Ugly ducklings: Double-digit EV growth, plenty of … See report end for details of Nomura’s...

134

Hedge your inflation risk Ugly ducklings: Double-digit EV growth, plenty of upside trading at ex-growth multiples Korean lifers have greatly underperformed the KOSPI since listing due to flattening of the yield curve. But we expect the long end of the yield curve to rise slowly but surely, starting in 2H11. Meanwhile, we expect Korean lifers to deliver double-digit EV growth for the next four years. BUY at the bottom of the rate cycle. Key analyses in this anchor report include: • Four-year projection of embedded value. • Long-term industry growth outlook – longevity market developing • SOTP valuation of Samsung Life – we think this is more accurate and our target price is top of the Street. EQUITY RESEARCH ANCHOR REPORT See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non-US affiliates are not registered or qualified as research analysts with FINRA in the US. May 16, 2011 Research analysts Korea Insurance Michael Na m[email protected] +82 2 3783 2334 Young Kwon Kim y[email protected] +82 2 3783 2339 Korea life insurance

Transcript of Ugly ducklings: Double-digit EV growth, plenty of … See report end for details of Nomura’s...

Hedge your inflation risk

Ugly ducklings: Double-digit EV growth, plenty of upside trading at ex-growth multiples

Korean lifers have greatly underperformed the KOSPI since listing due to flattening of the yield curve.

But we expect the long end of the yield curve to rise slowly but surely, starting in 2H11.

Meanwhile, we expect Korean lifers to deliver double-digit EV growth for the next four years.

BUY at the bottom of the rate cycle.

Key analyses in this anchor report include:

• Four-year projection of embedded value.

• Long-term industry growth outlook – longevity market developing

• SOTP valuation of Samsung Life – we think this is more accurate and our target price is top of the Street.

EQUITY RESEARCH

AN

CH

OR

RE

PO

RT

See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non-US affiliates are not registered or qualified as research analysts with FINRA in the US.

May 16, 2011

Research analysts

Korea Insurance

Michael Na [email protected] +82 2 3783 2334

Young Kwon Kim [email protected] +82 2 3783 2339

Korea life insurance

Rating: See report end for details of Nomura’s rating system.

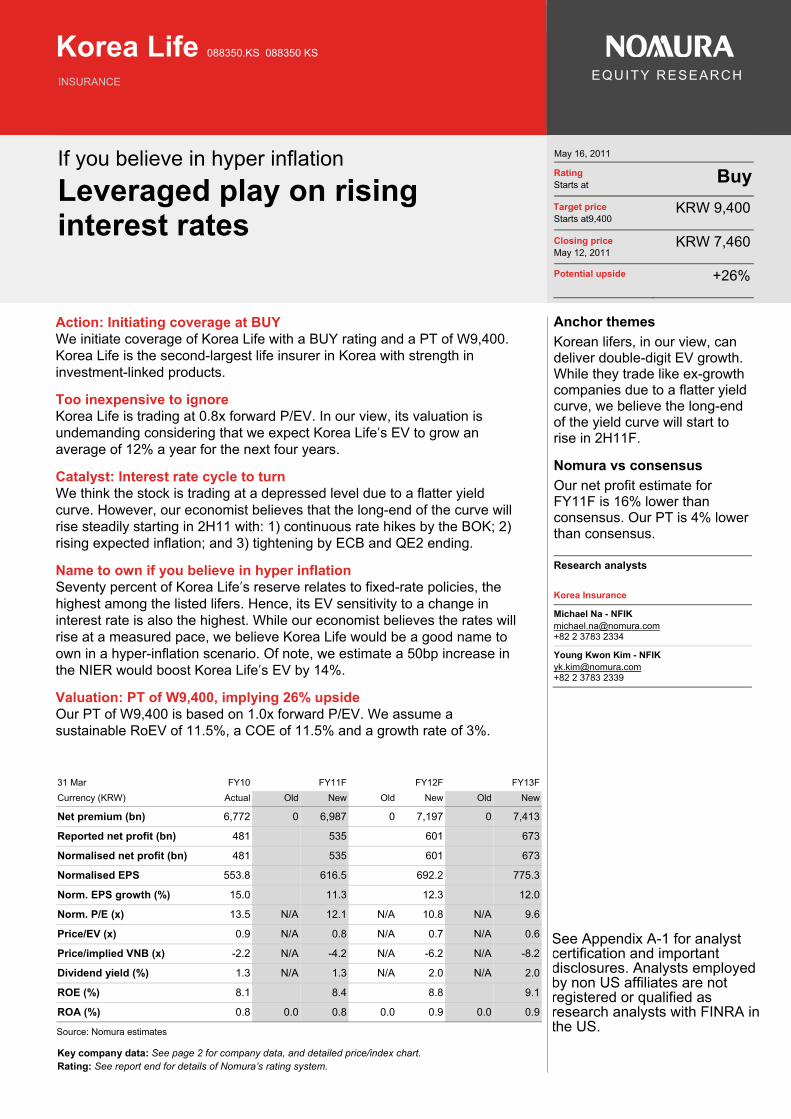

Korea Life Insurance

Insurance

EQUITY RESEARCH

Hedge your inflation risk

Ugly ducklings: Double-digit EV growth, plus plenty of potential upside at ex-growth multiples

May 16, 2011

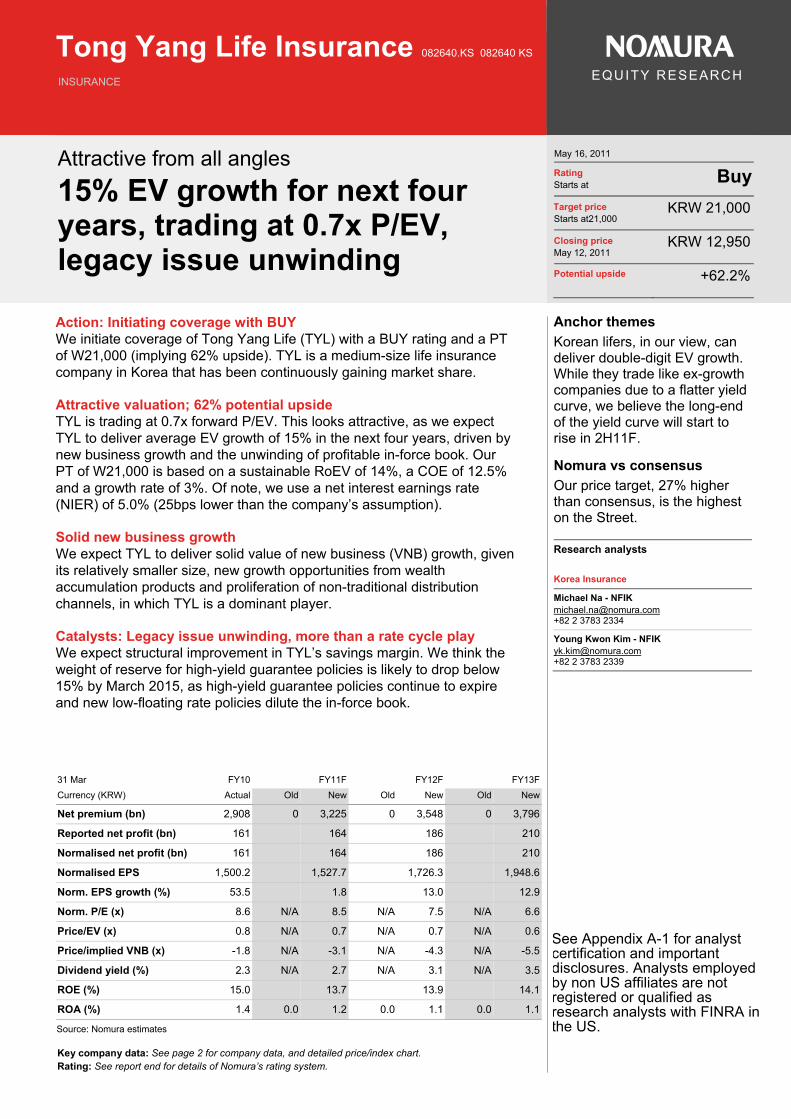

Action: Initiating with BUY We initiate coverage of Korean lifers, Samsung Life, Korea Life and Tong Yang Life with BUY calls and PTs of KRW150,000, KRW9,400 and KRW21,000, respectively. Korean lifers have underperformed the KOSPI since their IPOs due to the flattening yield curve. A flatter yield curve could continue to put pressure on the sector in the near term, but we would recommend accumulating on any weakness as we expect the long end of the yield curve to pick up slowly but surely from 2H11F.

Catalysts: Interest rate cycle to turn Our economist expects long-dated bond yields to rise from 2H11F at a measured pace on continued BOK rate hikes. We also look for rising inflation expectations, ECB tightening and the close of QE2 to lift pressure on the long end of the yield curve. The benefit of rising interest rates is clear for Korean lifers, which have significant exposure to fixed-rate liabilities (60% for Samsung Life, 70% for Korea Life and 56% for Tong Yang Life).

Korea can deliver double-digit EV growth We expect Samsung Life (ex-affiliate stakes), Korea Life and Tong Yang Life to deliver average EV growth of 16%, 12% and 15% over the next four years, driven by strong growth in value of in-force (VIF) business and improvement in the profitability of in-force business.

Priced ex-growth We believe the Korean lifers are priced ex-growth, despite having strong EV growth profiles. Samsung Life (ex-affiliate stakes), Korea Life and Tong Yang Life are trading at 0.8x, 0.8x and 0.7x FY11F P/EV, respectively.

Most upside for Samsung Life and Tong Yang Life, in our view We like Samsung Life for its strong EV growth and given our bullish stance on Samsung Electronics and Samsung Card. We also like Tong Yang Life, as we see a cheap entry point considering its solid growth profile and the likelihood that it will be the first of the lifers to be free of negative spread legacy issues; thus, it is more than just a rate cycle play.

Upside potential for Korea Life from faster-than-expected rate hikes We expect the least upside for Korea Life (26%, vs. 53% for Samsung and 62% for Tong Yang) due to its slower EV growth, and it will likely take time to rebuild a profitable in-force book. But in a hyper inflation scenario, it would be good to own, given it is the most exposed to fixed-rate liabilities.

Fig. 1: Korea life insurance coverage summary

Note: As of 11 May 2011

Anchor themes

Korean lifers, in our view, can del ver double-digit EV growth. While they trade like ex-growth companies due to a flatter yield curve, we believe the long-end of the yield curve will start to rise in 2H11F.

Nomura vs consensus

Our PTs for SLI and TYL are 11% and 27%, respectively higher than consensus, the highest on the Street. Our FY11F net profit estimate for KLI is 16% lower than consensus.

Research analysts

Korea Insurance

Michael Na - NFIK [email protected] +82 2 3783 2334

Young Kwon Kim - NFIK [email protected] +82 2 3783 2339

Stock Rating Price (W) Target Price (W)

Samsung Lif e [032830 KS] BUY 98,000 150,000

Korea Lif e [088350 KS] BUY 7,460 9,400

Tongy ang Lif e [082640 KS] BUY 12,950 21,000

See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non US affiliates are not registered or qualified as research analysts with FINRA in the US.

