TRS and Other Benefits Issues Arising in Collective Bargaining and Administrator Contracts Andrew...

25

Arising in Arising in Collective Collective Bargaining and Bargaining and Administrator Administrator Contracts Contracts Andrew Malahowski Andrew Malahowski Franczek Sullivan P.C. Franczek Sullivan P.C.

-

Upload

madeleine-nash -

Category

Documents

-

view

221 -

download

1

Transcript of TRS and Other Benefits Issues Arising in Collective Bargaining and Administrator Contracts Andrew...

TRS and Other Benefits TRS and Other Benefits Issues Arising in Collective Issues Arising in Collective

Bargaining and Bargaining and Administrator ContractsAdministrator Contracts

Andrew MalahowskiAndrew Malahowski

Franczek Sullivan P.C.Franczek Sullivan P.C.

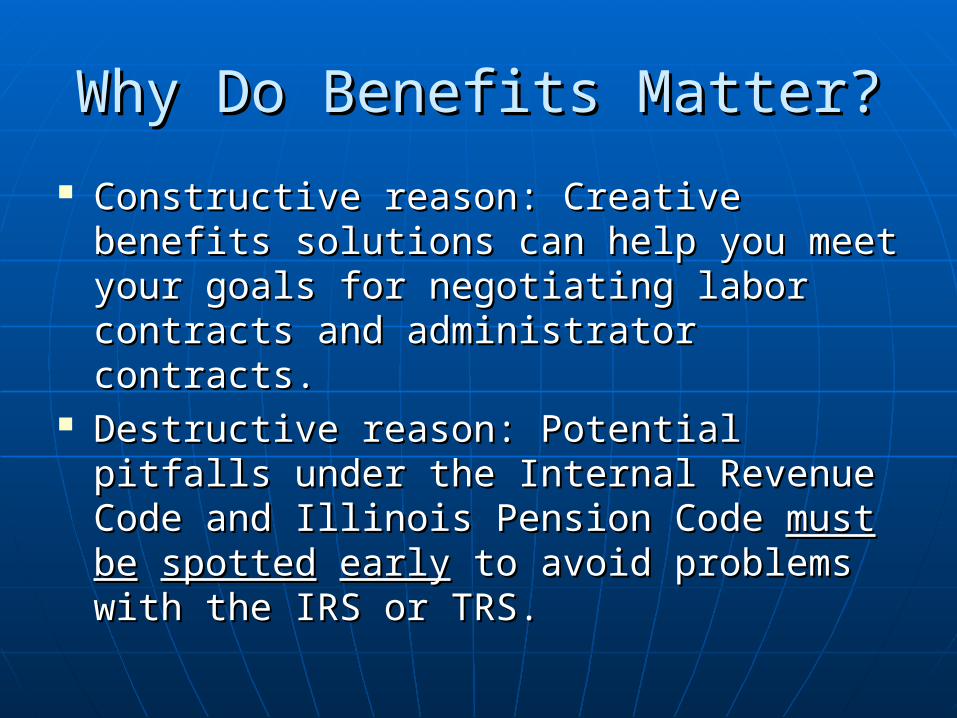

Why Do Benefits Matter?Why Do Benefits Matter?

Constructive reason: Creative benefits Constructive reason: Creative benefits solutions can help you meet your goals for solutions can help you meet your goals for negotiating labor contracts and negotiating labor contracts and administrator contracts.administrator contracts.

Destructive reason: Potential pitfalls under Destructive reason: Potential pitfalls under the Internal Revenue Code and Illinois the Internal Revenue Code and Illinois Pension Code Pension Code mustmust bebe spottedspotted earlyearly to to avoid problems with the IRS or TRS. avoid problems with the IRS or TRS.

