TRENDS AND FACTS 2017 - Hannover · Lehrte GVZ mega hub A 352 A 37 A 7 A 7 A 2 A 2 ... Pattensen...

52

BUSINESS PROMOTION Location information Issue 3 / 2017 TRENDS AND FACTS 2017

Transcript of TRENDS AND FACTS 2017 - Hannover · Lehrte GVZ mega hub A 352 A 37 A 7 A 7 A 2 A 2 ... Pattensen...

BUSINESS PROMOTION

Location information Issue 3 / 2017

TRENDS AND FACTS 2017

2 TRENDS AND FACTS 2017

TRENDS AND FACTS 2017

A nationwide comparison shows that the Hannover Region is an attractive business location with a high quality of life.

The Hannover Region Business and Employment Promotion department has compiled and presents the most important metrics about the Hannover economic area in this brochure.

We look forward to advising you on any and all topics relating to the loca-tion and consider ourselves to be a service provider for local and foreign companies. So whether you have a question about administration, would like advice on financing and funding opportunities for your company, are looking for land or property or need help with your company to cope with a difficult situation, we are at your service.

Your Hannover Region Business and Employment Promotion department

3

TABLE OF CONTENTS

Location & infrastructure

Population

Employment

Commuter interrelationships

Job market

Economic metrics

Purchasing power & retail

Business enterprises

Key sectors

Education & science

Commercial properties

Commercial plots

Tax assessment rates

Residential

Tourism

Trade fairs

Imprint

4

6

8

14

16

17

18

20

24

30

36

39

40

41

46

48

51

4 TRENDS AND FACTS 2017

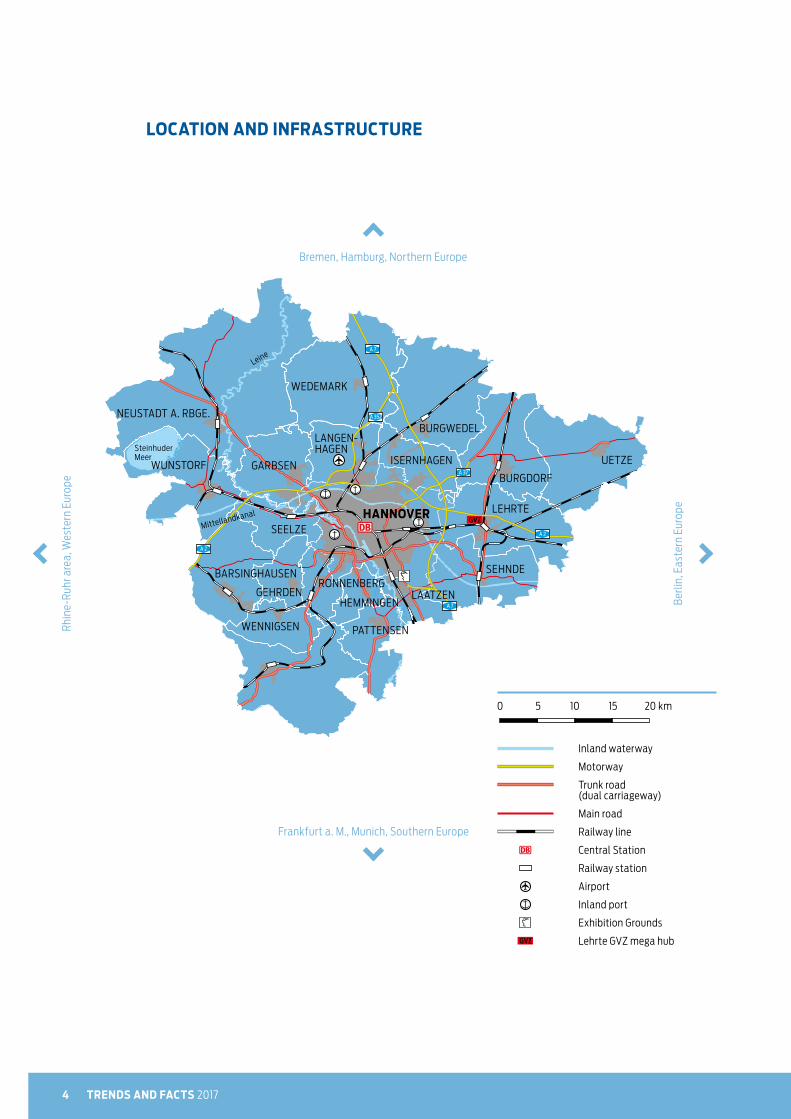

LOCATION AND INFRASTRUCTURE

Bremen, Hamburg, Northern Europe

Frankfurt a. M., Munich, Southern Europe

Rhin

e-Ru

hr a

rea,

Wes

tern

Eur

ope

Berli

n, E

aste

rn E

urop

e

0 5 10 15 20 km

Inland waterway

Motorway

Trunk road (dual carriageway)

Main road

Railway line

Central Station

Railway station

Airport

Inland port

Exhibition Grounds

Lehrte GVZ mega hub

A 352

A 37

A 7

A 7

A 2

A 2

NEUSTADT A. RBGE.

WUNSTORF GARBSEN

LANGEN- HAGEN

WEDEMARK

Leine

Steinhuder Meer

Mittellandkanal

BURGWEDEL

ISERNHAGEN

BURGDORF

UETZE

LEHRTE

SEHNDE

PATTENSEN

HEMMINGEN

WENNIGSEN

BARSINGHAUSEN

GEHRDEN

SEELZEHANNOVER

LAATZENRONNENBERG

5LOCATION AND INFRASTRUCTURE

The Hannover Region is a vital hub within the European

passenger, freight and goods transport infrastructure:

motorways, railway networks, airport, and inland water-

ways provide optimum connections to national and

international economic zones.

This infrastructure is complemented by one of Germany’s best

local public transport systems including a highly integrated

transport network comprising 170 bus lines and 12 LRT lines,

9 regional and 9 suburban railway lines serving 1,900 stops to

ensure excellent connections everywhere. Hannover’s local public

transport system (GVH) counted a record number of passengers

in 2016 – 216.2 million. The high and climbing user figures under-

pin the importance of Hannover as a transport hub.

Travel time by ICE high-speed trainfrom Hannover to (in h:m)

Berlin 01:35

Bremen 00:59

Dortmund 01:38

Dresden 03:52

Essen 02:03

Frankfurt am Main 02:19

Hamburg 01:15

Cologne 02:38

Leipzig 02:40

Munich 04:35

Nuremberg 02:57

Stuttgart 03:54

This close to ...

Traffic figures

Hannover Central Station 250,000 passengers622 regional and intercity trains

dailydaily

Hannover local public transport system (GVH) 216.2 million passengers 2016

Hannover Langenhagen airport 5.41 million passengers 2016

Source: Figures provided by transport and operating companies

6 TRENDS AND FACTS 2017

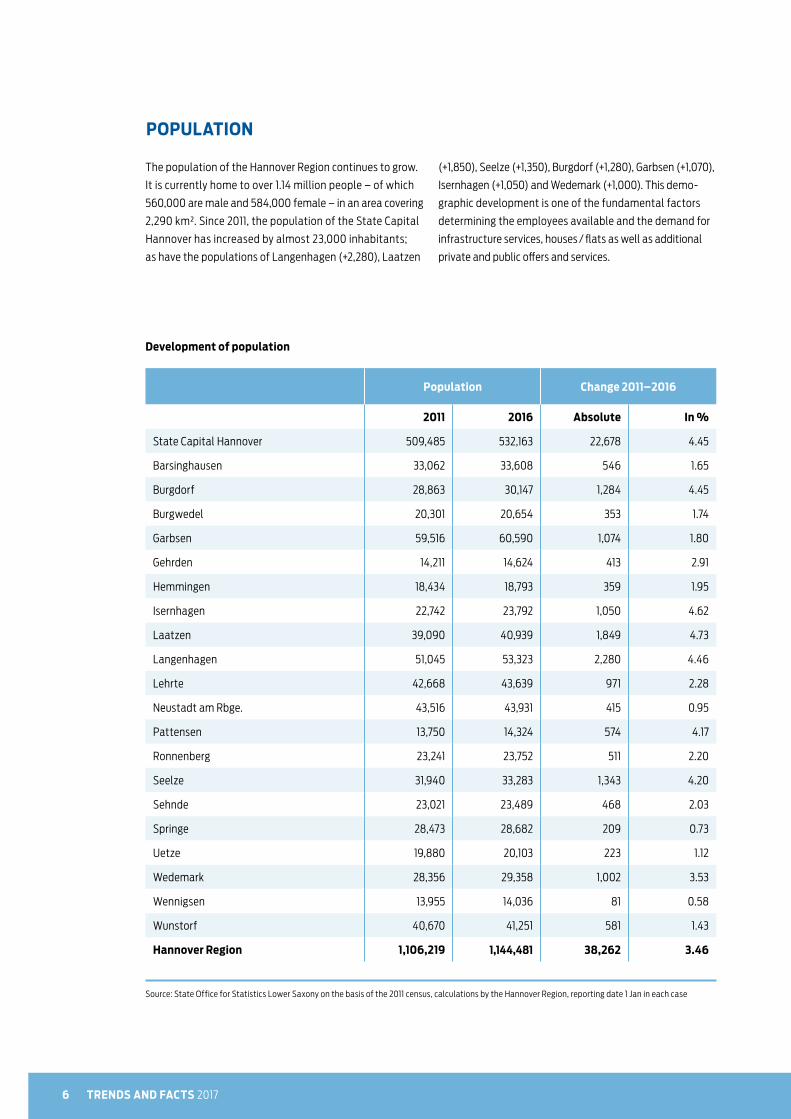

POPULATION

The population of the Hannover Region continues to grow.

It is currently home to over 1.14 million people – of which

560,000 are male and 584,000 female – in an area covering

2,290 km². Since 2011, the population of the State Capital

Hannover has increased by almost 23,000 inhabitants;

as have the populations of Langenhagen (+2,280), Laatzen

(+1,850), Seelze (+1,350), Burgdorf (+1,280), Garbsen (+1,070),

Isernhagen (+1,050) and Wedemark (+1,000). This demo-

graphic development is one of the fundamental factors

determining the employees available and the demand for

infrastructure services, houses / flats as well as additional

private and public offers and services.

