TREVI – Finanziaria Industriale S.p.A. · PDF fileTREVI – Finanziaria Industriale...

192

TREVI – Finanziaria Industriale S.p.A. Financial Statements and Consolidated Financial Statements at 31 December 2016 TREVI – Finanziaria Industriale S.p.A. Registered Office Cesena (Forlì-Cesena) – Via Larga 201 – Italy Share capital Euro 82,391,632.50 fully paid-up Forlì – Cesena Chamber of Commerce Business Register no. 201,271 Tax code, VAT no. and Forlì – Cesena Business Registry: 01547370401 Website: www.trevifin.com

Transcript of TREVI – Finanziaria Industriale S.p.A. · PDF fileTREVI – Finanziaria Industriale...

TREVI – Finanziaria Industriale S.p.A. Financial Statements and Consolidated Financial Statements at

31 December 2016

TREVI – Finanziaria Industriale S.p.A. Registered Office Cesena (Forlì-Cesena) – Via Larga 201 – Italy

Share capital Euro 82,391,632.50 fully paid-up Forlì – Cesena Chamber of Commerce Business Register no. 201,271

Tax code, VAT no. and Forlì – Cesena Business Registry: 01547370401 Website: www.trevifin.com

2

CONTENTS

KEY FINANCIAL FIGURES OF THE GROUP Board of Directors’ Report on Operations for the Consolidated and Parent Company Financial Statements. CONSOLIDATED FINANCIAL STATEMENTS AT 31 DECEMBER 20 16 Consolidated Statement of Financial Position, Consolidated Income Statement, Consolidated Statement of Comprehensive Income, Consolidated Statement of Changes in Net Equity, Consolidated Statement of Cash Flows Explanatory Notes to the Consolidated Financial Statements Appendices to the Explanatory Notes to the Consolidated Financial Statements Independent Auditors’ Report pursuant to Articles 14 and 16 of Legislative Decree 27.1.2010, no.39 Report of the Board of Statutory Auditors pursuant to Article 153 of Legislative Decree no. 58/1998 and of Article 2429 paragraph 3 of the Italian Civil Code. FINANCIAL STATEMENTS AT 31 DECEMBER 2016

Statement of Financial Position, Income Statement, Statement of Comprehensive Income, Statement of Changes in Net Equity, Statement of Cash Flows Explanatory Notes to the Financial Statements Independent Auditors’ Report pursuant to Articles 14 and 16 of Legislative Decree 27.1.2010, no.39

3

MEMBERS OF THE CORPORATE BODIES CHAIRMAN Davide Trevisani EXECUTIVE DEPUTY CHAIRMAN Gianluigi Trevisani DEPUTY CHAIRMAN Cesare Trevisani MANAGING DIRECTOR Stefano Trevisani BOARD OF DIRECTORS Marta Dassù (Non-executive and independent director) Umberto della Sala (Non-executive and independent director) Cristina Finocchi Mahne (Non-executive and independent director) Monica Mondardini (Non-executive and independent director) Guido Rivolta (Non-executive director) Rita Rolli (Non-executive and independent director) Simone Trevisani (Executive director) BOARD OF STATUTORY AUDITORS Standing Statutory Auditors Milena Motta (Chairperson) Adolfo Leonardi Giancarlo Poletti

Supplementary Statutory Auditors Marta Maggi Stefano Leardini

OTHER CORPORATE BODIES Director responsible for the internal control system and risk management Gianluigi Trevisani Risk Management Committee Monica Mondardini (Chairperson) Cristina Finocchi Mahne Rita Rolli

Committee to oversee the Organisational Model Luca Moretti (Chairperson and internal member) Floriana Francesconi Enzo Spisni

Director of Administration, Finance and Control Daniele Forti Appointed Manager responsible for the preparation of company accounts by the Board of Directors on 14 May 2007 Lead Independent Director Monica Mondardini Audit Firm Reconta Ernst &Young S.p.A. (Appointed on 29 April 2008 and until the Shareholders’ Meeting to approve the Financial Statements at 31 December 2016)

4

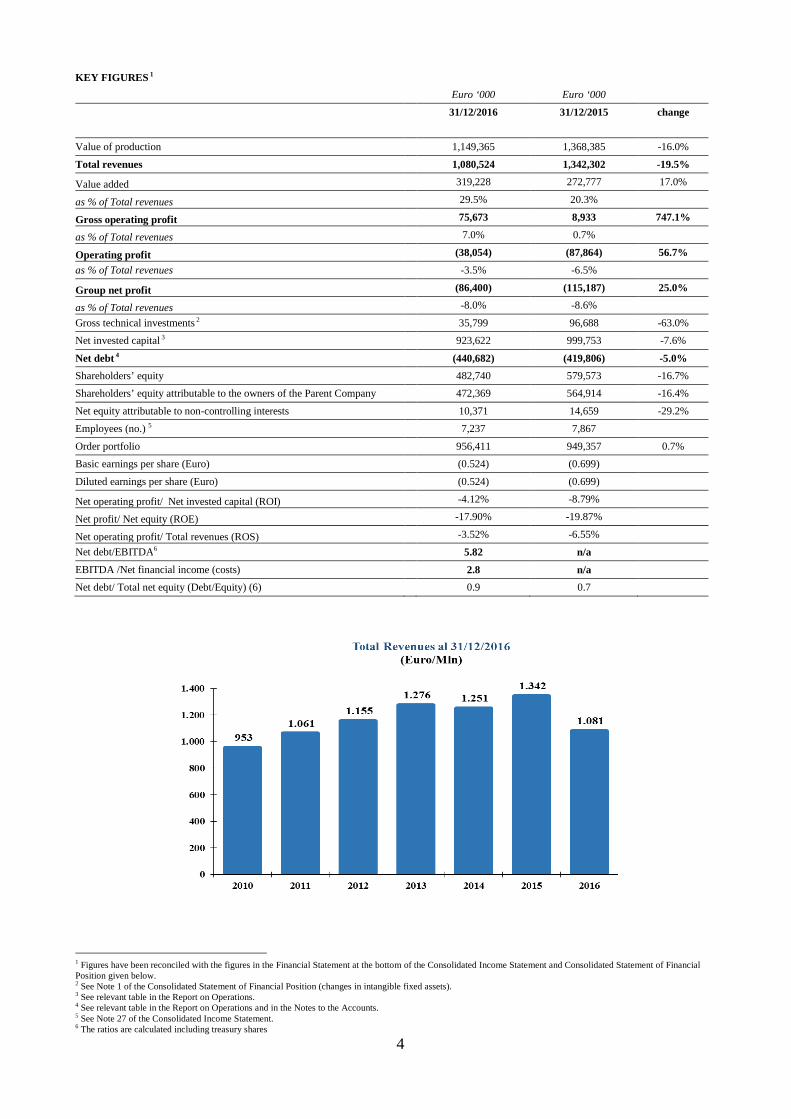

KEY FIGURES 1

Euro ‘000 Euro ‘000

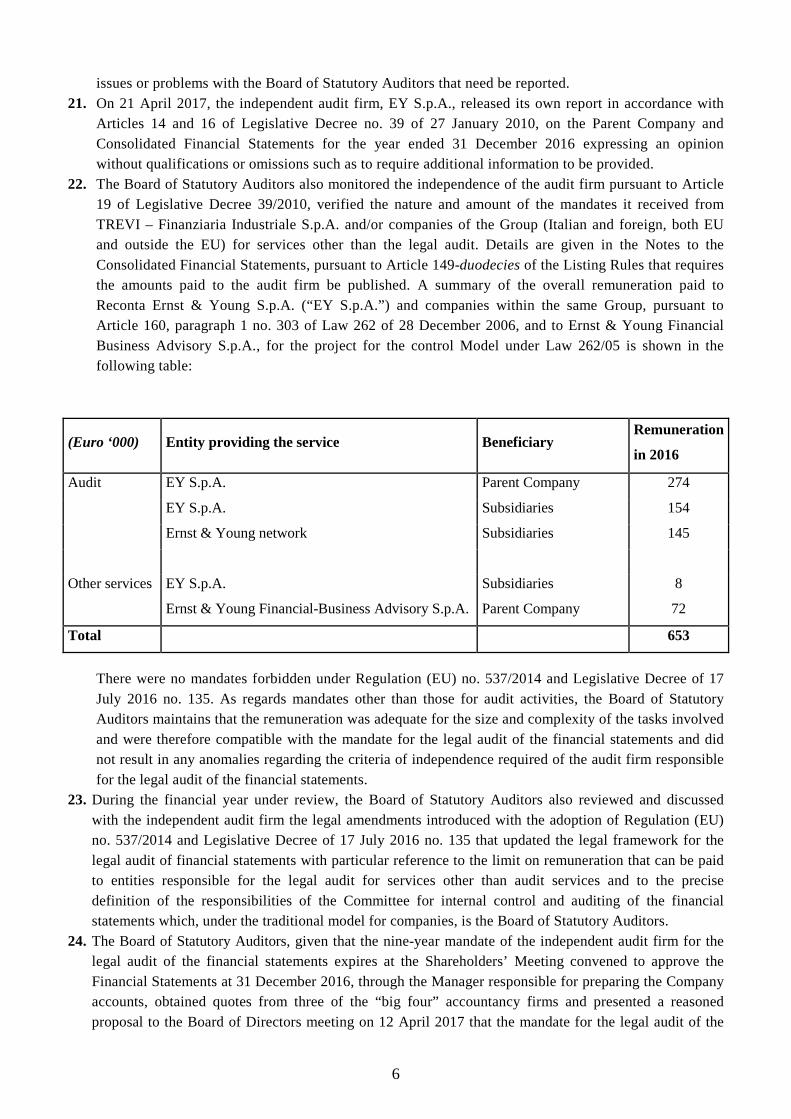

31/12/2016 31/12/2015 change

Value of production 1,149,365 1,368,385 -16.0%

Total revenues 1,080,524 1,342,302 -19.5%

Value added 319,228 272,777 17.0%

as % of Total revenues 29.5% 20.3%

Gross operating profit 75,673 8,933 747.1%

as % of Total revenues 7.0% 0.7%

Operating profit (38,054) (87,864) 56.7%

as % of Total revenues -3.5% -6.5%

Group net profit (86,400) (115,187) 25.0%

as % of Total revenues -8.0% -8.6%

Gross technical investments 2 35,799 96,688 -63.0%

Net invested capital 3 923,622 999,753 -7.6%

Net debt 4 (440,682) (419,806) -5.0%

Shareholders’ equity 482,740 579,573 -16.7%

Shareholders’ equity attributable to the owners of the Parent Company 472,369 564,914 -16.4%

Net equity attributable to non-controlling interests 10,371 14,659 -29.2%

Employees (no.) 5 7,237 7,867

Order portfolio 956,411 949,357 0.7%

Basic earnings per share (Euro) (0.524) (0.699)

Diluted earnings per share (Euro) (0.524) (0.699)

Net operating profit/ Net invested capital (ROI) -4.12% -8.79%

Net profit/ Net equity (ROE) -17.90% -19.87%

Net operating profit/ Total revenues (ROS) -3.52% -6.55%

Net debt/EBITDA6 5.82 n/a EBITDA /Net financial income (costs) 2.8 n/a

Net debt/ Total net equity (Debt/Equity) (6) 0.9 0.7

1 Figures have been reconciled with the figures in the Financial Statement at the bottom of the Consolidated Income Statement and Consolidated Statement of Financial Position given below. 2 See Note 1 of the Consolidated Statement of Financial Position (changes in intangible fixed assets). 3 See relevant table in the Report on Operations. 4 See relevant table in the Report on Operations and in the Notes to the Accounts. 5 See Note 27 of the Consolidated Income Statement. 6 The ratios are calculated including treasury shares

5

BOARD OF DIRECTORS’ REPORT ON OPERATIONS FOR THE CO NSOLIDATED AND

PARENT COMPANY FINANCIAL STATEMENTS AT 31 DECEMBER 2016

Dear shareholders, In the 2016 financial year, consolidated revenues were approximately Euro 1,080 million with the

Special Foundations Division accounting for approximately 76% of total revenues and the Oil & Gas

Division decreasing to approximately 24% of revenues.

The order portfolio was almost unchanged compared to the end of the previous financial year at

approximately Euro 960 million (+0.7%), of which 80% is due to be completed in 2017.

EBITDA was Euro 75.7 million, a margin of 7% of total revenues (Euro 8.9 million in 2015). The

Group net result was a loss of Euro 86.4 million (a loss of Euro 115 million in 2015). Net debt was

almost unchanged compared to 2015 (+5%).

Following a broadly positive first semester that closed with Group financial ratios that were highly

satisfactory, in the second semester there was a significant decrease in the order portfolio of the Oil

& Gas Division. The continued negative performance of the global energy sector in 2016 forced oil

companies to reschedule their investments in research and exploration and also in extraction from

existing oil fields.

However, by year-end, there were concrete signs that the oil price would stabilise, particularly in the

second half of 2017, which increased expectations of a recovery in the long-term. This was

confirmed by Drillmec winning an important contract to supply its technologically advanced and

highly efficient oil rigs to Bolivia. A cost reduction programme is being implemented not only in the

Oil & Gas sector but across the Group that is aimed at ensuring it remains ready and adaptable to

tackle new and important contracts.

Although there continues to be no signs of recovery in the domestic construction market, the Group,

which for years has had its main focus in markets outside Europe, finalised contracts for several

important projects in the USA and in the Middle East, the largest of which was for the repairs to the

Mosul Dam in Iraq. This is a highly technological project given the logistical challenges involved

6

and the sensitivity of the area in which it is located. However, it is an affirmation of the experience,

capability and adaptibility of TREVI in facing highly complex engineering challenges – the practical

demonstration of which was the unanimous approval won by TREVI from the three countries

involved in the contract: Italy, Iraq and the United States.

Our task remains that of ensuruing both operating segments achieve solid profitability and balanced

growth while respecting risk and financial ratios and, at the same time, ensuring an improvement in

the Group’s worldwide execution ability.

