TRUTH IN SAVINGS DISCLOSURE - Personal & Business...

23

TRUTH IN SAVINGS DISCLOSURE Account Type: Account #: Date: Minimum Balance Requirements Free Checking A minimum deposit of $20 is required to open account Service Charges Interest Additional Terms There is no monthly service cycle charge for this account. No interest will be paid on this account Additional Fees This account does not qualify for Debit/Credit Card Reward Points. * A $5.00 monthly Dormant fee will be assessed if your account reaches Dormant account status. (See Additional Terms below) Your account will be placed in Dormant Status after 12 months of Inactivity. Once an account reaches Dormant account status, you will no longer receive periodic statements and/or eStatement notifications. This disclosure contains the rules which govern your deposit account. Unless it would be inconsistent to do so, words and phrases used in this disclosure should be construed so that the singular includes the plural and the plural includes the singular. If the primary account holder is not actively enrolled in eStatements at any time, for any reason, the account will be converted to an Easy Checking account. Upon conversion, paper statement fee may be assessed. See Easy Checking Disclosure on page 2* for paper statement fee provisions. If the primary account holder has enrolled in eStatements, they will receive an email notification when their statement is ready for viewing at www.gulfbank.com. (see Gulf Coast Bank & Trust Co. Internet Banking and eSign Disclosure). Images of processed items are available online. Active internet banking account and email address is required at all times. See Notice of Disclosure for Services and Fees for a list of additional fees that may apply. Check printing fees may apply - Prices will vary 200 St. Charles Ave., New Orleans, LA 70130 504-561-6124 1-800-223-2060 If the primary account holder has not enrolled for eStatements within 30 days from account opening, the account will be converted to an Easy Checking Account. Upon conversion, paper statement fee may be assessed. See Easy Checking Disclosure on page 2* for paper statement fee provisions. Page 1 FREETIS-1 REV 9/15 The primary account holder MUST enroll in eStatements via their personal computer at www.gulfbank.com within 30 days of opening the account. The primary account holder MUST maintain an active internet banking account and current, active email address. (See Gulf Coast Bank and Trust Co. Internet Banking and eSign Disclosure).

Transcript of TRUTH IN SAVINGS DISCLOSURE - Personal & Business...

TRUTH IN SAVINGS DISCLOSUREAccount Type:Account #:Date:

Minimum Balance Requirements

Free Checking

A minimum deposit of $20 is required to open account

Service Charges

Interest

Additional Terms

There is no monthly service cycle charge for this account.

No interest will be paid on this account

Additional Fees

This account does not qualify for Debit/Credit Card Reward Points.

* A $5.00 monthly Dormant fee will be assessed if your account reaches Dormant account status. (See AdditionalTerms below)

Your account will be placed in Dormant Status after 12 months of Inactivity. Once an account reachesDormant account status, you will no longer receive periodic statements and/or eStatement notifications.

This disclosure contains the rules which govern your deposit account. Unless it would be inconsistent to do so,words and phrases used in this disclosure should be construed so that the singular includes the plural and theplural includes the singular.

If the primary account holder is not actively enrolled in eStatements at any time, for any reason, the account willbe converted to an Easy Checking account. Upon conversion, paper statement fee may be assessed. SeeEasy Checking Disclosure on page 2* for paper statement fee provisions.

If the primary account holder has enrolled in eStatements, they will receive an email notification when theirstatement is ready for viewing at www.gulfbank.com. (see Gulf Coast Bank & Trust Co. Internet Banking andeSign Disclosure). Images of processed items are available online. Active internet banking account and emailaddress is required at all times.

See Notice of Disclosure for Services and Fees for a list of additional fees that may apply.

Check printing fees may apply - Prices will vary

200 St. Charles Ave., New Orleans, LA 70130 504-561-6124 1-800-223-2060

If the primary account holder has not enrolled for eStatements within 30 days from account opening, the accountwill be converted to an Easy Checking Account. Upon conversion, paper statement fee may be assessed.See Easy Checking Disclosure on page 2* for paper statement fee provisions.

Page 1

FREETIS-1 REV 9/15

The primary account holder MUST enroll in eStatements via their personal computer at www.gulfbank.com within30 days of opening the account. The primary account holder MUST maintain an active internet banking accountand current, active email address. (See Gulf Coast Bank and Trust Co. Internet Banking and eSign Disclosure).

TRUTH IN SAVINGS DISCLOSURE

Account Type:Account #:Date:

Minimum Balance Requirements

Easy Checking Converted from Free Checking

A minimum deposit of $20 is required to open account

Service Charges

Interest

Additional Terms

There is no monthly service cycle charge for this account.

No interest will be paid on this account

Additional Fees

This account does not qualify for Debit/Credit Card Reward Points.

A $5.00 monthly Dormant fee will be assessed if your account reaches Dormant account status.

Your account will be placed in Dormant Status after 12 months of Inactivity. Once an account reaches Dormantaccount status, you will no longer receive periodic statements and/or eStatement notifications.

This disclosure contains the rules which govern your deposit account. Unless it would be inconsistent to do so, words andphrases used in this disclosure should be construed so that the singular includes the plural and the plural includes thesingular.

If the primary account holder is not actively enrolled in eStatements at any time, for any reason, they will receivea monthly paper statement mailed to their address of record. (See Additional Fees above) *

If the primary account holder has enrolled in eStatements, they will receive an email notification when theirstatement is ready for viewing at www.gulfbank.com. (see Gulf Coast Bank & Trust Co. Internet Banking andeSign Disclosure). Images of processed items are available online. Active internet banking account and emailaddress is required at all times.

See Notice of Disclosure for Services and Fees for a list of additional fees that may apply.

Check printing fees may apply - Prices will vary

200 St. Charles Ave., New Orleans, LA 70130 504-561-6124 1-800-223-2060

Page 2

FREETIS-2 REV 7/17

If the primary account holder decides to cancel their eStatement at any time or we have reason to believe that theyare not receiving their eStatement or eNotification, a $4.85 monthly paper statement fee will be assessed unless theaverage month to date balance of $5,000 or greater OR average month to date balance of $25,000 or greater inqualifying deposits applies.The primary account holder must maintain an active internet banking account and current , active email address. (See Gulf Coast Bank and Trust Co. Internet Banking and eSign Disclosure)

Monthly Paper Statement fee of $4.85. Monthly paper statement fee waived if one of the following is met:

Average month to date balance of $5,000 or greater ORAverage month to date balance of $25,000 or greater in qualifying deposits (See Additional Terms for qualifyingaccounts) ORAccount is set up for eStatements

Qualifying deposits includes all personal or business checking, savings or certificates of deposits that are directlylinked to this account.

Important Information About Procedures

To help the government fight the funding of terrorism and money

laundering activities, Federal law requires all financial institutions

to obtain, verify, and record information that identifies each

person who opens an account. What this means for you: When

you open an account, we will ask for your name, address, date of

birth, and other information that will allow us to identify you. We

will ask to see your driver's license or other identifying

documents.

for Opening a New Account

CIP-1 REV 10/08

GULF COAST BANK & TRUST COMPANYFUNDS AVAILABILITY POLICY

As a customer of our financial services, you need to know when the funds you deposit by check to your checking account areavailable for you to withdraw and use…

What is it?Funds Availability refers to the time that passes before funds deposited in your account are actually available to you for checkwriting and cash withdrawals. Our policy has been designed to give you quality service, meet regulatory requirements and protectboth you and ourselves from loss.This policy is in effect beginning August 1 2016, and if we decide to change or further improve any of the availability scheduleslisted in this disclosure, we will notify you within 30 days of any such change.

This information should take some of the 'guesswork' out of the management of your personal finances. We recommend that youkeep this brochure with your other account records so that you may refer to it in the future.

If you have any questions, please stop in and ask…we'd be happy to answer your questions.

When deposits are available for withdrawalOur policy is to make funds from your deposits available to you on the next business day after the day of your deposit. Electronicdirect deposits will be available on the day we receive your deposit. Once they are available, you can withdraw the funds in cash andwe will use the funds to pay checks that you have written.

For determining the availability of your deposits, every day is a business day, except Saturdays, Sundays, and Federal holidays. Ifyou make a deposit before 6:00 p.m. on a business day that we are open, we will consider that day to be the day of your deposit.However, if you make a deposit after 6:00 p.m. or on a day we are not open we will consider that the deposit was made on the nextbusiness day we are open.

