![Laboratory Microchem Silliker Private Limited, A-513 ... Fibre GAFTA 2003 [10:0] IS: 12711 - 1989 (Reaffirmed 1994) 1 - 30 % ... 5 - 99 % Sodium Chloride (Salt) IS: 2860 - 1964 (Reaffirmed](https://static.fdocuments.us/doc/165x107/5aa219487f8b9ada698c7644/laboratory-microchem-silliker-private-limited-a-513-fibre-gafta-2003-100.jpg)

TURKEY 0.091288848 0.31 Credit & Issue Rating Banking ... · private equity, leasing, factoring and...

20

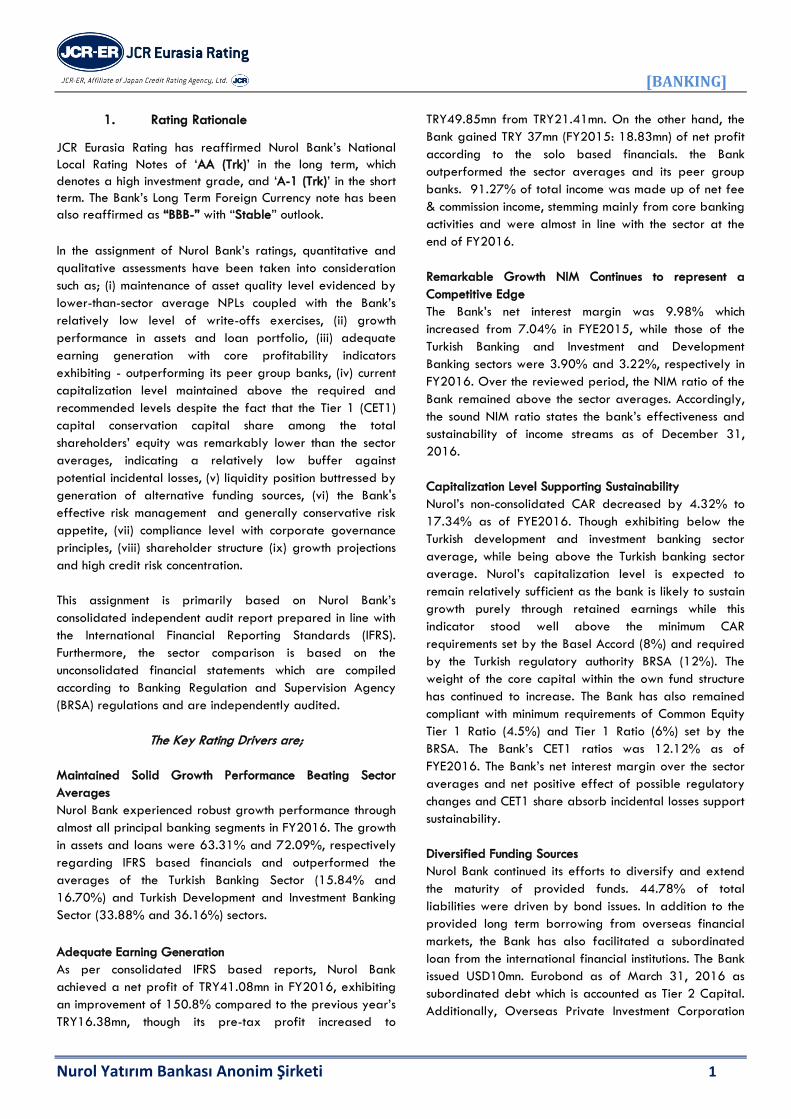

TURKEY Copyright © 2007 by JCR Eurasia Rating. 19 Mayıs Mah., 19 Mayıs Cad., Nova Baran Plaza No:4 Kat: 12 Şişli-İSTANBUL Telephone: +90(212)352.56.73 Fax: +90 (212) 352.56.75 Reproduction is prohibited except by permission. All rights reserved. All information has been obtained from sources JCR Eurasia Rating believes to be reliable. However, JCR Eurasia Rating does not guarantee the truth, accuracy and adequacy of this information. JCR Eurasia Rating ratings are objective and independent opinions as to the creditworthiness of a security and issuer and not to be considered a recommendation to buy, hold or sell any security or to issue a loan. This rating report has been composed within the methodologies registered with and certified by the SPK (CMB-Capital Markets Board of Turkey), BDDK (BRSA-Banking Regulation and Supervision Agency) and internationally accepted rating principles and guidelines but is not covered by NRSRO regulations. http://www.jcrer.com.tr Credit & Issue Rating Updated Banking [Financial Institutions] Long Term Short Term International Foreign Currency BBB- A-3 Local Currency BBB A-3 Outlook FC Stable Stable LC Stable Stable Issue Rating n.a. n.a. National Local Rating AA(Trk) A-1(Trk) Outlook Stable Stable Issue Rating AA(Trk) A-1(Trk) Sponsor Support 1 - Stand Alone AB - Sovereign* Foreign Currency BBB- - Local Currency BBB- - Outlook FC Stable - LC Stable - *Affirmed by Japan Credit Rating Agency on October 7,2016 Chief Analyst: Orkun İNAN +90 212 352 56 73 [email protected] 9.977248812 7.038781998 6.398667315 4.437502728 6.183027592 0 2 4 6 8 10 12 NIM (%) 63.31 12.16 45.48 73.21 34.94 0.00 20.00 40.00 60.00 80.00 Growth Rate (%) 5.287183697 3.160331535 3.744637723 0.091288848 2.112945816 0 2 4 6 ROAA (%) 17.34 21.66 16.89 14.20 19.01 0.00 5.00 10.00 15.00 20.00 25.00 2016 2015 2014 2013 2012 CAR (%) 14.38 18.00 16.64 20.60 44.62 0.00 10.00 20.00 30.00 40.00 50.00 2016 2015 2014 2013 2012 Equity / Assets (%) 33.55 18.21 20.52 0.31 5.05 0.00 20.00 40.00 60.00 ROAE (%) Nurol Yatırım Bankası A.Ş. F i n a n c i a l D a t a 2016* 2015* 2014* 2013* 2012* Total Assets (000 USD) 390,384 246,300 275,358 206,021 142,552 Total Assets (000 TRY) 1,169,551 716,141 638,527 438,907 253,401 Total Net Loans (000 TRY) 742,918 431,711 356,456 241,190 150,576 Equity (000 TRY) 168,218 128,936 106,222 90,422 113,057 Net Profit (00 TRY) 41,083 16,381 15,867 0,516 3,872 Market Share (%) ** 0.043 0.0305 0.0318 0.0250 0.0181 ROAA (%) 5.29 3.16 3.74 0.09 2.11 ROAE (%) 33.55 18.21 20.52 0.31 5.05 Equity/T. Assets (%) 14.38 18.00 16.64 20.60 44.62 CAR - Capital Adequacy Ratio (%) 17.34 21.66 16.89 14.20 19.01 Asset Growth Rate (Annual) (%) 63.31 12.16 45.48 73.21 34.94 * End of Year - Based on IFRS Financials ** On Solo Basis Among the Turkish Banking Sector Overview Nurol Yatırım Bankası A.Ş. (hereinafter “Nurol Bank” or the “Bank”), was incorporated in August,1998 and started its operations in May,1999. The Bank carries out operations in the fields of financial consulting, structured finance, private equity, leasing, factoring and cash loans- guarantees through a workforce of 44 as of December 31,2016. Nurol is a small-sized Investment Bank in Turkish Development and Investment Banking Sector, accounting for 0.82% of total assets as of December 31,2016. The Bank ranked 35 th (FYE2015:37 th ) in terms of assets size among the 47 banks in the Turkish financial market and had a 0.043% market share in the entire banking sector at the end of FY2016. The majority shareholders of the Bank were Nurol Holding A.Ş. (78.16%) and Nurol İnşaat ve Tic. A.Ş. (15.96%), which also has direct and indirect control over the Nurol Group-has operations in construction, defense, finance, tourism, health, mining, real estate, marketing and manufacturing industries through 33 firms within the Group. Strengths • Although its sector wide downward trend, the Bank’s profitability indicators with recurring revenue components outperforming sectorial averages, • Despite expanding its loan portfolio, high level of asset quality regarding below-the-sector NPL figures, • Strengthened liquidity structure thanks to diversified and extended the maturity of funds, • Loan book growth rate, being above the Turkey’s banking sector average despite weaker credit demand as interest rates gradually picked up in the country, • High level of compliance regarding corporate governance implementations and sustainability accompanied by well- established managerial practices and advanced risk management system. Constraints • High penetration level of the Turkish financial system increasing risks for sectorial growth, • Declining in the capital adequacy ratio in line with the banking sector's average despite setting aside sufficient capital to withstand shocks, • Continuation of high credit risk concentration among the top ten cash and non-cash loans customers, • Scarce alternative delivery channels to provide continuity of efficiency rates, • Domestic and international political instability, which like a domino effect on macro indicators and translation into national currency depreciation and more expensive funding.

-

Upload

phunghuong -

Category

Documents

-

view

215 -

download

0

Transcript of TURKEY 0.091288848 0.31 Credit & Issue Rating Banking ... · private equity, leasing, factoring and...

TURKEY

Copyright © 2007 by JCR Eurasia Rating. 19 Mayıs Mah., 19 Mayıs Cad., Nova Baran Plaza No:4 Kat: 12 Şişli-İSTANBUL Telephone: +90(212)352.56.73 Fax: +90 (212) 352.56.75

Reproduction is prohibited except by permission. All rights reserved. All information has been obtained from sources JCR Eurasia Rating believes to be reliable. However, JCR Eurasia

Rating does not guarantee the truth, accuracy and adequacy of this information. JCR Eurasia Rating ratings are objective and independent opinions as to the creditworthiness of a

security and issuer and not to be considered a recommendation to buy, hold or sell any security or to issue a loan. This rating report has been composed within the methodologies

registered with and certified by the SPK (CMB-Capital Markets Board of Turkey), BDDK (BRSA-Banking Regulation and Supervision Agency) and internationally accepted rating

principles and guidelines but is not covered by NRSRO regulations. http://www.jcrer.com.tr

Credit & Issue Rating

Updated

Banking

[Financial Institutions]

Long Term Short Term

Inte

rna

tiona

l Foreign Currency BBB- A-3

Local Currency BBB A-3

Outlook FC Stable Stable

LC Stable Stable

Issue Rating n.a. n.a.