Collective BargainingCollective Bargaining

Goals:Goals:• Reach a deal that is affordableReach a deal that is affordable

Figure out expectationsFigure out expectations Know that something unexpected will Know that something unexpected will

happenhappen

• Reach a deal that you can sell to the Reach a deal that you can sell to the BoardBoard

• Reach a deal that the Union can sell to Reach a deal that the Union can sell to the Union membership for ratificationthe Union membership for ratification

• Avoid TRS penaltiesAvoid TRS penalties

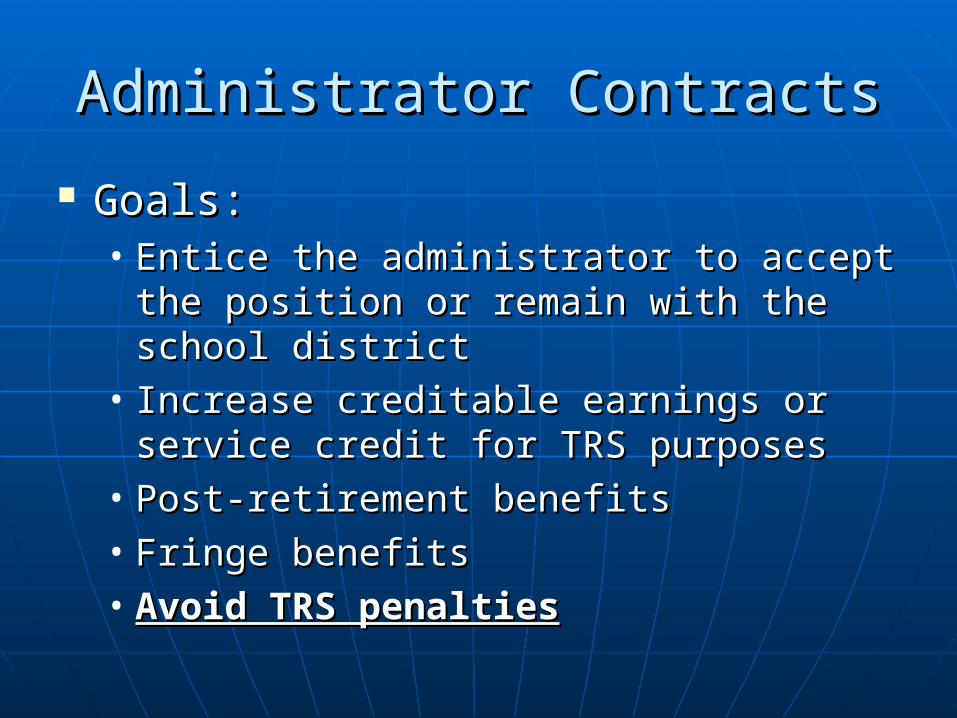

Administrator ContractsAdministrator Contracts

Goals: Goals: • Entice the administrator to accept the Entice the administrator to accept the

position or remain with the school position or remain with the school districtdistrict

• Increase creditable earnings or service Increase creditable earnings or service credit for TRS purposescredit for TRS purposes

• Post-retirement benefitsPost-retirement benefits• Fringe benefitsFringe benefits• Avoid TRS penaltiesAvoid TRS penalties

