TURKEY’S MACHINERY INDUSTRY - ilker topal · development of the textile industry gave rise to a...

13

1 Szent Istvan University Faculty of Mechanical Engineering TURKEY’S MACHINERY INDUSTRY A General Outlook A.İLKER TOPAL January 2011

Transcript of TURKEY’S MACHINERY INDUSTRY - ilker topal · development of the textile industry gave rise to a...

1

Szent Istvan University

Faculty of Mechanical Engineering

TURKEY’S MACHINERY INDUSTRY

A General Outlook

A.İLKER TOPAL

January 2011

2

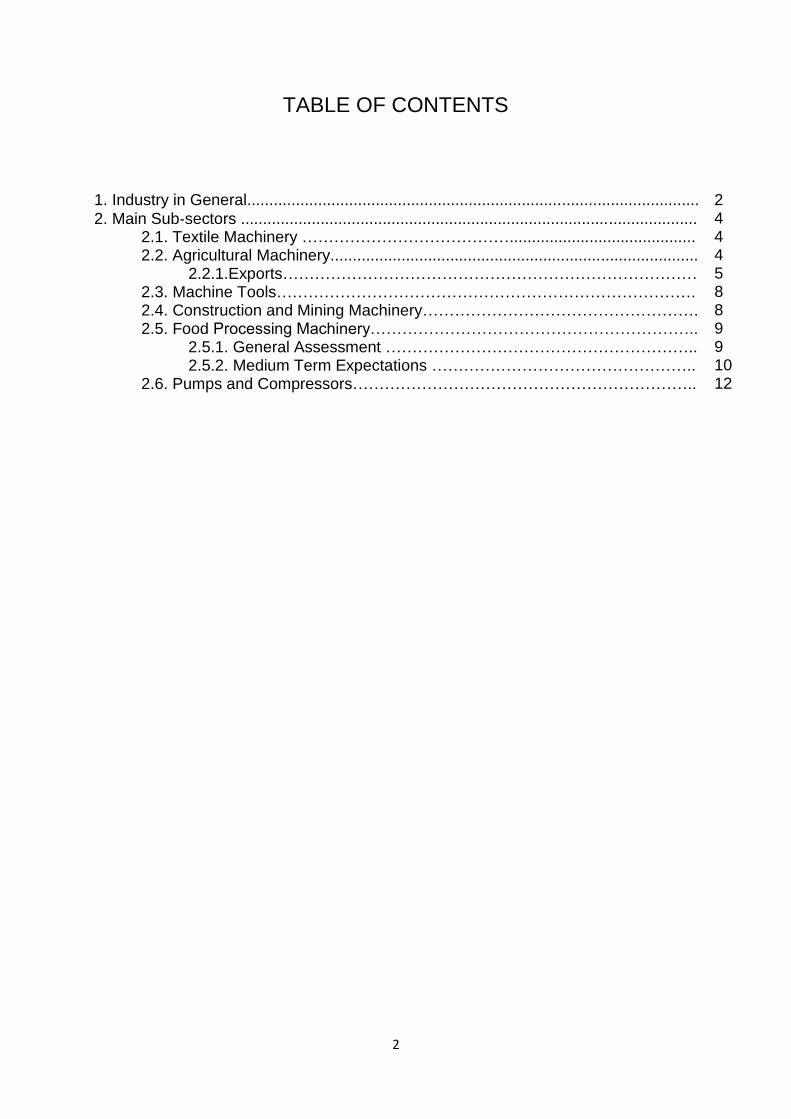

TABLE OF CONTENTS 1. Industry in General......................................................................................................

2. Main Sub‐sectors ....................................................................................................... 2.1. Textile Machinery ………………………………….......................................... 2.2. Agricultural Machinery...................................................................................

2.2.1.Exports…………………………………………………………………… 2.3. Machine Tools…………………………………………………………………….

2.4. Construction and Mining Machinery……………………………………………. 2.5. Food Processing Machinery……………………………………………………..

2.5.1. General Assessment ………………………………………………….. 2.5.2. Medium Term Expectations …………………………………………..

2.6. Pumps and Compressors………………………………………………………..

2 4 4 4 5 8 8 9 9 10 12

3

TURKEY’S MACHINERY INDUSTRY

1. Industry in General

Throughout the five-year development plan periods implemented since 1963, "industry based growth" has been one of the main objectives in Turkey. However, the industrialisation strategies adopted and economic policies followed have shown great differences before and after 1980. An import substitution policy had been implemented until 1980. However, after 1980, significant progress has been made towards establishing the principles and fundamentals of a market economy through the introduction of export-oriented industrialisation.