7

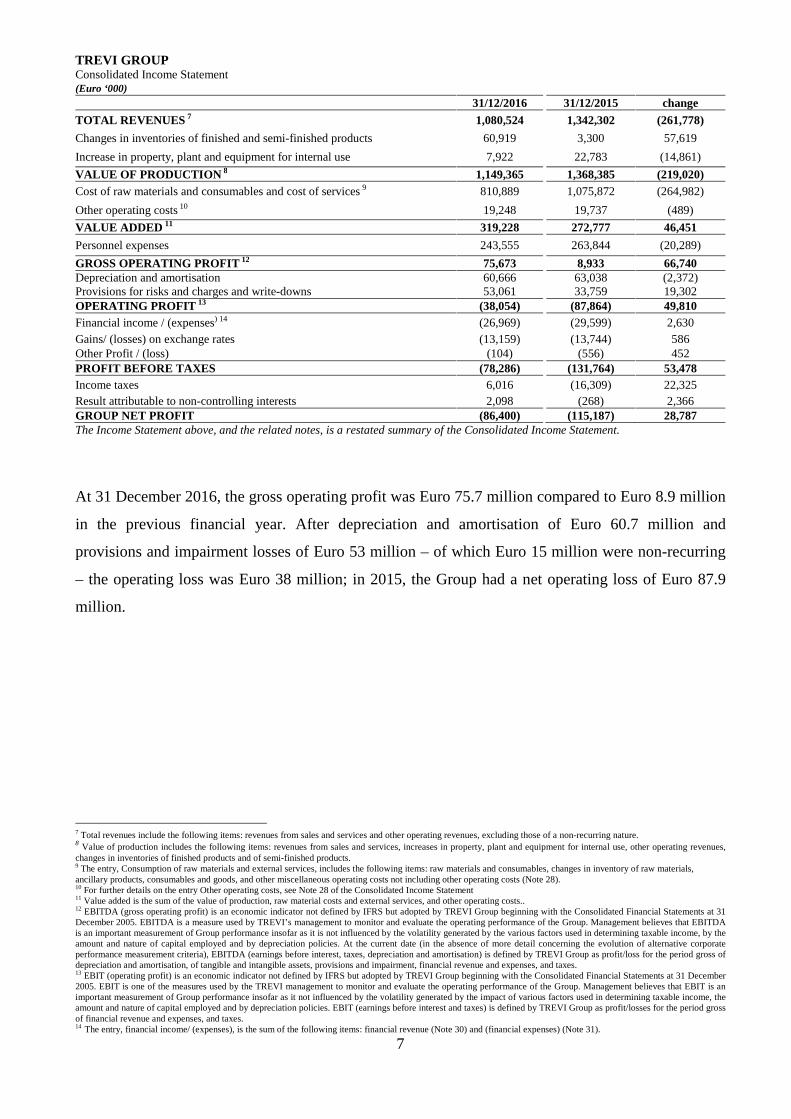

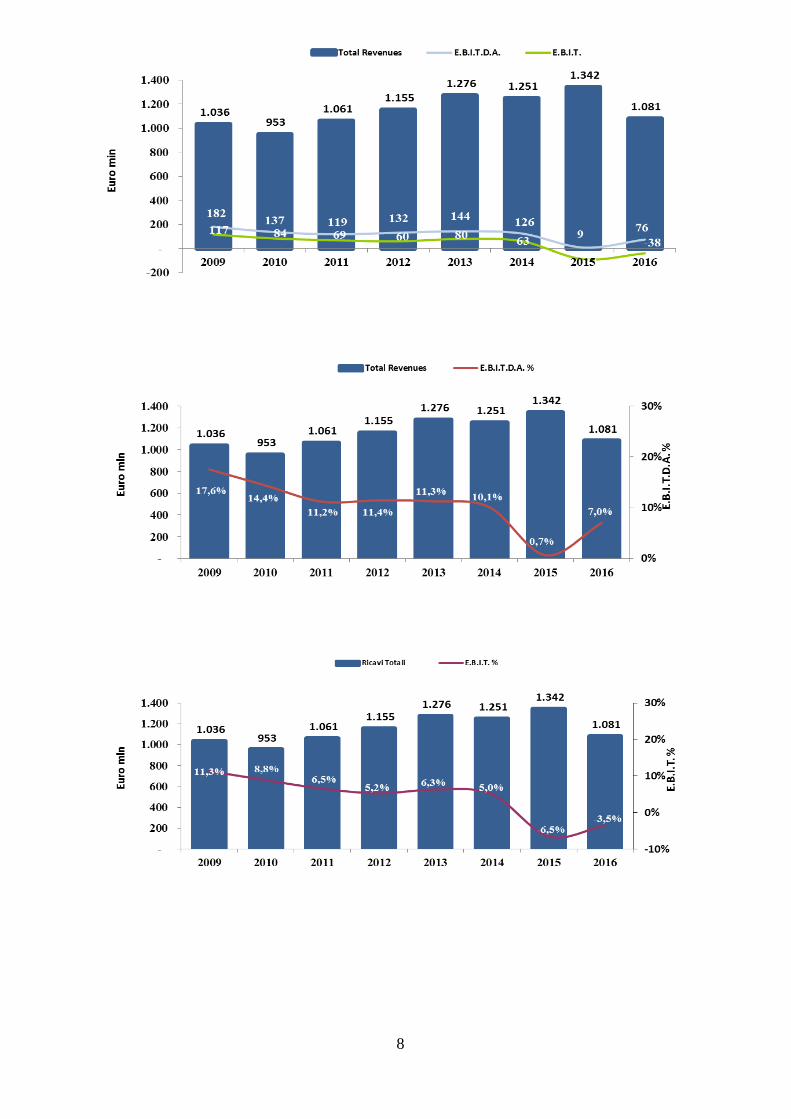

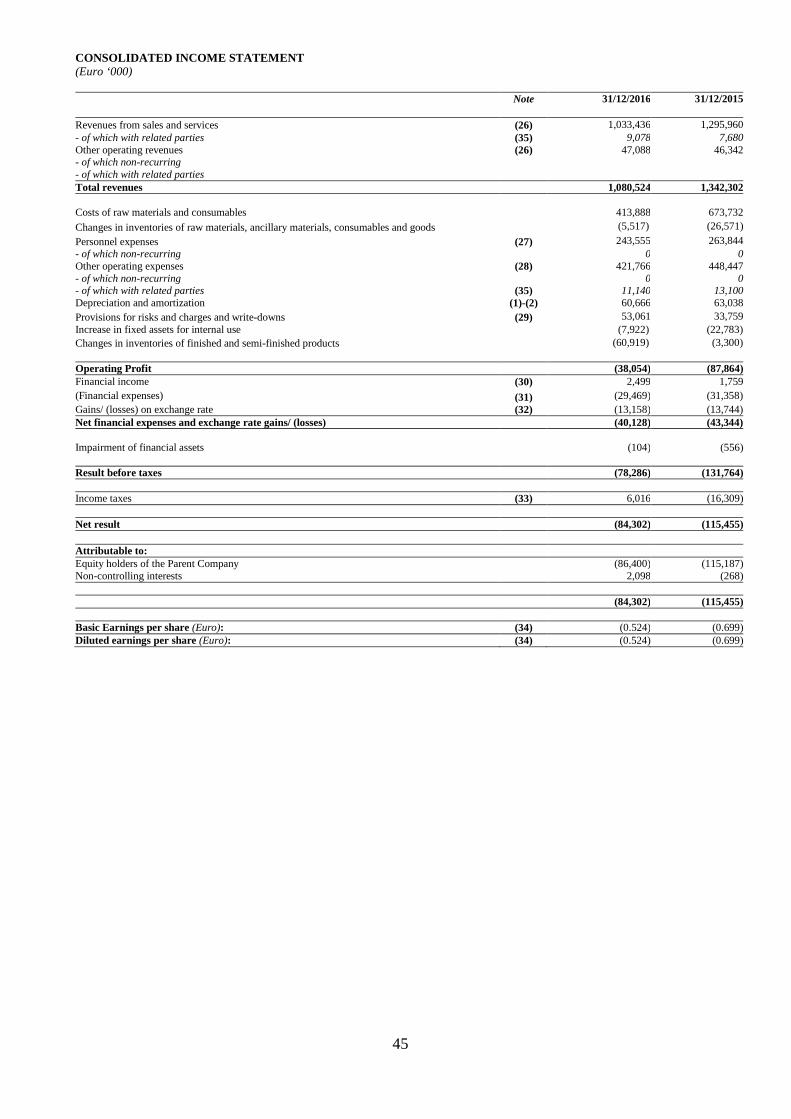

TREVI GROUP Consolidated Income Statement (Euro ‘000) 31/12/2016 31/12/2015 change TOTAL REVENUES 7 1,080,524 1,342,302 (261,778)

Changes in inventories of finished and semi-finished products 60,919 3,300 57,619

Increase in property, plant and equipment for internal use 7,922 22,783 (14,861)

VALUE OF PRODUCTION 8 1,149,365 1,368,385 (219,020) Cost of raw materials and consumables and cost of services 9 810,889 1,075,872 (264,982)

Other operating costs 10 19,248 19,737 (489)

VALUE ADDED 11 319,228 272,777 46,451

Personnel expenses 243,555 263,844 (20,289)

GROSS OPERATING PROFIT 12 75,673 8,933 66,740 Depreciation and amortisation 60,666 63,038 (2,372) Provisions for risks and charges and write-downs 53,061 33,759 19,302 OPERATING PROFIT 13 (38,054) (87,864) 49,810 Financial income / (expenses) 14 (26,969) (29,599) 2,630 Gains/ (losses) on exchange rates (13,159) (13,744) 586 Other Profit / (loss) (104) (556) 452 PROFIT BEFORE TAXES (78,286) (131,764) 53,478 Income taxes 6,016 (16,309) 22,325 Result attributable to non-controlling interests 2,098 (268) 2,366 GROUP NET PROFIT (86,400) (115,187) 28,787 The Income Statement above, and the related notes, is a restated summary of the Consolidated Income Statement.

At 31 December 2016, the gross operating profit was Euro 75.7 million compared to Euro 8.9 million

in the previous financial year. After depreciation and amortisation of Euro 60.7 million and

provisions and impairment losses of Euro 53 million – of which Euro 15 million were non-recurring

– the operating loss was Euro 38 million; in 2015, the Group had a net operating loss of Euro 87.9

million.

7 Total revenues include the following items: revenues from sales and services and other operating revenues, excluding those of a non-recurring nature. 8 Value of production includes the following items: revenues from sales and services, increases in property, plant and equipment for internal use, other operating revenues, changes in inventories of finished products and of semi-finished products. 9 The entry, Consumption of raw materials and external services, includes the following items: raw materials and consumables, changes in inventory of raw materials, ancillary products, consumables and goods, and other miscellaneous operating costs not including other operating costs (Note 28). 10 For further details on the entry Other operating costs, see Note 28 of the Consolidated Income Statement 11 Value added is the sum of the value of production, raw material costs and external services, and other operating costs.. 12 EBITDA (gross operating profit) is an economic indicator not defined by IFRS but adopted by TREVI Group beginning with the Consolidated Financial Statements at 31 December 2005. EBITDA is a measure used by TREVI’s management to monitor and evaluate the operating performance of the Group. Management believes that EBITDA is an important measurement of Group performance insofar as it is not influenced by the volatility generated by the various factors used in determining taxable income, by the amount and nature of capital employed and by depreciation policies. At the current date (in the absence of more detail concerning the evolution of alternative corporate performance measurement criteria), EBITDA (earnings before interest, taxes, depreciation and amortisation) is defined by TREVI Group as profit/loss for the period gross of depreciation and amortisation, of tangible and intangible assets, provisions and impairment, financial revenue and expenses, and taxes. 13 EBIT (operating profit) is an economic indicator not defined by IFRS but adopted by TREVI Group beginning with the Consolidated Financial Statements at 31 December 2005. EBIT is one of the measures used by the TREVI management to monitor and evaluate the operating performance of the Group. Management believes that EBIT is an important measurement of Group performance insofar as it not influenced by the volatility generated by the impact of various factors used in determining taxable income, the amount and nature of capital employed and by depreciation policies. EBIT (earnings before interest and taxes) is defined by TREVI Group as profit/losses for the period gross of financial revenue and expenses, and taxes. 14 The entry, financial income/ (expenses), is the sum of the following items: financial revenue (Note 30) and (financial expenses) (Note 31).

8

9

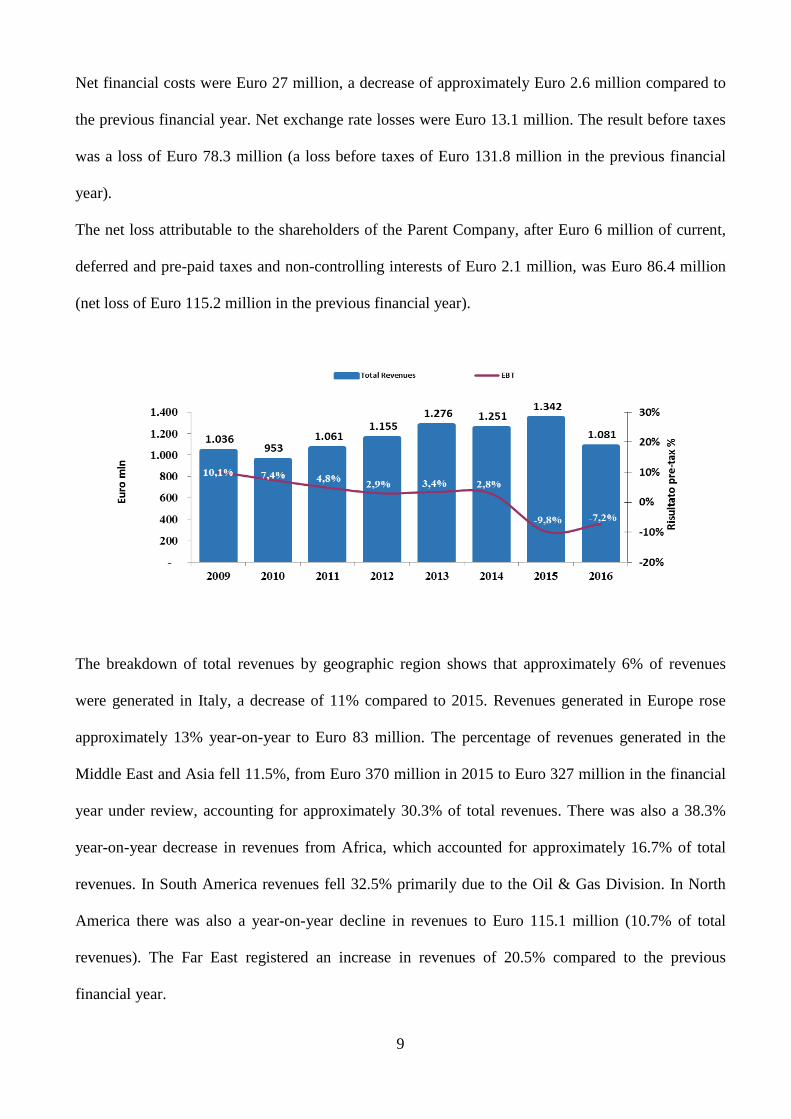

Net financial costs were Euro 27 million, a decrease of approximately Euro 2.6 million compared to

the previous financial year. Net exchange rate losses were Euro 13.1 million. The result before taxes

was a loss of Euro 78.3 million (a loss before taxes of Euro 131.8 million in the previous financial

year).

The net loss attributable to the shareholders of the Parent Company, after Euro 6 million of current,

deferred and pre-paid taxes and non-controlling interests of Euro 2.1 million, was Euro 86.4 million

(net loss of Euro 115.2 million in the previous financial year).

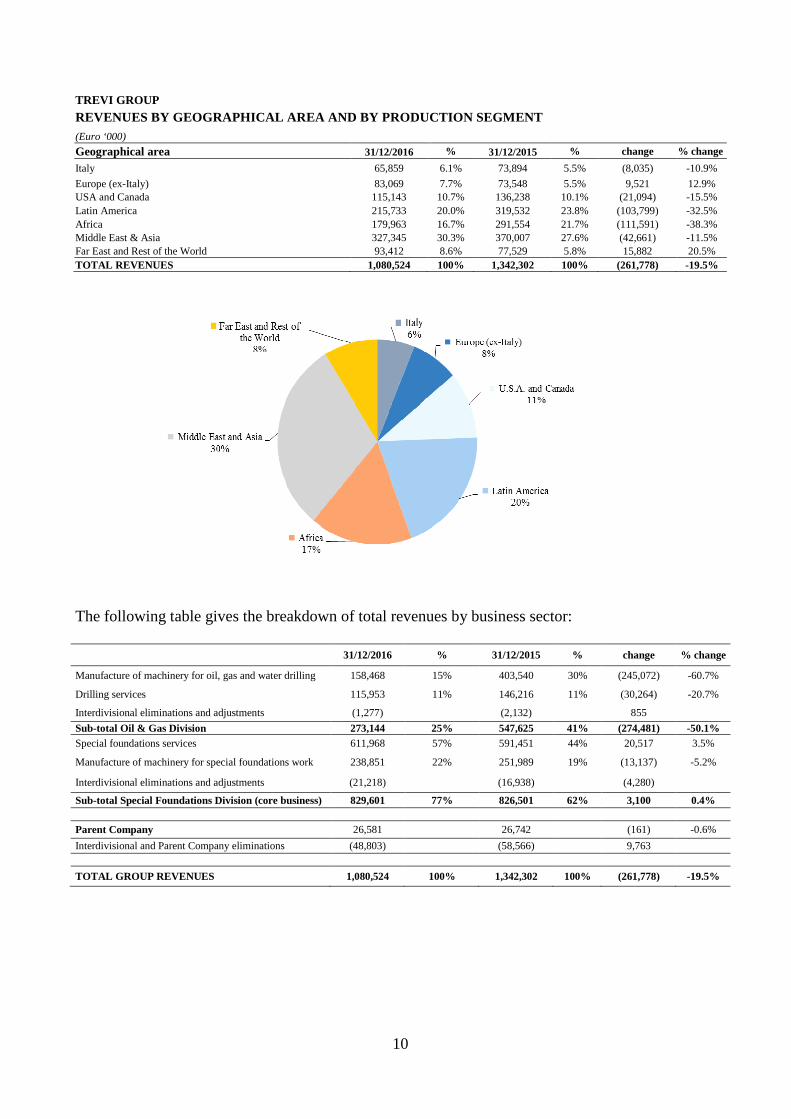

The breakdown of total revenues by geographic region shows that approximately 6% of revenues

were generated in Italy, a decrease of 11% compared to 2015. Revenues generated in Europe rose

approximately 13% year-on-year to Euro 83 million. The percentage of revenues generated in the

Middle East and Asia fell 11.5%, from Euro 370 million in 2015 to Euro 327 million in the financial

year under review, accounting for approximately 30.3% of total revenues. There was also a 38.3%

year-on-year decrease in revenues from Africa, which accounted for approximately 16.7% of total

revenues. In South America revenues fell 32.5% primarily due to the Oil & Gas Division. In North

America there was also a year-on-year decline in revenues to Euro 115.1 million (10.7% of total

revenues). The Far East registered an increase in revenues of 20.5% compared to the previous

financial year.

