Tryg Forsikring uk fuldt sæt Tryg Forsikring årsrapport UK_12-1683.… · companies within...

32

$QQXDO5HSRUWDQG$FFRXQWV 7U\J)RUVLNULQJ$6 (Bus reg no 24260666)

Transcript of Tryg Forsikring uk fuldt sæt Tryg Forsikring årsrapport UK_12-1683.… · companies within...

$QQXDO�5HSRUW�DQG�$FFRXQWV�����

7U\J�)RUVLNULQJ�$�6(Bus reg no 24260666)

&RQWHQWV

Company information 1

Directors’ report 2

Investment activities 4

Subsidiary undertakings of Tryg Forsikring 4

Management’s signatures 8

Auditors’ reports 9

Accounting policies 11

Income statement 15

Balance sheet 17

Notes to the accounts 21

7U\J�)RUVLNULQJ�$�6��

&RPSDQ\�LQIRUPDWLRQ

6XSHUYLVRU\�%RDUGClaus Høeg Madsen, Attorney, ChairmanJørgen Høeg Pedersen, Managing Director, Deputy ChairmanConnie Borgen, Senior ClerkMogens Jacobsen, FarmerThorleif Krarup, Group Chief Executive Officer of NordeaJens Lyngbo, Managing Director, MSc(Eng), BComAntony Mærsk, Regional head of Personal InsuranceMikael Olufsen, Managing DirectorBirthe Petersen, Senior ClerkNiels Erik Schultz-Petersen, Landowner, MSc(Agricultural Science)Per Skov, Managing Director

([HFXWLYH�0DQDJHPHQWHugo AndersenStine BosseStig Ellkier-PedersenPeter Falkenham

,QWHUQDO�$XGLWSøren Lund, Chief AuditorAne Marie Christensen, Deputy Chief Auditor

$XGLWRUVDeloitte & Touche, Statsautoriseret Revisionsaktieselskab

KPMG

$GGUHVVTryg Forsikring A/SKlausdalsbrovej 601DK-2750 Ballerup

Tel +45 44 20 20 20Fax +45 44 20 66 00www.tryg.dk

7U\J�)RUVLNULQJ�$�6��

'LUHFWRUV¶�UHSRUW

*HQHUDO�LQIRUPDWLRQThe Directors’ report comprises that part of the Danish general insurance business which is carried on inthe legal unit Tryg Forsikring A/S itself. Furthermore, a brief description is given of the general and lifeinsurance activities carried on in separate subsidiary undertakings in Denmark, Poland and Finland.

The overall insurance activities in the Nordea Group also comprise the activities carried on by large sistercompanies within general insurance in Norway (Vesta Forsikring AS) and by the pension and lifeinsurance companies in Norway, Sweden and Finland.

Nordea’s Board of Directors has invited Tryg i Danmark smba to enter into a dialogue aiming atexploring the possibilities of a change in the ownership structure so that Nordea in the future becomes aminority owner of the general insurance group. The Supervisory Board of Tryg i Danmark smba hasaccepted the invitation. The aim is to be able to enter into an agreement on a new ownership structure anda strategic partnership between Nordea and Tryg i Danmark smba before the end of the first quarter of2002.

Financial highlights for the parent company Tryg Forsikring A/S

5HVXOW�IRU�WKH�\HDUThe result of the underlying insurance operations shows a profit of DKK 135m, excluding a run-off loss,net of reinsurance, of DKK 344m. The run-off loss can be explained mainly by a significant deteriorationof the claims performance in third-party motor insurance, attributable to personal injuries.

The result for the year after tax was a loss of DKK 249m against a profit of DKK 677m in 2000. At 31December 2001 total shareholders’ equity amounted to DKK 5,655m.

'..P ���� ���� ���� ���� ����

,QFRPH�VWDWHPHQWGross earned premiums 5,846 5,737 5,640 5,683 5,719

Earned premiums, net of reinsurance 5,296 5,315 5,235 5,243 5,227Claims incurred, net of reinsurance -4,505 -4,581 -3,897 -3,853 -4,096Insurance operating expenses, net of reinsurance 1,243 -1,400 -1,426 -1,453 -1,348Technical resultt -209 -324 226 95 -67Profit/loss on investment activities aftertransfer of technical interest -73 1,025 1,494 997 1,386Profit/loss for the year -249 677 1,550 954 1,319

Run-off result, net of reinsurance -344 -530 256 76 54

%DODQFH�VKHHWTechnical provisions, net of reinsurance 8,113 7,544 7,236 6,986 6,786Shareholders’ equity 5,655 5,904 6,477 8,327 7,987Assets 14,740 15,738 18,109 17,183 15,900

7U\J�)RUVLNULQJ�$�6��

The Supervisory Board proposes that the loss for the year should be distributed as indicated in thedistribution of profit.

3UHPLXPVGross earned premiums increased by approximately 2% in 2001 to DKK 5,846m. Earned premiums, netof reinsurance, amounted to DKK 5,296m.

During the financial year Tryg Forsikring paid DKK 550m in premiums to reinsurers. Together withequalisation provisions amounting to DKK 131m at the end of 2001, reinsurance cover constitutes theCompany’s total financial resources for covering catastrophic losses. In addition, the equalisationprovisions include DKK 74m relating to workmen’s compensation insurance.

5DWLRV�DQG�NH\�ILJXUHVThe below key ratios are disclosed in compliance with the Executive Order on the presentation offinancial statements by general insurance companies to facilitate comparison with prior years.

&ODLPVClaims incurred, net of reinsurance, amounted to DKK 4,161m excluding a run-off loss of DKK 344m,which is significantly above the expected level.

Excluding a run-off loss on motor insurance, the gross run-off loss for 2001 totalled DKK 152m,primarily relating to workmen’s compensation insurance and commercial liability insurance. Workmen’scompensation insurance and third-party motor insurance are characterised by long run-off periods andinfluence from the decisions of the National Board of Industrial Injuries. In addition the claims pattern ofthe commercial business was unsatisfactory.

����

����

����

����

����

����

����

����

����

���� ���� ���� ���� ����

0LR�NU�

���� ����� ����� ���� ����

Claims ratio, net of reinsurance 86.5 86.7 75.5 73.9 79.4Expense ratio, net of reinsurance 23.7 26.5 27.5 28.0 26.0Combined ratio, net of reinsurance 110.2 113.2 103.0 101.9 105.4

Return on shareholders’ equity (%) -4.3 10.9 17.0 11.7 17.7Solvency cover 2.0 3.6 4.3 7.0 6.4

'LVWULEXWLRQ�RI�SURILW�

Available for distribution:

Loss for the year -249

Transfer from Contingency reserve 527

278

Proposed distribution:

Transfer to Revaluation account 48

Transfer to Net revaluation reserve

according to the equity method 64

Tranfer to Retained profit 167

278

*URVV�SUHPLXPV

7U\J�)RUVLNULQJ�$�6��

,QVXUDQFH�RSHUDWLQJ�H[SHQVHVAcquisition costs and administrative expenses decreased by DKK 103m. This is due to cost savingsthrough efficiency-enhancing measures, including a reduction in the number of service centres.Reinsurance commission income increased by DKK 54m. Total net cost savings thus came toDKK 157m, corresponding to a reduction of total expenses to DKK 1,243m.

