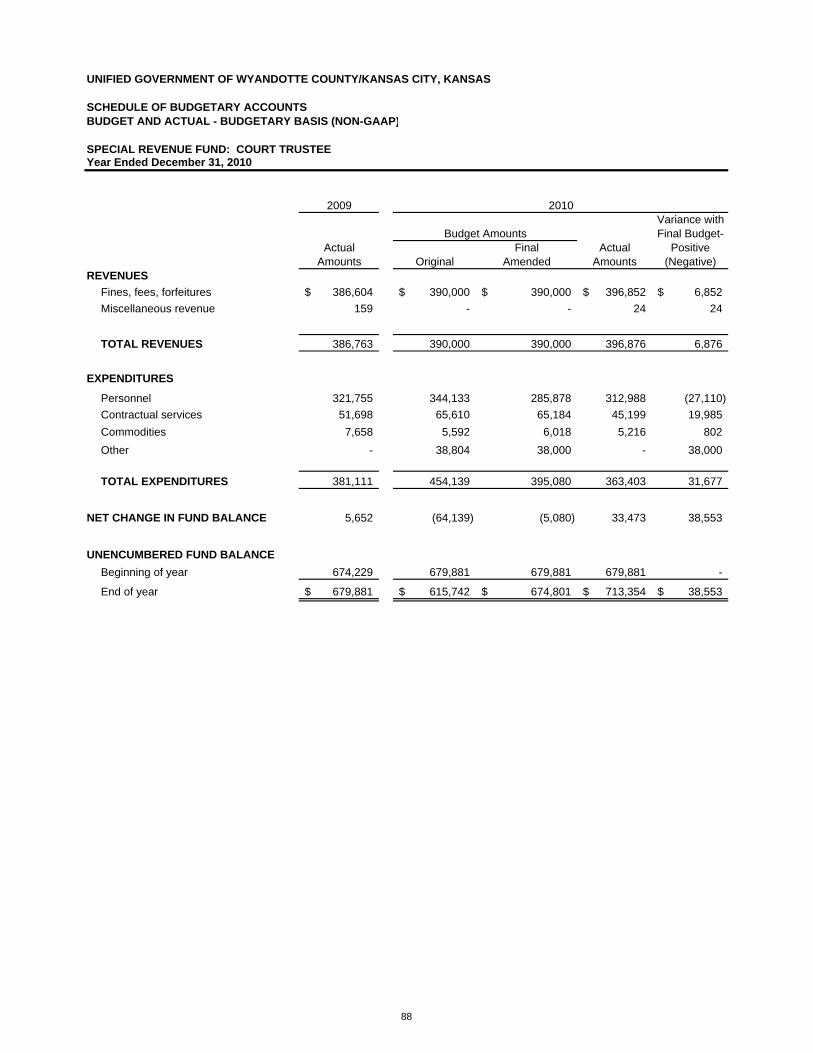

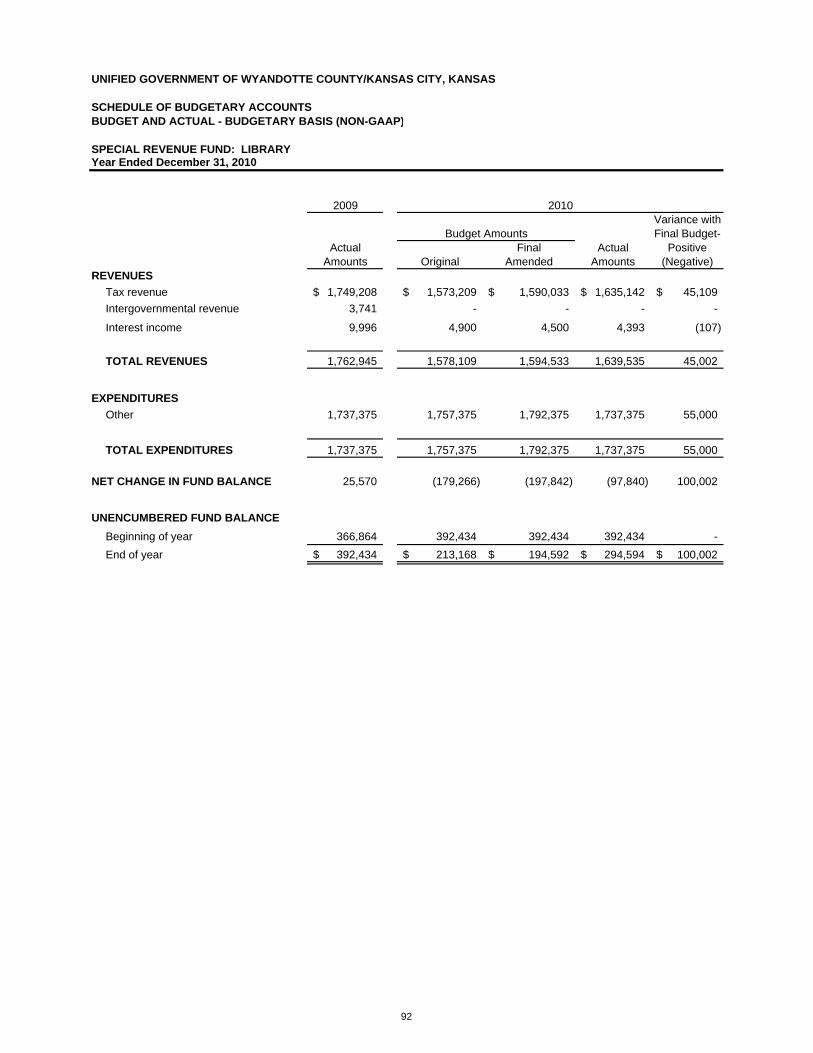

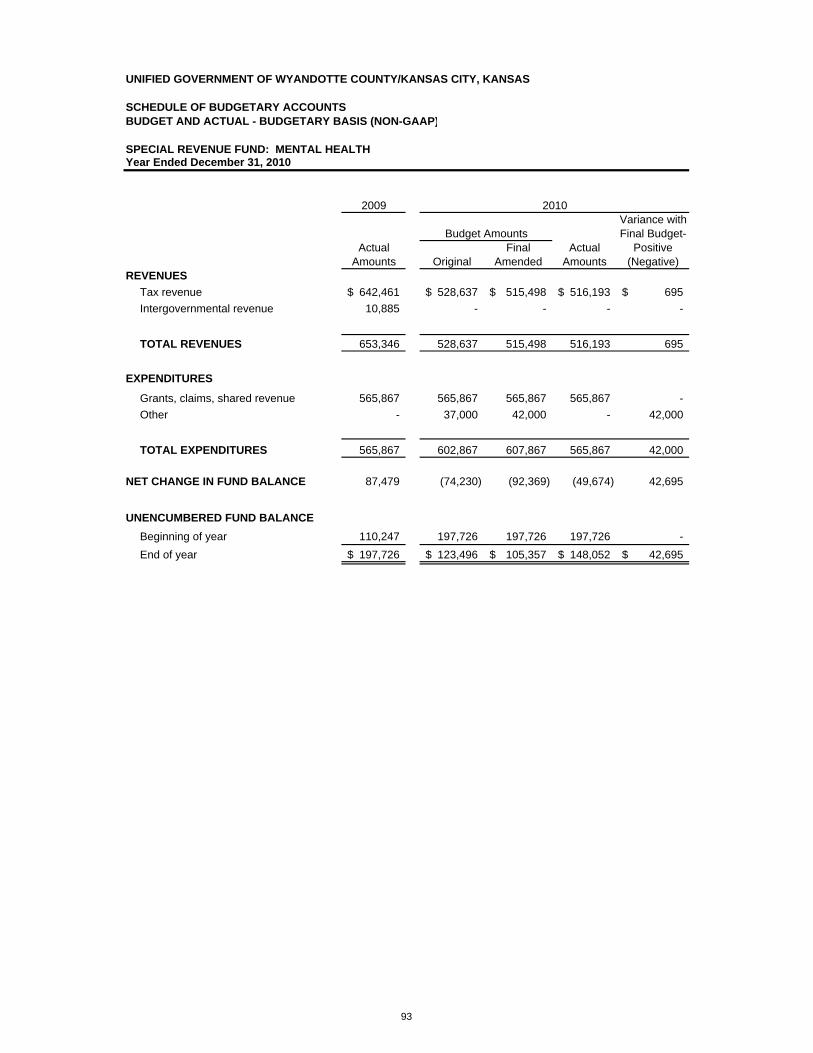

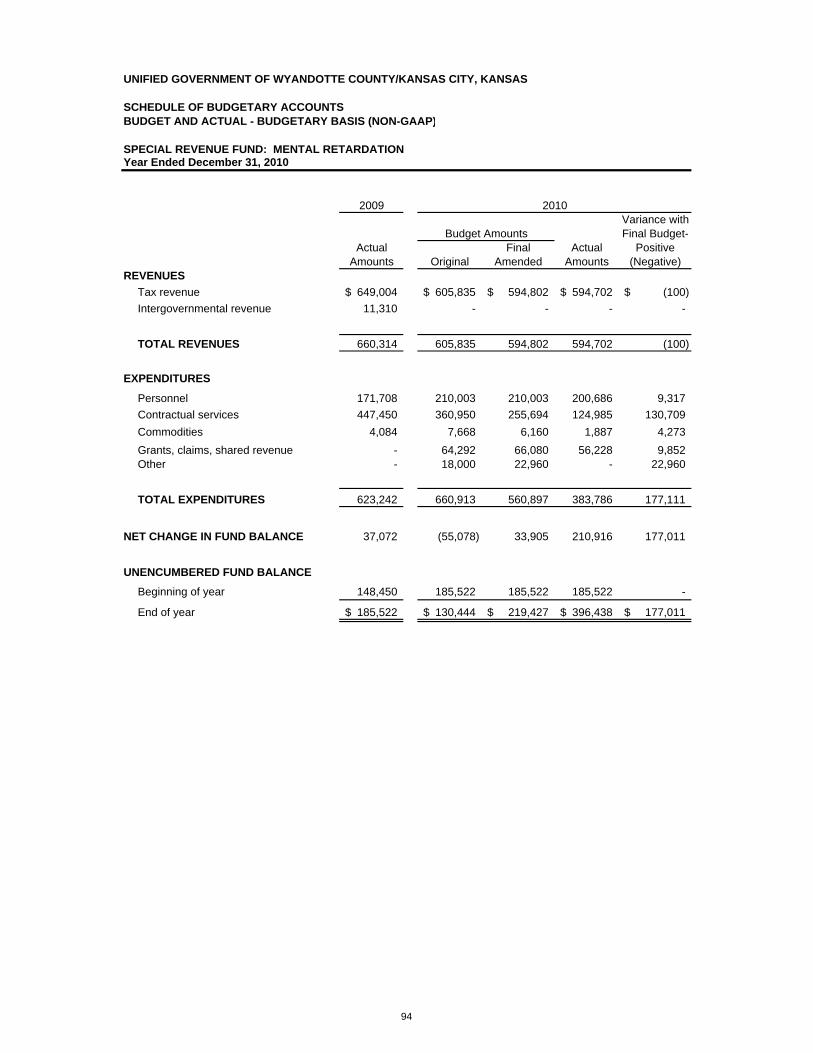

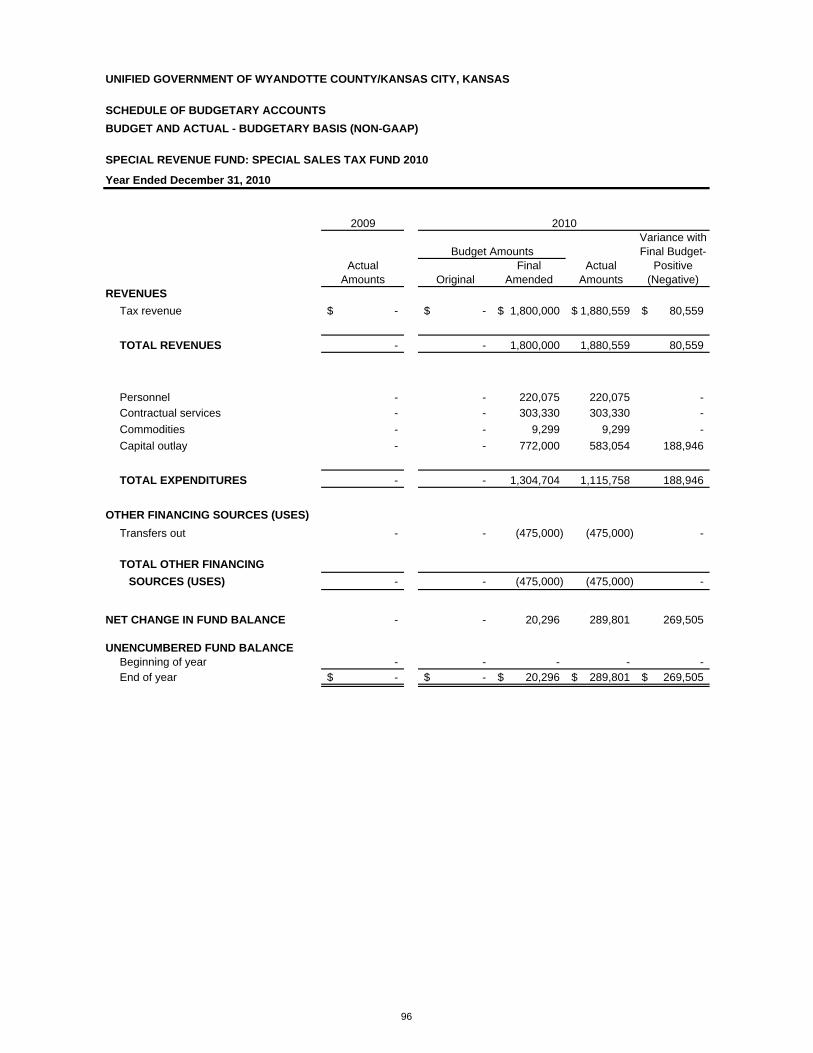

Budgetary Schedules (continued): Special Revenue Funds: Court Trustee ---------------------------------------------------------------------------------- 88 Elections ---------------------------------------------------------------------------------------- 89

