UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

of 21

-

Upload

nc-policy-watch -

Category

Documents

-

view

217 -

download

0

Transcript of UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

1/21

Economic Impact of Proposed Tax Reductionsin North Carolina

Prepared by:

G. Jason Jolley, Ph .D. , E. Brent Lane, & Aaron Nousaine 1

UNC Center for Competitive Economies (C 3E),

Kenan Institute/Kenan-Flagler Business School

UNC-Chapel Hill

April 15, 2011

Ab stract

The North Carolina G eneral Assembly asked the UNC Center for Competitive Economies (C 3E) to assist inestimating the economic impacts of reduced taxation in North Carolina . Specifically, C3E was asked toestimate the employment effects of the following tax policy changes:

y Expiration of the 1-cent sales taxy Expiration of personal and corporate income surtaxesy R eduction in the corporate tax rate effective tax year 2012y R eduction in business income taxes for S-corporation, limited liability corporations

(LLCs), and sole proprietorships, including exemption of the first $50,000 in non-passivebusiness income from taxation .

The cumulative impacts for fiscal year 2011-2012 and fiscal year 2012-2013 are represented below . Theinitial tax changes will result in a total of $1 .8 billion in increased industry output, $564 million in laborincome, and the creation of 16,0 8 3 new jobs at an average wage of $35,0 8 2. Once the tax reductionimpacts are fully realized in fiscal year 2012-2013, the total industry output will increase to $2 .3 billionand labor income will increase to nearly $700 million . A total of 19,439 new jobs are projected (16,0 8 3in the FY 2011-12 and an additional 3,356 in FY 2012-2013) at an average wage of $35,969 .

S ummary of Cumulative Impacts, FY 2012-2013

Direct Indirect Induced Total MultiplierIndustry Output $1,365,3 8 4,000 $409,765,000 $534,073,000 $2,309,220,000 1 .69Employment 11,65 8 2,917 4, 8 64 19,439 1 .67Lab or Income $405,964,000 $126,599,000 $166,627,000 $699,1 8 9,000 1 .72

Ave. Income Per Jo b $35,969Note: Totals may not sum due to rounding

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

2/21

SECTI ON I:

ECONOMIC IMPACT ANALYSIS METH OD OLOG Y The North Carolina G eneral Assembly asked the UNC Center for Competitive Economies (C 3E) to assist inestimating the economic impacts of reduced taxation in North Carolina . Specifically, C3E was asked toestimate the employment effects of the following tax policy changes:

y Expiration of the 1-cent sales taxy Expiration of personal and corporate income surtaxesy R

eduction in the corporate tax rate effective tax year 2012y R eduction in business income taxes for S-corporation, limited liability corporations

(LLCs), and sole proprietorships, including exemption of the first $50,000 in non-passivebusiness income from taxation .

The North Carolina G eneral Assembly s Fiscal R esearch D ivision provided estimates of the tax savings foreach of these reductions as follows in table 1:

Tab le 1: Prospective Tax Changes

FY2011-2012 FY2012-2013

Expiration of the 1-cent sales tax $1,124,330,000 $1,137,970,000

Expiration of personal income surtaxes: $172,100,00 $174,200,000

Expiration of corporate income surtaxes: $29,000,000 $29,300,000

R eduction in the corporate tax rate effective tax year 2012: $135,000,000 $30 8 ,500,000

R eduction in business income taxes for S-corporation, limitedliability corporations (LLCs), and sole proprietorships, includingexemption of the first $50,000 in non-passive business incomefrom taxation:

$131,600,000 $336,400,000

T

otal: $1,592,030,000 $1,98

6,330,000Note: Totals may not sum due to rounding

C3E calculated the estimated direct, indirect, and induced impacts of these tax reductions, using IMPLANProfessional software 2. IMPLAN is an input-output modeling program that permits researchers toestimate the projected effects of an exogenous increase in demand, such as an infusion of tax reductionmonies in a specified geographic region such as North Carolina

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

3/21

y Indirect effects include the impacts on all local industries resulting from industries purchasingfrom industries in multiple iterations as a consequence of this increase in final demand .

y Induced effects are the increases in spending by households resulting from the increases in incomeand population that were caused by both the direct and indirect effects . The total effect of the newinvestments from the proposed projects is represented by the sum of all three effects - direct,indirect and induced .

T ime and data limitations do not allow the researchers to conduct a true counterfactual analysis . Thisdocument provides a rough estimation of the economic impacts of tax reduction given the availabledata, assumptions, and limitations outlined in this analysis . No assumptions are made about the public

sector impacts of having reduced tax revenues, which may limit the net effects of the benefits outlinedhere .