,QYHVWPHQW�DFWLYLWLHVThe parent company recorded a loss of DKK 73m on investment activities after transfer of technicalinterest. The investment return was significantly affected by the negative market trends for Danish andinternational shares and upward revaluations of properties.

The return on the property portfolio, excluding upward revaluations of DKK 46m, came to 7.6% in 2001.

The total return on equities was –14.4%, corresponding to the market return. The return on the bondportfolio was 8.3% compared with the market return of 6.4%. At year-end the duration of the bondportfolio was 3.9 years.

In Tryg Forsikring and its subsidiary undertakings revaluations were made in 2001 of the estimatedmarket value of properties, by DKK 161m relating to general insurance, and DKK 522m relating to lifeinsurance. Of the revaluation relating to life insurance the greater part is attributable to the policyholders.The positive impact on the result of Tryg Forsikring of the revaluation relating to life insurance is thuslimited to DKK 30m.

6XEVLGLDU\�XQGHUWDNLQJV�RI�7U\J�)RUVLNULQJTotal profit from subsidiary undertakings came to DKK 168m in 2001 against DKK 626m in 2000. Theresult is included in the income statement under the item "Profit from group undertakings". In theaccounts of the parent company, shares in subsidiary undertakings are stated at the parent company’sshare of the net asset value, which amounted to DKK 6,133m at the end of 2001 against DKK 6,007m atthe end of 2000.

7U\J¶V�OLIH�LQVXUDQFH�JURXSTryg Forsikring, livsforsikringsselskab A/S (Tryg Liv) is the parent company of all Danish life insuranceand pension companies of the Tryg Group. The major part of new business written within individualpension savings is placed in Tryg Liv, whereas company pension schemes are placed in Tryg Pension.Tryg Invest handles unit-linked savings. At the end of 2001 the group’s portfolio consisted of 650,000polices. Benefits are being paid under 65,000 policies.

The result for the year after tax was a loss of DKK 135m against a profit of DKK 435m in 2000. Theresult for the year was mainly affected by the negative development in financial markets and losses insubsidiary undertakings. At 31 December 2001 the shareholders’ equity of the parent company totalledDKK 2,906m.

7U\J�)RUVLNULQJ�$�6��

'DQVN�.DXWLRQVIRUVLNULQJV�$NWLHVHOVNDEDansk Kaution is responsible for the Group’s activities within guarantee insurance and is a market leaderwithin this line of insurance in Denmark. The company also writes reinsurance within credit andguarantee insurance.

Profit after tax amounted to DKK 140m for 2001, corresponding to a return on average shareholders’equity of 32.2%. Like in 2000, the profit was positively affected by run-off gains in connection with thetermination of a number of old insurance contracts.

At the end of 2001 total shareholders’ equity amounted to DKK 404m after allocation of dividend ofDKK 100m.

7U\J�)RUVLNULQJ�,,�$�6Tryg Forsikring II has specialised in advice on and sales of insurance products through Nordea BankDanmark’s branches in conjunction with other advisory services relating to personal finances.

The result for the year after tax was a loss of DKK 14m. The result of the underlying insurance operationsamounted to DKK 7m, excluding a run-off loss, net of reinsurance, of DKK 21m. In 2000 the technicalresult amounted to DKK 1m. Earned premiums, net of reinsurance, amounted to DKK 356m,corresponding to approximately 23% growth.

In 2001 the company launched the sale of insurance products in Finland via the Internet and through thebranch network of Nordea Bank Finland.

7U\J�%DOWLFD�LQWHUQDWLRQDO�$�6Tryg-Baltica international (TBi) writes reinsurance contracts and business within selected internationalniche lines. In 2001 Tryg Forsikring’s marine insurance business was transferred to TBi. Furthermore, theTryg Group’s total outward reinsurance is ceded via TBi to obtain the best possible terms for reinsurancebusiness ceded for the Group.

In 2001 accounting policies were adjusted to comply with the accounting policies of the Group. Thechange in accounting policies in 2001 had a positive net impact of DKK 46m on the result before tax anda negative net impact of DKK 31m on shareholders’ equity. Reference is made to Accounting policies.

The result for the year was a loss of DKK 33m against a loss of DKK 77m in 2000 after adjustment ofcomparative figures.

The company experienced considerable growth in premiums, mainly because 2001 was characterised bysignificant premium rate increases in a number of TBi’s business areas.

The main reason for the loss in 2001 is that the energy business showed a poorer performance thanexpected. Following a reassessment of the development opportunities it was decided in the summer of2001 to cease writing energy business.

The World Trade Center catastrophe resulted in claims incurred, net of reinsurance, of around DKK 6mas the company writes USA-exposed business only to a limited extent.

7U\J�)RUVLNULQJ�$�6��

The company holds an A- rating (Excellent) from A.M. Best and a BBB+ rating (Good) from Standard &Poor’s. For the moment, both ratings are placed under review due to the ongoing process of changing theownership structure of Nordea’s General Insurance business area.

1RUGHD�8EH]SLHF]HQLD�6�$�During the year Tryg Forsikring acquired an additional 17.7% of the shares in Nordea Ubezpieczenia,bringing the total shareholding to 69% at year-end. The company has its registered office in Poland andcarries on insurance business in Poland mainly within motor insurance and fire insurance of buildings.The company has a market share of 1.8% in Poland.

The result for the year before minority interests was a loss of DKK 12m. The technical result was a lossof DKK 8m.

Despite fierce competition in the Polish market, gross earned premiums increased from DKK 372m in2000 to DKK 462m in 2001, corresponding to a growth rate of 24%.

The accounting policies were adjusted in 2001. Reference is made to Accounting policies.

7U\J�5HMVH�RJ�6XQGKHG�$�6��IRUPHUO\�.RPSDV�5HMVHIRUVLNULQJ�$�6�As a company in the Tryg Group, Tryg Rejse og Sundhed specialises in international travel, sickness,accident and contents insurance, and in healthcare insurance, which is a growth area.

The profit for the year was DKK 7m. The technical result shows a profit of DKK 6m against DKK 3m in2000.

At DKK 96m, premium income shows a slight decline on 2000, primarily owing to an improvement of

the international portfolio and to continued intense competition in the travel insurance market.

Furthermore the cooperation with Danske Bank on distribution was discontinued in the middle of 2001.

7U\J�(MHQGRPPH�,�$�6At the end of the year, the company’s property portfolio consisted of 43 properties. The company’s

average occupancy rate was 93 at year-end. At the end of 2001 the properties were valued at

DKK 1,404m, including an upward revaluation of DKK 113m made in 2001.

At 31 December 2001 shareholders’ equity stood at DKK 1,819m after transfer of the profit for the yearof DKK 211m to retained profit.

