TRC Q2 2017 Earnings Slides

23

www.trcsolutions.com Q2 Fiscal 2017 Investor Review February 2, 2017 Chris Vincze Tom Bennet Chairman & CEO Chief Financial Officer TRR

-

Upload

trcsolutions -

Category

Investor Relations

-

view

723 -

download

4

Transcript of TRC Q2 2017 Earnings Slides

www.trcsolutions.com

Q2 Fiscal 2017 Investor Review

February 2, 2017Chris Vincze Tom BennetChairman & CEO Chief Financial Officer

T R R

Safe Harbor Statement

2

Certain statements in this presentation may be forward-looking statements within the meaning of Section 27A of the Securities Act of

1933 and Section 21E of the Securities Exchange Act of 1934. You can identify these statements by forward-looking words such as

"may," "expects," "plans," "anticipates," "believes," "estimates," or other words of similar import. You should consider statements that

contain these words carefully because they discuss TRC’s future expectations, contain projections of the Company’s future results of

operations or of its financial condition, or state other "forward-looking" information. TRC believes that it is important to communicate

its future expectations to its investors. However, there may be events in the future that the Company is not able to accurately predict

or control and that may cause its actual results to differ materially from the expectations described in its forward-looking statements.

Investors are cautioned that all forward-looking statements involve risks and uncertainties, and actual results may differ materially

from those discussed as a result of various factors, including, but not limited to, circumstances which could create large cash outflows,

such as contract losses, litigation, uncollectible receivables and income tax assessments; regulatory uncertainty; the availability of

funding for government projects; the level of demand for TRC’s services; product acceptance; industry-wide competitive factors; the

ability to continue to attract and retain highly skilled and qualified personnel; the availability and adequacy of insurance; capital

availability and project investment by our clients; and general political or economic conditions. Furthermore, market trends are subject

to changes which could adversely affect future results. See the risk factors and additional discussion in TRC’s Annual Report on Form

10-K for the fiscal year ended June 30, 2016, Quarterly Reports on Form 10-Q, and other factors detailed from time to time in the

Company’s other filings with the Securities and Exchange Commission.

These slides are intended as a visual aid to TRC’s commentary on the Second Quarter Fiscal Year 2017 Financial Results Conference

Call. As such, they should be considered in the full context of that commentary, the transcript of that conference call and TRC’s second

quarter 2017 Form 10-Q and Financial Results Press Release. Also, this presentation contains references to non-GAAP metrics such as

EBITDA, gross margin, free cash flow and various adjusted metrics. A reconciliation of GAAP to non-GAAP metrics can be found on

slides 17-21.

Q2 Fiscal 2017 Overview

3

NSR1 increased 14% YOY to $127.4MPower +1%, Environmental -2%, Infrastructure +7%, Oil & Gas NSR of $21.3M

NSR backlog increased 2% YOY to $350MPower +16%, Environmental -3%, Infrastructure -16%, Oil & Gas backlog of $43M

(1) TRC believes net service revenue (gross revenue less subcontractor costs and other direct reimbursable charges) best reflects the value of services provided to its customers and is the most meaningful indicator of its revenue performance.

Operating cash flow of $21.4MDSO performance provides strong cash position

Net income increased 2% YOY to $4.0MStrong Infrastructure performance aided earnings, offset by $1.5M amortization expense increase