These reforms made significant contribution to the dynamism of the private

sector and improved the adaptability of Turkish economy to internal and external impacts. Therefore, the source of industrial growth in recent years has been investments and the dynamism of the private sector.

As a result, industry has shown a great performance, except the years in

which economic crises occurred. Considerable increases were recorded in industrial value added, in the volume of exports and share of manufacturing industry in exports. As a result of economic growth, the volume of imports especially for investment and intermediate goods has also increased.

Following a severe contraction in industry in the year 2001 as a result of the

recent economic crises, signs of recovery was observed starting from the first quarter of 2002 and continued at a higher rate with positive developments in the Turkish economy. Due to recovery in domestic demand and sustained export performance, there has been a considerable increase in production and capacity utilization in the manufacturing industry since then.

Turkish industry mainly depends on the private sector activities. The share of

public sector in the manufacturing industry has been decreased through privatisation activities in recent years. Currently, more than 80 % of production and about 95 % of gross fixed investment in the manufacturing industry is realized by the private sector. The main objective for the improvement of industrial sectors emphasized in the Eighth Five Year Development Plan is to increase competitiveness and productivity of the industry, and to promote and maintain sustainable growth within an outward oriented structure, in the face of increased global competition. This objective will be achieved within the framework of market principles and in compliance with international agreements.

In that respect, Turkish industry shall have a structure, in which it will utilise, as

possible, domestic resources, produce in compliance with environmental norms, consider consumer health and preferences, use well-qualified labour, apply strategic management techniques, attach importance to R&D, generate technology, create original designs and trademarks and thus take its proper place in international markets.

4

In order to reach those targets it is of vital importance that private sector gives emphasis to investments, which aim at creating high value added, enhancing competitiveness, increasing employment, productivity and exports and enabling development and/or transfer of appropriate technologies. Foreign direct investments will certainly play an important role in that process. Information and technology intensive industries such as defence and aviation, machinery, chemicals, electronics, software and biotechnology will be promoted, the use of advanced technologies in industry will be increased and the competitiveness of traditional industries will be enhanced.

The machinery industry in Turkey is largely composed of private companies

rather than state‐run companies, which dominate many other sectors. Turkey has established itself not only as a major producer of machinery ($20 billion USD in 2006), but also as a major market for machinery sales. Turkey is listed among the 10 largest markets in Europe for machinery, with roughly $28 billion USD in sales. The industry is highly versatile, producing machines ranging from building and drilling machinery to hand tools. For decades, the industry focused on producing machinery for sale and use inside of Turkey. Since 1980, the focus has been on producing machinery for sale and use in foreign markets. The machinery sector is responsible for the livelihoods of nearly 200,000 employees working for around 11,000 companies. Quick Facts: 1. The production volume of the Turkish machinery industry in 2006 was close to

$20 billion USD. 2. The export volume in this sector was $8.7 billion USD in 2007, as compared to

$6.5 billion USD in 2006 3. The import volume was $22.5 billion USD in 2007, as compared to $19.1 billion

USD in 2006. 4. The industry employs between 180,000 and 200,000 people. 5. Turkey is among the largest 10 markets of machinery in Europe, with around $28

billion USD total machinery sales.

6. Turkey is the 16th‐largest manufacturer among 29 machine tools manufacturing countries.

The Turkish machinery industry has a wide product range. Today, the industry

produces building machinery; heavy industrial machinery; machine tools; hand tools; drilling machines; pumps and compressors; textile machinery; food processing machinery; internal combustion engines and turbines; sewing machines; refrigerators; washing machines; dishwashers; valves; conveying and hoisting machines; cutting and bending machines; air conditioning units; woodworking machinery; boilers and burners. The industry is also capable of producing parts and

accessories for the above‐mentioned machinery types. The share of the local inputs used in the production of these machineries is around 80 percent.

5

2. Main Sub‐sectors 2.1. Textile Machinery

Turkey has an advanced textile and clothing industry and has become quite

strong in almost all sub‐sectors of textiles. Steadily increasing textile production has meant a continuous and increasing demand for textile machinery. Consequently, the development of the textile industry gave rise to a huge textile machinery park in Turkey.

