Tropical Bank Limited - financial statements 2012 final · The Bank's risk management strategy is...

58

31 December 2012 Financial Statements Tropical Bank Limited Annual Report and

Transcript of Tropical Bank Limited - financial statements 2012 final · The Bank's risk management strategy is...

31 December 2012

Financial Statements

Tropical Bank Limited

Annual Report and

TROPICAL BANK LIMITEDANNUAL REPORT AND FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2012

CONTENTS PAGES

Corporate Information 2 - 3

Chairman's statement 4 - 6

Report of the directors 7 - 12

Statement of directors' responsibilities 13

Report of the independent auditors 14 - 15

Financial statements:

Statement of comprehensive income 16

Statement of financial position 17

Statement of changes in equity 18

Statement of cash flows 19

Notes to the financial statements 20 - 59

1

TROPICAL BANK LIMITEDCORPORATE INFORMATIONFOR THE YEAR ENDED 31 DECEMBER 2012

DIRECTORSThe directors who held office during the year and to the date of this report were as follows:

Gerald M Ssendaula + - Chairman Abdulmonam Geat Ali Tbigha ++ - Deputy ChairmanOsama Rami Serrag ++ - Managing DirectorEzzeddin Mohamend Ibrahim Amer ++ - DirectorKassim Nakibinge Kakungulu+ - Executive Director

++ Libyan+ Ugandan

COMPANY AND BOARD SECRETARY Mrs. Addah T. WeguloPlot 27 Kampala RoadP.O. Box 9485Kampala, Uganda

REGISTERED OFFICE Plot 27 Kampala RoadP.O. Box 9485Kampala, Uganda

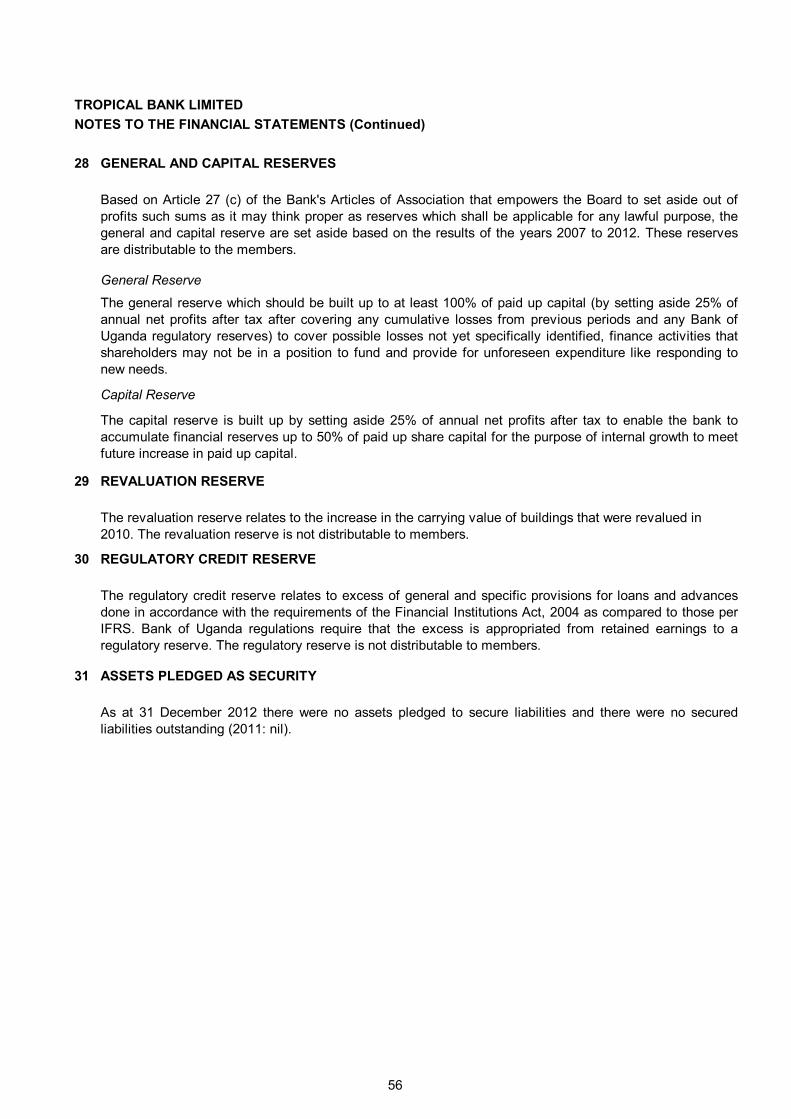

BRANCHES Plot 2, Birch Avenue Plot 34/38 Nakivubo RoadMasaka NakivuboP.O. Box 39 P.O. Box 9485Masaka, Uganda Kampala, Uganda

Plot 17, Main Street Plot 1 Kimera RoadJinja NtindaP.O. Box 100 P.O. Box 9485Jinja, Uganda Kampala, Uganda

Plot 3144 Kawempe Plot 5277 Ggaba roadP.O. Box 9485 KansangaKawempe P.O. Box 9485Kampala, Uganda Kampala, Uganda

2

TROPICAL BANK LIMITEDCORPORATE INFORMATION (Continued)FOR THE YEAR ENDED 31 DECEMBER 2012

AUDITORS Ernst & YoungCertified Public Accountants (Uganda)Shimoni Office Village18 Clement Hill RoadP.O. Box 7215 Kampala, Uganda

SOLICITORS MMAKS Advocates3rd Floor Diamond Trust BuildingP.O. Box 7166Kampala, Uganda

Muwema & Mugerwa AdvocatesFirst Floor Rwenzori CourtPlot 2 & 4ANakasero Kampala, Uganda

A.F. MpangaAdvocates & Solicitors9th Floor Workers House, North Wing1 Pilkington RoadP.O. Box 1520Kampala, Uganda

Lule Godfrey & Lule Company Advocates3rd Floor, Raja ChambersPlot 3 Parliament AvenueP.O. Box 36027Kampala, Uganda

3

On the other hand, Bank of Uganda, following the drop in inflationary rates, relaxed its Central Bank Rates(CBR) in a bid to influence reduction of interest rates in the market. Consequently, both Treasury Bills andBonds rates decreased during the period. The 91-day Treasury Bills rate initially peaked at 23% in January2012, then significantly declined to 9.80% in November 2012. These effects helped to lower the averagelending rates in the industry from 27.0% to an average of 21% towards the end of the year.

CHAIRMAN'S STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2012

TROPICAL BANK LIMITED

During the same period, the Uganda Shilling remained stable against the US Dollar and other internationalcurrencies fluctuating within Ushs 2,414 per US Dollar in January 2012 to Ushs 2,492 as at August 2012, butfaced some pressure during the last quarter of the year, depreciating from Ushs 2,515 per US dollar inSeptember 2012 to Ushs 2,622 per US Dollar towards the end of 2012. This slight depreciation is attributed tothe high demand for the US Dollar, in a bid to re-stock for the end of year season festivities.

Generally, the asset portfolio of the commercial banking sector grew by 19% increasing from Ushs 12.9 trillionto Ushs 15.4 trillion, deposits rose by 17% from Ushs 8.9 trillion to Ushs 10.4 trillion.While loans and advancesgrew by 9% rising from Ushs 6.8 trillion to Ushs 7.4 trillion. During the year 2012, it is worth noting that two newcommercial banks, NC Bank and Bank of India, were granted operating licences, increasing the number ofcommercial banks in Uganda to 25.

On behalf of the Board of Directors of Tropical Bank Limited, I have the pleasure to present the Bank'sfinancial statements for the year 2012, during the 35th Annual General Meeting. The year 2012 witnessed thelifting of UN Sanctions imposed on all Libyan Government assets and entities that subsequently led to the returnof the Libyan seconded staff to the management of the Bank.

Overall, the economy demonstrated significant steps towards recovery, as indicated by the trends in theeconomic parameters throughout the year. Headline inflation drastically declined from 27% in January 2012 to3.9% as at 31 December 2012. Food crop inflation also dropped from 21.4% in February 2012 to 4.4% as atOctober 2012 , then slightly rose to 7.5% towards the end of year, while core inflation continuously declinedthroughout the year, falling from 29.20% in December 2011, to 3.8 % towards the end of December 2012.These improving trends in inflation are attributed to increased supply in food stuffs and the decline ininternational crude oil prices, which eventually allowed Bank of Uganda to re-adjust its monetary policy stanceby reducing the Central Bank Rate (CBR) from 23% in January 2012 to 12% towards the end of 2012.

Perfomance in the financial sector

The financial sector continued to experience liquidity strains that forced many banks into aggressive depositmobilisation campaigns during the last quarter of the year. Similary, under the circumstance , branch and ATMexpansion remained slow and the industry players had to make adjustments in their operations and interestrates in order to adapt to the monetary policy changes that Bank of Uganda had introduced to curb theescalating inflationary rates and the depreciating Uganda Shilling against other international currencies.