&DSLWDO�DQG�RZQHUVKLSTryg Forsikring is a member of the Tryg Group, which forms part of the Nordic financial services groupNordea. The share capital of DKK 1,000m is wholly owned by Tryg A/S, Ballerup.

As part of the restructuring of the Group with a view to establishing a life group and a general insurancegroup, it was decided on 21 December 2001 to allot the shares in the wholly owned Tryg Forsikring,livsforsikringsselskab A/S to Tryg A/S by a reduction in the share capital of Tryg Forsikring A/S. Theactual allotment of shares to Tryg A/S awaits the expiry of the relevant statutory period of notice on 5April 2002. The reduction in the share capital will reduce Tryg Forsikring A/S’s shareholders’ equity byapproximately DKK 3.0bn.

7U\J�)RUVLNULQJ�$�6��

The Company is included the consolidation of the accounts of Nordea AB, Stockholm(www.nordea.com).

6XSHUYLVRU\�%RDUG�DQG�([HFXWLYH�0DQDJHPHQWIn November 2001 Stig Ellkier-Pedersen joined the Executive Management. Ib Mardahl-Hansen resignedfrom the Executive Management at the same time.

Leif Hede Nielsen resigned from the Supervisory Board in September 2001.

3RVW�EDODQFH�VKHHW�HYHQWVNo events have occurred after the balance sheet date which, in the opinion of management, materiallyaffect the evaluation of the financial position of the Company.

2XWORRNTryg Forsikring and its subsidiary undertakings will play a central role in offering general and lifeinsurance products and services to the Nordic market.

In the Danish market the Company expects to increase its market share within Personal and to maintainits market share within Commercial while improving profitability and strengthening customer loyalty.

The continued focus on cost containment is expected to lead to a further reduction in the expense ratio in2002.

Management’s target is still a combined ratio of maximum 100 in general insurance. However, 2000 and2001 have shown that a stronger focus on profitability is necessary, particularly in commercial insurancein Denmark and in TBi, to reach this ambitious target. Poland is a development market for Tryg’s generalinsurance activities requiring IT investments and a changed distribution strategy while maintaining thegood profitability.

The technical result for 2002 is expected to show a significant improvement on 2001. The overall resultfor 2002 will also be influenced by conditions in the financial markets.

7U\J�)RUVLNULQJ�$�6��

0DQDJHPHQW¶V�VLJQDWXUHV

The Supervisory Board and the Executive Management have today adopted the financial statements andthe directors’ report.

The financial statements have been prepared in accordance with general accounting standards. Weconsider the accounting policies adopted appropriate so that the financial statements give a true and fairview.

We propose to the Annual General Meeting that the financial statements should be adopted.

Ballerup, 20 February 2002

([HFXWLYH�0DQDJHPHQW

+XJR�$QGHUVHQ 6WLQH�%RVVH

6WLJ�(OONLHU�3HGHUVHQ 3HWHU�)DONHQKDP

�&DUVWHQ�,EVHQ

6XSHUYLVRU\�%RDUG

&ODXV�+¡HJ�0DGVHQ -¡UJHQ�+¡HJ�3HGHUVHQ

Chairman Deputy Chairman

&RQQLH�%RUJHQ 0RJHQV�-DFREVHQ� 7KRUOHLI�.UDUXS

-HQV�/\QJER $QWRQ\�0 UVN� 0LNDHO�2OXIVHQ

%LUWKH�3HWHUVHQ� 1LHOV�(ULN�6FKXOW]�3HWHUVHQ 3HU�6NRY

$GRSWHG�E\�WKH�$QQXDO�*HQHUDO�0HHWLQJ�RI�WKH�&RPSDQ\�RQ����$SULO������

&KDLUPDQ�RI�WKH�$QQXDO�*HQHUDO�0HHWLQJ�

7U\J�)RUVLNULQJ�$�6��

$XGLWRUV¶�UHSRUW

,QWHUQDO�DXGLWRUV¶�UHSRUW

We have audited the financial statements of Tryg Forsikring A/S for 2001 presented by management.

%DVLV�RI�RSLQLRQThe audit was performed on the basis of the Danish Financial Supervisory Authority’s Executive Orderconcerning financial institutions and financial groups and in accordance with generally accepted Danishauditing standards. Based on an evaluation of the materiality and risk our audit has included anexamination of business procedures and evidence supporting the amounts and other disclosures in thefinancial statements.

Our audit has not given rise to qualifications.

2SLQLRQIn our opinion, the financial statements have been presented in accordance with the accounting provisionsof Danish legislation and give a true and fair view of the Company’s assets and liabilities, financialposition and result.

Ballerup, 20 February 2002

6¡UHQ�/XQG $QH�0DULH�&KULVWHQVHQChief Auditor Deputy Chief Auditor

7U\J�)RUVLNULQJ�$�6���

$XGLWRUV¶�UHSRUW

$XGLWRUV¶�UHSRUW

We have audited the financial statements of Tryg Forsikring A/S for 2001 presented by management.

%DVLV�RI�RSLQLRQWe have planned and conducted our audit in accordance with generally accepted Danish auditing

standards and International Standards on Auditing (ISAs) so as to obtain reasonable assurance about

whether the financial statements are free of material misstatement. Based on an evaluation of the

materiality and risk our audit has included an examination of evidence supporting the amounts and other

disclosures in the financial statements. We have assessed the accounting policies applied and the

accounting estimates made as well as evaluated the overall financial statement presentation.

Our audit has not given rise to qualifications.

2SLQLRQIn our opinion, the financial statements have been presented in accordance with the accounting provisions

of Danish legislation and give a true and fair view of the Company’s assets and liabilities, financial

position and result.

Ballerup, 20 February 2002

'�(�/�2�,�7�7�(����7�2�8�&�+�( .30*�&��-HVSHUVHQStatsautoriseret Revisionsaktieselskab

%HQW�+DQVHQ /RQH�0¡OOHU�2OVHQ )LQQ�/��0H\HU 6YHQ�&DUOVHQState-Authorised State-Authorised State-Authorised State-Authorised

Public Accountant Public Accountant Public Accountant Public Accountant

7U\J�)RUVLNULQJ�$�6���

$FFRXQWLQJ�SROLFLHV

%DVLV�RI�SUHSDUDWLRQ

The financial statements have been prepared in accordance with the Danish Consolidated InsuranceBusiness Act and the Danish Financial Supervisory Authority’s Executive Order on the presentation offinancial statements by general insurance companies.

Consolidated financial statements are not prepared as the Company is a wholly owned subsidiary ofNordea AB, Stockholm, which prepares the consolidated financial statements.

As a result of an adjustment of accounting policies in the subsidiary undertakings in Tryg Forsikring,shareholders’ equity at 1 January has been reduced by DKK 105m. The changes in the accountingpolicies have been implemented as from the beginning of 2001. Comparative figures and financialhighlights for 2000 have been restated. Apart from this, no changes have been made to the accountingpolicies applied in the previous year.