Sales Tax Expiration Models:

IMPLAN 2.0 software allows researchers to estimate the economic effects of a change in income acrossmultiple household income categories . IMPLAN estimates how the change in income would impact theeconomy based on the average spending patterns of households in the specified income range . R educing the state sales tax would have an impact on both businesses and households in North Carolina . To simplify the analysis, C 3E assumes that 100% of the benefits of sales tax reduction will accrue tohouseholds and models that effect . C3E utilizes the October 2010 Consumer Expenditure Survey fromthe U . S. Bureau of Labor Statistics (BLS) to estimate the percentage of retail sales for each householdincome category . BLS s survey is based on consumer units which roughly approximate households inaverage size and income characteristics . The specified income levels for these consumer units do notprecisely match the IMPLAN categories, so the researchers estimated down based on the lowerincome ranges in North Carolina relative to the U .S. average .

For example, input data for the income range of $50,000 to $75,000 in the IMPLAN model was derivedusing the BLS income categories $50,000-$69,999 and $70,000-$79,999 . Based on the percentage of retail sales that occur in each income category, the researchers approximate the household incomelevels where the benefits of a sales tax reduction are likely to occur . This additional revenue for eachcategory of household income also serves as the input for that income category in the IMPLAN model . Table 2 demonstrates that total tax savings does accrue to higher income households, since thesehouseholds typically spend more money on retail sales . Many scholars regard the sales tax as regressivebecause lower income households pay a disproportionately higher percentage of their disposal incomeon items subject to a sales tax . For this reason, there may be additional benefits from a reduced salestax that accrue to lower income North Carolinians that is beyond the scope of this economic model .

IMPLAN models the traditional basket or mix of goods that households spend money on in eachhousehold income bracket . This allows a prediction of the economic impacts across multiple sectors,which are then aggregated to determine the total effect of this spending

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

4/21

Tab le 2: S ales Tax Reduction Model

HouseholdIncome Category

BLS Estimates of Total Consumer

S pending(in Thousands)

Percentage of BL S Estimates of Total

Retail S pending

FY2011-12

Percentage of AdditionalRevenue toHousehold

Category from1% NC S ales Tax

Reduction

FY2012-13

Percentage of AdditionalRevenue toHousehold

Category from1% NC S ales Tax

Reduction$150K $1,050,012,7 8 2 18 % $199,293,304 $201,711,064Total $5,923,735,769 100% $1,124,330,000 $1,137,970,000

Source: October 2010 Consumer Expenditure Survey from the U .S. Bureau of Labor Statistics (BLS) andSales tax reduction savings estimates provided by D ivision of Fiscal R esearch, N .C. G eneral Assembly . Note: Totals may not sum due to rounding

Personal Income Surtax Expiration Models:

The State of North Carolina imposes 2-3% surtaxes on personal income for certain taxpayers . For thosemarried filing jointly the applicable percentage is 2% for taxable income greater than $100,000 but

less than $250,000 and 3% for those with taxable income greater than $250,000 . The level of surtax (if any) is dependent on filing status and North Carolina taxable income as outlined in table 3 .

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

5/21

Tab le 3: S urtax Percentage Ta b le

If Filing S tatus isAnd NC Taxa b le Income on Line 13,

Form D-400 isThe Applica b lePercentage is

Married FilingJointly/Qualifying Widow(er)

G reater than $100,000 but does notexceed $250,000

2%

G reater than $250,000 3%

H ead of H ouseholdG reater than $ 8 0,000 but does notexceed $200,000

2%

G reater than $200,000 3%

Single

G reater than $60,000 but does notexceed $150,000

2%

G reater than $150,000 3%

Married Filing Separately

G reater than $50,000 but does notexceed $125,000

2%

G reater than $125,000 3%

Source: North Carolina D epartment of R evenue, http://www .dornc . com/taxes/individual/surtax .html

The IMPLAN model is based on household income prior to any deductions and not taxable householdincome after standard/itemized deductions are taken . It is assumed that only a small percentage of individuals with household income in the range of $75,000 to $100,000 will have taxable incomes in theranges impacted by this surtax expiration . Estimations of the effects of this reduction are apportionedand modeled as follows in table 4 .

Tab le 4: A llocation of Personal Income S urtax ExpirationHousehold

IncomePercentage of Total

Benefiting from PersonalIncome Surtax Expiration

FY2011-2012 A dditionalRevenue from Personal

Income S urtax Expiration

FY2012-2013 AdditionalRevenue from Personal

Income S urtax Expiration$75-$100K 10% $17,210,69 8 $17,419,577

$100k-$150k 40% $6 8 ,8 42,791 $69,67 8 ,228 >$150K 50% $ 8 6,053,4 88 $8 7,097,7 8 5

Total 100% $172,100,000 $174,200,000Source: T otal savings estimates provided by D ivision of Fiscal R esearch, N .C. G eneral AssemblyN T l d di

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

6/21

Tab le 5: A llocation of Personal Income Surtax Expiration (sensitivity analysis)