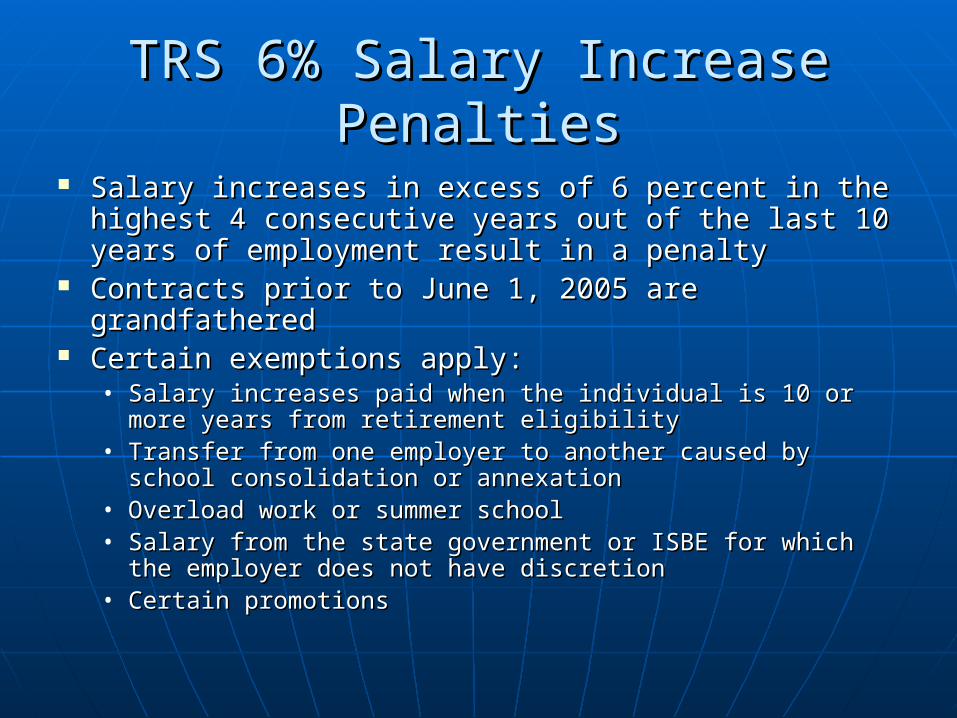

TRS 6% Salary Increase PenaltiesTRS 6% Salary Increase Penalties

Salary increases in excess of 6 percent in the Salary increases in excess of 6 percent in the highest 4 consecutive years out of the last 10 highest 4 consecutive years out of the last 10 years of employment result in a penaltyyears of employment result in a penalty

Contracts prior to June 1, 2005 are grandfatheredContracts prior to June 1, 2005 are grandfathered Certain exemptions apply:Certain exemptions apply:

• Salary increases paid when the individual is 10 or more Salary increases paid when the individual is 10 or more years from retirement eligibilityyears from retirement eligibility

• Transfer from one employer to another caused by school Transfer from one employer to another caused by school consolidation or annexationconsolidation or annexation

• Overload work or summer schoolOverload work or summer school• Salary from the state government or ISBE for which the Salary from the state government or ISBE for which the

employer does not have discretionemployer does not have discretion• Certain promotionsCertain promotions

TRS 6% Salary Increase PenaltiesTRS 6% Salary Increase Penalties

Promotion exemption: salary increases resulting Promotion exemption: salary increases resulting from a promotion are excluded if all of the from a promotion are excluded if all of the following conditions are met:following conditions are met:• The employee is required to hold a certificate or The employee is required to hold a certificate or

supervisory endorsement that is a different certification supervisory endorsement that is a different certification or endorsement than is required for the employee’s or endorsement than is required for the employee’s previous positionprevious position

• The position has existed and has been filled by a The position has existed and has been filled by a member for no less than one academic yearmember for no less than one academic year

• The increase results in an amount of salary no greater The increase results in an amount of salary no greater than the lesser of the average salary paid for other than the lesser of the average salary paid for other similar positions in the district requiring the same similar positions in the district requiring the same certification or the amount stipulated in the collective certification or the amount stipulated in the collective bargaining agreement for a similar position requiring the bargaining agreement for a similar position requiring the same certification same certification

What Are TRS Creditable What Are TRS Creditable Earnings?Earnings?

More than just base salaryMore than just base salary But, less than every dollar and fringe But, less than every dollar and fringe

benefit that an employee receivesbenefit that an employee receives Before you negotiate a new payment Before you negotiate a new payment

or fringe benefit for an employee, it or fringe benefit for an employee, it is critically important to determine is critically important to determine whether or not it counts as TRS whether or not it counts as TRS creditable earningscreditable earnings

Non-Salary TRS Non-Salary TRS Creditable EarningsCreditable Earnings

2.2 Upgrade2.2 Upgrade

Allows a participant with TRS-Allows a participant with TRS-covered service prior to June, 1998 to covered service prior to June, 1998 to have his or her retirement benefit have his or her retirement benefit calculation increasedcalculation increased• Fairly common in administrator Fairly common in administrator

contractscontracts• Sometimes offered as a retirement Sometimes offered as a retirement

incentive in collective bargaining incentive in collective bargaining agreementsagreements

District “Pick-Up” of TRS District “Pick-Up” of TRS ContributionsContributions

TRS members are required to contribute 9.4 TRS members are required to contribute 9.4 percent of creditable earningspercent of creditable earnings

If the District picks up these contributions, that If the District picks up these contributions, that results in additional creditable earnings that are results in additional creditable earnings that are also subject to contributionsalso subject to contributions

TRS Factors: A pick up of the entire 9.4 percent TRS Factors: A pick up of the entire 9.4 percent results in a factor of 10.3753 percent being added results in a factor of 10.3753 percent being added to creditable earningsto creditable earnings

Common in administrator contracts; not common Common in administrator contracts; not common in collective bargaining agreementsin collective bargaining agreements

