Trends in Messaging - acgcsd.org 3_SWIFT... · Bangladesh Burma Laos ... Hong Kong Taiwan South...

48

Trends in Messaging ACG Korea Adam Wilson, Director Securities Markets, Asia November 2011

Transcript of Trends in Messaging - acgcsd.org 3_SWIFT... · Bangladesh Burma Laos ... Hong Kong Taiwan South...

Trends in Messaging ACG Korea

Adam Wilson, Director

Securities Markets, Asia

November 2011

Tends

• ISO and global use

• RMB implications on Securities messaging

• Settlement & Reconciliation Study

• Legal Entity Identifier (LEI)

• MyStandards

200908 FileAct Overview 2

Trend towards Standardisation

including ISO

India

Maldives

Sri Lanka

Nepal Bhutan

Bangladesh Burma Laos

Thailand

Cambodia

Brunei

Vietnam

Malaysia

Singapore

Indonesia East Timor

Philippines Hong Kong

Taiwan

South Korea

North Korea

Japan

China

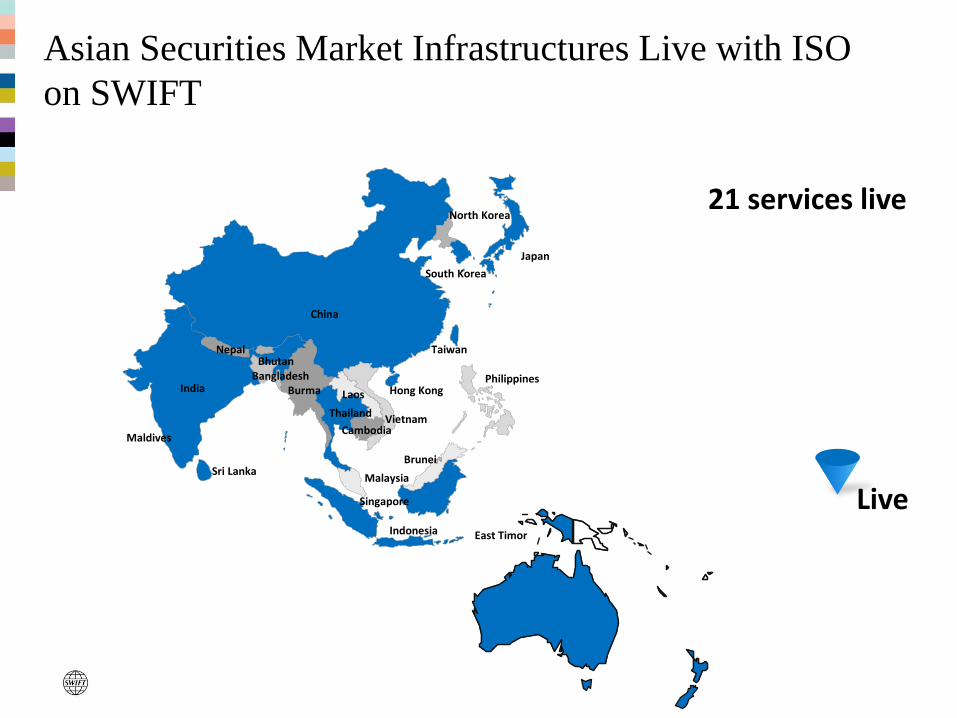

Asian Securities Market Infrastructures Live with ISO

on SWIFT

4

Australia

Live

21 services live

India

Maldives

Sri Lanka

Nepal Bhutan

Bangladesh Burma Laos

Thailand

Cambodia

Brunei

Vietnam

Malaysia

Singapore

Indonesia East Timor

Philippines

Hong Kong

Taiwan

South Korea

North Korea

Japan

China

Implementing

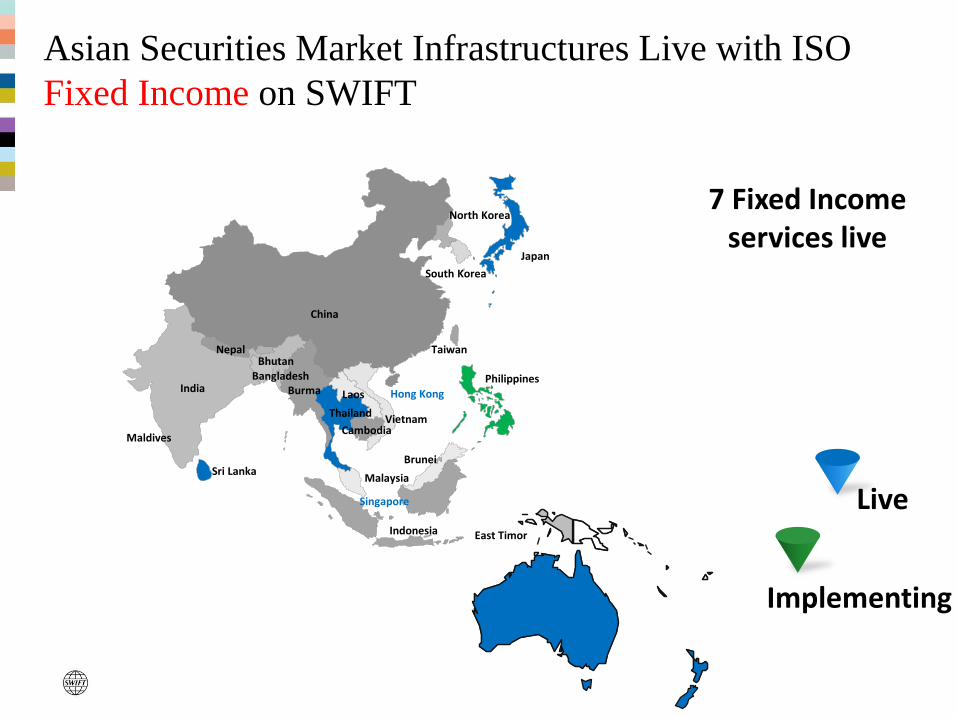

Asian Securities Market Infrastructures Live with ISO

Fixed Income on SWIFT

5

Australia

Live

7 Fixed Income services live

India

Maldives

Sri Lanka

Nepal Bhutan

Bangladesh Burma Laos

Thailand

Cambodia

Brunei

Vietnam

Malaysia Singapore

Indonesia East Timor

Philippines

Hong Kong

Taiwan

South Korea

North Korea

Japan

China

Implementing

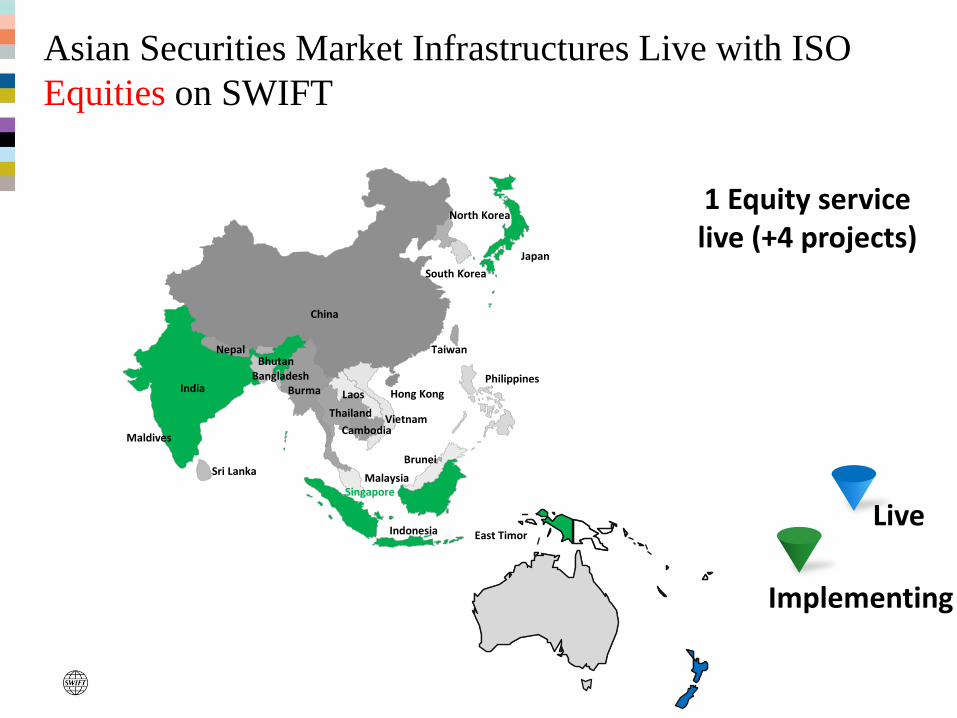

Asian Securities Market Infrastructures Live with ISO

Equities on SWIFT

6

Australia

Live

1 Equity service live (+4 projects)

India

Maldives

Sri Lanka

Nepal Bhutan

Bangladesh Burma Laos

Thailand

Cambodia

Brunei

Vietnam

Malaysia Singapore

Indonesia East Timor

Philippines

Hong Kong

Taiwan

South Korea

North Korea

Japan

China

Live

Implementing

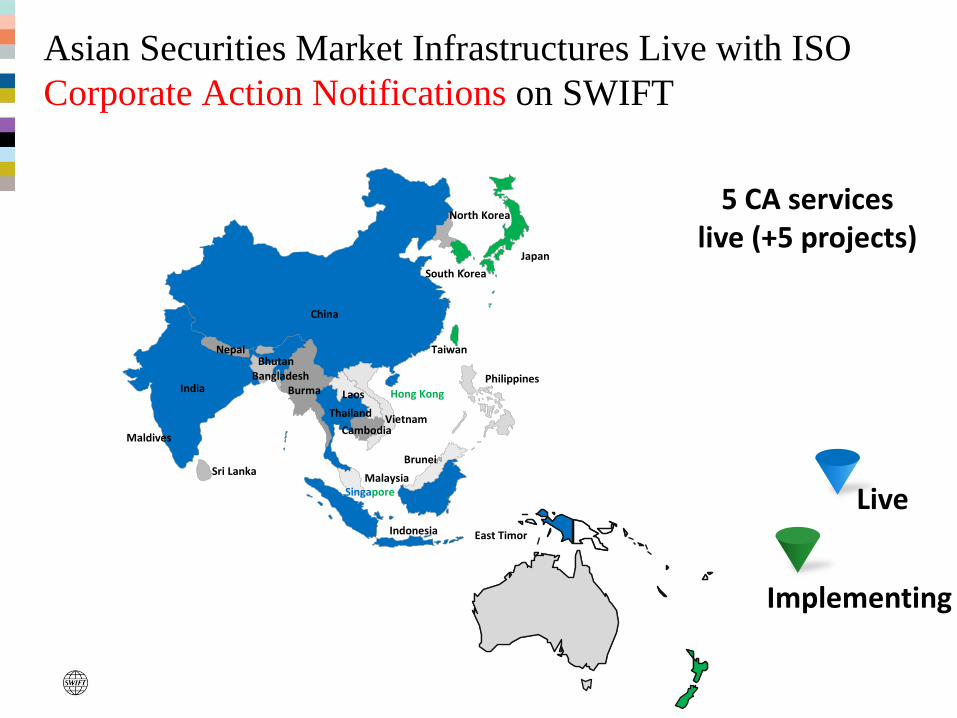

Asian Securities Market Infrastructures Live with ISO

Corporate Action Notifications on SWIFT

7

Australia

5 CA services live (+5 projects)