HouseholdIncome

Percentage of TotalBenefiting from PersonalIncome Surtax Expiration

FY2011-2012 A dditionalRevenue from Personal

Income S urtax Expiration

FY2012-2013 AdditionalRevenue from Personal

Income S urtax Expiration$75-$100K 5% $ 8 ,605,349 $ 8 ,709,779

$100k-$150k 35% $60,237,442 $60,96 8 ,450>$150K 60% $103,264,1 8 6 $104,517,342

Total 100% $172,100,000 $174,200,000Source: T otal savings estimates provided by D ivision of Fiscal R esearch, N .C. G eneral Assembly

Note: Totals may not sum due to rounding

Corporate Income Surtax Expiration, Lower Corporate Income Tax, and LowerBusiness Income Tax Models:

The North Carolina G eneral Assembly Fiscal R esearch D ivision provided estimates of the savings totaxpayers based on three additional, prospective changes to the tax code . These include 1) expiration of the corporate income surtax, 2) lowering the corporate income tax rate to 4 . 9% (down from 6 .5%) in taxyear 2012, and lowering business income taxes for S-corporations, limited liability corporations (LLCs),and sole proprietorships by exempting the first $50,000 of non-passive business income .

It is challenging to precisely and accurately model the economic effects of such changes given the timeand resource constraints . H owever, the researchers can roughly approximate the benefits of suchchanges using the IMPLAN modeling software and some basic assumptions about where these taxsavings might accrue . In the absence of income tax and taxes paid by industry type, two alternativesexist to proportion the tax savings among industry/business sectors: 1) as a proportion of employmentor 2) as a proportion of contribution to gross state product . Since this analysis focuses on income, grossstate product contribution is a better proxy for who will receive the benefit of reduced taxation .

According to the U .S. Bureau of Economic Analysis, the top eight industry sectors contributing to NorthCarolina s gross state product (i .e . gross domestic product) in 2009 were

y Manufacturingy Finance and insurancey R

eal estatey H ealth care and social assistancey Professional and technical servicesy R etail tradey Wholesale tradey Construction

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

7/21

7 UNC Center for Competitive Economies

Tab le 6: Model of Additional Tax Reduction to Industry S ectors b y Proportion of Gross S tate Product

Expiration of CorporateIncome S urtax

Lower Corporate Income Tax(Tax Year 2012)

Lower Business Income TaxRates for S -Corps, LLCs, and

S ole Proprietorships, exemptfirst $50,000 of non-passive

b usiness income.

Industry

Sector

% of

GDP

% used for

model FY 2012 FY 2013 FY 2012 FY 2013 FY 2013 FY 2013

Manufacturing 22% 2 8 % $7,994,975 $ 8 ,077,6 8 2 $37,217,9 8 9 $8 5,049,997 $36,2 8 0,647 $92,741,714Finance andinsurance 13% 17% $4, 8 28 ,213 $4, 8 78 ,160 $22,476,163 $51,362,195 $21,910,097 $56,007,269R eal estate 12% 16% $4,567,397 $4,614,646 $21,262,022 $4 8 ,58 7,659 $20,726,534 $52,9 8 1,8 10H ealth careand socialassistance 8 % 11% $3,050, 8 93 $3,0 8 2,454 $14,202,434 $32,455,193 $13, 8 44,743 $35,390,362Professionaland technicalservices 6% 8 % $2,360, 8 35 $2,3 8 5,25 8 $10,990,095 $25,114,401 $10,713,307 $27,3 8 5,68 7R etail trade 6% 8 % $2,332,416 $2,356,545 $10, 8 57, 8 01 $24, 8 12,0 8 5 $10,5 8 4,345 $27,056,031Wholesaletrade 6% 8 % $2,272, 8 36 $2,296,34 8 $10,5 8 0,443 $24,17 8 ,272 $10,313,973 $26,364, 8 97Construction 4% 5% $1,592,434 $1,60 8 ,907 $7,413,053 $16,940,19 8 $7,226,354 $1 8 ,472,229Total 7 8 % 100% $29,000,000 $29,300,000 $135,000,000 $30 8 ,500,000 $131,600,000 $336,400,000Source: Percentage of State GD P, 2009 U .S. Bureau of Economic Analysis . Level of tax savings, N .C. G eneral Assembly Fiscal R esearch D ivision

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

8/21

SECTI ON II :

ECONOMIC IMPACTS OFT AXR ED UCTI ON This section of the report outlines the direct, indirect, and induced impacts of each prospective taxchange . R eported are industry output (value of goods and services produced/provided), employment,labor income, and average income per job . IMPLAN considers all jobs as full-time and does not generatea full-time equivalent calculation . This explains the relatively low-wage rates in some of the retailindustry positions, which are more likely to be part-time and lower paying . Multipliers are also reported . A multiplier value of 1 .5 means that for every dollar of new investment (or tax savings), it generates a

total of $1 .50 in output/income . Multipliers of 3 or less are generally expected to be observed in mostimpact assessments . It is important to note that in each model, the job creation reported in the firstfiscal year (2011-2012) represents the initial job creation . The employment numbers reported in fiscalyear two (2012-2013) represent the new jobs sustained from year one and any additional new jobscreated from the tax change being fully realized . For example: a change might yield 100 new jobs infiscal year one . In fiscal year two, 120 new jobs are reported . This should be interpreted as 100 new jobsbeing sustained from year one and 20 new jobs being added in year two . Job numbers are not additiveacross fiscal years! The models addressing corporate surtax, corporate income tax, and lower business