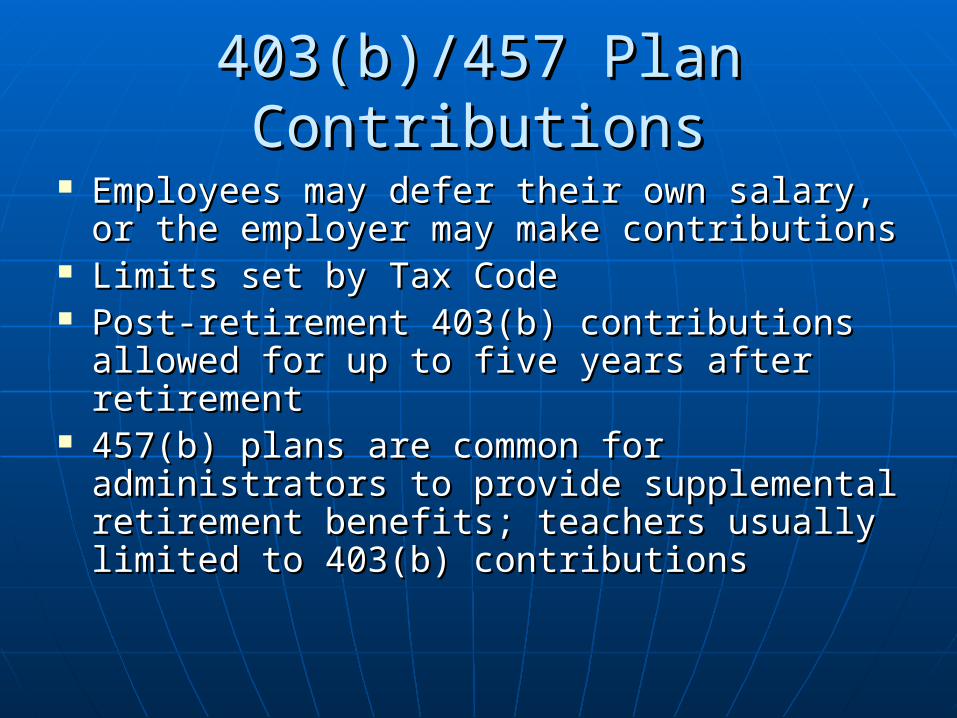

403(b)/457 Plan Contributions403(b)/457 Plan Contributions

Employees may defer their own salary, or Employees may defer their own salary, or the employer may make contributionsthe employer may make contributions

Limits set by Tax CodeLimits set by Tax Code Post-retirement 403(b) contributions Post-retirement 403(b) contributions

allowed for up to five years after allowed for up to five years after retirementretirement

457(b) plans are common for 457(b) plans are common for administrators to provide supplemental administrators to provide supplemental retirement benefits; teachers usually retirement benefits; teachers usually limited to 403(b) contributionslimited to 403(b) contributions

403(b) Plans403(b) Plans

The IRS will require all 403(b) plans The IRS will require all 403(b) plans to be administered pursuant to a to be administered pursuant to a formal plan document, starting on formal plan document, starting on January 1, 2008January 1, 2008

A plan document must contain the A plan document must contain the basic terms of the 403(b) plan:basic terms of the 403(b) plan:• Eligibility, benefits, limits, form of and Eligibility, benefits, limits, form of and

time of distributions, as well as time of distributions, as well as permissive features such as loans, permissive features such as loans, hardship distributions, etc. hardship distributions, etc.

Flexible Spending AccountsFlexible Spending Accounts

May provide a choice between May provide a choice between qualified benefits and cashqualified benefits and cash

May either be part of a district-wide May either be part of a district-wide FSA, and will be tax-free, or can be FSA, and will be tax-free, or can be offered solely to a select group of offered solely to a select group of administrators, and will be taxableadministrators, and will be taxable

All contributions to FSA are All contributions to FSA are reportable as creditable earningsreportable as creditable earnings

Benefits That Do Not Count Benefits That Do Not Count As TRS Creditable As TRS Creditable

EarningsEarnings

Reimbursements and AllowancesReimbursements and Allowances

Not TRS creditable earningsNot TRS creditable earnings May be excludable for federal tax May be excludable for federal tax

purposespurposes Common for administratorsCommon for administrators

Retiree Medical CoverageRetiree Medical Coverage Less and less common for administrators; not Less and less common for administrators; not

common, and not recommended for teachers (at least common, and not recommended for teachers (at least in its traditional form)in its traditional form)