EBITDA increased 20% YOY to $11.4MAdjusted EBITDA increased 6% YOY

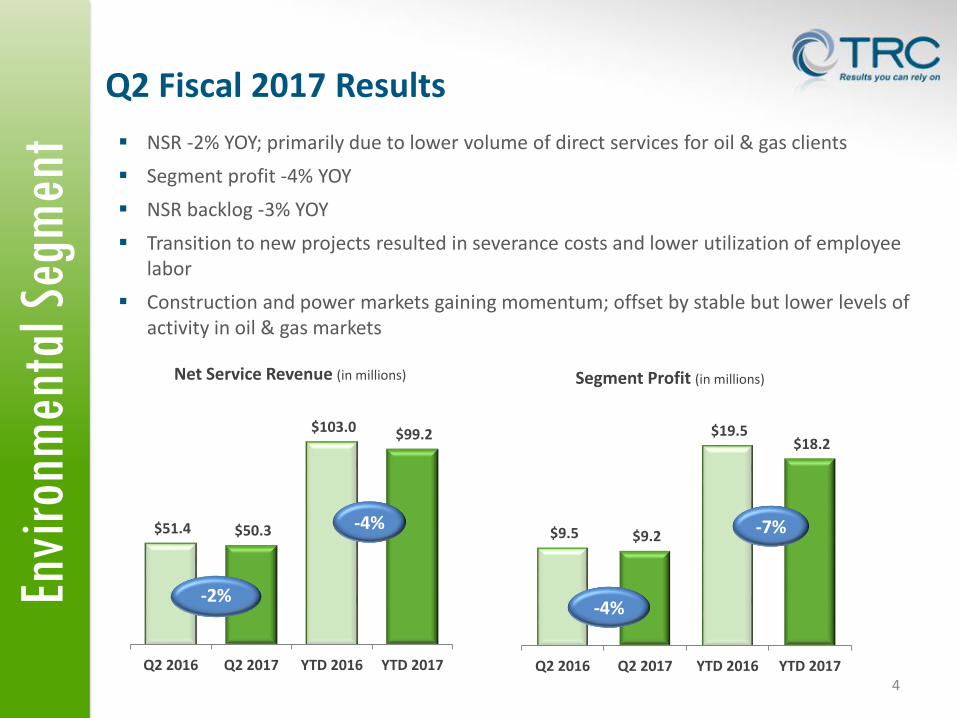

Envi

ronm

enta

l Seg

men

t

$9.5 $9.2

$19.5 $18.2

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Segment Profit (in millions)

-7%

-4%

$51.4 $50.3

$103.0 $99.2

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Net Service Revenue (in millions)

-2%

-4%

4

NSR -2% YOY; primarily due to lower volume of direct services for oil & gas clients

Segment profit -4% YOY

NSR backlog -3% YOY

Transition to new projects resulted in severance costs and lower utilization of employee labor

Construction and power markets gaining momentum; offset by stable but lower levels of activity in oil & gas markets

Q2 Fiscal 2017 Results

Pow

er S

egm

ent

5

NSR +1% YOY

Segment profit unchanged YOY

NSR backlog +16% YOY on program management project increase

Increasing demand for energy efficiency, testing / commissioning, and distribution engineering services

$39.8 $40.3

$74.1 $77.4

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Net Service Revenue (in millions)

+4%$9.5 $9.5

$16.8 $17.5

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Segment Profit (in millions)

+4%

Unchanged+1%

Q2 Fiscal 2017 Results

Infr

astr

uctu

re S

egm

ent

6

Q2 Fiscal 2017 Results

NSR +7% YOY, driven by large, ongoing PPP projects

Segment profit +37% YOY

NSR backlog -16% YOY; delay in timing of several large contract awards

Benefitting from increased scale and project size

Private investment and state-level legislation expanding PPP programs

$13.7 $14.6

$27.3

$31.2

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Net Service Revenue (in millions)

+15%

$2.5

$3.5

$5.4

$7.8

Q2 2016 Q2 2017 YTD 2016 YTD 2017

Segment Profit (in millions)

+37%

+43%

+7%

Oil

& G

as S

egm

ent

7

NSR $21.3 million

Segment profit of $1.5 million, improved by cost reduction initiatives

NSR backlog $43 million

Increasing stability in oil & gas market

Consistent segment performance led by pipeline integrity-related services

$21.5 $20.8 $21.3 $21.3

$42.7

Q3 2016 Q4 2016 Q1 2017 Q2 2017 YTD 2017

Net Service Revenue (in millions)

Q2 Fiscal 2017 Results

$(3.1) $(3.2)

$1.4 $1.5

$2.8

Q3

20

16

Q4

20

16

Q1

20

17

Q2

20

17

YTD

20

17

Segment Profit (in millions)

