U HOTELS FINANCIAL POLICY MANUAL R

283

May 2019 | CEO U HOTELS & RESORTS FINANCIAL POLICY MANUAL

Transcript of U HOTELS FINANCIAL POLICY MANUAL R

Page | 1

May 2019 | CEO

U HOTELS

&

RESORTS FINANCIAL POLICY MANUAL

Page | 2

TABLE OF CONTENTS

SECTION 1 ADMINISTRATION

ADM – 100 CHANGES, ADDITIONS AND MODIFICATIONS ............................................................. 9

ADM – 101 ROLE AND RESPONSIBILITY .............................................................................................. 11

ADM – 102 ACCOUNTING PRINCIPLES ............................................................................................... 15

ADM – 103 INTERNAL CONTROLS........................................................................................................ 17

ADM – 104 CODE OF ETHICS ................................................................................................................. 18

ADM – 105 CRITICAL DATE LIST ........................................................................................................... 20

ADM – 106 GUEST SAFETY DEPOSIT BOXES ...................................................................................... 21

ADM – 107 MASTER KEYS ........................................................................................................................ 22

ADM – 108 MOBILE PHONE AND PAGER CONTROL ....................................................................... 29

ADM – 109 LICENSE AND PERMITS ...................................................................................................... 32

ADM – 110 CONTRACTS .......................................................................................................................... 33

ADM – 111 LITIGATION AND OTHER CONTINGENCIES ............................................................... 35

ADM – 112 HOTEL OPERATING AGREEMENT ADMINISTRATION .............................................. 36

ADM – 113 LAW ENFORCEMENT AUTHORITIES .............................................................................. 37

ADM – 114 ADMINISTRATION PHONE USAGE ................................................................................. 38

ADM – 115 STAFF INCENTIVE PROGRAMS ......................................................................................... 39

ADM – 116 CONTROL OF BANK CHEQUES ........................................................................................ 42

ADM – 117 FINANCIAL CONTROLLER HANDOVER ........................................................................ 44

ADM – 118 RECORDS RETENTION ....................................................................................................... 49

ADM – 119 ACCESS TO RECORDS ......................................................................................................... 50

ADM – 120 INTELLECTUAL PROPERTY ............................................................................................... 52

ADM – 121 CONTINGENCY PLANS ....................................................................................................... 53

ADM – 122 FRAUD AND THEFT ............................................................................................................. 54

SECTION 2 ACCOUNT RECEIVABLE

A/R – 100 CREDIT APPROVALS ............................................................................................................ 56

A/R – 101 CREDIT MEETINGS .............................................................................................................. 58

Page | 3

A/R – 102 CREDIT – FRONT OFFICE ................................................................................................... 59

A/R – 103 DIRECT BILLING ................................................................................................................... 63

SECTION 2 ACCOUNT RECEIVABLE

A/R – 104 CREDIT CARD PROCEDURES ........................................................................................... 64

A/R – 105 COLLECTIONS ....................................................................................................................... 65

A/R – 106 USE OF COLLECTION AGENCIES .................................................................................... 66

A/R – 107 COLLECTION LETTERS ....................................................................................................... 67

A/R – 108 RETURNED ITEM – CHEQUES AND CREDIT CARDS ................................................. 68

A/R – 109 ACCOUNTS RECEIVABLE BALANCING ......................................................................... 70

A/R – 110 ACCOUNTS BALANCE VERIFICATION .......................................................................... 71

A/R – 111 PAYMENTS / POSTING TO CITY LEDGER ...................................................................... 72

A/R – 112 RESERVE FOR DOUBTFUL DEBTS ................................................................................... 73

A/R – 113 WRITE OFF BAD DEBTS ...................................................................................................... 74

SECTION 3 REVENUE CONTROL

REV – 100 PRICING POLICY ................................................................................................................... 76

REV – 101 ROOMS REVENUE ................................................................................................................ 77

REV – 102 FOOD & BEVERAGE REVENUE ........................................................................................ 79

REV – 103 OTHER REVENUE ................................................................................................................. 81

REV – 104 GROUP CONTRACTS........................................................................................................... 83

REV – 105 BANQUET POSTING REVIEW ............................................................................................ 84

REV – 106 ALLOWANCES AND REBATES........................................................................................... 86

REV – 107 BARTER AGREEMENTS ....................................................................................................... 87

REV – 108 OUTBOOKINGS ..................................................................................................................... 89

REV – 109 NIGHT AUDIT / INCOME AUDIT PROCEDURES ......................................................... 90

REV – 110 BREAKFAST INCLUDED AND PACKAGE PROGRAMS ................................................ 97

REV – 111 GUEST CHARGES AFTER DEPARTURE .......................................................................... 99

REV – 112 NO-SHOW, CANCELLATION AND GUARANTEED BOOKINGS .............................. 100

REV – 113 GIFT CERIFICATES ............................................................................................................. 101

REV – 114 COMPLIMENTARY ROOMS .............................................................................................. 103

Page | 4

REV – 115 ADVANCE DEPOSIT REFUNDS ....................................................................................... 104

REV – 116 PROMOTIONAL CHARGES .............................................................................................. 105

REV – 117 INTERCOMPANY CHARGES ............................................................................................ 107

SECTION 4 CASH

CSH – 100 ESTABLISHING / CLOSING BANK ACCOUNTS .......................................................... 109

CSH – 101 BANK ACCOUNT RECONCILIATIONS.......................................................................... 110

CSH – 102 CASHIER FUNDS / FLOATS / HOUSE BANKS ............................................................. 113

CSH – 103 DAILY CASHIER DEPOSITS .............................................................................................. 117

CSH – 104 CASHIER OVER / SHORT REPORTING ......................................................................... 119

CSH – 105 BANK DEPOSITS .................................................................................................................. 120

CSH – 106 DAILY DEPOSIT WITNESS LOGS ..................................................................................... 121

CSH – 107 CASHIER DUE BACKS ........................................................................................................ 122

CSH – 108 TRAVELLERS CHEQUES ................................................................................................... 123

CSH – 109 GUEST PAID OUTS ............................................................................................................. 124

CSH – 110 PETTY CASH ......................................................................................................................... 125

CSH – 111 PAYMENTS RECEIVED BY MAIL ...................................................................................... 126

CSH – 112 FLOAT INCREASES ............................................................................................................. 127

CSH – 113 DEBT ...................................................................................................................................... 129

CSH – 114 CASH MANAGEMENT ........................................................................................................ 130

SECTION 5 INVENTORY

INV – 100 RECEIVING PROCEDURES............................................................................................... 132

INV – 101 INVENTORY STOREROOMS ............................................................................................ 134

INV – 102 REQUISITIONS .................................................................................................................... 136

INV – 103 BEVERAGE CONTROL ....................................................................................................... 137

INV – 104 SMALL OPERATING EQUIPMENT .................................................................................. 139

INV – 105 STOCK CARD ....................................................................................................................... 140

INV – 106 MONTHLY AND ANNUAL STOCK - TAKE .................................................................... 141

SECTION 6 EXPENDITURE

Page | 5

EXP – 100 APPROVAL LEVELS ............................................................................................................. 143

EXP – 101 PURCHASE ORDERS .......................................................................................................... 144

EXP – 102 VENDOR CREDIT APPLICATIONS.................................................................................. 147

EXP – 103 PAYMENTS ............................................................................................................................ 148