10

TREVI GROUP

REVENUES BY GEOGRAPHICAL AREA AND BY PRODUCTION SEG MENT

(Euro ‘000)

Geographical area 31/12/2016 % 31/12/2015 % change % change

Italy 65,859 6.1% 73,894 5.5% (8,035) -10.9%

Europe (ex-Italy) 83,069 7.7% 73,548 5.5% 9,521 12.9% USA and Canada 115,143 10.7% 136,238 10.1% (21,094) -15.5% Latin America 215,733 20.0% 319,532 23.8% (103,799) -32.5% Africa 179,963 16.7% 291,554 21.7% (111,591) -38.3% Middle East & Asia 327,345 30.3% 370,007 27.6% (42,661) -11.5% Far East and Rest of the World 93,412 8.6% 77,529 5.8% 15,882 20.5% TOTAL REVENUES 1,080,524 100% 1,342,302 100% (261,778) -19.5%

The following table gives the breakdown of total revenues by business sector:

31/12/2016 % 31/12/2015 % change % change

Manufacture of machinery for oil, gas and water drilling 158,468 15% 403,540 30% (245,072) -60.7%

Drilling services 115,953 11% 146,216 11% (30,264) -20.7%

Interdivisional eliminations and adjustments (1,277) (2,132) 855

Sub-total Oil & Gas Division 273,144 25% 547,625 41% (274,481) -50.1% Special foundations services 611,968 57% 591,451 44% 20,517 3.5%

Manufacture of machinery for special foundations work 238,851 22% 251,989 19% (13,137) -5.2%

Interdivisional eliminations and adjustments (21,218) (16,938) (4,280)

Sub-total Special Foundations Division (core business) 829,601 77% 826,501 62% 3,100 0.4% Parent Company 26,581 26,742 (161) -0.6%

Interdivisional and Parent Company eliminations (48,803) (58,566) 9,763

TOTAL GROUP REVENUES 1,080,524 100% 1,342,302 100% (261,778) -19.5%

11

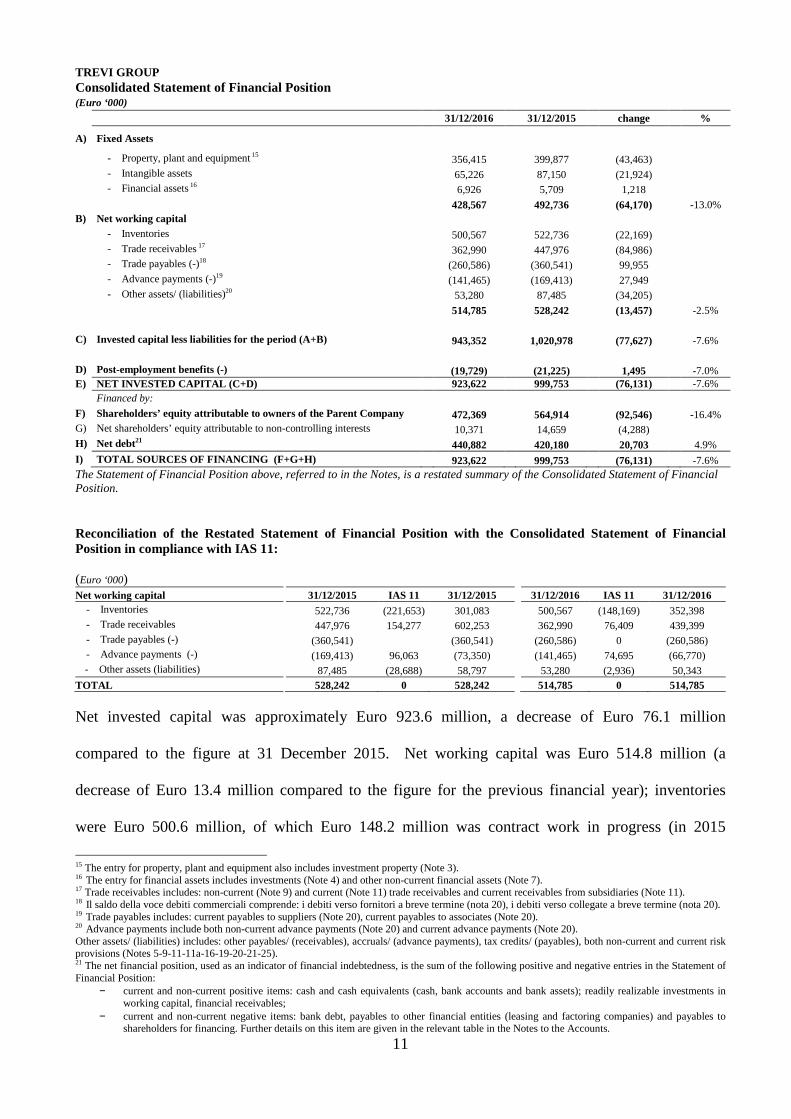

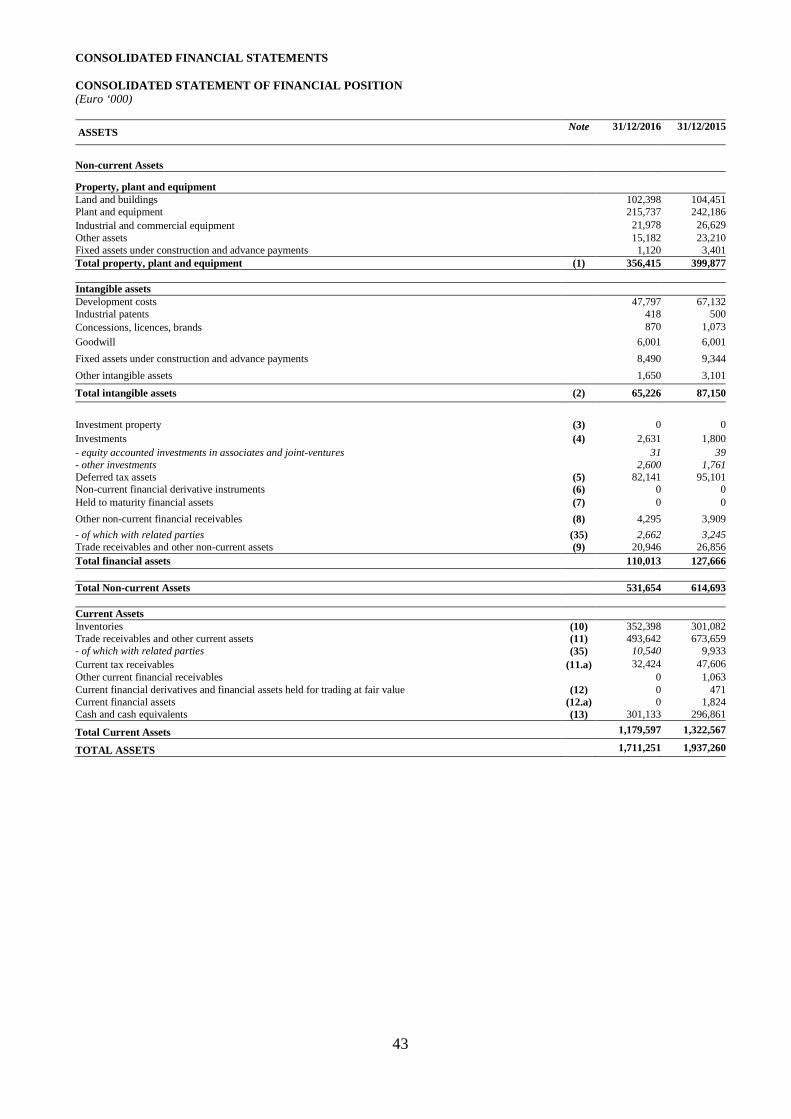

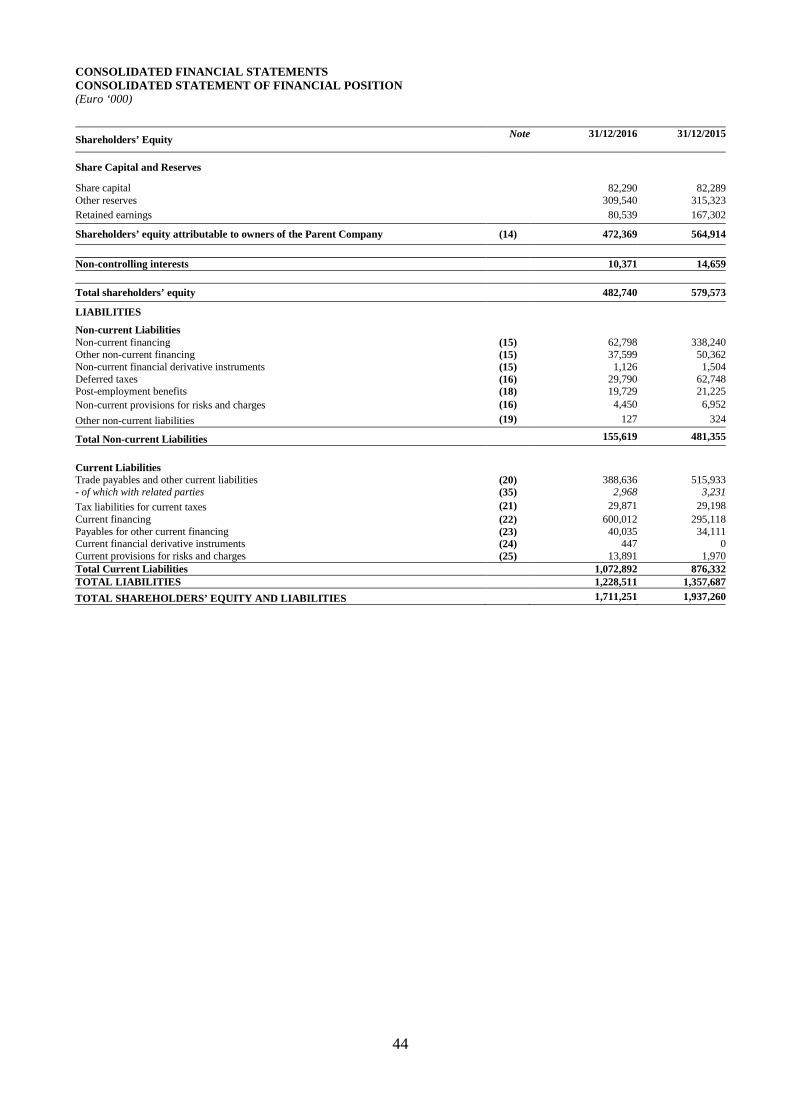

TREVI GROUP Consolidated Statement of Financial Position (Euro ‘000)

31/12/2016 31/12/2015 change %

A) Fixed Assets

- Property, plant and equipment 15 356,415 399,877 (43,463) - Intangible assets 65,226 87,150 (21,924) - Financial assets 16 6,926 5,709 1,218 428,567 492,736 (64,170) -13.0% B) Net working capital

- Inventories 500,567 522,736 (22,169) - Trade receivables 17 362,990 447,976 (84,986) - Trade payables (-)18 (260,586) (360,541) 99,955 - Advance payments (-)19 (141,465) (169,413) 27,949 - Other assets/ (liabilities)20 53,280 87,485 (34,205) 514,785 528,242 (13,457) -2.5% C) Invested capital less liabilities for the period (A+B) 943,352 1,020,978 (77,627) -7.6% D) Post-employment benefits (-) (19,729) (21,225) 1,495 -7.0% E) NET INVESTED CAPITAL (C+D) 923,622 999,753 (76,131) -7.6% Financed by:

F) Shareholders’ equity attributable to owners of the Parent Company 472,369 564,914 (92,546) -16.4% G) Net shareholders’ equity attributable to non-controlling interests 10,371 14,659 (4,288) H) Net debt21 440,882 420,180 20,703 4.9% I) TOTAL SOURCES OF FINANCING (F+G+H) 923,622 999,753 (76,131) -7.6% The Statement of Financial Position above, referred to in the Notes, is a restated summary of the Consolidated Statement of Financial Position. Reconciliation of the Restated Statement of Financial Position with the Consolidated Statement of Financial Position in compliance with IAS 11: (Euro ‘000) Net working capital 31/12/2015 IAS 11 31/12/2015 31/12/2016 IAS 11 31/12/2016 - Inventories 522,736 (221,653) 301,083 500,567 (148,169) 352,398 - Trade receivables 447,976 154,277 602,253 362,990 76,409 439,399 - Trade payables (-) (360,541) (360,541) (260,586) 0 (260,586) - Advance payments (-) (169,413) 96,063 (73,350) (141,465) 74,695 (66,770)

- Other assets (liabilities) 87,485 (28,688) 58,797 53,280 (2,936) 50,343 TOTAL 528,242 0 528,242 514,785 0 514,785

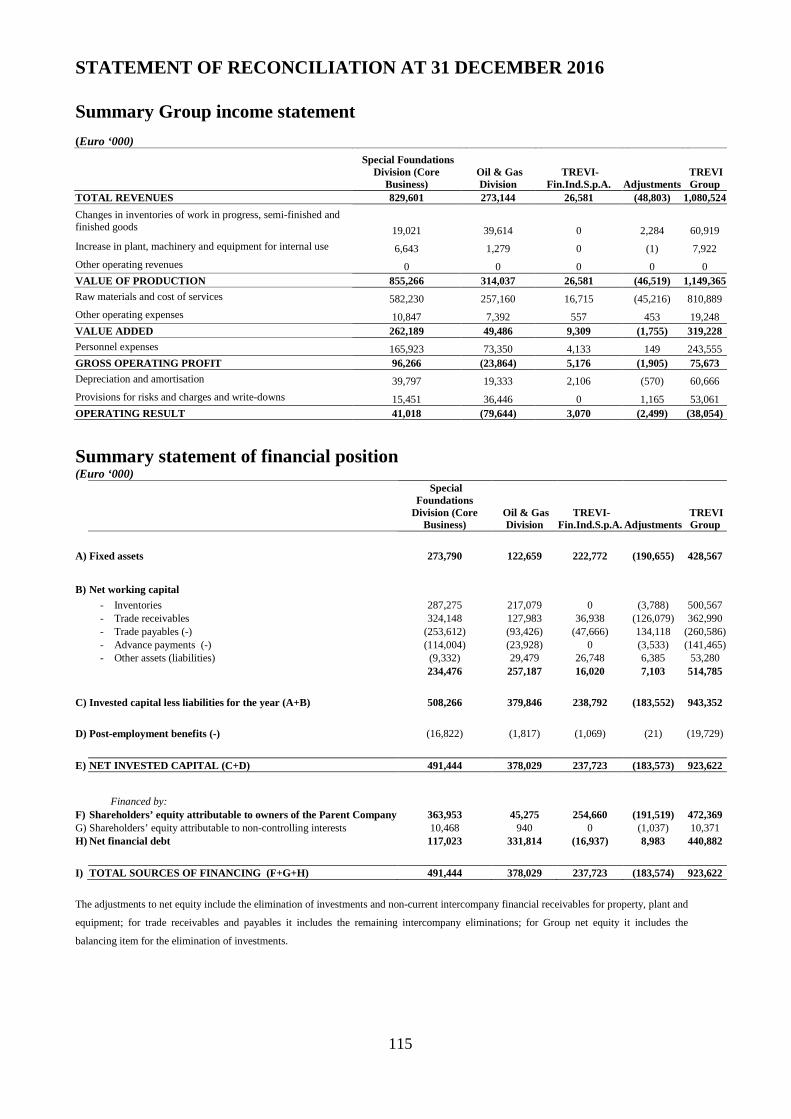

Net invested capital was approximately Euro 923.6 million, a decrease of Euro 76.1 million

compared to the figure at 31 December 2015. Net working capital was Euro 514.8 million (a

decrease of Euro 13.4 million compared to the figure for the previous financial year); inventories

were Euro 500.6 million, of which Euro 148.2 million was contract work in progress (in 2015

15 The entry for property, plant and equipment also includes investment property (Note 3). 16 The entry for financial assets includes investments (Note 4) and other non-current financial assets (Note 7).

17 Trade receivables includes: non-current (Note 9) and current (Note 11) trade receivables and current receivables from subsidiaries (Note 11). 18 Il saldo della voce debiti commerciali comprende: i debiti verso fornitori a breve termine (nota 20), i debiti verso collegate a breve termine (nota 20).

19 Trade payables includes: current payables to suppliers (Note 20), current payables to associates (Note 20).

20 Advance payments include both non-current advance payments (Note 20) and current advance payments (Note 20).

Other assets/ (liabilities) includes: other payables/ (receivables), accruals/ (advance payments), tax credits/ (payables), both non-current and current risk provisions (Notes 5-9-11-11a-16-19-20-21-25). 21 The net financial position, used as an indicator of financial indebtedness, is the sum of the following positive and negative entries in the Statement of Financial Position:

− current and non-current positive items: cash and cash equivalents (cash, bank accounts and bank assets); readily realizable investments in working capital, financial receivables;

− current and non-current negative items: bank debt, payables to other financial entities (leasing and factoring companies) and payables to shareholders for financing. Further details on this item are given in the relevant table in the Notes to the Accounts.