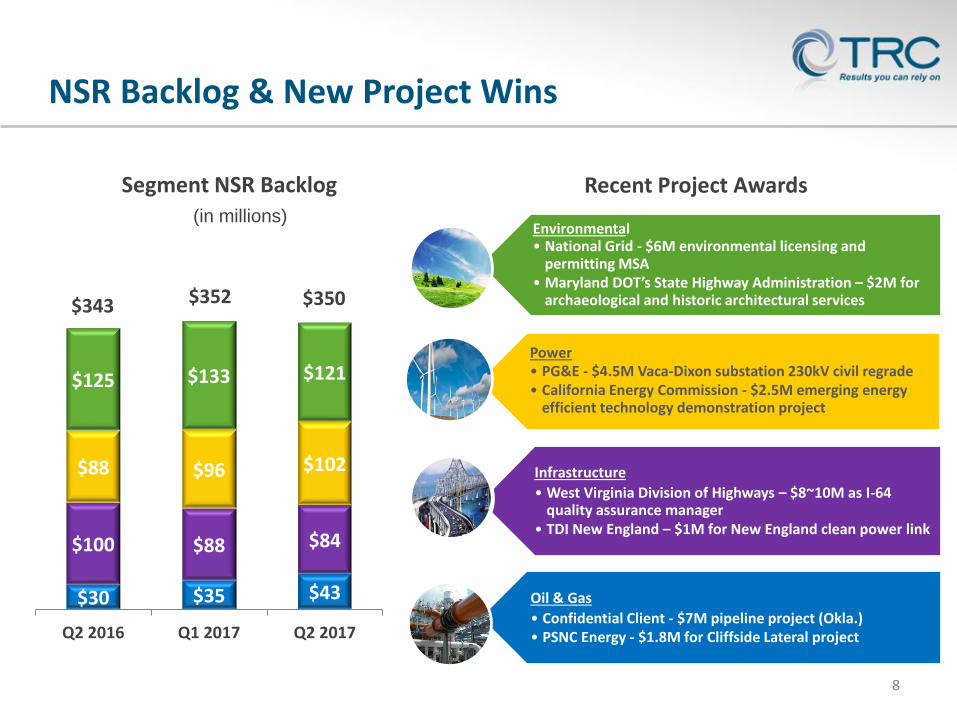

$30 $35 $43

$100 $88 $84

$88 $96 $102

$125 $133 $121

Q2 2016 Q1 2017 Q2 2017

Segment NSR Backlog

$350

NSR Backlog & New Project Wins

8

(in millions)

$343 $352

Power• PG&E - $4.5M Vaca-Dixon substation 230kV civil regrade• California Energy Commission - $2.5M emerging energy

efficient technology demonstration project

Environmental• National Grid - $6M environmental licensing and

permitting MSA• Maryland DOT’s State Highway Administration – $2M for

archaeological and historic architectural services

Infrastructure

• West Virginia Division of Highways – $8~10M as I-64 quality assurance manager

• TDI New England – $1M for New England clean power link

Oil & Gas

• Confidential Client - $7M pipeline project (Okla.)• PSNC Energy - $1.8M for Cliffside Lateral project

Recent Project Awards

9

Applied Energy Group (N.J. Office) Acquisition

TRC pursuing strategic acquisitions to expand our platform in key North

American markets

Acquired New Brunswick, N.J. office of Applied Energy Group (AEG) from

Ameresco in January 2017

Administrator of New Jersey Clean Energy Program

Broadening capabilities to support diverse portfolio of energy sources

Enhances TRC’s leadership position as growing, national leader in the

energy efficiency services market

Key Strategies and Initiatives

10

Invest in organic growth opportunities; new five-year profitable growth strategy

Increase focus on strategic markets:

Power / Utility – Continued investment to modernize gas & electric systems; significant renewable generation investment and focus on energy efficiency

Public policy promoting strong investment in distributed generation and microgrids; expected to expand to other utilities across the nation

Infrastructure – Bipartisan and Administration support for significant infrastructure investment, focusing on transportation