income taxes were derived using the same distribution of industry beneficiaries, which explains why theestimated average labor income is the same across models . In cases where the direct impacts for eachevent sum to less that the total tax reduction, this results from some of the resulting expenditure beingleaked from the state in the form of foreign and domestic out-of-state trade (i . e . imported goods andservices) which IMPLAN accounts for in the model . These purchases by households and industry of non-North Carolina inputs are accounted for the in the model using regional purchase coefficients ( R PCs) foreach category modeled .

Sales Tax Expiration Models:Tables 7 and 8 report the economic impacts of an expiration in the one-cent retail sales tax in fiscal year2011-2012 and fiscal year 2012-2013, respectively . D irect, indirect, and induced effects are interpreteddifferently in this type of model than outlined earlier in the model description . D irect impacts reflect theinitial round of spending by households of the tax savings, while indirect and induced reflect the secondand third rounds of economic activity in the economy generated from household spending of the taxsavings . In fiscal year 2011-2012 the total industry output is $1 .33 billion dollars and 11,720 jobs are

expected to be created at an average wage of $34,200 according to IMPLAN estimates . Tab le 7: Impacts of Retail S ales Tax Expiration, FY 2011-2012

Direct Indirect Induced Total MultiplierIndustry Output $766,759,000 $223,160,000 $337,691,000 $1,327,611,000 1 . 73

Employment 7,030 1,620 3,070 11,720 1 . 67L b I $226 217 000 $69 2 8 4 000 $105 391 000 $400 8 92 000 1 77

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

9/21

Tab le 8: Impacts of Retail S ales Tax Expiration, FY 2012-2013Direct Indirect Induced Total Multiplier

Industry Output $766,061,000 $225, 8 68 ,000 $341,7 88 ,000 $1,343,717,000 1 . 73Employment 7,110 1,640 3,110 11, 8 70 1 . 67Lab or Income $22 8 ,961,000 $70,124,000 $106,670,000 $405,755,000 1 . 77

Ave. Income Per Jo b $34,200Note: Totals may not sum due to rounding

Personal Income Surtax Expiration Models:

Tables 9 and 10 report the economic impacts of an expiration in the personal income surtax in fiscal year2011-2012 and fiscal year 2012-2013, respectively . D irect, indirect, and induced effects are interpreteddifferently in this type of model than outlined earlier in the model description, as well . D irect impactsreflect the initial round of spending by households of the tax savings, while indirect and induced reflectthe second and third rounds of economic activity in the economy generated from household spending of the tax savings . These models assume a distribution of personal income surtax expiration benefits asfollows: 10% to households with incomes of $75,000-$100,000, 40% to households with incomes of $100,000 to $150,000, and 50% to households with greater than $150,000 in income . Again, direct

impacts reflect the initial round of spending by these households of the tax savings, while indirect andinduced reflect the second and third rounds of economic activity in the economy in generated fromhousehold spending of the tax savings . In fiscal year 2011-2012 the total industry output is $207 milliondollars and 1, 8 68 jobs are expected to be created at an average wage of $33,370 according to IMPLANestimates . In fiscal year 2012-2013, the industry output rises to $209 million and an additional 22 new

jobs are created (for a total of 1, 8 90 jobs) .

Tab le 9: Impacts of Personal Income Tax Expiration, S cenario 1, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $119,591,000 $35,007,000 $52,490,000 $207,0 88 ,000 1 . 73Employment 1,134 256 47 8 1,8 68 1. 65Lab or Income $34,993,000 $10,939,000 $16,3 8 2,000 $62,314,000 1 . 78 A ve. Income Per Jo b $33,370Note: Totals may not sum due to rounding

Tab

le 10: Impacts of Personal Income Tax Expiration,S

cenario 1, FY 2012-2013Direct Indirect Induced Total MultiplierIndustry Output $121,043,000 $35,431,000 $53,127,000 $209,601,000 1 . 73Employment 1,14 8 259 4 8 4 1,8 90 1 . 65Lab or Income $35,41 8 ,000 $11,072,000 $16,5 8 1,000 $63,070,000 1 . 78 A ve. Income Per Jo b $33,370

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

10/21

with greater than $150,000 in income . These models yield little substantive changes, which suggest themodel is fairly robust to the distribution of the tax savings; therefore the economic impact estimates are

unlikely to change substantively if the actual distribution is different than modeled here . For this reason,scenario 1 impacts are reported in cumulative totals .