12

contract work in progress was Euro 221.6 million). Property, plant and equipment totalled Euro 428.5

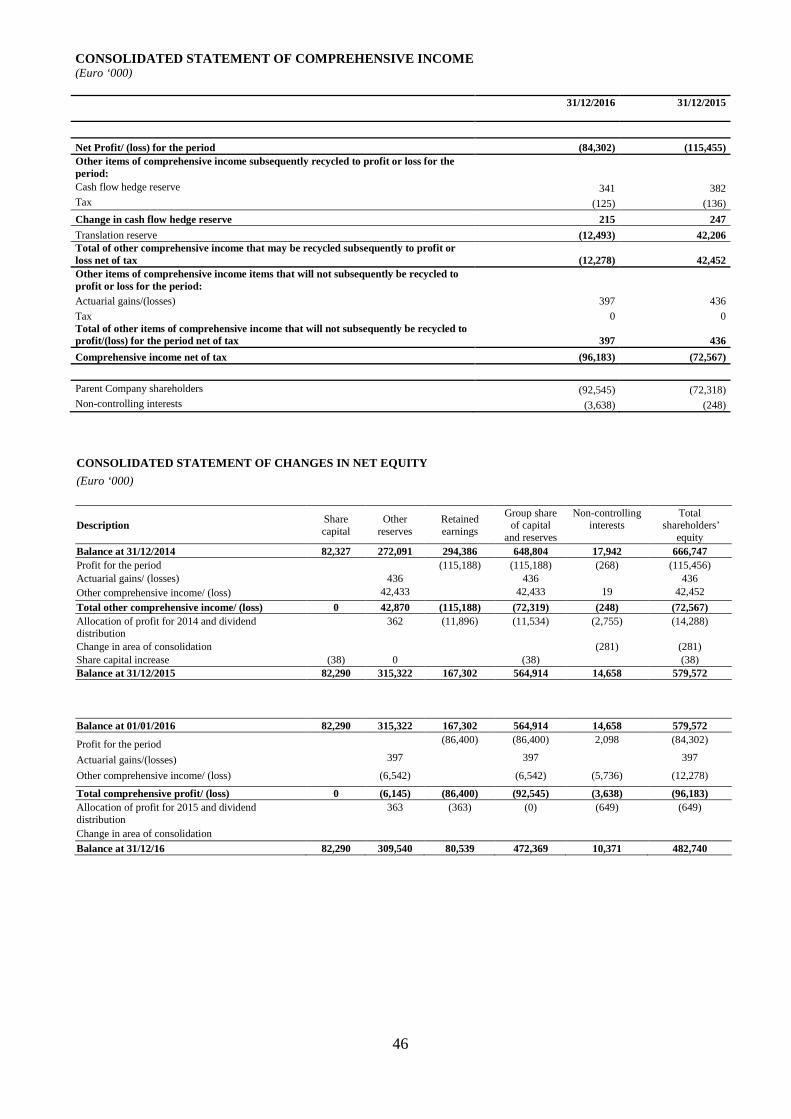

million (-13%). Group net equity decreased by approximately Euro 92.5 million (-16.4%).

The net loss generated by the Group contributed Euro 86.4 million to this figure and there was also a

negative impact from the decrease in the translation reserve (of approximately Euro 6.7 million),

primarily due to fluctuations in the US dollar (and of currencies linked to the US dollar, in particular

the currencies of the countries of the Arabian Gulf) against the Euro.

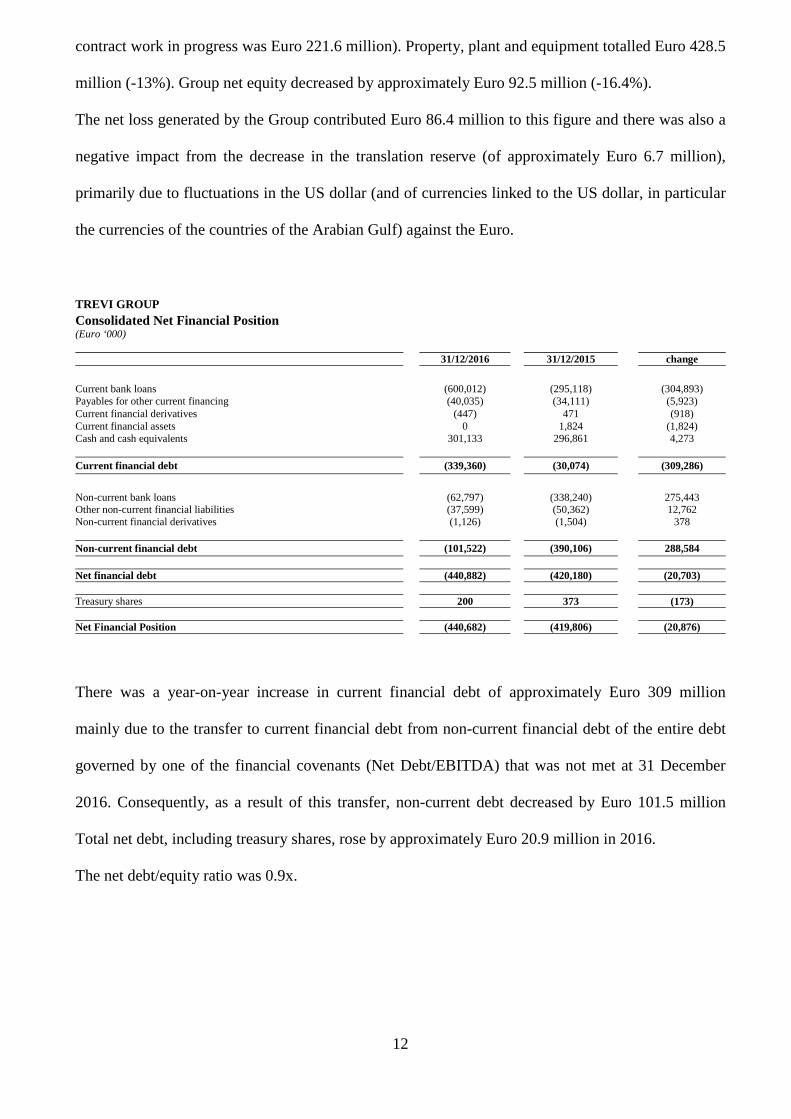

TREVI GROUP Consolidated Net Financial Position (Euro ‘000)

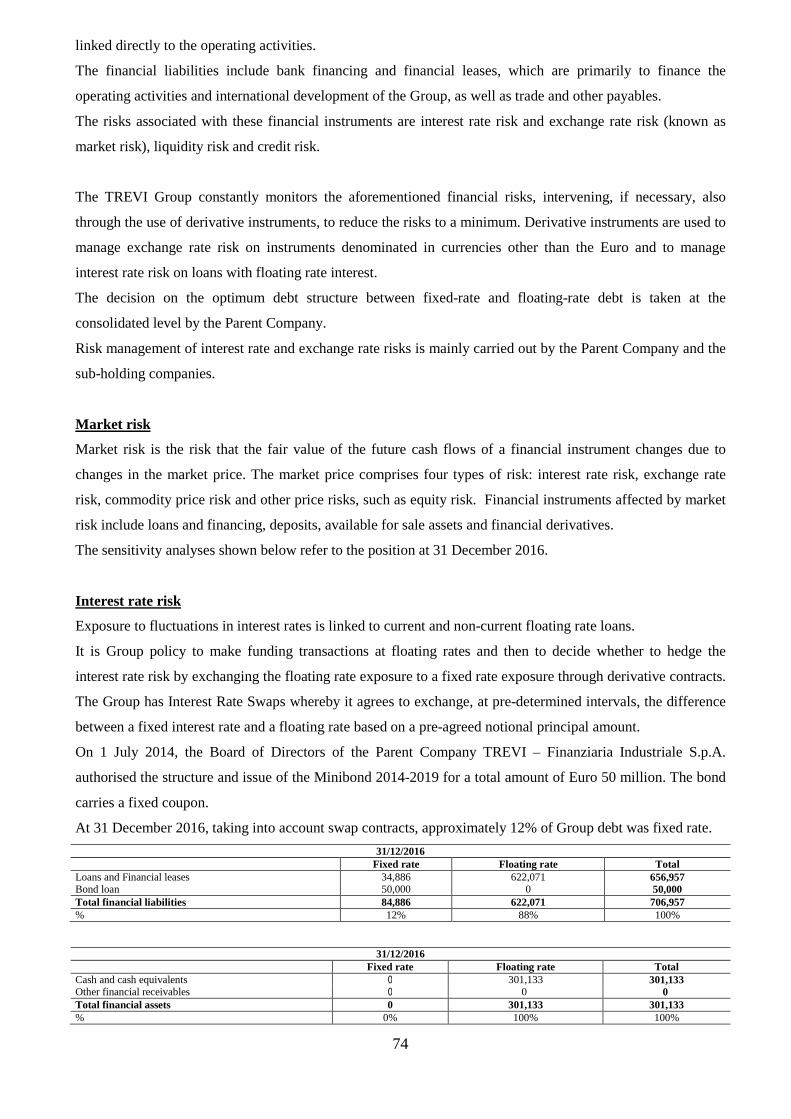

31/12/2016 31/12/2015 change

Current bank loans (600,012) (295,118) (304,893) Payables for other current financing (40,035) (34,111) (5,923) Current financial derivatives (447) 471 (918) Current financial assets 0 1,824 (1,824) Cash and cash equivalents 301,133 296,861 4,273

Current financial debt (339,360) (30,074) (309,286)

Non-current bank loans (62,797) (338,240) 275,443 Other non-current financial liabilities (37,599) (50,362) 12,762 Non-current financial derivatives (1,126) (1,504) 378 Non-current financial debt (101,522) (390,106) 288,584 Net financial debt (440,882) (420,180) (20,703) Treasury shares 200 373 (173) Net Financial Position (440,682) (419,806) (20,876)

There was a year-on-year increase in current financial debt of approximately Euro 309 million

mainly due to the transfer to current financial debt from non-current financial debt of the entire debt

governed by one of the financial covenants (Net Debt/EBITDA) that was not met at 31 December

2016. Consequently, as a result of this transfer, non-current debt decreased by Euro 101.5 million

Total net debt, including treasury shares, rose by approximately Euro 20.9 million in 2016.

The net debt/equity ratio was 0.9x.

13

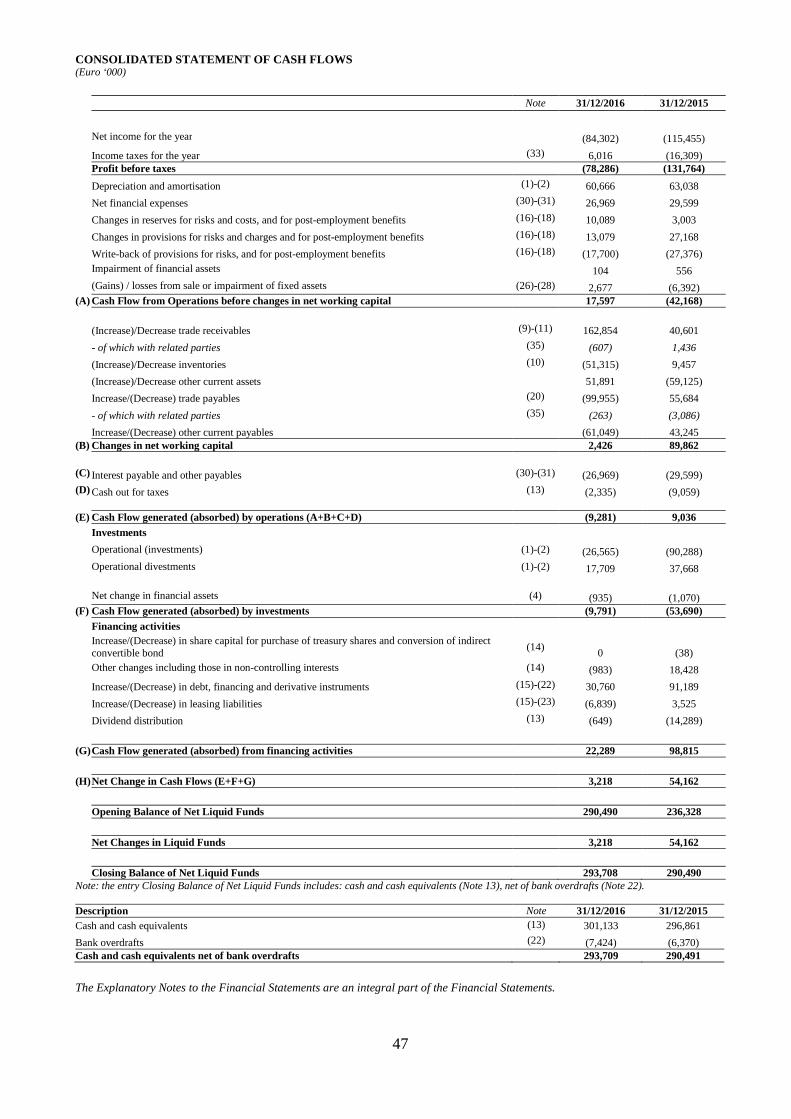

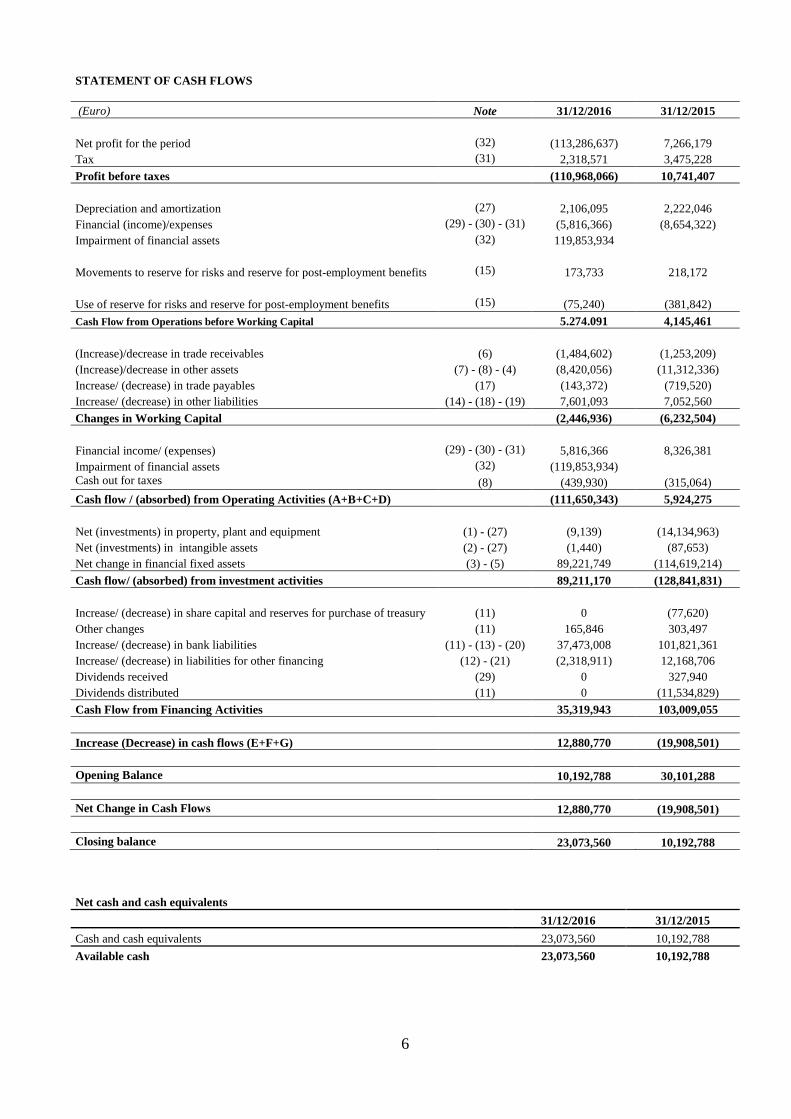

Free Cash Flow 22 was Euro 22.6 million (Euro 2 million in 2015) and was affected by Euro 13.4

million of changes in net working capital and by approximately Euro 7.4 million of investments in

tangible and intangible assets net of exchange rate translation effects.

Investments

Gross investments in property, plant and equipment by the TREVI Group were approximately Euro

33 million in the 2016 financial year and were for the acquisition of plant and machinery for the Oil

& Gas and Special Foundations Divisions.

The most significant investments were those made in the Middle East and Latin America.

Divestments totalled approximately Euro 18 million net of depreciation. Depreciation and

amortisation of property, plant and equipment totalled Euro 50 million. At 31 December 2016, the

net value of property, plant and equipment was Euro 356.4 million (approximately Euro 400 million

at 31 December 2015) including Euro 9.9 million of negative translation differences caused by the

difference between historic exchange rates and those prevailing at 31 December 2016.

Research and Development

The research and development efforts of Drillmec concentrated on bringing to market a range of

innovative products that focused on automation and also a range of accessories and services that

would generate considerably higher average profitability than that realised on the sale of single units

of plant and equipment.

The research and development activities of Drillmec in 2016 - in addition to executing orders

acquired - also had the following objectives:

1. To develop new MPD (managing pressure drilling) technologies and applications for HOD

(heart of drilling) in oil and geothermal drilling;

2. To review the range of mud pumps in order to reduce production costs and develop new

proprietary technologies, in particular for the FE mud pumps;

22 Free Cash Flow is not defined by the IFRS but has been used by the TREVI Group since the Consolidated Financial Statements at 31 December 2005;

it is a Statement of Financial Position indicator calculated by subtracting the taxes of the period, provisions, depreciation and amortisation, changes in

net working capital and gross investments for the period from the EBIT for the financial period.