Nomura | AEJ Korea Life Insurance May 16, 2011

2

Contents

4 Initiating coverage with BUY

4 Priced ex-growth

4 Long end likely to pick up

5 Korea can deliver double-digit EV growth, in our view

5 Samsung Life outpacing peers

5 Long-term positive industry outlook

6 Addressing concerns on PF loans

7 Risk factors

8 Valuation

8 Samsung Life: PT of W150,000 implies 53% potential upside

10 Korea Life: PT of W9,400 implies 26% potential upside

11 Tong Yang Life: PT of W21,000 implies 62% potential upside

12 Valuation would be higher using appraisal valuation method

14 Valuation sensitivity

15 Changes in PT assuming a 50bp increase in NIER

17 Valuation comps

18 Buying at the bottom of a rate cycle

18 Flatter yield curve putting pressure on insurers

19 Long-end should be lifted

21 Benefits from rising rates

23 Long-term positive industry outlook

23 Now entering the longevity market

24 Korean retirees not prepared for longevity risk

Nomura | AEJ Korea Life Insurance May 16, 2011

3

26 Plenty of room for growth

29 Wealth accumulation products to drive growth

32 Corporate pension market to grow rapidly

35 Embedded profitability to improve

35 Loading margin to improve

36 Spread on savings premium to improve gradually

39 Risk margin to stabilise

40 Second tiers gaining market share

40 The Big Three losing market share

41 Second tiers gaining market share

41 Tong Yang benefiting from financial crisis

43 Appendix 1: Calculating EV

46 Appendix 2: Life insurer M&A landscape

47 Samsung Life

81 Korea Life

102 Tong Yang Life Insurance

128 Appendix A-1

Nomura | AEJ Korea Life Insurance May 16, 2011

4

Initiating coverage with BUY We initiate coverage of Korean life insurers with BUY ratings and target prices of W150,000 for Samsung Life (53% potential upside), W9,400 for Korea Life (26% potential upside), and W21,000 (62% potential upside) for Tong Yang Life.

Priced ex-growth

Korean lifers have significantly underperformed Korean life insurers have significantly underperformed the KOSPI since their IPOs (Samsung Life by 45%, Korea Life 46% and Tong Yang Life 56%).

Korea can deliver double-digit EV growth We expect the Korean lifers to deliver double-digit EV growth over the next four years. However, despite the prospects of strong EV growth, we believe the Korean lifers are priced ex-growth. In our view, the depressed valuations are attributable to a flattening yield curve.

Long end of the yield curve sinking despite BOK rate hikes Despite a 100bp rate hike by the central bank, Bank of Korea (BOK), since July 2010, the three-year treasury yield has dropped by 22bp to 3.68%. During the same period, the five-year treasury yield has fallen by 51bp to 4.1%.

Lifers extremely sensitive to interest rates Korean lifers' valuation depends heavily on interest rates, given their significant exposure to fixed-rate policies. The reserve for fixed-rate policies as a proportion of the total interest-bearing reserve is 60% for Samsung Life, 70% for Korea Life and 56% for Tong Yang Life. Of note, a 50bp increase in our investment yield assumption boosts the EV by 8% for Samsung Life, 14% for Korea Life and 9% for Tong Yang Life.

Long end likely to pick up

Rate hike campaign to continue Nomura Korea economist Mr Young Sun Kwon expects two more rate hikes in May and July, and another two in 1H12F, which would lift the terminal policy rate of the current cycle to 4.0% by 2Q12F. Meanwhile, he expects real policy rates to remain negative, doing little to limit inflationary pressure unless it is combined with won appreciation.

Bond market will eventually react to growing concerns on inflation Mr Kwon forecasts CPI inflation will rise above 4% in 2011F, exceeding the BOK's target band. Interest rate hikes coupled with a stronger local currency and price controls should partly offset cost-push inflation pressures from higher oil prices, but rising nominal wages and housing rents are also fueling inflation. Mr Kwon forecasts CPI inflation will rise from 2.9% in 2010 to 4.4% in 2011F, before easing to 3.6% in 2012F. Thus, we think the long end of the bond market will eventually react to growing concerns on inflation.

Foreign capital inflow to slow Whether hunting for better yields or anticipating Korean won appreciation, the inflow of foreign capital has been adding pressure on the long end since 2H09. However, with the European Central Bank (ECB) turning hawkish and the US Federal Reserve's QE2 programme winding down, we expect the foreign capital inflow to slow and possibly even turn into an outflow going forward. We think that the long end of the yield curve could rise on interest rate hikes in developed markets, as we had seen in 4Q10. In addition, recent won appreciation could hinder foreign capital inflow lured in by market anticipation of a further rise in the Korean won, which would further ease pressure on the long end.

Long end to rise slowly Our Korea economist forecasts the five-year treasury yield to start to pick up in 3Q11F and reach 4.5% by end-1H12F (from the current 4.1%), and the three-year treasury yield to edge up to 4.2% by end-1H12F (from the current 3.6%).

Nomura | AEJ Korea Life Insurance May 16, 2011

5

Korea can deliver double-digit EV growth, in our view

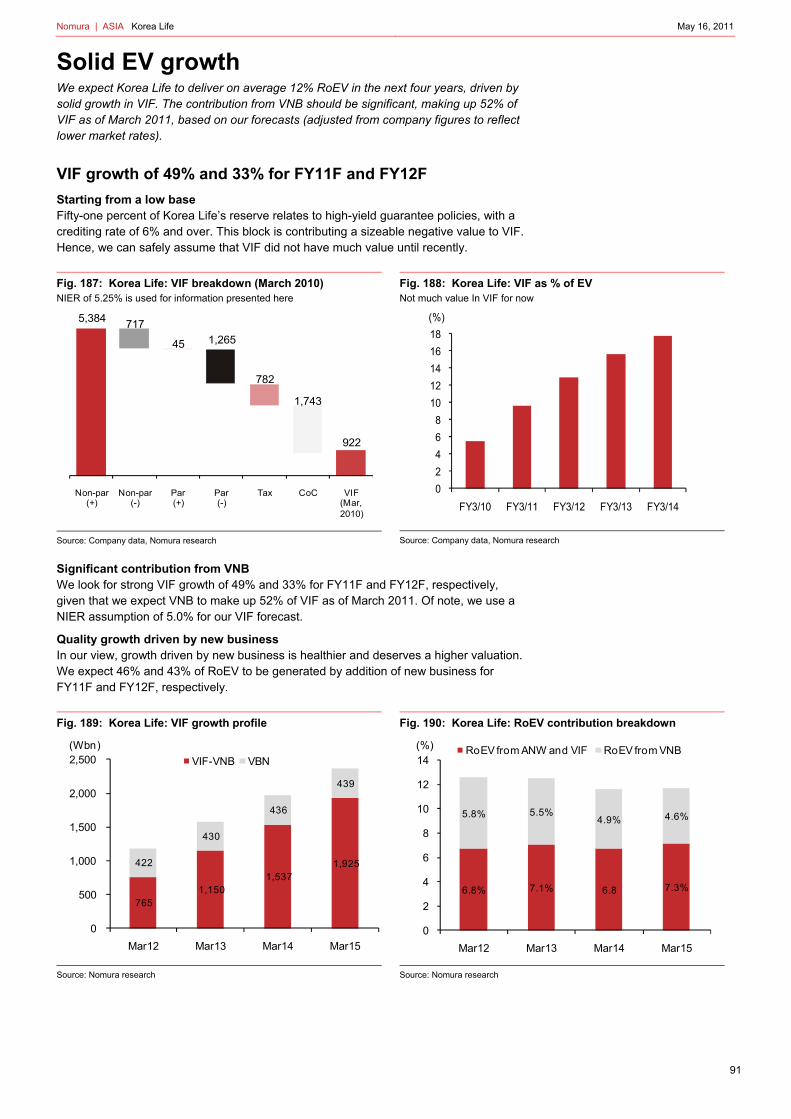

Starting from a low base Up until 1998, government regulations required life insurers to pay 9% on non-participating policies and 7.5% on participating policies. The Korean government lowered the crediting rate by 100bp in 1999 and fully deregulated in 2000. Meanwhile, the Korean bond market has experienced a secular bull market over the past two decades. In 1995, the average rate on the three-year treasury was 13%, compared with the current rate of 3.6%. Consequently, Korean lifers are stuck with huge negative spread books that make their value of in-force (VIF) business extremely small relative to their business volume.

Fast rebuilding in-force book The VIF business only recently turned positive for most of the Korean life insurers. Hence, the value of new business (VNB) makes up a significant proportion of the VIF book. The VNB as a proportion of the VIF was 29% for Samsung Life, 52% for Korea Life and 29% for Tong Yang Life as of March 2011.

Plenty of new business We note that the three-year average 25th-month lapse ratio for Korean lifers stands at 39%. This means that nearly four out of 10 contracts are no longer in-force after two years. Although a higher lapse ratio has a negative impact on the VIF, it would have a positive impact on new business volumes. Currently, the reported VIFs by Korean lifers already reflect such high lapse ratios. That said, we see little downside to new business volumes for the Korean lifers.

Samsung Life outpacing peers

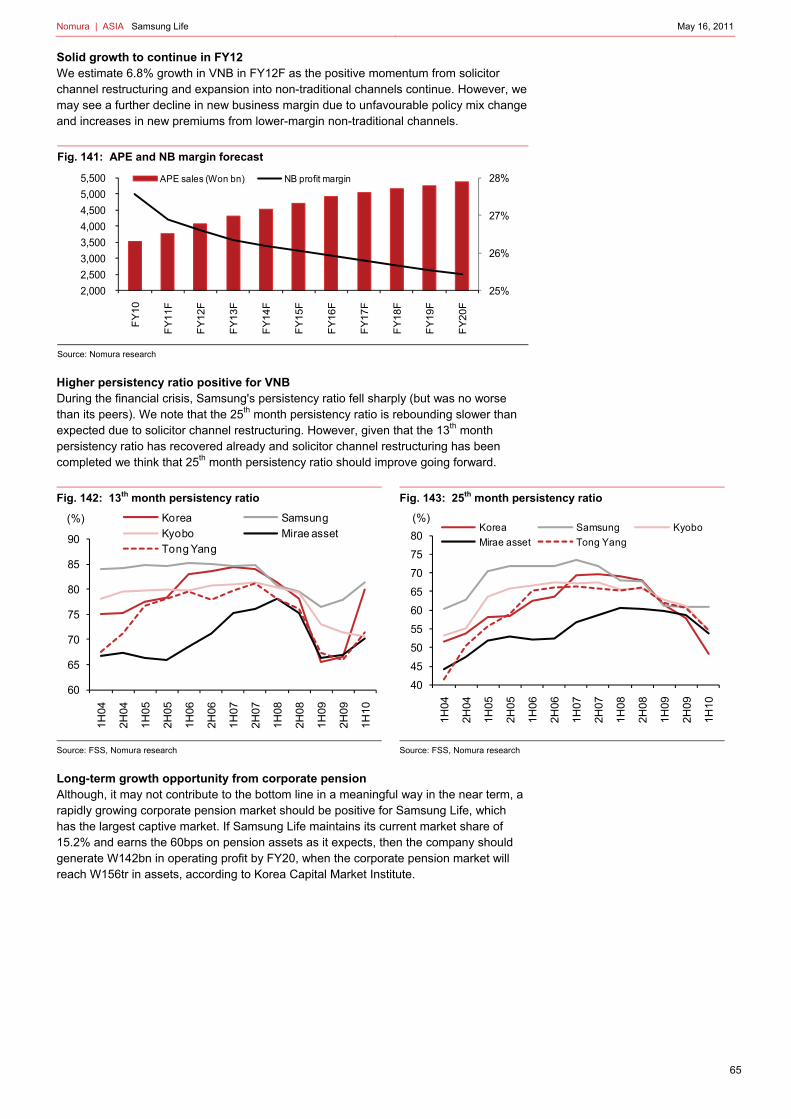

Samsung Life: average EV growth of 16% for next four years We expect Samsung Life to deliver RoEV of 16.7% and 16.1% for FY11F and FY12F, respectively, driven by strong growth in the VIF business and the unwinding of profitable in-force book. We forecast 25% and 22% growth in VIF for FY11F and FY12F, respectively. Growth contributions from VNB will likely be significant as it makes up 30% of VIF. We also expect solid VNB growth as the company starts its hiring cycle and ventures into non-traditional channels.