SECTION 6 EXPENDITURE

EXP – 104 TRAVEL AND EXPENSE REIMBURSEMENT ................................................................. 150

EXP – 105 PREPAID EXPENSES ............................................................................................................ 156

EXP – 106 RECEIVING ........................................................................................................................... 157

EXP – 107 IN-HOUSE FUNCTIONS ..................................................................................................... 158

EXP – 108 ACCRUALS ........................................................................................................................... 159

EXP – 109 DEFERRED EXPENSES........................................................................................................ 161

EXP – 110 TRAVEL AGENT COMMISSIONS ..................................................................................... 162

EXP – 111 SEGREGATION OF DUTIES .............................................................................................. 163

EXP – 112 STAFF LOANS AND ADVANCES ...................................................................................... 164

EXP – 113 EXTERNAL CONSULTANT AND SERVICE ................................................................... 165

SECTION 7 INTERNAL CONTROL OVER FINANCIAL REPORTING

REP – 100 FINANCIAL REPORTING STANDARDS ......................................................................... 167

REP – 101 JOURNAL ENTRY STANDARDS ....................................................................................... 168

REP – 102 FOOD AND BEVERAGE INTRA – DEPARTMENT ALLOCATION ............................ 169

REP – 103 ALLOCATION OF SHARED EXPENSES .......................................................................... 170

REP – 104 LAUNDRY DEAPTMENT ACCOUNTING ...................................................................... 171

REP – 105 STATEMENT OF FINANCIAL POSITION RECONCILIATIONS ................................. 172

REP – 106 FINANCIAL STATEMENTS ANALYSIS ............................................................................ 174

REP – 107 INTERCAOMPANY BILLINGS ........................................................................................... 176

REP – 108 GENERAL LEDGER ACCOUNT APPROVAL ................................................................. 177

REP – 109 FC MONTHLY CHECKLIST ............................................................................................... 178

REP – 110 INTERNAL CONTROL CHECKLIST ................................................................................ 180

REP – 111 STATEMENT OF FINANCIAL POSITION REVIEWS..................................................... 181

Page | 6

REP – 112 INTERNAL AUDIT ............................................................................................................... 182

REP – 113 EXTERNAL AUDIT REPORTS ........................................................................................... 183

SECTION 8 CAPITAL EXPENDITURE

CAP – 100 DEFINITION OF CAPITAL EXPENDITURE .................................................................... 185

CAP – 101 ANNUAL CAPEX BUDGET ................................................................................................ 187

SECTION 8 CAPITAL EXPENDITURE

CAP – 102 MONTHLY REPORT ............................................................................................................ 188

CAP – 103 CAPITAL EXPENDITURE AUTHORITY .......................................................................... 189

CAP – 104 ASSET DISPOSAL ................................................................................................................. 192

CAP – 105 LEASES ................................................................................................................................... 193

CAP – 106 DEPRECIATION AND AMORTIZATION ........................................................................ 194

CAP – 107 FIXED ASSET REGISTER .................................................................................................... 197

CAP – 108 SMALL OPERATING EQUIPMENT .................................................................................. 199

SECTION 9 BEST PRACTICE

BEP – 100 REVENUE CONTROL ......................................................................................................... 202

BEP – 101 PROCUREMENT, ACCOUNTS PAYABLE, TRAVEL EXPENSES ................................ 206

BEP – 102 ACCOUNTS RECEIVABLE ................................................................................................ 210

BEP – 103 INVENTORY ......................................................................................................................... 213

BEP – 104 PAYROLL ............................................................................................................................... 216

SECTION 10 INFORMATION TECHNOLOGY GENERAL CONTROL

ITGC – 100 INFORMATION SYSTEMS SECURITY POLICY ............................................................. 222

ITGC – 101 IT ORGANIZATION ............................................................................................................. 223

ITGC – 102 SOFTWARE DEVELOPMENT,ACQUISITION AND MAINTENANCE ...................... 224

ITGC – 103 LOGICAL SCCESS TO PROGRAM AND DATA ............................................................. 225

ITGC – 104 BACK-UP RECOVERY AND CONTIGENCY PLAN ....................................................... 227

SECTION 11 BUSINESS PLAN/BUDGET GUIDELAINES

BP – 100 BUSINESS PLAN SUBMISSION ......................................................................................... 230

Page | 7

BP – 101 BUSINESS PLAN SENSITIVITY .......................................................................................... 231

BP – 102 MARKET SEGMENT STATICITICS .................................................................................. 232

BP – 103 ROOM DIVISION ................................................................................................................. 233

BP – 104 FOOD AND BEVERAGE DIVISION ................................................................................. 236

BP – 105 TELEPHONE DEPARTMENT ............................................................................................. 240

BP – 106 BUSINESS CENTER DEPARTMENT ................................................................................ 242

BP – 107 FITNESS CENTER DEPARTMENT .................................................................................... 243

BP – 108 GUEST LAUNDRY DEPARTMENT................................................................................... 245

SECTION 11 BUSINESS PLAN/BUDGET GUIDELAINES

BP – 109 LOBBY SHOP DEPARTMENT ............................................................................................ 247

BP – 110 GARAGE/CARPARK DEPARTMENT ............................................................................... 249

BP – 111 OTHER INCOME AND RENTALS .................................................................................... 250

BP – 112 ADMINISTRATION AND GENERAL DIVISION ............................................................ 252

BP – 113 HUMAN RESOURCE DIVISION ....................................................................................... 254

BP – 114 EMPLOYEE RESTAURANT DEPARTMENT .................................................................... 255

BP – 115 SALE AND MARKETING DIVISION ................................................................................. 256

BP – 116 PROPERTY OPERATIONS AND MAINTENANCE DIVISION ..................................... 258

BP – 117 PAYROLL AND RELATED EXPENSES ............................................................................. 261

BP – 118 PROVISION FOR REPLACEMENT OF OPERATING EQUIPMENT ........................... 264

BP – 119 FIXED CHARGES AND OTHER DEDUCTIONS ............................................................ 265

Page | 8

SECTION 1

ADMINISTRATION

Page | 9

Finance Policy and Procedure

Subject: Changes, Additions and Modifications Department: Finance Reference # ADM 100 Page: 1/2 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 100 CHANGES, ADDITIONS AND MODIFICATIONS POLICY Any suggested changes, variations, additions or modifications to this Finance Policy and Procedure Manual must be reviewed and approved by the CEO before implementation. All Financials Controllers must ensure that manuals assigned to their area of responsibility are updated when required and that any revised policies and procedures are distributed and implemented within the periods indicated. Deviation to policy will be considered where the specific policy is not applicable, would be detrimental to operations, or otherwise impose undue hardship to the Hotel. PROCEDURE 1. Financial Controllers are responsible for full compliance with the accounting policies and procedures within the

manual. 2. CEO will approve changes, additions or modifications to the manual, which will be done via written

memorandum. This will include and necessary revised index and dates which the revisions become effective and also when the revision must be implemented.

3. Financial Controllers must ensure that all manuals assigned to their hotel contain the most recent policies and procedures.

4. Any suggested changes, additions or modifications to the manual are invited and should be forwarded to the Regional Managing Director, Regional Finance leader and Corporate Finance leader for consideration who will liaise with the CEO on possible incorporate or adjustment to existing policies.

5. If, for any reason, a given policy or procedure cannot be implemented at a hotel, it is the Financial Controllers’ responsibility to advise the Regional Managing Director and Regional Finance leader as well as Corporate Finance. An Approval Exception Form must be completed with details of the relevant Standard Operating Procedure (SOP) to be considered for exemption, stating why the exemption is justified and submitting an alternative policy or procedure which meets the relevant control within the operating environment of the hotel.