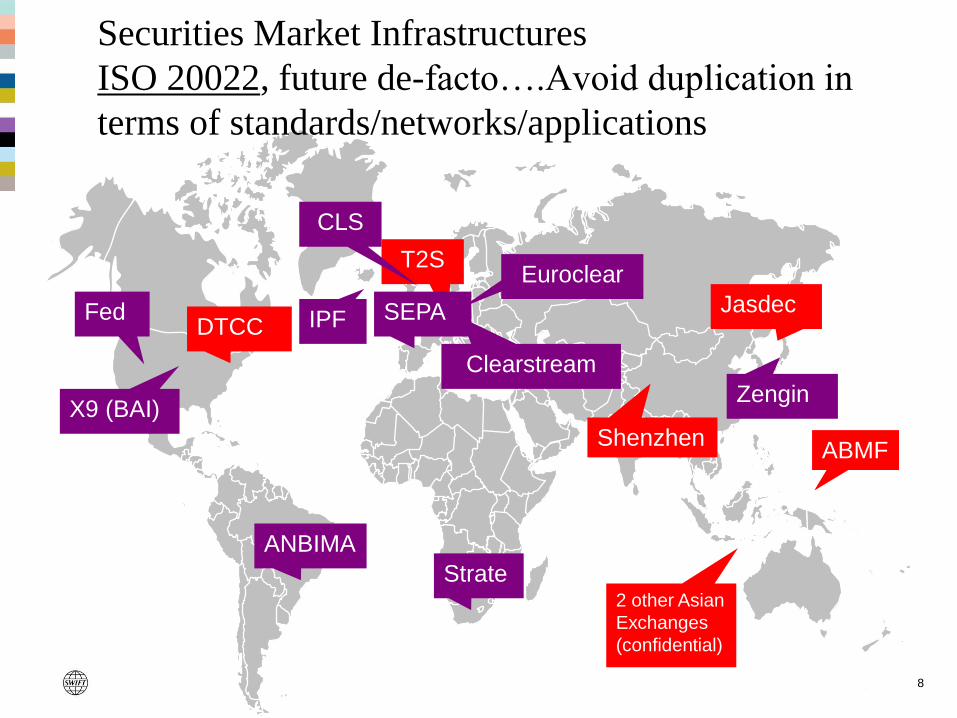

Securities Market Infrastructures

ISO 20022, future de-facto….Avoid duplication in

terms of standards/networks/applications

DTCC Jasdec

T2S

Zengin

Fed

Euroclear

Clearstream

IPF

X9 (BAI)

ANBIMA

Strate

SEPA

CLS

8

ABMF Shenzhen

2 other Asian

Exchanges

(confidential)

ABMF

10

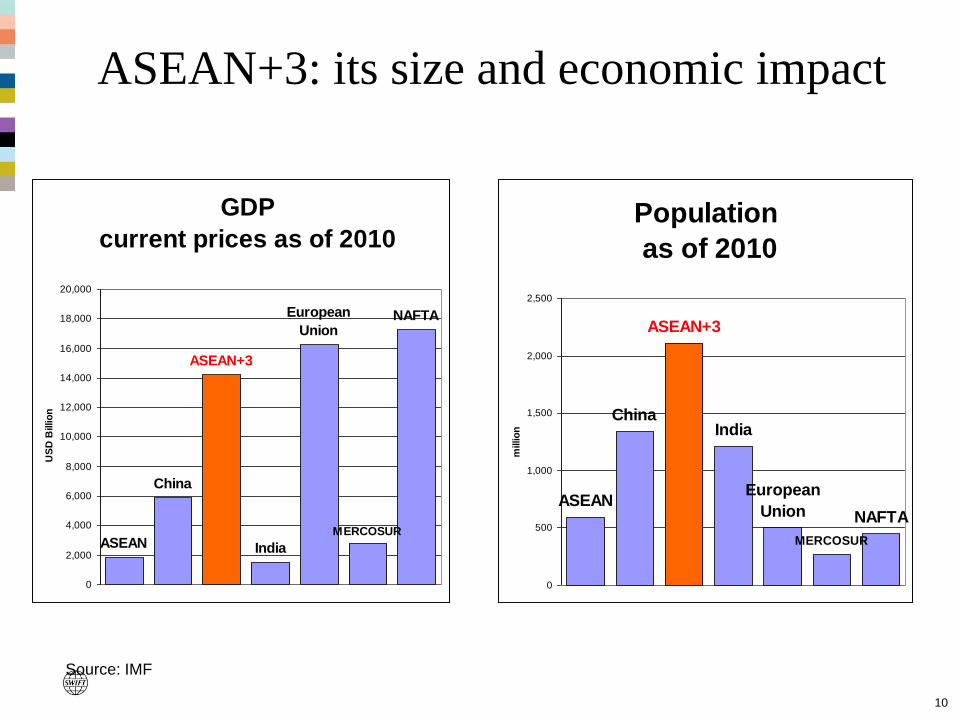

ASEAN+3: its size and economic impact

Source: IMF

GDP

current prices as of 2010

ASEAN

China

India

NAFTA

MERCOSUR

European

Union

ASEAN+3

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

US

D B

illio

n

Population

as of 2010

ASEAN

ChinaIndia

European

Union NAFTA

MERCOSUR

ASEAN+3

0

500

1,000

1,500

2,000

2,500

millio

n

11

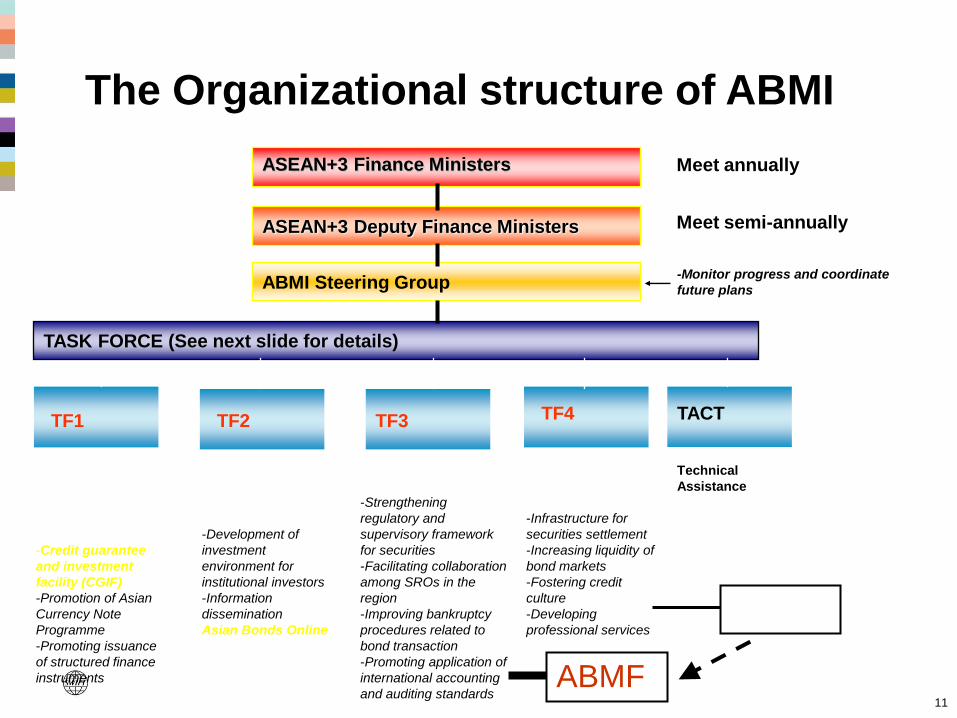

Promoting

Issuance of Local

Currency

Denominated

Bonds

-Credit guarantee

and investment

facility (CGIF)

-Promotion of Asian

Currency Note

Programme

-Promoting issuance

of structured finance

instruments

Facilitating the

Demand of Local

Currency-

Denominated Bonds

-Development of

investment

environment for

institutional investors

-Information

dissemination

Asian Bonds Online

Improving Regulatory

Framework

-Strengthening

regulatory and

supervisory framework

for securities

-Facilitating collaboration

among SROs in the

region

-Improving bankruptcy

procedures related to

bond transaction

-Promoting application of

international accounting

and auditing standards

Improving Related

Infrastructure for the

Bond Market

-Infrastructure for

securities settlement

-Increasing liquidity of

bond markets

-Fostering credit

culture

-Developing

professional services

Technical

Assistance

-Monitor progress and coordinate

future plans

TF1

ABMI Steering Group

ASEAN+3 Finance Ministers

ASEAN+3 Deputy Finance Ministers

TASK FORCE (See next slide for details)

Meet annually

Meet semi-annually

TF2 TF3 TF4 TACT

The Organizational structure of ABMI

ABMF

GoE

12

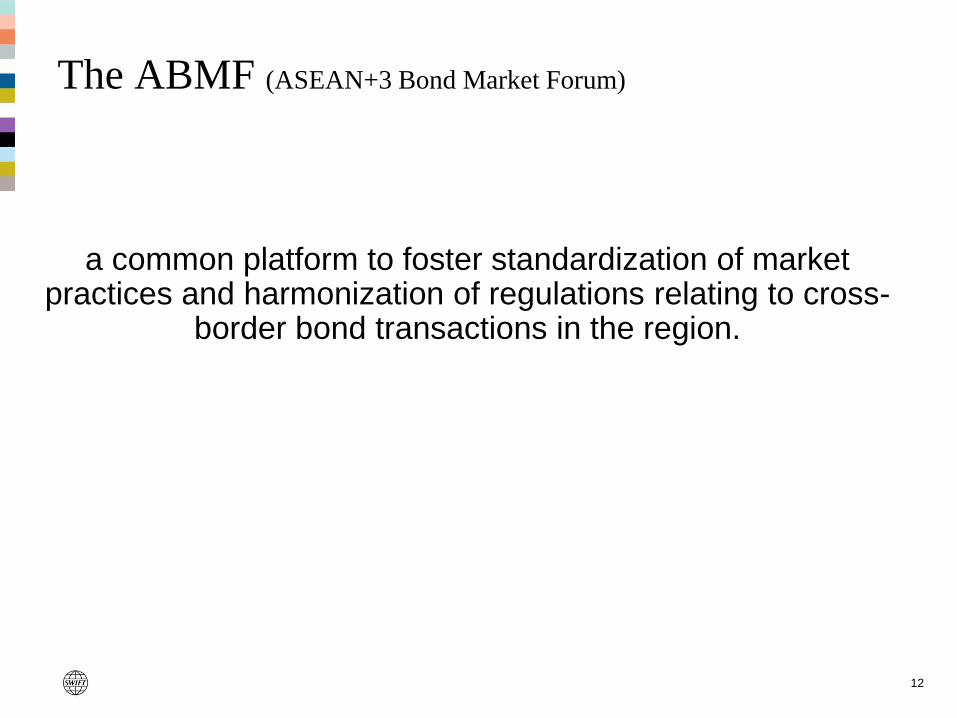

The ABMF (ASEAN+3 Bond Market Forum)

a common platform to foster standardization of market practices and harmonization of regulations relating to cross-

border bond transactions in the region.

