Understanding Options

35

Understanding Options Alddon Christner C. Ang Basfin2 Source: BMA

-

Upload

arja-kitane -

Category

Documents

-

view

14 -

download

0

description

Basfin 2

Transcript of Understanding Options

Understanding OptionsAlddon Christner C. Ang

Basfin2

Source: BMA

Outline

Calls, Puts and Shares

Financial Alchemy with Options

What Determines Option Values?

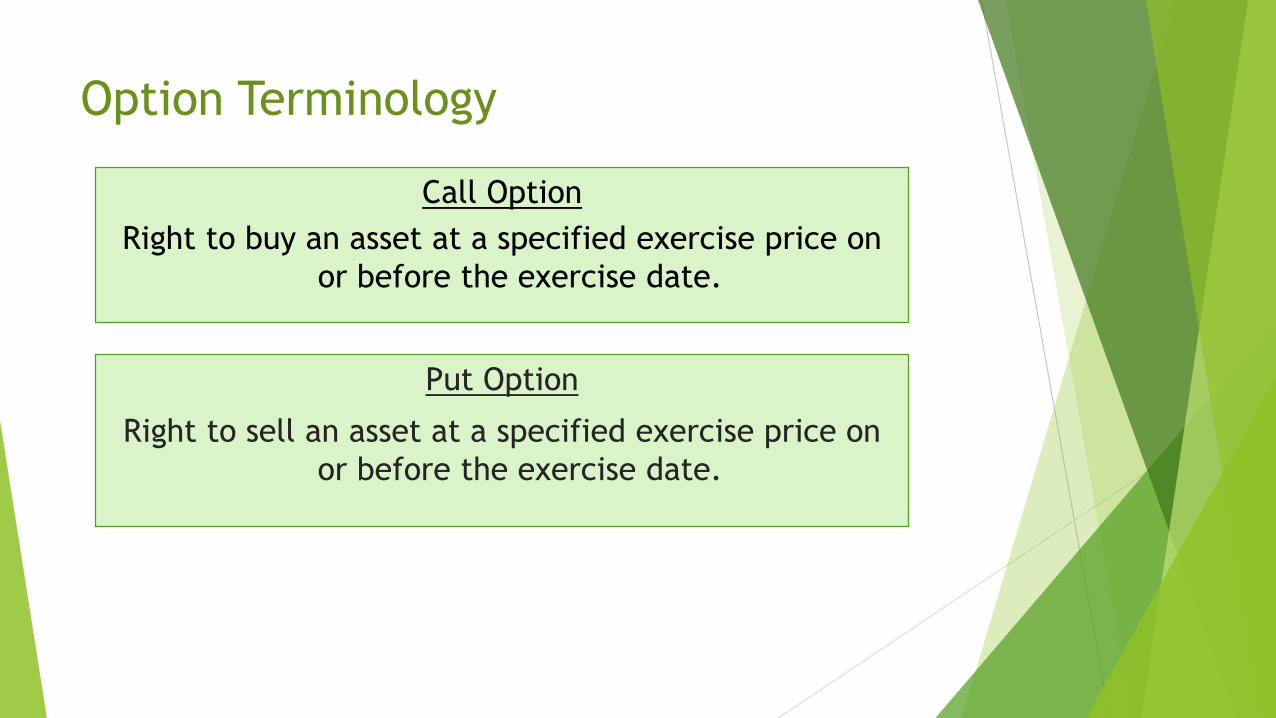

Option Terminology

Put Option

Right to sell an asset at a specified exercise price on

or before the exercise date.

Call Option

Right to buy an asset at a specified exercise price on

or before the exercise date.

Option Obligations

assetbuy toObligationasset sell Right tooptionPut

asset sell toObligationassetbuy Right tooption Call

ShortLong

Buyer/

Holder

Seller/

Writer

Right to buy

Obligation to sell

Buyer/

Holder

Seller/

Writer

Right to sell

Obligation to buy

Call option

Put option

Option Terminology

Derivatives - Any financial instrument that is derived from another. (e.g.. options, warrants, futures, swaps, etc.)

Option - Gives the holder the right to buy or sell a security at a specified price during a specified period of time.

Call Option - The right to buy a security at a specified price within a specified time.

Put Option - The right to sell a security at a specified price within a specified time.

Option Premium - The price paid for the option, above the price of the underlying security.

Intrinsic Value - Difference between the strike price and the stock price

Option Terminology

Time Premium - Value of option above the intrinsic value

Exercise Price - (Striking Price) The price at which you

buy or sell the security.

Expiration Date - The last date on which the option can

be exercised.

American Option - Can be exercised at any time prior to

and including the expiration date.

European Option - Can be exercised only on the

expiration date.

Example

A call option to buy five thousand shares of ABC Co. stocks

at PHP 80 per share at the end of six months. The option

price is PHP 1,000.

3 1

2

5

4

The financial variable from which the derivative derives its

value

The stated price for which an underlying may be purchased

or sold

The quantity of the underlying to which the contract

applies

(1)

Underlying

(2)

Exercise Price

(3)

Notional Amount

Example

A call option to buy five thousand shares of ABC Co. stocks

at PHP 80 per share at the end of six months. The option

price is PHP 1,000.