Longer delays may apply

In some cases, we will not make all of the funds that you deposit by check available to you on the next business day of yourdeposit. Depending on the type of check that you deposit, funds may not be available until the second business day after the dayof your deposit. However, the first $200 of your deposit will be available on the next business day.

If we are not going to make all of the funds from your deposit available on the next business day, we will notify you at the time youmake your deposit. We will also tell you when the funds will be available. If your deposit is not made directly with one of ouremployees, or if we decide to take this action after you have left the premises, we will mail you the notice by the day after wereceive your deposit.If you will need the funds from a deposit right away, you should ask us when the funds will be available.In addition, funds you deposit by check may be delayed for a longer period under the following circumstances:

-We believe a check you deposit will not be paid. -You deposit checks totaling more than $5,000 on any one day. -You redeposit a check that has been returned unpaid. -You have overdrawn your account repeatedly in the last six months. -There is an emergency, such as failure of communications or computer equipment.

We will notify you if we delay your ability to withdraw funds for any of these reasons, and we will tell you when the funds will beavailable. They will generally be available no later than the seventh business day after the day of your deposit.

Special rules for new accountsIf you are a new customer, the following special rules may apply during the first 30 days your account is open.

Funds from electronic direct deposits to your account will be available on the day we received the deposit. Funds from deposits ofcash, wire transfers and the first $5,000 of a day's total deposits of cashier's, certified, teller's traveler's and Federal, state and localgovernment checks will be available on the next business day after the day of your deposit if the deposit meets certain conditions.For example, the checks must be payable to you. If your deposit of these checks (other than a U.S. Treasury check) is not made inperson to one of our employees, the first $5,000 will not be available until the second business day after the day of your deposit.The excess over $5,000 will be available on the ninth business day after the day of the deposit.

Funds from all other check deposits will be available on the ninth business day after the day of your deposit.

FUNDS Rev.2/18

If you make a deposit after the ATM cutoff time, we will consider the deposit to have been made on the next business day. TheATM screen will notify you of the cutoff time.

Terms and Conditions of Your Account

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 1 of 10

Contents:Important Information about Procedures forOpening a New AccountAgreementLiabilityDepositsWithdrawals

Ownership of Account and BeneficiaryDesignation

Business, Organization, and AssociationAccountsStop PaymentsTelephone TransfersAmendments and TerminationNoticesStatements

(13)(14)(15)(16)(17)(18)

(19)(20)(21)(22)(23)(24)(25)(26)(27)(28)(29)(30)(31)(32)(33)

(34)(35)(36)(37)(38)(39)

Direct DepositsTemporary Account AgreementSetoffCheck ProcessingCheck CashingTruncation, Substitute Checks, and OtherCheck ImagesRemotely Created ChecksUnlawful Internet Gambling NoticeACH and Wire TransfersFacsimile SignaturesAuthorized SignerRestrictive Legends or IndorsementsAccount TransferIndorsementsDeath or IncompetenceFiduciary AccountsCredit VerificationLegal Actions Affecting Your AccountSecurityTelephonic InstructionsMonitoring and Recording Telephone Callsand Consent to Receive CommunicationsClaim of LossEarly Withdrawal PenaltiesAddress or Name ChangesResolving Account DisputesWaiver of NoticesAdditional Terms

1.

(1)

(2)(3)(4)(5)

(6)

(7)

(8)(9)(10)(11)(12)

What this means for you: When you open an account, wewill ask for your name, address, date of birth, and otherinformation that will allow us to identify you. We may alsoask to see your driver' s license or other identifyingdocuments.

(1) Important Information about Procedures forOpening a New Account. To help the government fightthe funding of terrorism and money laundering activities,federal law requires all financial institutions to obtain,verify, and record information that identifies each personwho opens an account.

to use the account, you agree to these rules. You willreceive a separate schedule of rates, qualifying balances, andfees if they are not included in this document. If you haveany questions, please call us.

summarize some laws that apply to commontransactions;

2. establish rules to cover transactions or events which thelaw does not regulate;

This agreement is subject to applicable federal laws, thelaws of the state of Louisiana and other applicable rules suchas the operating letters of the Federal Reserve Banks andpayment processing system rules (except to the extent thatthis agreement can and does vary such rules or laws). Thebody of state and federal law that governs our relationshipwith you, however, is too large and complex to bereproduced here. The purpose of this document is to:

GenerallyPostdated ChecksChecks and Withdrawal RulesA Temporary Debit Authorization HoldAffects Your Account BalanceOverdraftsMultiple Signatures, Electronic CheckConversion, and Similar TransactionsNotice of Withdrawal

Individual Account Joint AccountRevocable Trust or Pay-On-Death Account

Your Duty to Report UnauthorizedSignatures, Alterations, and Forgeries Your Duty to Report Other Errors Errors Relating to Electronic Fund Transfersor Substitute Checks

(2) Agreement. This document, along with any otherdocuments we give you pertaining to your account(s), is acontract that establishes rules which control your account(s)with us. Please read this carefully and retain it for futurereference. If you sign the signature card or open or continue

an interest in your account. This also includes any actionthat you or a third party takes regarding the account thatcauses us, in good faith, to seek the advice of an attorney,whether or not we become involved in the dispute. All costsand attorneys' fees can be deducted from your account whenthey are incurred, without notice to you.

(5) Withdrawals.Generally. Unless clearly indicated otherwise on theaccount records, any of you, acting alone, who signs toopen the account or has authority to make withdrawalsmay withdraw or transfer all or any part of the accountbalance at any time. Each of you (until we receive writtennotice to the contrary) authorizes each other person whosigns or has authority to make withdrawals to indorse anyitem payable to you or your order for deposit to thisaccount or any other transaction with us.Postdated Checks. A postdated check is one whichbears a date later than the date on which the check iswritten. We may properly pay and charge your accountfor a postdated check even though payment was madebefore the date of the check, unless we have receivedwritten notice of the postdating in time to have areasonable opportunity to act. Because we process checksmechanically, your notice will not be effective and wewill not be liable for failing to honor your notice unless it

4. give you disclosures of some of our policies to whichyou may be entitled or in which you may be interested.

establish rules for certain transactions or events whichthe law regulates but permits variation by agreement;and

3.

Each of you also agrees to be jointly and severally (insolido) liable for any account shortage resulting fromcharges or overdrafts, whether caused by you or anotherwith access to this account. This liability is dueimmediately, and can be deducted directly from the accountbalance whenever sufficient funds are available. You haveno right to defer payment of this liability, and you are liableregardless of whether you signed the item or benefited fromthe charge or overdraft.

You will be liable for our costs as well as for our reasonableattorneys' fees, to the extent permitted by law, whetherincurred as a result of collection or in any other disputeinvolving your account. This includes, but is not limited to,disputes between you and another joint owner; you and anauthorized signer or similar party; or a third party claiming

(3) Liability. You agree, for yourself (and the person orentity you represent if you sign as a representative ofanother) to the terms of this account and the schedule ofcharges. You authorize us to deduct these charges, withoutnotice to you, directly from the account balance as accrued.You will pay any additional reasonable charges for servicesyou request which are not covered by this agreement.

"Party" means a person who, by the terms of an account,has a present right, subject to request, to payment from theaccount other than as a beneficiary or agent.

If any provision of this document is found to beunenforceable according to its terms, all remainingprovisions will continue in full force and effect. We maypermit some variations from our standard agreement, but wemust agree to any variation in writing either on the signaturecard for your account or in some other document. Nothingin this document is intended to vary our duty to act in goodfaith and with ordinary care when required by law.

(4) Deposits. We will give only provisional credit untilcollection is final for any items, other than cash, we acceptfor deposit (including items drawn "on us"). Beforesettlement of any item becomes final, we act only as youragent, regardless of the form of indorsement or lack ofindorsement on the item and even though we provide youprovisional credit for the item. We may reverse anyprovisional credit for items that are lost, stolen, or returned.Unless prohibited by law, we also reserve the right to chargeback to your account the amount of any item deposited toyour account or cashed for you which was initially paid bythe payor bank and which is later returned to us due to anallegedly forged, unauthorized or missing indorsement,claim of alteration, encoding error or other problem whichin our judgment justifies reversal of credit. You authorize usto attempt to collect previously returned items withoutgiving you notice, and in attempting to collect we maypermit the payor bank to hold an item beyond the midnightdeadline. Actual credit for deposits of, or payable in,foreign currency will be at the exchange rate in effect onfinal collection in U.S. dollars. We are not responsible fortransactions by mail or outside depository until we actuallyrecord them. We will treat and record all transactionsreceived after our "daily cutoff time" on a business day weare open, or received on a day we are not open for business,as if initiated on the next business day that we are open. Atour option, we may take an item for collection rather thanfor deposit. If we accept a third-party check for deposit, wemay require any third-party indorsers to verify or guaranteetheir indorsements, or indorse in our presence.