4

TROPICAL BANK LIMITEDCHAIRMAN'S STATEMENT (CONTINUED)FOR THE YEAR ENDED 31 DECEMBER 2012

Generally, the Bank remained steady throughout the year 2012, after the return of the Libyan seconded staff to themanagement of the Bank. The strong public relations campaigns during the 2011/2012 coupled with unfreezing ofthe Libyan owned assets restored confidence to the customers and the general public, which led to stability inperfomance of the bank.

Performance of the bank

During the year the Bank made a profit after tax of Ushs 1.652 billion compared to a loss of Ushs 624 million in2011, recording a significant growth partly attributed to the improving economic environment and stability of theBank. Advances grew by 1% from Ushs 104 billion to Ushs 105 billion. On the other hand, overall liabilitiesincreased by 12%, from Ushs 192.2 billion to Ushs 215.3 billion.

Key developments

During the year, the Bank's application for partnership with Agribusiness Initiative Trust(ABI) was approved, tofacilitate a 50% grant contribution to establish a branch in Kaliro Town, for support of the sugar cane out growers inthe region,as well as a restructuring of the Credit Department to include an Agricultural division and the review of allthe Bank's products. The branch is expected to be officially opened by June 2013. Furthermore, in a bid to increaseits delivery channels, the Bank received a no objection from Bank of Uganda to open a branch in Katwe TradingCenter, Kampala to help support the SME outlets in the area.

The Bank was also able to launch two electronic products namely; e-water payments, in partnership with NationalWater and Sewerage Corporation and NSSF e-collections for payments of members contribution to National SocialSecurity Fund. The Visa card project is under finalisation and expected to be launched by April 2013.

Furthermore, in a bid to improve the Bank's visibility and image awareness, the Bank initiated the process ofrebranding its corporate logo from the original two green colors into red, black and green, which is expected to belaunched in April 2013. The new image is a promise to our customers and the general public off our commitment toserve our customers better.

5

TROPICAL BANK LIMITED

ACTIVITIES

RESULTS2012 2011

Ushs '000 Ushs '000Profit before tax 1,345,377 201,479 Income tax credit/ (charge) 306,294 (825,630)

Profit / (loss) for the year 1,651,672 (624,151)

CAPITAL ADEQUACY

Capital Tier 1 2012 2011Ushs '000 Ushs '000

Share capital fully paid up 30,000,000 30,000,000Retained earnings 6,401,695 8,284,216Capital reserve 5,017,372 4,604,454General reserve 4,250,081 4,250,081Less: Unrealised foreign exchange gains (208,884) (160,368) Prohibited loans - (21,844,844) Deferred income tax credit (1,084,507) (778,213) Intangible assets (509,582) (114,970)

Total Tier 1-Core capital 43,866,174 24,240,356

Supplementary Capital Tier 2Revaluation reserve 2,286,672 2,303,750Regulatory reserve 3,307,872 1,528,219Surbodinated debt 21,933,087 12,120,178

Total Tier 2-Supplementary capital 27,527,631 15,952,147

Total Capital: Tier 1 +Tier 2 71,393,806 40,192,504

REPORT OF THE DIRECTORS

The market risk approach covers the general market risk and the risk of open positions in currencies, debt andequity securities. Assets are weighted according to broad categories of notional credit risk being assigned a riskweighting according to the amount of capital deemed to be necessary to support them. Four categories of riskweights (0%, 20%, 50% and 100%) are applied. Cash and money market instruments have a zero risk weightingwhich means that no capital is required to support the holding of these assets. A placement with a parent orrelated group bank or main correspondent bank which has a minimum long term rating by internationallyrecognized agencies of AAA to AA- will be subject to risk weight of 20%. A rating of A+ to A-, will attract a riskweight of 50%. Property and equipment carry 100% risk weighting meaning that these assets must be supportedby capital equal to 8% of the carrying amount. Other asset categories have intermediate weightings.

Off-statement of financial position related commitments are taken into account by applying different categoriesof credit conversion factors, designed to convert these items into statement of financial position equivalents. Theresulting credit equivalent amounts are weighted for credit risk using the same percentages as for the statementof financial position assets.

Tier 1 Capital consists of shareholders’ equity and tier 2 Capital includes the Bank’s supplementary capital whichshould not exceed 100% of tier 1. Subordinated term debt should not exceed 50% of tier 1. Tier 1 and tier 2used in computation of capital adequacy ratios on page 8 is indicated below:-

FOR THE YEAR ENDED 31 DECEMBER 2012

The directors present their report together with the audited financial statements of Tropical Bank Limited ('theBank') for the year ended 31 December 2012 which disclose the state of affairs of the Bank.

The principal business activities involve banking and provision of related services. The Bank is licensed under the Financial Institutions Act, 2004.

The Bank monitors the adequacy of its capital using ratios established by the Bank for International Settlements(BIS) and the Bank of Uganda. These ratios measure capital adequacy by comparing the Bank’s eligible capitalwith its statement of financial position assets, off-statement of financial position commitments, market and otherrisk positions at a weighted amount to reflect their relative risk.

7

2012 2011 2012 2011Ushs '000 Ushs '000 Ushs '000 Ushs '000

Balances with Bank of Uganda 12,602,362 5,400,301 - - Cash at hand 6,973,698 6,099,617 - -

53,890,840 36,557,576 40,242,676 16,578,135 Current income tax recoverable 779,597 779,597 779,597 779,597 Government securities 23,913,530 26,791,474 - - Net advances to customers 105,461,246 104,827,223 105,461,246 104,827,223Property and equipment 6,617,949 7,910,917 6,617,949 7,910,917Operating lease prepayments 280,600 284,781 280,600 284,781Intangible assets 509,582 114,970 - - Other assets 3,186,111 2,709,703 3,186,111 2,709,703

214,215,515 191,476,159 156,568,179 133,090,356

Off-statement of financial positions

Commitment on loans 4,050,665 12,029,959 2,025,333 6,014,980 Letters of Guarantee 1,532,876 7,319,801 1,532,876 7,319,801 Letters of Credit 7,559,264 8,854,919 1,511,853 1,770,984 Performance Bonds 260,491 267,211 130,246 133,606

Credit related commitments 13,403,296 28,471,890 5,200,307 15,239,370

Total risk-weighted assets 227,618,811 219,948,049 161,768,486 148,329,726

BIS capital ratios2012 2011

% %

Tier 1 capital 43,866,174 24,240,356 27.12% 16.34%

Tier 1 + Tier 2 capital 71,393,806 40,192,504 44.13% 27.10%

TROPICAL BANK LIMITED

The FIA 2004 capital adequacy percentanges shows the ratio of the capital in relation to total risk weighted assets.Minimum for tier 1 is 8%, while mimimum for tier 2 is 12%. The above computations indicate ratios above 12% for both core and total capital. The Bank therefore complies with the capital adequacy requirements under Section 27 of theFinancial Institutions Act, 2004.

Deposits and balances due from banking institutions

FOR THE YEAR ENDED 31 DECEMBER 2012REPORT OF THE DIRECTORS (CONTINUED)

Statement of financial position assets (net of provisions)

Statement of financial position amountsNominal

amountsRisk weighted

FIA Capital Adequacy Ratios

8

CORPORATE GOVERNANCE

Philosophy of corporate governance

Board of Directors

Board Committees

a) Non Executive Director Chairman Non Executive Director MemberManaging Director MemberExecutive Director MemberDeputy General Manager In AttendanceSenior Manager Risk & Compliance In AttendanceSenior Manager Credit In AttendanceSenior Manager Operations In AttendanceSenior Manager Credit Control In AttendanceAg. Manager Legal In AttendanceBoard Secretary Secretary

Risk/Compliance committee

The Board works through sub committees to develop and implement Bank policies and coordinate activities in the Bank. These included the Risk/Compliance, Assets and Liability (ALCO), Human Resource and Compensation, and Audit Committees.

During the financial year and up to the date of this report, other than disclosed in note 27 to the financial statements, no director has received or become entitled to receive any benefit other than directors' fees, and amounts receivable by the executive directors under employment contracts and the expatriate staff remuneration scheme. The aggregate amount of emoluments for directors' services rendered in the financial year is disclosed in Note 27 to the financial statements.

Neither at the end of the financial year nor at any time during the year did there exist any arrangement to which the Bank is a party whereby directors might acquire benefits by means of the acquisition of shares in or debentures of the Bank or any other body corporate.

The Board is responsible for good corporate governance and business performance of the Bank ensuring thatthe business of the Bank is carried out in compliance with all applicable laws and regulations and is conduciveto safe and sound banking practices among other responsibilities.

REPORT OF THE DIRECTORS (Continued)FOR THE YEAR ENDED 31 DECEMBER 2012

TROPICAL BANK LIMITED

Tropical Bank Limited has established a tradition of best practice in corporate governance. The corporate governance framework in the Bank is based on an effective independent board, the separation of the board’s supervisory role from the executive management and the constitution of board committees generally comprising a majority of non-executive directors. Since May 2009, the committees are chaired by non-executive directors to oversee critical areas.

The Bank’s corporate governance philosophy encompasses not only regulatory and legal requirements, but also several voluntary practices aimed at a high level of business ethics, effective supervision and enhancement of value for all stakeholders.