Today, the production varies from basic models to advanced textile machinery

and highly automated equipment, such as atmospheric jet dyeing or blow dyeing machinery. Most of the manufacturers range from small to medium sized and are located in Istanbul and İzmir. Exports of the sector reached $225 million USD in 2006. Main destinations were India, Bangladesh, Pakistan, Uzbekistan, Syria, Iran, Germany and Egypt. 2.2. Agricultural Machinery

Turkey is one of the few countries of the world which are self sufficient in food.

At present Turkey is the largest producer and exporter of agricultural products in the Near East and North Africa. In fact, Turkey has traditionally been described as the world’s food storehouse by many analysts. Such a huge agricultural sector has resulted in a strong agricultural machinery sector in Turkey

According to the 2008 figures 24.7/% of Turkey’s population is engaged in

agriculture and livestock production. About 7.5% of total income in Turkey is obtained from agriculture.

The agricultural machinery sector is expected to further develop with the

development and completion of the Southeastern Anatolia Project (GAP) which takes a new start in 2008. The prooject area covers 9 provinces in the Euphrates-Tigris basins and Upper Mesopotamia plains (Adıyaman, Batman, Diyarbakır, Gaziantep, Kilis, Mardin, Siirt, Şanlıurfa and Şırnak). The GAP is a comprehensive group of projects which includes construction of dams, hydroelectric power plants and irrigation systems as well as providing developments in agricultural infrastructure, transportation, industry, education, health and in other sectors. The basic development objective of the GAP is to transform Southeastern Anatolia into an “Export Centre based in Agriculture”. One of the ultimate objectives of the project is to widen the irrigation schemes in an area extending over 1.7 million hectares (At present, total irrigated area in GAP region is 225 thousand hectares). Consequently, there will be substantial changes in crop pattern and output. Agriculture based industrial development will capitalize on such products as soybeans, peanuts, corn and sunflowers which have not been grown much prior to irrigation as well as oil seeds and fodder crops. Due to these developments, the agricultural machinery industry is expected to increase its capacity, quality and product range and become a primary branch of the Turkish machinery sector.

The agricultural machinery production industry is a branch of the industrial

sector, which produces investment goods. All of the agricultural pmachinery and

6

almost all of the tractors manufactured in the sector are used in agricultural production activities (a very small percentage of tractors are used in other activities, mostly in the construction sector). These products, which are also called “Agricultural Mechanization Tools/devices”, are very important agricultural inputs which increase the efficiency of employment in agricultural production, decrease costs and support product quality and productivity by ensuring the use of modern production technologies and by having agricultural operations done on time and in accordance with agrotechnical demand.

At present the following products are in the product range of the Turkish

agricultural machinery industry: Farm tractors, engined single-axe hoes, engined mower machines, soil preparing/earth moving and seed bed preparing machinery and equipment, seed drilling, sowing, seeding, transplanting machinery and equipment, manuring machines, plant protection and irrigation/sprinkling tools and equipment, harvesting/reaping machines, threshing, drying, throwing, cleaning, classifying, processing etc. Machinery, machinery and equipment for animal products, other machinery and equipment for field and garden agricultural production.

The agricultural machinery industry has two main categories: tractors and

agricultural machinery. The agricultural machinery industry is comprised of about 1000 manufacturers countrywide. About 225 manufacturers organized under the Turkish Association of Agricultural Machinery and Equipment Manufacturers – TARMAKBİR. Companies manufactureing agricultural machinery and equipment except tractors are mostly small and medium size companies. The sector employs about 15,000 workers.

