UK Economic Outlook · UK Economic Outlook November 2019 16 1 UK economic growth has slowed since...

34

November 2019 UK Economic Outlook

Transcript of UK Economic Outlook · UK Economic Outlook November 2019 16 1 UK economic growth has slowed since...

November 2019

UK Economic Outlook

PwC

Contents

1. Global growth trends and prospects2. UK economic trends and prospects3. The Productivity Puzzle revisited: why has UK productivity lagged behind other advanced economies?4. What drives regional productivity gaps across the UK and how can these be closed?

2November 2019UK Economic Outlook

Global growth trends and prospects

PwC

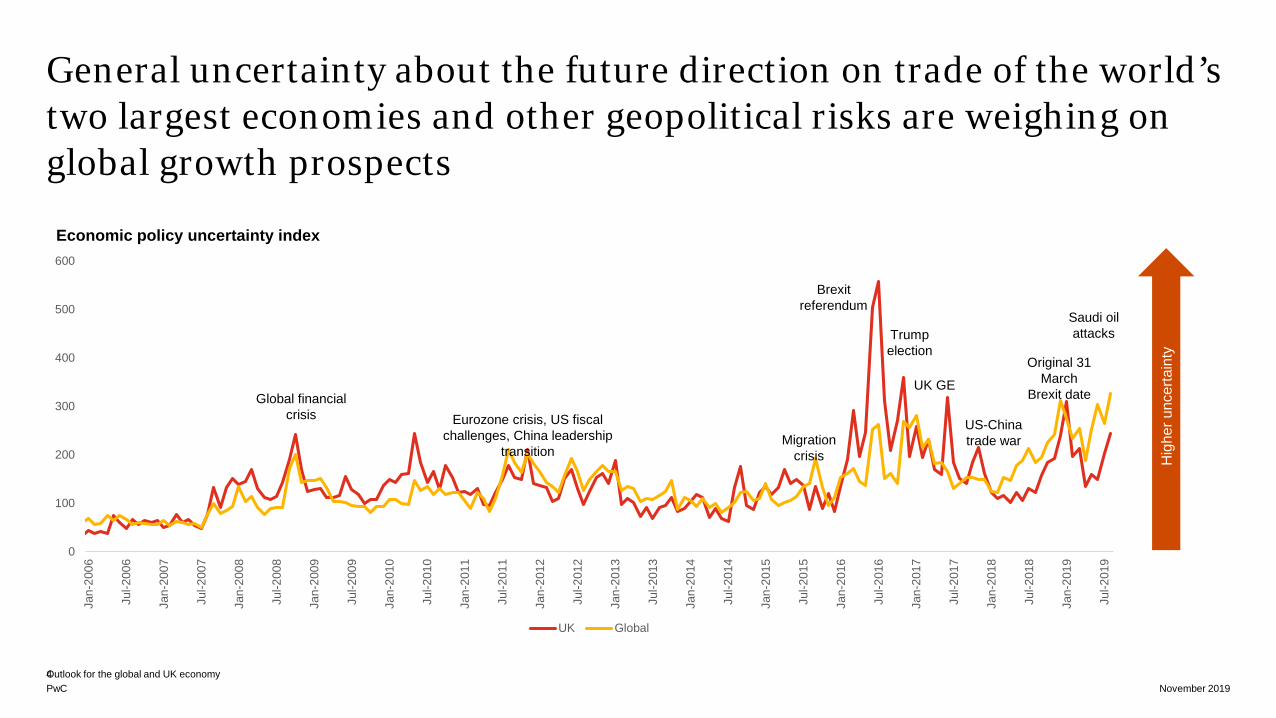

General uncertainty about the future direction on trade of the world’s two largest economies and other geopolitical risks are weighing on global growth prospects

Outlook for the global and UK economyNovember 2019

4

0

100

200

300

400

500

600

Jan-

2006

Jul-2

006

Jan-

2007

Jul-2

007

Jan-

2008

Jul-2

008

Jan-

2009

Jul-2

009

Jan-

2010

Jul-2

010

Jan-

2011

Jul-2

011

Jan-

2012

Jul-2

012

Jan-

2013

Jul-2

013

Jan-

2014

Jul-2

014

Jan-

2015

Jul-2

015

Jan-

2016

Jul-2

016

Jan-

2017

Jul-2

017

Jan-

2018

Jul-2

018

Jan-

2019

Jul-2

019

UK Global

Global financial crisis Eurozone crisis, US fiscal

challenges, China leadership transition

Migration crisis

Brexit referendum

Trump election

UK GE

Original 31 March

Brexit date

US-China trade war

Saudi oil attacks

Economic policy uncertainty index

Hig

her u

ncer

tain

ty

PwC

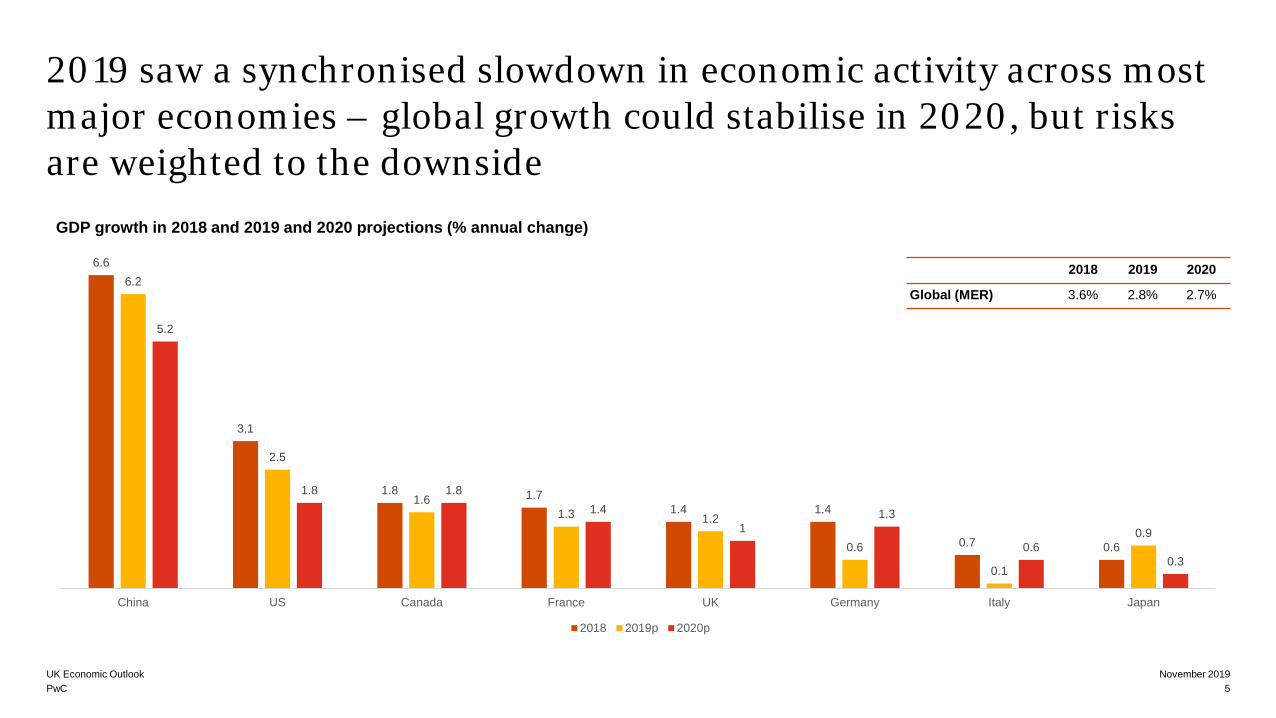

6.6

3.1

1.8 1.71.4 1.4

0.7 0.6

6.2

2.5

1.61.3 1.2

0.6

0.1

0.9

5.2

1.8 1.81.4

11.3

0.60.3

China US Canada France UK Germany Italy Japan

2018 2019p 2020p

2019 saw a synchronised slowdown in economic activity across most major economies – global growth could stabilise in 2020, but risks are weighted to the downside

GDP growth in 2018 and 2019 and 2020 projections (% annual change)

2018 2019 2020

Global (MER) 3.6% 2.8% 2.7%

5November 2019UK Economic Outlook

UK economic trends and prospects

PwC

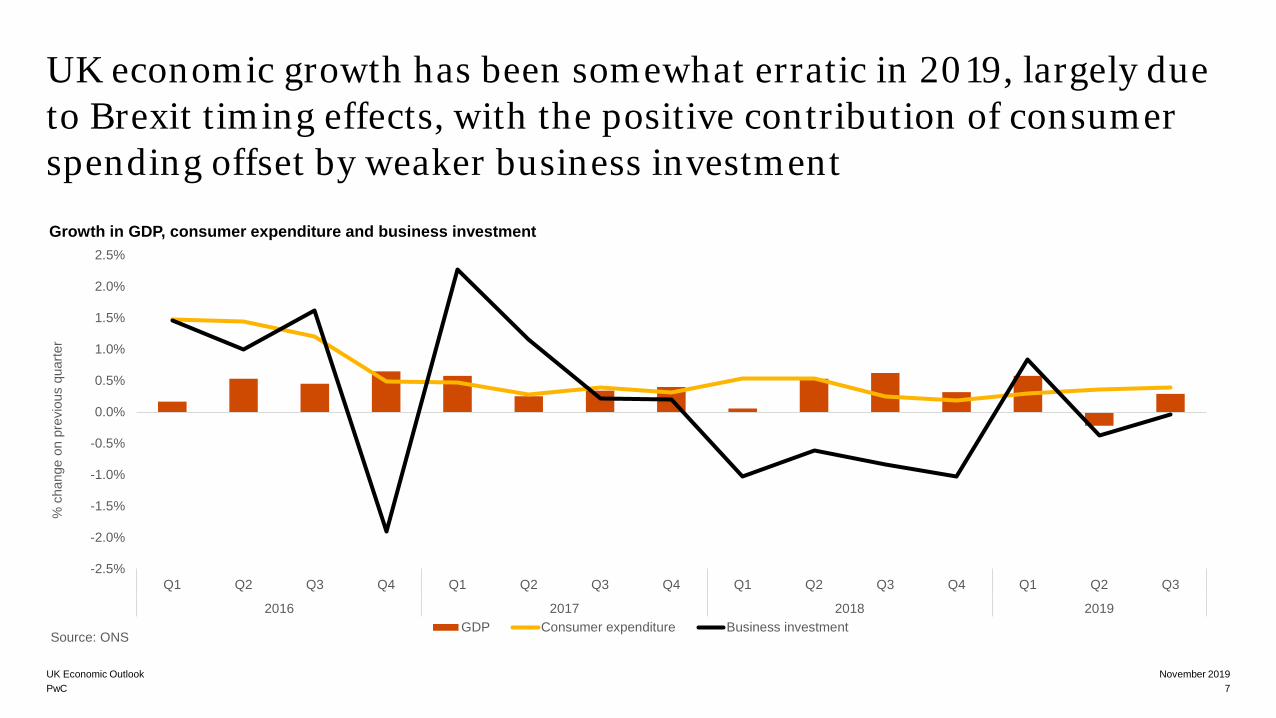

UK economic growth has been somewhat erratic in 2019, largely due to Brexit timing effects, with the positive contribution of consumer spending offset by weaker business investment

