TRUST AND PARTICIPATION IN AN EMERGING...

40

TRUST AND PARTICIPATION IN AN EMERGING MARKET: LEADING AND LAGGING EFFECTS OF SOCIAL TIES ON CORRUPTION Christopher B. Yenkey Univ. of Chicago Booth School of Business Draft: Please do not cite without permission of the author Abstract This paper analyzes the effects of social ties between investors and a corrupt stock broker as they relate to the broker’s selection of victims for a fraud and investors’ subsequent reactions to experiencing the fraud. In contrast with earlier work linking interpersonal relationships with malfeasance, I first ask whether shared group membership between investors and their broker is positively or negatively related to being selected as a victim. Second, I ask whether shared group membership mediates victims’ reactions to the fraud, looking to see how post-fraud levels of investing differ between investors who share group-level ties with the corrupt broker and those who belong to rival groups. The empirical setting is the tribally diverse and contentious population of investors in Kenya’s emerging stock market, where investors and their stockbrokers can be members of the same or rival tribal groups. Analysis of investor-level data from a major stockbroker scandal in 2008 suggests that corrupt brokers disproportionately target clients from their own tribal group for theft of cash and shares but avoid stealing from the accounts of investors belonging to rival tribes. Investors sharing the tribal tie to the corrupt broker continue to increase the value of their investments post-scandal, while members of rival tribes reduce the value of their investments. Investors belonging to the broker’s tribe reduce future investments primarily in response to increased personal financial losses or when a great number of fellow tribe members also experience the fraud. In contrast, the negative reactions of investors belonging to the rival tribe do not intensify with either rising personal financial losses or with an increase in the number of proximate other victims. Taken together, results suggest that group-level ties increase the likelihood of experiencing the fraud but also increase the severity of fraud necessary to trigger a reduction in trust in the market. Keywords: fraud, social networks, group identity, emerging market This research was supported by a grant from the National Science Foundation (Grant No. 0802469), the University of Chicago Booth School Of Business, the Center for the Study of Economy and Society at Cornell University, and Cornell University’s Graduate School. Direct correspondence with the author at [email protected].

Transcript of TRUST AND PARTICIPATION IN AN EMERGING...

TRUST AND PARTICIPATION IN AN EMERGING MARKET: LEADING AND LAGGING EFFECTS OF SOCIAL TIES ON CORRUPTION

Christopher B. Yenkey Univ. of Chicago Booth School of Business

Draft: Please do not cite without permission of the author

Abstract

This paper analyzes the effects of social ties between investors and a corrupt stock broker as they relate to the broker’s selection of victims for a fraud and investors’ subsequent reactions to experiencing the fraud. In contrast with earlier work linking interpersonal relationships with malfeasance, I first ask whether shared group membership between investors and their broker is positively or negatively related to being selected as a victim. Second, I ask whether shared group membership mediates victims’ reactions to the fraud, looking to see how post-fraud levels of investing differ between investors who share group-level ties with the corrupt broker and those who belong to rival groups. The empirical setting is the tribally diverse and contentious population of investors in Kenya’s emerging stock market, where investors and their stockbrokers can be members of the same or rival tribal groups. Analysis of investor-level data from a major stockbroker scandal in 2008 suggests that corrupt brokers disproportionately target clients from their own tribal group for theft of cash and shares but avoid stealing from the accounts of investors belonging to rival tribes. Investors sharing the tribal tie to the corrupt broker continue to increase the value of their investments post-scandal, while members of rival tribes reduce the value of their investments. Investors belonging to the broker’s tribe reduce future investments primarily in response to increased personal financial losses or when a great number of fellow tribe members also experience the fraud. In contrast, the negative reactions of investors belonging to the rival tribe do not intensify with either rising personal financial losses or with an increase in the number of proximate other victims. Taken together, results suggest that group-level ties increase the likelihood of experiencing the fraud but also increase the severity of fraud necessary to trigger a reduction in trust in the market. Keywords: fraud, social networks, group identity, emerging market

This research was supported by a grant from the National Science Foundation (Grant No. 0802469), the University of Chicago Booth School Of Business, the Center for the Study of Economy and Society at Cornell University, and Cornell University’s Graduate School. Direct correspondence with the author at [email protected].

1

Introduction

The goal of this paper is to deepen our understanding of the role of social ties in the

causes and consequences of malfeasance. I address two primary questions. First, I revisit the

question posed by Baker and Faulkner (2004) about the protective versus harmful effects of

social ties on experiencing fraud from the perspective of group membership. Instead of

contrasting the potentially protective effects of interpersonal ties between principals and agents

against the potentially harmful effects of ties as they might lead to increased opportunity for

being recruited into a fraud, I study how a corrupt agent selects victims from his existing client

base of the membership of each in the same or rival social groups. In doing so, I analyze the

likelihood of becoming a target of fraud not as it relates to interpersonal connections between

principals and agents, but instead as it relates to the larger context of ties to sympathetic or

antagonistic groups. The primary question asked here is whether corrupt agents select victims

from their own social group or from a rival group?

Second, I analyze the reactions of actors that experience the fraud as a function of these

group-level ties between the victim and the perpetrator. This line of analysis is interested in

better understanding whether the expected negative effects of fraud are mediated by social ties

between victims and perpetrators. The primary question asked here is whether actors who are

victimized by a member of their own social group react more strongly to the event than do

victims belonging to a rival group?

In both lines of inquiry, I focus on the role of social ties at the group rather than the

individual level. Starting with data on dyadic pairings between investors and their stockbroker, I

observe the membership of each in close-knit ethnic groups. With data on almost 400,000

geographically disparate investors who become clients of a limited number of stockbrokers, I

2

assume that there are few if any pre-existing interpersonal relationships. Put simply, the formal

tie in this study is the investor-broker relationship without any assumption that they know each

other personally. These ties, however, are embedded in a larger social structure in which each

actor embodies a meaningful social identity resulting from membership in close-knit ethnic

groups. The empirical context is Kenya’s tribally diverse and contentious population, where the

stockbroker is a member of the economically dominant Kikuyu tribe. Investors can be members

of three different tribal groups: members of the same economically dominant tribal group, one of

two rival tribes who compete at the local and national level for economic resources, and a third

group of investors belonging to one of nine non-rival tribes not in strong competition for

resources..

The empirical analysis focuses on the 2008 corruption case of Nyaga Stockbrokers, a

case of intermediate fraud (Clinard 1984) where an initially legitimate business later defrauded a

subset of its clients, resulting in the broker’s expulsion from Kenya’s Nairobi Securities

Exchange (NSE). In early 2008, Nyaga served as the market intermediary for approximately 25

per cent of Kenya’s 400,000 investors. While Nyaga legitimately served as the intermediary for

most of its clients, it actively stole from about 18,000 investors either by stealing cash or shares

from their electronic account. With access to the NSE’s investor database, I am able to see which

investors were affected and measure their tribal group membership. I then estimate the likelihood

of each account being targeted as well as the reactions of all investors as a function of a dyadic

measure of the investor’s membership in the same, rival, or non-rival tribal groups compared to

her stockbroker.

Results suggest that the 18,000 victims are disproportionately members of the

stockbroker’s same tribe. In contrast, clients who are members of the rival tribe are significantly

3

less likely to be targeted for the fraud, while members of tribes who are non-rivals to the broker

are insignificantly affected. Investor reactions to experiencing the fraud differ along the lines of

group membership as well, but in a somewhat opposite direction. Although all investors exposed

to the fraud curtail future investments somewhat, members of the rival group are more sensitive

to experiencing fraud, reducing future investments simply as a function of having been a client of

a corrupt broker, while inv. Investors who share the tribal group tie to the corrupt broker seem to

react more negatively only when the financial value of their personal losses is greater or when

they are in closer proximity to a greater number of other defrauded investors in their tribe. Put

another way, investors who are cheated by a member of their own group seem to have a higher

threshold for tolerating the fraud, but once this threshold is met they reduce future investments

disproportionately. Rival group investors, however, are quick to reduce their future investments,

but this negative reaction does not seem to grow as their personal losses increase or as more

members of their group experience the fraud. I interpret these results as suggesting that social

ties at the level of group membership make one more vulnerable to fraud but also increase the

threshold for negative reactions to the fraud, with negative reactions more easily triggered in

rivals but that the disproportionately negative reactions of in-group members predicted by

theories of social network closure resulting from more severe exposure to the fraud.

