Unifi High Yield Fund

24

Unifi High Yield Fund

Transcript of Unifi High Yield Fund

Unifi High Yield Fund

Preface

Investor Predicament

Conventional Equity •High / above average return potential •Accompanied by extreme volatility

Conventional Debt •Low / below average volatility •Hardly any real returns post tax and inflation

Cyclicality of asset values combined with misconstructed risk-return expectations push investors to either • settle for sub-par returns (or) • bear volatility beyond one’s temperament leading to capital loss

Unifi HYF Proposition

High Yield Fund

•Consistent above average returns •Minimal / below average volatility

Risk adjusted arbitrage and fixed income opportunities arising from

• corporate events

• macro-economic cycles

• emerging credit

The following table presents the backdrop of choices and challenges that we typically face in planning our investments. Every one of these 4 choices suffers from at-least one serious flaw that renders it suboptimal. Equity is the one option that earns an attractive return, but its deep cyclicality naturally limits the proportion of capital that most investors are willing to expose to it. Unifi High Yield Fund (HYF) seeks to address this investor dilemma i.e. finding a middle path that could consistently generate a solid return over inflation, without any restrictions on free and unfettered access to one’s own money. We set ourselves a goal of earning a real return of 3% - 4% p.a. after inflation, taxes and all costs, using strategies that we understand and trust.

CAGR RETURNS FOR PAST 28 YEARS

Bank deposit/

Debt mutual

funds5

8.92-8.94%1 Just barely beats inflation post tax

Real Estate 10.20%2 Illiquid, highly cyclical, high transaction costs, complex

title & project specific issues

Gold 10.64%3 Driven purely by psychological factors, cyclical & volatile

Equity 14.30%4

The predicament of having to time one’s need for capital

with the right moment in the cycle, limits the proportion

of savings that one can deploy

Preface (Contd.)

Preface (Contd.)

Our real challenge is to diligently find the pockets of opportunity that are constantly

created by the ebb and flow of economic trends, corporate actions and human-emotion. We closely monitor a wide range of asset classes and devise simple methods to continually access the market’s evolving energy, always mindful of probable scenarios that could surprise us.

Unifi High Yield Fund was started in April 2013 and over the past five years has earned a compounded annual return of 15.02% (9.68% post tax) after all expenses with a standard deviation of just 1.8%. Additional highlight is the fund’s outperformance over the category average of comparable debt mutual funds in all of these five years.