Oil & Gas – Changing midstream and LDC market dynamics resulting in focus on repair / maintenance, upgrade and monitoring of existing assets using technology based solutions

Increased permitting / planning and capital project commitments expected with new Administration support for pipeline projects

Path to new PHMSA rules expected to continue due to enhanced safety benefits

Pursue acquisitions that provide geographic expansion and enhanced technical capabilities or new adjacent services

Continue focus on improving margin and operating cash flow

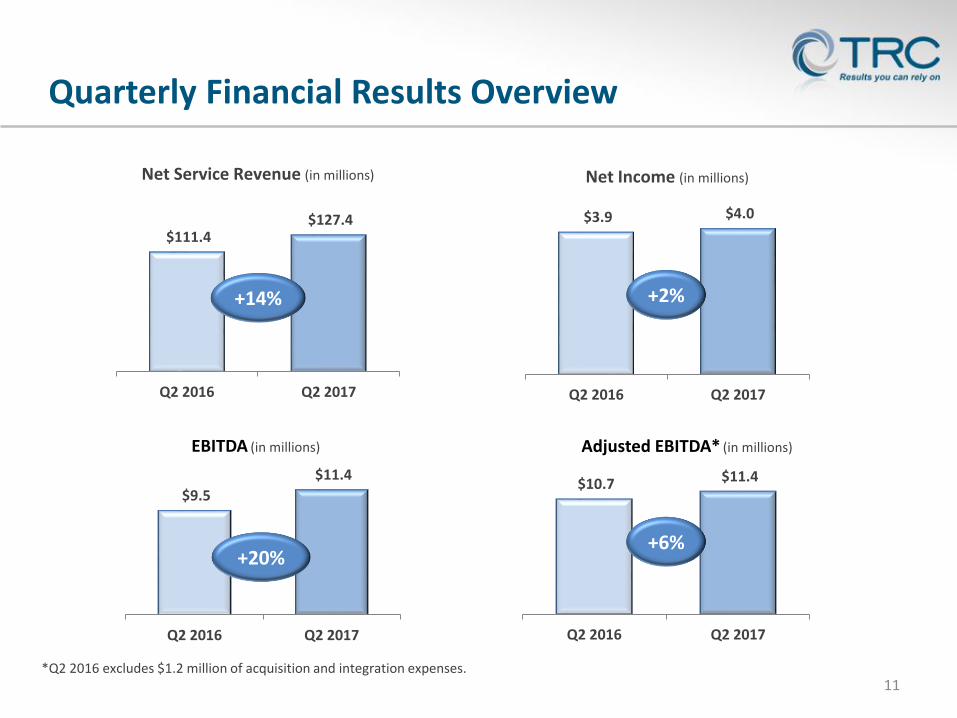

$9.5

$11.4

Q2 2016 Q2 2017

EBITDA (in millions)

Quarterly Financial Results Overview

11

$111.4 $127.4

Q2 2016 Q2 2017

Net Service Revenue (in millions)

+14%

$10.7 $11.4

Q2 2016 Q2 2017

Adjusted EBITDA* (in millions)

+6%

*Q2 2016 excludes $1.2 million of acquisition and integration expenses.

+20%

$3.9 $4.0

Q2 2016 Q2 2017

Net Income (in millions)

+2%

Q2 2016

$111.4

$1.1

$93.7

15.9%

$8.0

7.2%

$1.2

$6.7

$7.9

$9.5

8.5%

$10.7

9.6%

$3.9

$4.7

$0.13

$0.15

Q2 2017

$127.4

$0.7

$105.6

17.1%

$11.0

8.7%

--

$7.0

$7.0

$11.4

9.0%

$11.4

9.0%

$4.0

$4.0

$0.13

$0.13

12

(In millions, except per share data)

Quarterly Income Statement Highlights

84.1%82.9%

Q2 2016 Q2 2017

Cost of Services as % of NSR

7.2%

8.7%

Q2 2016 Q2 2017

G&A Expenses as % of NSR

Net service revenue

Insurance recoverables and other income

Cost of services (COS)

Gross margin %

General and administrative expenses

G&A as % of NSR

Acquisition and integration expenses

Operating income

Adjusted operating income1

EBITDA

EBITDA as a % of NSR

Adjusted EBITDA1

Adjusted EBITDA as a % of NSR

Net income

Adjusted net income1, 2

Diluted earnings per common share

Adjusted diluted earnings per common share1, 2

1Q2 2016 excludes $1.2 million of acquisition and integration expenses. 2Excludes acquisition and integration-related expense in note 1, net of an income tax benefit of $0.5 million.

