Ulusoy Electriculusoyelektrik.com.tr/Uploads/Other/PageDocument/3q17-yatirimci... · November 2017...

27

Ulusoy Electric Q3’ 17 Results November 2017

Transcript of Ulusoy Electriculusoyelektrik.com.tr/Uploads/Other/PageDocument/3q17-yatirimci... · November 2017...

Ulusoy ElectricQ3’ 17 Results

November 2017

Enis UlusoyVice Chairman

Table of

Contents

Q3’17 Highligts

Sector and Ulusoy Elektrik

Financials

5

8

18

Q3’17 Highlights

November 2017 Q3’17 Results

Q3’17 Highlights

5

• All time highest revenue since establishment, (excluding strongest last quarter)

• Increase in margins continuing , 26,3 % EBITDA

• Higher domestic demand leading boost in prices ( appx. 10% increase)

• Capacity increase with system improvements, additional shifts, machine and mould investments (< 1M USD)

• Diversified Exports, Indonesia & Algeria homologation files completed, new countries in the radar; Egypt, Azerbaijan & Saudi Arabia

• Strong Order Book for the upcoming quarters

• Free float increased to 21,6%

Sector and Ulusoy Elektrik

November 2017 Q3’17 Results

Sector (Domestic)

7

ELECTRICITY DISTRIBUTION COMPANIES

Investment Implementation PeriodInvestmentBudget (TL)

2006-2010 (before privatization) 550 M

2011-2015 3,69 B

2016-2020 18,4 B2016 (official investment result) 3,7 B

Q3’16 Dist.Co. Sales Q3’17 Dist.Co. Sales

24.1 M TL 47.0 M TL % 95

*2017 expectation + 4 Billion

Q2 31,1 MTL

November 2017 Q3’17 Results

Sector (Domestic)

8

RETAILERS

Q3’16 Retailers Sales Q3’17 Retailers Sales

8.5 M TL 29.3 M TL % 245

• Positive Economic Environment• Residential & Industrial Investments• New Distributors

Q2 20,9 MTL

November 2017 Q3’17 Results

Sector (Domestic)

9

DIRECT SALES

Q3’16 Direct Sales Q3’17 Direct Sales

13.9 M TL 33,9 M TL % 144

• Solar & Wind Electricity Generation Projects • 500 MW Wind Project in the coming 5 years (already been awarded)• 1000MW YEKA tender (generation & turbine production)

Q2 31,8 MTL

November 2017 Q3’17 Results

Sector (Domestic)

10

DOMESTIC REVENUE BREAKDOWN BY CUSTOMER SEGMENTS

52%18%

30%

Q3’16

Dist.Co. Retailers

Direct Sales

110.2 M TL 46.5 M TL

% 139

43%

27%

30%

Q3’17

Dist. Co. Retailers

Direct Sales

November 2017 Q3’17 Results

Sector (Export)

11

• Diversified and Sustainable Export• Transformer as a driving force for export markets• Indonesia & Algeria local Certifications Completed• New markets; KSA, Egypt & Azerbaijan• Strong order intake and 2018 expectations

Q3’17

41%

9%7%5%4%

4%

4%

4%

4%19%

JORDAN IRAQMOROCCO AFGHANISTANUKRAINE IRANETHIOPIA SENEGALFINLAND GEORGIAOTHER 17 COUNTRIES

47%

13%

7%

6%

4%

4%

3% 15%

SUDAN TURKMENISTAN

LITHUANIA TUNISIA

PALESTINE MOROCCO

GEORGIA OTHER 11 COUNTRIES

Q3’16

November 2017 Q3’17 Results

Sector (Export)

12

EXPORT REVENUES

Q3’ 17Q2’ 17

17.2 M 12.9 M-%25

9M’16 9M’17

28.6 M 48.8 M% 71

November 2017 Q3’17 Results

Revenue Breakdown

13

TL mn Q3'16 Q3'17 change

Cable Accessories 1,5 2,0 33%Concrete Compact Substations 6,6 13,7 108%

Distribution Transformers 2,5 10,2 313%

Metal Clad 1,3 3,9 192%

Metal Enclosed 25,1 64,0 155%

Other Sales(Trade Goods, Auxilary Materials) 10,1 13,4 30%Railway Overhead Line Equipments 0,3 1,6 427%

RMU 7,0 12,8 85%

Metal Compact Substations 0,1 - n.a.