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018 2019

% c

hang

e on

pre

viou

s qu

arte

r

Source: ONSGDP Consumer expenditure Business investment

November 2019UK Economic Outlook7

Growth in GDP, consumer expenditure and business investment

PwC

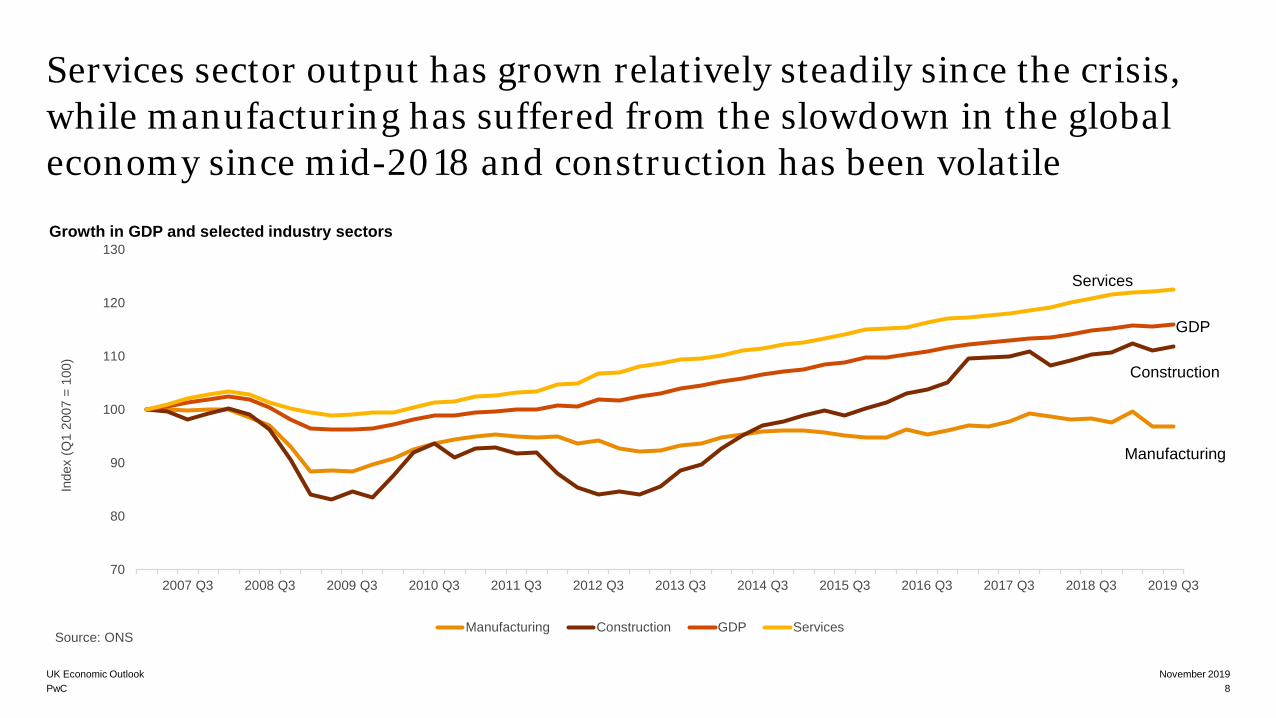

Services sector output has grown relatively steadily since the crisis, while manufacturing has suffered from the slowdown in the global economy since mid-2018 and construction has been volatile

70

80

90

100

110

120

130

2007 Q3 2008 Q3 2009 Q3 2010 Q3 2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3 2017 Q3 2018 Q3 2019 Q3

Inde

x (Q

1 20

07 =

100

)

Source: ONSManufacturing Construction GDP Services

Services

GDP

Manufacturing

Construction

November 2019UK Economic Outlook8

Growth in GDP and selected industry sectors

PwC

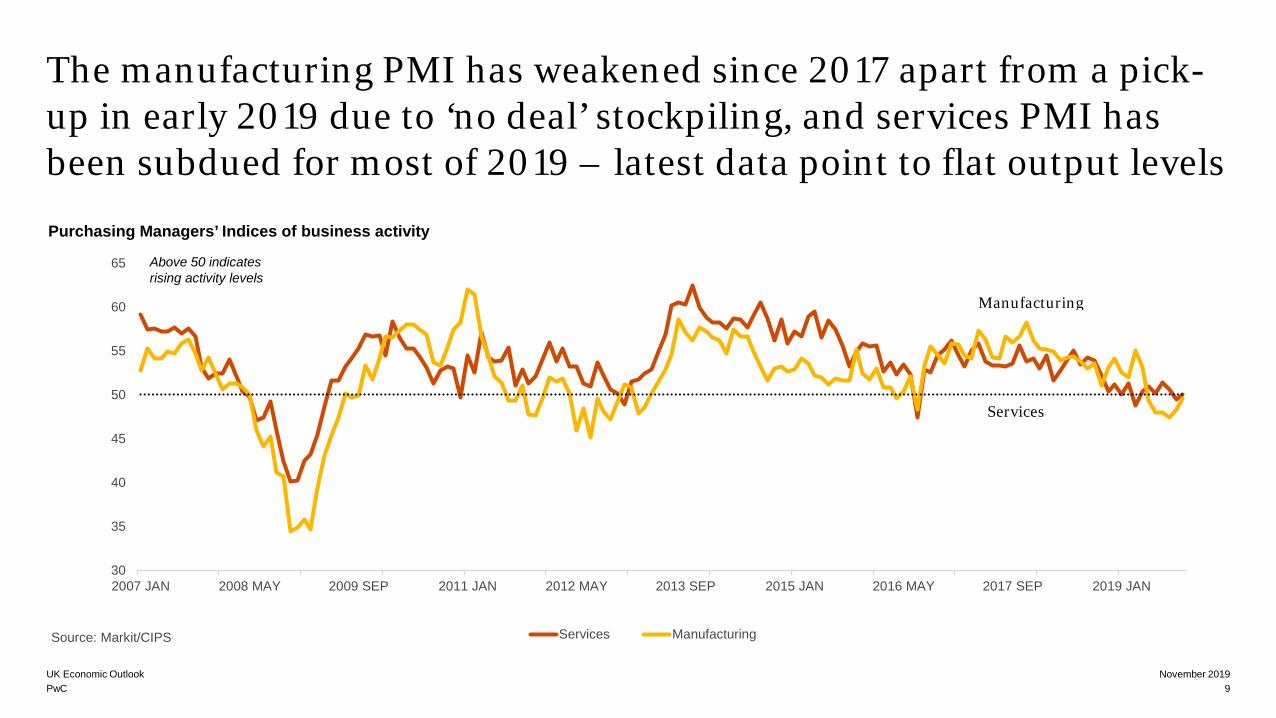

The manufacturing PMI has weakened since 2017 apart from a pick-up in early 2019 due to ‘no deal’ stockpiling, and services PMI has been subdued for most of 2019 – latest data point to flat output levels

November 2019UK Economic Outlook9

Purchasing Managers’ Indices of business activity

30

35

40

45

50

55

60

65

2007 JAN 2008 MAY 2009 SEP 2011 JAN 2012 MAY 2013 SEP 2015 JAN 2016 MAY 2017 SEP 2019 JAN

Source: Markit/CIPS Services Manufacturing

Above 50 indicates rising activity levels

Services

Manufacturing

PwC

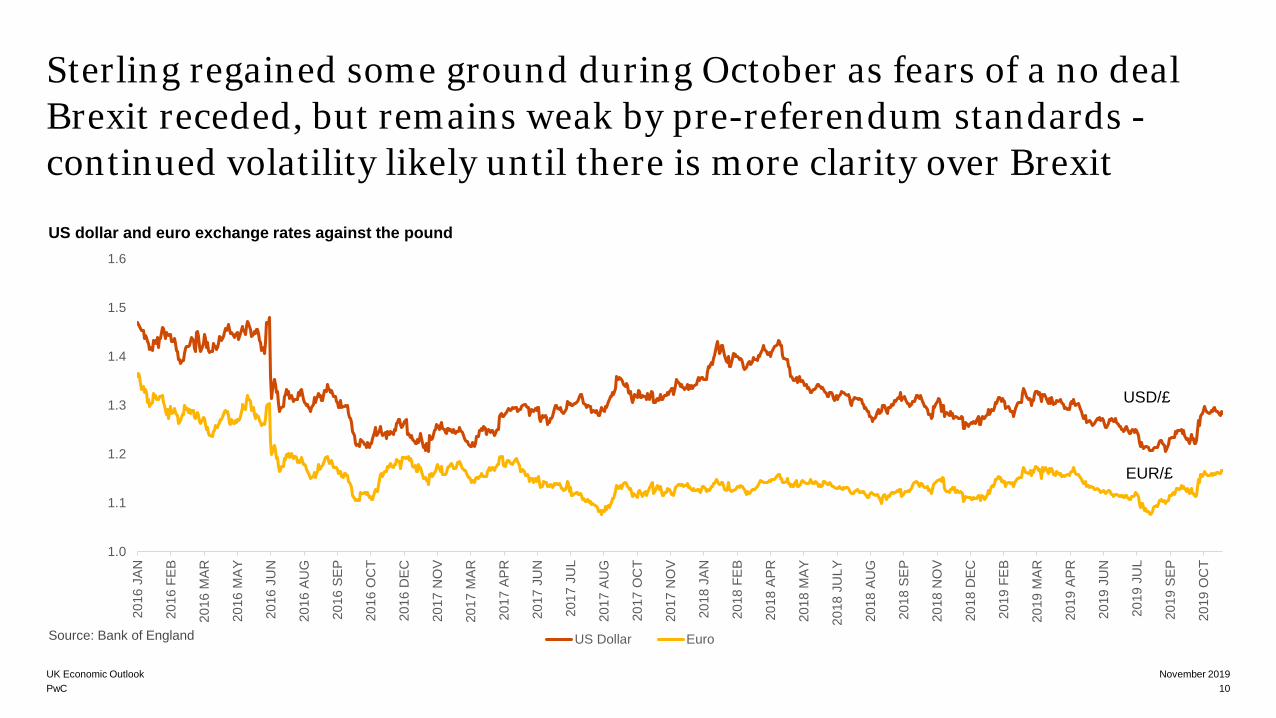

Sterling regained some ground during October as fears of a no deal Brexit receded, but remains weak by pre-referendum standards -continued volatility likely until there is more clarity over Brexit