$19.4 $21.9

YTD 2016 YTD 2017

EBITDA (in millions)

YTD 2017 Financial Results Overview

13

$211.5

$251.7

YTD 2016 YTD 2017

Net Service Revenue (in millions)

+19%

$21.5 $21.9

YTD 2016 YTD 2017

Adjusted EBITDA* (in millions)

+2%+13%

$8.4 $7.6

YTD 2016 YTD 2017

Net Income (in millions)

-9%

*YTD 2016 excludes $2.1 million of acquisition and integration expenses.

YTD 2016$211.5

$1.8

$176.7

16.5%

$15.2

7.2%

$2.1

$14.4

$16.5

$19.4

9.2%

$21.5

10.2%

$8.4

$9.7

$0.27

$0.31

YTD 2015

$192.5

$5.5

$163.8

14.9%

$16.4

$12.9

$17.8

9.2%

$7.5

$0.2514

(In millions, except per share data)

YTD 2017 Income Statement Highlights

83.5% 83.2%

YTD 2016 YTD 2017

Cost of Services as % of NSR

7.2%

8.7%

YTD 2016 YTD 2017

G&A Expenses as % of NSR

1Excludes $2.1 million of acquisition and integration expenses. 2Excludes acquisition and integration-related expense in note 1, net of an income tax benefit of $0.8 million.

Net service revenue

Insurance recoverables and other income

Cost of services (COS)

Gross margin %

General and administrative expenses

G&A as % of NSR

Acquisition and integration expense

Operating income

Adjusted operating income1

EBITDA

EBITDA as a % of NSR

Adjusted EBITDA1

Adjusted EBITDA as a % of NSR

Net income

Adjusted net income1, 2

Diluted earnings per common share

Adjusted diluted earnings per common share1, 2

YTD 2017

$251.7

$1.4

$209.3

16.8%

$21.9

8.7%

--

$13.0

$13.0

$21.9

8.7%

$21.9

8.7%

$7.6

$7.6

$0.24

$0.24

Credit Facility Update

15

$73

$180 $27

$70

$75

$27 $6

PreviousFacility

DebtRepaid Nov.

2015-Dec. 2016

NewFacility

Term Loan Payment

Revolver Payment

Term Loan Drawn

Revolving Credit Facility Draw

Unused Amount

Previous$175M Facility

New$250M facility2

Used for Willbros

acquisition

New $250 million facility1

Five-year tenor, all revolver format

Borrowing capacity linked to trailing 12 month Consolidated EBITDA

Citizens Bank led eight-member bank group

Term loan component eliminated All-revolver structure aids tactical

management of cash flow and borrowings

Flexibility for future interest rate hedging

Existing borrowing spreads maintained Borrowing rates tied to one- to six-month

LIBOR plus 1.5% to 2.75%, depending on current leverage ratio

2Q leverage ratio of 1.4x, results in borrowing rate of LIBOR plus 1.5%

$15 million of balance sheet cash applied at closing, reducing leverage to 1.11x

Key element of growth strategy

Supports working capital, organic growth and acquisition initiatives

1 Subject to leverage limit of 3x trailing 12-month Consolidated EBITDA2 Prior to additional debt repayment conducted as part of the closing process for the new facility

16

Balance Sheet Highlights

Cash and cash equivalents

Days sales outstanding (DSO)

Acquisition-related debt repayment

Acquisition-related debt balance

Cash Flow Highlights

Cash flow from operations

Capital expenditures

Free cash flow

Q2 2016

--

--

$(1.0)

$(2.0)

$(3.0)

Q2 2017

$(1.4)

