UK (United Kingdom) Supermarket Strategy. Beating Back ......Beating Back Hard Discounters Update:...

3

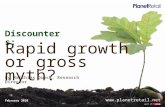

Executive Insights Over the past 18 months, the supermarket price war has become an ever more common narrative in the U.K. national news, and this certainly appears to be reflected in national statistics. Since mid-2014 food and non-alcohol consumer prices have declined at 2.1% per annum. But the question remains whether the U.K.’s big four supermarkets — Sainsbury’s, Tesco, Asda and Morrisons — have done enough to win the battle with the continental hard discounters, Aldi and Lidl. Beating Back Hard Discounters Update: Have the U.K.’s Big Four Supermarkets Done Enough? was written by Jonathan Simmons and Geoff Parkin, partners in L.E.K. Consulting’s Consumer Products and Retail practice, and Jonathon Green, a manager. Jonathan, Geoff and Jonathon are based in London. For more information, please contact [email protected]@lek.com In our Executive Insights Beating Back Hard Discounters: Lessons From France for the U.K.’s Big Four Supermarkets we examined how the U.K.’s ‘big four’ were struggling with the insurgent threat posed by the hard discounters. At the time of our report in October 2014, these two retailers had increased their U.K. grocery market share from 5% at the start of 2012 to more than 8%. We observed how the big four priced at a substantial premium to the hard discounters on both branded and private label goods, with Morrisons and Tesco being 30% more expensive on the latter. So, has the tide turned? The answer, as Figure 1 illustrates, is not yet. Both Lidl and Aldi have continued to steadily take U.K. market share — and at a rate that outstrips their growth in new stores. In fact, the two discounters took over 10% of the U.K. market for the first time in the 12 weeks to November 2015 (although their share fell slightly over the Christmas period). This continued gain in market share comes despite substantial price reductions at the big supermarkets since late 2014. During that period Asda, Tesco and Morrisons closed the price gap on both national brands and private label goods (see Figure 2). However all of the big four remain substantially more expensive than Aldi, with a bigger gap on private label goods than on Beating Back Hard Discounters Update: Have the UK’s Big Four Supermarkets Done Enough? Volume XVIII, Issue 8 Grocer market share Source: Kantar Worldpanel Aldi Lidl Feb-14 Feb-15 Feb-16 0 5 10% 4.1 4.9 5.6 7.2 8.4 9.8 3.1 3.5 4.2 Figure 1 U.K. grocery market share of hard discounters 12 weeks prior to date shown The supermarket price war is heating up. But are the U.K.’s big four doing enough to win the battle with the continental hard discounters?

Transcript of UK (United Kingdom) Supermarket Strategy. Beating Back ......Beating Back Hard Discounters Update:...

Executive Insights

Over the past 18 months, the supermarket price

war has become an ever more common narrative

in the U.K. national news, and this certainly

appears to be reflected in national statistics.

Since mid-2014 food and non-alcohol consumer prices have declined at 2.1% per annum. But the question remains whether the U.K.’s big four supermarkets — Sainsbury’s, Tesco, Asda and Morrisons — have done enough to win the battle with the continental hard discounters, Aldi and Lidl.

Beating Back Hard Discounters Update: Have the U.K.’s Big Four Supermarkets Done Enough? was written by Jonathan Simmons and Geoff Parkin, partners in L.E.K. Consulting’s Consumer Products and Retail practice, and Jonathon Green, a manager. Jonathan, Geoff and Jonathon are based in London.

For more information, please contact [email protected]@lek.com

In our Executive Insights Beating Back Hard Discounters: Lessons From France for the U.K.’s Big Four Supermarkets we examined how the U.K.’s ‘big four’ were struggling with the insurgent threat posed by the hard discounters. At the time of our report in October 2014, these two retailers had increased their U.K. grocery market share from 5% at the start of 2012 to more than 8%. We observed how the big four priced at a substantial premium to the hard discounters on both branded and private label goods, with Morrisons and Tesco being 30% more expensive on the latter.

So, has the tide turned? The answer, as Figure 1 illustrates, is not yet. Both Lidl and Aldi have continued to steadily take U.K. market share — and at a rate that outstrips their growth in new stores. In fact, the two discounters took over 10% of the U.K. market for the first time in the 12 weeks to November 2015 (although their share fell slightly over the Christmas period).

This continued gain in market share comes despite substantial price reductions at the big supermarkets since late 2014. During that period Asda, Tesco and Morrisons closed the price gap on both national brands and private label goods (see Figure 2).

However all of the big four remain substantially more expensive than Aldi, with a bigger gap on private label goods than on

Beating Back Hard Discounters Update:Have the UK’s Big Four Supermarkets Done Enough?

