Tuesday Jan. 31, - Bloomberg.com · according to the S&P/LSTA US Leveraged Loan 100 Index....

13

Tuesday Jan. 31, 2017 Jan. 31, 2017 Must Reads Paragon Litigation: Offshore will try again after a judge tossed out its previous restructuring . plan Relative Value: Cemex got a lift from Trump's border wall talk, but it may not offer the best among peers. value Q&A: Wells Fargo's George sees a yield advantage Bory in short-term junk debt and likes energy companies. By Eliza Ronalds-Hannon Oppenheimer Funds is loading up on loans to soften potential blows from future interest rate hikes by the Federal Reserve and the Trump administration’s fiscal stimulus plans. Since the November election, the $200 billion asset manager has bought as many corporate bank loans as possible, including boosting the allocation in its flagship Global Strategic Income Fund to an unprecedented 12 percent, Chief Investment Officer said. Krishna Memani “Loans are probably going to be best performing asset class this year, perhaps by a wide margin,” Memani said by phone from his office in lower Manhattan, adding that he expects the sector to return around 5 percent this year. “Wherever we have the flexibility to do so, we have allocated into loans.” The debt gained 10.9 percent in 2016, after losing close to 3 percent the year before, according to the S&P/LSTA US Leveraged Loan 100 Index. Oppenheimer Turns to Leveraged Loans to Hedge Fed Loans carry less credit risk than bonds because they’re senior in a company’s capital structure. This is part of what appeals to Memani, who believes markets are underestimating the financial risks of the Trump era. “More contradictions are manifesting themselves every day in terms of what the policy objectives are,” Memani said. “The risks are rising.” As an example, Memani pointed to Trump’s fiscal spending plans and how they contrast with the hawkishness of his nominee for budget chief, Representative Mick Mulvaney, whowants to rein in deficits. The prospect of increased infrastructure expenditures helped inspire the so-called “animal spirits” that have buoyed risk assets since election day. Junk bond spreads narrowed and the Dow Jones Industrial Average reached fresh highs before Trump even took office. Much of what Memani appreciates about loans comes down to duration. The average life of a corporate bank loan is usually around three years due to issuers’ use of call options. But it has shortened further recently as companies embark on repricing sprees. Memani acknowledges the repricing risk in loans, but contends it’s minor compared to how much value bonds can lose as interest rates climb. Loans may have limited upside, but to Memani their limited downside is what matters most this year. Editor's note: Feb. 7 will be the last issue of Leveraged Capital & Distress Brief. We will start publishing a new Credit & Rates Strategy Brief on Feb. 14. Click for here more resources on terminal. "High yield out to five years has a nice yield advantage." – George , head of credit strategy at Bory Wells Fargo Securities Quote of the Week > meeting Jan. 31: Navistar, on $1.03b TLB > Jan. 31: ABC Supply, commitments due on $1.875b 1L TL > Feb. 6: Metinvest, creditors vote on restructuring plan For calendar items click here What to Watch Distressed Bond Monitor The Week In Leveraged Capital & Distress Source: Bloomberg Avaya's 7 percent bond due April 2019 was the most traded in U.S. distressed debt last week, according to Jan. 30 data. Figures are for average daily volume. Bond Demand Pushes Yields Below Loans

Transcript of Tuesday Jan. 31, - Bloomberg.com · according to the S&P/LSTA US Leveraged Loan 100 Index....

Tuesday

Jan. 31, 2017

Jan. 31, 2017

Must Reads Paragon Litigation:

Offshore will try again after a judge tossed out its previous restructuring .plan

Relative Value: Cemex got a lift from Trump's border wall talk, but it may not offer the best among peers.value

Q&A: Wells Fargo's George sees a yield advantage Bory

in short-term junk debt and likes energy companies.

By Eliza Ronalds-HannonOppenheimer Funds is loading up on loans to soften potential blows from future interest rate hikes by the Federal Reserve and the Trump administration’s fiscal stimulus plans.

Since the November election, the $200 billion asset manager has bought as many corporate bank loans as possible, including boosting the allocation in its flagship Global Strategic Income Fund to an unprecedented 12 percent, Chief Investment Officer

said.Krishna Memani“Loans are probably going to be best performing asset class this year, perhaps by a

wide margin,” Memani said by phone from his office in lower Manhattan, adding that he expects the sector to return around 5 percent this year. “Wherever we have the flexibility to do so, we have allocated into loans.”

The debt gained 10.9 percent in 2016, after losing close to 3 percent the year before, according to the S&P/LSTA US Leveraged Loan 100 Index.

Oppenheimer Turns to Leveraged Loans to Hedge Fed

Loans carry less credit risk than bonds because they’re senior in a company’s capital structure. This is part of what appeals to Memani, who believes markets are underestimating the financial risks of the Trump era.

“More contradictions are manifesting themselves every day in terms of what the policy objectives are,” Memani said. “The risks are rising.”

As an example, Memani pointed to Trump’s fiscal spending plans and how they contrast with the hawkishness of his nominee for budget chief, Representative Mick Mulvaney, whowants to rein in deficits. The prospect of increased infrastructure expenditures helped inspire the so-called “animal spirits” that have buoyed risk assets since election day. Junk bond spreads narrowed and the Dow Jones Industrial Average reached fresh highs before Trump even took office.

Much of what Memani appreciates about loans comes down to duration. The average life of a corporate bank loan is usually around three years due to issuers’ use of call options. But it has shortened further recently as companies embark on repricing sprees.

Memani acknowledges the repricing risk in loans, but contends it’s minor compared to how much value bonds can lose as interest rates climb. Loans may have limited upside, but to Memani their limited downside is what matters most this year.

