Turning a new page - Straumann...4 1Market growth data based on total business for Straumann, Nobel...

36

Turning a new page Vontobel Summer Conference, 11 June 2014 Thomas Dressendörfer, CFO

Transcript of Turning a new page - Straumann...4 1Market growth data based on total business for Straumann, Nobel...

Turning a new pageVontobel Summer Conference, 11 June 2014

Thomas Dressendörfer, CFO

2

This presentation contains certain forward-looking statements that reflect the current views of management. Such statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Straumann Group to differ materially from those expressed or implied in this presentation. Straumann is providing the information in this presentation as of this date and does not undertake any obligation to update any statements contained in it as a result of new information, future events or otherwise.

The availability and indications/claims of the products illustrated and mentioned in this presentation may vary according to country.

Disclaimer

Regional and business review

4

1Market growth data based on total business for Straumann, Nobel Biocare, Zimmer Dental/Biomet 3i (pro-forma), Dentsply Implants –based on company and SEC reports as well as management comments. 2Market share data based on MRG and iData for the respective global implant and abutment sales (i.e. excl. CADCAM sales) in 2013.

Steady outperformance except for time ofrestructuring

Nobel Biocare

17%

Dentsply Implants

13%Zimmer / Biomet 3i

12%

Others 39%

Global market for dental implants/ abutments (2013: CHF 3bn 2013)2

Straumann 19%

1

5.2%4.1% 8.3% 28.6%

Change in l.c.

5

Good growth in Q1 across all regions; Europe contributes >40% to growth

(3.1%)

2013 2014

6.0% in l.c.