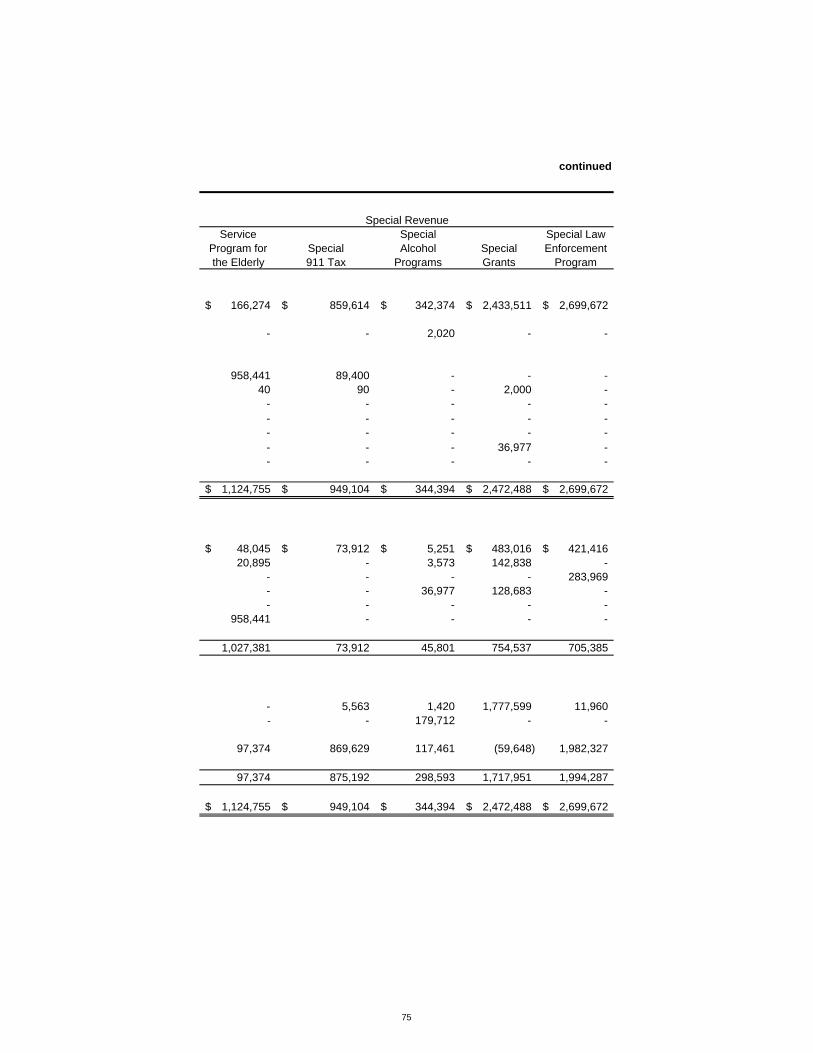

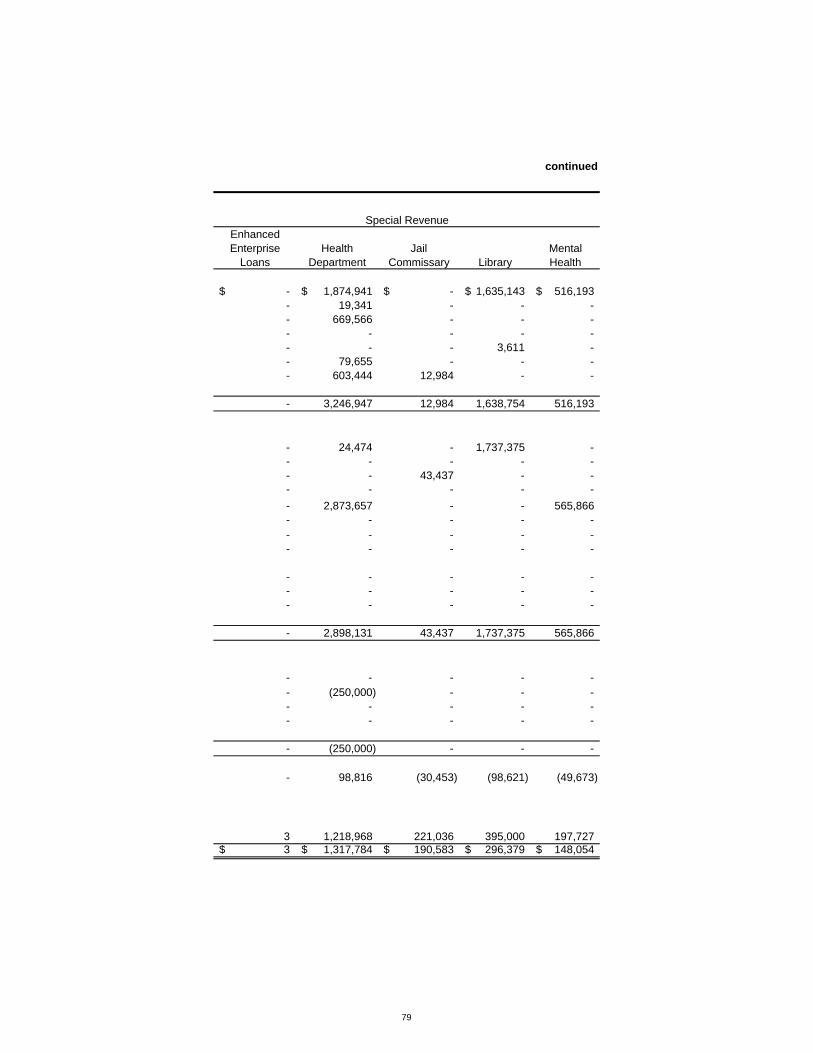

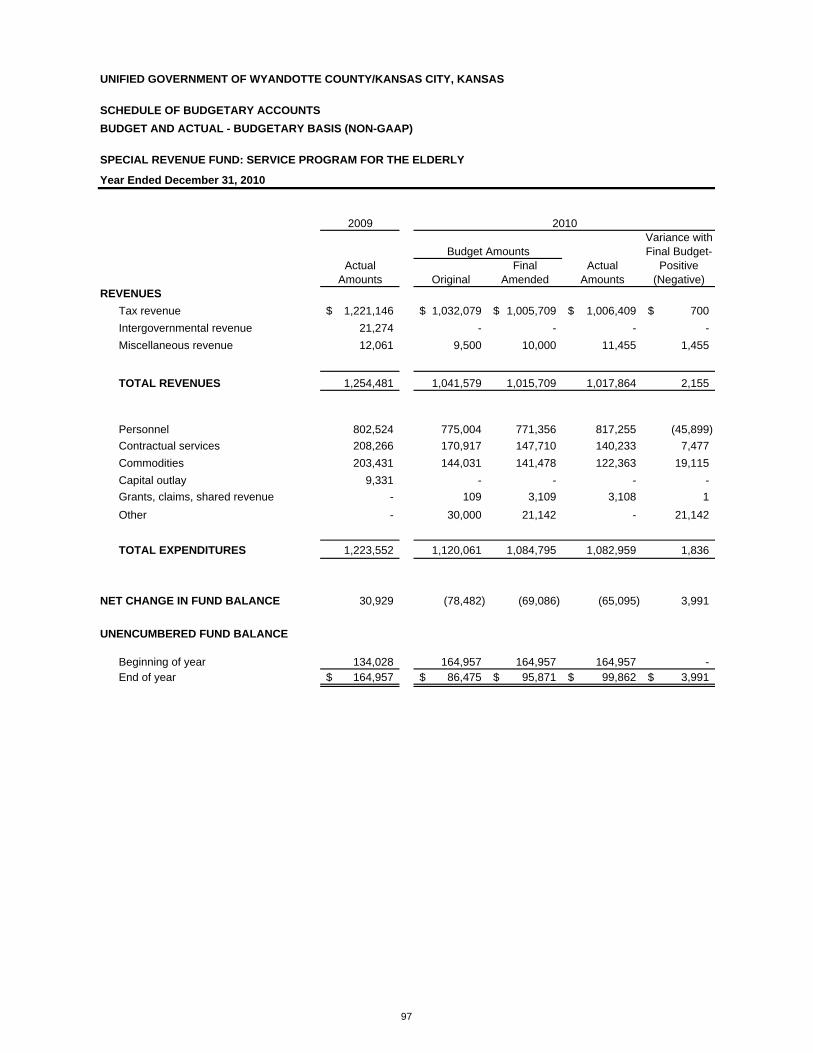

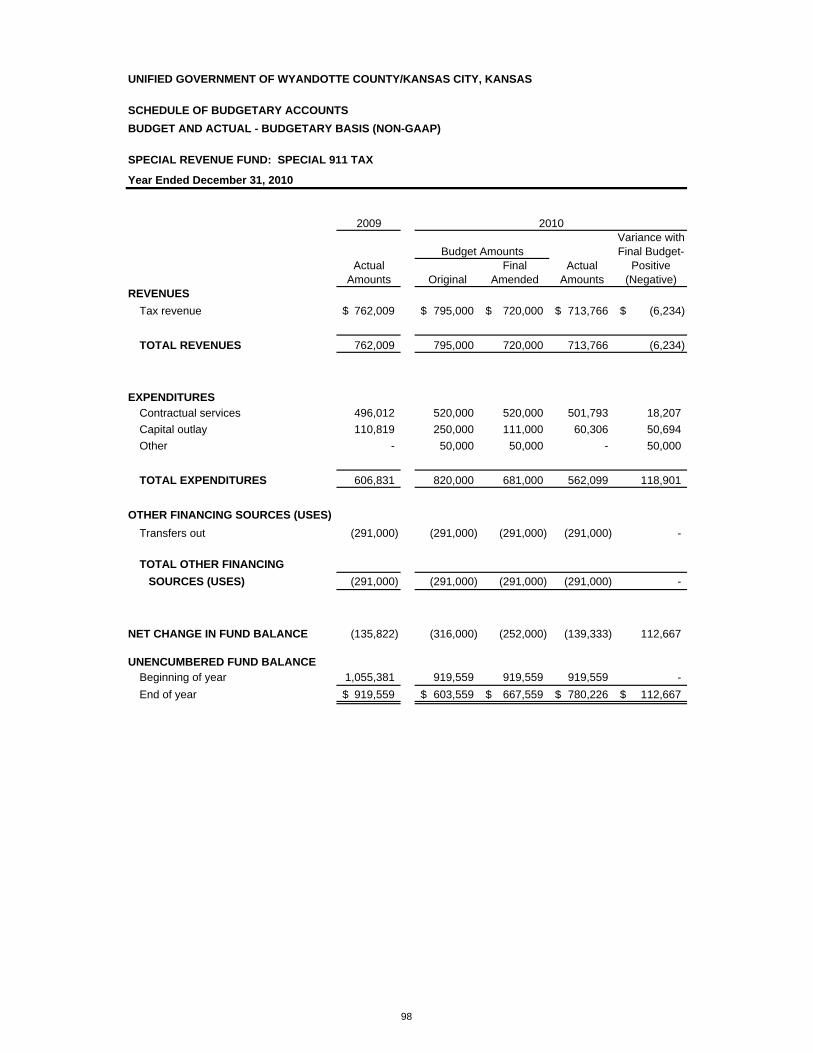

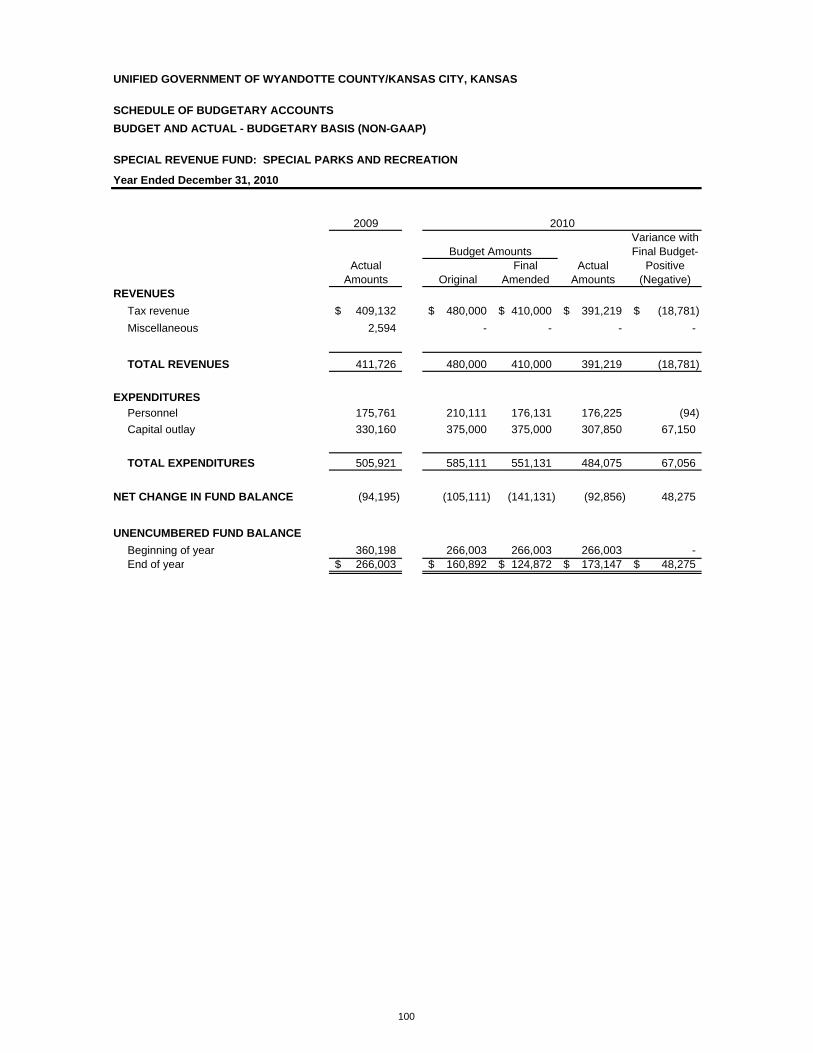

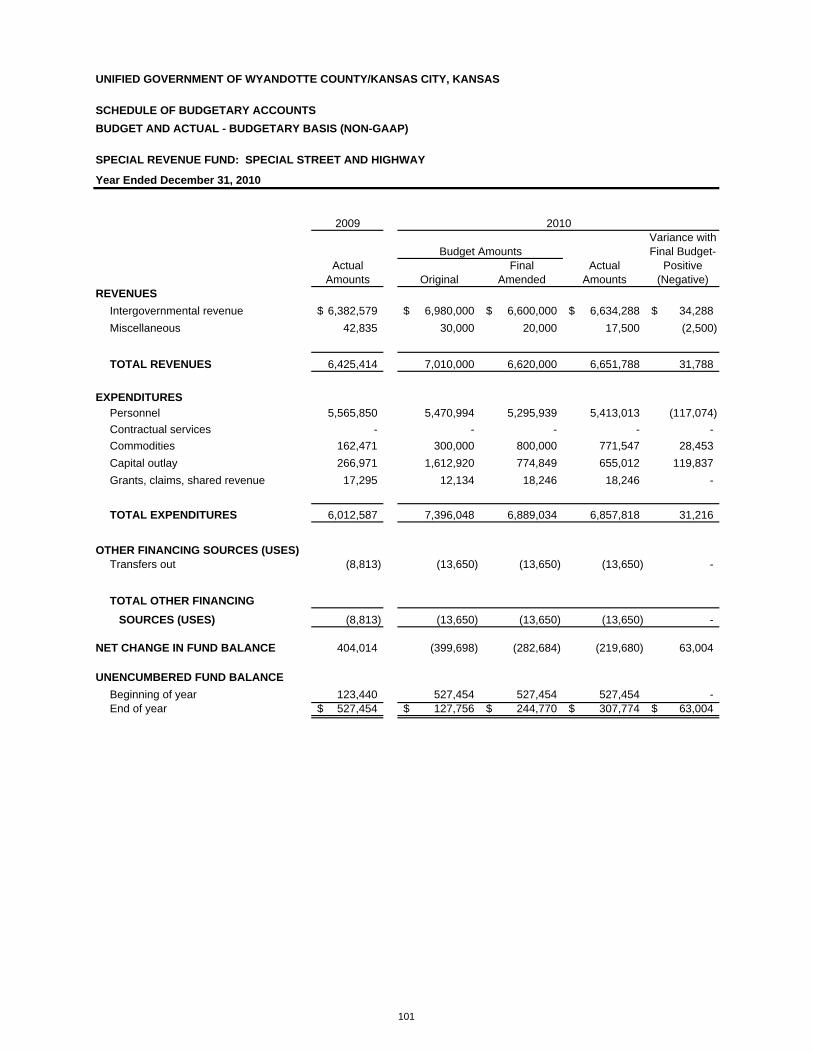

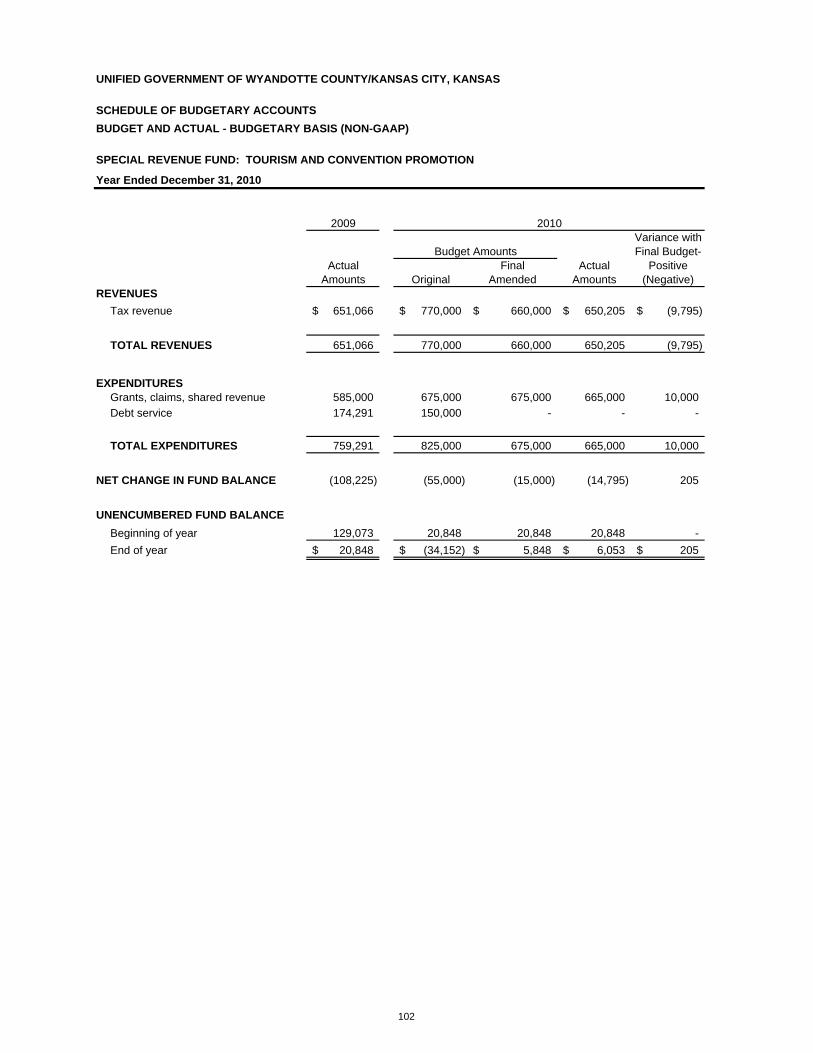

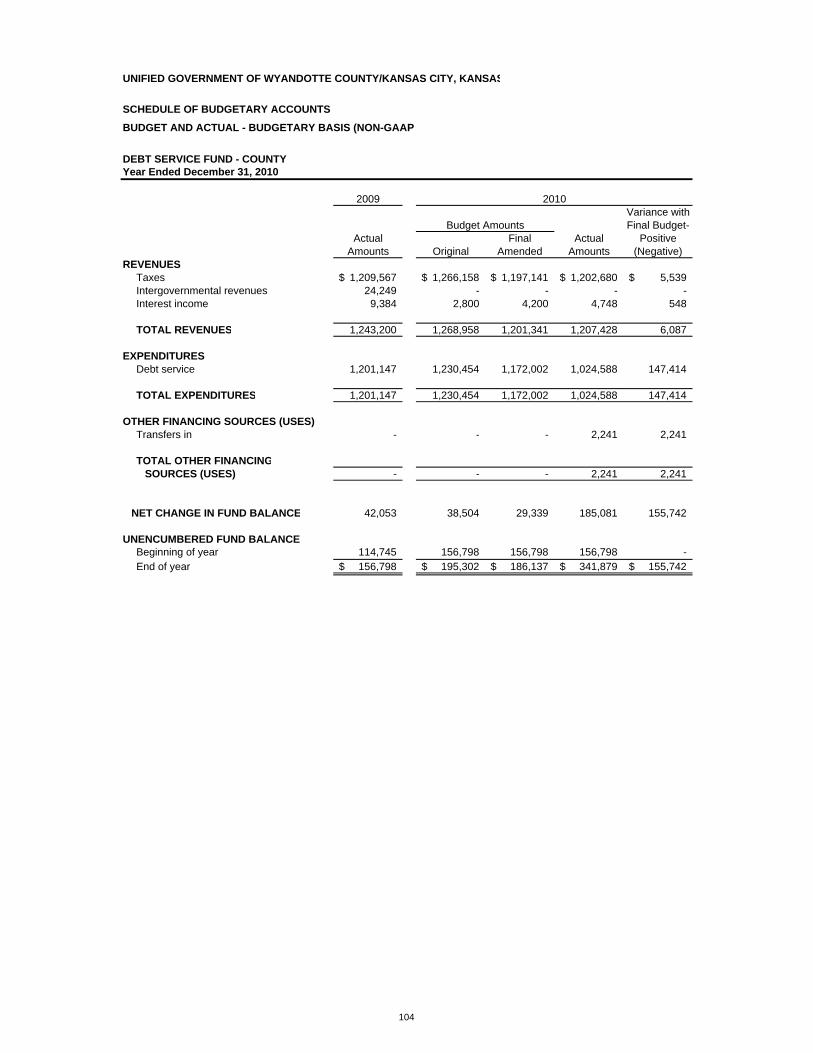

Health Department --------------------------------------------------------------------------- 90 Jail Commissary ------------------------------------------------------------------------------ 91 Library ------------------------------------------------------------------------------------------- 92 Mental Health ---------------------------------------------------------------------------------- 93 Mental Retardation --------------------------------------------------------------------------- 94 Register of Deeds Technology Fund ---------------------------------------------------- 95 Special Sales Tax ---------------------------------------------------------------------------- 96 Service Program for the Elderly ----------------------------------------------------------- 97 Special 911 Tax ------------------------------------------------------------------------------- 98 Special Alcohol and Drug Programs ----------------------------------------------------- 99 Special Parks and Recreation ----------------------------------------------------------- 100 Special Street and Highway ------------------------------------------------------------- 101 Tourism and Convention Promotion --------------------------------------------------- 102 Debt Service Funds: City --------------------------------------------------------------------------------------------- 103 County ----------------------------------------------------------------------------------------- 104

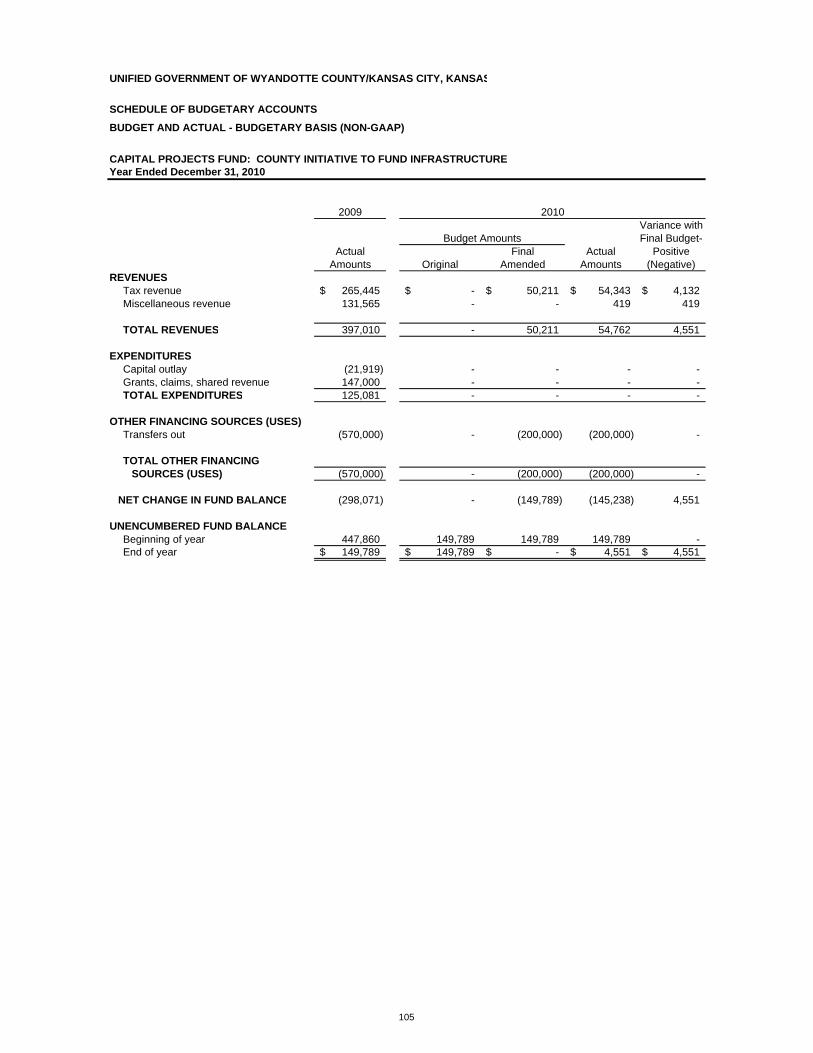

Capital Project Fund: County Initiative to Fund Infrastructure ----------------------------------------------- 105