Editor's note: Feb. 7 will be the last issueof Leveraged Capital & Distress Brief. Wewill start publishing a new Credit & Rates Strategy Brief on Feb. 14. Click for heremore resources on terminal.

"High yield out to five years has a nice yield advantage."

– George , head of credit strategy at Bory

Wells Fargo Securities

Quote of the Week

> meeting Jan. 31: Navistar,on $1.03b TLB > Jan. 31: ABC Supply,commitments due on $1.875b 1L TL > Feb. 6: Metinvest, creditors vote on restructuring plan

For calendar items click here

What to Watch

Distressed Bond Monitor

The Week In Leveraged Capital & Distress

Source: Bloomberg

Avaya's 7 percent bond due April 2019 was the most traded in U.S. distressed debt last week, according to Jan. 30 data. Figures are for average daily volume.

Bond Demand Pushes Yields Below Loans

Leveraged Capital & Distress 2 Jan. 31, 2017

The Week In Leveraged Capital & Distress

Two companies that may face a future restructuring, and have hired Rothschild to help advise them on options. Gymboree Rue21,'s debt leverage may remain far above that of peers even after the purchase of a clothing maker, according to Moody's. Nine West

's shares soared after the company said it wants to avoid a court-led bankruptcy.Takata

News

A group of ’s lenders hired Gymboree to advise them as the Rothschild Inc.

retailer faces a potential restructuring of its $1 billion debt this year, a person familiar said.Full on terminalstory

Peabody Energy will exit bankruptcy on its own terms after facing down a rival plan in a battle among sophisticated distressed-debt investors who seek to benefit from the recent rise in coal prices.

Full on terminalstory

Billionaire Tom Gores' Platinum Equityis selling $600 million of payment-in-kind toggle notes tied to a takeover it Vertiv,completed in November.

on terminalFull story

hired to help tame its Rue21 Rothschild nearly $1 billion debt load, people familiar said.Full on webstory

Toisa’s diversified shipping business andaggressive cost-cutting weren’t enough tostave off the effect of declining oil prices, the company said in a bankruptcy filing Sunday.

on terminalFull story

Elliott Management is proposing an injection of as much as 9 billion reais ($2.9 billion) into to restructure its Oi SAdebt and pull it out of bankruptcy protection, people familiar said.Full on terminalstory

Nine West Holdings's purchase of a women’s clothing maker could still leave its debt level far above that of peers at 18 times adjusted earnings, Moody’s Investors Service said.

on terminalFull story

A group of shareholders Linn Energyobjected to the driller’s reorganization plan, arguing that oil and natural gas assets should be revalued now that fuel prices have recovered.Full on terminalstory

Takata's stock surged in Tokyo trading after the air-bag maker reiterated it wants to avoid a court-led bankruptcy that could disrupt the supply of its parts.Full on terminalstory

Brunswick Rail bondholders, who are competing to buy the troubled railcar lessor, said a rival offer could put the company at further risk.Full on web/terminalstory

KKR took command of a deal to reprice ’s Ultimate Fighting Championship

buyout loan from banks after regulators reprimanded the lenders for flouting risk guidelines on the original deal.

Full on webstory

Ineos said it will repay all term loans due 2018, for approximately $1.315 billion, with cash on hand. It will also convert term loans due 2020 and 2022, totaling about 1.935 billion euros and $1.49 billion to new tranches of term loans due 2022 at lower rates. The company also announced a bond refinancing.

on terminalFull story

China Railway Materials’ recent debt restructuring may foreshadow further cuts in interest payments by defaulted borrowers.Full on story terminal

Shipping companies are rushing to the Norwegian junk bond market with new deals after a rally all but erased the market’s pummeling since 2014.Full onstory terminal

Crude prices have doubled but offshore oil service companies are still in for a lot of pain, according to Scandinavia’s largest bank.Full on story terminal

“Euro fast fashion” has taken the U.S. by storm and distressed specialty apparel retailers are among the biggest casualties.Full on webstory

JPMorgan banker is Ray Doodyplanning to join in a senior HSBC position in the bank’s leveraged finance team.

on terminalFull story

U.K. High Yield

Tempur Bonds Deflate

Source: Bloomberg

Tempur Sealy International's bond yields surged after the mattress maker lost a key contract. Data are through Jan. 30.

China Defaults Soar

Source: Bloomberg

Leveraged Capital & Distress 3 Jan. 31, 2017

U.K. High Yield

By Marianna Aragao and Edith FishtaDeteriorating credit outlooks for two U.K. retailers serving different ends of the wealth spectrum show that investors may drive a hard bargain when those companies next tap the debt market.

First, downgraded value clothing chain to CCC, citing the likelihood the S&P Matalancompany, which has cut earnings guidance, will buy back debt at below face value in the secondary market, amounting to a "selective default."

Then Moody’s Investors Service changed its outlook on upmarket department store group to negative from stable, highlighting mounting challenges to its House of Fraserbottom line such as fragile consumer confidence.