As used in this document the words "we," "our," and "us"mean the financial institution and the words "you" and"your" mean the account holder(s) and anyone else with theauthority to deposit, withdraw, or exercise control over thefunds in the account. However, this agreement does notintend, and the terms "you" and "your" should not beinterpreted, to expand an individual' s responsibility for anorganization' s liability. If this account is owned by acorporation, partnership or other organization, individualliability is determined by the laws generally applicable tothat type of organization. The headings in this document arefor convenience or reference only and will not govern theinterpretation of the provisions. Unless it would beinconsistent to do so, words and phrases used in thisdocument should be construed so the singular includes theplural and the plural includes the singular.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 2 of 10

You have $120 in your account. You swipe your card atthe card reader on a gasoline pump. Since it is unclearwhat the final bill will be, the gas station' s processingsystem immediately requests a hold on your account in aspecified amount, for example, $80. Our processingsystem authorizes a temporary hold on your account inthe amount of $80, and the gas station' s processingsystem authorizes you to begin pumping gas. You fillyour tank and the amount of gasoline you purchased isonly $50. Our processing system shows that you have$40 in your account available for other transactions ($120- $80 = $40) even though you would have $70 in youraccount available for other transactions if the amount ofthe temporary hold was equal to the amount of yourpurchase ($120 - $50 = $70). Later, another transactionyou have authorized is presented for payment from youraccount in the amount of $60 (this could be a check youhave written, another debit card transaction, an ACHdebit or any other kind of payment request). This othertransaction is presented before the amount of thetemporary hold is adjusted to the amount of yourpurchase (remember, it may take up to three days for theadjustment to be made). Because the amount of this othertransaction is greater than the amount our processingsystem shows is available in your account, our paymentof this transaction will result in an overdraft transaction.Because the transaction overdraws your account by $20,your account will be assessed the overdraft fee of $35according to our overdraft fee policy. You will becharged this $35 fee according to our policy even thoughyou would have had enough money in your account tocover the $60 transaction if your account had only beendebited the amount of your purchase rather than theamount of the temporary hold or if the temporary holdhad already been adjusted to the actual amount of yourpurchase.

precisely identifies the number, date, amount and payeeof the item.

If we are presented with an item drawn against youraccount that would be a "substitute check," as defined bylaw, but for an error or defect in the item introduced inthe substitute check creation process, you agree that wemay pay such item.See the funds availability policy disclosure forinformation about when you can withdraw funds youdeposit. For those accounts to which our fundsavailability policy disclosure does not apply, you can askus when you make a deposit when those funds will beavailable for withdrawal. An item may be returned afterthe funds from the deposit of that item are made availablefor withdrawal. In that case, we will reverse the credit ofthe item. We may determine the amount of availablefunds in your account for the purpose of decidingwhether to return an item for insufficient funds at anytime between the time we receive the item and when wereturn the item or send a notice in lieu of return. We needonly make one determination, but if we choose to make asubsequent determination, the account balance at thesubsequent time will determine whether there areinsufficient available funds.

transactions will be reduced by the amount of thetemporary hold. If another transaction is presented forpayment in an amount greater than the funds left after thededuction of the temporary hold amount, that transactionwill be a nonsufficient funds (NSF) transaction if we donot pay it or an overdraft transaction if we do pay it. Youwill be charged an NSF or overdraft fee according to ourNSF or overdraft fee policy. You will be charged the feeeven if you would have had sufficient funds in youraccount if the amount of the hold had been equal to theamount of your purchase.

Here is an example of how this can occur - assume forthis example the following: (1) you have opted-in to ouroverdraft services for the payment of overdrafts on ATMand everyday debit card transactions, (2) we pay theoverdraft, and (3) our overdraft fee is $35 per overdraft,but we do not charge the overdraft fee if the transactionoverdraws the account by less than $10.

Checks and Withdrawal Rules. If you do not purchaseyour check blanks from us, you must be certain that weapprove the check blanks you purchase. We may refuseany withdrawal or transfer request which you attempt onforms not approved by us or by any method we do notspecifically permit. We may refuse any withdrawal ortransfer request which is greater in number than thefrequency permitted, or which is for an amount greater orless than any withdrawal limitations. We will use the datethe transaction is completed by us (as opposed to the dateyou initiate it) to apply the frequency limitations. Inaddition, we may place limitations on the account untilyour identity is verified.

Overdrafts. You understand that we may, at ourdiscretion, honor withdrawal requests that overdraw youraccount. However, the fact that we may honor

Even if we honor a nonconforming request, we are notrequired to do so later. If you violate the statedtransaction limitations (if any), in our discretion we mayclose your account or reclassify it as a transactionaccount. If we reclassify your account, your account willbe subject to the fees and earnings rules of the newaccount classification.

A Temporary Debit Authorization Hold AffectsYour Account Balance. On debit card purchases,merchants may request a temporary hold on your accountfor a specified sum of money, which may be more thanthe actual amount of your purchase. When this happens,our processing system cannot determine that the amountof the hold exceeds the actual amount of your purchase.This temporary hold, and the amount charged to youraccount, will eventually be adjusted to the actual amountof your purchase, but it may be up to three days beforethe adjustment is made. Until the adjustment is made, theamount of funds in your account available for other

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 3 of 10

Multiple Signatures, Electronic Check Conversion,and Similar Transactions. An electronic checkconversion transaction is a transaction where a check orsimilar item is converted into an electronic fund transferas defined in the Electronic Fund Transfers regulation. Inthese types of transactions the check or similar item iseither removed from circulation (truncated) or given backto you. As a result, we have no opportunity to review thecheck to examine the signatures on the item. You agreethat, as to these or any items as to which we have noopportunity to examine the signatures, you waive anyrequirement of multiple signatures.

Revocable Trust or Pay-on-Death Account. If two ormore of you create such an account, you own the accountjointly and the respective interests of each of you shall bedeemed equal, unless otherwise stated in our accountrecords. Beneficiaries acquire the right to withdraw onlyif: (1) all persons creating the account die, and (2) thebeneficiary is then living. If two or more beneficiaries arenamed and survive the death of all persons creating theaccount, such beneficiaries will own this account in equalshares, unless otherwise stated in our account records.The person(s) creating either of these account typesreserves the right to: (1) change beneficiaries, (2) changeaccount types, and (3) withdraw all or part of the accountfunds at any time.

(8) Stop Payments. Unless otherwise provided, the rulesin this section cover stopping payment of items such aschecks and drafts. Rules for stopping payment of othertypes of transfers of funds, such as consumer electronicfund transfers, may be established by law or our policy. Ifwe have not disclosed these rules to you elsewhere, you mayask us about those rules.

You may stop payment on any item drawn on your accountwhether you sign the item or not. Generally, if yourstop-payment order is given to us in writing it is effectivefor six months. Your order will lapse after that time if youdo not renew the order in writing before the end of thesix-month period. If the original stop-payment order was

withdrawal requests that overdraw the account balancedoes not obligate us to do so later. So you can NOT relyon us to pay overdrafts on your account regardless ofhow frequently or under what circumstances we have paidoverdrafts on your account in the past. We can changeour practice of paying overdrafts on your account withoutnotice to you. You can ask us if we have other accountservices that might be available to you where we committo paying overdrafts under certain circumstances, such asan overdraft protection line-of-credit or a plan to sweepfunds from another account you have with us. You agreethat we may charge fees for overdrafts. For consumeraccounts, we will not charge fees for overdrafts causedby ATM withdrawals or one-time debit card transactionsif you have not opted-in to that service. We may usesubsequent deposits, including direct deposits of socialsecurity or other government benefits, to cover suchoverdrafts and overdraft fees.

to the heirs, legatees, or creditors of the deceased party tothe extent the funds withdrawn by the survivors wereowed to the deceased. If any party to a joint accountsends notice to us to prevent withdrawals from theaccount by another party or parties, we may require theparty to withdraw the balance and close the account or wemay refuse to allow any further withdrawals from theaccount except upon the written consent of all parties toit. The remedy we choose is entirely at our discretion.