Korea Life: average EV growth of 12% for next four years We expect Korea Life to deliver RoEV of 12.6% for FY11F and FY12F, driven by strong growth in VIF business. We forecast 49% and 33% growth in VIF for FY11F and FY12F, respectively. The growth contribution from VNB is likely to be significant, as it made up 52% of VIF as of March 2011. However, our EV growth forecasts for Korea Life are slower than for its peers, to reflect the company’s lack of profitable in-force book and statutory earnings will likely be depressed in the near term.

Tong Yang Life: average EV growth of 15% for next four years We also expect Tong Yang Life to deliver strong EV growth. We forecast RoEV of 15.6% and 14.4% for FY11F and FY12F, respectively, driven by new business growth and the unwinding of its profitable in-force book. We expect VNB growth of 5% for each of FY11F and FY12F. Tong Yang looks set to deliver solid VNB growth given its relatively small size, increasing market share and improving profitability on the back of increasing operating leverage.

Long-term positive industry outlook

Insurance density is relatively low The Korean life insurance sector may seem mature based on insurance penetration levels (premium/GDP), which rank Korea the tenth most penetrated life insurance market globally. However, we note that based on insurance density (premium per capita), Korea ranks 24th after Austria.

Demographic changes to have positive impact We expect strong growth in demand for products that manage longevity risk (eg, income annuities and long-term care insurance) as the first 8mn baby boomers (16% of total

Nomura | AEJ Korea Life Insurance May 16, 2011

6

population, born in 1955–1964) start to retire this year. In our opinion, the boomers will seek sources of lifetime income and long-term care insurance given limited pension and healthcare support from the government and corporations. We also expect the second group of baby boomers (14% of total population, born in 1968–1975) to be a continued source of demand for death insurance and wealth accumulation products.

Separate account business to drive growth We believe separate accounts, which include investment-linked insurance and corporate pension, will remain the main growth driver for the Korean life insurers. The life insurance industry is uniquely positioned as the only sector that can provide protection against longevity risk. Life insurers can provide guaranteed streams of income with potential for upside with investment-linked insurance to retirees. Growth in the corporate pension market has been somewhat disappointing, but we expect to see meaningful growth starting this year, given tax benefits on retirement insurance.

General account profitability normalisation to continue The spread on savings premiums should improve as high-yield guarantee policies continue to expire and new low-yield floating-rate policies dilute the in-force book.

Separate account growth to improve capital efficiency ROE should improve as we expect separate account premium growth to outpace general account premium growth given that separate accounts require less capital.

Addressing concerns on PF loans

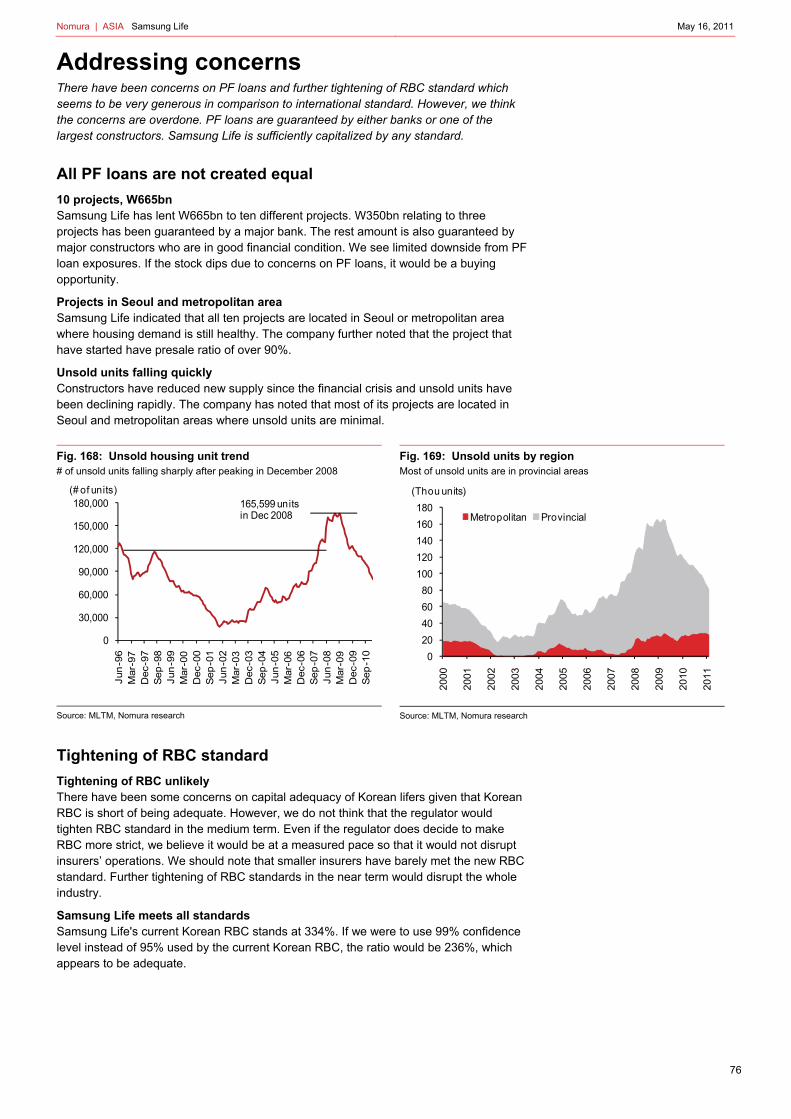

Court receivership / workout of construction companies Earlier this year, we witnessed the court receivership / workout cases of several construction companies ranked in the Top 100 by building capacity. The names include World Construction, Jin Heung Corp, LIG E&C, Dongyang E&C and Sambu Construction.

Restructuring of construction sector winding down However, exposure for the insurance sector remains limited with a smaller project financing (PF) loan balance of KRW4.9tn, which translates to only 7% of the total KRW67tn in PF loans remaining in the system. In addition, almost 40 constructors previously ranked in the Top 100 have entered court receivership / workout programmes. That said, the possibility of more firms following suit remains low, in our view.

Fig. 2: Constructors ranked in Top 50 that have entered workout / court receivership

Source: Edaily, MLTM, Nomura research

Limited downside risk Going forward, we expect default from the construction sector to be largely mitigated, given: 1) continuing signs of recovery in the domestic housing market; and 2) high likelihood for major shareholders to make capital injections to free up liquidity. According to local press (Korea Economic Daily, 3 May, 2011), Doosan Group announced a capital injection of KRW500bn to its affiliate Doosan E&C. Hyosung, STX Group and Daelim Industrial have followed suit with similar capital injections to free up liquidity for affiliates in the construction sector.

Rank Construction Firm Rank Construction Firm

12 Kumho Industrial 38 Namkw ang Corp

17 Kyeongnam Corp 39 Hanil Construction

22 Halla E&C 40 Jinheung Corp.

25 Poonglim Industrial 47 Samho

26 Byucksan E&C 46 Kumkw ang Corp

31 Shindongah Construction 44 Dongyang E&C

35 Namyang E&C

Nomura | AEJ Korea Life Insurance May 16, 2011

7

Risk factors

Asset allocation Shinsegae and CJ Group own a combined 16.6% of Samsung Life. KDIC and Daewoo International own a combined 24.8% of Korea Life. Given that all the aforementioned parties have expressed interest to off-load their stakes and the lock-up period is over, we see potential risk from an asset allocation perspective.

IFRS phase II implementation Although implementation looks to be a few years away, the liability adequacy test required by IFRS phase II could have a material impact on Korean life insurers. If the test identifies that the insurance liability is inadequate, the entire deficiency would be recognised in the P&L immediately. Insurers may have to reserve for "negative spread books", which would significantly lower book values and capital adequacy ratios. Lifers may have to raise additional capital if the liability adequacy test uses risk-free rates.

Solvency II implementation Given that Korea only recently implemented the Risk Based Capital (RBC) evaluation system, we think that Solvency II implementation will be many years away. However, to prepare insurers for Solvency II, the regulator could tighten the Korean RBC system, which is currently far less strict than the international RBC system.

Nomura | AEJ Korea Life Insurance May 16, 2011

8

Valuation We believe Korean lifers are priced like ex-growth stocks, despite offering prospects of double-digit EV growth for the next three years.

Samsung Life: PT of W150,000 implies 53% potential upside

Value of affiliate stakes is one of the key share price drivers In our view, Samsung Life share price is driven by three key factors: 1) EV growth, 2) market rates, and 3) value of affiliate stakes. The first two factors should be the same for all life insurers. However, given that affiliate stakes amounts to half of its book value, we cannot treat it like other equity investments, especially when one single stock (Samsung Electronics) represents 68% of the total affiliate stakes.

Yes, Samsung Electronics' share price performance affects Samsung Life Samsung Life outperformed Korea Life by 8.2% when Samsung Electronics outperformed the KOSPI by 28% from 3 November 2010 to 28 January 2011. However, when the outperformance of Samsung Electronics halted, Samsung Life moved in tandem with Korea Life. This means that we have to take a view on Samsung Electronics when analyzing Samsung Life.

Valuation attractive, trading at 0.8x forward P/EV We subtract the value of affiliate stakes in order to obtain an appropriate EV multiple. Based on our analysis, Samsung Life's insurance business is currently trading at 0.8x forward P/EV. The implied multiple appears to be attractive given that we expect average EV growth of 16% a year through FY14F.

Insurance business: W100,000 per share We value Samsung Life's insurance business on an embedded-value basis, applying a P/EV multiple of 1.5x forward EV. We have assumed a sustainable RoEV of 15%, a COE of 11% and a growth rate of 3%. Of note, we expect EV growth of 17.5% and 16.4% for FY11F and FY12F, respectively. We have assumed lower net investment earnings rate (NIER) for the purpose of our EV forecast. Samsung Life uses NIER of 5.2% for its FY10 EV calculation. In comparison, we assume 5.0% (20bps lower than Samsung Life's assumption). In addition, we used risk discount rate of 11% (50bps higher than Samsung Life’s assumption of 10.5%).

Fig. 3: Samsung Life: EV projection and PT Sustainable RoEV of 15%-plus through FY14F

Source: Company data, Nomura estimates

(Wbn) FY09 FY10 FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 13,685 16,284 17,136 18,085 19,154 20,529 Affiliate stakes (A) 5,084 8,242 8,242 8,242 8,242 8,242 Insurance business book (ANW-A) 8,601 8,042 8,894 9,843 10,912 12,287 Value of in-force business (VIF) 2,954 4,141 5,058 6,042 7,042 7,997 Embedded value (EV) 11,555 12,183 13,952 15,885 17,954 20,284 Growth of EV (RoEV) 8.9% 17.5% 16.4% 15.5% 15.2%Current mkt cap 19,620 19,620 19,620 19,620 19,620 19,620 Mkt Cap - A 14,536 11,378 11,378 11,378 11,378 11,378 P/EV 1.26 0.93 0.82 0.72 0.63 0.56 VNB 1,070 972 1,015 1,084 1,138 1,188 NBM 2.79 (0.83) (2.54) (4.16) (5.78) (7.50)

Target multiple 1.5 Target mkt cap for insurance business 20,000 TP for insurance business 100,000Implied NBM 6.0

Nomura | AEJ Korea Life Insurance May 16, 2011

9

Holding company: W50,000 per share As shown below, Samsung Life's affiliate stakes amount to W14.6tr as of 31 March. Among its holdings, Samsung Electronics makes up 68% of the total value of the affiliate stakes. The company books valuation gains from affiliate stakes as other comprehensive income net of tax and policyholder proportion (currently at 32.1%). We have applied our PT (or current price for unrated stocks) to derive our target NAV.