The next section describes the empirical setting of the study in order to familiarize the

reader with the empirical facts of the case used in this study, including the social setting in which

the rival social identities operate. The following section provides a theoretical discussion of the

competing predictions offered by earlier work in sociology, criminology, and social psychology,

contrasting the large body of work on the protective role of networks with that of more recent

work that looks at the effects of social ties on the negative outcomes of fraud and over

4

commitment. A section describing the novel dataset and empirical framework is followed by

presentation of results. Concluding sections discuss interpretations of the results and briefly

outline the next steps in the analysis.

Empirical context

The recent history of the Nairobi Securities Exchange (NSE) has seen both high levels of

investor recruitment as well as several notable scandals. By 2005, fifty years after its founding,

the NSE had mobilized only 140,000 total investors from a national population of about

2,500,000 households with the financial resources to do so. Following a package of state-adopted

market liberalization reforms adopted in 2005, a wave of investor recruitment occurred between

May 2006 and December 2008. In this short period, the number of total investors soared ten

times to approximately 1.4 million. Yenkey (2012) argues that communication within tribal

groups was a primary pathway through which information and influence traveled in Kenya,

showing that potential investors often entered the market as a result of learning about the benefits

of shareholding from co-ethnics rather than geographically proximate prior adopters.

Three notable scandals occurred during this dynamic growth period on the NSE. In May

2006, publicly traded Uchumi Supermarkets filed for bankruptcy and delisted, leaving 7,213

uncompensated investors at a time when there were approximately 175,000 investors in the

market. In March 2007, the stockbrokerage firm Francis Thuo and Partners was expelled from

the market for the practice of stealing funds from clients’ accounts and trading in their shares,

forcing all of their 4,000 clients, an unknown number of which suffered financial losses from

theft and fraudulent trading, to transfer their accounts to another intermediary.

5

The third and largest of the scandals was the collapse of Nyaga Stockbrokers in April

2008. As the largest brokerage in Kenya at the time, Nyaga was the intermediary for about 25

per cent of the 397,413 investors in the market. Among Nyaga clients, 18,006 were direct

victims as a result of Nyaga agents stealing cash or shares from their electronic accounts.

Nyaga’s fraud began as agents using clients’ shares for trades in the secondary market, keeping

the resulting profits and then returning those shares to the client’s account. However, unexpected

losses began to mount from those trades, resulting in rogue agents making both cash withdrawals

from client accounts and permanently selling shares and keeping the proceeds, both as a means

of covering losses. The extent of theft reached such a level that the brokerage was suspended

from operations on March 5, 2008, and placed under statutory management by the NSE and the

state regulatory agency, the Capital Markets Authority (CMA). Since that time, evidence has

surfaced that officials at the NSE and the Capital Markets Authority had been aware of the fraud

for some time before they shut it down. Even those Nyaga clients that were not direct victims

were non-trivially exposed to the fraud, as they were notified by the NSE that their stockbroker

had been expelled from the market as a result of fraudulent practices and their accounts had to be

transferred to another broker before any further transactions could take place. Due to the highly

infrequent use of online accounts, the majority of investors accomplished this by traveling to the

NSE in Nairobi, often on multiple occasions, to fill out to necessary paperwork. For almost two

months, the NSE’s offices in downtown Nairobi were the site of a queue of Nyaga clients and

victims that at times stretched for blocks. No investor associated with Nyaga, even those who

were not directly stolen from, escaped the experimental prime of being associated with a corrupt

and collapsed broker.1

1 Corruption is a common event in Kenya. The 2007 Transparency International Corruption Perception Index estimated that 87% of Kenyans paid bribes to access basic services in some form (e.g. payments to police, local or

6

The analysis presented here focuses on the effects of the Nyaga scandal rather than the

other two for several reasons. First, more complete data is available for this scandal than for the

previous two. Following the first brokerage collapse (Francis Thuo and Partners), the Kenyan

state established the Investor Compensation Fund to reimburse investors who lost money due to

corrupt practices in the market. Because Nyaga victims were eligible for reimbursement, each

was provided with a statement of all past activity (cash withdrawals or share trades) on the

account. If an investor found an unordered trade or an unrequested withdrawal of funds in her

account, she could submit a claim for reimbursement. The NSE management team shared their

list of the 18,006 verified claims from the Nyaga collapse, thus allowing me to measure the

intensity of each investor’s exposure to the fraud. Second, the Nyaga scandal directly preceded

the largest IPO in Kenyan history- the listing of state-owned telecom Safaricom. In contrast, the

Thuo scandal was followed by the listing of a small, relatively unknown private advertising

conglomerate that drew less popular demand. Given the extraordinary public appeal of the

Safaricom IPO and the widespread exposure of the Nyaga scandal, I argue that this specific event

makes for a more suitable natural experiment of the effects of fraud by providing a more

measurable single instance of fraud tied with a locally meaningful opportunity for investors to

respond. The Safaricom IPO subscription period began just six weeks after the collapse of the

Nyaga brokerage, enough time for investors to transfer to another broker but not sufficient time

for them to be compensated by the Investor Compensation Fund.

Tribal group membership is the primary mode of social identity I consider in this study

precisely because it is so salient in Kenyan society. Tribal membership has long been known to

play a key role in the formation of social identity in East Africa, an in Kenya in particular

(Brewer 1969). In addition to the author’s work on investor recruitment mentioned above, national government, utility providers), ranking it 150th internationally.

7

anthropologists have shown that tribal membership, particularly in Kenya, is a key institution

through which economic activity is organized. Ensminger (1996) shows this with the

development of market institutions among the Orma in northeastern Kenya, while van Ufford

and Zaal (2004) explain the development of a national beef market in Kenya in the 1990s as a

product of inter-tribe distrust. Here, butchers and traders from disparate parts of Kenya, each

representing the tribe of their home region, travel to the Tanzanian border to buy directly from

herdsmen there, preferring to form a closed supply chain within the tribe over long distances

rather than entrust purchases to out-group middle men.

An in-depth historical account of ethnic tensions in Kenya is beyond the scope of this

paper. In order to illustrate the salience of the three groups I operationalize, a brief description of

ethnic conflict at the time of the Nyaga stockbroker scandal should suffice. The Kenyan

presidential election in December 2007 saw the sitting president, a member of the economically

dominant Kikuyu tribe, challenged by a coalition ticket comprised of members of the Luo and

Kalenjin tribes, both traditional rivals to the Kikuyu for political and economic power dating

back to the colonial era. Both campaigns made extensive use of tribal tensions to mobilize

support, and both groups are widely understood to have engaged in vote rigging (Gutierrez-

Romero, forthcoming). Two weeks after the election, the Kikuyu candidate was announced as

the winner in an awkward and suspicious series of events. Members of the ethnic opposition

began violent raids on Kikuyu communities in an organized pattern that suggested preparations

had been made ahead of time. A number of similarly organized Kikuyu groups retaliated,

producing several weeks of ethnic clashes that left approximately 1,300 dead and more than

400,000 internally displaced. Both major presidential candidates publicly accused the other of

ethnic genocide, and five years later the case is still being heard by the International Criminal

8

Court, with major political figures on both sides under indictment for crimes against humanity. It

was in this environment in March 2008, just weeks after Kofi Annan brokered a peace deal

between the two sides, that Kenyan investors belonging to these three groups (the Kikuyu, their

Luo and Kalenjin rivals, and the remaining non-rival tribes) received the news that their Kikuyu

stockbroker had been expelled from the market because of fraud and that they should check their

accounts for lost funds and begin the search for a new intermediary.

There is on additional aspect of the empirical setting that deserves our attention, given the

research questions being asked: what is the role of tribal ties in creating client ties between

investors and stockbrokers? Data is being collected on the tribal affiliation of all 27

intermediaries licensed by the NSE in order to include this important initial question in the full

analysis. At the current time, however, I only know that the Nyaga Stockbrokerage is a fully

Kikuyu-run organization, and I know the tribal affiliation of their clients relative to all other

investors in the market. At the time of the Nyaga scandal, approximately 60 per cent of all Nyaga

clients were Kikuyu, while only six per cent of clients were members of rival tribes, and 34 per

cent of clients were non-rivals to the Kikuyu. Among non-Nyaga clients in the market,

approximately 42 per cent are Kikuyu, 10 per cent are rivals, and 40 per cent are members of

non-rival tribes. These descriptive statistics strongly suggest that Kikuyu investors make up a

disproportionate number of Nyaga clients. These summary data will not surprise sociologists that

have long demonstrated the role of shared ethnicity and related forms of homophily on the

creation of social and economic ties.