13

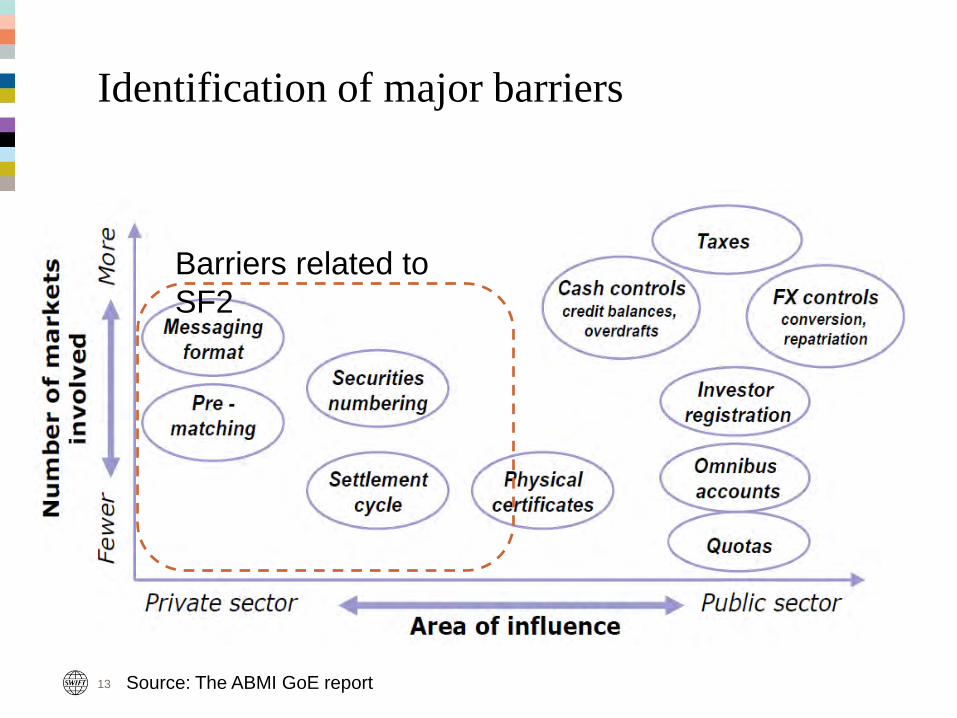

Identification of major barriers

Barriers related to

SF2

Source: The ABMI GoE report

14

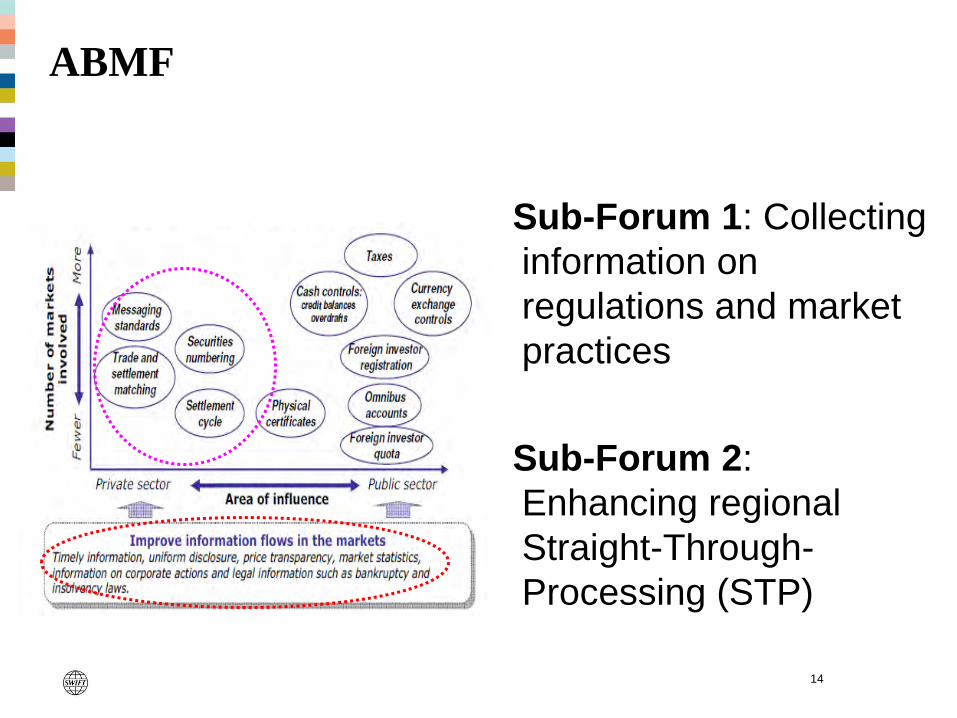

ABMF

Sub-Forum 1: Collecting

information on

regulations and market

practices

Sub-Forum 2:

Enhancing regional

Straight-Through-

Processing (STP)

15

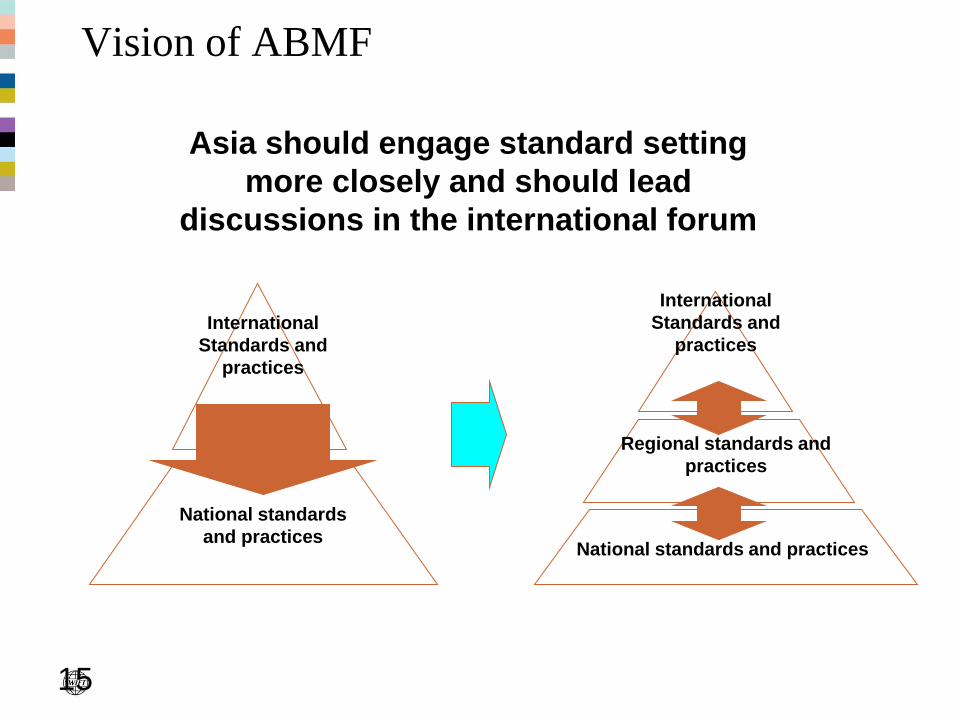

Vision of ABMF

National standards

and practices

International

Standards and

practices

International

Standards and

practices

Regional standards and

practices

National standards and practices

Asia should engage standard setting

more closely and should lead

discussions in the international forum

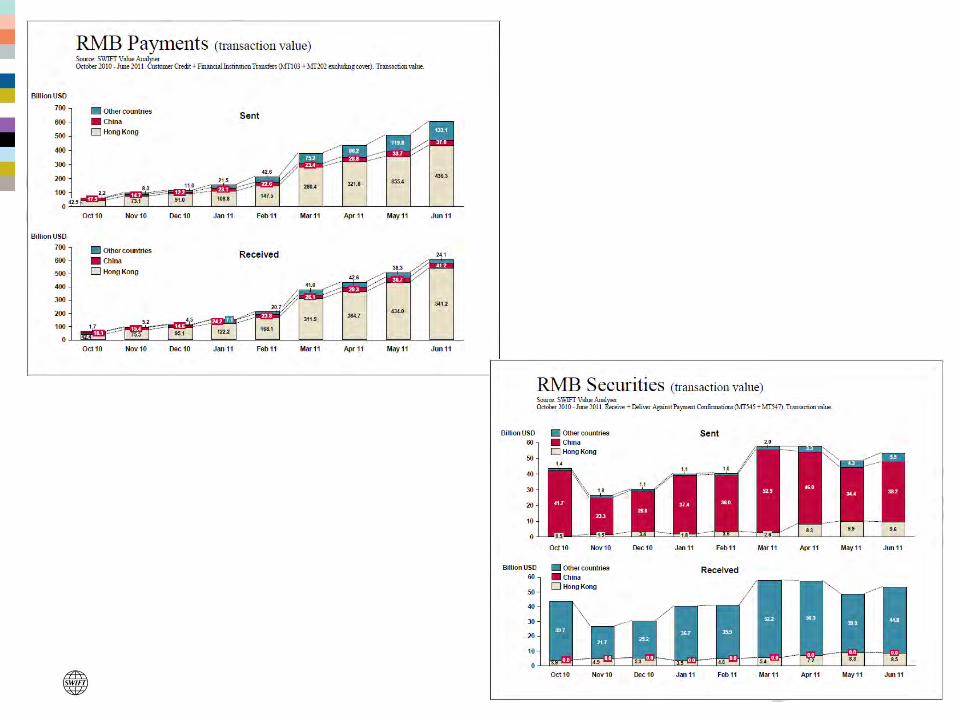

RMB implications for

Securities

17

Increasing Opportunities

• RMB-QFII (also known as mini-QFII)

• Overseas investors to use offshore RMB to invest with an initial

quota of RMB 20B (3.1B USD)

• RMB bonds in Hong Kong (Dim Sum Bonds) & FDI

• Mainland Chinese non-financial corporations issue HK bonds

• The remittance of proceeds back to the mainland is expected to be

made easier based on the revamp FDI rules (transparent and

standardized framework).