The district may agree to pay an individual’s portion of The district may agree to pay an individual’s portion of TRS medical premiums after retirementTRS medical premiums after retirement

In the alternative, the individual may be kept on the In the alternative, the individual may be kept on the district’s retirement plandistrict’s retirement plan

Not subject to federal income taxationNot subject to federal income taxation Non-traditional alternative: HRA or VEBA contributions Non-traditional alternative: HRA or VEBA contributions

during employment and use after retirementduring employment and use after retirement• VEBA contributions funded by deductions from VEBA contributions funded by deductions from

salary would be creditable compensation for TRS salary would be creditable compensation for TRS purposespurposes

What is a VEBA?What is a VEBA?

VEBA stands for “Voluntary Employees VEBA stands for “Voluntary Employees Beneficiary Association.”Beneficiary Association.”• It is a tax exempt entity (usually a trust) that is It is a tax exempt entity (usually a trust) that is

established to provide medical, dental, established to provide medical, dental, prescription drug, accident, life insurance, and prescription drug, accident, life insurance, and other qualified benefits to its members or their other qualified benefits to its members or their dependentsdependents

• Contributions to the trust are not taxable to Contributions to the trust are not taxable to employees employees

• Payments from the trust are not taxed if they are Payments from the trust are not taxed if they are used to pay for or provide tax qualified benefitsused to pay for or provide tax qualified benefits

Post-Retirement/Post-Resignation Post-Retirement/Post-Resignation PaymentsPayments

Compensation paid after the individual’s Compensation paid after the individual’s final day of work and after his or her final final day of work and after his or her final paycheck for regular earnings are not TRS paycheck for regular earnings are not TRS creditable earningscreditable earnings

Note on post-retirement payments: Note on post-retirement payments: governed by Section 457(f)governed by Section 457(f)

Note on post-resignation payments to Note on post-resignation payments to administrator: payments after an administrator: payments after an employee’s resignation would still be TRS employee’s resignation would still be TRS creditable earnings if he or she continues creditable earnings if he or she continues to work for another TRS-covered employer to work for another TRS-covered employer after resignationafter resignation

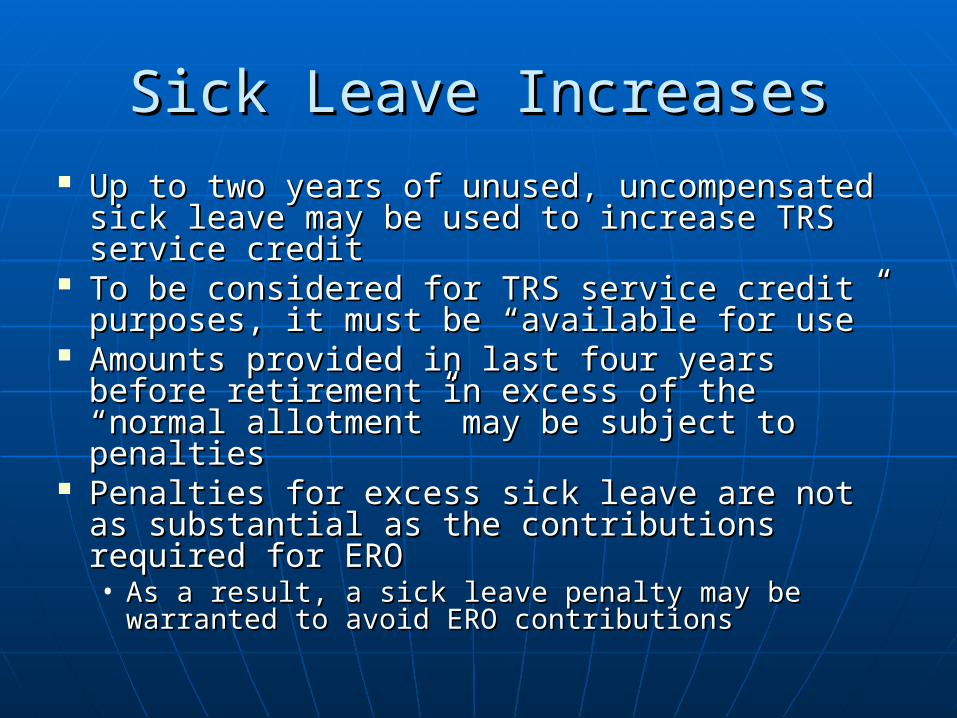

Sick Leave IncreasesSick Leave Increases Up to two years of unused, uncompensated Up to two years of unused, uncompensated

sick leave may be used to increase TRS sick leave may be used to increase TRS service creditservice credit