Fund / Returns FY2018 FY2017 FY2016 FY2015 FY2014

Unifi High Yield Fund 14.47% 13.70% 14.67% 16.82% 14.40%

Debt MFs - Dynamic bond category average 4.69% 12.13% 6.55% 10.54% 5.86%

- Dynamic bond category topper 7.98% 14.40% 8.07% 15.13% 10.36%

Debt MFs - Credit funds category average 7.70% 10.65% 8.99% 9.28% 8.41%

- Credit funds category topper 9.43% 11.50% 10.02% 11.87% 11.12%

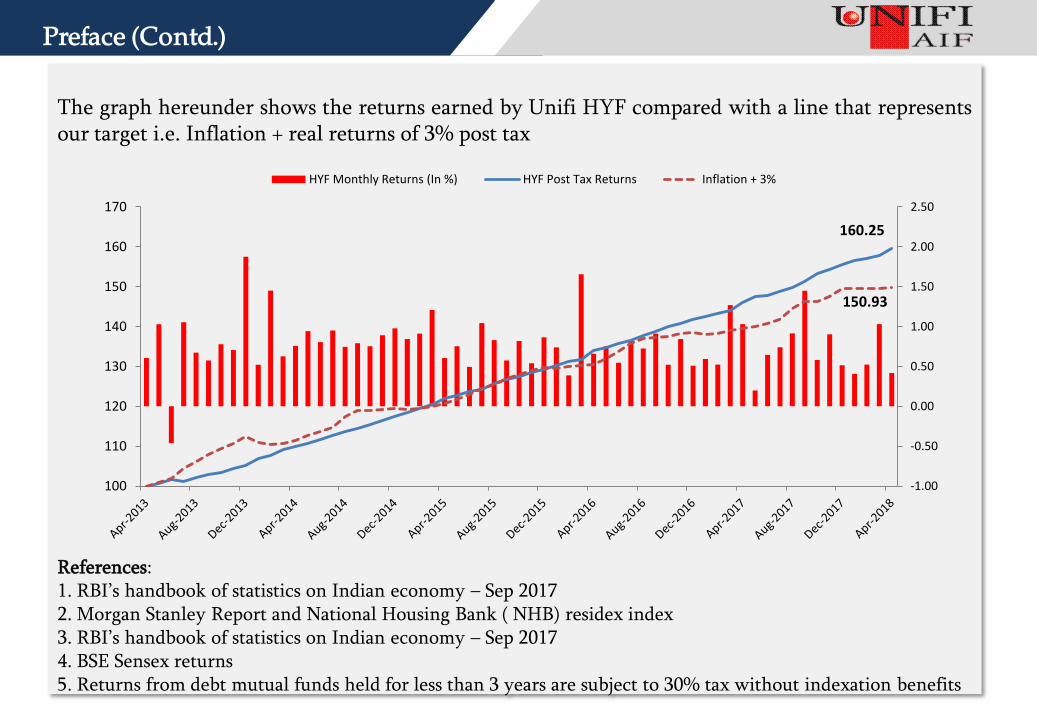

The graph hereunder shows the returns earned by Unifi HYF compared with a line that represents our target i.e. Inflation + real returns of 3% post tax References: 1. RBI’s handbook of statistics on Indian economy – Sep 2017 2. Morgan Stanley Report and National Housing Bank ( NHB) residex index 3. RBI’s handbook of statistics on Indian economy – Sep 2017 4. BSE Sensex returns 5. Returns from debt mutual funds held for less than 3 years are subject to 30% tax without indexation benefits

Preface (Contd.)

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

100

110

120

130

140

150

160

170

HYF Monthly Returns (In %) HYF Post Tax Returns Inflation + 3%

160.25

150.93

Overview

Investment Objective

Unifi High Yield AIF is a discretionary fund focusing on event arbitrage and structured investment opportunities across

multiple asset classes with an objective to generate absolute returns of 15% p.a with a standard deviation of 12% or less.

The endeavor is to consistently generate superior compounded annual returns than conventional fixed income

instruments with uncompromising emphasis on capital preservation.

Unifi Capital Pvt. Ltd. Fund Manager

Min Investment INR 1 crore

Performance Reporting

Monthly NAV & Quarterly Review

Independent Custodian & Accountant

IL&FS Securities Services Ltd

Lock in period None

Tenure Open ended; Monthly subscription and redemption

Fees 1% per annum fixed and 20% performance over hurdle rate (Monthly Chargeable)

Valuation S&P CRISIL

Launch Date 04-Apr-2013.

AUM (INR Crs) INR 518 crores

Hurdle Rate Non cumulative pre tax return of 10% per annum

Setup Fees None

Investment Allocation Approach

Rise

Fall

Unifi AIF’s core investment strategy is

to exploit corporate event arbitrage

opportunities that inherently have

limited correlation to economic cycles

and market volatility. In the debt

segment, the focus is on high yield

opportunities with an accrual mindset

besides tax efficiency.