3 1

2

5

4

The maturity date, which gives rise to the notion of an

option’s time to expiration

Also known as option price, which is the money paid

when the option contract is initiated

(4)

Expiration Date

(5)

Option Premium

Option Terminology

American Option - Can be exercised at any time prior to

and including the expiration date.

European Option - Can be exercised only on the

expiration date.

Grant date

Grant date

Expiry date

Expiry date

Exercise only on this date

Exercise anytime before expiry

Option Value

The value of an option at expiration is a function of the

stock price and the exercise price.

Example - Option values given a exercise price of $80

00001020ValuePut

302010000Value Call

110100908070$60PriceStock

Moneyness of an Option

In the future, the option buyer will find it beneficial to

Exercise the option when its payoff is positive, i.e. the

option is in-the-money

Not exercise the option when its payoff is nil, i.e. the

option is at-the-money or out-of-the-money

Possible Outcomes

Market > Exercise Market = Exercise Market < Exercise

Call Option In-the-money At-the-money Out-of-the-money

Put Option Out-of-the-money At-the-money In-the-money

Example

Selected

prices for puts

and calls of

Google Shares

September

2008

Option Value

Google Call option value (of buyer) given a $430 exercise

price.

Share Price

Call o

pti

on v

alu

e

$430

$430

Option Value

Google Put option value (of buyer) given a $430 exercise

price.

Share Price

Put

opti

on v

alu

e

$430

$430

Option Value

Google Call option payoff (to seller) given a $430 exercise

price.

Share Price

Call o

pti

on p

ayoff

$430

$430

Option Value

Google Put option payoff (to seller) given a $430 exercise

price.

Share Price

Put

opti

on p

ayoff

$430

$430

Option Value

Call buyer profit – assume strike of $430 and option price

of $54.35

Share Price

Posi

tion V

alu

e

430 484.35

-54.35

Break even

Option Value

Put seller profit – assume strike of $430 and option price

of $48.55

Share Price

Posi

tion V

alu

e

Short put

381.45 430

+48.55

Break even

Option Value

Masochists Strategy?- Long stock and short call

Share Price

Posi

tion V

alu

e

Short Call

Long Stock

“Silly Strategy”

Option Value

Protective Put - Long stock and long put

Share Price

Posi

tion V

alu

e Protective Put

Long Put

Long Stock

Option Value

Straddle - Long call and long put

Strategy for profiting from high volatility

Share Price

Posi

tion V

alu

e

Straddle

Long put Long call

Financial Alchemy

Financial Alchemy

Financial Alchemy

Financial Alchemy

Financial Alchemy

Components of Option Price

1. Underlying stock price = Ps

2. Striking or Exercise price = S

3. Volatility of the stock returns (standard deviation of

annual returns) = v

4. Time to option expiration = t = days/365

5. Time value of money (discount rate) = r

6. PV of Dividends = D = (div)e-rt

Components of Option Price

For a call, intrinsic value is the greater of nil and the

excess of market price over exercise price

For a put, intrinsic value is the greater of nil and the

excess of exercise price over the market price

𝐶 = max(𝑃𝑆 − 𝑆, 0)

𝑃 = max(𝑆 − 𝑃𝑆, 0)

The component of an option’s market value that

can be realized by exercising the option

immediately

Intrinsic Value

Components of Option Price

Expiry date

European options: As time to maturity increases, both a call and put

option increases in value

Expiry dateDividend payment

American options: Generally similar to European options. However, if a

dividend payment takes place, which decreases the value of a stock, the

call option decreases in value and the put option increases in value.

Time Decay Chart

Option prices decline, ceteris paribus, when the time to

expiration declines.

Option

Price

Stock Price

90 days to

expiration 60 days to

expiration

30 days to

expiration

Components of Option Price

Theoretically, increasing the risk-free interest rates

(which normally serves as the discount rate) leads to an

increase in the expected return required by stock

investors. The present value of future cash flows received

by the holder of the option decreases.

Call Option

Current

Stock

Price

Strike

Price

Put OptionStrike

Price

Current

Stock

Price

Components of Option Price

The greater the distribution

of possible outcomes,

relative to the final price of

the stock, the higher the

value of the option. This is

due to the greater potential

for profit. Thus, Y will have

a higher option price, ceteris

paribus.

Components of Option Price

Similar to time decay, the value of an option will be

higher when more volatility exists.

Summary

*For American options, could be increasing or decreasing

These are considered as “fundamental” in the sense that as long as investors are presumed to take advantage of arbitrage opportunities, these variables must matter.

Determining FactorsEffect of increase on:

Call Value Put Value

1. Current asset price Increase Decrease

2. Strike price Decrease Increase

3. Stock price volatility Increase Increase

4. Risk-free interest rate Increase Decrease

5. Term to expiration Increase* Increase*

6. Expected dividends Decrease Increase

Which would you prefer?