Chapter 12 Money and Financial Institutions Section 12.1 Money and Banking.

Upload

clare-austinCategory

view

231download

0

Understanding MoneyUnderstanding Moneyand Financial Institutionsand Financial Institutions

Understanding MoneyUnderstanding Moneyand Financial Institutionsand Financial Institutions

Chapter 20

Chapter 2Chapter 200 Learning Goals Learning Goals

1.1. WWhat is money, what are its characteristics and functions, and what are the three parts of the U.S. money supply?

2.2. WWhat are the basic functions of the Federal Reserve System, and what tools does it use to manage the money supply?

3.3. WWhat are the key financial institutions, and what role do they play in the process of financial intermediation?

Chapter 2Chapter 200 Learning Goals Learning Goals (cont’d.)(cont’d.)

4.4. HHow does the Federal Deposit Insurance Corporation protect depositors’ funds?

5.5. WWhat role do U.S. banks play in the international marketplace?

6.6. WWhat trends are reshaping the banking industry?

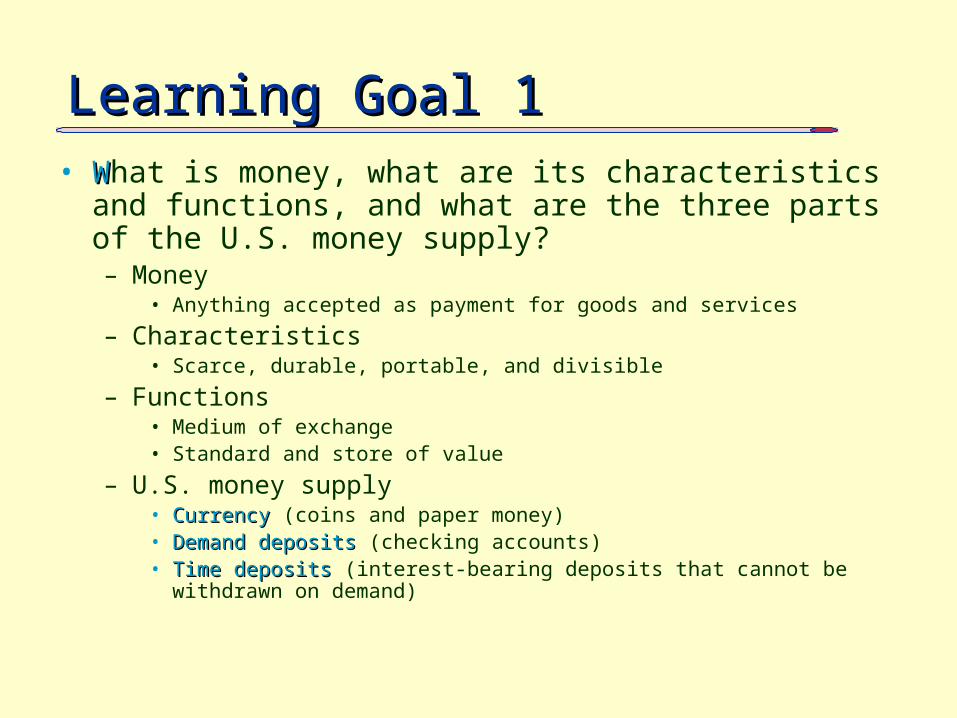

Learning Goal 1Learning Goal 1• WWhat is money, what are its characteristics and

functions, and what are the three parts of the U.S. money supply?– Money

• Anything accepted as payment for goods and services

– Characteristics• Scarce, durable, portable, and divisible

– Functions• Medium of exchange• Standard and store of value

– U.S. money supply• Currency Currency (coins and paper money)• Demand depositsDemand deposits (checking accounts)• Time depositsTime deposits (interest-bearing deposits that cannot be withdrawn on

demand)

MoneyMoney::