Development of population

Population Change 2011–2016

2011 2016 Absolute In %

State Capital Hannover 509,485 532,163 22,678 4.45

Barsinghausen 33,062 33,608 546 1.65

Burgdorf 28,863 30,147 1,284 4.45

Burgwedel 20,301 20,654 353 1.74

Garbsen 59,516 60,590 1,074 1.80

Gehrden 14,211 14,624 413 2.91

Hemmingen 18,434 18,793 359 1.95

Isernhagen 22,742 23,792 1,050 4.62

Laatzen 39,090 40,939 1,849 4.73

Langenhagen 51,045 53,323 2,280 4.46

Lehrte 42,668 43,639 971 2.28

Neustadt am Rbge. 43,516 43,931 415 0.95

Pattensen 13,750 14,324 574 4.17

Ronnenberg 23,241 23,752 511 2.20

Seelze 31,940 33,283 1,343 4.20

Sehnde 23,021 23,489 468 2.03

Springe 28,473 28,682 209 0.73

Uetze 19,880 20,103 223 1.12

Wedemark 28,356 29,358 1,002 3.53

Wennigsen 13,955 14,036 81 0.58

Wunstorf 40,670 41,251 581 1.43

Hannover Region 1,106,219 1,144,481 38,262 3.46

Source: State Office for Statistics Lower Saxony on the basis of the 2011 census, calculations by the Hannover Region, reporting date 1 Jan in each case

7POPULATION

POPULATION

Change 2011–2016 in %

Change in population 2011–2016 in %

more than 4

2 to below 4

0 to below 2

Population

Change 2011–2016 absolute

Increase

10,000

750

1,500

Barsinghausen

Burgdorf

Burgwedel

Garbsen

GehrdenHem- mingen

Isernhagen

Laatzen

Langenhagen

Hannover

Lehrte

Springe

Neustadt a. Rbge.

Sehnde

Seelze

Wunstorf

Ronnen- berg

Pattensen

Wedemark

Wennigsen

Uetze

8 TRENDS AND FACTS 2017

Change According to gender

2015 2016 Absolute In % Male Female

State Capital Hannover 308,272 313,018 4,746 1.54 164,895 148,123

Barsinghausen 7,492 7,804 312 4.16 4,128 3,676

Burgdorf 5,456 5,694 238 4.36 2,451 3,243

Burgwedel 8,844 9,169 325 3.67 4,090 5,079

Garbsen 14,367 13,618 –749 –5.21 6,629 6,989

Gehrden 3,238 3,472 234 7.23 1,570 1,902

Hemmingen 3,825 3,766 –59 –1.54 2,151 1,615

Isernhagen 9,755 10,010 255 2.61 6,132 3,878

Laatzen 15,128 15,512 384 2.54 8,499 7,013

Langenhagen 32,031 32,429 398 1.24 20,207 12,222

Lehrte 12,580 12,799 219 1.74 7,505 5,294

Neustadt am Rbge. 9,404 9,488 84 0.89 4,338 5,150

Pattensen 3,531 3,502 –29 –0.82 1,730 1,772

Ronnenberg 4,258 4,574 316 7.42 2,581 1,993

Seelze 5,697 5,972 275 4.83 3,533 2,439

Sehnde 5,829 5,888 59 1.01 2,852 3,036

Springe 6,796 6,617 –179 –2.63 3,245 3,372

Uetze 3,201 3,335 134 4.19 1,811 1,524

Wedemark 7,021 7,162 141 2.01 3,790 3,372

Wennigsen 2,492 2,570 78 3.13 1,195 1,375

Wunstorf 11,597 11,587 –10 –0.09 6,010 5,577

Hannover Region 480,814 487,986 7,172 1.49 259,342 228,644

EMPLOYMENT

One key indicator for the economic growth and prosperity

of a region is a positive development in employment figures.

In the Hannover Region the number of employees in work

and paying social insurance contributions has again risen

year-on-year to reach an absolute record high of over

488,000 (+7,200), of which 259,300 are men and 228,650

women. The key centre of employment in the region is the

State Capital Hannover with a workforce of over 313,000.

Around 175,000 people are employed in the surrounding

area. The largest relative growth was achieved in Ronnen-

berg and Gehrden.

Employees paying social insurance contributions at their place of work

Source: Federal Labour Office, audited results, calculations by the Hannover Region, reporting date 1 Jan in each case

9EMPLOYMENT

Employees paying social insurance contributions at their place of work

change 2015–2016 in %

Change 2015–2016 in %

more than 4

2 to below 4

0 to below 2

–6 to below 0

Employees

Increase Decrease

7,000

250

500

Barsinghausen

Burgdorf

Burgwedel

Garbsen

GehrdenHem- mingen

Isernhagen

Laatzen

Langenhagen

Hannover

Lehrte

Springe

Neustadt a. Rbge.

Sehnde

Seelze

Wunstorf

Ronnen- berg

Pattensen

Wedemark

Wennigsen

Uetze

10 TRENDS AND FACTS 2017

The share of employees in the Hannover Region with an

academic professional qualification has again risen and

is now at 18.2 %, much higher than in Lower Saxony and

Germany as a whole.

The proportion of employees aged between 15 and 24 has

again fallen year-on-year. There has been a slight increase

in the proportion of foreign employees (9.6 %)

Employees paying social

insurance contributions

according to gender

Employees paying social

insurance contributions in

full-time employment

Employees paying social

insurance contributions in

part-time employment

Source: Federal Labour Office, audited results, calculations by the Hannover Region, reporting date 30.06.2016

100 %

80 %

60 %

40 %

20 %

0 %

Germany

53.6 46.4

100 %

80 %

60 %

40 %

20 %

0 %

Lower Saxony Germany

Female

Male

65.1 34.9 68.6 31.4 66.133.9

100 %

80 %

60 %

40 %

20 %

0 %

Hannover Region Lower Saxony Germany

20.4 79.617.7

82.322.7 77.3

Hannover Region

53.146.9

228,644

259,342

Lower Saxony

54.2 45.8

1,290,553

1,529,704

14,544,681

16,829,010

Hannover Region

122,159

227,986

635,013

1,388,629

7,741,590

15,083,746

106,477

31,349

655,500

141,019

6,802,785

1,744,845

Female

Male

Female

Male

11EMPLOYMENT

Employees paying social

insurance contributions

according to nationality

Employees paying social insurance

contributions according to level

of education

Source: Federal Labour Office, audited results, calculations by the Hannover Region, reporting date 30.06.2016

100 %

80 %

60 %

40 %

20 %

0 %

Hannover Region

9.6 90.4

Lower Saxony

7.1 92.9

Germany

1090

100 %

80 %

60 %

40 %

20 %

0 %

18.2

68.6

13.2

Lower Saxony

373,225

2,073,528

373,504

Germany

5,266,669

21,972,129

4,134,893

13.2

73.5

13.3 16.8

70

13.2

2,617,869

201,344

440,823

46,833

28,227,842

3,129,357

Hannover Region

88,884

334,918

64,184

German

Foreign

Employees paying social insurance

contributions according to

age structure

100 %

80 %

60 %

40 %

20 %

0 %

72.6

9.217.3

0.9

70.9

10.817.5

0.9

71.7

9.817.7

0.8

Hannover Region

44,797

354,414

84,617

4,158

Germany

3,084,668

22,482,643

5,551,853

254,526

Lower Saxony

303,543

1,998,702

493,415

24,597

Academic professional qualification

Vocational training

No vocational training

15–24 years of age

25–49 years of age

50–64 years of age

over 65 years of age

12 TRENDS AND FACTS 2017

The Hannover Region boasts a balanced economic structure

and a diverse spectrum of dynamic business sectors. This is

reflected in the distribution of people in work and paying

social insurance contributions according to economic sec-

tors. The number of persons paying social insurance contri-

butions rose in almost all economic sectors in comparison

to the previous year. Most jobs are in health and social services

(69,900), in manufacturing industries (67,530) and in trade

(65,180). Almost all economic sectors have seen a year on year

increase in job figures. There was significant jobs growth in art,

entertainment and recreation (+6.9 %) and in health and

social services (+5.3 %).

13EMPLOYMENT

2015 2016 Change

Absolute Share in % Absolute Share in % Absolute In %

Agriculture, forestry, fishing 1,297 0.3 1,270 0.3 –27 –2.1

Mining and pit & quarry industries 1,700 0.4 1,468 0.3 –232 –13.6

Manufacturing industries 67,505 14.0 67,528 13.8 23 0.0

Energy supply, water supply; sewage and waste disposal, and cleaning up environmental contamination

4,011 0.8 3,855 0.8 –156 –3.9

Other supply and disposal industries 3,983 0.8 3,891 0.8 –92 –2.3

Construction industry 20,450 4.3 21,042 4.3 592 2.9

Trading; maintenance and repair of vehicles 64,998 13.5 65,176 13.4 178 0.3

Transport and warehousing 31,918 6.6 32,276 6.6 358 1.1

Hospitality sector 14,954 3.1 15,299 3.1 345 2.3

Information and communication 20,119 4.2 20,058 4.1 –61 –0.3

Financial and insurance service providers 25,020 5.2 25,364 5.2 344 1.4

Real estate and property sector 3,701 0.8 3,808 0.8 107 2.9

Freelance, scientific and technical service providers

34,103 7.1 34,393 7.0 290 0.9

Other economic service providers 46,470 9.7 48,257 9.9 1,787 3.8

Public sector, defence; social insurance 31,536 6.6 32,656 6.7 1,120 3.6

Child care and education 22,107 4.6 20,607 4.2 –1,500 –6.8

Health and social services 66,499 13.8 69,993 14.3 3,494 5.3

Art, entertainment and recreation 5,537 1.2 5,920 1.2 383 6.9

Other service providers 14,333 3.0 14,541 3.0 208 1.5

Private households 559 0.1 584 0.1 25 4.5

Total 480,800 100.0 487,986 100.0 7,186 1.5

Source: Federal Labour Office, audited results, calculations by the Hannover Region, reporting date 30.06.2016

Employees paying social insurance contributions according to economic sector

14 TRENDS AND FACTS 2017

COMMUTING INTERRELATIONSHIPS

2016 saw the number of commuters coming into the

Hannover Region from outside rise to almost 125,000, a

figure approximately 25,000 higher than only 10 years ago.

Most of the incoming commuters come from the adjacent

districts of Hildesheim, Schaumburg, Celle, Peine, Hameln-

Pyrmont, Nienburg / Weser, Heidekreis and Gifhorn.

However, many commuters travel within the Hannover

Region. In addition to the State Capital Hannover (+115,200),

positive net commuter figures are also reported by Langen-

hagen (+11,800), Isernhagen (+1,700), Burgwedel (+1,800)

and Laatzen (+1,100).

*EPSI : Employees in jobs paying social insurance contributions

Source: Federal Labour Office, audited results, calculations by the Hannover Region, reporting date 30.06.2016

Commuting interrelationships

Inward commuters

Outward commuters Net

in % of EPSI* at the place

of residence

State Capital Hannover 173,315 58,132 115,183 58.3

Barsinghausen 4,410 8,883 –4,473 –36.4

Burgdorf 3,244 8,401 –5,157 –47.5

Burgwedel 6,920 5,130 1,790 24.3

Garbsen 8,927 18,125 –9,198 –40.3

Gehrden 2,563 4,279 –1,716 –33.1

Hemmingen 2,927 5,674 –2,747 –42.2

Isernhagen 8,639 6,942 1,697 20.4

Laatzen 12,701 11,628 1,073 7.4

Langenhagen 26,471 14,684 11,787 57.2

Lehrte 8,548 12,583 –4,035 –24.0

Neustadt am Rbge. 4,406 10,977 –6,571 –40.9

Pattensen 2,534 4,416 –1,882 –35.0

Ronnenberg 3,495 7,805 –4,310 –48.5

Seelze 4,081 11,195 –7,114 –54.4

Sehnde 4,283 7,442 –3,159 –34.9

Springe 3,588 7,231 –3,643 –35.5

Uetze 1,611 5,877 –4,266 –56.2

Wedemark 4,529 8,294 –3,765 –34.5

Wennigsen 1,822 4,138 –2,316 –47.4

Wunstorf 6,804 10,201 –3,397 –22.7

Hannover Region 124,301 60,520 63,781 15.0

15COMMUTING INTERRELATIONSHIPS

IN 2016, THE HANNOVER REGION COUNTED ALMOST 125,000 COMMUTERS COMING IN FROM OUTSIDE THE REGION, WHICH IS AROUND 25,000 HIGHER THAN THE FIGURE ONLY 10 YEARS AGO.