6. Any approved exemptions must be filed in the Policy Manual attached to the relevant SOP.

Page | 10

Reference: Changes/Addition/Exception Request Form

U Hotels & Resort

Finance Policy - Change / Addition / Exception Request

No:

Hotel: Date:

Policy Manual

Section:

Subject:

Code:

Issued Date:

Proposed Hotel Policy/Procedure

Reason for Change / Exception

Page | 11

Attach recommended procedure (must be typed)

Signatures

General Manager: Date:

Financial Controller: Date:

Regional Managing Director: Date:

Regional/Corporate Finance: Date:

Finance Policy and Procedure

Subject: Role and Responsibility Department: Finance Reference # ADM 101 Page: 1/4 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 101 ROLE AND RESPONSIBILITY POLICY All hotel Financial Controllers have a dual relationship. First, on a functional basis the Financial Controller will report to the Regional Finance Leader. Second being the Hotel Management Team. Primary responsibility of the Financial Controller is to provide support to the General Manager in achieving the established business goals and targets. It is essential that a spirit of teamwork to be maintained with operations management at each level within the organization. At no time will any violation of the Company’s policies or accepted practices be tolerated, nor may the independent reporting of such incidences in any way be overridden, except within the Financial Controller’s organizational structure or where policy so directs. The Financial Controller should provide sound business and financial management support; management of internal control, and timely accurate management reporting and analysis in order to ensure objectives are achieved or

Page | 12

exceeded. The Financial Controller must use broad business approaches in decision-making, communicating these effectively and providing support where necessary. The Financial Controller and General Manager are jointly responsible for compliance with the contractual and legal obligations of the hotel. In addition, they are also responsible in ensuring that the hotel is compliant with the Finance Standard Operating Procedures, Management Contract and any other corporate policies. Any deviations from these documents must be authorized in writing by the appropriate level of authority The Financial Controller must review and discuss the financial results of the hotel on a timely basis and ensure any risks are addressed. The Financial Controller must ensure that the General Manager is aware of all reporting deadlines and that the General Manager has reviewed and approved the reports before submission to the corporate office and owners. On a day to day basis the Financial Controller is to maintain control over a Hotel’s revenue, expenditure, assets and cash flow. The Financial Controller is also responsible for providing effective budgeting documents and controls in conjunction with analysis of current financial statements. PROCEDURE Principal accountabilities include, but are not restricted to, the following: • Directs, prepares and provides financial analysis of operations for use by management. • Implements control functions ensuring that reasonable and effective internal accounting and procedural controls

are in place. • Directs the operation of the hotel’s accounting department, and ensures that a consistent review of all work is

performed accurately. • Ensures timely and accurate management and financial reporting. • Assists the General Manager in Manager in maximizing financial performance. • Serves as the highest financial executive member of his respective organization, and accordingly, represents the

Company on matters pertaining to banking, credit, contracts, legal issues, interaction with owners, lenders, etc. as required.

• Ensures strict compliance with local fiscal regulation. • Manages the IT department/requirements within the property, where appropriate. • Organizes an efficient treasury function, which provides proper management of the hotels working capital and

cash flow within U Hotels & Resorts guidelines and the requirements of the hotel’s management contract. Standards of Performance

Hotel Financial Controllers are responsible for supporting the financial goals of the Hotel Executive committee and department heads. Hotel Financial Controllers must provide the financial support that the General Managers need to meet their bottom line objectives. In addition, Hotel Financial Controllers are expected to meet with General Managers on a regular basis to assist in hotel development and guest satisfaction efforts. Hotel Financial Controllers must take a pro-active role in recommending revenue enhancement and cost reduction opportunities to the Hotel Executive Committee. They must also encourage their subordinates to raise and discuss their own ideas for revenue enhancement and cost reduction and present the forum to do so. Hotel Financial Controllers are responsible for recording and safeguarding the assets of the hotel. Hotel Financial Controllers must work to support the hotel’s service standards and accept nothing less from their subordinates. Hotel Financial Controllers may not delegate responsibility of service to department staff. Hotel Financial Controllers must take the lead in developing an environment in which all department heads take responsibility for forecasting the hotel’s operating and financial performance. The Hotel Financial Controllers must ensure all departmental heads have been advised of their contribution required to complete an accurate forecast. All heads of departments must understand that forecasting is used as an early warning system of potential future problems/ issues enabling corrective action to take place.

Page | 13

Following the production of the period end accounts the Financial Controller must present clear variance analyses of the monthly performance to the General Manager and department heads. Hotel Financial Controllers must take personal responsibility for auditing Statement of Financial Position accounts. Reconciliations must be prepared and cleared on a monthly basis. Hotel Financial Controllers are responsible for the timely delivery of all reports required by Head office. Hotel Financial Controllers must actively manage cash flow with a view to maintaining working capital balances at a minimum. Float balances must be reviewed to verify that the correct amount of money is in circulation. Food and beverage inventories and accounts receivables must be maintained at minimum levels Prepaid Expenditure must be maintained at a minimum with no amount prepaid more than twelve months ahead. Non-disputed invoices and dues to government bodies must be settled on a timely basis. Travel agent commissions must be paid as soon as possible after the departure of the guest. Surplus finds must be delivered to the owner as specified in the management contract. Hotel Financial Controllers are responsible for conducting performance evaluations of all supervised staff. A copy of the appraisal must be submitted to the human resources department for their files. Hotel Financial Controllers are responsible for their self-development and are expected to participate in internal or external management and technical training programs. Hotel Financial Controllers are expected to review, train, and develop their subordinates. In conjunction with the Human Resource Department, Hotel Financial Controllers must prepare a continuity plan to determine their future staffing needs and to identify individuals with high potential in their departments. Hotel Financial Controllers must take personal responsibility for the management and maintenance of their hotels’ IT systems. In addition, they must ensure that all data is processed in a timely manner, without corruption and then department heads understand and take advantage of the systems’ full capabilities. Hotel Financial Controllers must take the full annual leave accruing to them by law or employment contract, and ensure that their staff does the same. Without prior approval of the General Manager, personnel are not permitted to carry over their annual leave to the following year. Hotel Financial Controllers must be ready to respond to ad-hoc request by owners, the hotel General Manager, colleagues, and guest on a timely basis without any significant impact on their ongoing duties.

Reporting Relationships of Hotel Controllers Hotel Financial Controllers have a dual reporting relationship. First, on a functional basis Hotel Financial Controllers report directly to the Regional Finance leader. This reporting relationship is an essential business approach and a key line of communication that must be kept open at all times. Second, and equally important, Financial Controllers are members of the hotel Executive committee and an integral part of the hotel management team. The Financial Controller’s primary responsibility as a member of the Executive Committee is to provide support to the General Manager in achieving established business goals. At all times, the Hotel Financial Controller must be responsive to the General Manager by providing sound business and financial management support; appropriate and practical management of internal control; and timely, accurate management reporting and analysis in order to ensure that bottom line objectives are achieved or exceeded.