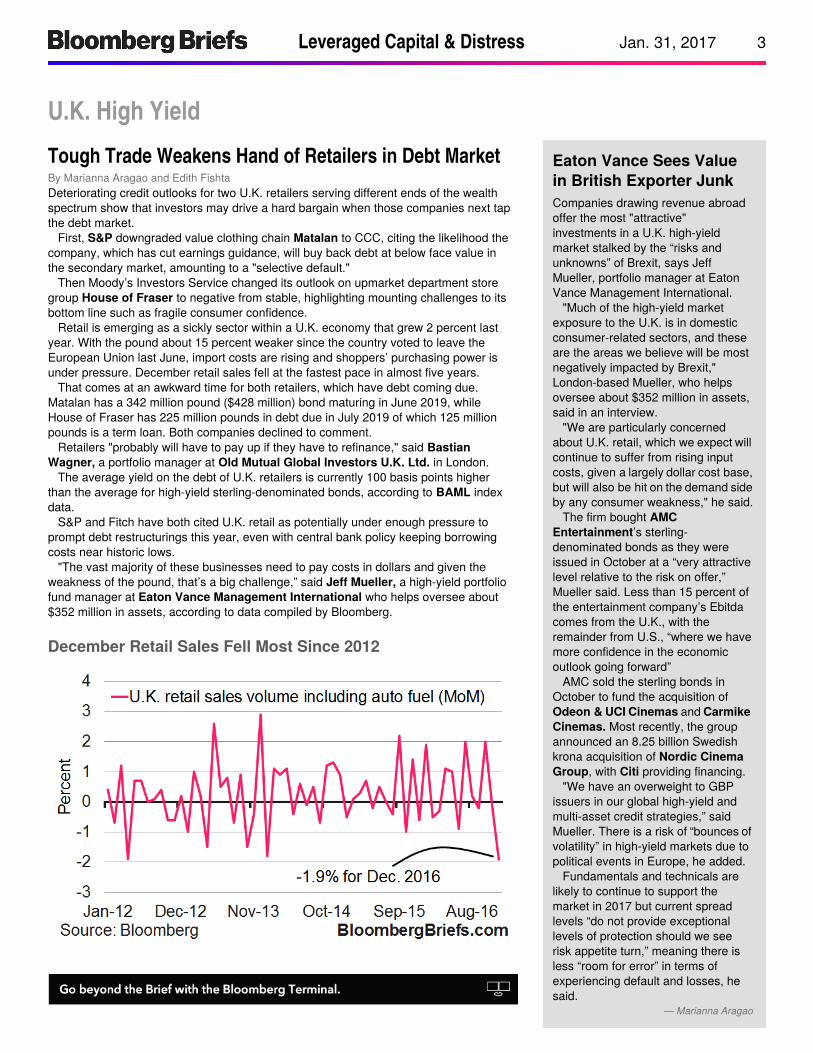

Retail is emerging as a sickly sector within a U.K. economy that grew 2 percent last year. With the pound about 15 percent weaker since the country voted to leave the European Union last June, import costs are rising and shoppers’ purchasing power is under pressure. December retail sales fell at the fastest pace in almost five years.

Tough Trade Weakens Hand of Retailers in Debt Market

That comes at an awkward time for both retailers, which have debt coming due. Matalan has a 342 million pound ($428 million) bond maturing in June 2019, while House of Fraser has 225 million pounds in debt due in July 2019 of which 125 million pounds is a term loan. Both companies declined to comment.

Retailers "probably will have to pay up if they have to refinance," said Bastian a portfolio manager at in London.Wagner, Old Mutual Global Investors U.K. Ltd.

The average yield on the debt of U.K. retailers is currently 100 basis points higher than the average for high-yield sterling-denominated bonds, according to index BAMLdata.

S&P and Fitch have both cited U.K. retail as potentially under enough pressure to prompt debt restructurings this year, even with central bank policy keeping borrowing costs near historic lows.

"The vast majority of these businesses need to pay costs in dollars and given the weakness of the pound, that’s a big challenge,” said a high-yield portfolio Jeff Mueller, fund manager at who helps oversee about Eaton Vance Management International$352 million in assets, according to data compiled by Bloomberg.

Companies drawing revenue abroad offer the most "attractive" investments in a U.K. high-yield market stalked by the “risks and unknowns” of Brexit, says Jeff Mueller, portfolio manager at Eaton Vance Management International.

"Much of the high-yield market exposure to the U.K. is in domestic consumer-related sectors, and these are the areas we believe will be most negatively impacted by Brexit," London-based Mueller, who helps oversee about $352 million in assets, said in an interview.

"We are particularly concerned about U.K. retail, which we expect willcontinue to suffer from rising input costs, given a largely dollar cost base,but will also be hit on the demand sideby any consumer weakness," he said.

The firm bought AMC ’s sterling-Entertainment

denominated bonds as they were issued in October at a “very attractive level relative to the risk on offer,” Mueller said. Less than 15 percent of the entertainment company’s Ebitda comes from the U.K., with the remainder from U.S., “where we have more confidence in the economic outlook going forward”

AMC sold the sterling bonds in October to fund the acquisition of

andOdeon & UCI Cinemas CarmikeMost recently, the group Cinemas.

announced an 8.25 billion Swedish krona acquisition of Nordic Cinema

, with providing financing.Group Citi "We have an overweight to GBP

issuers in our global high-yield and multi-asset credit strategies,” said Mueller. There is a risk of “bounces ofvolatility” in high-yield markets due to political events in Europe, he added.

Fundamentals and technicals are likely to continue to support the market in 2017 but current spread levels “do not provide exceptional levels of protection should we see risk appetite turn,” meaning there is less “room for error” in terms of experiencing default and losses, he said.

— Marianna Aragao

Eaton Vance Sees Value in British Exporter Junk

Relative Value

December Retail Sales Fell Most Since 2012

Leveraged Capital & Distress 4 Jan. 31, 2017

Relative Value

Trump Put Cemex in Spotlight, But Some Peers May Offer Higher YieldsBy Richard BedardPresident Donald Trump's plans to build a wall along the U.S. border with Mexico are giving a boost to builders and materials suppliers. Mexico's may be poised to profit; its shares Cemexrose 7.5 percent in the two days through Jan. 25.