Volume XVIII, Issue 8

Grocer market share

Source: Kantar Worldpanel

Aldi Lidl

Feb-14

Feb-15

Feb-16

0 5 10%

4.1

4.9

5.6

7.2

8.4

9.8

3.1

3.5

4.2

Figure 1

U.K. grocery market share of hard discounters

12 weeks prior to date shown

The supermarket price war is heating up. But are

the U.K.’s big four doing enough to win the battle

with the continental hard discounters?

national brands (see Figure 3). This story is a marked contrast to what happened in France. Our first Executive Insights on this topic explained that big supermarkets were able to seize back the

initiative by pricing at parity with the discounters on national brand items and, perhaps more notably, pricing private label budget items at a 10-15% discount.

Executive Insights

Page 2 L.E.K. Consulting / Executive Insights, Volume XVIII, Issue 8 INSIGHTS@WORK®

Figure 3

Price comparison of U.K. supermarkets vs. hard discounters (February 2016)

Figure 2

Price reductions amongst U.K. supermarkets and hard discounters (August 2014 - February 2016)

Relative price of a basket of branded goods

s s

200

100

0

Aldi Asda Tesco

100109

123

98 103111

Aug -14 Feb -16

-2% -6% -10%s

Relative price of a basket of equivalent private label goods

200

100

0

Aldi Asda Morrisons Tesco

100118

137 133

97 104118 125

-3% -12% -14% -6%

Sept -14 Feb -16

s s s s

Price of a basket of national brand items Price of a basket of equivalent private label goods

80

40

0

Aldi

46.59

Asda

49.88

+7%

Morrisons

56.69

+22%

Tesco

59.65

+28%

Sainsbury’s

60.43

+30%

80

40

0

Aldi

27.60

Asda

29.03

+5%

Morrisons

30.48

+10%

Tesco

31.39

+14%

Sainsbury’s

32.65

+18%

Source: L.E.K. analysis

Note: Indexed Aldi 2014 = 100 Source: L.E.K. analysis

Pou

nd

s

Pou

nd

s

Pou

nd

s

Pou

nd

s

Whilst the big four have certainly made progress since late 2014, our analysis proves that they still have some way to go if they are to effectively address the threat. As we previously outlined, L.E.K. recommends six key initiatives for U.K. supermarkets to regain their leadership:

1. Redefine consumer pricing strategy and collaborate closelywith suppliers to scrutinize all elements of supplier costsand pricing

2. Drive rigorous zero-base cost reduction across theiroperations and supply chain

3. Review private label strategy to offer better value andcompete more effectively against discounter’s own ranges

4. Continue to review store footprint and format to driveincreased footfall and consumer expenditure in store

5. Clearly define target consumer segments and deliver adifferentiated proposition

6. Rationalize non-core businesses that do not directly supportthe fundamental customer proposition

These six strategic initiatives are all aimed at passing efficiency gains to consumers through lower pricing, while ensuring profit protection and an eventual return to growth.

Executive Insights

Page 3 L.E.K. Consulting / Executive Insights, Volume XVIII, Issue 8

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other productsand brands mentioned in this document are properties of their respective owners. © 2016 L.E.K. Consulting LLC

About L.E.K. Consulting

L.E.K. Consulting is a global management consulting firm that uses deep industry expertise and rigorous analysis to help businessleaders achieve practical results with real impact. We are uncompromising in our approach to helping clients consistently make betterdecisions, deliver improved business performance and create greater shareholder returns. The firm advises and supports global companiesthat are leaders in their industries — including the largest private and public sector organizations, private equity firms and emergingentrepreneurial businesses. Founded more than 30 years ago, L.E.K. employs more than 1,200 professionals across the Americas, Asia-Pacific and Europe. For more information, go to www.lek.com.

About the Authors

Geoff Parkin is a partner in L.E.K. Consulting’s London office. He has been with L.E.K. for more than 15 years and has broad experience assisting U.K. and international clients with strategy development and due diligence assignments. Prior to joining L.E.K. in 1999, Geoff worked in commercial line management roles for British Airways and American Express,

based in London, Copenhagen and Amsterdam.

Jonathan Simmons is a partner in L.E.K. Consulting’s London office. He has almost 30 years of strategy consulting experience and leads L.E.K.’s European Retail and Consumer ProductsPractice. Jonathan has provided strategic adviceto a broad range of U.K. and European-basedcompanies, and companies from other regionsseeking European market entry, with a particular

focus on specialty retail, apparel and accessories, sports retail and brands, airport retail, automotive services and grocery retail.