Tab le 11: Impacts of Personal Income Tax Expiration, S cenario 2, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $119, 8 73,000 $35,102,000 $52,535,000 $207,510,000 1 . 73Employment 1,141 257 47 8 1,8 76 1 . 64Lab or Income $35,003,000 $10,969,000 $16,396,000 $62,36 8 ,000 1 . 78 A ve. Income Per Jo b $33,240Note: Totals may not sum due to rounding

Tab le 12: Impacts of Personal Income Tax Expiration, S cenario 2, FY 2012-2013Direct Indirect Induced Total Multiplier

Industry Output $121,32 8 ,000 $35,52 8 ,000 $53,173,000 $210,02 8 ,000 1 . 73Employment 1,155 260 4 8 4 1,8 99 1 . 64Lab or Income $35,427,000 $11,102,000 $16,595,000 $63,124,000 1 . 78 A ve. Income Per Jo b $33,240Note: Totals may not sum due to rounding

Corporate Income Surtax Expiration, Lower Corporate Income Tax, and LowerBusiness Income Tax Models:

Tables 13 and 14 report the economic impact of expiration of the corporate income surtax . In fiscal year2011-2012 the total industry output is $32 million dollars and 245 jobs are expected to be created at anaverage wage of $40,530 according to IMPLAN estimates . In fiscal year 2012-2013, the industry outputrises to $32 million and an additional 2 new jobs are created (for a total of 247 jobs) .

Tab le 13: Corporate Income S urtax Expiration, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $20,143,000 $6,3 8 6,000 $5,9 8 6,000 $32,514,000 1 . 61Employment 146 44 55 245 1 . 67Lab or Income $6,090,000 $1,953,000 $1, 8 66,000 $9,909,000 1 . 63

Ave. Income Per Jo b $40,530Note: Totals may not sum due to rounding

Tab le 14: Corporate Income S urtax Expiration, FY 2012-2013Di I di I d d T l M l i li

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

11/21

Tables 15 and 16 report the economic impact of expiration of the corporate income tax . In fiscal year2011-2012 the total industry output is $151 million dollars and 1,13 8 jobs are expected to be created at

an average wage of $40,530 according toIMPLAN estimates

.

In fiscal year 2012-2013, the industryoutput rises to $345 million and an additional 1,463 new jobs are created (for a total of 2,601 jobs) .

Tab le 15: Lower Corporate Income Tax, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $93,767,000 $29,72 8 ,000 $27, 8 65,000 $151,360,000 1 . 61Employment 68 0 204 254 1,13 8 1. 67

Lab or Income $28 ,351,000 $9,091,000 $ 8 ,68 5,000 $46,127,000 1 . 63Ave. Income Per Jo b $40,530Note: Totals may not sum due to rounding

Tab le 16: Lower Corporate Income Tax, FY 2012-2013Direct Indirect Induced Total Multiplier

Industry Output $214,275,000 $67,935,000 $63,676,000 $345, 88 5,000 1 . 61Employment 1,554 466 5 8 0 2,601 1 . 67

Lab or Income $64,7 8 6,000 $20,776,000 $19, 8 48 ,000 $105,410,000 1 . 63A ve. Income Per Jo b $40,530Note: Totals may not sum due to rounding

Tables 17 and 1 8 report the economic impact of a lower business income tax . In fiscal year 2011-2012the total industry output is $147 million dollars and 1,109 jobs are expected to be created at an averagewage of $40,530 according to IMPLAN estimates . In fiscal year 2012-2013, the industry output rises to$377 million and an additional 1,727 new jobs are created (for a total of 2, 8 36 jobs) .

Tab le 17: Lower Business Income Tax, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $91,405,000 $2 8 ,98 0,000 $27,163,000 $147,54 8 ,000 1 . 61Employment 663 199 24 8 1,109 1 . 67Lab or Income $27,637,000 $ 8 ,8 62,000 $ 8 ,467,000 $44,966,000 1 . 63

Ave. Income Per Jo b $40,530Note: Totals may not sum due to rounding

Tab le 18: Lower Business Income Tax, FY 2012-2013Direct Indirect Induced Total Multiplier

Industry Output $223,654,000 $74,079,000 $69,434,000 $377,434,000 1 . 61Employment 1,694 509 633 2, 8 36 1 . 67L b I $70 646 000 $22 654 000 $21 643 000 $114 943 000 1 63

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

12/21

SECTI ON III :

SUMMAR YThis section of the report outlines the cumulative impacts of the tax reductions/expirations discussed inthis report . T ime and data limitations do not allow the researchers to conduct a true counterfactualanalysis . This is a rough estimation of the economic impacts of tax reduction given the available data,assumptions, and limitations outlined in this analysis . No assumptions are made about the public sectorimpacts of having reduced tax revenues, which may limit the net effects of the benefits outlined here . Additionally, no assumptions are made about the fiscal impacts (i . e . tax generate) created by thiseconomic activity .