Hannover

Neustadt a. Rbge.

Wunstorf

Garbsen

Wedemark Burgwedel

Burgdorf UetzeIsernhagen

Seelze Lehrte

SehndeBarsinghausen

Wennigsen

Springe

Pattensen

HemmingenGehrden Ronnen-

berg

Langenhagen

Laatzen

7,23

1

3,58

8

4,41

6

2,53

44,13

8

1,822

5,67

4

2,92

77,805

3,49

5

4,27

9

2,56

3

8,88

3

4,41

0

11,19

5

4,08

1

11,6

28

12,7

01 7,442

4,28

3

12,5

83

8,54

8

58,13

2

173,

315

10,2

01

6,80

4

18,12

5

8,92

7 14,6

84

26,4

71

6,94

2

8,63

9

8,40

1

3,22

4

5,87

7

1,611

5,13

0

6,92

0

8,29

4

4,52

9

10,9

77

4,40

6

more than 45 %

0 % to below 45 %

–45 % to below 0 %

more than –45 %

Inward commuters

Outward commuters

Commuter interrelationships

16 TRENDS AND FACTS 2017

JOB MARKET

Source: Federal Labour Office, calculations by the Hannover Region

Unemployment figures in the Hannover Region

The number of unemployed and the

unemployment rates in Hannover Region

have again fallen compared to the previous

year. In June 2017, some 43,500 (–2,250)

people were out of work; this corresponds

to an unemployment rate of 7.1 % (–0.4 %)

with respect to the total civil workforce.

There are approximately 18,000 persons

registered as long-term unemployed,

of which 14,200 are foreigners, 2,000

severely disabled, 13,200 older persons

and 3,900 people under the age of 25.

Figures in % Change in % points

With respect to ... June 2016 June 2017

Total civil workforce

7.5 7.1 –0.4

Male 8.0 7.4 –0.6

Female 6.9 6.7 –0.2

15 to less than 25 years of age

7.3 6.4 –0.9

15 to less than 20 years of age

5.3 4.2 –1.1

50 to less than 65 years of age

7.2 6.8 –0.4

55 to less than 65 years of age

7.6 7.1 –0.5

Source: Federal Labour Office, calculations by the Hannover Region

Unemployment rate in the Hannover Region

June 2016 June 2017 Change

Absolute Share in % Absolute Share in % Absolute In %

Total 45,753 100.0 43,495 100.0 –2,258 –4.9

Male 25,492 55.7 23,945 55.1 –1,547 –6.1

Female 20,261 44.3 19,550 44.9 –711 –3.5

15 to less than 25 years of age

4,450 9.7 3,934 9.0 –516 –11.6

Over 50 years of age 13,800 30.2 13,246 30.5 –554 –4.0

Long-term unemployed

19,267 42.1 18,118 41.7 –1,149 –6.0

Severely disabled 2,188 4.8 2,025 4.7 –163 –7.4

Foreigners 14,595 31.9 14,210 32.7 –385 –2.6

17

ECONOMIC METRICS

The gross domestic product (GDP) per head of the working

population is a key metric for employment productivity.

The GDP per capita is a key metric for the prosperity of a

region. In the Hannover Region both of these parameters

fall well above the federal and state averages: GDP per

head of the working population is € 69,300 while GDP per

capita is approx. € 40,500. The gross added value, which

reflects the total value of all produced goods and services,

also shows the Hannover Region having per-capita values

higher than the federal and state figures. This highlights

the strong competitiveness of the Hannover Region.

JOB MARKET . ECONOMIC METRICS

Source: National accounts of the states, federal and state statistics offices, calculations by the Hannover Region

Source: National accounts of the states, federal and state statistics offices, calculations by the Hannover Region

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

per capita in € per working person in €2013

35,9

19

27,9

90

31,4

57

2014

36,4

83

28,6

31

32,3

90

2013

61,8

91

56,0

08

59,9

33

2014

62,3

81

56,8

59

61,4

26

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

per capita in € per working person in €2013

39,9

39

31,12

3

34,9

78

2014

40

,552

31,8

24

36,0

03

201368

,819

62,

277

66,6

42

2014

69,3

38

63,2

01

68,2

77 Hannover Region

Lower Saxony

Germany

Hannover Region

Lower Saxony

Germany

Gross added value

Gross Domestic Product

18 TRENDS AND FACTS 2017

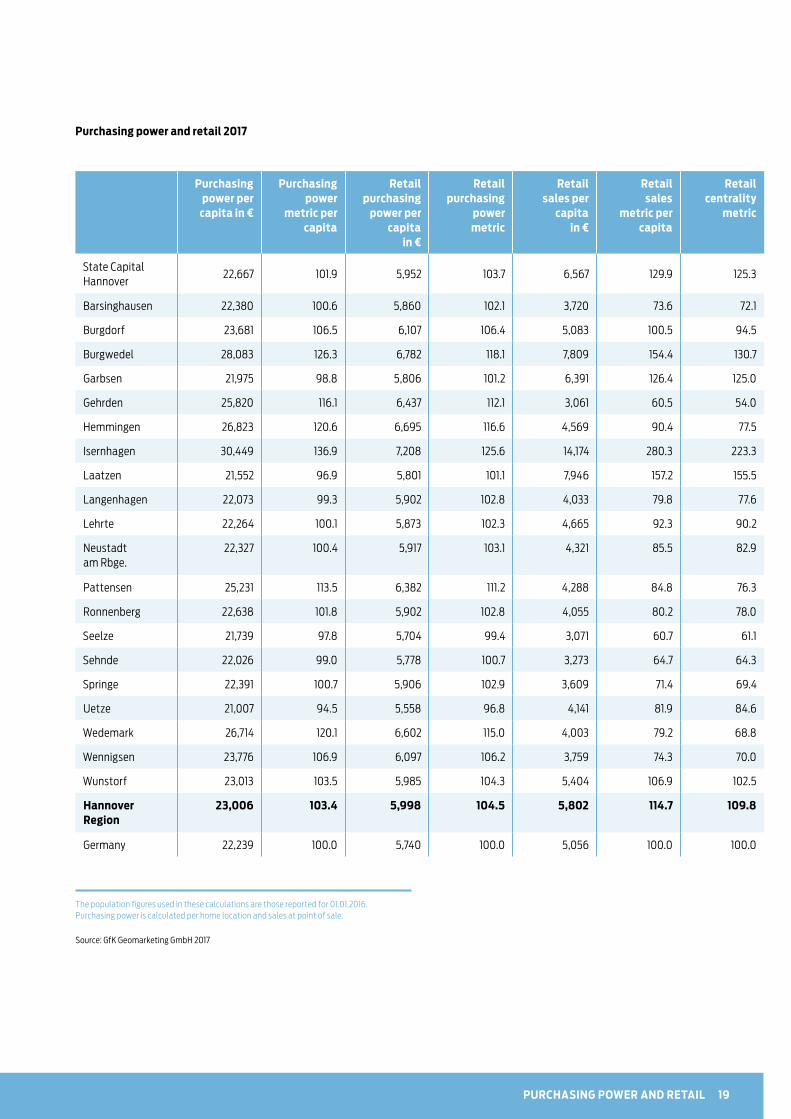

PURCHASING POWER AND RETAIL TRADE

Purchasing power

Purchasing power is defined as total net income of the population with respect to their place of residence. This figure includes net income from self-employed or non-self-employed work, as well as investment income and state transfer payments. This available income covers all expenses incurred by a consumer such as living costs, insurance, rent payments and ancillary costs, clothing, and savings. The purchasing power metric indicates the deviation from the federal average in per cent (index level = 100).

Retail-relevant purchasing power

The retail-relevant purchasing power is determined by only including those parts available for purchasing from retailers, including food and non- essential food items, clothing, shoes, household goods, body and health care, education and entertainment, and personal furnishings. Expenditure associated with vehicles and fuel, as well as services and repairs, are not included. The retail-relevant purchasing power metric shows the deviation in per cent from the federal average (index level = 100).

Retail sales

The retail sales reflect the actual distribution of stationary retail sales. Unlike the retail purchasing power, which is reported for the locations where the consumers live, the retail sales metric is reported for the location of the retail outlets. The sales metric shows the deviation in per cent from the federal average (index level = 100). Positive deviations above the base level indicate a retail sector with strong sales, whilst a negative deviation below the base level indicates relatively low sales.

Retail centrality

Retail centrality is calculated from the ratio of the potential retail pur- chasing power of a location and the actual retail sales at a location. It is therefore a measure of the attractiveness of a city or region as a shopping destination. Figures above 100 indicate a net inflow of purchasing power, i.e. retail sales at the specific location are higher than the amount spent on shopping by the local inhabitants. A figure below 100 means a net outflow of purchasing power, i.e. local retailers report lower sales than actually spent by the local inhabitants.

Begriffserklärung:

The purchasing power in

Hannover Region totals € 25.36

billion, corresponding to an

average purchasing power of

€ 23,006 per capita or 103.4 %

of the average purchasing

power in Germany.

The retail purchasing power

totals € 6.86 billion. The

average retail purchasing

power per capita is € 5,998 or

104.5 % of the average retail

purchasing power in Germany.

The actual retail sales amount

to € 6.64 billion. This corresponds

to retail sales of € 5,802 per

capita, or 114.7 % of the average

retail sales in Germany.

19PURCHASING POWER AND RETAIL

Purchasing power per

capita in €

Purchasingpower

metric percapita

Retailpurchasing

power percapita

in €

Retailpurchasing

powermetric

Retailsales per

capitain €

Retailsales

metric percapita

Retailcentrality

metric

State Capital Hannover

22,667 101.9 5,952 103.7 6,567 129.9 125.3

Barsinghausen 22,380 100.6 5,860 102.1 3,720 73.6 72.1

Burgdorf 23,681 106.5 6,107 106.4 5,083 100.5 94.5

Burgwedel 28,083 126.3 6,782 118.1 7,809 154.4 130.7

Garbsen 21,975 98.8 5,806 101.2 6,391 126.4 125.0

Gehrden 25,820 116.1 6,437 112.1 3,061 60.5 54.0

Hemmingen 26,823 120.6 6,695 116.6 4,569 90.4 77.5

Isernhagen 30,449 136.9 7,208 125.6 14,174 280.3 223.3

Laatzen 21,552 96.9 5,801 101.1 7,946 157.2 155.5

Langenhagen 22,073 99.3 5,902 102.8 4,033 79.8 77.6

Lehrte 22,264 100.1 5,873 102.3 4,665 92.3 90.2

Neustadt am Rbge.