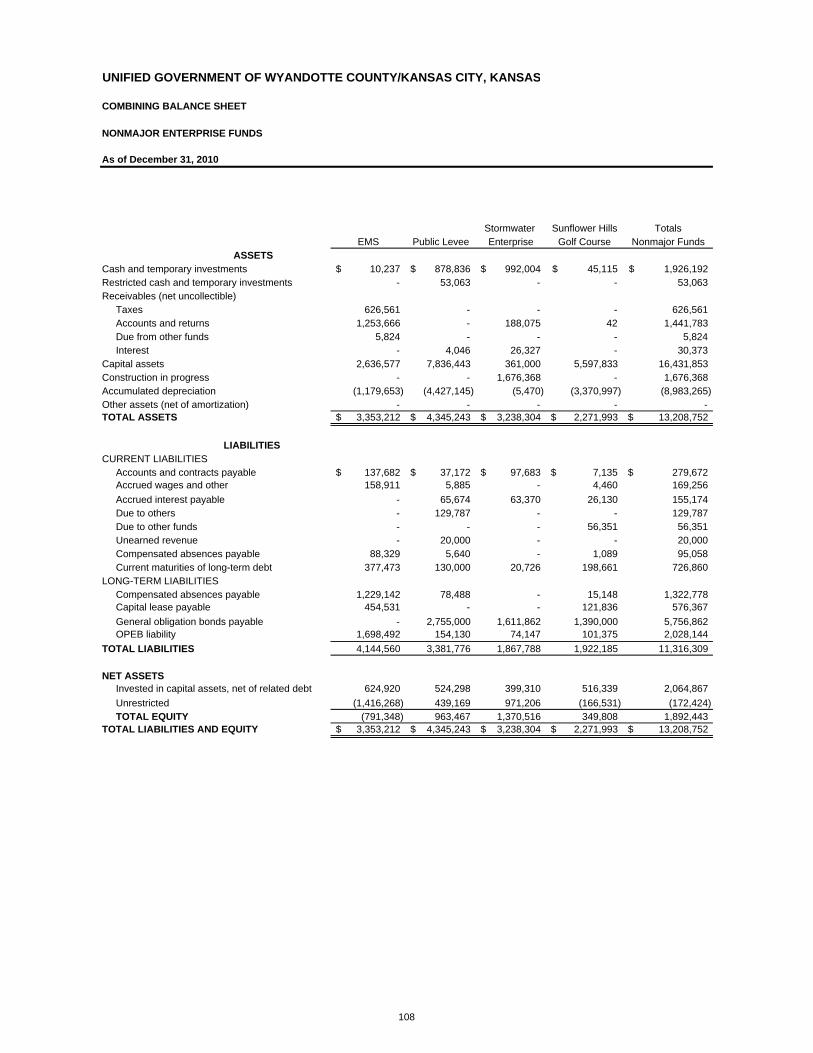

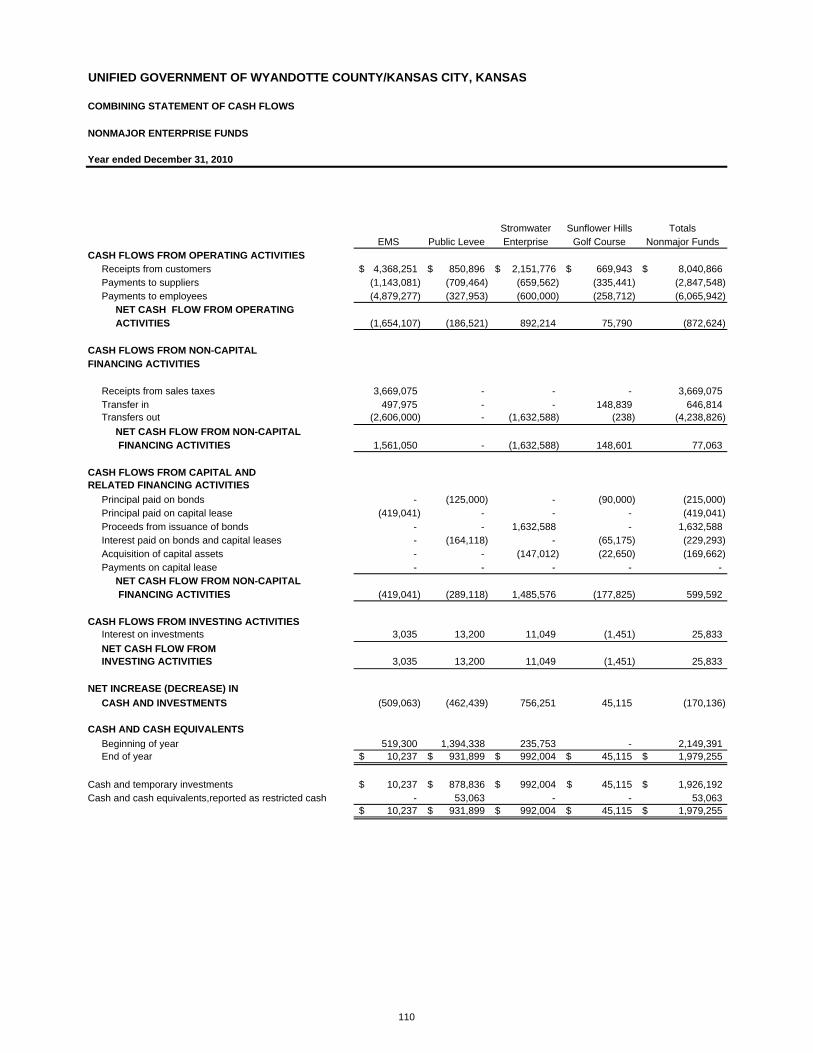

Enterprise Funds ------------------------------------------------------------------------------------------------ 107 Combining Balance Sheet – NonMajor Enterprise Funds ---------------------------------------- 108 Combining Statement of Revenues, Expenses and Changes in Fund Net Assets – NonMajor Enterprise Funds -------------------------------------------- 109 Combining Statement of Cash Flows – NonMajor Enterprise Funds -------------------------- 110 Schedule of Budgetary Accounts - Budget and Actual – Budgetary Basis (Non-GAAP)

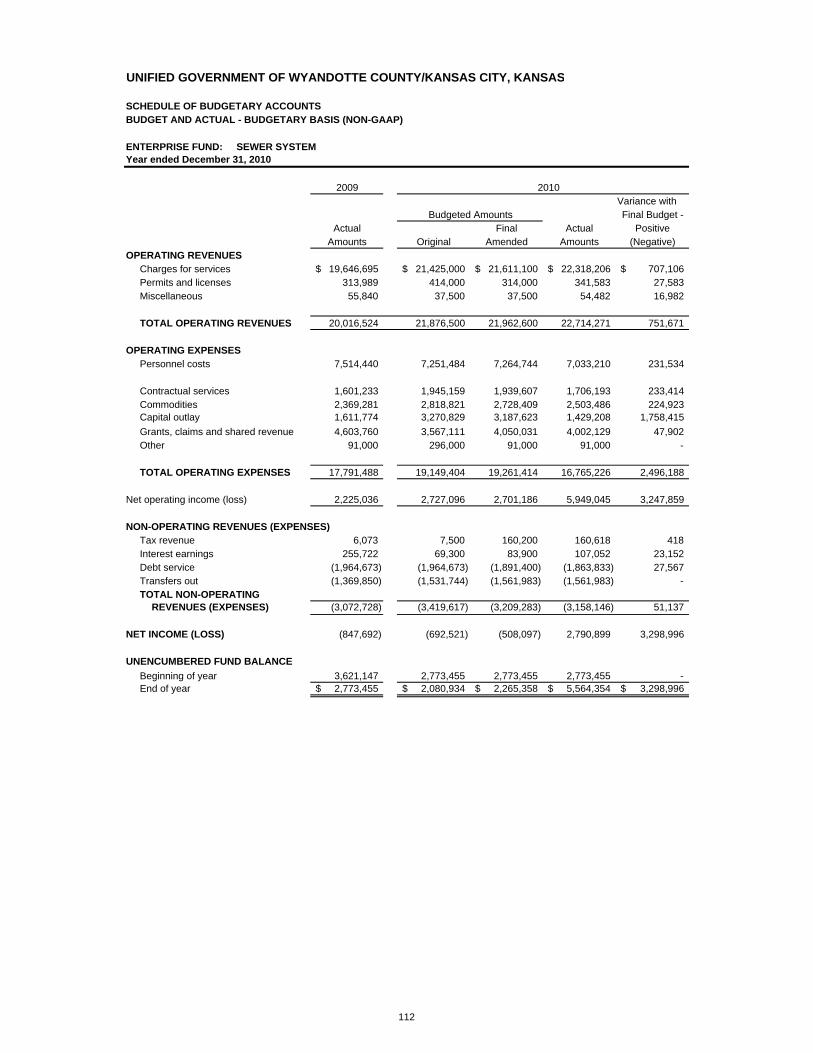

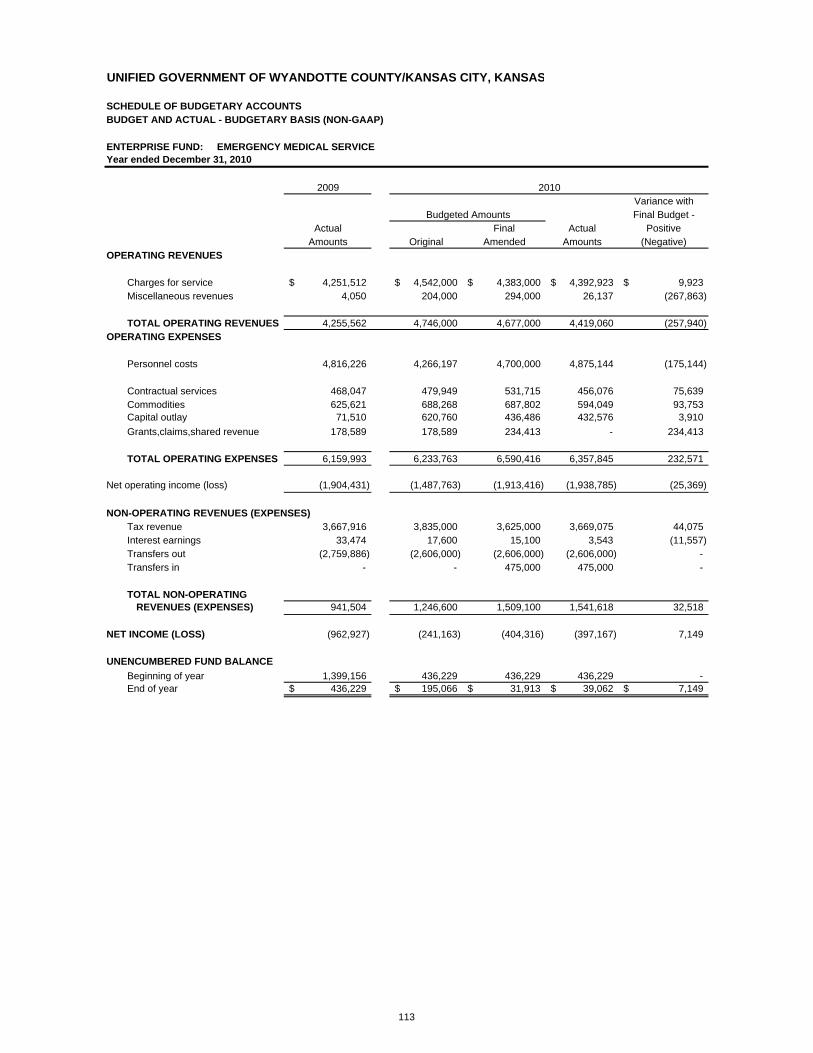

Sewer System ------------------------------------------------------------------------------------ 112 Emergency Medical Service ------------------------------------------------------------------ 113 Public Levee -------------------------------------------------------------------------------------- 114

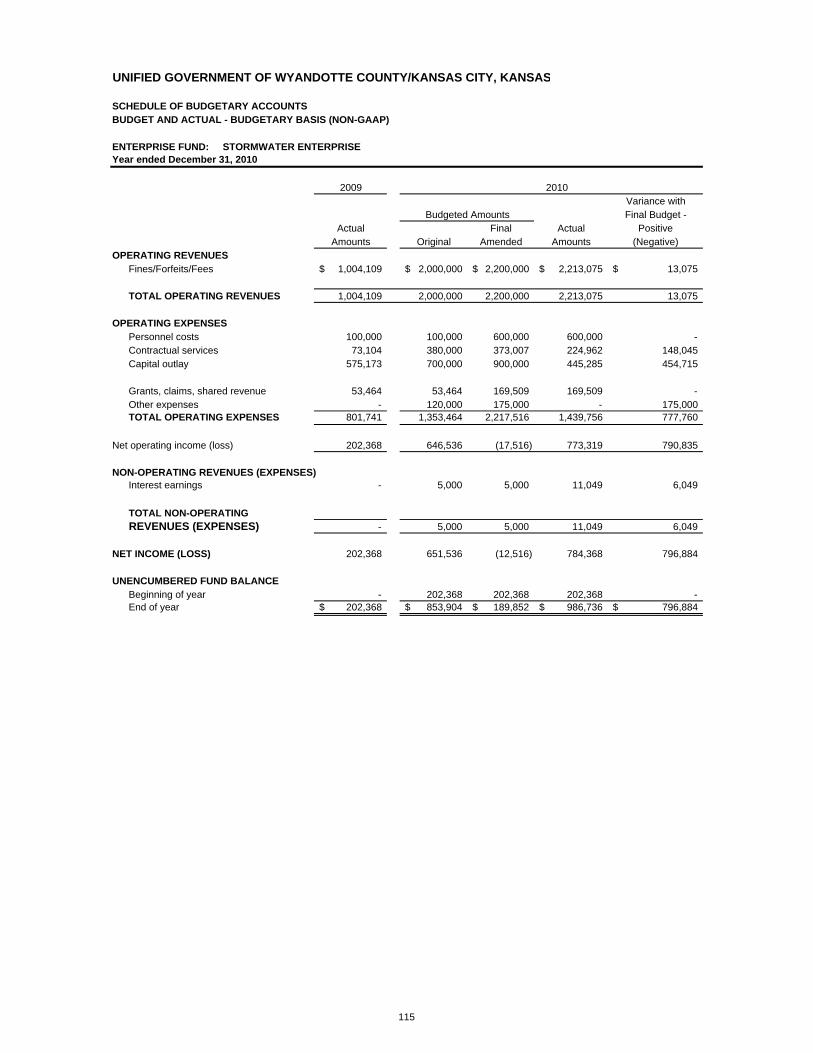

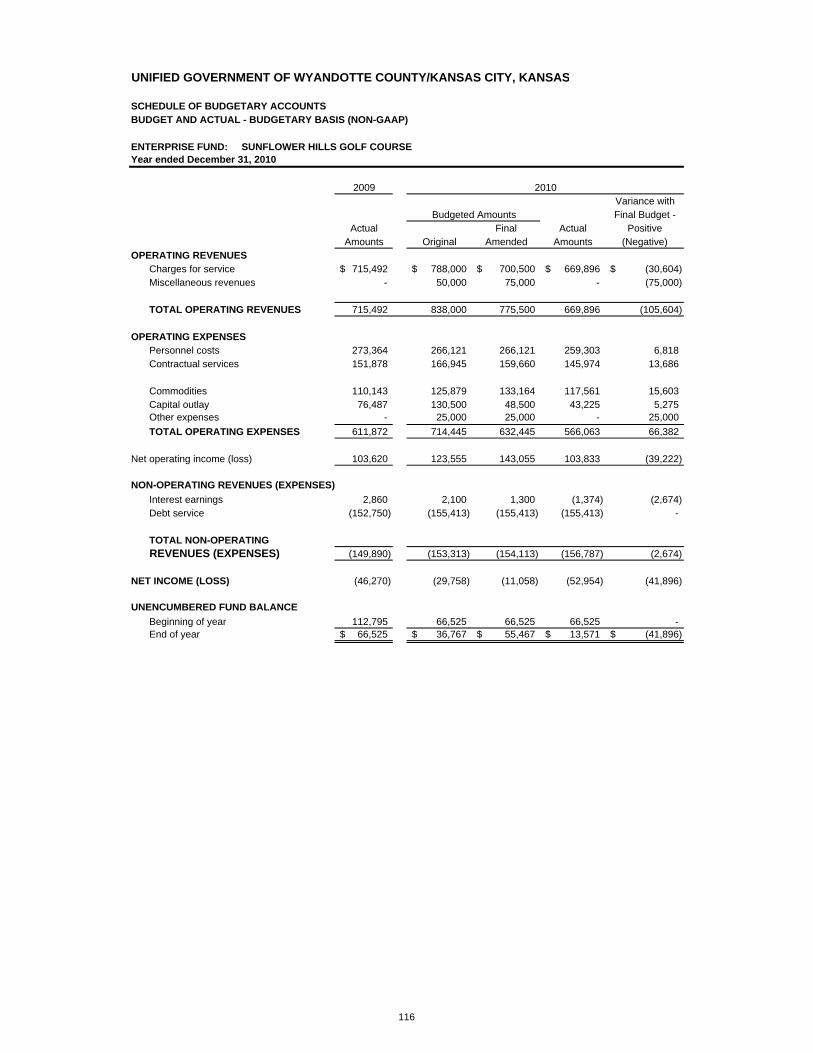

Stormwater Utility Enterprise----------------------------------------------------------------- 115 Sunflower Hills Golf Course ------------------------------------------------------------------- 116