14

3. To develop 4.0 software for resident technologies and for IoT (Internet of things) technologies

together with other Group companies;

4. To develop a 1500 HP package for shale gas.

As regards the first point, during the financial year under review several patents that had been

registered in periods prior to 2016 were granted and field tests were carried out.

As regards the second point, various technical and economic feasibility studies were carried out on

design concepts for pump products and new equipment for motopumps (electric and diesel) and

development started on a proprietary design for a rapid change FE mud pump so as to avoid

purchasing products from third parties, for example, the pumps manufactured by P-Quip and/or

South West.

As regards the third point, development of software to obtain and manage drilling data and for

maintenance that is linked to inventories of spare parts is at an advanced stage. The resident software

is called Rig Eye and is called DMS for the IoT part that has been developed for Cloud application.

The research and development activity of Soilmec in 2016 had the following objectives:

1. To manage, promote and protect the intellectual property and know-how of the company;

2. To analyse new technologies and carry out technical reviews of existing technologies;

3. To develop 2.0 electrical plant for the existing equipment range.

As regards the first point, several new patents were registered in 2016 that cover the technological

areas that are of major interest to the company. Several patents that had already been registered prior

to 2016 were granted during the year.

As regards the second point, several technical and economic feasibility studies were carried out on

new equipment and on highly innovative technical solutions.

15

SECTOR REVIEW

Parent Company performance

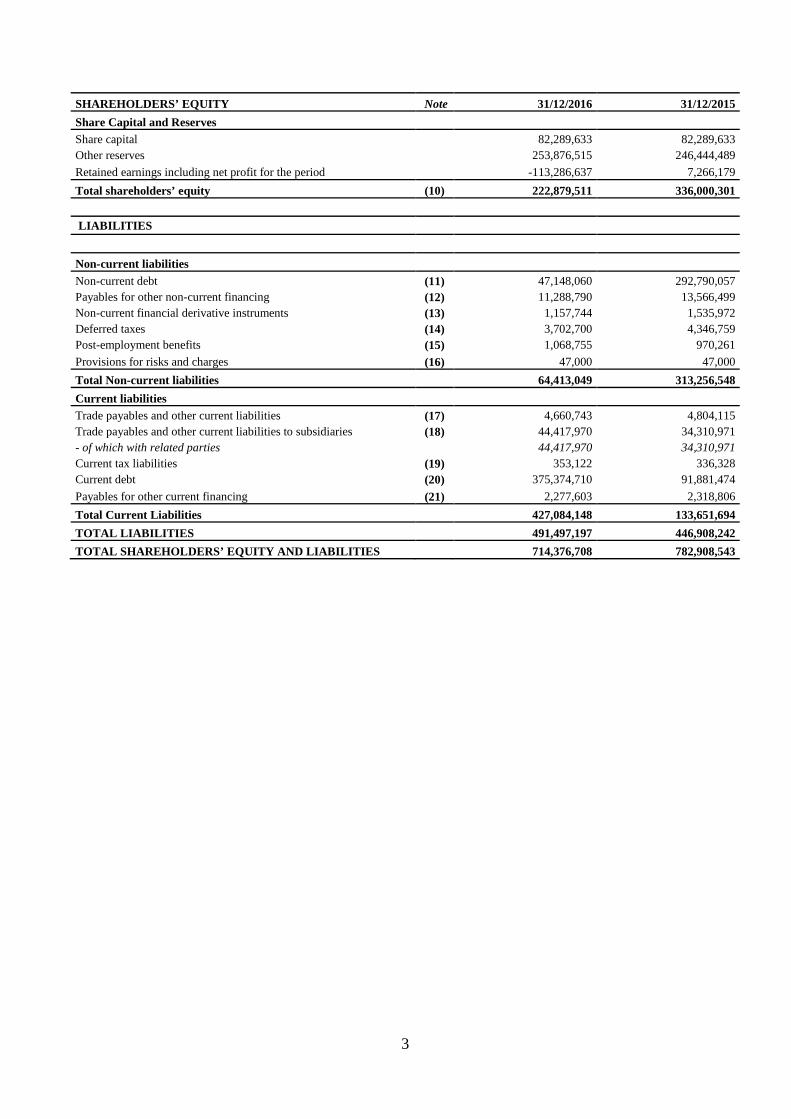

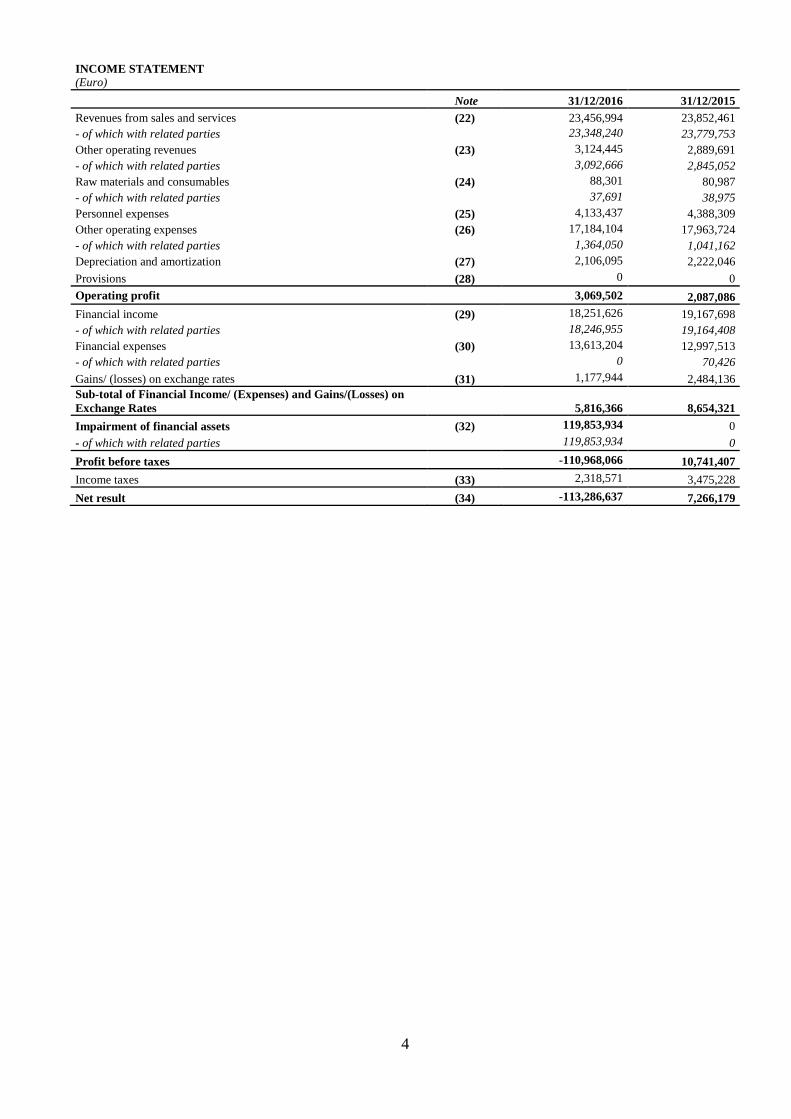

The 2016 Financial Statements, prepared by the Parent Company in accordance with IAS/IFRS

accounting standards, showed revenues from sales and services of Euro 23.457 million (a decrease

of Euro 0.395 million compared to the figure of Euro 23.852 million in the previous financial year);

other revenues of Euro 3.124 million (an increase of Euro 0.235 million compared to the figure of

Euro 2.890 million in the preceding year); financial income of Euro 18.252 million (a decrease of

Euro 0.916 million compared to the figure of Euro 19.168 million in the preceding year); and

impairment losses on financial assets of Euro 119.854 million. The net loss for the year was Euro

113.287 million (a decrease of Euro 120.553 million compared to the net profit of Euro 7.266

million in the 2015 financial year) and mainly impairment charges on financial assets as detailed

below in this Report.

In addition to plant and equipment hire, the activities carried out by the Parent Company on behalf

of subsidiaries included planning, research and development, operational and administrative

management support, human resources and personnel services, IT services and corporate integrated

management software, management of Group communications, investment management and

financing agreements with subsidiaries.

In the 2016 financial year, there was no income from subsidiaries (Euro 0.328 million in 2015) and

there was a decrease in interest on loans given by the Company to subsidiaries (Euro 18.247 million

in the 2016 financial year compared to Euro 18.836 million in 2015); loans to subsidiaries carry

interest rates in line with market rates.

Net exchange rate gains in 2016 were Euro 1.178 million compared to Euro 2.484 million in the

previous financial year. The exchange rate gains were mainly unrealised gains and it was therefore

decided to make a provision, in compliance with the accounting standards and enacted law, net of the

provision made in the previous financial year, to a reserve that cannot be distributed until the gains

are realised, as described in the Report on Operations.

16

There was also a decrease in the total tax payable by the Company; the loss pre-tax of Euro 110.97

million in 2016 compared to a profit pre-tax of Euro 10.74 million in the previous financial year.

There were no significant investments in property, plant and equipment in the financial period under

review.

During 2016, the Company made advance payments of Euro 45.000 million for a share capital

increase of Drillmec S.p.A. and of Euro 100 million for Trevi Energy S.p.A. However, in the last

quarter of 2016, the Company generated impairment losses by adjusting the carrying value of

financial assets to its share of the accounting net equity of these investments. The new value was

considered to be the fair value of these investments given their future outlook as incorporated in the

2017-2021 Group Business Plan approved by the Board of Directors of TREVI- Finanziaria

Industriale S.p.A. on 3 March 2017. The aforementioned value adjustments were: i) Euro 111.781

million for Drillmec S.p.A. and ii) Euro 8.073 million for Trevi Energy S.p.A. for a total of Euro

119.854 million (the difference between the historic costs of the investments and the net carrying

value of the percentage of net equity held in each subsidiary).

The Extraordinary Shareholders’ Meeting of 13 May 2016 approved the amendments to Article 25 of

the Articles of Association (composition of the administrative body) that increased the maximum

number of members of the Board of Directors from eleven to thirteen.

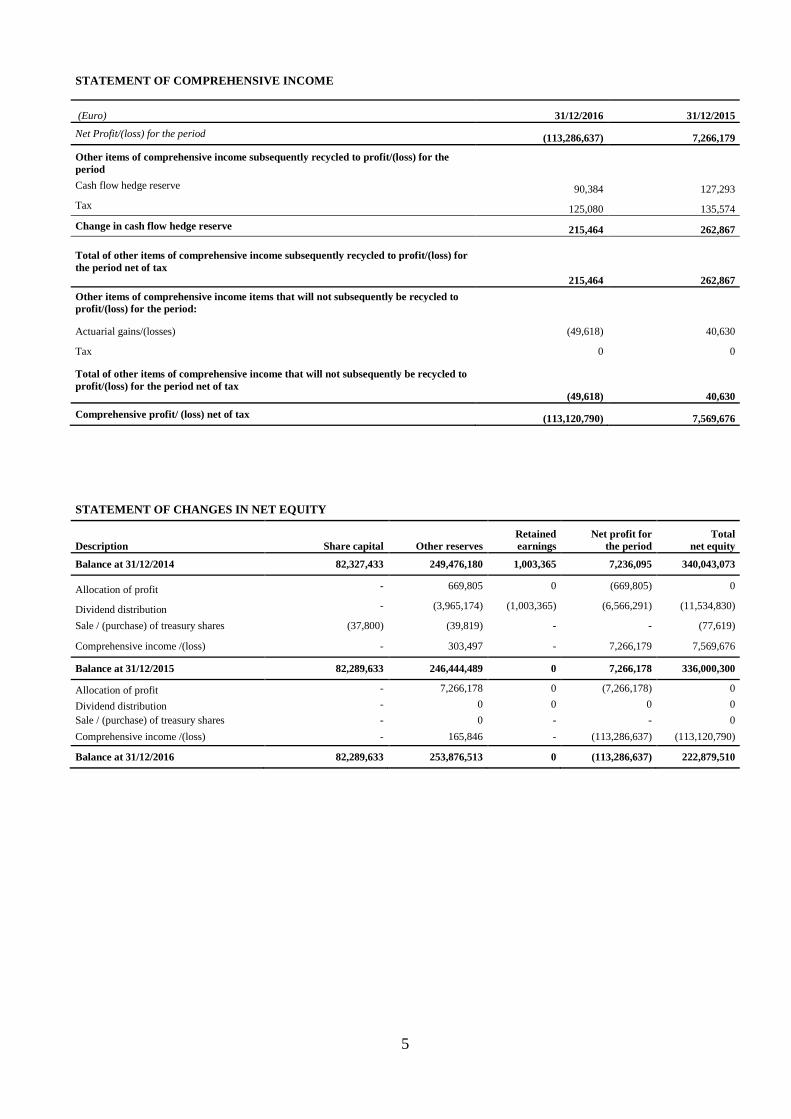

The Shareholders’ Meeting of 13 May 2016 also approved the allocation of the entire profit for the

2015 financial year to reserves and the proposal that there been no dividend distributed. The profit

was allocated as follows:

• 5% or Euro 363,309 to the legal reserve;

• Euro 4,033,228 to the translation reserve to ensure that this reserve covered unrealised gains on

exchange rates;

• Euro 2,869,642 to the extraordinary reserve.

The same Shareholders’ Meeting of 13 May 2016 also:

• approved the proposal of the Board of Directors that the plan to purchase and sell up to a

17

maximum of 2,500,000 treasury shares be extended. This authority was not exercised in 2016;

• appointed Marta Dassù to the Board of Directors, pursuant to Article 2386 of the Italian Civil

Code, until the approval of the Financial Statements at 31 December 2017;

• approved maintaining the current composition of the Board of Directors with eleven Directors

and postponing to a future occasion any decision to increase the number of members of the

Board of Directors to more than eleven Directors;

• approved the appointment of the Board of Statutory Auditors for the 2016 – 2017 – 2018

financial years and their members: Milena Motta (Chairperson), Adolfo Leonardi and Giancarlo

Poletti (Standing Statutory Auditors), Marta Maggi and Stefano Leardini (Supplementary

Statutory Auditors); it also approved remuneration of Euro 40,000 for the Chairperson and Euro

30,000 for each of the Standing Statutory Auditors;

• approved, pursuant to and in compliance with Article 114-bis of the Consolidated Finance Act,

and agreed the reasons for adopting a share incentive scheme to be called the “2016 Stock Grant

Plan” for certain employees and executives with specific responsibilities in the Company and its

subsidiaries. Under the Plan a maximum of 500,000 shares of the Company would be allocated

under the terms, conditions and activation mechanisms described in the information document

attached to the Report of the Board of Directors. Given approval of this proposal, the Board of

Directors meeting on 29 July 2016 decided to allocate free of charge a total of 444,841 rights to a

similar number of shares in the Company under the terms and conditions of the 2016 Stock

Grant Plan; the beneficiaries were permanent employees and executives with specific roles

within the Company and its subsidiaries in accordance with Article 2359 of the Italian Civil

Code.

As regards the memorandum accounts, it should be noted that guarantees given to credit institutions

for non-current loans and for commercial guarantees received are centralised in the Parent Company

and totalled Euro 618.513 million at 31 December 2016, compared to Euro 505.493 million at 31

December 2015, an increase of Euro 113.020 million due to the use of non-current credit lines by

some of the subsidiaries.

18

Guarantees given to insurance companies totalled Euro 15.163 million at 31 December 2016,

compared to Euro 37.501 million in the previous financial year, a decrease of Euro 22.337 million;

these guarantees are reduced in proportion to the amount of work still outstanding and are primarily

given for projects in the USA.

The Explanatory Notes to the Financial Statements of TREVI - Finanziaria Industriale S.p.A.

provide detailed information on individual entries in the Financial Statements.

The table at the end of this section provides a reconciliation of the results for the period and the net

equity of the Group with the figures of the Parent Company (DEM/6064293 of 28 July 2006).

Further details regarding the composition of the Board of Directors and the Board of Statutory

Auditors is given in other sections of these Financial Statements and in the Report on Corporate

Governance.

It should also be noted that in 2016 and in 2017, prior to the approval of the present Report, the

organisation and management of the Company was strengthened and details of this are given in the

Report on Corporate Governance and Ownership Structure; specifically, a Risk Management

department was set up and the new role of Central Director was created. This office is held by Mr

Marco Andreasi.

Lastly, given the negative performance of the Oil & Gas Division, which had a material effect on the

Consolidated Financial Statements and the economic and financial figures for the second semester

2016 and for the full-year 2016, meant that the Company was unable to respect one of the financial

covenants based on the consolidated figures at 31 December 2016 in the loan agreements (the Net

Debt/ EBITDA ratio) and two of the financial covenants in the terms and conditions of the Euro 50

million bond loan (the Net Debt/ EBITDA ratio and the EBITDA/ Net financial costs ratio); further

information on this subject is provided in the section on General Presentation Criteria in the Notes to

the Accounts.