But is it too late for a bond investor to jump onto the Cemex bandwagon? How does the debt stack up against its peers?

We looked at 56 bonds in the materials industry in the Bloomberg Barclays Global High Yield Index, including more than half a dozen from Cemex, that all have the same B+ rating from . Cemex bonds, shown in orange on the chart below, S&Ptrade on the relatively rich side of the second-order polynomial trend line calculated by Microsoft Excel, Bloomberg data show.

The bonds that seem to trade richest, shown in pink, include a 4 percent security due 2023 that has an Crown Americas

option-adjusted spread of 195 basis points. Compare that with 's 7.5 percent bond due in 2021 with a Century Aluminum

spread of 529 basis points.

Cemex: At a Glance

The builder's fourth-quarter profit is expected to rise 72 percent based on consensus when it reports 2016 earnings next month, Bloomberg Intelligence reported.

Its U.S. shares rose 50 percent last year and were up 16 percent this year through Jan. 30.

The cement maker, which is the largest in the Americas, plans to sell $1.5 billion to $2.5 billion of assets by 2019.

Last year, Cemex made $630 million of divestments and agreed to sell $700 million of its U.S. assets to Cementos Chihuahhua and Eagle Materials, according to BI.

The U.S. and Mexico account for half of Cemex sales, while Europe is 24 percent, BI data shows.

Cemex's operating Ebitda rose 22 percent in the first nine months of 2016.

For more Cemex analysis, click .here— Richard Bedard

Q&A

Some Cemex Bonds Appear to Trade Rich Compared to Global Peers

All values are as of Jan. 27. Bubbles represent bonds in the materials sector of the Bloomberg Barclays Global High Yield Index rated B+ by S&P. Size corresponds to amount outstanding. Cemex bonds are marked in orange. Bonds in pink appear to be trading rich relative to the trend line, while bonds colored green appear cheapest in relative terms. All other bonds are marked blue.

Leveraged Capital & Distress 5 Jan. 31, 2017

Q&A

Tech, Energy, Metals and Mining Offer Attractive Value, Says Wells Fargo's Bory

Credit spreads will probably tighten; high-yield bonds up to five-year maturity have "yield advantage."

Overweight parts of energy; high-tech sector is deleveraging, particularly at low end of rating spectrum.

Biggest risk is political. Removing interest deductibility would put highly levered companies at a disadvantage.

Interviewed by Claire Boston on Jan. 20 and 27. Comments have been edited and condensed for clarity.

George Bory, head of credit strategy, Wells Fargo Securities

Q: What's your U.S. and global macro outlook?A: We have 2.2 percent U.S. growth penciled in for this year. That doesn't include any benefit from potential stimulus or fiscal policy changes. Globally, we expect around 3 percent with modest improvements in most developed countries.

Q: How many times will the Fed raise rates this year?A: We're in the two-to-three-times camp. Pro-cyclical fiscal policies late in the economic cycle likely come with tighter monetary policy.

Q: Where are the opportunities in credit in the next six to nine months?A: Credit spreads have a good chance of modestly tightening this year. Our message to credit investors is try and focus on spread compression and closely manage interest-rate volatility. To capture total returns, our favorite spot is short-end high yield. High yield out to five years has a nice yield advantage. Credit quality is improving as default rates come down, and there's not a lot of funding requirements by a large number of high-yield issuers. For excess returns, we like the long end of investment-grade credit curves, setting up for what we'd call credit-spread flattening along the curve.

As it relates to sectors, we have a cyclical bias. We're overweight parts of energy in both investment grade and high yield. We like some metals and materials names in investment grade. High tech is showing some nice deleveraging trends and some meaningful improvements at the low end of the spectrum, with CCCs and the like.

Q: What are the biggest themes to watch in high-yield?A: There's two factors. Last year, high-yield was almost a one-sector trade: Energy and everything else. This year, yields are much more compressed with a lot less differentiation. Our expectation is that dispersion at the sector level increases because energy is now pricing like everything else. Thesis number two is the migration of default trends. Improvement across the commodity complex means defaults are going to drop dramatically this year across those sectors. On the flip side, you have sectors like consumer discretionary, some of the retail names, and in particular health care, that are notably at risk.

Q: How do you view CCC rated bonds?A: Generally, if capital markets stay open, CCCs should hold up OK. Parts of CCCs like energy, technology and some industrials are doing OK. We've got some companies migrating into CCCs, like retail and health care. We're not terribly enthusiastic about either of those two sectors.

Q: Are energy companies out of the woods?

Energy's pretty complicated and A:segmented. The MLPs, the pipelines are low BBB rated credits that have a lot of leverage, but very predictable cash flows.Those are not that risky, and we like those

trades. In high yield, E&P operators who are doing well at $45-$55 a barrel, those are good trades. Then you have the servicers. Some parts are doing OK, and others are more vulnerable.

Q: What are the biggest risks right now?A: Unequivocally, the biggest risk is political. The agenda being proposed in Congress, much of it would be quite good in the sense that lower taxes, less regulation and more favorable trade termsare pretty good for corporate America. Butnot every company is a winner. It would really rescript the rules. One example is interest deductibility: It's been proposed as something to eliminate. The balance sheet of corporate America is built on the assumption that there's a tax shield for the interest cost of borrowed debt. If you remove that, a lot of highly levered companies are at a distinct disadvantage.

Q: Where are you the most contrarian?A: There's sort of a deeply embedded view that the economy in Europe is weak and not going to recover. We see signs of recovery. The non-consensus view right now would be to invest in European credit in the front-end of the curve and swap it back to U.S. dollars. The swap rate itself is worth about 60 basis points. That's because a lot of Europeans want to invest in the U.S. so they're selling euros, buying dollars.