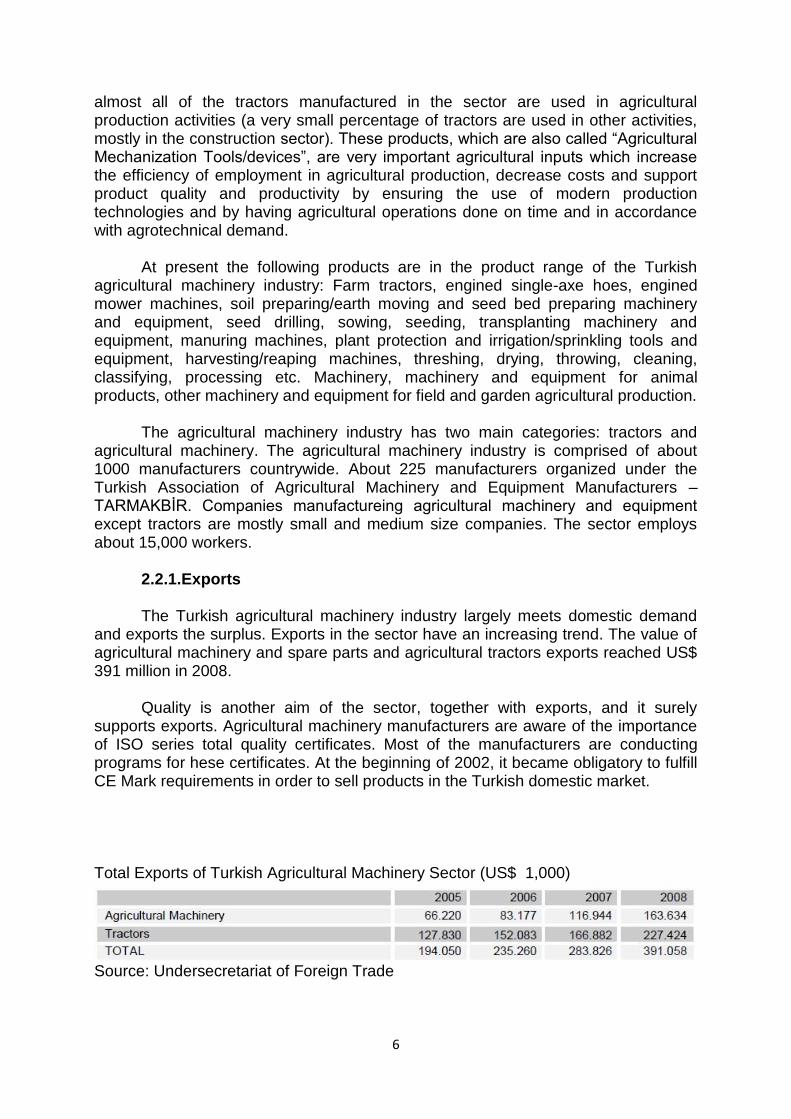

2.2.1.Exports The Turkish agricultural machinery industry largely meets domestic demand

and exports the surplus. Exports in the sector have an increasing trend. The value of agricultural machinery and spare parts and agricultural tractors exports reached US$ 391 million in 2008.

Quality is another aim of the sector, together with exports, and it surely

supports exports. Agricultural machinery manufacturers are aware of the importance of ISO series total quality certificates. Most of the manufacturers are conducting programs for hese certificates. At the beginning of 2002, it became obligatory to fulfill CE Mark requirements in order to sell products in the Turkish domestic market.

Total Exports of Turkish Agricultural Machinery Sector (US$ 1,000)

Source: Undersecretariat of Foreign Trade

7

Turkey’s Exports of Agricultural Machinery

Source: Undersecretariat of Foreign Trade

The main products exported are: tractors, parts and components of harvesting,

threshing machines, other thresher machines, other harrow, cultivator etc. Machines, machines for cleaning grains, leguminous etc., machines for preparing feeds, sprayers/mistblowers, combine harvesters, other poultry machines, ploughs, parts and components of their field, garden, forestry, bee keeping machines, milking machines, fertilizer spreaders, other diary machines, other harvesting machines.

Turkish agricultural machinery industry products are exported to a wide range

of countries in the world. Major export markets are France, Bulgaria, Morocco, Sudan

8

and Italy in agricultural machinery; the USA, Morocco, South Africa, Mexico and Australia in tractors.

Exports of Agricultural Machinery by Countries (US$ 1,000)

Source: Undersecretariat of Foreign Trade Exports of Agricultural Tractors by Countries (US$ 1,000)

Source: Undersecretariat of Foreign Trade

9

The major trade fairs related to agriculture and agricultural machinery industry which will be held in Turkey in 2009 are as follows (those fairs are organized annually):

Agrodays – Agriculture Fair April 2009, Mersin

Animalia International Cattle Breeding Fair June 2009, Istanbul

Agrotec 2009 – International Agriculture Technologies Fair August 2009, Ankara

BurTarım – Bursa Agriculture, Stockbreeding, Poultry, Seed Raising, Saplings and Dairy Industry Fair October 2009, Bursa

Adana Agriculture – Agriculture, Stockbreeding, Poultry and Dairy Industry Fair November 2009, Adana

Growtech Eurasia – International Horticulture, Agriculture, Floriculture and Technologies Fair December 2009 Antalya

AGROEURASIA – Istanbul Agriculture, Stock Breeding, Seed Raising, Saplings, Poultry and Dairy Industry Fair December 2009, Istanbul