Fig. 4: Affiliate stake valuation We see 32% upside for the value of affiliate stakes

Note: * reflects current price as of May 11, 2011

Source: Company data, Nomura research

Shareholders’ proportion rising Unrealised gains from affiliate holdings are split between shareholders and policyholders. The policyholders' proportion is the part of reserve relating participating policies to total reserve. Currently, the policyholders’ and shareholders’ proportions are 32% and 68%, respectively. We expect the shareholders’ proportion to increase by 1.0-1.4pp in a year’s time as the reserve relating to participating policies as a proportion of the total reserve declines.

Fig. 5: Shareholders’ proportion of unrealised gains on AFS Shareholders' proportion should increase by 1.0-1.4pp per annum

Source: Company data, Nomura estimates

Accounting # of Shares % holdingMar11Price

Mar11(Wbn)

TP orCurrent

price

Mar12F(Wbn)

Samsung Electronics Cost 10,622,814 7% 932,000 9,900 1,350,000 14,341

Samsung Card Equity 32,468,868 26% 55,500 1,802 67,000 2,175

Samsung F&M Cost 4,905,718 10% 242,500 1,190 223,000 * 1,094

Samsung Securities Cost 7,603,659 11% 80,600 613 83,800 * 637

Samsung C&T Cost 7,476,102 5% 71,800 537 85,000 635

Samsung Heavy Cost 7,800,000 3% 39,900 311 45,300 * 353

S1 Cost 2,030,476 5% 56,300 114 50,900 * 103

Hotel Shilla Cost 2,865,158 7% 25,550 73 27,100 * 78

Samsung Techw in Cost 289,800 1% 79,800 23 95,000 28

Samsung SDI Cost 10,155 0% 168,000 2 160,000 2

Cheil Industries Cost 6,871 0% 116,500 1 160,000 1

Samsung Futures Equity 1,025,000 41% 41 41

Samsung Asset Management Cost 1,024,000 5% 21 21

Samsung Economic Research Institute Cost 1,776,000 15% 10 10

Samsung Corning Precision Glass Cost 2,176 0% 2 2

Total Value 14,639 19,521

Net of holding company discount (27%) 10,687 14,250

Shareholders' proportion (69.6%) 7,438 9,918

Per share (Won) 38,000 50,000

39.1% 36.4% 34.5% 33.3% 32.1% 30.7%

60.9% 63.6% 65.5% 66.7% 67.9% 69.3%

Mar07 Mar08 Mar09 Mar10 Mar11 Mar12F

Policyholders' proportion Shareholders' equity

Nomura | AEJ Korea Life Insurance May 16, 2011

10

We apply a 27% holding company discount Theoretically, we think the holding company discount should be the corporate tax rate (22%). However, in reality, the holding company discount varies based on the performance of its holdings and market liquidity. The holding company discount narrows when its holdings outperform the market and vice versa. In addition, abundant market liquidity lowers the discount. Given that we are bullish on Samsung Group, the holding company discount could be lower than the tax rate. However, for the purpose of our valuation, we apply a 27% discount, which is the five-year average NAV discount for LG Corp. We select LG Corp as our benchmark as we believe it is one of the purest holding companies in Korea with most of its holdings being listed.

Fig. 6: LG Corp discount to NAV Average discount to NAV for the past five years of 27%

Source: Nomura research

Korea Life: PT of W9,400 implies 26% potential upside

Our PT is based on 1.0x P/EV We forecast EV growth of 12.6% for each of FY11F and FY12F. We believe Korea Life can sustain 11.5%-plus RoEV for the next four years. Our PT of KRW9,400 is based on 1.0x forward P/EV. We assume a sustainable medium-term RoEV of 11.5%, a COE of 11.5% and a growth rate of 3%. Of note, we assume a lower net investment earnings rate (NIER) of 5.0% for the purpose of our EV forecast, compared with the 5.25% used by Korea Life in its FY09 EV calculation.

Priced ex-growth Korea Life is trading at 0.8x forward P/EV. We think the current valuation is attractive as we expect sustainable RoEV of 11.5% in the medium term. The current implied NBM (new business multiple) is in negative territory despite the company’s solid growth profile and potential upside from rising interest rates.

Fig. 7: Korea Life: EV projection and PT Sustainable RoEV of 11.5%-plus through FY14F

Source: Company data, Nomura research

-20%

-10%

0%

10%

20%

30%

40%

50%

2-May-06 2-May-07 2-May-08 2-May-09 2-May-10 2-May-11

NAV Discount Average St Dev +1 St Dev -1

(Wbn) FY09 FY10F FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 6,100 6,601 7,055 7,569 8,112 8,737 Value of in-force business (VIF) 408 795 1,187 1,580 1,973 2,365 Embedded value (EV) 6,508 7,396 8,242 9,150 10,085 11,102 Growth of EV (RoEV) 15.0% 12.6% 12.6% 11.6% 11.8%Current mkt cap 6,418 6,418 6,418 6,418 6,418 6,418 P/EV 0.99 0.87 0.78 0.70 0.64 0.58 VNB 410 411 422 430 436 439 NBM (0.22) (2.38) (4.32) (6.35) (8.41) (10.66)

Target multiple 1.0 Target mkt cap 8,242 Target price 9,400 Implied NBM -

Nomura | AEJ Korea Life Insurance May 16, 2011

11

Tong Yang Life: PT of W21,000 implies 62% potential upside

Our PT is based on 1.2x P/EV We expect Tong Yang Life (TYL) to deliver EV growth of 15.5% and 14.6% for FY11F and FY12F, respectively. We also expect TYL to sustain RoEV of 14%-plus through FY14F. Our PT of W21,000 is based on 1.2x forward P/EV. We assume a sustainable RoEV of 14.0%, a COE of 12.5% and a growth rate of 3%. We assume a higher COE than for other life insurers given Korea Life’s relatively smaller size and liquidity. Of note, we assume a lower net investment earnings rate (NIER) of 5.0% for the purpose of our EV forecast, compared with the 5.25% used by TYL in its FY09 EV calculation.

TYL looks attractive even on a PBR methodology… As more profitable new business continues to flow into in-force book, we think the return on shareholders' equity will improve and reach a sustainable level of 15% in the medium term. A PBR valuation derives a valuation of W15,000, implying 18% potential upside.

…but PBR could be misleading Given the long-tail nature of life insurance, we think current earnings and book value do not capture the value of current in-force book, especially if there is a significant difference in profitability between in-force book and new business (which is the case for Korean lifers who have been suffering from negative spread on legacy products). That said, investor should not miss out on TYL who looks attractive even on PBR.

Fig. 8: Tong Yang Life: EV projection and PT Sustainable RoEV of 14%-plus through FY14F

Source: Company data, Nomura estimates

(Wbn) FY09 FY10F FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 1,019 1,127 1,260 1,400 1,559 1,750 Value of in-force business (VIF) 472 546 635 728 837 953 Embedded value (EV) 1,491 1,673 1,895 2,128 2,396 2,703 Growth of EV (RoEV) 14.4% 15.5% 14.6% 14.9% 14.8%Current mkt cap 1,334 1,334 1,334 1,334 1,334 1,334 P/EV 0.9 0.8 0.7 0.6 0.6 0.5 VNB 142 154 161 169 179 190 NBM (1.1) (2.2) (3.5) (4.7) (5.9) (7.2)

Target multiple 1.2 Target mkt cap 2,274 Target price 21,000Implied NBM 2.4

Nomura | AEJ Korea Life Insurance May 16, 2011

12

Valuation would be higher using appraisal valuation method

We calculate an even higher valuation using 10-year DCF model Using an appraisal valuation method we calculate an even higher valuation for TYL, as its VNB is the largest as a percentage of EV. In addition, we believe that NBM will increase, as we expect the company to continue to gain market share. Of note, we only reflect a 10-year projection in our NBM calculation. Typically, a 30-year DCF model is used in the region to drive NBM. However, due to the infancy of the EV valuation methodology in Korea, we do not want to pay for more than 10 years.

Samsung Life insurance business at KRW109,000 per share if using the appraisal valuation method For Samsung Life, the implied NBM is 6.0x our PT. However, if we were to use the appraisal value methodology, we could justify up to a 7.7x NBM.

Fig. 9: Samsung Life: target NBM based on appraisal valuation method

Source: Nomura estimates

Korea Life valuation at KRW12,800 if using the appraisal valuation method For Korea Life, the implied NBM is 0x at our PT. However, using the appraisal value methodology, we could justify up to a 6.9x NBM.

Fig. 10: Korea Life: target NBM based on appraisal valuation method

Source: Nomura estimates

Tong Yang Life PT at KRW30,000 if using the appraisal valuation method For TYL, the implied NBM is 2.3x our PT. However, using the appraisal value method, we could justify up to 8.0x NBM.

Fig. 11: Tong Yang Life: target NBM based on appraisal valuation method

Source: Nomura research

But we think it is more appropriate to use the P/EV methodology While there is upside potential to our PTs using the appraisal value methodology, we think it is more appropriate to use P/EV for the Korea life insurers given some variances we encountered in EV, which may not be captured in the NBM technique. In addition, we think the appraisal valuation method ignores near-term EV growth profile changes that companies may face such as Korea Life who may take a while to rebuild profitable VIF.

(Wbn) FY11F FY12F FY13F FY14F FY15F FY16F FY17F FY18F FY19F FY20FAnnualized premium equivalent (APE) 3,773 4,075 4,319 4,535 4,716 4,905 5,052 5,153 5,256 5,362 New business margin 26.9% 26.6% 26.4% 26.2% 26.1% 25.9% 25.8% 25.7% 25.6% 25.4%Value of new business (VNB) 1,015 1,084 1,138 1,188 1,230 1,272 1,304 1,323 1,343 1,363 Discount factor 1.0 1.1 1.2 1.4 1.5 1.7 1.9 2.1 2.3 2.6 PV of VNB 1,015 976 924 869 810 755 697 637 583 533 Sum of PV 7,799 Implied multiple 7.7

(Wbn) FY11F FY12F FY13F FY14F FY15F FY16F FY17F FY18F FY19F FY20FAnnualized premium equivalent (APE) 2,271 2,351 2,421 2,482 2,531 2,582 2,634 2,686 2,740 2,795 New business margin 18.6% 18.3% 18.0% 17.7% 17.5% 17.4% 17.4% 17.3% 17.3% 17.3%Value of new business (VNB) 422 430 436 439 443 450 458 466 475 484 Discount factor 1.0 1.1 1.2 1.4 1.5 1.7 1.9 2.1 2.3 2.6 PV of VNB 422 388 354 321 292 267 245 224 206 189 Sum of PV 2,908 Implied multiple 6.9

(Wbn) FY11F FY12F FY13F FY14F FY15F FY16F FY17F FY18F FY19F FY20FAnnualized premium equivalent (APE) 992 1,062 1,136 1,210 1,282 1,353 1,421 1,477 1,536 1,598 New business margin 16.2% 15.9% 15.8% 15.7% 15.7% 15.6% 15.5% 15.5% 15.5% 15.5%Value of new business (VNB) 161 169 179 190 201 211 221 229 238 248 Discount factor 1.0 1.1 1.2 1.4 1.5 1.7 1.9 2.1 2.3 2.6 PV of VNB 161 152 145 139 132 125 118 110 103 97 Sum of PV 1,283 Implied multiple 8.0