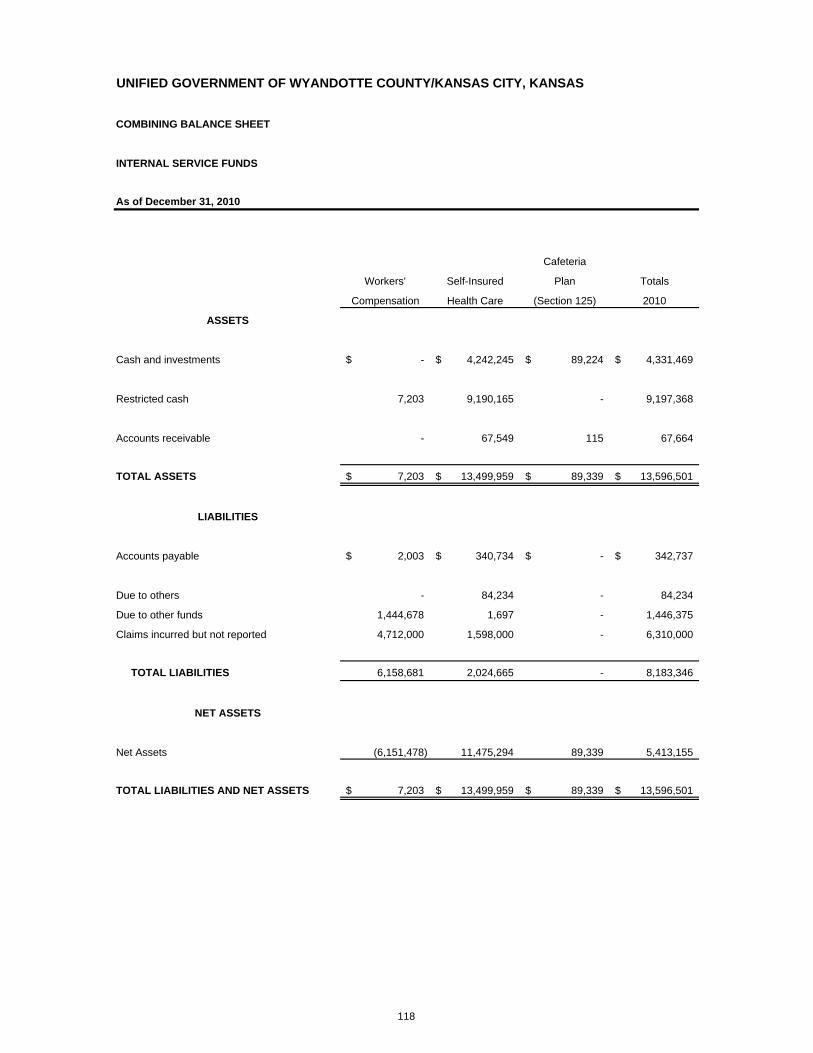

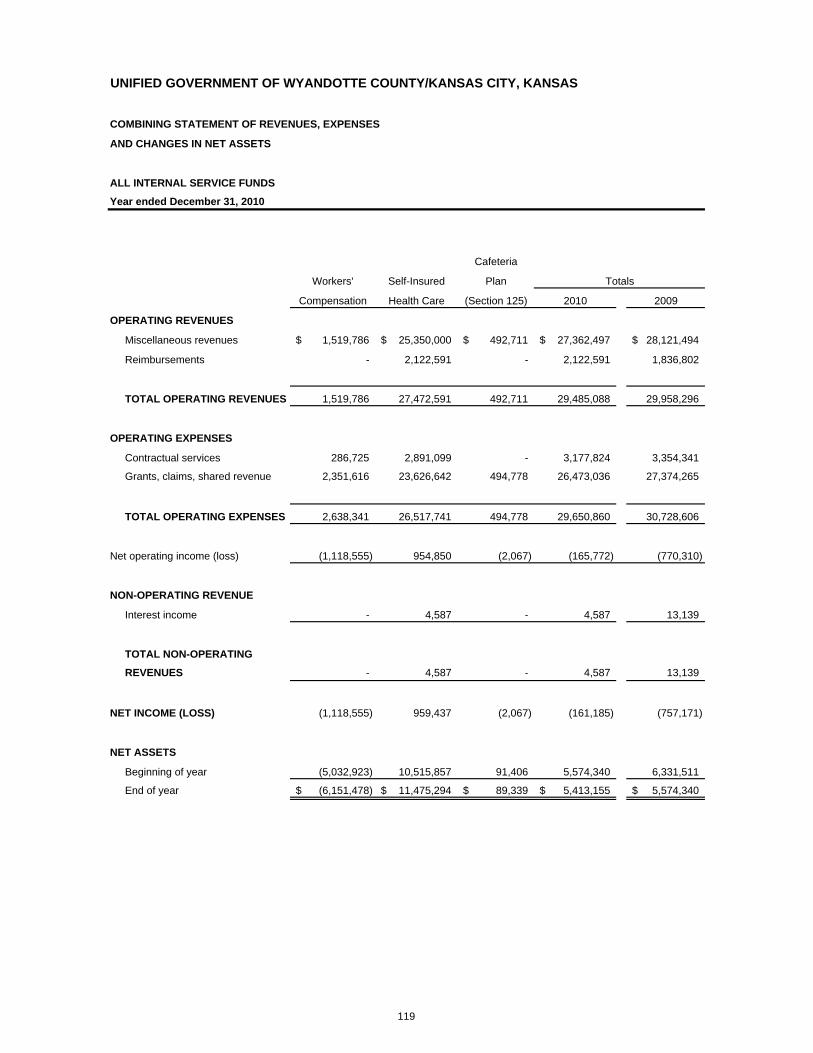

Internal Service Funds ---------------------------------------------------------------------------------------- 117 Combining Balance Sheet -------------------------------------------------------------------------------- 118 Combining Statement of Revenues, Expenses and Changes in Net Assets ---------------- 119

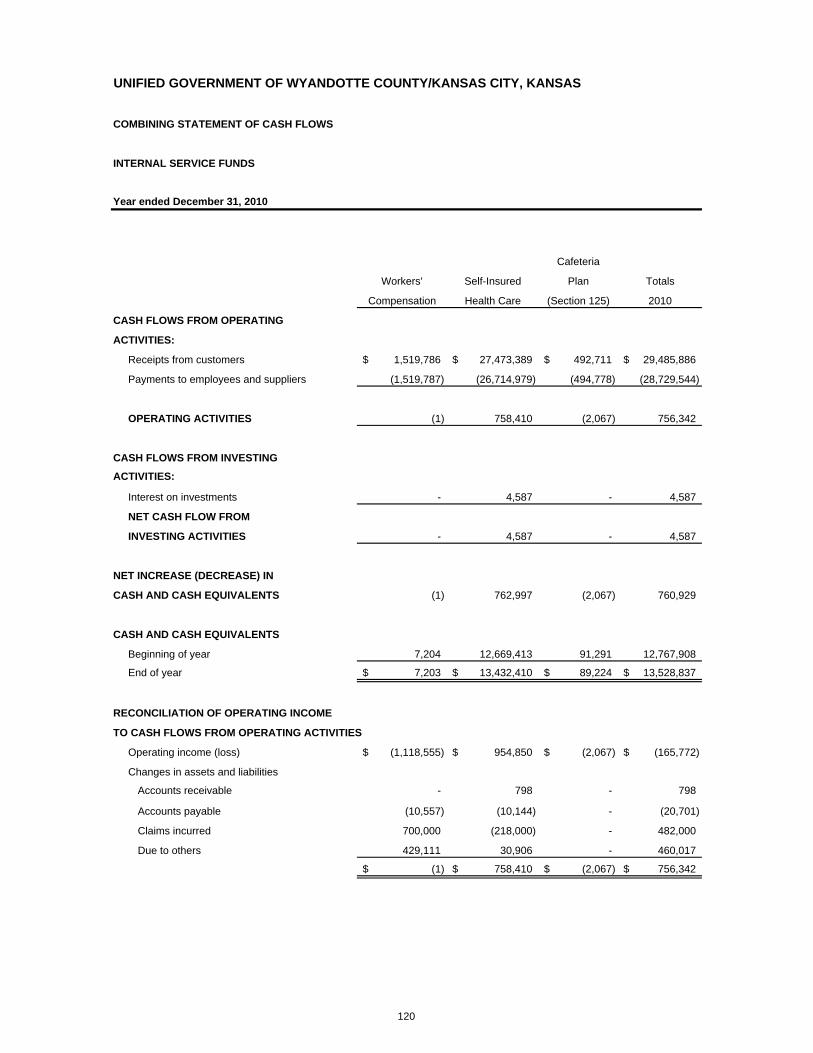

Combining Statement of Cash Flows----------------------------------------------------------------- 120

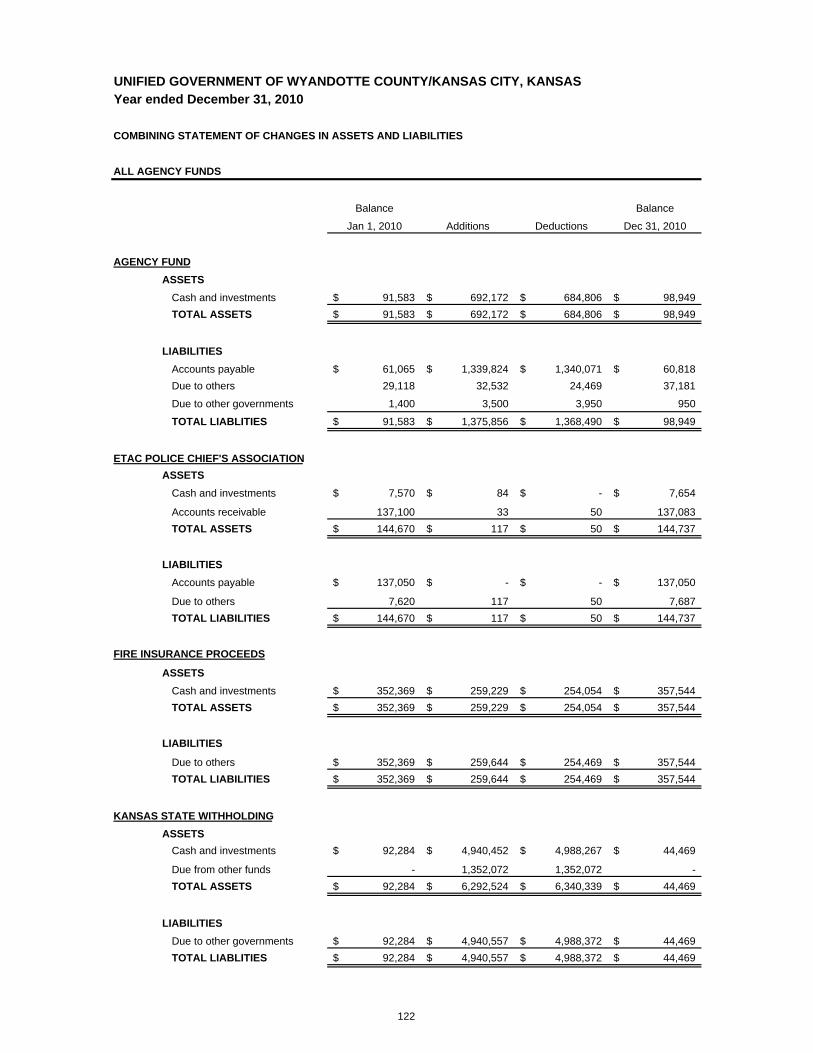

Agency Funds ---------------------------------------------------------------------------------------------------- 121 Combining Statement of Changes in Assets and Liabilities – All Agency Funds ----------- 122

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS COMPREHENSIVE ANNUAL FINANCIAL REPORT For the year ended DECEMBER 31, 2010

STATISTICAL SECTION -------------------------------------------------------------------------------------------------- 125

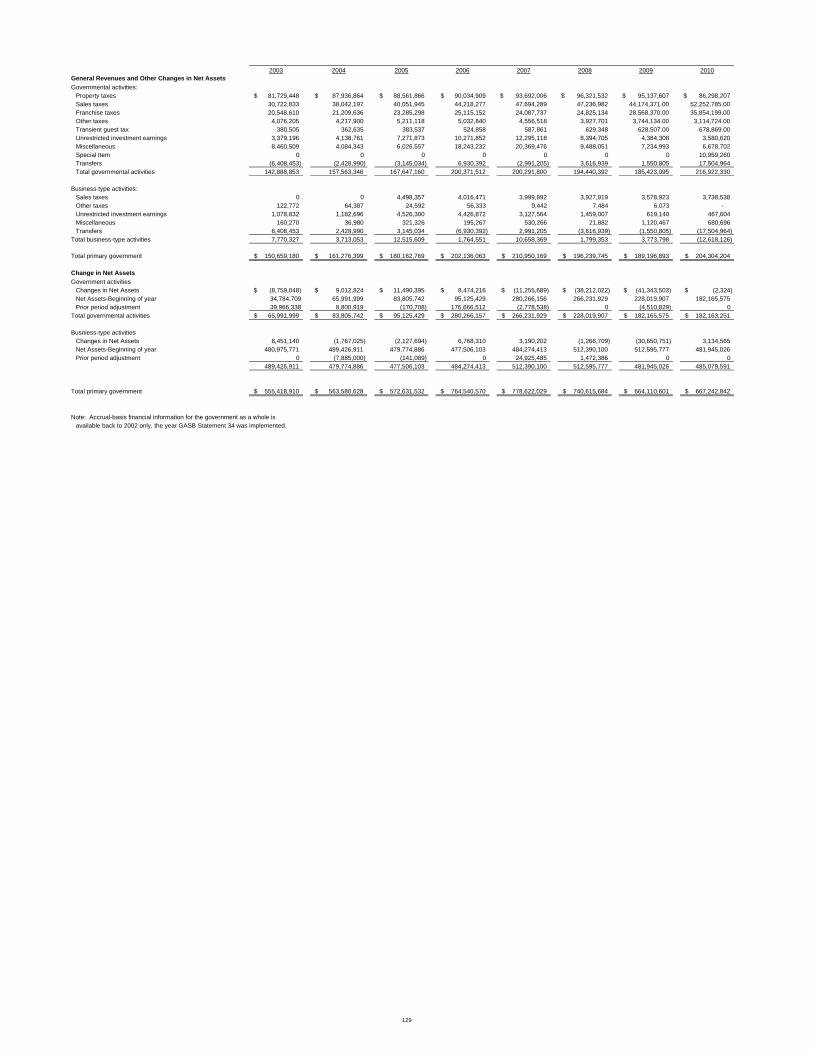

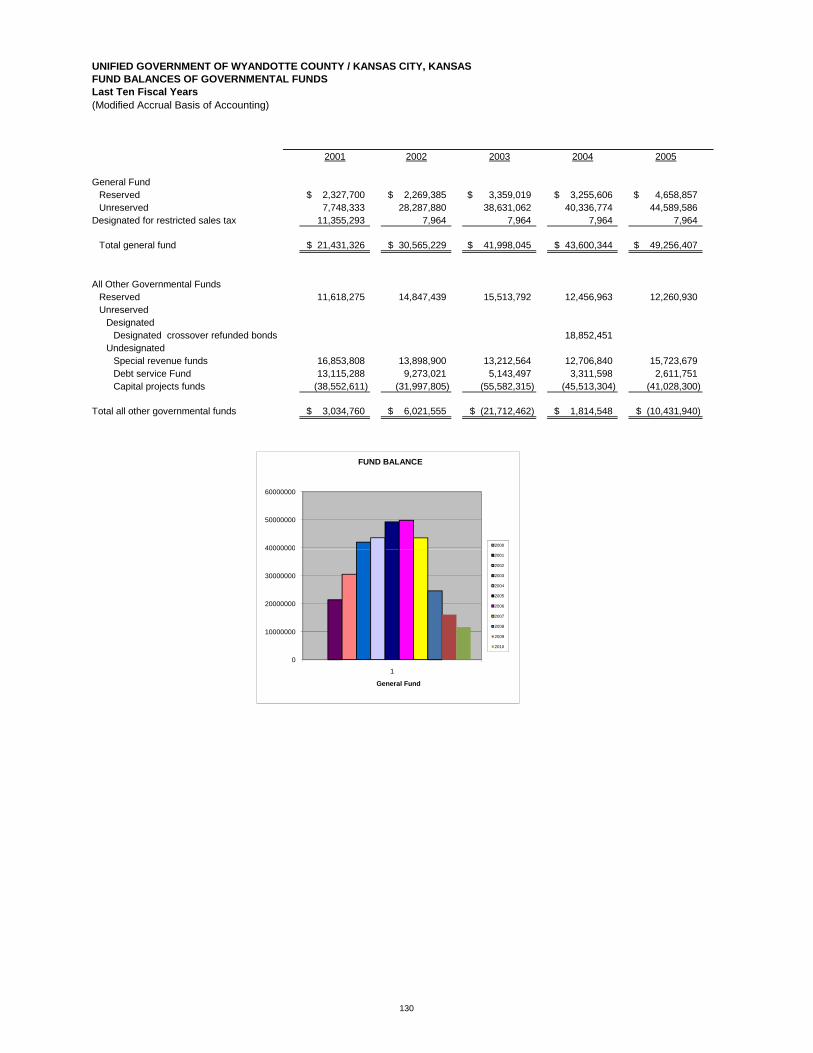

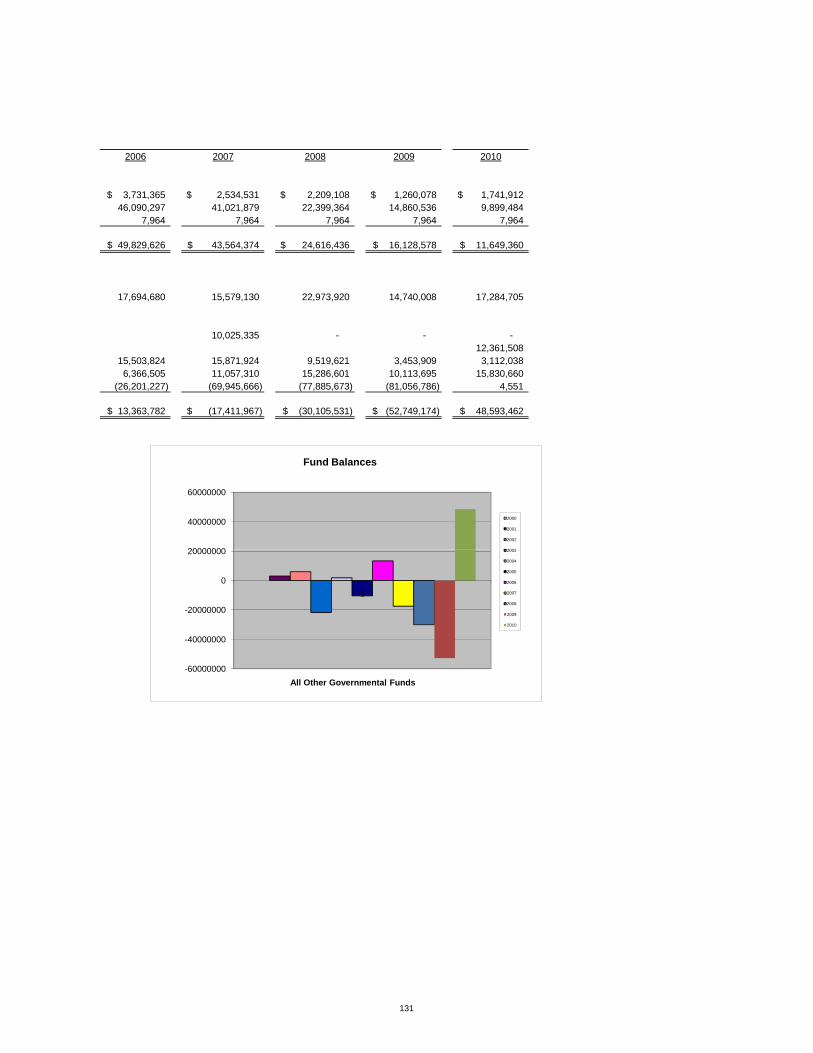

Financial Trends ------------------------------------------------------------------------------------------------------- 126 Net Assets by Component – Last Seven Fiscal Years -------------------------------------------- 126 Changes in Fund Balances of Governmental Funds - Last Ten Fiscal Years -------------- 127 Changes in Net Assets - Last Seven Fiscal Years ------------------------------------------------ 128 Fund Balances of Governmental Funds - Last Ten Fiscal Years ------------------------------ 130