The change in the accounting policies of Tryg-Baltica international represents a shift in methods so thatthe recognition of premiums, commissions and claims follows the financial year. Previously these itemswere stated with a time lag. The change in accounting policies in 2001 had a positive net impact ofDKK 46m on the result before tax and a negative net impact of DKK 31m on shareholders’ equity.

The change in accounting policies in Nordea Ubezpieczenia in Poland relates to an adjustment ofunearned premiums provisions and full depreciation in the year of acquisition of intangible fixed assets.The change in accounting policies in 2001 had a net impact on the result before tax of DKK 0m and anegative net impact of DKK 15m on shareholders’ equity.

,QFRPH�VWDWHPHQW

,QVXUDQFH�DFWLYLWLHV

Earned premiums, net of reinsurance, represent gross premiums due for the year, net of outwardreinsurance premiums and changes in unearned premiums provisions, corresponding to an accrual ofpremiums to the period of coverage of the policy.

Technical interest, net of reinsurance, represents a calculated return on the average technical provisions,net of reinsurance. The interest rate applied is the year’s average yield on bonds with a term to maturity ofless than three years.

Claims incurred, net of reinsurance, represent claims paid during the year adjusted for changes inoutstanding claims provisions and provisions for annuities less reinsurers’ share. Amounts to coverexpenses incurred to combat and contain losses and to survey and assess claims are included in the item.In addition, the item includes prior-year run-off gains/losses. That part of the increase in technicalprovisions which can be ascribed to discounting is transferred to technical interest, net of reinsurance.

Premium rebates represent premium reimbursements where the amount reimbursed depends on the claims

7U\J�)RUVLNULQJ�$�6���

record, and for which the criteria for payment have been laid down prior to the financial year or when thebusiness was written.

Insurance operating expenses, net of reinsurance, represent acquisition costs and administrative expensesless reinsurance commissions received. Expenses relating to acquiring and renewing the insuranceportfolio are charged to the income statement at the time of writing the business. Administrativeexpenses, including salaries, taxes etc, are accounted for on an accrual basis to match the financial year.Subsidiary undertakings pay shares of joint expenses according to their consumption of resources, whichare settled on cost-covering terms.

,QYHVWPHQW�DFWLYLWLHV

Profit from group and associated undertakings includes a part of the total profit and revaluation of sharesin subsidiary undertakings and associated undertakings. Exchange rate differences arising on thetranslation of foreign subsidiary undertakings’ net asset value at the beginning of the year are includedunder the item "Currency translation adjustment”.

Interest, dividends etc represent interest earned, dividends received, etc during the financial year. Inaddition, the item includes realised gains on bonds drawn for redemption and repayments on loans as wellas realised gains on the sale of bonds drawn for redemption.

Realised investment gains/losses represent realised net gains/losses on the sale of investments, includingfinancial instruments, calculated in proportion to the value at the beginning of the financial year or thecost of acquisition during the year. Furthermore, the item includes gains/losses on the sale of subsidiaryundertakings and the sale of the Company’s portfolio of own shares.

Unrealised investment gains/losses represent unrealised net gains/losses on investments marked-to-market, including financial instruments, when marked to market at the end of the financial year,calculated in proportion to the value at the beginning of the financial year or the cost of acquisition duringthe year.

Investment administrative expenses represent expenses relating to the management of investments.Brokerage and commission are included in the purchase and sale prices of investments.

Currency translation adjustment represents that part of the valuation adjustments of all financial items andsales gains and losses which can be ascribed to exchange rate differences arising on the translation intoDanish kroner, including the translation of the opening balance of the net asset value of foreign subsidiaryundertakings and the opening technical provisions. The net asset value of foreign subsidiary undertakingsand other assets and liabilities denominated in foreign currency, including forward currency contracts, aretranslated at the exchange rate ruling at year-end. The results of foreign subsidiary undertakings are basedon translation of the items in the income statement at average exchange rates. Other income and expensesdenominated in foreign currency are translated at the exchange rate ruling on the date of the transaction.

Tryg Forsikring is taxed jointly with the majority of its subsidiary undertakings. The item ”Tax”

represents estimated Danish and foreign corporation tax for the year and movements in deferred tax or

deferred tax assets. Tax relating to the jointly taxed income is charged proportionately to the jointly taxed

companies. Changes in deferred tax or deferred tax assets are posted in the companies having the liability

7U\J�)RUVLNULQJ�$�6���

or the claim.

%DODQFH�VKHHW

$VVHWV

Land and buildings are stated at estimated market value in accordance with the guidelines issued by theDanish Financial Supervisory Authority. The market value is determined based on a capitalisation of thereturn on the property. The capitalisation factor depends on the type and location of the property. Newbuildings and buildings in the course of construction are stated at the cost of acquisition or the cost ofproduction.

Shares in group and associated undertakings are stated at the proportionate share of the shareholders’equity of the undertakings. The year’s net revaluation is transferred to shareholders’ equity under the item"Net revaluation reserve according to the equity method".

Listed shares and bonds etc are stated at officially quoted year-end prices. Unlisted shares and fixed-interest loans etc are stated at a conservatively estimated market value.

Unsettled financial instruments, including forward contracts and open securities transactions, are stated atthe market value on the balance sheet date. The gross amounts are disclosed in a note to the financialstatements.

Deposits with ceding undertakings comprise amounts owed to the Company in respect of reinsurancebusiness accepted and retained by the ceding undertaking pursuant to the reinsurance contract.

Debtors are stated at nominal value less a provision to cover anticipated losses.

Deferred tax assets comprise deferred net tax assets calculated as 30% of the present value of net positivetiming differences between accounting and taxable profits, plus tax losses to the extent they are expectedto be offset against future taxable income.

In accordance with the guidelines issued by the Danish Financial Supervisory Authority, deferred tax isnot provided on the untaxed part of the contingency reserves. It is not expected that future movements intechnical provisions will result in a crystallisation of tax on the contingency reserves.

Furniture, computers, other equipment, motor cars etc are valued at cost of acquisition less accumulateddepreciation. Depreciation is charged on a straight-line basis over four to five years. Furniture andequipment etc costing less than DKK 100,000 are written off fully in the year of acquisition, except forassets acquired as part of a specific project, which are treated as one asset.

/LDELOLWLHV

Unearned premiums provisions, net of reinsurance, represent the proportion of premiums and reinsurancepremiums collected which relates to subsequent financial years.

Outstanding claims provisions, net of reinsurance, represent amounts to cover claims incurred but notsettled at the end of the year, less reinsurers’ share. Outstanding claims provisions are calculated on the

7U\J�)RUVLNULQJ�$�6���

basis of information available concerning the extent of the losses plus an amount based on pastexperience to cover claims incurred but not reported. The provisions include amounts to combat andcontain losses and to survey and assess claims.

Provisions for premium rebates represent amounts expected to be repaid to policyholders in view of theclaims experience during the financial year.

Equalisation provisions are calculated statistically and represent amounts provided to cover future claimsin areas where experience has shown that claims vary from year to year. For workmen’s compensationinsurance, equalisation provisions are calculated as the difference between the technical provisions, madeup at a basic interest rate of 2.00% and 2.75%, respectively.