Nomura | AEJ Korea Life Insurance May 16, 2011

13

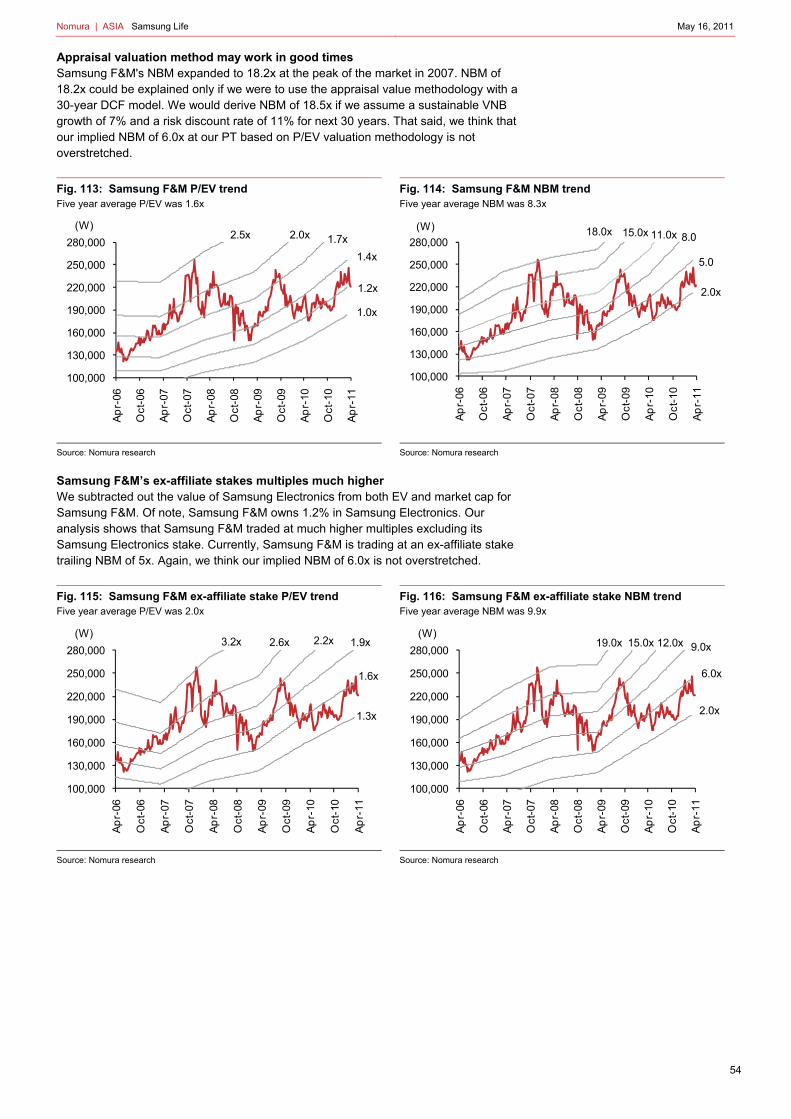

Appraisal value methodology may work in good times Samsung F&M's NBM expanded to 18.2x at the peak of the market in 2007. NBM of 18.2x could be explained only if we were to use the appraisal value methodology with a 30-year DCF model. We would derive NBM of 18.5x if we assume a sustainable VNB growth of 7% and a risk discount rate of 11% for next 30 years. That said, we think that our implied NBM of 6.0x at our PT based on P/EV valuation methodology is not overstretched.

Fig. 12: Samsung F&M P/EV trend Five-year average P/EV of 1.6x

Source: Nomura research

Fig. 13: Samsung F&M NBM trend Five-year average NBM of 8.3x

Source: Nomura research

Ex-affiliate multiples much higher We subtracted out the value of Samsung Electronics from both EV and market cap for Samsung F&M. Of note, Samsung F&M owns 1.2% in Samsung Electronics. Our analysis shows that Samsung F&M traded at much higher multiples excluding its Samsung Electronics stake. Currently, Samsung F&M is trading at an ex-affiliate stake trailing NBM of 5x. Again, we think our implied NBM of 6.0x is not overstretched.

Fig. 14: Samsung F&M ex-affiliate stake P/EV trend Five-year average P/EV of 2.0x

Source: Nomura research

Fig. 15: Samsung F&M ex-affiliate stake NBM trend Five-year average NBM of 9.9x

Source: Nomura research

50,000

100,000

150,000

200,000

250,000

300,000

Ap

r-06

Oct-

06

Ap

r-07

Oct-

07

Ap

r-08

Oct-

08

Ap

r-09

Oct-

09

Ap

r-10

Oct-

10

Ap

r-11

(W)

1.0x

1.2x

1.4x

1.6x1.8x2.0x

50,000

100,000

150,000

200,000

250,000

300,000

Ap

r-06

Oct-

06

Ap

r-07

Oct-

07

Ap

r-08

Oct-

08

Ap

r-09

Oct-

09

Ap

r-10

Oct-

10

Ap

r-11

(W)

2.0x

5.0x

8.0x11.0x14.0x17.0x

50,000

100,000

150,000

200,000

250,000

300,000

Ap

r-06

Oct-

06

Ap

r-07

Oct-

07

Ap

r-08

Oct-

08

Ap

r-09

Oct-

09

Ap

r-10

Oct-

10

Ap

r-11

(W)

1.3x

1.7x

2.1x2.5x2.9x3.3x

50,000

100,000

150,000

200,000

250,000

300,000

Mar-

06

Sep

-06

Mar-

07

Sep

-07

Mar-

08

Sep

-08

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Mar-

11

(W)

2.0x

5.0x

8.0x

11.0x14.0x17.0x

Nomura | AEJ Korea Life Insurance May 16, 2011

14

Valuation sensitivity

Korea Life is most sensitive to interest rates Korea Life has the highest EV sensitivity to the net interest earnings rate (NIER) assumption as the company has the highest proportion of fixed-rate liabilities at 70% compared to 60% for Samsung Life and 56% for TYL. We estimate a 50bp increase in the NIER assumption would increase Korea Life’s EV by 13.8%, Samsung Life’s by 13.5% and TYL’s by 9.5%.

A 50bp increase in NIER assumption to increase Samsung Life’s EV by 12.8% Samsung Life used an NIER assumption of 5.2% for its FY10 EV calculation. We believe Samsung’s assumption is aggressive given current market rates. For the purpose of our analysis, we adjust the NIER to 5.0%. Note that Samsung Life’s EV is also sensitive to changes in the claims ratio.

Fig. 16: Samsung Life: EV sensitivity (KRW)

Source: Company data, Nomura research

Fig. 17: Samsung Life: EV sensitivity (%)

Source: Company data, Nomura research

A 50bp increase in NIER assumption to increase Korea Life’s EV by 13.8% Korea Life used an NIER assumption of 5.25% for its FY09 EV calculation. We believe Korea Life’s assumption is aggressive given the current market rates. For the purpose of our analysis, we adjust the NIER to 5.0%. We note that Korea Life is less sensitive to changes in the claims ratio, unlike Samsung Life.

Fig. 18: Korea Life’s EV sensitivity (KRW)

Source: Company data, Nomura research

Fig. 19: Korea Life’s EV sensitivity (%)

Source: Company data, Nomura research

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

RB

C ±

50p

pt

Lap

se ±

10%

Cla

ims ±

10%

Main

ten

ance

±10%

AF

S a

ffilia

te s

takes ±

10%

(Wbn)

12.8% 14.4%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

RB

C ±

50p

pt

Lap

se ±

10%

Cla

ims ±

10%

Main

ten

ance

±10%

AF

S a

ffilia

te s

takes ±

10%

1,028

(1,500)

(1,000)

(500)

0

500

1,000

1,500

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

Cla

ims R

ate

±10p

pt

Lap

se R

ate

±10p

pt

(Wbn)

13.8%11%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

Cla

ims R

ate

±10p

pt

Lap

se R

ate

±10p

pt

Nomura | AEJ Korea Life Insurance May 16, 2011

15

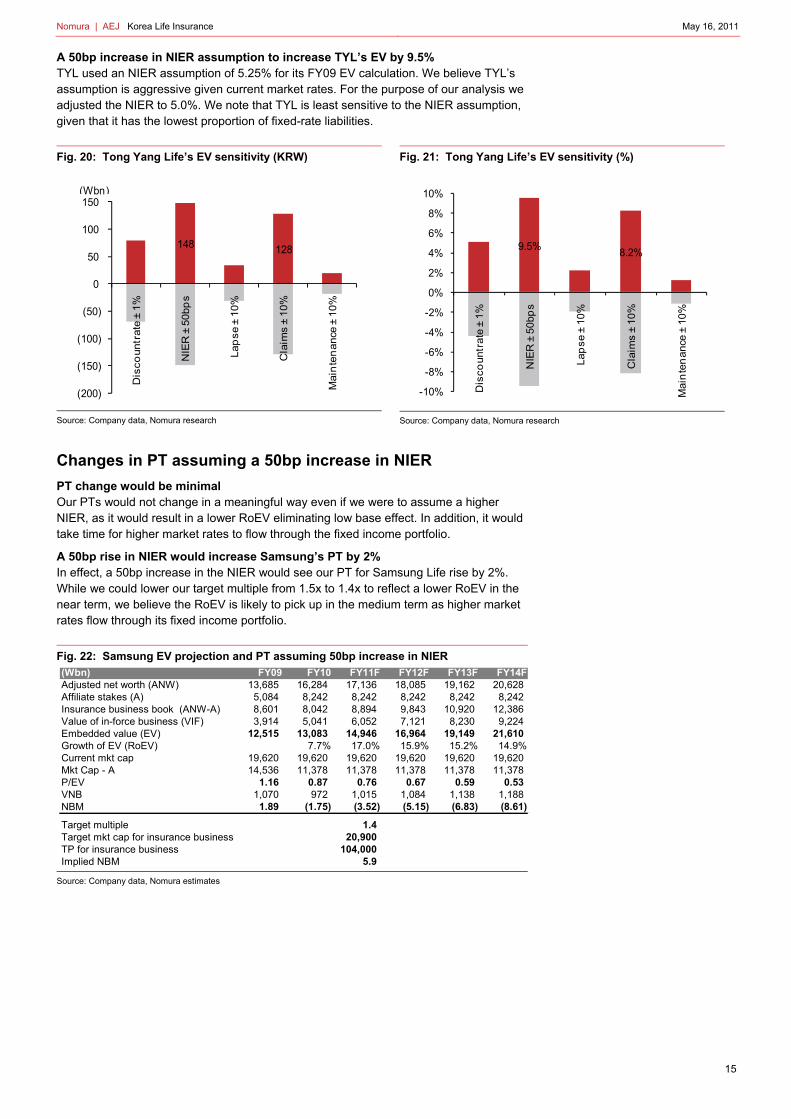

A 50bp increase in NIER assumption to increase TYL’s EV by 9.5% TYL used an NIER assumption of 5.25% for its FY09 EV calculation. We believe TYL’s assumption is aggressive given current market rates. For the purpose of our analysis we adjusted the NIER to 5.0%. We note that TYL is least sensitive to the NIER assumption, given that it has the lowest proportion of fixed-rate liabilities.

Fig. 20: Tong Yang Life’s EV sensitivity (KRW)

Source: Company data, Nomura research

Fig. 21: Tong Yang Life’s EV sensitivity (%)

Source: Company data, Nomura research

Changes in PT assuming a 50bp increase in NIER

PT change would be minimal Our PTs would not change in a meaningful way even if we were to assume a higher NIER, as it would result in a lower RoEV eliminating low base effect. In addition, it would take time for higher market rates to flow through the fixed income portfolio.

A 50bp rise in NIER would increase Samsung’s PT by 2% In effect, a 50bp increase in the NIER would see our PT for Samsung Life rise by 2%. While we could lower our target multiple from 1.5x to 1.4x to reflect a lower RoEV in the near term, we believe the RoEV is likely to pick up in the medium term as higher market rates flow through its fixed income portfolio.