9

Social ties as a cause of and reaction to fraud

Seminal work in the social sciences demonstrates that similarity breeds tie formation and

those ties subsequently foster more trustworthy behavior and minimize the risk of malfeasance.

The expected outcomes of two alternative but not uncommon scenarios have received less

attention: the risk of malfeasance in networks formed between antagonistic groups, and how

victims’ reactions to malfeasance might differ according to membership in the same versus rival

groups as the perpetrator. In this section, I revisit the question of the expected protective versus

harmful role played by shared social ties on the likelihood of malfeasance and then extend that

discussion by theorizing how victims’ reactions to fraud might vary according to their

membership in shared versus rival group as the perpetrator.

Brokers choosing victims

Baker and Faulkner (2004) were the first to empirically test the competing predictions of

the role of social ties in malfeasance. Sociologists have long argued that social ties play a

protective role against malfeasance in numerous ways. Social ties provide a higher degree of

information about more risky transactions (DiMaggio and Louch 1998), create closure within

social groups which facilitates monitoring and enforcement of productive group norms (Coleman

1990; Burt 1992), and creates an environment in which the cost of cheating a member of one’s

group escalates considerably with the possibility of other group members discovering the fraud

(Granovetter 1992). In contrast, criminologists tend to focus on the harmful nature of social ties,

which can be used to facilitate recruitment of victims into a fraud through the use of shared

social ties including group membership. Here, shared social ties create a false sense of trust,

reducing the likelihood that an actor will conduct due diligence before entering the exchange.

10

Baker and Faulkner (2004) were the first to empirically test these contradictory

outcomes of social ties, using a strategic case in which interpersonal ties between investors and

an oil exploration firm could have been use to either recruit new victims or insure repayment of

investment when the firm faced financial difficulty. They found that interpersonal ties between

investors and the firm’s principals served a protective role, helping investors who knew

principals personally avoid losing their full investment. Secondary ties, those investors whose

contacts had personal relations with company principals, were not similarly protected.

Although illuminating, this single empirical case cannot capture the full range of possible

outcomes where social ties are part of a large scale fraud. Social ties operationalize in myriad

ways across empirical settings, but most existing work studies social ties as direct, interpersonal

ties. In contrast, the case studied here considers the possible outcomes when ties are formed

between economic actors belonging to the same versus rival social groups. Operationalizing

social ties in a way that allows group membership to matter and adds the additional dimension of

known antagonism between groups shifts the focus of the analysis more to the social context in

which ties are formed and away from the degree of inter-personal connections between the

actors.

Geertz (1968), Coleman (1990), and Biggart (2001) each studied the high trust

environments in which rotating savings and credit organizations (rosca’s) operate in developing

countries, finding that dense interpersonal ties in these local savings groups facilitate trust by

make malfeasance “unthinkable” in small, close knit communities. We know little, however,

about the prevalence of malfeasance in groups comprised of members of rival social groups.

Exchange relations between members of rival groups are, of course, less likely to form, but this

does not mean that such situations are not still fairly common. Examples might include shop

11

keepers whose businesses serve customers from antagonistic social groups, real estate agents

who broker purchases for members of their own as well as rival groups, or grant writers seeking

funding from an expectedly reticent source. In these settings, do we expect that social ties at the

level of the group will protect exchange partners from malfeasance or make them more

vulnerable? If more dense social ties within the group increase monitoring and enforcement, then

the fraud is more likely to be discovered, the agent would be more likely to suffer both social and

economic sanctions as a result of increased communication within the victim’s group, and

therefore the agent should be less likely to cheat his own group. But as predicted by

criminologists, potential victims are more likely to trust and less likely to perform due diligence

on agents from their same social group, thus creating a better opportunity for a corrupt agent to

successfully steal from them. Alternatively, the corrupt shop keeper might be less likely to cheat

a member of an antagonistic group because of the expectation that such rivals increase due

diligence and monitoring, suggesting that the agent will be less likely to cheat his rivals because

their increased scrutiny makes it more likely that the fraud will be discovered.

Studying stockbrokers who serve investors belonging to both the same and rival social

groups provides a productive setting for revisiting the contrasting theoretical arguments made by

sociologists and criminologists presented by Baker and Faulkner, looking for the harmful versus

protective effects of social ties at the level of contentious groups. Either outcome once again

seems plausible. Corrupt stockbrokers might be more likely to steal from in-group members

because they expect them to be less likely to be monitoring against malfeasance and hence the

crime goes unnoticed, or they may avoid cheating in-group members because they expect greater

monitoring and enforcement among group members which would increase the likelihood of

discovery and loss of future business. These basic propositions can be similarly applied to

12

members of rival groups, as they could be more likely to detect the fraud due to heightened due

diligence and/or more likely to react more strongly as a result of the underlying tensions between

the groups. Ex ante, either outcome seems plausible:

Research Question 1 (RQ1): Are corrupt agents more or less likely to target members of their social group or a rival group when conducting a fraud?

Reactions to the fraud: future participation

Prior research in sociology has tended to focus on the social arrangements that facilitate

trustworthy behavior, with much less attention paid to instances where trust has been violated.

Studies of local savings groups in Africa and Asia document the close knit social structure that

leads to high trust (Geertz 1968; Biggart 2001), but there are no follow up studies on what

happens when a group member does in fact violate that trust. Greif (1993) convincingly argues

that kinship-based ties increased trust between principals and agents making long distance trade

possible in the Mediterranean almost 1,000 years ago, but we have no data on what happened in

those presumably rare events when a member of such a group did abscond with a shipment of

goods. Surely not even the strongest advocate of the sociological argument that social ties protect

actors from malfeasance would argue that such an outcome is absolute? Baker and Faulkner

(2004) show us a lower risk for losing an investment if there is a direct social tie between the

investor and the corrupt agent, but unless this risk is reduced to zero, it should be productive to

consider how investors might respond to a fraud as a function of their shared versus rival ties to

the corrupt agent. I consider the possible reactions of in-group versus rival group victims of

fraud.

13

Reactions of in-group victims

A relatively new line of work among sociologists investigates the negative effects of

social ties on economic outcomes. The generalized finding is that actors form biased assessments

of prior exchange partners, which can either create higher performance by way of a self-fulfilling

prophecy by extending better terms of trade to our social contacts which then improves

performance (Kollock 1994), or we reduce the objectivity of our post-exchange assessments and

bias performance calculations upward as a result of affective attachment to our contacts (Lawler

1992). Sorenson and Waguespack (2006) demonstrate that actors overestimate the quality and

trustworthiness of prior exchange partners in a study of historical ties between Hollywood film

producers and distributors that result in the latter investing inordinate levels of resources to

promoting and releasing the formers’ films, resulting in lower economic gains for the distributor.

Biased assessments of prior connections quite easily extend beyond dyadic past exchange

relations and into the realm of ethnic group membership, particularly in a setting like Kenya

where tribal group membership is a fundamental pathway through which resources flow in a

patronage system. In a reanalysis of Kanter’s (1968, 1972) work on pathways of group

commitment, Hall (1988) finds that ethnic group membership is the strongest underlying factor

aiding group-level survival across a population of utopian societies. Lawler (1992) similarly

finds that greater emotional attachment occurs between individuals and group-level identities

that strengthen their generalized sense of control. Sgourev and Zuckerman (2011) find that

secondary emotional attachment to connections within a business peer network reduce the

likelihood of exiting the group, even in the presence of a decreased assessment of the group’s

contribution to an individual’s economic interests.

14

Experimental evidence from social psychologists presents a contrasting prediction.

Yamagishi et al. (2009) find evidence that expectations of fair behavior are higher among in-

group members than for out-group members, a concept directly relevant here. If expectations are

higher for fair behavior within the social group, then it should follow that more negative

reactions ensue when those expectations are not met. In such cases, we would expect Kikuyu

investors who are exposed to fraud by their in-group stockbroker to react more negatively. This

prediction is in line with the bulk of social network theory discussed above, including the

expectation that more dense social ties create increased monitoring and enforcement of group

norms (Coleman 1990; Burt 2000).