22,327 100.4 5,917 103.1 4,321 85.5 82.9

Pattensen 25,231 113.5 6,382 111.2 4,288 84.8 76.3

Ronnenberg 22,638 101.8 5,902 102.8 4,055 80.2 78.0

Seelze 21,739 97.8 5,704 99.4 3,071 60.7 61.1

Sehnde 22,026 99.0 5,778 100.7 3,273 64.7 64.3

Springe 22,391 100.7 5,906 102.9 3,609 71.4 69.4

Uetze 21,007 94.5 5,558 96.8 4,141 81.9 84.6

Wedemark 26,714 120.1 6,602 115.0 4,003 79.2 68.8

Wennigsen 23,776 106.9 6,097 106.2 3,759 74.3 70.0

Wunstorf 23,013 103.5 5,985 104.3 5,404 106.9 102.5

Hannover Region

23,006 103.4 5,998 104.5 5,802 114.7 109.8

Germany 22,239 100.0 5,740 100.0 5,056 100.0 100.0

The population figures used in these calculations are those reported for 01.01.2016. Purchasing power is calculated per home location and sales at point of sale.

Source: GfK Geomarketing GmbH 2017

Purchasing power and retail 2017

20 TRENDS AND FACTS 2017

BUSINESS ENTERPRISES

NORD/LB publishes an annual ranking of Lower Saxony’s

businesses with the highest sales and value added results.

These companies safeguard the jobs and incomes of the

neighbouring commercial, trade and services enterprises

and are therefore the economic backbone of the location.

27 of the 100 companies in Lower Saxony with the highest

sales have their registered head offices in the Hannover

Region. 15 of these companies work in the manufacturing

sector. They are dominated by the automotive industry

and its subcontractors, and also include businesses in the

electronic engineering, aircraft construction, chemical and

food sectors. Large trading and service companies are also

headquartered in the Hannover Region.

Of the 50 companies in Lower Saxony with the highest value

added, 22 are located in the Hannover Region, including

enterprises working in the health, insurance and financial

sectors which are not reported under the companies with

the highest sales values.

Company Registered seat

Sales in € million

Employees Sector Ranking in Lower

Saxony

Continental AG (K)

ContiTech AG (K)Hannover

39,232.0

5,367.0

207,461

42,648

Automotive subcontracting industry

2

TUI AG (K)** Hannover 20,011.6 71,242 Tourism 3

Volkswagen Nutzfahrzeuge Hannover 10,341.0 20,800Commercial vehicle construction

1

AGRAVIS Raiffeisen AG (K) Hannover 6,934.5 6,233 Agricultural trading 6

DIRK ROSSMANN GMBH Burgwedel 5,024.6 26,318Wholesale and retail (drugstore articles)

8

Stadtwerke Hannover AG Hannover 2,311.6 2,274Energy supplies, energy services

19

Johnson Controls Power Solutions Europe (K)**

Johnson Controls Autobatterie GmbH & Co. KGaA **

Hannover

1,854.4

1,249.7

3,106

482

Accumulator and battery production

23

Expert AG(K)** Langenhagen 1,749.7 1,509Wholesale and retail (elec-trical and electronic devices)

24

Siemens AG** Laatzen 1,618.5 3,792 Electrical engineering 24

WABCO Holding GmbH (K) Hannover 1,200.9 2,552Automotive subcontracting industry

32

Konica Minolta Business Solutions Europe GmbH*

Langenhagen 1,186.4 415Production and marketing of printers and photocopiers

33

TÜV NORD Gruppe (K) Hannover 1,116.6 9,861 Technical services 35

Solvay Deutschland (Group) Hannover 1,110.4 2,639 Chemical industry 36

Companies with highest sales based in the Hannover Region

21BUSINESS ENTERPRISES

Company Registered seat

Sales in € million

Employees Sector Ranking in Lower

Saxony

MTU Maintenance Hannover GmbH Langenhagen 1,078.6 1,855 Aircraft engine maintenance 37

NEXANS DEUTSCHLAND GMBH GRUPPE (K) Hannover 965.7 11,437 Cable manufacturing 42

BauKing AG (K) Hannover 826.4 3,349Wholesale and retail (construction materials)

46

Sonepar Deutschland/ Region Nord-Ost GmbH

Hannover 804.6 1,558 Wholesale (electronics) 47

Toto-Lotto Niedersachsen GmbH Hannover 747.8 155 Lottery company 50

Sennheiser electronic GmbH & Co. KG (K) Wedemark 682.2 2,704 Electro-acoustics 57

Verlagsgesellschaft Madsack GmbH & Co. KG (K)

Hannover 649.5 5,280 Publishing 59

GP Günter Papenburg AG (K) Hannover 635.6 3,252 Construction industry 62

Klinikum Region Hannover GmbH Hannover 571.4 5,626 Health sector 67

Delticom AG (K) Hannover 559.8 129 Retail 68

Bahlsen Gruppe (K)

Bahlsen GmbH & Co. KGHannover

533.7

382.4

2,400

1,563Food industry 73

Konica Minolta Business Solutions Deutschland GmbH*

Langenhagen 461.4 1,781Production and marketing of computers and photocopiers

79

Kone GmbH (K) Hannover 412.5 1,912Production of elevators and escalators

88

CB-Group (K) Hannover 370.2 645 Chemical distribution 93

22 TRENDS AND FACTS 2017

Company Registered seat

Turnover in € million

Employees Sector Ranking in Lower

Saxony

Talanx AG (K)Hannover

2,758.0 21,892Insurance, re-insurance 4

Hannover Rück SE (K) 2,483.1 2,568

NORD/LB (K)Hannover

1,306.6 6,023Financial services 6

NORD LB 533.3 4,070

Medizinische Hochschule Hannover Hannover 484.5 7,842 Health 16

VHV Vereinigte Hannoversche Versicherung a.G. (K)

VHV Allgemeine Versicherung AG

Hannover

443.1

205.2

2,914

367

Insurance 19

Nds. Wach- und Schließgesellschaft Eggeling u. Schorling KG (K)

Hannover 176.1 5,100 Personal and property security 47

Versicherungsgruppe Hannover VGH Hannover 170.3 1,827 Insurance 49

Sparkasse Hannover Hannover 169.5 2,025 Financial services 50

Companies with the highest sales based in the Hannover Region (extract)

K = consolidated conglomerate or group

* Figures for the 2015/2016 financial year

** Figures for the 2014/2015 financial year

Methodology: The companies are considered in their entirety as conglome-rates or groups to reflect the particular role played by group HQs in economic terms. However, this also means that not all turnover, added value and employees reported here apply to the Hannover Region specifically. The NORD/LB analysis only considers companies domiciled in Lower Saxony or who provide data on activities in Lower Saxony. Other companies, for example units of major companies, who may be of high regional economic importance, but are not separately reported, are not included in the NORD/LB listings.

Source: NORD/LB (November 2016): Niedersachsen Report – 100 biggest companies in Lower Saxony

23

Almost 51,000 businesses in a range of economic sectors

are registered in the Hannover Region, including around

44,000 mini businesses with less than 9 employees, and

over 237 major businesses with more than 250 employees.

Almost one in five of these businesses works in the trading

sector. This is followed by freelance and scientific services

businesses (e.g. firms of architects or engineers, legal and

tax consultants, advertising companies and market

research companies), the property and housing sector,

building industry, and health and social services.

BUSINESS ENTERPRISES

AbsoluteShare

in %

Mining and pit and quarry industries 22 0.04

Manufacturing industry 2,268 4.46

Energy supplies 381 0.75

Water supplies, wastewater and waste disposal

114 0.22

Construction industry 4,426 8.70

Trading; servicing and repair of motor vehicles

9,545 18.76

Transport and storage 1,853 3.64

Hospitality sector 3,258 6.40

Information and communications 2,063 4.06

Finance and insurance services 1,098 2.16

Property and housing industry 4,517 8.88

Freelance, scientific and technical services 8,144 16.01

Other business services 3,097 6.09

Child care and education 1,332 2.62

Health and social services 3,825 7.52

Art, entertainment and recreation 1,586 3.12

Other services 3,338 6.56

Total 50,867 100.00

Businesses in the Hannover Region according to economic sector

Source: State Office of Statistics Lower Saxony, calculations by the Hannover Region, reporting date 29 Feb 2016

0 to 9 44,601

10 to 49 4,894

50 to 249 1,135

250 and more 237

Total 50,867

Businesses in the Hannover Region according to size of workforce

Source: State Office of Statistics Lower Saxony, calculations by the Hannover Region, reporting date 29 Feb 2016

24 TRENDS AND FACTS 2017

KEY SECTORS

The current business structure in the Hannover Region is

characterised by 12 key sectors boasting major innovation

and job creation potential. More than 70 % of all emplo-

yees paying social insurance contributions work in these

key sectors.

hannoverimpuls, the region’s business promotion organi-

sation, targets funding to the key sectors in the fields of

“energy and mobility”, “digital economy and production

Automotive industry

23,500 EPSIs* in the whole automotive value chain (4.9 % of TW**)

Together with Braunschweig and Wolfsburg, the Hannover Region is one of

the most significant international automotive centres

Resident companies: VW Nutzfahrzeuge, Continental AG, as well as

numerous subcontractors such as WABCO and Johnson Controls

Main activities: commercial vehicles, tyres, drive systems, special compo-

nents, braking systems, battery technology, vehicle information systems

Education and research institutes: 30 institutes and university facilities

associated with the automotive industry

The metropolitan region was subsidised by the federal programme

“Schaufenster Elektromobilität” (E-mobility showcase)

ITS Automotive as a cross-disciplinary mobility cluster for research

group projects

Flagship trade fairs: IAA commercial vehicles, Mobilitec incorporated within

Hannover Messe

Energy solutions

4,100 EPSIs* (0.9 % of TW**) in 65 companies

Resident companies: power station operators E.ON Kernkraft and enercity

as well as the largest energy utility and companies involved in the develop-

ment and implementation of new technologies (e.g. CHP-manufacturer

A-Tron, energiewerkstatt or Kraftwerk, Windwärts Energie, GeoNet –

Umweltconsulting)

Education and research organisations: 20 institutes and university facilities

involved in the energy industry, for example in wind power

Networks: Leibniz research centre Energie 2050 ForWind (research network

into wind power), climate protection agency Hannover Region,

Geozentrum Hannover

The world’s first wind turbine tower with a wooden construction and the first

biogas plant in North Germany which can feed biogas into natural gas grid

Flagship trade fairs: BioEnergy Decentral and Energy and wind, both

incorporated in the Hannover Messe

engineering”, “life sciences and medical technology” and

“the creative sector and multimedia”.

Other important sectors in the Hannover Region’s job

market continue to be the logistics industry, financial

services, knowledge-based services and the trades. The

conference and trade fair sector boosts national and

international awareness of the business location and

has a positive impact on Hannover Region’s image.