• Greater Integration between Hong Kong and Mainland

China

• China likely to increase the issuance of sovereign bonds

• HK Exchange-traded fund (ETF) will allow Chinese investment

• More mainland enterprises encouraged to IPO in Hong Kong.

• Hong Kong banks will be allowed to engage in Mainland mutual fund

business

SSC_OffsiteMeetingSlides_1105_v1.pptx 18

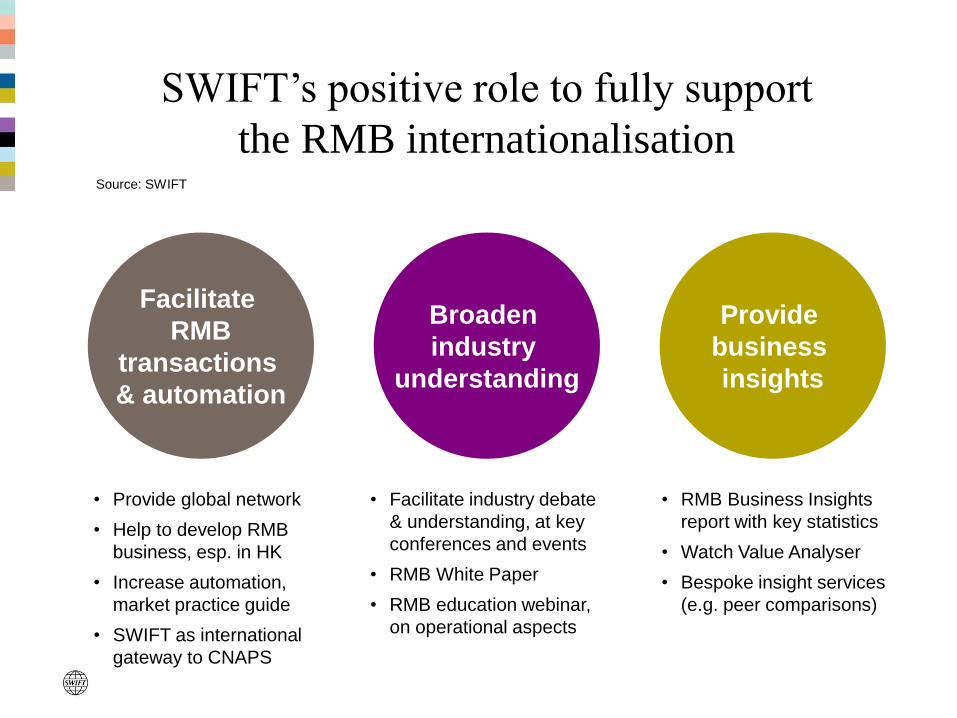

• Provide global network

• Help to develop RMB

business, esp. in HK

• Increase automation,

market practice guide

• SWIFT as international

gateway to CNAPS

• Facilitate industry debate

& understanding, at key

conferences and events

• RMB White Paper

• RMB education webinar,

on operational aspects

• RMB Business Insights

report with key statistics

• Watch Value Analyser

• Bespoke insight services

(e.g. peer comparisons)

SWIFT’s positive role to fully support

the RMB internationalisation Source: SWIFT

Facilitate

RMB

transactions

& automation

Broaden

industry

understanding

Provide

business

insights

Settlement & Reconciliation Study

Market Trends December 2010

21

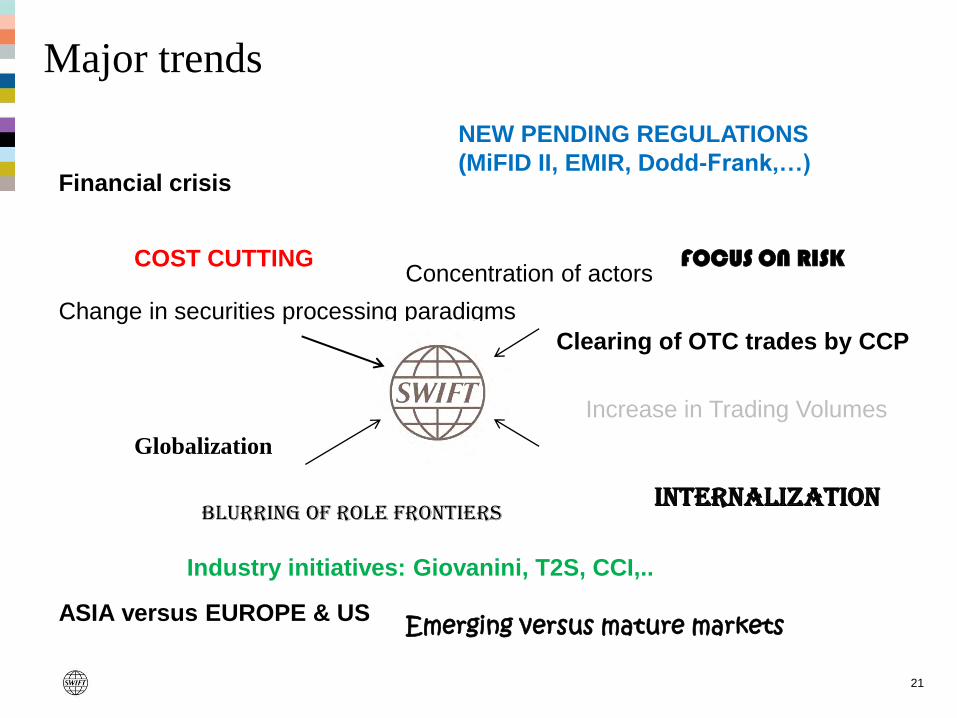

Major trends

COST CUTTING

Financial crisis

NEW PENDING REGULATIONS

(MiFID II, EMIR, Dodd-Frank,…)

Concentration of actors

Change in securities processing paradigms

Globalization

Clearing of OTC trades by CCP

FOCUS ON RISK

Blurring of role frontiers

Industry initiatives: Giovanini, T2S, CCI,..

Increase in Trading Volumes

Internalization

ASIA versus EUROPE & US Emerging versus mature markets

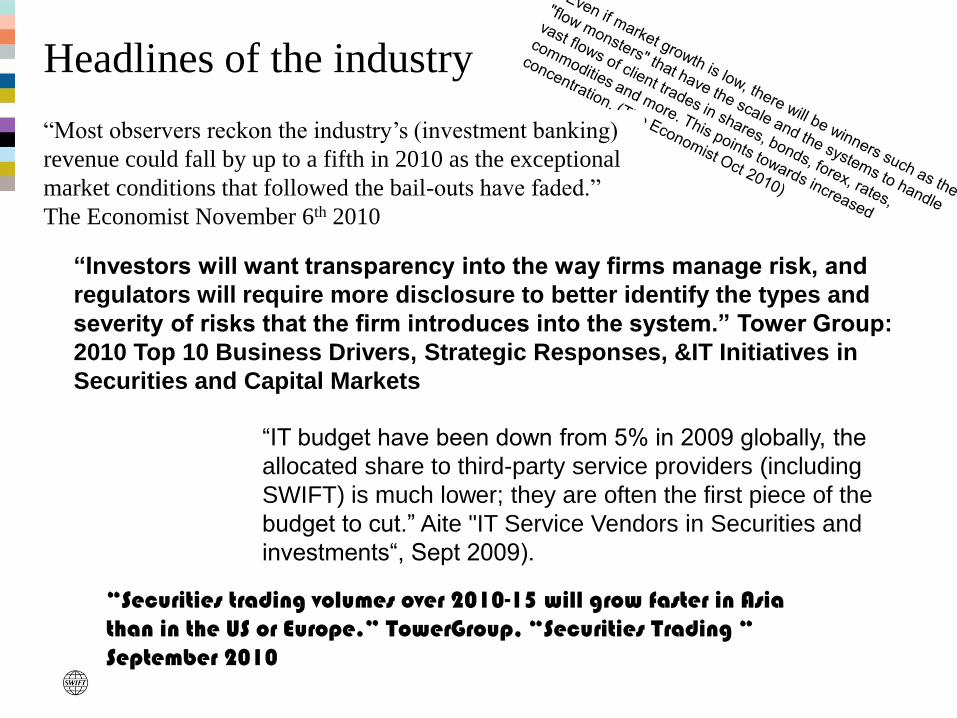

Headlines of the industry

“Most observers reckon the industry’s (investment banking)

revenue could fall by up to a fifth in 2010 as the exceptional

market conditions that followed the bail-outs have faded.”

The Economist November 6th 2010

“IT budget have been down from 5% in 2009 globally, the

allocated share to third-party service providers (including

SWIFT) is much lower; they are often the first piece of the

budget to cut.” Aite "IT Service Vendors in Securities and

investments“, Sept 2009).

“Securities trading volumes over 2010-15 will grow faster in Asia than in the US or Europe.” TowerGroup, “Securities Trading “ September 2010

“Investors will want transparency into the way firms manage risk, and

regulators will require more disclosure to better identify the types and

severity of risks that the firm introduces into the system.” Tower Group:

2010 Top 10 Business Drivers, Strategic Responses, &IT Initiatives in

Securities and Capital Markets

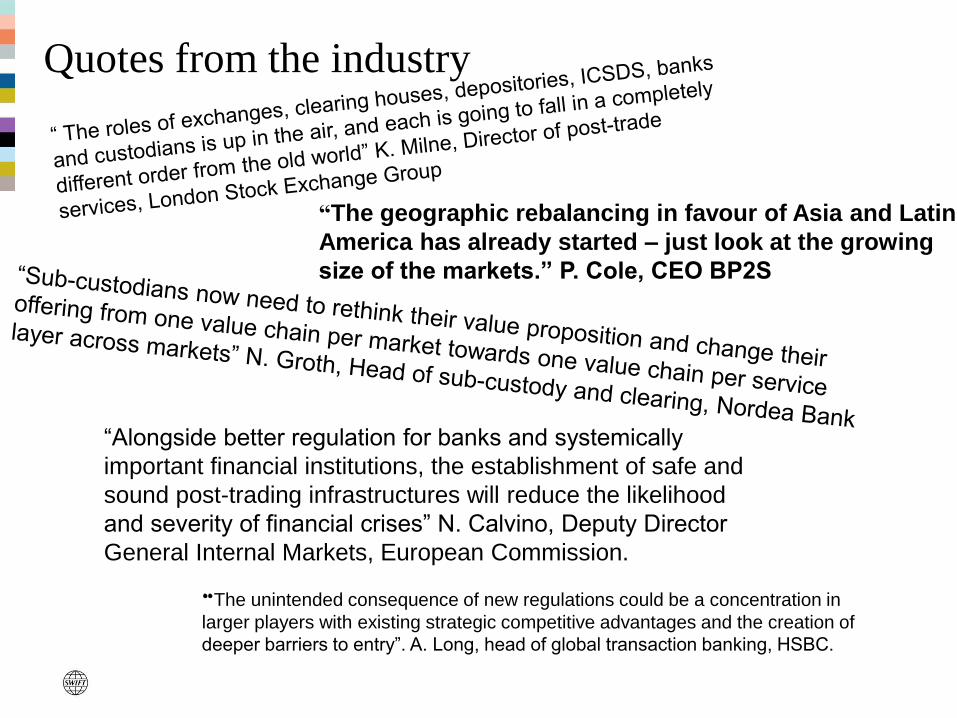

Quotes from the industry

“The geographic rebalancing in favour of Asia and Latin

America has already started – just look at the growing

size of the markets.” P. Cole, CEO BP2S

“Alongside better regulation for banks and systemically

important financial institutions, the establishment of safe and

sound post-trading infrastructures will reduce the likelihood

and severity of financial crises” N. Calvino, Deputy Director

General Internal Markets, European Commission.