9

CORPORATE GOVERNANCE (continued)

b) Asset and Liability Committee

Non Executive Director Chairman Non Executive Director MemberManaging Director MemberExecutive Director MemberDeputy General Manager In AttendanceSenior Manager Treasury In AttendanceSenior Manager Finance & Accounts In AttendanceSenior Manager Risk & Compliance In AttendanceSenior Manager Business Development In AttendanceSenior Manager Credit In AttendanceSenior Manager Credit Control In AttendanceSenior Manager ICT In AttendanceBoard Secretary Secretary

c) Human Resource & Compensation Committee

Non Executive Director Chairman Non Executive Director Deputy ChairmanManaging Director MemberExecutive Director MemberDeputy General Manager In AttendanceSenior Manager Human Resource In AttendanceSenior Manager ICT In AttendanceSenior Manager Risk & Compliance In AttendanceSenior Manager Business Development In AttendanceSenior Manager Legal Services In AttendanceBoard Secretary Secretary

d) Audit Committee

Non Executive Director ChairmanNon Executive Director MemberManager Internal Auditor In AttendanceSenior Manager Treasury In AttendanceSenior Manager Finance & Accounts In AttendanceExternal Auditors In AttendanceBoard Secretary Secretary

The Board Risk Management Committee is responsible for the assessment, management and mitigation ofrisk in the Bank and is accountable to the Board of Directors.

TROPICAL BANK LIMITEDREPORT OF THE DIRECTORS (Continued)FOR THE YEAR ENDED 31 DECEMBER 2012

RISK MANAGEMENT

Risk is an integral part of the banking business and the Bank aims at the delivery of superior shareholder value by achieving an appropriate trade-off between risk and returns. The Bank is exposed to various risks, including credit risk, market risk and operational risk. The Bank's risk management strategy is based on a clear understanding of the various risks, disciplined risk assessment and measurement procedures and continuous monitoring. The policies and procedures established for this purpose are continuously benchmarked with the industry best practices. The risk management function is supported by a Board Risk Management Committee using a comprehensive range of quantitative tools.

10

TROPICAL BANK LIMITEDREPORT OF THE DIRECTORS (Continued)FOR THE YEAR ENDED 31 DECEMBER 2012

Credit Risk

Market Risk

DIVIDEND

The directors do not recommend a dividend. In accordance with the standing resolution of the previous AnnualGeneral Meeting, 25% of net profit after tax is transferred to the Capital Reserve and 25% of the net profit aftertax after covering any cumulative losses from previous periods, and any Bank of Uganda regulatory reserve tothe General Reserve.

RISK MANAGEMENT (continued)

Credit risk is the risk that a borrower is unable to meet its financial obligations to the lender. The Bankmeasures, monitors and manages credit risk for each borrower and also at the portfolio level. The Bank has astandardised credit approval process, which includes a well established procedure of comprehensive creditappraisal and rating. Internal credit rating methodologies for rating obligors as well as for products and facilitieshave been developed. The credit risk attached to every borrower is reviewed at least annually and for higherrisk credits and large exposures at shorter intervals.

Sector knowledge has been institutionalised across the Bank through the availability of sector-specificinformation from the various publications of Bank of Uganda and Ministry of Finance and is included in theCredit Risk Policy. Industry knowledge is constantly updated through field visits, interactions with clients,regulatory bodies and industry experts. In respect of the retail credit business, the Bank has a system ofcentralised approval of all products and policies and monitoring of the retail portfolio.

Market risk is the risk of loss resulting from changes in interest rates, foreign currency exchange rates andcommodity prices. The Bank’s exposure to market risk is a function of its asset and liability managementactivities and its role as a financial intermediary in customer related transactions. The objective of market riskmanagement is to minimise the impact of losses due to market risks on earnings and equity capital. Market riskpolicies include Asset-Liability Management (ALM) policies approved by the Board of Directors. The role of theBoard Asset and Liability Committee encompasses stipulating liquidity and interest rate risk limits, monitoringrisk levels by ensuring adherence to set limits, articulating the Bank's interest rate view and determiningbusiness strategy in the light of the current and expected business environment. These sets of policies andprocesses are articulated in the ALM policy.

Operational Risk

Operational risk can result from a variety of factors, including failure to obtain proper internal authorisations,improperly documented transactions, failure of operational and information security procedures, computersystems and software or equipment, fraud, inadequate training and employee errors. The bank mitigatesoperational risk by maintaining a comprehensive system of internal controls, establishing systems andprocedures to monitor transactions, maintaining key back-up procedures and undertaking regular contingencyplanning. The Internal Audit Department undertakes a comprehensive audit of all business functions, inaccordance with a risk-based audit plan. This plan allocates audit resources based on an assessment of theoperational risks in the various businesses. The Internal Audit Department conceptualises and recommendsimproved systems of internal controls to minimise operational risk.

11

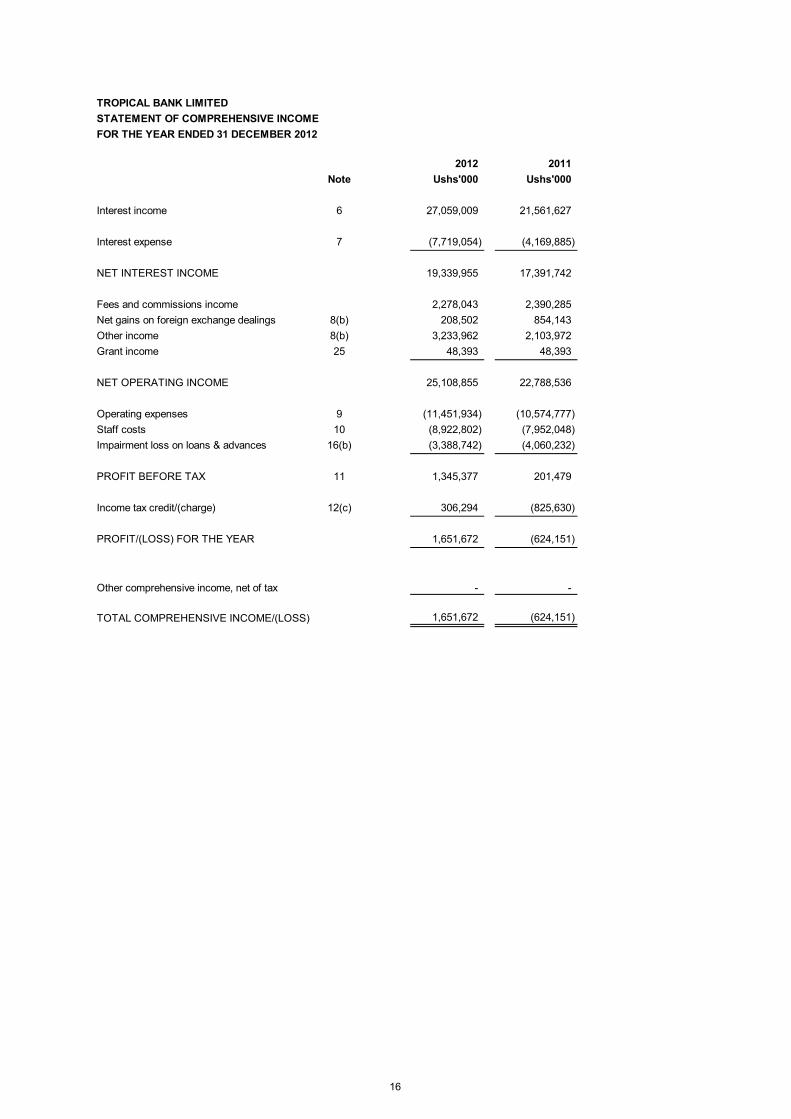

STATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2012

2012 2011Note Ushs'000 Ushs'000

Interest income 6 27,059,009 21,561,627

Interest expense 7 (7,719,054) (4,169,885)

NET INTEREST INCOME 19,339,955 17,391,742

Fees and commissions income 2,278,043 2,390,285 Net gains on foreign exchange dealings 8(b) 208,502 854,143 Other income 8(b) 3,233,962 2,103,972 Grant income 25 48,393 48,393

NET OPERATING INCOME 25,108,855 22,788,536

Operating expenses 9 (11,451,934) (10,574,777) Staff costs 10 (8,922,802) (7,952,048) Impairment loss on loans & advances 16(b) (3,388,742) (4,060,232)

PROFIT BEFORE TAX 11 1,345,377 201,479

Income tax credit/(charge) 12(c) 306,294 (825,630)

PROFIT/(LOSS) FOR THE YEAR 1,651,672 (624,151)

Other comprehensive income, net of tax - -

TOTAL COMPREHENSIVE INCOME/(LOSS) 1,651,672 (624,151)

TROPICAL BANK LIMITED

16

TROPICAL BANK LIMITEDSTATEMENT OF CHANGES IN EQUITY

Issued Retained Capital General Revaluation Regulatorycapital earnings reserve reserve reserve credit reserve Total

Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000(Note 26) (Note 28) (Note 28) (Note 29) (Note 30)

At 1 January 2011 30,000,000 7,560,258 4,604,454 4,250,081 2,320,828 2,859,250 51,594,871

Loss for the year - (624,151) - - - - (624,151) Other comprehensive income, net of tax - - - - - - - Total comprehensive income - (624,151) - - - - (624,151)

Transfer of excess depreciation - 24,397 - - (24,397) - - Defered tax on excess depreciation - (7,319) - - 7,319 - - Transfer from regulatory reserve (Note 16 (c)) - 1,331,031 - - - (1,331,031) -

At 31 December 2011 30,000,000 8,284,216 4,604,454 4,250,081 2,303,750 1,528,219 50,970,720

At 1 January 2012 30,000,000 8,284,216 4,604,454 4,250,081 2,303,750 1,528,219 50,970,720

Profit for the year - 1,651,672 - - - - 1,651,672 Other comprehensive income, net of tax - - - - - - - Total comprehensive income - 1,651,672 - - - - 1,651,672

Transfer to general and capital reserves - (412,918) 412,918 - - - Transfer of excess depreciation - 24,397 - - (24,397) - - Defered tax on excess depreciation - (7,319) - 7,319 Transfer from/to Regulatory reserve (1,779,653) 1,779,653 Payment of dividends (1,358,700) (1,358,700)

At 31 December 2012 30,000,000 6,401,695 5,017,372 4,250,081 2,286,672 3,307,872 51,263,692

The revaluation and the regulatory credit reserve are not distributable as dividends to members.