25KEY SECTORS

Health care

66,200 EPSIs* (13.8 % of TW**) in some 3,400 en-

terprises

Strong university and extra-university research and

education: Hannover Medical School, University

of Veterinary Medicine Hannover, Life Science at

Leibniz University Hannover, Hannover Clinical Trial

Centre, Fraunhofer Institute for Toxicology and

experimental medicine (ITEM), Lower Saxony

Centre for Biomedical Technology, Implant Research

and Development (NIFE), Clinical Research Centre

(CRC), Twincore Centre for Experimental and Clinical

Infection Research

Key clinic site and major players such as

Abbot Pharmaceuticals, Boehringer Ingelheim,

KIND Hörgeräte

Medical Park Hannover is the central business and

research location focusing on biomedical technology,

transplants, implants, regenerative medicine, diagnos-

tics, pre-clinical and clinical research and training

Network: Gesundheitswirtschaft Hannover e. V.

Flagship fairs: Altenpflege and Biotechnica –

Labvolution

Production engineering

12,400 EPSIs* (2.6 % of TW**) in 455 enterprises

Education and research: production Engineering

Centre (PZH), mechanical engineering faculty of

Leibniz University Hannover, mechanical engineering,

electrical engineering and information technology

departments of the University of Applied Sciences

and Arts Hannover

Cooperation with the Laser Centre Hannover (LZH),

the Institute for Integrated Production Hannover

(IPH), the Mechatronics Centre Hannover (MZH)

and the German Institute for Rubber Technology

(DIK)

Robotation Academy as a training and event centre

for robots and automation technology

Location of the German government’s Mittelstand 4.0

competence centre for Lower Saxony and Bremen

Networks: e.g. mit uns digital, competence network

optical technologies

Flagship fairs: Hannover Messe, EuroBLECH,

Agritechnica, EMO and LIGNA

* EPSI: employees paying social insurance contributions ** TW: total workforce

Source: Hannover Region (Business report 2016)

26 TRENDS AND FACTS 2017

Information and communications technology

22,800 EPSIs* (4.7 % of TW**)

Key companies including: Finanz Informatik, TUI,

InfoTec, htp, Sennheiser, Madsack, NDR etc.

Highly diversified sector structure specialising in

IT services

Education and research institutes: 25 institutes and

university facilities active in the IT and communi-

cations sector, including IT and multimedia campus

“Expo Park” and L3S

Networks: Hannover IT e. V.

Flagship fairs: CeBIT and the Digital Factory

incorporated in Hannover Messe

Creative sector

20,670 EPSIs* (4.3 % of TW**)

Key segment music industry: University for Music,

Drama and Theatre, important players like NDR Radio-

philharmonie, Peppermint Park, Sennheiser

Many projects and events as part of the UNESCO

City of Music

Start-up centre HALLE 96 with offices and work

places and shared infrastructure

Network: kre|H|tiv Netzwerk e. V. as the fastest

growing national and largest industry network

of its kind

Logistics economy

54,000 EPSIs* (11.2 % of TW**) in some 3,000

enterprises (sectoral approach)

Key players: DHL, Kühne+Nagel, DB Schenker,

Dachser, UPS, TNT, Hellmann, Hermes, DPD,

Syncreon etc.

Main focuses: industry logistics, trade logistics,

e-commerce, courier, express and parcel services,

contract logistics, after-sales

European and national distribution centres for VW

Commercial Vehicles, Mercedes-Benz, arvato, Bahlsen,

Lyreco, Sonepar, Weatherford, Delticom, EDC etc.

Logistics-centric research institutes: institute for

transport and automation technology, institute for

integrated production, institute for factory systems

and logistics

Networks: Logistikportal Niedersachsen e. V.,

roundtable Personnel Logistics of Region Hannover

Flagship fairs: CeMAT, the world’s largest exhibition

for intralogistics

27KEY SECTORS

Financial services

25,000 EPSIs* (5.2 % of TW**)

Head offices of key national insurance companies

(e.g. Talanx, Vereinigte Hannoversche Versicherung,

Versicherungsgruppe Hannover, Concordia

Versicherungsgruppe, Mecklenburgische

Versicherungsgruppe, Wertgarantie Technische

Versicherung, HannoverRück-Gruppe)

Head offices of Nord/LB, of Deutsche Hypotheken-

bank, of Niedersächsischen Börse as well as one of

the largest savings banks (Sparkasse) in Germany

Key training and education centres: Sparkasse Academy,

Vocational Academy for the Banking Industry, Insurance

Industry Training Centre, Insurance Sciences Inter-

disciplinary Competence Centre

Trade fair and congress industry

1,400 EPSIs* (0.3 % of TW**)

World’s largest exhibition ground with Deutsche Messe AG as strong player

69 shows in 2016 with 1.24 million visitors

Location of leading international flagship fairs such as CeBIT, Hannover

Messe, Agritechnica, IAA Trucks, EMO, Biotechnica/Labvolution

Number of major congresses and conferences climbs every year enjoying

national coverage

Conference and congress centres such as Convention Center, Hannover

Congress Centrum, Herrenhausen Palace

* EPSI: employees paying social insurance contributions ** TW: total workforce

Source: Hannover Region (Business report 2016)

28 TRENDS AND FACTS 2017

Trades

60,000 EPSIs* (13.5 % of TW**) in 11,400 enter-

prises, with annual sales of approx. € 4.7 billion

Main sectors: building and interior finishing (3,240

enterprises), health/body care/cleaning (3,120 enter-

prises) and the metal industry (2,810 enterprises)

Important stimulus for innovation which is also

applied in other economic areas, e.g. the energy sector

One in five trainees in the Hannover Region are

trade apprenticeships

Research and service facilities:

Heinz-Piest-Institut (HPI) for the trades

Training and education: training and education

centre of the chamber of trades Hannover

29KEY SECTORS

Knowledge-based company-centric services

32,800 EPSIs* (6.8 % of TW**) in legal, tax and

management consulting firms, architects and

engineering service companies, and advertising and

market research

Resident companies: branch offices of major service

companies such as Pricewaterhouse-Coopers,

Deloitte, Ernst & Young

The creation of an innovation and research campus at

Hannover Garbsen offers more future potential, in

particular for organisations in the engineering sector

Science and research

7,900 EPSIs* (1.7 % of TW**)

Characterised by the medical sector (Hannover

Medical School, University of Veterinary Medicine

Hannover, Leibniz University Hannover, Fraunhofer

Gesellschaft, Medical Park)

Above average number of start-ups

Above average number of third-party-funded jobs

Cooperation between science and industry’s manu-

facturing sector, above all in the automotive sector

* EPSI: employees paying social insurance contributions ** TW: total workforce

Source: Hannover Region (Business Report 2016)

30 TRENDS AND FACTS 2017

EDUCATION AND SCIENCE

The Hannover Region boasts super-regional significance

as an education location. Compared with the rest of Lower

Saxony and Germany, an above average number of pupils

gain university entrance qualifications (39.9 %). Overall,

approximately 11,300 pupils gained school leaving certi-

ficates in the Hannover Region in 2015 at one of the more

than 100 secondary schools.

100 %

90 %

80 %

70 %

60 %

50 %

40 %

30 %

20 %

10 %

0 %

Hannover Region Lower Saxony Germany

39.9 %

3.2 %

40.3 %

11.9 %

4.7 %

32.5 %

2.1 %

47.4 %

13 %

5.0 %

34.0 %

2.1 %

41.7 %

16.5 %

5.6 %

School leavers

University entrance qualification

Applied science university entrance

qualification

Secondary school leaving certificate

Lower secondary school leaving

certificate

Special needs school leaving

certificate or no school

leaving certificate*

* No distinction is made at a federal level between pupils leaving school with a special needs school leaving certificate or no school leaving certificate

Source: State Office of Statistics Lower Saxony, calculations by the Hannover Region, School Leaving Qualifications 2015

31EDUCATION AND SCIENCE

In terms of professional education, the Hannover Region

has a top ranking in Germany – taking as a measure the

number of vocational school students per head of popu-

lation. Almost 41,000 vocational students attend the wide

range of training establishments. These include not only

the vocational colleges focusing on training in specific

sectors – including specialist vocational colleges, technical

secondary schools, vocational grammar schools and

training colleges – but also a wide range of other school

types with a broad spectrum of training objectives and

entrance qualifications.

One third of the students learn business and administration

vocations, followed by technical professions covering elec-

trical engineering, mechanical engineering, automotive,

construction and printing technology as well as vocations

in the food/nutrition sector and social and health services.

Source: State Office of Statistics Lower Saxony, reporting date November 2015

Vocational training students

According to school type

Vocational school (part-time) 26,720

First year vocational training 427

Vocational preparation 742

Vocational college 6,637

Technical secondary school 2,683

Upper vocational school 35

Vocational grammar school 1,851

Technical college 2,321

Total 41,416

According to vocation

Agriculture 797

Construction 889

Chemistry, physics, biology 774

Printing technology 745

Electrical engineering 3,439

Paint technology/interior design 715

Health 2,065

Wood technology 372

Gardening and Landscaping 636

Body care 686

Social services 2,092

Mechanical engineering 3,393

Nutrition 2,217

Social services 2,947

Automotive 1,723

Other recognised vocational training 1,205

Technology 497

Various vocations 663

Without training contracts

(at a vocational school)322

Business and administration 14,240

Textile technology and clothing 244

Domestic science 755

Total 41,416

32 TRENDS AND FACTS 2017

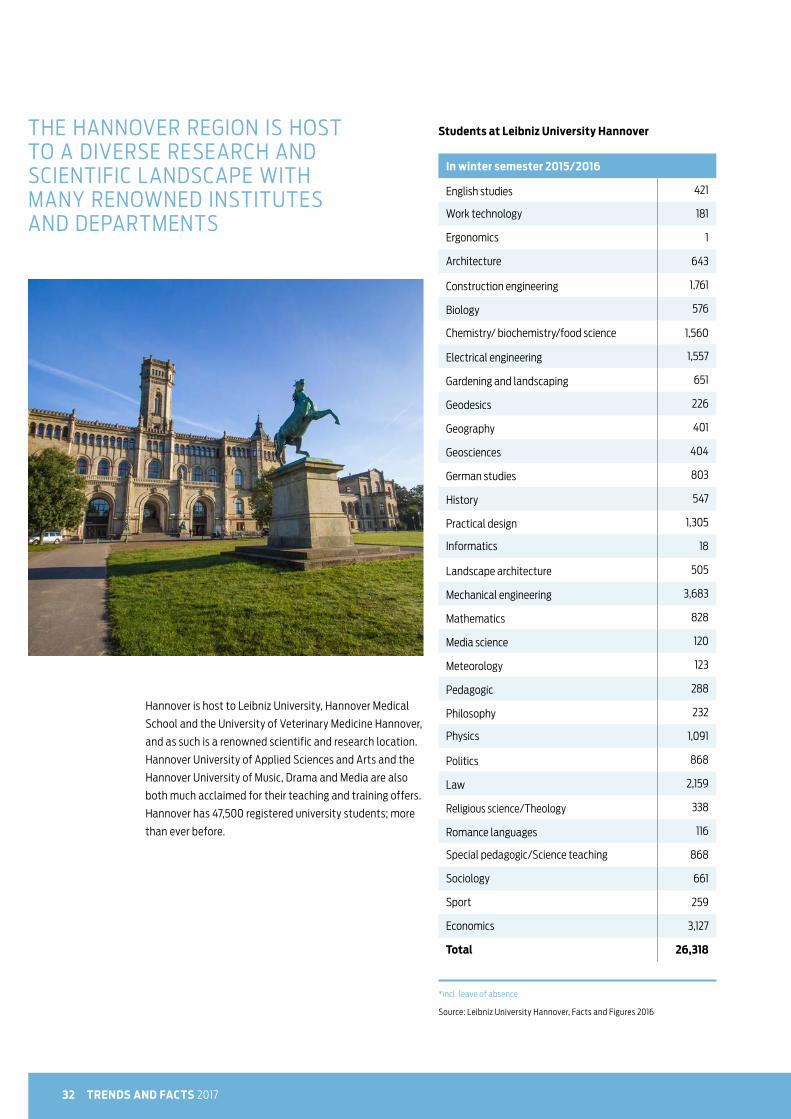

Hannover is host to Leibniz University, Hannover Medical

School and the University of Veterinary Medicine Hannover,

and as such is a renowned scientific and research location.

