Treasury A Perspective into Markets and Dealing. The Business Issues Introduction to Derivatives The...

29

Treasury A Perspective into Markets and Dealing

-

Upload

madison-bell -

Category

Documents

-

view

213 -

download

0

Transcript of Treasury A Perspective into Markets and Dealing. The Business Issues Introduction to Derivatives The...

Treasury

A Perspective into Markets and Dealing

The Business Issues Introduction to DerivativesThe Markets

Agenda

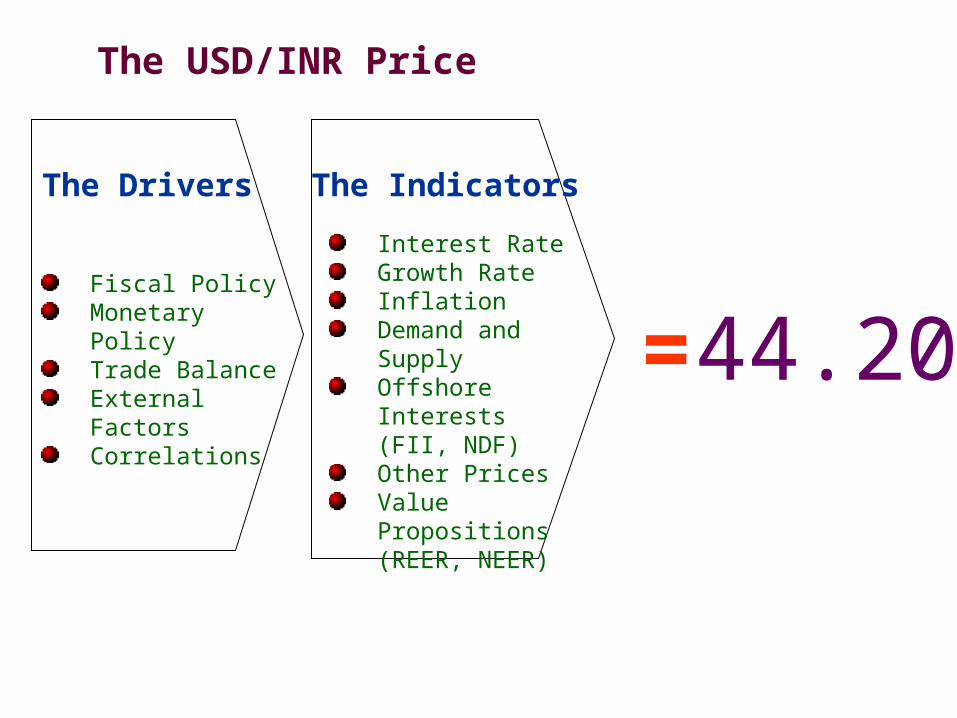

The USD/INR Price

The Drivers

Fiscal PolicyMonetary PolicyTrade BalanceExternal FactorsCorrelations

The Indicators

Interest RateGrowth RateInflationDemand and SupplyOffshore Interests (FII, NDF)Other PricesValue Propositions (REER, NEER)

= 44.20

Retails Oil

Oil Seller

Buys Oil at $60 per Barrel

Gives INR

Buy USD

(at Spot Rate)

Where are the risks?