Na

tiona

l Local Rating AA(Trk) A-1(Trk)

Outlook Stable Stable

Issue Rating AA(Trk) A-1(Trk)

Sponsor Support 1 -

Stand Alone AB -

Sove

reig

n* Foreign Currency BBB- -

Local Currency BBB- -

Outlook FC Stable -

LC Stable -

*Affirmed by Japan Credit Rating Agency on October 7,2016

Chief Analyst: Orkun İNAN

+90 212 352 56 73 [email protected]

9.977248812

7.0387819986.398667315

4.437502728

6.183027592

0

2

4

6

8

10

12

NIM (%)

63.31

12.16

45.48

73.21

34.94

0.00

20.00

40.00

60.00

80.00

Growth Rate (%)

5.287183697

3.160331535

3.744637723

0.091288848

2.112945816

0

2

4

6

ROAA (%)

17.34

21.66

16.89

14.20

19.01

0.00

5.00

10.00

15.00

20.00

25.00

20162015201420132012

CAR (%)

14.3818.0016.64

20.60

44.62

0.00

10.00

20.00

30.00

40.00

50.00

20162015201420132012

Equity / Assets (%)

33.55

18.2120.52

0.315.05

0.00

20.00

40.00

60.00

ROAE (%)

Nurol Yatırım Bankası A.Ş.

F i n a n c i a l D a t a 2016* 2015* 2014* 2013* 2012*

Total Assets (000 USD) 390,384 246,300 275,358 206,021 142,552

Total Assets (000 TRY) 1,169,551 716,141 638,527 438,907 253,401

Total Net Loans (000 TRY) 742,918 431,711 356,456 241,190 150,576

Equity (000 TRY) 168,218 128,936 106,222 90,422 113,057

Net Profit (00 TRY) 41,083 16,381 15,867 0,516 3,872

Market Share (%) ** 0.043 0.0305 0.0318 0.0250 0.0181

ROAA (%) 5.29 3.16 3.74 0.09 2.11

ROAE (%) 33.55 18.21 20.52 0.31 5.05

Equity/T. Assets (%) 14.38 18.00 16.64 20.60 44.62

CAR - Capital Adequacy Ratio (%) 17.34 21.66 16.89 14.20 19.01

Asset Growth Rate (Annual) (%) 63.31 12.16 45.48 73.21 34.94

* End of Year - Based on IFRS Financials ** On Solo Basis Among the Turkish Banking Sector

Overview

Nurol Yatırım Bankası A.Ş. (hereinafter “Nurol Bank” or the “Bank”), was

incorporated in August,1998 and started its operations in May,1999. The Bank

carries out operations in the fields of financial consulting, structured finance,

private equity, leasing, factoring and cash loans- guarantees through a

workforce of 44 as of December 31,2016.

Nurol is a small-sized Investment Bank in Turkish Development and Investment

Banking Sector, accounting for 0.82% of total assets as of December 31,2016.

The Bank ranked 35th (FYE2015:37th) in terms of assets size among the 47

banks in the Turkish financial market and had a 0.043% market share in the

entire banking sector at the end of FY2016.

The majority shareholders of the Bank were Nurol Holding A.Ş. (78.16%) and

Nurol İnşaat ve Tic. A.Ş. (15.96%), which also has direct and indirect control

over the Nurol Group-has operations in construction, defense, finance, tourism,

health, mining, real estate, marketing and manufacturing industries through 33

firms within the Group.

Strengths

• Although its sector wide downward trend, the Bank’s

profitability indicators with recurring revenue components

outperforming sectorial averages,

• Despite expanding its loan portfolio, high level of asset

quality regarding below-the-sector NPL figures,

• Strengthened liquidity structure thanks to diversified and

extended the maturity of funds,

• Loan book growth rate, being above the Turkey’s banking

sector average despite weaker credit demand as interest

rates gradually picked up in the country,

• High level of compliance regarding corporate governance

implementations and sustainability accompanied by well-

established managerial practices and advanced risk

management system.

Constraints

• High penetration level of the Turkish financial system increasing

risks for sectorial growth,

• Declining in the capital adequacy ratio in line with the banking

sector's average despite setting aside sufficient capital to

withstand shocks,

• Continuation of high credit risk concentration among the top ten

cash and non-cash loans customers,

• Scarce alternative delivery channels to provide continuity of

efficiency rates,

• Domestic and international political instability, which like a

domino effect on macro indicators and translation into national

currency depreciation and more expensive funding.

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 1

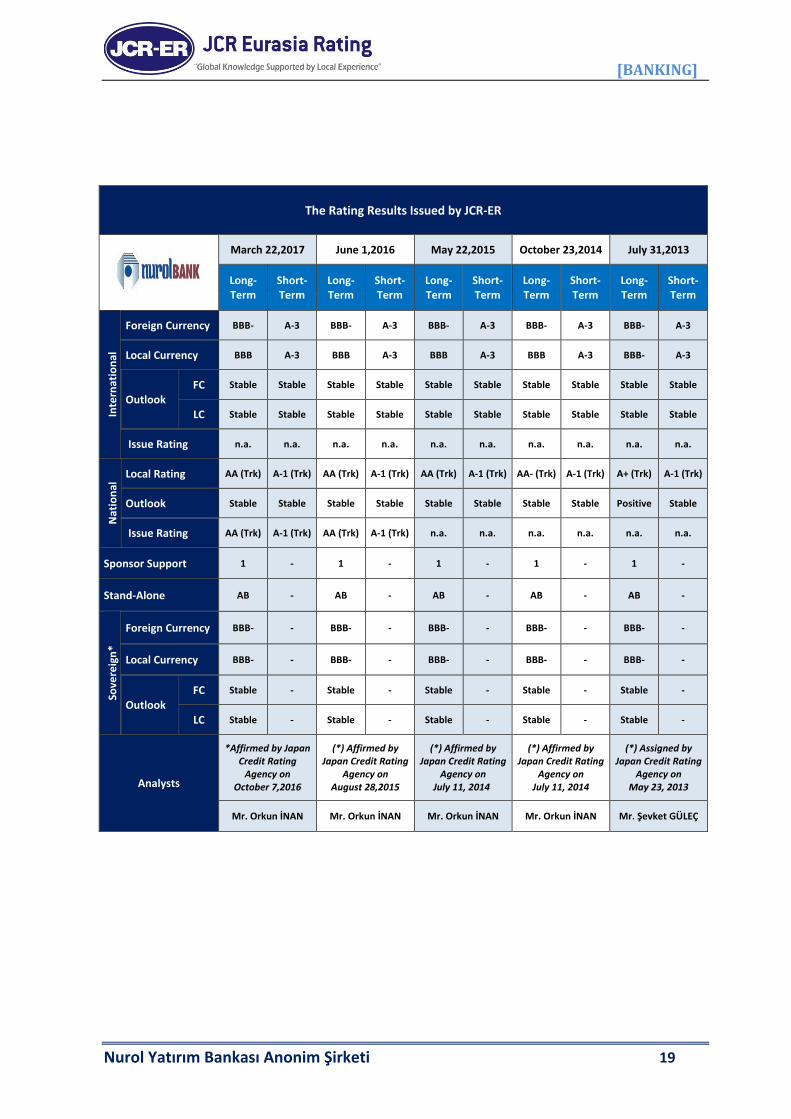

1. Rating Rationale

JCR Eurasia Rating has reaffirmed Nurol Bank’s National

Local Rating Notes of ‘AA (Trk)’ in the long term, which

denotes a high investment grade, and ‘A-1 (Trk)’ in the short

term. The Bank’s Long Term Foreign Currency note has been

also reaffirmed as “BBB-” with “Stable” outlook.

In the assignment of Nurol Bank’s ratings, quantitative and

qualitative assessments have been taken into consideration

such as; (i) maintenance of asset quality level evidenced by

lower-than-sector average NPLs coupled with the Bank’s

relatively low level of write-offs exercises, (ii) growth

performance in assets and loan portfolio, (iii) adequate

earning generation with core profitability indicators

exhibiting - outperforming its peer group banks, (iv) current

capitalization level maintained above the required and

recommended levels despite the fact that the Tier 1 (CET1)

capital conservation capital share among the total

shareholders’ equity was remarkably lower than the sector

averages, indicating a relatively low buffer against

potential incidental losses, (v) liquidity position buttressed by

generation of alternative funding sources, (vi) the Bank's

effective risk management and generally conservative risk

appetite, (vii) compliance level with corporate governance

principles, (viii) shareholder structure (ix) growth projections

and high credit risk concentration.

This assignment is primarily based on Nurol Bank’s

consolidated independent audit report prepared in line with

the International Financial Reporting Standards (IFRS).

Furthermore, the sector comparison is based on the

unconsolidated financial statements which are compiled

according to Banking Regulation and Supervision Agency

(BRSA) regulations and are independently audited.

The Key Rating Drivers are;

Maintained Solid Growth Performance Beating Sector

Averages

Nurol Bank experienced robust growth performance through

almost all principal banking segments in FY2016. The growth

in assets and loans were 63.31% and 72.09%, respectively

regarding IFRS based financials and outperformed the

averages of the Turkish Banking Sector (15.84% and

16.70%) and Turkish Development and Investment Banking

Sector (33.88% and 36.16%) sectors.