Hannover University of Applied Sciences and Arts and the

Hannover University of Music, Drama and Media are also

both much acclaimed for their teaching and training offers.

Hannover has 47,500 registered university students; more

than ever before.

English studies 421

Work technology 181

Ergonomics 1

Architecture 643

Construction engineering 1,761

Biology 576

Chemistry/ biochemistry/food science 1,560

Electrical engineering 1,557

Gardening and landscaping 651

Geodesics 226

Geography 401

Geosciences 404

German studies 803

History 547

Practical design 1,305

Informatics 18

Landscape architecture 505

Mechanical engineering 3,683

Mathematics 828

Media science 120

Meteorology 123

Pedagogic 288

Philosophy 232

Physics 1,091

Politics 868

Law 2,159

Religious science/Theology 338

Romance languages 116

Special pedagogic/Science teaching 868

Sociology 661

Sport 259

Economics 3,127

Total 26,318

Students at Leibniz University Hannover

In winter semester 2015/2016

*incl. leave of absence

Source: Leibniz University Hannover, Facts and Figures 2016

THE HANNOVER REGION IS HOST TO A DIVERSE RESEARCH AND SCIENTIFIC LANDSCAPE WITH MANY RENOWNED INSTITUTES AND DEPARTMENTS

33

Other universities and applied science universities

University of Applied Sciences and Arts Hannover 9,871

Hannover Medical School 3,456

University of Veterinary Medicine Hannover 2,402

University of Music, Drama and Media Hannover 1,556

Municipalities University of Administration in Lower Saxony

1,100

FOM University for Economics and Management 962

Leibniz Applied Science University 568

Applied Sciences University for Business 526

b.i.b International College 210

University of Applied Sciences of SME’s (FHM) 334

Vocational Academy of the Banking Sector 109

GISMA Business School 60

Total 21,154

Institute

Source: data provided by universities

Students in winter semester 2016/2017

EDUCATION AND SCIENCE

Science, Research, technology transfer,

start-up centres

Science and research represent cross-functional sectors

across various areas of the economy and are becoming

increasingly important in today’s globalised knowledge

economy. The Hannover Region is host to a very diverse

research and science sector with internationally acclaimed

institutes and faculties. Major strengths are in the medical

sector and the engineering disciplines – primarily in tech-

nology, research and knowledge-based segments of manu-

facturing industries, in particular in the automotive and

production engineering sectors.

Furthermore, Hannover-based research organisations

participate in a range of super-regional research networks,

e.g. ForWind-centre for wind energy research and the Audi-

tory Valley focusing on hearing. This creates a broad range

of opportunities for local cooperation in both research and

development as well as in the training and further training

of qualified skilled staff. The transfer of knowledge and

technology between research institutes and companies in

the Hannover Region is coordinated and supported by

numerous service providers and interfaces. Several start-up

centres support and assist innovative start-ups and young

enterprises in achieving their ideas. The Lower Saxony open

university coordinates the opening of new target groups, in

particular for those with vocational qualifications.

THE HANNOVER REGION BOASTS A VERY DIVERSE RESEARCH AND SCIENCE SECTOR WITH INTER- NATIONALLY ACCLAIMED INSTITUTES AND FACULTIES.

34 TRENDS AND FACTS 2017

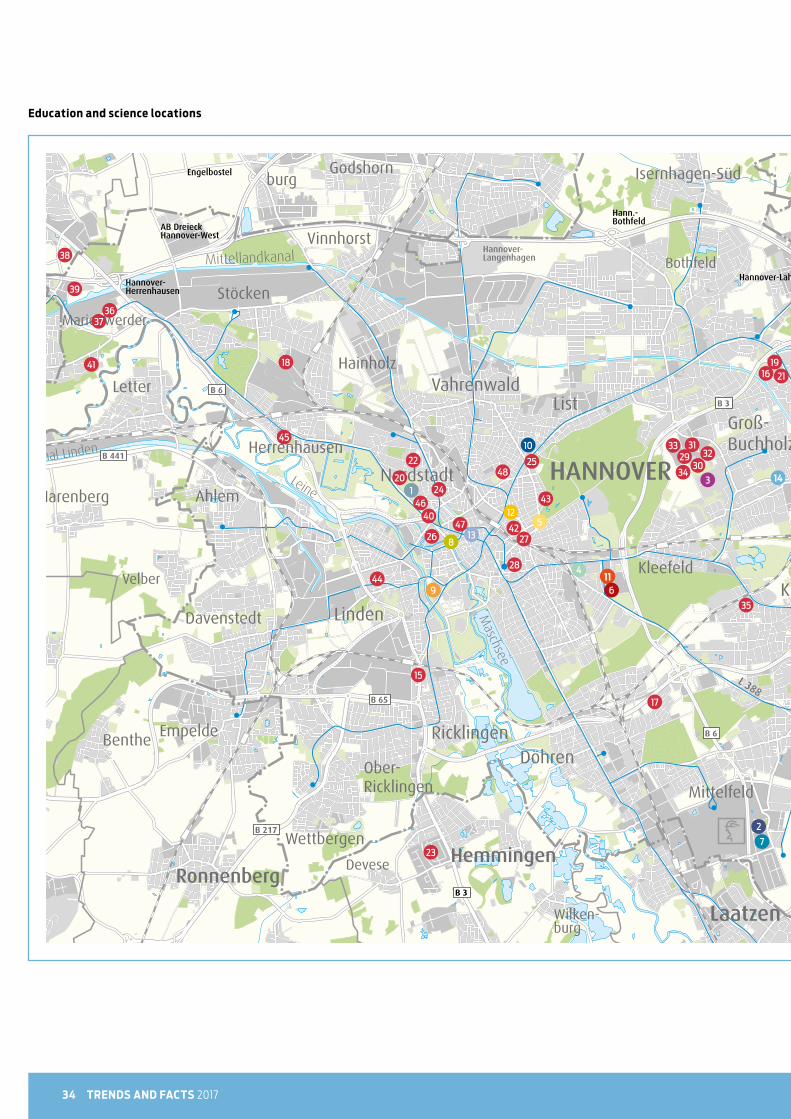

13

12

33

15

1

2

3

4

5

7

8

9

10

19

22

17

18

36

38

37

4116

20

21

23

24

25

2642

27

43

48

28

2931

3230

35

34

39

4047

45

44

46

14

116

Education and science locations

35EDUCATION AND SCIENCE

Universities

1 Leibniz University Hannover (main campus)

2 University of Applied Sciences and Arts

Hannover (main campus)

3 Hannover Medical School

4 University of Veterinary Medicine Hannover

(main campus)

5 University of Music, Drama and Media Hannover

6 Applied Sciences University for Business

7 Leibniz Applied Science University

8 GISMA Business School

9 Municipalities University in Lower Saxony

10 University of Applied Sciences of SME’s (FHM)

11 b.i.b International College

12 FOM University for Economics and Management

13 Service office Open University

14 Berufsakademie für Bankwirtschaft

Selected research and science institutes

Natural sciences

15 Limnology and Water Protection

16 Federal Institute for Geosciences and

Natural Resources (BGR)

17 German Institute for Rubber Technology (DIK)

18 Limestone-Sand Research Association

19 Institute for Joint Geo scientific Activities

20 Nano and Quantum Engineering Laboratory

21 Leibniz University for Applied Geophysics (LIAG)

22 Max Planck Institute for Gravitational Physics

(Albert Einstein Institute)

Construction engineering

23 District Heating Research Institute in Hannover

24 Institute for Engineering Hydrology

25 Institute for Construction Research

Social sciences and philosophy

26 Research Institute for Philosophy Hannover

27 ISP Eduard Pestel Institute for Systems Research

28 Social Sciences Institute of the Protestant

Church in Germany

Medicine

29 Hannover Clinical Trial Center GmbH

30 Fraunhofer Institute for Toxicology and

Experimental Medicine (ITEM)

31 International Neuroscience Institute

Hannover GmbH (INI)

32 IPF PharmaCeuticals GmbH

33 Lower Saxony Centre for Biomedical Technology,

Implant Research and Development (MFE)

34 Twincore

Production engineering

35 European Research Corporation for Metal (EFB)

36 IPH Institute for Integrated Production

Hannover GmbH

37 Laser Centre Hannover

38 Production Engineering Centre Hannover (PZH)

39 Test Centre for Load-bearing Structures

Economics

40 Hannover Center of Finance

41 Medium-sized Enterprise Institute Lower Saxony

42 Lower Saxony Institute for Economics Research

Architecture, spatial sciences, landscape planning

43 Academy for Spatial Research and Regional

Planning (ARL)

44 ECOLOG Institute for Socio-ecological Research

and Education gGmbH

45 Lower Saxony Institute for Historical

Regional Research

Other

46 Heinz Piest Institute for the Trades (HPI)

47 German Centre for University and Science Research

DZHW

48 Criminological Research Institute Lower Saxony

(KFN)

Source: Ministry for Science and Education Lower Saxony, CIMA Institute for Regional Economics, State Capital Hannover, Hannover Region; reporting date July 2017

36 TRENDS AND FACTS 2017

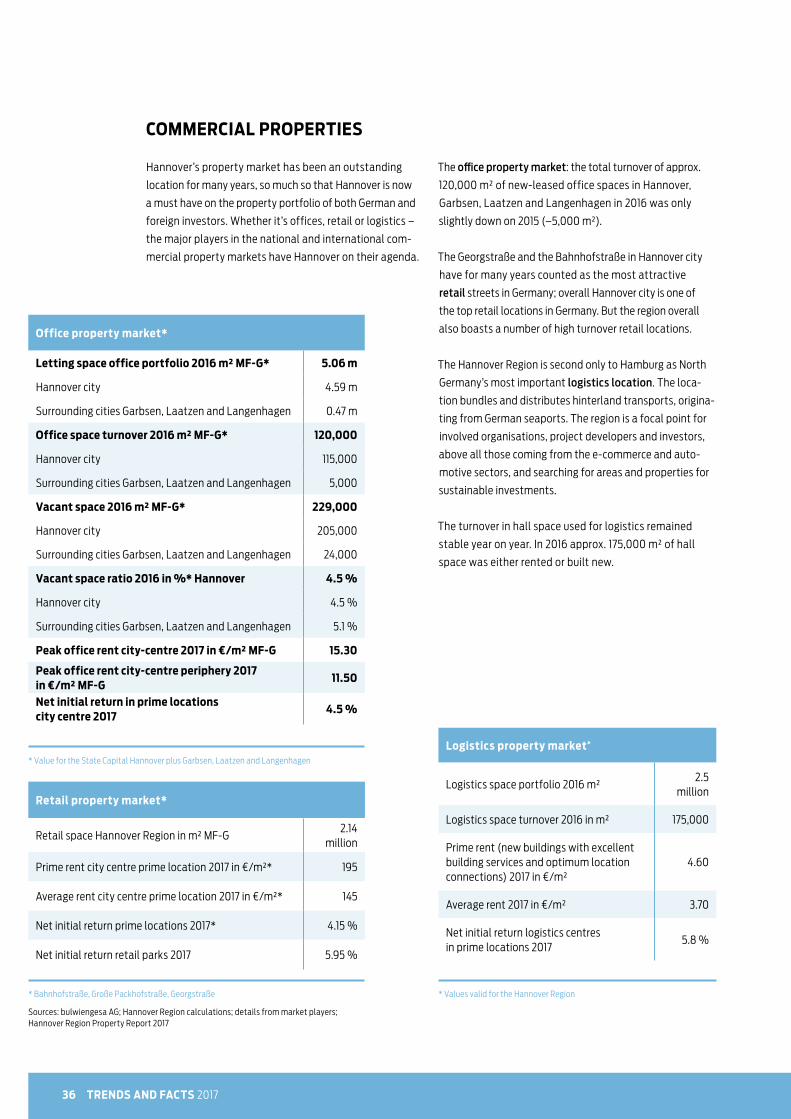

COMMERCIAL PROPERTIES

The office property market: the total turnover of approx.