Reporting line for the Financial Controllers

CEO Corporate Finance Leader

Page | 14

RMD Regional Finance Leader GM FC

The Hotel Financial Controller must take a broad business approach in decision making. The Financial Controller should contribute as a member of the hotel management team in a co-operative and supportive manner, stressing joint decision making and effective communication. The Hotel Financial Controller should approach communication with the General Manager, other Executive Committee members, and key department heads in a constructive and positive manner. All members of the Financial Controller’s Department should understand that they too are members of the Hotel Operations team. Therefore, they also must approach their communications with other operating departments in the same manner. The Financial Controller must give the General Manager the opportunity to provide input before financial reports are forwarded to owners and Head Office. In this regard, the Hotel Financial Controller should ensure that the General Manager is familiar with all reporting deadlines and other requirements. If the Hotel Financial Controller and General Manager disagree on any Financial Controllership or financial issue for any reason, and this difference cannot be resolved at the hotel level, the matter should be raised with the Regional Managing Director, Regional Finance leader and Corporate Finance Leaders for resolution. Every attempt should be made to reconcile these differences at the hotel level. The General Manager and Hotel Financial Controller should appeal to a higher authority only in exceptional circumstances. Regional Finance leader and Corporate Finance leader in conjunction with the Regional Managing Director: • Hotel Financial Controller appointments • All aspects of the Hotel Financial Controller’s compensation (initial salary and subsequent increases, and

bonuses)

Regional Managing Director, Regional Finance leader together with the General Manager will also approve: • All holidays and other absences from the hotel by the Hotel Financial Controller • The establishment of personal and business goals The General Manager and Regional Finance leader will conduct a performance evaluation of the Hotel Financial Controller at least once a year. The General Manager, in so far as is possible, will ensure that the duties detailed in the Hotel Financial Controller’s standards of performance are being fulfilled by the Hotel Financial Controller and will seek to ensure that deficiencies are addressed. Because Hotel Financial Controllers have the ultimate responsibility for compliance with the hotel finance policies, it is important that they fully understand all aspects of the Hotel Finance Policy and Procedure Manual and that the procedures implemented to achieve the objectives set out in the manual do not hinder the efficient operation of the hotel. Hotel Financial Controllers must take responsibility for communicating these procedures to the General Manager and Operations staff so that they also fully understand the implications of failing to comply with a particular policy or procedure.

Page | 15

Finance Policy and Procedure

Subject: Accounting Principles Department: Finance Reference # ADM 102 Page: 1/2 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 102 ACCOUNTING PRINCIPLES

Page | 16

POLICY U Hotels & Resorts reports its financial results in accordance with Generally Accepted Accounting Practice under International Financial Reporting Standards (IFRS) and financial reporting requirements of the local regulatory institutions. Results are must also complied with the reporting requirements for local statutory purposes and reported in functional currency. Generally Accepted Accounting Principles (GAAP) form the basis for the accounting principles, procedures, and practices used in summarizing, recording, and reporting the financial results of corporate operations. While there are differences in the various accounting procedures used from country to country, the basic underlying assumptions which support GAAP and form the basis of U Hotels & Resorts’ accounting standards, which are based on Generally Accepted Accounting Practice under International Financial Reporting Standards (IFRS). PROCEDURE These assumptions are as follows: 1. Objectivity Financial accounting statements must have a confirmable (objective) basis in fact. There must be a way to verify that financial transactions actually occurred before it can be recorded in the business’s financial records. 2. Understandability

Financial accounting statements are readily understandable by users. For this assumption, users are assumed to have a reasonable knowledge of business and economics activities and accounting and a willingness to study the information with the reasonable diligence.

3. Reliability In order for financial accounting statement’s to be reliable, they must free from material error and bias and can be depended upon by users to represent faithfully that which it either purports to represent or could reasonably be expected to represent.

4. Relevance Financial accounting statements must provide relevant information, which is responsive to the economic decisions of users by helping them evaluate past, present or future events of confirming, or correcting, their past evaluations.

5. Entity concept Financial accounting statements and records pertain to a specifically defined business entity separate and distinct from the owner or groups concerned with it. The entity concept directs that the account records should reflect only the activities of the business.

6. Going concern Financial accounting statements are normally prepared on the assumption that the business is a going concern and will continue in operation for the foreseeable future and that there is no intention to liquidate (sell) all of the assets of the business.

7. Unit of measurement The best common denominator in which diverse business transactions can be measured is money. Fluctuations in the value (purchasing power) of money can be ignored without any impairment of the usefulness or validity of the financial statements. The primary reporting currency is the functional currency of the hotel.

8. Matching concept Net income is best measured by a matching of costs against the revenues to which the costs have given rise. In this way, total resources used in operations are matched against total resources received from operations.

9. Accounting period The financial accounting process provides information about the economic activities of an enterprise for specified time periods that are shorter than the life of the enterprise. The shortest period is typically a month. The longest period is typically one year. U Hotels & Resorts uses fiscal months.

10. Revenue recognition Revenue should not be recognized until it has been earned and can be measure with a reasonable degree of reliability and objectivity. Revenues are effectively recognized when services have been substantially rendered taking into account with the stage of completion.

11. Historical cost

Page | 17

Assets are recorded at the fair value of the consideration given to acquire them at the time of their acquisition. Liabilities are recorded at the fair value of the consideration received in exchange for incurring the obligation at the time they were incurred. Replacement cost or current value accounting should not be used.

In addition to the basic underlying assumptions mentioned above, there are also several reporting standards that must be applied to the results obtained from accounting procedures. 1. Disclosure

Accounting reports should disclose fully and fairly the information they purport to represent. Full disclosure or completeness requires that any past or even future event which could material affect the financial standing of the business and that cannot be easily discerned from reading the business’s financial accounting statements must be separated reported. These reports, prepared in the form of footnotes, must be attached to the financial statements. The information given must not only be complete; it must be undisturbed by the value judgments or outlook of the person preparing it.

2. Comparability The conduct of comparative analyses between accounting periods constitutes one of the major characteristics assumed for the audience of financial accounting. Comparability calls for like events to be reported in the same manner. Comparability also requires that changes in accounting principles be restricted to situations where the new principle is clearly preferable to the old. When a change is made, its nature, effect and justification must be explained.

3. Consistency Closely allied to comparability is consistency. The entity must select and consistently report financial information under the rules of the specific system it elects. It is imperative that accounting policies/procedures be the same from period to period for the same accounting entity so that users will be able to gain a true understanding of its actual revenue and expense during a specific period.

Finally, two time-honored traditions – materiality and conservatism – may cause accounting practice to depart from the basic theory derived from the underlying assumptions and reporting standards. 1. Materiality

The concept of materiality states that any amount or transaction that has significant (material) effect on financial statements should be recorded and reported correctly. When the difference between the theoretical treatment of an item and a more practical treatment of it is immaterial in amount or importance, the item can be recorded in the practical manner.

2. Conservatism The tradition of conservatism is an outgrowth of the uncertain environment and the tentative measurements of accounting. Historically, conservatism has been viewed and sometimes applied as a rule requiring the understatement of assets and income. In modern accounting, it calls for caution and careful assessment of risks and uncertainties when making decision on what procedures and values to select in recording transactions.

Finance Policy and Procedure

Page | 18

Subject: Internal Controls Department: Finance Reference # ADM 103 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 103 INTERNAL CONTROLS POLICY Internal controls comprise the plan of organisation and all of the ordinate methods and measures adapted to: • Ensure the accuracy and reliability of accounting information and records keeping • Restrict unnecessary and potentially detrimental access to the assets of the business • Confirm, periodically, that those possible for safeguarding assets can account for them • Establish appropriate action steps for measuring and addressing variation between the expected and actual

performance.

Key controls listed below also act as an “aide memoir” to the hotel management who must ensure they have been considered each month.