$68.4

$21.4

$(1.0)

$20.4

(In millions)

Balance Sheet and Cash Flow Highlights

YTD 2016

$9.5

78 days

$13.4

$(4.0)

$9.4

YTD 2017

$26.7

79 days

$(2.8)

$68.4

$18.2

$(2.6)

$15.6

17

Reconciliation of Non-GAAP Measures

Item Q2 - 2017 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders 3,998$ 3,937$

Interest expense 841 461

Interest income (286) (137)

Provision for income taxes 2,473 2,439

Depreciation and amortization 4,371 2,780

Net loss applicable to noncontrolling interest 10 (2)

EBITDA 11,407 9,478

Less: Acquisition and integration expenses - 1,240

Adjusted EBITDA 11,407 10,718

Less: Stock-based compensation expense 2,286 1,511

Less: Other Adjustments 450 (18)

Consolidated Adjusted EBITDA Under the Citizens Credit Agreement 14,143$ 12,211$

Item Q2 - 2017 Q2 - 2016

Net service revenue 127,356$ 111,382$

Cost of services 105,613 93,676

Gross Margin 21,743$ 17,706$

Gross Margin % 17.1% 15.9%

Earnings Before Interest, Taxes, Depreciation, Amortization and Acquisition & Integration Expenses

Gross Margin and Gross Margin %

18

Reconciliation of Non-GAAP Measures

Item YTD - 2017 YTD - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders 7,637$ 8,429$

Interest expense 1,686 489

Interest income (564) (137)

Provision for income taxes 4,204 5,596

Depreciation and amortization 8,875 5,044

Net loss applicable to noncontrolling interest 30 (6)

EBITDA 21,868 19,415

Less: Acquisition and integration expenses - 2,118

Adjusted EBITDA 21,868 21,533

Less: Stock-based compensation expense 3,743 2,780

Less: Other Adjustments (23) (44)

Consolidated Adjusted EBITDA Under the Citizens Credit Agreement 25,588$ 24,269$

Item YTD - 2017 YTD - 2016

Net service revenue 251,661$ 211,545$

Cost of services 209,289 176,660

Gross Margin 42,372$ 34,885$

Gross Margin % 16.8% 16.5%

Earnings Before Interest, Taxes, Depreciation, Amortization and Acquisition & Integration Expenses

Gross Margin and Gross Margin %

19

Reconciliation of Non-GAAP Measures

Item Q2 - 2017 Q2 - 2016

Net cash provided by operating activities 21,403$ (952)$

Additions to property and equipment (1,037) (1,974)

Free Cash Flow 20,366$ (2,926)$

Free Cash Flow

Item YTD - 2017 YTD - 2016

Net cash provided by operating activities 18,217$ 13,436$

Additions to property and equipment (2,662) (4,013)

Free Cash Flow 15,555$ 9,423$

Free Cash Flow

20

Reconciliation of Non-GAAP Measures

Item Q2 - 2017 Q2 - 2016

Operating income 7,036$ 6,698$

Acquisition and integration expenses - 1,240

Adjusted Operating Income 7,036$ 7,938$

Item Q2 - 2017 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders 3,998$ 3,937$

Acquisition and integration expenses - 1,240

Tax effect of acquisition and integration expenses - (475)

Adjusted Net Income Applicable to TRC Companies, Inc's Common Shareholders 3,998$ 4,702$

Item Q2 - 2017 Q2 - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders 3,998$ 3,937$

Acquisition and integration expenses - 1,240

Tax effect of acquisition and integration expenses - (475)

Adjusted Net Income Applicable to TRC Companies, Inc's Common Shareholders 3,998$ 4,702$

Diluted shares outstanding (as disclosed) 31,966 31,369

Add back for dilutive shares - -

Adjusted diluted shares outstanding 31,966 31,369

Adjusted Diluted Earnings per Common Share 0.13$ 0.15$

Adjusted Diluted Earnings per Common Share

Adjusted Net Income Applicable to TRC Companies, Inc.'s Common Shareholders

Adjusted Operating Income

21

Reconciliation of Non-GAAP Measures

Item YTD - 2017 YTD - 2016

Operating income 12,993$ 14,371$

Acquisition and integration expenses - 2,118 Adjusted Operating Income 12,993$ 16,489$