Anything that is acceptable as payment for goods and services

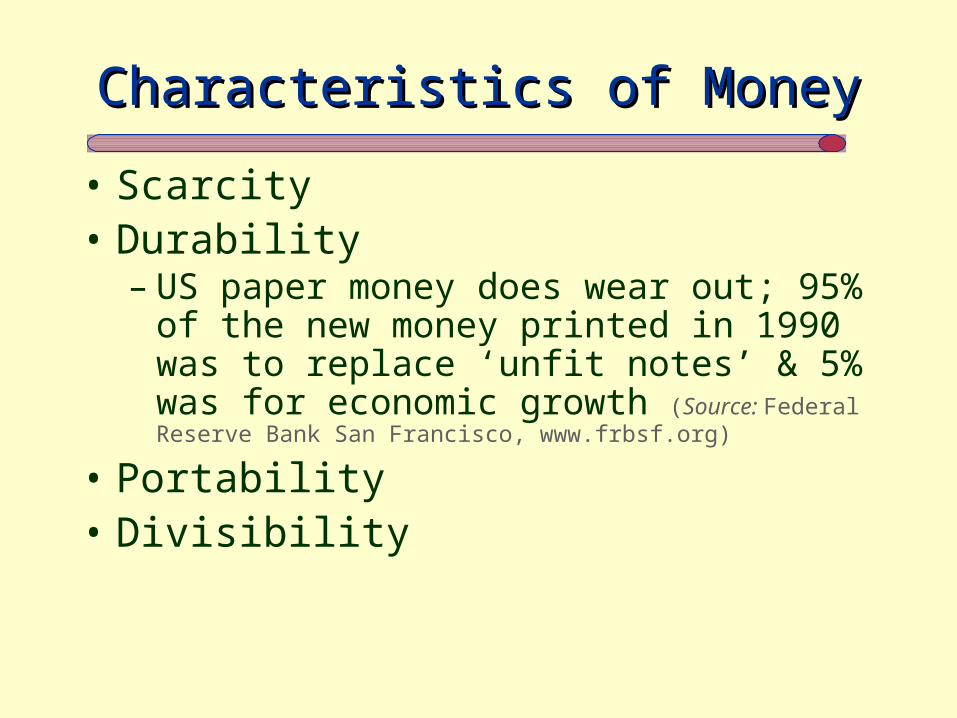

Characteristics of MoneyCharacteristics of Money

• Scarcity• Durability

– US paper money does wear out; 95% of the new money printed in 1990 was to replace ‘unfit notes’ & 5% was for economic growth (Source: Federal Reserve Bank San Francisco, www.frbsf.org)