“The unintended consequence of new regulations could be a concentration in

larger players with existing strategic competitive advantages and the creation of

deeper barriers to entry”. A. Long, head of global transaction banking, HSBC.

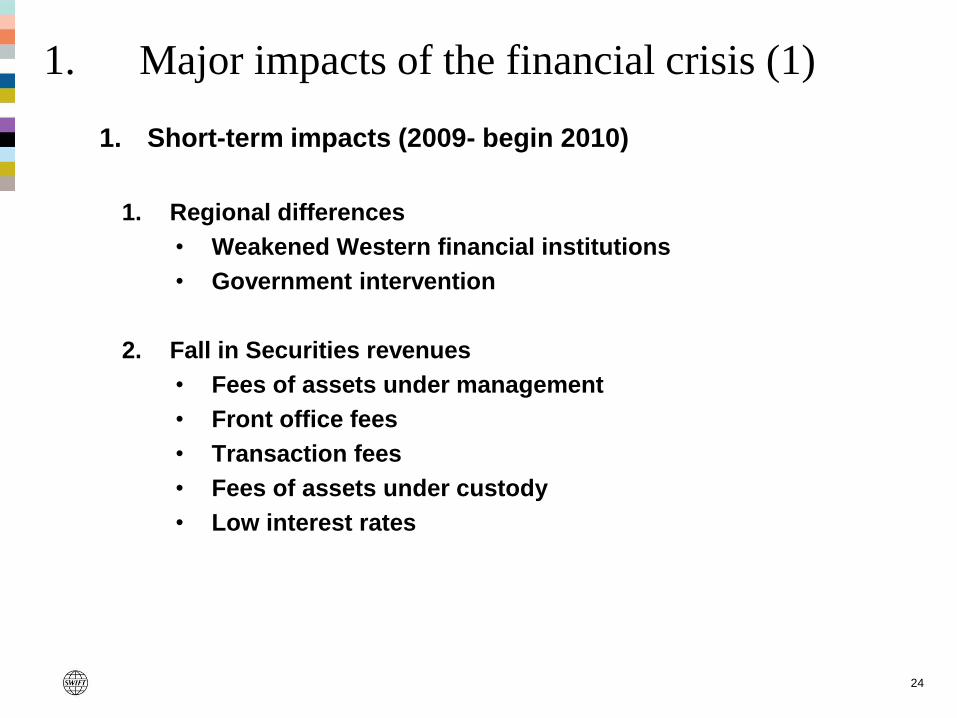

1. Major impacts of the financial crisis (1)

24

1. Short-term impacts (2009- begin 2010)

1. Regional differences

• Weakened Western financial institutions

• Government intervention

2. Fall in Securities revenues

• Fees of assets under management

• Front office fees

• Transaction fees

• Fees of assets under custody

• Low interest rates

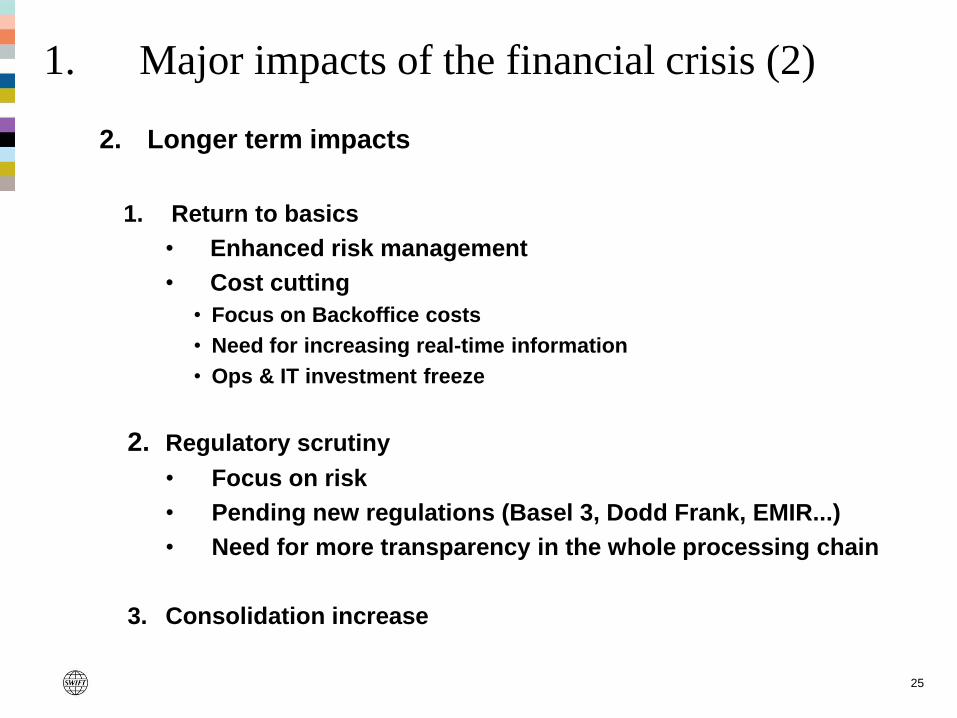

1. Major impacts of the financial crisis (2)

25

2. Longer term impacts

1. Return to basics

• Enhanced risk management

• Cost cutting

• Focus on Backoffice costs

• Need for increasing real-time information

• Ops & IT investment freeze

2. Regulatory scrutiny

• Focus on risk

• Pending new regulations (Basel 3, Dodd Frank, EMIR...)