November 2019UK Economic Outlook10

US dollar and euro exchange rates against the pound

1.0

1.1

1.2

1.3

1.4

1.5

1.6

2016

JAN

2016

FEB

2016

MAR

2016

MAY

2016

JU

N

2016

AU

G

2016

SEP

2016

OC

T

2016

DEC

2017

NO

V

2017

MAR

2017

APR

2017

JU

N

2017

JU

L

2017

AU

G

2017

OC

T

2017

NO

V

2018

JAN

2018

FEB

2018

APR

2018

MAY

2018

JU

LY

2018

AU

G

2018

SEP

2018

NO

V

2018

DEC

2019

FEB

2019

MAR

2019

APR

2019

JU

N

2019

JU

L

2019

SEP

2019

OC

T

US Dollar Euro

USD/£

EUR/£

Source: Bank of England

PwC

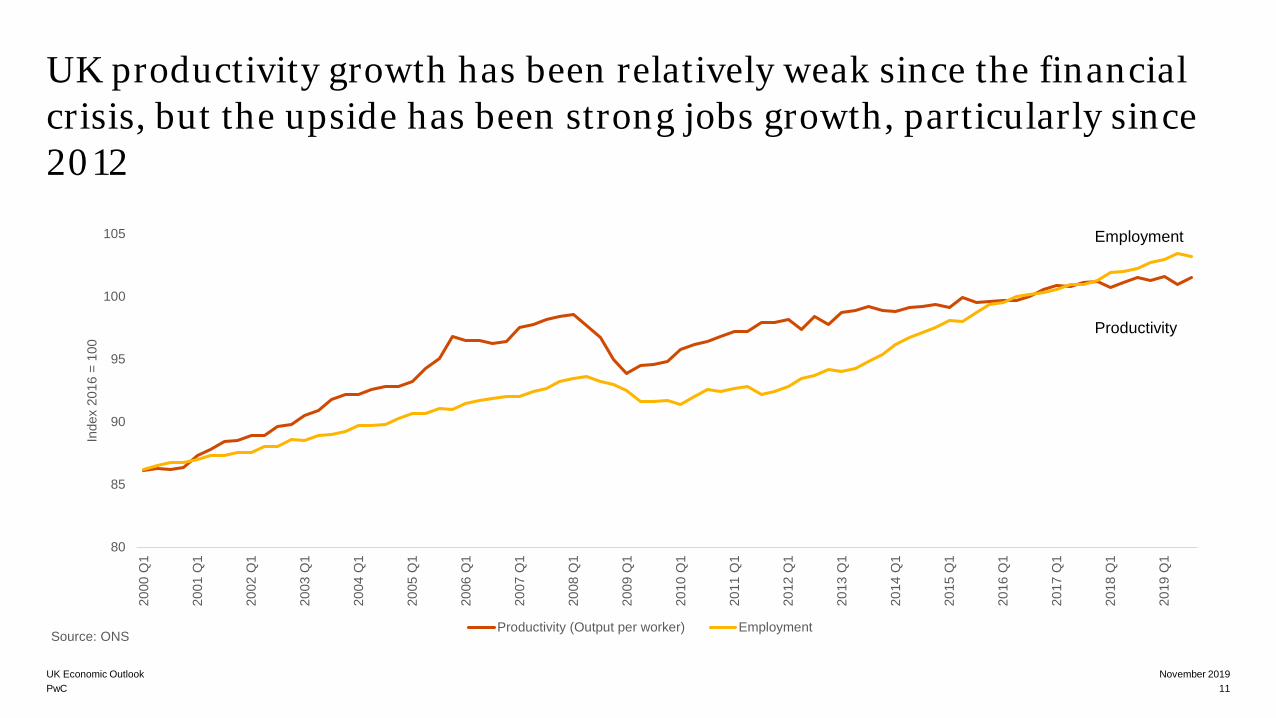

UK productivity growth has been relatively weak since the financial crisis, but the upside has been strong jobs growth, particularly since 2012

November 2019UK Economic Outlook11

Employment

Productivity

80

85

90

95

100

105

2000

Q1

2001

Q1

2002

Q1

2003

Q1

2004

Q1

2005

Q1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

Q1

2018

Q1

2019

Q1

Inde

x 20

16 =

100

Source: ONSProductivity (Output per worker) Employment

PwC

Projections

-8%

-6%

-4%

-2%

0%

2%

4%

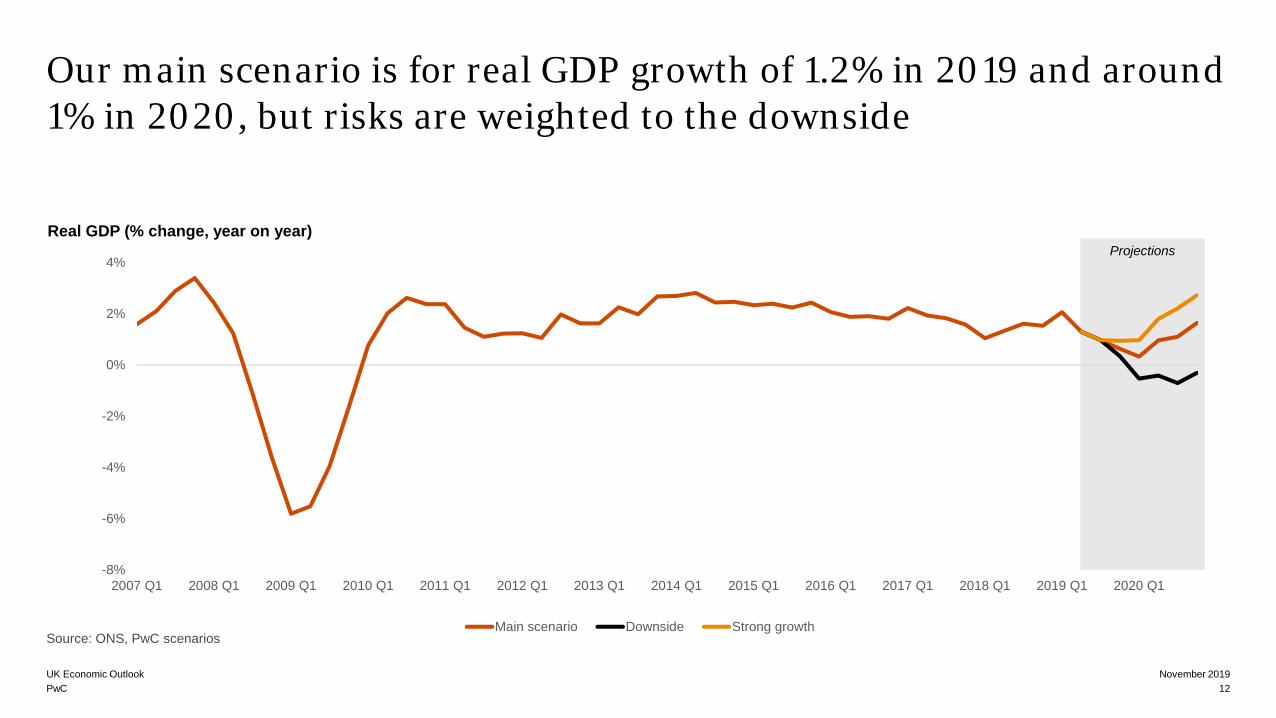

2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020 Q1

Main scenario Downside Strong growthSource: ONS, PwC scenarios

Our main scenario is for real GDP growth of 1.2% in 2019 and around 1% in 2020, but risks are weighted to the downside

November 2019UK Economic Outlook12

Real GDP (% change, year on year)

PwC

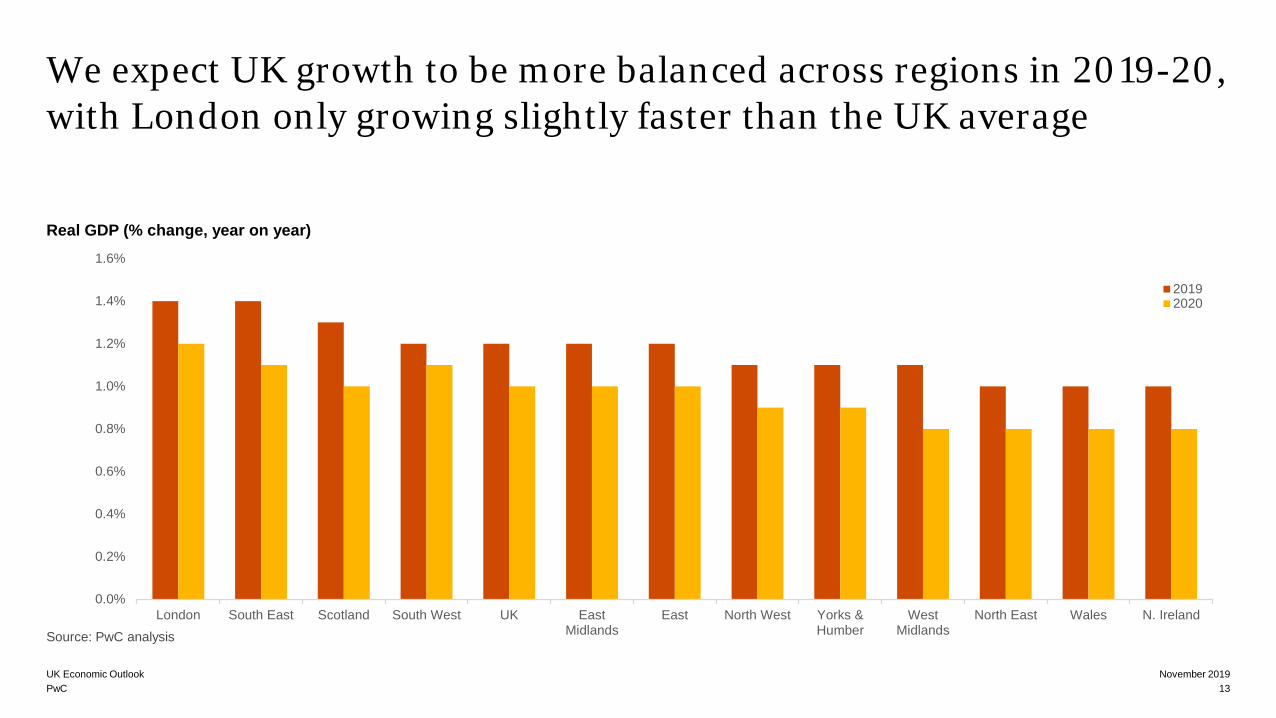

We expect UK growth to be more balanced across regions in 2019-20, with London only growing slightly faster than the UK average

November 2019UK Economic Outlook13

Real GDP (% change, year on year)

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

London South East Scotland South West UK EastMidlands

East North West Yorks &Humber

WestMidlands

North East Wales N. Ireland

20192020

Source: PwC analysis

PwC

Projections

0%

1%

2%

3%

4%

5%

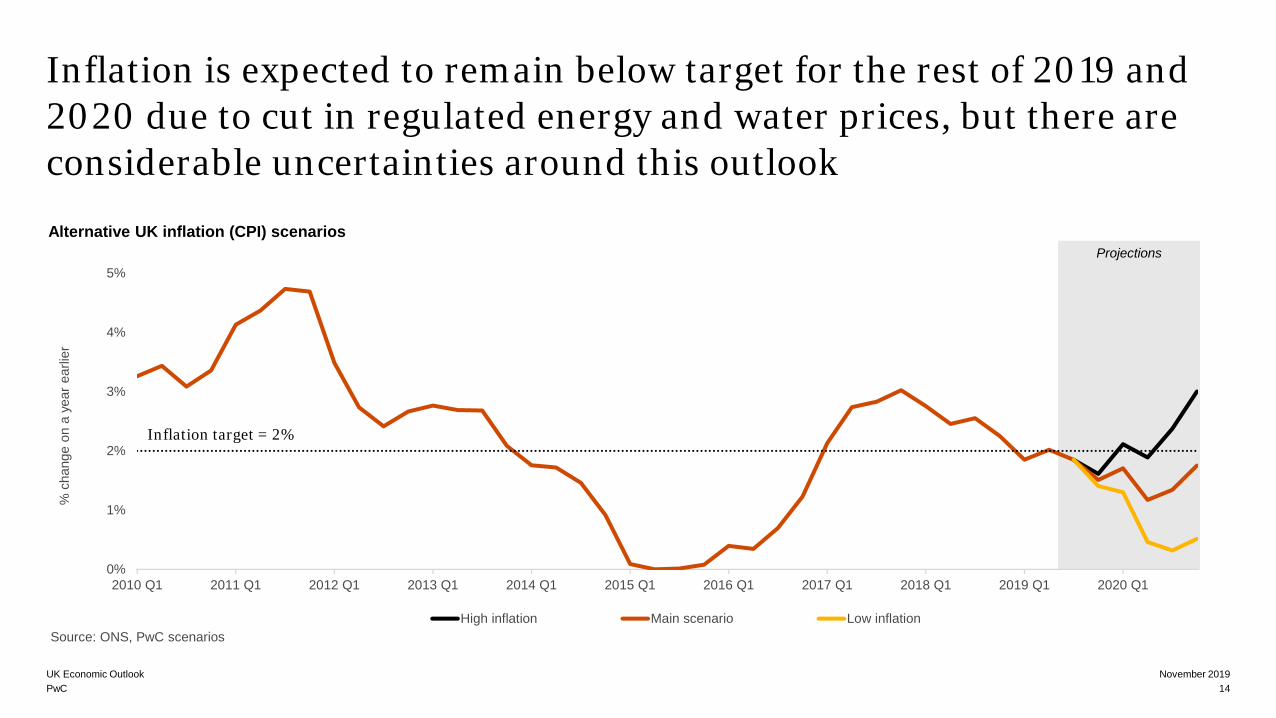

2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020 Q1

% c

hang

e on

a y

ear e

arlie

r

Source: ONS, PwC scenariosHigh inflation Main scenario Low inflation

Inflation target = 2%

Inflation is expected to remain below target for the rest of 2019 and 2020 due to cut in regulated energy and water prices, but there are considerable uncertainties around this outlook