FOR THE YEAR ENDED 31 DECEMBER 2012

18

TROPICAL BANK LIMITEDSTATEMENT OF CASH FLOWSFOR THE YEAR ENDED 31 DECEMBER 2012

2012 2011Note Ushs'000 Ushs'000

OPERATING ACTIVITIESProfit before tax 1,345,377 201,479 Adjustment for:Profit on disposal of property and equipment - (13,455)Write off of equipment 46,517 479 Amortisation 104,762 107,040 Depreciation 20 1,443,892 1,490,983 Unrealised foreign exchange losses 2,482,820 1,870,000 Grant income 25 (48,393) (48,393)

Profit before working capital changes 5,374,975 3,608,133

(Increase) / decrease in balances with Bank of Uganda (7,202,061) 18,666,761 Increase in loans and advances to customers (634,023) (20,457,305) Increase in other assets (476,407) (18,198) Increase in customer deposits 26,945,552 (40,334,589) Increase / (decrease) in administered funds 75,000 (25,654,202) Decrease in Government securities (maturing after 90 days) 5,749,444 22,091,998 (Decrease) / increase in other liabilities (6,732,694) 7,723,267

Net cash flows from / (used in) operating activities 23,099,786 (34,374,135)

INVESTING ACTIVITIESPurchase of property and equipment 20 (167,048) (1,695,308) Purchase of intangible assets 18 (495,193) (91,147) Proceeds from disposal of property and equipment - 13,456

Net cash flows used in investing activities (662,241) (1,772,999)

FINANCING ACTIVITIESPayment of dividends (1,358,700) -

Net increase / (decrease) in cash and cash equivalents 21,078,845 (36,147,134)

Cash and cash equivalents at 1 January 43,427,205 79,574,339

Cash and cash equivalents at 31 December 64,506,050 43,427,205

Represented by:

Cash in hand 13 6,973,698 6,099,617 Deposits and balances due from banking institutions 14 53,890,840 36,557,576 Government securities maturing within 90 days 3,641,512 770,012

64,506,050 43,427,205

19

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS

1 REPORTING ENTITY

2 NEW AND REVISED STANDARDS

IAS 1 Financial statement presentation (Amendment)The amendment is effective for annual periods beginning on or after 1 July 2012 and requires that items of other comprehensive income be grouped in Items that would be reclassified to profit or loss at a future point (for example, upon derecognition or settlement) and items that will never be reclassified. This amendment only effects the presentation in the financial statements and will have no impact on the Bank’s financial position or performance.

IAS 12 Income taxes (Amendment)The amendment is effective for annual periods beginning on or after 1 January 2012 and introduces a rebuttable presumption that deferred tax on investment properties measured at fair value will be recognised on a sale basis, unless an entity has a business model that would indicate the investment property will be consumed in the business. If consumed a use basis should be adopted. Furthermore, it introduces the requirement that deferred tax on non-depreciable assets that are measured using the revaluation model in IAS 16 always be measured on a sale basis of the asset. This amendment will have no impact on the Bank’s financial statements.

IFRS 1 First-time Adoption of international Financial Reporting Standards (Amendment) - Severe Hyperinflation and Removal of Fixed Dates for First-time Adopters (Amendment)The amendment is effective for annual periods beginning on or after 1 July 2011. The IASB has provided guidance on how an entity should resume presenting IFRS financial statements when its functional currency ceases to be subject to severe hyperinflation. A further amendment to the standard is the removal of the legacy fixed dates in IFRS 1 relating to derecognition and day one gain or loss transactions have also been removed. The standard now has these dates coinciding with the date of transition to IFRS. The amendment had no impact on the Bank’s financial statements.

IFRS 7 Financial Instruments: Disclosures - Transfer of financial assets (Amendment)The amendment is effective for annual periods beginning on or after 1 July 2011. The amendment requires additional quantitative and qualitative disclosures relating to transfers of financial assets, where:• Financial assets are derecognised in their entirety, but where the entity has a continuing involvement in them (e.g., options or guarantees on the transferred assets) - to enable the user to evaluate the nature of, and risks associated with, the entity’s continuing involvement in those derecognised assets• Financial assets are not derecognised in their entirety – to enable the user of the Bank’s financial statements to understand the relationship with those assets that have not been derecognised and their associated liabilities.

The amendments may be applied earlier than the effective date and this fact must be disclosed. Comparative disclosures are not required for any period beginning before the effective date. The amendment had no impact on the Bank’s financial statements.

Standards issued but not yet effective

Standards issued but not yet effective up to the date of issuance of the Bank’s financial statements are listed below. The Bank intends to adopt the standards applicable to its financial statements when they become effective. The Bank expects that adoption of these standards, amendments and interpretations in most cases not to have any significant impact on the Bank's financial position or performance in the period of initial application but additional disclosures will be required. In cases where it will have an impact the Bank is still assessing the possible impact.

Tropical Bank Limited (the Bank) is a limited liability company incorporated in Uganda and carries out its banking operations within Uganda. The Bank is a subsidiary of the Libyan Foreign Bank, which is the majority shareholder. The Libyan Foreign Bank is domiciled in Libya. Tropical Bank Limited is partially owned by the Government of Uganda, which is the minority shareholder.

The accounting policies adopted are consistent with those of the previous financial year.Amendments resulting from Improvements to IFRSs to the following standards did not have any impact on the accounting policies, financial position or performance of the Bank:

• IAS 1 Financial statement presentation (Amendment) – 1 July 2012• IAS 12 Income taxes (Amendment) – 1 January 2012• IFRS 1 First-time Adoption of international Financial Reporting Standards (Amendment) – 1 July 2011• IFRS 7 Financial Instruments: Disclosures (Amendment) – 1 July 2011

The adoption of the standards or interpretations is described below:

20

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

2 NEW AND REVISED STANDARDS (Continued)

Standards issued but not yet effective (continued)

IAS 19 Post employee benefits (Amendment)The amendments are effective for annual periods beginning on or after 1 January 2013. There are changes to post employee benefits in that pension surpluses and deficits are to be recognised in full (no more deferral mechanisms) and all actuarial gains and losses recognised in other comprehensive income as they occur with no recycling to profit or loss. The concept of expected returns on plan assets is also simplified and certain re-wording is made. Past service costs as a result of plan amendments are to be recognized immediately. Short and long-term benefits will now be distinguished based on the expected timing of settlement, rather than employee entitlement. The amendments are not expected to have an impact on the Bank’s financial statements.

IFRS 1 time Adoption of international Financial Reporting Standards (Amendment) - Government LoansThe amendment is effective for annual periods beginning on or after 1 January 2013. The IASB has added an exception to the retrospective application of IFRS 9 Financial Instruments (or IAS 39 Financial Instruments: Recognition and Measurement, as applicable) and IAS 20 Accounting for Government Grants and Disclosure of Government Assistance. These amendments require first-time adopters to apply the requirements of IAS 20 prospectively to government loans existing at the date of transition to IFRS. However, entities may choose to apply the requirements of IFRS 9 (or IAS 39, as applicable) and IAS 20 to government loans retrospectively if the information needed to do so had been obtained at the time of initially accounting for that loan. The exception would give first-time adopters relief from retrospective measurement of government loans with a below market rate of interest. As a result of not applying IFRS 9 (or IAS 39, as applicable) and IAS 20 retrospectively, first-time adopters would not have to recognise the corresponding benefit of a below-market rate government loan as a government grant. The amendments will not have an impact on the Bank’s financial statements.