Adequate Earning Generation

As per consolidated IFRS based reports, Nurol Bank

achieved a net profit of TRY41.08mn in FY2016, exhibiting

an improvement of 150.8% compared to the previous year’s

TRY16.38mn, though its pre-tax profit increased to

TRY49.85mn from TRY21.41mn. On the other hand, the

Bank gained TRY 37mn (FY2015: 18.83mn) of net profit

according to the solo based financials. the Bank

outperformed the sector averages and its peer group

banks. 91.27% of total income was made up of net fee

& commission income, stemming mainly from core banking

activities and were almost in line with the sector at the

end of FY2016.

Remarkable Growth NIM Continues to represent a

Competitive Edge

The Bank’s net interest margin was 9.98% which

increased from 7.04% in FYE2015, while those of the

Turkish Banking and Investment and Development

Banking sectors were 3.90% and 3.22%, respectively in

FY2016. Over the reviewed period, the NIM ratio of the

Bank remained above the sector averages. Accordingly,

the sound NIM ratio states the bank’s effectiveness and

sustainability of income streams as of December 31,

2016.

Capitalization Level Supporting Sustainability

Nurol’s non-consolidated CAR decreased by 4.32% to

17.34% as of FYE2016. Though exhibiting below the

Turkish development and investment banking sector

average, while being above the Turkish banking sector

average. Nurol’s capitalization level is expected to

remain relatively sufficient as the bank is likely to sustain

growth purely through retained earnings while this

indicator stood well above the minimum CAR

requirements set by the Basel Accord (8%) and required

by the Turkish regulatory authority BRSA (12%). The

weight of the core capital within the own fund structure

has continued to increase. The Bank has also remained

compliant with minimum requirements of Common Equity

Tier 1 Ratio (4.5%) and Tier 1 Ratio (6%) set by the

BRSA. The Bank’s CET1 ratios was 12.12% as of

FYE2016. The Bank’s net interest margin over the sector

averages and net positive effect of possible regulatory

changes and CET1 share absorb incidental losses support

sustainability.

Diversified Funding Sources

Nurol Bank continued its efforts to diversify and extend

the maturity of provided funds. 44.78% of total

liabilities were driven by bond issues. In addition to the

provided long term borrowing from overseas financial

markets, the Bank has also facilitated a subordinated

loan from the international financial institutions. The Bank

issued USD10mn. Eurobond as of March 31, 2016 as

subordinated debt which is accounted as Tier 2 Capital.

Additionally, Overseas Private Investment Corporation

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 2

(OPIC) provided USD10mn. loans as of December 12, 2016.

Short Term Funding Base Exert Pressure on Liquidity

Management

As an investment bank, Nurol Yatirim Bank is not entitled to

collect customer deposits. Therefore, the Bank is funded

through issued debt securities, borrowed funds from domestic

institutions, current balances of its loan customers and equity.

Adequate liquidity level without funding gap or violations

remaining compliant with BRSA parameters. Moreover, the

Bank has initiated some efforts to provide trade finance

facilities in FY2016.

Persisting High Credit Risk Concentration

The Bank’s largest 10 corporate customers constituted

78.60% of the total corporate cash outstanding loans and

72% of total non-cash loans, maintaining high concentration

levels. The Bank’s high concentration level, a by-product of

the Company’s decision to focus on larger corporate

customers, increases the exposure to a single-party risk.

High Level of Compliance regarding Corporate Governance

Implementations and Sustainability

Nurol has high compliance level with the corporate

governance principles particularly regarding the exercise of

shareholders’ rights, efficient and comprehensive system of

public disclosure and the Bank website together serving as

an effective platform in their supporting the transparency

level, comprehensive risk management system with

functionalized organizational units of internal control and

internal audit, contributions to publicly known event and

project.

2. Outlook

JCR Eurasia Rating has reaffirmed “Stable” outlooks on the

short and long term national and international ratings

perspectives of Nurol Yatırım Bank, regarding its capability

to maintain internal equity generation capacity, new funding

sources despite the slight deterioration in capital adequacy

ratio level-well above the legal and targeted boundaries

indicating the capacity to absorb incidental losses-.

Substantial factors that may be taken into consideration

for any future positive changes in ratings and outlook

status include: (i) an enhancement in capital strength through

a considerable cash equity injection, (ii) remarkable

improvements in profitability ratios,(iii) continuity of efforts to

diversify funding mix and extend the maturity profile, (iv)

notable improvement in market efficiencies, (v) steadiness of

recovery in the global economy, (vi) an upgrade of Turkey’s

country ceiling ratings.

Key considerations which would constrain the ratings are

(i) permanency of the deterioration in asset quality

through an increase in NPLs resulting from weakened

debt-servicing capability of real sector firms, (ii)

continuity of below sector average weak profitability

indicators, (iii) diminution in capital adequacy strength,

(iv) probable adversities of ongoing geopolitical risks, (v)

deterioration in liquidity ratios along with the possible

difficulties in accessing external fund resources and

downgrading the sovereign rating level of Turkey.

3. Sponsor Support and Stand Alone

Sponsor Support notes and risk assessments reflect the

financial strength and expected assistance of the

controlling shareholders. It is considered that the utmost

shareholder has the tendency and satisfactory financial

strength to offer financial support when liquidity needs

arise in the short or long term perspective. Based on

these assessments, the Sponsor Support Note of the Bank

has been reaffirmed as “1”, which denotes a strong

external support possibility.

On the other hand, even if the shareholders or public

authorities do not provide any assistance, the Bank is

expected to be able to manage its balance sheet risks

successfully given its own strong equity base and

capitalization levels which are adequate to absorb

incidental losses. Within this context, the Stand-Alone

Grade of the Bank has been reaffirmed as “AB” in JCR

Eurasia’s notation system, which signifies a strong and

credible bank.

4. Company Profile

a. History

Nurol Yatırım Bankası A.Ş. was established on August

6, 1998 as an investment Bank and commenced

operations in May 1999. The Bank was set up as a

subsidiary of Nurol Holding, a prominent conglomerate

in Turkey with stakes in various industries and a

primary focus on the Construction & Contracting,

Defence & Production, Energy, Trading & Service,

Finance and Tourism sectors. While the corporate,

retail, investment and regional banking constitute the

principal axis of Nurol Bank’s operations, the Bank also

offers financial leasing, factoring, trade finance and

consulting services.

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 3

b. Organization & Employees

The Bank’s headquarters is located in Istanbul. The Bank

has employed a staff force of 44 (FY2015: 39). The Board

of Nurol Bank consists of ten members, three of whom are

independent members and a general manager. According

to Capital Market Board (CMB) principles three of Board

Members should be independent and the members of the

audit committee of the BoD are accepted as independent

members. The Company’s organization structure includes

4- Committee (pricing committee, credit, corporate, audit,

asset and liability, discipline and personnel, information

systems strategy) 2 chief assistant general managers, 5

assistant general managers.

c. Shareholders, Subsidiaries

The main shareholder of Nurol Bank is Nurol Holding A.Ş.,

which holds 78.16% of total shares. Nurol Holding A.Ş.,

although set up in 1989; trace back to the establishment of

its flagship company Nurol İnşaat ve Ticaret A.Ş in 1966.

Nurol Holding is currently carrying out activities mainly in

construction and contracting sectors and in defence,

manufacturing industry, real estate investment, energy,

tourism, mining, finance, trade and service sectors with more

than 33 subsidiaries, affiliates, branch offices and project

partnerships within the country and abroad. Nurol Holding’s

total assets reached TRY9.20bn while total equity was

around TRY1.60bn. as of FYE2015. Additionally, the

Group’s sales revenue increased to TRY3.45bn in FY2015

from TRY2.51bn. in FY2014.

The table below indicates the detailed shareholding structure

of the Bank.

The table below indicates the detailed Nurol Holding

A.Ş.’s main engaged sectors.

Nurol Holding A.Ş.'s Engaged Sectors

Construction and Contracting

Nurol İnşaat ve Tic. A.Ş.

Nurol Gayrimenkul Yatırım Ort. A.Ş.

Nurol Makina ve Sanayi A.Ş. Çelik İşletmeleri

Otoyol Yatırım ve İşletme A.Ş.

Defence and Production

Nurol Makina ve Sanayi A.Ş.

Nurol Teknoloji San. ve Mad. Tic. A.Ş.

FNSS Savunma Sistemleri A.Ş.

Financial Services

Nurol Yatırım Bankası A.Ş.

Nurol Sigorta Aracılık Hizmetleri A.Ş.

Commercial and Services

Nurol İşletme ve Gayrimenkul Yönetim A.Ş.

Botim İşletme Yönetim ve Tic. A.Ş.

Energy and Mining Sector

TÜMAD Madencilik San. ve Tic. A.Ş.

Nurol Enerji Üretim ve Pazarlama A.Ş.

Nurol Göksu Elektrik Üretim A.Ş.

Enova Enerji Üretim A.Ş.

Tourism

Turser Turizm Serv. ve Tic. A.Ş.

Bosfor Turizm İşletmecilik A.Ş.

Nurol Kulüp Salima Tatil Köyü ve Turizm İşletmeleri A.Ş

Sheraton Batumi Otel

The following table shows the current shareholder

structure of Nurol Holding A.Ş. as of December,2015.