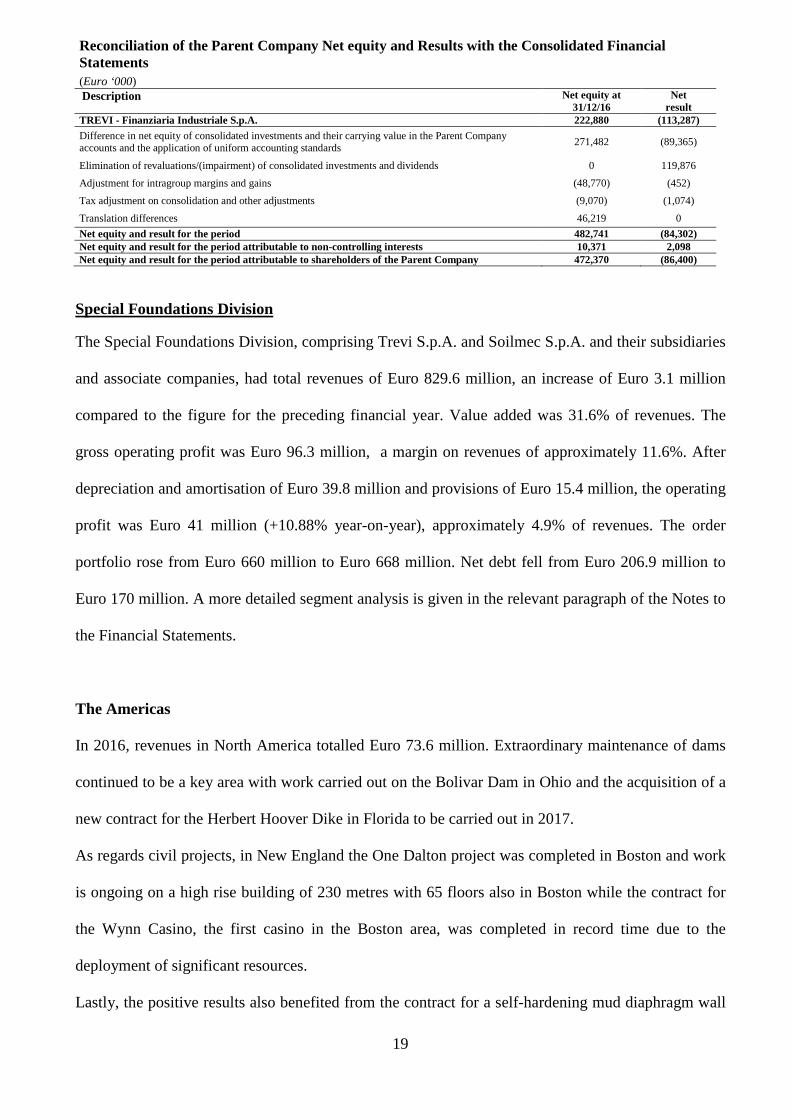

The table below gives the reconciliation of Parent Company net equity and results with the

consolidated net equity and results:

19

Reconciliation of the Parent Company Net equity and Results with the Consolidated Financial Statements (Euro ‘000) Description Net equity at

31/12/16 Net

result TREVI - Finanziaria Industriale S.p.A. 222,880 (113,287)

Difference in net equity of consolidated investments and their carrying value in the Parent Company accounts and the application of uniform accounting standards

271,482 (89,365)

Elimination of revaluations/(impairment) of consolidated investments and dividends 0 119,876

Adjustment for intragroup margins and gains (48,770) (452)

Tax adjustment on consolidation and other adjustments (9,070) (1,074)

Translation differences 46,219 0

Net equity and result for the period 482,741 (84,302) Net equity and result for the period attributable to non-controlling interests 10,371 2,098 Net equity and result for the period attributable to shareholders of the Parent Company 472,370 (86,400)

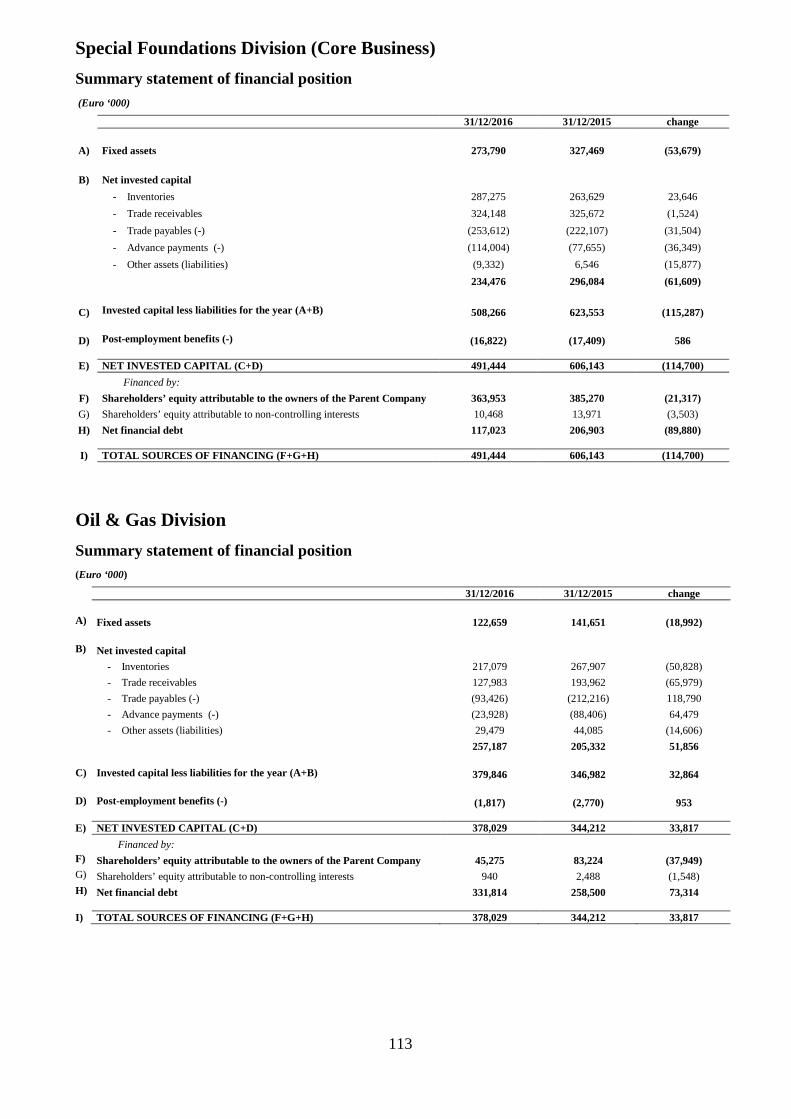

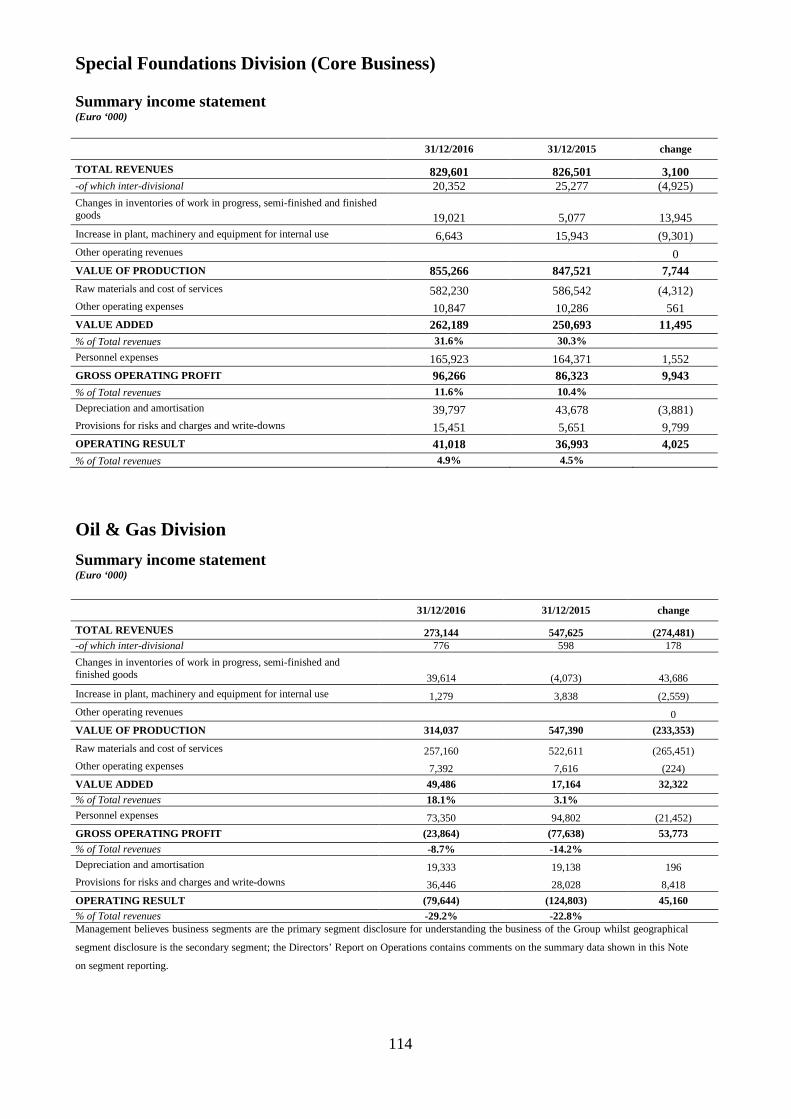

Special Foundations Division

The Special Foundations Division, comprising Trevi S.p.A. and Soilmec S.p.A. and their subsidiaries

and associate companies, had total revenues of Euro 829.6 million, an increase of Euro 3.1 million

compared to the figure for the preceding financial year. Value added was 31.6% of revenues. The

gross operating profit was Euro 96.3 million, a margin on revenues of approximately 11.6%. After

depreciation and amortisation of Euro 39.8 million and provisions of Euro 15.4 million, the operating

profit was Euro 41 million (+10.88% year-on-year), approximately 4.9% of revenues. The order

portfolio rose from Euro 660 million to Euro 668 million. Net debt fell from Euro 206.9 million to

Euro 170 million. A more detailed segment analysis is given in the relevant paragraph of the Notes to

the Financial Statements.

The Americas

In 2016, revenues in North America totalled Euro 73.6 million. Extraordinary maintenance of dams

continued to be a key area with work carried out on the Bolivar Dam in Ohio and the acquisition of a

new contract for the Herbert Hoover Dike in Florida to be carried out in 2017.

As regards civil projects, in New England the One Dalton project was completed in Boston and work

is ongoing on a high rise building of 230 metres with 65 floors also in Boston while the contract for

the Wynn Casino, the first casino in the Boston area, was completed in record time due to the

deployment of significant resources.

Lastly, the positive results also benefited from the contract for a self-hardening mud diaphragm wall

20

on the Lower Wood River in Illinois; this work involved constructing plastic diaphragm walls to

stabilise and impermeabilise faults along the banks of the Mississippi River and Wood River Creek.

The order backlog at the end of the financial year was sufficient to cover most of 2017 while the

current marketing initiatives and the policies of the new US administration give cause for hope that

new contracts will be received.

In Latin America, the Trevi division executed contracts in Argentina, Venezuela, Colombia and

Panama for a total of approximately Euro 61.2 million. In Argentina, two contracts covering Lots 1

and Lot 3 of an environmental project in Buenos Aires (the Riachuelo hydraulic reclamation project)

are in their final phases.

During the financial year under review, contracts were also won and are now being executed for

harbour infrastructure along the Paranà River and on the Atlantic coast for the major cereals

exporters in Argentina. Work was completed on the Rosario electricity generating plant and on

electric cable infrastructure in the province of Chaco.

In Panama, the Trevi division was involved in the final phases of the consolidation and foundation

work for the Tercer Juego de Esclusas of the new Panama Canal, which was inaugurated last year. It

is also constructing special foundations for Line 2 of the Metro and for Port Rodman on the Pacific

Ocean end of the canal.

In Colombia the two main projects underway are the Pedregal Business Center in Bogota and the

foundations for the Pumarejo Bridge at Barranquilla on the River Magdalena on behalf of the Spanish

company, Sacyr. The latter contract is for foundations on sunken piles for the longest bridge in

Colombia (2.28 km). Work is also continuing on some important civil projects in Bogota that include

the Colmedica building and El Eden shopping centre.

Despite the difficult macroeconomic and political problems of Venezuela, work continued in oil

industry infrastructure with the expansion of the Puerto la Cruz refinery and on a high quality

residential project in Caracas.

Considerable marketing was carried out in Chile and Peru where some important contracts were

21

actively pursued and it is hoped these will be finalised in 2017.

Europe

Work was carried out in Norway on behalf of OHL on transport infrastructure. Marketing activity,

together with investments aimed at winning business in North and Central Europe, should result in

orders in 2017.

Italy

Although 2016 could be considered a very negative year for the construction sector in Italy, the

Division managed to carry out some important contracts.

In addition to the Oil Dock in the Port of Naples that was concluded with good technical results at the

start of this year, it is worth noting the contract to repair the Lungarno Torreggiani in Florence, which

demonstrated the commitment, dedication, know-how and ability of the Division to carry out

complex works in a very short amount of time. It won recognition not just from the public authorities

but from the citizens affected by the works.

Work also continued on the dry dock for ships of up to 150,000 deadweight tonnage (dwt) in the Port

of Palermo whilst some medium-size contracts, for example, that for the new production facility of

Orogel in Cesena and the Immacolatella pier in the Port of Naples, were completed.

A positive note is provided by the size of the order portfolio, which, in addition to the contracts that

have been completed and are mentioned above, includes the contract for the Pagliari pier in the Port

of La Spezia, the work on the high speed railway hub in Florence and other contracts acquired at the

end of the 2016 financial year, for example, that with Syndial in Malcontenta Porto Marghera and

that with the Tiliaventum consortium on the Tagliamento River in Friuli Venezia Giulia.

Africa

The Trevi division had 2016 revenues of approximately Euro 109 million in Africa.

In Nigeria, an important contract for a fertiliser plant for Dangote, a leading local company, was

completed. Moreover, despite the crisis engulfing the country, activity continued on residential,

22

commercial and hotel construction and in structures and support work for the oil industry (the dock

works at Port Harcourt).

In Algeria, the Group continued to be active in several sectors in 2016. The most important was the

infrastructure work on the metro system. The Group has been the undisputed leader in this sector in

Algeria since 2004 and has worked on all the main lines. In 2015 it won contracts for all the

foundation work on the “MC1 Ain Naja – Baraky” and the “MC2 El Harrach – Aéreoport” stretches

of the network that are still being carried out.

These two stretches cover almost 12 km and will have 11 stations, 13 ventilation shafts, and one

viaduct. The work, which began in 2015 and will continue until 2019, is expected to generate strong

revenues and profitability.

Work also continued on the motorway network in Algeria (the Tizi Ouzou motorway and the East-

West motorway).

In Egypt work progressed on the support works for the motorway tunnels under the Suez Canal.

The Trevi Division was also active in Mozambique where it carried out requalification work on dams

and also drilled water wells.

Middle East, Asia and Oceania

The Trevi division generated revenues of approximately Euro 284 million in the Middle East in 2016.

In the United Arab Emirates, work began on the special foundations for a high rise building designed

by Foster + Partners and called ICD Brookfield Place that is one of the most important property

projects currently under construction in Dubai. In addition to this contract, there are also those in the

Arabian Gulf for the Tiara United Towers, Mediclinic Hospital and two high rise buildings in Muscat

in Oman.

Moreover, in the financial year under review, a government contract was acquired for a property

development in Abu Dhabi: the contract, won in consortium with a European company, involves

geological studies and the treatment and improvements to the solidity of the ground. Work began in

2016 and will continue throughout 2017.

23

This project is in addition to other contracts in the United Arab Emirates and in Kuwait, Qatar and

Oman in the sectors of motorway networks, maritime infrastructure, underground systems and

commercial buildings.

In Saudi Arabia, work is ongoing on the foundations of several stretches of the Riyadh metro system.

In the Philippines, the special foundations of a 14 kilometre, six-lane, urban motorway in Metro

Manila were constructed.

In Turkey, the Division is laying the special foundations for the Galata Cruise Terminal, a modern

complex for commercial activity that includes residential property and a luxury hotel, which will be

part of the tourist facilities on the Bosphorus. The Port of Istanbul (known as the Galata Port) is a

passenger terminal for cruise ships that stretches from the Galata Bridge on the Golden Horn to the

Salipazari quarter on the European side of the Bosphorus passing through the Karaköy district.

In 2016, the Division won the important repair contract for the Mosul Dam as was widely reported in

the national and international media.