Total 54,1 121,7 123%

November 2017 Q3’17 Results

TRANSFORMER FACTORY

14

*Varies on ratings and types

TRANSFORMER PRODUCTION UNITS

TRANSFORMER REVENUES (M TL)

48%52%domestic

export

AVG. UNIT PRICE*

20.527 TL5.800 USD

REVENUE BREAKDOWN

FY 2016 Q1’17 Q2’17 Q3’17 9M'17

863 173 699 641 1.513

FY 2016 Q1’17 Q2’17 Q3’17 9M'17

13 4,2 13,7 10,2 28,1

November 2017 Q3’17 Results

Strong Orderbook

15

2017 ORDER INTAKE

DOMESTIC EXPORT

72 M TL

Q1’17 Q2‘17 Q1’17 Q2’17

21.5 M TL19 M TL107.5 M TL

Q3’17 Q3’17

18.2 M TL132,7 M TL

Financials

November 2017 Q3’17 Results

Financial Review

17

TL mn Q3'16 Q3'17 changeRevenues 54,1 121,7 125%Domestic 46,5 110,2 137%Export 7,9 12,9 64%Gross Profit 11,0 36,4 232%EBITDA 7,8 32,0 310%Net Income 5,5 25,3 356%

Gross Margin 20,3% 29,9% 47%EBITDA Margin 14,4% 26,3% 82%Net Margin 10,2% 20,8% 103%ROE 17,1% 44,6% 160%

Depreciation&Amortization 1,2 1,3 10%Net Debt Position -11,3 -15,0 33%CAPEX 0,6 1,4 119%

Current Ratio 1,8 2,6 41%Current Assets/Total Assets 0,6 0,7 21%Current Liabilities/Total Liabilities 1,0 1,0 n.a.Total Liabilities/Total Assets 0,33 0,29 -14%

November 2017 Q3’17 Results

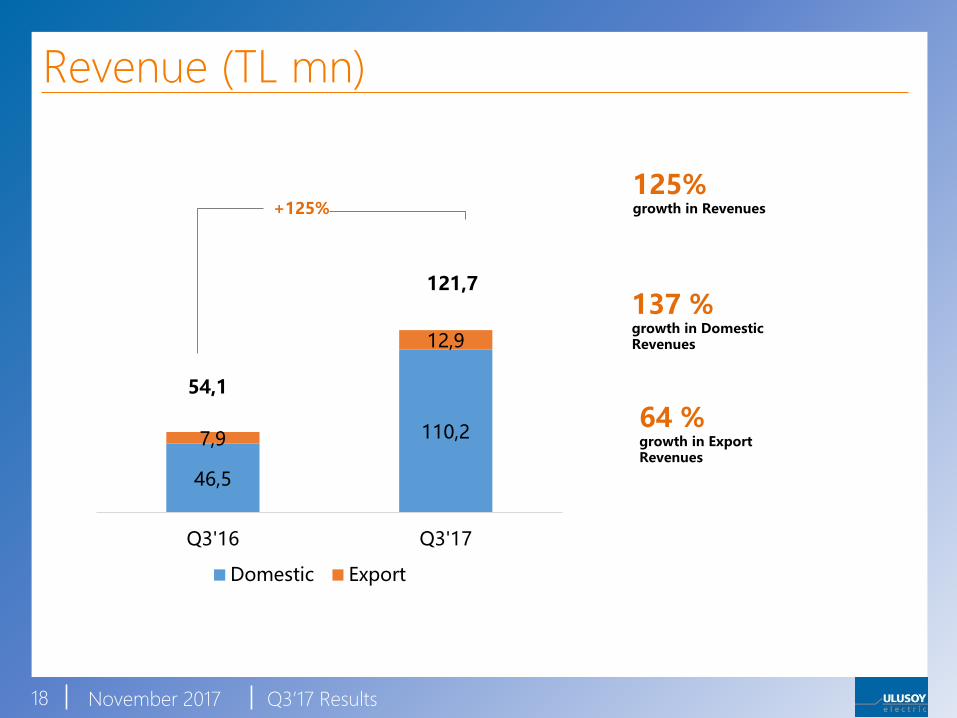

46,5

110,27,9

12,9

0

50

100

150

Q3'16 Q3'17

Domestic Export

Revenue (TL mn)