Cumulative Impacts:

The initial tax changes will result in a total of $1 .8 billion in increased industry output, $564 million inlabor income, and the creation of 16,0 8 3 new jobs at an average wage of $35,0 8 2. Once the taxreduction impacts are fully realized in fiscal year 2012-2013, the total industry output will increase to$2 . 3 billion and labor income will increase to nearly $700 million . A total of 19,439 new jobs areprojected (16,0 8 3 in the FY 2011-12 and an additional 3,356 in FY 2012-2013) at an average wage of $35,969 .

Tab le 19: Cumulative Impacts, FY 2011-2012Direct Indirect Induced Total Multiplier

Industry Output $1,091,665,000 $323,261,000 $451,195,000 $1, 8 66,121,000 1 .71Employment 9,652 2,322 4,10 8 16,0 8 3 1 .67Lab or Income $323,2 88 ,000 $100,129,000 $140,791,000 $564,20 8 ,000 1 .75

Ave. Income Per Jo b $35,0 8 2Note: Totals may not sum due to rounding

Tab le 20: Cumulative Impacts, FY 2012-2013Direct Indirect Induced Total Multiplier

Industry Output $1,365,3 8 4,000 $409,765,000 $534,073,000 $2,309,220,000 1 .69Employment 11,65 8 2,917 4, 8 64 19,439 1 .67Lab or Income $405,964,000 $126,599,000 $166,627,000 $699,1 8 9,000 1 .72

Ave. Income Per Jo b $35,969Note: Totals may not sum due to rounding

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

13/21

The following tables are also provided to allow for tax by tax comparisons of the relative impacts of eachprospective change by industry output, employment, and labor income effects .

Tab le 21: Impact on Economic Output, FY 2011-2012Direct Indirect Induced Total Multiplier

1-cent sales tax: $766,759,000 $223,160,000 $337,691,000 $1,327,611,000 1 . 73personal incomesurtaxes:

$119,591,000 $35,007,000 $52,490,000 $207,0 88 ,000 1 . 73

corporate incomesurtaxes:

$20,143,000 $6,3 8 6,000 $5,9 8 6,000 $32,514,000 1 . 61

Reduction in thecorporate tax rate: $93,767,000 $29,728 ,000 $27, 8 65,000 $151,360,000 1 . 61

Business incometaxes:

$91,405,000 $2 8 ,98 0,000 $27,163,000 $147,54 8 ,000 1 . 61

Total: $1,091,665,000 $323,261,000 $451,195,000 $1,866,121,000 1.71Note: Totals may not sum due to rounding

Tab le 22: Impact on Economic Output, FY 2012-2013

Direct Indirect Induced Total Multiplier1-cent sales tax: $776,061,000 $225, 8 68 ,000 $341,7 88 ,000 $1,343,717,000 1 . 73personal incomesurtaxes:

$121,043,000 $35,431,000 $53,127,000 $209,601,000 1 . 73

corporate incomesurtaxes:

$20,351,000 $6,452,000 $6,04 8 ,000 $32, 8 51,000 1 . 61

Reduction in thecorporate tax rate:

$214,275,000 $67,935,000 $63,676,000 $345, 88 5,000 1 . 61

Business incometaxes:

$233,654,000 $74,079,000 $69,434,000 $377,166,000 1 . 61

Total: $1,365,384,000 $409,765,000 $534,073,000 $2,309,220,000 1.69Note: Totals may not sum due to rounding

Tab le 23: Impact on Employment, FY 2011-2012Direct Indirect Induced Total Multiplier

1-cent sales tax: 7,029 1,620 3,074 11,723 1 . 67personal incomesurtaxes:

1,134 256 47 8 1,8 68 1. 67

corporate incomesurtaxes:

146 44 55 245 1 . 67

R d ti i th 68 0 204 254 1 13 8 1 67

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

14/21

Tab le 24: Impact on Employment, FY 2012-2013Direct Indirect Induced Total Multiplier

1-cent sales tax: 7,115 1,639 3,112 11,8

66 1.67personal income

surtaxes:1,14 8 259 4 8 4 1,8 90 1 . 67

corporate incomesurtaxes:

148 44 55 247 1 . 67

Reduction in thecorporate tax rate:

1,554 466 5 8 0 2,601 1 . 67

Business income

taxes:

1,694 509 633 2, 8 36 1 . 67

Total: 11,658 2,917 4,864 19,439 1.67Note: Totals may not sum due to rounding

Tab le 25: Impact on La b or Income, FY 2011-2012Direct Indirect Induced Total Multiplier

1-cent sales tax: $226,217,000 $69,2 8 4,000 $105,391,000 $400, 8 92,000 1 . 77personal income

surtaxes:

$34,993,000 $10,939,000 $16,3 8 2,000 $62,314,000 1 . 77

corporate incomesurtaxes:

$6,090,000 $1,953,000 $1, 8 66,000 $9,909,000 1 . 63

Reduction in thecorporate tax rate:

$28 ,351,000 $9,091,000 $ 8 ,68 5,000 $46,127,000 1 . 63

Business incometaxes:

$27,637,000 $ 8 ,8 62,000 $ 8 ,467,000 $44,966,000 1 . 63

Total: $323,288,000 $100,129,000 $140,791,000 $564,208,000 1.75Note: Totals may not sum due to rounding