Event Arbitrage

Nominal Bonds

High Yield Bonds

Select Equities

Event Arbitrage

High Yield Bonds

Select Equities

Event Arbitrage

Floating rate notes

Gold ETFs

Event Arbitrage - 100% acceptance

Nominal Bonds

Change in Economic Growth Rate Expectations

Change in Inflation Expectations

Rise

Fall

Rise Fall

Rise

Fall

-5.0

-

5.0

10.0

15.0

19

95

19

96

19

97

19

98

19

99

200

0 2

001

2

002

2

003

2

004

2

005

2

006

2

007

2

008

2

009

2

010

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Real GDP WPI Inflation

Investment Allocation

Strategies Instruments Indicative Allocation

Avg Allocation FY 2018

Avg Allocation FY 2017

Avg Allocation FY 2016

Event Arbitrage

Arbitrage opportunities in Listed Equities arising from open offers, delisting, mergers & de-mergers, IPOs, Cash-Futures

0 – 100% 21% 26.2% 16%

Nominal Bonds Conventional AAA & AA bonds of various Indian Companies – Typically HTM

0 – 50% 26% 23% 22%

Structured & High yield Debt

Structured Secured Corporate Debt, Commercial Papers, short term bonds and tax efficient Preference Shares of NBFCs focusing on Housing, SME , CV, Agri and Micro Finance.

0 – 75% 46% 46.3% 53%

Directional Calls Equity, G-Secs and AAA debt (duration calls)

0 – 10% 1% 1.8% 2%

Cash / Liquid For liquidity purposes/ temporary parking of funds.

6% 2.7% 7%

Investment Strategy

• Emerge from corporate events like acquisition, buyback regulation triggered / voluntary open offers made to the public by controlling shareholders, company delisting, merger of two listed companies etc.

• The risk- return pay-off in most of such deals is deal-specific and has limited correlation to market cycles.

• Emerge in such cases due to the perceived discount in the pre-event market price in relation to the open offer / post-event price, occurring largely due to asymmetric information distribution, difference in investment objectives and expectation amongst investors

Event Arbitrage opportunities

• Also emerge across asset classes including

• Conventional Debt (Wholesale-Retail Arbitrage; Subsidiary-Holding Company Arbitrage)

• Structured High Yield Debt issuances collateralized with home loan, auto loan, micro finance receivables etc (Asset Liability Management Arbitrage in Alternative NBFCs )

Debt Arbitrage opportunities

Unifi Event Arbitrage - Track Record

15+ Years

150+ investments (Out of 200+ opportunities reviewed)

1500+ crores deployed successfully

~ 15% CAGR returns with a standard deviation of ~ 7% (Adjusted for Cash)

Synopsis of past performance

Total no. of deals till Mar 2018

188

Profitable deals 165

Average returns per deal

6%

Average tenure of deals

3 - 4 months

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

0 20 40 60 80 100 120 140 160 180

% R

etu

rns

Sequential Event Arbitrage Deals

Event Arbitrage

In a typical open offer, the price movement during the period between public announcement and the offer closure is largely insulated from market volatility and delivers a debt like absolute return.

Particulars FY18 FY17 FY16 FY15 FY14 FY13 FY12

Total no. of offers

45 51 73 60 60 74 71

No. of offers participated

1 2 7 9 12 16 11

Average offer size (in crs)

70 186 161 287 3941 523 288

Largest Offer invested (in crs)

0.91 415 1621 11449 29200 5222 931

Smallest Offer invested (in crs)

0.91 115 26 251 30 40 27

175

185

195

205

215

225

0

10000

20000

30000

40000

14/07/2015 14/08/2015 14/09/2015 14/10/2015 14/11/2015 14/12/2015

Shar

e P

rice

Vo

lum

e (i

n 0

0's

)

IIFL Open Offer

Volumes (in 00's) Share Price

Similar to Debt Returns

PA Date: 14 Jul 2015 Purchase Date: 25 Aug 2015 Purchase Date: 185 Offer Price: 195

Payment Date: 8th Dec 2015 Acceptance: 100% Return: 5.40% Annualized Returns: 18.79%

0

20

40

60

80

100

120

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Historical No of Open Offers

Merger Arbitrage

Case Study – (HCL – Geometric Merger)