November 2019UK Economic Outlook14

Alternative UK inflation (CPI) scenarios

PwC

Projections

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

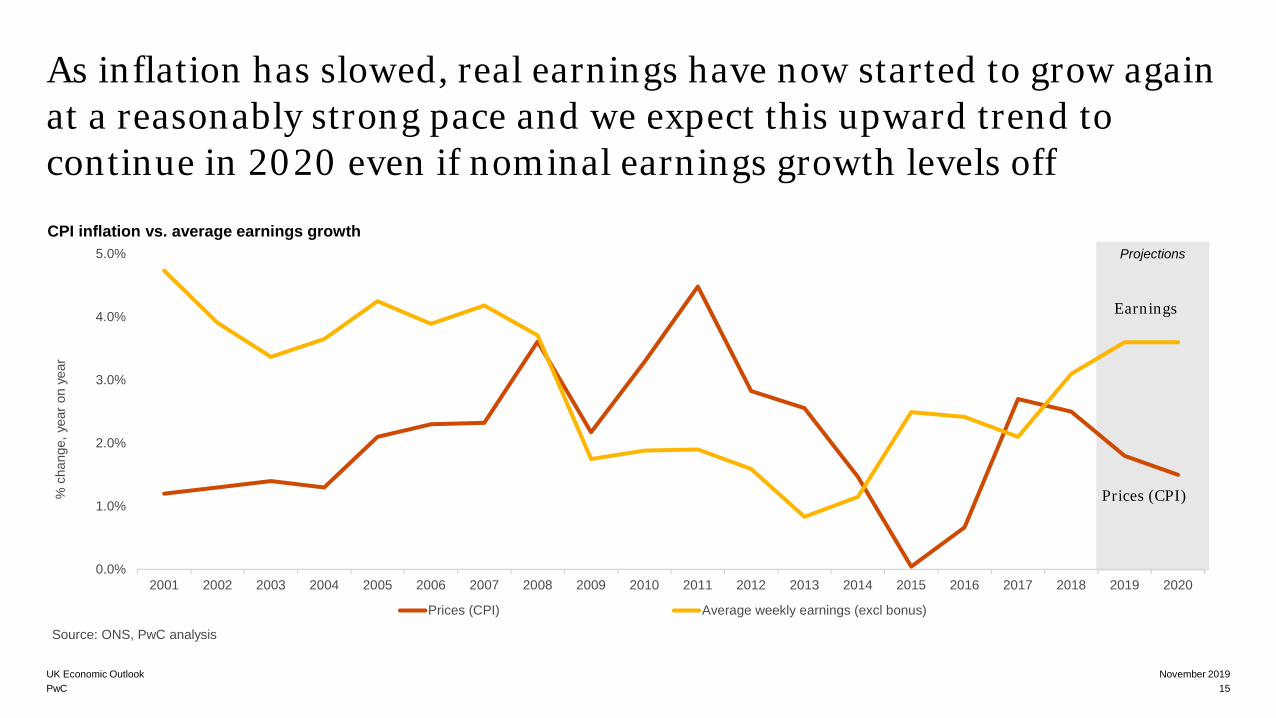

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

% c

hang

e, y

ear o

n ye

ar

Source: ONS, PwC analysis

Prices (CPI) Average weekly earnings (excl bonus)

Prices (CPI)

Earnings

As inflation has slowed, real earnings have now started to grow again at a reasonably strong pace and we expect this upward trend to continue in 2020 even if nominal earnings growth levels off

November 2019UK Economic Outlook15

CPI inflation vs. average earnings growth

PwC

Summary: UK economic prospects and policy implications

November 2019UK Economic Outlook16

1UK economic growth has slowed since early 2018 as Brexit-related uncertainty has dampened business investment, but consumer spending has held up better so far, supported by a recovery in real wages.

4The Bank of England is expected tokeep interest rates on hold until greater clarity has been provided on Brexit and the wider global economic outlook. The next move in rates could be either up or down depending on how events develop.

2Our main scenario is for UK GDP growth to remain subdued, growing by around 1% in 2020, assuming an orderly Brexit and moderate global growth. However, risks are weighted to the downside.

5There are particularly large uncertainties around UK economic projections at present. Organisations should stress test their business and investment plans against alternative economic and political scenarios.

3Most industry sectors are projected tosee relatively modest growth in 2019-20, although short-term trends remain volatile and highly dependent on how events develop on Brexit. Manufacturing also faces pressures from the downturn in global and particularly euro area growth over the past year owing to heightened trade tensions.

The Productivity Puzzle revisited: why has UK productivity lagged behind other advanced economies?

PwC

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

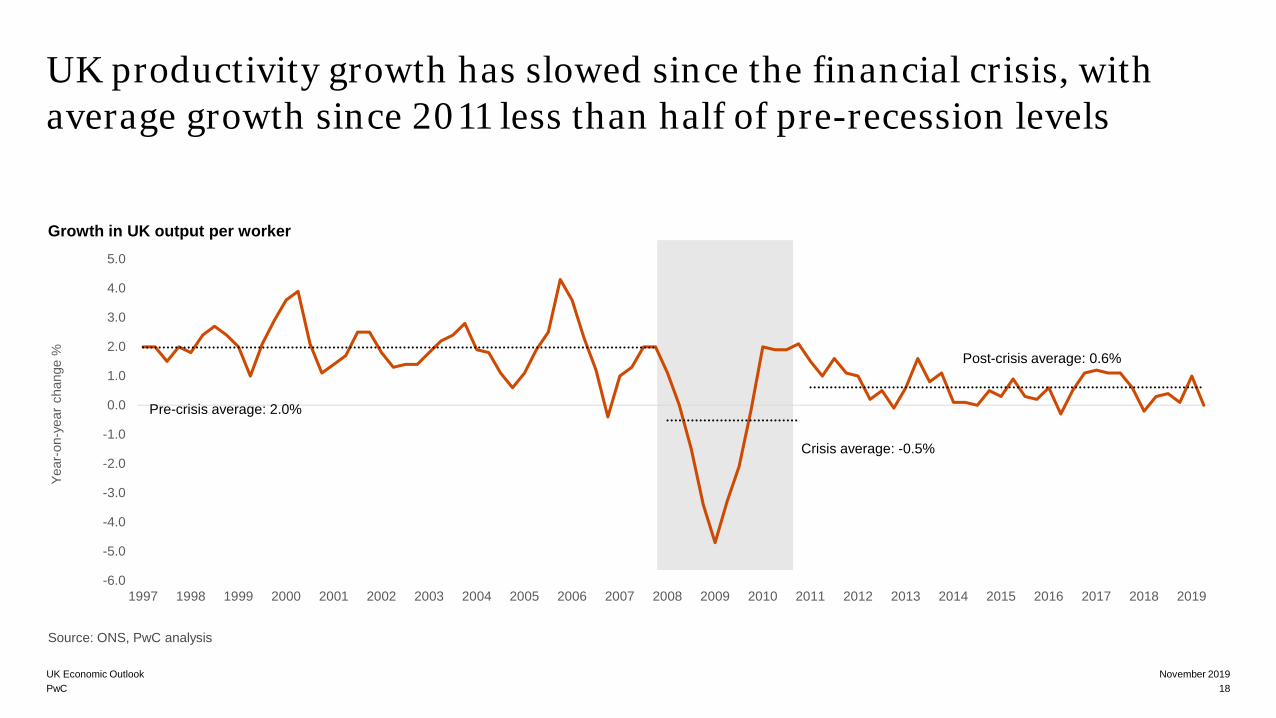

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Year

-on-

year

cha

nge

% Post-crisis average: 0.6%

Crisis average: -0.5%

UK productivity growth has slowed since the financial crisis, with average growth since 2011 less than half of pre-recession levels

November 2019UK Economic Outlook18

Source: ONS, PwC analysis

Pre-crisis average: 2.0%

Growth in UK output per worker

PwC

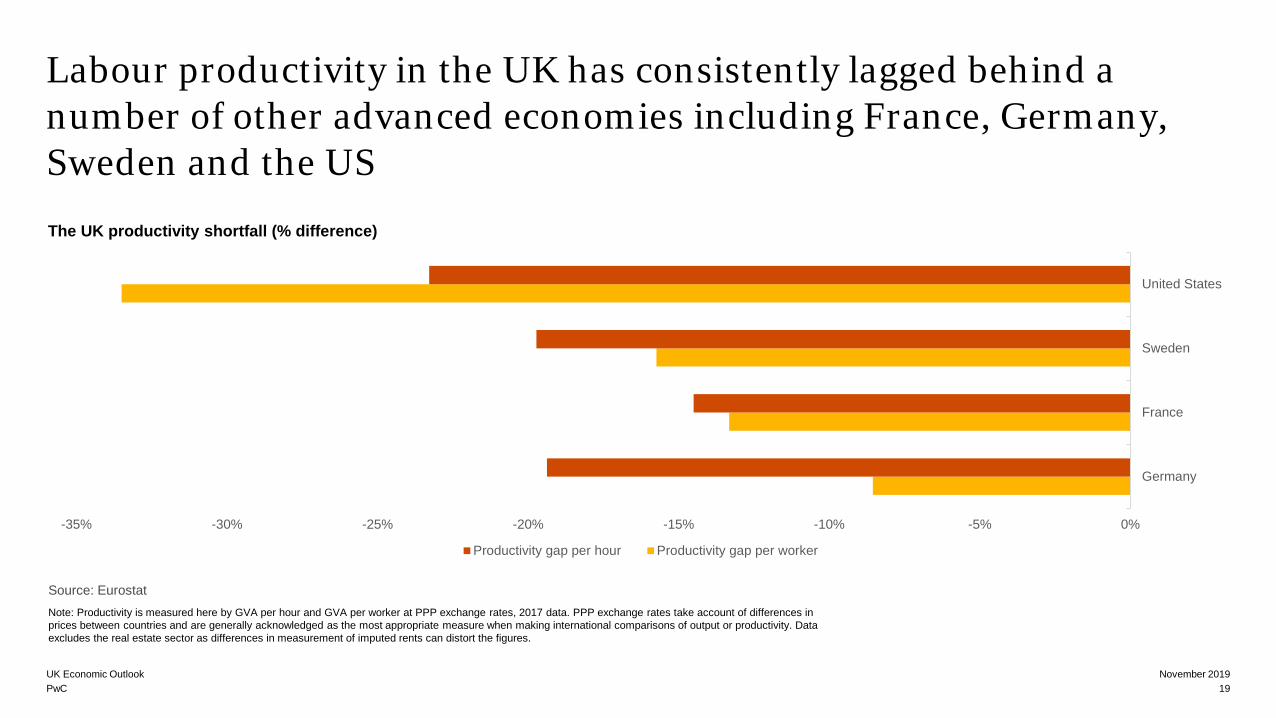

Labour productivity in the UK has consistently lagged behind a number of other advanced economies including France, Germany, Sweden and the US

November 2019UK Economic Outlook19

Source: EurostatNote: Productivity is measured here by GVA per hour and GVA per worker at PPP exchange rates, 2017 data. PPP exchange rates take account of differences in prices between countries and are generally acknowledged as the most appropriate measure when making international comparisons of output or productivity. Data excludes the real estate sector as differences in measurement of imputed rents can distort the figures.