The contract worth Euro 273 million is under the auspices of the Iraqi Ministry of Water Resources

(MoWR). Personnel and resources were immediately mobilised as this significant project requires

intense drilling and injecting of concrete mixes to consolidate the foundations of the dam, as well as

repair and maintenance of the bottom spillway galleries that have been damaged. The initial

mobilisation will include specialist training courses for technicians and local personnel in the use of

Soilmec drilling equipment.

The presence of an Italian military contingent and local security forces will guarantee the safety of

the over 450 technicians and personnel of Trevi. The work will be ongoing throughout 2017.

The Division also carried out contracts in New Zealand and won a contract in Australia for the metro

connecting Perth to the airport; this latter contract is the first that the Division has done in Australia

and should open up interesting growth opportunities in the local market.

Soilmec Division

2016 proved a highly successful year for Soilmec. Despite the slight fall in total revenues (-5% year-

24

on-year), strong revenues were generated in Asia and the Far East due to the subsidiaries in China,

Japan and Australia. In Europe, there were excellent results from the UK branch whilst revenues in

France experienced a slight decrease year-on-year. The results obtained in the Middle East in 2015

were consolidated. There was a small decrease in revenues from Egypt that was compensated by the

performance in the Turkish and Gulf markets. However, the US branches failed to build on their

performance in 2015. The strong focus on variable costs with a reduction in costs and an increase in

production efficiency resulted in a significant improvement in operating profitability compared to the

2015 financial year. Net debt was substantially unchanged compared to the previous financial year.

Oil & Gas Division

This division had 2016 revenues of Euro 273.1 million compared to Euro 547.6 million in the

previous financial year, a year-on-year decrease of 50%.

It had a gross operating loss of Euro 23.9 million compared to a gross operating loss of Euro 77.6

million in the previous financial year. The operating loss was Euro 79.6 million (an operating loss of

Euro 124 million in 2015) and net debt increased by approximately Euro 73 million to Euro 331.8

million. The order portfolio was substantially unchanged at Euro 290 million.

Drillmec Division

Drillmec had total revenues of approximately Euro 158.6 million in 2016 compared to Euro 403.5

million in the preceding financial year (-60.7%).

In 2016, the company continued to work on the contracts acquired in Algeria, Taiwan and India. The

persistent low oil price penalised revenues, which came in lower than those of the budget. The

decrease in revenues, combined with profitability that struggled to reach forecast levels, also

reflected strong competitive pressure.

In 2016, the Division continued to research and introduce new product lines, components and

specialist services that should help support and improve future profitability even on lower volume

sales.

25

Although no radical change is expected in the performance of the Oil & Gas market, there were some

encouraging signals from order inflows in the last part of 2016 and the first months of 2017.

There has been growing demand for on-shore plant and equipment in the USA, Argentina, the Middle

East, Russia and North Africa. A contract was signed in Tunisia to supply one HH102 and one G75

rig for geo-resource research, which should be followed by a contract to supply a third G75 plant.

There are also strong prospects that the Tunisian market will take one of two 2000 HP plants for deep

well drilling. In Russia, the increased interest in Drillmec’s Top Drive product range was confirmed

when a third contract was signed to supply three HTD250 drills in addition to the previous two

supplied, which brings to six the TDs under contract. This could lead to interesting developments in

this market that is considered strategic in the near future. The Divisions’s leadership position in this

market for workover equipment and rigs is confirmed by the over Euro 10 million of contracts

currently underway. A contract was signed in Oman to supply a sixth MR6000WO plant in addition

to the five already supplied. Lastly, an important contract was won in Bolivia to supply three

complete 2000 – 3000HP land rigs, which is the largest on-shore contract signed in recent times by

the Division. In the off-shore sector, the strong relationship with a client in Uzbekistan could lead to

an interesting contract with an international client for the potential supply of a modular package,

similar to that supplied in Mexico, to be used in the Caspian Sea. The negotiations are at an early

stage but Drillmec’s technical proposal has met with significant interest from the client and could

lead in the near future to a request for a quote. In Indonesia, there was a positive conclusion to an

important contract for an off-shore workover rig with a value of USD 21 million; this contract was

won from the same client who postponed until 2018 a contract signed in 2016 for an off-shore drill

rig. Lastly, an engineering report was completed for a client in Argentina who wants to agree a

purchase contract for an HH55 off-shore rig worth approximately USD 30 million in the near future.

The recently created Services Business Unit is demonstrating the validity of this strategy and is

signing the first certification and refurbishing contracts in various parts of the Middle East and North

Africa, as well as increasing its training services. The revenues of the first quarter 2017 and the order

portfolio (approximately Euro 10 million) make it probable that the target revenues of Euro 25-30

26

million in the services sector for the whole of 2017 will be met. Much will depend on signing

agreements with companies for the maintenance of plant and equipment they already own.

There are also interesting developments involving a client in Oman that have resulted in a contract

worth approximately Euro 1.3 million to supply pumps and services to several local companies. This

region, where there are more than 30 rigs built by Drillmec in the recent past, offers interesting

prospects of work on equipment with periodic certification that is expiring and which requires

extraordinary maintenance.

The continuous HoD (Heart of Drilling – continuous circulation system) for oil wells met with

significant technical success in the trials carried out with Shell. However, the contractual strength of

the leading companies (Schlumberger, WDI, Halliburton, Nabors, etc.) in this sector has required a

review of the strategy and led towards a diversified business model. There are some interesting

contacts with a leading Oil & Gas services company that may bear fruit in the 2017 financial year.

The 2016 order portfolio only partly covers the budget revenues for 2017. However, it is hoped that

some of the contracts where negotiations are well advanced will be signed to give continuity to the

production commitment and ensure that the revenues in the budget are met.

Petreven

The 2016 macroeconomic environment continued to be negative. The oil price, having reached a low

for the last thirteen years of less that USD 30 per barrel in the first months of 2016, continued to be

weakened by structural imbalances in the market aggravated by over supply and by uncertainties for

growth in energy demand. To support prices and protect the oil industry, the Opec countries decided

to cut production. Opec also increased its forecast for demand maintaining that low prices would

mean higher consumption even though this was not supported by economic growth. The outlook

remains uncertain and any significant recovery is postponed to later this year or beyond.

The extended crisis, longer than had initially been expected, and the ongoing weakness of the oil

price resulted in a profound change in market conditions a sharp reduction in the main economic and

financial performance of the Division compared to previous years. This and the reduction in the

27

order portfolio, which nevertheless offers good visibility, continues to put pressure on margins and

results. The Division is attempting to regain profitability by using its competitive advantages: strong

relations with clients, an avant-garde fleet and a structured approach to project execution. A new

model for project risk management has been implemented, which, through an appropriate process for

risk identification, risk measurement, management and monitoring should lead to the division

meeting its pre-set targets.

Operating activities

The Division is currently operating in South America on behalf of the leading oil majors and national

oil companies. It has seventeen operational rigs in the following countries: eleven in Argentina, two

in Venezuela, one in Chile, two in Peru and one in Colombia. It is also using a rig belonging to a

third-party in Chile. The operating activities had an average rig capacity utilisation of 69% (74% in

2015) and 205 wells were drilled. Revenues fell 20% year-on-year. Argentina is the country that

generated most revenues with approximately USD 80 million (63% of revenues), followed by

Venezuela and Chile.

The order portfolio was USD 81 million and covers almost all the forecast revenues for 2017. New

orders acquired totalled USD 84 million.

Argentina

Argentina is the market that generates most revenues: 63% of revenues from this segment. Work was

carried out for the leading companies using eight rigs and one workover rig (two in the Santa Cruz

region, two in the Rio Gallego region and five in the Neuquen region). Contracts ended (one in May

and one in September) for two rigs operating in Argentina. Operations were marked by strong trade

union unrest that slowed drilling operations and put some plants into extended stand by. The average

capacity utilisation of the rigs was 82% (89% in 2015) and 150 wells were drilled.

Peru

Work in the Talara province was completed in May 2016 but restarted in August with the use of two

28

drill rigs on behalf of different companies. The average capacity utilisation of the rigs was 50% (68%

in 2015) and 35 wells were drilled.

Venezuela

In Venezuela, work continued with two drill rigs in the municipality of Maturin. The average

capacity utilisation of the rigs was 100% (the same as 2015) and 11 wells were drilled.

Chile

In Chile, geothermal drilling activity continued in the Antofagasta Region while that in the

Magallanes Region was completed and two drill rigs were subsequently transferred to Argentina.

The average capacity utilisation of the rigs was 41% (37% in 2015) and nine wells were drilled.

TREVI Energy S.p.A.

The establishment and growth of this company, active in the sector of renewable energy, reflects

TREVI Group’s desire to adapt some of the technologies already developed and tested in its special

foundations and drilling businesses to this sector and to develop new specific and innovative

technological systems for a sector that is expected to have strong future growth.

As part of the development of the wind energy sector, research and innovation has focused not just

on the off-shore sector but also the on-shore sector with feasibility studies for an on-shore plant in

Sardinia (Porto Torres) with nominal installed capacity of 36 MW.

In the financial year under review, in accordance with enacted law, the administrative process begun

in previous years continued in order to obtain specific authorisations (state concessions, single

European authorisation and environmental impact assessments (VIA)) to develop off-shore wind

farms in Southern Italy and on-shore wind farms in Sardinia.

This activity has concentrated on the following sites :

• Porto Torres (on-shore site): leases have been signed to rent land on which five wind turbines

will be installed with total generating capacity of 15 MW. The approval that was expected to

29

be given in the first half of 2016 was rejected by the Region of Sardinia and the sums

capitalised over the years were written down to zero.

• Chieuti (an off-shore site with total capacity of 150 MW) and Manfredonia (an off-shore site

with total capacity of 195 MW): following the refusal by the Prime Minister’s Office for the

requested authorisation on 14 February 2014, an appeal was launched in the Regional

Administrative Court (TAR) of Rome. Given the uncertain outcome of this process, since

2013 prudent provisions for future risks have been made for an amount equal to the sums

already invested in the project. The 2016 Financial Statements included a provision for future

risks that equalled the investments made in 2016.

• In 2016, the authorisation process began for two new off-shore wind farms. The first is

located near Lesina Marina (Foggia) and is for 60 wind turbines with total capacity of 198

MW. The second is near Margherita di Savoia and is for 50 wind turbines with total capacity

of 165 MW.

The project to produce a prototype 3 MW wind turbine has been completed and the Company is

awaiting developments on the above authorisations before moving to the next phase of the prototype

and then eventually to industrial manufacturing.

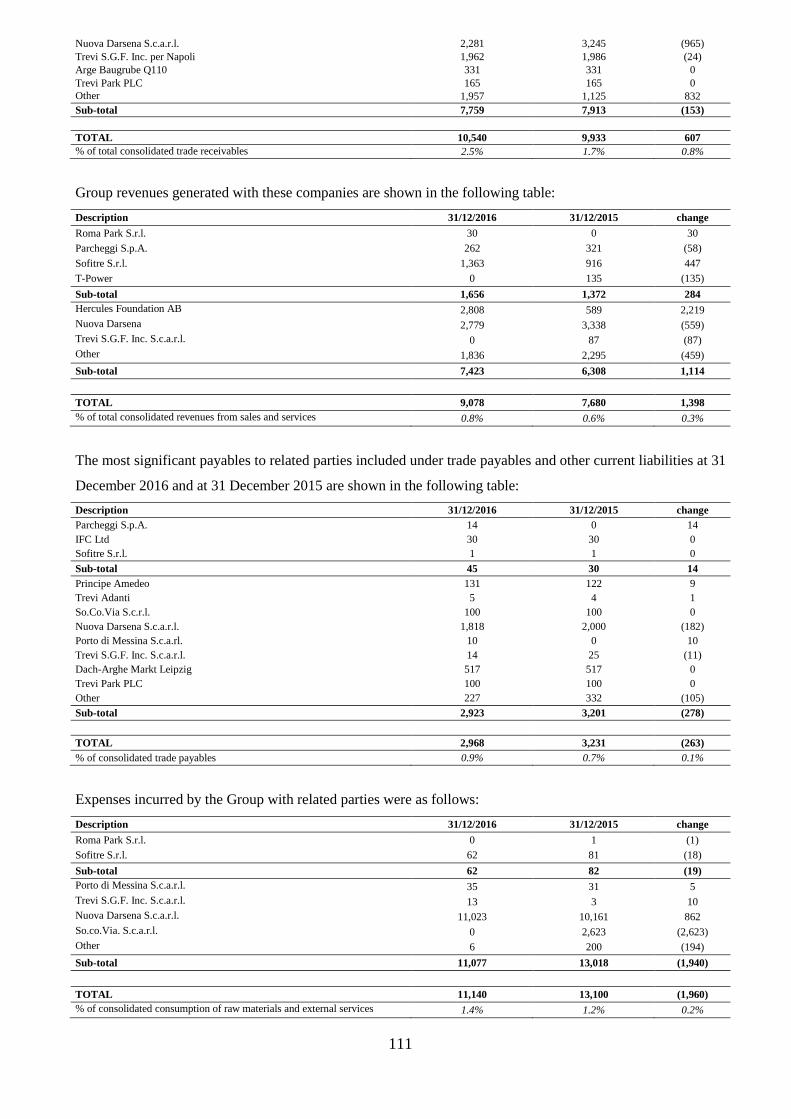

Group related-party transactions with non-consolidated subsidiaries, associates and controlling

companies, companies controlled by the latter and with other related parties

TREVI – Finanziaria Industriale S.p.A. has limited relations with Sofitre S.r.l. (see Note 35 of the

Notes to the Financial Statements), a company controlled 100% by the Trevisani family, and with the

companies it controls, which are mainly involved in the construction and management of car parks,

including T Power S.p.A., which is controlled by Trevi Holding SE. In the accounting period under

review, for the TREVI Group this relationship gave rise to revenues of Euro 1.656 million, costs of

Euro 0.062 million and, at 31 December 2016, receivables of Euro 2.781 million and payables of

Euro 0.045 million.

30

Transactions with related companies are done at normal market conditions. There are no financial or

capital relations with the parent company Trevi Holding SE and any relations with non-consolidated

subsidiaries and associate companies, described in Note 35 to the Consolidated Financial Statements,

are not material.

Risks and uncertainties

Exchange rate and interest rate risk

Due to its international structure, the Group is subject to market risks from exchange rate and interest

rate fluctuations. It has a policy for covering financial risks, which includes fixed term currency

contracts and financing and hedging in foreign currencies to cover expected cash flows at pre-

established rates. Detailed information on the transactions to hedge exchange rates and the valuation

criteria adopted for these is given in the Notes to the Financial Statements.

Credit risk

The sector and geographical diversification of the Group means that it has no significant

concentration of credit risk. Where possible, the Group demands suitable guarantees and sets up ad

hoc procedures for constant monitoring of trade receivables.

Liquidity risk The Group aims to maintain a balance between liquidity demand and supply using suitable bank

financing. In particular, the Group has signed long-term financing agreements aimed at covering its

investment programme and business development.

Risks pertaining to business activities abroad

The Group is exposed to the typical risks of doing business internationally; these include risks

pertaining to local political and economic instability and risks related to changes in the macro-

31

economic, fiscal and legislative environments. Identifying new initiatives for the Group in foreign

countries is always preceded by a careful appraisal of such risks, which are then constantly

monitored. It should be stressed that the activities of the Group are concentrated mainly in countries

covered by international insurance or where bilateral agreements exist between the Italian

government and the local government.

Use of estimates

The Special Foundations segment of the Group and the Drillmec division operate with contracts

where payment is determined at the time the contract is awarded. Any higher costs that the Group

incurs and/or suffers in executing these contracts must be met by the Group but may be recouped

from the client according to laws and/or terms and conditions contractually agreed. Consequently, the

margins made on such contracts may vary from the original estimates that were carefully made for

each contract based on the long-term experience the Group has acquired over the years with similar

contracts in both the Special Foundations and Oil & Gas sectors.

Risks pertaining to fluctuations in the cost of raw materials

Fluctuations, in some cases significant, in the costs of some raw materials can lead to an increase in

production costs, which, however, the Group tends to offset by a diversified supply policy,

framework agreements with strategic suppliers, and contractual clauses for revising prices. It should

also be mentioned that sales of drill rigs are subject to the investment policies of leading oil

nationals/private companies, which are themselves influenced by the trend in the oil price.

Personnel

32

The Group has always focused on personnel management; employee retention is encouraged by a

high degree of involvement, by remuneration and an incentive system, continuous and specific

training, the attention paid to the work environment and, for expatriate employees, a focus on the

living conditions not only of the employee but wherever possible of the entire family.

Given the business of the Group, personnel training is done through a dedicated structure called the

TREVI Academy, through “on the job” training and through specific training courses; the work

environment is free of conflict.

Further details are given in the Report on Remuneration, prepared in compliance with Article 123-ter

of Legislative Decree of 24 February 1998 no. 58 and available as required by enacted law at the

registered office of the Company, at Borsa Italiana S.p.A. and on the Company website

www.trevifin.com.