Other technical provisions, net of reinsurance, represent provisions for risk not yet run off as well asprovisions for risk increasing with age.

Provisions for risk not yet run off represent the amounts deemed necessary, in addition to unearnedpremiums provisions and future premium rates, to cover claims and expenses in later accounting periodsfor policies in force on the balance sheet date.

Provisions for risk increasing with age comprise amounts relating to sickness and personal accidentpolicies considered necessary to cover claims and expenses in later accounting periods for policies inforce on the balance sheet date.

Deposits received from reinsurers comprise amounts due in respect of reinsurance business accepted andretained pursuant to the reinsurance contract.

Liabilities are generally stated at nominal value. Liabilities relating to claims under mortgage guaranteesfor which repayment by regular instalments has been agreed have been provided at the value resultingfrom discounting the future payments at the market rate of interest.

2WKHU�LWHPV

Intragroup trading in investments is settled at market value. Intragroup services are paid for on cost-covering or market terms. Intragroup transactions and agreements of major significance are disclosed inthe accounts.

7U\J�)RUVLNULQJ�$�6���

,QFRPH�VWDWHPHQW

'..P ���� ����

Note*HQHUDO�LQVXUDQFH

(DUQHG�SUHPLXPV

Gross premiums written 5,975 5,797Outward reinsurance premiums -540 -430Change in gross unearned premiums provisions -129 -60Change in unearned premiums provisions, reinsurers’ share -10 8

1 (DUQHG�SUHPLXPV��QHW�RI�UHLQVXUDQFH ����� �����

2 7HFKQLFDO�LQWHUHVW��QHW�RI�UHLQVXUDQFH ��� ���

&ODLPV�LQFXUUHG

Gross claims paid -4,770 -5,958Reinsurers’ share 610 1,583Change in gross outstanding claims provisions -135 602Change in outstanding claims provisions, reinsurers’ share -210 -807

3 &ODLPV�LQFXUUHG��QHW�RI�UHLQVXUDQFH ������ ������

&KDQJH�LQ�RWKHU�WHFKQLFDO�SURYLVLRQV��QHW�RI�UHLQVXUDQFH ��� ��

3UHPLXP�UHEDWHV ��� ���

,QVXUDQFH�RSHUDWLQJ�H[SHQVHV

Acquisition costs -832 -799Administrative expenses -945 -940Reimbursement from group undertakings 425 283Reinsurance commissions and profit participation 109 56

4 7RWDO�LQVXUDQFH�RSHUDWLQJ�H[SHQVHV��QHW�RI�UHLQVXUDQFH ������ ������

&KDQJH�LQ�HTXDOLVDWLRQ�SURYLVLRQV � �

5 7HFKQLFDO�UHVXOW ���� ����

7U\J�)RUVLNULQJ�$�6���

,QFRPH�VWDWHPHQW

'..P ���� ����

Note1RQ�LQVXUDQFH�DFWLYLWLHV

,QYHVWPHQW�LQFRPH

6 Profit from group undertakings 168 626Profit from associated undertakings 0 2Income from land and buildings 57 60

7 Interest, dividends etc 343 4088 Realised investment gains 0 230

7RWDO�LQYHVWPHQW�LQFRPH ��� �����

8 8QUHDOLVHG�LQYHVWPHQW�JDLQV 0 ���

,QYHVWPHQW�H[SHQVHV

Investment administrative expenses -11 -10Interest expenses -16 -25

8 Realised investment losses -49 0

7RWDO�LQYHVWPHQW�H[SHQVHV ��� ���

8 Unrealised investment losses -192 0Currency translation adjustment 1 42

3URILW�RQ�LQYHVWPHQW�DFWLYLWLHV�EHIRUH

WUDQVIHU�WR�LQVXUDQFH�DFWLYLWLHV ��� �����

2 Technical interest transferred toinsurance activities -374 -431

7RWDO�SURILW�ORVV�RQ�LQYHVWPHQW�DFWLYLWLHV ��� �����

3URILW�EHIRUH�WD[ ���� ���

9 Tax 34 -25

3URILW�ORVV�IRU�WKH�\HDU ���� ���

7U\J�)RUVLNULQJ�$�6���

%DODQFH�VKHHW�DW����'HFHPEHU

'..P ���� ����

Note$VVHWV

,QYHVWPHQWV

10 /DQG�DQG�EXLOGLQJV ��� ���

,QYHVWPHQWV�LQ�JURXS�XQGHUWDNLQJV

11 Shares in group undertakings 6,133 6,007

7RWDO�LQYHVWPHQWV�LQ�JURXS�DQG

DVVRFLDWHG�XQGHUWDNLQJV ����� �����

2WKHU�ILQDQFLDO�LQYHVWPHQWV

12 Shares 1,575 1,810Bonds 3,665 3,875Loans secured by mortgages 189 185Other loans 84 88Deposits with credit institutions 0 59

13 7RWDO�RWKHU�ILQDQFLDO�LQYHVWPHQWV ����� �����

'HSRVLWV�ZLWK�FHGLQJ�XQGHUWDNLQJV � �

7RWDO�LQYHVWPHQWV ������ ������

7U\J�)RUVLNULQJ�$�6���

%DODQFH�VKHHW�DW����'HFHPEHU�

'..P ���� ����

Note'HEWRUV

Policyholders 191 218Insurance brokers 22 19Total debtors arising out ofdirect insurance operations 213 236Amounts owed by insurance companies 719 585Amounts owed by group undertakings 548 1,176Other debtors 119 227

7RWDO�GHEWRUV ����� �����

2WKHU�DVVHWV

Furniture, computers, other equipment, motor cars etc 207 276Cash at bank and in hand 141 101

