UK GAAP - A Year of Change | Accountex 2015

14

An overview of the New UK GAAP FRS 102 and other reporting issues

-

Upload

sageukofficial -

Category

Business

-

view

109 -

download

2

Transcript of UK GAAP - A Year of Change | Accountex 2015

An overview of the New UK GAAPFRS 102 and other reporting issues

Sage 2

An Overview of the New UK GAAPIntroduction

Amy NoblettCompliance Domain Specialist

Sage 3

Agenda1. The need for change2. The new standards3. Financial statements under FRS 1024. Key differences5. First-time adoption of FRS 1026. Reduced disclosures7. Changes to company law8. Impact on financial reporting standards9. Practical considerations

Sage 4

An Overview of the New UK GAAPThe need for change

• Consistency with IFRS• Reflects more up to date thinking• More proportionate reporting• Cost effective

Why?

• Majority of large and medium-sized UK entities• Entities that don’t apply EU-adopted IFRS• Entities that don’t apply FRSSE

Who?

• Accounting periods beginning on or after 1 January 2015

• Early adoption permitted• Transition date

When?

Sage 5

An Overview of the New UK GAAPThe new standards

• Which standards to apply• Application of SORPs• Transitional arrangements

FRS 100

• Disclosure exemptions from EU-adopted IFRS for qualifying entitiesFRS 101

• Succinct financial reporting based on IFRS for SMEs• Replaces current FRSs, SSAPs and UITFs • Includes reduced disclosures for qualifying entities

FRS 102

• Insurance contractsFRS 103

Sage 6

An Overview of the New UK GAAPFinancial statements under FRS 102

• Statement of financial position• Statement of comprehensive income or income

statement• Statement of changes in equity• Statement of cash flows

Primary statements

• Accounting policy changes• Statement of compliance • Transition note

Notes to the accounts

Sage 7

An Overview of the New UK GAAPKey differences

• Comprehensive accounting guidance• Classified as ‘basic’ or ‘other’• Derivatives on-balance sheet

Financial instruments

• Current service cost and net interest cost recognised in P&L with remeasurements in other comprehensive income

Defined benefit pension plans

• Revaluation gains and losses taken to profit or loss rather than reservesInvestment property

• More intangibles likely to be recognised separately from goodwill• Finite useful lives for goodwill and intangibles• Merger accounting only permitted for group reconstructions

Business combinations

• Timing difference plus approach could result in larger deferred tax liabilitiesDeferred tax

Sage 8

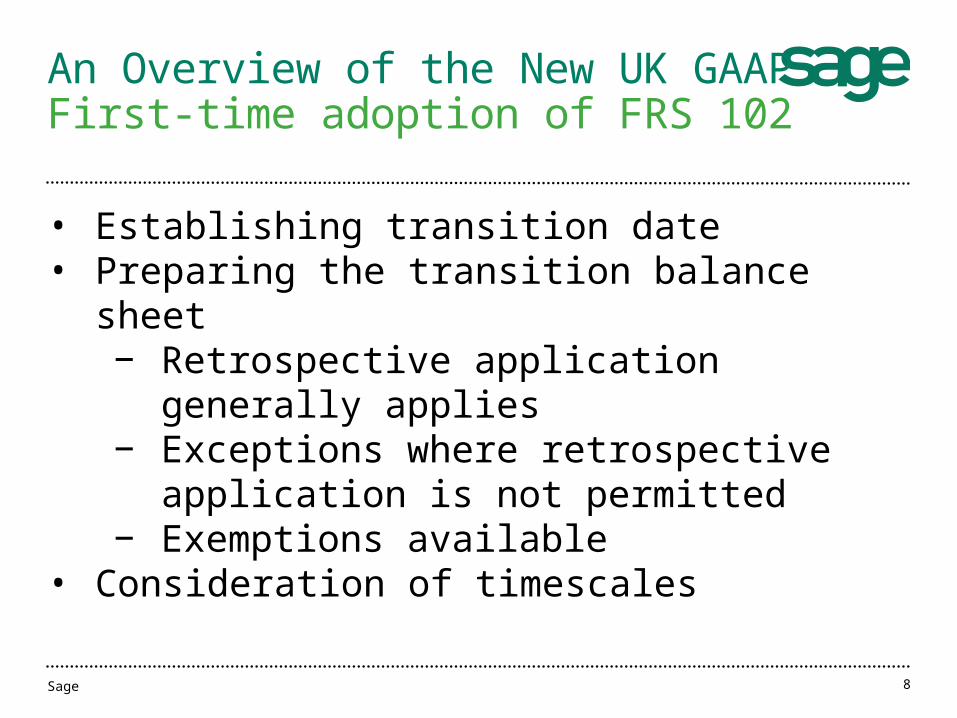

An Overview of the New UK GAAPFirst-time adoption of FRS 102

• Establishing transition date• Preparing the transition balance sheet

− Retrospective application generally applies− Exceptions where retrospective application is

not permitted− Exemptions available

• Consideration of timescales

Sage 9

An Overview of the New UK GAAPReduced disclosures

• Exemptions for qualifying subsidiaries and ultimate parents

• Areas affected:− Cash flow statement− Financial instruments− Share-based payments− Related party transactions− Share capital

• Certain requirements if exemptions are taken

Sage 10

An Overview of the New UK GAAPChanges for small companies

Small companies

Company Law:Small companies

regime

Accounting Standards:

FRSSE

Sage 11

An Overview of the New UK GAAPChanges to company law

• What’s changed?• Size thresholds

• Filing requirements• Disclosure requirements• Amendments for micro-entities• What next?

Small Medium

Net turnover £10.2m (£6.5m) £36m (£25.9m)

Balance sheet total

£5.1m (£3.26m) £18m (£12.9m)

Employees 50 250

Sage 12

An Overview of the New UK GAAPImpact on financial reporting standards

• Continued consistency between revised legal frameworks and the financial reporting frameworksWhy?

• Draft FRS 105• Based on the recognition and measurement

requirements of FRS 102FRED 58

• FRSSE withdrawn• New section of FRS 102 for small entitiesFRED 59

• Draft amendments to FRS 100 and FRS 101FRED 60• Expected to be finalised in July 2015• Mandatory for accounting periods beginning on or after

1 January 2016What next?

Sage 13

An Overview of the New UK GAAPPractical considerations

Staff training Software systems

Cost of transition Client management

An overview of the New UK GAAPSage Support

sage-exchange.com