HCL-Geometric merger was announced in Apr 2016 wherein for every 43 shares of Geometric, its shareholder would get 10 shares of HCL Tech and 43 preference shares of 3DL PLM (7% redeemable) with a face value of Rs.68 each. We started tracking the spreads and entered into the trade in April 2016 where we reckoned that we could make 14% per annum. We bought shares of Geometric and sold HCL Tech in the futures market. HCL Tech being a highly liquid F&O scrip enabled us to hedge our Geometric exposure completely and lock-in the desired spreads. All the deal related approvals were obtained by Jan 2017 and the spreads had also narrowed to 8% p.a by then. As we had realized the intended holding period return of 14% p.a, we exited the trade during February month just before the record date for share swap and moved into another opportunity with better yield. . Below is the timeline of approvals and respective spreads. Event Date

Annualized return

Merger Announcement date 1-Apr-16 25.22%

Unifi Entered the trade 4-Apr-16 14.97%

NOC approval from exchange 8-Jun-16 13.61%

CCI Approval 21-Aug-16 14.10%

Shareholders approval 4-Oct-16 16.50%

High Court Approval 14-Dec-16 11.55%

Copy of High court approval submitted to exchange 18-Jan-17 12.05% Unifi Exit prior to record date of 15-03-17 28-Feb-17 7.83%

80.00

90.00

100.00

110.00

120.00

130.00

140.00 HCL - Geometric Price Movement

HCL Tech Geometric

Debt Investments – Approach and Strategy

Investment Strategy - The focus would be on opportunities in the AA to Investment Grade

segment to optimize after tax yields while balancing risks. Typically, all debt investments are

made with Hold to Maturity (HTM) mindset but some of it could be traded opportunistically to

maximize capital appreciation or minimize risk. Arbitrage opportunities emerging from the

following possibilities will be actively pursued to enhance the overall portfolio yields.

Wholesale to Retail – Bulk Buying from Bank

Treasuries / Primary Issuances at finer rates and

selling in smaller lots with a mark-up to HNIs /

Private Provident Fund Treasuries.

Aggregator of Retail Lots – Provide the much

needed liquidity channel for retail bond

holders at market yields plus spread.

Subsidiary – Holding Company – Focus on 100%

Subsidiaries whose papers are rated lower than their

highly rated Parent companies but offer an higher

yield.

Tactical Calls - Consider macro-economy

driven opportunities like softening of Yield

Curve (duration play) due to fall in Interest

Rates and conducive Rating Upgrades cycle

resulting in capital gains.

Debt Investments – Approach and Strategy

Structured Papers from Emerging Financial Sectors- Consider high yield opportunities arising from

well-capitalized and professionally managed Alternative NBFCs focusing on

The following criteria is firmly applied for selection of investment opportunities in this segment -

Fundamentally sound and profitable business model

Management with proven track record

Robust process for credit evaluation, security creation, operations control and collections

Presence of seasoned Private Equity investors in the board

Recent round of promoter / private equity infusion strengthening the capital adequacy

Short Term Maturity and being in the top quadrant of the Company’s Liability

Repayment profile thereby placing our exposure in a positive Asset Liability bucket.

Affordable Housing SME Financing

backed by Mortgages

Commercial Vehicles Financing

Micro Financing

Debt Investments – Approach and Strategy

Case Study – (SME Finance) – Capital Float

We invested in a 13.85% interest yielding medium term (2 years) Non-convertible debentures of Bengaluru based Capital Float, an NBFC pursuing SME finance business with the support of fintech. Its current net-worth is about Rs.460 crs and its present AUM is about Rs.617 crs. Run by professional and experienced Management (Ex- Bajaj Finance, Ex-Deutsche Bank) 50+% of the company owned by credible PE and Foreign Institutions – Sequioa, SAIF, Creations Diversified lender base – 9 Banks & NBFCs – successful raising of long term debt Well capitalized NBFC tapping the SME market with innovative products like Cash advances against POS bills, Taxi loans , etc., Comfortable Asset Liability Profile with huge surplus The NCDs were issued to the company to enable it to expand its AUM and leverage its balance sheet. We had put a covenant to limit the leverage at 3x of equity. Subsequent to the NCD issue in Dec 2016, the management was able to expand its AUM and attracted further equity of Rs 293 Cr in Aug 2017.