The UK productivity shortfall (% difference)

-35% -30% -25% -20% -15% -10% -5% 0%

Germany

France

Sweden

United States

Productivity gap per hour Productivity gap per worker

PwC

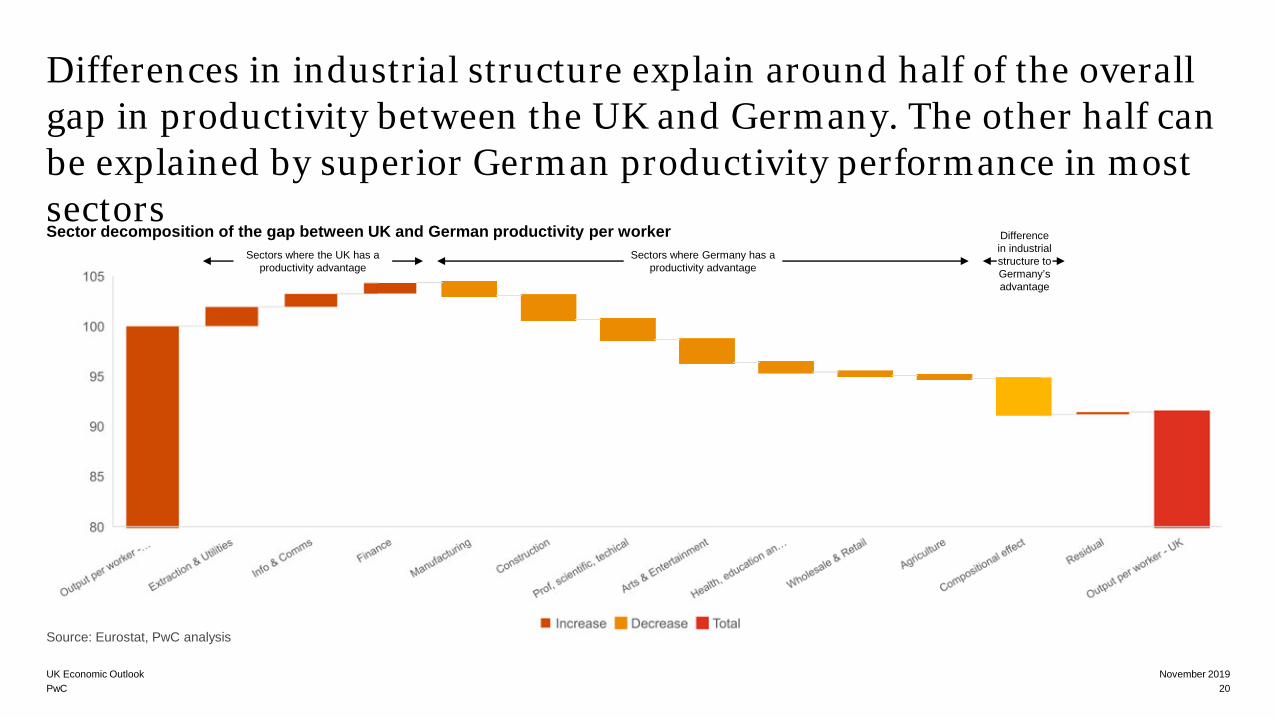

Differences in industrial structure explain around half of the overall gap in productivity between the UK and Germany. The other half can be explained by superior German productivity performance in most sectors

November 2019UK Economic Outlook20

Source: Eurostat, PwC analysis

Sector decomposition of the gap between UK and German productivity per worker Sectors where the UK has a

productivity advantageSectors where Germany has a

productivity advantage

Difference in industrial structure to Germany’s advantage

PwC

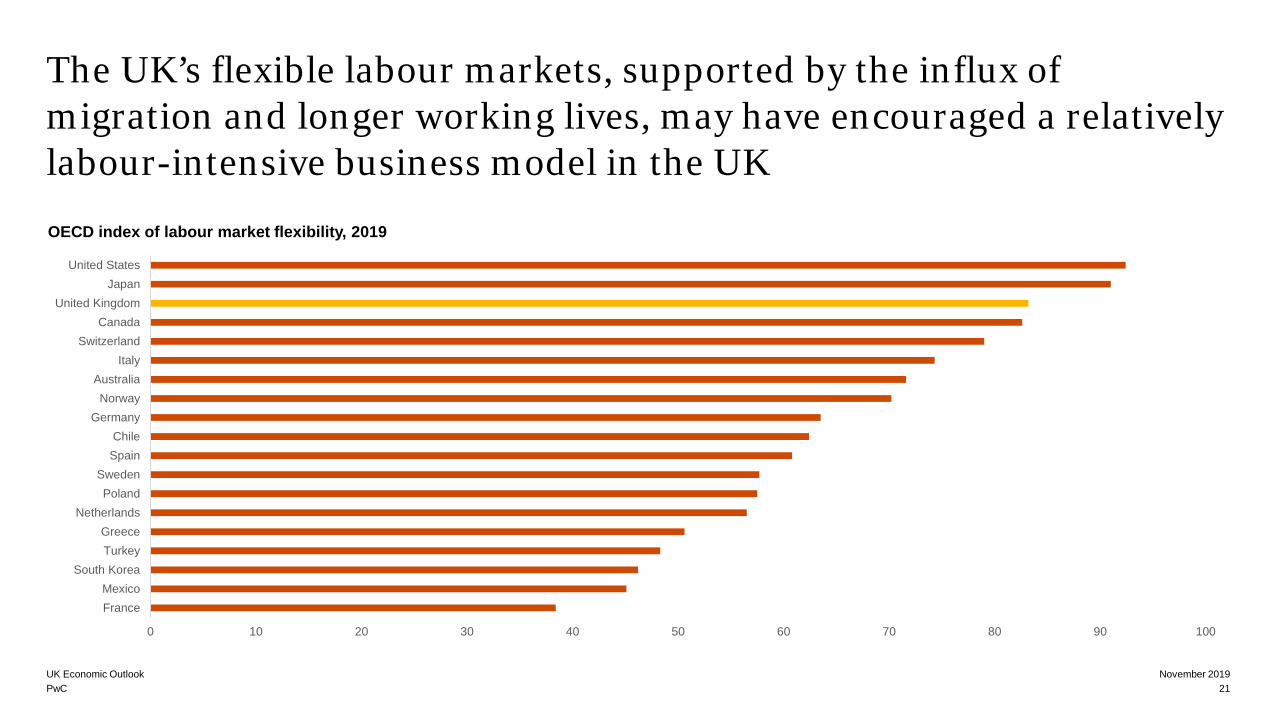

The UK’s flexible labour markets, supported by the influx of migration and longer working lives, may have encouraged a relatively labour-intensive business model in the UK

November 2019UK Economic Outlook21

0 10 20 30 40 50 60 70 80 90 100

United StatesJapan

United KingdomCanada

SwitzerlandItaly

AustraliaNorway

GermanyChile

SpainSwedenPoland

NetherlandsGreeceTurkey

South KoreaMexicoFrance

OECD index of labour market flexibility, 2019

PwC

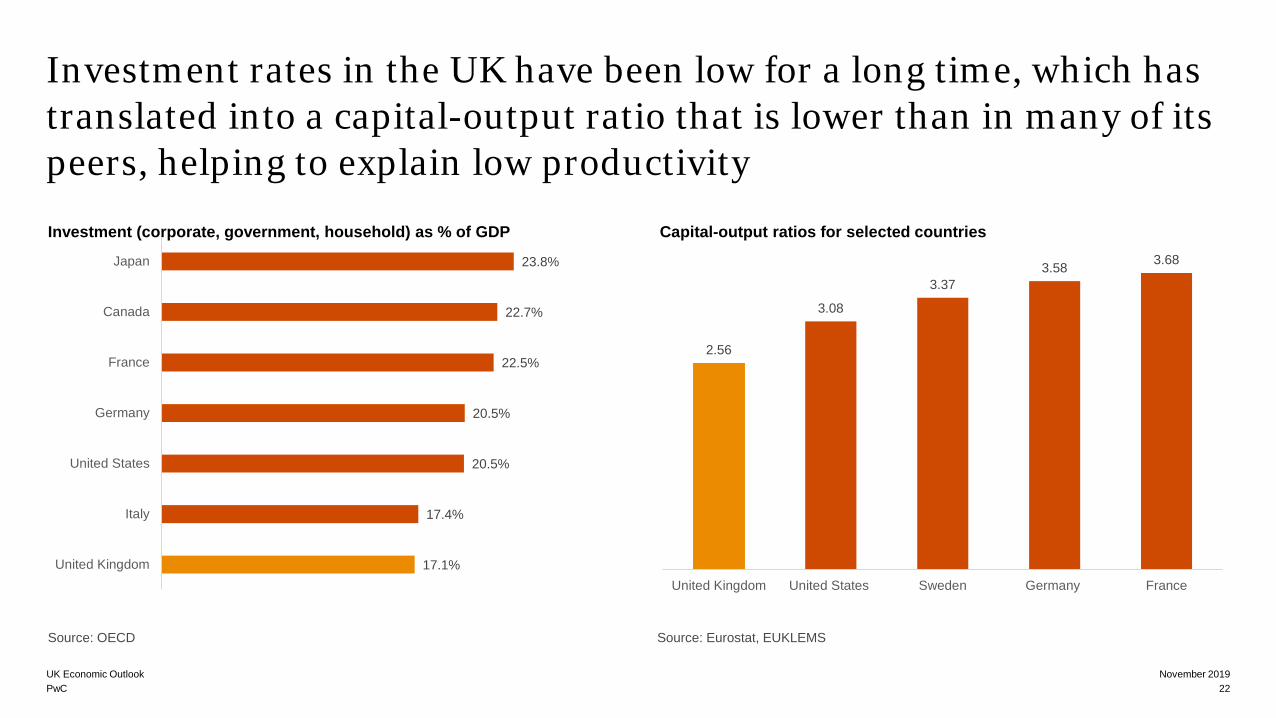

Investment rates in the UK have been low for a long time, which has translated into a capital-output ratio that is lower than in many of its peers, helping to explain low productivity