These arguments present competing predictions of how victims of fraud would react if

the perpetrator hails from the same social group. Would attachment to one’s primary social

group, especially in Kenya where tribal groups seek to control scarce resources, create a more or

less negative reaction to fraud when the perpetrator is a member of the same group? Evidence

from earlier work might predict either that the affective attachment embodied in such ties might

provide a protective bugger against such a departure from the expected trustworthy behavior, at

least in the short term or when the exposure to fraud is relatively small. Alternatively, a fraud

committed by an in-group member could trigger a disproportionately negative reaction by virtue

of its incongruence with the expectation of fair and trustworthy behavior.

Reactions of rival group members

Existing work from sociological studies of social ties and trust does not provide much

traction on the question of malfeasance by alters from antagonistic groups. Earlier work has

found structural differences in corrupt networks compared to networks of legitimate business

15

contacts, with corrupt networks more designed for concealing the identity of agents (Baker and

Faulkner 1993; Diesner, Frantz & Carley 2006; Aven 2012), as issue addressed in more detail

below. Logically, we might predict that the reduced likelihood of ties initially forming between

members of rival groups would either limit the expectations of rival group members of fair

treatment by the agent; alternatively, those members of the rival group that do form a tie to a

stockbroker from the rival group might represent the small subset of investors who are

disproportionately most likely to trust that the transaction will be handled according to the shared

interests of each party (Hardon 2006).

Social psychologists have addressed the question of how members of rival groups react

to stimuli more directly. Some earlier work suggests that reactions to fraud perpetrated by a rival

group member would be less negative as a result of the initially lower expectations of

trustworthy behavior that members of rival ethnic groups have for one another. Steele et al.

(2002) and Prudie, Steele & Davies (2004) find that trust between ethnic minority and majority

groups is less likely to develop in situations where minority groups have been historically

subjected to prejudice and discrimination at the hand of the majority group. Thus, actors in

general are less likely to trust members of other groups (Tajfel & Turner 1986), which leads to

less positive expectations for interactions with members of rival groups (Tropp 2003), and

therefore a lowered degree of felt victimization when a tie with a rival results in a fraud. In such

a setting, a defrauded rival group member, especially one whose rival group is in the minority,

might be expected to exhibit what sociologists have called “theory driven learning,” where

experiences that confirm theoretical priors are more heavily weighted in decisions about future

actions while experiences that run counter to one’s priors are discounted (Strang and Jung 2005).

16

Carr and Steele (2010), however provide reason to think that members of rival, minority

groups might react disproportionately negatively if the perceived stereotype assigned to their

group is confirmed. In experimental settings, these researchers find that subjects are more risk

averse in financial decisions when a negative stereotype about them is stimulated. In the Kenyan

case, members of the rival group are the negatively stereotyped group, having been relegated to a

less favored economic position in Kenyan society many years or decades prior and might be

expected to react disproportionately negatively to experiencing fraud, especially when it

confirms their stereotype as the minority, disadvantaged group.

There are conflicting expectations, then, when trying to predict the reaction of a

defrauded member from a rival group. The disadvantaged rival might discount the experience on

account of lower initial expectations of fair treatment, or the fraud might intensity her reaction to

being in the disadvantaged minority. In the Kenyan context studied here, if you already believe

that you are in the minority group and the market is rigged, then experiencing that could either

confirm what you already knew before entering the market and therefore not dissuade future

investments or serve as a final, direct indicator of expectations of unfair treatment and reduce

future investments.

Taking into account the contrasting predictions of how investors’ from the corrupt

broker’s same versus rival tribes might react to experiencing the fraud, I am content to simply

ask the question:

Research question 2 (RQ2): How do reactions to a fraud differ according to shared social group membership between victim and perpetrator?

17

Finally, it should be noted that both same and rival group investors can experience the

fraud in a range of ways that would be. First, the tension between victims and perpetrators might

differ according to whether the investors was just a client of the Nyaga brokerage, and therefore

received the stimulus that the broker was corrupt but did not steal directly from them. Second,

the investor may have been directly stolen from, and the sum stolen might differ in gross value or

percentage of an investor’s portfolio. Third, and especially relevant to the group-level dynamics

of interest here, investors may be located in closer proximity to greater numbers of other Nyaga

clients and victims. In settings where there is a greater concentration of others experiencing the

fraud, each investor’s private information about the fraud would increasingly constitute public,

shared information or felt experience. This might be especially true when the numbers of other

clients or victims are members of one’s own tribal group. This third approach, which accounts

for the prevalence of the fraud among members of the tribal group, accounts for the social

identity of affected investors in the context of their ties to a corrupt broker. If ex ante we expect

fraud to have a negative effect and that shared versus rival group ties to the perpetrator are

important, then it is necessary to consider not just the effects of dyadic differences in group

membership but also the location of each investor within the larger structure of victims

surrounding her.

Data and methods

Access to the NSE’s clearing and settlement database allows me to construct a unique

dataset of investor-level attributes, behaviors, and exposure to the Nyaga Stockbroker fraud.

NSE databases provide geographic location for most investors as well as the family name of each

account holder, with family name being highly related to tribal membership in Kenya.

18

Approximately 90 per cent of all NSE account contain a verified town of residence. Because an

important component of the analysis is geographic proximity to other investors exposed to the

fraud and a range of control variables are included based on location of residence, only investors

whose account contained a verified town of residence are included in the analysis. NSE account

data for 71,347 out of approximately 100,000 Nyaga clients contained a verifiable town of

residence.2 Investors lacking a verifiable town of residence don’t show patterns of bias in terms

of portfolio size, diversity, or tenure in the market.

Dependent variables

The outcome variable for research question 1 is a dichotomous measure indicating

whether or not an investor who was a Nyaga client also directly experienced theft of cash or

shares as reported by the Investor Compensation Fund. Investors’ reactions to the fraud, the

focus of the second research question, are measured as the natural log of the value of investment

made in the telecom privatization IPO six weeks after Nyaga’s expulsion from the market. For

this second analysis, I estimate the size of investment for all 397,413 investors in the market at

the time, with independent variables distinguishing Nyaga clients and/or victims from non-

affected investors.

2 Town of residence is self-reported by investors and hand entered by NSE clerks when the account is opened; as a result, the raw data contained numerous misspellings. To correct this without bias, I employed Basis Technologies’ Rosette Name Indexer algorithm (http://www.basistech.com/name-indexer/), which compared the provided town names against a list of verified names of legal administrative units gleaned from GIS databases referenced against the 2000 Kenyan Population Census. The algorithm assigned each provided name into a “true” town name, given a 99% confidence interval. Approximately 98% of all self-reported names were thus matched to a verified town.

19

Independent variables

Investors’ tribal membership was coded by eight independent coders, each indigenous

Kenyans representing Kenya’s six largest tribal groups. Coders were provided with a list of the

20,000 most commonly occurring family names from the NSE’s investor registration database,

which captures 94% of all investors, and a list of Kenya’s 12 largest tribal groups and two

common non-tribal groups (South Asian and English). Each coder would code each name

according to the group that coder felt more than 75% confident the name could represent. Names

could receive multiple tribal codes, which was more common for non-rival tribes which shared

common history and very rare for members of rival tribes. Each name was then assigned a score

according to the percentage of all coders who identified it in each tribal group. Inter-rater

reliability is exceedingly high. Using these scores from each of the 12 tribal groups, I created

scores for each investor according to their percentage membership in the Kikuyu tribe (that of

the stockbroker as well), one of two rival tribes (Luo or Kalenjin), or a non-rival group (all other

tribes). Investors count toward each group proportional to the score they have in each category;

although categories are non-exclusive and non-discrete, 95% of all coded investors have a

combined score of less than 1.5.