In CHF million

2.9% in CHF

174.8

‐5.2

169.6

4.12.2 1.7

2.2

179.8

Revenues Q12013

FX Effect Revenues Q12013 @ FX

2014

Europe North America APAC ROW Revenues Q12014

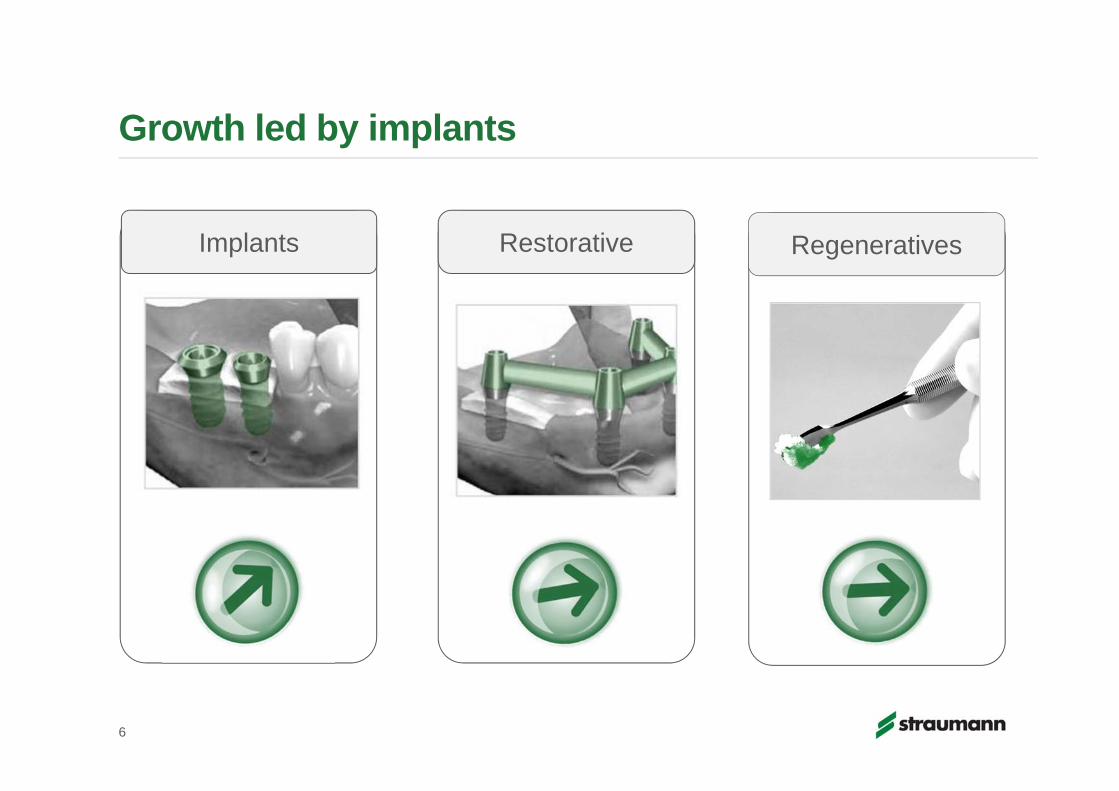

Implants

Growth led by implants

Restorative Regeneratives

6

7

Leading academic event in oral implantology

~4200 participants

Straumann Corporate Forum attendedby >2000 dental professionals

Special promotions offered

Highly successful ITI World Symposium –platform to promote new research and solutions

8

A new attractive pricing concept in Europe

8

‘More value, same price’ campaign

Roxolid® established as standard material Upgrade to Roxolid® SLA ® and SLActive®

implants with LOXIM™ transfer piece at same price as titanium equivalents with old transfer piece

Pricing structure adjusted in German-speaking countries on 01/01/14; pricing of ‘entry-level’ titanium SLA implant reduced to compete more effectively against value players (only in limited portfolio available)

Ti SLA

Ceramic

Ti SLA

Ti SLA

RoxolidSLA

RoxolidSLActive

2013 2014

RoxolidSLActive

TiSLActive

Good strategic progress

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

To source differentiated treatment components from single supplier is a differentiating factor

Prosthetics decision maker becoming more and more driver for implant choice

10

Pressure to adapt to new market realities

Source: iData Research, US data, 2012

2008

2014Implant specialistsGPs placing implantsGPs restoring implants

60 600

87 400GPs restorebut don’t place implants

15 900

29 700GPs place implants

GPs are increasingly important and have different preferences

11

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

To source differentiated treatment components from single supplier is a differentiating factor

Prosthetics decision maker becoming more and more driver for implant choice

12

Pressure to adapt to new market realities

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

To source differentiated treatment components from single supplier is a differentiating factor

Prosthetics decision maker becoming more and more driver for implant choice

13

Pressure to adapt to new market realities

14

Expanding our offering into the valuesegment through a multi-brand strategy

14Straumann has invested in convertible bonds of Biodenta and Megagen with an option to obtain a majority stake in the coming years..

2012: 49% equity stakeBrazilian leader in implant dentistry

2013: 51% equity stake German leader for cost‐

effective standard prosthetics

2014: Convertible bond

2013: 30% equity stake High‐end prosthetic solutions

2011: 44% equity stakeDigital CADCAM and

guided surgery solutions

2014: Convertible bond

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

To source differentiated treatment components from single supplier is a differentiating factor

Prosthetics decision maker becoming more and more driver for implant choice

15

Pressure to adapt to new market realities

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

Dentist prefer to source differentiated treatmentcomponents from single supplier

Prosthetic decision maker are increasingly influencing the choice of the implant system

16

Pressure to adapt to new market realities

Exclusive rights for Straumann to distribute botiss products in most Western/Central European countries and the Americas

Botiss to distribute Emdogain® in Germany, parts of Eastern Europe and Middle East

Leading position for dental bone & tissue regeneration in Europe; growing globally

Extensive range of proven biologic materials

Straumann to start selling in Europe in Q4; other regions to follow in 2016/17, pendingclearances

17

Combining strengths with botiss to provide complete regenerative solutions worldwide

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

Dentist prefer to source differentiated treatmentcomponents from single supplier

Prosthetic decision maker are increasingly influencing the choice of the implant system

18

Pressure to adapt to new market realities

Further streamlined prosthetic solutions and broader range of product combinations

New X-STREAM functionality in CARES Visual

Designing elements from one single scan

Milled in controlled environment for excellent fit and consistent quality

Turnaround time & shipping costs significantly reduced

Supports highly flexible Variobase™ with original connection for multiple CADCAM systems

Straumann CARES Visual 8.8 system

19

20

New prosthetic components for fixed full-arch restorations launched at ITI congress

Enhanced screw-retained prosthetic solution especially for edentulous patients

New range of screw-retained implant abutments offering increased flexibility

Low profile, different gingiva heights

0°, 17° and 30° angulations for challenging situations where the posterior implant has to be tilted

Very positive reactions in pre-market tests

The “Swiss made” has affected our financials...