Fig. 22: Samsung EV projection and PT assuming 50bp increase in NIER

Source: Company data, Nomura estimates

148 128

(200)

(150)

(100)

(50)

0

50

100

150

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

Lap

se ±

10%

Cla

ims ±

10%

Main

ten

ance

±10%

(Wbn)

9.5%8.2%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Dis

co

unt r

ate

±1%

NIE

R ±

50bp

s

Lap

se ±

10%

Cla

ims ±

10%

Main

ten

ance

±10%

(Wbn) FY09 FY10 FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 13,685 16,284 17,136 18,085 19,162 20,628 Affiliate stakes (A) 5,084 8,242 8,242 8,242 8,242 8,242 Insurance business book (ANW-A) 8,601 8,042 8,894 9,843 10,920 12,386 Value of in-force business (VIF) 3,914 5,041 6,052 7,121 8,230 9,224 Embedded value (EV) 12,515 13,083 14,946 16,964 19,149 21,610 Growth of EV (RoEV) 7.7% 17.0% 15.9% 15.2% 14.9%Current mkt cap 19,620 19,620 19,620 19,620 19,620 19,620 Mkt Cap - A 14,536 11,378 11,378 11,378 11,378 11,378 P/EV 1.16 0.87 0.76 0.67 0.59 0.53 VNB 1,070 972 1,015 1,084 1,138 1,188 NBM 1.89 (1.75) (3.52) (5.15) (6.83) (8.61)

Target multiple 1.4 Target mkt cap for insurance business 20,900 TP for insurance business 104,000Implied NBM 5.9

Nomura | AEJ Korea Life Insurance May 16, 2011

16

A 50bp rise in NIER would increase Korea Life’s PT by 3% In effect, a 50bp increase in the NIER would see our PT for Korea Life rise by 3%. While we could lower our target multiple from 1.0x to 0.9x to reflect a lower RoEV in near term, we think the RoEV is likely to pick up in the medium term as higher market rates flow through its fixed income portfolio. Eventually, we may be able to apply a higher target multiple.

Fig. 23: Korea Life’s EV projection and PT assuming 50bp increase in NIER

Source: Company data, Nomura estimates

TYL’s PT unchanged despite higher NEIR assumption For TYL, our target price would remain largely unchanged even if we were to assume a higher NIER assumption. While we could lower our target multiple from 1.2x to 1.1x to reflect a lower RoEV in the near term, we think the RoEV is likely to pick up in the medium term as higher market rates flow through its fixed income portfolio. Eventually, we should be able to apply higher target multiple.

Fig. 24: TYL’s EV projection and PT assuming 50bp increase in NIER

Source: Company data, Nomura estimates

(Wbn) FY09 FY10F FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 6,100 6,651 7,127 7,679 8,324 8,992 Value of in-force business (VIF) 1,436 1,823 2,222 2,630 3,052 3,487 Embedded value (EV) 7,536 8,474 9,348 10,309 11,375 12,478 Growth of EV (RoEV) 13.6% 11.3% 11.2% 11.6% 10.8%Current mkt cap 6,418 6,418 6,418 6,418 6,418 6,418 P/EV 0.9 0.8 0.7 0.6 0.6 0.5 VNB 410 423 441 458 477 498 NBM (2.7) (4.9) (6.6) (8.5) (10.4) (12.2)

Target multiple 0.9 Target mkt cap 8,413 Target price 9,700 Implied NBM (2.1)

(Wbn) FY09 FY10F FY11F FY12F FY13F FY14FAdjusted net worth (ANW) 1,019 1,127 1,261 1,398 1,571 1,787 Value of in-force business (VIF) 546 617 703 793 890 993 Embedded value (EV) 1,565 1,744 1,964 2,191 2,461 2,781 Growth of EV (RoEV) 13.5% 14.8% 13.7% 14.5% 15.0%Current mkt cap 1,334 1,334 1,334 1,334 1,334 1,334 P/EV 0.9 0.8 0.7 0.6 0.5 0.5 VNB 142 154 161 169 179 190 NBM (1.6) (2.7) (3.9) (5.1) (6.3) (7.6)

Target multiple 1.1 Target mkt cap for insurance business 2,161 Target price 21,000 Implied NBM 1.2

Nomura | AEJ Korea Life Insurance May 16, 2011

17

Valuation comps

Fig. 25: Insurance Valuation Comps

Note: *Represents Bloomberg estimates, pricing as of 11 May 2011

Source: Bloomberg, Nomura estimates

SamsungLife

KoreaLife

TongYang Life

SamsungF&M*

HyundaiF&M*

DongbuInsurance*

Ping AnLife

ChinaLife

Bloomgberg Ticker 032830 KS 088350 KS 082640 KS 000810 KS 001450 KS 005830 KS 2318 HK 2628 HKRecommendation BUY BUY BUY n.a n.a n.a Neutral BUYLocal Currency KRW KRW KRW KRW KRW KRW CNY CNYShare price (W) 98,000 7,460 12,950 220500 27450 48800 81.4 26.5Target price (W) 150,000 9,400 21,000 n.a n.a n.a 90.0 40.0Implied upside (downside) (%) 53% 26% 62% n.a n.a n.a 11% 51%Shares outstanding (mn) 200 869 108 47.375 89.4 70.8 7,640 28,260Market Cap. (bn) 19,600 6,479 1,393 10,446 2,454 3,455 622 749Market Cap. (US$mn) 18,095 5,982 1,286 9,644 2,266 3,190 7,640 28,260

Current MultiplesP/BV (x) FY09A 1.6 1.1 1.4 2.7 2.9 4.1 8.3 3.5

FY10A 1.3 1.1 1.2 2.1 2.3 2.9 6.1 3.6FY11E 1.2 1.0 1.1 1.4 1.4 1.5 4.9 2.9FY12E 1.1 0.9 1.0 1.3 1.2 1.3 3.9 2.4

P/E (x) FY09A 21.6 15.5 13.3 17.4 21.3 14.9 42.8 22.8FY10A 10.1 13.5 8.6 19.9 13.3 15.3 34.5 22.3FY11E 16.7 12.1 8.5 12.9 8.4 8.8 21.9 16.9FY12E 15.0 10.8 7.5 11.1 7.0 7.3 15.6 13.9

P/EV (x) FY09A 1.2 1.0 0.9 n.a. n.a. n.a. 3.8 2.6FY10A 1.0 0.9 0.8 n.a. n.a. n.a. 3.3 2.4FY11E 0.9 0.8 0.7 n.a. n.a. n.a. 2.6 2.0FY12E 0.8 0.7 0.7 n.a. n.a. n.a. 2.0 1.6

P/EV (ex. aff ilates) (x) FY09A 1.3 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY10A 0.9 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY11E 0.8 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY12E 0.7 n.a. n.a. n.a. n.a. n.a. n.a. n.a.

ProfitabilityROE (%) FY09A 9.3 9.0 12.6 15.5 13.8 27.6 19.0 15.5

FY10A 14.1 8.1 15.0 10.6 17.3 19.3 18.0 16.0FY11E 7.4 8.4 13.7 12.2 19.4 19.2 25.0 18.6FY12E 7.9 8.8 13.9 13.0 20.9 20.0 28.0 18.8

ROEV (%) FY09A 34.6 30.1 32.1 n.a. n.a. n.a. 9.0 11.5FY10A 25.2 15.0 14.4 n.a. n.a. n.a. 9.5 10.6FY11E 10.4 12.6 15.5 n.a. n.a. n.a. 11.8 11.7FY12E 10.3 12.6 14.6 n.a. n.a. n.a. 13.0 11.8

ROEV (ex. aff iliates) (%) FY09A 13.1 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY10A 8.9 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY11E 17.5 n.a. n.a. n.a. n.a. n.a. n.a. n.a.FY12E 16.4 n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Per Share DataEPS FY09A 4,530 482 977 12,638 1,288 3,270 1.9 1.2

FY10A 9,669 554 1,502 11,071 2,063 3,197 2.4 1.2FY11E 5,859 616 1,529 17,049 3,265 5,523 3.7 1.6FY12E 6,547 692 1,731 19,838 3,929 6,652 5.2 1.9

BVPS FY09A 60,664 6,540 9,494 81,540 9,343 11,867 9.8 7.5FY10A 76,950 7,098 10,495 104,281 11,923 16,574 13.3 7.4FY11E 81,009 7,620 11,767 154,100 19,027 32,341 16.5 9.2FY12E 85,755 8,162 13,099 167,986 22,202 36,994 21.0 11.0

EVPS FY09A 83,194 7,493 13,864 n.a. n.a. n.a. 21.1 10.1FY10A 102,125 8,516 15,555 n.a. n.a. n.a. 25.0 11.2FY11E 110,968 9,489 17,618 n.a. n.a. n.a. 31.6 13.4FY12E 120,635 10,535 19,782 n.a. n.a. n.a. 40.3 16.1

Nomura | AEJ Korea Life Insurance May 16, 2011

18

Buying at the bottom of a rate cycle We believe the BOK will continue with its rate hike campaign, taking the key policy rate to 4.0% by 2Q11F. We expect the long-end of yield curve to rise slowly along with rising policy rates. Korean lifers should benefit from rising interest rates given their large exposure to fixed-rate liabilities.

Flatter yield curve putting pressure on insurers

Long-end of the yield curve has been falling despite rate hikes by the BOK Despite hikes of 100bp by the BOK since July 2010, the three-year treasury yield fell by 22bp to 3.68%. During the same period, the five-year treasury yield fell by 15bp. The phenomenon happened in the early part of 2006, but it normalized thereafter.

Fig. 26: Interest rate trend

Source: CEIC, Nomura research

Lifers extremely sensitive to interest rates Korean lifers' valuation depends heavily on interest rates due to significant exposure to fixed-rate policies. The reserve for fixed rate policies as a proportion of total interest-bearing reserve amounts to 60% for Samsung Life, 70% for Korea Life, and 56% for Tong Yang Life. Of note, a 50bp increase in investment yield assumption would boost EV by 8% for Samsung Life, 14% for Korea Life and 9% for Tong Yang Life, according to our sensitivity analysis.

Fig. 27: Samsung Life share price vs. 3yr and 5yr treasury

Source: CEIC, Nomura research

Fig. 28: Korea Life share price vs. 3yr and 5yr treasury

Source: CEIC, Nomura research

Fig. 29: Tong Yang Life share price vs. 3yr and 5yr treasury

Source: CEIC, Nomura research

1

2

3

4

5

6

7

8

9

10

May-9

9O

ct-

99

Mar-

00

Aug

-00

Jan

-01

Jun

-01

No

v-0

1A

pr-

02

Sep

-02

Feb-0

3Jul-

03

Dec-0

3M

ay-0

4O

ct-

04

Mar-

05

Aug

-05

Jan

-06

Jun

-06

No

v-0

6A

pr-

07

Sep

-07

Feb-0

8Jul-

08

Dec-0

8M

ay-0

9O

ct-

09

Mar-

10

Aug

-10

Jan

-11

Policy Rate 3 Yr KTB 5 Yr KTB(%)

2.5

3.0

3.5

4.0

4.5

5.0

85

90

95

100

105

110

115

120

May

-10

Jul-

10

Sep

-10

No

v-10

Jan

-11

Mar

-11

SLI

3yr KTB

5yr KTB

(W'000) (%)

2.5

3.0

3.5

4.0

4.5

5.0

6778899

1010

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-10

Jan

-11

Mar

-11

KLI3yr KTB5yr KTB

(W'000) (%)

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6

8

10

12

14

16

18

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

TYL3yr KTB5yr KTB

(W'000) (%)