Exposure to the fraud is operationalized in multiple ways: at the individual and group

level, and in terms of simply being a Nyaga client versus having been a direct victim of theft. At

the level of the individual investor, I create a categorical variable indicating whether that investor

was a client of the corrupt Nyaga broker. An investor is coded as a Nyaga client if at least 50 per

cent of her investment in her most recent IPO subscription or her most recent share trades were

executed by the Nyaga brokerage. Access to the Investor Compensation Fund data shows the

value of each victim’s verified loss, with 18,006 of the 397,413 Nyaga investors experiencing

20

actual financial losses as a result of direct theft of cash or shares from their accounts. I also

measure the frequency of other Nyaga clients and victims in the investor’s home district, both as

a total count of other clients and as the total financial value of their losses. An additional district-

level measure of fraud exposure by members of the investor’s tribal group is calculating as the

number of other Nyaga clients and their actual financial losses among members of the same

tribal group within the district.

Controls

The analysis controls for a wide range of alternative predictors of the size of investment

in the telecom IPO following the Nyaga scandal, including portfolio composition, past

performance, exposure to other financial frauds, and level of exposure to the listing company and

its advertising campaigns. I control for each of these by including a range of control variables.

Portfolio value is the logged value of all shares held by the investor, calculated with share prices

at the end of trading the day prior to the start of the IPO subscription period modeled here.

Portfolio diversity is measured as the number of different equities held by the investor at the time

of the IPO. Portfolio performance is measured as the logged value of profits earned on the

previous IPO. Additionally, investors who entered the market prior to the rise in popular

participation in 2006 (discussed above) might also be more likely to participate in the telecom

IPO; a dichotomous variable indicating the investor’s entry into the market pre-2006 is included.

All models include a dummy variable indicating each investor’s location in one of

Kenya’s 68 administrative districts, roughly equivalent to counties in the U.S., which captures a

range of location-invariant attributes including the presence of offices or agents working on

21

behalf of each market intermediary. Controls for rates of stock market participation in the

investor’s district were estimated but not found to alter results and are not presented here.

I control for effects of generalized trust studied in the finance literature (Zignales 2008)

and specific experience with the listing firm by including district-level measures of instances of

fraud in financial organizations as well as use of cell phones (relevant because the Safaricom

telecommunications firm being listed in the period of interest had 87% market share in the

Kenyan cell phone market at the time). Rates of perceived and experienced fraud are calculated

by averaging district-level responses to the 2009 FinAccess survey, conducted by Financial

Sector Deepening-Kenya. Respondents were asked of about their experiences with fraud across a

wide range of organizations, including formal banks and insurance programs as well as informal

savings programs such as rotating savings and credit associations.

Finally, I control for the effects of advertising campaigns conducted leading up to the

IPO by including data on media expenditures by the telecom collected by a Nairobi-based market

research firm. Media buys are estimated based according to the duration and time of day of radio

advertisements promoting the telecom in the month preceding the start of the IPO subscription

period.

Methods

Selection of a Nyaga client for theft of cash or shares by a corrupt Nyaga agent, the focus

of research question 1, is modeled using binomial logistic regression predicting the 18,006

verified victims of financial losses from the population of 71,347 Nyaga clients. Reactions to the

fraud are modeled using OLS models predicting the logged value of each investor’s subscription

to the telecom IPO that followed the fraud. This model estimates the effects of varying exposure

22

to the Nyaga fraud across the full population of 397,413 investors in the market at the time,

subject to the controls described above.

Results

Descriptive results of the population of victims

Before presenting results of models addressing the two stated research questions, it is worth

noting some interesting descriptive patterns in the data. The first is the fact that victims were

drawn from the full range of portfolio values across all Nyaga clients (results not shown here).

Although there is a slight trend toward targeting investors with higher than average portfolio

values, victims were selected from all deciles of the distribution of portfolio values. Victims

were chosen between the 10th smallest and 213th largest investors in the market at the time.

Second, victims are evenly distributed across geographic areas in direct proportion to the number

of Nyaga clients in each district. Figure 1 shows a district-level scatterplot of the percentage of

Nyaga clients living in each district (horizontal axis) plotted against the percentage of Nyaga

victims living in the same district. The trend line demonstrates that victims are evenly distributed

geographically across the at-risk population. Although I do not have data to conclusively

demonstrate that this was an explicit strategy on the behalf of Nyaga agents to separate the

victims, this descriptive result is consistent with earlier work that demonstrates the intentionally

sparse structure of corrupt networks, a feature that aids detection avoidance (Baker and Faulkner

1993; Diesner, Frantz & Carley 2006).

**Figure 1 about here**

Finally, the size of theft within each account is large. Figure 2 presents data showing the

post-scandal portfolio value of the 18,006 Nyaga victims (black line, left axis), the financial

23

value of cash and shares stolen in the fraud (red bars, left axis), and the percentage of pre-scandal

portfolio value that was stolen (green bars, right axis). These data show that corrupt agents stole

a rather consistent and high percentage of the portfolio value of each victim’s account. On

average, victims lost approximately 30 per cent of portfolio value to theft, but the modal level of

theft exceeds 50 per cent. Taken together, Figures 1 and 2 suggest that corrupt agents may have

been more concerned with concealing knowledge of the fraud across investors rather than

limiting the potential within any given victim to notice it.

**Figure 2 about here**

Brokers choosing victims

Table 1 contains summary statistics and correlations for all variables in the analysis of

which Nyaga clients were targeted for theft of cash or shares from their accounts. Table 2

presents logistic regression estimates of an investor experiencing theft of cash or shares given

that she is a Nyaga client. Coefficients in Model 1 suggest that Kikuyu investors, those sharing

the tribal group membership with the corrupt Nyaga agents, are almost 13 per cent more likely to

be targeted for the fraud from among the population of at-risk clients, while members of rival

tribal groups are 15 per cent less likely to be targeted. Model 2 controls for the proportion of

Nyaga clients in each district who are Kikuyu or Kikuyu rivals but produces estimates consistent

with model 1, suggesting that agents’ targeting of Kikuyu investors is not a function of the

increased opportunity created by the available population of Kikuyu or rival tribe members.

**Tables 1 and 2 about here**

Models 3-5 estimate the effects of tribal group membership separately for three

illustrative geographic districts: the tribally diverse capital district of Nairobi as well as two

districts where either Kikuyu or rival populations are highly concentrated (Thika and Kisumu,

24

respectively). The diverse capital district of Nairobi exhibits the same nationally aggregated

trend seen in models 1 and 2, with victims are more likely to be from the same Kikuyu tribe as

the corrupt agent. However, model 4 suggests that in a district dominated by the Kikuyu,

investors from rival tribes are 55 per cent more likely to be targeted for theft. In the district

dominated by rival tribe members, however, Kikuyu investors are 265 per cent more likely to be

targeted for theft relative to the rival tribe members who make up the dominant tribal group in

the district.

These results seem to be consistent with an agentic process by which the perpetrator is

attempting to socially isolate victims. On the aggregate, the corrupt agent will target members of

his own tribal group, but his selection of victims differs across these social groups according to

the concentration of members of that group in the district. Assuming that members of

antagonistic tribal groups would be less likely to communicate with each other (Yenkey 2012),

this could be an effective way to isolate victims of the fraud in a way that limits their opportunity

for collective recognition and/or action.

Investor reactions to fraud

Table 3 contains summary statistics and correlations for all variables in the analysis of

size of future investment according to exposure to the fraud, the subject of research question 2.

Tables 4 and 5 present OLS regression coefficients predicting the logged value of investments in

the telecom IPO following the Nyaga scandal. Model 1 in Table 4 contains the full set of control

variables as well the baseline effect of both being an Nyaga client and levels of experienced

losses from theft. Estimates do not differ significantly when each indicator of exposure to the

fraud are modeled separately. Not surprisingly, being an Nyaga client is predictive of smaller

25

future investments, but the baseline effect of an investor’s personal losses from theft are

positively related to size of future investment. One interpretation consistent with a performance

strain arguments (cite) is that experienced losses, such as this from theft, increase risky behaviors

in the form of additional investments in order to compensate for the loss.

**Tables 3 and 4 about here**

Model 2 adds the baseline effects of each investor’s tribal group membership, showing

that net of controls and exposure to the two forms of Nyaga scandal, Kikuyu investors are

expected to make larger investments in the telecom IPO than are rival tribe investors. Rival tribe

members, however, are predicted to make larger investments than are non-rival tribe investors.