0.6

0.8

1

1.2

1.4

1.6

1.8

2008 2009 2010 2011 2012 2013

USDCHF EURCHF JPYCHF

Sales

Costs

21

...but we made a first step towards our goal ofrestoring historic l.c. margins in 2013Underlying EBIT margin

15-20%

2008 2012 2013

14.5% 10-15%

18.2%

27.4%

Straumann Dental benchmark1

1 Peers comprise Nobel Biocare, Dentsply, Patterson, Henry Schein, Osstem, and Sirona.

10%

15%

20%

25%

22

20.7%@ 2013 FX rates

10-15%

2014 outlook helped by an exciting roll-out program

First clinically validated ceramic implant to reach market1

Made of zirconium-dioxide ceramic

ZLA™ surface comparable to SLA®, designed to offer a structure for cell attachment

Natural translucent ivory color

Monotype design, two abutment heights – more to follow

High reliability through innovative manufacturing and individual testing

241 Seven-year development program backed by seven pre-clinical studies and an extensive clinical study program; 98% survival rate at one year with zero fractures

Straumann PURE Ceramic Implantfor esthetic, metal-free solutions

25

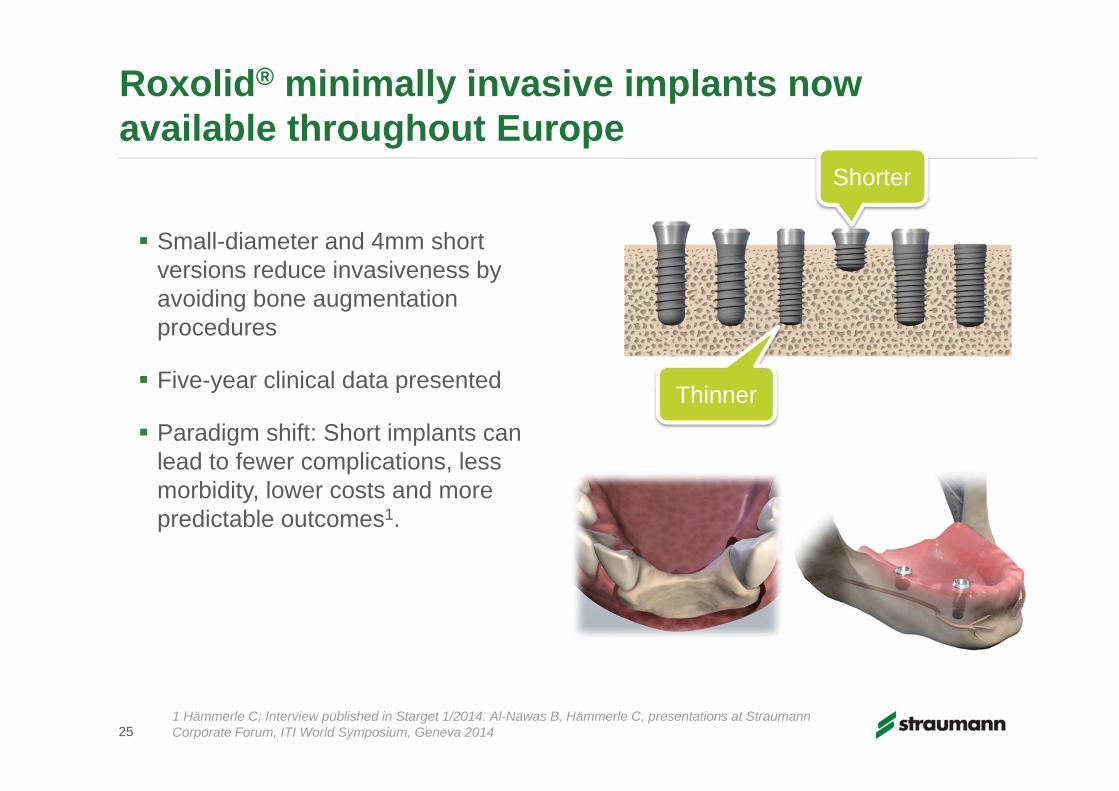

Small-diameter and 4mm short versions reduce invasiveness by avoiding bone augmentation procedures

Five-year clinical data presented

Paradigm shift: Short implants can lead to fewer complications, less morbidity, lower costs and more predictable outcomes1.