Nomura | AEJ Korea Life Insurance May 16, 2011

19

Long-end should be lifted

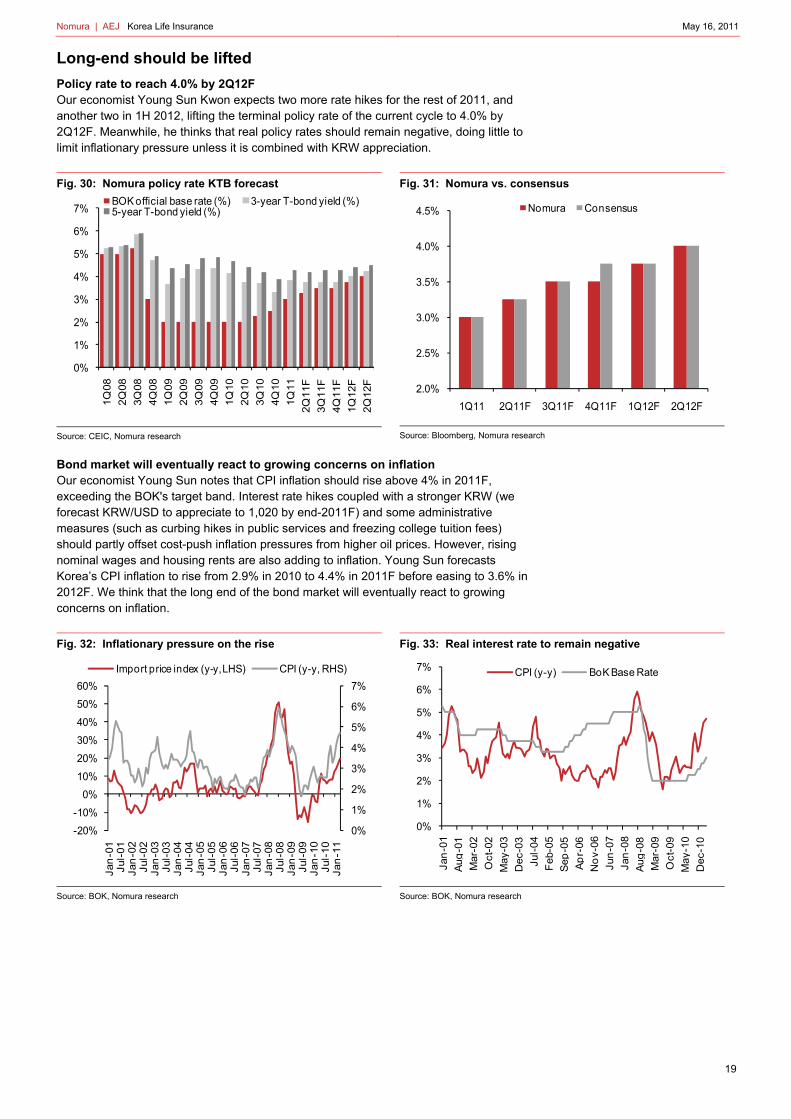

Policy rate to reach 4.0% by 2Q12F Our economist Young Sun Kwon expects two more rate hikes for the rest of 2011, and another two in 1H 2012, lifting the terminal policy rate of the current cycle to 4.0% by 2Q12F. Meanwhile, he thinks that real policy rates should remain negative, doing little to limit inflationary pressure unless it is combined with KRW appreciation.

Fig. 30: Nomura policy rate KTB forecast

Source: CEIC, Nomura research

Fig. 31: Nomura vs. consensus

Source: Bloomberg, Nomura research

Bond market will eventually react to growing concerns on inflation Our economist Young Sun notes that CPI inflation should rise above 4% in 2011F, exceeding the BOK's target band. Interest rate hikes coupled with a stronger KRW (we forecast KRW/USD to appreciate to 1,020 by end-2011F) and some administrative measures (such as curbing hikes in public services and freezing college tuition fees) should partly offset cost-push inflation pressures from higher oil prices. However, rising nominal wages and housing rents are also adding to inflation. Young Sun forecasts Korea’s CPI inflation to rise from 2.9% in 2010 to 4.4% in 2011F before easing to 3.6% in 2012F. We think that the long end of the bond market will eventually react to growing concerns on inflation.

Fig. 32: Inflationary pressure on the rise

Source: BOK, Nomura research

Fig. 33: Real interest rate to remain negative

Source: BOK, Nomura research

0%

1%

2%

3%

4%

5%

6%

7%

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11F

3Q

11F

4Q

11F

1Q

12F

2Q

12F

BOK official base rate (%) 3-year T-bond yield (%) 5-year T-bond yield (%)

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

1Q11 2Q11F 3Q11F 4Q11F 1Q12F 2Q12F

Nomura Consensus

0%

1%

2%

3%

4%

5%

6%

7%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Import price index (y-y, LHS) CPI (y-y, RHS)

0%

1%

2%

3%

4%

5%

6%

7%

Jan

-01

Aug

-01

Mar-

02

Oct-

02

May-0

3

Dec-0

3

Jul-

04

Feb-0

5

Sep

-05

Ap

r-06

No

v-0

6

Jun

-07

Jan

-08

Aug

-08

Mar-

09

Oct-

09

May-1

0

Dec-1

0

CPI (y-y) BoK Base Rate

Nomura | AEJ Korea Life Insurance May 16, 2011

20

Foreign capital inflow putting pressure on the long-end We believe that foreign capital inflow (especially from dollar block economies) into Korea has been putting pressure on the long end of the yield curve. We think that exceptionally low rates in developed countries and expectation for KRW appreciation are the primary reasons for capital inflow into Korea.

Fig. 34: 5-year KTB vs. foreign net bond buy Foreigners appetite for KTB has been strong

Source: CEIC, Nomura research

Fig. 35: Net bond buy by origin of capital The US and China money main source of capital inflow

Source: CEIC, Nomura research

Fig. 36: KRW vs. foreign net bond buy Foreign capital inflow betting on KRW appreciation?

Source: CEIC, Nomura research

Fig. 37: Flattening of Yield curve Long-end falling despite the rise in policy rate

Source: CEIC, Nomura research

Foreign capital inflow to slow Whether hunting for better yields or expecting KRW appreciation, foreign capital inflows have been adding pressure on the long-end since 2H09. However, with the ECB turning hawkish and the Fed's QE2 programme winding down, foreign capital inflows may slow and we may even witness outflows going forward. We think that the long-end of the yield curve could be lifted with rising interest rates in developed markets, as we have seen in 4Q10. In addition, the recent strengthening of KRW could hinder foreign capital inflows (funds pouring into Korea on expectations of KRW appreciation), further lifting pressure on the long-end.

0

50

100

150

200

250

300

350

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

May-10 Jun-10 Jul-10 Aug-10

KTB 5yr (LHS) Net bond buy (RHS)(%) (Wtn)

(4)

(2)

0

2

4

6

8

10

12

14

Jan

-09

Mar-

09

May-0

9

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar-

10

May-1

0

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

US UK Thailand China(Wtn)

1,0501,0701,0901,1101,1301,1501,1701,1901,2101,2301,250

3

103

203

303

403

503

603

May-1

0

Jun

-10

Jul-

10

Aug

-10

Sep

-10

Oct-

10

No

v-1

0

Dec-1

0

Jan

-11

Feb-1

1

Mar-

11

Ap

r-11

Net bond buy (LHS) FX (KRW:USD)(Wtn) (W)

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

KTB1y MSB2y KTB3y KTB5y KTB10y KTB20y

12/1/2010 1/1/2011

2/1/2011 3/1/2011

(%)

Nomura | AEJ Korea Life Insurance May 16, 2011

21

Fig. 38: Foreign net bond buy vs. US rate

Source: FSS, KOFIA, Nomura research

Fig. 39: US rate vs. KTB rate

Source: FSS, KOFIA, Nomura research

Long-end expected to rise slowly but surely Young Sun forecasts that the five-year treasury yield will start to rise in 3Q11F and reach 4.5% by the end of 1H12F from the current yield of 4.0%, and the three-year treasury will reach 4.2% by the end of 1H12F from the current yield of 3.6%.

Fig. 40: Nomura interest rate forecast

Source: BOK, Nomura research

Benefits from rising rates

Korean lifers have significant exposure to fixed-rate policies The benefit from rising rates is clearly evident for life insurers with large exposure to fixed-rate policies, in our view. The reserve for fixed-rate policies as a proportion of interest-bearing reserve amounts to 60% for Samsung Life, 70% for Korea Life and 56% for Tong Yang Life.

Valuation sensitivity highest for Korea Life Our valuation sensitivity is the highest for Korea Life given that it has the largest exposure to fixed rate policies. Korea Life has the highest exposure to fixed-rate policies given the company’s focus on variable insurance. Although we think it is the right strategy for the company given its capital constraints, the approach has resulted in a larger duration gap than its peers. Variable products require less capital than traditional

300

320

340

360

380

400

420

440

460

480

500

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11

US TN 5y (LHS) Net bond buy (RHS)(%) (Wtn)

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11

US TN 5y (LHS) KTB 5yr (LHS)(%) (%)

1%

2%

3%

4%

5%

6%

7%

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

F

3Q

11

F

1Q

12

F

3yr T-bond yield 5yr T-bond yield BoK base rate

Forecast

Nomura | AEJ Korea Life Insurance May 16, 2011

22

products, but as savings premium gets booked to a separate account, it would not have dilutive effect in terms of general account crediting rate.

But Korea Life also has the highest hurdle Although Korea Life is most sensitive to rising rates, we do not think the stock will outperform its peers given that its hurdle rate is the highest among the Korean Lifers and we expect a slow rise in the long-end of the yield curve.

Fig. 41: % of fixed rate liabilities (December 2010)

Source: Company data, Nomura research

Fig. 42: Proportion of high yield guarantee policies yielding 6% and over

Source: Company data, Nomura research

70%

60% 58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Korea Life Samsung Life TYL

5.4%

5.6%

5.8%

6.0%

6.2%

6.4%

6.6%

Jun09 Sep09 Dec09 Mar10 Jun10 Sep10 Dec10

Korea Life Samsung Life Tong Yang Life

Nomura | AEJ Korea Life Insurance May 16, 2011

23

Long-term positive industry outlook We believe the Korean life insurance market still has room to grow, given relatively low insurance density. We expect investment-linked products and corporate pension to continue to provide growth opportunities. We also believe the profitability of lifers will likely improve as negative spread books mature and new low-yield floating rate policies dilute their in-force book.

Now entering the longevity market

Second baby boomers the source of traditional life insurance Traditional life insurance (eg, whole life and term life) started to grow meaningfully only in early 2000s. Demand for traditional life insurance could fall as baby boomers start to retire, in our view. However, Korea has the second group of 7mn baby boomers (14% of total population, born in 1968–1976) that could be a continued source of demand for traditional life insurance. The ‘second baby boomers’ are now having families and are seeking protection for their family in case of death or critical illness.

Demand for wealth accumulation products still rising Investment-linked insurance in Korea, introduced only in recent years, started to show a meaningful growth only in late 2000s. Although new business volume fell sharply due to the global credit crisis, the volume has been picking up again as the market recovers. We remain positive on the long-term demand for investment linked insurance given that they could provide guaranteed stream of income for life with potential for upside and tax advantages (e.g., variable annuity).

First baby boomers now looking for protection against longevity risk We expect strong growth in demand for products that manage longevity risk (eg, income annuities and long-term care insurance) as the first group of 8mn baby boomers (16% of total population, born in 1946-1964) start to retire this year. People are healthier and living longer, and are fearful of outliving their assets (ie, longevity risk). Hence, boomers will seek sources of lifetime income and long-term care insurance given limited pension and healthcare support from the government and corporations.

Fig. 43: Life insurance product migration Korea now entering the third stage "longevity market"

Source: Nomura research

PROTECTION2000 ~

ACCUMULATION2005 ~

LONGEVITY2010 ~

Mortality Risk

Morbidity Risk

Asset Accumulation

Tax Avoidance

Estate Planning

Asset Protection

Longevity Risk

Quality of Life

Nomura | AEJ Korea Life Insurance May 16, 2011

24

Korean retirees not prepared for longevity risk

Rapidly changing demographic to support life industry We expect a rapid change in demographics for the next ten years. In 2020, all of the first baby boomers will be in retirement, and all of the second baby boomers will face retirement. However, it seems like both the first and second baby boomers are not fully prepared for retirement. That said, we think demand for wealth accumulation and longevity products should remain healthy for the next 10 years.