Environmental awareness and occupational health and safety

Environmental awareness and occupational health and safety have always been among the top

priorities of the Group. The Group constantly strives to maintain a safe work environment and to

provide personnel, according to their roles, with all the equipment necessary to avoid any risk or

danger to their persons. The Group production facilities, offices and operating systems adhere to the

required safety standards. The Group also acts in a way that preserves and protects the environment,

in compliance with existing environmental legislation, as well as the rules and procedures that the

Group itself has prepared. Lastly, security systems are used to guard Company property and, in

particular, all forms of inventory.

Corporate Social Responsibility

The TREVI Group considers sustainability to be an integral part of its business as it represents a

guarantee of long-term growth and value creation through the effective involvement of all

stakeholders.

33

In order to adhere to the Principles of Sustainability, the TREVI Group has chosen to adopt a

Corporate Social Responsibility programme that is continually updated, monitored and agreed on by

persons of all levels of responsibility.

The nature, type and complexity of the Group businesses have always necessitated a particular focus

on the environmental and social aspects of executing a project.

Furthermore, the profile of the countries and regions in which the Group operates means it has

always had a distinctive approach to sustainability in order to contribute to the socio-economic

development of the regions in which it is present through an effective strategy of local content that

focuses mainly on local employment.

There are numerous examples of collaborations and joint ventures in which the Group is involved

that demonstrate its exceptional adaptability to various local cultures and its considerable skill in

project managing important contracts.

Another strong point of the Group regarding local content is the ever-increasing diversity of its

employees – a pool of young talent from a multitude of countries whose professionalism grows with

that of TREVI on the various projects in which they are involved, either in their own countries or

abroad, and wherever there are support structures like engineering and logistics centres for

warehousing of construction and worksite equipment.

The call to behave responsibly and with integrity, contained in the Code of Ethics, and the reference

to value creation is embedded in the corporate mission statement: "The mission of the TREVI Group

is to design, manufacture and offer innovative technologies and services for all types of foundations

engineering projects".

The Social Responsibility model adopted and which guides the Company policies reflects these

principles and may be described as follows:

• Provide accurate and transparent reports to stakeholders not only on the financial performance

but also on the social, cultural and environmental results of the Company’s activities.

34

• Contribute to the development of communities in which it is present through investments in

cultural, sporting, educational and social initiatives.

• Devote increasing attention to the environment through a programme that monitors and helps

reduce the environmental impact of its businesses.

• Contribute to the wellbeing of employees not only in the workplace but also, in the case of

expatriates, by focusing on living conditions and logistics regarding families and the

education of children.

Social projects supported by TREVI Group include:

• Iraq “Restarting in Erbil”. Support given to the nursery “Casa del bambino” that houses

over 130 children on the outskirts of Erbil.

• Romagna Solidale, a non-profit organisation (Italy): membership fee and project support

• Caritas: donation

• Romagna Iniziative (a consortium to promote youth sport, art and culture in the region):

membership fee and project support

• Support given to the Nuova Famiglia for healthcare projects for able and disabled persons

(Italy)

• RiminiForMutoko: donation to the association of volunteers working in Zimbabwe

• Italian Home for Children, Boston (USA): donation

• “Planeta Amor” Foundation: educational and nutritional support for infants and

adolescents with HIV/AIDS

• Asociación Trabajo y Persona of Caracas, Venezuela: donation

• Support given to the Jardín Nuestra Señora del Valle Orphanage in Argentina

• Support given to the Merendero GabyMar project in Argentina

• Support given to youth sporting activities (Basketball Cesena, Cesena Volleyball, Rugby

Cesena)

35

• Various donations to orphanages and local schools in the Philippines

These donations demonstrate the focus and involvement of the Group in daily life and the Company’s

ability to integrate the social dimension into its business activities.

Business outlook

The Group has prepared a 2017-2021 Business Plan with help of an international consultant. The

Plan was approved by the Board of Directors at its meeting on 3 March 2017.

Internal Dealing

In 2016, nine internal dealing notifications were made by: Trevi Holding SE (seven), CDP Equity

S.p.A. and FSI Investimenti S.p.A.

All the notifications were deposited with Borsa Italiana and are available on its website and on the

Company website, www.trevifin.com under the investor relations section in a sub-section for internal

dealing notifications and in the subs-section for communications on the purchase of treasury shares

by the Company.

Other information

In accordance with Consob communication of 28 July 2006 no. DEM/6064293, it is stated that, in

2016, the TREVI Group did not carry out any atypical and/or unusual transactions, as defined in the

Communication.

Significant events after the end of the reporting period:

Details of events subsequent to the end of the reporting period are given in Note 38 of the Notes to

the Financial Statements.

Report on Corporate Governance and on the Company’s Ownership Structure

At its meeting on 14 November 2016, the Board of Directors approved the adoption of the Self-

regulatory Code of Conduct for Listed Companies issued by the Committee for Corporate

36

Governance – Borsa Italiana S.p.A. in July 2015.

To fulfil the requirements of Article 123-bis of the Consolidated Finance Act, the Company has

prepared a Report on Corporate Governance and Ownership Structure, which has been made publicly

available at the same time as the present Financial Statements at the registered office of the

Company, at Borsa Italiana and on the Company website www.trevifin.com in the Investor Relations

– Corporate Governance section, which contains all the documentation relating to the corporate

governance of the Company; this Report has been deposited in Borsa Italiana S.p.A. and in the

centralised storage mechanism E Market Storage (www.emarketstorage.it), as required by the Rules.

At its meeting on 12 April 2017, the Board of Directors approved the Report for the 2016 financial

year, which follows the indications given by Borsa Italiana S.p.A. in the Format per la Relazione sul

Governo Societario e gli Assetti Proprietari, 6th edition – January 2017.

Report on Remuneration

To comply with regulatory requirements and to give shareholders further information for an

understanding of the Company, a Report on Remuneration has been prepared in compliance with

Article 123-ter of the Consolidated Finance Act, which has been made publicly available at the same

time as the present Financial Statements at the registered office of the Company, at Borsa Italiana and

on the Company website www.trevifin.com in the Investor Relations – Corporate Governance

section; this communication has been deposited in Borsa Italiana S.p.A. and in the authorised storage

mechanism, E Market Storage (www.emarketstorage.it), as required by the Rules.

The Report on Remuneration was approved by the Board of Directors at its meeting on 12 April 2017

and complies with the indications of Consob Resolution no. 18049 of 23 December 2011, published

in the Gazzetta Ufficiale no. 303 on 30 December 2011.

37

ADDITIONAL INFORMATION

SHARE CAPITAL

The issued and fully paid-up share capital of TREVI – Finanziaria Industriale S.p.A. at 31 December

2016 was Euro 82,391,632.50 comprising 164,783,265 ordinary shares each of nominal value Euro

0.50.

The company is controlled by Trevi Holding SE, which is 51% controlled by I.F.I.T. S.r.l. According

to data held by Consob at 31 December 2016, Trevi Holding SE owns 54,328,717 ordinary shares,

equal to 32.97% of the share capital.

At 31 December 2016 (according to Consob data) shareholders, other than the majority shareholder,

registered as having a shareholding in excess of 3% of the share capital were FSI Investimenti S.p.A.

with 16.852% and Polaris Capital Management LLC (USA) with a shareholding of 10.0072%.

During 2016, CDP Equity S.p.A. (previously Fondo Strategico S.p.A.) sold to FSI Investimenti

S.p.A. (both companies belonging to Cassa Depositi e Prestiti S.p.A., which, in turn, is controlled by

the Ministry of Economy and Finance (Ministero dell’Economia e delle Finanze)) its shareholding of

8.426%.

Treasury shares or shares and investments in controlling shareholders

At 31 December 2016 and at the date of these Financial Statements, the Company held 204,000

treasury shares, equal to 0.124% of the share capital; during the 2016 financial year, the Company

did not exercise the buy-back mandate given it by the Shareholders’ Meeting.

The Company does not own, directly or indirectly through any subsidiaries, shares and/or

shareholdings in the controlling shareholder, Trevi Holding SE.

Branches

Since March 2004, the Company has had a branch in Venezuela for the activities of the consortium

of Trevi S.p.A. (50%) - TREVI – Finanziaria Industriale S.p.A. (45%) - SC Sembenelli S.r.l. (5%),

which won the contract from CADAFE in Venezuela for the repair of the Borde Seco Dam. The

38

branch is not operational.

Procedures for Related-party Transactions

With the approval of the Committee for Related-party Transactions, all of whose members are

independent Directors, the Board of Directors meeting of 16 October 2014 updated the Procedures

for Related-party Transactions, prepared in compliance with Consob Rule no. 17221/2010 and

subsequent amendments and additions, previously approved on 26 November 2010; these procedures

are expected to be updated during the 2017 financial year.

The Committee for Related-party Transactions in office at 31 December 2016 and at the date of these

Financial Statements was appointed by the Board of Directors on 15 January 2015 and is made up of

the following independent and non-executive Directors:

- Rita Rolli (Chairperson)

- Cristina Finocchi Mahne

- Monica Mondardini

The Procedures for Related-party Transactions of the Company are available on the Company

website www.trevifin.com.

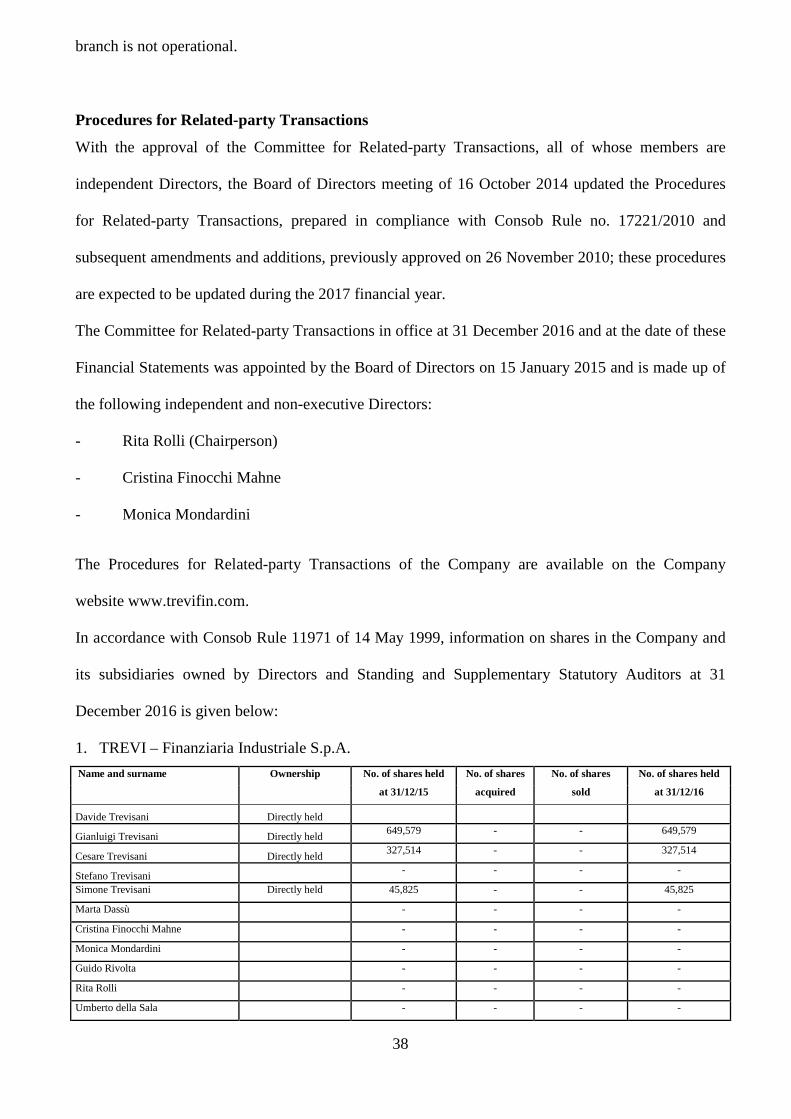

In accordance with Consob Rule 11971 of 14 May 1999, information on shares in the Company and

its subsidiaries owned by Directors and Standing and Supplementary Statutory Auditors at 31

December 2016 is given below:

1. TREVI – Finanziaria Industriale S.p.A.

Name and surname Ownership No. of shares held No. of shares No. of shares No. of shares held

at 31/12/15 acquired sold at 31/12/16

Davide Trevisani Directly held

Gianluigi Trevisani Directly held 649,579 - - 649,579

Cesare Trevisani Directly held 327,514 - - 327,514

Stefano Trevisani - - - -

Simone Trevisani Directly held 45,825 - - 45,825

Marta Dassù - - - -

Cristina Finocchi Mahne - - - -

Monica Mondardini - - - -

Guido Rivolta

- - - -

Rita Rolli

- - - -

Umberto della Sala - - - -

39

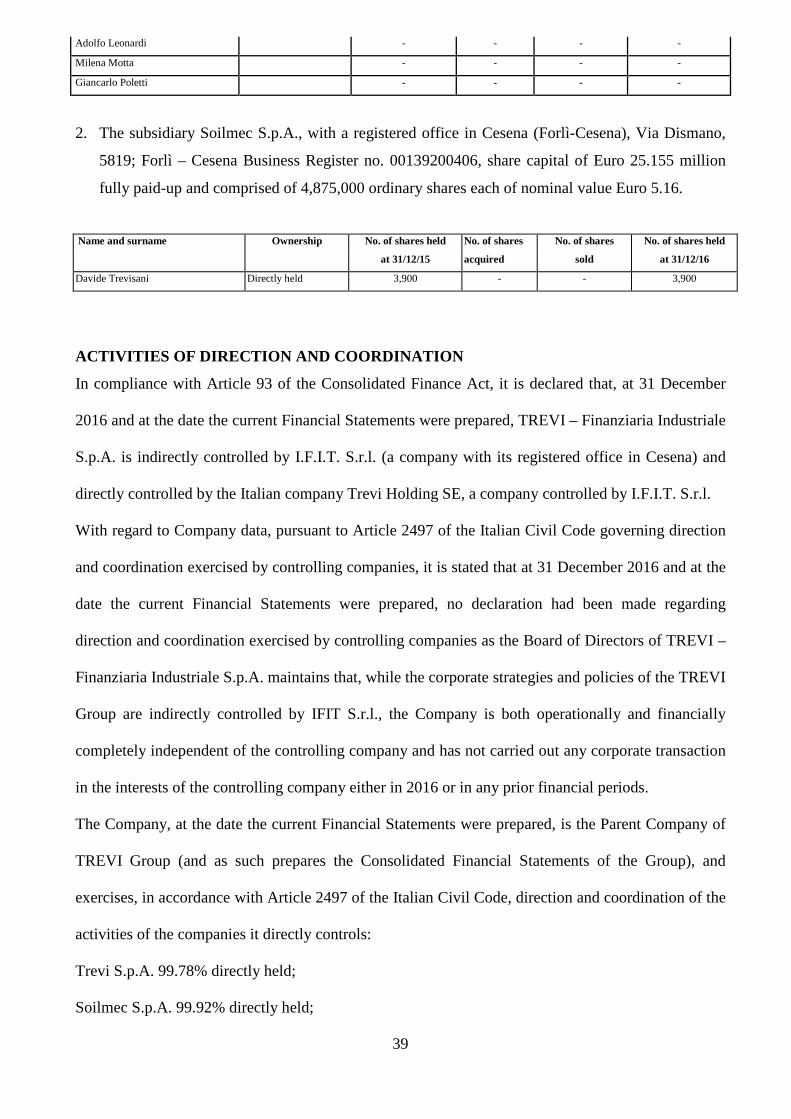

Adolfo Leonardi

- - - -

Milena Motta

- - - -

Giancarlo Poletti - - - -

2. The subsidiary Soilmec S.p.A., with a registered office in Cesena (Forlì-Cesena), Via Dismano,

5819; Forlì – Cesena Business Register no. 00139200406, share capital of Euro 25.155 million

fully paid-up and comprised of 4,875,000 ordinary shares each of nominal value Euro 5.16.

Name and surname Ownership No. of shares held No. of shares No. of shares No. of shares held

at 31/12/15 acquired sold at 31/12/16

Davide Trevisani Directly held 3,900 - - 3,900

ACTIVITIES OF DIRECTION AND COORDINATION

In compliance with Article 93 of the Consolidated Finance Act, it is declared that, at 31 December

2016 and at the date the current Financial Statements were prepared, TREVI – Finanziaria Industriale

S.p.A. is indirectly controlled by I.F.I.T. S.r.l. (a company with its registered office in Cesena) and

directly controlled by the Italian company Trevi Holding SE, a company controlled by I.F.I.T. S.r.l.

With regard to Company data, pursuant to Article 2497 of the Italian Civil Code governing direction

and coordination exercised by controlling companies, it is stated that at 31 December 2016 and at the

date the current Financial Statements were prepared, no declaration had been made regarding

direction and coordination exercised by controlling companies as the Board of Directors of TREVI –