Notice of Withdrawal. We reserve the right to requirenot less than 7 days' notice in writing before eachwithdrawal from an interest-bearing account other than atime deposit or demand deposit, or from any othersavings account as defined by Regulation D. (The lawrequires us to reserve this right, but it is not our generalpolicy to use it.) Withdrawals from a time account priorto maturity or prior to any notice period may be restrictedand may be subject to penalty. See your notice of penaltyfor early withdrawal.

(6) Ownership of Account and BeneficiaryDesignation. These rules apply to this account dependingon the form of ownership and beneficiary designation, ifany, specified on the account records. We make norepresentations as to the appropriateness or effect of theownership and beneficiary designations, except as theydetermine to whom we pay the account funds.

Individual Account. This is an account in the name ofone person.Joint Account. This is an account in the names of twoor more persons. Any one of such persons, acting alone,has complete access to the account. Upon the death ofany party to such account, we are permitted to pay theaccount balance to the surviving parties, but this authorityprotects us only. The surviving joint parties may be liable

(7) Business, Organization, and AssociationAccounts. Earnings in the form of interest, dividends, orcredits will be paid only on collected funds, unlessotherwise provided by law or our policy. You represent thatyou have the authority to open and conduct business on thisaccount on behalf of the entity. We may require thegoverning body of the entity opening the account to give usa separate authorization telling us who is authorized to acton its behalf. We will honor the authorization until weactually receive written notice of a change from thegoverning body of the entity.

We may accept an order to stop payment on any item fromany one of you. You must make any stop-payment order inthe manner required by law and we must receive it in timeto give us a reasonable opportunity to act on it before ourstop-payment cutoff time. Because stop-payment orders arehandled by computers, to be effective, your stop-paymentorder must precisely identify the number, date, and amountof the item, and the payee.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 4 of 10

If you stop payment on an item and we incur any damagesor expenses because of the stop payment, you agree toindemnify us for those damages or expenses, includingattorneys' fees. You assign to us all rights against the payeeor any other holder of the item. You agree to cooperate withus in any legal actions that we may take against suchpersons. You should be aware that anyone holding the itemmay be entitled to enforce payment against you despite thestop-payment order.

Our stop-payment cutoff time is one hour after the openingof the next banking day after the banking day on which wereceive the item. Additional limitations on our obligation tostop payment are provided by law (e.g., we paid the item incash or we certified the item).

(9) Telephone Transfers. A telephone transfer of fundsfrom this account to another account with us, if otherwisearranged for or permitted, may be made by the samepersons and under the same conditions generally applicableto withdrawals made in writing. Unless a different limitationis disclosed in writing, we restrict the number of transfersfrom a savings account to another account or to thirdparties, to a maximum of six per month (less the number of"preauthorized transfers" during the month). Other accounttransfer restrictions may be described elsewhere.

reasonable opportunity to act on it. If the notice is regardinga check or other item, you must give us sufficientinformation to be able to identify the check or item,including the precise check or item number, amount, dateand payee. Written notice we give you is effective when it isdeposited in the United States Mail with proper postage andaddressed to your mailing address we have on file. Notice toany of you is notice to all of you.

(11) Notices. Any written notice you give us is effectivewhen we actually receive it, and it must be given to usaccording to the specific delivery instructions providedelsewhere, if any. We must receive it in time to have a

Your Duty to Report Unauthorized Signatures,Alterations, and Forgeries. You must examine yourstatement of account with "reasonable promptness." Ifyou discover (or reasonably should have discovered) anyunauthorized signatures or alterations, you must promptlynotify us of the relevant facts. As between you and us, ifyou fail to do either of these duties, you will have toeither share the loss with us, or bear the loss entirelyyourself (depending on whether we used ordinary careand, if not, whether we substantially contributed to theloss). The loss could be not only with respect to items onthe statement but other items with unauthorized signaturesor alterations by the same wrongdoer.

You agree that the time you have to examine yourstatement and report to us will depend on thecircumstances, but will not, in any circumstance, exceeda total of 30 days from when the statement is first sent ormade available to you.

You further agree that if you fail to report anyunauthorized signatures, alterations or forgeries in youraccount within 60 days of when we first send or make thestatement available, you cannot assert a claim against uson any items in that statement, and as between you and usthe loss will be entirely yours. This 60-day limitation iswithout regard to whether we used ordinary care. Thelimitation in this paragraph is in addition to that containedin the first paragraph of this section.

Your Duty to Report Other Errors. In addition to yourduty to review your statements for unauthorizedsignatures, alterations and forgeries, you agree toexamine your statement with reasonable promptness forany other error - such as an encoding error. In addition,if you receive or we make available either your items orimages of your items, you must examine them for anyunauthorized or missing indorsements or any otherproblems. You agree that the time you have to examineyour statement and items and report to us will depend onthe circumstances. However, this time period shall notexceed 60 days. Failure to examine your statement anditems and report any errors to us within 60 days of whenwe first send or make the statement available precludesyou from asserting a claim against us for any errors onitems identified in that statement and as between you andus the loss will be entirely yours.

(12) Statements.

oral your stop-payment order will lapse after 14 calendardays if you do not confirm your order in writing within thattime period. We are not obligated to notify you when astop-payment order expires. A release of the stop-paymentrequest may be made only by the person who initiated thestop-payment order.

(10) Amendments and Termination. We may changeany term of this agreement. Rules governing changes ininterest rates are provided separately in the Truth-in-Savings disclosure or in another document. For otherchanges, we will give you reasonable notice in writing or byany other method permitted by law. We may also close thisaccount at any time upon reasonable notice to you andtender of the account balance personally or by mail. Itemspresented for payment after the account is closed may bedishonored. When you close your account, you areresponsible for leaving enough money in the account tocover any outstanding items to be paid from the account.Reasonable notice depends on the circumstances, and insome cases such as when we cannot verify your identity orwe suspect fraud, it might be reasonable for us to give younotice after the change or account closure becomes effective.For instance, if we suspect fraudulent activity with respectto your account, we might immediately freeze or close youraccount and then give you notice. If we have notified you ofa change in any term of your account and you continue tohave your account after the effective date of the change, youhave agreed to the new term(s).

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 5 of 10

(14) Temporary Account Agreement. If the accountdocumentation indicates that this is a temporary accountagreement, each person who signs to open the account orhas authority to make withdrawals (except as indicated to thecontrary) may transact business on this account. However,we may at some time in the future restrict or prohibit furtheruse of this account if you fail to comply with therequirements we have imposed within a reasonable time.

(15) Setoff. We may (without prior notice and whenpermitted by law) set off the funds in this account againstany due and payable debt any of you owe us now or in thefuture. If this account is owned by one or more of you asindividuals, we may set off any funds in the account againsta due and payable debt a partnership owes us now or in thefuture, to the extent of your liability as a partner for thepartnership debt. If your debt arises from a promissorynote, then the amount of the due and payable debt will bethe full amount we have demanded, as entitled under theterms of the note, and this amount may include any portionof the balance for which we have properly accelerated thedue date.

(16) Check Processing. We process items mechanicallyby relying solely on the information encoded in magnetic

(17) Check Cashing. We may charge a fee for anyonethat does not have an account with us who is cashing acheck, draft or other instrument written on your account.We may also require reasonable identification to cash such acheck, draft or other instrument. We can decide whatidentification is reasonable under the circumstances and suchidentification may be documentary or physical and mayinclude collecting a thumbprint or fingerprint.(18) Truncation, Substitute Checks, and Other CheckImages. If you truncate an original check and create asubstitute check, or other paper or electronic image of theoriginal check, you warrant that no one will be asked tomake payment on the original check, a substitute check orany other electronic or paper image, if the paymentobligation relating to the original check has already beenpaid. You also warrant that any substitute check you createconforms to the legal requirements and generally acceptedspecifications for substitute checks. You agree to retain theoriginal check in conformance with our internal policy forretaining original checks. You agree to indemnify us for anyloss we may incur as a result of any truncated checktransaction you initiate. We can refuse to accept substitutechecks that have not previously been warranted by a bank orother financial institution in conformance with the Check 21Act. Unless specifically stated in a separate agreementbetween you and us, we do not have to accept any otherelectronic or paper image of an original check.(19) Remotely Created Checks. Like any standard checkor draft, a remotely created check (sometimes called atelecheck, preauthorized draft or demand draft) is a check ordraft that can be used to withdraw money from an account.Unlike a typical check or draft, however, a remotely createdcheck is not issued by the paying bank and does not containthe signature of the account owner (or a signature purportedto be the signature of the account owner). In place of asignature, the check usually has a statement that the ownerauthorized the check or has the owner' s name typed orprinted on the signature line.