Shareholders Structure 2015 (TRY) Share %

Nurettin Çarmıklı 258,454,800 0.3330603

Erol Çarmıklı 258,454,800 0.3330603

Mehmet Oğuz Çarmıklı 258,454,800 0.3330603

Eyüp Sabri Çarmıklı 93,030 0.0001199

Gaye Çarmıklı 93,030 0.0001199

Gürol Çarmıklı 62,020 0.0000799

Gürhan Çarmıklı 62,020 0.0000799

Gözde Çarmıklı 62,020 0.0000799

Eda Çarmıklı Yolcu 62,020 0.0000799

S. Ceyda Çarmıklı 62,020 0.0000799

Oğuzhan Çarmıklı 62,020 0.0000799

Aynur Türkan Çarmıklı 38,710 0.0000499

Müjgan Sevgi Kayaalp 22,408 0.0000289

Melih Kayaalp 8,151 0.0000105

Semih Kayaalp 8,151 0.0000105

Paid Capital (000 TRY) 776,000,000 100

Shareholders Structure 2016

Share Amount Share %

Nurol Holding A.Ş. 35,171 78.1578

Nurol İnşaat ve Tic A.Ş. 7,182 15.9600

Nurol Otelcilik ve Tur İşl. A.Ş. 397 0.8822

Nurettin Çarmıklı 400 0.8889

Erol Çarmıklı 400 0.8889

Mehmet Oğuz Çarmıklı 400 0.8889

Eyüp Sabri Çarmıklı 350 0.7778

Oğuzhan Çarmıklı 350 0.7778

Gürol Çarmıklı 175 0.3889

Gürhan Çarmıklı 175 0.3889

Paid Capital (000 TL) 45,000 45,000

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 4

d. Corporate Governance

Although Nurol Bank is not a publicly traded company, Nurol

Bank carries out its operations under Banking Law and the

Banking Regulation and Supervision Authority (BRSA)

regulations. The Bank mostly complies with the Communiqué

on Corporate Governance Principles of Banks’ published on

November 1, 2006 by BRSA. In accordance with the

regulation, the Bank has a Corporate and Remuneration

committee and disclosed its mission, vision, strategies,

periodic financials, annual reports and ethical rules. In

addition, The Bank’s web site provides information and

documentation in terms of transparency and contains the

shareholder structure, curriculum vitae of the BoD and top

management, articles of association and organization chart.

Nurol Bank has a Corporate Governance Committee

responsible for monitoring whether the Corporate

Governance Principles are complied with expressing the

issues that may originate stemming from non-compliance and

submitting reformative activity to its Board of Directors. In

this regard, the compliance level of the Bank is satisfactory.

The Bank revises the articles of association and other internal

regulations as deemed necessary. Moreover, the Bank has

an Investor Relations Department.

The Bank’s Board is composed of ten members and

qualifications of the members meet the terms expressed in

the principles. As can be seen in the resumes found on the

Bank’s website, the members possess the necessary

qualifications in terms of education, professional and

managerial experience. According to Capital Market Board

(CMB) principles, three of Board Members should be

independent and the members of the audit committee of the

BoD are accepted as independent members.

We, as JCR Eurasia Rating, are of the opinion that the senior

management of the Company is adequate in terms of

education, experience and managerial skills.

5. Sector Analysis

The Turkish banking sector, regulated by the BRSA-Banking

Regulation and Supervision Agency; consists of deposit

banks, development and investment banks, and participation

banks which operates on the basis of dividends in the

framework of Islamic rules. The asset size of the banking

sector, which has the largest share in the Turkish financial

system, was USD 799bn. (TRY2.73bn) by the end of 2016.

SUMMARY OF KEY INDICATORS OF THE TURKISH BANKING SECTOR

(000.000) 2016 2015 2014 2013

Asset Size -TL 2,730,942 2,357,386 1,994,263 1,732,382

Asset Size-USD 799,129 807,850 857,047 813,172

Equity-TL 300,171 262,213 231,941 193,704

Profit-TL 37,532 26,052 24,610 24,664

ROAE% 1.86 1.52 1.69 2.01

ROAE% 16.81 13.38 14.79 16.59

NPL Ratio% 3.23 3.09 2.85 2.75

Capital Adequacy Ratio %

15.57 15.56 16.30 15.30

Equity / Total Assets

10.99 11.12 11.63 11.18

Loans / Deposits% 1.16 1.18 1.17 1.10

Asset / GDP ratio in Turkey is close to the level of

developing countries, but lower than the average of

developed countries. Therefore, the growth potential of

the Turkish banking sector is still high compared to the

average.

Although the Turkish banking sector achieved an increase

in profitability by 44.06% in absolute terms in 2016

compared to the previous year, the profitability

performance of the banking sector was 23.01% in dollar

terms due to the extraordinary depreciation of TRY.

Macro prudential measures taken to curb the current

account deficit, especially using credit cards and vehicle

credits, have resulted with changes at the business model

and competitiveness level of the banking sector.

However, the system was loosened in 2016 with new

regulations in this area.

The financial strength of the Turkish banking sector to

support the economic activity and growth remains largely

preserved in 2016, although the exceptional value losses

of the TRY caused this strength to be weakened and the

potential of the Sector’s ability to reach out new

resources is rasped. The borrowing costs of the banks

from abroad is in an increasing trend, due to the Fed’s

contractionary monetary policy. On the other hand, the

increase in the monetary expansion of the European and

Far East markets is limiting the side effects of Fed’s

attitude. limiting the increase. The loose monetary

policies of the European Central Bank will continue to

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 5

support the Turkish banking sector in terms of funding costs in

2017.

Turkey is not exposed to the risk of refinancing the banks in

Turkey, although it is stated that the banking sector will be

put under pressure due to the poor record of the tourism

sector, the weak Turkish Lira, and the energy sector

pressured by low energy prices. In addition, the Turkish

banking sector has always been able to expand its long-

term expansion and increase the credit volume thanks to its

high capital adequacy level. Because the Turkish banking

sector has double-buffer in terms of Capital Adequacy

Ratio. Therefore, according to JCR-ER, the outlook of the

Turkish banking sector is stable, not negative.

Although the average interest margins of the Turkish banking

system, which are downed to the 3-3.5%, are still higher

than developed countries. The Turkish banking sector still

maintains its high net profit margins on local currency and

the efforts continue to increase non-interest income steadily.

Despite its low asset size, the Sector maintained its positive

position in 2016, with high profitability, high deposit share,

high capital ratio, high inflation and high real growth.

However, the continuation of the growth rate in 2017

depends on the stability of the local currency.

In the Turkish Banking Sector, the number of banks operating

in 2014 rose from 51 to 52 in 2015 and to 53 in 2016.

Internet, ATM and POS investments are continuing to increase

in order to increase the accessibility of the banking services.

The concentration of assets, loans and deposits in the sector

is quite high. In all three areas, the share of the top five

banks is close up to 60%. The highest concentration is in

deposits, loans and profit generated, respectively.

The share of non-residents in the equity structure of the

sector is quite high.

NUMBER OF BANKS

State Banks

Private Banks

SDIF Bank

Foreign Banks

TOTAL

DEPOSIT BANKS (*) 3 9 1 21 34

DEVELOPMENT & INVESTMENT BANKS (*)

4 4 - 5 13

PARTICIPATION BANKS 2 - 1 3 6

TOPLAM 9 13 2 29 53

NUMBER OF BRANCHES

State Banks

Private Banks

SDIF Bank

Foreign Banks

TOTAL

DEPOSIT BANKS (*) 3,699 4.225 1 3,018 10,943

DEVELOPMENT & INVESTMENT BANKS (*)

24 13 - 5 42

PARTICIPATION BANKS 77 - - 886 963

TOPLAM 3,800 4.238 1 3,909 11,948

NUMBER OF STAFF

State Banks

Private Banks

SDIF Bank

Foreign Banks

TOTAL

DEPOSIT BANKS (*) 57,509 74,097 221 60,583 192,41

DEVELOPMENT & INVESTMENT BANKS (*)

3,994 1,100 - 215 5,309

PARTICIPATION BANKS 1,116 - - 13,402 14,518

TOPLAM 62,619 75,197 221 74,200 212,23

7

The legal framework of the Turkish banking sector, which

overlaps with the main lines of the EU legislation, except

for abroad branches and deposit guarantees, has been

shaped in accordance with the criteria of consolidation of

integration with global economies, the Basel Accords and

the capital requirement directives (CRD). Within this

context, the European Commission affirmed that both the

control framework and the regulatory framework of the

Turkish banking sector were largely compatible and

equivalent to the EU regime, as of December 2016.

Regarding the regulatory framework, this high level of

equivalence was considered to have originated from the

advanced implementation of Basel III in Turkish

legislation. In terms of risk management, the Turkish

banking sector is capable of managing its pricing and

balance sheet balances in international norms.

The banking sector that is the one that most affected by

national and international regulations, constantly

changing customer demands, developing technology, and

social-political structural changes. In this aspect, it is

expected that banks' agenda will be increasingly

engaged in key issues such as capital, liquidity,

profitability, cost management and digitalization of

internal processes. Especially in 2017, digitalization will

gain importance in cost management and competition.

The Turkish banking sector has a highly dynamic structure

in product and service formations, which is structured with

a flexibility that is in line with the ever-changing

expectations of credit and deposit customers and

investors within the scope of innovative and sustainable

business models. The deepening of capital markets with

the strong capital structure of banking will also continue

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 6

in 2017 as an advantage in collecting deposits and in

inward / outward borrowing.

The Turkish banking sector, which is not yet at the desired

level of scale and cost efficiency, will intensify its structuring

and growth strategies in this particular area.

In the Turkish banking sector, while innovative approaches to

branching and alternative channels are being demonstrated,

the importance of multi-branching still remains. The elasticity

coefficients of the Turkish banking sector are well above the

global optimum levels in terms of lending capacity, interest

volatility and regulatory pressures. Legal arrangements

increase the resilience of banks to crises, as well as create

downward pressure on productivity and profitability.

However, financial innovations created at the national and

global level can significantly eliminate the negative effects

of regulatory constraints.

Banks mainly provide deposit-based financing, while the use

of alternative sources is also increasing. Due to the increasing

funding opportunities, parallel to the expansion of the

quantities in the developed countries, the foreign liabilities of

the banks have increased in recent years. The external debt

restructuring rate of the banking sector is above 100 percent

and the long-term funding from abroad contributes to the

prolongation of the passive market. Banks' securities issuance

continues to grow in an accelerating rate.