IFRS 1 Government Loans — Amendments to IFRS 1The amendment is effective for annual periods beginning on or after 1 January 2013. The IASB has added an exception to the retrospective application of IFRS 9 Financial Instruments (or IAS 39 Financial Instruments: Recognition and Measurement, as applicable) and IAS 20 Accounting for Government Grants and Disclosure of Government Assistance. These amendments require first-time adopters to apply the requirements of IAS 20 prospectively to government loans existing at the date of transition to IFRS. However, entities may choose to apply the requirements of IFRS 9 (or IAS 39, as applicable) and IAS 20 to government loans retrospectively if the information needed to do so had been obtained at the time of initially accounting for those loans. The exception will give first-time adopters relief from retrospective measurement of government loans with a belowmarket rate of interest. As a result of not applying IFRS 9 (or IAS 39, as applicable) and IAS 20 retrospectively, first-time adopters will not have to recognise the corresponding benefit of a below-market rate government loan as a government grant. The amendments are not expected to have an impact on the bank’s financial statements.

IAS 27 Separate Financial Statements (as revised in 2011)As a consequence of the new IFRS 10 and IFRS 12, what remains of IAS 27 is limited to accounting for subsidiaries, jointly controlled entities, and associates in separate financial statements. The amendment becomes effective for annual periods beginning on or after 1 January 2013. The Bank does not present separate financial statements and therefore the amendment is not expected to have an impact on its financial statements.

IAS 28 Investments in Associates and Joint Ventures (as revised in 2011)As a consequence of the new IFRS 11 and IFRS 12. IAS 28 has been renamed IAS 28 Investments in Associates and Joint Ventures, and describes the application of the equity method to investments in joint ventures in addition to associates. The amendment becomes effective for annual periods beginning on or after 1 January 2013 and is not expected to have an impact on the Bank’s financial statements.

IAS 32 Financial Instruments: Presentation - Offsetting Financial Assets and Financial LiabilitiesThe amendments clarify the meaning of ‘currently has a legally enforceable right of set-off’; and that some gross settlement systems may be considered equivalent to net settlement. The amendments are effective for annual periods beginning on or after 1 January 2014 and are required to be applied retrospectively. The Bank is still assessing the impact of the amendments on its financial statements.

21

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

2 NEW AND REVISED STANDARDS (Continued)

Standards issued but not yet effective (continued)

IFRS 7 Disclosures — Offsetting Financial Assets and Financial Liabilities — Amendments to IFRS 7The amendment is effective for annual periods beginning on or after 1 January 2013. These amendments require an entity to disclose information about rights of set-off and related arrangements (e.g., collateral agreements). The disclosures would provide users with information that is useful in evaluating the effect of netting arrangements on an entity’s financial position. The new disclosures are required for all recognised financial instruments that are set off in accordance with IAS 32 Financial Instruments: Presentation. The disclosures also apply to recognised financial instruments that are subject to an enforceable master netting arrangement or ‘similar agreement’, irrespective of whether they are set off in accordance with IAS 32. The Bank is still assessing the impact the amendments would have on the financial statements.

IFRS 9 Financial Instruments: Classification and MeasurementIFRS 9 as issued reflects the first phase of the IASBs work on the replacement of IAS 39 and applies to classification and measurement of financial assets and liabilities as defined in IAS 39. IFRS 9 initially required the adoption of the standard for annual periods on or after 1 January 2013. Amendments to IFRS 9 Mandatory Effective Date of IFRS 9 and Transition Disclosures, issued in December 2011, moved the mandatory effective date of both the 2009 and 2010 versions of IFRS 9 from 1 January 2013 to 1 January 2015. In subsequent phases, the Board will address impairment and hedge accounting. The completion of this project is expected during 2013. The adoption of the first phase of IFRS 9 will primarily have an effect on the classification and measurement of the Bank’s financial assets but will potentially have no impact on classification and measurements of financial liabilities. The Bank is currently assessing the impact of adopting IFRS 9, however, the impact of adoption depends on the assets held by the Bank at the date of adoption, it is not practical to quantify the effect.

IFRS 10 Consolidated Financial Statements; IFRS 11 Joint Arrangements; IFRS 12 Disclosure of Interest in Other EntitiesIFRS 10 replaces the portion of IAS 27 Consolidated and Separate Financial Statements that addresses the accounting for consolidated financial statements. It also includes the issues raised in SIC 12 Consolidation – Special Purpose Entities. IFRS 10 establishes a single control model with a new definition of control that applies to all entities. The changes are not expected to have an impact on the Bank’s financial statements.

IFRS 11 Joint ArrangementsIFRS 11 replaces IAS 31 Interest in Joint Ventures and SIC 13 Jointly Controlled Entities – Non-monetary Contributions by Ventures. IFRS 11 uses some of the terms that were used in IAS 31 but with different meanings which may create some confusion as to whether there are significant changes. IFRS 11 focuses on the nature of the rights and obligations arising from the arrangement compared to the legal form in IAS 31. IFRS 11 uses the principle of control in IFRS 10 to determine joint control which may change whether joint control exists. IFRS 11 addresses only two forms of joint arrangements; joint operations where the entity recognises its assets, liabilities, revenues and expenses and/or its relative share of those items and joint ventures which is accounted for on the equity method (no more proportional consolidation). These changes are not expected to have an impact on the Bank’s financial statements.

IFRS 12 Disclosure of Involvement with Other EntitiesIFRS 12 includes all the disclosures that were previously required relating to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities as well as a number of new disclosures. An entity is now required to disclose the judgements made to determine whether it controls another entity. The standard is not expected to have an impact on the Bank’s financial statements.

IFRS 10 Consolidated Financial Statements – Investment entities (Amendment)The amendment is effective for annual periods beginning on or after 1 January 2014 and provides an exception to the consolidation requirement for entities that meet the definition of an investment entity. The exception to consolidation requires investment entities to account for subsidiaries at fair value through profit or loss in accordance with IFRS 9 Financial Instruments. The amendment is not expected to have an impact on the Bank’s financial statements.

IFRS 13 Fair Value MeasurementIFRS 13 establishes a single framework for all fair value measurement (financial and non-financial assets and liabilities) when fair value is required or permitted by IFRS. IFRS 13 does not change when an entity is required to use fair value but rather describes how to measure fair value under IFRS when it is permitted or required by IFRS. There are also consequential amendments to other standards to delete specific requirements for determining fair value. The Group will need to consider the new requirements to determine fair values going forward. IFRS 13 will be effective for the Bank from 1 July 2013.

22

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

2 NEW AND REVISED STANDARDS (Continued)

Standards issued but not yet effective (continued)

IFRIC 20, Stripping Costs in the Production Phase of a Surface MineThis new interpretation provides guidance on how to account for stripping costs in the development phase of a surface mine and requires such costs to be capitalised as part of an asset (the ‘stripping activity asset’) if certain criteria are met. The stripping activity asset is to be depreciated on a unit of production basis unless another method is more appropriate. This interpretation is effective 1 January 2013 and is not expected to have an impact on the Bank’s financial statements.

Improvements to IFRSs – 2009 – 2011 Cycle (issued in 2012 effective for annual periods beginning on or after 1 January 2013)• IFRS 1 First-time Adoption of International Financial Reporting Standards (Amendments):o Repeated application of IFRS 1 - clarifies that an entity that has stopped applying IFRS may choose to either:(i) Re-apply IFRS 1, even if the entity applied IFRS 1 in a previous reporting period; or(ii) Apply IFRS retrospectively in accordance with IAS 8 (i.e., as if it had never stoppedapplying IFRS) in order to resume reporting under IFRS. If the entity re-applies IFRS 1 or applies IAS 8, it must disclose the reasons why it previously stopped applying IFRS and subsequently resumed reporting in accordance with IFRS. This

• IAS 1 Presentation of Financial Statements (Amendments)The amendment clarifies the difference between voluntary additional comparative information and the minimum required comparative information. Generally, the minimum required comparative period is the previous period. The improvement will not have an impact on the Bank’s financial statements.

• IAS 32 Financial Instruments: PresentationThe amendment removes existing income tax requirements from IAS 32 and requires entities to apply the requirements in IAS 12 to any income tax arising from distributions to equity holders. The amendment is not expected to have an impact on the Bank’s financial statements.

o Borrowing costs - clarifies that, upon adoption of IFRS, an entity that capitalised borrowing costs in accordance with its previous GAAP, may carry forward, without adjustment, the amount previously capitalised in its opening statement of financial position at the date of transition. Once an entity adopts IFRS, borrowing costs are recognised in accordance with IAS 23, including those incurred on qualifying assets under construction. The improvement is not applicable to the Bank’s financial statements.

• IAS 16 Property, Plant and Equipment (Amendment)The amendment clarifies that major spare parts and servicing equipment that meet the definition of property, plant and equipment are not inventory. The amendment is not expected to have an impact on the Bank’s financial statements.

• IAS 34 Interim Financial Reporting The amendment clarifies the requirements in IAS 34 relating to segment information for total assets and liabilities for each reportable segment to enhance consistency with the requirements in IFRS 8 Operating Segments. Total assets and liabilities for a particular reportable segment need to be disclosed only when the amounts are regularly provided to the chief operating decision maker and there has been a material change in the total amount disclosed in the entity’s previous annual financial statements for that reportable segment. The amendment is not expected to have an impact on the Bank’s financial

23

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation and statement of compliance

Functional and presentation currency

Use of estimates and judgements

INTEREST INCOME AND EXPENSE

FEES AND COMMISSIONS

In the normal course of business, the Bank earns fees and commission income from a diverse range of services to its customers. Fees and commission income and expenses that are integral to the effective interest rate on a financial asset or liability are included in the measurement of the effective interest rate.