20 Deferred tax asset 168 128

7RWDO�RWKHU�DVVHWV ��� ���

3UHSD\PHQWV�DQG�DFFUXHG�LQFRPH

Accrued interest and rent 70 100Other prepayments and accrued income 35 52

7RWDO�SUHSD\PHQWV�DQG�DFFUXHG�LQFRPH ��� ���

14 7RWDO�DVVHWV ������ ������

7U\J�)RUVLNULQJ�$�6���

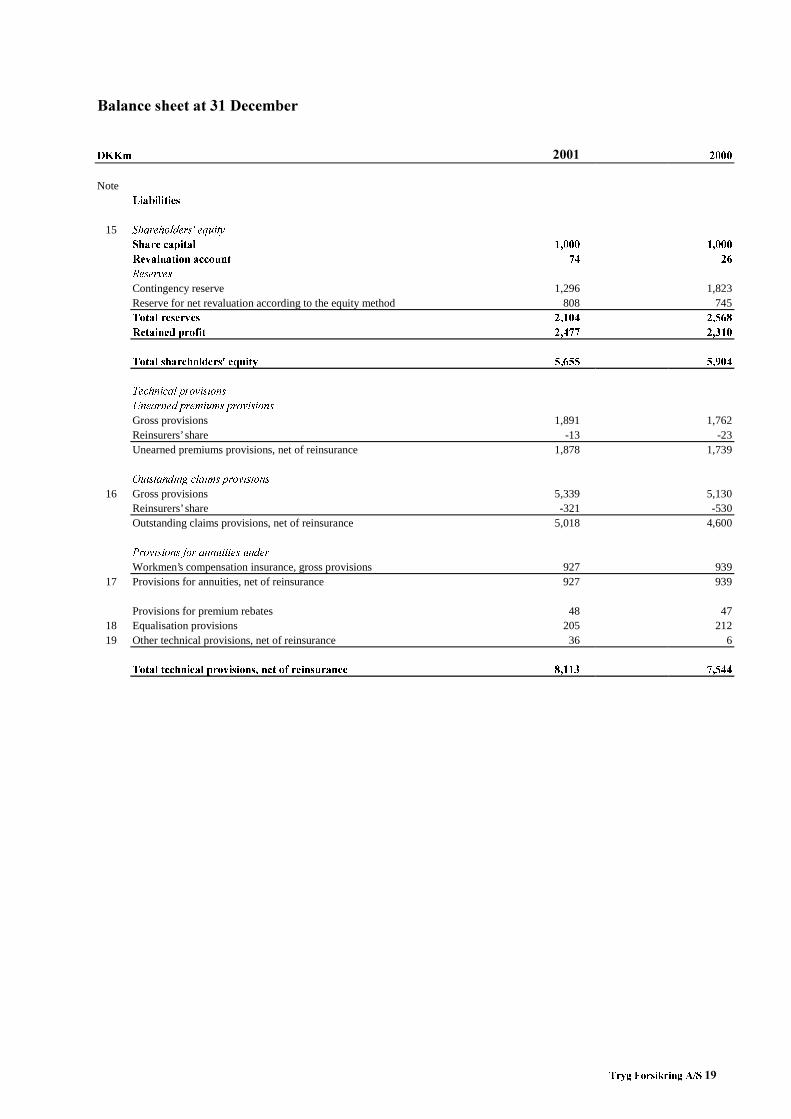

%DODQFH�VKHHW�DW����'HFHPEHU

'..P ���� ����

Note/LDELOLWLHV

15 6KDUHKROGHUV�HTXLW\

6KDUH�FDSLWDO ����� �����

5HYDOXDWLRQ�DFFRXQW �� ��

5HVHUYHV

Contingency reserve 1,296 1,823Reserve for net revaluation according to the equity method 808 7457RWDO�UHVHUYHV ����� �����

5HWDLQHG�SURILW ����� �����

7RWDO�VKDUHKROGHUV�HTXLW\ ����� �����

7HFKQLFDO�SURYLVLRQV

8QHDUQHG�SUHPLXPV�SURYLVLRQV

Gross provisions 1,891 1,762Reinsurers’ share -13 -23Unearned premiums provisions, net of reinsurance 1,878 1,739

2XWVWDQGLQJ�FODLPV�SURYLVLRQV

16 Gross provisions 5,339 5,130Reinsurers’ share -321 -530Outstanding claims provisions, net of reinsurance 5,018 4,600

3URYLVLRQV�IRU�DQQXLWLHV�XQGHU

Workmen’s compensation insurance, gross provisions 927 93917 Provisions for annuities, net of reinsurance 927 939

Provisions for premium rebates 48 4718 Equalisation provisions 205 21219 Other technical provisions, net of reinsurance 36 6

7RWDO�WHFKQLFDO�SURYLVLRQV��QHW�RI�UHLQVXUDQFH ����� �����

7U\J�)RUVLNULQJ�$�6���

%DODQFH�VKHHW�DW����'HFHPEHU

'..P ���� ����

Note3URYLVLRQV�IRU�RWKHU�ULVNV�DQG�H[SHQVHV

Provisions for pensions and similar obligations 17 24

7RWDO�SURYLVLRQV�IRU�RWKHU�ULVNV�DQG�H[SHQVHV �� ��

&UHGLWRUV

Creditors arising out of direct insurance operations 48 43Creditors arising out of reinsurance operations 2 5Amounts owed to credit institutions 23 177Amounts owed to group undertakings 259 68Corporation tax 0 127Other creditors 619 587Dividend for the financial year 0 1,250

21 7RWDO�FUHGLWRUV ��� �����

$FFUXDOV�DQG�GHIHUUHG�LQFRPH � ��

7RWDO�OLDELOLWLHV ������ ������

22 6ROYHQF\�PDUJLQ�DQG�FRUH�FDSLWDO

23 )RUZDUG�WUDQVDFWLRQV�HWF

24 &RQWLQJHQW�OLDELOLWLHV

25 ,QWUDJURXS�WUDQVDFWLRQV

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

1 (DUQHG�SUHPLXPV��QHW�RI�UHLQVXUDQFH

Direct insurance 5,836 5,719Reinsurance 10 18

5,846 5,737Outward reinsurance premiums -550 -422

����� �����

'LUHFW�LQVXUDQFH�E\�ORFDWLRQ�RI�ULVN

Denmark 5,793 5,645Other EU countries 14 25Other countries 29 49

5,836 5,719

2 7HFKQLFDO�LQWHUHVW��QHW�RI�UHLQVXUDQFH

Transferred from investment activities 374 431Discounting -57 -64

��� ���

3 &ODLPV�LQFXUUHG��QHW�RI�UHLQVXUDQFH

Direct insurance -4,862 -5,342Reinsurance -42 -14

-4,905 -5,356Reinsurers’ share 400 776

������ ������

5XQ�RII�UHVXOW�UHJDUGLQJ�SUHYLRXV�\HDUV��QHW�RI�UHLQVXUDQFH

Gross run-off result regarding previous years -450 -798Run-off result regarding previous years, reinsurers’ share 106 268

-344 -530

6SHFLILFDWLRQ�RI�UXQ�RII�UHVXOW��QHW�RI�UHLQVXUDQFH

Accident and sickness insurance 53 30Workmen’s compensation insurance -18 -2Motor insurance, third-party liability -321 1Motor insurance, comprehensive 48 -35Marine, aviation and cargo insurance 19 7Fire and contents insurance (personal) -48 -173Fire and contents insurance (commercial) 0 -387Liability insurance -51 20Credit and bond insurance 1 8Other direct insurance 14 0Total direct insurance -303 -531Reinsurance -41 1

-344 -530

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

4 ,QVXUDQFH�RSHUDWLQJ�H[SHQVHV��QHW�RI�UHLQVXUDQFH

Commissions relating to direct insurance -95 -106Other acquisition costs -738 -692Total acquisition costs -832 -799Total administrative expenses -945 -940Gross insurance operating expenses -1,777 -1,738Reimbursement from group undertakings 425 283

-1,352 -1,455Reinsurance commissions etc 109 56

������ ������

*URVV�LQVXUDQFH�RSHUDWLQJ�H[SHQVHV

LQFOXGH�WKH�IROORZLQJ�VWDII�FRVWV�

Salaries -1,088 -1,073Commissions -5 -32Pension costs -182 -181Other social security costs -5 -5Payroll taxes etc -122 -119