The ratio of non-performing loans to equity was 12.87% in

2012, 15.29% in 2013, 15.69% in 2014, 18.13% in 2015

and 19.35% in 2016. In 2016, the ratio of non-performing

loans highly increased by 22.15% in nominal terms and the

share of the problematic loans compared to the previous

year in total credits was mathematically higher than the

previous year because the nominal increase rate in total

loans (16.90%). As of 2016, the conversion rate to non-

performing loan is 3.23%. It should also be noted that

banking sector sells certain impaired receivables in bundles

to “asset management companies”, reducing the impaired

receivable amount in the balance sheet and reducing the

NPL ratio.

As of the end of 2012, the capital adequacy ratio of the

sector increased from 17,90% to 15,30% at the end of

2013 and rose to 16,30% at the end of 2014 and rose to

15,56% at the end of 2015, and lastly to 15.57% in 2016.

The fact that 84.40% of legal equity is composed of main

capital has shown that the industry maintains good quality of

equity structure, but the level of 90% in the past is gradually

decreasing.

In 2016, as in 2015, the banking sector has

fundamentally funded its asset growth from loans and

required reserves through an increase in deposits, equity,

issued securities and borrowings.

SECTOR 2013 2014 2015 2016

PARTICIPATION BANKS 5.55 5.23 5.10 4.87

DEVELOPMENT AND INVESTMENT BANKS

4.05 4.24 4.52 5.23

DEPOSIT BANKS 90.41 90.53 90.37 89.91

Total 100.00 100.00 100.00 100.00

As of the end of 2016, 89.91% of the banking sector is

comprised of deposit banks, whereas 5.23% and 4.87%

belongs to participation banks development and

investment banks respectively. Cumulatively in the last 13

years, the Turkish banking sector has grown almost every

year and this growth has reached a very high rate of

1149.45% between 2004-2016.

On the basis of the USD, the Turkish banking sector grew

by 388.53% over the years 2003-2016. For the last two

years, Turkish banking sector shrank in dollar terms due

to the depreciation of TL.

In 2016, development and investment banks sustained

the most growth at 33.88%. The annual growth rate of

participation banks was 10.50% and the growth rate of

deposit banks was 15.24%, year on year. Contrary to

previous years, the low growth of participation banking

stemmed from the transfer of Bank Asya to the SDIF in

2014 and the problems of the public sector.

In 2015, the Turkish banking sector's total assets grew by

15.84%, with TRY 7.58 billion in foreign currency and

8.26% in TRY resources. Asset growth was 8.13% in

foreign currency assets and 7.71% in TL assets.

In terms of contributing to growth in resources, foreign

currency deposits were ranked first, borrowing from

banks were ranked second, and TRY deposits were

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 7

ranked third. In terms of contributing to growth within the

assets, the first order was TRY loans, the second order was

foreign currency loans, and the third order was obligatory.

The share of deposits in total resources has decreased from

61.9% in 2005, to 52.83% at the end of 2015 and to

53.23% in 2016, while the basic funding balance within

banking resources is still deposits.

In terms of assets, the weight of the securities in the Turkish

banking sector decreased gradually to 12,75%. Credits

increased from 38.93% in 2005 to 63.51% at the end of

2016. The highest increase among the assets due to the

CBRT's reserve ratios within macroeconomic policies has been

challenged in the item of required reserved items. Provisions

constituting 3.68% of assets in 2005 accounted for 6.74% of

assets at the end of 2016. There is a desire to slow down

credit growth as the basis for raising the allowance rates.

While the Turkish banking sector has generally started to

show a downward trend in its profitability indicators, the

current relatively high levels continued in 2016 as well. The

funding structure of the sector is dominated by deposits,

necessitating more branching and operating expenses, which

in turn causes downward reflection on the sector's

profitability. On the other hand, the banks fully reflect the

expected loss rates in the lending process to interest margins

on prudential principles. This weakens the return on assets.

The high level of non-interest expenses indicates that banks

might still need to increase their operational efficiency.

The sector achieved an asset return of 1.86% and an equity

return of 16.81%. One of the reasons for the high

profitability in 2016 is the one-off income items obtained in

2016.

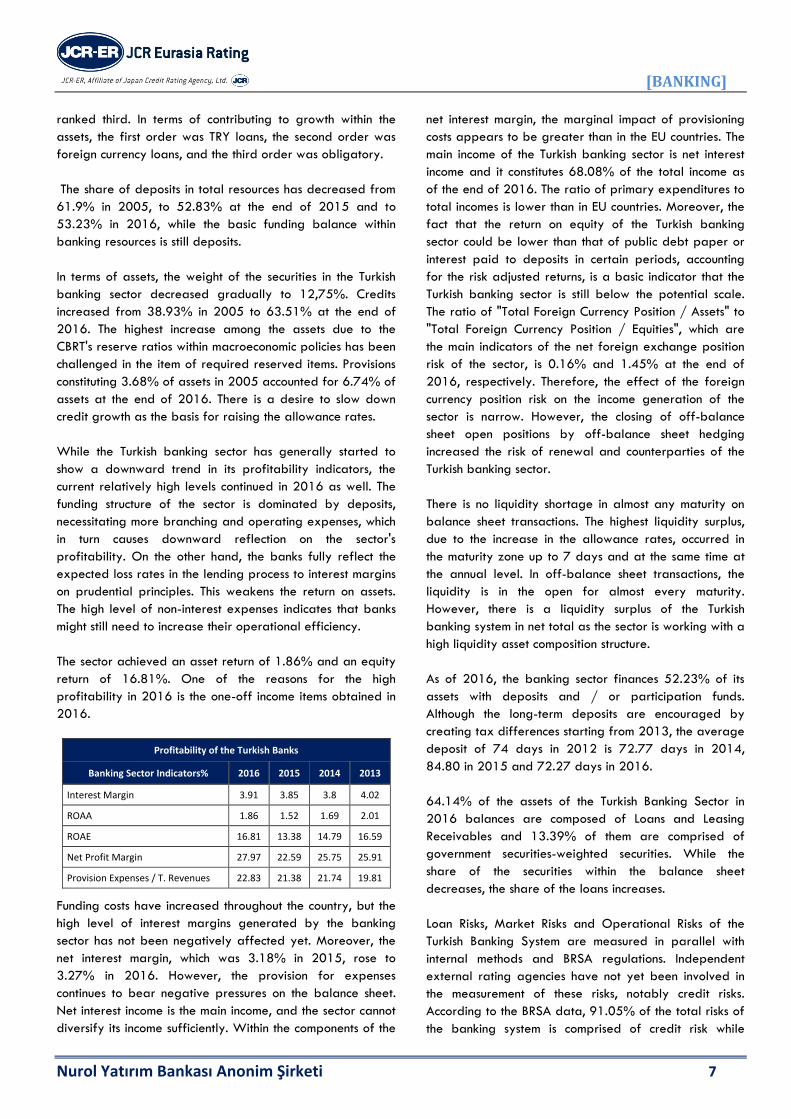

Profitability of the Turkish Banks

Banking Sector Indicators% 2016 2015 2014 2013

Interest Margin 3.91 3.85 3.8 4.02

ROAA 1.86 1.52 1.69 2.01

ROAE 16.81 13.38 14.79 16.59

Net Profit Margin 27.97 22.59 25.75 25.91

Provision Expenses / T. Revenues 22.83 21.38 21.74 19.81

Funding costs have increased throughout the country, but the

high level of interest margins generated by the banking

sector has not been negatively affected yet. Moreover, the

net interest margin, which was 3.18% in 2015, rose to

3.27% in 2016. However, the provision for expenses

continues to bear negative pressures on the balance sheet.

Net interest income is the main income, and the sector cannot

diversify its income sufficiently. Within the components of the

net interest margin, the marginal impact of provisioning

costs appears to be greater than in the EU countries. The

main income of the Turkish banking sector is net interest

income and it constitutes 68.08% of the total income as

of the end of 2016. The ratio of primary expenditures to

total incomes is lower than in EU countries. Moreover, the

fact that the return on equity of the Turkish banking

sector could be lower than that of public debt paper or

interest paid to deposits in certain periods, accounting

for the risk adjusted returns, is a basic indicator that the

Turkish banking sector is still below the potential scale.

The ratio of "Total Foreign Currency Position / Assets" to

"Total Foreign Currency Position / Equities", which are

the main indicators of the net foreign exchange position

risk of the sector, is 0.16% and 1.45% at the end of

2016, respectively. Therefore, the effect of the foreign

currency position risk on the income generation of the

sector is narrow. However, the closing of off-balance

sheet open positions by off-balance sheet hedging

increased the risk of renewal and counterparties of the

Turkish banking sector.

There is no liquidity shortage in almost any maturity on

balance sheet transactions. The highest liquidity surplus,

due to the increase in the allowance rates, occurred in

the maturity zone up to 7 days and at the same time at

the annual level. In off-balance sheet transactions, the

liquidity is in the open for almost every maturity.

However, there is a liquidity surplus of the Turkish

banking system in net total as the sector is working with a

high liquidity asset composition structure.

As of 2016, the banking sector finances 52.23% of its

assets with deposits and / or participation funds.

Although the long-term deposits are encouraged by

creating tax differences starting from 2013, the average

deposit of 74 days in 2012 is 72.77 days in 2014,

84.80 in 2015 and 72.27 days in 2016.

64.14% of the assets of the Turkish Banking Sector in

2016 balances are composed of Loans and Leasing

Receivables and 13.39% of them are comprised of

government securities-weighted securities. While the

share of the securities within the balance sheet

decreases, the share of the loans increases.

Loan Risks, Market Risks and Operational Risks of the

Turkish Banking System are measured in parallel with

internal methods and BRSA regulations. Independent

external rating agencies have not yet been involved in

the measurement of these risks, notably credit risks.