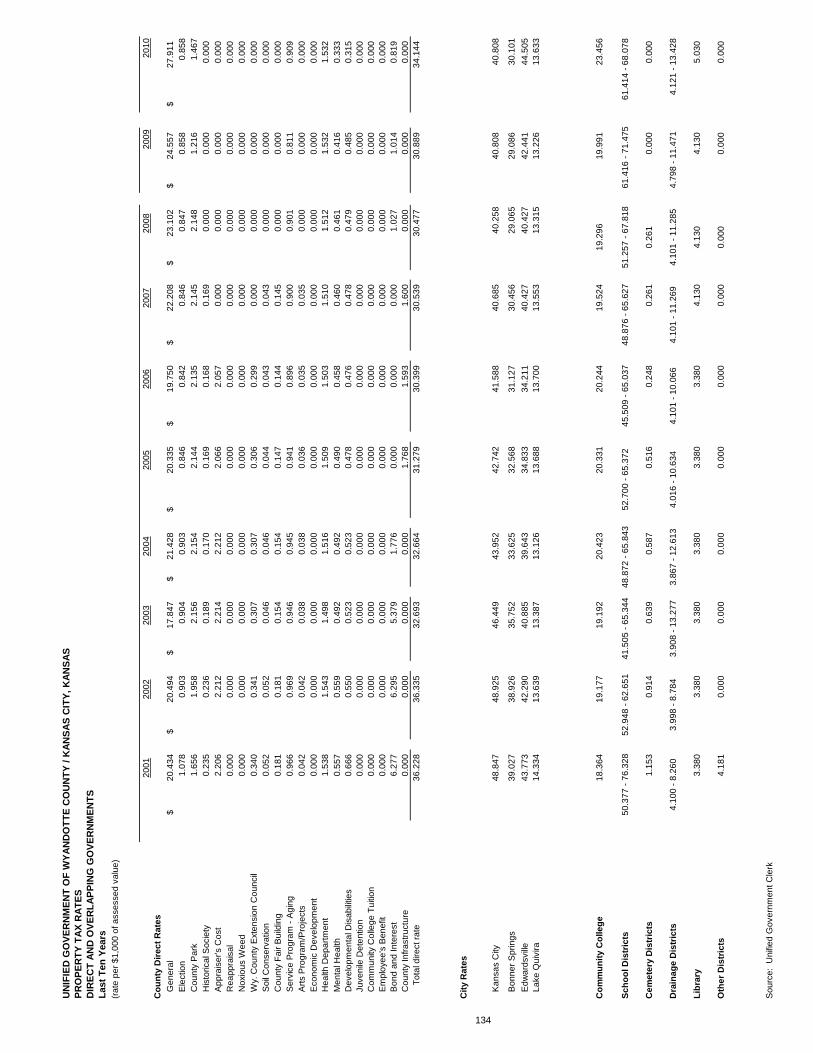

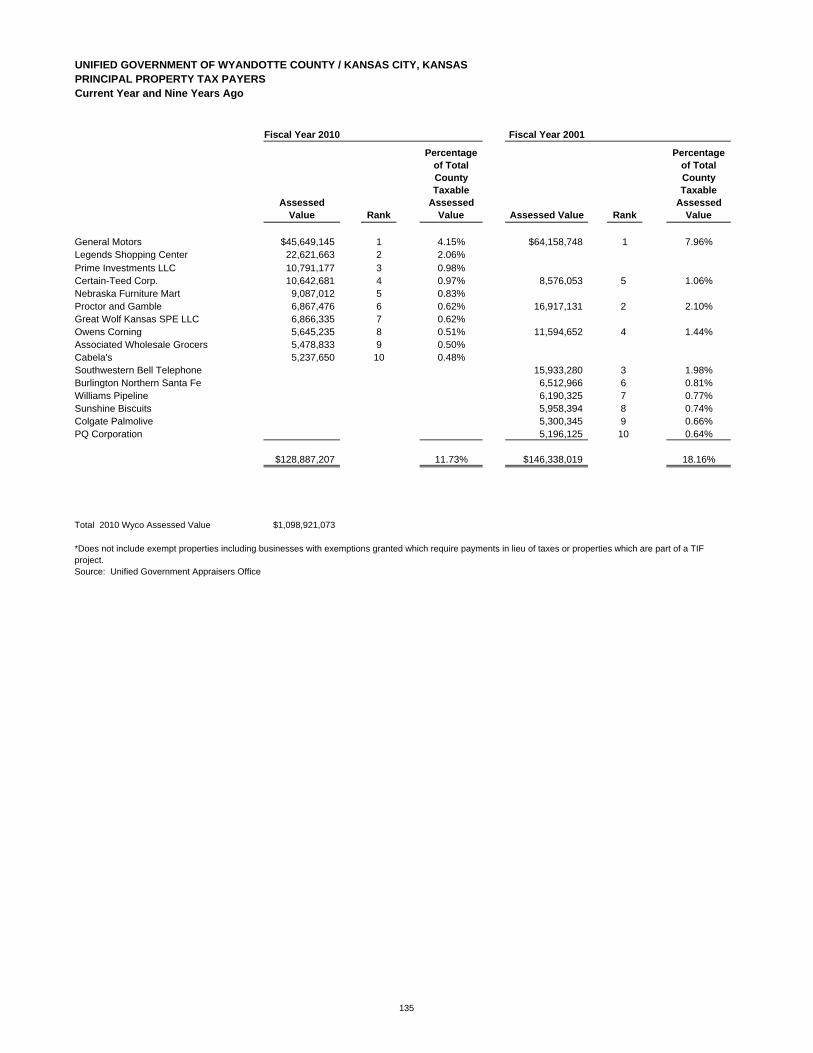

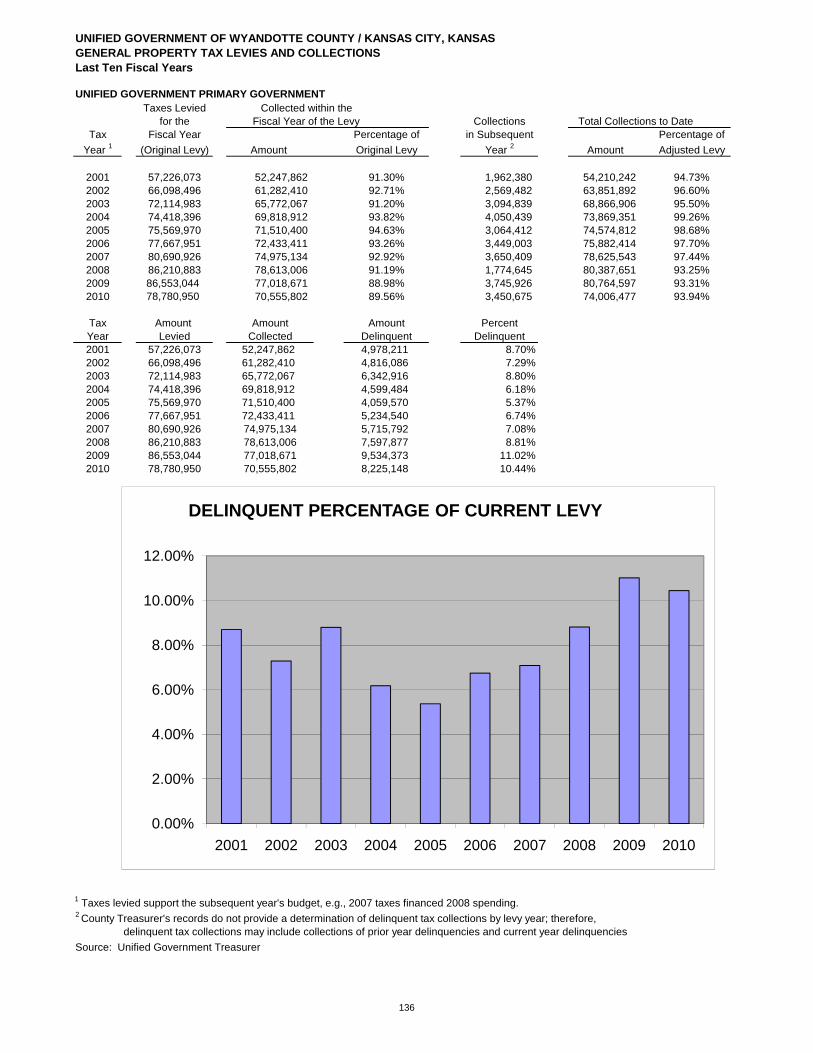

Revenue Capacity ----------------------------------------------------------------------------------------------------- 132 Assessed and Estimated Actual Values of Taxable Tangible Property-Last Ten Years - 132 Direct and Overlapping Governments-Last Ten Fiscal Years ----------------------------------- 134 Principal Property Tax Payers-Current Year and Nine Years Ago ----------------------------- 135 General Property Tax Levies and Collections-Last Ten Fiscal Years ------------------------- 136

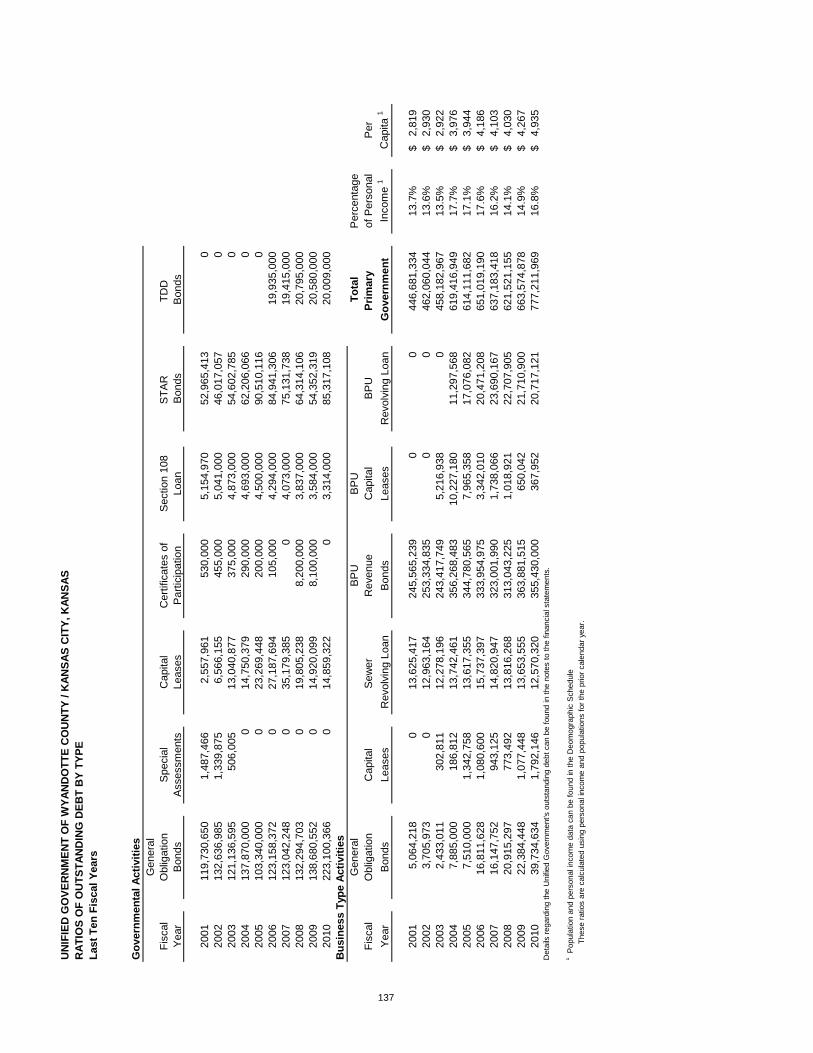

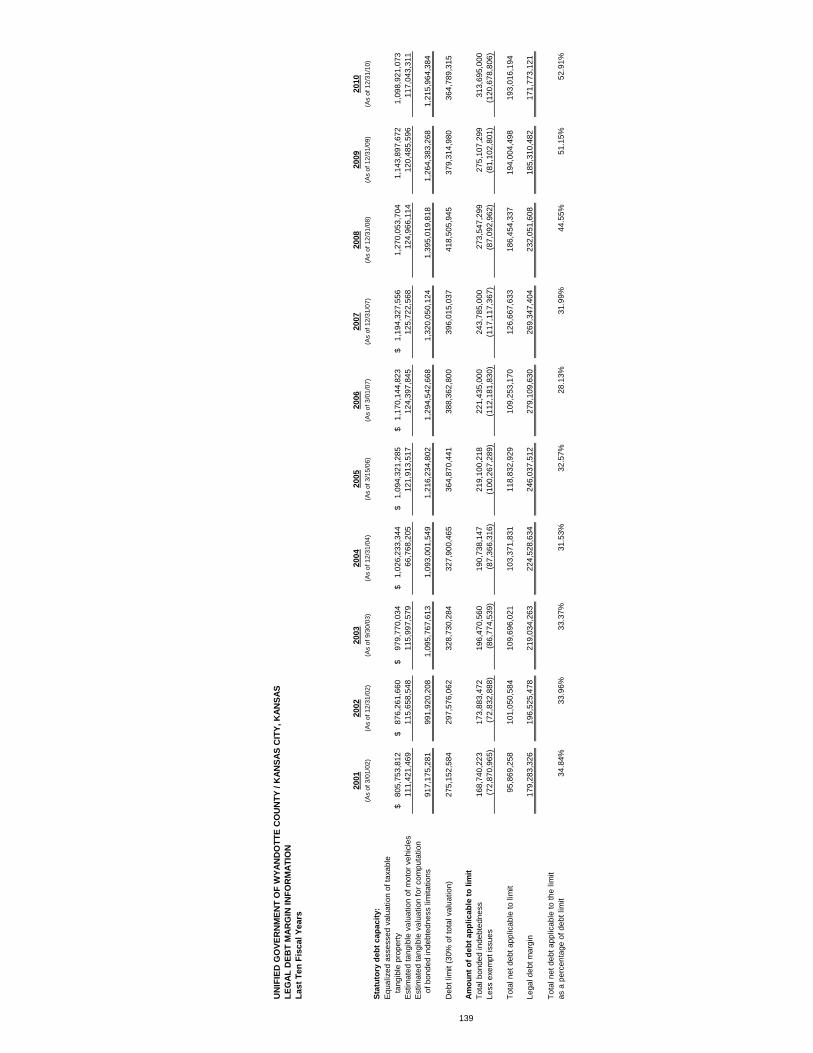

Debt Capacity ----------------------------------------------------------------------------------------------------------- 137 Ratios of Outstanding Debt by Type-Last Ten Fiscal Years ------------------------------------- 137 Ratios of General Bonded Debt Outstanding-Last Ten Fiscal Years -------------------------- 138 Legal Debt Margin Information-Last Ten Fiscal Years -------------------------------------------- 139 Pledged-Revenue Coverage-Last Ten Fiscal Years ---------------------------------------------- 140

Demographic and Economic Information --------------------------------------------------------------------- 141 Demographic and Economic Statistics-Last Ten Fiscal Years ---------------------------------- 141 Principal Employers-Current Year and Nines Years Ago ---------------------------------------- 142

Operating Information ----------------------------------------------------------------------------------------------- 143 Full-time Equivalent County Government Employees by Function- Last Ten Years ------ 143 Operating Indicators by Function-Last Ten Fiscal Years ----------------------------------------- 144 Capital Asset Statistics by Function-Last Ten Fiscal Years ------------------------------------- 145

i

July 6, 2011 To the Honorable Mayor, the Unified Board of Commissioners and Citizens of the Unified Government of Wyandotte County/Kansas City, Kansas: The Office of the Chief Financial Officer and the Office of the County Administrator are pleased to submit to you the Unified Government’s 2010 Comprehensive Annual Financial Report (CAFR). Management has prepared and is responsible for the financial statements and for the integrity and consistency of other information in the Comprehensive Annual Financial Report. The financial statements, which necessarily include amounts based on management estimates and judgments, have been prepared in conformity with Generally Accepted Accounting Principles (GAAP). Management is responsible for the accuracy, completeness, and fairness of the presented data, including all disclosures. The data, as presented, is accurate in all material aspects. It is presented in a manner designed to fairly set forth the financial position and results of the operation of the Unified Government as measured by the financial activity of its various fund types. It also includes all disclosures necessary to enable the reader to gain an understanding of the Unified Government’s financial affairs. The Unified Government maintains a system of internal controls designed to provide reasonable assurance that: assets are safeguarded; transactions are executed in accordance with the Unified Government's authorization requirements and policies; and transactions are properly recorded to allow preparation of financial statements that fairly present financial position and results of operations in conformity with generally accepted accounting principles. Internal accounting controls are augmented by written policies covering standards of personal and business conduct and organizational structure providing for division of responsibility and authority. The effectiveness of and compliance with established control systems is monitored through a continuous program of internal controls. In recognition of cost-benefit relationships and inherent limitations, some features of the control system are designed to detect rather than prevent errors, irregularities and departures from approved policies and practices. Management believes the system of controls has prevented or detected on a timely basis any occurrences that could be material to the financial statements and that timely corrective actions have been initiated when appropriate. The Unified Board of Commissioners has engaged the firm of Allen, Gibbs & Houlik, L.C., independent auditors, to render an opinion on the financial statements. To the best of our knowledge, the independent auditors were provided access to all information and records necessary to render their opinion. The independent audit of the financial statements of the Unified Government is part of a broader, federally mandated “Single Audit” designed to meet the special needs of federal grantor agencies. The

County Administrator’s Office Unified Government of Wyandotte County/

Kansas City, Kansas Dennis Hays, County Administrator

701 North Seventh Street Kansas City, Kansas 66101 (913) 573-5660 • FAX (913) 573-5006

ii

standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statements, but also on the audited government‘s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards. These reports are available in the Unified Government’s separately issued Single Audit Report. The CAFR follows the organization, form and content of the revised principles prescribed by the Governmental Accounting Standards Board (GASB), State of Kansas, Unified Government policy, and the Government Finance Officers Association. There are two groups who are primarily responsible for determining current governmental accounting and reporting practices. They are the American Institute of Certified Public Accountants (AICPA), and GASB. The Unified Government of Wyandotte County/Kansas City, Kansas has adopted these reporting guidelines as its policy and complies with them. GAAP require that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The Unified Government’s MD&A can be found immediately following the report of the independent auditors. General Information The Unified Government of Wyandotte County/Kansas City, Kansas was created October 1, 1997, based on a citizen vote to consolidate the operations of the City of Kansas City, Kansas and Wyandotte County, Kansas. Wyandotte County is located at the confluence of the Kansas and Missouri Rivers and at the crossroads of two transcontinental interstate highways. Two large railroad-switching yards are located in the Unified Government, which is also the base for several truck freight companies. The Unified Government is also the home to the Kansas Speedway Corporation, owners and operators of the 1.5 mile super speedway, which opened in the spring of 2001. The super speedway is located in the northwest corner of the junction of I-435 and I-70. Government Structure The Unified Government is the government for both Wyandotte County and the City of Kansas City, Kansas. The governing body of the Unified Government consists of a ten-member Commission and a Mayor/Chief Executive Officer. Eight Commission positions are elected within geographic districts. Two Commission positions cover half of the County; each with candidates selected in the primary election within their district and in the general election on a countywide vote. The Mayor runs countywide in the primary and the general elections. In addition, the Mayor appoints the County Administrator with approval of the Commission. The Commission annually adopts a balanced budget and establishes the amount of taxes to be levied for the support of Unified Government programs. The County Administrator has the responsibility of administering these programs in accordance with policies and the annual budget adopted by the Commission. Economic Condition and Outlook The Unified Government is the government for both Wyandotte County and the City of Kansas City, KS. Wyandotte County accounts for a large number of manufacturing, transportation and distribution, including rail, and health care jobs in the metropolitan area. Many of these jobs are high paying and contribute to the positive statistics regarding gross payroll and gross sales. Development remains an important priority for the Unified Government.

iii

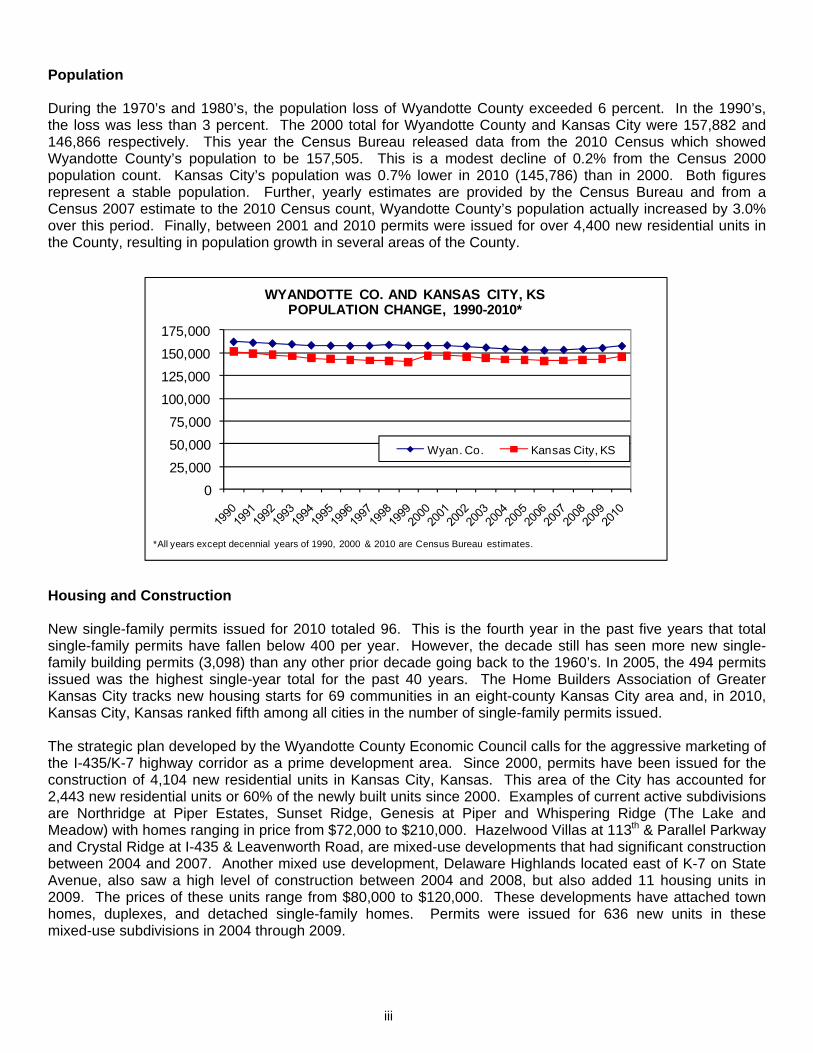

025,00050,00075,000

100,000125,000150,000175,000

Wyan. Co. Kansas City, KS

WYANDOTTE CO. AND KANSAS CITY, KSPOPULATION CHANGE, 1990-2010*

*All years except decennial years of 1990, 2000 & 2010 are Census Bureau estimates.