Rs. in Crore Favourable Asset Liability Profile at the time of Investment - Dec 2016

<30

days

31 - 60

days

61-90

days

91 - 365

days 1 -2 years

2-3

years

> 3

years Total

Total Assets (a)

119.84

21.55

13.88

103.26

58.05

23.58

4.99

345.15

Total Liabilities (b)

37.70

5.44

7.47

47.87

30.96

0.00

215.71

345.15

Mismatch (a-b) 82.14 16.11 6.41 55.39 27.09 23.58 (210.72)

-

Cumulative Mismatch 82.14 98.25 104.66 160.05 187.14 210.72 0

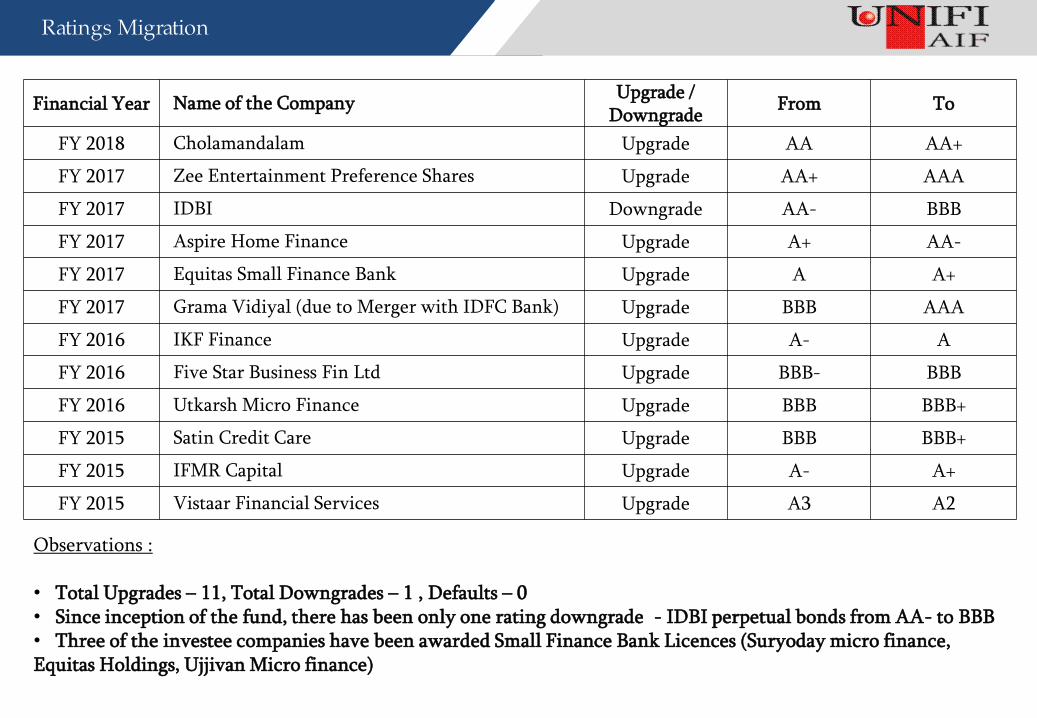

Ratings Migration

Financial Year Name of the Company Upgrade /

Downgrade From To

FY 2018 Cholamandalam Upgrade AA AA+

FY 2017 Zee Entertainment Preference Shares Upgrade AA+ AAA

FY 2017 IDBI Downgrade AA- BBB

FY 2017 Aspire Home Finance Upgrade A+ AA-

FY 2017 Equitas Small Finance Bank Upgrade A A+

FY 2017 Grama Vidiyal (due to Merger with IDFC Bank) Upgrade BBB AAA

FY 2016 IKF Finance Upgrade A- A

FY 2016 Five Star Business Fin Ltd Upgrade BBB- BBB

FY 2016 Utkarsh Micro Finance Upgrade BBB BBB+

FY 2015 Satin Credit Care Upgrade BBB BBB+

FY 2015 IFMR Capital Upgrade A- A+

FY 2015 Vistaar Financial Services Upgrade A3 A2

Observations : • Total Upgrades – 11, Total Downgrades – 1 , Defaults – 0 • Since inception of the fund, there has been only one rating downgrade - IDBI perpetual bonds from AA- to BBB • Three of the investee companies have been awarded Small Finance Bank Licences (Suryoday micro finance, Equitas Holdings, Ujjivan Micro finance)

Latest Holdings – Key Attributes

Average Exposure in May 2018

Event Arbitrage 5.6%

Fixed Income (Debt) 82.6%

Directional Calls 2%

Cash / (Leverage) 9.8%

Debt Quants as on May 2018

Weighted Average Maturity 1.85 Yrs

Carry Yield 11.47%

Ratings Exposure of Fixed Income as on May2018

Rating wise Modified duration

As on May 2018

AAA 1.62 Yrs