According to the BRSA data, 91.05% of the total risks of

the banking system is comprised of credit risk while

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 8

7.04% correspond to operational risks and 1.91% to market

risk. The total amount of risk is 2.029.181 Million TRY.

The Turkish Banking Sector generally covers the on-balance

sheet foreign currency short position with off-balance sheet

foreign currency long position. The net foreign currency net

general position of the sector has been at low levels for

many years.

In the sector, as a whole, the share of equity in the balance

sheet declined from 13.17% in 2012, to 11.19% in 2013, to

11.64% in 2014, 11.12% in 2015 and to 10.99% in 2016.

Participation banks have the lowest equity / total resources

ratio in the sector.

On the other hand, despite the fact that development and

investment banking has lost its attractiveness in developed

countries due to the worsening equity balance of assets,

Turkey still maintains its high capital and high capital ratios

and continues its attractiveness.

The capital adequacy ratio of the sector is calculated

according to Basel II rules. For many years, CAR still

maintains its high level. As of 2015, the CAR is 15.57%.

Country ratings of Fitch, Moody's, S&P, JCR, DBRS and IIRA

rating institutions are used in determining the credit quality

stages of foreign currency receivables due from central

governments and central banks. Rating scales of Fitch,

Moody's, S & P, JCR, DBRS and IIRA rating agencies are

used to determine the level of credit quality of receivables

from the banks and intermediary institutions, regional

administrations or local administrations, administrative units

and non-commercial enterprises, multilateral development

banks, if the institutions are resident abroad.

JCR Eurasia Rating has been authorized to determine the risk

weights of the collective receivable classes from banks,

borrowing instruments issued by banks, financial institutions

other than banks, borrowing instruments issued by financial

institutions other than banks, corporate companies not

included in Small and Medium Size Enterprises, by corporate

companies not included in Small and Medium Enterprises, of

domestic and/or foreign residence. However, since the notes

issued by JCR Eurasia Rating have not yet been matched to

appropriate risk weights, the CAR is calculated at 100% risk

weight assuming that the bank receivables in this scope are

not rated.

Despite high profitability and capital adequacy ratios in the

Turkish banking sector in 2016, and the high level of

problematic receivables transferred to restructuring and

asset management companies, the increase in the conversion

rate of the assets to impaired receivable class could not be

prevented. The reason for this trend is the deterioration

of the borrowers’ balance sheets in the wake of

significant foreign currency rate increases.

6. Financial Analysis

a. Financial Indicators & Performance

i. Indices Relating to Size

Nurol Bank completed FY2016 with an asset growth rate

of 63.24%, highly up from the previous year’s figure of

13.42%. The graphs below display the growth of the

Bank’s asset base in comparison to those of the sectors.

Up to FY2016, while the overall asset base growth

performance of the Bank stayed well above the sectors’

cumulative averages.

The Bank’s annual asset base growth performance over

the reviewed period stayed well above the sector

averages and nearly fourfold that of the average

annual growth of the Turkish Banking Sector and almost

doubled that of the Development & Investment Banking

Sector. The Bank's strategy is to create a diversified

corporate loan book targeting high-quality corporate

credits with a range of customers. Nurol Bank has

focused on developing its capacity to offer a wide range

of products to its current and new corporate clients.

Turkish development and investment banking sector

experienced a moderate growth reflecting the

uncertainties in the domestic market and macro-

prudential measures enacted by the regulatory agencies

so as to control the credit expansion. Turkish

development and investment banking sector’s asset

growth displayed a 33.88% expansion in FY2016,

higher than the Turkish Banking Sector’s growth rate of

15.84%.

15.84 18.21 15.11

26.38 12.57

33.8826.1320.58

32.94

26.70

63.24

13.42

46.49

74.25

36.07

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

20162015201420132012

Annual Asset Growth Rates %

Turkish Banking Sector

Turkish Devolopment and Investment Banking Sector

Nurol Yatırım Bankası A.Ş.

The Bank’s asset size market shares figures, with regard

to both Development & Investment banks and the entire

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 9

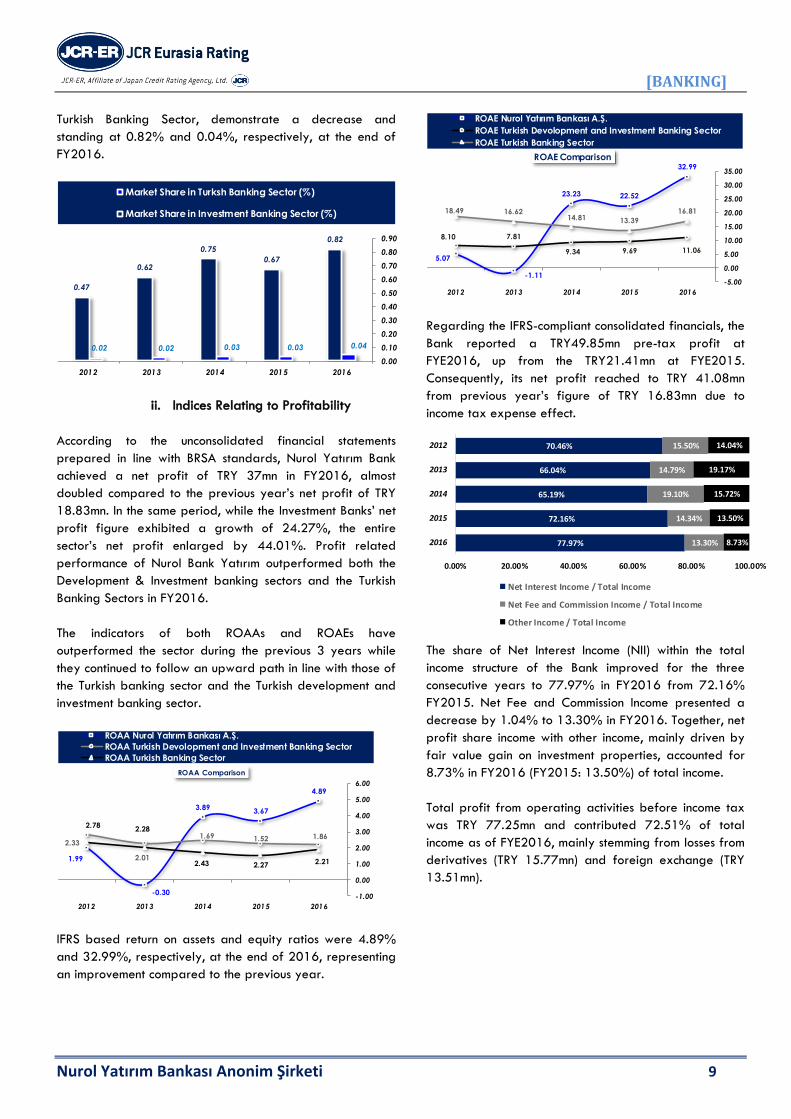

Turkish Banking Sector, demonstrate a decrease and

standing at 0.82% and 0.04%, respectively, at the end of

FY2016.

0.040.030.030.020.02

0.82

0.67

0.75

0.62

0.47

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

20162015201420132012

Market Share in Turksh Banking Sector (%)

Market Share in Investment Banking Sector (%)

ii. Indices Relating to Profitability

According to the unconsolidated financial statements

prepared in line with BRSA standards, Nurol Yatırım Bank

achieved a net profit of TRY 37mn in FY2016, almost

doubled compared to the previous year’s net profit of TRY

18.83mn. In the same period, while the Investment Banks’ net

profit figure exhibited a growth of 24.27%, the entire

sector’s net profit enlarged by 44.01%. Profit related

performance of Nurol Bank Yatırım outperformed both the

Development & Investment banking sectors and the Turkish

Banking Sectors in FY2016.

The indicators of both ROAAs and ROAEs have

outperformed the sector during the previous 3 years while

they continued to follow an upward path in line with those of

the Turkish banking sector and the Turkish development and

investment banking sector.

4.89

3.673.89

-0.30

1.99 2.212.272.43

2.282.78

1.861.521.69

2.01

2.33

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

20162015201420132012

ROAA Comparison

ROAA Nurol Yatırım Bankası A.Ş.

ROAA Turkish Devolopment and Investment Banking Sector

ROAA Turkish Banking Sector

IFRS based return on assets and equity ratios were 4.89%

and 32.99%, respectively, at the end of 2016, representing

an improvement compared to the previous year.

32.99

22.5223.23

-1.11

5.0711.069.699.34

7.818.10

16.81

13.3914.8116.6218.49

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

20162015201420132012

ROAE Comparison

ROAE Nurol Yatırım Bankası A.Ş.

ROAE Turkish Devolopment and Investment Banking Sector

ROAE Turkish Banking Sector

Regarding the IFRS-compliant consolidated financials, the

Bank reported a TRY49.85mn pre-tax profit at

FYE2016, up from the TRY21.41mn at FYE2015.

Consequently, its net profit reached to TRY 41.08mn

from previous year’s figure of TRY 16.83mn due to

income tax expense effect.

77.97%

72.16%

65.19%

66.04%

70.46%

13.30%

14.34%

19.10%

14.79%

15.50%

8.73%

13.50%

15.72%

19.17%

14.04%

0.00% 20.00% 40.00% 60.00% 80.00% 100.00%

2016

2015

2014

2013

2012

Net Interest Income / Total Income

Net Fee and Commission Income / Total Income

Other Income / Total Income

The share of Net Interest Income (NII) within the total

income structure of the Bank improved for the three

consecutive years to 77.97% in FY2016 from 72.16%

FY2015. Net Fee and Commission Income presented a

decrease by 1.04% to 13.30% in FY2016. Together, net

profit share income with other income, mainly driven by

fair value gain on investment properties, accounted for

8.73% in FY2016 (FY2015: 13.50%) of total income.

Total profit from operating activities before income tax

was TRY 77.25mn and contributed 72.51% of total

income as of FYE2016, mainly stemming from losses from

derivatives (TRY 15.77mn) and foreign exchange (TRY

13.51mn).