The financial statements have been prepared on the historical cost basis of accounting as modified by the revaluation of property and certain financial instruments which are accounted for at fair value. The financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) and the requirements of the Ugandan Companies Act (Cap 110) and Financial Institutions Act, 2004.

The financial statements are presented in Uganda Shillings (Ushs), which is also the Bank's functional currency. Except as indicated, financial information presented in Uganda Shillings has been rounded to the nearest thousand.

The preparation of financial statements requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reported period. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised and in any future periods affected.

During the period, the areas involving a higher degree of judgement or complexity or where assumptions and estimates are significant to the financial statements are disclosed in note 5 .

The principal accounting policies adopted in the preparation of these financial statements are set out below. These policies have been applied consistently throughout the year.

Interest income and expense for all interest bearing financial instruments are recognised within profit or loss on accrual basis using the effective interest method. The effective interest rate is the rate that exactly discounts the estimated future cash payments and receipts through the expected life of the financial instruments (or, where appropriate, a shorter period) to the carrying amount of the financial instruments. The effective interest rate is established on initial recognition of the financial asset and liability and is not revised subsequently.

The calculation of the effective interest rate includes all fees and points paid or received transaction costs, and discounts or premiums that are an integral part of the effective interest rate. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or liability.

24

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

FEES AND COMMISSIONS (Commissions)

FOREIGN CURRENCIES

FINANCIAL INSTRUMENTS

Financial assets at fair value through profit or loss

Loans, advances and receivables

Held to maturity

Available-for-sale financial assets

Other fees and commission income, including account servicing fees, investment management fees, placement fees and syndication fees, are recognised as the related services are performed. When a loan commitment is not expected to result in the draw-down of a loan, loan commitment fees are recognised on a straight-line basis over the commitment period.

A financial asset or liability is recognised when the Bank becomes party to the contractual provisions of the instrument.

The Bank classifies its financial assets into the following categories: Financial assets at fair value through profit or loss; loans, advances and receivables; held- to- maturity investments; and available-for-sale assets. Management determines the appropriate classification of its investments at initial recognition.

This category has two sub-categories: Financial assets held for trading and those designated at fair value through profit or loss at inception. A financial asset is classified in this category if acquired principally for the purpose of selling in the short term or if so designated by management. Derivatives are also categorised as held for trading.

Loans, advances and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise when the Bank provides money, goods or services directly to a customer with no intention of trading the receivable.

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that management has the positive intention and ability to hold to maturity. Where a sale occurs other than an insignificant amount of held-to-maturity assets, the entire category would be tainted and classified as available-for-sale.

These are financial assets that are not (a) financial assets at fair value through profit or loss, (b) loans, advances and receivables, or (c) financial assets held-to-maturity.

Other fees and commission expenses relate mainly to transaction and service fees, which are expensed as the services are rendered.

Transactions in foreign currencies are translated to the functional and reporting currency of the Bank at exchange rates ruling at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated to the functional currency at the exchange rate at that date. The resultant foreign currency gain or loss is recognised in profit or loss. Non–monetary items that are measured in terms of historical cost in a foreign currency are translated using thespot exchange rates as at the date of recognition. Non–monetary items measured at fair value in a foreigncurrency are translated using the spot exchange rates at the date when the fair value was determined.

25

NOTES TO THE FINANCIAL STATEMENTS (Continued)

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

FINANCIAL INSTRUMENTS (Continued)

Measurement

Impairment and uncollectability of financial assets

Borrowings and other financial liabilities

Objective evidence that financial assets are impaired can include default or delinquency by a borrower, restructuring of a loan or advance by the Bank on terms that the Bank would not otherwise consider, indications that a borrower or issuer will enter bankruptcy, the disappearance of an active market for a security, or other observable data relating to a group of assets such as adverse changes in the payment status of borrowers or issuers in the bank, or economic conditions that correlate with defaults in the Bank.

Loan impairments are recognised promptly when there is objective evidence that impairment has occurred.

Borrowings and other financial liabilities are recognised initially at fair value, being issue proceeds (fair value of consideration received) net of transaction costs incurred. Borrowings are subsequently stated at amortised cost; any difference between proceeds net of transaction costs and the redemption value is recognised in profit or loss over the period of the borrowings using the effective interest method.

TROPICAL BANK LIMITED

Available-for-sale financial assets and financial assets at fair value through profit or loss are subsequently carried at fair value. Loans, advances and receivables and held-to-maturity investments are carried at amortised cost using the effective interest method. Gains and losses arising from changes in the fair value of “financial assets at fair value through profit or loss” are included in profit or loss in the period in which they arise. Gains and losses arising from changes in fair value of available-for-sale are recognised in other comprehensive income and accumulated in the investments revaluation reserve with the exception of impairment losses, interest calculated using the effective interest method, and foreign exchange gains and losses on monetary assets, which are recognised in profit or loss. Where available-for-sale investments is disposed of or is determined to be impaired, the cumulative gain or loss previously accumulated in the investments revaluation reserve is reclassified to profit or loss. Dividends on available-for-sale instruments are recognised in profit or loss when the Bank’s right to receive payment is established.

Fair values of quoted investments in active markets are based on quoted bid prices.

At each reporting date, the Bank assesses whether there is objective evidence that financial assets not carried at fair value through profit or loss are impaired. Financial assets are impaired when objective evidence demonstrates that a loss event has occurred after the initial recognition of the asset, and that the loss event has an impact on the future cash flows on the asset that can be established reliably.

Financial assets are initially recognised at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets are derecognised when the rights to receive cash flows from the financial assets have expired or where the Bank has transferred substantially all risks and rewards of ownership.

26

NOTES TO THE FINANCIAL STATEMENTS (Continued)

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

FINANCIAL INSTRUMENTS (Continued)

Origination of loans and provision for loan impairments

PROPERTY AND EQUIPMENT

Motor vehicles 25%Machinery and equipment - Computers, ATM hardware, software 33.3%Machinery and equipment 14.3%Furniture 12.5%Buildings 4.0%Fixtures and fittings 33.3%

LEASEHOLD LAND

INTANGIBLE ASSETS

Acquired computer software licenses are capitalised on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortised on the basis of the expected useful lives.

TROPICAL BANK LIMITED

Loans and advances are recognised when cash is advanced to borrowers. They are categorised as originated loans and carried at amortised cost.

Provisions for loan impairment are established if there is objective evidence that the Bank will not be able to collect all amounts due according to the original contractual terms of loans. The amount of the provision is the difference between the carrying amount and the recoverable amount, being the present value of expected cash flows, including amounts recoverable from guarantees and collateral, discounted at the original effective interest rate of loans.

Specific provisions are recognised for loans and advances that are individually significant. General provision is measured and recognised on a portfolio basis where there is objective evidence that probable losses are present in components of the loan portfolio at the reporting date. This is estimated based upon historical patterns of losses in each component, the credit ratings allocated to the borrowers and reflecting the current economic climate in which the borrowers operate.

All property and equipment other than buildings are stated at cost less accumulated depreciation and any accumulated impairment loss. Buildings are shown at market value based on valuations by external independent valuers, less subsequent depreciation. Increases in the carrying amount arising on revaluation are recognised in other comprehensive income and credited to a revaluation reserve. Decrease that offset previous increase of the same asset are charged against the revaluation reserve; all other decreases are charged to profit or loss. Each year the difference in depreciation based on the revalued carrying amount of the asset (the depreciation charged to profit or loss) and depreciation based on the asset's original cost is transferred from the revaluation reserve to retained earnings net of the related deferred tax effect.

DEPRECIATION

Depreciation is calculated on a straight line basis to write down the cost of each asset, or the revalued amounts, to their residual values over their estimated useful life as follows:

Payments to acquire interests in leasehold land are treated as operating lease prepayments and amortised over the term of the related lease.

Useful lives, residual values and depreciation methods are reassessed at each year end and adjusted prospectively if needed.

27

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

INTANGIBLE ASSETS (continued)

IMPAIRMENT

FIDUCIARY ACTIVITIES

LEASES

The Bank as lessor

The Bank as lessee

OFFSETTING OF ASSETS AND LIABILITIES

GRANTS

Grants relating to assets are presented in the statement of financial position by setting them up as deferred income. The grants are recognised as income over the lifetime of the assets to which they relate.

Assets and income arising from fiduciary activities together with related undertakings to return such assets to customers are excluded from these financial statements where the Bank acts in a fiduciary capacity such as nominee, trustee or agent. The results of these activities are disclosed in note 32.

The Bank assesses at each reporting date whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Bank estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (CGU) fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Amounts due from lessees under finance leases are recorded as receivables at the amount of the Bank’s net investment in the leases. Finance lease income is allocated to accounting periods so as to reflect a constant periodic rate of return on the Bank’s net investment outstanding in respect of the leases.Rental income from operating leases is recognised on a straight line basis over the terms of the relevant leases.

Rentals payable under operating leases are charged to profit or loss on a straight-line basis over the term of the relevant lease.