18

121,7

54,1

+125%125% growth in Revenues

137 % growth in Domestic Revenues

64 % growth in Export Revenues

November 2017 Q3’17 Results

Revenue (TL mn) price vs volume

19

34,5

62,2

+7

+21

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

1Q16 Revenues Volume change Price change 1Q17 Revenues

TLm

n

November 2017 Q3’17 Results

Revenue (TL mn) price vsvolume

20

50,5

102,0

+10

+41

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

Q2'16 Revenues Volume change Price change Q2'17 Revenues

TLm

n

November 2017 Q3’17 Results

Revenue (TL mn) price vsvolume

21

54,6

121,5

+34

+33

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

Q3'16 Revenues Volume change Price change Q3'17 Revenues

TLm

n

November 2017 Q3’17 Results

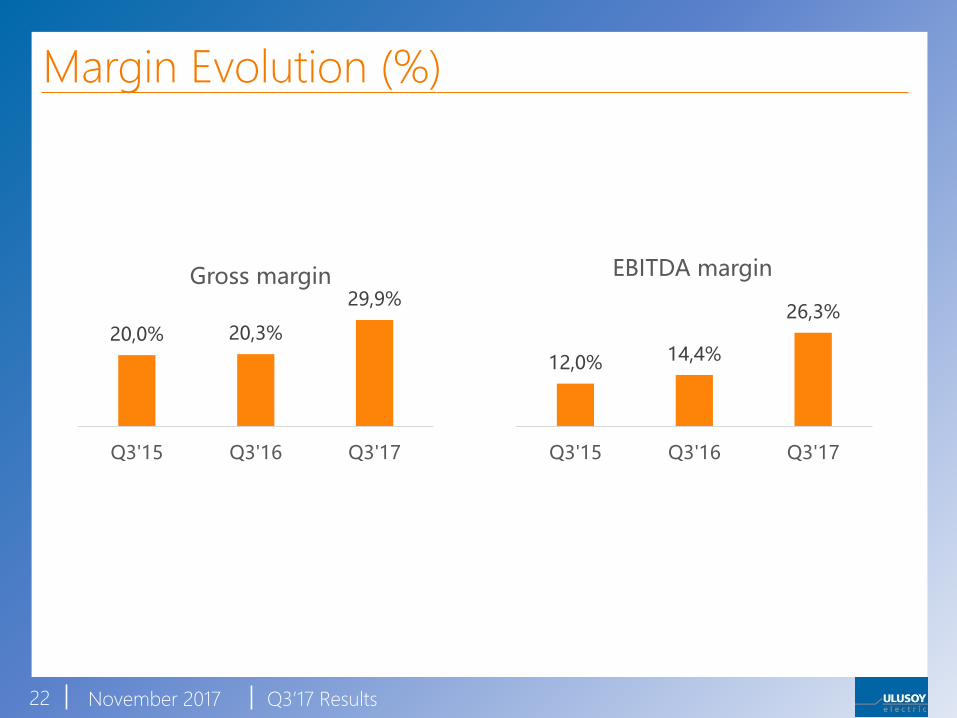

Margin Evolution (%)