To be considered for TRS service credit To be considered for TRS service credit purposes, it must be “available for use”purposes, it must be “available for use”

Amounts provided in last four years before Amounts provided in last four years before retirement in excess of the “normal retirement in excess of the “normal allotment” may be subject to penaltiesallotment” may be subject to penalties

Penalties for excess sick leave are not as Penalties for excess sick leave are not as substantial as the contributions required for substantial as the contributions required for EROERO• As a result, a sick leave penalty may be As a result, a sick leave penalty may be

warranted to avoid ERO contributionswarranted to avoid ERO contributions

TRS Early Retirement OptionTRS Early Retirement Option Employer and member contributions, though the member Employer and member contributions, though the member

contribution may be picked up by the employer (not contribution may be picked up by the employer (not common for teachers)common for teachers)

For employees who have at least 55 years of age and 20 For employees who have at least 55 years of age and 20 years of service, and who are both under age 60 and have years of service, and who are both under age 60 and have less than 35 years of serviceless than 35 years of service

Contribution rates for ERO have increased:Contribution rates for ERO have increased:• The participant contribution increased from 7% to 11.5% The participant contribution increased from 7% to 11.5%

multiplied by the lesser of the administrator’s years or partial multiplied by the lesser of the administrator’s years or partial years under 35 years of service or 60 years of ageyears under 35 years of service or 60 years of age

• The employer contribution increased from 20% to 23.5% The employer contribution increased from 20% to 23.5% multiplied by the number of years the administrator is under multiplied by the number of years the administrator is under 60 years of age60 years of age

10% cap permitted by TRS10% cap permitted by TRS IRC 414(h) language is necessaryIRC 414(h) language is necessary

TRS 6% Salary Increase PenaltiesTRS 6% Salary Increase Penalties(Revisited)(Revisited)

Avoiding the penalty:Avoiding the penalty:• Retirement incentive plan offering 6% Retirement incentive plan offering 6%

increasesincreases• Provide non-creditable compensationProvide non-creditable compensation• Follow the 6 percent salary increase Follow the 6 percent salary increase

penalty exemptionspenalty exemptions• Provide post-retirement compensationProvide post-retirement compensation• Agree to pay increases in excess of 6 Agree to pay increases in excess of 6

percent five or more years before percent five or more years before retirement (common for administrators)retirement (common for administrators)

TRS 6% Salary Increase PenaltiesTRS 6% Salary Increase Penalties(Example A)(Example A)

Salary w/ 4% Salary w/ 4% annual increaseannual increase

Salary w/ 4% Salary w/ 4% annual increase annual increase and two 20% and two 20% increasesincreases

Increase Increase Amount Amount Exceeding 6%Exceeding 6%

2007-20082007-2008

2008-20092008-2009

2009-20102009-2010

2010-20112010-2011

2011-20122011-2012

170,000170,000

176,800176,800

183,872183,872

191,227191,227

198,876198,876

170,000170,000

176,800176,800

183,872183,872

220,646220,646

264,776264,776

------

------

------

25,74225,742

30,89130,891

Total Creditable Total Creditable Earnings in Final 4 Earnings in Final 4 Years/ AverageYears/ Average

750,775 /750,775 /

187,694187,694846,094 /846,094 /

211,524211,524------

TRS Annual TRS Annual Benefit (Assuming Benefit (Assuming a 75% annuity)a 75% annuity)