PROCEDURE There are a variety approaches that can be used to view accounting information controls systems. The effective systems consist of: 1. Revenue cycle by means of income audit 2. Purchase cycle by means of authorisation of purchases and disbursements 3. Accounts receivable and collection of debts by means of credit control 4. Adequacy and security of inventory by means of inventory management 5. Adequacy of cash controls including electronic processing to ensure cash security and banking 6. Payroll controls by means of authorisation of employment and correct recording of hours and payroll records 7. Authorisation of documents, keeping of up-to-date and accurate books of account for management information,

audit and legal purposes

Both General Manager and Hotel Financial Controllers must take responsibility for developing, operating and monitoring the effectiveness of internal control and providing assurance to the corporate office that it done so. In addition to the regular review process, General Manager and Hotel Financial Controllers should: • Consider what are the significant risks and assess how they have been identified, evaluated and managed; • Assess the effectiveness of the related system of internal control in managing the significant risks, having regard,

in particular, to any significant failings or weakness the have been reported • Consider whether necessary actions are being taken promptly to remedy any significant failings or weakness; and • Consider whether the findings indicate a need for more extensive monitoring of the system of internal control.

Page | 19

Finance Policy and Procedure

Subject: Code of Ethics Department: Finance Reference # ADM 104 Page: 1/2 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 104 CODE OF ETHICS POLICY The following Code of Ethics must be utilized when representing or conducting business on U Hotels & Resorts’ behalf. Failure to abide by the Code of Ethics will result in disciplinary actions up to and including termination. PROCEDURE U Hotels & Resorts’ employees are required and expected, at all times, to act in accordance with the following code of ethics: 1. Use of Company Name

There is a value in the name and reputation of U Hotels & Resorts and all subsidiaries. All employees are expected to use the company name, and other company trade names and trademarks, only in approved activities.

2. Quality and Fairness The products and services that we deliver should never be less than that which is promised or expected by our customers.

3. Assets and Funds Any employee with responsibility for the use of the company’s physical assets or funds is accountable for their proper conduct as a fiduciary in relation to the use or protection of those assets.

4. Internal Financial Reporting Accounts and records will be maintained and financial reports will be prepared in a manner which conforms to the company’s policies and procedures.

5. Communications Reasonable measures must be taken to ensure the accuracy of information that is authorized for release to outside parties.

6. Selection of Suppliers No employee may select a supplier for any reason other than its ability to fulfill the company’s needs. No employee should accept any goods, services or other forms of compensation/favors from a supplier for less than market value. This provision is not intended to apply to routine, reasonable business entertainment.

7. Relationship to Suppliers No employee may own an interest in the business of a supplier of be a creditor of a supplier.

8. Use of Suppliers No employee may utilize a supplier, consultant, subcontractor or employee of U Hotels & Resorts to work on their personal residence(s) or those of related persons without prior written approval from their Superiors.

9. Improper Payments Kickbacks, gifts, fees, commissions or any form of “bribes” intended to induce or reward favorable decisions or governmental actions are unacceptable and prohibited. No employee may, in violation of any law, pay or offer to pay or give anything of value to a customer, governmental entity or political party, to induce or reward favorable action in any business transaction or governmental matter. This provision is not intended to apply to routine, reasonable business entertainment or gifts of U Hotels & Resorts value, customary in local business relationships, provided that no law or company policy is violated and full disclosure is made.

10. Outside Activities For all business relationships with outside individuals, companies or organizations, and for all personal undertakings, employees are expected to: a) act in accordance with the law; b) consider the rights, interests and responsibilities of the outside parties; c) protect their own reputation and the interests of the company against

Page | 20

actual or potential conflicting interest with outside parties and d) avoid personal transactions or situations in which their own interests conflict or might be construed to conflict with those of the company.

No employee may directly or indirectly buy, sell or lease any facility, service or equipment from or to the company, or use any such facility, service or equipment for personal benefit. Violations of this policy will result in disciplinary action, up to and including termination. If you are involved in any situations or transactions which conflict or may appear to conflict with the intent of this code of ethics, you must report it immediately to the Regional Managing Director, Regional Finance leader and Corporate Finance leader. Failure to promptly disclose involvement in any such activity may result in disciplinary actions, up to and including termination of employment with U Hotels & Resorts.

Page | 21

Finance Policy and Procedure

Subject: Critical Date List Department: Finance Reference # ADM 105 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 105 CRITICAL DATE LIST POLICY To ensure that all Critical Dates pertaining to reporting requirements and/or contractual obligations are addressed in a timely manner, the Hotel Financial Controller will maintain a listing of all critical dates pertaining to his/her hotel. Such a listing must be updated no less than quarterly. Copies of the Critical Date List must be provided to the Regional Finance Leader on a quarterly basis. PROCEDURE The Critical Date List should be formatted and contain, at a minimum, information concerning the following: 1. Taxes – account numbers, payee, amounts 2. Licenses and Permits – type, payee 3. Mortgages 4. Leases 5. Utilities 6. Insurance – list all types of insurance and coverage 7. Maintenance and Service Contracts 8. Other Agreements 9. Space Rental Information – tenants 10. Loan Agreements and/or Interest Payment, Capital Projects, when required 11. Credit Card Processing Information – account numbers, merchants, card types, phone numbers and discount

rates 12. Dues & Subscriptions – department, name, reason 13. U Hotels & Resorts – Contractual issues, fees, payments 14. Phone Systems – list of lines billed

Page | 22

Finance Policy and Procedure

Subject: Guest Safety Deposit Boxes Department: Finance Reference # ADM 106 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 106 GUEST SAFETY DEPOSIT BOXES POLICY New and existing hotels require assurance that all duplicate keys to the hotel safe deposit boxes have been destroyed to ensure each box has only two keys (control key and guest’s key). Periodic audits should be performed to ensure an adequate inventory of safe boxes and that no valuables have been mistakenly left by guests. PROCEDURE 1. Strict control should apply to the storage, issue and receipt of keys. 2. Only two keys (control key and guest’s key) per box should exist for each safe deposit box. The destruction of any

duplicates should be witnessed by the General Manager, and the record of the event maintained in the Financial Controller’s files.

3. Front Office management should perform on a surprise basis for monthly inventory of the available safe boxes, ensuring that either two keys or safe deposit record is available for each box. And, key for unused boxes should be kept in the Front office Cash drawer or some other locked place, not in the key holes.

4. The identity of the guests must be verified before access is granted and guests should be given privacy or a discreet distance when they are placing or removing articles from their box. And, two keys should be requiring to open any safe deposit boxes (control key and guest’s key).

5. After guests have returned for their belongings, the completed safe deposit box agreements and safe and safe deposit activity log should be forwarded to Accounting, for filing alphabetically, by month and by guest name. (Evidential records may be required in the event of a subsequent loss report, related to such valuables previously held by the hotel in safekeeping).

6. Any guest safe that must be “drilled” for any reason should be done so only with a minimum of three witnesses (one being the Front Office Manager, HOD, Financial Controller, or similar level). The contents of the safe box should be inventoried and receipted with the General Cashier for security in the house safe. The manager in charge of the inventory must make a complete written report to the General Manager for their further handling.

7. When guest(s) check-out, the Front Office Clerk should ensure safe deposit box keys are return. The guest concerned must sign on the reverse side of the Safe Deposit Box Record Card. This is the hotel’s release of liability.