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 10

8.92

9.69 8.43

7.85 6.72

16.73

13.39

11.81

10.1310.23

7.82

3.70 3.38 2.28 3.51

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20162015201420132012

Interest Margin %

Interest Rate for Costly Liabilities (avg.) %

Interest Rate for Earning Assets (avg.) %

Margin %

Although the average interest income and expense rates for

the last five years exhibited a fluctuating pattern, following

FY2012, the NIM maintained its upward path during

FY2016 with contributions mainly from loans, and funds

borrowed & bond issues.

9.98

7.04

6.40

4.44

6.18

3.51

3.22 3.45 3.64 3.67

4.43

4.29 3.90 3.84 3.80

4.02

4.42

3.86

0.00

2.00

4.00

6.00

8.00

10.00

12.00

201620152014201320122011

Nurol Yatırım Bankası A.Ş.

Turkish Devolopment and Investment Banking Sector

Turkish Banking Sector

Net Interest Margin %

At the end of FY2016, the net interest margin (NIM) ratio of

the Bank clearly increased to 9.98% from 7.04% in

FYE2015 and remained above both the Turkish Banking and

the Development & Investment Banking sectors average

levels. The high and above sector average NIM ratio

specifies the bank’s effectiveness and stronger returns in

interest base incomes. The Bank’s loan books grew by

72.09% to TRY742.92mn. in FYE2015 which triggered NIM

during the period.

b. Asset Quality

As in the previous years, loans held the largest share in the

Bank’s total asset dispersion with a below the sector average

(64.14%) rate of 63.52%, despite a slight decrease

compared to the previous year’s figure of 60.28%. The

loans-weighted asset structure of Nurol Bank, despite

increasing the risk exposure, considers the efficiency of the

Bank’s financial intermediary business.

63.52%60.28%55.82%54.95%59.42%

16.52%29.69%

31.69%

18.52%5.44%

2.30%

8.05%10.01%

20.45%25.63%

17.66%1.98%2.48%6.08%

9.51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20162015201420132012

Asset Distribution %

Other Assets Securities

Banks and Other Earnings Assets Loans and Receivables

The Bank’s non-performing loans portfolio which are

transferred to an asset management company assets

amounted to TRY 9.04mn at the end of FY2016. he NPL

ratios of the Bank remained below the sector averages

for the last three years.

63.52%60.28%55.82%54.95%

59.42%

16.52%

29.69%31.69%18.52%5.44%

17.66%

1.98%2.48%6.08%9.51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20162015201420132012

Asset Distribution

Other Assets Banks and Other Earnings Assets

Loans and Receivables

Higher loan exposure provides greater advantages than

fixed rate secure instruments in growing economies. On

the other hand, when the economy slows down, increasing

NPLs rate deteriorates asset quality. Measures

implemented by the CBRT and BRSA to limit credit

growth and individual consumption and ongoing unrest in

some bordering countries add uncertainties and pull

down Turkey’s economic growth forecast. Under these

circumstances, we, as JCR Eurasia Rating, estimate an

upward trend in NPLs in the Banking Sector in 2017.

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 11

82.34%

98.02%97.52%

93.92%

90.49%

87.16%

70.00%

75.00%

80.00%

85.00%

90.00%

95.00%

100.00%

201620152014201320122011

Total Earning Assets / Total Assets (%)

The earning assets of the bank accounted for 82.34% of its

total assets, tying the asset quality directly into the quality of

the receivables of portfolio.

0.0

0

0.1

2

2.7

0

0.2

3

0.2

8

0.5

9

0.6

5

0.8

3

0.9

1

0.9

7

3.2

3

3.0

9

2.8

4

2.7

4

2.8

6

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

20162015201420132012

NPL %

Nurol Yatırım Bankası A.Ş.

Turkish Devolopment and Investment Banking Sector

Turkish Banking Sector

At the end of FY2015, the non-performing loans portfolio of

Nurol as a proportion of its equity decreased to 0.44%

(FY2014: 9.78%) – but stayed well below both the Turkish

banking sector and development & investment banking

sectors.

0.0

2

0.4

4

9.7

8

0.6

8

0.4

0 2.2

8

2.0

4

2.2

7

2.2

2

1.7

6

19.3

5

18.1

3

15.6

9

15.2

7

12.8

7

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

20162015201420132012

Impaired Loans / Equity %

Nurol Yatırım Bankası A.Ş.

Turkish Devolopment and Investment Banking Sector

Turkish Banking Sector

The doubtful receivables are covered with provisions to a

great extent, the impact on the equity is thought to be

insignificant.

c. Funding & Adequacy of Capital

As an investment bank, Nurol Bank is not entitled to collect

customer deposits and this situation directs the Bank to

alternative, new and innovative fund resources. The Bank’s

funding sources exhibited an alteration in the last two

consecutive years. The Bank’s ability to access alternative

funding sources such as funds borrowed from overseas

financial markets and bond issues increased.

Nurol Bank continued its efforts to diversify and extend

the maturity of provided funds. 44.78% of total

liabilities were driven by bond issues. In addition to the

provided long term borrowing from overseas financial

markets, the Bank has also facilitated subordinated loans

from the international financial institutions. The Bank

issued USD10mn. Eurobond as of March 31, 2016 as

subordinated debt which is accounted as Tier 2 Capital.

Additionally, Overseas Private Investment Corporation

(OPIC) provided USD10mn. loans as of December 12,

2016.

61.3675.96

50.74

77.56

49.2359.62

24.266.04

32.63

1.83

6.152.32

14.3818.0016.6420.60

44.6238.06

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

201620152014201320122011

Resource Distribution %

Equity Non-Costly Liabilities Other Borrowing Collected Fund

The Bank’s collected fund, which embraces issued debt

securities and current balances of loan customers,

accounted for 14.38% of the total fund resources. Other

borrowing consisting of bank loans formed 61.36% of

total sources.

The Bank continued issuances of TRY denominated bills

and notes and enhanced its Short-Term Schedule. In the

wake of significant FX movements, the share of foreign

currency liabilities deteriorates profitability in case of

the depreciation of the TRY. The Bank’s total deposits

was TRY 140.09mn at FYE2016 on a solo basis and

presented a growth of 253.88% YoY basis.

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 12

17.34 21.66

16.89 14.20

19.01 17.23

23.44

28.26

32.83 32.69 34.21

48.14

15.57 15.56 16.28 15.30

17.90 16.46

0.00

10.00

20.00

30.00

40.00

50.00

60.00

201620152014201320122011

CAR (%) Nurol Yatırım Bankası A.Ş.

CAR (%) Turkish Devolopment and Investment Banking Sector

CAR (%) Turkish Banking Sector

Nurol’s non-consolidated CAR decreased by 4.32% to

17.34% as of FYE2016. Though exhibiting below the Turkish

development and investment banking sector average, while

being above the Turkish banking sector average. Nurol’s

capitalization level is expected to remain relatively sufficient

as the bank is likely to sustain growth purely through

retained earnings while this indicator stood well above the

minimum CAR requirements set by the Basel Accord (8%) and

required by the Turkish regulatory authority BRSA (12%).

The weight of the core capital within the own fund structure

has continued to increase. The Bank has also remained

compliant with minimum requirements of Common Equity Tier

1 Ratio (4.5%) and Tier 1 Ratio (6%) set by the BRSA. The

Bank’s CET1 ratios was 12.12% as of FYE2016. The Bank’s

net interest margin over the sector averages and net positive

effect of possible regulatory changes and CET1 share

absorb incidental losses support sustainability.

According to the audited IFRS report, Nurol’ s Tier1 capital,

principally consisting of paid-up capital, profit and legal

reserves increased to TRY155.85mn. in FYE2016 from to TRY

125.41mn as of FYE2015, displaying sufficient capital

quality. Additionally, The Bank issued USD10mn. Eurobond

as of March 31, 2016 as subordinated debt which is

accounted as Tier 2 Capital.

69.89%

95.63%95.39%

81.19%71.41%

90.77%

30.11%

4.37%4.61%

18.81%28.59%

9.23%

0%

20%

40%

60%

80%

100%

120%

201620152014201320122011

Own Fund Structure

Core Capital Supplementary Capital

The share of core capital, principally consisting of paid-up

capital and retained earnings, accounted for 69.89% of the

Bank’s total own fund structure in FYE2016 (FYE2015:

95.63%). Above ratios specify the Bank’s lower reliance

on Tier second capital, which is not considered to be loss

absorbing.

7. Risk Profile & Management

a. Risk Management Organization & Its

Function – General Information

A separate risk management department was

established within the Bank, which reports to the Board

and is entitled to carry out risk management operations

independent of executive activities. On the other hand,

development of relevant policies and strategies and their

control are amongst the responsibilities of the Board. All

of the mechanisms related to the establishment of

standards, information flow, determination of compliance

with standards and the decision making and applications

processes are encompassed throughout the risk

management system.

All of the mechanisms related to the establishment of

standards, information flow, determination of compliance

with standards and the decision making and applications

processes are encompassed throughout the risk

management system.

The Board of Directors has the overall responsibility of

establishing and supervising the Bank’s risk management

framework. The Bank has set up Assets and Liabilities

Committee, Audit Committee, Liquidity Risk Management

Committee, Market Risk Committee, Credit Risk

Committee, Operational Risk Committee under the BoD.

Furthermore, in order to maintain a thorough and

complete risk management system, an Anti-Fraud

Monitoring Committee, Sustainability Committee, Internal

Control Unit and departments of Risk Management,

Internal Audit, Anti- Fraud Monitoring and Compliance

were also set up for further surveillance.

b. Credit Risk

The Bank's credit risk management policy is initially set

on three pillars; customer selection, credit allocation and

credit pricing for its corporate, commercial and medium

sized enterprise loan portfolio, involving statistical

methods on historical data to assess its customers based

on objective criteria and assigning grades. In this sense,

through the guides of comprehensive risk management

framework, the Bank manages its credit risk by the

allocation of loan limits for customers and customer

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 13

groups as well as the definition of limits for sectors with

considerations of maximizing risk-adjusted returns. Moreover,

concentration risk is monitored on monthly basis in terms of

industry, rating by risk group and customer.