Receives INR

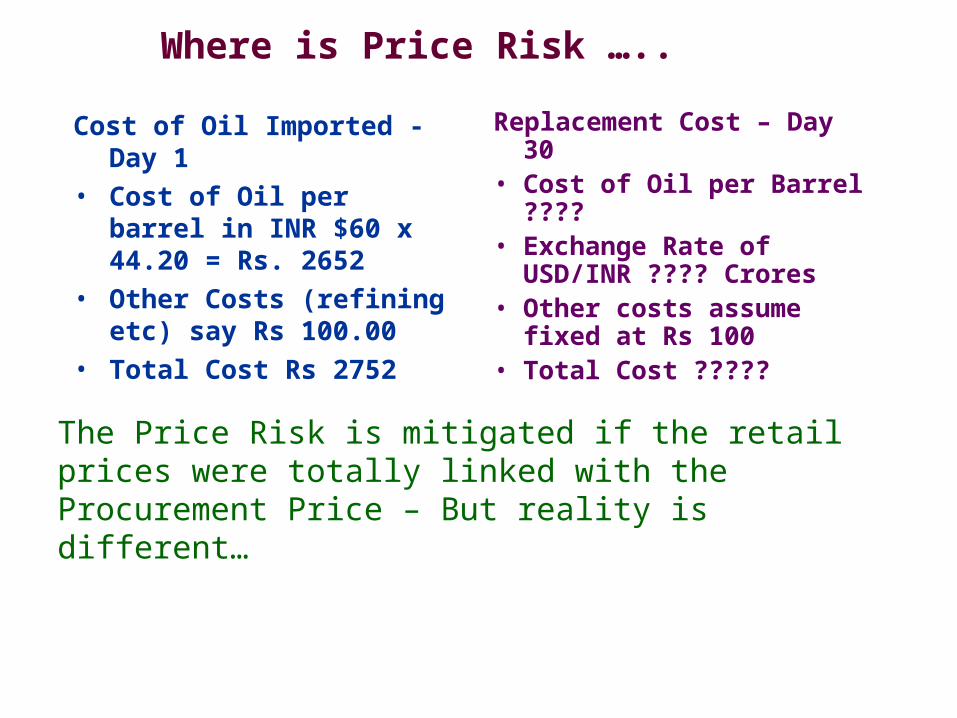

Where is Price Risk …..

Cost of Oil Imported - Day 1

• Cost of Oil per barrel in INR $60 x 44.20 = Rs. 2652

• Other Costs (refining etc) say Rs 100.00

• Total Cost Rs 2752

Replacement Cost – Day 30• Cost of Oil per Barrel ????• Exchange Rate of

USD/INR ???? Crores• Other costs assume fixed at

Rs 100• Total Cost ?????

The Price Risk is mitigated if the retail prices were totally linked with the Procurement Price – But reality is different…

The Reality is

1000

1500

2000

2500

3000

3500

1015202530354045505560657075

Procurement Price

WTC Oil

USD/INR

Retail Price

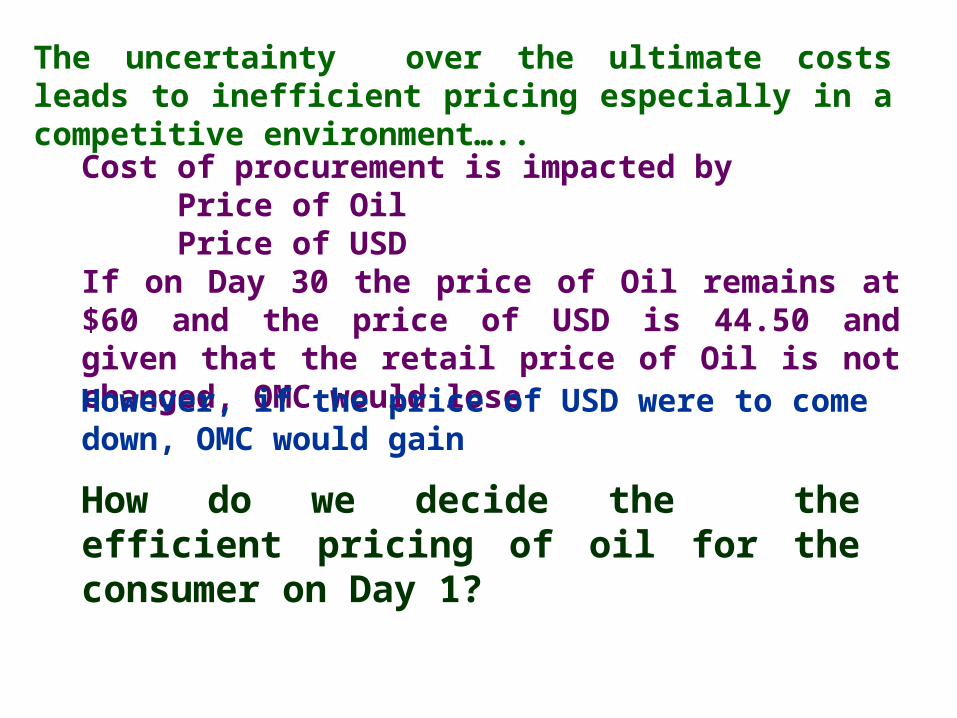

The uncertainty over the ultimate costs leads to inefficient pricing especially in a competitive environment…..

Cost of procurement is impacted byPrice of OilPrice of USD

If on Day 30 the price of Oil remains at $60 and the price of USD is 44.50 and given that the retail price of Oil is not changed, OMC would lose

How do we decide the the efficient pricing of oil for the consumer on Day 1?