At a Glance

Education: Siena College, bachelor's degree in economicsCareer: Wells Fargo, UBS, J.P. Morgan Fleming Investment Management

The NewsroomRecommended TV show:Favorite vacation spot: Block Island, Rhode Island

Markets

Leveraged Capital & Distress 6 Jan. 31, 2017

Markets

Navient, Avaya Among Biggest Distressed MoversNavient was the worst performer in the CDS market with a 21.5 percent increase in

spread in the week through Jan. 30. cut the company to BB- from BB while S&P sentiment on the company, measured by using a proprietary Bloomberg algorithm, fell to minus 0.86, where minus 1 is most negative.

Tempur Sealy International's bond due in 2023 was among the leading high-yield decliners in the through Jan. 30. The mattress manufacturer's share price fell the weekmost in four and a half years on Jan. 30 after it said contracts for all product lines were being terminated with retailer Mattress Firm Holdings.

Two first-lien loans from saw some of the biggest price drops in the week Avaya through Jan. 30, according to Bloomberg data. As sues Avaya for alleged BlackBerry patent infringement, a bankruptcy filing from the struggling business communications provider disclosed total assets at $5.5 billion and total debt at almost $6.4 billion.

— Dana Pardini

Downgrade Watch

Navient Risk Rises

Bonds: Jack Cooper Declined the Most

Source: Bloomberg, Trace

Loans: Total Safety Term Loan Saw Biggest Price Drop for Second Week

Source: BVAL Notes (both lists):Rankings are based on percentage price decline over the week to Jan. 30. Avg. daily volume is for latest week and represents amount of trading in currency of issuance.White circle on trend lines is the last price. Purple diamond is the 20-day moving average. Line endpoints represent the low and high for the last four weeks.

Leveraged Capital & Distress 7 Jan. 31, 2017

Downgrade Watch

S&P Reduces Rue21 Due to Potential Restructuring, Cuts Navient on Litigation RiskBy Richard Bedard

S&P downgraded retailer to CCC- from CCC, citing "weakened liquidity expectations" and concern that the company will Rue21undergo a restructuring in the next six months.

S&P cut its ratings on to BB- from BB on rising litigation risk and a large amount of unsecured debt maturing in 2018-2020. NavientThe Consumer Financial Protection Bureau is suing Navient over its servicing of student loans.

COMPANY CUT TO FROM AGENCY DATE RATING TYPE

Rue21 CCC- CCC S&P 1/30/17 LT Local Issuer Credit, Foreign Issuer Credit

Teamviewer B B+ S&P 1/30/17 LT Local Issuer Credit, Foreign Issuer Credit

Velocity Pooling Vehicle CCC CCC+ S&P 1/30/17 LT Local Issuer Credit, Foreign Issuer Credit

GameStop BB BB+ S&P 1/27/17 LT Local Issuer Credit, Foreign Issuer Credit

Appvion Caa1 B2 Moody's 1/26/17 LT Corp Family Rating

Interface Security Systems Holdings CCC CCC+ S&P 1/26/17 LT Foreign Issuer Credit, Local Issuer Credit

Talos Energy CCC+ B- S&P 1/26/17 LT Foreign Issuer Credit, Local Issuer Credit

WD Wolverine Holdings Caa1 B3 Moody's 1/26/17 LT Corp Family Rating

Infor B- B S&P 1/25/17 LT Foreign Issuer Credit, Local Issuer Credit

Navient BB- BB S&P 1/25/17 LT Local Issuer Credit, Foreign Issuer Credit

Nielsen Holdings BB+ BB+ S&P 1/25/17 LT Foreign Issuer Credit, Local Issuer Credit

Novartex CC CCC S&P 1/25/17 LT Local Issuer Credit, Foreign Issuer Credit

Sears Roebuck Acceptance C CC Fitch 1/25/17 Senior Unsecured Debt Source: Bloomberg RATC <GO>

Note: Table shows selection of downgrades for sub-investment grade companies in the Jan. 24-Jan. 30 period.