Errors Relating to Electronic Fund Transfers orSubstitute Checks (For consumer accounts only). Forinformation on errors relating to electronic fund transfers(e.g., computer, debit card or ATM transactions) refer toyour Electronic Fund Transfers disclosure and thesections on consumer liability and error resolution. Forinformation on errors relating to a substitute check youreceived, refer to your disclosure entitled SubstituteChecks and Your Rights.

(13) Direct Deposits. If we are required for any reason toreimburse the federal government for all or any portion of abenefit payment that was directly deposited into youraccount, you authorize us to deduct the amount of ourliability to the federal government from the account or fromany other account you have with us, without prior noticeand at any time, except as prohibited by law. We may alsouse any other legal remedy to recover the amount of ourliability.

ink along the bottom of the items. This means that we donot individually examine all of your items to determine ifthe item is properly completed, signed and indorsed or todetermine if it contains any information other than what isencoded in magnetic ink. You agree that we have exercisedordinary care if our automated processing is consistent withgeneral banking practice, even though we do not inspecteach item. Because we do not inspect each item, if you writea check to multiple payees, we can properly pay the checkregardless of the number of indorsements unless you notifyus in writing that the check requires multiple indorsements.We must receive the notice in time for us to have areasonable opportunity to act on it, and you must tell us theprecise date of the check, amount, check number and payee.We are not responsible for any unauthorized signature oralteration that would not be identified by a reasonableinspection of the item. Using an automated process helps uskeep costs down for you and all account holders.

This right of setoff does not apply to this account ifprohibited by law. For example, the right of setoff does notapply to this account if: (a) it is an Individual RetirementAccount or similar tax-deferred account, or (b) the debt iscreated by a consumer credit transaction under a credit cardplan (but this does not affect our rights under anyconsensual security interest), or (c) the debtor' s right ofwithdrawal only arises in a representative capacity, or (d)setoff is prohibited by the Military Lending Act or itsimplementing regulations. We will not be liable for thedishonor of any check when the dishonor occurs because weset off a debt against this account. You agree to hold usharmless from any claim arising as a result of our exerciseof our right of setoff.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 6 of 10

(20) Unlawful Internet Gambling Notice. Restrictedtransactions as defined in Federal Reserve Regulation GGare prohibited from being processed through this account orrelationship. Restricted transactions generally include, butare not limited to, those in which credit, electronic fundtransfers, checks, or drafts are knowingly accepted bygambling businesses in connection with the participation byothers in unlawful Internet gambling.

(24) Restrictive Legends or Indorsements. Theautomated processing of the large volume of checks wereceive prevents us from inspecting or looking for restrictivelegends, restrictive indorsements or other specialinstructions on every check. Examples of restrictive legendsplaced on checks are "must be presented within 90 days" or"not valid for more than $1,000.00." The payee' s signatureaccompanied by the words "for deposit only" is an exampleof a restrictive indorsement. For this reason, we are notrequired to honor any restrictive legend or indorsement orother special instruction placed on checks you write unlesswe have agreed in writing to the restriction or instruction.Unless we have agreed in writing, we are not responsiblefor any losses, claims, damages, or expenses that resultfrom your placement of these restrictions or instructions onyour checks.

(22) Facsimile Signatures. Unless you make advancearrangements with us, we have no obligation to honorfacsimile signatures on your checks or other orders. If wedo agree to honor items containing facsimile signatures, youauthorize us, at any time, to charge you for all checks,drafts, or other orders, for the payment of money, that aredrawn on us. You give us this authority regardless of bywhom or by what means the facsimile signature(s) may havebeen affixed so long as they resemble the facsimile signaturespecimen filed with us, and contain the required number ofsignatures for this purpose. You must notify us at once ifyou suspect that your facsimile signature is being or hasbeen misused.

(23) Authorized Signer (Agent) (Individual Accountsonly). A single individual is the owner. The authorizedsigner (hereinafter "agent") is merely designated to conducttransactions on the owner' s behalf. The owner does not giveup any rights to act on the account, and the agent may not inany manner affect the rights of the owner or beneficiaries, ifany, other than by withdrawing funds from the account. Theowner is responsible for any transactions of the agent. Weundertake no obligation to monitor transactions to determinethat they are on the owner' s behalf. The owner mayterminate the agency at any time, and the agency isautomatically terminated by the death of the owner.However, we may continue to honor the transactions of theagent until: (a) we have received written notice or haveactual knowledge of the termination of the agency, and (b)we have a reasonable opportunity to act on that notice orknowledge. We may refuse to accept an agent.

(25) Account Transfer. This account may not betransferred or assigned without our prior written consent.

(26) Indorsements. We may accept for deposit any itempayable to you or your order, even if they are not indorsedby you. We may give cash back to any one of you. We maysupply any missing indorsement(s) for any item we acceptfor deposit or collection, and you warrant that allindorsements are genuine.To ensure that your check or share draft is processedwithout delay, you must indorse it (sign it on the back) in aspecific area. Your entire indorsement (whether a signatureor a stamp) along with any other indorsement information(e.g., additional indorsements, ID information, driver' slicense number, etc.) must fall within 1 1/2" of the "trailingedge" of a check. Indorsements must be made in blue orblack ink, so that they are readable by automated checkprocessing equipment.As you look at the front of a check, the "trailing edge" isthe left edge. When you flip the check over, be sure to keepall indorsement information within 1 1/2" of that edge.

You warrant and agree to the following for every remotelycreated check we receive from you for deposit or collection:(1) you have received express and verifiable authorization tocreate the check in the amount and to the payee that appearson the check; (2) you will maintain proof of theauthorization for at least 2 years from the date of theauthorization, and supply us the proof if we ask; and (3) if acheck is returned you owe us the amount of the check,regardless of when the check is returned. We may takefunds from your account to pay the amount you owe us, andif there are insufficient funds in your account, you still oweus the remaining balance.

(21) ACH and Wire Transfers. This agreement is subjectto Article 4A of the Uniform Commercial Code - FundTransfers as adopted in the state in which you have youraccount with us. If you originate a fund transfer and youidentify by name and number a beneficiary financialinstitution, an intermediary financial institution or abeneficiary, we and every receiving or beneficiary financialinstitution may rely on the identifying number to makepayment. We may rely on the number even if it identifies afinancial institution, person or account other than the onenamed. You agree to be bound by automated clearing houseassociation rules. These rules provide, among other things,that payments made to you, or originated by you, areprovisional until final settlement is made through a FederalReserve Bank or payment is otherwise made as provided inArticle 4A-403(a) of the Uniform Commercial Code. If wedo not receive such payment, we are entitled to a refundfrom you in the amount credited to your account and theparty originating such payment will not be considered tohave paid the amount so credited. Credit entries may bemade by ACH. If we receive a payment order to credit anaccount you have with us by wire or ACH, we are notrequired to give you any notice of the payment order orcredit.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 7 of 10

(29) Credit Verification. You agree that we may verifycredit and employment history by any necessary means,including preparation of a credit report by a credit reportingagency.

(30) Legal Actions Affecting Your Account. If we areserved with a subpoena, restraining order, writ ofattachment or execution, levy, garnishment, search warrant,or similar order relating to your account (termed "legalaction" in this section), we will comply with that legalaction. Or, in our discretion, we may freeze the assets in theaccount and not allow any payments out of the account untila final court determination regarding the legal action. Wemay do these things even if the legal action involves lessthan all of you. In these cases, we will not have any liabilityto you if there are insufficient funds to pay your itemsbecause we have withdrawn funds from your account or inany way restricted access to your funds in accordance withthe legal action. Any fees or expenses we incur inresponding to any legal action (including, without limitation,attorneys' fees and our internal expenses) may be chargedagainst your account. The list of fees applicable to youraccount(s) provided elsewhere may specify additional feesthat we may charge for certain legal actions.