Models 3-5 interact tribal group membership with the dichotomous measure of having

been a Nyaga client. The interaction term is negative for all three tribal groups, but interestingly

the negative effect of the interaction only produces an overall expected reduction in the size of

future investing for the non-Kikuyu groups. The positive effect of being a Kikuyu investor

exceeds the negative effect of the Nyaga client interaction term, predicting that Kikuyu clients of

the corrupt Kikuyu broker still make larger investments in the subsequent IPO on average, albeit

lower than if they were not an Nyaga client. In contrast, the negative effect of the interaction

term for both rival and non-rival tribal groups creates a net negative prediction for size of future

investing. Taken together, these results suggest that the aggregate effect of being a Nyaga client

is negative, but that this negative effect does not hold for members of the corrupt agent’s Kikuyu

tribe.

Models 6 – 8, however, suggest that the leniency of Kikuyu investors has its limits. Here,

the interaction effect of the financial value of the losses from theft is negative and significant for

Kikuyu investors (model 6) but not significant for investors from the rival tribe (model 7).

26

However, the magnitude of the negative interaction for Kikuyu investors is lower than the

baseline positive effect of these losses, suggesting that the increases in future investments

stimulated by actual loss are merely slowed for Kikuyu investors. I interpret this result as

suggesting that an increase in actual financial losses for clients sharing the social tie with their

broker restrict future investments for these in-group investors. For rival group investors,

however, mere exposure to the scandal via a client tie to the corrupt broker is sufficient for

trigging an overall reduction in future investing. Future models will need to investigate non-

linearity in the negative interaction term for financial losses of in-group investors in order to

ascertain the level at which predicted future investments might become negative.

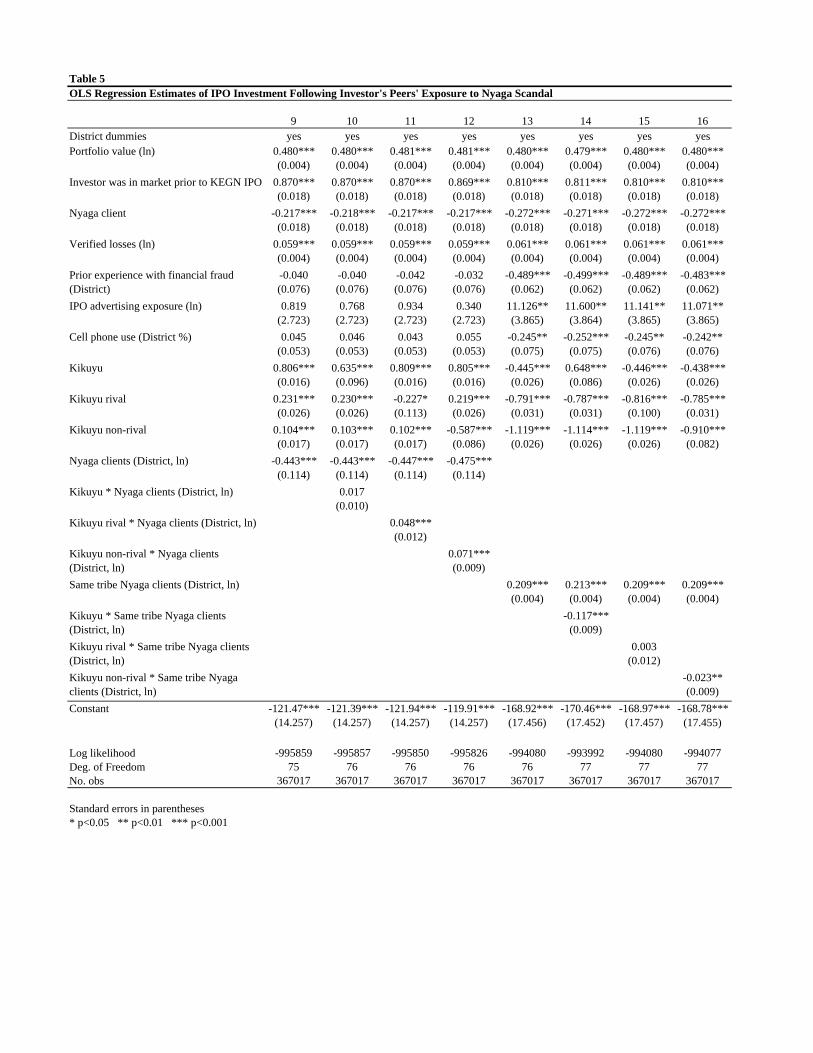

**Table 5 about here**

Table 5 presents a similar set of estimates, but rather than estimating the effects each

investor’s own exposure to the fraud these models estimate the effect of the district’s other

investors’ exposure to the Nyaga fraud. Models 9 – 12 show a baseline negative effect on future

investing when there are more Nyaga clients in the district; on the aggregate, being

geographically proximate to more investors who had to transfer their accounts due to the Nyaga

scandal seems to reduce the size of future investments for those investors in the market.

However, this effect seems to differ across investors in the three tribal groups. Kikuyu investors

are unaffected by increased numbers of Nyaga clients in their district (model 10), leaving them

with lower expected levels of future investing when in the presence of higher numbers of other

Nyaga clients. In contrast, the negative effect of proximity to other Nyaga clients is attenuated

for investors from rival and non-rival tribes (models 11 and 12), whose baseline negative effect

of proximity to other Nyaga clients is reduced as the number of other similarly f . It is important

to remember that these models estimate future investing for all investors in the market, not just

27

for Nyaga clients themselves. Accordingly, the relevant result here is that Kikuyu investors are

not particularly affected by higher rates of fraud-exposed investors in their district, but non-

Kikuyu investors seem to be positively affected by higher rates of fraud occurrence in their

district. One possible interpretation of this is that these out-group members take the presence of

greater numbers of defrauded others as indication that exposure to the fraud is not unique, which

might have the effect of reversing the negative effects of stereotype threat or reducing the

negative felt experience of being a member of a disadvantaged minority who is cheated by a

member of the majority group.

This pattern is reversed, though, when we look at the effects of proximity to Nyaga

clients who are also members of the investor’s same tribe. Models 13-16 show a baseline

positive effect of the number of Nyaga clients in an investor’s district who are also a member of

his tribal group. However, the interaction is insignificant for rival tribe investors while it is

negative and significant for Kikuyu investors and their non-rivals. Results from models focusing

on the reactions of Kikuyu investors (models 10 and 14) seem to suggest that these in-group

investors require negative experiences to be concentrated within the tribal group before

additionally reducing their willingness to invest in the market. In contract, models focusing on

investors from rival groups (models 11 and 15) suggest that the initial negative reaction to

exposure to the fraud will trigger any negative reaction while increased experience with the fraud

within the rival tribal group serves to ameliorate its negative effects.

Discussion

Taken together, the preliminary results presented here suggest that the corrupt

stockbroker studied here disproportionately targets members of his own tribal group for theft.

28

Model results suggest that although this is true on the aggregate, the perpetrator may also be

targeting victims according to their expected level of social interaction with proximate peers: in

districts with populations heavily oriented toward the Kikuyu tribe or its rivals, victims are

heavily drawn from the population of investors that represents the minority group in the area.

Subsequent to experiencing the fraud either personally or among other investors in one’s district,

investors from the same tribe as the corrupt broker continue to increase the value of future

investments while members of rival and non-rival tribes are expected to reduce future

investments. This pattern of less negative reactions to the fraud by investors who belong to the

corrupt broker’s tribe reduces, however, when the actual financial losses from direct theft of cash

and shares increase. Taken together, these results suggest that thresholds for negative reaction to

experiencing the fraud differ according to the mix of contentious group-level context in which

investor-broker ties are embedded, with same-group investors requiring a more direct, substantial

fraud to be perpetrated before reacting more negatively.

An alternative way to discuss these results would be to see them as a diagnostic tool for

thinking about how each member of the dyad sees the relationship are replaceable. Thinking

about the results as representative of the fungibility of ties according to the group-level contexts

in which they are embedded provides an opportunity to consider how corrupt agents may value

same-group ties differently from investors and how investors from the same or rival groups as

the perpetrator might differ in their reactions.