2.3. Machine Tools

Turkey is the 16th‐largest manufacturer among 29 machine tools manufacturing countries. Turkey produces various machine tools, such as universal/vertical milling machines, universal/turret turning lathes, cylindrical/surface grinding machines, tool grinding machines, radial grinding machines, etc. Exports of the industry exceed $365 million USD, and the main destinations are Italy, Germany, Russian Federation, Spain, Iran, Bulgaria, Romania, the US, the UK, Iraq and Israel. 2.4. Construction and Mining Machinery

The development of the construction industry has resulted in a large and diversified product range of building materials, a dynamic and respectable contracting

services sector and a well‐established construction and mining industry. There are 1,200 manufacturers engaged in the construction and mining machinery. They are mainly located in Istanbul, Konya and Ankara.

The industry is capable of producing pulley tackles; hoists; winches; capstans;

jacks; derricks; cranes; straddle carriers; forklift trucks; lifting; handling; loading and

unloading machinery; self‐propelled bulldozers; graders and excavators; scraping and boring machinery for earth, stone and mineral elements; spare parts of construction machinery, work trucks and lifting equipment for factories and airports, etc.

10

Exports of the industry reached $530 million USD in 2006. The main destinations were Germany, the UK, Italy, Iraq, Algeria, the US, the Russian Federation, France, Belgium, Bulgaria, Kazakhstan, Azerbaijan and Kuwait. 2.5. Food Processing Machinery

2.5.1. General Assessment Turkish food industry contributes around 5 per cent of the GNP. Food industry

has a 20 per cent share in total production of manufacturing sector by 2002. Food sector employs more than 100 thousand registered workers and technical staff in more than 28 thousand enterprises which are mostly SMEs. Two thousand of these enterprises are relatively modern and bigger in the sector. In 1990, the number of enterprises producing foodstuffs were around 25 thousand.

In most of the sub-sectors of food industry capacity utilization is approximately

at a level of 50 per cent. This fact is generally caused by changing domestic and foreign consumption trends and consumer preferences, the weak financial structure of SMEs in the sector, wrong investment decisions, instability in export markets, seasonality of agricultural production and insufficient integration or coordination between agriculture and industry.

2.5.1.1. Main Policies and Related Legislation

The issue of food safety has been a priority area after the Customs Union with the EU in 1996. Decree Law no. 560 Regarding the Manufacture, Consumption and Inspection of the Foodstuffs has been put into force in 1995 and harmonization of food legislation to the EU acquis has been started by the government. This Decree Law enforces food safety controls in the context of the Turkish Food Codex to be conducted by the Ministry of Agriculture and Rural Affairs (MARA) in production and export/import stages and by the Ministry of Health in the market. MARA has been responsible for official food control up to the marketing stage, production permissions, and import licencing.

The Ministry of Health has been responsible for the technical and hygienic

inspection of manufacturing plants and the control of the foodstuffs in the market regarding health concerns. However, a draft law which is consistent with the EU food law, is prepared to build a unified and improved official control system for food safety in the country that works under the responsibility of MARA.

In order to prevent the public health risks originating from food and to provide

a better perspective to the agricultural and food trade, the new food safety system will emerge into one that will be based upon the HACCP (Hazard Analysis Critical Control Points), GMP (Good Manufacturing Practices), GHP (Good Hygiene Practices), risk analysis (risk evaluation, management, and communication) based on the .farm-to-table. safe food objectives of the EU along with an effective coordination between related bodies.

11

2.5.1.2. Public Enterprises in the Sector and Privatization

In only a few sub-sectors of the food industry, such as sugar, meat and tea industries, there are state owned enterprises in Turkey. However, these state enterprises do not have monopoly power and private firms coexist at the production and marketing stages of the products. In the mid-1990.s state owned factories in milk and feed industries and a number of meat combines were privatized.

It is important to mention that a roadmap of privatization for 26 state owned

sugar factories (owner is a company named TSFAS) were declared by the government in 2003. Privatization process is expected to be completed by the end of 2004. Sugar factories has a market share of more than 70 per cent in the domestic market and there are no price controls for both sugar beet and sugar in the domestic market.

2.5.1.2.1. Strengths

No difficulty finding raw materials, like agricultural produces, packaging material etc.,

Variety and quantity of agricultural production,

Relatively cheap workforce,

Large domestic market and young population,

Presence of widespread local communication networks and infrastructure,

Sufficient educated and specialized workforce,

Developing markets close to Turkey,

Increasing volume of foreign trade,

Perpective for EU accession.