Sentiment Monitor

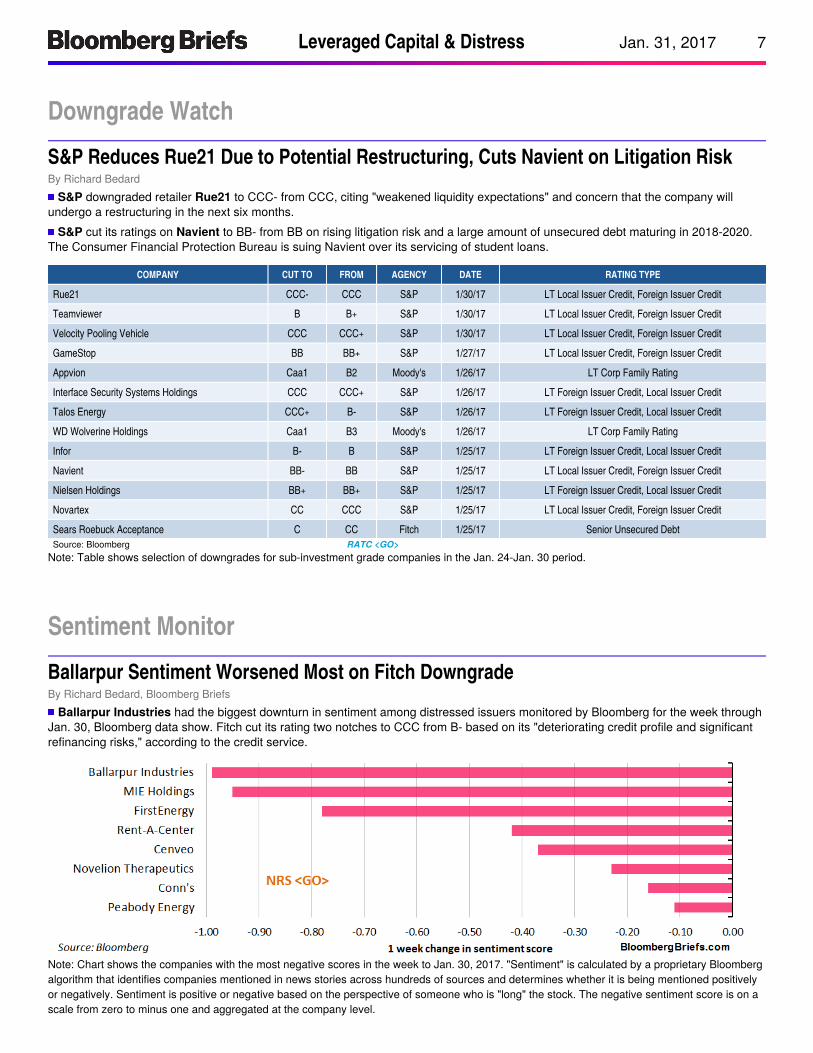

Ballarpur Sentiment Worsened Most on Fitch DowngradeBy Richard Bedard, Bloomberg Briefs

Ballarpur Industries had the biggest downturn in sentiment among distressed issuers monitored by Bloomberg for the week through Jan. 30, Bloomberg data show. Fitch cut its rating two notches to CCC from B- based on its "deteriorating credit profile and significant refinancing risks," according to the credit service.

Litigation Watch

Note: Chart shows the companies with the most negative scores in the week to Jan. 30, 2017. "Sentiment" is calculated by a proprietary Bloomberg algorithm that identifies companies mentioned in news stories across hundreds of sources and determines whether it is being mentioned positively or negatively. Sentiment is positive or negative based on the perspective of someone who is "long" the stock. The negative sentiment score is on a scale from zero to minus one and aggregated at the company level.

Leveraged Capital & Distress 8 Jan. 31, 2017

Litigation Watch

Paragon Offshore to File New Chapter 11 Plan After Judge Rejects Prior ProposalBy Julia Winters, Bloomberg Intelligence Litigation Analyst

Paragon Offshore has come up with a new strategy to exit Chapter 11 after a judge rejected terms of its previous proposal.

Paragon Offshore Paragon announced a new Chapter 11 exit strategy after Bankruptcy Judge Christopher Sontchi denied confirmation of its plan to reinstate term loan lenders and swap bondholders' debt for $285 million in cash and 47% new equity. The new deal would give secured lenders, including the term loans, $421 million in cash, $85 million in new debt and 58% of new equity. Unsecured bondholders would receive $50 million cash and 42% equity, a large reduction from their proposed recoveries under the rejected plan.Next key event: Filing of amended plan, likely by Feb. 14

$2.47 BillionASSETS: $2.96 BillionLIABILITIES:

Paragon Offshore Plc and 25 SubsidiariesDEBTORS: AMOUNT OWED: Revolving Credit Facility / $708 MillionSecured Term Loan / $640 Million6.75% Senior Notes Due 2022 / $457 Million7.25% Senior Notes Due 2024 / $527 MillionMORE: Click here

Europe Loan Pipeline

Leveraged Capital & Distress 9 Jan. 31, 2017

Borrower UOP Type Size (m) RankTenor (yrs)

Talk FlexCov-Lite

Call Lead(s) Commits

Keter ACQ TLB €300 1L 6E+425, 1%, 97.75-

98- - - BNP/JPM/RBC/UBS

1/31/2017

Corialis LBO TL €355 1L 7E+375-400, 0%,

PARDown Y

101(6M)

BNP/CS/DB/RABO/UBS 2/1/2017

TL £128 1L 7 L+500, 0%, 99.5 - Y101(6M)

BNP/CS/DB/RABO/UBS 2/1/2017

REV €125 1L 6 E+400, 0% - - - BNP/CS/DB/RABO/UBS 2/1/2017

Cooper REFI TLB 598 1L 6E+375-400, 0%,

PAR- Y - MS/NOM 2/2/2017

Morrison Utility Services

ACQ TLB £93 1L 6.5 L+550, 0% - N - BOI/HSBC/SG 2/2/2017

Xella LBO TLB €1,400 1L 7E+400-425, 0%,

99.75Down Y -

BARC/BNP/CA/CS/DB/GS/JEFF/MS/UNI

2/2/2017

REV €175 1L 6.5 - - - -BARC/BNP/CA/CS/DB/GS/JEFF/MS

/UNI2/2/2017

B&B Hotels REFI TLB €379 1L 6E+450, 0%, 99.75-

100- -

101(6M)

BNP/CA/CS/NAT/SG 2/3/2017

CAPEX €40 1L 5 E+375, 0% - - - BNP/CA/CS/NAT/SG 2/3/2017

REV €70 1L 5 E+375, 0% - - - BNP/CA/CS/NAT/SG 2/3/2017

Parkdean LBO TL £575 1L 7 L+500, 0%, 99-99.5 - N - BARC/BAML/JPM/RBC/SMBC 2/8/2017

Ferro REFI TLB €230 1L 7E+275-300, 0%,

99.5- Y

101(6M)