• Need for more transparency in the whole processing chain

3. Consolidation increase

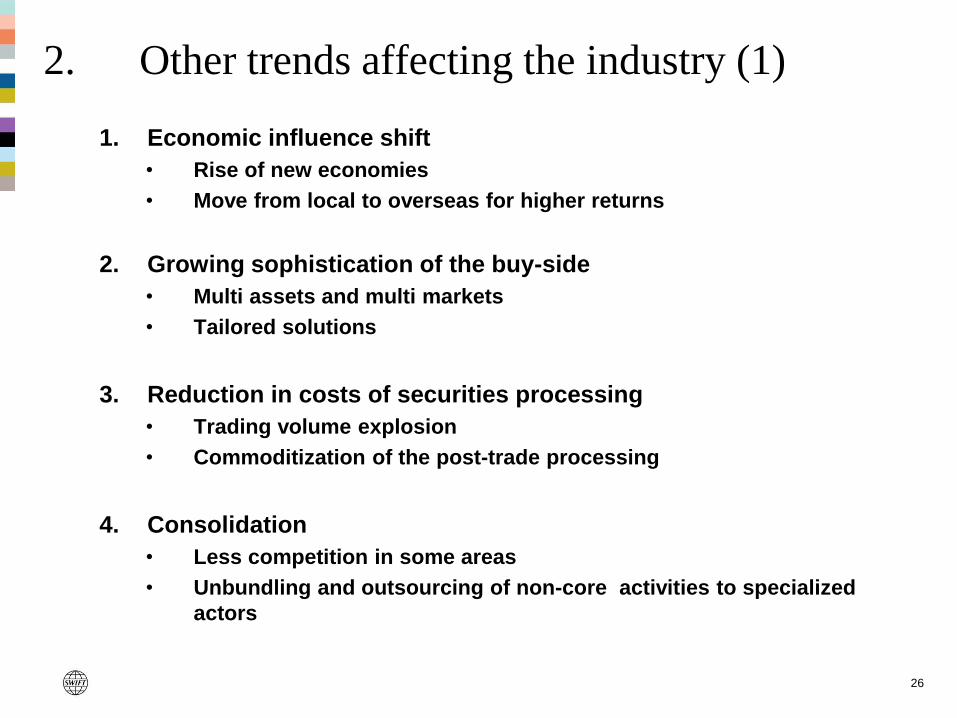

2. Other trends affecting the industry (1)

26

1. Economic influence shift

• Rise of new economies

• Move from local to overseas for higher returns

2. Growing sophistication of the buy-side

• Multi assets and multi markets

• Tailored solutions

3. Reduction in costs of securities processing

• Trading volume explosion

• Commoditization of the post-trade processing

4. Consolidation

• Less competition in some areas

• Unbundling and outsourcing of non-core activities to specialized

actors

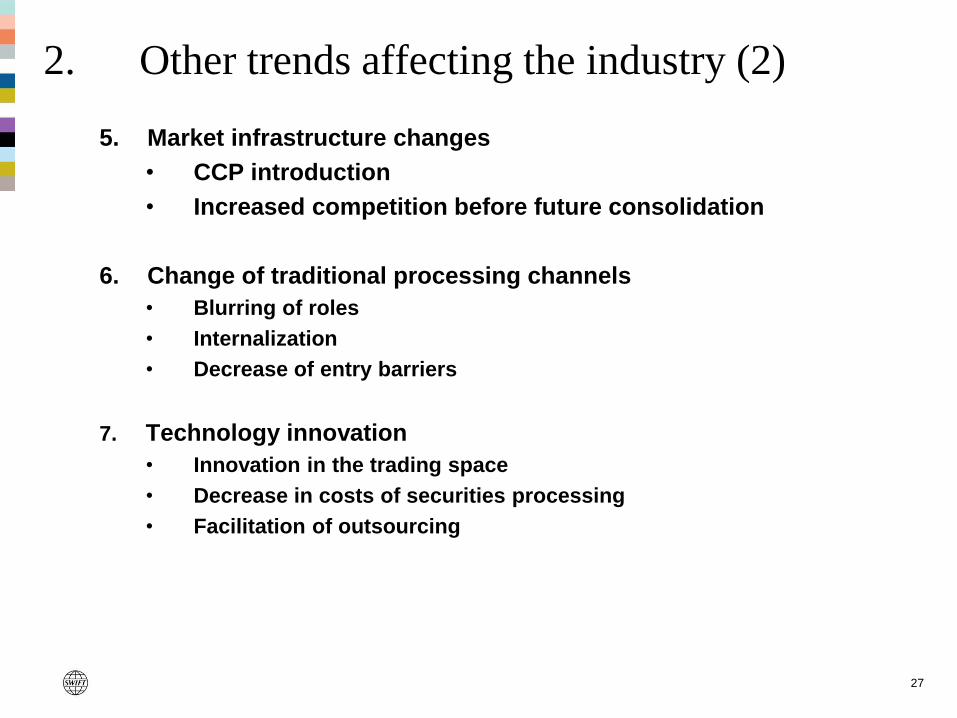

27

5. Market infrastructure changes

• CCP introduction

• Increased competition before future consolidation

6. Change of traditional processing channels

• Blurring of roles

• Internalization

• Decrease of entry barriers

7. Technology innovation

• Innovation in the trading space

• Decrease in costs of securities processing

• Facilitation of outsourcing

2. Other trends affecting the industry (2)

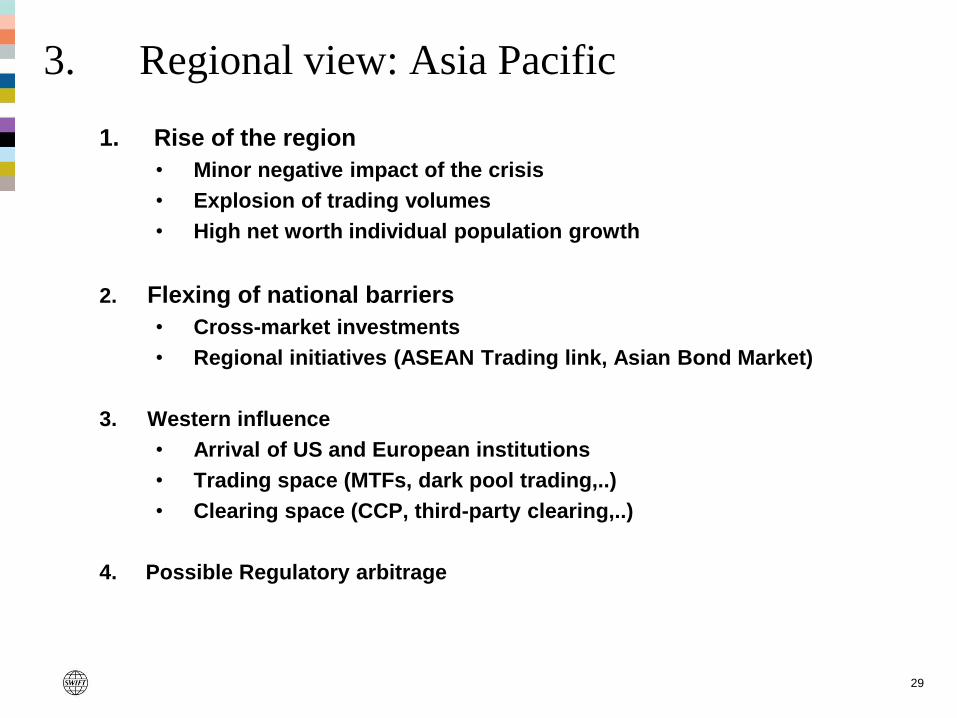

29

1. Rise of the region

• Minor negative impact of the crisis

• Explosion of trading volumes

• High net worth individual population growth

2. Flexing of national barriers

• Cross-market investments

• Regional initiatives (ASEAN Trading link, Asian Bond Market)

3. Western influence

• Arrival of US and European institutions

• Trading space (MTFs, dark pool trading,..)

• Clearing space (CCP, third-party clearing,..)

4. Possible Regulatory arbitrage

3. Regional view: Asia Pacific

Legal Entity Identifier (LEI)

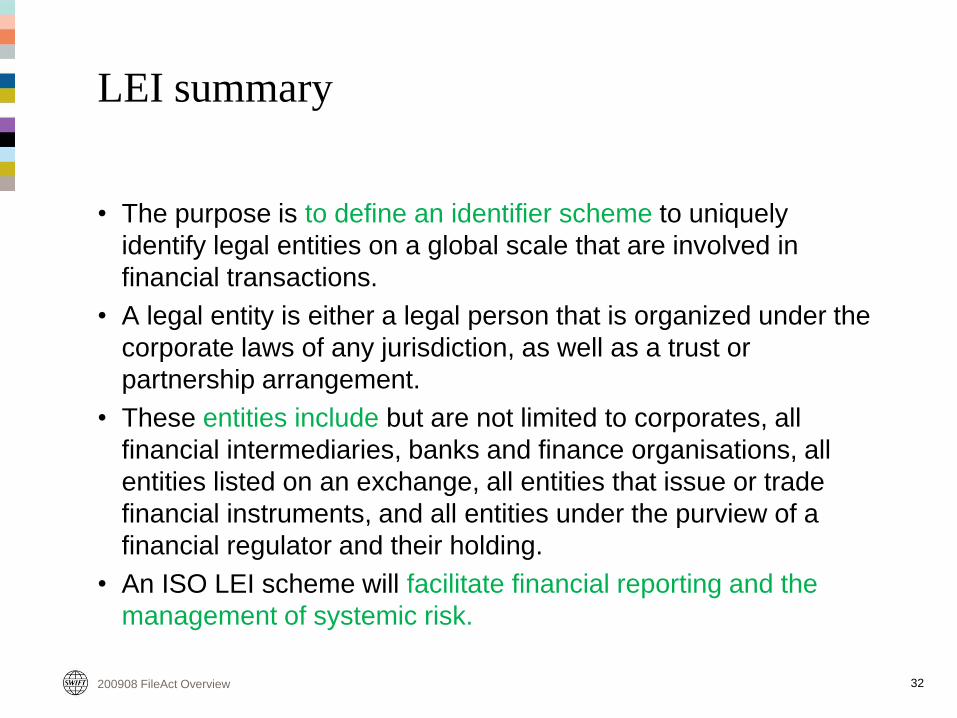

LEI summary

• The purpose is to define an identifier scheme to uniquely

identify legal entities on a global scale that are involved in

financial transactions.

• A legal entity is either a legal person that is organized under the

corporate laws of any jurisdiction, as well as a trust or

partnership arrangement.

• These entities include but are not limited to corporates, all

financial intermediaries, banks and finance organisations, all

entities listed on an exchange, all entities that issue or trade

financial instruments, and all entities under the purview of a

financial regulator and their holding.

• An ISO LEI scheme will facilitate financial reporting and the

management of systemic risk.

200908 FileAct Overview 32

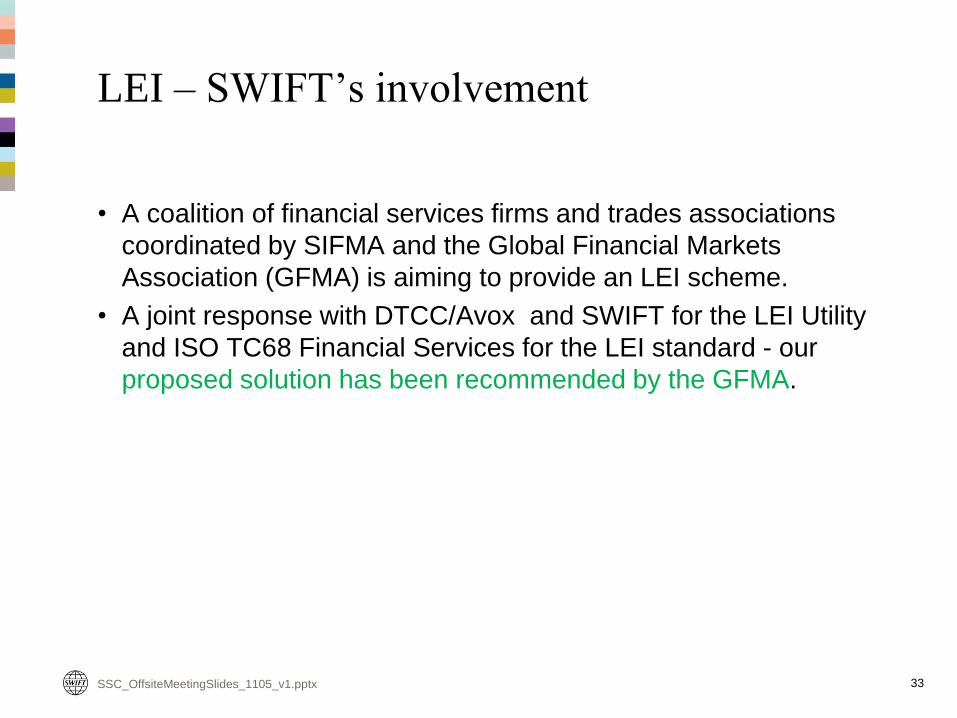

LEI – SWIFT’s involvement

• A coalition of financial services firms and trades associations

coordinated by SIFMA and the Global Financial Markets

Association (GFMA) is aiming to provide an LEI scheme.

• A joint response with DTCC/Avox and SWIFT for the LEI Utility

and ISO TC68 Financial Services for the LEI standard - our

proposed solution has been recommended by the GFMA.

SSC_OffsiteMeetingSlides_1105_v1.pptx 33

LEI implementation

• Engagement - we are working actively with the SIFMA Executive

Committee and with the global regulatory community to keep the

momentum and facilitate the appropriate implementation and adoption

of the LEI solution in line with current and future legislative

requirements

– While we initially expected a mandate by the US based Office for

Financial Research (OFR), the FSB has taken the lead and will

ensure a truly global solution changing the perception that LEI is

an US driven solution.

• Structure and Governance - work cooperatively with all parties

involved in defining and establishing the LEI Utility structure and

agreeing the governance model, the funding model and the regulatory

oversight

– The LEI solution will be based on ISO17442 standard

– SWIFT has been appointed Registration Authority for this new standard.

– ISO has its own governance model and approval processes.

SSC_OffsiteMeetingSlides_1105_v1.pptx 34

LEI implementation

• Planning - The implementation timeline will be driven by the global

regulators

• We anticipate that the first requirements will be based on identification

of counterparties for the OTC derivatives in the Swap Data

Repositories (SDRs) (possibly Q1 2012).

• The first phase of the LEI solution will be based on leveraging and

expanding the existing infrastructure both from DTCC/Avox and from

SWIFT to be able to meet the needs of the regulators and the financial

industry for the SDRs (ie 30-40k enitites).

• Financials - The LEI solution will operate on a cost recovery model

based on revenues generated by the self-registration of legal entities

and the annual maintenance fee supported by the legal entities

identified with LEI.

• Service Development - new areas for service development in entity

and security reference data will emerge outside of the scope of the LEI

Utility.

SSC_OffsiteMeetingSlides_1105_v1.pptx 35

OTC Derivatives

OTC Derivatives summary

• Asia constitutes a small part of the global OTC markets (notional

outstanding volumes total $600,000bn) - trading volumes are rising

fast and most international dealers have established footholds across

in the region (source BIS).