23.8%

22.7%

22.5%

20.5%

20.5%

17.4%

17.1%

Japan

Canada

France

Germany

United States

Italy

United Kingdom

2.56

3.08

3.373.58 3.68

United Kingdom United States Sweden Germany France

November 2019UK Economic Outlook22

Source: OECD

Capital-output ratios for selected countriesInvestment (corporate, government, household) as % of GDP

Source: Eurostat, EUKLEMS

PwC

300 350 400 450 500 550

Japan

Canada

Finland

Korea

Germany

Switzerland

Denmark

Australia

United Kingdom

Sweden

France

Spain

United States

Italy

Mathematics Reading Science

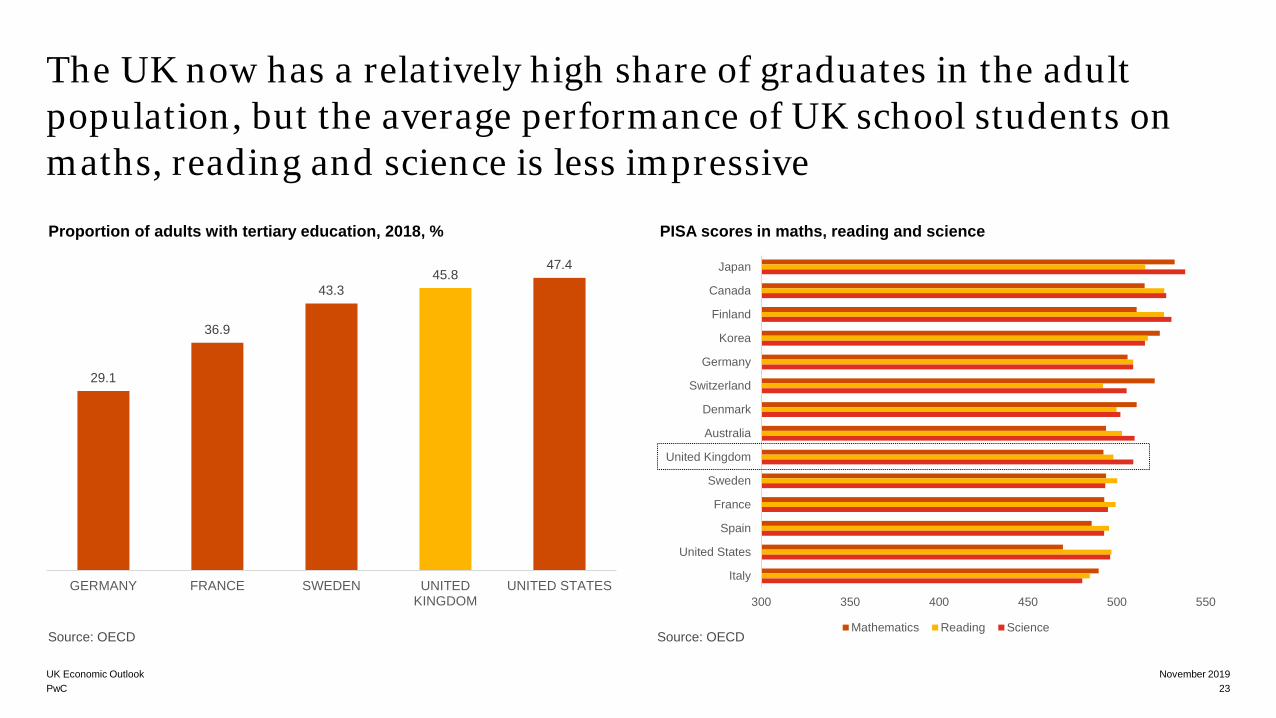

The UK now has a relatively high share of graduates in the adult population, but the average performance of UK school students on maths, reading and science is less impressive

29.1

36.9

43.345.8

47.4

GERMANY FRANCE SWEDEN UNITEDKINGDOM

UNITED STATES

November 2019UK Economic Outlook23

Source: OECD

Proportion of adults with tertiary education, 2018, % PISA scores in maths, reading and science

Source: OECD

PwC

Summary: International productivity analysis and policy implications

November 2019UK Economic Outlook24

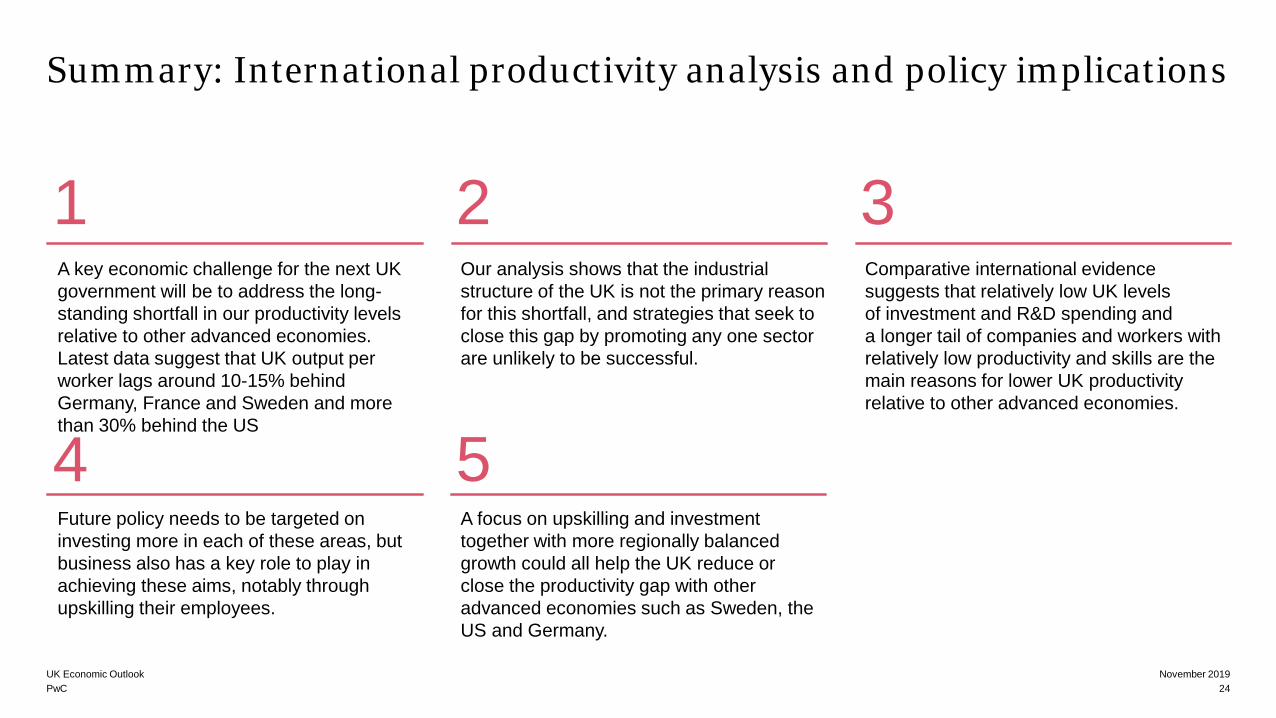

1A key economic challenge for the next UK government will be to address the long-standing shortfall in our productivity levels relative to other advanced economies. Latest data suggest that UK output per worker lags around 10-15% behind Germany, France and Sweden and more than 30% behind the US

4Future policy needs to be targeted on investing more in each of these areas, but business also has a key role to play in achieving these aims, notably through upskilling their employees.

2Our analysis shows that the industrial structure of the UK is not the primary reason for this shortfall, and strategies that seek to close this gap by promoting any one sector are unlikely to be successful.

5A focus on upskilling and investmenttogether with more regionally balanced growth could all help the UK reduce or close the productivity gap with other advanced economies such as Sweden, the US and Germany.

3Comparative international evidencesuggests that relatively low UK levelsof investment and R&D spending anda longer tail of companies and workers with relatively low productivity and skills are the main reasons for lower UK productivity relative to other advanced economies.

What drives regional productivity gaps across the UK and how can these be closed?

PwC

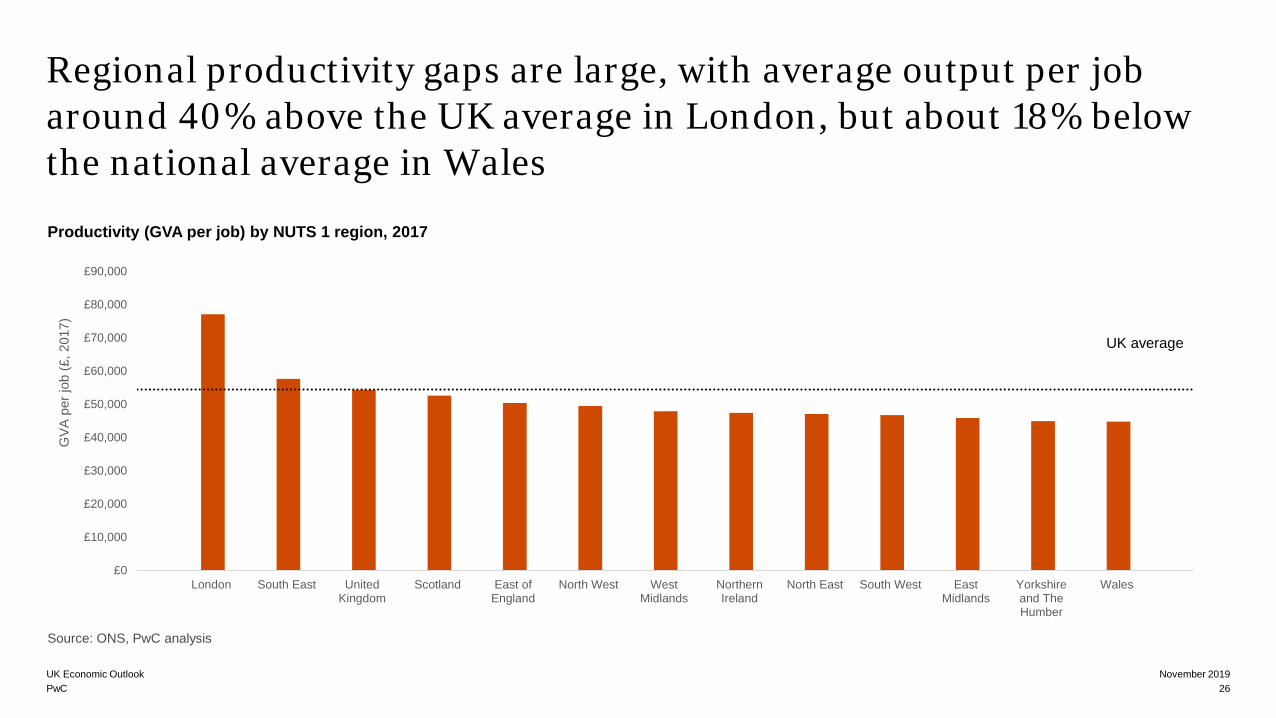

Regional productivity gaps are large, with average output per job around 40% above the UK average in London, but about 18% below the national average in Wales

November 2019UK Economic Outlook26

£0

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

£90,000

London South East UnitedKingdom

Scotland East ofEngland

North West WestMidlands

NorthernIreland

North East South West EastMidlands

Yorkshireand TheHumber

Wales

GVA

per

job

(£, 2

017)