However, if the price of USD were to come down, OMC would gain

The Business IssueIntroduction to DerivativesThe Markets

Agenda

Issues• Business accruals in INR• Procurement in USD• Two factor pricing (Oil and USD)• Inability to link Retail Pricing to

ProcurementNeed Identified• Minimize the impact of the Price

Risk between retail and procurement

Solution• Use customized hedges to suit

requirement

Issues, Need and Solution

Effect

Business accruals in INR

Price Risk covered for the period of Forward Hedge

Achieve more efficient pricing

Classical Interest Rate Parity

Spot FX

Forward FX

Interest Rate 1Currency 1

Currency 2 Interest Rate 2

Therefore the Hedging “Cost” is nothing else but the Interest Rate Differential

between the two Currencies

Hedging – Some Issues

When To HedgeArrive at the Cost of Operations + Margins

= Net Cost

As and when levels are seen over the Net

Cost

View Based

What period to hedgeHedge price risk for the period of resetting

of Retail Prices

“ To my knowledge no model projecting movements in rates is superior to tossing a coin”

Alan Greenspan

Former Chairman Federal Reserve

USD/INR NYMEX OIL

The Business IssueIntroduction to DerivativesThe Markets

Agenda

Financial instruments whose value is DERIVED from some other Underlying AssetExamples of Derivatives

•Futures and Forwards •Swaps •Options

Types of Underlying Assets include:Equity SharesInterest Rates (including

Government Bonds)Foreign Exchange Commodities

Buyer - acquires the Right but not the

obligation

Seller – sells the right but has the obligation

Option is a contract where the Buyer buys the Right but not the Obligation….

CONFIDENCE

HIGH LOW

USD FIRMING

FORWARD RATE TO BE LOCKED IN

BUY AN USD CALL

OPTION

V I E

W

USD FALLING

KEEP THE EXPOSURE

OPEN

BUY AN USD

CALL OPTION

CONFIDENCE

HIGH LOW

USD FIRMING

FORWARD RATE TO BE LOCKED IN

BUY AN USD CALL

OPTION

V I E

W

USD FALLING

KEEP THE EXPOSURE

OPEN

BUY AN USD

CALL OPTION

46

FORWARDUSD/INR

48

47

43

44

42

45

USD/INR

CALL

ITM CALL

ATM CALL

OTM CALL

Illustration

Illustration

CALL

PREMIUM 46

FORWARDUSD/INR

48

47

43

44

42

45

ITM CALL

ATM CALL

OTM CALL

PremiumLower

PremiumHigher

Zero Cost Strategy

44.0044.00

46.0046.00

BUY CALL

SELL PUT

Buy from the Bank

Losses Limited

Buy from the Market

Unlimited Profit potential

Exercise CALLBuy USD @ 46.00

Exercise PUTBuy USD @ 44.00

Sacrifice Profits Below 44.00

The Business IssueIntroduction to DerivativesThe Markets

Agenda

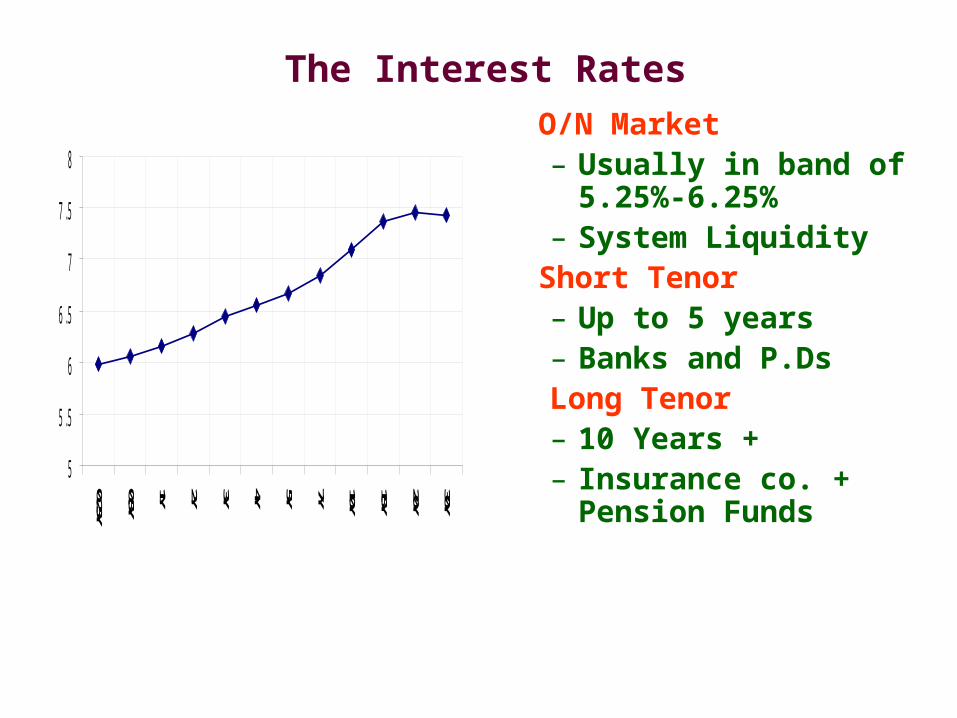

The Interest Rates

5

5 . 5

6

6 . 5

7

7 . 5

8

0.25Y0.5Y1Y 2Y 3Y 4Y 5Y 7Y 10Y 15Y 20Y 30Y

O/N Market– Usually in band of

5.25%-6.25%– System Liquidity

Short Tenor– Up to 5 years– Banks and P.DsLong Tenor– 10 Years +– Insurance co. +