AA 1.32 Yrs

A 0.97 Yrs

BBB 1.48 Yrs

Overall Debt 1.25 Yrs

AAA

Rated, 4%

AA Rated,

32%

A Rated,

35%

BBB Rated,

29%

MF &

REIT, 0%

AIF Performance

Monthly Performance in (%)

Year Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Annual

FY14 0.92% 1.56% -0.70% 1.60% 1.02% 0.87% 1.18% 1.07% 2.84% 0.79% 2.20% 0.95% 14.40%

FY15 1.15% 1.43% 1.22% 1.44% 1.13% 1.20% 1.14% 1.36% 1.48% 1.28% 1.38% 1.83% 16.82%

FY16 0.92% 1.14% 0.75% 1.58% 1.26% 0.87% 1.24% 0.82% 1.31% 1.12% 0.59% 2.51% 14.67%

FY17 1.00% 1.14% 0.83% 1.24% 1.10% 1.38% 0.79% 1.28% 0.77% 0.90% 0.80% 1.97% 13.70%

FY18 1.60% 0.32% 1.00% 1.15% 1.42% 2.25% 0.90% 1.40% 0..80% 0.63% 0.81% 1.60% 14.47%

FY19 0.65% 0.31% 0.95%

Returns

UNIFI AIF

Birla Sh. Opp.

Fund(G)

Fran. Corp. Bond

fund(G)

BSL Dynamic

Bond Fund(G)

Reliance Dynamic Bond(G)

Average Monthly Return

1.17% 0.75% 0.79% 0.71% 0.68%

CAGR 14.72% 9.34% 9.88% 8.69% 8.33%

Cumulative Returns 105.38% 58.62% 62.70% 53.83% 51.22%

Largest Monthly Gain 2.84% 2.34% 3.06% 4.85% 4.28%

Largest Monthly Loss -0.70% -1.17% -2.10% -3.63% -3.81%

% of positive Months 98.39% 91.94% 93.55% 75.81% 72.58%

Risk

Standard Deviation (Annualised)

1.83% 2.16% 2.25% 4.74% 4.94%

UNIFI AIF Vs Debt Fund's

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

50

70

90

110

130

150

170

190

210

230 A

pr/

13

May/

13

Jul/13

Sep/1

3

Nov/1

3

Jan/1

4

Mar/

14

May/

14

Jul/14

Sep/1

4

Nov/1

4

Jan/1

5

Mar/

15

May/

15

Jul/15

Sep/1

5

Nov/1

5

Jan/1

6

Mar/

16

May/

16

Jul/16

Sep/1

6

Nov/1

6

Jan/1

7

Mar/

17

May/

17

Jul/17

Sep/1

7

Nov/1

7

Jan/1

8

Mar/

18

May/

18

Month

ly R

etu

rns

Valu

e o

f R

s.1

00 I

nveste

d

Monthly Returns UNIFI AIF Birla Sh. Term Opp. Fund Fran Temp Corp. Bond BSL Dynamic Bond Fund(G) Reliance Dynamic Bond(G)