Productivity (GVA per job) by NUTS 1 region, 2017

UK average

Source: ONS, PwC analysis

PwC

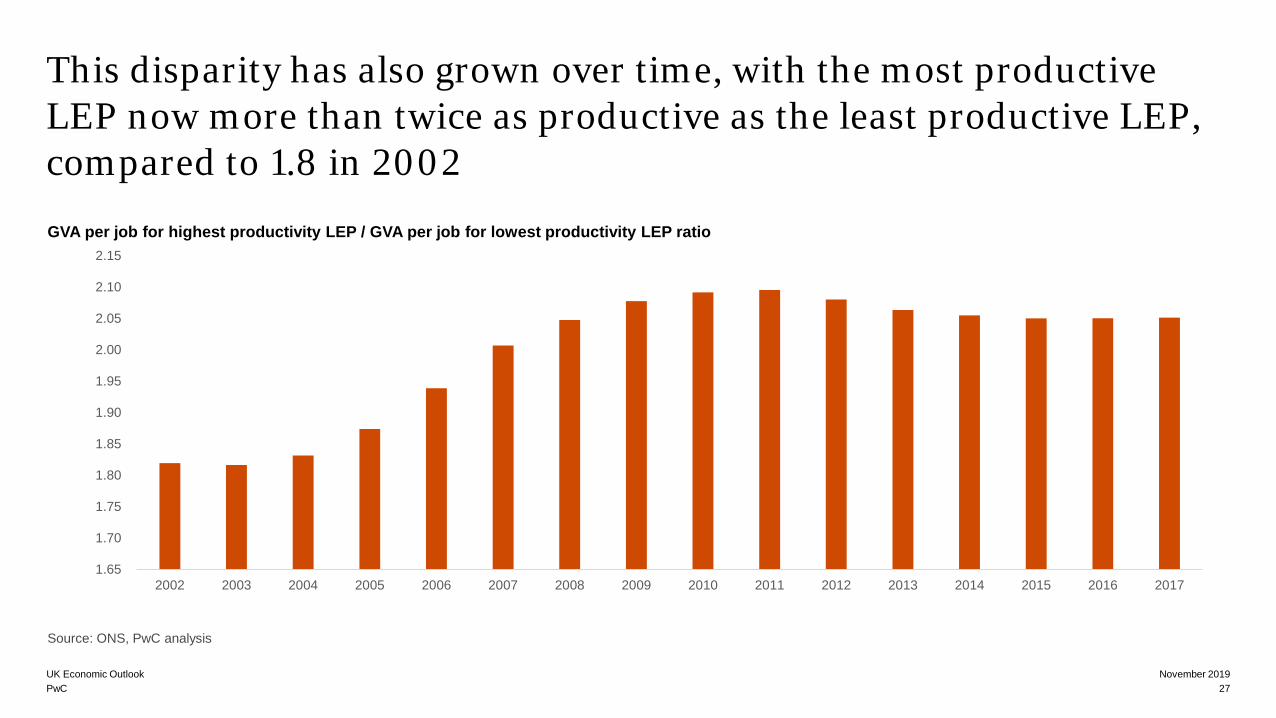

This disparity has also grown over time, with the most productive LEP now more than twice as productive as the least productive LEP, compared to 1.8 in 2002

November 2019UK Economic Outlook27

1.65

1.70

1.75

1.80

1.85

1.90

1.95

2.00

2.05

2.10

2.15

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GVA per job for highest productivity LEP / GVA per job for lowest productivity LEP ratio

Source: ONS, PwC analysis

PwC

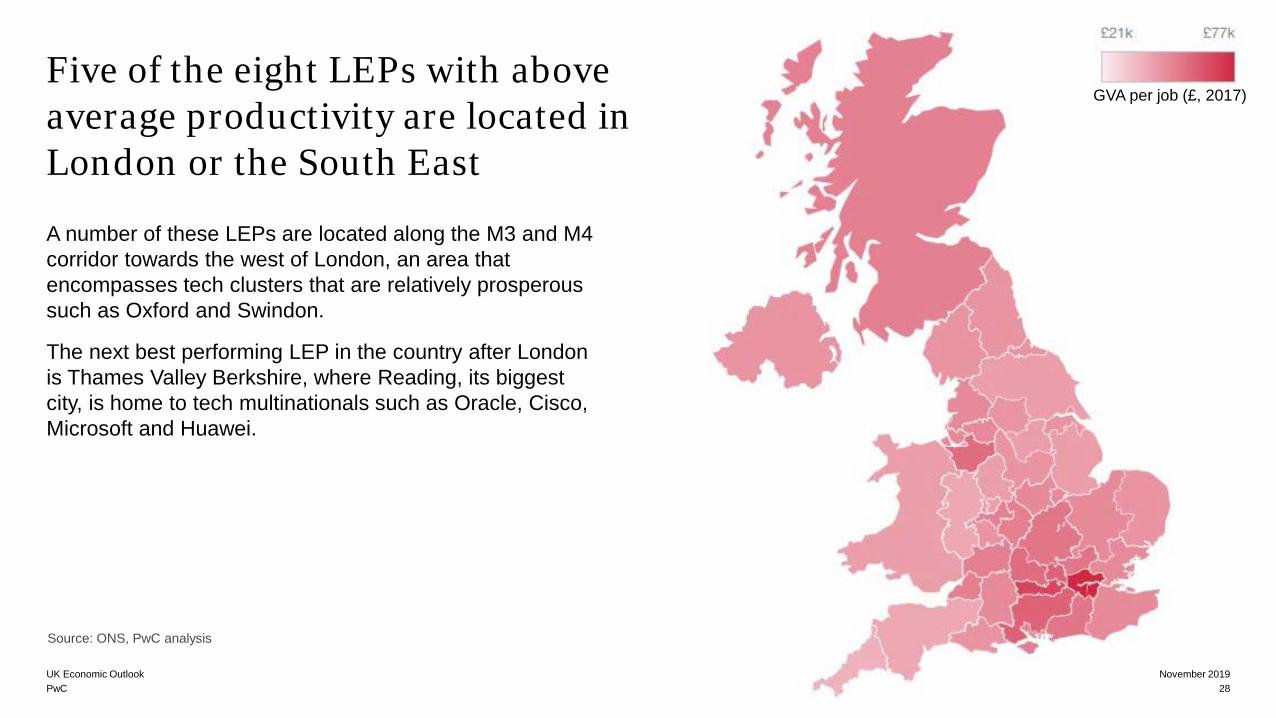

Five of the eight LEPs with above average productivity are located in London or the South East

A number of these LEPs are located along the M3 and M4 corridor towards the west of London, an area that encompasses tech clusters that are relatively prosperous such as Oxford and Swindon.

The next best performing LEP in the country after London is Thames Valley Berkshire, where Reading, its biggest city, is home to tech multinationals such as Oracle, Cisco, Microsoft and Huawei.

November 2019UK Economic Outlook28

GVA per job (£, 2017)

Source: ONS, PwC analysis

PwC

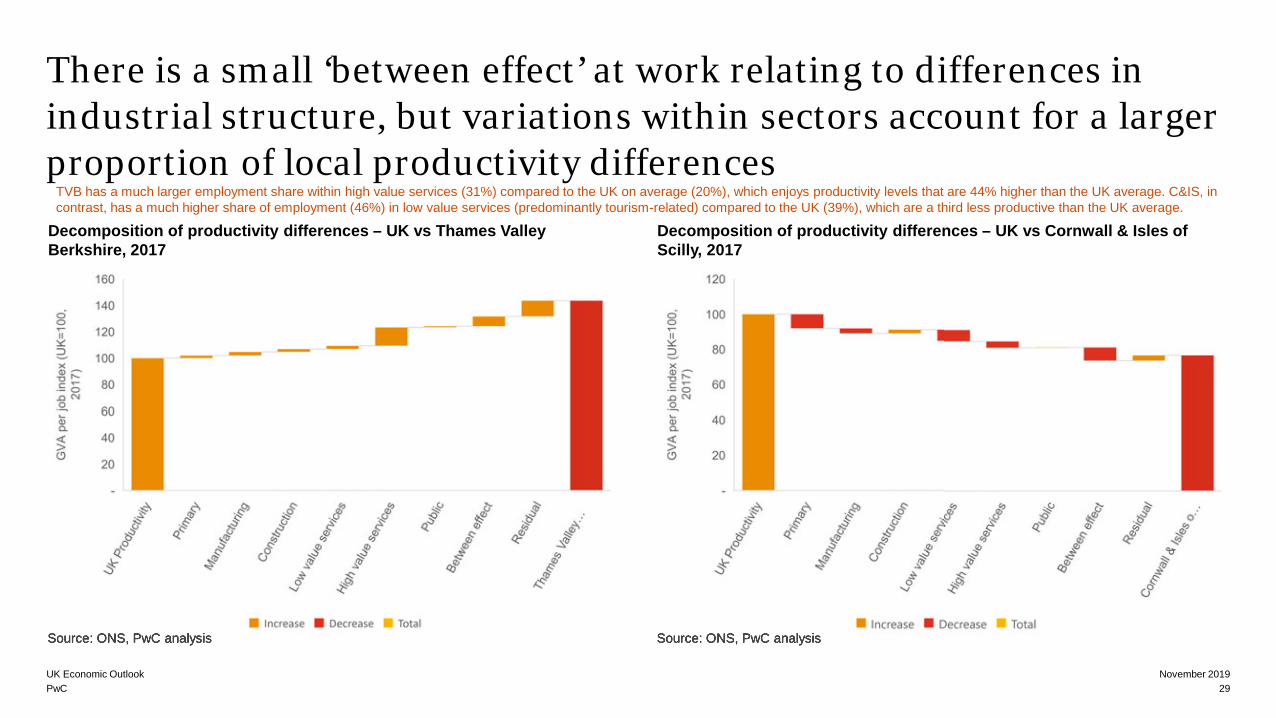

There is a small ‘between effect’ at work relating to differences in industrial structure, but variations within sectors account for a larger proportion of local productivity differences

November 2019UK Economic Outlook29

Decomposition of productivity differences – UK vs Thames Valley Berkshire, 2017

Source: ONS, PwC analysis Source: ONS, PwC analysis

Decomposition of productivity differences – UK vs Cornwall & Isles of Scilly, 2017

Source: ONS, PwC analysisSource: ONS, PwC analysis

TVB has a much larger employment share within high value services (31%) compared to the UK on average (20%), which enjoys productivity levels that are 44% higher than the UK average. C&IS, in contrast, has a much higher share of employment (46%) in low value services (predominantly tourism-related) compared to the UK (39%), which are a third less productive than the UK average.