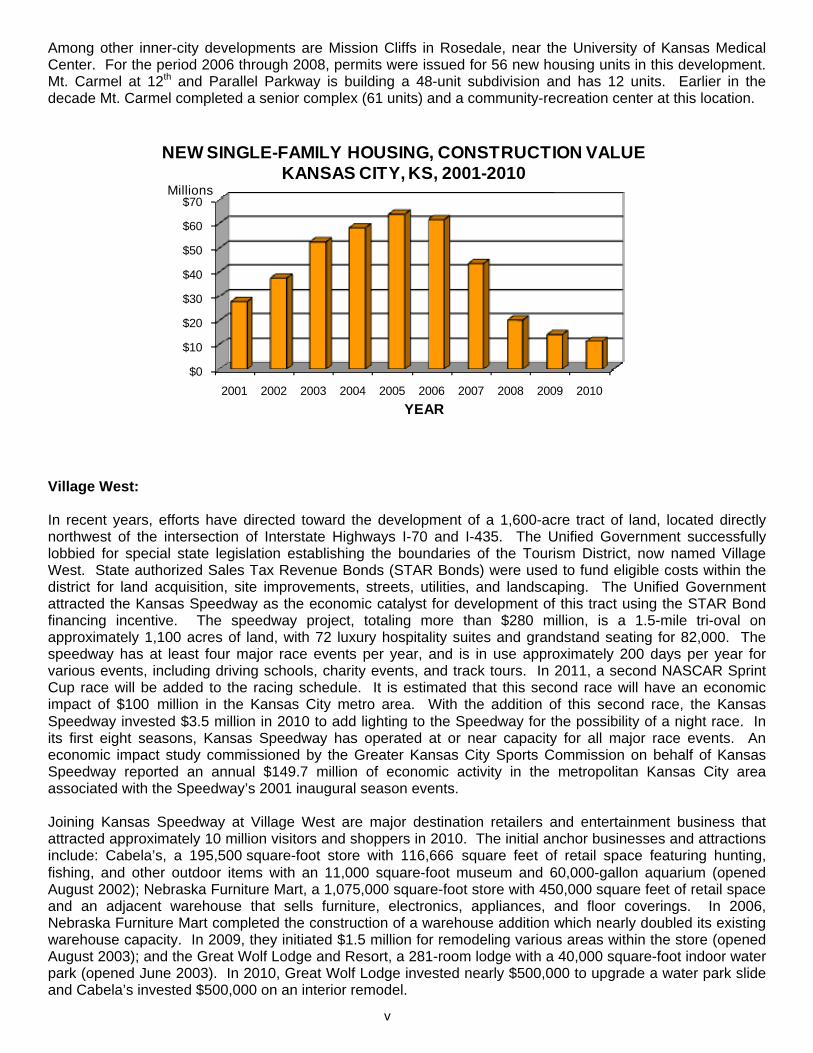

Population During the 1970’s and 1980’s, the population loss of Wyandotte County exceeded 6 percent. In the 1990’s, the loss was less than 3 percent. The 2000 total for Wyandotte County and Kansas City were 157,882 and 146,866 respectively. This year the Census Bureau released data from the 2010 Census which showed Wyandotte County’s population to be 157,505. This is a modest decline of 0.2% from the Census 2000 population count. Kansas City’s population was 0.7% lower in 2010 (145,786) than in 2000. Both figures represent a stable population. Further, yearly estimates are provided by the Census Bureau and from a Census 2007 estimate to the 2010 Census count, Wyandotte County’s population actually increased by 3.0% over this period. Finally, between 2001 and 2010 permits were issued for over 4,400 new residential units in the County, resulting in population growth in several areas of the County.

Housing and Construction New single-family permits issued for 2010 totaled 96. This is the fourth year in the past five years that total single-family permits have fallen below 400 per year. However, the decade still has seen more new single-family building permits (3,098) than any other prior decade going back to the 1960’s. In 2005, the 494 permits issued was the highest single-year total for the past 40 years. The Home Builders Association of Greater Kansas City tracks new housing starts for 69 communities in an eight-county Kansas City area and, in 2010, Kansas City, Kansas ranked fifth among all cities in the number of single-family permits issued. The strategic plan developed by the Wyandotte County Economic Council calls for the aggressive marketing of the I-435/K-7 highway corridor as a prime development area. Since 2000, permits have been issued for the construction of 4,104 new residential units in Kansas City, Kansas. This area of the City has accounted for 2,443 new residential units or 60% of the newly built units since 2000. Examples of current active subdivisions are Northridge at Piper Estates, Sunset Ridge, Genesis at Piper and Whispering Ridge (The Lake and Meadow) with homes ranging in price from $72,000 to $210,000. Hazelwood Villas at 113th & Parallel Parkway and Crystal Ridge at I-435 & Leavenworth Road, are mixed-use developments that had significant construction between 2004 and 2007. Another mixed use development, Delaware Highlands located east of K-7 on State Avenue, also saw a high level of construction between 2004 and 2008, but also added 11 housing units in 2009. The prices of these units range from $80,000 to $120,000. These developments have attached town homes, duplexes, and detached single-family homes. Permits were issued for 636 new units in these mixed-use subdivisions in 2004 through 2009.

iv

A new senior housing project called Pemberton Senior Village is located just south of Parallel Parkway on 82nd St. This $64.5 million housing project will have a total of 80 units, nearly all of them duplexes. A community center will also be built. Through March 2011, a total of 34 permits have been issued for a total of 59 units. The City of Kansas City, Kansas currently has 2,000 buildable lots in 60 subdivisions. The city is poised to continue its positive housing construction trend once the local and national economies begin to improve. Several other developments of interest are located generally north of State Avenue and east of I-635. Peregrine Falcon Estates had its first five homes for sale in 2008. The 30-home first phase will have homes ranging in value from $200,000 to $240,000. Located on 50 acres in the northeast portion of the city, Peregrine Falcon Estates is part of a TIF district that will eventually include 150 new single-family homes, 21 townhomes and 40 renovated homes. Also located in far northeast Kansas City, Kansas, Fairfax Bluff Apartments began renting refurbished units in 2008. A total of 254 units in 47 buildings make up the Fairfax Bluffs Apartment complex. These buildings were initially constructed during the 1940’s to house workers building bombers in the Fairfax Industrial Business District. Finally, the former Northeast Junior High School near 4th and Troup was converted to a 40-unit senior apartment complex in 2007. The conversion represents a $6 million investment and is heading into its second phase. Community Housing Wyandotte County (CHWC) is a non-profit, community development corporation, whose mission is to stabilize, revitalize, and reinvest in Wyandotte County through improved housing and other related developments. CHWC focuses its programs in the urban core neighborhoods of Kansas City, Kansas/Wyandotte County. CHWC was created through the merger of Catholic Housing of Wyandotte County and Neighborhood Housing Services of Kansas City, Kansas. Jointly, these agencies have built and sold over 150 new single-family homes in the urban core of Kansas City, Kansas, and rehabbed over 50 existing homes in the neighborhoods of Prescott, St. Peters/Waterway, St. Joseph/St. Benedict, Bethany, Chelsea, Riverview, and Strawberry Hill. 65 homes have been constructed or rehabbed in the St. Peter’s/Waterway Neighborhood, which is the largest redevelopment project to-date. In addition, CHWC has provided more than $2,000,000 in grants, minor home repair loans, and mortgages to low- and moderate-income households in our community, allowing them to make much needed improvements to their homes. Thus far in 2011, CHWC has completed construction and full occupancy of 20 new single-family homes in the Bethany Neighborhood (the first new construction in the neighborhood in more than 85 years). These homes are part of a program called “House-to-Home Bethany”, which is a 15-year lease to purchase program for families. At the end of the 15 years, the family will take full ownership of the house. In partnership with the Unified Government of Wyandotte County, CHWC is combating foreclosures in our neighborhoods through the utilization of the Neighborhood Stabilization Program, administered through the Community Development Department. CHWC has renovated and sold 10 foreclosed homes back to new families, and currently are working to rehab and sell an additional 14 foreclosures. It is CHWC’s goal to ensure that these vacant and foreclosed homes do not negatively impact the community and the neighborhoods we serve. Another project that CHWC hopes to complete pre-construction activities on in 2011 is titled the “Cottages at Bethany.” This entails plans to build 22 single-family cottages for 55 and older households looking for maintenance-free living in the Bethany neighborhood. The intent is to have this project completed in 2012. In 2010 alone, CHWC invested over $3.1 million dollars into the urban core neighborhoods of Kansas City, Kansas through revitalization efforts. CHWC assisted over 30 families achieve homeownership and through construction efforts created and/or sustained the equivalent of 23 full-time construction-related jobs. Finally, CHWC has been officially named a HUD Approved Counseling Agency. While CHWC has long provided homebuyer education services, it has always been a goal to be recognized and recommended by the Department of Housing and Urban Development as a place that families and individuals can come to seek the support they need when making the decision to purchase a home.

v

$0

$10

$20

$30

$40

$50

$60

$70

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010YEAR

Millions

NEW SINGLE-FAMILY HOUSING, CONSTRUCTION VALUEKANSAS CITY, KS, 2001-2010

Among other inner-city developments are Mission Cliffs in Rosedale, near the University of Kansas Medical Center. For the period 2006 through 2008, permits were issued for 56 new housing units in this development. Mt. Carmel at 12th and Parallel Parkway is building a 48-unit subdivision and has 12 units. Earlier in the decade Mt. Carmel completed a senior complex (61 units) and a community-recreation center at this location.

Village West: In recent years, efforts have directed toward the development of a 1,600-acre tract of land, located directly northwest of the intersection of Interstate Highways I-70 and I-435. The Unified Government successfully lobbied for special state legislation establishing the boundaries of the Tourism District, now named Village West. State authorized Sales Tax Revenue Bonds (STAR Bonds) were used to fund eligible costs within the district for land acquisition, site improvements, streets, utilities, and landscaping. The Unified Government attracted the Kansas Speedway as the economic catalyst for development of this tract using the STAR Bond financing incentive. The speedway project, totaling more than $280 million, is a 1.5-mile tri-oval on approximately 1,100 acres of land, with 72 luxury hospitality suites and grandstand seating for 82,000. The speedway has at least four major race events per year, and is in use approximately 200 days per year for various events, including driving schools, charity events, and track tours. In 2011, a second NASCAR Sprint Cup race will be added to the racing schedule. It is estimated that this second race will have an economic impact of $100 million in the Kansas City metro area. With the addition of this second race, the Kansas Speedway invested $3.5 million in 2010 to add lighting to the Speedway for the possibility of a night race. In its first eight seasons, Kansas Speedway has operated at or near capacity for all major race events. An economic impact study commissioned by the Greater Kansas City Sports Commission on behalf of Kansas Speedway reported an annual $149.7 million of economic activity in the metropolitan Kansas City area associated with the Speedway’s 2001 inaugural season events. Joining Kansas Speedway at Village West are major destination retailers and entertainment business that attracted approximately 10 million visitors and shoppers in 2010. The initial anchor businesses and attractions include: Cabela’s, a 195,500 square-foot store with 116,666 square feet of retail space featuring hunting, fishing, and other outdoor items with an 11,000 square-foot museum and 60,000-gallon aquarium (opened August 2002); Nebraska Furniture Mart, a 1,075,000 square-foot store with 450,000 square feet of retail space and an adjacent warehouse that sells furniture, electronics, appliances, and floor coverings. In 2006, Nebraska Furniture Mart completed the construction of a warehouse addition which nearly doubled its existing warehouse capacity. In 2009, they initiated $1.5 million for remodeling various areas within the store (opened August 2003); and the Great Wolf Lodge and Resort, a 281-room lodge with a 40,000 square-foot indoor water park (opened June 2003). In 2010, Great Wolf Lodge invested nearly $500,000 to upgrade a water park slide and Cabela’s invested $500,000 on an interior remodel.

vi

In addition to the Great Wolf Lodge, four other hotels have opened in Village West, including a Hampton Inn (opened in 2003 with 76 rooms), the Chateau Avalon (opened in 2004 with 62 rooms), a Holiday Inn Express (opened in 2005 with 96 rooms) and Country Inn (opened in 2008 with 117 rooms). A permit for an 86-room Best Western has been issued with construction beginning in 2010. This hotel will be located close to the Kansas Speedway. The Legends at Village West is a more than $230 million shopping center housing nearly 855,000 square feet of retail, dining, and entertainment. In March 2010 the Legends repositioned itself as a destination for upscale outlet shopping. Since then, the Legends has reported a 9 percent increase in revenue and 5 percent increase in traffic. The Legends 14 Theatre complex (87,000 square feet) with state-of-the-art seating and sound systems is the largest of the tenants. In 2011 all 14 screens were upgraded with digital projection and seven of the auditoriums are now available for 3D presentation. Dave and Buster’s, with nearly 50,000 square feet, is a large restaurant/arcade. In 2006, the grand opening of the Legends Center occurred. Currently, over 100 businesses are open with many of the stores and restaurants new to the Kansas City area, creating a unique destination. Backfire BBQ opened in December 2009 and offers attractions that feature dining, entertainment and retail. Backfire BBQ is a partnership between the creators of the T-Rex restaurant located at the Legends and Orange County Chopper Inc. Also opening in 2009 were Five Guys Burgers and Fries and Vanity Fair Outlet. Several stores opened at the Legends in 2010, including Christopher & Banks, LOFT Outlet, Sephoria and the Treasure Chest. Thus far in 2011 three new retailers have announced they will be opening at the Legends - Chico’s, Soma Intimates and Saks Fifth Avenue Off 5th. In April 2006, approximately 235,000 square feet of the original STAR Bond area that provided the financial mechanism to create the Kansas Speedway and the Village West tourism district was removed. This tract of land, which the Unified Government successfully petitioned to be removed, is located in the original northwest corner of the tourism district. Currently, five businesses are operating in the area and local sales taxes generated are being retained by the local entities. These businesses include two large department store retailers, JC Penney and Target (both opened in 2006) as well a Taco Bueno (opened 2007), Payless Shoesource, Panda Express restaurant, a National Tire and Battery and a 117-room Country Inn and Suite (all of which opened in 2008).

vii

Village West and the Legends truly is a unique retail experience. The Unified Government has been awarded the International Economic Development Council (IEDC) 2009 Excellence in Economic Development award in the Public-Private Partnership Category for the Village West Project. IEDC is the largest and most respected professional economic development organization with members worldwide. As of December 2010, 101 businesses, including 29 restaurants, were open in Village West, employing nearly 5,700 persons. These businesses generated over $550 million in retail sales with local and state sales tax, use and transient guest tax collections of over $48 million. The 2010 real and personal property taxes levied for this development area was just over $11 million. Design and construction of two major new developments within the Village West were underway in 2010. The Unified Government, Zimmer Real Estate Services, Inc. and the Kansas Unified Development, LLC entered into a Multi-Sport Stadium Venture Agreement (“Stadium Agreement”) for the construction of an 18,000-seat multi-sport stadium complex that will be the permanent home to the Sporting Kansas City, a Major League Soccer team. Under the Stadium Agreement, the Unified Government has issued STAR Bonds that result in $147,000,000 of net funding for the Stadium Project. The STAR Bonds are payable from State and local sales and transient guest taxes. Construction has commenced for the Stadium Project and the stadium is anticipated to be open in June 2011. In addition to the stadium, a tournament style soccer field complex will be constructed nearby and three recreational soccer fields will be constructed in Kansas City, Kansas. The Unified Government, Zimmer Real Estate Services, Inc. and Cerner Corporation entered into Land Transfer and Specific Venture Agreement in which Cerner Corporation proposes to construct approximately 600,000 square feet of Class A office buildings to accommodate 4,000 Cerner employees. Cerner Corporation is an international supplier of healthcare technology. Construction of the first office building is to begin no later than December 1, 2011 with the entire office complex to be completed by December 1, 2016. The Stadium Project, Class A office buildings and ancillary improvements are expected to cost in excess of $400 million. CommunityAmerica Ballpark is the home of the Kansas City T-Bones, a member of independent baseball’s Northern League. Since the T-Bones moved to Kansas City, Kansas and built their ballpark in 2003, they have proven to be one of the most popular independent teams in the country, averaging 6,000 fans per game. The T-Bones also host area high school and college games and tournaments, as well as Kansas City Kansas Community College games. CommunityAmerica Ballpark has also seen performances by Bob Dylan, Willie Nelson, Def Leppard, Bryan Adams, and various other entertainment acts. The T-Bones have also designed a cash element for their charity outreach: the T-Bones Uncommitted Recreation Fund (TURF). This fund, while administered by the Greater Kansas City Community Foundation, is solely created and funded by the T-Bones. TURF deposits have to date registered in excess of $500,000. TURF’s purpose is to fund capital improvements for Wyandotte County’s Parks & Recreation Department. The fund is specifically not directed toward the department’s annual operating budget, but instead is designed to create a long-lasting, accessible infrastructure for children’s recreation and sports activities. Recent TURF projects included playground and playing field renovations at: Heathwood Park, Pierson Park, Eisenhower Park and Regan Park, which annually hosts the metro-wide Special Olympics softball tournament. Entering their ninth season, the T-Bones have garnered numerous awards, including Northern League Organization of the Year honors in 2004 and 2007, and Kansas City Kansas Chamber of Commerce Small Business of the Year in 2006. The T-Bones also brought championship baseball back to Kansas City with a Northern League Championship in 2008. In 2009, CommunityAmerica Ballpark was named Playing Surface of the Year for both the Northern League and Major League Soccer. The T-Bones welcomed their two-millionth fan into Wyandotte County in the 2010 season. Major Initiatives In 2005, plans for Schlitterbahn Vacation Village were approved by the Kansas Secretary of Commerce to allow for up to $225 million in STAR Bond financing. This represents a second STAR Bond approval and is separate from the STAR Bonds issued for the Kansas Speedway and Village West Project. The total cost of the Schlitterbahn development will be nearly $750 million. Plans for the development include a riverwalk, water-park resort, marine park, lodging, and retail amenities. The site is located on 370 acres east of I-435 between State Avenue and Parallel Parkway and will complement the Village West development. A 24-acre

viii

first phase of the water park opened in July 2009. For the 2011 season, plans were unveiled for a multi-million dollar expansion that will include six new attractions. Construction began in early 2011 on one of these new slides. Company representatives were encouraged by the 2010 season which exceeded expectations. In 2010, the water park drew visitors from all 50 states, as well as the District of Columbia, the Virgin Islands, Puerto Rico, Canada and Mexico. The first phase includes 16 attractions with 24 slides and created 350 seasonal staff positions. Once the STAR Bonds are retired, these developments will become a major source of the new sales and guest tax revenues for local and state governments. In 2007, Wyandotte County voters approved a measure to legalize gambling. In December 2009, the Kansas Lottery Gaming Facilities Review Board approved the construction of a casino in Wyandotte County. Kansas Entertainment, the casino developer, began construction of phase one of the project in the summer of 2010. This project is valued at $386 million and is being built on Turn 2 of the Kansas Speedway. The first phase of the project will include 2,300 slot machines, 86 table games, restaurants and bars. The proposal also includes a second Sprint Cup NASCAR race in 2011 and construction of a Grand-Am sports car road course at Kansas Speedway. The casino project is expected to create 1,500 construction jobs and 1,100 new casino jobs. In the second phase of the project, a 300-room hotel with convention space will be built, along with an entertainment district featuring more restaurants and nightclubs, expanded gaming floor, and a spa. It is anticipated that the casino will be opened by spring 2012.