• Portability• Divisibility

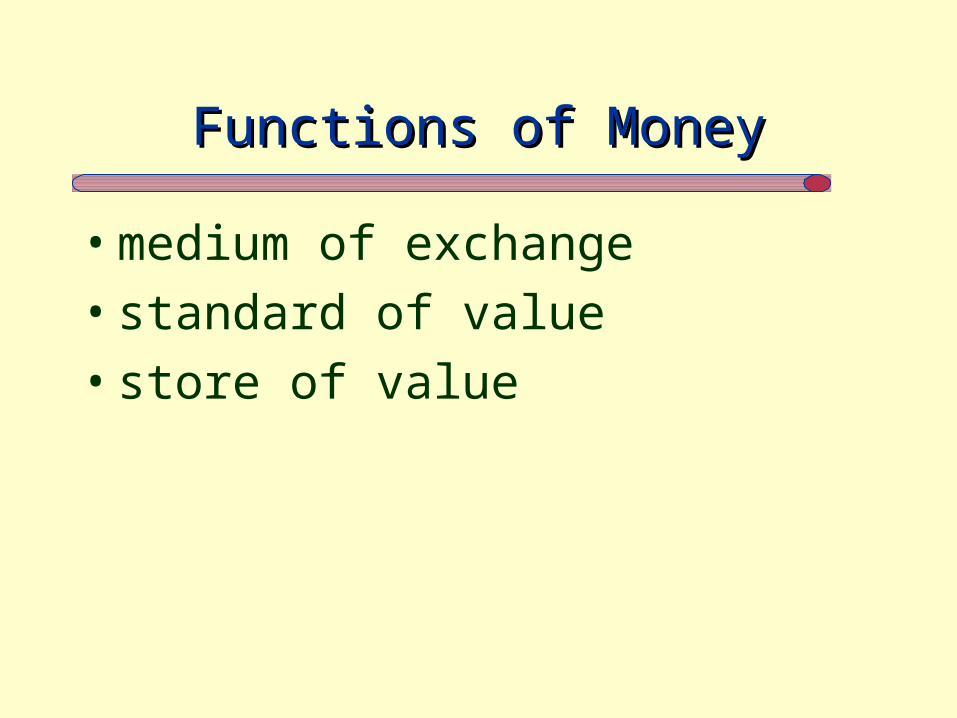

Functions of MoneyFunctions of Money

• medium of exchange

• standard of value

• store of value

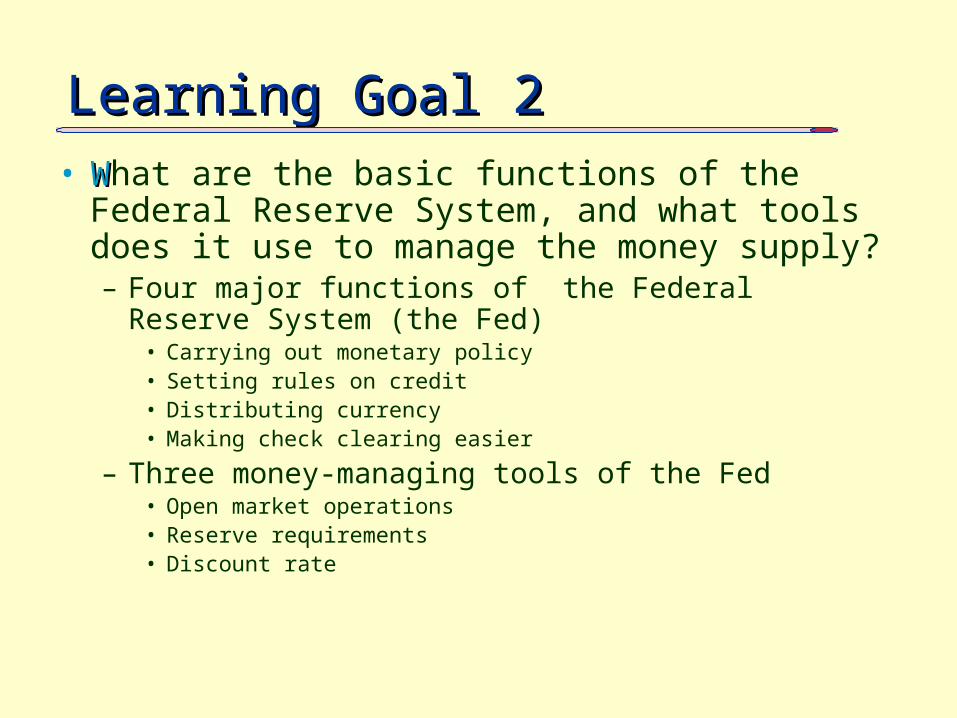

Learning Goal Learning Goal 22• WWhat are the basic functions of the Federal

Reserve System, and what tools does it use to manage the money supply?– Four major functions of the Federal Reserve System

(the Fed)• Carrying out monetary policy• Setting rules on credit• Distributing currency• Making check clearing easier

– Three money-managing tools of the Fed• Open market operations• Reserve requirements• Discount rate