Item YTD - 2017 YTD - 2016

Net income applicable to TRC Companies, Inc.'s common shareholders 7,637$ 8,429$

Acquisition and integration expenses - 2,118

Tax effect of acquisition and integration expenses - (845)

Adjusted Net Income Applicable to TRC Companies, Inc's Common Shareholders 7,637$ 9,702$

Item YTD - 2017 YTD - 2016Net income applicable to TRC Companies, Inc.'s common shareholders 7,637$ 8,429$

Acquisition and integration expenses - 2,118

Tax effect of acquisition and integration expenses - (845)

Adjusted Net Income Applicable to TRC Companies, Inc's Common Shareholders 7,637$ 9,702$

Diluted shares outstanding (as disclosed) 31,783 31,347

Add back for dilutive shares - -

Adjusted diluted shares outstanding 31,783 31,347

Adjusted Diluted Earnings per Common Share 0.24$ 0.31$

Adjusted Operating Income

Adjusted Net Income Applicable to TRC Companies, Inc.'s Common Shareholders

Adjusted Diluted Earnings per Common Share

22

Earnings Before Interest, Taxes, Depreciation, Amortization (EBITDA)

The Company presents EBITDA because it believes that it is a useful tool for the Company, its lenders

and its investors to measure the Company’s ability to meet debt service, capital expenditure and

working capital requirements. As used in the presentation, EBITDA is operating income plus

depreciation and amortization.

Adjusted Earnings Before Interest, Taxes, Depreciation, Amortization (Adjusted EBITDA)

As used in the presentation, Adjusted EBITDA is defined as EBITDA plus acquisition and integration

expenses.

Consolidated Adjusted Earnings Before Interest, Taxes, Depreciation, Amortization

(Consolidated Adjusted EBITDA Under the Citizens Credit Agreement)

As used in the Citizens Credit Agreement, Consolidated Adjusted EBITDA is defined as EBITDA plus

acquisition and integration expenses, stock based compensation expense, and interest and penalties

on federal and state income taxes, less interest expense on excluded indebtedness.

Gross Margin and Gross Margin %

The Company presents Gross Margin and Gross Margin % to allow investors to better evaluate short-

term and long-term profitability trends. The definition of Gross Margin is equal to Net Service Revenue

less Cost of Services. Gross Margin % is equal to Gross Margin Divided by Net Service Revenue.

Definitions for Non-GAAP Measures

23

Free Cash Flow

The Company presents free cash flow, and ratios based on it, to conduct and evaluate its business

because, although it is similar to cash flow from operations, the Company believes it is a useful

measure of cash flows since purchases of fixed assets are a necessary component of ongoing

operations. The definition of Free Cash Flow is equal to net cash provided by (used in) operating

activities plus additions to property and equipment.

Adjusted Operating Income

The Company presents Adjusted Operating Income because it believes that it is a useful tool for the

Company, its lenders and its investors to measure the Company’s underlying operating performance.

As used in the presentation, Adjusted Operating Income is defined as operating income plus

acquisition and integration expenses and the amount of the goodwill impairment.

Adjusted Net Income

The Company presents Adjusted Net Income because it believes that it is a useful tool for the

Company, its lenders and its investors to measure the Company’s financial performance. As used in

the presentation, Adjusted Net Income is defined as net income applicable to TRC Companies, Inc.

plus the tax effected acquisition and integration expenses and the amount of the goodwill impairment.

The Company utilizes its effective tax rate for the period in calculating the tax effect.

Adjusted Diluted Earnings Per Share (Adjusted Diluted EPS)

The Company presents Adjusted Diluted EPS because it believes that it is a useful tool for the

Company, its lenders and its investors to measure the Company’s financial performance. As used in

the presentation, Adjusted Diluted EPS is defined as Adjusted Net Income divided by diluted weighted

average shares outstanding.

Definitions for Non-GAAP Measures