Pension Funds

Global Interest Rates

– US • “number of rate increases…probably not be large..” – FOMC

minutes.

– UK• BoE Cut policy rate in response to weakening economic activity.

– Euro• ECB hiking and may continue until inflation no longer exceeds

target 2.0% (currently 2.3%)

– Japan• Mild deflation continues. (-0.3%)

Inflation – the Drivers

Inflation ExpectationsWPI Components

02468

101214

Mar'03 Sep'03 Mar'04 Sept'04 Mar,05 Sept'05 Dec'05

Primary Articles Manufactured products

Fuel, Power, Light and Lubricants

Month End

WPI Inflation

Dec’05 4.40%

Jan’06 4.78%

Feb’06 5.09%

Mar’06 4.96%

Apr’06 4.16%

May’06 4.42%

Indian Inflation is OIL driven

CorrelationsC o r r e l a t i o n : I N R / $ V s E u r / $

1 . 1 5

1 . 2

1 . 2 5

1 . 3

1 . 3 5

1 . 4

Ja

n-0

5

Ja

n-0

5

Fe

b-0

5

Fe

b-0

5

Ma

r-05

Ma

r-05

Ap

r-05

Ap

r-05

Ma

y-0

5

Ma

y-0

5

Ju

n-0

5

Ju

n-0

5

Ju

n-0

5

Ju

l-05

Ju

l-05

Au

g-0

5

Au

g-0

5

Se

p-0

5

Se

p-0

5

Oc

t-05

Oc

t-05

No

v-0

5

No

v-0

5

No

v-0

5

De

c-0

5

De

c-0

5

Ja

n-0

6

0 . 0 2 1 5

0 . 0 2 1 7

0 . 0 2 1 9

0 . 0 2 2 1

0 . 0 2 2 3

0 . 0 2 2 5

0 . 0 2 2 7

0 . 0 2 2 9

0 . 0 2 3 1

0 . 0 2 3 3E u r / $ IN R / $

• High Correlation with Dollar movements in international markets.

Exchange Rate

I N R / $

0 . 0 2 0 5

0 . 0 2 1

0 . 0 2 1 5

0 . 0 2 2

0 . 0 2 2 5

0 . 0 2 3

0 . 0 2 3 5

13-Jan-04

13-Mar-04

13-May-04

13-Jul-04

13-Sep-04

13-Nov-04

13-Jan-05

13-Mar-05

13-May-05

13-Jul-05

13-Sep-05

13-Nov-05

Rupee +ve– FII/FDI Inflows

– External Commercial Borrowings

– Service Exports

Rupee –ve– Trade Deficit

• OIL

The Trade Flows

Current Account

-10000

-5000

0

5000

10000

15000

20000

Apr'04-Jun'04

Jul'04-Sept'04

Oct'04-Dec'04

Jan'05-Mar'05

Apr'05-Jun'05

Current Account Trade Deficit Invisibles Surplus

I n d i a ' s E x t e r n a l F l o w s

- 1 0 0 0 0

- 5 0 0 0

0

5 0 0 0

1 0 0 0 0

1 5 0 0 0

Ap

r'0

4-

Ju

n'0

4

Ju

l'04

-

Se

pt'

04

Oc

t'0

4-

De

c'0

4

Ja

n'0

5-

Ma

r'0

5

Ap

r'0

5-

Ju

n'0

5

C u r r e n t A c c o u n t C a p i ta l A c c o u n t

Commodity Imports

• Oil is 32% of India’s commodity Imports. Growth in Oil imports =

43%• Growth in import of

machinery goods = 44%

Overall, merchandise trade deficit

Surpassed Invisibles surplus

The SBI advantage

• Largest in – Size , Network and Market Presence

• Total understanding of the PSU Environment

• Is the Business Partner in the growth of the Indian PSU Incorporated

• Has large pool of Expert Resources available for advice

• Preferred choice of major Corporates

• Transparent working

• Relationship based on Trust

Thank You