Page | 23

8. In the event that a guest’s box has to be opened when the guest is not present, the Director of Rooms, Financial Controller and Security Manager must be present. A detailed list of contents must prepare in quadruplicate and each person present should sign each copy. The guest, or his authorized representative, will receive the original, and one copy will be retained by each of three signatories.

9. The Front Office Clerk should under no circumstances accept possession of the guest’s safe deposit key, unless the box is being surrounded. If a key is delivered to the Front Office Clerk as having been found somewhere on the premises, or if received by mail, it should immediately be sealed under dual control and the guest notified to call for his/her key.

Finance Policy and Procedure

Subject: Master Keys Department: Finance Reference # ADM 107 Page: 1/7 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 107 MASTER KEYS POLICY To ensure guests are provided with maximum security and safety, any property keys are to be issued to the authorized persons only and with proper written authorization. Missing/lost/misplaced room or service keys are to be reported immediately for action. The Financial Controller in conjunction with the General Manager has the responsibilities and control of the property master keys and service keys. PROCEDURE 1. Allocation and Control

At the opening of the hotel, all keys should be normally divided into three levels as follows; Emergency Master Key

• Open all guest room doors, even they are double locked. • It can be used to enter a room when the guest need aids and is unable to reach or open the door.

Master Key

• Open all guest room doors that are not double locked. • May be further established as a section master, floor master, or grand master. • It can be used by housekeeping supervisor who is providing a quality check on service.

Guestroom Key

• Open a single guest room door that is not double locked.

Page | 24

All of above, the Financial Controller must obtain from the supplier of the locks a full list of all master keys and service keys as ordered by the hotel. Based on these documents, a physical control of all master keys is performed by the Financial Controller in the presence of General Manager, Resident Manager, Executive Housekeeper and Loss Prevention (or at least two of these four persons) and records the identification of each key in an “Allocation Inventory and Control Register”. This Register must contain One (1) page to be used for each master key with the indication of the type of key (GMK, EMK, etc.) the reference shown on the key and the various premises for which the key is usable. Thereafter, each key is put in a sealed envelope, signed by both General Manager and Financial Controller and locked in the Financial Controller safe. Any allocation of master keys must be authorized in writing by the General Manager and this is done through the standard form “Authorization of Master Keys Allocation”. This form is completed in two copies and then transmitted to the Financial Controller. When the Financial Controller receives these two copies, he/she makes sure that the receiver of the master key has duly countersigned the form after handwriting “read, signed and accepted”. The allocation is recorded in the inventory register on the page reserved for the master key concerned and countersigned by Loss Prevention and the Receiver. Finally, the master key concerned is handed over. One of the two copies of the “Authorization of Master Keys Allocation” is transferred to Human Resources for filing in the personal file of the receiver. The following responsibilities apply; General Manager – authorization for allocation of Master Keys Financial Controller – maintenance of the master key register and holder of spare keys Loss Prevention – management, circulation and control of issued master keys

At least four times per year, the Financial Controller must make a physical inventory of all circulating master keys. For this purpose, the form “Inventory of Circulating Master Keys” is to be used. This periodical physical inventory does not exclude surprise counts which must also be taken into consideration. When a master key holder goes on vacation or is away from the property for more than 3 days, he/she must return the key (keys) which he/she has received back to the Financial Controller. Any transfer of master keys to a successor or an assistant must go through the inventory register and generate a return and then a new allocation with the required authorization by the General Manager may be issued. When a master key holder leaves his job, Human Resources must mention the surrender of the key during the exit interview. The Financial Controller must personally recover the master key before settling the final pay. When there is a new Financial Controller, the handover of the master key must be made in the presence of General Manager who countersigns the inventory register together with the new Financial Controller. 2. Replacement

Broken or worn-out master keys

A new master key cannot be cut unless the broken or worn–out key is surrendered. The replacement of broken or worn-out master keys is carried out by the Financial Controller. The Financial Controller must keep in its safe all master key blanks needed for replacement.

Page | 25

The Financial Controller follows the same procedure as for the cutting of normal keys (authorization by General Manager, recorded on a special page of the inventory register for key blanks and opening of a new page for the newly cut key). Lost, Missing or misplaced master keys

It is strictly forbidden to replace a lost (EMK, GMK, RMK) master key. All losses, missing or misplaced keys must be reported immediately to Loss Prevention for investigation. Loss Prevention must sure the General Manager and Financial Controller has been immediately informed. Instructions are issued for the necessary actions to be taken (special security safeguard, police enquiry, change of locks, combinations, etc….). In case of juridical or insurance coverage on the file treatment, the Financial Controller must contact Corporate Office. Lost, missing or misplaced Guestroom Keys (RMK) represent a risk to guests occupying the room, accordingly the lock must be changed to a new master from the blanks kept with Financial Controller.

3. Utilization

Emergency Master Key (EMK)

There should be a minimum of 3 Emergency Master Keys; EMK 1 – retained by Loss Prevention in a secured locked box in a 24-hour manned area. EMK 2 – retained by Front Office Manager in a safe deposit box EMK 3 – retained by Financial Controller in the FC safe The emergency key is put in an envelope by the Financial Controller in the presence of General Manager and deposited with Loss Prevention, Front Office and Financial Controller. The envelope is sealed and countersigned by the three persons, time stamped, and identified by EMK number. A control book is opened at both Loss Prevention and the Front Office Duty Manager’s desk exclusively for the control and follow–up of this key. Each Loss Prevention and F.O. Duty Manager must countersign the control book at the beginning of his/her shift in order to certify the physical presence of the emergency key envelope. The utilization of this key is to be recorded on the control book. The General Manager establishes a list of people authorized to use this key. This list is attached to the control book. Two persons are always required for the issuing of the key and must sign jointly in order to obtain the key. After use, a new envelope is prepared in the same manner and countersigned by the two persons. A sequence number following the one shown on the previous envelope is entered on the new envelope. All used envelopes are transferred monthly to the General Cashier who files them in numerical order for one year. Grand Master Key (GMK)

Only one grand master key is in circulation at any time and will be held by Loss Prevention. The grand master key in circulation is to be joined to a welded wire ring of a 30cm diameter is permanently retained by Loss Prevention in a secured locked box in a 24-hour manned area. This key must be identified by a docket marked “GRAND MASTER. The movement of this key is controlled by records in the grand master key control book. The use of this key requires the signature of two persons (The General Manager establishes a list of authorized personnel to obtain the use of the key, and a copy of this list is attached to the control book). Section Master Key (SMK)

Page | 26

These keys are those used to have access to a particular section of the hotel (e.g., One Guest Room floor) and are allocated by instruction of the General Manager to the various Department Heads. The allocation and control procedure are the same as the one defined in the section “Allocation”. These keys are allocated to the Department Heads or Supervisors concerned in accordance with the procedure of master keys allocation. The Department Heads concerned must establish a control book for each key allocated. Each master key holder must establish a control book for any sub-delegation that they have initiated. Each Department Head has the responsibility to control regularly (at least on a monthly basis) the physical presence of the master keys allocated to him or the department. The control of these master keys can equally be carried out by the General Manager or Financial Controller or any other persons who are qualified to carry out such a control. Guestroom Key (RMK)

These keys are those used to have access to a specific guest room in the hotel. Only two guestroom keys are to in circulation at any time and will be held by Front Office. The use of this key is restricted to the registered guests of the specific room. All losses, missing or misplaced keys must be reported immediately to Loss Prevention for investigation in accordance with the replacement policy above. Service area keys These keys are used to have access to service areas such as laundry, storerooms, offices, etc… Outside duty hours, these keys are kept at the Loss Prevention 24-hour manned area where responsibility to control the movement of each key is exercised by using the control book. Any use of keys, by persons other than those responsible of the given area, must obtain two signatures of which the General Manager will name these persons are authorized to obtain such keys outside normal working hours. A list of these names is attached to each control book. The access to locked areas, when the employees responsible for such areas are not present, must have an exceptional justification. Circulation of keys

All keys will be retained and secured with Loss Prevention in a 24-hour manned area. All keys will be signed out and signed in daily. Loss Prevention will check and record all keys not returned at the appointed time. Any key issued to an individual is their personal responsibility and is NOT to be loaned or passed between associates. Master Keys must never leave the property and will be audited daily by Loss Prevention. All key blanks will be retained by the Financial Controller.