• In Japan - the biggest market in the region - the notional outstanding

amount of interest-rate swaps expanded by 47% between June 2007

and June 2009, according to the Bank of Japan, reaching $27,100bn,

or about 6% of the global interest-rate swap market.

• G20 and Dodd Frank regulations are leading the establishment of

regulation for “Trade Repositories” and “CCP’s”. The proliferation of

initiatives has led to concern that there could be too many

CCPs… A fragmented approach will lead to weaker institutions

and greater risk.

37

The G20 countries

• Argentina

• Australia

• Brazil

• Canada

• China

• European Union

• France

• Germany

• India

• Indonesia

• Italy

• Japan

• Mexico

• Russia

• Saudi Arabia

• South Africa

• South Korea

• Turkey

• United Kingdom

• United States

38 Red indicates Asian member

Asian steps for G20 agreement compliance

Country Steps taken

Australia ASX announced domestic clearing of OTC IR products

($30bn per day market) – no timelines

Hong Kong* Will start to clear OTC NDF and IRS in 2012

India Has developed the Clearing Corporation of India to act as

a central counterparty (CCP) and trade repository for the

domestic OTC market

Japan Yen based OTC trades to be cleared in JP

Singapore* SGX already live with NDF clearing

South Korea Finalised plans for mandatory clearing of OTC derivatives

[Market scientism as to whether this occurs]

39 *Non G20 Country

Solution and CCP fragmentation

• The G20 mandated that nations create clearing solutions. Fragmentation is emerging as a result.

• This results in too many CCPs, splitting liquidity in OTC products across the globe, with regulators having insufficient oversight over them all

• The Financial Stability Board (FSB) in April noted that it was “concerned with the substantial variation across jurisdictions in the pace of implementation”

• ISDA identified what it called the “potentially significant extraterritorial effects and the proliferation of central clearing solutions in the region”

• Asian markets “don’t want to necessarily have solutions imposed on them by other jurisdictions”

• Asian regulators want to ensure that trades in which institutions in their jurisdictions are involved are cleared through entities over which they have some control

40

Paul Landless, a senior associate at the Hong Kong office of Clifford Chance, says: “Trying to

reconcile Asia into the global dynamics [of OTC regulation] is going to be a challenge.”

Available and planned ISO/MT messages

flows with CCPs (1/4)

41

Major European CCPs already use SWIFT for:

• payments and settlement

• CCP to member communication

CCP - Member messaging live and planned

• CCP to settlement system messaging – live

• CCP to clearing member messaging – live H2 2011

• Accord to CCP messaging for OTC EQ/FI – live H2 2011

•Strong synergies between FX & Securities services

•Interoperability flows (TBD)

Key (SWIFT flows)

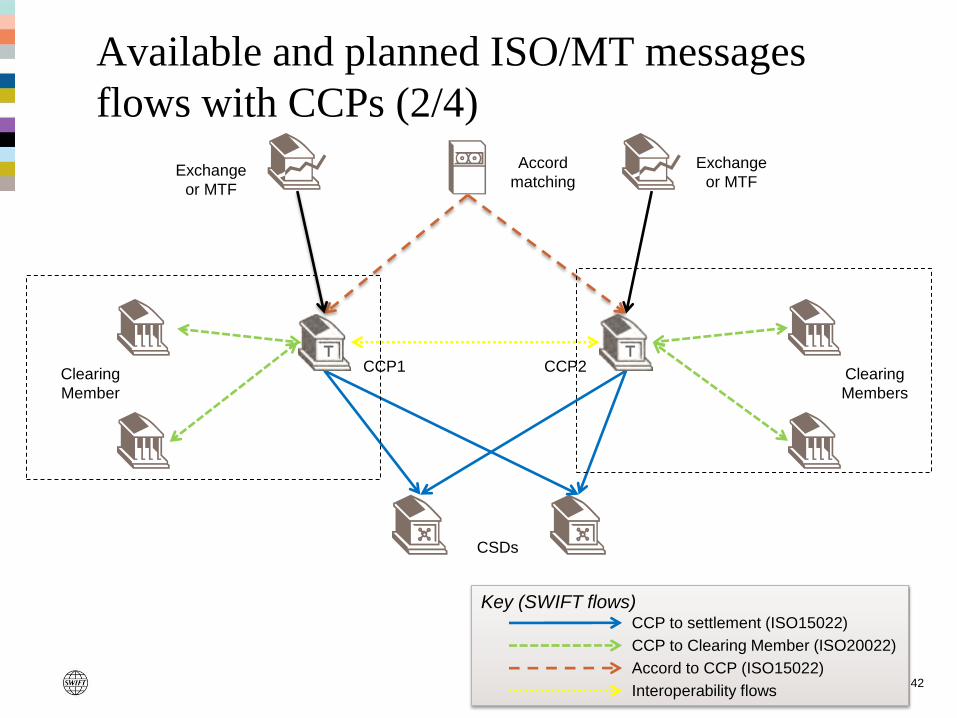

Available and planned ISO/MT messages

flows with CCPs (2/4)

42

Clearing

Member

Clearing

Members

Accord

matching

CSDs

CCP1 CCP2

CCP to settlement (ISO15022)

CCP to Clearing Member (ISO20022)

Accord to CCP (ISO15022)

Interoperability flows

Exchange

or MTF

Exchange

or MTF

Available and planned ISO/MT messages

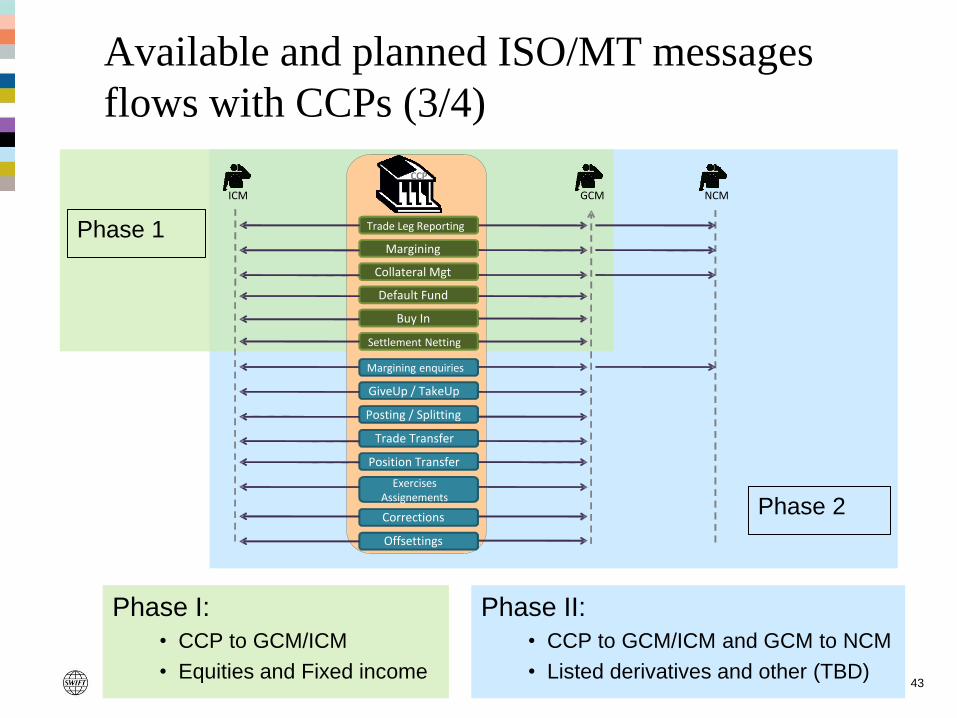

flows with CCPs (3/4)

Phase I:

• CCP to GCM/ICM

• Equities and Fixed income 43

ICM GCM NCM

CCP

Trade Leg Reporting

Margining

Collateral Mgt

Default Fund

Settlement Netting

Buy In

GiveUp / TakeUp

Posting / Splitting

Trade Transfer

Position Transfer

Exercises Assignements

Corrections

Offsettings

Margining enquiries

Phase 1

Phase 2

Phase II:

• CCP to GCM/ICM and GCM to NCM

• Listed derivatives and other (TBD)

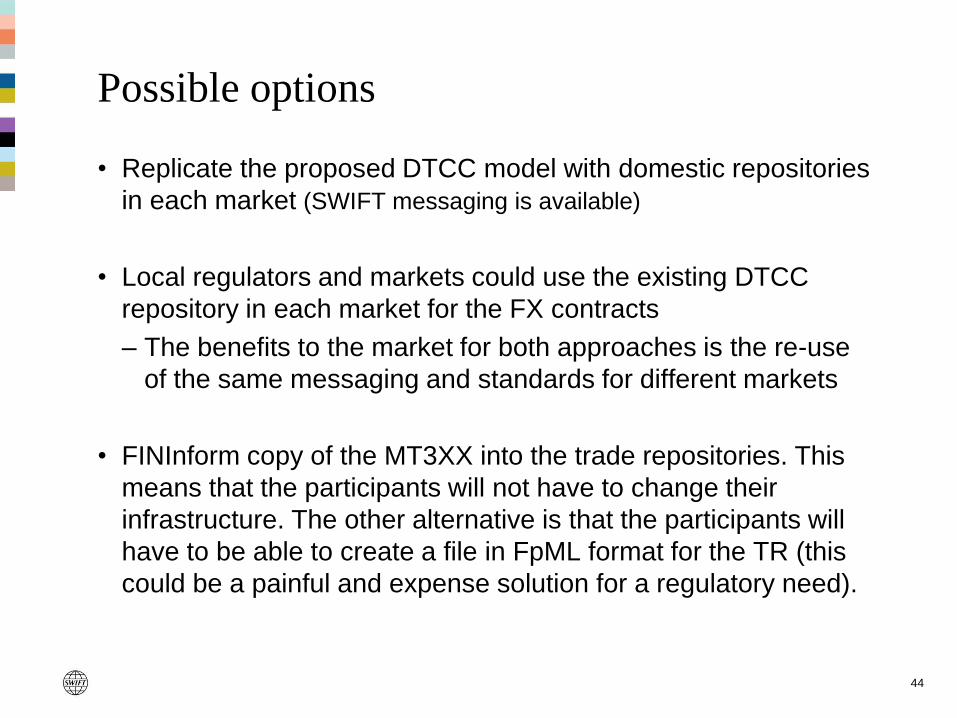

Possible options

• Replicate the proposed DTCC model with domestic repositories

in each market (SWIFT messaging is available)

• Local regulators and markets could use the existing DTCC

repository in each market for the FX contracts

– The benefits to the market for both approaches is the re-use

of the same messaging and standards for different markets

• FINInform copy of the MT3XX into the trade repositories. This

means that the participants will not have to change their

infrastructure. The other alternative is that the participants will

have to be able to create a file in FpML format for the TR (this

could be a painful and expense solution for a regulatory need).