(28) Fiduciary Accounts. Accounts may be opened by aperson acting in a fiduciary capacity. A fiduciary is someonewho is appointed to act on behalf of and for the benefit ofanother. We are not responsible for the actions of afiduciary, including the misuse of funds. This account maybe opened and maintained by a person or persons named asa trustee under a written trust agreement, or as executors,administrators, or conservators under court orders. Youunderstand that by merely opening such an account, we arenot acting in the capacity of a trustee in connection with thetrust nor do we undertake any obligation to monitor orenforce the terms of the trust or letters.

(27) Death or Incompetence. You agree to notify uspromptly if any person with a right to withdraw funds fromyour account(s) dies or is adjudicated (determined by theappropriate official) incompetent. We may continue to honoryour checks, items, and instructions until: (a) we know ofyour death or adjudication of incompetence, and (b) we havehad a reasonable opportunity to act on that knowledge. Youagree that we may pay or certify checks drawn on or beforethe date of death or adjudication of incompetence for up toten (10) days after your death or adjudication ofincompetence unless ordered to stop payment by someoneclaiming an interest in the account.

It is important that you confine the indorsement informationto this area since the remaining blank space will be used byothers in the processing of the check to place additionalneeded indorsements and information. You agree that youwill indemnify, defend, and hold us harmless for any loss,liability, damage or expense that occurs because yourindorsement, another indorsement, or information you haveprinted on the back of the check obscures our indorsement.These indorsement guidelines apply to both personal andbusiness checks.

(31) Security. It is your responsibility to protect theaccount numbers and electronic access devices (e.g., anATM card) we provide you for your account(s). Do notdiscuss, compare, or share information about your accountnumber(s) with anyone unless you are willing to give themfull use of your money. An account number can be used bythieves to issue an electronic debit or to encode your numberon a false demand draft which looks like and functions likean authorized check. If you furnish your access device andgrant actual authority to make transfers to another person (afamily member or coworker, for example) who then exceedsthat authority, you are liable for the transfers unless we havebeen notified that transfers by that person are no longerauthorized. Your account number can also be used toelectronically remove money from your account, andpayment can be made from your account even though youdid not contact us directly and order the payment. You mustalso take precaution in safeguarding your blank checks.Notify us at once if you believe your checks have been lostor stolen. As between you and us, if you are negligent insafeguarding your checks, you must bear the loss entirelyyourself or share the loss with us (we may have to sharesome of the loss if we failed to use ordinary care and if wesubstantially contributed to the loss).Except for consumer electronic funds transfers subject toRegulation E, you agree that if we offer you servicesappropriate for your account to help identify and limit fraudor other unauthorized transactions against your account,such as positive pay or commercially reasonable securityprocedures, and you reject those services, you will beresponsible for any fraudulent or unauthorized transactionswhich could have been prevented by the services weoffered, unless we acted in bad faith or to the extent our

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 8 of 10

Your consent does not authorize us to contact you fortelemarketing purposes (unless you otherwise agreedelsewhere).

(36) Address or Name Changes. You are responsible fornotifying us of any change in your address or your name.Unless we agree otherwise, change of address or name mustbe made in writing by at least one of the account holders.Informing us of your address or name change on a checkreorder form is not sufficient. We will attempt tocommunicate with you only by use of the most recentaddress you have provided to us. If provided elsewhere, wemay impose a service fee if we attempt to locate you.

(37) Resolving Account Disputes. We may place anadministrative hold on the funds in your account (refusepayment or withdrawal of the funds) if it becomes subject toa claim adverse to (1) your own interest; (2) others claimingan interest as survivors or beneficiaries of your account; or(3) a claim arising by operation of law. The hold may beplaced for such period of time as we believe reasonablynecessary to allow a legal proceeding to determine themerits of the claim or until we receive evidence satisfactoryto us that the dispute has been resolved. We will not beliable for any items that are dishonored as a consequence ofplacing a hold on funds in your account for these reasons.(38) Waiver of Notices. To the extent permitted by law,you waive any notice of non-payment, dishonor or protestregarding any items credited to or charged against youraccount. For example, if you deposit a check and it isreturned unpaid or we receive a notice of nonpayment, wedo not have to notify you unless required by federalRegulation CC or other law.

If necessary, you may change or remove any of thetelephone numbers or email addresses at any time using anyreasonable means to notify us.

}

Your consent is limited to this account, and asauthorized by applicable law and regulations.

}

To provide you with the best possible service in our ongoingbusiness relationship for your account we may need tocontact you about your account from time to time bytelephone, text messaging or email. However, we must firstobtain your consent to contact you about your accountbecause we must comply with the consumer protectionprovisions in the federal Telephone Consumer ProtectionAct of 1991 (TCPA), CAN-SPAM Act and their relatedfederal regulations and orders issued by the FederalCommunications Commission (FCC).

With the above understandings, you authorize us to contactyou regarding this account throughout its existence usingany telephone numbers or email addresses that you havepreviously provided to us or that you may subsequentlyprovide to us.This consent is regardless of whether the number we use tocontact you is assigned to a landline, a paging service, acellular wireless service, a specialized mobile radio service,other radio common carrier service or any other service forwhich you may be charged for the call. You furtherauthorize us to contact you through the use of voice, voicemail and text messaging, including the use of pre-recordedor artificial voice messages and an automated dialing device.

(33) Monitoring and Recording Telephone Calls andConsent to Receive Communications. We may monitoror record phone calls for security reasons, to maintain arecord and to ensure that you receive courteous and efficientservice. You consent in advance to any such recording. Weneed not remind you of our recording before each phoneconversation.

(32) Telephonic Instructions. Unless required by law orwe have agreed otherwise in writing, we are not required toact upon instructions you give us via facsimile transmissionor leave by voice mail or on a telephone answering machine.

concerning your account, the transaction, and thecircumstances surrounding the loss. You will notify lawenforcement authorities of any criminal act related to theclaim of lost, missing, or stolen checks or unauthorizedwithdrawals. We will have a reasonable period of time toinvestigate the facts and circumstances surrounding anyclaim of loss. Unless we have acted in bad faith, we will notbe liable for special or consequential damages, includingloss of profits or opportunity, or for attorneys' fees incurredby you. You agree that you will not waive any rights youhave to recover your loss against anyone who is obligated torepay, insure, or otherwise reimburse you for your loss.You will pursue your rights or, at our option, assign themto us so that we may pursue them. Our liability will bereduced by the amount you recover or are entitled to recoverfrom these other sources.

negligence contributed to the loss. If we offered you acommercially reasonable security procedure which youreject, you agree that you are responsible for any paymentorder, whether authorized or not, that we accept incompliance with an alternative security procedure that youhave selected.

(34) Claim of Loss. If you claim a credit or refundbecause of a forgery, alteration, or any other unauthorizedwithdrawal, you agree to cooperate with us in theinvestigation of the loss, including giving us an affidavitcontaining whatever reasonable information we require

(35) Early Withdrawal Penalties (and involuntarywithdrawals). We may impose early withdrawal penalties ona withdrawal from a time account even if you don' t initiatethe withdrawal. For instance, the early withdrawal penaltymay be imposed if the withdrawal is caused by our setoffagainst funds in the account or as a result of an attachmentor other legal process. We may close your account andimpose the early withdrawal penalty on the entire accountbalance in the event of a partial early withdrawal. See yournotice of penalty for early withdrawals for additionalinformation.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 9 of 10

(39) Additional Terms.

,* VMP- 2016

TC-LA 3/1/2016Wolters Kluwer Financial Services

Terms and Conditions-LABankers Systems

Page 10 of 10

ELECTRONIC FUND TRANSFERSYOUR RIGHTS AND RESPONSIBILITIES

The Electronic Fund Transfers we are capable of handling for consumers are indicated below, some of which may notapply to your account. Some of these may not be available at all terminals. Please read this disclosure carefully becauseit tells you your rights and obligations for these transactions. You should keep this notice for future reference.

Make payments fromtoGet checking account(s) informationGet savings account(s) information

l

lll

l

l

l

(d) Point-Of-Sale Transactions.Using your card:l

l

ll

(e) Computer Transfers. You may access your account(s)by computer by

and using yourto:

lll

l

l

l

l

lll

l

You may access your l checking accountl account(s) to purchasegoods (l in person, l by phone, l by computer),pay for services (l in person, l by phone,l by computer), get cash from a merchant, if themerchant permits, or from a participating financialinstitution, and do anything that a participatingmerchant will accept.You may not exceed more than $ intransactions per .