-1,402 -1,411

6DODULHV�DQG�HPROXPHQWV�HWF

Supervisory Board -3 -2Executive Management -13 -7

-16 -9

Number of employees (full-time equivalents) at 31 December 2,707 2,769

Average number of employees (full-time equivalents) during the year 2,713 2,807

$GPLQLVWUDWLYH�H[SHQVHV�LQFOXGH�IHHV�WR�WKH�DXGLWRUV

DSSRLQWHG�E\�WKH�*HQHUDO�0HHWLQJ

Deloitte & Touche -1.0 -1.5KPMG -0.8 -0.4

-1.7 -1.9

2I�ZKLFK�UHPXQHUDWLRQ�IRU�QRQ�DXGLW�VHUYLFHV�

Deloitte & Touche -0.2 -0.6KPMG -0.3 0.0

-0.5 -0.6

7U\J�)RUVLNULQJ�$�6���

Notes

DKKm1 1 2 2 3 3 4 4 5 5

5 Technical result, net of reinsurance, by line of insurance

Accident Workmen’s Marine,and sickness compensation Motor, third- Motor, aviation and

insurance insurance party liability comprehensive cargo2001 2000 2001 2000 2001 2000 2001 2000 2001 2000

Gross premiums written 381 335 312 312 753 773 1,486 1,439 133 213

Gross earned premiums 366 328 306 309 743 767 1,468 1,417 139 214Gross claims incurred -335 -290 -341 -303 -1,163 -704 -909 -1,038 -75 -163Change in othertechnical provisions 0 0 0 0 -30 13 0 0 0 0Premium rebates -2 -2 0 0 -2 -2 -34 -23 -5 -4Gross operating expenses -101 -98 -41 -48 -140 -161 -271 -294 -36 -61Profit/loss on business ceded 56 44 53 44 11 -5 0 1 6 10Change in equalisation provisions 2 0 0 4 8 1 -1 2 -11 -7Technical interest, net of reinsurance 33 38 34 35 71 78 34 39 8 11

Technical result 19 20 11 41 -502 -13 287 104 26 0

Gross claims ratio 92.0 89.0 111.4 98.1 161.0 90.3 63.4 74.5 56.0 77.6

Gross expense ratio 27.7 30.1 13.4 15.5 18.9 21.0 18.9 21.1 26.9 29.0

Fire and Fire and

contents contents Liability Other

(personal) (commercial) insurance insurance Total

2001 2000 2001 2000 2001 2000 2001 2000 2001 2000

Gross premiums written 1,339 1,240 1,223 1,133 319 301 29 51 5,975 5,797

Gross earned premiums 1,281 1,227 1,199 1,129 311 294 33 52 5,846 5,737

Gross claims incurred -934 -1,028 -838 -1,604 -265 -201 -44 -25 -4,904 -5,356

Change in other

technical provisions 0 0 0 0 0 0 0 0 -30 13

Premium rebates -6 -7 -3 -4 0 0 0 -1 -52 -43

Gross operating expenses -286 -301 -366 -370 -97 -98 -14 -24 -1,352 -1,455

Profit/loss on business ceded -33 21 -117 276 -17 21 0 -2 -41 410

Change in equalisation provisions 2 -8 -3 18 10 -6 0 -1 7 3

Technical interest, net of reinsurance 48 53 51 69 33 38 5 7 317 368

Technical result 72 -43 -77 -486 -25 48 -20 6 -209 -324

Gross claims ratio 73.3 84.3 70.1 142.6 85.2 68.4 133.3 49.0 85.2 93.8

Gross expense ratio 22.4 24.7 30.6 32.9 31.2 33.3 42.4 47.1 23.3 25.6

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

6 3URILW�IURP�JURXS�XQGHUWDNLQJV

Tryg Forsikring, livsforsikringsselskab A/S -135 435Tryg Forsikring II A/S -13 7Dansk Kautionsforsikrings-Aktieselskab 140 132Tryg-Baltica Forsikring, internationalt forsikringsselskab A/S -33 -79Tryg-Baltica International (UK) Ltd. 0 14Tryg Forsikring, Rejse og Sundhed A/S 7 5Tryg Ejendomme I A/S 211 123Nordea Ubezpieczenia, Poland -8 -12

��� ���

7 ,QWHUHVW��GLYLGHQGV�HWF

Dividend on shares 39 27Interest on securities etc 314 388Capital gains on drawing of and repayments on securities etc -10 -8

��� ���

8 5HDOLVHG�DQG�XQUHDOLVHG�LQYHVWPHQW

JDLQV�DQG�ORVVHV

Land and buildings 46 17Other shares -327 390Listed bonds, excluding index-linked bonds 38 -54Loans secured by mortgages 0 1Other loans 1 0

���� ���

:KLFK�KDYH�EHHQ�DOORFDWHG�WR�WKH�IROORZLQJ�LWHPV�LQ�WKH�DFFRXQW�

Net realised investment gains/losses -49 230Net unrealised investment gains/losses -192 123

���� ���

9 7D[

Tax relating to previous years 6 0Tax on the year’s income -12 -127Reimbursement from jointly-taxed companies 0 105Change in deferred tax asset*) 41 -3

�� ���

Tax paid on account in the accounting year 62 167

*) Of which change due to reduction of the corporation tax rate from 32% to 30%: 0 8

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

10 /DQG�DQG� XLOGLQJV

&RVW�RI�DFTXLVLWLRQ

Balance at 1 January 805 805Investments 2 4Sales 0 -4Balance at 31 December 807 805

8 ZD G� HYDOXDWLRQ

Balance at 1 January 26 12Upward revaluation 49 19Upward revaluation relating to previous years written back -2 -5Balance at 31 December 74 26

'RZQZD G� HYDOXDWLRQ

Balance at 1 January -8 -10Write-down -9 -2Downward revaluation relating to previous years written back 7 3Balance at 31 December -10 -8

��� ���

%RRN�YDOXH�E\�W\ H�RI� R H W\

Retail property 58 58Office property 647 625Residential property 166 139

��� ���

Of which properties held for the companies’ own use 86 69

Most recent property value (property valuation) 795 759Property not subject to public valuation 11 12

Mortgage debt amounts to DKK 67mon land and buildings with a book value of DKK 179m

In the determination of the market value of propertiesthe following rates of return have been used:

Lowest Average Highest(%) (%) (%)

2001/2000 2001/2000 2001/2000

Retail property 8,0 / 9,0 8,0 / 9,0 8,0 / 9,0Office property 6,3 / 6,8 7,3 / 8,0 8,0 / 9,0Residential property 5,5 / 6,0 6,1 / 6,8 8,0 / 8,0

All property 5,5 / 6,0 7,1 / 7,9 8,0 / 9,0

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

11 6KDUHV�LQ�JURXS�XQGHUWDNLQJV

&RVW�RI�DFTXLVLWLRQ

Balance at 1 January 5,782 5,124Additions 53 690Disposals -1 -32Balance at 31 December 5,834 5,782