1 Hämmerle C; Interview published in Starget 1/2014. Al-Nawas B, Hämmerle C, presentations at StraumannCorporate Forum, ITI World Symposium, Geneva 2014

Roxolid® minimally invasive implants now available throughout Europe

Shorter

Thinner

New

SR

ab

utm

ents

Value-adding solutions to meet clinician and patient needs

26 Bubble sizes illustrate market volume potential

Single tooth Multiple tooth Edentulous

Ceramic implants

Standard implant solution

packages

Simpleedentulous solutions

Fixed immediate edentulous solutions

Smaller, less invasive implants

Implants for narrow spaces

Esthetic, fast implant solutions with single crown / small bridge

Low

High

Cost-effective, open platform restoration

Leve

l of s

ophi

stic

atio

n

Stra

uman

n O

NE

Cer

amic

im

plan

t

Rox

olid

Stra

uman

n Va

rioba

se

27

We expect the global implant market to develop positively in 2014 and our revenue to grow in the low-single-digit range (l.c.).

After a promising Q1, we expect a softer Q2 given the later Easter break this year.

We will continue to invest in dental growth markets and to extend the reach of our non-premium offering.

Despite this, and thanks to the full impact of our cost-reduction measures last year, we expect to further expand operating income margin in 2014.

In the mid-term, we aim to return to solid growth with further operating margin improvements.

Outlook for 2014 unchanged Barring unforeseen circumstances

27

While US and Japan are improving, the European economy may remain fragile for some time