Adjacent to Kansas University Medical Center a $39 million mixed-use economic development project, 39th & Rainbow, will begin construction this spring. During the first week of April 2011, the existing Sun Inn Hotel was demolished to make way for this project. Plans for this development include approximately 10,000 square feet of first-floor retail space and, on the second through fourth floors, an 83-room Holiday Inn Express & Suites. This area is attractive for new retail development due to the area’s dense resident population and the proximity to the KU Medical Center and Hospital. This area draws more than 10,000 persons daily. Downtown Several major investments have occurred in the downtown area during the past seven years. The Unified Government, through a public/private partnership with KCK Investors, LLC, owns a 49.5% interest in KCK Hotel Group, LLC. This group constructed a Hilton Garden Inn and refurbished the Jack Reardon Convention Center in the urban core. The Hilton Garden Inn Hotel has 147 rooms, a full service restaurant and lounge and adjoins the Jack Reardon Convention Center providing a first-class hotel and convention center to downtown Kansas City, Kansas. In 2011, the hotel and convention center, managed by the Raphael Hotel Group completed its tenth year of operation. Built with and adjoining the hotel is a new 100,000 square-foot headquarters facility for the Board of Public Utilities (BPU). A 485-space parking garage funded in part by a $1.5 million grant from the Economic Development Administration completes this development. In 2003, the Environmental Protection Agency completed the construction of a new lab facility at a cost exceeding $16 million in the downtown area. This lab is adjacent to the EPA Regional Office, a $55 million complex for 600 employees. The EPA has announced plans to move out of Kansas City, Kansas effective April 2012. The current owner of the EPA building in the City has filed a formal protest with the U.S. General Services Administration in an attempt to stop the move. The Mayor of the City has also filed a request with the White House to review the recommendation by the U.S. General Services Administration that gave permission for the EPA to move its offices. The Gateway Office complex located between 4th & 5th Streets south of State Avenue has been transformed into the Children’s Campus of Kansas City. The Children’s Campus serves as a national model in early childhood services focusing on pre-kindergarten children. The 3-story, 72,000 square-foot building valued at $13 million, opened in the summer of 2010. The Children’s Campus houses early childhood education services, family support services, and health, oral health, and mental health services for young children and their families. A $12 million office building housing Kansas Social and Rehabilitation Services employees was completed in 2008. This building is adjacent to the Children’s Campus.

ix

Industrial Park Developments The Unified Government currently has four major industrial parks: Fairfax Industrial Business District, Central Industrial Business District, Armourdale Industrial Business District, and the Santa Fe Industrial Business Park. These four industrial areas represent 80% of the industrial development in the Unified Government. The Unified Government has several other industrial park developments in the Hart Business Park located at 55th and K-32, Woodend Industrial Park along the I-435 Corridor, the Muncie Industrial Park located at 62nd and K-32 and the I-635 Industrial Park at I-635 and Metropolitan. Edwardsville has also developed an industrial/warehouse area near I-435 and the Kansas River. In the Fairfax Industrial Business District, the General Motors Fairfax Plant completed a $116 million expansion in order to produce a line of Saturn automobiles. In 2007, General Motors began building a redesigned Chevrolet Malibu. This change to the Fairfax plant was a $190 million investment. In 2008, General Motors built a $2.5 million addition to one of its buildings. In 2009, General Motors began production of the Buick LaCrosse. This move added 375 jobs at the Fairfax plant. A third shift was added in January 2010, creating approximately 900 jobs. It was announced in April 2010 that General Motors will invest $136 million in its Kansas City plant to rebuild its next-generation Chevrolet Malibu and a hybrid version of the Buick LaCrosse. Kellogg’s Snack Division, also located in the Fairfax Industrial District, underwent a $33 million expansion in 2007 to manufacture three new product lines. Also in 2007, Owens Corning has placed in service an $8.8 million J-3 Insulation production line. Exide Technologies, which manufactures lead-acid batteries, plans to spend $7 million to expand operations at its Fairfax plant. Advanced Building Composites, which develops economical, light-weight, high-strength composite building materials, began operations in early 2010. The Armourdale Industrial Business District has several major on-going developments. In 2006, Proctor & Gamble began a $70 million expansion for both a new product line and packaging line. Prime Investments built a $5 million industrial/warehouse building and the PQ Corporation constructed a $1.8 million conversion of a warehouse facility in 2007. Further, in 2011 PQ was issued a building permit valued at $6 million for a new chemical manufacturing facility. In 2009, mattress-maker Sealy Corporation signed a 10-year lease for a new 123,000 square-foot plant in Armourdale and will move its operations from the Fairfax Industrial Business District. In 2010, it was announced that Zeolyst International, manufacturer of zeolite powders used in a variety of industrial applications, will make a $83 million capital investment to its Kansas City, Kansas location, including a 43,000 square-foot addition. The company also plans to add 33 positions. The project is expected to be completed in late 2012 or early 2013.

x

In the Santa Fe Industrial Business Park, Display Studios opened a $4.4 million manufacturing facility in 2007. Burlington Northern Santa Fe Railroad built a $1.5 million commercial building in 2008. Also in 2008, just outside the Santa Fe Industrial Business Park, Swartz Road Warehouse built a $1.4 million addition. In 2009, two more businesses announced there were moving to the Santa Fe Industrial Business Park. A Sara Lee meat-slicing plant will occupy an existing 187,000 square-foot building and bring 250 jobs to the area. This plant became fully operational in 2011. GMJ, a parent company for six transportation related businesses, will occupy a previously vacant 120,000 square-foot building. The Ranpark Corporation expanded into the Central Industrial Business District. Ranpark manufactures paper packaging materials and spent approximately $1 million on the plant in 2007. In 2009, Package Development Corp. spent $1 million to purchase and equip a building that will be used to create packaging for food industry customers. Weyerhaeuser constructed a new $6.2 million lumber product distribution center near I-435 and K-32 in 2003. Griffin Wheel finished a $13 million expansion of its rail car wheel manufacturing facility in the K-32 Muncie area in 2005. In 2007, Griffin Wheel constructed a $1.25 million building addition. Plastic Packaging, located just off Holliday Drive and 65th Street, undertook a $1.2 million building expansion in 2006. Recent developments in other areas include: Kansas City Steaks spent $4 to 5 million on additional equipment and added 30 to 40 employees at its location in Armourdale; locally owned Liberty Fruit Company in 2010 expanded its operations in the Argentine neighborhood in Kansas City, Kansas by increasing its warehouse capacity 50% ($1.3 million building addition) and hiring 25 additional employees; Frito Lay spent $2 million on a distribution center in the Melrose Business Park, near I-635 and Metropolitan; Midland Pharmaceuticals recently expanded its facility through a $4.6 million investment in the Rosedale/Shawnee Heights area of Wyandotte County; and Fastenal and Quill opened new distribution facilities in the Edwardsville I-435 industrial area at an aggregate investment of $14.4 million. In the Cambridge Business Park, located just west of Kansas City, Missouri and north of I-35, Rite Maid Paper built a $5 million office/warehouse facility in 2007. Further, in 2010, Western Blue, a printing company, announced plans to relocate to this area from Kansas City, Missouri. Western Blue will move into a 20,000 square-foot industrial building which will improve the company’s visibility and access. Another move into the Cambridge Business Park includes McAnany Van Cleave & Phillips PA, a prominent Kansas City, Kansas law firm. They moved into a 26,500 square-foot office space in early 2011. Office and Service The downtown area, with approximately 6,000 employees, has the largest concentration of office workers. In addition to the downtown area, there are active office parks in Cambridge Terrace, Meadowlark Lane, Woodlands West and assorted office and medical facilities in different locations throughout the community. The Unified Government owns and operates the 111-acre Public Levee facility in the Fairfax Industrial Business District. At the close of 2009, the Public Levee has 569,000 square feet of warehouse and office space. 72% of the warehouse and 48% of the office space is under lease, with warehouse space accounting for over 91% of total Levee space. In addition, a large grain elevator facility, with 253,000 square feet and a five story cold storage facility containing 164,000 square feet, remains leased. .

xi

Several offices and service buildings have been constructed directly north of Village West, near 110th and Parallel Parkway. The cost of development associated with these office facilities is in excess of $5 million. The firms locating in this area include: Heartland Primary Care, a medical group; Security National Bank; Mid America Bank and Trust; and a general office building. In 2008, construction began on a new $2.5 million Discover Vision Center office building in this general area. This building opened in 2009 and provides essential vision related services to Wyandotte County residents. Woodlands West, directly east of I-435 and Leavenworth Road, has also experienced recent development. Two office buildings have opened since 2004. In 2007, two new hotels opened in the I-435 corridor: Comfort Suites (84 rooms) located at I-435 & Leavenworth Rd. and Candlewood Inn (98 rooms) at 110th & Parallel. In 2008, Byrd’s Dance and Gymnastics studio opened. Adjacent to Byrd’s a newly constructed Masonic lodge opened in 2009. The combined value of these projects is over $2 million. Retail In addition to the Village West development, several other developments have seen growth in recent years. The State Avenue midtown area has had several developments. Earlier in the decade Walgreens built a new pharmacy/discount store at 78th and State Avenue. Lowes constructed an $8.1 million 125,000 square-foot home improvement store at 72nd and State Avenue. In 2007, a Walgreens located at 28th and State Avenue opened. In 2009, a new Taco Bell restaurant opened at 73rd and State Avenue. The Save-A-Lot grocery store chain has remodeled a grocery store that has been closed for several years located at 81st and State Ave. The store was remodeled in 2010 is currently open. Also in the midtown area at 54th and Leavenworth Road, a grocery store was remodeled and opened in November 2008 at a cost of nearly $1 million. This redevelopment brought a much needed quality grocery store to this part of town. A Church’s Chicken opened in 2010 at 82nd and Parallel Parkway. In the southeast portion of the city the Shawnee Plaza shopping area is undergoing redevelopment. In 2011 permits were issued for a Sunfresh Market grocery store remodel and a façade renovation for the other retail stores. Parking lot resurfacing is also occurring. The value of these projects totaled $1.2 million. Other new retail stores for 2010 in various parts of the city include: a new CVS Pharmacy ($1.5 million) located in the southwest corner of the city; a new Dollar General store located at 60th and Leavenworth Road; and a new Casey’s General Store ($1.0 million) located at 130th and State Ave. All of these stores began construction in 2010. Piper Plaza has completed its second phase with the development of a neighborhood strip center. Piper Plaza is located near Village West at 110th and Parallel Parkway, but has more of a neighborhood focus, with tenants such as a dry cleaner, UPS delivery store, bar and grill and dental office. Its development costs are in excess of $3 million. Not far from Piper Plaza, several banks have opened with a combined value of $4.3 million. These include Security Bank (2005), Country Club Bank (2005), and First State Bank and Trust (2007). In late 2006, the Unified Government Commission approved a $190 million project called Plaza at the Speedway, a tax increment project located on the north side of Parallel Parkway across from the Legends shopping area. This development will provide 775,000 square feet of retail shopping and is expected to create over 2,100 jobs. The shopping area is anchored by a Best Buy that opened in the spring of 2009 and a Wal-mart Supercenter that opened in October 2009. A Taco Bell opened in April 2010 and an Olive Garden restaurant opened in May 2010. Other openings are as follows: Kohl’s retail store - September 2010; Chick-Fil-A restaurant - October 2010; and Red Lobster - March 2011. A building permit was issued in April 2011 for a Jack In the Box restaurant. Finally, just on the other side of Interstate I-435 from Village West, a new Toyota dealership is under construction and is valued at $6 million.

xii

Recreation A new YMCA facility, completed in 2006 at a cost of approximately $4 million, was built adjacent to the Providence Medical Center. Mt. Carmel Development built a community center, with a cost similar to the YMCA, in the eastern area of Wyandotte County near 12th and Parallel Parkway and opened in 2006. In November 2006, Heart of America Volleyball Association completed a conversion of an existing building to offices and a volleyball recreation facility which has five tournament courts. This building will serve as a practice facility and will also host local and regional volleyball tournaments. In 2010, the Wyandotte County Fair Board spent $800,000 on grading for a new site for the Wyandotte County Fair to be located in the vicinity of 137th and Polfer road in the northwest portion of Wyandotte County. Internal Accounting Controls Financial Control: The Unified Government of Wyandotte County/Kansas City, Kansas, has adopted a comprehensive system of internal controls designed to reasonably safeguard Unified Government assets, check the accuracy and reliability of its accounting data, promote operational efficiency, and encourage adherence to prescribed managerial policies within the Unified Government. Basic management responsibilities emphasize that the accounting system must have a strong relationship with all other management control systems. The Unified Government's internal accounting controls reasonably safeguard assets and provide reasonable assurance of proper recording of all financial transactions. As part of the continuing effort to improve fiscal stewardship and financial accountability, the Unified Government utilizes a fully computerized financial accounting management information system, the Cayenta Financials System (CFS). The system is an integrated, online municipal government financial management system, comprised of many subsystems. Modifications and enhancements are continually being made to this system in order to keep abreast of rapidly changing accounting techniques and principles. CFS is based on the single transaction concept of processing, in which all relevant files and reports are updated from a single input of information. Look-up tables are used to tailor all accounting and classification treatments and are changed by file maintenance initiated by the Financial System Administrator. Budgetary Control: The Unified Government maintains budgetary controls, which have the objective of ensuring compliance with legal provisions embodied in the annual appropriated budget approved by the Unified Board of Commissioners. Activities of the General Fund, Special Revenue Funds, Debt Service Fund, and Proprietary Funds are included in the annual appropriated budget. The Unified Government has the following levels of budgetary control: • The legal level of control is established at the fund level by State statutes, which also permits the transfer

of budgeted amounts from one object or purpose to another within the same fund.

• The Unified Government further controls spending by requiring that no expenditures be committed that would exceed the amount appropriated for the spending category (e.g., Personnel Services, Contractual Services) without the department first obtaining approval.

• As allowed by State statute, the governing body can increase the fund level expenditures by amending the budget. An amendment may only be made for previously unbudgeted increases in revenue other than ad valorem taxes. To do this, a notice of public hearing to amend the budget must be published in the local newspaper. At least ten days after the publication, the hearing may be held and the governing body may amend the budget at that time.

The Unified Government's annual budget is prepared in conformance with and certified as required by Kansas State Statutes. The Unified Government Administrator and the Unified Board of Commissioners evaluate budget proposals of the various Unified Government departments to determine funding for operating, capital and public service programs. After giving due consideration to the input received from citizens, the Unified Board of Commissioners adopts the budget. Thus, the adopted budget is a document which places before the people of the Unified Government a clear and precise picture of the cost of public services which are to be

xiii

provided. The budget process is automated and appropriately controlled through an online accounting system to assure effective fiscal management and accountability. Property Tax Levies and Collections In accordance with applicable state statutes, property taxes levied during the current year are revenues to be used to finance the budget of the ensuing year. Taxes are assessed on a calendar year basis and are levied and become a lien on the property on November 1 of each year. The County Treasurer is the tax collection agent for all taxing entities within the County. Property owners have the option of paying one-half of the full amounts of the taxes levied on or before December 20 during the year levied with the balance to be paid on or before May 10 of the ensuing year. State statutes prohibit the County Treasurer from distributing taxes collected in the year levied prior to January 1 of the ensuing year. Consequently, for revenue recognition purposes, the taxes levied during the current year are not due and receivable until the ensuing year. At December 31, such taxes are a lien on the property and are recorded as taxes receivable, net of anticipated delinquencies, with a corresponding amount recorded as unearned revenue. It is not practicable to apportion delinquent taxes held by the County Treasurer at the end of the year and the amounts thereof are not material in relationship to the financial statements taken as a whole. The November 2010 certified assessed valuation for Wyandotte County was $1.1 billion. Real property value accounted for 84% of this overall figure. The overall total was 4% below the prior year total. Residential and commercial property valuations continue to be impacted by the nation’s 2008 economic recession; however the total 4% decline in property valuation in 2010 was significantly less than the prior-year loss of 10.9%. Personal property valuation is still affected by the 2006 legislation that exempts new machinery and equipment purchases from the tax roll. Personal property assessed value declined by $13.3 million or 11% from 2009 to 2010. The Unified Government 2010 tax levy for the 2011 budget is $79.3 million. In 2009, the Unified Government levied $78.8 million in property taxes for budget year 2010. Current property tax revenue collections in 2010 were $70.6 million. In comparison, in 2009 the current tax collections were $77 million, derived from a 2008 tax levy of $86.6 million. The collection rate for current property taxes increased from 89% in 2009 to 90% in 2010. This improvement can be attributed to the settlement of several commercial property valuation appeals in the prior year. Special and Extraordinary Items Three special items occurred in 2010, impacting the financials. First all employees, with the exception of public safety personnel were subject to 12 mandatory furlough days. This action resulted in salary reductions of $2.2 million on an annual basis. The General Fund represented 72% or $1.6 million of the savings. Offsetting this savings was an early retirement incentive program that 76 individuals committed to. Accrued pay and benefits for these individuals totaled $2.7 million, with a General Fund expense of $2.5 million. Voters approved a 3/8th cent dedicated sales tax in April 2010. The tax began July 1st of 2010 and the government received four months of tax distributions in 2010 totaling $1,880,559. A special revenue fund was established for the receipt of these tax payments and for budgeted expenditures from the fund. Cash Management All idle cash is invested during the year in certificates of deposit, US Treasury Notes, the Kansas Municipal Investment Pool, U.S. Government agencies, bank trust department municipal pools, temporary notes or no fund warrants, repurchase agreements and overnight investments in the Unified Government’s primary depositories. At December 31, 2010 the carrying amount of such investments was $201,801,531. The Unified Government earned interest income in the amount of $1,156,385 during the year ended December 31, 2010. The Unified Government pools its operating funds in order to maximize interest revenue. As provided by State law (K.S.A. 9-1402), the Unified Government’s depositories pledge securities with market value at least equal

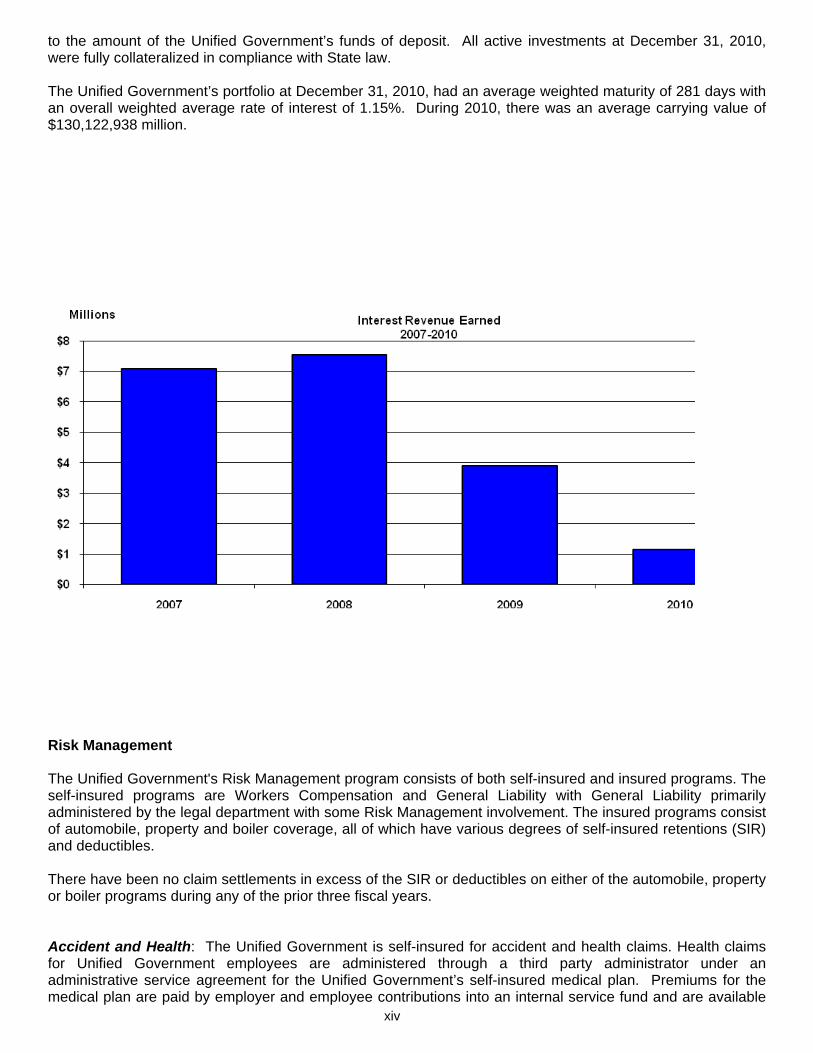

xiv

to the amount of the Unified Government’s funds of deposit. All active investments at December 31, 2010, were fully collateralized in compliance with State law. The Unified Government’s portfolio at December 31, 2010, had an average weighted maturity of 281 days with an overall weighted average rate of interest of 1.15%. During 2010, there was an average carrying value of $130,122,938 million.