Assets and liabilities are offset and the net amount reported in the statement of financial position when there is a legally enforceable right to set off the recognised amounts and there is an intention to settle on a net basis or realize the asset and settle the liability simultaneously.

Useful lives and amortisation methods are reassesed at each year end and adjusted prospectively if needed.

TROPICAL BANK LIMITED

Costs associated with developing or maintaining computer software programs are recognised as an expense as incurred. Costs that are directly associated with the production of identifiable and unique software products controlled by the Bank and that, that will probably generate economic benefits exceeding costs beyond one year, are recognised as intangible assets. Direct costs include software development, employee costs and an appropriate portion of relevant overheads.Computer software development costs recognised as assets are amortised using the straight-line method over their useful lives.

NOTES TO THE FINANCIAL STATEMENTS (Continued)

28

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

CASH AND CASH EQUIVALENTS

TAXES(i) Current tax

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date.

Current tax assets and liabilities for the current and prior years are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted by the reporting date.

Deferred tax is provided on temporary differences at the reporting date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred tax liabilities are recognised for all taxable temporary differences, except:- Where the deferred tax liability arises from the initial recognition of goodwill or of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss- In respect of taxable temporary differences associated with investments in subsidiaries, where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future.

Deferred tax assets are recognised for all deductible temporary differences, carry forward of unused tax credits and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, and the carry forward of unused tax credits and unused tax losses can be utilised except:- Where the deferred tax asset relating to the deductible temporary difference arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss- In respect of deductible temporary differences associated with investments in subsidiaries, deferred tax assets are recognised only to the extent that it is probable that the temporary differences will reverse in the foreseeable future and taxable profit will be available against which the temporary differences can be utilised.

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax asset to be utilised. Unrecognised deferred tax assets are reassessed at each reporting date and are recognised to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered.

TROPICAL BANK LIMITED

For the purposes of the statement of cash flows, cash and cash equivalents comprise balances with less than 90 days maturity from the date of acquisition, including cash and balances with Bank of Uganda, treasury bills and other eligible bills and balances with other financial institutions.

NOTES TO THE FINANCIAL STATEMENTS (Continued)

(ii) Deferred tax

Current tax and deferred tax relating to items recognised directly in other comprehensive income or equity are also recognised in other comprehensive income or equity and not in the statement of comprehensive income.

Deferred tax assets and deferred tax liabilities are offset if a legally enforceable right exists to set off current tax assets against current tax liabilities and the deferred taxes relate to the same taxable entity and the same taxation authority.

29

3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

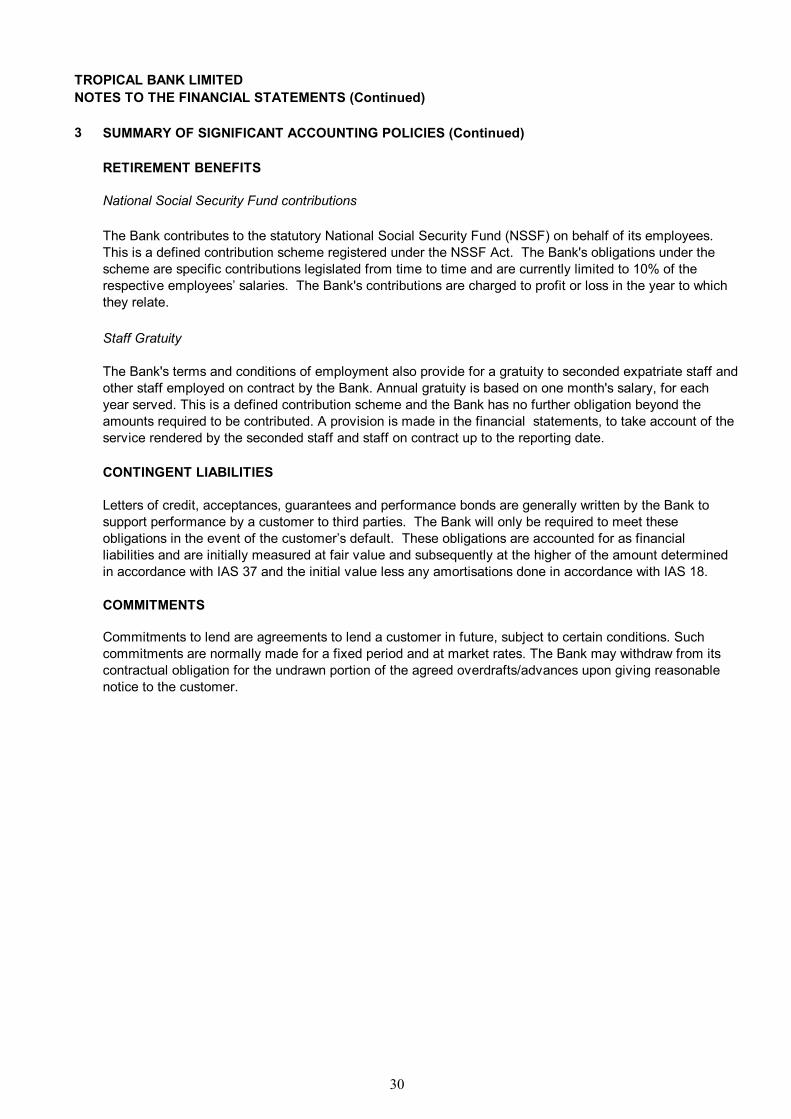

RETIREMENT BENEFITS

National Social Security Fund contributions

Staff Gratuity

CONTINGENT LIABILITIES

COMMITMENTS

The Bank contributes to the statutory National Social Security Fund (NSSF) on behalf of its employees. This is a defined contribution scheme registered under the NSSF Act. The Bank's obligations under the scheme are specific contributions legislated from time to time and are currently limited to 10% of the respective employees’ salaries. The Bank's contributions are charged to profit or loss in the year to which they relate.

The Bank's terms and conditions of employment also provide for a gratuity to seconded expatriate staff and other staff employed on contract by the Bank. Annual gratuity is based on one month's salary, for each year served. This is a defined contribution scheme and the Bank has no further obligation beyond the amounts required to be contributed. A provision is made in the financial statements, to take account of the service rendered by the seconded staff and staff on contract up to the reporting date.

Letters of credit, acceptances, guarantees and performance bonds are generally written by the Bank to support performance by a customer to third parties. The Bank will only be required to meet these obligations in the event of the customer’s default. These obligations are accounted for as financial liabilities and are initially measured at fair value and subsequently at the higher of the amount determined in accordance with IAS 37 and the initial value less any amortisations done in accordance with IAS 18.

Commitments to lend are agreements to lend a customer in future, subject to certain conditions. Such commitments are normally made for a fixed period and at market rates. The Bank may withdraw from its contractual obligation for the undrawn portion of the agreed overdrafts/advances upon giving reasonable notice to the customer.

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

30

4 FINANCIAL RISK MANAGEMENT

Strategy in using Financial Instruments

a) Credit risk

TROPICAL BANK LIMITED

Exposure to credit risk is managed through regular analysis of the ability of borrowers and potentialborrowers to meet interest and capital repayment obligations and by changing these lending limitswhere appropriate. Exposure to credit risk is also managed in part by obtaining collateral andcorporate and personal guarantees, but a portion is personal lending where no such facilities can beobtained.

By their nature, the Bank's activities are principally related to the use of financial instruments. TheBank accepts deposits from customers at fixed rates and for various periods, and seeks to earn aboveaverage interest margins by investing these funds in high-quality assets. The Bank seeks to increasethese margins by consolidating short-term funds and lending for longer periods at higher rates, whilemaintaining sufficient liquidity to meet all claims that might fall due.

The Bank also seeks to raise its interest margins by obtaining above average margins, net ofallowances, through lending to commercial and retail borrowers with a range of credit standing. Suchexposures involve not just on-statement of financial position loans and advances; the Bank also entersinto guarantees and other commitments such as letters of credit and performance and other bonds.

The Bank also trades in financial instruments where it takes positions in traded and over-the-counterinstruments, to take advantage of short-term market movements in bonds and in currency andinterest rate. The Board places trading limits on the level of exposure that can be taken in relation toovernight market positions. Foreign exchange and interest rate exposures associated with thesefinancial instruments are normally offset by entering into counter-balancing positions, therebycontrolling the variability in the net cash amounts required to liquidate market positions.

The Bank takes on exposure to credit risk, which is the risk that a counter party will be unable to payamounts in full when due. Impairment provisions are provided for losses that have been incurred at thereporting date. Significant changes in the economy, or in the health of a particular industry segmentthat represents a concentration in the Bank's portfolio, could result in losses that are different fromthose provided for at the reporting date. Management therefore carefully manages its exposure tocredit risk.

The Bank structures the levels of credit risk it undertakes by placing limits on the amount of riskaccepted in relation to one borrower, or group of borrowers, and to geographical and industrysegments. Such risks are monitored on a revolving basis and subject to quarterly review. Limits on thelevel of credit risk by product, industry sector and by country are approved annually by the Board ofDirectors. The exposure to any one borrower including banks is further restricted by sub-limits coveringon and off-statement of financial position exposures. Actual exposures against limits are monitoreddaily.