8SZDUG�UHYDOXDWLRQ�DFFRUGLQJ�WR�WKH�HTXLW\�PHWKRG

Balance at 1 January 734 673Upward revaluation 64 61Balance at 31 December 798 734

'RZQZDUG�UHYDOXDWLRQ

Balance at 1 January -509 -310Downward revaluation -41 -199Dividend distributed -100 0Downward revaluation relating to previous years written back 151 0Balance at 31 December -499 -509

%RRN�YDOXH�DW����'HFHPEHU ����� �����

Profit/loss Share-Shareholding for holders’

1DPH�DQG�UHJLVWHUHG�RIILFH (%) the year equity

Tryg Forsikring, livsforsikringsselskab A/S, Ballerup 100 -135 2,906Tryg Ejendomme I A/S, Ballerup 100 211 1,819Tryg-Baltica Forsikring,internationalt forsikringsselskab A/S, Ballerup 100 -33 559Dansk Kautionsforsikringsaktieselskab, Ballerup 100 140 404Nordea Ubezpieczenia, Poland 69 -12 249Tryg Forsikring II A/S, Ballerup 100 -13 210Tryg Forsikring, Rejse og Sundhed A/S, Ballerup 100 7 59A/S KBIL 9 nr. 2032, Ballerup 100 0 5

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P� ���� ����

12 6KDUHV

%RRN�YDOXH ����� �����

Cost of acquisition 1,253 1,358

6KDUHKROGLQJV�H[FHHGLQJ����RI�WKH�FRPSDQLHV�VKDUH Shareholders’ ShareholdingFDSLWDO�DFFRUGLQJ�WR�WKH�ODWHVW�DQQXDO�DFFRXQWV� equity (%)

���� ����

Account Data A/S, Copenhagen 1 14A/S Forsikringens hus, Copenhagen 43 12Glud og Marstrand Invest A/S, Løsning 310 5Rungstedgaard A/S, Lyngby-Taarbæk 26 18

13 2WKHU�ILQDQFLDO�LQYHVWPHQWV

%RRN�YDOXH

Shares 1,575 1,810Ordinary bonds 3,003 3,433International bonds 662 442Loans secured by mortgages 189 185Other loans 84 88Deposits with credit institutions 0 59

����� �����

&RVW�RI�DFTXLVLWLRQ

Shares 1,253 1,358Bonds 3,597 3,906Loans secured by mortgages 185 179Other loans 83 87Deposits with credit institutions 0 59

����� �����

14 7RWDO�DVVHWV

Assets include group undertakings as follows:Shares 23 86Bonds 160 33Cash at bank and in hand 9 0

192 119

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

15 6KDUHKROGHUV�HTXLW\

6KDUH�FDSLWDO

Balance at 1 January 1,000 1,000Balance at 31 December ����� �����

The share capital is divided into shares of DKK 20 each.

5HYDOXDWLRQ�DFFRXQW

Balance at 1 January 26 12Transferred according to the distribution of profit 48 14Balance at 31 December �� ��

&RQWLQJHQF\�UHVHUYH

Balance at 1 January 1,823 2,514Transferred according to the distribution of profit -527 -691Balance at 31 December ����� �����

According to the Articles of Association, the funds of the contingency reservemay be applied for covering losses in connection with the payment of insurance liabilitiesor otherwise for the benefit of the policyholders. The contingency reserve is taxed.

1HW�UHYDOXDWLRQ�UHVHUYH�DFFRUGLQJ�WR�WKH�HTXLW\�PHWKRG

Balance at 1 January 745 668Transferred according to the distribution of profit 64 77Balance at 31 December ��� ���

5HWDLQHG�SURILW

Balance at 1 January 2,310 2,283Profit retained for the year 167 27Balance at 31 December ����� �����

7RWDO�VKDUHKROGHUV�HTXLW\ ����� �����

16 *URVV�SURYLVLRQV

�RXWVWDQGLQJ�FODLPV�SURYLVLRQV� ����� �����

Of which provisions calculated in view ofdiscounting:Accident and sickness insurance 101 109

Running-off period 11 år 12 årDiscount rate 3,0% 3,0%Inflation 0.0% 0.0%

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

17 3URYLVLRQV�IRU�DQQXLWLHV

Workmen’s compensation insurance 927 939

Running-off period 15 years 15 yearsDiscount rate 2,75% 2,75%Inflation 0% 0%

18 (TXDOLVDWLRQ�SURYLVLRQV

Workmen’s compensation 74 74Large claims 21 55Storms 110 83

��� ���

19 2WKHU�WHFKQLFDO�SURYLVLRQV��QHW�RI�UHLQVXUDQFH

Provisions for risk increasing with age 4 4Provisions for risk not yet run off 32 2

�� �

20 'HIHUUHG�WD[�DVVHW

Land and buildings 9 -2Bonds and loans secured by mortgages -22 5Machinery, equipment and provisions etc 181 125

168 128

7D[�DVVHWV ��� ���

21 &UHGLWRUV ��� �����

Of which amounts falling due after 5 years 67 67

22 6ROYHQF\�PDUJLQ�DQG�FRUH�FDSLWDO

Solvency margin 1,038 834

Core capital (shareholders’ equity) according to the balance sheet 5,655 5,904Tax asset -168 -128Solvency requirements of subsidiary undertakings -3,386 -2,778Total core capital 2,101 2,998

Total free core capital 1,063 2,164

7U\J�)RUVLNULQJ�$�6���

1RWHV

'..P ���� ����

23 )RUZDUG�WUDQVDFWLRQV�HWF

Forward transactions0DUNHW�YDOXHV

Forward currency sold 1,302 531Unsettled transactions 85 0

&RVW�RI�DFTXLVLWLRQ

Forward currency sold 1,279 540Unsettled transactions 86 0

24 &RQWLQJHQW�OLDELOLWLHV

Non-insurance guarantee and lease commitments etcdo not exceed 200 125

Tryg Forsikring A/S has an annual liability towards Danica to pay rent for the head office at Ballerup. The annual rent and taxes etc currently amount to DKK 65m.The remaining term of the lease is 24 years.

The Company is jointly taxed with the majority of the companies of the Tryg Group,and is jointly and severally liable with these companies for the payment of corporation tax.

In terms of payroll tax and VAT, the Company is jointly registered with the majority ofthe companies of the Nordea AB Group, and is jointly and severally liable with thesecompanies for the payment of such taxes.

25 ,QWUDJURXS�WUDQVDFWLRQV

Tryg Forsikring A/S provides administrative services for the majority of the companiesof the Tryg Group. The management fee has been fixed on a cost basis.

Portfolio management for the Tryg Group is undertaken by Nordea Bank Danmark A/Swith settlement on market-based terms

A significant part of the Group’s securities trading is undertaken by Nordea Bank Danmark A/S.Furthermore securities have been traded between companies of the insurance group.All such transactions have been settled at market value.

The Company has entered into reinsurance contracts and agreements with other companies of the Group on intragroup balances on market-based terms.

The Company has commitments with Nordea Bank Danmark A/S in the form of debt securities in issue and lending.