PwC

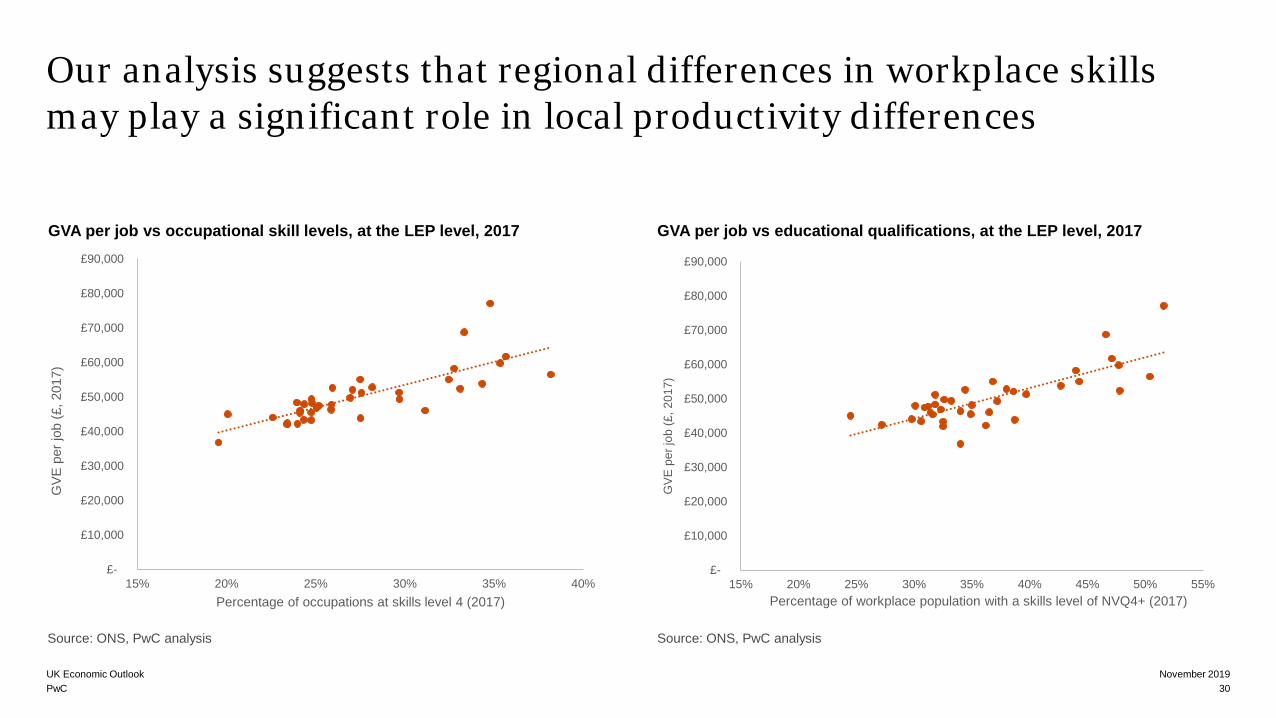

Our analysis suggests that regional differences in workplace skills may play a significant role in local productivity differences

November 2019UK Economic Outlook30

£-

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

£90,000

15% 20% 25% 30% 35% 40%

GVE

per

job

(£, 2

017)

Percentage of occupations at skills level 4 (2017)

£-

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

£90,000

15% 20% 25% 30% 35% 40% 45% 50% 55%

GVE

per

job

(£, 2

017)

Percentage of workplace population with a skills level of NVQ4+ (2017)

GVA per job vs occupational skill levels, at the LEP level, 2017 GVA per job vs educational qualifications, at the LEP level, 2017

Source: ONS, PwC analysis Source: ONS, PwC analysis

PwC

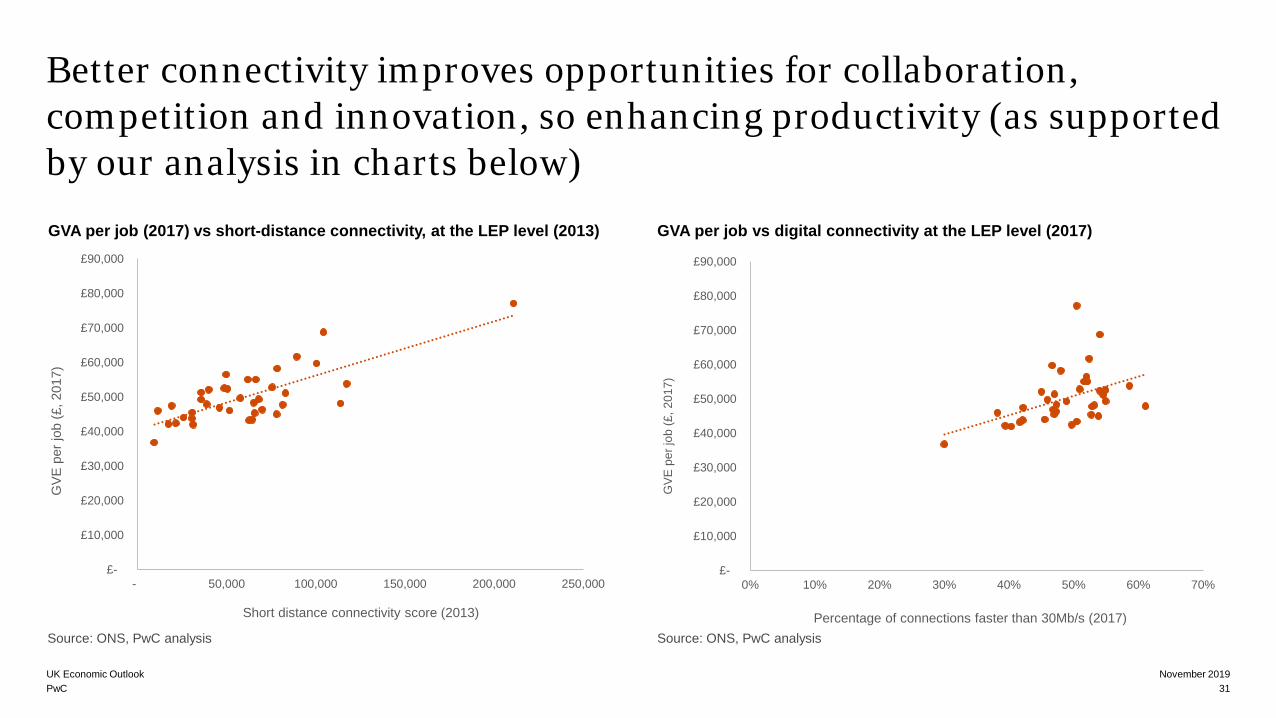

Better connectivity improves opportunities for collaboration, competition and innovation, so enhancing productivity (as supported by our analysis in charts below)

November 2019UK Economic Outlook31

£-

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

£90,000

- 50,000 100,000 150,000 200,000 250,000

GVE

per

job

(£, 2

017)

Short distance connectivity score (2013)

£-

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

£70,000

£80,000

£90,000

0% 10% 20% 30% 40% 50% 60% 70%

GVE

per

job

(£, 2

017)

Percentage of connections faster than 30Mb/s (2017)

GVA per job (2017) vs short-distance connectivity, at the LEP level (2013) GVA per job vs digital connectivity at the LEP level (2017)

Source: ONS, PwC analysis Source: ONS, PwC analysis

PwC

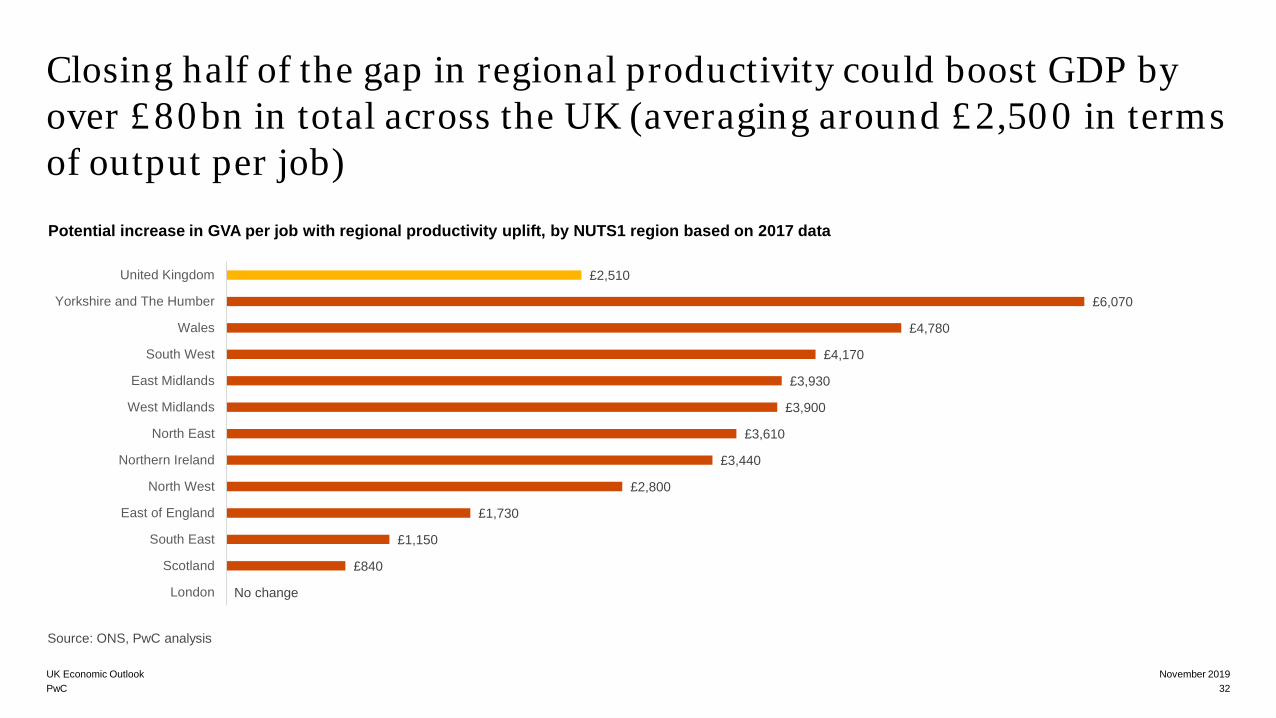

Closing half of the gap in regional productivity could boost GDP by over £80bn in total across the UK (averaging around £2,500 in terms of output per job)

November 2019UK Economic Outlook32

£2,510

£6,070

£4,780

£4,170

£3,930

£3,900

£3,610

£3,440

£2,800

£1,730

£1,150

£840

No change

United Kingdom

Yorkshire and The Humber

Wales

South West

East Midlands

West Midlands

North East

Northern Ireland

North West

East of England

South East

Scotland

London

Potential increase in GVA per job with regional productivity uplift, by NUTS1 region based on 2017 data

Source: ONS, PwC analysis

PwC

Summary: Regional productivity analysis and policy implications

November 2019UK Economic Outlook33

1Regional productivity gaps are large, and are growing over time, with the most productive LEP now more than twice as productive as the least productive LEP in 2017, compared to 1.8 times in 2002.

4

Investing to improve the quality andcapacity of local infrastructure couldhelp boost the connectivity of a place. LEPs should work in collaboration to strengthen intra-regional connectivity and access to economic hubs.

2While differences in industrial structure can explain some regional productivity differences, other issues such as skills, connectivity and innovation appear more significant in general.

5The economic prize from closing the gap is significant. If LEPs and countries that are currently performing below the UK average can halve this productivity gap, we estimate that it could lift UK GDP by around £83 billion (c.4%).

3

Policymakers and businesses needto focus on upskilling workers,particularly in areas such as self-management and leadership skills, as well as digital capabilities.

PwC

Contacts for more information about this report

John HawksworthChief [email protected]

Thanh DinhEconomistHoai.thanh.dinh @pwc.com

Alex TuckettSenior [email protected]

Natasha [email protected]

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.© 2019 PricewaterhouseCoopers LLP. All rights reserved. PwC refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

pwc.co.uk/economics

Jing TeowSenior Economistyong.jing.teow @pwc.com

For more information about our Economics services, or to access the full report, please see our website at:http://www.pwc.co.uk/economics http://www.pwc.co.uk/ukeo

34November 2019UK Economic Outlook