For example, the increased likelihood that a corrupt broker will choose a victim from his

own tribal group while those in-group investors continue to increase investments after being

exposed to the fraud suggest that the degree of tribe-level social identity and commitment is

higher for investors than it is for the corrupt broker. This finding is consistent with earlier work

29

from criminology that argues that social ties increase vulnerability to malfeasance. In a similar

way, the faster exit of rival group investors from the market suggests that they place a low value,

or have low expectations, of the outcomes of such ties.

Future directions

Three important questions remain to be addressed in order to provide a more complete analysis

of the role of social ties in the causes and consequences of the fraud studied here. Having already

mentioned the need to account for investor selection of a broker in the earlier section, I briefly

outline two additional issues that future work will need to address.

Earlier work has argued that affinity fraud is successful because those with ties to the

perpetrator, either at the interpersonal or group level, are more likely to assume that the agent is

trustworthy and therefore less likely to conduct due diligence. In the case considered here, there

is the potential for due diligence to play a role. Even though Nyaga stockbrokers operated a large

scale legitimate stockbrokerage business, the 18,000 or so clients that were stolen from would

have experienced those losses in the months leading up to Nyaga’s expulsion from the market in

March 2008. NSE investors are able to transfer their accounts to any intermediary at any point,

creating the potential that investors who did pay close attention to activity on their accounts

would have been at an increased likelihood to observe the fraud and take the corrective step of

transferring to another broker. The theoretical expectation is that investors from rival tribes

whom are known to have been direct victims would be more likely to transfer out of Nyaga prior

to the collapse. Future iterations of the analysis will want to account for this possibility.

Given that I am measuring investor reaction to fraud committed by an intermediary by

looking at future market participation, there exists the possibility that the affected investor’s

30

selection of another stockbroker in the time between the fraud and the next round of investing

would affect her level of trust in the market and therefore willingness to continue to invest. A

range of intermediaries with seats on the NSE exist, including brokers of all tribal affiliations as

well as more tribally neutral commercial banks that can execute share trades and IPO

subscriptions. Therefore, there is the possibility that investors who experienced the Nyaga fraud

could have selected a broker with a different set of characteristics, and in doing so indicate that

the lost trust was embodied in the attributes of the corrupt broker rather than in the market itself.

That is, selecting a qualitatively different intermediary could have the effect of re-establishing

trust in the stock market and therefore mitigate the impact of fraud on market performance.

Future iterations of the analysis will need to control for the intermediary that the defrauded

investors select after the Nyaga collapse and before the telecom IPO subscription.

31

References

Baker, W. E., & Faulkner, R. R. (1993). The social organization of conspiracy: Illegal networks

in the heavy electrical equipment industry. American Sociological Review, 837-860. Baker, W. E., & Faulkner, R. R. (2004). Social networks and loss of capital. Social Networks,

26(2), 91-111. Biggart, N. W. (2001). Banking on each other: the situational logic of rotating savings and credit

associations. Advances in Qualitative Organization Research, 3(1), 129-152. Boyle, J. M., Heinzelmann, F., & Titus, R. (1995). The Anatomy of Fraud: Report of a

Nationwide Survey. National Institute of Justice journal. Brass, D. J., Butterfield, K. D., & Skaggs, B. C. (1998). Relationships and unethical behavior: A

social network perspective. Academy of Management Review, 14-31. Brewer, M. B. (1968). Determinants of social distance among East African tribal groups. Journal

of Personality and Social Psychology, 10(3), 279-289. Brewer, M. B. (1981). Ethnocentrism and Its Role in Interpersonal Trust Scientific Inquiry and

the Social Sciences. New York: Jossey-Bass.

Burt, R. S., & Knez, M. (1995). Kinds of Third-Party Effects on Trust. Rationality and Society, 7(3), 255-292.

Carr, P. B., & Steele, C. M. (2010). Stereotype threat affects financial decision making. Psychol

Sci, 21(10), 1411-1416. Clinard, M. R. (1984). The Phantom Capitalists: The Organization and Control of Long-Firm

Fraud by Michael Levi. The British Journal of Sociology, 35(1), 141. Coleman, J. S. (1988). Social capital in the creation of human capital. American Journal of

Sociology, 95-120. Coleman, J. S. (1990). Relations of Trust Foundations of Social Theory. Cambridge, MA:

Belknap Press of Harvard University Press. DiMaggio, P., & Louch, H. (1998). Socially Embedded Consumer Transactions: For What Kinds

of Purchases Do People Most Often use Networks? American Sociological Review, 63(5), 619-637.

Dincer, O. C. (2011). Ethnic Diversity and Trust. Contemporary Economic Policy, 29(2), 284-

293. Elischer, S. (2008). Ethnic Coalitions of Convenience and Commitment: Political Parties and

Party Systems in Kenya. GIGA German Institute of Global and Area Studies(68).

32

Foddy, M., Platow, M. J., & Yamagishi, T. (2009). Group-Based Trust in Strangers: The Role of

Stereotypes and Expectations. Psychological Science, 20(4), 419-422. Geertz, C. (1962). The Rotating Credit Association: A "Middle Rung" in Development.

Economic Development and Cultural Change, 10(3), 241-263. Georgarakos, D., & Pasini, G. (2011). Trust, Sociability, and Stock Market Participation. Review

of Finance, 15(4), 693-725. Granovetter, M. (1985). Economic action and social structure: the problem of embeddedness.

American Journal of Sociology, 481-510. Granovetter, M. (1992). Problems of explanation in economic sociology. In N. Nohria & R.

Eccles (Eds.), {Networks and Organizations: Structure, Form, and Action} (pp. 25-56): Harvard University School Press.

Guiso, L., Sapienza, P., & Zingales, L. (2008). Trusting the Stock Market. The Journal of

Finance, 63(6), 2557-2600. Gutierrez-Romero, R. The Role of Ethnic Identity and Economic Issues in the 2007 Kenyan

Elections. Hall, J. R. (1988). Social Organization and Pathways of Commitment: Types of Communal

Groups, Rational Choice Theory, and the Kanter Thesis. American Sociological Review, 53(5), 679-692.

Kossinets, G., & Watts, Duncan J. (2009). Origins of Homophily in an Evolving Social

Network1. American Journal of Sociology, 115(2), 405-450. Kramer, R. M. (1999). Trust and distrust in organizations: Emerging perspectives, enduring

questions. Annual review of psychology, 50(1), 569-598. Lawler, E. J. (1992). Affective Attachments to Nested Groups: A Choice-Process Theory.

American Sociological Review, 57(3), 327-339. McEvily, B., Perrone, V., & Zaheer, A. (2003). Trust as an organizing principle. Organization

Science, 91-103. Peng, Y. (2004). Kinship Networks and Entrepreneurs in China’s Transitional Economy.

American Journal of Sociology, 109(5), 1045-1074. Portes, A., & Sensenbrenner, J. (1993). Embeddedness and Immigration: Notes on the Social

Determinants of Economic Action. American Journal of Sociology, 98(6), 1320.

33

Rao, H., Davis, G. F., & Ward, A. (2000). Embeddedness, Social Identity and Mobility: Why Firms Leave the NASDAQ and Join the New York Stock Exchange. Administrative Science Quarterly, 45(2), 268-292.

Risen, J. L., Gilovich, T., & Dunning, D. (2007). One-shot illusory correlations and stereotype

formation. Pers Soc Psychol Bull, 33(11), 1492-1502. Seligman, A. B. (1998). Trust and Sociability. American Journal of Economics and Sociology,

57(4), 391-404. Sgourev, S. V., & Zuckerman, E. W. (2011). Breaking up is hard to do: Irrational inconsistency

in commitment to an industry peer network. Rationality and Society, 23(1), 3-34. Sorenson, O., & Waguespack, D. M. (2006). Social structure and exchange: Self-confirming

dynamics in Hollywood. Administrative Science Quarterly, 51(4), 560-589. Tropp, L. R., Stout, A. M., Boatswain, C., Wright, S. C., & Pettigrew, T. F. (2006). Trust and

Acceptance in Response to References to Group Membership: Minority and Majority Perspectives on Cross-Group Interactions1. Journal of Applied Social Psychology, 36(3), 769-794.

Tyler, T. R. (2001). Why Do People Rely on Others? In K. S. Cook (Ed.), Trust in Society. New

York: Russell Sage Foundation. van Ufford, P. Q., & Zaal, F. (2011). The Transfer of Trust: Ethnicities as Economic Institutions

in the Livestock Trade in West and East Africa. Africa, 74(02), 121-145. Zak, P. J., & Knack, S. (2001). Trust and Growth. The Economic Journal, 111, 295-321.