Transfer funds from checking to savingsTransfer funds from savings to checkingTransfer funds fromtoTransfer funds fromtoMake payments from checking to loan accountswith usMake payments fromtoMake payments fromtoGet checking account(s) informationGet savings account(s) information

Preauthorized credits. You may make arrangementsfor certain direct deposits to be accepted into yourl checking and/or l savings account(s).Preauthorized payments. You may makearrangements to pay certain recurring bills from yourl checking and/or l savings account(s).

Transfer funds from checking to savingsTransfer funds from savings to checkingTransfer funds fromtoTransfer funds fromtoMake payments from checking to loan accountswith usMake payments fromtoMake payments fromtoGet checking account(s) informationGet savings account(s) information

Make deposits to checking accountsMake deposits to savings accountsGet cash withdrawals from checking accounts youmay withdraw no more than perGet cash withdrawals from savings accounts youmay withdraw no more than perTransfer funds from savings to checkingTransfer funds from checking to savingsTransfer funds fromtoMake payments from checking account to

(a) Prearranged Transfers.l

l

l

(b) Telephone Transfers. You may access your account(s)by telephone at using a touch tone phone, your account numbers, and

to:lll

l

l

l

l

lll

l

(c) ATM Transfers. You may access your account(s) byATM using your and personal identification number to:lll

l

lll

l

- 2014 Page 1 of 5,ETM-2-LAZ 10/18/2014

TYPES OF TRANSFERS, FREQUENCY AND DOLLARLIMITATIONS

l

l

l

Electronic Fund Transfers Disclosure

Wolters Kluwer Financial Services* VMPBankers Systems

XX

X XX

X X

X504-561-6123

Your Personal Identification NumberXXX loan accounts

checkingX loan accounts

savingsX

X savingsloan accounts with us

XX

XATM and/or Debit Card

X

X$500.00 day

X$500.00 day

XX

XXX Some of these services may not be available at all terminals.

X

X X

X X XX X

X

X 3,000day on pin based transactions. The

amount on hold for signature based transactions combined withpin based transactions can not exceed $3,000.00, $500.00 forEasy Student Debit Card, $1,000.00 for HSA Debit Card

Xvisiting www.gulfbank.com

user name and passwordXXX your account with Gulf Coast Bank

your account with another financial institution

X

X your account with Gulf Coast BankPay Bills

X your account with Gulf Coast Bankpay individuals

XXX Transfer funds from your account with another institution to your

account with Gulf Coast BankX Transfer funds from checking to checking and from savings to

savings

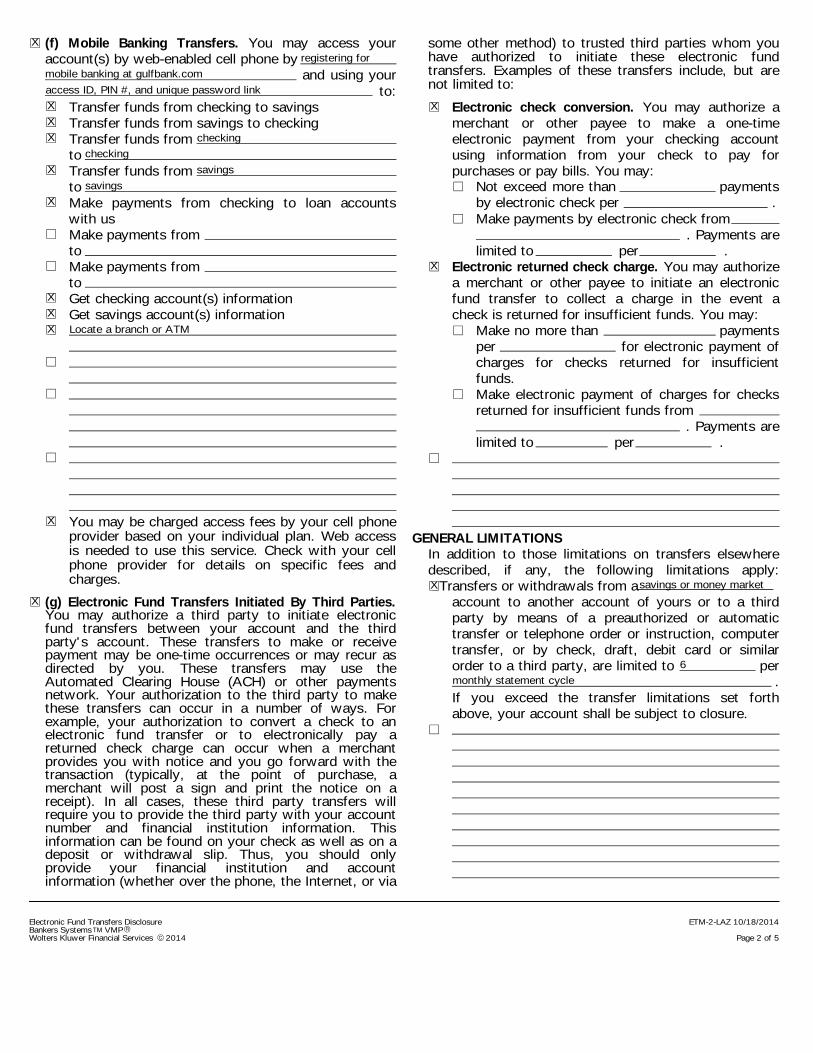

GENERAL LIMITATIONSIn addition to those limitations on transfers elsewheredescribed, if any, the following limitations apply:

l

l

l

l

Not exceed more than paymentsby electronic check per .Make payments by electronic check from

. Payments arelimited to per .

Make no more than paymentsper for electronic payment ofcharges for checks returned for insufficientfunds.Make electronic payment of charges for checksreturned for insufficient funds from

. Payments arelimited to per .

l

Electronic check conversion. You may authorize amerchant or other payee to make a one-timeelectronic payment from your checking accountusing information from your check to pay forpurchases or pay bills. You may:

Electronic returned check charge. You may authorizea merchant or other payee to initiate an electronicfund transfer to collect a charge in the event acheck is returned for insufficient funds. You may:

l

You may be charged access fees by your cell phoneprovider based on your individual plan. Web accessis needed to use this service. Check with your cellphone provider for details on specific fees andcharges.

- Page 2 of 5

l

l

Transfers or withdrawals from a account to another account of yours or to a thirdparty by means of a preauthorized or automatictransfer or telephone order or instruction, computertransfer, or by check, draft, debit card or similarorder to a third party, are limited to per

.If you exceed the transfer limitations set forthabove, your account shall be subject to closure.

l

l

some other method) to trusted third parties whom youhave authorized to initiate these electronic fundtransfers. Examples of these transfers include, but arenot limited to:

lll

l

l

l

l

lll

l

l

l

l

(f) Mobile Banking Transfers. You may access youraccount(s) by web-enabled cell phone by

and using yourto:

l

Transfer funds from checking to savingsTransfer funds from savings to checkingTransfer funds fromtoTransfer funds fromtoMake payments from checking to loan accountswith usMake payments fromtoMake payments fromto Get checking account(s) informationGet savings account(s) information

(g) Electronic Fund Transfers Initiated By Third Parties.You may authorize a third party to initiate electronicfund transfers between your account and the thirdparty's account. These transfers to make or receivepayment may be one-time occurrences or may recur asdirected by you. These transfers may use theAutomated Clearing House (ACH) or other paymentsnetwork. Your authorization to the third party to makethese transfers can occur in a number of ways. Forexample, your authorization to convert a check to anelectronic fund transfer or to electronically pay areturned check charge can occur when a merchantprovides you with notice and you go forward with thetransaction (typically, at the point of purchase, amerchant will post a sign and print the notice on areceipt). In all cases, these third party transfers willrequire you to provide the third party with your accountnumber and financial institution information. Thisinformation can be found on your check as well as on adeposit or withdrawal slip. Thus, you should onlyprovide your financial institution and accountinformation (whether over the phone, the Internet, or via

,Electronic Fund Transfers Disclosure

Wolters Kluwer Financial Services* VMPBankers SystemsETM-2-LAZ 10/18/2014

2014

Xregistering for

mobile banking at gulfbank.com access ID, PIN #, and unique password linkXXX checking

checkingX savings

savingsX

XXX Locate a branch or ATM

X

X

X

X

X savings or money market

6monthly statement cycle

(4) l if you give us written permission.l as explained in the separate Privacy Disclosure.l

CONFIDENTIALITYWe will disclose information to third parties about your

account or the transfers you make:(1)(2)

(3)

where it is necessary for completing transfers; orin order to verify the existence and condition of youraccount for a third party, such as a credit bureau ormerchant; orin order to comply with government agency or courtorders; or

If, through no fault of ours, you do not have enoughmoney in your account to make the transfer.If the transfer would go over the credit limit on youroverdraft line.If the automated teller machine where you are makingthe transfer does not have enough cash.If the terminal or system was not working properly andyou knew about the breakdown when you started thetransfer.If circumstances beyond our control (such as fire orflood) prevent the transfer, despite reasonableprecautions that we have taken.There may be other exceptions stated in our agreementwith you.