Tab le 26: Impact on La b or Income, FY 2012-2013Direct Indirect Induced Total Multiplier

1-cent sales tax: $22 8 ,961,000 $70,124,000 $106,670,000 $405,755,000 1 . 77personal incomesurtaxes:

$35,41 8 ,000 $11,072,000 $16,5 8 1,000 $63,070,000 1 . 77

corporate incomesurtaxes:

$6,153,000 $1,973,000 $1, 88 5,000 $10,011,000 1 . 63

Reduction in thecorporate tax rate:

$64,7 8 6,000 $20,776,000 $19, 8 48 ,000 $105,410,000 1 . 63

Business incometaxes:

$70,646,000 $22,654,000 $21,643,000 $114,943,000 1 . 63

T l $405 964 000 $126 599 000 $166 627 000 $699 189 000 1 72

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

15/21

APPEND IX:The following tables contain detailed information and descriptions utilized in the Corporate IncomeSurtax Expiration, Lower Corporate Income Tax, and Lower Business Income Models . In each model, weapportioned the tax savings to the top eight industry sectors contributing to North Carolina s gross stateproduct (i .e . gross domestic product) using U . S. Bureau of Economic Analysis 2009 estimates . Thecategories included:

y Manufacturingy Finance and insurancey R eal estatey H

ealth care and social assistancey Professional and technical servicesy R etail tradey Wholesale tradey Construction

Each category was then reconstructed in the IMPLAN model using a crosswalk table to transcribe theseNAICS (North American Industrial Classification System) codes into IMPLAN sector codes . The tax savings

was then apportioned to each of the IMPLAN sector codes comprising each of the eight categories . Inthe case of manufacturing, the potential IMPLAN sectors numbered 27 8 and were too cumbersome tomodel in their entirety . Therefore, the top 25 IMPLAN sectors comprising 50 percent of the state smanufacturing output were used in constructing the entire manufacturing sector .

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

16/21

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

17/21

17 UNC Center for Competitive Economies

Tab le A -2: Construction Model in IMPL AN

Construction Corporate Income S urtax Lower Corporate Rate Lower Business Income

IMPLAN Industry Sector FY11-12 FY12-13 FY11-12 FY12-13 FY11-12 FY12-13

34Construction of new nonresidential commercial and health carestructures $443,799 $44 8 ,390 $2,065,961 $4,721,103 $2,013,929 $5,14 8 ,068

35 Construction of new nonresidential manufacturing structures $53,7 8 1 $54,337 $250,360 $572,119 $244,055 $623, 8 60

36 Construction of other new nonresidential structures $264,01 8 $266,749 $1,229,050 $2, 8 08 ,607 $1,19 8 ,096 $3,062,610

37Construction of new residential permanent site single- andmulti-family structures $4 8 7,174 $492,214 $2,267, 8 79 $5,1 8 2,523 $2,210,762 $5,651,21 8

38 Construction of other new residential structures $152,577 $154,156 $710,273 $1,623,106 $692,3 8 5 $1,769, 8 96

39 Maintenance and repair construction of nonresidentialmaintenance and repair $159,120 $160,767 $740,733 $1,692,713 $722,07 8 $1,8 45,79 8

40 Maintenance and repair construction of residential structures $31,964 $32,294 $14 8 ,797 $340,02 8 $145,049 $370,779

$1,592,434 $1,608,907 $7,413,053 $16,940,198 $7,226,354 $18,472,229

Tab le A -3: Wholesale Trade Model in IMPL AN

Wholesale Trade Corporate Income S urtax Lower Corporate Rate Lower Business Income

IMPLAN Industry Sector FY11-12 FY12-13 FY11-12 FY12-13 FY11-12 FY12-13

319 Wholesale trade $2,272, 8 36 $2,296,34 8 $10,5 8 0,443 $24,17 8 ,272 $10,313,973 $26,364, 8 97

$2,272,836 $2,296,348 $10,580,443 $24,178,272 $10,313,973 $26,364,897

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

18/21

18 UNC Center for Competitive Economies

Tab le A -4: Retail Trade Model in IMPL AN

Retail Trade Corporate IncomeS

urtax Lower Corporate Rate Lower Business Income320 R etail - Motor vehicle and parts $472, 8 73 $477,765 $2,201,307 $5,030,394 $2,145, 8 67 $5,4 8 5,331

321 R etail - Furniture and home furnishings $116,000 $117,200 $540,001 $1,234,002 $526,401 $1,345,602

322 R etail - Electronics and appliances $92,160 $93,113 $429,019 $9 8 0,388 $41 8 ,214 $1,069,052

323 R etail - Building material and garden supply $25 8 ,402 $261,075 $1,202,904 $2,74 8 ,8 59 $1,172,609 $2,997,460

324 R etail - Food and beverage $259,211 $261, 8 92 $1,206,670 $2,757,465 $1,176,2 8 0 $3,006, 8 43

325 R etail - H ealth and personal care $16 8 ,041 $169,7 8 0 $7 8 2,261 $1,7 8 7,611 $762,560 $1,949,27 8

326 R etail - G asoline stations $14 8 ,379 $149,914 $690,729 $1,57 8 ,443 $673,332 $1,721,193327 R etail - Clothing and clothing accessories $145,5 88 $147,094 $677,737 $1,54 8 ,754 $660,66 8 $1,6 88 ,8 19