Figure 1: Scatterplot of Percentage of Nyaga Clients and Victims, by district

Note: Five largest districts not shown.

Figure 2: Pre- and Post-Scandal Portfolio Values and % Lost by the 18,006 Nyaga Victims

Note: All 18,006 accounts with ICF verified claims shown.

y = 0.9553x + 0.0657

0

0.5

1

1.5

2

0 0.5 1 1.5 2

% o

f al

l Nya

ga v

icti

ms

in t

he

dis

tric

t

% of all Nyaga clients in the district

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

% of p

ort value lost

Por

t. v

alu

e an

d v

erif

ied

loss

(K

sh)

Post-scandalportfoliovalue (leftaxis)

Verifiedclaim (leftaxis)

% ofportfoliovalue stolen(right axis)

Table 1Descriptive Statistics and Correlation Matrix, verified losses from theft among Nyaga clients (N=71,347):

Variable Mean Std. Dev. Min Max 1 2 3 4 5 6 7 81 Nyaga victim 0.25 0.43 0 12 Kikuyu 0.60 0.41 0 1 0.053 Kikuyu rival 0.06 0.20 0 1 -0.04 -0.334 Kikuyu non-rival 0.36 0.34 0 1 -0.02 -0.34 -0.125 Portoflio value (ln) 9.92 1.75 3.22 20.43 0.14 -0.02 -0.02 -0.016 Portfolio diversity 2.40 2.34 1 50 0.15 0.01 -0.02 0.01 0.667 More experienced investor 0.24 0.43 0 1 0.08 0.00 -0.02 0.00 0.53 0.478 Nyaga clients who are Kikuyu (District %) 60.34 13.46 0 79.82 0.07 0.33 -0.17 -0.17 -0.02 0.00 0.009 Nyaga clients who are Kikuyu rivals (District %) 35.90 7.74 2.08 100 -0.04 -0.25 0.01 0.22 0.02 0.01 0.00 -0.77

Table 2

Logistic Regression Estimates of Having a Verified Loss from Nyaga Theft (N=71,347):

1 2 3 4 5

District dummies yes yesNairobi

onlyKikuyu district

Rival district

Portoflio value (ln) 0.106*** (0.007)

0.106*** (0.007)

0.115*** (0.010)

0.093*** (0.020)

0.447* (0.211)

Portfolio diversity 0.091*** (0.006)

0.091*** (0.006)

0.061*** (0.008)

0.108*** (0.018)

0.006 (0.115)

Investor was in market prior to KEGN IPO -0.075** (0.025)

-0.075** (0.025)

-0.061 (0.039)

-0.179** (0.065)

-0.594 (0.924)

Kikuyu 0.127*** (0.026)

0.127*** (0.026)

0.288*** (0.036)

-0.050 (0.073)

2.649** (0.994)

Kikuyu rival -0.150** (0.052)

-0.150** (0.052)

-0.093 (0.065)

0.545** (0.201)

1.178 (0.904)

Kikuyu non-rival -0.026 (0.029)

-0.026 (0.029)

-0.008 (0.041)

0.005 (0.081)

-1.013 (1.196)

Nyaga clients who are Kikuyu (District %)

0.003

(0.008) Nyaga clients who are Kikuyu rivals (District %)

-0.058* (0.025)

Constant -2.520*** (0.071)

-0.430 (1.352)

-2.634*** (0.098)

-2.033*** (0.191)

-7.511*** (2.008)

Log likelihood -39066 -39066 -18269 -5711 -44Chi-squared 2096 2096 733 184 29Deg. of Freedom 65 65 6 6 6No. obs 71327 71327 34261 9710 183

Coefficients presented as odds ratios; robust standard errors in parentheses.A22* p<0.05 ** p<0.01 *** p<0.001

Table 3Descriptive Statistics and Correlation Matrix, future investments following the Nyaga scandal (N=397,413)

Variable Mean Std. Dev. Min Max 1 2 3 4 5 6 7 8 9 10 11 12 13 141 Investment size (ln) 3.69 3.85 0 18.352 Kikuyu 0.45 0.44 0 1 0.083 Kikuyu rival 0.09 0.26 0 1 -0.03 -0.304 Kikuyu non-rival 0.40 0.38 0 1 -0.02 -0.22 -0.145 Same tribe Nyaga clients (District, ln) 7.36 3.58 0 10.76 0.08 0.53 0.01 0.406 Financial losses of other Nyaga clients in same tribe (District) 14.58 6.62 0 19.47 0.09 0.52 0.04 0.42 0.987 Nyaga clients (District, ln) 9.51 1.85 0 10.77 -0.03 0.08 -0.09 -0.04 0.37 0.238 Nyaga client 0.18 0.38 0 1 0.01 0.16 -0.06 -0.04 0.10 0.11 0.019 Verified theft (ln) 0.33 1.66 0 16.59 0.04 0.08 -0.04 -0.03 0.05 0.05 0.00 0.42

10 Profit on previous investment (ln) 15.85 0.01 15.60 18.04 0.04 -0.02 -0.01 -0.01 -0.03 -0.03 0.01 -0.01 0.0011 Portfolio value (ln) 10.07 1.85 2.82 23.02 0.27 -0.06 -0.04 -0.03 -0.06 -0.07 0.01 -0.04 0.05 0.0812 Investor was in market prior to KEGN IPO 0.22 0.41 0 1 0.21 0.02 -0.02 0.00 0.03 0.04 -0.01 0.03 0.06 0.02 0.5013 Prior experience with financial fraud (District) 4.17 1.76 0 28.53 -0.04 -0.12 0.13 -0.02 -0.06 -0.08 -0.02 -0.08 -0.04 0.00 0.01 0.0014 IPO advertising exposure (ln) 4.93 0.56 2.59 5.33 -0.06 -0.07 0.01 0.01 0.24 0.11 0.79 -0.05 -0.03 0.01 0.02 -0.03 0.0315 Cell phone use (District %) 69.59 14.60 7.93 79.83 -0.05 -0.04 0.00 -0.02 0.26 0.14 0.84 -0.07 -0.04 0.01 0.02 -0.04 0.15 0.81

Table 4OLS Regression Estimates of IPO Investment Following Investor's Exposure to Nyaga Scandal

1 2 3 4 5 6 7 8District dummies yes yes yes yes yes yes yes yesProfit on previous investment (ln) 6.905***

(0.630)7.332*** (0.628)

7.362*** (0.628)

7.334*** (0.628)

7.339*** (0.628)

7.339*** (0.628)

7.332*** (0.628)

7.336*** (0.628)

Portfolio value (ln) 0.463*** (0.004)

0.480*** (0.004)

0.481*** (0.004)

0.480*** (0.004)

0.480*** (0.004)

0.481*** (0.004)

0.480*** (0.004)

0.480*** (0.004)

Investor was in market prior to KEGN IPO 0.918*** (0.018)

0.870*** (0.018)

0.868*** (0.018)

0.870*** (0.018)

0.870*** (0.018)

0.870*** (0.018)

0.870*** (0.018)

0.870*** (0.018)

Nyaga client -0.151*** (0.018)

-0.217*** (0.018)

-0.020 (0.028)

-0.195*** (0.019)

-0.168*** (0.024)

-0.219*** (0.018)

-0.217*** (0.018)

-0.216*** (0.018)

Verified theft (ln) 0.061*** (0.004)

0.059*** (0.004)

0.060*** (0.004)

0.058*** (0.004)

0.059*** (0.004)

0.089*** (0.007)

0.060*** (0.004)

0.072*** (0.005)

Prior experience with financial fraud (District)

-0.381*** (0.063)

-0.397*** (0.063)

-0.399*** (0.063)

-0.396*** (0.063)

-0.397*** (0.063)

-0.396*** (0.063)

-0.397*** (0.063)

-0.397*** (0.063)

IPO advertising exposure (ln) 9.369* (3.898)

9.571* (3.884)

9.644* (3.883)

9.541* (3.884)

9.596* (3.884)

9.582* (3.883)

9.569* (3.884)

9.580* (3.884)

Cell phone use (District %) -0.182* (0.076)