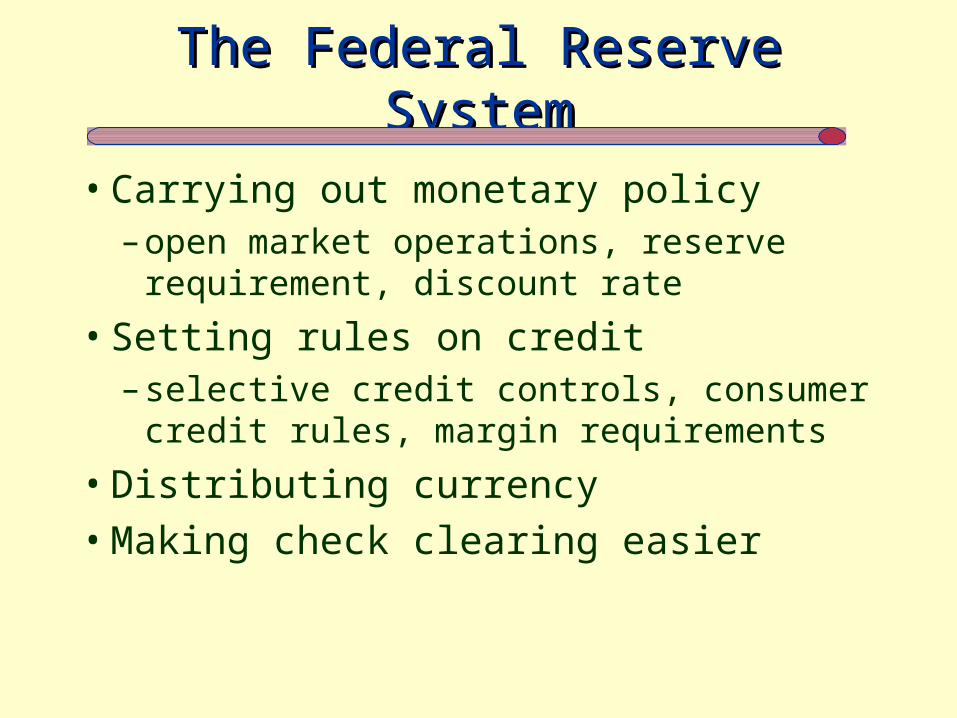

The Federal Reserve SystemThe Federal Reserve System

• Carrying out monetary policy– open market operations, reserve

requirement, discount rate

• Setting rules on credit– selective credit controls, consumer credit

rules, margin requirements

• Distributing currency

• Making check clearing easier

Distributing CurrencyDistributing Currency

• $150 billion$150 billion in cash typically exists at the Federal Reserve & at banks

• Anticipating a high demand for cash prior to Y2K, the Federal Reserve printed an extra $70 billionextra $70 billion– the extra money was distributed to banks– this was enough for every US citizen