BAML/DB/HSBC/PNC 2/9/2017

Concardis LBO TL € - 1L - - - - - GS/HSBC/MS -

Lumileds LBO TL $/€ - 1L - - - - - BNP/CS/DB/ING/RABO -

Micro Focus ACQ TL €950 1L - - - - - BARC/HSBC/JPM/RBS -

Profi Rom Food LBO TLARON 311

1L 6 R+300 - - - CITI/ERSTE/ING/RBI/UNI -

TLBRON 799

1L 7 R+350 - - - CITI/ERSTE/ING/RBI/UNI -

CAPEXRON 220

1L 6 R+300 - - - CITI/ERSTE/ING/RBI/UNI -

REV RON 50 1L 6 R+300 - - - CITI/ERSTE/ING/RBI/UNI -

TeamViewer REFI TL €155 1L 7 - - Y - BAML -Source: Bloomberg

Europe Loan Pipeline

Keter, Corialis Loan Commitments Are DueBy Galina Shurova, Bloomberg Data

> Commitments are due Jan. 31 on a term loan for and the following day for , Bloomberg data show. Following Keter Corialisare details of European loans with commitments due. For more information on the Bloomberg terminal, click .here

This table was compiled by a Bloomberg LP employee involved with sales support and was edited by the News Department. To suggest ideas or provide

feedback, contact the editor Richard Bedard at [email protected] or +212 617 3590

U.S. Loan Pipeline

Leveraged Capital & Distress 10 Jan. 31, 2017

U.S. Loan Pipeline

Ascensus, American Builders Have Commitments Due This WeekBy Marcus Lefkandinos, Bloomberg Data

Borrower UOP Type Size (m) Rank Tenor (yrs) Talk Cov-Lite Call Ratings Lead Commits

Ascensus REFI TL $421 1L 5.75 L+400, 1%, 100 - 101(6M) -/- CS 1/31/2017

American Builders REFI TL $1875 1L 6.75 L+225, 0.75%, 100 Y 101(6M) -/- DB 1/31/2017

Booz Allen REFI TLB $399 1L 6.5 L+225, 0%, 100 Y 101(6M) -/- BAML 1/31/2017

Infor REFI TL $2400 1L 5 L+275, 1%, 99.5-99.75 Y 101(6M) -/- BAML 1/31/2017

Power Products LBO REV $30 1L - - - - B/B1 RBC 1/31/2017

TL $270 1L - L+450, 1%, 99 - - B/B1 RBC 1/31/2017

TL $92.5 2L - - - - -/- RBC 1/31/2017

Worldwide Express LBO REV $60 1L - - - - B/B1 Antares 1/31/2017

TL $360 1L 7 L+475, 1%, 99 - 101(6M) B/B1 Antares 1/31/2017

Array Canada REFI TL $275 1L 6 L+500, 1%, 99 - 101(6M) B/B2 UBS 2/1/2017

DDTL $45 1L 6 L+500, 1%, 99 - 101(6M) B/B2 UBS 2/1/2017

REV $40 1L 5 - - - B/B2 UBS 2/1/2017

Daseke ACQ TL $250 1L 7 L+500, 1%, 98.5 - 101(6M) -/B1 CS 2/2/2017

DDTL $100 1L 7 L+500, 1%, 98.5 - - -/B1 CS 2/2/2017

Dell REFI TL $5000 1L 6.5 L+250-275, 0.75%, 99.875 - 101(6M) -/- CS 2/1/2017

TL $500 1L 6.5 L+250-275, 0.75%, 99.875 - 101(6M) -/- CS 2/1/2017

PODS REFI TLB $620.77 1L 5 L+300-325, 1%, 100 Y 101(6M) -/- MS 2/1/2017

Change Healthcare ACQ REV $500 1L 5 - - - B+/Ba3 BAML 2/2/2017

TLB $4865 1L 7 L+275-300, 1%, 99.5 Y 101(6M) B+/Ba3 BAML 2/2/2017

Extended Stay REFI TLB $1300 1L 6.5 L+250, 0%, 100 Y 101(6M) -/- DB 2/2/2017

Harland Clarke REFI TLB $370 1L 5 L+600, 1%, 98 Y 101(6M) BB-/B1 CS 2/2/2017

Herbalife REFI REV $150 1L 5 L+300, 0.75% - - BB+/Ba1 CS 2/2/2017

TLB $1175 1L 7 L+375, 0.75%, 99 Y 101(6M) BB+/Ba1 CS 2/2/2017

Leslie's Poolmart LBO TLB $808 1L 6.5 L+325, 1%, 100 Y 101(6M) -/- Nomura 2/2/2017

TLB $50 1L 6.5 L+325, 1%, 99.75 Y 101(6M) B/B1 Nomura 2/2/2017

Milk Specialties REFI TL $475 1L 6.5 L+400-425, 1%, 100 Y 101(6M) -/- CS 2/2/2017

Victory Capital DIVID TL $100 1L 4.75 L+750, 1%, 99.75-100 - - -/- MS 2/2/2017

Go Daddy ACQ TLB $2470 1L 7 L+275, 0%, 99.5 Y 101(6M) BB-/- Barc 2/3/2017

Lionbridge Technologies LBO REV $40 1L 5 - - - B/Ba3 CS 2/3/2017

TL $200 1L 7 L+550, 1%, 99 - 101(6M) B/Ba3 CS 2/3/2017

TL $85 2L 8 L+975, 1%, 98 - 103/102/101 CCC+/Caa1 CS 2/3/2017

Apple Leisure Group LBO TL $600 1L 7 L+450, 1%, 99 Y 101(6M) B/B2 CS 2/7/2017

REV $125 1L 7 - - - B/B2 CS 2/7/2017

TL $225 2L 8 L+850, 1%, 98 Y 102/101 CCC+/Caa2 CS 2/7/2017

> Commitments are due Jan. 31 on term loans for and Bloomberg data show. Following are Ascensus American Builders,details of U.S. loans with commitments due through Feb. 7. For more information, click .here