Page | 27

All Master Keys must be carried only by the authorized person while on property and are not to be left unattended. 4. Electronic Locks

In general, the principles of allocation and control are identical to those described above. However, if the system used implies the set-up of different procedures, copies of such procedures must be sent to Regional Managing Director and Regional Finance leader for approval.

Authorization of Master Keys Allocation

TO: DATE:

FROM:

SUBJECT : Authorization for master key allocation

1. Mr. (or Ms) Position: Here under

named “Holder” is authorized to receive after signing a master key type for access to

the following areas:

Page | 28

2. The holder undertakes to use the master key allocated to him exclusively for working purposes and to return it to

the Hotel Financial Controller immediately when and if so requested.

3. In case of loss of the master key allocated to him, the holder must immediately report it to the Financial

Controller by establishing a report pointing out the circumstances of the loss.

4. The use of this master key strictly reserved for working purposes. Any fraudulent use and its loss will constitute

serious offenses which will be subsequently penalized.

5. The master key will never be taken out of the working site.

6. The holder recognizes of having been informed of the responsibility which falls on him and of the limits in the

use of the master key allocated to him.

THE HOLDER THE GENERAL MANAGER

Write: read, agreed and accepted” before signing

RECEIPT RESTITUTION

Mr/Mrs/Ms: Master key

Recognizes having Allocated to:

Received Master key No: On:

Signature of Holder: Signature of Financial Controller:

Page | 29

ALLOCATION INVENTORY AND CONTROL REGISTER

(One Page per key/card) TYPE OF KEY (EMK, GMK, SMK, RMK)

FOR ACCESS TO AREAS :

KEY REFERENCE

ISSUED TO & RECEIVED BY RETURNED TO

DATE NAME POSITION SIGNATURE INITIALS-FC DATE NAME POSITION SIGNATURE INITIALS-FC

Page | 30

INVENTORY OF CIRCULATING MASTER KEYS Date:

LIST OF ALL

MASTER KEYS REF. NO HOLDER PRESENT (including all blanks) Yes/No Details of any missing key/variances: Signed: Financial Controller Signed: General Manager

Page | 31

Finance Policy and Procedure

Subject: Mobile Phone and Pager Control Department: Finance Reference # ADM 108 Page: 1/3 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 108 MOBILE PHONE AND PAGER CONTROL POLICY U Hotels & Resorts is committed to providing consistent communication between departments of a hotel and therefore provides mobile phones, radios and pagers to key individuals designated by the General Manager. It is the Financial Controller’s responsibility to ensure that a control mechanism is in place to account for all of these phones, radios and pagers at all times. The General Manager will designate the department responsible for the issuance and return. PROCEDURE 1. The General Manager and the Financial Controller will evaluate the need for purchasing mobile phones,

radios and pagers for the hotel. 2. The General Manager will designate the department that will handle the issuance and return of these phones,

radios and pagers. 3. A Master Mobile Phone, Radio & Pager Control Log must be initiated and maintained by the Financial

Controller listing the unit number, serial number, make and model of each. This information will be noted on an Issuance & Control Log. All units must have a separate log.

4. Before a unit is issued out, the name of the individual requesting a unit must be verified against the designated list of individuals authorized for issuance. The requesting individual must sign his/her name in the log noting his/her department, the date of issue, the time, and the expected date of return. The issuing individual will then transfer this log from the “available” section to the “in use” section of the binder.

5. Upon return of a unit, the individual returning the unit must sign off on the log and the return must be acknowledged by the receiving individual. The specific log for the unit is then transferred from the “in use” to the “available” section of the binder.

6. It is the responsibility of the designated issuing department to ensure all units are accounted for on a daily basis. If a unit is considered “missing” of unaccounted for, the immediate supervisor must be notified immediately and the unit tracked, based on the Issuance and Control Log.

7. If a unit cannot be located, a missing property report is prepared, describing the steps taken to recover the unit and signed by both the individual who discovered the loss and the immediate supervisor. A copy of the report is given to the Financial Controller.

8. Periodically, the Financial Controller must perform an audit of the units to ensure controls are in place and the total inventories are accounted for.

9. If a unit is damaged, malfunctions or inoperable, the information is noted on the specific unit log and a copy must be attached to a purchase order to replace the unit and forwarded to the Financial Controller and General Manager for approval.

10. Expenditure authority for charges of this equipment is covered in the expense policy.

Page | 32

ALLOCATION MOBILE PHONE AND PAGER CONTROL REGISTER

(One Page per mobile phone/pager)

TYPE :

RESPONIBLE BY :

UNIT NO. :

SERIAL NO. :

MODEL :

RECEIVED AND ISSUED BY RETURNED AND RECEIVED BY

DATE NAME POSITION DEPT SIGNATURE RECEIVED

SIGNATURE ISSUED

DATE NAME POSITION DEPT SIGNATURE RETURNED

SIGNATURE RECEIVED

Page | 33

INVENTORY OF CIRCULATING MOBILE PHONE AND PAGER CONTROL REGISTER Date:

LIST OF ALL MOBILE PHONE &

PAGER REF. NO HOLDER PRESENT (including all blanks) Yes/No Details of any missing mobile phone and pager /variances: Signed: Financial Controller Signed: General Manager

Page | 34

Finance Policy and Procedure

Subject: Licenses and Permits Department: Finance Reference # ADM 109 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 109 LICENSE AND PERMITS POLICY U Hotels & Resorts will operate within all local and country required permits. It is the Financial Controller’s responsibility to be certain these permits are maintained and renewed on a timely basis. PROCEDURE 1. The Financial Controller must be aware of the proper legal entity in whose name permits are to be obtained and

maintained, as well as knowledge of the appropriate signatories for these entities. 2. License and permit expiration dates need to be monitored in accordance with the Critical Date List. 3. Most jurisdictions require licenses and permits to be displayed in a certain place or manner. The Financial

Controller must be aware of these rules and ensure the hotel is in compliance. 4. Original licenses and permits are to be maintained in a binder in the Financial Controller’s office. Copies of

licenses and permits are to be used for display where applicable. Wherever the law requires that originals must be displayed, the Financial Controller must maintain a copy the binder, along with a notation of where the original document is posted.