Unemployment rate Private consumption

Source: NZZ newspaper April 201428

We aim to bring our Ebit margin back to 20%+Underlying EBIT margin

15-20%

2008 2012 2013 2014/15

14.5% 10-15%

18.2%

>20%

27.4%

Straumann Dental benchmark1

1 Peers comprise Nobel Biocare, Dentsply, Patterson, Henry Schein, Osstem, and Sirona.

10%

15%

20%

25%

29

10-15%

20.7%@ 2013 FX rates

10-15%

30

Questions & Answers

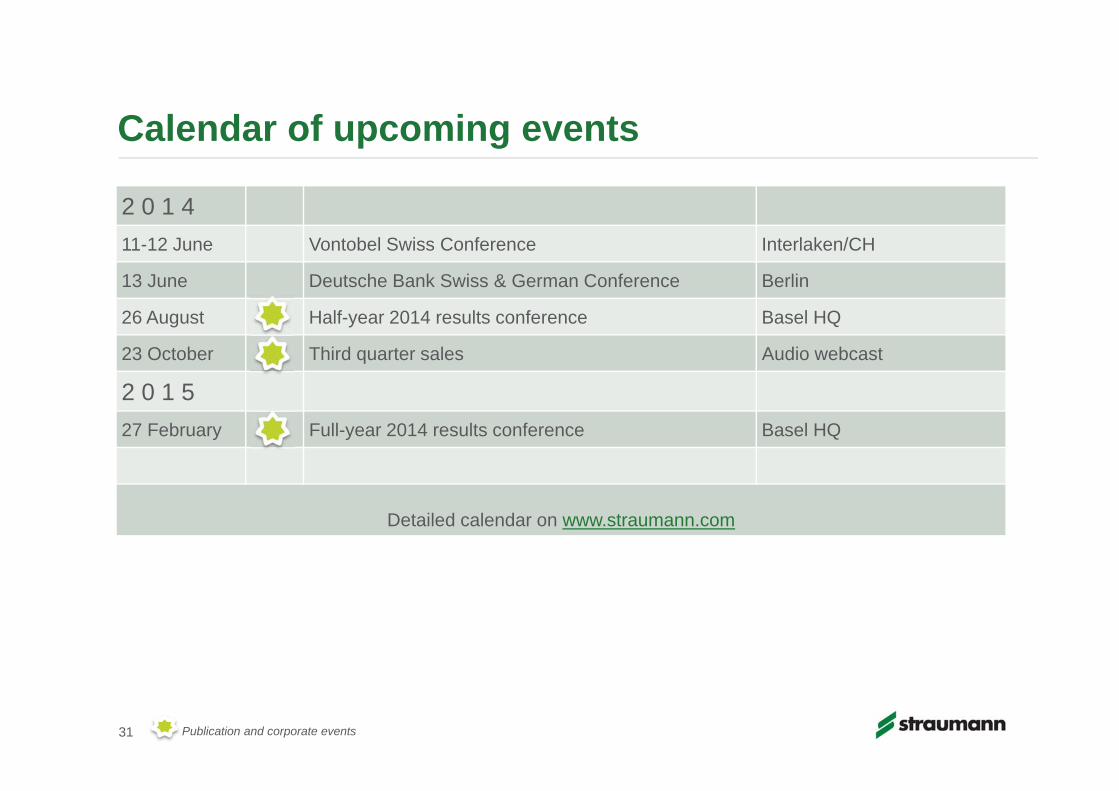

Calendar of upcoming events

2 0 1 4 11-12 June Vontobel Swiss Conference Interlaken/CH

13 June Deutsche Bank Swiss & German Conference Berlin

26 August Half-year 2014 results conference Basel HQ

23 October Third quarter sales Audio webcast

2 0 1 5 27 February Full-year 2014 results conference Basel HQ

Detailed calendar on www.straumann.com

3131 Publication and corporate events

Your IR contacts

Fabian HildbrandCorporate Investor RelationsTel. +41 (0)61 965 13 27Email [email protected]

Rahel SchafrothInvestor Relations CoordinatorTel. +41 (0)61 965 16 78Email [email protected]

32

33

Straumann’s currency exposure

Cost breakdown 20131

Revenue breakdown 2013

1 These distribution charts represent the total net revenues and the total COGS as well as OPEX expenses in the various currencies. All numbers are rounded and based on 2013 figures.

Average exchange rates (rounded) FX sensitivity (+/- 10%) on...

FY 2013 YTD 2014 Revenue EBIT

EURCHF 1.23 1.22 +/- 25 million +/- 15 million

USDCHF 0.93 0.90 +/- 17 million +/- 7 million

JPYCHF 0.95 0.87 +/- 4 million +/- 2 million

Development of Straumann’s main exchange rates since 2012

33

EUR 40%

CHF 12%

USD / CAD / AUD 28%

Other 20%

EUR 21%

CHF 45%

USD / CAD /

AUD 22%

Other 12%

60

80

100

120

2012 2013 2014

USDCHF EURCHF JPYCHF

Organization adapted to match market development

2 201 2 170

2 3612 452

2 517

2 217

2008 2009 2010 2011 2012 2013

Global workforce (year-end)

34

Headcount reduced by 300 to pre-economic crisis level

Overall restructuring/downsizing costs in 2013 amount to a net CHF 8m1

An incremental CHF 10 million savings in 2014 expected

Strong, engaged team of professionals retained

New organizational set-up focuses more on customer needs

Cost optimization

measures implemented

1 Including severance packages and curtailed pension obligations

35

Founded in 2002, MegaGen is one of Korea’s fastest-growing dental implant companies

Straumann purchases 3%-interest-bearing convertible bonds for a total of CHF 27 million

Capital injection will accelerate MegaGen’s expansion plans

Option to convert bonds into shares in 2016 and to obtain a majority stake in MegaGen

Foothold in the value segment of the Asia/Pacific region

Investment in MegaGen to drive expansion in value implant segment in Asia

A combination to eclipse the market leader

36 *US only

Straumann botiss GeistlichBone allografts *Bone xenograftsBone synthetic graftsBone blocksCustom bone blocksBone ringsCollagen conesFleeces & spongesMembranesSoft-tissue graftsBiologics