This table was compiled by a Bloomberg LP employee involved with sales support and was edited by the News Department. To suggest ideas or provide

feedback, contact the editor Richard Bedard at [email protected] or +212 617 3590

Distress & Bankruptcy Calendar

Leveraged Capital & Distress 11 Jan. 31, 2017

DATE COMPANY EVENT NOTES, STORY LINKS

Jan. 31 J. Crew Group Quarterly payments due on term loan equal to $3.9m S&P sees distressed exchange or buyback likely in 1H

Jan. 31 Ruby Tuesday Expiration of waivers of covenant breaches Talks underway with lenders for amendments

Jan. 31 21st Century Oncology End of forbearance for missed payment on 11% notes due 2023 Co. previously issued “going concern” warning

Feb. 1 Community Health Coupons due on 2021 secured notes and 2022 unsecured notes Co. at risk of covenant breach in 2017 based on leverage

Feb. 1 Intelsat Coupon payment on 5.5% senior notes maturing 2023 S&P cut ratings and cited risk of "conventional default"

Feb. 1 SunEdison Hearing on sale of Minnesota projects Docket

Feb. 1 Exco Resources Extended deadline for borrowing-base redetermination Co. in November disclosed talks with lenders

Feb. 2 KrisEnergy Expected trading date for co.’s S$140m zero-coupon notes Co. says most 2017, 2018 noteholders favor debt amendments

Feb 3 Hanjin Shipping Deadline to submit rehabilitation plan to local court

Feb. 3 Kaiser Gypsum OBJ deadline for application to pay professionals Docket

Feb. 3 iHeartMedia Extended expiration of debt-swap offer Lenders reportedly seek better terms for the exchange

Feb. 6 Metinvest Creditors vote on debt-restructuring plan

Feb. 6 Dowling College Motion for 2004 exam of Cigna Health and Life, and Healthplex Docket

Feb. 7 Bumi Resources Co. to hold shareholder meeting to seek consent for share issue Jakarta court ratified debt-restructuring plan

Feb. 7 Sherwin Alumina Confirmation hearing Docket

Feb. 7 III Exploration II Motion to amend transition services agreement, extend deadlines Docket

Feb. 9 Privatbank Coupon due on $220m Feb. 2021 bond Ukraine bank creditors said to plan arbitration claim on losses

Feb. 13 Rent-A-Center Co. reports 4Q results Moody’s may downgrade on potential need for covenant relief

Feb. 14 Premier Oil Target date for refinancing agreement with lenders

Feb. 15 Vanguard Natural Res. Interest of $2.6m due on 2023 senior secured second-lien notes Bankruptcy “may be unavoidable," co. said in 10-Q filing

Feb. 15 Hornbeck Offshore Co. reports 4Q results after-market Co. hired PwC to assess maturities and strategic options

Feb. 17 China Shanshui Cement EGM on share placement and stock option Co. seeks to issue 910m to 950m new shares

Feb. 23 Seadrill Co. reports earnings for fiscal 2016 Seadrill has April 30 target for debt-restructuring agreement

Feb. 28 Farstad Shipping End of standstill on secured debt

March 1 China City Construction Annual coupon on CNY1.8b 2021 notes is due Co. sold assets to repay defaulted 2017 notes

March 2 CGG Co. expected to report 4Q earnings Shares have fallen on plans to restructure $2.9b of debtSource: Bloomberg News/Bloomberg Intelligence

Distress & Bankruptcy Calendar

Intelsat Faces Coupon Payment; Metinvest Creditors Vote on Plan to RestructureBy Luca Casiraghi, Joe Mayes, Steven Church, Andrew Dunn, Dawn McCarty, Tiffany Kary, Jodi Xu Klein, Rick Green

> In the U.S., must come up with a coupon payment on senior notes that mature in 2023.Intelsat> In Europe, creditors will be voting on a plan to restructure the holding company's debt.Metinvest

Leveraged Capital & Distress 12 Jan. 31, 2017

Bloomberg Briefs: Leveraged Capital & Distress

Newsletter

Managing Editor

Bloomberg News

Managing Editor

Newsletter

Editors

Paul Smith

Shannon Harrington

Richard Bedard

James Crombie

Terminal Sales

Marketing & Partnership

Director

Advertising

Reprints

& Permissions

Mark Betteridge

Courtney Martens

+1-212-617-2447

Lucy Rosen

+1-212-617-6759

Lori Husted

+1-717-505-9701 x2204

Interested in learning more

about the Bloomberg terminal?

Request a free demo .here

This newsletter and its

contents may not be forwarded

or redistributed without the

prior consent of Bloomberg.

Please contact our reprints and

permissions group for more

information. © 2017 Bloomberg

LP. All rights reserved.

Resources

Leveraged Capital & Distress 13 Jan. 31, 2017

Resources

Bloomberg Briefs will stop publishing the Leveraged Capital & Distress brief on Feb. 7. We will instead publish a Credit & Rates Strategy brief starting Feb. 14.

The Bloomberg terminal is a rich source of news and data for readers wanting more on high-yield and distressed debt. The functions below are useful for Bloomberg users.

If you have questions or comments about the Leveraged Capital & Distress brief, feel free to contact its editor, Richard Bedard, at rbe or [email protected]

Where to Find News, Alerts and Data on the Bloomberg Terminal