328 R etail - Sporting goods, hobby, book and music $59,142 $59,754 $275,315 $629,145 $26 8 ,38 1 $6 8 6,044

329 R etail - G eneral merchandise $345,117 $34 8 ,68 7 $1,606,577 $3,671,327 $1,566,116 $4,003,353

330 R etail - Miscellaneous $120,11 8 $121,361 $559,170 $1,277, 8 06 $545,0 8 7 $1,393,36 8

331 R etail - Nonstore $147,3 8 7 $14 8 ,912 $6 8 6,111 $1,567, 8 91 $66 8 ,8 31 $1,709,6 8 7

$2,332,416 $2,356,545 $10,857,801 $24,812,085 $10,584,345 $27,056,031

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

19/21

19 UNC Center for Competitive Economies

Tab le A -5: Professional S ervices Model in IMPL AN

ProfessionalS

ervices Corporate IncomeS

urtax Lower Corporate Rate Lower Business Income367 Legal services $304,302 $307,450 $1,416,577 $3,237,141 $1,3 8 0,900 $3,529,900

368 Accounting, tax preparation, bookkeeping, and payroll services $193,376 $195,376 $900,197 $2,057,117 $ 8 77,525 $2,243,157

369 Architectural, engineering, and related services $364,336 $36 8 ,105 $1,696,045 $3, 8 75,777 $1,653,330 $4,226,293

370 Specialized design services $40,65 8 $41,079 $1 8 9,271 $432,520 $1 8 4,505 $471,636

371 Custom computer programming services $23 8 ,555 $241,023 $1,110,515 $2,537,732 $1,0 8 2,546 $2,767,239

372 Computer systems design services $142,992 $144,471 $665,653 $1,521,140 $64 8 ,888 $1,65 8 ,709

373Other computer related services, including facilitiesmanagement $104,221 $105,299 $4 8 5,165 $1,10 8 ,692 $472,946 $1,20 8 ,959

374 Management, scientific, and technical consulting services $324,123 $327,476 $1,50 8 ,8 48 $3,447,99 8 $1,470, 8 48 $3,759, 8 26

375 Environmental and other technical consulting services $64,7 8 2 $65,452 $301,571 $6 8 9,147 $293,976 $751,471

376 Scientific research and development services $249,133 $251,710 $1,159,756 $2,650,256 $1,130,547 $2, 88 9,939

377 Advertising and related services $115,914 $117,113 $539,59 8 $1,233,0 8 0 $526,00 8 $1,344,597

378 Photographic services $23,2 8 1 $23,522 $10 8 ,379 $247,666 $105,649 $270,064

379 Veterinary services $69,333 $70,050 $322,755 $737,556 $314,627 $ 8 04,259

38 0All other miscellaneous professional, scientific, and technicalservices $125, 8 31 $127,133 $5 8 5,764 $1,33 8 ,58 0 $571,012 $1,459,63 8

$2,360,835 $2,385,258 $10,990,095 $25,114,401 $10,713,307 $27,385,687

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

20/21

-

8/6/2019 UNC C3E Economic Impact of Proposed Tax Reductions in NC Report April 18 2011

21/21

21 UNC Center for Competitive Economies

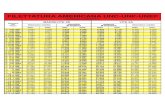

Tab le A -8: Finance Model in IMPL AN

Finance Corporate IncomeS

urtax Lower Corporate Rate Lower Business Income354 Monetary authorities and depository credit intermediation $2,137,252 $2,159,362 $9,949,27 8 $22,735,942 $9,69 8 ,703 $24,792,126

355 Nondepository credit intermediation and related activities $496,9 8 4 $502,126 $2,313,54 8 $5,2 8 6,88 5 $2,255,2 8 1 $5,765,01 8

356Securities, commodity contracts, investments, and relatedactivities $722,147 $729,61 8 $3,361,719 $7,6 8 2,150 $3,277,053 $ 8 ,376,906

357 Insurance carriers $9 8 0,497 $990,640 $4,564,3 8 2 $10,430,45 8 $4,449,427 $11,373,764

358 Insurance agencies, brokerages, and related activities $359,666 $363,3 8 7 $1,674,30 8 $3,8 26,105 $1,632,141 $4,172,129

359 Funds, trusts, and other financial vehicles $131,666 $133,02 8 $612,92 8 $1,400,655 $597,492 $1,527,327

$4,828,213 $4,878,160 $22,476,163 $51,362,195 $21,910,097 $56,007,269