2.5.1.2.2. Weaknesses

Insufficient integration and cooperation between agriculture and industry,

Quality and safety problems in the agriculture,

Technology and capacity utilization problems of most food producing SMEs,

Need to improve the official food control system in line with the EU legislation.

The Turkish food processing machinery and equipment industry is the most modern in the Middle East, North Africa, Balkans, Baltic and Central Asia. The industry is

capable of producing flour and grain mill machinery; bakery and pasta‐making machinery; bakery ovens; industrial machinery for food and drink preparation; machinery for extraction/preparation of fats and oils; machinery for cleaning/sorting/grading seeds and grains; cacao and confectionary machinery; presses and crushers for wine, fruit juice and beverages; pasteurizers and sterilizers; and poultry processing machinery; milking and dairy machinery; machinery for the preparation of fruits and vegetables; cream separators; brewery machinery, etc.

Most manufacturers are located in Istanbul, Konya, Ankara, İzmir and

Gaziantep. Industry exports have reached $196 million USD. The main destinations

12

are Saudi Arabia, Kazakhstan, the Russian Federation, Iraq, Azerbaijan, Romania, Tunisia, Syria, Egypt, Iran and Algeria.

2.5.2. Medium Term Expectations In the coming ten years, domestic market is foreseen to grow more in real

terms than in the 1990-2002 period. The reason is that no economical and political crisis are expected in the near future and this would lead the country to grow in stability, improving the net income. The food demand of the young generation in Turkey is diverse and consumption trends are quiet different from that of the most EU countries..

On the other side, food production depends heavily on the changes in

agricultural production. Agricultural production in Turkey is expected to be more commercial and to get more capital-based in the coming years, in order to become more productive and competitive in the EU market. Increasing agricultural production and developing food industry would increase the accessibility of people to food and create sufficient conditions to increase exports. Inward processing regime is another tool to increase exports in Turkey when firms find new markets to export food but have shortages of raw material in the domestic market.In almost all sub-sectors, investments by technology transfer, structural improvement or merger would help the enterprises to grow rapidly and become more competitive in the markets.

In animal product (meat and milk) processing industries, if the safety of raw

material and vertical integration in the sector would be improved in line with agricultural infrastructure, these industries are believed to promise considerable development in the medium term. The production of animal husbandry sector is expected to be raised via governmental support which would lead to the improvement of the diet of the society.

Demand for processed fishery products increased around 8 per cent during

1990-2002 period. Considering the rich water resources in Turkey, fish processing is foreseen to have a great potential for investment. Fruit and vegetable processing industry has had a considerable growth since the beginning of 1990.s. The number of varieties, improving quality and cultural consumption patterns in Turkey promote new investments in this sub-sector. The price advantage and marketing opportunities are among the other reasons to stimulate future investments or mergers in the sector.

Sugar confectionery, cocoa products, pasta and pastry production are seen to

be potential industries with supply of abundant domestic raw materials, namely cereals and sugar. Sugar confectionery production grew by nearly 2 per cent, chocolate and other food preparations containing cocoa by 9 per cent and pasta and bakery products by more than 2 per cent annually in 1990-2002 period. When the export markets in the neigbourhood of Turkey and young Turkish population are taken into account, these industries are predicted to have a continuous growth potential.

13

Moreover, functional and herbal foods can be produced and launched to the Turkish market or to world markets according to consumer preferences. Because of increasing health concerns in developed countries, olive oil and processed organic products are believed to generate more income in Turkey.

Additionally, privatization of sugar factories is believed to give an opportunity

of entering to a large market to investors to meet the demand of a vastly consumed product in Turkey. With the EU membership perpective, Turkish agriculture would be more knowledge based and capital intensive in order to be more competitive and productive and to become closer to the standards of the developed countries. This would help much the food industry to produce and trade more in the world markets as well as nourishing the nation 2.6. Pumps and Compressors

The pumps and compressors industry is mainly located in Istanbul, Konya and İzmir. The main products are pumps fitted with a measuring device; hand pumps; fuel; lubricating or cooling medium pumps for internal combustion piston engines; concrete pumps; reciprocating positive displacement pumps; rotary positive displacement pumps; centrifugal pumps; parts of pumps for liquids; and compressors.

Exports of the sector are around $340 million USD, and the main destinations are Germany, the US, the UK, Iraq, France, the Russian Federation, Italy, Romania and Azerbaijan.