FINANCIAL INSTITUTION'S LIABILITY(a) Liability for failure to make transfers. If we do not

complete a transfer to or from your account on time or inthe correct amount according to our agreement with you,we will be liable for your losses or damages. However,there are some exceptions. We will not be liable, forinstance:

l We charge for each stop payment.

PREAUTHORIZED PAYMENTS(a) Right to stop payment and procedure for doing so. If

you have told us in advance to make regular payments outof your account, you can stop any of these payments.Here's how:

Call or write us at the telephone number or addresslisted in this disclosure, in time for us to receive yourrequest 3 business days or more before the payment isscheduled to be made. If you call, we may also require youto put your request in writing and get it to us within 14days after you call.

Page 3 of 5-

You will get a quarterly statement from us on yoursavings account if the only possible electronictransfer to or from the account is a preauthorizedcredit.

l

l

l

l

If you bring your passbook to us, we will record anyelectronic deposits that were made to your accountsince the last time you brought in your passbook.

(b) Preauthorized Credits. If you have arranged to havedirect deposits made to your account at least once every60 days from the same person or company, you can callus at the telephone number listed below to find outwhether or not the deposit has been made.

(c) In addition,You will get a monthly account statement from us,unless there are no transfers in a particular month.In any case you will get a statement at leastquarterly.

l You may not get a receipt if the amount of the

transfer is $15 or less.}

}

}

}

}

}

balance in thefalls belowduring the

.l

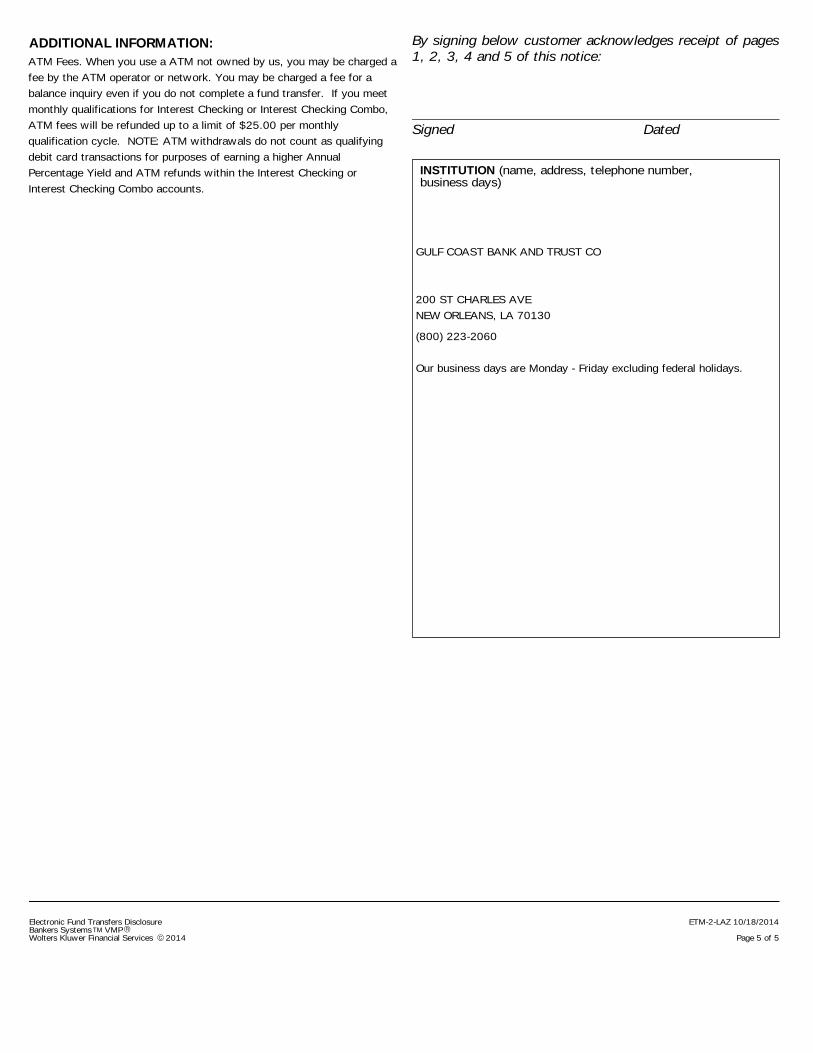

l

Except as indicated above, we do not charge forElectronic Fund Transfers.ATM Operator/Network Fees: When you use an ATM notowned by us, you may be charged a fee by the ATMoperator or any network used (and you may be charged afee for a balance inquiry even if you do not complete afund transfer).

l We charge eachbut only if the

DOCUMENTATION(a) Terminal Transfers. You can get a receipt at the time

you make a transfer to or from your account using a(n)l automated teller machinel point-of-sale terminal.

(b) Notice of varying amounts. If these regular paymentsmay vary in amount, the person you are going to pay willtell you, 10 days before each payment, when it will bemade and how much it will be. (You may choose insteadto get this notice only when the payment would differ bymore than a certain amount from the previous payment, orwhen the amount would fall outside certain limits that youset.)

(c) Liability for failure to stop payment of preauthorizedtransfer. If you order us to stop one of these payments 3business days or more before the transfer is scheduled,and we do not do so, we will be liable for your losses ordamages.

l We charge eachto our customers whose accounts

are set up to use.

FEES

,Electronic Fund Transfers Disclosure

Wolters Kluwer Financial Services* VMPBankers SystemsETM-2-LAZ 10/18/2014

2014

XX

X

X

X $45

XX

Page 4 of 5-

l MasterCard, Debit Card. Additional Limits on Liabilityfor .

(b) Contact in event of unauthorized transfer. If youbelieve your card and/or code has been lost or stolen, callor write us at the telephone number or address listed atthe end of this disclosure. You should also call the numberor write to the address listed at the end of this disclosureif you believe a transfer has been made using theinformation from your check without your permission.

Tell us your name and account number (if any).Describe the error or the transfer you are unsureabout, and explain as clearly as you can why youbelieve it is an error or why you need moreinformation.Tell us the dollar amount of the suspected error.

UNAUTHORIZED TRANSFERS(a) Consumer Liability. Tell us at once if you believe

your card and/or code has been lost or stolen, or if youbelieve that an electronic fund transfer has been madewithout your permission using information from yourcheck. Telephoning is the best way of keeping yourpossible losses down. You could lose all the money in youraccount (plus your maximum overdraft line of credit). Ifyou tell us within 2 business days after you learn of theloss or theft of your card and/or code, you can lose nomore than $50 if someone used your card and/or codewithout your permission. Also, if you do NOT tell us within2 business days after you learn of the loss or theft of yourcard and/or code, and we can prove we could havestopped someone from using your card and/or codewithout your permission if you had told us, you could loseas much as $500. Also, if your statement shows transfersthat you did not make, including those made by card, codeor other means, tell us at once. If you do not tell us within60 days after the statement was mailed to you, you maynot get back any money you lost after the 60 days if wecan prove that we could have stopped someone fromtaking the money if you had told us in time.

If a good reason (such as a long trip or a hospital stay)kept you from telling us, we will extend the time period.

ERROR RESOLUTION NOTICEIn Case of Errors or Questions About Your Electronic

Transfers, Call or Write us at the telephone number oraddress listed below, as soon as you can, if you think yourstatement or receipt is wrong or if you need moreinformation about a transfer listed on the statement orreceipt. We must hear from you no later than 60 days afterwe sent the FIRST statement on which the problem orerror appeared.

(1)(2)

(3)If you tell us orally, we may require that you send us

your complaint or question in writing within 10 businessdays.