The Bank continuously monitors customer credit assessments,

takes necessary precautions and reviews allocated limits

when necessary. In accordance with the lending policies,

collaterals such as cash, bank guarantees, mortgages,

pledges, cheques & notes and personal or corporate

guarantees are required in line with the financial position of

the debtor and its creditworthiness.

The Bank granted 93.82% of its loan book as corporates

and the remaining 5.97% was factoring loans. On the other

hand, 6% of the Bank’s non-cash loans directly or indirectly

were given to group companies.

The Bank’s (i) largest 10 cash loan customers composed

78.60% (FY2015:82.20%) of the total cash loan portfolio as

of FYE2016, (ii) largest 10 non-cash loan customers

composed 72.20% (FY2015:59.90%) of the total non-cash

loan portfolio as of FYE2016.

Customer Concentration (Cash)

2016 2015

First 10

78.60% 82.20%

First 20

95.20% 94.80%

First 50

100.0% 100.0%

Customer Concentration (Non-Cash) 2016 2015

First 10 72.0% 59.90%

First 20 91.90% 83.10%

First 50 99.80% 99.60%

The following table shows the sectorial cash and non-cash

loan book composition of the Bank in FYE2016.

Sectorial Concentration (Cash) (First-5) %

Energy 21.5

Other 17.6

Textile 16.6

Automotive 10.7

Non-Bank FI s 7.7

Sectorial Concentration (Non-Cash) (First-5) %

Banks 34.8

Energy 28.2

Infrastructure 12.3

Fuel Oil Trade 7.8

Real Estate (Investment / Rental) 3.7

Nurol Bank has exposure to concentration risk where its

business activities focus particularly on a similar type of

customers and industrial sectors in Turkey. Nurol is

constrained by customer and sector concentrations which

are applicable for most banks in Turkey and high

related party lending. Although we, as JCR Eurasia

Rating, have not assessed the individual risk level of

those companies and allocated credits, these credits are

presumed to be paid back.

The Bank’s foreign currency risk exposure complies with

BRSA regulations. The Bank’s interest rate risk is also

limited and risk arising from interest rate fluctuations is

monitored on a daily basis and managed by the asset

and liability committee.

c. Market Risk

Nurok Bank measures its market risk daily with the value

at risk (VaR) methodology, considering its trading and

available-for-sale portfolios. Regular back testing is also

conducted to test the reliability of the model. As part of

risk management activities, global and national

developments are also followed to be used in scenario

analyse for the market risk management and

determination of limits.

Additionally, The Bank performs and monitors its market

risks and takes appropriate and timely actions in

accordance with the Communiqué on Measurement and

Evaluation of Capital Adequacy of Banks. The Bank

calculates and reports general market risk, commodity

risk, currency risk, specific risk, clearing risk and

counterparty credit risk using the ‘Standard Method’, in

line with the methodology outlined in the regulations of

BRSA.

The Bank’s foreign currency risk exposure is restricted

and complies with BRSA regulations. The Bank was short

in USD and Euro long in denominated liabilities. The

Bank’s total foreign currency position to assets and

equity ratios are 6.67% and 46.39%, at the end of

FYE2016 (FYE2015: 7.50% and 41.66%, respectively).

d. Liquidity Risk

Treasury and financial institutions department manages

liquidity risk in order to take necessary measures in a

timely and accurate manner to meet its obligations even

in stressed conditions and accomplishes the regulations

regarding liquidity implemented by the BRSA. The Bank

calculates and follows up the liquidity risk, cash flows,

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 14

gap analyses, stress tests and scenario analyses which are

periodically reported by the Risk Management Department

to the Senior Management and Audit Committee.

In addition to the requirement of legal liquidity ratios, by the

Assets and Liabilities Committee (ALCO) sets internal liquidity

ratios such as liquid assets to total assets and liquid assets to

portfolio of issued bank bonds. Risk management unit closely

monitors the liquidity conditions under the pre-determined

limits.

In overcoming the liquidity risk considering short and long

term liquidity requirements, the Bank has been in an effort to

develop alternative funding channels and to diversify its

funding sources through instruments such as bond issuances,

local and foreign borrowings.

The Bank's liquidity ratios in FYE2016 and FYE2015 are as

follows,

Period (Avg.)

First maturity bracket (weekly)

Second maturity bracket (monthly)

FC (%) Total (%) FC (%) Total (%)

2016 176 238 106 137

2015 302 262 108 137

Accordingly, the Bank’s liquidity ratios were above the

requirement levels and remained compliant with BRSA

parameters in 2016. On the other hand, according to the

decision of BRSA dated 24 December 2015 and number of

6613;

The Development and Investment Banks will;

- Maintain for calculating and reporting liquidity ratios as

per the framework of the ‘Communiqué on Measurement and

Evaluation of Liquidity Adequacy of Banks’ weekly and

monthly liquidity ratios on a bank-only basis for foreign

currency assets/liabilities and total assets/liabilities should

stand at a minimum of 80% and 100%, respectively.

- Calculate liquidity coverage ratios as zero up to FYE2017.

8. Budget & Debt Issue

The estimated budget projection between the years of

FYE2017 and FYE2018 submitted by Nurol Bank. The Bank

recorded growths of 63.31% and 70.53% in asset and

liabilities respectively in FY2016 and surpassed the

previously projected growth of 38.85% and 45.13%

respectively in those fields. Additionally, realized figures in

equity and net profit of -30.47% and 96.56% respectively

in FYE2016 were remarkably stayed above the

projected figures.

According to the base scenario developed by the Nurol

Bank Management, some of the planned topics are

shown in the graphs below;

58.18 26.51 48.61 80.39

135.35 140.32

---- 34.94

-51.57

240.03281.36

522.82583.48

20.66

-99.56

357.66 404.87

760.92

855.81

----200

0

200

400

600

800

1,000

2012 2013 2014 2015 2016 2017

Cumulative Equity Growth Rate %

Cumulative Asset Growth Rate %

Cumulative Liability Growth Rate %

Within the framework of projections and budgeting

activities in FY2017, the Bank projected growths of

9.74%, 2.11% and 11.02% in asset, liabilities and

equity respectively.

31,5

38

64

,643

88,6

54

150,

113

127,

592

17,6

42

34,6

14

49

,384

85

,532

72,4

88

-1,0

36

20,7

69

24

,809

46,3

06

24,1

84

-55

1

16,4

15

18,8

26

37

,00

4

19,3

47

-20,000

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2013 2014 2015 2016 2017e

Interest Income Interest Expenses Pre tax Profit Net Profit

In addition, the Bank projected a 2017 year-end interest

income and net profit sizes of TRY127.59mn. and

TRY19.35mn., respectively.

[BANKING]

Nurol Yatırım Bankası Anonim Şirketi 15

FYE FYE FYE FYE FYE FYE FYE FYE As % of As % of As % of FYE FYE FYE

Nurol Yatırım Bankası A.Ş. 2016 2016 2016 2015 2015 2014 2014 2013 2016 2015 2014 2016 2015 2014

BALANCE SHEET - ASSET USD TRY TRY TRY TRY TRY TRY TRY Assets Assets Assets Growth Growth Growth

(000) (Converted) (Original) (Average) (Original) (Average) (Original) (Average) (Original) (Original) (Original) (Original) Rate % Rate % Rate %

A- TOTAL EARNING ASSETS ( I+II+III ) 321,434 962,984 832,484 701,984 662,331 622,677 517,452 412,226 82.34 98.02 97.52 37.18 12.74 51.05

I- LOANS AND LEASING RECEIVABLES (net) 247,978 742,918 587,315 431,711 394,084 356,456 298,823 241,190 63.52 60.28 55.82 72.09 21.11 47.79

a) Short Term Loans 78,715 235,822 236,532 237,241 193,863 150,484 157,403 164,321 20.16 33.13 23.57 -0.60 57.65 -8.42

b) Lease Assets 0 0 4,396 8,792 10,564 12,336 14,965 17,594 n.a 1.23 1.93 -100.00 -28.73 -29.89

c) Medium & Long Term Loans 169,053 506,467 344,574 182,681 181,966 181,250 118,166 55,082 43.30 25.51 28.39 177.24 0.79 229.05

d) Over Due Loans 9 28 284 540 7,419 14,298 7,427 556 0.00 0.08 2.24 -94.81 -96.22 2,471.58

e) Others 0 0 0 0 0 0 2,014 4,027 n.a n.a n.a n.a n.a -100.00

f) Receivable from Customer due to Brokerage Activities 2,146 6,430 6,099 5,768 2,884 0 0 0 0.55 0.81 n.a 11.48 n.a n.a

g) Allowance for Loan and Receivables Losses (-) -1,946 -5,829 -4,570 -3,311 -2,612 -1,912 -1,151 -390 -0.50 -0.46 -0.30 76.05 73.17 390.26

II- OTHER EARNING ASSETS 64,475 193,161 202,901 212,640 207,485 202,330 141,804 81,277 16.52 29.69 31.69 -9.16 5.10 148.94

a) Balance With Banks -Time Deposits 31,223 93,541 100,073 106,604 107,907 109,210 84,012 58,814 8.00 14.89 17.10 -12.25 -2.39 85.69

b) Money Market Placements 14,172 42,459 52,406 62,353 73,703 85,053 52,033 19,012 3.63 8.71 13.32 -31.91 -26.69 347.36

c) Reserve Deposits at CB (*) 19,080 57,161 50,412 43,663 25,640 7,616 3,808 0 4.89 6.10 1.19 30.91 473.31 n.a