(including children) to have $255

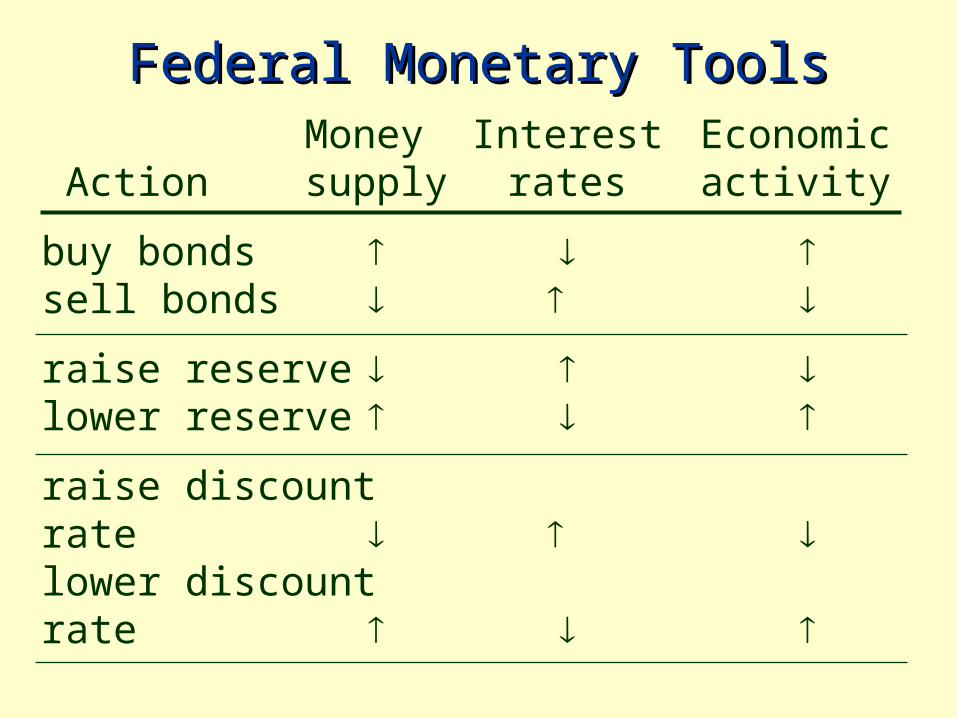

Federal Monetary ToolsFederal Monetary ToolsMoney Interest Economic

Action supply rates activity

buy bonds sell bonds

raise reserve lower reserve

raise discountrate lower discountrate

Financial Intermediation ProcessFinancial Intermediation Process

Demanders of funds: businesses, governments

Financial intermediaries: banks,life insurance companies, pension funds

Suppliers of funds: households

$$

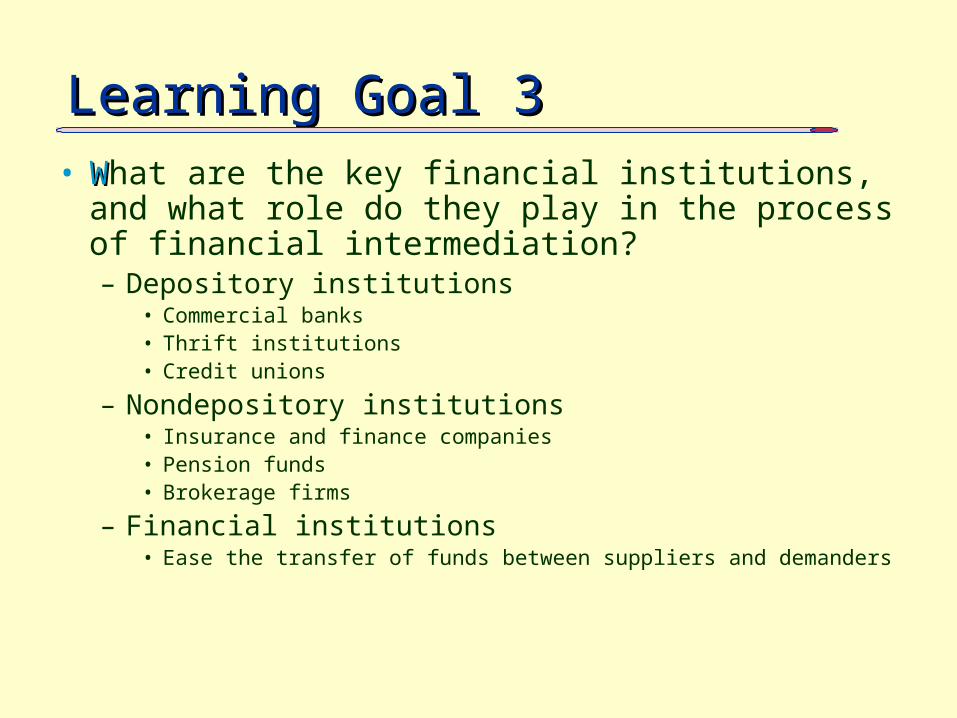

Learning Goal 3Learning Goal 3• WWhat are the key financial institutions, and what

role do they play in the process of financial intermediation?– Depository institutions

• Commercial banks• Thrift institutions• Credit unions

– Nondepository institutions• Insurance and finance companies• Pension funds• Brokerage firms

– Financial institutions• Ease the transfer of funds between suppliers and demanders

The US Financial SystemThe US Financial System

• Depository financial institutions– commercial banks, thrift institutions,

credit unions

• Nondepository financial institutions– insurance companies, pension funds,

brokerage firms, finance companies

Learning Goal 4Learning Goal 4

• HHow does the Federal Deposit Insurance Corporation protect depositors’ funds?– Federal Deposit Insurance Corporation

(FDIC) • Insures deposits in commercial banks through

the Bank Insurance Fund• Deposits in thrift institutions through the Savings

Association Insurance Fund• Sets banking policies and practices• Reviews banks annually to ensure that they

operate fairly and profitably

Insuring Bank DepositsInsuring Bank Deposits

• Federal Deposit Insurance Corporation (FDIC)– protection for bank failure– insures deposits up to $100,000 per

account– backed by the credit of the US government– all banks in the Federal Reserve must

have insurance

Learning Goal Learning Goal 55

• WWhat role do U.S. banks play in the international marketplace?– U.S. banks

• Provide loans and trade-related services to– Foreign governments– Foreign businesses

• Offer specialized services– Cash management– Foreign currency exchange

International BankingInternational Banking

• Some countries do not allow US banks to enter

• Foreign banks have fewer regulations

• International banking is high-risk

• US banks provide loans to foreign governments and businesses

International BankingInternational Banking

Top 5 Global Banks:

1.1. Deutsche Bank (Germany)

2. 2. Sanwa Bank (Japan)

3. 3. Sumitomo (Japan)

4. 4. Dai-Ichi Kangyo (Japan)

5. 5. Fuji (Japan)

Source: Corporate Finance Network, corpfinet.com

Learning Goal 6Learning Goal 6

• WWhat trends are reshaping the banking industry?– Banks are delivering more online services– Bank mergers and acquisitions are:

• Consolidating the banking industry• Helping banks to improve their operating efficiency• Reducing costs• Extending their geographic reach

– Passage of bank reform legislation• Allows banks to market securities and insurance products• Helps banks compete with nondepository institutions

Trends in BankingTrends in Banking

Online banking

Consolidation one expert predicts that 12 finance

companies will hold 85% of the world’s private-sector financial assets by 2020 (Source: Eugene Ludwig in The Arizona Republic, Jan. 3, 2000, p. D1)

Trends in BankingTrends in Banking

Integration of banking, brokerage, & insurance services– Congress passed the Gramm-Leach-Bliley

Act of 1999 allowing companies in these areas to offer each other’s services

– The legislation is expected to lead to healthy competition & lower prices for consumers (Source: Georgia Bankers Association, www.gabankers.com)

– This will likely lead to cross-industry mergers (Source: The Arizona Republic, Jan. 3, 2000, p. D1)