120,000 m² of new-leased office spaces in Hannover,

Garbsen, Laatzen and Langenhagen in 2016 was only

slightly down on 2015 (–5,000 m²).

The Georgstraße and the Bahnhofstraße in Hannover city

have for many years counted as the most attractive

retail streets in Germany; overall Hannover city is one of

the top retail locations in Germany. But the region overall

also boasts a number of high turnover retail locations.

The Hannover Region is second only to Hamburg as North

Germany’s most important logistics location. The loca-

tion bundles and distributes hinterland transports, origina-

ting from German seaports. The region is a focal point for

involved organisations, project developers and investors,

above all those coming from the e-commerce and auto-

motive sectors, and searching for areas and properties for

sustainable investments.

The turnover in hall space used for logistics remained

stable year on year. In 2016 approx. 175,000 m² of hall

space was either rented or built new.

Hannover’s property market has been an outstanding

location for many years, so much so that Hannover is now

a must have on the property portfolio of both German and

foreign investors. Whether it’s offices, retail or logistics –

the major players in the national and international com-

mercial property markets have Hannover on their agenda.

Office property market*

Letting space office portfolio 2016 m² MF-G* 5.06 m

Hannover city 4.59 m

Surrounding cities Garbsen, Laatzen and Langenhagen 0.47 m

Office space turnover 2016 m² MF-G* 120,000

Hannover city 115,000

Surrounding cities Garbsen, Laatzen and Langenhagen 5,000

Vacant space 2016 m² MF-G* 229,000

Hannover city 205,000

Surrounding cities Garbsen, Laatzen and Langenhagen 24,000

Vacant space ratio 2016 in %* Hannover 4.5 %

Hannover city 4.5 %

Surrounding cities Garbsen, Laatzen and Langenhagen 5.1 %

Peak office rent city-centre 2017 in €/m² MF-G 15.30

Peak office rent city-centre periphery 2017 in €/m² MF-G

11.50

Net initial return in prime locations city centre 2017

4.5 %

* Value for the State Capital Hannover plus Garbsen, Laatzen and Langenhagen

Retail property market*

Retail space Hannover Region in m² MF-G 2.14

million

Prime rent city centre prime location 2017 in €/m²* 195

Average rent city centre prime location 2017 in €/m²* 145

Net initial return prime locations 2017* 4.15 %

Net initial return retail parks 2017 5.95 %

* Bahnhofstraße, Große Packhofstraße, Georgstraße

Sources: bulwiengesa AG; Hannover Region calculations; details from market players; Hannover Region Property Report 2017

Logistics property market*

Logistics space portfolio 2016 m² 2.5

million

Logistics space turnover 2016 in m² 175,000

Prime rent (new buildings with excellent building services and optimum location connections) 2017 in €/m²

4.60

Average rent 2017 in €/m² 3.70

Net initial return logistics centres in prime locations 2017

5.8 %

* Values valid for the Hannover Region

37

* Net basic rent

Source: IVD Commercial Property Price Comparison 2016/2017

Utility value, average in € per m²

Basic Moderate Good

Berlin 6.25 8.88 15.25

Bremen 4.50 7.00 9.00

Dortmund 5.50 7.50 9.50

Dresden 5.00 6.50 9.00

Essen 4.00 5.60 11.50

Frankfurt am Main 10.00 14.40 18.50

Hamburg 6.90 9.70 14.50

Hannover 5.50 6.75 11.00

Cologne 6.50 12.00 16.50

Leipzig 6.50 9.00 10.00

Munich 16.50 22.50 31.00

Nuremberg 6.60 8.07 9.64

Stuttgart 6.50 10.00 15.00

Office rents in selected cities*

COMMERCIAL PROPERTIES

The level of office and shop rents as well as the cost of

building land are key metrics for business location policy.

The price level is determined primarily by location factors,

such as the vicinity to Hannover’s city centre, transport

connections and near-by surrounding areas. The costs per

m² of office space in the State Capital Hannover range from

€ 5.50 per basic utility values up to € 11.00 for good utility

values. Shop rents in main shopping centres have a range

from € 14.00 to up to € 160.00, with a range of € 5.00 up to

€ 15.00 in adjacent core areas. These rental costs are mode-

rate when compared with other German cities.

Shopping area, average in € per m²

Prime site Secondary site

small (approx.

60 m²)

large (approx. 150 m²)

small(approx.

60 m²)

large (approx. 150 m²)

Berlin 180.00 125.00 35.00 25.00

Bremen 125.00 80.00 30.00 15.00

Dortmund 220.00 120.00 20.00 15.00

Dresden 110.00 n.a. n.a. n.a.

Essen n.a. n.a. n.a. n.a.

Frankfurt am Main 240.00 200.00 90.00 40.00

Hamburg 130.00 90.00 37.00 21.00

Hannover 160.00 80.00 25.00 14.00

Cologne 260.00 130.00 45.00 24.00

Leipzig 120.00 100.00 n.a. 30.00

Munich 410.00 320.00 170.00 110.00

Nuremberg 107.96 83.56 15.31 12.39

Stuttgart n.a. n.a. n.a. n.a.

Secondary core, average in € per m²

Prime site Secondary site

small (approx.

60 m²)

large (approx. 150 m²)

small(approx.

60 m²)

large (approx. 150 m²)

35.00 25.00 12.00 9.00

25.00 15.00 9.00 7.00

24.00 15.00 8.50 6.00

25.00 15.00 15.00 9.00

n.a. n.a. n.a. n.a.

55.00 40.00 20.00 18.00

27.00 21.00 16.00 11.00

15.00 10.00 7.00 5.00

25.00 12.00 7.00 6.00

25.00 15.00 12.00 10.00

110.00 40.00 35.00 23.00

19.70 12.91 8.47 6.68

n.a. n.a. n.a. n.a.

Shop rents in selected cities*

* Net basic rent, ground level

Source: IVD Commercial Property Price Comparison 2016/2017

38 TRENDS AND FACTS 2017

Utility value, average in € per m²

simple medium good

Berlin 60.00 100.00 145.00

Bremen 50.00 90.00 140.00

Dortmund 60.00 80.00 130.00

Dresden 30.00 50.00 70.00

Essen 65.00 95.00 150.00

Frankfurt am Main 225.00 300.00 450.00

Hamburg 100.00 135.00 160.00

Hannover 100.00 130.00 190.00

Cologne 110.00 135.00 160.00

Leipzig 35.00 60.00 100.00

Munich n.a. n.a. n.a.

Nuremberg 102.85 117.75 182.67

Stuttgart 250.00 400.00 650.00

Building plots in commercial areas *

* Incl. development costs / no subsidised prices

Source: IVD Commercial Property Price Comparison 2016/2017

39

COMMERCIAL PLOTS

A very important location factor for any business is the

availability of adequate qualitative and quantitative

commercial plots. The portfolio of immediately marketable

plots in the Hannover Region totals 88 ha, of which 37.7 ha is

classified as near-motorway. A further 274.2 ha are covered

by approved building plans, although these commercial

plots have either not yet been developed and/or are in

private ownership. Another 412.9 ha are incorporated in the

land development plan. As a result of competition for land

use and the demands for the protection of open spaces,

the opportunities for developing new commercial plots

are increasingly approaching their limits. In this situation

the potential to re-use brown field sites is particularly

important: 178.5 ha are current available.

in ha

Total commercial plot availability 775.1

Of which immediately marketable (officially authorised B-plan, developed, public property) 88.0

Of which motorway-near (max 2 km to German motorways) 37.7

Of which marketable at a later date (officially authorised B-plan, not developed and/or private property) 274.2

Of which land utilisation plan (still without a B-plan) 412.9

Potentially reusable brown field sites 178.5

Shortlisted business park/industrial estate (areas scheduled for planning by municipalities, still without F/B plans, possibly marketable in the medium to long term)

953.6

Source: Hannover Region Commercial Plot Monitoring Report 2017

Commercial plot availability in Hannover Region 2017

COMMERCIAL PROPERTIES . COMMERCIAL PLOTS

For more informationsee the latest Hannover Region Commercial Plot

Monitoring Report

40 TRENDS AND FACTS 2017

TAX ASSESSMENT RATES

The trade tax and the property tax are municipal taxes

whose assessment rates are revised annually as part of

municipal budget discussions. This empowers the munici-

palities to influence the size of the taxes paid by enter-

prises and to actively manage location policies. The tax

assessment rates in larger cities are generally higher than

those in their surrounding areas.

Source: Hannover Region

Trade tax Property tax A Property tax B

State Capital Hannover 480 530 600

Barsinghausen 470 560 560

Burgdorf 450 465 465

Burgwedel 400 430 430

Garbsen 430 430 430

Gehrden 390 490 490

Hemmingen 400 440 460

Isernhagen 400 450 450

Laatzen 460 600 600

Langenhagen 440 430 430

Lehrte 440 440 440

Neustadt am Rbge. 430 440 440

Pattensen 430 430 430

Ronnenberg 450 480 480

Seelze 460 550 550

Sehnde 440 460 460

Springe 395 450 450

Uetze 450 490 490

Wedemark 440 440 440

Wennigsen 440 460 460

Wunstorf 460 490 490

Property tax and trade assessment rates 2017

41

RESIDENTIAL

The demand and supply of residential property markets

are primarily influenced by regional providers and private

households. In the future, demand for housing will con-

tinue to be driven by further increases in the population of

the State Capital Hannover and in the number of surround-

ing municipalities. In contrast, vacant housing has been at

a very low level for many years (less than 2%) and is there-

fore significantly below the fluctuation reserve.