Risk Management The Unified Government's Risk Management program consists of both self-insured and insured programs. The self-insured programs are Workers Compensation and General Liability with General Liability primarily administered by the legal department with some Risk Management involvement. The insured programs consist of automobile, property and boiler coverage, all of which have various degrees of self-insured retentions (SIR) and deductibles. There have been no claim settlements in excess of the SIR or deductibles on either of the automobile, property or boiler programs during any of the prior three fiscal years. Accident and Health: The Unified Government is self-insured for accident and health claims. Health claims for Unified Government employees are administered through a third party administrator under an administrative service agreement for the Unified Government’s self-insured medical plan. Premiums for the medical plan are paid by employer and employee contributions into an internal service fund and are available

xv

to pay health claims and administrative costs of the plan. An excess insurance policy covers individual claims paid in excess of $250,000 per person, per year for all non-job related injuries and for job-related claims paid for members of the Kansas City, Kansas Fire Department. The Board of Public Utilities (BPU) is essentially 100% self-insured for health care claims and is responsible for the first $500,000 of general liability and automobile insurance claims. In addition, any general liability or automobile claims greater than $35,000,000 are the responsibility of BPU. Workers’ Compensation: The Unified Government is self-insured for workers' compensation. An excess coverage insurance policy covers individual claims in excess of $750,000. Effective January 1, 2000, the former county’s workers’ compensation program was consolidated with the former city’s program, which is self-insured. The BPU is self-insured to the first $350,000 per employee/per occurrence for workers' compensation. Claims exceeding $350,000 and up to $35,000,000 per employee/per occurrence are fully insured. General Liability: The Unified Government is also self-insured for liability claims with no premium paid to any insuring firm. All liability claims are reviewed, challenged if appropriate, and processed for payment at the agreed amount by the Legal Department. Kansas statutes limit the liability in tort cases to $500,000. Conduit Debt In order to encourage economic and industrial development, the Unified Government issues tax exempt industrial revenue bonds to assist local companies in financing the construction or renovation of industrial facilities on Unified Government land or acquisition of equipment. The proceeds of the bonds issued are deposited with local financial institutions, which act as trustees. As of December 31, 2010, a total of $547.7 million in industrial revenue bonds had been issued for various capital investment initiatives and remain outstanding. This amount includes in excess of $295.9 million of current issues for the Kansas City, KS General Motors’ automobile assembly plant. Independent Audit The basic financial statements for 2010 were examined by Allen, Gibbs, & Houlik, L.C., and their opinion has been included in this report. They have provided the Unified Government with an unqualified opinion. Additionally, the Unified Government is required to undergo an annual single audit in conformity with the provisions of the Single Audit Act of 1996 and U.S. Office of Management and Budget Circular A-133, entitled Audits of States, Local Governments and Non-Profit Organizations. Information related to this single audit, including the Schedule of Expenditures of Federal Awards, findings and questioned costs, and auditor's reports on the internal control structure and compliance with applicable laws and regulations are included in a separate report issued annually by the Unified Government. Certificate of Achievement for Excellence in Financial Reporting The Government Finance Officers Association (GFOA) of the United States and Canada awarded a Certificate of Achievement for Excellence in Financial Reporting to the Unified Government for its Comprehensive Annual Financial Report for the fiscal year ended December 31, 2009. This is the ninth consecutive year that the government has achieved this prestigious award. In order to be awarded a Certificate of Achievement, the government must publish an easily readable and efficiently organized report, which conforms to applicable program standards, generally accepted accounting principles, and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. The Unified Government believes that our current Comprehensive Annual Financial Report continues to meet the Certificate of Achievement Program’s requirements and we are submitting the 2010 Comprehensive Annual Financial Report to GFOA to determine its eligibility for another certificate.

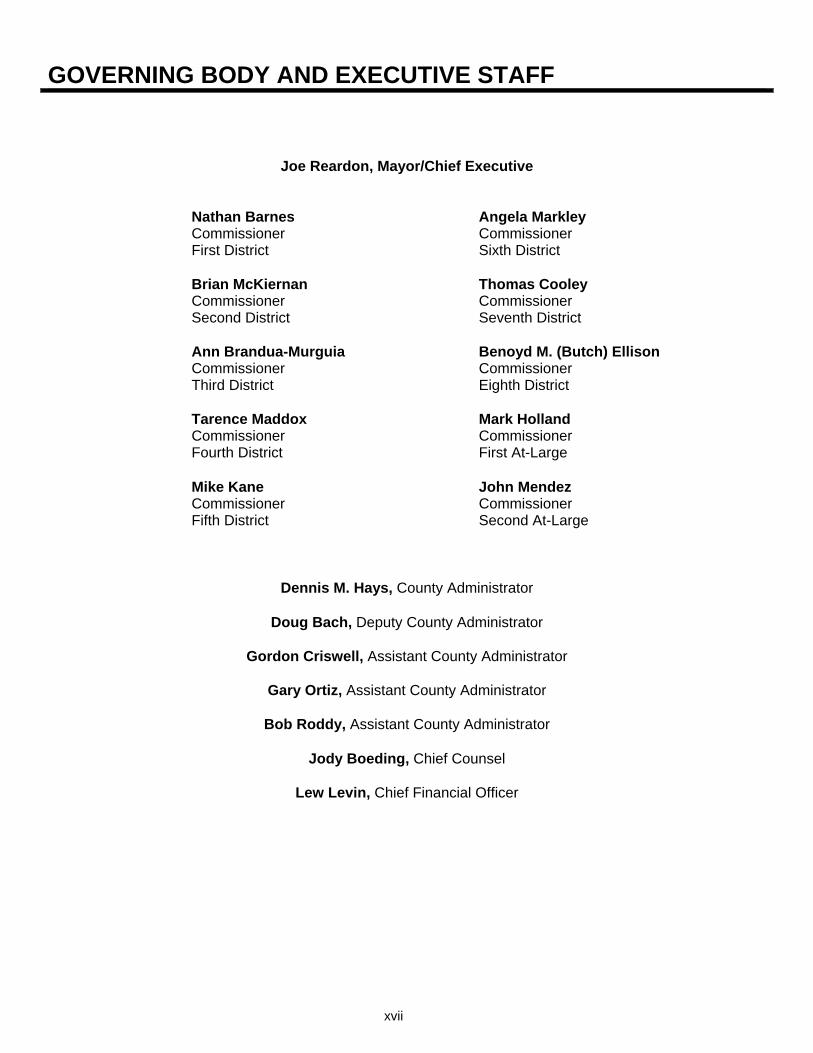

xvii

GOVERNING BODY AND EXECUTIVE STAFF

Joe Reardon, Mayor/Chief Executive

Nathan Barnes Angela Markley Commissioner Commissioner First District Sixth District

Brian McKiernan Thomas Cooley Commissioner Commissioner Second District Seventh District

Ann Brandua-Murguia Benoyd M. (Butch) Ellison Commissioner Commissioner Third District Eighth District Tarence Maddox Mark Holland Commissioner Commissioner Fourth District First At-Large Mike Kane John Mendez Commissioner Commissioner Fifth District Second At-Large

Dennis M. Hays, County Administrator

Doug Bach, Deputy County Administrator

Gordon Criswell, Assistant County Administrator

Gary Ortiz, Assistant County Administrator

Bob Roddy, Assistant County Administrator

Jody Boeding, Chief Counsel

Lew Levin, Chief Financial Officer

xviii

xix

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY/KANSAS CITY, KANSAS COMPREHENSIVE ANNUAL FINANCIAL REPORT For the year ended DECEMBER 31, 2010

FINANCIAL SECTION

The Financial Section is the Unified Government’s audit report. It includes the opinion of the Independent Auditors, Management’s Discussion and Analysis (MD&A), the Basic Financial Statements and Combining Statements and Schedules. The Basic Financial Statements reflect all financial activity of the Unified Government combined into nine (9) schedules. Notes to the Financial Statements are adjunctive to the Basic Financial Statements, serving to explain the numbers and to highlight required disclosures. The Combining Statements and Schedules reflect greater detail of the Unified Government’s financial activities. Also included are schedules showing the extent of each fund’s compliance to state budget laws.

1

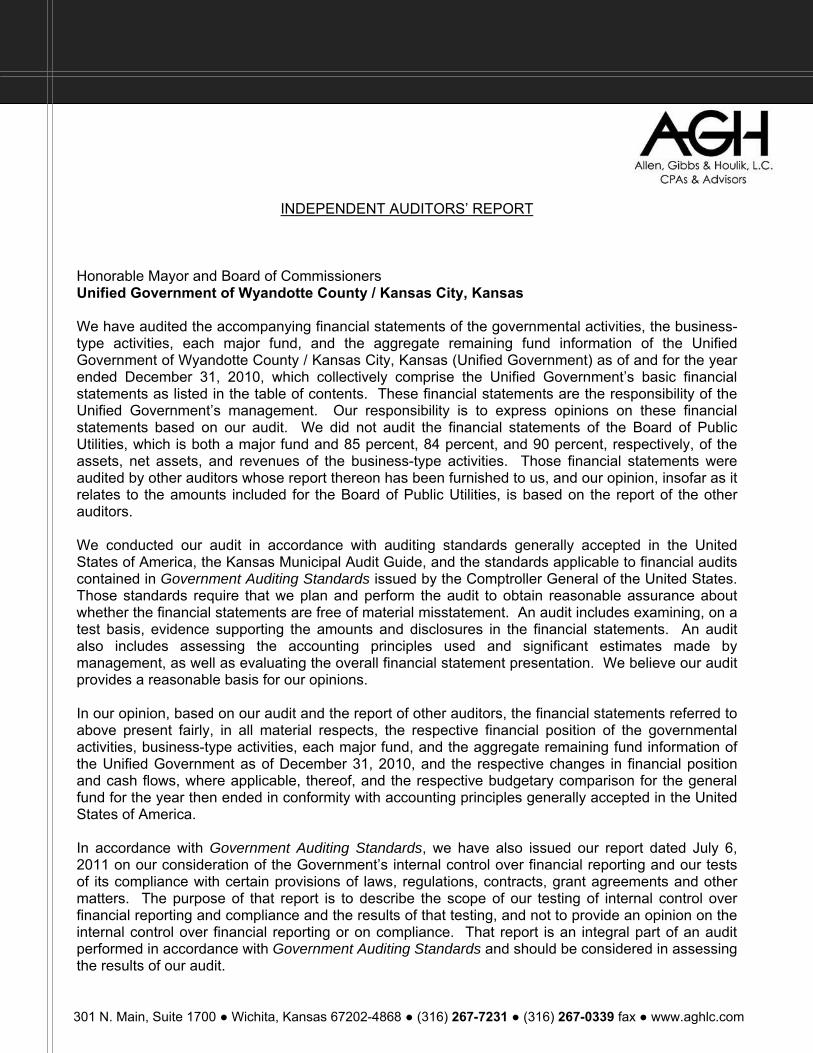

301 N. Main, Suite 1700 ● Wichita, Kansas 67202-4868 ● (316) 267-7231 ● (316) 267-0339 fax ● www.aghlc.com

INDEPENDENT AUDITORS’ REPORT Honorable Mayor and Board of Commissioners Unified Government of Wyandotte County / Kansas City, Kansas We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Unified Government of Wyandotte County / Kansas City, Kansas (Unified Government) as of and for the year ended December 31, 2010, which collectively comprise the Unified Government’s basic financial statements as listed in the table of contents. These financial statements are the responsibility of the Unified Government’s management. Our responsibility is to express opinions on these financial statements based on our audit. We did not audit the financial statements of the Board of Public Utilities, which is both a major fund and 85 percent, 84 percent, and 90 percent, respectively, of the assets, net assets, and revenues of the business-type activities. Those financial statements were audited by other auditors whose report thereon has been furnished to us, and our opinion, insofar as it relates to the amounts included for the Board of Public Utilities, is based on the report of the other auditors. We conducted our audit in accordance with auditing standards generally accepted in the United States of America, the Kansas Municipal Audit Guide, and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe our audit provides a reasonable basis for our opinions. In our opinion, based on our audit and the report of other auditors, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, business-type activities, each major fund, and the aggregate remaining fund information of the Unified Government as of December 31, 2010, and the respective changes in financial position and cash flows, where applicable, thereof, and the respective budgetary comparison for the general fund for the year then ended in conformity with accounting principles generally accepted in the United States of America. In accordance with Government Auditing Standards, we have also issued our report dated July 6, 2011 on our consideration of the Government’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

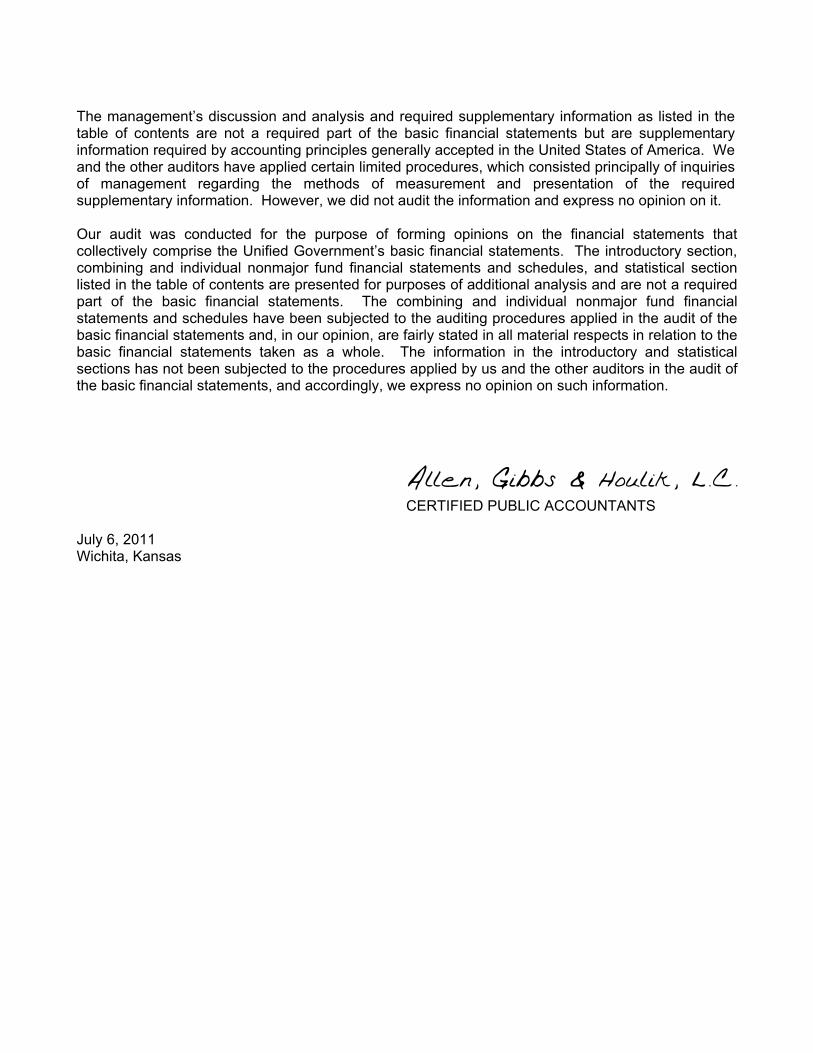

The management’s discussion and analysis and required supplementary information as listed in the table of contents are not a required part of the basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. We and the other auditors have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it. Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Unified Government’s basic financial statements. The introductory section, combining and individual nonmajor fund financial statements and schedules, and statistical section listed in the table of contents are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual nonmajor fund financial statements and schedules have been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, are fairly stated in all material respects in relation to the basic financial statements taken as a whole. The information in the introductory and statistical sections has not been subjected to the procedures applied by us and the other auditors in the audit of the basic financial statements, and accordingly, we express no opinion on such information.

Allen, Gibbs & Houlik, L.C.

CERTIFIED PUBLIC ACCOUNTANTS July 6, 2011 Wichita, Kansas

4

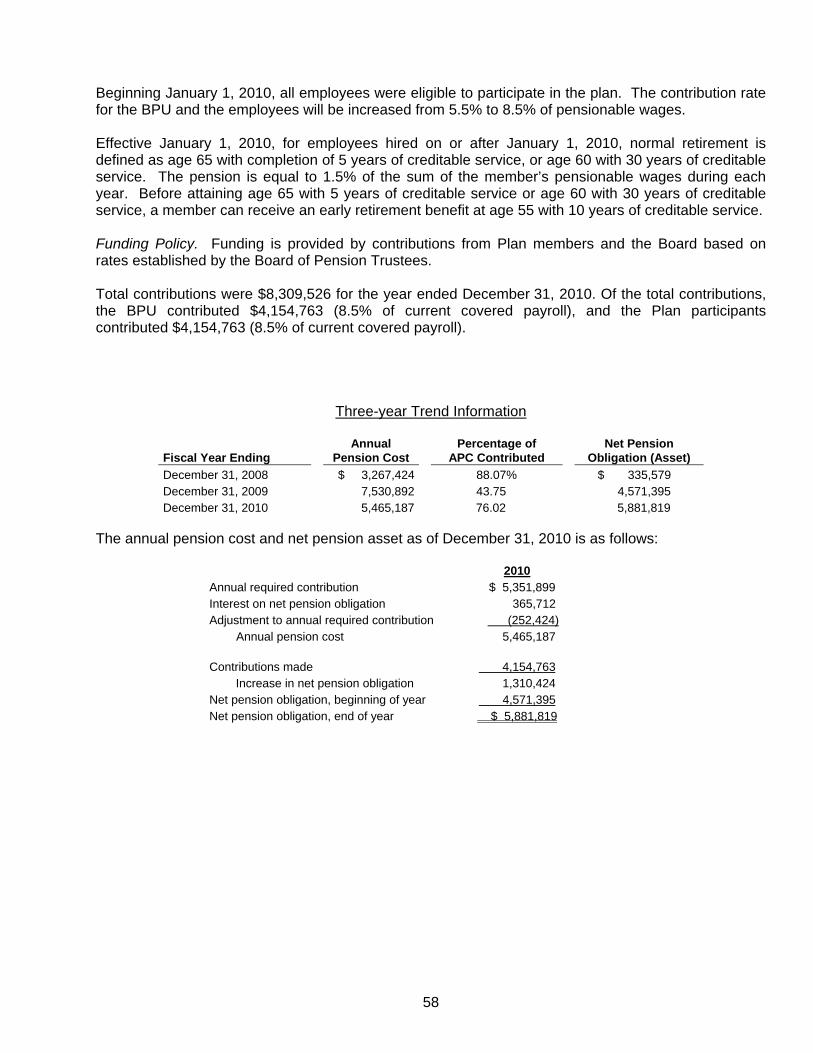

Management’s Discussion and Analysis This discussion and analysis are intended to serve as an introduction to the Unified Government’s basic financial statements. The Unified Government’s basic financial statements comprise three components: 1) government-wide financial statements; 2) fund financial statements; and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Overview of the Financial Statements Government-wide financial statements. The government-wide financial statements are designed to provide readers with a broad overview of the Unified Government’s finances, in a manner similar to a private-sector business. The statement of net assets presents information on all of the Unified Government’s assets and liabilities, with the difference between the two reported as net assets. Over time, increases or decreases in net assets may serve as a useful indicator of whether the financial position of the Unified Government is improving or deteriorating. The statement of activities presents information showing how the government’s assets changed during the most recent fiscal year. All changes in net assets are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave). Both of the government-wide financial statements distinguish functions of the Unified Government that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are included to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the Unified Government include general government, health and welfare, public safety, public works, parks and recreation, and planning and development services. The business-type activities of the Unified Government include electric and water systems, sewer system, EMS, public levee, storm water and Sunflower Hills Golf Course. The government-wide financial statements can be found as listed in the Table of Contents. Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The Unified Government, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the Unified Government can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities.

5