22

20,0% 20,3%

29,9%

Q3'15 Q3'16 Q3'17

Gross margin

12,0% 14,4%

26,3%

Q3'15 Q3'16 Q3'17

EBITDA margin

November 2017 Q3’17 Results

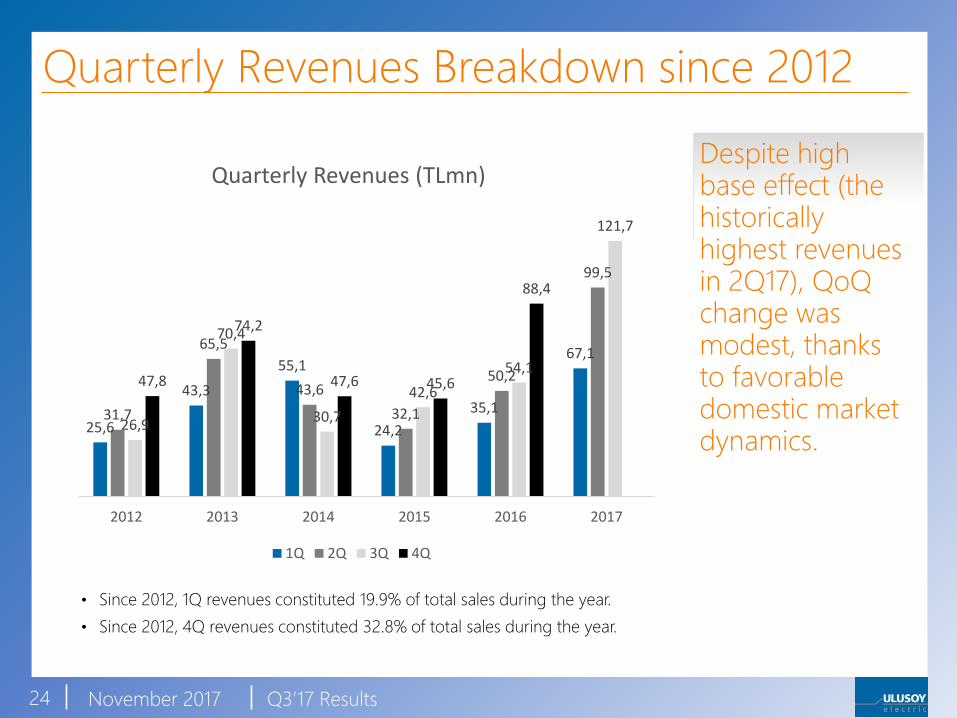

Quarterly Revenues Breakdown since 2012

23

1Q is the weakest while 4Q is the strongest quarters

25,631,7

26,9

47,843,3

65,570,4 74,2

55,1

43,6

30,7

47,6

24,232,1

42,645,6

35,1

50,254,1

88,4

67,1

99,5

121,7

0

20

40

60

80

100

120

140

1Q 2Q 3Q 4Q

Quarterly Revenues (TLmn)

2012 2013 2014 2015 2016 2017

• Since 2012, 1Q revenues constituted 19.9% of total sales during the year.

• Since 2012, 4Q revenues constituted 32.8% of total sales during the year.

November 2017 Q3’17 Results

Quarterly Revenues Breakdown since 2012

24

Despite high base effect (thehistorically highest revenues in 2Q17), QoQchange was modest, thanks to favorable domestic market dynamics.

25,6

43,3

55,1

24,2

35,1

67,1

31,7

65,5

43,6

32,1

50,2

99,5

26,9

70,4

30,7

42,6

54,1

121,7

47,8

74,2

47,6 45,6

88,4

0

20

40

60

80

100

120

140

2012 2013 2014 2015 2016 2017

Quarterly Revenues (TLmn)

1Q 2Q 3Q 4Q

• Since 2012, 1Q revenues constituted 19.9% of total sales during the year.

• Since 2012, 4Q revenues constituted 32.8% of total sales during the year.

November 2017 Q3’17 Results

Quarterly Revenues Changes since 2013

25

-9%

-26%

-49%

-23%-24%

51%

-21%

33%43%

98,00%

7%

-30%

33%

8%

22,00%

5%

55%

7%

63%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

2013 2014 2015 2016 2017

Revenues change (Quarterly)

1Q 2Q 3Q 4Q

• On average, 2Q revenues declined by 27% QoQ since 2013.

• On average, 4Q revenues increased by 35% QoQ since 2013.

November 2017 Q3’17 Results

Shareholder Structure

Pre IPO Post IPO Current

26

70,0%

30,0%

Family Free Float

78,4%

21,6%

Family Free Float

53,0%

18,4%

14,3%

14,3%

Sait UlusoyAkgül UlusoyKubilay Hakkı UlusoyEnis Ulusoy

Thank YouFor further information please e-mail

or call Ulusoy Electric Investor Relations

at (+90 312 267 0712)