Investment Allocation & Returns Attribution

Returns Attribution Investment Allocation

16% 11% 16% 26% 21%

71% 84% 75% 69%

72%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Event Arbitrage Fixed Income

Directional Calls Liquid Funds / (Leverage)

5%

2% 2% 4%

5%

9% 14%

11% 9% 6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Event Arbitrage Fixed Income

Directional Calls Liquid Funds / (Leverage)

Investment Process

Idea Origination

Opportunity validation, review and evaluation of risk / return scenarios

Investment Committee Review

Initiation of Investment

Unifi Capital (P) Ltd – Fund Manager to the Trust

Post Investment Monitoring and Risk Management

CIO, Head-Research and Head-Relationship

AIF Trustees

Internal Review

Statutory Auditors

Portfolio Parameters

Pre-trade

Ongoing Surveillance

Post-trade Firm Infrastructure

In-depth bottom-up review of all investment

opportunities by documented and well

seasoned evaluation process

Sensible Exposure Limits:

- Theme Specific

- Company Specific (not more than 10%)

‘Marketable Liquidity’ Assessment

Rigorous due-diligence on structure and

security w.r.t debt investment opportunities

Maximum Leverage limit including

derivative exposures capped at 1.5 times the

fund corpus

Daily Mark-to-Market assessment including

detailed review of extreme movements

Real-time monitoring of economic developments,

corporate communications to stock exchanges and

methodical tracking of economy and company

specific developments

Periodical meeting / calls with management of all

the investment companies to measure progress,

review results and revalidate assumptions

Opportunistic hedging/tactical trading to respond

to short-term, counter-theme market moves

Best-in-class IT infrastructure with

back-up

Documented Process Flow

Reputed Trustees, Custodian, Valuer

etc

Research Access to premium

databases capturing economic, sector

and company specific trends

Periodical Internal Review and

Statutory Audit

Risk Management Framework

Why Unifi High Yield Fund

• Successful 5 year performance record of Unifi High Yield Fund

• Stable and Experienced Investment Management Team that co-founded

the company in 2001

• Focus on result oriented unique investment themes; even willing to

sacrifice scale (AUM growth) in favor of desired risk adjusted returns

• Scope for consistent compound returns with low volatility

• Robust risk management and operational risk controls

P . S . - The Power of Compounding

The power of compounding is the eight wonder of the world – Einstein. A portfolio with consistent above average compounded returns over years creates more wealth than a one offering high returns at a higher volatility. See the example below – Even one bad year in a 5 yr time period could significantly bring down the returns and dilute the power of compounding.

Year 1 Year 2 Year 3 Year 4 Year 5

Portfolio A 100 18% 16% 17% 19% 15%

219

Portfolio B 100 40% 27% -38% 24% 22%

167

For further information visit:

www.unificap.com

CHENNAI: 11, Kakani Towers 15 Khader Nawaz Khan Road Nungambakkam High Road Chennai - 600 006. INDIA Ph: +91-44-3022 4466 +91-44-2833 1556 Fax: +91-44-2833 2732

BANGALORE: 511, Barton Centre 84, M.G. Road Bangalore - 560 001. INDIA Ph: +91-80-255 9418/19

HYDERABAD: H No. 6-3-346/1, Road No. 1 Banjara Hills Scotia Bank Building Hyderabad – 500 034. INDIA Ph: +91-40-6675 2622/23

MUMBAI: Shiv Sagar Estate, A Block, 8th Floor, Dr. Annie Besant Road, Worli, Mumbai – 400018. Ph: +91-22-24927671 +91-22-24925319 Fax: +91-22-24950580

Thank You

DELHI: No.818, International Trade Tower, Nehru Place , Delhi – 110 019. Ph: +91-8800333799