Despite the dynamic developments seen by the residential

property market, residential rents and purchase prices for

building land and owner-occupied apartments in Hannover

are still moderate when compared with other German cities.

TAX ASSESSMENT RATES . RESIDENTIAL

The residential property market in Hannover is currently

enjoying a renaissance. Proximity to the city centre, local

services and very good transport connections are key qual-

ity criteria in the selection of sites. These requirements are

satisfied by new housing areas, both in the state capital as

well as in towns and municipalities in the surrounding area

in the Hannover Region.

Living quality, average in € per m2

Medium Good Excellent

Berlin 9.80 12.00 n.a.

Bremen 9.50 11.75 12.75

Dortmund 8.00 9.90 n.a.

Dresden 8.00 9.50 10.50

Essen 8.20 10.25 n.a.

Frankfurt am Main 11.00 12.50 13.50

Hamburg 12.00 13.90 15.90

Hannover 10.00 11.50 13.00

Cologne 8.00 9.50 n.a.

Leipzig 7.00 8.80 11.20

Munich 14.80 16.60 21.00

Nuremberg 8.77 9.60 11.42

Stuttgart 12.40 13.50 14.90

* New builds – first tenancy, with respect to 3-room apartment, approx. 70 m2, not including publicly subsidised residential properties

Source: IVD residential comparison 2015/2016

Residential rents in selected cities, new builds - first tenancy

42 TRENDS AND FACTS 2017

* Completions from 1949, with respect to 3-room apartment, approx. 70 m2, not including publicly subsidised residential properties

Source: IVD residential comparison 2015/2016

Residential rents in selected cities, completions from 1949*

Living quality, average in € per m2

Basic Medium Good Excellent

Berlin 5.80 7.85 9.00 n.a.

Bremen 6.00 7.75 9.50 11.5

Dortmund 5.00 5.90 7.60 n.a.

Dresden 5.80 6.50 7.50 9.00

Essen 4.90 7.15 8.40 n.a.

Frankfurt am Main 7.80 9.00 10.50 13.00

Hamburg 7.50 9.25 12.00 14.6

Hannover 5.70 7.90 9.90 11.75

Cologne 7.50 9.50 12.00 n.a.

Leipzig 4.60 5.55 7.10 8.80

Munich 10.20 12.60 14.50 17.90

Nuremberg 6.37 7.58 8.72 10.87

Stuttgart 9.30 10.90 12.00 14.20

43RESIDENTIAL

Living quality, average in € per m2

Medium Good Excellent

Berlin 1,950 2,700 3,550

Bremen 1,300 2,200 3,000

Dortmund 1,450 2,100 2,650

Dresden 1,400 2,000 2,800

Essen 1,100 1,950 2,800

Frankfurt a. M. 2,200 3,500 5,500

Hamburg 2,500 3,400 5,000

Hannover 1,400 2,550 3,500

Cologne 2,300 3,400 4,600

Leipzig 1,250 1,750 2,450

Munich 4,200 5,300 7,400

Nuremberg 1,589 2,141 2,636

Stuttgart 2,950 3,650 4,850

Residential location, average in € per m2

Medium Good Excellent

Berlin 200 340 610

Bremen 160 270 500

Dortmund 270 335 500

Dresden 140 200 375

Essen 320 430 575

Frankfurt a. M. 450 630 850

Hamburg 350 480 740

Hannover 285 400 535

Cologne 440 750 1,200

Leipzig 130 220 420

Munich 1,350 1,850 2,900

Nuremberg 339 486 706

Stuttgart 685 850 1,025

Living quality, average in € per m2

Medium Good Excellent

Berlin 3,050 4,100 4,600

Bremen 2,600 3,800 4,500

Dortmund 2,350 2,800 3,950

Dresden 2,800 3,000 3,500

Essen 2,050 2,750 3,900

Frankfurt a. M. 3,200 3,800 4,300

Hamburg 3,600 4,600 6,500

Hannover 2,600 3,100 4,550

Cologne 3,200 3,900 5,200

Leipzig 2,820 3,100 3,600

Munich 5,900 6,900 9,000

Nuremberg 2,750 3,241 3,622

Stuttgart 4,400 5,500 7,350

Purchase prices for owner-occupied apartments in

selected cities – existing portfolio

Purchase price for building land in selected cities*

Purchase prices of owner-occupied apartments in

selected cities – new builds

* Detached and semi-detached houses, approx. 600 – 800 m2 plots

Source: IVD residential comparison 2016/2017

For more information see the latest Hannover

Property Report

44 TRENDS AND FACTS 2017

Living quality, average in €

Basic, approx. 100 m2

Medium, approx. 125 m2

Good, approx. 150 m2

Excellent, approx. 200 m2

Berlin n.a. 295,000 385,000 620,000

Bremen 120,000 220,000 410,000 800,000

Dortmund 250,000 350,000 440,000 720,000

Dresden 180,000 260,000 450,000 n.a.

Essen 240,000 365,000 535,000 840,000

Frankfurt am Main

350,000 470,000 700,000 1,100,000

Hamburg 260,000 370,000 565,000 1,000,000

Hannover 175,000 295,000 440,000 710,000

Cologne 300,000 430,000 620,000 1,500,000

Leipzig 175,000 245,000 350,000 660,000

Munich 620,000 840,000 1,300,000 2,250,000

Nuremberg 293,571 352,857 452,857 640,929

Stuttgart 390,000 595,000 900,000 1,500,000

* Detached privately-owned houses (including garage and usual size of plot in the locality)

Source: IVD residential comparison 2016/2017

Purchase prices for detached houses (ready for immediate occupation) in selected cities*

45

0 100 150 20050 250 300 350

State Capital Hannover

Wedemark

Springe

Wennigsen

Uetze

Barsinghausen

Lehrte

Garbsen

Isernhagen

Hemmingen

Pattensen

Gehrden

Wunstorf

Seelze

Neustadt am Rbge.

Laatzen

Burgwedel

Ronnenberg

Langenhagen

Sehnde

Burgdorf

126 ¤ / qm

119 ¤ / qm

117 ¤ / qm

180 ¤ / qm

284 ¤ / qm

301 ¤ / qm

168 ¤ / qm

161 ¤ / qm

159 ¤ / qm

145 ¤ / qm

207 ¤ / qm

227 ¤ / qm

233 ¤ / qm

176 ¤ / qm

210 ¤ / qm

127 ¤ / qm

139 ¤ / qm

112 ¤ / qm

94 ¤ / qm

116 ¤ / qm

108 ¤ / qm

Average purchase price in € per m2 Average Hannover Region 155 €/m2

* Building plots requiring no development costs. The average values only provide an overview of the current market. They do not reflect the fact that the prices are dependent on value-relevant features of each individual plot.

Source: Expert panel for real estate values Hamelin-Hannover, Real Estate Market Report 2017

Building plots for detached and semi-detached houses*

RESIDENTIAL

46 TRENDS AND FACTS 2017

TOURISM

The State Capital Hannover attracted more

than 2.24 million overnight stays annually

to achieve a new record and consolidate its

position as the city with the most overnight

guests in Lower Saxony. The overnight stays

in the surrounding area are also climbing: at

1.65 million overnight stays, the towns and

municipalities of the Hannover Region better

cities such as Bremen, Essen and Dortmund.

Overall, the Hannover Region counted over

3.9 million overnight stays in 2016.

Hannover Region State Capital Hannover Surrounding area

* These figures include overnight stays in accommodation establishments open for business with at least 10 beds, and camping sites open for business with at least 10 pitches.

Source: State Office of Statistics Lower Saxony, Hannover Region calculations

20062007

20082009

2010 20112012

20132014

20152016

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

Overnight stays in the Hannover Region*

THE STATE CAPITAL HANNOVER ACHIEVED A NEW RECORD OF 2.2 MILLION OVERNIGHTS.

47

Hannover Adventure Zoo, the Royal Gardens of Herren-

hausen, the home games of Hannover 96 football team,

the productions in the state theatre and the numerous

museums are all attractions in their own right. In the sur-

rounding area, the Steinhuder Meer lake, the Deister hills

and the Marienburg Castle are the main tourist magnets.

The Hannover Region offers a wide range of cultural, spor-

ting, entertainment and recreation attractions. Top events

include the Maschseefest, Hannover Schützenfest (marks-

men’s fair), the Lister Meile Fest, Regionsentdeckertag

(discovery day), the Hannover marathon, the Fête de la

Musique, the international fireworks competition and the

Kleines Fest im Großen Garten (outdoor variety festival in

the Royal Gardens of Herrenhausen).

TOURISM

Events

Hannover Christmas markets 1,900,000

Maschseefest 1,780,000

Schützenfest (Marksmen’s Fair) 1,000,000

Lister Meile Fest 250,000

Hannover Marathon 220,000

Entdeckertag (Discovery Day) 130,000

Fête de la Musique 80,000

Kleines Fest im Großen Garten 65,000

International fireworks competition 50,000

Beer festival 50,000

Steintorfest 30,000

N-Joy Starshow 25,000

NDR2 Plaza Festival 25,000

Maker Faire Hannover 15,000

Festival of Cultures 14,000

Kunstfestspiele Herrenhausen 14,000

Fährmannsfest 12,000

Classic in the Old Town 10,000

Tourist attractions

Hannover Adventure Zoo 1,160,000

Hannover 96, season 2016/17 623,000

Royal Gardens of Herrenhausen 545,000

State Theatre Hannover (opera, theatre) 370,000

Marienburg Castle 190,000

GOP variety theatre 183,700

Theater am Aegi 176,000

Sprengel-Museum 148,500

State Museum Lower Saxony 113,000

Hannover Museum of history 50,000

Wilhelm-Busch Museum 46,400

Parkbühne open air season 45,400

August-Kestner Museum 34,900

Kommunales Kino 26,600

Kestnergesellschaft 20,000

Selected events and tourist attractions in the Hannover Region

Source: Figures provided by event organisers and institutions

Visitor numbers 2016 Visitor numbers 2016

48 TRENDS AND FACTS 2017

TRADE FAIRS

the flagship of the information and communications tech-

nology sector; HANNOVER MESSE as the broad-based

forum for industry as a whole; Agritechnica as the world’s

largest agricultural machinery show; and the IAA Trucks as

the world’s leading show for trucks, mobility and transport.

In 2016, 69 shows took place in Hannover, attracting

approximately 1.24 million visitors.

The Hannover fairs and exhibitions are a vital factor in

raising awareness of Hannover as a business location and

have a positive knock-on effect on the image of the region

as a whole. Hannover is host to the world’s largest exhibition

grounds, with around 463,000 m2 covered exhibition space –

including top quality exhibition areas and halls. Hannover is

home to major flagship trade fairs: examples being CeBIT,

IN 2016 69 SHOWS TOOK PLACE IN HANNOVER, ATTRACTING APPROX. 1.24 MILLION VISITORS.

Hall space

in m2

Outdoor space in m2

Visitors to domestic trade

fairs 2016

Deutsche Messe AG Hannover 463,285 58,000 1,240,000

Messe Frankfurt GmbH 366,637 96,078 1,560,000

Koelnmesse GmbH 284,000 100,000 1,300,000