Page | 35

Page | 36

Finance Policy and Procedure

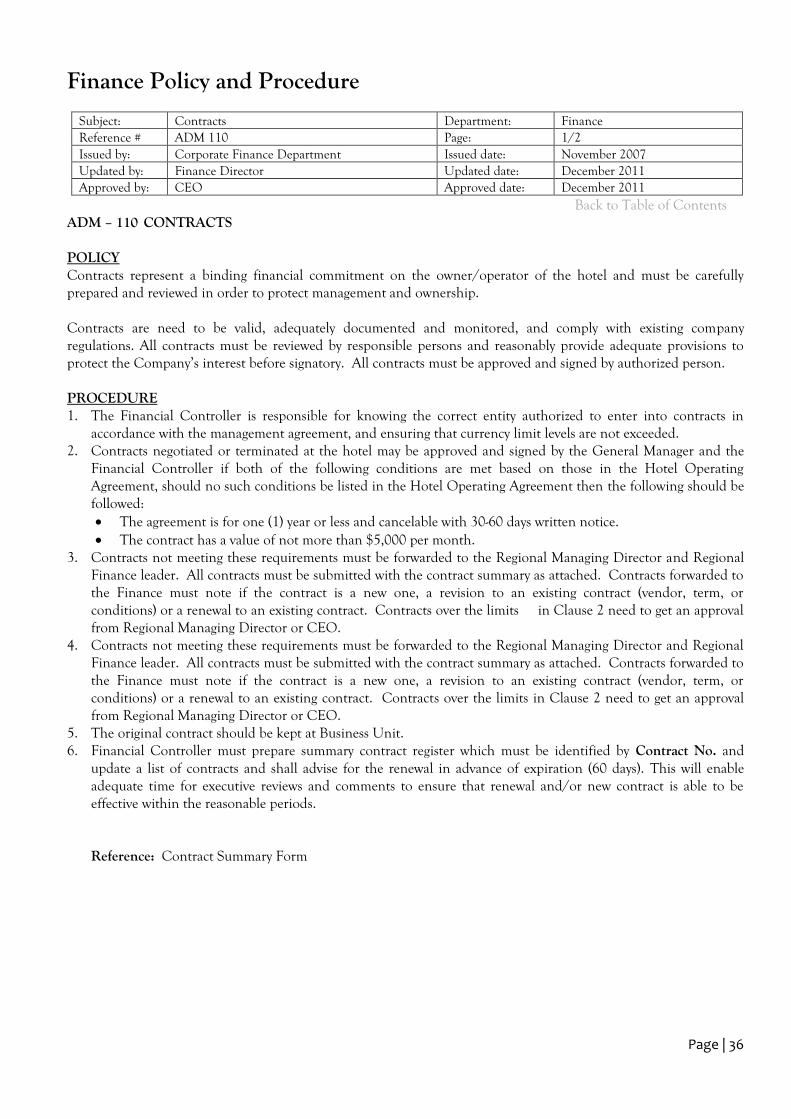

Subject: Contracts Department: Finance Reference # ADM 110 Page: 1/2 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 110 CONTRACTS POLICY Contracts represent a binding financial commitment on the owner/operator of the hotel and must be carefully prepared and reviewed in order to protect management and ownership. Contracts are need to be valid, adequately documented and monitored, and comply with existing company regulations. All contracts must be reviewed by responsible persons and reasonably provide adequate provisions to protect the Company’s interest before signatory. All contracts must be approved and signed by authorized person. PROCEDURE 1. The Financial Controller is responsible for knowing the correct entity authorized to enter into contracts in

accordance with the management agreement, and ensuring that currency limit levels are not exceeded. 2. Contracts negotiated or terminated at the hotel may be approved and signed by the General Manager and the

Financial Controller if both of the following conditions are met based on those in the Hotel Operating Agreement, should no such conditions be listed in the Hotel Operating Agreement then the following should be followed: • The agreement is for one (1) year or less and cancelable with 30-60 days written notice. • The contract has a value of not more than $5,000 per month.

3. Contracts not meeting these requirements must be forwarded to the Regional Managing Director and Regional Finance leader. All contracts must be submitted with the contract summary as attached. Contracts forwarded to the Finance must note if the contract is a new one, a revision to an existing contract (vendor, term, or conditions) or a renewal to an existing contract. Contracts over the limits in Clause 2 need to get an approval from Regional Managing Director or CEO.

4. Contracts not meeting these requirements must be forwarded to the Regional Managing Director and Regional Finance leader. All contracts must be submitted with the contract summary as attached. Contracts forwarded to the Finance must note if the contract is a new one, a revision to an existing contract (vendor, term, or conditions) or a renewal to an existing contract. Contracts over the limits in Clause 2 need to get an approval from Regional Managing Director or CEO.

5. The original contract should be kept at Business Unit. 6. Financial Controller must prepare summary contract register which must be identified by Contract No. and

update a list of contracts and shall advise for the renewal in advance of expiration (60 days). This will enable adequate time for executive reviews and comments to ensure that renewal and/or new contract is able to be effective within the reasonable periods. Reference: Contract Summary Form

Page | 37

U HOTELS & RESORTS

CONTRACT INTELLIGENCE MEMORANDAM

CONTRACT NO.:

HOTEL:

DATE:

CONTRACT: New Revision: Renewal:

Contractor Name: Self-explanatory. Contractor Address: Self-explanatory. Contractor Contact/Phone Number: State the name, title and phone number of principal contacts. Service: State the type of services provided (i.e. cable TV service, in-house

movies, valet parking, etc.).

Effective Date: Self-explanatory.

Expiration Date: Self-explanatory.

Renewal Provision: State the terms upon which the contract is renewable.

Termination Provision: State whether the contract can be terminated with thirty (30) days’ notice and without penalty, etc.

Contract Amount: State the payment amount.

Payment Terms: State the payment frequency (monthly, quarterly, etc.)

Budget Variance: State whether the contract is included in the budget and in accordance

with the annual plan. Describe any variances.

U Hotels & Resorts Property Approval: Signature, name, and title of U Hotels & Resorts personnel submitting the contract.

U Hotels & Resorts Corporate Approval: Signature, name, and title of U Hotels & Resorts Corporate

personnel approving the contract.

Page | 38

Finance Policy and Procedure

Subject: Litigation and Other Contingencies Department: Finance Reference # ADM 111 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011

Back to Table of Contents ADM – 111 LITIGATION AND OTHER CONTINGENCIES POLICY All lawsuits should be coordinated with the assistance of the regional/corporate office as well as the property owners in accordance with the Hotel Operating Agreement. PROCEDURE The Financial Controller or General Manager is responsible for immediately notifying the regional/corporate offices, and owning company of any claim against the hotel. Any such correspondences should be copied to the Regional Managing Director. Regional Finance leader will determine the need to inform both Chief Executive Officer and Corporate Finance leader. Any correspondence or notification relating to U Hotels & Resorts employment matters should be directed to Corporate Human Resources. Such notification will include. 1. Any communication from an attorney or legal counsel indicating there is a claim on or against the hotel,

including any insurance-related claims. 2. Incidents within the property that may give rise to future claims, such as:

• Serious injuries to guest or employee • Sizeable thefts or damage to guest or employee • Arrest of guest or employee on the premises upon request of the property • Substantial failure of equipment that may seriously affect the operations of the property, etc.

3. Receipt of any documents from any Court of Law or from any state or local agency or local agency or commission, to include but not limited to the following: direct subpoena to property (not to employees) and bankruptcy notices (not employee garnishment). Such documents should be received by the General Manager or Financial Controller.

4. The property must update Corporate monthly with any information relating to outstanding litigations.

Page | 39

Finance Policy and Procedure

Subject: Hotel Operating Agreement Administration Department: Finance Reference # ADM 112 Page: 1/1 Issued by: Corporate Finance Department Issued date: November 2007 Updated by: Finance Director Updated date: December 2011 Approved by: CEO Approved date: December 2011