Fig. 44: 2010 demographic First baby boomers about to retire

Source: KOSIS, Nomura research

Fig. 45: 2020 demographic Demand for wealth accumulation & longevity products to increase

Source: KOSIS, Nomura research

Retirees don’t have enough income from insurance and annuities… The first baby boomers are about to retire. However, retirees are not fully prepared for life after retirement. Insurance and annuities only make up a small proportion of Korean retirees' income. In addition, government pension only makes up 7% of retirees' income. Therefore, most of retirees in Korea are still dependant heavily on family support, or have to work even after retirement.

Fig. 46: US retirees’ income breakdown

Source: Korea Institute for Health and Social Affairs, Nomura research

Fig. 47: Korea retirees’ income breakdown

Source: Korea Institute for Health and Social Affairs, Nomura research

3,000 2,000 1,000 0 1,000 2,000 3,000

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 7475 - 7980 - 8485 - 8990 - 94

Female Male

1st Baby boom generationAge 47 - 56 (1955-64)

('000)

2nd Baby boom generationAge 36 - 43 (1968-75)

(Age)

2,500 1,500 500 500 1,500 2,500

0 - 45 - 9

10 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 7475 - 7980 - 8485 - 8990 - 94

Female Male

1st Baby boom generationAge 57 - 66 (1955-64) 2nd Baby boom generation

Age 46 - 53 (1968-75)

('000)

(Age)

Public pension,

55%

Support from family,

2%

Savings, insurance & annuities,

23%

Earned income,

16%

Others, 4%Public

pension, 7%

Support from family,

56%

Savings, insurance & annuities,

10%

Earned income,

27%

Nomura | AEJ Korea Life Insurance May 16, 2011

25

…because Koreans depend heavily on real estate for wealth accumulation We think that one of the key reasons is a heavy dependence on real estate for wealth accumulation and a reluctance to cash out of real estate due to expectation of capital gains. However, we think that as expected returns from real estate investment decline, the proportion of insurance and pension as a percentage of total household assets will likely increase going forward.

Fig. 48: Household asset breakdown (2006) Koreans depends heavily on real estate for wealth accumulation

Source: BOK, CEIC, Nomura research

Fig. 49: Household financial asset breakdown (2009) Koreans have most of their financial assets in bank deposits

Source: BOK, CEIC, Nomura research

Family support may not be an option anymore In our view, retirees will soon realise that they cannot depend on family support for retirement income any more. A demographic transition is in progress in Korea. Decreasing fertility along with lengthening life expectancy is reshaping the age structure of the population. According to the Korean Statistical Information Service (KOSIS), Korea recorded a birth rate of 1.15 in 2009, which is the lowest globally. This means that support from kids can no longer serve as a substitute for insurance and pensions.

National pension system is not reliable In addition, the change in demographic will likely put pressure on national pension system. National Pension System Chairman warned that due to the change in demographic, the national pension fund could be depleted by year 2064. This means that the payout scheme could be changed to preserve the fund, and so Koreans cannot rely on national pension as a primary source of income after retirement.

23%

46%

61%67%

77%

54%

39%33%

0

10

20

30

40

50

60

70

80

90

100

Korea UK Japan US

Financial assets Tangible assets(%)

24% 27% 28%

50%

46%

56%

18%

32%

12%

6%

10%

1%

18% 7%

24%

12%

3%

20%

5%

0

10

20

30

40

50

60

70

80

90

100

Korea Japan US UK

Insurance & pension Cash & deposit Bond Stock Other(%)

Nomura | AEJ Korea Life Insurance May 16, 2011

26

Fig. 50: Koreans are having fewer kids Korean retirees cannot rely on family support anymore

Source: KOSIS, Nomura research

Fig. 51: Korean population aging fast Age 60 and over as a proportion of population to reach 30% by 2030

Source: KOSIS, Nomura research

Plenty of room for growth

Korean life insurance market appears to be a mature market Korea is already one of the largest life insurance markets globally. Korea is the eighth-largest life insurance market after Italy and the third-largest in Asia after China by premium volume. In addition, the penetration ratio (premium as % of GDP) of life insurance is fairly high at 6.5%. Note that as Korean non-life insurers are multi-liners that participate in the life business, the actual penetration ratio should be even higher.

Fig. 52: Korea is eighth-largest life insurance market (2009)

Source: Swiss re sigma

Fig. 53: Korea is 10th most penetrated market (2009)

Source: Swiss re sigma

Survey says most households already own life insurance According to a survey conducted by Korea Life Insurance Association (KLIA) in 2009, most of Korea’s households (with an exception of poor and uneducated) already own life insurance.

0

1

2

3

4

5

0

200

400

600

800

1,000

1,2001

970

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

Number of births ('000) Birth rate (%)

0

10

20

30

40

50

60

199019921994199619982000200220042006200820102012201420162018202020222024202620282030

(mn) Below 20 20~64 Above 65

050

100150200250300350400450500

US

Jap

an

UK

fran

ce

Germ

any

Ch

ina

Italy

Ko

rea

Ind

ia

Taiw

an

Can

ad

a

Sp

ain

(US$ bn)

0

2

4

6

8

10

12

14

Taiw

an

So

uth

Afr

ica

UK

Ho

ng K

ong

Jap

an

Fin

land

Fra

nce

Den

mark

Irela

nd

Ko

rea

Po

rtug

al

(%)

Nomura | AEJ Korea Life Insurance May 16, 2011

27

Fig. 54: Percentage of households owning life insurance by income level (2009) 84.5% of households already have life Insurance

Source: Nomura research

Fig. 55: Percentage of households owning life insurance by education level (2009)

Source: Nomura research

But insurance density shows a different picture However, based on insurance density it appears that the Korean market is still underdeveloped. We think that one of the key reasons is due to fewer females in Korea participating in the workforce than more developed countries (and lower wage level than that of males). In addition, the insurance penetration ratio, which is measured based on the GDP figure, could be overstated given that the Korean economy is more trade oriented.

Fig. 56: Proportion of female in workforce trend (Korea) Female employment rising continuously

Source: CEIC, Nomura research

Fig. 57: Proportion of female in workforce by country (2009)Fewer Korean females participate in workforce

Source: CEIC, Nomura research

0 10 20 30 40 50 60 70 80 90 100

~W12m 12~24m 24~36m 36~48m 48~60m W60m~

Average =84.5%

(%)

0 10 20 30 40 50 60 70 80 90 100

Elementary Middle High College

(%)

38 38 39 39 40 40 41 41 42 42 43

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

(%)

40

41

42

43

44

45

46

47

48

US Japan Korea

(%)

Nomura | AEJ Korea Life Insurance May 16, 2011

28

Fig. 58: Insurance density: premium per capita in USD (2009)

Source: Swiss re sigma

Further study by KLIA survey shows a different picture According to KLIA’s survey, 84.5% of households surveyed own life insurance. However, a breakdown of insurance products shows that most of the households have healthcare and casualty policies with low monthly payments and a large proportion of the households acknowledge that their current insurance assets seem insufficient.

Fig. 59: Most households that own life insurance have very little exposure to wealth accumulation products (2009) Current ownership is skewed to healthcare and casualty products with low monthly payments

Source: KLIA, Nomura research

Fig. 60: More households that already own life insurance feel their insurance assets are insufficient (2009) Even among the households that already own wealth accumulation products feel the need for more

Source: KLIA, Nomura research

Ranking Country Life business Non-life Total

1 Denmark 3,816 1,713 5,529

2 UK 3,528 1,051 4,579

3 Ireland 3,437 1,079 4,516

4 Sw itzerland 3,405 2,853 6,258

5 Finland 3,380 873 4,253

6 Luxembourg 3,229 1,998 5,227

7 Japan 3,139 840 3,979

8 France 2,980 1,289 4,269

9 Hong Kong 2,887 417 3,304

10 Sw eden 2,690 850 3,540

11 Liechtenstein 2,350 23 2,373

12 Belgium 2,323 1,171 3,494

13 Taiw an 2,257 495 2,752

14 Norw ay 2,074 1,351 3,425

15 Netherlands 2,046 4,508 6,554

16 Singapore 1,912 645 2,557

17 Italy 1,878 851 2,729

18 US 1,603 2,107 3,710

19 Autralia 1,525 1,307 2,832

20 Germany 1,360 1,518 2,878

21 Portugal 1,357 549 1,906

22 Canada 1,300 1,644 2,944

23 Austria 1,236 1,507 2,743

24 Korea 1,180 710 1,890

25 Spain 853 949 1,802

26 New Zealand 249 1,318 1,567

27 Malaysia 207 115 322

28 Thailand 92 62 154

29 India 48 6 54

30 Indonesia 22 10 32

0 10 20 30 40 50 60 70 80 90 100

Healthcare Casualty Death Pension Savings Variable

(%)

20

30

40

50

60

Healthcare Casualty Death Pension Savings Variable

Sufficient Insufficient(%)

Nomura | AEJ Korea Life Insurance May 16, 2011

29

Plenty of new business We should note that Korean lifers' average 25th month lapse ratio for the past seven years has stood at 36%. This means that nearly four out of ten contracts are no longer in-force after two years. Although a higher lapse ratio has a negative impact on VIF, it tends to have a positive impact on new business volume. Currently reported VIF by Korean lifers already reflect such a high lapse ratio. That said, we think there is little downside to new business volume for Korean lifers.

Fig. 61: Current 13th month persistency ratio is 76%

Source: FSS, Nomura research

Fig. 62: Current 25th month persistency ratio is 56%

Source: FSS, Nomura research

Underdeveloped compared to the banking sector The banking sector has gone through several rounds of restructuring since 1998 at the onset of the Asian Financial Crisis. As a result, the banking sector has emerged significantly healthier and profitable, in our view. We think that there are too many players with very little capital in the life insurance sector. We expect the government to introduce initiatives (such as a transition to risk-based capital) as part of its ongoing effort to restructure the financial sector.

Fig. 63: Total assets by sector (FY10)

Source: FISIS, Nomura research

Fig. 64: Shareholders' equity by sector (FY10)

Source: FISIS, Nomura research

Wealth accumulation products to drive growth

Death insurance growth slowing but not over yet Until late 1990s, Korean life insurers sold mostly savings type policies that have a very limited risk premium. We think savings type policies are mere substitutes for deposits. In addition, savings type policies have been a money-losing business for most of the life

60

65

70

75

80

85

90

1H

04

2H

04

1H

05

2H

05

1H

06

2H

06

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

(%) Korea Samsung KyoboMirae asset Tong Yang

40

45

50

55

60

65

70

75

80

1H

04

2H

04

1H

05

2H

05

1H

06

2H

06

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

(%) Korea Samsung KyoboMirae asset Tong Yang

0

200

400600

800

1,000

1,200

1,400

1,600

1,800

Bank Insurance Brokers

(Wtn)

0

20

40

60

80

100

120

140

Bank Insurance Brokers

(Wtn)

Nomura | AEJ Korea Life Insurance May 16, 2011

30

insurers. That said, we think growth of protection type policies that has a higher embedded margin is better than what we could infer from the insurance penetration rate.

Fig. 65: Premium growth by product (general account)

Source: KLIA, Nomura research

Fig. 66: Premium income by function

Source: KLIA, Nomura research

Separate account to derive growth We expect separate accounts, which include investment-linked insurance and corporate pension, to remain as the main growth driver for the Korean life insurers. The separate account business will increase insurers’ commission income with a minimum charge of capital cost, as investment risks transfer to policyholders of separate account products. The demand for variable insurance and pension products should increase with need for wealth accumulation and financial security, in our view.