140,770140,770 158,643158,643 ------

TRS 6% Salary TRS 6% Salary Increase PenaltyIncrease Penalty

------ 138,381138,381 ------

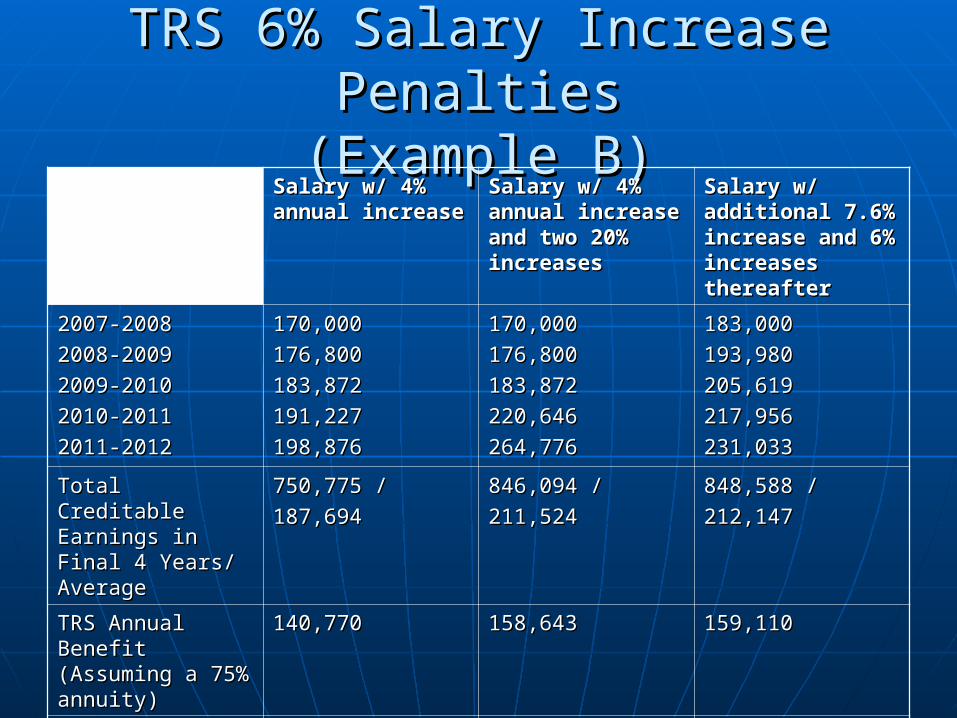

TRS 6% Salary Increase PenaltiesTRS 6% Salary Increase Penalties(Example B)(Example B)

Salary w/ 4% Salary w/ 4% annual increaseannual increase

Salary w/ 4% Salary w/ 4% annual increase annual increase and two 20% and two 20% increasesincreases

Salary w/ Salary w/ additional 7.6% additional 7.6% increase and increase and 6% increases 6% increases thereafterthereafter

2007-20082007-2008

2008-20092008-2009

2009-20102009-2010

2010-20112010-2011

2011-20122011-2012

170,000170,000

176,800176,800

183,872183,872

191,227191,227

198,876198,876

170,000170,000

176,800176,800

183,872183,872

220,646220,646

264,776264,776

183,000183,000

193,980193,980

205,619205,619

217,956217,956

231,033231,033

Total Creditable Total Creditable Earnings in Final 4 Earnings in Final 4 Years/ AverageYears/ Average

750,775 /750,775 /

187,694187,694846,094 /846,094 /

211,524211,524848,588 /848,588 /

212,147212,147

TRS Annual TRS Annual Benefit (Assuming Benefit (Assuming a 75% annuity)a 75% annuity)

140,770140,770 158,643158,643 159,110159,110

TRS 6% Salary TRS 6% Salary Increase PenaltyIncrease Penalty

------ 138,381138,381 ------

Collective Bargaining Agreement Collective Bargaining Agreement 6% Retirement Incentive Plans6% Retirement Incentive Plans

Common to offer 1, 2, 3, or 4 years of 6% Common to offer 1, 2, 3, or 4 years of 6% increases as a retirement incentiveincreases as a retirement incentive

Post-retirement incentives can be useful to Post-retirement incentives can be useful to persuade teachers to elect the planpersuade teachers to elect the plan

Other 6% protections:Other 6% protections:• Recoup penalties? (disfavored by TRS)Recoup penalties? (disfavored by TRS)• Recoup excess salary over 6%? (disfavored by Recoup excess salary over 6%? (disfavored by

TRS)TRS)• Make an employee “ineligible” for benefits not Make an employee “ineligible” for benefits not

yet receivedyet received• Require early documentation of TRS creditable Require early documentation of TRS creditable

serviceservice

Questions?Questions?