NOTES TO THE FINANCIAL STATEMENTS (Continued)

31

4 FINANCIAL RISK MANAGEMENT (continued)a) Credit risk (continued)

Maximum exposure to credit risk before collateral held

2012 2011Credit exposures Ushs '000 Ushs '000On-statement of financial position items

Deposits and balances due frombanking institutions 53,890,840 36,557,576 Loans and advances to customers 105,461,246 104,827,223 Government securities 23,913,530 26,791,474 Other assets - trade receivables 3,186,111 2,709,703

186,451,727 170,885,976 Off-statement of financial position itemsLetters of credit 7,815,065 9,117,005 Guarantee and performance bonds 2,291,493 8,390,607

10,106,558 17,507,612

196,558,285 188,393,588

Concentrations of risk

Loans and advances to customers

Economic risk concentration within gross loans and advances portfolio is as follows:

2012 2011Ushs'000 Ushs'000

Trade and commerce 11,554,874 11,833,706 Manufacturing 13,273,169 15,247,597 Agriculture 14,545,487 13,633,869 Transport, communication, electricity and water 6,531,717 15,472,171 Others 61,924,639 50,762,173

107,829,886 106,949,516

TROPICAL BANK LIMITED

The effective interest rates on loans and advances as at 31 December 2012 was 23% (2011: 15.85%).

The above represents the worst case scenario of credit exposure for both years, without taking into account any collateral held or other credit enhancements attached.

Deposits and balances due from banking institutions, comprise 28% (2011: 20%) of the total maximum exposure.

The Bank monitors concentration of risk by economic sector in line with set limits per sector. An analysis of concentrations within the gross loan and advances to customers are as follows:

NOTES TO THE FINANCIAL STATEMENTS (Continued)

32

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

4 FINANCIAL RISK MANAGEMENT (Continued)

a) Credit risk (continued)Credit-related commitments

b) Interest rate risk

0-3 3-12 1-5 Non interest31 December 2012 months months years bearing Total

Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000Financial AssetsCash at hand - - - 6,973,698 6,973,698 Balances with bank of Uganda - - - 12,602,362 12,602,362 Deposits and balances due from - banking institutions 53,890,840 - - - 53,890,840

Government securities 3,641,512 13,741,415 6,530,603 - 23,913,530

Loans and advances to customers 23,177,766 37,695,750 44,587,730 - 105,461,246 Total financial assets 80,710,118 51,437,165 51,118,333 19,576,060 202,841,676

Non financial assets - - - 12,458,346 12,458,346

Total assets 80,710,118 51,437,165 51,118,333 32,034,406 215,300,022

Financial liabilitiesCustomer deposits 85,683,587 29,806,754 39,304 - 115,529,645 Administered funds - - - 1,075,000 1,075,000 Loans from parent company - 29,793,213 - - 29,793,213 Total financial liabilities 85,683,587 59,599,967 39,304 1,075,000 146,397,858

Non financial liabilities - - - 17,638,472 17,638,472

Total liabilities 85,683,587 59,599,967 39,304 18,713,472 164,036,330

Equity - - - 51,263,692 51,263,692

Total liabilities and equity 85,683,587 59,599,967 39,304 69,977,164 215,300,022

Interest sensitivity gap on financial instruments (4,973,469) (8,162,802) 51,079,029 37,942,758

Off-statement of financial position items - - - 13,403,296 13,403,296

The primary purpose of these instruments is to ensure that funds are available to a customer as required. Guarantees andstandby letters of credit (which represent irrevocable assurances that the Bank will make payments in the event that acustomer cannot meet its obligations to third parties) carry the same credit risk as loans. Documentary and commercial lettersof credit (which are written undertakings by the Bank on behalf of customer authorising a third party to draw drafts on the Bankup to a stipulated amount under specific terms and conditions) are collateralised by the underlying shipments of goods towhich they relate and therefore carry less risk than a direct borrowing.

Commitments to extend credit represent unused portions of authorization to extend credit in the form of loans, guarantees orletters of credit. With respect to credit risk on commitments to extend credit, the Bank is potentially exposed to loss in anamount equal to the total unused commitments. However, the likely amount of loss is less than the total unused commitments,as most commitments to extend credit are contingent upon customers maintaining specific credit standards. The Bankmonitors the term to maturity of credit commitments because longer-term commitments generally have a greater degree ofcredit risk than shorter-term commitments.

The Bank is exposed to various risks associated with the effects of fluctuations of the levels of prevailing market interest rateson its financial position and cash flows. The table below summarizes the exposure to interest rate risk. Included in the tablebelow are the Bank’s assets and liabilities at carrying amounts, categorized by the earlier of contractual repricing or maturitydates. The Bank does not bear any interest rate risk on off-statement of financial position items.

33

TROPICAL BANK LIMITEDNOTES TO THE FINANCIAL STATEMENTS (Continued)

4 FINANCIAL RISK MANAGEMENT (Continued)

b) Interest rate risk (continued)

0-3 3-12 1-5 Non interestAt 31 December 2011 months months years bearing Total

Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000Financial assetsCash at hand - - - 6,099,617 6,099,617 Balances with bank of Uganda - - - 5,400,301 5,400,301 Deposits and balances due frombanking institutions 36,557,576 - - - 36,557,576 Government securities 770,012 5,826,249 20,195,213 - 26,791,474 Loans and advances to customers 15,220,867 47,481,917 42,124,439 - 104,827,223 Total financial assets 52,548,455 53,308,166 62,319,652 11,499,918 179,676,191

Non financial assets - - - 12,578,181 12,578,181

Total assets 52,548,455 53,308,166 62,319,652 24,078,099 192,254,372

Financial liabilitiesCustomer deposits 59,189,533 29,201,570 192,990 - 88,584,093 Administered funds - - - 1,000,000 1,000,000 Other liabilities - - - 23,041,736 23,041,736 Loans from parent company - - 27,280,000 - 27,280,000 Total financial liabilities 59,189,533 29,201,570 27,472,990 24,041,736 139,905,829

Non financial liabilities - - - 1,377,823 1,377,823 Total liabilities 59,189,533 29,201,570 27,472,990 25,419,559 141,283,652

Equity - - - 50,970,720 50,970,720

Total liabilities and equity 59,189,533 29,201,570 27,472,990 76,390,279 192,254,372

Interest sensitivity gap on financial instruments (6,641,078) 24,106,596 34,846,662 52,312,180

Off-statement of financial position items - - - 28,471,890 28,471,890

34

NOTES TO THE FINANCIAL STATEMENTS (Continued)

4 FINANCIAL RISK MANAGEMENT (Continued)

c) Liquidity risk analysis (Continued)

At 31 December 2012Weighted Less than 1-3 3-12 1-5

average 1 Month Months months Years Totaleffective Ushs'000 Ushs'000 Ushs'000 Ushs'000 Ushs'000

interest rateAssetsNon-interest bearingCash and balances at BOU 19,576,060 - - - 19,576,060 Fixed assets - - - 7,408,131 7,408,131 Other assets - - 3,186,111 1,864,104 5,050,215

19,576,060 - 3,186,111 9,272,235 32,034,406

Fixed interest rate instruments 11.96%Deposits due from Banks 53,890,840 - - - 53,890,840 Investments securities 2,660,063 - 14,722,863 6,530,604 23,913,530 Net loans and advances 16,015,496 7,162,270 37,695,750 44,587,730 105,461,246

72,566,399 7,162,270 52,418,613 51,118,334 183,265,616

Total assets 92,142,459 7,162,270 55,604,724 60,390,569 215,300,022

Liabilities

Non-interest bearingDemand deposits 58,728,677 - - - 58,728,677 Administered funds - - - 1,075,000 1,075,000 Bills payable - 6,984,380 - 76,204 7,060,584 Other liabilities 203,213 10,432,708 - 145,180 10,781,101

58,931,890 17,417,088 - 1,296,384 77,645,362

Fixed interest rate instrumentsBanks time deposits - 631,739 631,739 Time deposits 4,945,421 1,805,820 29,806,754 39,304 36,597,299 Savings deposits 19,571,930 19,571,930 Subordinated debt - - 29,590,000 - 29,590,000

24,517,351 1,805,820 60,028,493 39,304 86,390,968

Equity 51,263,692 51,263,692

Total liabilities and equity 83,449,241 19,222,908 60,028,493 52,599,380 215,300,022

Off statement of financial position itemsCommitments 4,050,655 4,050,655 Guarantees & bonds 1,088,345 17,000 615,391 72,630 1,793,366 Letters of Credit 1,746,545 - 432,719 5,380,000 7,559,264 Total 6,885,545 17,000 1,048,110 5,452,630 13,403,285

Total liabilities & off statement of financial position items 90,334,786 19,239,908 61,076,603 58,052,010 228,703,307

Net liquidity gap 1,807,673 (12,077,638) (5,471,879) 2,338,559 (13,403,285)

TROPICAL BANK LIMITED

35

NOTES TO THE FINANCIAL STATEMENTS (Continued)

4 FINANCIAL RISK MANAGEMENT (Continued)

c) Liquidity risk analysis (Continued)

At 31 December 2011Weighted Less than 1-3 3-12 1-5