44

MyStandards & Standards

Developer Kit

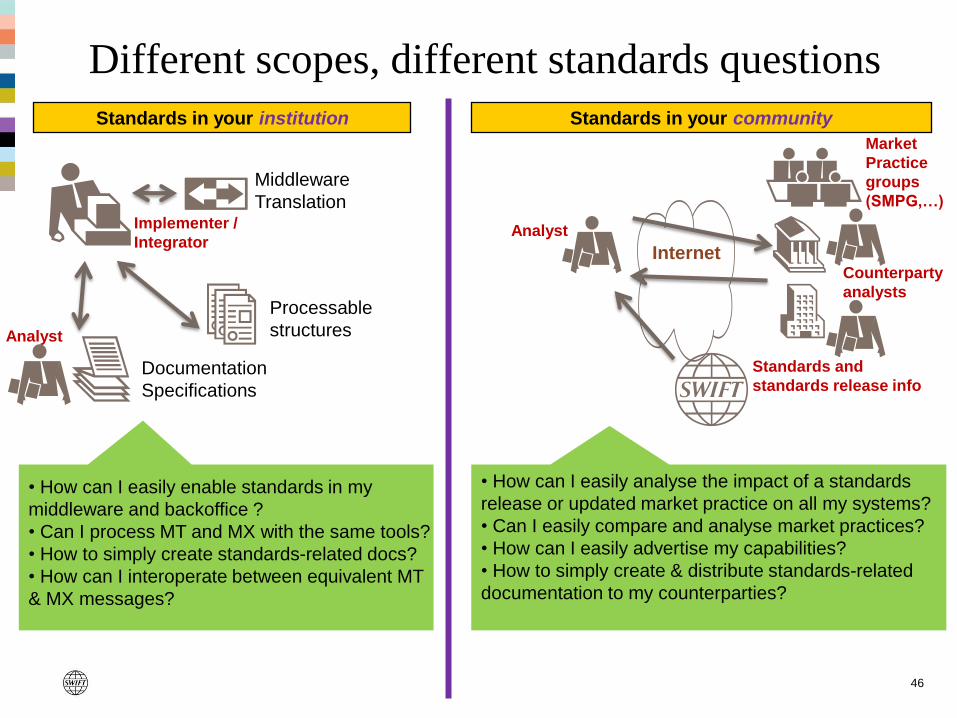

Different scopes, different standards questions

46

Standards in your community Standards in your institution

Middleware

Translation

Processable

structures

Documentation

Specifications

Implementer /

Integrator

Analyst

• How can I easily analyse the impact of a standards

release or updated market practice on all my systems?

• Can I easily compare and analyse market practices?

• How can I easily advertise my capabilities?

• How to simply create & distribute standards-related

documentation to my counterparties?

• How can I easily enable standards in my

middleware and backoffice ?

• Can I process MT and MX with the same tools?

• How to simply create standards-related docs?

• How can I interoperate between equivalent MT

& MX messages?

Analyst

Market

Practice

groups

(SMPG,…)

Counterparty

analysts

Standards and

standards release info

Internet

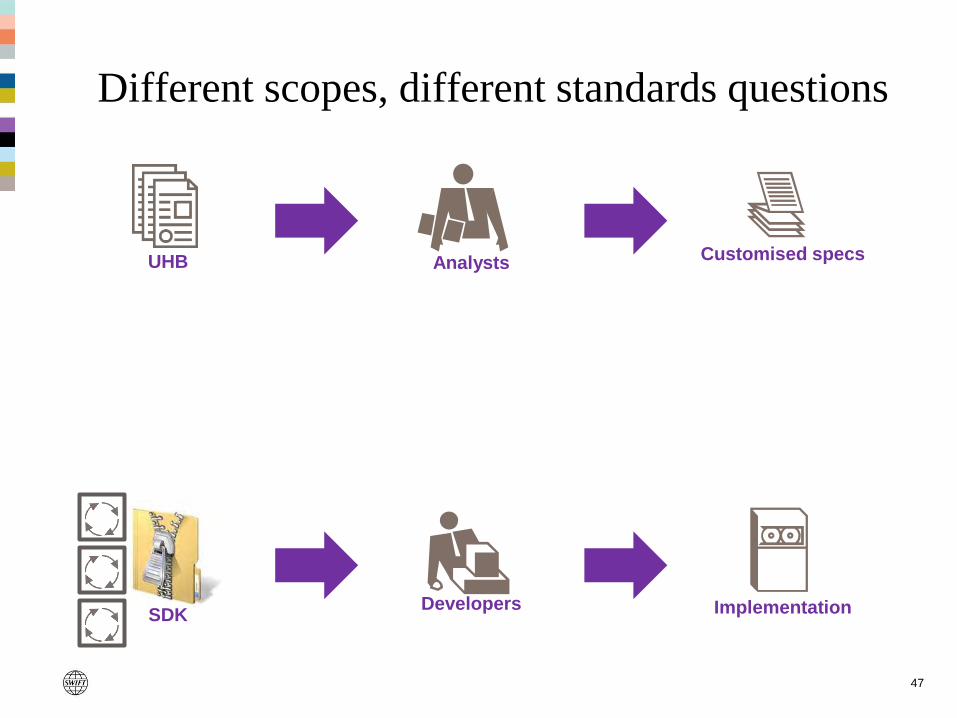

Different scopes, different standards questions

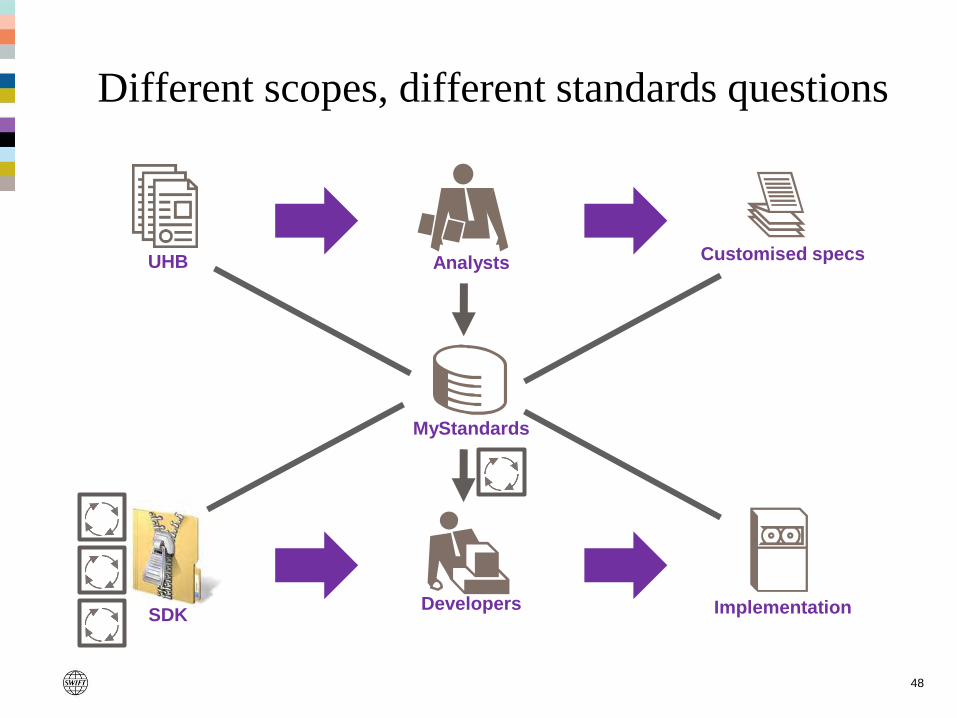

47

UHB

SDK

Analysts Customised specs

Developers Implementation

Different scopes, different standards questions

48

MyStandards

UHB

SDK

Analysts Customised specs

Developers Implementation

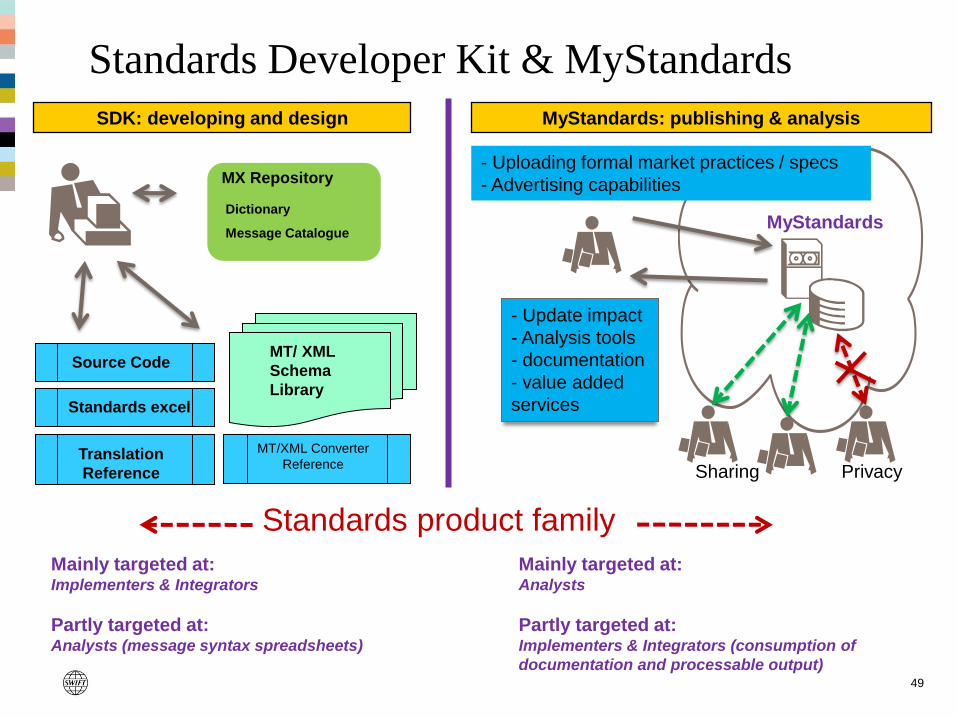

Standards Developer Kit & MyStandards

49

MyStandards: publishing & analysis

- Uploading formal market practices / specs

- Advertising capabilities

MyStandards

- Update impact

- Analysis tools

- documentation

- value added

services

Sharing Privacy

MX Repository

Dictionary

Message Catalogue

MT/ XML

Schema

Library

Translation

Reference

MT/XML Converter

Reference

Standards excel

Source Code

SDK: developing and design

Standards product family

Mainly targeted at: Implementers & Integrators

Partly targeted at: Analysts (message syntax spreadsheets)

Mainly targeted at: Analysts

Partly targeted at: Implementers & Integrators (consumption of

documentation and processable output)

53

Thank you